SBA Communications: Building the Invisible Infrastructure of the Digital Age

I. Cold Open & Setup

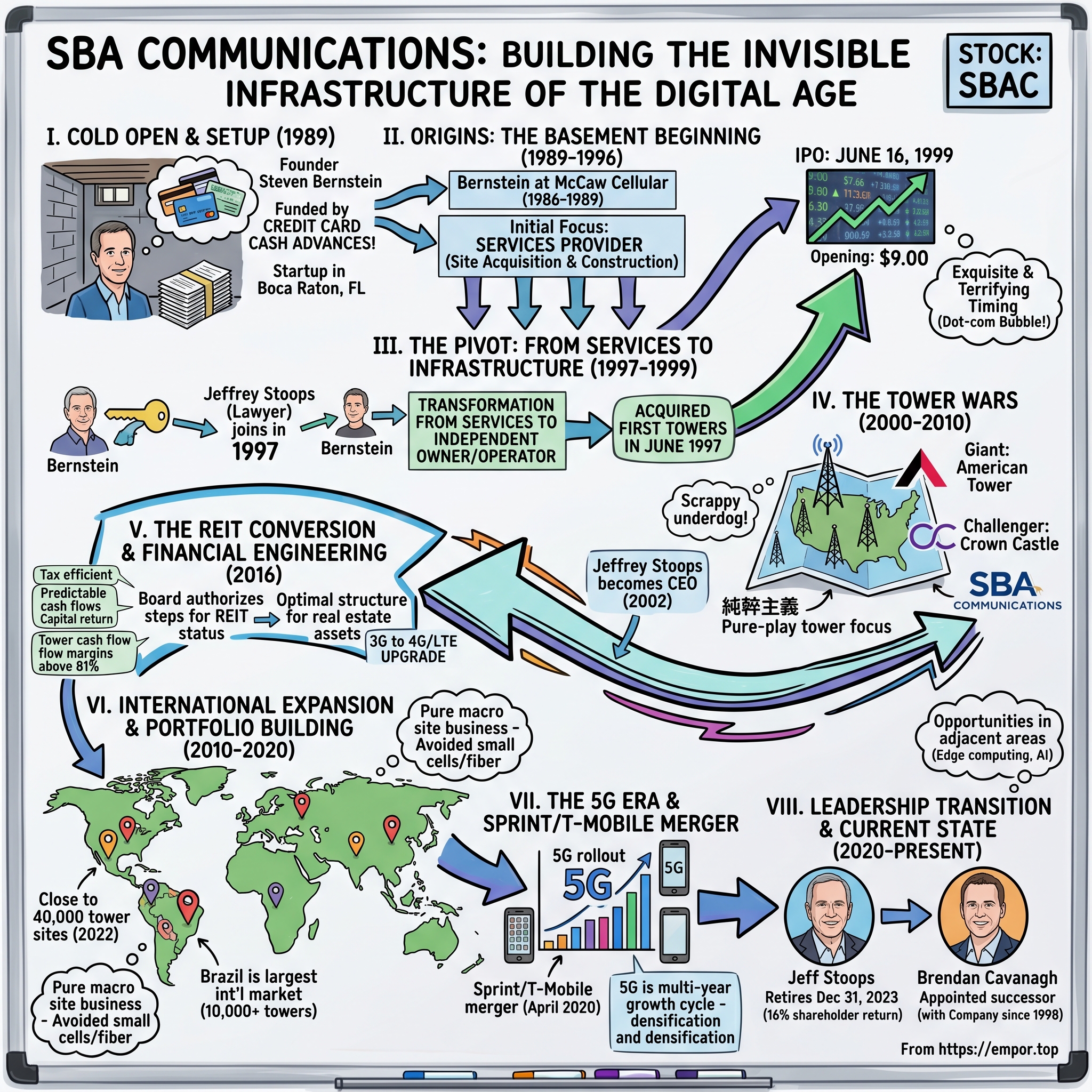

Picture this: It's 1989, and a lawyer named Steven Bernstein is sitting in a basement office in Boca Raton, Florida, shuffling through rejection letters from banks. His desk is cluttered with business plans, telecommunications industry reports, and—most importantly—a stack of credit card applications. While the Berlin Wall is coming down and the world is transforming, Bernstein is about to do something that would make any financial advisor cringe: he's going to fund his startup with credit card cash advances.

Fast forward to today, and that basement startup has become SBA Communications Corporation, a $30 billion tower empire that's part of the S&P 500 Index and ranks among the top Real Estate Investment Trusts by market capitalization. Every time you send a text, stream a video, or make a call on your smartphone, there's a good chance your data is pinging off one of SBA's nearly 40,000 towers scattered across 16 countries. The story of how a lawyer with credit cards built a $24.59 billion telecommunications infrastructure giant is one of the most improbable tales in American business. It's a narrative that spans the entire history of mobile communications—from those brick-sized car phones of the 1980s to today's 5G networks beaming data at gigabit speeds.

But here's what makes this story truly fascinating: SBA doesn't make phones, doesn't sell data plans, and most people have never heard of them. Yet with a portfolio of more than 39,000 communications sites throughout the Americas and in Africa, they've built one of the most valuable real estate empires in America by owning the most boring, utilitarian structures imaginable—cell towers.

Think about it: every Instagram story, every TikTok video, every Zoom call—they all depend on these unglamorous steel lattices dotting the landscape. SBA has figured out how to turn these towers into money-printing machines, with economics so attractive that Warren Buffett himself would blush. We're talking about a business that generates $2.67 billion in annual revenue with profit margins that would make a software company jealous.

This is the story of how Steven Bernstein and his successor Jeffrey Stoops built the invisible backbone of our digital lives, turning rejected loan applications and maxed-out credit cards into one of the most successful infrastructure plays of the past three decades. It's about recognizing that in the gold rush of wireless communications, the real money wasn't in selling phones or service plans—it was in owning the land where everyone needed to plant their flags.

II. Origins: The Basement Beginning (1989-1996)

The year 1989 was a watershed moment in telecommunications history. While Craig McCaw was orchestrating his audacious $3.5 billion bid for LIN Broadcasting—a move that would help create the first truly national cellular network—a young executive named Steven Bernstein was watching from the inside. From 1986 to 1989, Mr. Bernstein was employed by McCaw Cellular Communications ('McCaw'). While at McCaw, Mr. Bernstein was responsible for the development of the initial Pittsburgh cellular system and the start up of the Pittsburgh sales network.

Think about the context: McCaw Cellular was hemorrhaging money—losing over $250 million a year with debt representing nearly 90% of its capital. The company was burning through cash to build out networks, acquire licenses, and convince Americans that they needed a phone in their car. It was the Wild West of wireless, and Bernstein had a front-row seat to both the chaos and the opportunity.

But while McCaw was playing the acquisition game at the highest levels, Bernstein saw a different angle. The carriers were so focused on spectrum licenses and customer acquisition that they were neglecting a crucial piece of the puzzle: the actual infrastructure. Someone had to build and manage the towers that would carry all those cellular signals. And in typical entrepreneurial fashion, Bernstein decided that someone should be him.

In 1989, Steven founded & launched Steven Bernstein and Associates with credit card cash advances in a basement office. Let that sink in for a moment. This wasn't venture capital or private equity backing. This was a University of Florida real estate major maxing out his credit cards to start a telecommunications infrastructure company. The audacity is breathtaking—imagine explaining to your spouse that you're quitting your job at one of the hottest companies in tech to start a business funded by Visa and MasterCard.

The company initially operated as a services provider to wireless carriers, essentially acting as an outsourced construction and site acquisition arm for the cellular operators who were too busy fighting over licenses and customers to build their own infrastructure efficiently. It was unglamorous work—negotiating land leases, managing construction crews, dealing with zoning boards—but it gave Bernstein something invaluable: deep knowledge of the infrastructure business and relationships throughout the industry.

The cellular industry in the early 1990s was experiencing explosive growth, but it was also incredibly fragmented. The FCC had divided the country into 734 cellular markets, with two licenses per market. This created a patchwork of regional operators, each building their own towers, often right next to their competitor's towers. The inefficiency was staggering—imagine two gas stations built side by side, each serving only Ford or Chevy drivers.

What Bernstein understood, perhaps from his real estate background, was that towers were essentially vertical real estate. And unlike spectrum, which was jealously guarded by each carrier, tower space could be shared. A single tower could host equipment from multiple carriers, dramatically improving the economics for everyone involved. But in the early 1990s, most carriers still thought of towers as proprietary assets, not shared infrastructure.

The business model that would eventually make SBA worth billions was hiding in plain sight, but it would take a chance meeting with a sharp Florida lawyer to unlock it. As the 1990s progressed, Steven Bernstein and Associates (the company kept the founder's full name until 1997) continued to grow its services business, building expertise and relationships that would prove invaluable. But the real transformation—the pivot from services company to infrastructure owner—was still to come.

III. The Pivot: From Services to Infrastructure (1997-1999)

The story of SBA's transformation begins with a cold call at lunchtime in 1996. Jeffrey Stoops was a partner with Gunster, Yoakley & Stewart, a Florida law firm, in 1996 when he met Steven E. Bernstein, whose company, SBA Communications, was a client of the firm. Bernstein was seeking legal advice after being approached by a blind public shell company that wanted to merge with SBA and give him a small payout. "One day, I got a call," Stoops said. "It was lunch time. I was at my desk working. It was SBA asking me if my law firm did any M&A (mergers and acquisitions) work. From that phone call, I met Steven Bernstein."

What happened next would change the trajectory of both men's lives and create one of the most successful infrastructure companies in America. Stoops ended up advising Bernstein against merging SBA with the shell company and instead to bring on investors. A partnership was born. "Steven really didn't initially understand the value of SBA," Stoops said. "I helped him see that value and avoid that deal. I think we all would agree that selling to the shell company would have been a big mistake."

Think about the dynamics here: Bernstein had built a successful services business over seven years, but he was about to sell it for what amounted to pocket change to a shell company. It took an outsider—a securities lawyer who understood capital markets—to recognize that what Bernstein had built was far more valuable than even its founder realized. The services relationships, the industry knowledge, the operational expertise—these weren't just worth a small payout from a shell company. They were the foundation for something much bigger.

Before the round of funding was closed, Bernstein made Stoops an offer to join the company. Stoops decided to leave his comfortable position as a law firm partner to join the upstart firm as senior vice president and general counsel in March 1997. "I have to say, another element of personal success is a comfort and ability to take risk," Stoops said. "Measured risk. What I like to call calculated risks. Certainly, leaving Gunster and joining SBA was one of those. When you look back in time, you have to agree that my timing was exquisite. And obviously, who could have known? I have to consider myself a very fortunate guy to have gotten into this business back when it was just getting off the ground." Stoops had been with the law firm for 13 years, working his way up from first-year associate to partner in the corporate, securities and mergers-and-acquisitions area of the firm.

The decision to leave a law partnership for a small services company might have seemed insane. When Stoops finally made the decision to join SBA, he came home and told his wife he was leaving Gunster after 13 years, where he had started out as a first-year associate and worked his way up to partner. They'd just had twins so they had four young kids. In the initial shock of their decision, all his wife Aggie could ask was, 'Do they have health insurance?'

But Stoops saw what others didn't: the tower business was about to explode. Jeff Stoops joined SBA in March, 1997, initially as Executive Vice President and General Counsel, with the primary charge of leading SBA's transition from a services provider to the U.S. wireless carrier industry to an independent owner and operator of wireless communications towers. SBA acquired its first towers in June, 1997.The transformation from services company to tower owner happened with remarkable speed. SBA acquired its first towers in June, 1997. Just two years later, the company was ready for the public markets. Their stock opened with $9.00 in its Jun 16, 1999 IPO. Stoops later served as the Company's Chief Financial Officer, including during its initial public offering in June, 1999.

The IPO timing was exquisite—and terrifying. This was 1999, the peak of the dot-com bubble, when companies with no revenue were going public at billion-dollar valuations. SBA was different—they had real assets, real revenues, and real customers—but they were still swimming in the same frothy waters as pets.com and webvan. The company received all of the net proceeds from the sale of the shares, which were sold at the initial public offering price of $9.00 per share.

The business model that Stoops and Bernstein had constructed was elegant in its simplicity. They would build or acquire towers, then lease antenna space to multiple wireless carriers. Each additional tenant on a tower required minimal incremental cost but generated substantial additional revenue. It was vertical real estate with network effects—the more towers you owned, the more attractive you became to carriers who needed comprehensive coverage.

But what really set SBA apart was their focus. While competitors were diversifying into fiber, data centers, and other telecom infrastructure, SBA stayed laser-focused on towers. This wasn't sexy—in fact, it was deliberately boring. But boring can be beautiful when it comes with predictable cash flows and 80%+ margins.

The capital raised from the IPO fueled an acquisition spree. SBA used the proceeds to finance the construction and acquisition of towers, pay off debt, and position itself for the coming wireless boom. They were building a platform that could scale dramatically as wireless usage exploded—which is exactly what happened as the new millennium dawned.

IV. The Tower Wars: Competing with Giants (2000-2010)

The dawn of the new millennium brought both opportunity and existential challenge to SBA. The dot-com crash of 2000-2001 vaporized trillions in market value and sent telecom companies into bankruptcy. WorldCom, Global Crossing, and countless wireless startups disappeared overnight. For a company that depended on wireless carriers as customers, this was terrifying.

But here's where the tower business model proved its resilience. Even as carriers struggled financially, they couldn't afford to turn off their networks. People still needed to make calls. The towers kept generating cash flow. While the telecom equipment manufacturers and service providers were decimated, the tower companies survived—and then thrived.

There are three main players in the wireless tower space: $86-billion market value American Tower, $53-billion Crown Castle International—both structured as real-estate investment trusts, or REITs—and $23 billion SBA Communications (SBAC). By the mid-2000s, a clear hierarchy had emerged in the tower industry, with American Tower as the giant, Crown Castle as the aggressive challenger, and SBA as the scrappy underdog.

Each company took a different strategic approach. American Tower went global early and aggressively, expanding into Latin America, Africa, and Asia. Crown Castle doubled down on the U.S. market and began diversifying into fiber and small cells. SBA? They stayed focused on towers—just towers—and executed with surgical precision. The year 2002 marked a crucial inflection point. He has been Chief Executive Officer since January 1, 2002. Jeffrey Stoops, the lawyer who had joined five years earlier, was now running the company. Bernstein remained as Chairman, but the operational reins were in Stoops' hands. This transition happened just as the wireless industry was emerging from the telecom crash and beginning its next growth phase.

Under Stoops' leadership, SBA adopted a contrarian strategy. While American Tower was buying thousands of towers internationally and Crown Castle was making massive domestic acquisitions, SBA took a different approach. As the smallest among the top 3 US tower companies, SBA missed out on large tower portfolios acquired by Crown and ATC a decade ago. But instead of trying to compete head-to-head with the giants, they focused on operational excellence and smart, targeted acquisitions.

The 2008 financial crisis tested every infrastructure company in America. Credit markets froze, construction stopped, and wireless carriers slashed capital spending. But towers are perhaps the most recession-resistant assets imaginable. People might cancel their cable TV or stop buying new phones, but they don't stop making calls. The monthly lease payments from AT&T, Verizon, Sprint, and T-Mobile kept flowing.

SBA's focused strategy during this period was vindicated. While diversified telecom companies struggled with their various business lines, SBA's pure-play tower model generated consistent cash flow. They used the crisis as an opportunity to acquire towers from distressed sellers at attractive prices, setting the stage for explosive growth in the coming decade.

The transition from 3G to 4G/LTE networks beginning around 2010 was a goldmine for tower companies. Carriers needed to add new equipment to every tower to support the faster speeds. Better yet, 4G required more towers to deliver the same coverage as 3G, driving demand for new sites. SBA was perfectly positioned to capitalize on this upgrade cycle, with their streamlined operations and strategic tower locations generating exceptional returns.

V. The REIT Conversion & Financial Engineering

October 3, 2016 marked a watershed moment in SBA's history. SBA Communications Corporation (NASDAQ:SBAC) ("SBA") announced today that its Board of Directors has authorized SBA to take all necessary steps for it to qualify as a real estate investment trust ("REIT") for tax purposes. SBA intends to elect to be taxed as a REIT commencing with its taxable year ending December 31, 2016.

"We are pleased to announce this plan for conversion because we believe REIT status is the optimal structure for our business given the real estate nature of our assets," stated Jeffrey A. Stoops, SBA's President and Chief Executive Officer. "We believe a REIT structure will provide many opportunities for creating long-term shareholder value. We have been working on this plan for approximately two years. We expect our conversion to a REIT to have little to no effect on our operations, as we have been operating in compliance with REIT rules since prior to the beginning of 2016."

The REIT conversion was financial engineering at its finest. By converting to a REIT, SBA could avoid corporate-level taxes as long as it distributed at least 90% of its taxable income to shareholders as dividends. For a business generating massive cash flows from long-term leases, this was transformative. The tax savings could be returned to shareholders or reinvested in growth—a win-win proposition.

But the real genius of the tower REIT model goes deeper than tax efficiency. Towers are essentially vertical real estate with extraordinary economics. Operates in two segments: Site Leasing and Site Development, leasing antenna space to wireless service providers on towers that it owns or operates. Each tower can host multiple tenants, and the incremental cost of adding a new tenant is minimal—maybe $1,000-2,000 in ground rent versus $20,000+ in annual lease revenue. It's like owning an apartment building where each new tenant requires no additional construction, maintenance, or utilities.

The numbers tell the story: Tower cash flow margins above 81% in the U.S. These aren't software margins achieved through lines of code—they're infrastructure margins achieved through steel, concrete, and strategic positioning. Once a tower is built and has its first tenant, each additional tenant is almost pure profit. The capital allocation framework that emerged from the REIT conversion was sophisticated yet straightforward. SBA's towers currently average about two tenants each, leaving substantial room for growth. The economics become even more compelling when you understand the revenue breakdown: Seventy-six percent of its revenue comes from domestic carriers and 24% from international carriers. In the US, this revenue comes from the following carriers: AT&T (23%), Sprint (24%), T-Mobile (14%), and Verizon (13%).

This customer concentration might seem risky, but it's actually a strength. These are some of the most creditworthy corporations in America, with multi-year contracts that include specific rent escalators, which average 3% 4% per year, including the renewal option periods. The contracts are structured with an initial term of five years with four 5-year renewal periods at the option of the tenant, creating visibility into cash flows that extends decades into the future.

Perhaps most importantly, SBA controls the ground space under approximately 70% of their towers for a period of time equalling 20 years or more. This land control is crucial—it provides certainty that the tower will remain in place and limits the ability of landowners to hold the company hostage during lease renewals.

The REIT structure also enabled a more aggressive capital return strategy. With the obligation to distribute 90% of taxable income, shareholders could count on regular, growing dividends while the company retained enough capital to fund growth through tower acquisitions and new builds. It was financial engineering that aligned perfectly with the underlying business model—predictable, growing cash flows supporting regular distributions to investors.

VI. International Expansion & Portfolio Building (2010-2020)

The decade from 2010 to 2020 would prove transformative for SBA, as the company evolved from a primarily domestic operator to a truly international infrastructure platform. The strategy was deliberate and calculated: expand into markets with similar wireless growth dynamics to the U.S. but at an earlier stage of development.

As of December 31, 2022, SBA was operating in 16 countries, and owned close to 40,000 tower sites. But this expansion didn't happen overnight. It was a methodical march into carefully selected markets across the Americas, Africa and in Asia. Each market was chosen based on specific criteria: stable regulatory environments, growing wireless penetration, multiple carriers needing infrastructure, and the ability to achieve U.S.-like economics over time.

Brazil became the crown jewel of SBA's international portfolio. Its biggest market is Brazil where the company owns over 10,000 towers. The Brazilian market offered everything SBA was looking for: a massive population increasingly dependent on mobile services, multiple well-capitalized carriers, and a regulatory environment that supported independent tower ownership. The economics weren't quite as attractive as the U.S. initially, but the growth potential was enormous.

The international expansion strategy stood in stark contrast to SBA's approach in other areas. While competitors were diversifying into fiber networks, data centers, and small cells, SBA remained laser-focused on macro towers. This wasn't stubbornness—it was discipline. The small cells decision exemplified SBA's disciplined approach. SBA Communications CEO Jeffrey Stoops said that it had doubled its initial $43 million investment in ExteNet over five years, and that the company had learned a lot from the experience. "We had a window seat there for a very long time and we saw … 10, 20, 30 reasons why we simply prefer the macro site business," said Stoops. The company exited with a $150 million profit—a nice return—but more importantly, they avoided being drawn into a lower-margin, capital-intensive business that didn't fit their model.

CEO Jeffrey Stoops said they doubled their $43 million investment in ExteNet over five years but concluded it was "a lower margin, capital-intensive business". The decision to exit wasn't about whether small cells were real or important—they clearly were. It was about capital allocation and focus. "We just frankly don't want to be a fiber company," Stoops said bluntly.

This discipline extended to every aspect of international expansion. Each new market was evaluated not just on its growth potential but on whether SBA could achieve its target returns. The company walked away from opportunities that others pursued aggressively if the economics didn't meet their standards. It was the anti-empire building strategy—growth for the sake of returns, not growth for the sake of size.

By 2020, the international portfolio had become a significant contributor to SBA's value proposition. While international markets generated lower margins than the U.S. initially, they offered tremendous growth potential as wireless penetration increased and carriers densified their networks. The playbook was the same everywhere: acquire or build towers, add tenants over time, generate increasing cash flows with minimal incremental investment.

VII. The 5G Era & Sprint/T-Mobile Merger

The 5G revolution and the Sprint/T-Mobile merger represented both the greatest opportunity and the greatest challenge in SBA's history. The ongoing rollout of 5G networks is a major driver for tower companies like SBAC, as carriers densify their networks to support higher data speeds and lower latency. But 5G also brought complexity—new spectrum bands, new equipment, and most challenging of all, massive industry consolidation.

The Sprint/T-Mobile merger, which closed in April following years of unsuccessful attempts, with new T-Mobile undertaking "very aggressive" government-mandated build-out requirements, created seismic shifts in the tower industry. For SBA, which had significant exposure to both carriers, this presented a unique challenge. When two carriers merge, they often decommission redundant sites, potentially reducing tower revenues.

But the merger also created opportunities. The combined T-Mobile was required to meet aggressive 5G coverage targets as a condition of regulatory approval. This meant massive network investments, new equipment deployments, and ultimately more revenue for tower companies. The key was managing the transition—the churn from decommissioned sites versus the growth from new 5G deployments.

The 5G buildout itself was unlike any previous network upgrade. While 3G to 4G was largely about adding new equipment to existing towers, 5G required fundamental changes to network architecture. New spectrum bands meant new equipment. Mid-band spectrum required different propagation patterns. The networks needed to be denser, with more sites and more equipment per site.

For SBA, this translated into a multi-year growth cycle. Fixed wireless growth creating additional opportunities for tower leasing, and relentless growth in mobile data consumption driving demand for tower space. Every tower in the portfolio became more valuable as carriers added 5G equipment alongside their existing 4G infrastructure. The beauty of the tower model—that incremental tenants and equipment generate minimal incremental costs—was on full display.

The competitive dynamics also shifted. With T-Mobile emerging as a strengthened third player alongside AT&T and Verizon, and with DISH building a greenfield 5G network, the industry had more players needing infrastructure than ever before. Even as some redundant sites were decommissioned, the overall demand for tower space increased dramatically.

VIII. Leadership Transition & Current State (2020-Present)

February 21, 2023 marked the end of an era and the beginning of a new chapter. SBA Communications Corporation (NASDAQ: SBAC) ("SBA" or the "Company"), a leading global owner and operator of communications infrastructure, announced today that Jeff Stoops will retire from his positions as President and Chief Executive Officer on December 31, 2023. SBA's Board of Directors has appointed Brendan Cavanagh, SBA's Executive Vice President and Chief Financial Officer, to succeed Mr. Stoops as President and CEO.

The numbers spoke for themselves: During Mr. Stoops' tenure as CEO, through December 31, 2022, SBA has delivered annualized total shareholder returns of 16% and annualized growth in enterprise value of 17%. These aren't tech startup returns built on hype—these are infrastructure returns built on steel, concrete, and long-term contracts.

Jeff Stoops retired from President and CEO positions on December 31, 2023, with Brendan Cavanagh appointed as successor. Stoops remains on the Board as non-executive Chairman, while Steven Bernstein continues to serve on the Board. This wasn't a sudden departure or a crisis succession—it was a carefully orchestrated transition years in the making.

Cavanagh has been with SBA since 1998 and served as CFO since 2008, working closely with former CEO Jeff Stoops, now retired, to lead and build the organization into the international tower company that it is today. "I am extremely thankful to Jeff for his guidance and support over the last quarter century," said Brendan Cavanagh, the Company's next President and CEO. "I am also very excited for the future of SBA. I see many opportunities to support our customers in their continuing efforts to expand the capabilities and depth of their wireless networks in order to meet the constantly growing demand for enhanced wireless services."

The transition represented continuity rather than disruption. Steven Bernstein, current Chairman of the Board of SBA, said "Jeff has had a tremendous impact on our company and industry. The Board is grateful for his leadership over two decades, a period of time driven by clear and focused vision, outstanding operational execution and integrity. During that time our shareholders have been rewarded handsomely, our customers well-served and the lives of our employees and communities improved."

Under Cavanagh's leadership, SBA has maintained its disciplined approach while adapting to new market realities. The company continues to focus on its core tower business while carefully evaluating opportunities in adjacent areas. The strategy remains consistent: own exclusive assets, maintain pricing power, generate superior returns on invested capital.

The current environment presents both challenges and opportunities. Higher interest rates have increased the cost of capital, making acquisitions more expensive. Some carriers have slowed their network investments. But the long-term trends remain intact: data consumption continues to grow exponentially, 5G networks require densification, and new applications like AI and edge computing will drive additional infrastructure needs.

IX. Business Model & Competitive Advantages

The brilliance of SBA's business model lies in its simplicity. At its core, the company owns vertical real estate and rents space on it to multiple tenants. But the economics of this simple model are extraordinary.

76% of revenue from domestic carriers: AT&T (23%), Sprint (24%), T-Mobile (14%), and Verizon (13%). This customer concentration might seem like a risk, but it's actually a moat. These are the only companies with the spectrum licenses, capital, and customer bases to operate nationwide wireless networks. They need SBA's towers, and SBA needs them. It's a symbiotic relationship that has proven remarkably stable over decades.

SBA's towers currently average about two tenants each, which means there's significant room for growth without building a single new tower. The economics of adding tenants are compelling: the first tenant essentially pays for the tower, the second tenant is highly profitable, and the third and fourth tenants are almost pure profit. Tower cash flow margins above 81% in the U.S. demonstrate this leverage.

The operational excellence extends beyond just the tower economics. SBA controls the ground space under approximately 70% of their towers for 20 years or more. This land control is crucial—it provides certainty and limits the leverage of ground lessors. The company has systematically extended ground lease terms and, where economical, purchased the land outright.

But perhaps the most important competitive advantage is what SBA doesn't do. While competitors have diversified into fiber, data centers, small cells, and other adjacent businesses, SBA has remained focused on towers. This focus enables superior execution, better capital allocation, and higher returns on invested capital.

The pure-play strategy also makes SBA more valuable to its customers. Wireless carriers know that SBA isn't trying to compete with them in any way—they're purely an infrastructure provider. This clarity of purpose strengthens relationships and can lead to better deal terms.

The REIT structure adds another layer of advantage. The requirement to distribute 90% of taxable income forces disciplined capital allocation. Management can't hoard cash or make empire-building acquisitions. Every investment must meet strict return thresholds. This structural discipline has served shareholders well over the years.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube