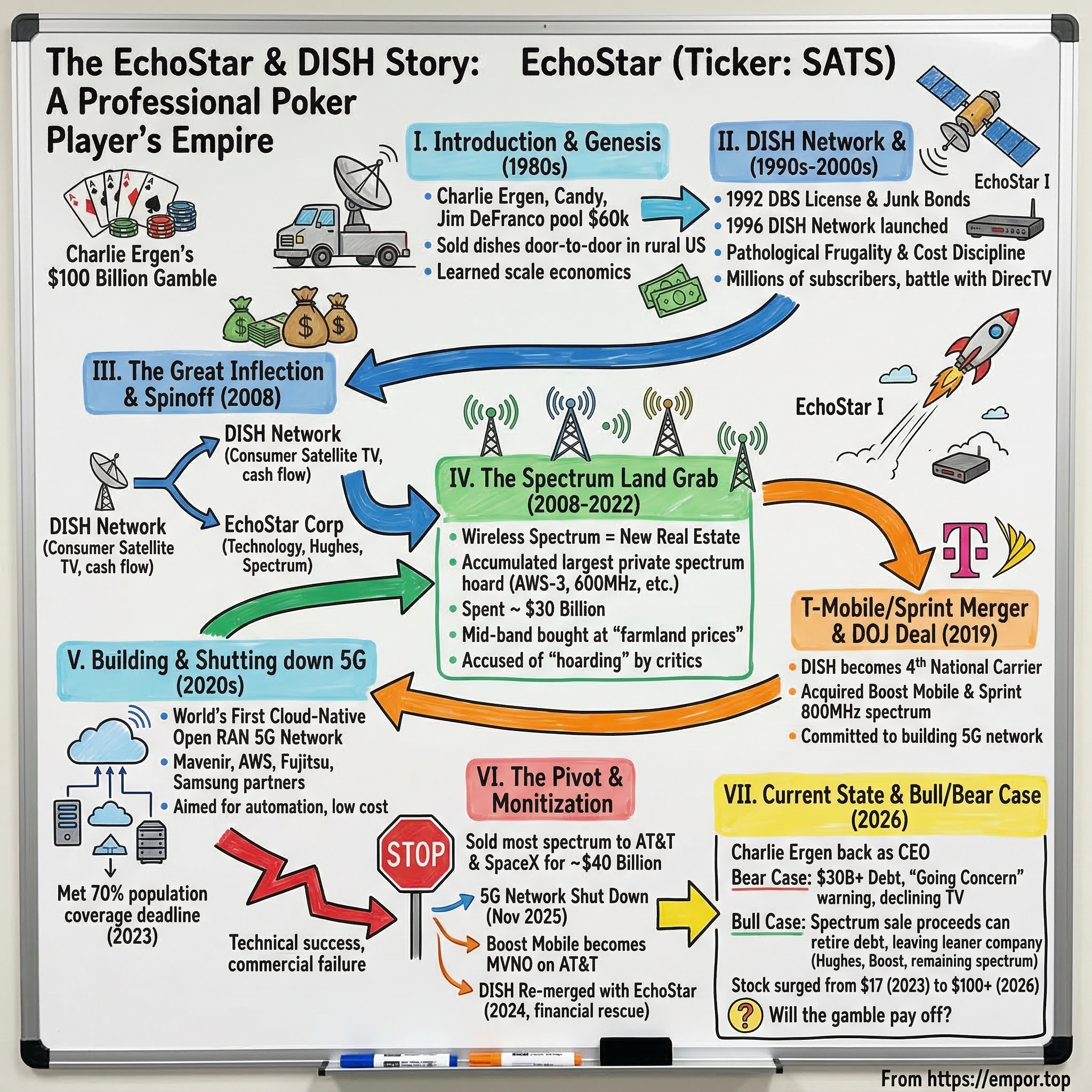

The Professional Poker Player's Empire: The EchoStar and DISH Story

I. Introduction: The $100 Billion Gamble

There is a photograph from 1980 that tells you everything you need to know about EchoStar. In it, a twenty-seven-year-old Charlie Ergen stands next to a flatbed truck in rural Colorado, a massive C-band satellite dish strapped to the back. He has sixty thousand dollars in his pocket, most of it earned counting cards at blackjack tables in Lake Tahoe. His future wife, Candy, and his gambling buddy Jim DeFranco are with him. They are about to drive that truck across the American West, knocking on doors in towns too remote for cable television, selling the promise of a hundred channels beamed from space.

Forty-six years later, that same man controls a company worth north of thirty billion dollars. But it is not the satellite dishes that made the fortune. It is the airwaves themselves, the invisible electromagnetic spectrum that carries every phone call, every text message, every video stream in America. Charlie Ergen spent four decades and roughly thirty billion dollars accumulating the largest private hoard of wireless spectrum in the United States. And then, in the span of a few months in 2025, he sold most of it for approximately forty billion dollars to AT&T and Elon Musk's SpaceX.

The EchoStar story is not a simple rise-and-fall narrative, nor is it a straightforward success story. It is something far more unusual: a multi-decade, high-stakes capital allocation play orchestrated by a professional gambler who understood one thing better than almost anyone else in American business. Scarce assets become more valuable over time, and the player who accumulates the most chips before the final hand wins.

The stakes today are enormous. EchoStar carries more than thirty billion dollars in debt. Its standalone 5G network, once heralded as the world's first cloud-native wireless infrastructure, was shut down in November 2025. Its satellite television business, DISH Network, continues to hemorrhage subscribers. Its auditor, KPMG, issued a "going concern" warning in the 2025 annual filing, the accounting profession's equivalent of a yellow flag on the last lap.

And yet the stock has surged from roughly seventeen dollars in late 2023 to over a hundred dollars in early 2026. The market is betting that the spectrum sales will close, the debt will be retired, and what emerges on the other side will be a leaner, more focused company built around Hughes satellite broadband, a wholesale wireless MVNO arrangement with AT&T, and whatever Charlie Ergen dreams up next.

This is a story about the tension between vision and execution, between accumulating assets and monetizing them, between the patience of a card counter and the urgency of a debt maturity schedule. It is the story of a man who bet everything on a thesis about spectrum scarcity, and who, depending on how the next twelve months unfold, will either be vindicated as one of the greatest capital allocators of his generation or remembered as the architect of one of the most spectacular collapses in telecom history.

The cards are on the table. Let us see how the hand was dealt.

II. The Genesis: From the Back of a Truck to the Sky

The origin story of EchoStar begins not in a boardroom or a garage, but in a casino. Charlie Ergen was born in 1953 in Oak Ridge, Tennessee, a company town built during the Manhattan Project. His father was a nuclear physicist. Ergen attended the University of Tennessee, earned an MBA from Wake Forest University in 1976, and took a conventional first job as a financial analyst at Frito-Lay. He lasted about two years. The corporate world bored him. What did not bore him was probability.

Ergen had discovered a book called "Playing Blackjack as a Business" and became obsessed with card counting. He left Frito-Lay at twenty-five and moved to the casinos of Lake Tahoe, where he made a living at the blackjack tables. It was there that he met Jim DeFranco, a kindred spirit who shared his appetite for calculated risk. The two became a team, with DeFranco sometimes lip-syncing card counts across the table. One night in 1980, a security guard caught DeFranco mid-signal, and they were ejected from the casino. Standing in the parking lot, looking for what to do next, they saw a truck hauling a giant C-band satellite dish down the highway. Ergen had an idea.

The satellite television industry in 1980 was the Wild West. The dishes were enormous, ten to twelve feet across, and they cost thousands of dollars. But in rural America, where cable companies had no economic incentive to lay wire, these dishes were the only way to get more than three channels. Ergen, Candy, and DeFranco pooled their sixty thousand dollars and founded EchoSphere Corporation. They bought satellite dishes wholesale and drove across Colorado, Wyoming, and Montana, selling them door to door from the back of a truck. Candy handled the books. DeFranco helped with sales. Ergen did everything else.

The business was marginal but educational. Ergen learned the satellite industry from the ground up, literally installing dishes on rooftops and troubleshooting signal issues in the snow. More importantly, he learned something about the economics of broadcasting: the cost of beaming a signal from a satellite was essentially fixed, whether one person was watching or one million. The marginal cost of adding a subscriber was near zero once the infrastructure was in place. This insight, the power of scale economics in a fixed-cost business, became the foundation of everything that followed.

By the late 1980s, Ergen had a bigger vision. The FCC was auctioning licenses for Direct Broadcast Satellite, a new technology that used much smaller dishes and could deliver hundreds of channels to a compact receiver. In 1992, EchoStar received a DBS license and its own geostationary orbital slot. Ergen raised three hundred thirty-five million dollars in junk bonds, a breathtaking sum for a company that had been selling dishes from a truck a decade earlier, and used the money to fund the construction and launch of EchoStar I, which reached orbit in 1995.

The following year, EchoStar launched the DISH Network brand. The pitch was simple: more channels, lower prices, smaller dishes than what cable offered. And unlike cable, DISH could reach every home in America with a clear view of the southern sky. The timing was perfect. The cable industry in the mid-1990s was complacent, raising prices and offering poor customer service. DISH undercut them on price and overwhelmed them on channel count. By the early 2000s, DISH had millions of subscribers and was locked in a fierce battle with DirecTV for satellite television supremacy.

What set Ergen apart from every other television executive was not his ability to grow subscribers. It was his pathological frugality. DISH headquarters in Englewood, Colorado, was famously spartan. No mahogany conference tables, no corporate art collections. Ergen was known for sharing hotel rooms on business trips and flying coach. Employees joked that the company's idea of a perk was a functioning vending machine. This was not theater. It was philosophy. Ergen believed that every dollar saved on overhead was a dollar that could be deployed into spectrum, satellites, or technology. The fat incumbents at AT&T and Verizon, with their layers of middle management and their gleaming headquarters, were spending billions on things that did not generate returns. Ergen refused to do the same.

That culture of relentless cost discipline would prove critical in the decades ahead, as Ergen pivoted from building a satellite television empire to executing perhaps the most audacious spectrum accumulation strategy in the history of American telecommunications. The man who once counted cards at Lake Tahoe was about to start counting megahertz.

III. The Great Inflection: The 2008 Spinoff and the Spectrum Land Grab

To understand the genius and the risk of what Charlie Ergen did next, you need to understand one concept: wireless spectrum is the new real estate. Every wireless signal, every phone call, every streaming video, travels over a specific band of electromagnetic frequencies. The FCC controls who gets to use which frequencies in the United States, and it allocates them through auctions. Once a band of spectrum is sold, it is gone. You cannot manufacture more. You cannot 3D-print a new slice of the electromagnetic spectrum. It is the ultimate scarce resource, and Ergen recognized this decades before the rest of the industry caught on.

In January 2008, Ergen executed the first major structural move in his long game. He split EchoStar Communications Corporation into two publicly traded companies. DISH Network Corporation kept the consumer satellite television business, the subscribers, the billing systems, the remote controls. EchoStar Corporation kept the technology: the satellites, the set-top box manufacturing, the uplink centers, a company called Sling Media that was pioneering streaming video, and critically, the spectrum licenses that were not core to DISH's TV operations.

The stated rationale was to "unlock value" by allowing each company to pursue its own strategy independently. But the real purpose was more subtle. By separating the cash-generating television business from the capital-hungry technology and spectrum side, Ergen created a structure where DISH could fund aggressive spectrum acquisitions without spooking TV investors, while EchoStar could develop new technologies without being judged by quarterly subscriber metrics. Ergen maintained controlling stakes in both companies, giving him the ability to coordinate strategy across both entities even as they operated as separate public companies.

And then the spending began. Over the next fifteen years, while analysts and investors obsessed over DISH's declining television subscriber counts, treating the company as a "melting ice cube," Ergen was executing a strategy of breathtaking scale and patience. Through FCC auctions and private acquisitions, the DISH and EchoStar entities accumulated one of the largest portfolios of wireless spectrum in the United States.

The numbers are staggering. In the AWS-3 auction in 2015, DISH spent approximately thirteen billion dollars, making it one of the largest single bidders in FCC auction history. In 2022, the company spent another seven point three billion dollars on 3.45 GHz licenses. In between, Ergen accumulated 600 MHz, 700 MHz E-block, AWS-4, PCS H-block, and millimeter wave spectrum through a combination of auctions and strategic purchases. By the time the dust settled, EchoStar and DISH controlled an average of roughly one hundred forty-four megahertz of nationwide sub-6 GHz spectrum, a portfolio that rivaled those of carriers with ten times their subscriber base.

The pricing tells the story of Ergen's advantage. When Ergen was buying mid-band spectrum in the mid-2010s, the market considered it a speculative asset. Nobody was sure when or how it would be deployed. Ergen was acquiring spectrum for roughly fifty to seventy cents per MHz-pop, a measure that divides the total cost by the number of megahertz times the population covered. By comparison, when the major carriers fought over C-band spectrum in 2021, prices exceeded a dollar per MHz-pop. Ergen had been buying the equivalent of Manhattan real estate at farmland prices, simply because he was willing to buy before anyone else saw the value.

To put this in simpler terms, think of spectrum like oceanfront property. There is only so much coastline in the world. The carriers who own it can charge tolls for everyone who wants to use it. Ergen was buying beachfront lots in the 1990s and 2000s when everyone else was investing in inland strip malls. By the time the rest of the industry realized that wireless data demand would make mid-band spectrum extraordinarily valuable, Ergen already owned the beach.

Critics called him a "spectrum hoarder" and a "squatter." Wall Street analysts questioned whether DISH would ever build a network or whether the spectrum was simply a bargaining chip. The FCC imposed build-out requirements: use the spectrum by certain deadlines or lose it. Ergen treated these deadlines the way he treated a poker bluff, pushing right up to the edge, seeking extensions, and always managing to stay just barely in compliance.

Then came the moment that transformed the entire game. In 2019, T-Mobile and Sprint announced a twenty-six-and-a-half-billion-dollar merger. The deal would reduce the number of major U.S. wireless carriers from four to three. The Department of Justice had a problem: approving the merger without creating a new fourth competitor would concentrate too much market power. They needed someone with enough spectrum, enough ambition, and enough tolerance for risk to step into the void. There was only one candidate.

On July 26, 2019, the DOJ announced the conditions for approving the T-Mobile/Sprint merger. DISH would purchase Sprint's prepaid businesses, including Boost Mobile, along with fourteen megahertz of 800 MHz spectrum, for a combined five billion dollars. In exchange, DISH committed to building a 5G network covering seventy percent of the U.S. population by June 2023, with a two-point-two-billion-dollar penalty for failure. DISH also secured a seven-year MVNO agreement with T-Mobile, allowing it to resell T-Mobile's network service while building its own infrastructure.

The professional poker player had just been dealt into the biggest hand of his life. He had spent two decades accumulating chips. Now he had to play them.

IV. The "New" EchoStar: Management and the Ergen Doctrine

In March 2022, EchoStar brought in a new CEO: Hamid Akhavan, a man whose resume read like a telecom integration playbook. Akhavan held a bachelor's degree in electrical engineering from Caltech and a master's from MIT. He had served as CEO of T-Mobile International, sitting on the board of management at Deutsche Telekom, one of the world's largest telecommunications conglomerates. After that, he ran Unify (formerly Siemens Enterprise Communications), then moved into private equity as a founding partner at Long Arc Capital and later a partner at Twin Point Capital. He was, in short, a man who understood how to build, integrate, and operate large-scale telecom networks.

Akhavan's mandate was clear: take Ergen's spectrum portfolio and build a functioning national wireless carrier. This was not a job for a visionary. It was a job for an executor. Ergen, who retained the title of Executive Chairman, would continue to set strategic direction. Akhavan would make the trains run on time.

The dynamic between the two men illustrated something fundamental about EchoStar's corporate culture. Ergen has always been the "architect," the man who sees the board five moves ahead and is willing to endure years of pain for a payoff that may never come. He is famous for telling investors, "We don't care about the next quarter; we care about the next decade." This is not corporate platitude. It is an operational reality enabled by one structural feature that makes EchoStar unlike almost any other public company in America.

Charlie Ergen controls EchoStar through a dual-class share structure. Class A shares, the ones traded on the Nasdaq, carry one vote each. Class B shares, held almost entirely by Ergen and his affiliates, carry ten votes each. The result: Ergen owns roughly half the economic equity but controls approximately eighty to ninety percent of the total voting power. He can appoint and remove board members at will. He can approve or reject any merger, any financing, any strategic pivot. No activist investor, no matter how large their stake, can challenge him. No proxy fight can unseat him.

This structure is both EchoStar's greatest strength and its most significant governance risk. On the strength side, it allows Ergen to make long-term bets that would get any accountable-to-the-quarterly-cycle CEO fired. The stock dropped from over forty dollars in 2014 to under seven dollars in 2023. Ergen did not flinch. He kept buying spectrum, kept investing in the 5G build-out, kept telling investors that the payoff was coming. A conventional CEO answering to institutional shareholders and activist funds would have been forced to monetize the spectrum years earlier, likely at far lower prices.

On the risk side, Ergen's absolute control means there are no guardrails. If his judgment is wrong, there is no mechanism to course-correct. The board functions largely as an advisory body. Jim DeFranco, the original co-founder from the Lake Tahoe days, still serves as a director and executive vice president. This is a family operation masquerading as a public company, and investors need to understand that when they buy shares, they are buying a ticket on the Charlie Ergen express with no ability to change the destination.

The management incentive structure reinforced this long-term orientation. Rather than tying compensation primarily to EBITDA or revenue growth, EchoStar's management was heavily incentivized on network deployment milestones, specifically meeting the FCC's build-out requirements for their spectrum licenses. Miss the deadline, lose the spectrum. Lose the spectrum, and the entire thesis collapses. This created an interesting alignment: management was paid to build infrastructure, not to maximize short-term profitability. In theory, this is exactly the right incentive structure for a company making a generational infrastructure bet. In practice, it meant years of cash burn and balance sheet deterioration while the network was under construction.

By late 2025, the management picture had shifted dramatically. Akhavan transitioned from CEO to lead the newly formed EchoStar Capital division, focused on strategic investments and M&A. Ergen himself resumed the CEO title. The move signaled that the company was entering a new phase, one defined not by network construction but by asset monetization and corporate restructuring. The architect was back in the captain's chair for what may be the final act of a forty-year drama.

V. M&A Deep Dive: The Boost Mobile Acquisition and the DISH Re-Merger

On July 1, 2020, DISH completed the acquisition of Boost Mobile from T-Mobile for one point four billion dollars. The deal, mandated by the DOJ as a condition of the T-Mobile/Sprint merger approval, included nine point three million prepaid customer accounts, hundreds of employees, thousands of independent retail locations, and the seven-year MVNO agreement with T-Mobile that would allow Boost to continue operating on T-Mobile's network while DISH built its own infrastructure.

Was one point four billion a good price? Context matters. T-Mobile had just paid twenty-six and a half billion dollars for the entirety of Sprint, including its spectrum, infrastructure, and tens of millions of customers. By that yardstick, getting nine million customers and a launch pad for a fourth national carrier for a fraction of the price seemed like a steal. But there was a catch, and it was a significant one: Boost was a "leaky bucket." Prepaid wireless customers are notoriously fickle. They switch carriers for five dollars a month in savings. They have no contracts, no device financing ties, no switching costs. DISH was buying a customer base that would begin evaporating the moment they took ownership.

And evaporate it did. From nine point three million subscribers at acquisition, Boost's base declined steadily, dropping to approximately seven and a half million by the fourth quarter of 2025. The "$hrink-It!" plan, which started at forty-five dollars per month and dropped by five-dollar increments with each on-time payment, was creative but could not stem the tide. The competitive dynamics of prepaid wireless in America are brutal. T-Mobile's Metro, AT&T's Cricket, and a constellation of smaller MVNOs all compete ferociously on price. Boost, running on a network it did not own and could not fully control, was perpetually at a disadvantage.

In July 2024, EchoStar merged the postpaid "Boost Infinite" brand and the prepaid "Boost Mobile" brand into a single unified Boost Mobile identity, offering unlimited 5G plans starting at twenty-five dollars per month with a price-lock guarantee. The consolidation was an acknowledgment that the two-brand strategy had created confusion in the market. But by then, the subscriber bleeding was a secondary concern. The real drama was happening at the corporate level.

On January 1, 2024, EchoStar completed its all-stock acquisition of DISH Network, reuniting the two companies after sixteen years of separation. The re-merger was not a victory lap. It was a financial rescue mission.

Here is why. By late 2023, the combined DISH/EchoStar ecosystem was staring at a wall of debt maturities. DISH Network, which had taken on enormous leverage to fund the spectrum acquisitions and 5G build-out, owed billions that would come due starting in 2024. EchoStar, the separate entity, had the satellite assets, the Hughes broadband business, and a cleaner balance sheet. The re-merger allowed the combined entity to pool its resources, using the cash flows from the satellite businesses to service the wireless debt, and giving the company more flexibility to refinance, sell assets, or raise capital.

The transaction was structured as an all-stock deal to avoid triggering change-of-control provisions in DISH's bond indentures, which would have accelerated debt payments and potentially forced a default. It was financial engineering born of necessity rather than opportunity.

How does this compare to other telecom M&A disasters? When AT&T acquired DirecTV in 2015 for forty-nine billion dollars, it was buying a declining satellite TV business with no strategic synergy beyond bundling. When Verizon acquired Yahoo for four point five billion dollars, it was buying a fading internet brand with no connection to its core wireless business. Both deals destroyed shareholder value. The EchoStar/DISH re-merger was fundamentally different. EchoStar was not buying "content" or "brands." It was consolidating infrastructure, specifically spectrum licenses, satellite capacity, and wireless network assets, under a single corporate umbrella to improve financial flexibility. Whether this distinction matters depends entirely on whether the company can survive its debt maturities, a question that would dominate the next two years.

A critical two-billion-dollar debt payment came due in November 2024. To bridge it, EchoStar secured two and a half billion dollars in financing from TPG and DirecTV. Meanwhile, EchoStar attempted to sell the DISH TV and Sling TV businesses to DirecTV, which would have created a satellite television monopoly in the United States. The deal fell apart in November 2024 when DBS noteholders rejected the exchange offer. The satellite TV business, the original cash cow, could not be separated from the corporate body, at least not yet.

VI. The Hidden Businesses: Beyond the Satellite Dish

The Open RAN 5G Network: A Noble Experiment

To understand what EchoStar tried to build with its 5G network, imagine the difference between building a house with custom-fabricated components from a single manufacturer versus building one with off-the-shelf parts from a hardware store. Traditional wireless networks, the ones operated by AT&T, Verizon, and T-Mobile, are like the custom-fabricated house. They use proprietary hardware from Nokia or Ericsson, equipment that only works with other components from the same vendor. If you want to upgrade, you are locked into that vendor's ecosystem. It is expensive, inflexible, and controlled by a small oligopoly of European equipment manufacturers.

EchoStar set out to build something radically different: the world's first cloud-native, standalone 5G Open RAN network. "Open RAN" stands for Open Radio Access Network. Instead of proprietary hardware, the network used software running on standard servers, much of it hosted on Amazon Web Services' public cloud. Mavenir, a Texas-based software company, provided the radio access network software. Fujitsu and Samsung supplied the radios. The 5G core, the brain of the network, ran as code on AWS data centers rather than on dedicated telecom hardware.

The potential was extraordinary. A traditional carrier like Verizon employs tens of thousands of people to manage its network. EchoStar's vision was to run a national carrier with roughly two thousand employees, using software automation and cloud infrastructure to replace human labor. The cost structure would be fundamentally different. Network upgrades would be software patches rather than hardware replacements. New features could be rolled out in days rather than months. And because the network was built on open standards, EchoStar could mix and match vendors, avoiding the lock-in that keeps the Big Three tethered to Nokia and Ericsson.

It was an audacious technical bet. And it worked, at least partially. DISH certified to the FCC that its network met the seventy-percent population coverage milestone by the June 2023 deadline, claiming download speeds of at least thirty-five megabits per second. The company initially aimed for eighty percent coverage by end of 2024, and the FCC granted extensions on additional per-license-area requirements, pushing deadlines to December 2026.

But the commercial reality never matched the technical ambition. The Boost Infinite launch, the postpaid product running on DISH's own 5G network, was plagued by coverage gaps, dropped calls, and customer complaints. CEO Akhavan publicly acknowledged the launch was "not optimized." Building a network from scratch is one thing. Operating it reliably across thousands of cell sites in hundreds of markets is another. DISH was trying to do in three years what the major carriers had spent decades perfecting.

Then, in August and September 2025, EchoStar made the decision that stunned the industry. Rather than continue pouring capital into the 5G build-out, the company agreed to sell approximately fifty megahertz of spectrum (3.45 GHz and 600 MHz bands) to AT&T for twenty-three billion dollars, and its AWS-4 and H-block spectrum to SpaceX for seventeen billion dollars. The combined forty billion dollars in spectrum sales represented perhaps the single largest monetization of wireless spectrum in history. On November 15, 2025, EchoStar shut down its standalone 5G network entirely and transitioned Boost Mobile to an MVNO arrangement on AT&T's network.

The shutdown was described by industry observers as a devastating blow to the global Open RAN movement. Mavenir, which had built its business around the DISH partnership, stopped manufacturing Open RAN radios in June 2025. EchoStar declared "force majeure" on tower leases and vendor contracts, triggering lawsuits and industry backlash. The dream of a software-defined fourth carrier, built from the ground up on open standards, was over.

Was the 5G experiment a failure? In one sense, absolutely. Billions of dollars were spent on infrastructure that was operational for less than three years. The company took a sixteen-billion-dollar impairment charge in the fourth quarter of 2025, the accounting recognition of a massive capital misallocation. But in another sense, the 5G build-out served its purpose: it kept the FCC satisfied that EchoStar was using its spectrum, which prevented license revocation and preserved the option to sell that spectrum at peak prices. Whether this was the plan all along or a improvisation born of desperation is a question only Charlie Ergen can answer.

Hughes Network Systems: The Enterprise Engine

While the 5G drama consumed headlines, the quietest part of EchoStar's business continued to generate cash. Hughes Network Systems is the "boring" business that provides satellite internet to more than one million residential subscribers and approximately five hundred thousand enterprise sites across North and South America. It provides connectivity to gas stations, retail chains, and bank branches that need reliable internet in locations where terrestrial broadband is unavailable or unreliable. It provides in-flight Wi-Fi to airlines and cellular backhaul for mobile network operators.

The crown jewel of the Hughes fleet is JUPITER-3, launched on July 29, 2023, aboard a SpaceX Falcon Heavy rocket from Kennedy Space Center. It entered commercial service in December 2023 and holds the distinction of being the largest commercial communications satellite ever built, weighing approximately nine metric tons. JUPITER-3 processes more than five hundred gigabits per second, doubling the capacity of the entire existing Hughes JUPITER satellite fleet. This massive capacity injection made Hughes competitive with Starlink in specific enterprise niches, particularly for multi-site businesses that need managed connectivity with service level agreements rather than consumer-grade best-effort service.

Hughes operates in a different competitive space than Starlink. SpaceX's constellation targets individual consumers and small businesses with easy-to-install terminals and no long-term contracts. Hughes targets enterprise customers who need managed network services, guaranteed uptime, and integration with their existing IT infrastructure. Think of a national restaurant chain that needs every location connected to headquarters for point-of-sale processing, inventory management, and security cameras. Hughes provides the network, the equipment, the monitoring, and the support as a single managed service. This is a stickier, higher-margin business than consumer broadband, and it is less vulnerable to Starlink's disruption.

Hughes also carries its own debt burden, including approximately one and a half billion dollars maturing in August 2026. The fate of this subsidiary is tightly linked to the broader corporate restructuring.

Private 5G and Network as a Service

Even after the shutdown of the public 5G network, EchoStar has retained capabilities in private 5G networking, an emerging market where companies, factories, and military installations deploy their own dedicated wireless networks. The pitch is "Network as a Service," providing enterprises with the coverage and capacity of a cellular network without the complexity of building and operating one themselves. This business is small today, but it represents one potential path for EchoStar to monetize its remaining spectrum and network expertise in a capital-light model.

VII. The Playbook: Strategic Analysis

Hamilton Helmer's 7 Powers

The EchoStar story is best understood through the lens of Hamilton Helmer's "7 Powers" framework, which identifies the sources of durable competitive advantage.

Cornered Resource has always been EchoStar's primary power. Wireless spectrum is the textbook example of a cornered resource. It is finite, government-allocated, and essential for any wireless business. You cannot build a wireless network without it, and the FCC is not making more. For two decades, Ergen accumulated this resource at prices that now look like generational bargains. The forty billion dollars in spectrum sales in 2025 validated the thesis: the spectrum was worth multiples of what Ergen paid for it.

But there is a critical nuance here. EchoStar has now sold most of its cornered resource. After the AT&T and SpaceX transactions close, the company's remaining sub-6 GHz spectrum portfolio drops to approximately seventy-six megahertz nationally, a fraction of what it once held and well behind T-Mobile's three hundred seventy-six megahertz, AT&T's three hundred fourteen megahertz (post-acquisition), and Verizon's two hundred seventy-nine megahertz. The cornered resource that defined EchoStar's investment thesis for twenty years is being liquidated.

Scale Economies apply to the Hughes satellite business, where the high fixed cost of launching and operating a geostationary satellite is spread across millions of subscribers and enterprise endpoints. Each additional subscriber added to the JUPITER fleet costs almost nothing in marginal terms. This is classic satellite economics, and it gives Hughes a cost advantage in markets where terrestrial broadband infrastructure is uneconomical.

Counter-Positioning was the theoretical power behind the Open RAN strategy. By using software-based infrastructure instead of proprietary hardware, EchoStar could theoretically have offered wholesale 5G services at significantly lower cost than AT&T or Verizon, whose legacy networks are built on expensive Ericsson and Nokia equipment. The incumbents could not easily switch to Open RAN because doing so would cannibalize their existing vendor relationships and require massive retraining. This power was never fully realized because the network was shut down before it achieved commercial scale.

Porter's Five Forces

Threat of New Entrants in the wireless industry remains extremely low. The barrier to entry is not just the billions of dollars required for spectrum, but the physical infrastructure, regulatory approvals, and decade of operational experience needed to build and run a national network. EchoStar's own failed attempt to become a fourth carrier, despite spending more than thirty billion dollars on spectrum alone, demonstrates how formidable these barriers are. Even with the assets, execution proved nearly impossible.

Bargaining Power of Buyers is high in the consumer wireless market. Consumers can switch carriers with relative ease, particularly in the prepaid segment. This is precisely why EchoStar's Boost Mobile subscriber base eroded so rapidly. The shift toward enterprise customers, wholesale arrangements, and managed services through Hughes represents a strategic pivot toward buyer segments with higher switching costs and less price sensitivity.

Rivalry Among Existing Competitors is intense and growing. T-Mobile has emerged as the clear winner of the wireless wars, using its Sprint spectrum acquisition to build the largest mid-band 5G network in the country. AT&T, once it absorbs EchoStar's spectrum, will significantly close the gap. Verizon continues to invest heavily in C-band deployment. The competitive landscape that EchoStar was supposed to disrupt has instead consolidated further.

Threat of Substitutes is evolving. For Hughes' satellite broadband business, Starlink represents a genuine substitution threat in the consumer segment, though less so in the enterprise segment where managed services and SLAs matter more. For wireless service, Wi-Fi offloading and fixed wireless access represent partial substitutes, though cellular networks remain dominant for mobile connectivity.

Bargaining Power of Suppliers is a factor that cut both ways for EchoStar. The company's Open RAN approach was explicitly designed to reduce supplier power by using multiple vendors and open-source software. But when the company declared force majeure on vendor contracts in 2025, it damaged relationships across the tower and equipment vendor ecosystem, potentially increasing supplier reluctance to work with EchoStar in the future.

VIII. Bear vs. Bull Case

The Bear Case: The Debt Wall

The bear case for EchoStar is straightforward and terrifying: the company owes more than thirty billion dollars in total debt, and the proceeds from the spectrum sales may not arrive before the next major maturities hit.

The numbers tell the story. EchoStar's consolidated debt stood at approximately thirty-one billion dollars at the end of 2025. Cash on hand was roughly one point nine billion dollars. Free cash flow for fiscal 2025 was negative one billion dollars. KPMG's going concern warning was not a formality; it was a genuine expression of doubt about the company's ability to continue operating.

The forty billion dollars in combined spectrum sales to AT&T and SpaceX would, if completed, more than cover the debt. But "if completed" is doing an enormous amount of work in that sentence. Both transactions require regulatory approval from the FCC and potentially the DOJ. The AT&T deal is expected to close around mid-2026. The SpaceX transaction, involving Elon Musk's increasingly controversial empire, could face additional regulatory scrutiny. If either transaction is delayed, blocked, or renegotiated, EchoStar faces approximately two billion dollars in debt maturing in July 2026 and another one point four billion at Hughes in August 2026. A failure to meet these obligations could trigger cross-default provisions that would accelerate approximately thirty billion dollars in total debt, almost certainly forcing a bankruptcy filing.

There is also the "melting ice cube" problem. DISH's satellite television business, which once served more than fourteen million subscribers, has been in structural decline for over a decade. The cord-cutting trend is accelerating. Every quarter, DISH loses hundreds of thousands of subscribers who leave for streaming services. The cash flow from satellite TV, which was supposed to fund the transition to wireless, is shrinking. The company reported revenue of fifteen billion dollars in fiscal 2025, down from eighteen point six billion in 2022. The trajectory is clear, and it points in one direction.

Finally, the impairment charge. EchoStar recorded a twenty-three-billion-dollar net loss in fiscal 2025, driven primarily by a sixteen-billion-dollar write-down of 5G network assets. While impairment charges are non-cash accounting entries, they represent a formal acknowledgment that billions of dollars in capital investment were destroyed. The write-down reduced total assets from sixty-one billion to forty-three billion dollars and slashed stockholders' equity from twenty billion to five point eight billion. The balance sheet now looks far more precarious than it did a year ago.

The Bull Case: The Spectrum Arbitrage

The bull case is equally compelling. Charlie Ergen may have executed one of the most successful asset accumulation and monetization strategies in corporate history.

Consider the math. Over two decades, EchoStar and DISH spent approximately twenty to thirty billion dollars acquiring wireless spectrum through FCC auctions and private purchases. In 2025, they agreed to sell a portion of that spectrum for forty billion dollars. Even after accounting for the costs of the failed 5G build-out, the interest on the debt used to finance the spectrum purchases, and the operational losses along the way, the net return on the spectrum investment is potentially in the tens of billions of dollars.

Some analysts have estimated that EchoStar's total spectrum portfolio, including the portions being retained, was worth sixty to eighty billion dollars at peak market prices. The enterprise value of the company before the spectrum sale announcements was a fraction of that figure. This "sum of the parts" discount was the core of the bull thesis that drove the stock from under seven dollars in mid-2023 to over a hundred dollars by early 2026, an increase of roughly fifteen times.

If the spectrum sales close on schedule, EchoStar will be transformed. The debt can be largely retired. The remaining company, built around Hughes satellite broadband, the Boost Mobile MVNO business, remaining spectrum holdings, and EchoStar's satellite infrastructure, would be far smaller but also far cleaner. The "new" EchoStar would have a strong enterprise connectivity business in Hughes, a consumer wireless brand in Boost with over seven million subscribers, and no longer be crushed under the weight of impossible debt maturities.

The stock price, which has rallied dramatically on the spectrum sale announcements, reflects this optimism. But it also reflects a significant amount of execution risk. The market is pricing in a successful completion of two of the largest spectrum transactions in history, a complex corporate restructuring, and a resolution of vendor disputes and regulatory investigations, all within the next twelve months.

The KPIs That Matter

For investors tracking EchoStar's ongoing performance, two metrics matter above all others.

First: Spectrum Sale Closing Timeline. Nothing else matters until the AT&T and SpaceX transactions close and proceeds are received. Every quarterly update, every investor presentation, every earnings call should be evaluated primarily through the lens of whether these deals are on track. Any regulatory delay, renegotiation of terms, or change in the political environment that affects FCC approvals is material to the thesis.

Second: Hughes Subscriber and Revenue Trends. Once the debt is resolved, Hughes becomes the core operating asset. Investors should track residential subscriber counts, enterprise site counts, and average revenue per user across both segments. The trajectory of these numbers will determine whether the "new" EchoStar can generate sufficient cash flow to justify its post-restructuring valuation and compete effectively against Starlink and terrestrial broadband alternatives.

IX. Conclusion: The Narrative Arc

The EchoStar story is, at its core, a story about the relationship between patience and leverage. Charlie Ergen spent forty years building a portfolio of scarce assets, enduring decades of criticism, stock price declines, and near-death corporate experiences along the way. He did this with the conviction of a card counter who knows the math is on his side, even when the table is cold.

The "Dish Wars" of the 1990s and 2000s, when Ergen battled cable companies and DirecTV for satellite television supremacy, were the opening act. The "Spectrum Wars" of the 2010s and 2020s, when Ergen outmaneuvered the major carriers to build the largest private spectrum portfolio in America, were the main event. And the denouement, the forty-billion-dollar spectrum liquidation of 2025, may prove to be one of the most profitable asset trades in American corporate history.

Or it may not. The deals have not closed. The debt has not been retired. The regulatory approvals have not been granted. The vendor lawsuits have not been settled. KPMG's going concern warning remains on the most recent filing. Between here and resolution lies a minefield of execution risk that could derail the entire plan.

What is beyond dispute is the audacity of the attempt. In an era of corporate bureaucrats, quarterly earnings management, and risk-averse institutional decision-making, Ergen built and ran EchoStar like a personal fiefdom, making bets that would have been inconceivable at any conventionally governed public company. The dual-class share structure that gave him this freedom is the same structure that made his shareholders captive passengers on a ride they could not control. Whether that ride ends at the winner's circle or the bankruptcy court will be determined in the months ahead.

EchoStar is the last of the great founder-led telecom companies in an era of professional managers. Whether Ergen's legacy is that of a visionary capital allocator or a gambler who pushed his luck one hand too far depends on events that have not yet occurred. The cards are still being dealt.

X. Epilogue: The Latest Hand

As of early 2026, the regulatory clock is ticking. The AT&T spectrum transaction is expected to close around mid-2026, with FCC review ongoing. The SpaceX deal faces its own regulatory timeline. EchoStar's exchange offers on approximately four point seven billion dollars in 2025 and 2026 notes achieved over ninety-six percent participation, extending maturities to 2029 and reducing near-term obligations to roughly one hundred thirty-nine million. This bought time, but not certainty.

The Boost Mobile brand continues to operate as an MVNO on AT&T's network, serving approximately seven and a half million subscribers. Hughes continues to provide satellite broadband and managed enterprise connectivity to its installed base, with JUPITER-3 providing substantially increased capacity. The FCC ended its investigation into EchoStar's spectrum utilization after the company agreed to sell its spectrum, removing one regulatory overhang.

Charlie Ergen, seventy-three years old, is back in the CEO seat. Jim DeFranco, his partner from the Lake Tahoe blackjack tables, remains at the company. The corporate headquarters in Englewood, Colorado, remain as spartan as ever. The culture has not changed. The stakes, however, have never been higher.

This is the perfect example of what might be called "complexity investing." The company is nearly impossible to model with a standard discounted cash flow analysis. The value resides not in operating earnings but in asset monetization, regulatory outcomes, and corporate restructuring, domains where traditional financial analysis yields to game theory, legal analysis, and the judgment of a single controlling shareholder. For investors comfortable navigating that complexity, EchoStar presents a genuinely asymmetric situation. For those who are not, the volatility of the past three years, a stock that moved from seven dollars to over a hundred and thirty dollars and back, offers a clear warning about the price of admission.

The professional poker player from Oak Ridge, Tennessee, is still at the table. He always has been.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube