Sanmina Corporation: From Silicon Valley Startup to Global EMS Powerhouse

I. Introduction & Episode Roadmap

Picture a business where your operating margins hover around five or six percent on a good day, your largest customers wield immense bargaining power, your competitors range from a Taiwanese giant with nine hundred thousand employees to scrappy regional shops, and one bad quarter can wipe out a year's worth of profits. Now imagine surviving in that business for forty-five years, outlasting nearly every peer that started alongside you, and emerging on the other side as a seven-billion-dollar-plus revenue company with operations spanning six continents. That is the story of Sanmina Corporation.

Sanmina is one of the world's leading Electronics Manufacturing Services providers and Original Design Manufacturers, with more than twenty thousand employees operating out of nearly eighty manufacturing facilities across twenty-three countries. The company designs, manufactures, and repairs some of the most complex electronic products on earth, serving customers in cloud infrastructure, defense and aerospace, medical devices, industrial automation, and automotive electronics.

In its most recent fiscal quarter, revenue surged fifty-nine percent year over year to three-point-two billion dollars, fueled by its transformative acquisition of ZT Systems' data center infrastructure business from AMD. Just yesterday, on March 12, 2026, the stock plunged twenty percent after cautious forward guidance rattled investors. That kind of single-day volatility tells you everything about the market Sanmina operates in: a business where the gap between stellar execution and investor disappointment is measured in basis points of margin.

The central question of this deep dive is deceptively simple: How did a 1980 Silicon Valley contract manufacturer, founded by two Croatian immigrants with a passion for printed circuit boards, survive when almost all its peers either failed, got acquired, or faded into irrelevance?

The answer involves a masterclass in consolidation strategy, vertical integration, customer diversification born of near-death experience, and a prescient bet on manufacturing geography that the China-plus-one megatrend would validate decades later.

What makes Sanmina's story particularly compelling for investors and business students alike is that the company operates in what might be the most brutally competitive segment of the technology supply chain. Electronics manufacturing services is a business where the product is essentially someone else's product. Your customer can always threaten to bring manufacturing back in-house or switch to a cheaper provider. A single customer loss can crater your utilization rates overnight.

Sanmina has navigated all of these hazards and emerged as perhaps the most vertically integrated of the major Western EMS players, a distinction that increasingly looks like a genuine competitive advantage rather than a capital-intensive liability.

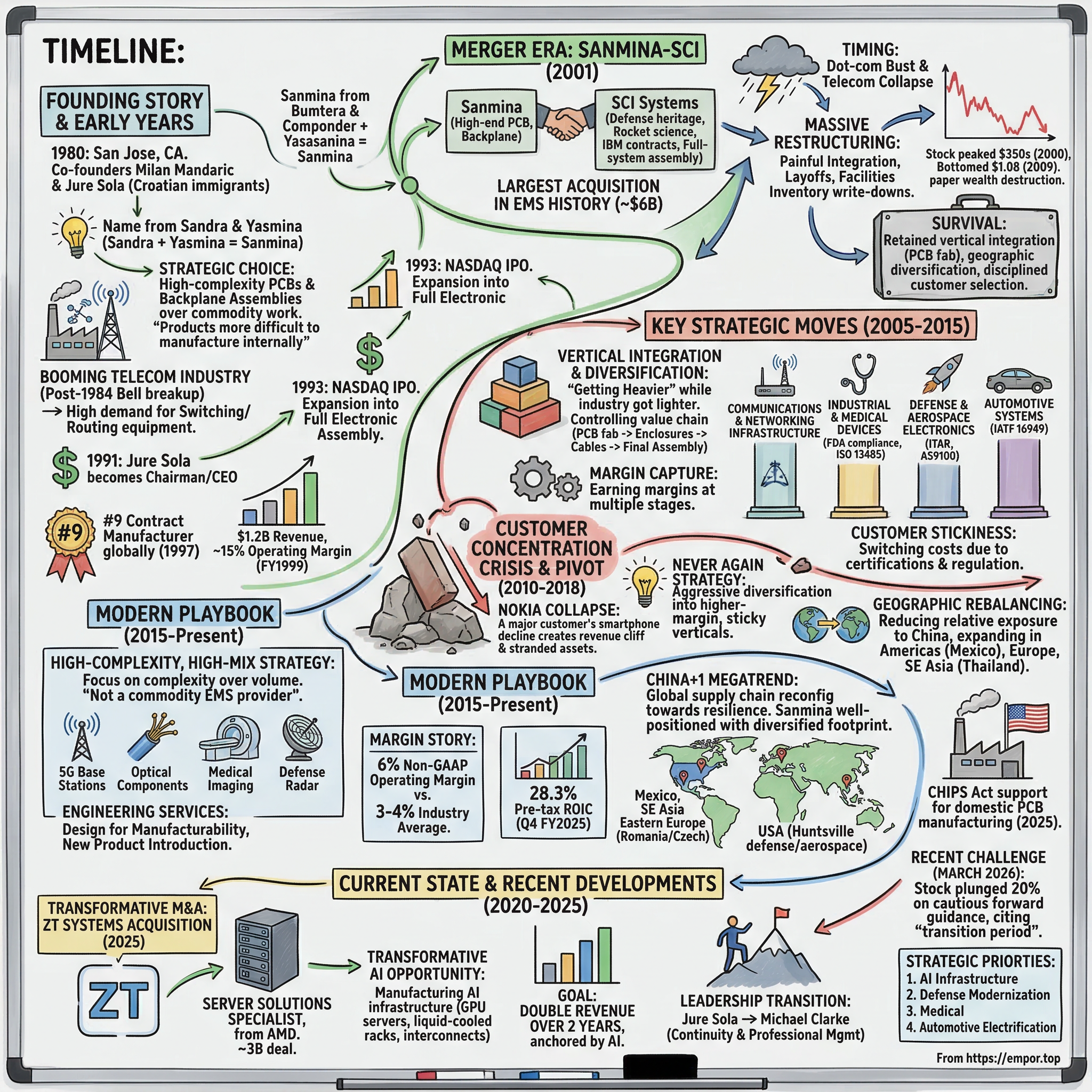

II. Founding Story & Early Years (1980-1995)

In 1969, a twenty-one-year-old Croatian named Milan Mandaric stepped off a plane in California carrying little more than ambition and the memory of a communist government that had grown hostile to his success. Back in Yugoslavia, Mandaric had taken control of his father's machine shop at age twenty-one and by twenty-six had built it into one of the largest private businesses in the country. Under Tito's communist regime, that kind of entrepreneurial achievement made you a political target rather than a hero. Mandaric packed up his family and left for the United States, settling in the heart of what would become Silicon Valley.

Within two years, Mandaric founded Lika Corporation, named after his home region in Croatia. The company manufactured computer components and printed circuit boards during the dawn of the microprocessor era. Mandaric had an extraordinary eye for emerging demand. By 1976, Lika Corporation was reportedly the largest manufacturer of computer components in the United States. Perhaps most remarkably, Mandaric secured one of Apple's very first manufacturing contracts, making Lika an early partner to Steve Jobs and Steve Wozniak during their garage-to-empire days. In 1980, Mandaric sold Lika to Tandy Corporation, the parent company of RadioShack, for a significant return.

Enter Jure Sola. Born in Croatia in 1951, Sola had emigrated to the United States at seventeen, just a year before Mandaric arrived. Sola pursued engineering at San Jose State University, graduating in 1972, and then went to work at Mandaric's Lika Corporation. For eight years, Sola absorbed everything about electronics manufacturing, from transducers and control instruments to factory automation. When Mandaric sold Lika, the two men had an idea for their next venture.

In 1980, Mandaric and Sola co-founded Sanmina Corporation in San Jose, California. The company name came from Mandaric's two daughters: Aleksandra, called Sandra, and Yasmina. Take "San" from Sandra and "mina" from Yasmina, and you get Sanmina. It was a personal touch in what would become a very large industrial enterprise.

From day one, Sanmina chose the hard path. Rather than chasing commodity printed circuit board work, the company focused on high-complexity PCBs and backplane assemblies, the intricate interconnect boards that allow multiple circuit cards to communicate within telecom and networking equipment. As Sola later explained the philosophy: "We go after the products that are more difficult to manufacture internally." This was a deliberate strategy to avoid competing on price alone and instead compete on engineering capability and manufacturing precision.

By 1981, just a year after founding, Sanmina began manufacturing backplane assemblies. For those unfamiliar with the term, a backplane is essentially a large circuit board that acts as the nervous system inside a piece of telecom or networking equipment. It connects all the other circuit boards together, carrying signals and power between them. Think of it as the highway system inside a router or a telephone switch. Backplanes are notoriously difficult to manufacture because they are large, multilayered, and require extremely precise signal routing to maintain integrity at high data speeds. Companies that could build reliable backplanes commanded premium prices and earned customer loyalty that simpler board fabricators could not match.

Throughout the 1980s, the company expanded steadily by serving the booming telecommunications industry, which was undergoing massive infrastructure investment following the 1984 Bell System breakup. The court-ordered dismemberment of AT&T into regional Bell operating companies created an explosion of demand for new switching and routing equipment, and every one of those systems needed backplanes and complex PCBs. Sanmina rode this wave expertly.

Sola became Chairman and CEO in 1991 as Mandaric stepped back from daily operations to pursue other interests. Mandaric had always been a serial entrepreneur at heart, and his attention turned to European football, where he would go on to own Portsmouth FC, Leicester City FC, and Sheffield Wednesday FC in England, as well as clubs in Belgium, France, and his native Serbia. His path from Yugoslav machine shop to Silicon Valley pioneer to English Premier League chairman is one of the more extraordinary entrepreneurial journeys in modern business history.

The IPO came on April 14, 1993, when Sanmina listed on the NASDAQ. The timing was propitious. The EMS industry was about to enter its explosive growth phase, and Sanmina needed capital to participate. In October 1993, the company expanded beyond bare PCB and backplane fabrication into full electronic assembly and turnkey manufacturing services, a pivotal strategic step that took Sanmina from being a component supplier to an integrated manufacturing partner. By 1997, Sanmina ranked ninth among contract manufacturers globally. By fiscal 1999, revenue had reached $1.2 billion with approximately fifteen percent operating margins, a figure that would have made peers green with envy and that reflected the premium pricing power that came from specializing in complex, difficult-to-manufacture products.

Milan Mandaric passed away on October 4, 2025, at age eighty-seven in Belgrade, Serbia, after a short illness. He left behind a legacy as one of Silicon Valley's pioneering electronics manufacturers, a man who escaped communist Yugoslavia with nothing and built companies that helped create the modern electronics supply chain. For investors, Sanmina's founding DNA matters because the company's emphasis on complexity and engineering excellence, established in those earliest years, remains its strategic North Star four and a half decades later.

III. The EMS Industry Gold Rush & Competitive Landscape (Mid-1990s)

The 1990s represent one of the most dramatic structural shifts in modern manufacturing history. Across the technology industry, a simple but powerful idea took hold: why should companies that design brilliant products also own the factories that build them?

The logic was compelling. Electronics manufacturing required massive capital investment in surface-mount technology lines, wave soldering equipment, testing infrastructure, and clean room facilities. An EMS provider could spread those fixed costs across dozens of customers. OEMs could convert manufacturing from a fixed cost to a variable cost, freeing capital for research and development, sales, and marketing.

Wall Street loved the asset-light model, rewarding OEMs that shed their factories with higher stock multiples. The message from analysts was clear: design products, outsource manufacturing, and watch your return on assets soar. It was a seductive proposition, and one that an entire generation of technology executives embraced.

The outsourcing wave accelerated through the decade. Lucent Technologies announced plans to sell most of its twenty-nine manufacturing facilities. Nortel Networks outsourced several manufacturing operations. Ericsson, IBM, and Hewlett-Packard all divested assembly plants to contract manufacturers. Each divestiture validated the model further and created a virtuous cycle: as EMS companies grew larger, they could invest in better equipment and processes, making them even more attractive to the next round of OEM customers.

The competitive landscape was crowded and fierce. Solectron Corporation, founded in 1977 in Milpitas, California, was the industry's poster child. Led by Dr. Winston Chen, Solectron won the Malcolm Baldrige National Quality Award twice, in 1991 and 1997, the first manufacturer to achieve that distinction. Revenue grew from $265 million in 1991 to nearly four billion dollars by 1997.

Flextronics International, which received Sequoia Capital funding in 1993, grew revenues at an average of forty-eight percent annually through the decade. Celestica, spun out of IBM's Canadian manufacturing operations, quickly became a top-tier player. Jabil Circuit was rising fast. And SCI Systems in Huntsville, Alabama, with its defense heritage and IBM contracts, ranked among the largest contract manufacturers in the world.

It was a genuine gold rush. Investors poured money into EMS stocks, and the companies used their inflated stock prices as currency to make acquisitions, which drove revenue growth, which drove stock prices higher, creating a feedback loop that would eventually prove unsustainable.

At its core, the EMS business model is deceptively simple and brutally difficult. You buy components on behalf of your customer, assemble them into finished products using specialized equipment, test them, and ship them out. Your margin comes from the conversion fee, the value you add through manufacturing expertise. Typical operating margins range from two to six percent. Working capital intensity is punishing because you carry enormous inventories of components, often on behalf of customers who can cancel orders with relatively short notice. The business rewards scale, operational discipline, and supply chain management prowess, but offers little room for error.

To understand why this matters, consider what "surface-mount technology" actually involves. Imagine placing components the size of a grain of sand, with connector pins spaced fractions of a millimeter apart, onto a printed circuit board at speeds of tens of thousands of placements per hour. The equipment to do this costs millions of dollars per line. You need automated optical inspection systems to verify placement accuracy, reflow ovens precisely calibrated to melt solder at exactly the right temperature profile, and testing equipment that can verify functionality at the board level and the system level. The capital investment is enormous, the engineering knowledge required to manage these processes is deep, and the consequences of errors, including scrap, rework, and customer warranty claims, are financially punishing at these margins.

Sanmina's early strategic choice to focus on high-mix, low-volume work, the complex telecom and networking equipment where engineering difficulty creates natural barriers, proved prescient. In high-volume manufacturing, the same product runs for weeks or months on a single production line. Changeovers are infrequent, and efficiency comes from repetition. In high-mix manufacturing, the production line might run a different product every few hours or even every few units. Each changeover requires reprogramming pick-and-place machines, changing solder stencils, reconfiguring test fixtures, and verifying first-article quality. This is fundamentally harder than high-volume work, and it is precisely the complexity that keeps commodity assemblers out and protects margins.

While competitors raced to build massive factories in China and Southeast Asia for high-volume consumer electronics assembly, Sanmina built its reputation on the products that were genuinely hard to manufacture. The strategic divergence that emerged in the 1990s, commodity scale versus engineering complexity, would determine which companies survived the coming crash and which did not.

IV. The Merger Era: Sanmina-SCI (2001)

To understand the SCI Systems acquisition, you first need to understand what SCI was, because this was no ordinary target. SCI Systems was born from rocket science, literally. In 1961, three engineers in Huntsville, Alabama, pooled $21,000 and set up shop in a basement. Their names were Olin B. King, Bill Greaver, and Joe Kirk, and they called their company Space Craft Inc. King had previously worked with Wernher von Braun on the U.S. satellite program at RCA. The company's original vision was to build components for the nascent space industry after President Eisenhower's 1959 announcement enabling private companies to own orbiting satellites.

SCI became a key NASA subcontractor, building subsystems for the Saturn V rocket, the Skylab space station, Titan III missiles, and Poseidon submarine-launched ballistic missiles. The company went public in 1966. After the Apollo program ended in 1972, SCI pivoted to military contracts, supplying electronics for Pershing missiles, the MX missile system, and F-15, F-16, and F-18 fighter aircraft. Then came the contract that changed everything: in 1976, IBM hired SCI to manufacture desktop terminal subassemblies. Revenue exploded from $2.5 million in 1978 to $45 million in 1981. By 1987, IBM contracts represented roughly forty percent of SCI's revenue, and SCI had become a Fortune 500 company. Revenue crossed one billion dollars in 1990.

Before the SCI deal, Sanmina set the stage with another major acquisition. In April 2000, the company acquired Hadco Corporation, a major PCB fabrication company based in New Hampshire, for $1.3 billion in stock. Hadco brought manufacturing operations in Phoenix, Santa Clara, Loveland, Austin, and Malaysia, and firmly established Sanmina as the global leader in PCB fabrication technology.

Then came the big one. On July 16, 2001, Sanmina and SCI announced a definitive merger agreement. Each share of SCI common stock would convert into 1.36 shares of Sanmina stock, valuing the transaction at approximately six billion dollars including debt assumption. It was the largest acquisition in EMS industry history. The strategic logic was clear: Sanmina was the master of high-end PCB fabrication and backplane manufacturing, but it lacked full-system assembly capabilities. SCI brought exactly those capabilities, plus a defense electronics heritage that would prove invaluable decades later. As Sola explained: "We built the company to a certain level with niche technology, but we needed to have the fundamentals of system assembly in place."

There was a curious wrinkle to the deal structure. Sanmina was only about half the size of SCI at the time, yet Sanmina was the acquirer. The reason was financial positioning. Sanmina's core telecommunications business was performing well and generating strong cash flow, while SCI's lower-margin businesses, particularly personal computer manufacturing, were struggling. Sanmina had the currency, in the form of its still-valuable stock, to make the deal happen.

The merger closed on December 6, 2001, and the combined company was renamed Sanmina-SCI Corporation. Sola became Co-Chairman and CEO, while SCI's longtime leader A. Eugene Sapp Jr. became Co-Chairman. The projected synergies were $150 to $200 million in annual savings, and the combined entity would have approximately twelve billion dollars in annual revenue.

The timing could not have been worse. The deal closed right into the teeth of the dot-com bust and telecom collapse. On a pro forma basis, combined revenue fell 21.1 percent from $12.7 billion to $10.0 billion in fiscal 2002. The communications sector, which had been Sanmina's bread and butter, was in freefall.

The restructuring was massive and painful. The company announced two restructuring plans: Phase One contemplated approximately $730 million in restructuring costs, and Phase Two, announced in October 2002, added up to $250 million more. Nearly a billion dollars in combined restructuring charges. Facilities were shuttered across multiple continents. Thousands of employees were laid off. Raw materials inventory worth $152.6 million was written down as components that were purchased for products that would never be built became worthless.

Sanmina's stock chart tells the most dramatic version of the story. Shares had peaked at approximately $354 to $363 in August through October 2000, during the height of the bubble. They would eventually bottom at $1.08 on March 9, 2009, a decline of more than ninety-nine percent from peak to trough. An investor who bought at the peak and held through the trough would have lost virtually everything. The paper wealth destruction was staggering, and it taught an entire generation of EMS investors about the cyclical risks inherent in the business model.

Yet Sola's vision held. The combined company had the scale, the geographic footprint, and the vertical integration to survive what many competitors could not. Consider the counterfactual: had Sanmina not acquired SCI, it would have remained a roughly five-billion-dollar PCB and backplane specialist when the telecom market collapsed. Without SCI's diversified customer base spanning defense, industrial, and consumer electronics, the revenue decline would have been even more severe. Without SCI's system assembly capabilities, Sanmina could not have moved up the value chain into higher-margin, full-system manufacturing. The merger, painful as it was, gave Sanmina the foundation for everything that followed.

The cultural integration was perhaps the most underappreciated challenge. Sanmina was a Silicon Valley company: fast-moving, engineering-driven, with a startup's bias toward innovation and risk-taking. SCI was a Huntsville defense contractor: methodical, process-oriented, with a culture shaped by decades of military specifications and government oversight. Merging these cultures required patience and pragmatism. Sola kept many of SCI's senior managers in place, recognizing that defense manufacturing expertise was not something you could import from Silicon Valley. The Huntsville operation retained significant operational autonomy, which proved critical for maintaining security clearances and customer trust.

The "SCI" name was eventually dropped, and the company became simply Sanmina Corporation again, a brand consolidation that signaled the integration was complete and it was time to move forward. The SCI Technology subsidiary in Huntsville, Alabama, continues to operate as a Sanmina company, still building defense electronics for avionics, tactical communications, and counter-drone systems, a direct line back to those rocket engineers in Olin King's basement. For investors evaluating the ZT Systems acquisition today, the SCI merger provides the most relevant historical precedent: a transformative deal, executed at a challenging moment, that required years of painful integration but ultimately created the platform for long-term survival and growth.

V. The Great EMS Shakeout (2001-2008)

The dot-com bust and telecom crash of 2001 through 2003 represented an extinction-level event for the EMS industry. The sector had expanded at breakneck speed through the late 1990s, adding factory capacity, hiring tens of thousands of workers, and accumulating enormous component inventories based on customer forecasts that assumed demand would keep rising forever. When demand collapsed virtually overnight, the industry was caught holding the bag.

The underlying problem was structural and devastating. EMS companies had become enormous repositories of risk. Here is how the cycle worked: OEM customers would provide demand forecasts, often inflated during boom times by optimistic sales projections. EMS providers would purchase components based on those forecasts, locking up billions of dollars in inventory. When demand collapsed, the OEMs would cancel or defer orders, but the EMS providers were left holding components that were now worth a fraction of their purchase price, if they were worth anything at all. The EMS industry had essentially become the shock absorber for the entire technology supply chain, absorbing the impact of demand volatility that OEMs had outsourced along with their manufacturing.

The numbers were staggering. EMS companies' combined inventory ratio ballooned to over seventy percent of revenue from below fifty percent in 1999. Flextronics saw its inventory ratio double. The global semiconductor market plunged thirty-two percent in 2001, sending shockwaves through the entire electronics supply chain. Most EMS companies had not become significant players until the 1990s and had never experienced a major downturn. The previous double-digit semiconductor decline had been in 1985, before most of these companies had achieved meaningful scale. They had built their business plans, their capacity expansion, and their investor narratives around the assumption of perpetual growth. When that assumption proved wrong, the consequences were catastrophic.

No company embodied the rise and fall more dramatically than Solectron. The two-time Baldrige Award winner had peaked at $18.7 billion in revenue with as many as 114,000 employees globally. Then it fell apart.

Fiscal 2001 brought a net loss of $123.5 million and restructuring charges exceeding $500 million. Over forty thousand positions were eliminated by early 2003. Pre-tax restructuring charges exceeded $1.1 billion across fiscal 2001 and 2002. Facilities closed across Georgia, Australia, Washington State, and Ireland.

Solectron attempted to reposition toward higher-value services, acquiring Stream International for $367 million to build after-market repair capabilities. But industry observers described the turnaround as a "never-ending saga." The company could never achieve gross margin leverage in a market with too much capacity and too little demand. The fundamental problem was that Solectron had grown through acquisitions funded by an inflated stock price, and when the stock price collapsed, the debt remained while the revenue evaporated.

On June 4, 2007, Flextronics announced its acquisition of Solectron for approximately $3.6 billion in equity value, a small fraction of what Solectron had been worth at its peak. The deal closed on October 1, 2007, the eve of Solectron's thirtieth anniversary. It was an ignominious end for what had once been the crown jewel of the EMS industry.

Sanmina's survival playbook during this carnage had several key elements. First, Jure Sola made the counterintuitive decision to retain PCB fabrication capabilities when many competitors were divesting them as "non-core." Industry analyst Pamela Gordon of Technology Forecasters praised this decision. While rivals shed vertical capabilities to shore up short-term balance sheets, Sanmina held onto the assets that would differentiate it long-term. Second, the company engaged in aggressive facility consolidation, closing underperforming plants while retaining strategic manufacturing locations in the United States and Western Europe for higher-value-added work. Third, Sola maintained disciplined customer selection, preferring complex, high-mix programs over commodity volume.

The industry that emerged from the shakeout looked fundamentally different from the one that entered it. Foxconn, the Taiwanese giant, had risen to dominance on the strength of Apple and other consumer electronics contracts, growing to become the world's largest EMS provider with over forty percent market share and revenues that would eventually exceed two hundred billion dollars. Among Western EMS providers, Flextronics (later renamed Flex) had absorbed Solectron to become the largest, with combined operations spanning more than thirty countries and over two hundred thousand employees. Jabil continued to grow through disciplined expansion. Celestica contracted painfully but survived. Smaller players like Avex and Bull Electronics were absorbed by larger competitors.

And Sanmina, battered but intact, began repositioning for the next phase. By fiscal year ending September 2006, the combined Sanmina-SCI generated $10.4 billion in revenues across operations in eighteen countries on five continents. The company that had entered the decade as a high-end PCB fabricator with nine hundred million dollars in revenue had become a ten-billion-dollar diversified manufacturer. The price of that transformation was enormous: restructuring charges approaching a billion dollars, a stock price that had lost more than ninety-five percent of its peak value, and thousands of lost jobs. But Sanmina was still standing, and many of its former peers were not.

The survivors learned a painful lesson: in a business with razor-thin margins, the difference between survival and extinction comes down to discipline, differentiation, and the willingness to endure years of pain without abandoning your strategic convictions. This period also revealed a deeper truth about the EMS business model: the companies that tried to be everything to everyone, chasing volume at the expense of margin and stretching their capabilities across too many end markets, were the ones that broke under the strain. The survivors were the ones that knew what they were, knew what they were good at, and had the discipline to stay in their lane even when the temptation to chase easy revenue was overwhelming.

VI. Key Strategic Moves: Vertical Integration & Diversification (2005-2015)

While the rest of the EMS industry was racing to become lighter, leaner, and more focused on pure assembly, Sanmina under Jure Sola was doing something that looked almost contrarian: getting heavier. The company was building out an integrated manufacturing ecosystem that encompassed PCB fabrication, backplane assembly, enclosures, cable assemblies, mechanical systems, and optical components. The strategy was to control as much of the value chain as possible, capturing margin at multiple stages rather than just at the final assembly step.

Think of it this way. In a traditional EMS model, you buy a printed circuit board from a board fabricator, buy an enclosure from a metal shop, buy cable assemblies from a cable house, then assemble everything together and ship it to the customer. Your margin is only on that final assembly and test step. In Sanmina's model, the company fabricates the PCB internally, builds the enclosure internally, manufactures the cable assemblies internally, and then performs the final assembly. Margin accrues at every stage. By fiscal 2025, this approach was clearly visible in the financials: Sanmina's Components, Products, and Services segment generated $448 million in quarterly revenue at a 14.5 percent non-GAAP gross margin, dramatically higher than the 7.8 percent gross margin in its assembly-oriented Integrated Manufacturing Solutions segment. The components business, in other words, was running at roughly double the margin of the assembly business.

The company also built deep sector-specific expertise during this period. Rather than being a generalist assembler that would build anything for anyone, Sanmina developed specialized capabilities in four key verticals: communications and networking infrastructure, industrial and medical devices, defense and aerospace electronics, and automotive systems.

Each vertical required different certifications, different quality systems, and different engineering competencies. Medical devices demanded ISO 13485 certification and FDA compliance, meaning that every manufacturing process had to be validated, documented, and auditable by government regulators. Aerospace required AS9100 certification. Automotive needed IATF 16949, the quality management system standard for the automotive supply chain.

These certifications take years to obtain and maintain, creating meaningful switching costs for customers who might otherwise be tempted to move production to a cheaper provider. A medical device OEM cannot simply move its production to the lowest bidder; the new manufacturer must first demonstrate compliance with the same regulatory standards, a process that can take twelve to eighteen months and cost millions of dollars. This is the kind of structural friction that creates genuine customer stickiness in an industry where loyalty is otherwise measured in cents per unit.

The risk of this approach was real and substantial. Vertical integration in a low-margin business means committing capital to factories and equipment that must be kept running at high utilization to earn acceptable returns. If demand drops or a major customer leaves, you are stuck with expensive, specialized capacity that cannot easily be repurposed. Sola was essentially betting that the differentiation benefits of controlling the value chain would outweigh the capital intensity risks. It was a bet that required patience and conviction, because the payoff would not be immediate and the downside during cyclical troughs would be amplified.

The SCI Technology subsidiary in Huntsville, Alabama, became the cornerstone of Sanmina's defense and aerospace capabilities. With more than sixty years of heritage stretching back to the Saturn V rocket program, SCI Technology provided ITAR-compliant manufacturing for avionics, tactical communications, counter-drone systems, and space-flight programs. Huntsville was America's center for defense and aerospace excellence, and having a deeply embedded presence there gave Sanmina credibility with defense prime contractors that no amount of marketing could replicate.

By the end of this period, Sanmina had transformed from a PCB fabrication house with assembly capabilities into something much more comprehensive: an end-to-end design, manufacturing, and lifecycle services partner. The company could take a customer's product from initial concept through new product introduction, volume manufacturing, global logistics, and post-sale repair. This evolution from tactical supplier to strategic manufacturing partner was critical, because it moved customer relationships from transactional price negotiations toward longer-term partnerships where switching costs were genuinely high.

VII. Customer Concentration Crisis & Pivot (2010-2018)

Every EMS company lives with the nightmare scenario of customer concentration. When a significant portion of your revenue depends on a handful of customers, the loss of any one of them can be catastrophic. Sanmina learned this lesson in the most painful way possible during the 2010s when the collapse of Nokia's mobile phone business sent shockwaves through its customer base.

Nokia had been one of Sanmina's largest customers, generating substantial revenue through manufacturing contracts for the Finnish company's telecom infrastructure equipment. Nokia's story is well known: once the world's dominant mobile phone maker, the company was caught flat-footed by the iPhone's touchscreen revolution in 2007 and spent the next several years in a death spiral of market share loss, strategic missteps, and organizational paralysis. By 2013, Nokia had sold its Devices & Services division to Microsoft for $7.2 billion. But the impact on Nokia's supply chain was felt years before the Microsoft sale. As Nokia's volumes declined, manufacturing orders to EMS providers like Sanmina shrank correspondingly. What had been a reliable, high-volume revenue stream evaporated over the course of just a few years. For Sanmina, this meant a revenue cliff, a capacity utilization crisis, and the painful realization that being too dependent on any single customer or industry vertical was an existential risk.

The Nokia collapse was not unique in the EMS world. Celestica experienced a similar crisis with BlackBerry maker Research In Motion, which went from being one of the most important smartphone manufacturers in the world to a niche player in less than a decade. The pattern was consistent: EMS providers would invest in capacity and capabilities around a major customer, building dedicated manufacturing lines and hiring specialized workforces. When that customer's market position eroded, the EMS provider was left with stranded assets and a revenue hole that could not be quickly filled.

The broader telecommunications and networking sector compounded Sanmina's challenges during this period. Cisco shifted manufacturing strategies, moving more production to lower-cost locations. Ericsson restructured its supply chain across multiple rounds. The telecom equipment market consolidated as carriers reduced their vendor lists, meaning fewer OEM customers were placing orders. Each change created uncertainty and potential revenue loss for EMS providers that had built capacity around specific customer programs.

Sanmina's response was what management privately called a "never again" strategy. The company embarked on an aggressive customer diversification campaign, deliberately seeking business in verticals that had nothing to do with telecommunications.

Medical devices became a priority, offering the attractive combination of higher margins, regulatory barriers to entry, and long product lifecycles that created sticky customer relationships. A medical device might remain in production for ten to fifteen years, compared to two to three years for a consumer electronics product, providing much greater revenue visibility.

Industrial automation represented a growing market as factories worldwide adopted more sophisticated electronics for robotics, process control, and monitoring systems. Automotive electronics, driven by the proliferation of sensors, displays, and electronic control units in modern vehicles, offered secular growth. The average car contained approximately three thousand dollars worth of electronics content in 2015; by the mid-2020s, that figure had roughly doubled for internal combustion vehicles and was substantially higher for electric vehicles.

Defense electronics, already a strength through SCI Technology, received renewed emphasis as government spending on modernization increased following years of budget austerity.

The diversification was not easy or quick. Entering medical devices required obtaining ISO 13485 certification, building clean room facilities, and developing the quality documentation processes that FDA regulations demanded. Automotive required IATF 16949 certification and the ability to meet zero-defect quality standards across production volumes that ran for five to ten years. Defense required ITAR compliance, security clearances, and the patience to navigate the Pentagon's glacial procurement timelines. Each new vertical demanded years of investment before generating meaningful revenue.

Geographic rebalancing accompanied the customer diversification. Sanmina began reducing its relative exposure to China while building manufacturing presence in the Americas and Europe. The company invested in Mexico for automotive, medical, and industrial applications serving North American customers. Its Thailand facility, which had been supporting customers in the region for more than thirty years, received expanded capabilities for optical and radio frequency microelectronic assemblies. Facilities in Romania and the Czech Republic served European customers who wanted manufacturing closer to home.

The financial impact of the concentration crisis and subsequent diversification was felt for years. Revenue growth stalled. Margins compressed as the company invested in new capabilities while losing high-volume telecom work. But the strategy worked. By the end of this period, Sanmina's revenue base was meaningfully more diversified across end markets and customers. The company had set internal limits on customer concentration, ensuring that no single customer could again represent such a large share of revenue that its loss would threaten the enterprise.

For investors, the customer concentration crisis of 2010 through 2018 is the defining episode in understanding Sanmina's risk management philosophy. The company experienced what amounted to a near-death experience from customer loss and emerged with a fundamentally more resilient business model. That resilience would prove invaluable when the next set of challenges arrived.

VIII. The Modern Playbook: High-Complexity, High-Mix Strategy (2015-Present)

Walk into a Sanmina facility today and you will not find endless rows of identical smartphones being assembled at maximum speed. What you will find is something far more interesting: a medical imaging system being assembled in one bay, a defense radar subsystem being tested in another, optical transceivers for 5G networks being built in a third, and AI server racks being integrated in a fourth.

This is high-mix, low-volume manufacturing, and it is fundamentally different from the commodity assembly that dominates the EMS industry.

The repositioning narrative that Sanmina has pushed over the past decade can be summarized in a single sentence: "We are not a commodity EMS provider." Every strategic choice the company makes reinforces this positioning.

The focus areas reflect the most complex, engineering-intensive segments of electronics manufacturing. Optical components for cloud infrastructure require precision alignment at the micron level. Think about what that means: the fiber optic connections that carry data between servers in a data center depend on laser assemblies where the light source must be aligned to a glass fiber with an accuracy of a few millionths of a meter. If the alignment is off by even a tiny fraction, the signal degrades and the link fails.

5G base station electronics involve radio frequency engineering that demands specialized test equipment and expertise. Medical devices must meet regulatory standards where a manufacturing defect can literally cost lives, and the traceability requirements mean that every component, every solder joint, and every test result must be documented and auditable for the life of the product. Defense electronics require security clearances, environmental testing for extreme conditions, and the ability to maintain production lines for decades-old platforms alongside cutting-edge next-generation systems.

The engineering services emphasis has become a key differentiator. Sanmina offers New Product Introduction capabilities, where the company works with customers during the design phase to optimize products for manufacturability. This is enormously valuable because decisions made during design determine the vast majority of manufacturing cost. A product designed without manufacturing input might require specialized tooling, manual assembly steps, or exotic components that drive up cost. A product designed in collaboration with an EMS partner's manufacturing engineers can be optimized for automated assembly, standard components, and efficient test coverage. This "design for manufacturing" collaboration creates switching costs because the customer's product has literally been designed around Sanmina's manufacturing capabilities.

How does Sanmina stack up against its peers? The competitive landscape among Western EMS providers has consolidated into a clear set of differentiated players, each with a distinct strategic identity. Jabil, with roughly thirty billion dollars in revenue, has positioned itself as the diversified giant. In late 2023, Jabil divested its $2.2 billion Mobility business, primarily Apple-related manufacturing, to BYD Electronic, a decisive signal that the company was choosing margin over volume and pivoting toward AI infrastructure, healthcare, and automotive. Before the divestiture, Apple had accounted for as much as twenty-eight percent of Jabil's revenue, a concentration level that management decided was both risky and margin-dilutive. Post-divestiture, no single customer exceeds roughly sixteen percent of revenue.

Flex, at around twenty-five billion dollars, positions as a broad-based provider with particular strength in automotive and industrial applications, operating manufacturing sites in over thirty countries. Celestica, at roughly eight to ten billion dollars, has undergone perhaps the most dramatic strategic transformation in the EMS industry, repositioning itself as an AI and data center infrastructure specialist. Celestica's stock surged as investors rewarded this positioning, and its return on invested capital reached an industry-leading 37.5 percent, driven by its Hardware Platform Solutions business where it designs and sells its own networking and storage hardware rather than simply assembling other companies' products. Celestica's top two customers account for nearly forty percent of total revenue, however, highlighting the perennial concentration tension.

Sanmina, at around eight billion dollars standalone before the ZT Systems acquisition, occupies the vertical integration and high-complexity niche. Its differentiator is not scale, where Foxconn and Jabil are dominant, and not AI specialization, where Celestica has arguably staked the clearest claim. Sanmina's differentiator is the breadth of its internally manufactured components and the depth of its engineering services across multiple regulated verticals.

The margin story is where the rubber meets the road. Sanmina's non-GAAP operating margin of six percent puts it at the top of the EMS peer group. The industry average hovers around three to four percent for pure-play assembly providers.

That two to three percentage point gap might sound modest in absolute terms. It is not. On billions of dollars of revenue, it translates into hundreds of millions of dollars of additional operating income. At eight billion dollars of revenue, the difference between four percent and six percent operating margins is $160 million in annual operating profit. That is the difference between a company that generates adequate returns and one that can meaningfully invest in growth and return capital to shareholders.

The question investors must answer is whether this margin premium is sustainable or whether competitive pressures will erode it over time. Sanmina's vertical integration and certification-based switching costs suggest the premium has structural support, but the company must continuously invest to maintain its edge. The moment Sanmina stops investing in new capabilities, its differentiation begins to erode, and the business risks sliding back toward commodity margins.

IX. The China+1 Megatrend & Sanmina's Positioning (2018-Present)

If there is a single secular trend that has transformed Sanmina's competitive position more than any other over the past seven years, it is the global supply chain reconfiguration known as China-plus-one.

The concept is straightforward: companies that had concentrated manufacturing in China are diversifying to at least one additional country, driven by a convergence of trade tensions, pandemic supply chain disruptions, and geopolitical decoupling between the United States and China.

The inflection point came with the U.S.-China trade war that began in 2018 under the Trump administration. Tariffs on Chinese goods, initially ten percent and then escalating to twenty-five percent on many categories, suddenly made manufacturing there more expensive for products destined for the American market. Companies that had spent two decades optimizing their supply chains for Chinese production costs found themselves paying significant tariff penalties that erased the cost advantages they had worked so hard to capture.

Then COVID-19 struck in 2020, and the resulting supply chain chaos, with factory shutdowns, port congestion, and component shortages, demonstrated the catastrophic risk of geographic concentration. Companies that sourced everything from a single Chinese province suddenly had nothing. The geopolitical dimension intensified further as tensions over Taiwan raised the specter of a scenario where the world's most important chip manufacturing island could become the site of military conflict. For corporate risk managers, the message was impossible to ignore: supply chain concentration in any single country, no matter how cost-efficient, had become an unacceptable risk.

Sanmina found itself unusually well positioned for this shift. Unlike competitors who had aggressively concentrated capacity in China during the 2000s and 2010s to chase cost savings, Sanmina had maintained a genuinely diversified manufacturing footprint. The company had always operated significant capacity in the Americas, including multiple facilities in the United States and a growing presence in Mexico. Its European footprint included facilities in Romania, the Czech Republic, Germany, and Finland. In Asia, its presence was spread across Thailand, Malaysia, India, Israel, and other markets rather than concentrated solely in China.

Mexico has emerged as the biggest geographic winner of the nearshoring trend, and Sanmina has been a direct beneficiary. The country offers proximity to the U.S. market, competitive labor costs, USMCA trade agreement benefits, and an increasingly skilled manufacturing workforce. Sanmina's Mexican operations serve the automotive, medical, and industrial sectors. For customers who need products manufactured in North America for regulatory, security, or logistics reasons, Sanmina's Mexican footprint offers an immediately available alternative to Chinese production without requiring the years-long lead time of building greenfield capacity.

Southeast Asia represents another key pillar. Sanmina's Thailand facility, which has supported customers for more than thirty years, received a significant expansion in 2020 with advanced custom packaging and assembly capabilities for optical, high-speed, and radio frequency microelectronic products. Malaysia provides additional capacity for complex electronics manufacturing. These facilities serve customers who want Asian manufacturing costs but prefer alternatives to China.

In Eastern Europe, Sanmina's Romanian and Czech facilities cater to European OEM customers who want manufacturing closer to their end markets. These locations offer competitive costs by European standards, a skilled technical workforce, and the advantage of operating within the European Union's regulatory and trade framework.

The reshoring narrative has been validated by hard data. U.S. companies announced 287,000 jobs from reshoring and foreign direct investment in 2023, the second-highest year on record, with electronics and electrical products accounting for roughly thirty-nine percent of those announcements. Nearly one in two U.S. businesses reported plans to increase nearshoring volumes in 2025. In January 2025, the U.S. Department of Commerce announced two billion dollars in CHIPS Act grants specifically targeting smaller PCB and component manufacturers, aiming to close gaps in domestic supply chains by mid-2026. This is separate from the larger CHIPS Act subsidies for semiconductor fabrication and specifically addresses the printed circuit board manufacturing gap that Sanmina has long warned about. The United States today manufactures less than four percent of the world's PCBs, down from roughly thirty percent in the 1990s. For Sanmina, which maintained domestic PCB fabrication capacity when most competitors abandoned it to Asia, this government support creates additional tailwinds.

In Europe, the nearshoring trend has played out through Mediterranean manufacturing hubs, with Morocco seeing demand surges of fifty-three percent year-over-year, Egypt seventy-three percent, and Tunisia thirty-five percent. Sanmina's Romanian and Czech facilities are positioned to benefit from European OEMs who want production closer to home and within the EU regulatory framework, avoiding the tariff and compliance risks of importing from Asia.

The strategic implication for investors is significant. Manufacturing geography has shifted from being a cost-optimization variable to a strategic capability. Customers increasingly prioritize supply chain resilience over pure cost minimization. They want multiple manufacturing options across regions. They want the ability to shift production between geographies if trade policies change or geopolitical risks escalate. Sanmina's distributed footprint provides exactly this flexibility, and it took decades to build. A competitor starting from scratch today would need years and billions of dollars of capital to replicate it.

There is also an important distinction between nearshoring rhetoric and reality. Many companies have announced nearshoring plans, but the actual pace of production relocation is constrained by workforce availability, infrastructure development, and the time required to qualify new manufacturing locations. EMS providers that already have established, qualified facilities in nearshore locations have a genuine time-to-market advantage. Sanmina's Thai facility has been operating for over thirty years, its Mexican operations serve multiple end markets with proven quality systems, and its European facilities have long-standing relationships with continental OEMs. These are not new capabilities being hastily assembled in response to trade tensions. They are mature operations with deep institutional knowledge, and that maturity is itself a competitive advantage.

X. Leadership Transitions & Corporate Governance

Jure Sola's tenure as Sanmina's leader spanned nearly four decades, from founding the company in 1980 through his service as Chairman and CEO until 2019. That kind of founder-led longevity is rare in any industry and virtually unprecedented in the high-turnover world of technology manufacturing. Sola's leadership style was characterized by strategic patience and a willingness to endure short-term pain for long-term positioning. He kept PCB fabrication when others divested it. He pushed vertical integration when the industry was moving toward asset-light models. He maintained geographic diversification when China-concentration was the conventional wisdom.

The transition to Michael Clarke, who moved from CFO to CEO, represented a deliberate choice of continuity over disruption. Clarke knew the business intimately from his years managing its finances. He understood the capital allocation discipline that had allowed Sanmina to survive industry downturns that destroyed competitors. The transition was designed to preserve institutional knowledge and strategic direction while bringing fresh energy and a more professionally managed operational cadence.

Under Clarke's leadership, Sanmina's capital allocation philosophy has emphasized operational excellence over aggressive deal-making. For most of the period between the SCI acquisition and the ZT Systems deal, the company avoided transformative M&A, preferring to invest in organic capability building, facility optimization, and selective technology development. This was a marked contrast to competitors like Jabil and Celestica, which made multiple mid-size acquisitions to enter new verticals or geographies. Sola and then Clarke believed that the biggest risk in EMS was not missing a growth opportunity but overextending the balance sheet in a cyclical business. Share buybacks have been a consistent feature, with the company repurchasing significant volumes of stock during periods of undervaluation, reflecting management's conviction that the market chronically underprices the company's assets and earnings power.

The ZT Systems acquisition in 2025 represented a decisive break from this conservative capital allocation pattern, signaling that Clarke and the board saw AI infrastructure as a once-in-a-generation opportunity worth stretching for. The three-billion-dollar price tag was the largest deal since SCI, and the strategic rationale, doubling down on hyperscale data center manufacturing, represented the boldest bet the company had made in decades.

The board composition reflects Sanmina's evolution from a founder-controlled enterprise to a professionally governed corporation. Private equity firms have periodically expressed interest in taking Sanmina private, attracted by the company's strong cash generation and the potential to optimize its portfolio away from public market scrutiny. That Sanmina has remained public suggests management and the board believe the company's value is better realized through public ownership and the strategic flexibility it provides.

This brings us to the company's most recent financial results. In Q1 fiscal 2026, for the quarter ended December 27, 2025, Sanmina reported revenue of $3.19 billion, beating the projected $3.09 billion and marking a fifty-nine percent year-over-year increase. Non-GAAP operating margin came in at six percent. Non-GAAP diluted earnings per share reached $2.38. The numbers reflected the early impact of the ZT Systems integration, which was proceeding in line with management expectations.

However, the market reaction on March 12, 2026, was brutal. Sanmina shares plunged twenty percent after management provided cautious forward guidance, citing a "transition period" involving ZT Systems and delays in program ramps for legacy industrial segments. Q2 FY2026 guidance of $3.1 to $3.4 billion in revenue and non-GAAP diluted EPS of $2.25 to $2.55 was perceived as tepid relative to expectations. The stock performance and shareholder returns remain a mixed picture: extraordinary long-term appreciation from the 2009 lows but persistent volatility driven by the cyclical nature of the business and the execution risks of the ZT Systems integration.

XI. Current State & Recent Developments (2020-2025)

The COVID-19 pandemic hit the EMS industry like a Category Five hurricane. Factory shutdowns in Asia disrupted production schedules. Component shortages, particularly in semiconductors, made it impossible to complete assemblies even when factory capacity was available. Logistics nightmares, including port congestion, container shortages, and air freight cost spikes, added weeks to delivery timelines. For a business built on just-in-time manufacturing and lean inventory management, the pandemic was the ultimate stress test.

Sanmina navigated this period by leveraging its global footprint to shift production between facilities when specific locations faced restrictions. When a factory in one country shut down due to lockdowns, production could be redirected to facilities in other regions that remained operational. This geographic agility, which had been built over decades for cost and customer proximity reasons, suddenly became a survival tool.

The company's vertical integration proved unexpectedly valuable during the component shortage crisis. Internal PCB fabrication capacity meant one fewer link in the strained supply chain. While competitors were scrambling to source PCBs from external fabricators who were themselves struggling with material shortages and capacity constraints, Sanmina could manufacture its own. This advantage was not theoretical: it translated directly into the ability to fulfill customer orders that competitors could not.

Cash generation remained strong throughout the pandemic period, with fiscal 2025 producing $621 million in cash flow from operations. Liquidity was robust, with $926 million in cash and no borrowings on its $800 million revolving credit facility. The balance sheet strength gave management the confidence to pursue the ZT Systems acquisition from a position of financial security rather than desperation.

The transformative event of this period was the acquisition of ZT Systems' data center infrastructure manufacturing business from AMD, completed in 2025 for approximately three billion dollars, including up to $450 million in contingent payments. ZT Systems was a server-solutions specialist with an annual revenue run-rate of approximately five to six billion dollars. The deal roughly doubled Sanmina's revenue base and positioned the company squarely in the hyperscale data center and AI infrastructure build-out.

The ZT Systems acquisition represents Sanmina's biggest strategic bet since the SCI merger a quarter century ago. The rationale is that AI infrastructure, from GPU servers to liquid-cooled racks to high-density interconnect systems, represents a multibillion-dollar manufacturing opportunity that plays directly to Sanmina's strengths in complex, engineering-intensive production. Management has articulated a goal of doubling revenue over two years, anchored by what it describes as a transformative AI opportunity. Core Sanmina, excluding ZT, is projected to grow at a high single-digit rate in fiscal 2026, with longer-term operating margin targets moving toward six to seven percent or higher.

The strategic priority list reads like a catalog of the most important technology trends of the next decade. AI infrastructure is the headline act: the hyperscale data center build-out requires enormous volumes of complex server systems, networking equipment, and power distribution hardware that must be assembled with precision and delivered at scale. Sanmina, through the ZT Systems acquisition, is now manufacturing the physical infrastructure that makes large language models and generative AI applications possible. This is not glamorous work compared to designing the AI models themselves, but it is essential work, and there is a tremendous amount of it to be done.

Defense modernization is the second major priority. Global military spending has been rising steadily as geopolitical tensions intensify. The United States defense budget alone exceeded eight hundred billion dollars in fiscal 2024, and allied nations across Europe and the Indo-Pacific are increasing their own spending. Sanmina's SCI Technology subsidiary in Huntsville sits at the heart of this trend, building avionics, tactical communications systems, and counter-drone technology for programs that often run for decades. Defense revenue tends to be more stable than commercial revenue, with longer contract timelines and less pricing pressure, making it an attractive counterbalance to the cyclicality of Sanmina's commercial business.

Medical device manufacturing and automotive electrification round out the strategic priorities. Both sectors offer the combination of regulatory complexity, long product lifecycles, and engineering intensity that plays to Sanmina's strengths. The transition to electric vehicles alone is creating massive new demand for battery management systems, power electronics, charging infrastructure electronics, and advanced driver-assistance systems, all of which require precisely the kind of high-reliability, high-complexity manufacturing that Sanmina has spent four decades perfecting.

Culturally, the company has evolved from a founder-led enterprise where Jure Sola's instincts drove strategy to a more professionally managed organization where decisions are informed by data analytics, systematic customer portfolio management, and structured strategic planning processes. Whether this evolution represents an improvement or a loss of entrepreneurial edge is a question that will only be answered by long-term performance. What is clear is that the company Sola and Mandaric founded in a San Jose office in 1980 has become something far larger and more complex than either founder could have imagined.

XII. Business Model Deep Dive & Unit Economics

There is a common misconception among generalist investors that all EMS companies are essentially the same: interchangeable contract manufacturers competing on price alone. This perception is reflected in the relatively modest valuation multiples the sector commands. But the economics of EMS are more nuanced than they appear, and understanding them is essential to evaluating whether Sanmina's strategy creates real value or merely rearranges costs.

Revenue comes from three sources.

First, manufacturing services: this is the core assembly and test business, where Sanmina takes a customer's design, procures the components, assembles the product, tests it, and ships it out. This is the bulk of revenue.

Second, engineering services: this includes design-for-manufacturing consultation, new product introduction, and sustaining engineering, where Sanmina helps customers optimize their products for efficient production and manages engineering changes throughout a product's lifecycle.

Third, components: the internally manufactured PCBs, backplanes, enclosures, and cable assemblies. This is particularly interesting because it allows Sanmina to capture margin at a stage where external suppliers would normally take their cut. The essence of the vertical integration value proposition is right here: by manufacturing these components internally, Sanmina earns two margins on a single customer engagement instead of one.

Why are five to seven percent operating margins considered "good" in this industry? The answer lies in the revenue composition. A large portion of EMS revenue represents pass-through component costs. When a customer's product requires a hundred-dollar microprocessor, that cost flows through the EMS provider's revenue and cost of goods sold. The provider adds no value to the microprocessor itself, merely purchasing and placing it. The actual value-add, the manufacturing conversion, might represent only twenty to thirty percent of total revenue. Measured against conversion revenue rather than total revenue, operating margins are actually much healthier than the headline numbers suggest. But because accounting conventions require reporting total revenue including pass-through component costs, the margins look thin.

Working capital management is where EMS companies live or die. Days Inventory Outstanding is the most critical metric. You must carry component inventory to ensure production continuity, but every dollar of inventory is a dollar of cash tied up in the balance sheet rather than being available for investment or shareholder returns. Jabil leads the industry with 5.4 times inventory turns; Flex runs at 3.9 times. The best operators manage their payables cycle to partially offset inventory investment, negotiating extended payment terms with component suppliers while collecting promptly from customers. The cash conversion cycle, the number of days between paying for components and collecting from customers, is the single most telling metric for operational efficiency in EMS.

Return on invested capital presents a more encouraging picture than raw margins might suggest. Sanmina reported a non-GAAP pre-tax ROIC of 28.3 percent in the fourth quarter of fiscal 2025. That is an outstanding return by any industrial standard and reflects the company's ability to generate significant profits relative to its invested capital base. The key is that Sanmina's vertical integration, while capital-intensive on the asset side, generates outsized returns because the internally manufactured components carry substantially higher margins than pure assembly.

Contract structures in EMS typically involve some form of "bill of materials plus conversion fee" pricing. Here is how it works in practice: the customer specifies the design, including the exact components to be used and often the approved suppliers for those components. The EMS provider procures the components, sometimes carrying them in inventory for weeks or months before the customer actually orders finished products. The provider then assembles, tests, and ships the finished product. The revenue reported includes both the pass-through component cost and the manufacturing conversion fee. This is why reported margins look so thin: if a product costs a hundred dollars in components and the EMS provider adds ten dollars of conversion value, the one-hundred-and-ten-dollar revenue figure makes the ten-dollar margin look like nine percent, even though the return on the actual value-add is a hundred percent.

Volume commitments from customers help ensure capacity utilization, but the reality is that EMS providers have limited pricing power. Sophisticated OEM customers run competitive bidding processes, benchmark pricing across multiple providers, and use the threat of multi-sourcing or in-sourcing to extract concessions. Some EMS providers charge a holding fee, sometimes called a weighted average acquisition cost adder, of up to fifteen percent annually on inventory carried on behalf of customers, which helps offset the working capital burden. But the fundamental dynamic remains: margin expansion in EMS comes primarily from operational efficiency improvements and product mix management, moving toward higher-complexity, higher-margin programs, rather than pricing power.

The cash conversion cycle deserves special attention because it is where operational excellence shows up most clearly in EMS. Jabil leads the industry with a cash conversion cycle of roughly thirty-seven days, meaning the company converts its working capital investment into cash faster than any peer. Flex runs at about sixty-seven days. The difference between the best and worst operators in cash conversion translates directly into free cash flow generation, balance sheet strength, and the ability to fund growth without excessive borrowing.

XIII. Strategic Frameworks Analysis

Analyzing Sanmina through the lens of competitive strategy frameworks reveals a company with meaningful but not impregnable advantages operating in a structurally challenging industry.

Starting with the competitive environment, the threat of new entrants is moderate but varies dramatically by market segment. Building a credible EMS operation at the high end requires significant capital investment, with modern surface-mount technology lines costing five to fifteen million dollars each, and a full-scale facility requiring dozens of such lines plus testing, warehousing, and logistics infrastructure.

Quality certifications for regulated end markets take years to obtain: ISO 13485 for medical, AS9100 for aerospace, IATF 16949 for automotive. Customer relationships in complex manufacturing are deep and trust-based, creating natural barriers.

However, at the low end of the market, smaller regional players can enter with modest capital and compete on cost for simpler assembly work. The real barrier is competing for Tier 1 OEM business, which requires multi-billion-dollar revenue capacity, a global footprint, and the financial strength to carry substantial inventory on behalf of customers.

The bargaining power of customers, the OEMs that Sanmina serves, is the single most important competitive force in the EMS industry and it is high. OEM customers are large, sophisticated buyers who can and do multi-source across multiple EMS providers. They run competitive bidding processes. They can threaten to bring manufacturing back in-house. When a single customer represents a meaningful portion of your revenue, the power dynamic tilts heavily in their favor. This is why customer concentration management is so critical, and why Sanmina's diversification efforts following the Nokia experience were an existential priority rather than a mere strategic preference.

Supplier power is moderate and cyclical, but it can be devastating during shortage periods. During normal times, EMS providers with scale can negotiate volume discounts on components, giving them procurement advantages over smaller competitors. Sanmina's annual component purchasing volume runs in the billions of dollars, which provides meaningful leverage with distributors and component manufacturers. But during shortage periods, as the 2020-2022 semiconductor crisis vividly demonstrated, component suppliers hold enormous power. Lead times for basic microcontrollers stretched from weeks to over a year. Prices for some commodity chips increased by ten to twenty times. EMS providers were squeezed between contractually fixed prices with their customers and rising component costs from their suppliers. Companies without strong supplier relationships and diversified sourcing strategies simply could not fulfill their orders.

Sanmina's vertical integration helps mitigate supplier power because internally manufactured PCBs, backplanes, enclosures, and mechanical components are not subject to the same supply-demand dynamics as externally sourced semiconductors. When the component crisis hit, Sanmina did not need to compete with other EMS providers for PCB supply because it manufactured its own. This is a meaningful structural advantage that pure assembly houses cannot replicate without making the same capital investments Sanmina made over decades.

The threat of substitutes comes primarily from OEMs choosing to bring manufacturing in-house, regional specialists undercutting on price, and ODMs that offer both design and manufacturing. The long-term trend has been toward outsourcing, but periodic reversals occur. In-sourcing risk is real but declining as manufacturing technology grows more complex and capital-intensive.

Competitive rivalry among the remaining major players is intense. The industry has consolidated significantly from the dozens of players that existed in the 1990s to a handful of large survivors, but those survivors compete fiercely for every program. Price competition is the default, and differentiation through vertical integration, engineering capability, and geographic footprint is the only path to margins above the commodity floor.

Through Hamilton Helmer's Seven Powers framework, Sanmina possesses moderate switching costs in regulated verticals where qualifying a new EMS partner involves extensive audits, testing, and regulatory submissions. A medical device customer that has validated Sanmina's manufacturing processes with the FDA faces real cost and risk in switching to an alternative provider. In defense, ITAR compliance and security clearances create similar stickiness.

The company demonstrates process power through its manufacturing excellence, quality systems, and supply chain management, but this advantage is replicable given sufficient time and investment. Sanmina's vertical integration represents a form of counter-positioning: the company invested in PCB fabrication and component manufacturing when the industry consensus was to divest such capabilities, creating a differentiated position that would be costly for competitors to replicate now. Scale economies exist in procurement and overhead absorption but are limited because the market is not winner-take-all.

Network effects, branding power in the B2B context, and cornered resources (beyond specialized engineering talent in certain verticals) are minimal. The honest assessment is that Sanmina has moderate switching costs and process power in specific verticals, but lacks the kind of durable, structural competitive advantages that characterize businesses with wide moats. Success depends heavily on execution and market positioning rather than an unassailable competitive position.

The Celestica comparison is particularly instructive here. Celestica has achieved a return on invested capital of 37.5 percent, substantially higher than Sanmina's 28.3 percent, by concentrating on AI and data center infrastructure where demand is exploding and design complexity creates natural barriers. But Celestica's top two customers represent nearly forty percent of revenue, a concentration level that would make Sanmina's management deeply uncomfortable. The tradeoff between concentration-fueled returns and diversification-driven resilience is the core strategic tension in EMS. Neither approach is objectively superior; they represent different bets on what the future holds. If AI infrastructure demand continues to surge, Celestica's concentration is brilliantly focused. If a major customer shifts direction or a downturn hits cloud spending, that concentration becomes a vulnerability.

The myth versus reality check on Sanmina is worth stating directly. The consensus narrative is that EMS is a terrible business with no competitive advantages where anyone with a factory can compete. The reality is more nuanced. Sanmina's vertical integration, its regulatory certifications across medical, defense, and automotive, and its established global manufacturing footprint create real barriers that take years and significant capital to replicate. These are not impenetrable moats, but they are meaningful friction points that protect the company's position and support above-industry-average margins. The question is not whether these advantages exist but whether they are durable enough to withstand the relentless competitive pressure that characterizes the industry.

XIV. Bull vs. Bear Case

The bull case for Sanmina rests on several converging favorable trends, and it begins with understanding how dramatically the world has changed in the company's favor over the past five years. The nearshoring and friend-shoring megatrend is perhaps the most powerful secular tailwind in the company's history. As companies worldwide diversify their manufacturing supply chains away from China, Sanmina's distributed geographic footprint, built over decades rather than reactively assembled in the past few years, represents a genuine competitive advantage. The company already has the facilities, the certifications, the workforce, and the customer relationships in Mexico, Southeast Asia, Eastern Europe, and the United States. Competitors that concentrated in China are now scrambling to build alternatives.

Customer diversification, achieved through years of painful effort following the Nokia-era concentration crisis, has created a more resilient revenue base. Medical devices and defense electronics offer better margins and longer product lifecycles than the telecom equipment that dominated Sanmina's revenue a decade ago. Vertical integration creates differentiation that pure assembly houses cannot match and contributes to the industry-leading six percent non-GAAP operating margin. Management's track record of disciplined capital allocation, strong cash generation, and share buybacks provides a floor of shareholder value creation. The ZT Systems acquisition, if successfully integrated, could transform Sanmina into a truly scale player in AI infrastructure manufacturing. And with the stock trading at a significant discount to its recent highs following the March 2026 selloff, the valuation argument has become more compelling for patient investors.

The bear case is equally substantive and deserves the same rigorous consideration. EMS is a structurally low-margin business with limited competitive moats. Customer bargaining power remains overwhelming because OEMs are large, sophisticated buyers who can always multi-source or in-source. The six percent operating margin that looks attractive relative to EMS peers still represents a thin cushion against operational missteps, customer losses, or demand downturns. Capital intensity limits return on invested capital over full cycles, even if point-in-time ROIC numbers look strong. Technology changes rapidly in the end markets Sanmina serves, requiring constant reinvestment in new manufacturing capabilities. The geographic diversification that is an advantage in one geopolitical scenario could become a liability in another, with manufacturing facilities in regions like Israel, India, and Thailand all carrying their own political and operational risks. Attracting top engineering talent to a contract manufacturer, rather than to a brand-name technology company, remains a persistent challenge. And the ZT Systems integration, the largest deal since SCI, carries meaningful execution risk in a business where integration mistakes are punished by customer defection and margin compression.

The KPIs that matter most for tracking Sanmina's ongoing performance are operating margin trajectory and revenue mix by end market. Operating margin, specifically whether the company can sustain six percent non-GAAP operating margins and move toward the seven percent target, is the single best indicator of whether the vertical integration strategy and customer mix management are working. Revenue mix by end market, specifically the share of revenue from higher-margin verticals like medical, defense, and cloud infrastructure versus lower-margin legacy segments, tells you whether the company's strategic repositioning is proceeding or stalling. These two numbers, tracked quarter by quarter, will tell you more about Sanmina's trajectory than any earnings surprise or headline revenue figure.

XV. Lessons & Playbook for Founders & Investors

Sanmina's forty-five-year journey offers a masterclass in survival and adaptation within a brutally competitive industry. In an era when technology companies are celebrated for disruption, rapid growth, and billion-dollar exits, Sanmina represents a different archetype entirely: the company that wins by refusing to die. Several lessons stand out with particular clarity.