Science Applications International Corporation (SAIC): Engineering the Invisible War

I. Introduction and Episode Roadmap

There is a company headquartered in Reston, Virginia, that pulls in more than seven billion dollars a year in revenue. Its engineers sit inside some of the most sensitive facilities in the United States government. Its software runs on classified networks that most Americans will never hear about. Its employees hold security clearances that take the better part of a year to obtain. And yet, if you walked down any street in America and asked a hundred people whether they had heard of SAIC, you would be lucky to find one who had.

That anonymity is not an accident. It is a feature of the business.

Science Applications International Corporation is one of the Pentagon's most trusted partners, a company woven so deeply into the fabric of American national security that its work is, almost by design, invisible. It modernizes the information technology that the Air Force uses to fly missions. It builds the ground systems that connect satellites to warfighters. It architects the cybersecurity frameworks that protect the intelligence community from adversaries who never sleep.

And it does all of this in near-total obscurity, its name appearing in procurement databases and defense trade publications rather than on the front page of the Wall Street Journal.

The paradox of SAIC is that its obscurity is both its greatest strength and its most persistent challenge. The company does mission-critical work, the kind where failure is measured not in lost revenue but in compromised national security, and yet it trades at a discount to flashier government technology companies that have mastered the art of the earnings call narrative. SAIC's story is not the story of a rocketship startup. It is the story of a small think tank spinoff founded by a nuclear physicist in 1969 that became one of the largest government contractors in the country, got absorbed into what became Leidos, and then re-emerged as a separate company that had to figure out what it was all over again.

This is a story about the economics of government contracting, an industry where your only customer is the federal government, where every contract eventually comes up for rebid, and where the most valuable asset you own walks out the door every evening with a security badge around its neck. It is a story about the split and merger arbitrage that created and then recreated SAIC, about why boring businesses can be beautiful investments, and about what happens when a company built on the idealism of employee ownership has to grow up and face Wall Street.

The key metrics that matter most for tracking SAIC's ongoing performance are two.

First, the book-to-bill ratio, which measures the dollar value of new contracts won relative to revenue recognized in a given period. A ratio above one means the backlog is growing and future revenue is secured. A ratio below one means the company is burning through its pipeline faster than it can replenish it.

Second, adjusted EBITDA margin, which captures the company's ability to shift its contract mix from low-margin commodity work toward higher-value mission integration. These two numbers, taken together, tell you whether SAIC is winning the right work at the right price.

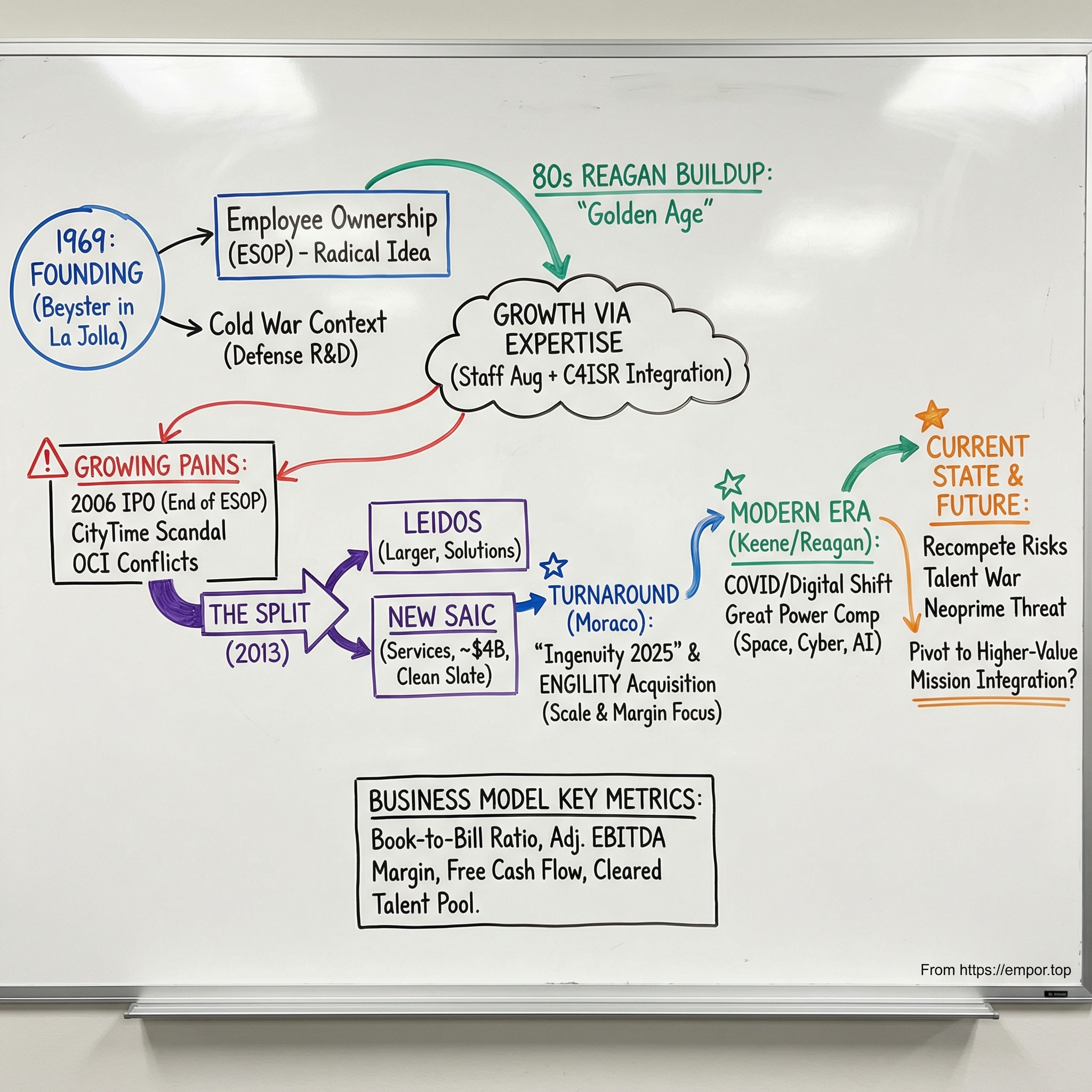

To understand where SAIC stands today, we need to go back to where it all began: a nuclear physicist in La Jolla who believed that scientists should own the companies they built.

II. Founding Context: Cold War America and the Rise of the Beltway Bandits

J. Robert Beyster was not the kind of man who dreamed of building a corporate empire. Born in 1924, he earned his doctorate in physics from the University of Michigan and spent the early years of his career at Los Alamos National Laboratory, the birthplace of the atomic bomb. He was a National Science Foundation Fellow, a man who spoke the language of neutron cross-sections and nuclear energy with the fluency of someone who had spent years at the frontier of Cold War science. By the late 1960s, he was working at General Atomics in San Diego, running a group of nuclear physicists, and growing increasingly frustrated.

The frustration was not about the science. It was about the economics. Beyster watched as the scientists around him did groundbreaking work for defense and intelligence clients, and then watched as the financial rewards flowed upward to shareholders and executives who had never set foot in a laboratory.

He believed, with the conviction of someone who had seen how Los Alamos operated during the war, that the people who did the work should own the results of that work. In 1969, he left General Atomics and founded Science Applications Incorporated with a dozen employees and a radical idea: the company would be owned by the people who worked there.

The founding was modest in every way except ambition. Beyster set up shop in La Jolla, California, a sun-drenched coastal enclave better known for its surfing than its defense contracting. The company had no venture capital, no outside investors, and no grand business plan. What it had was a group of scientists who knew how to solve problems that the government needed solved, and a founder who believed that shared ownership would create shared commitment.

The timing was exquisite. The late 1960s and 1970s were the golden age of defense research and development spending. The Cold War was in full swing. NASA was sending men to the moon. The intelligence community was expanding in ways that would not become public for decades. The Department of Energy was funding nuclear weapons research at a pace that made Los Alamos and Sandia look like small cities. And the Pentagon was beginning to realize that it needed outside expertise to solve problems that its own bureaucracy could not handle.

This was the era that gave birth to what Washington insiders called the Beltway Bandits, a constellation of companies that clustered around the capital and made their living solving the government's hardest technical problems. MITRE, Booz Allen Hamilton, and dozens of smaller firms emerged during this period, each carving out a niche in the vast ecosystem of federal contracting.

What made Beyster's company different from day one was the ownership structure. SAIC operated an Employee Stock Ownership Plan that was unlike anything else in the industry. There was no sales team in the traditional sense. Technical excellence was the only calling card.

The internal stock market that Beyster created was ingenious in its design. The board of directors set the stock price quarterly using a formula based on net income, shares outstanding, and a "market factor" that compared SAIC's performance against twenty-five similar publicly traded companies. This allowed the stock to reflect market conditions without being subject to the short-term speculation of public markets. Employees could buy and sell shares during quarterly trading windows, and stock grants were awarded based on individual contribution to specific programs, not seniority or title. A support for employee ownership was a requirement to serve on the board. Scientists and engineers won contracts by being the smartest people in the room, and then they were rewarded with ownership stakes in the company they were building.

The early clients were exactly who you would expect. The Navy needed help with submarine warfare analysis. The Department of Energy needed expertise in nuclear weapons testing. The intelligence agencies needed people who could solve problems that did not officially exist.

SAIC's employees worked in SCIFs, Sensitive Compartmented Information Facilities, the windowless rooms where America's most classified work gets done. A SCIF is, to use a simple analogy, a vault within a vault: a room with no windows, shielded walls, and electronic countermeasures designed to prevent any signal from leaking in or out. The people who work inside them hold clearances, Secret, Top Secret, or Top Secret/SCI, that take months to obtain and that function as a de facto barrier to entry for any competitor that tried to poach them.

Beyster ran the company with a philosophy he described as radical decentralization. He created internal markets where different groups within SAIC competed for contracts and resources, almost like independent businesses operating under a single corporate umbrella. The hierarchy was flat. Engineers reported to engineers.

The culture was one of missionary zeal, the kind of environment where people worked eighty-hour weeks not because they were told to but because they owned a piece of what they were building. The system, as Beyster later described it, "made millionaires out of hundreds of its workers." It was not a system designed for passive investors. It was a system designed for people who believed that ownership and contribution should be the same thing.

By the time the Reagan defense buildup began in the early 1980s, SAIC was perfectly positioned to ride the wave.

III. The Golden Age: Scaling Through Expertise

When Ronald Reagan took office in January 1981 and declared that it was "morning in America," it was certainly morning for SAIC. The Reagan defense buildup was the largest peacetime military expansion in American history, and it sent a torrent of money flowing into exactly the kind of work that SAIC did best. The defense budget rose from roughly $144 billion in fiscal year 1980 to more than $300 billion by fiscal year 1989, and the contractors who could solve the Pentagon's most complex technical problems grew alongside it.

SAIC's business model during this era was a hybrid that the industry would later describe as staff augmentation meets systems integration.

At its simplest, staff augmentation meant placing cleared engineers and scientists inside government facilities to work alongside federal employees on programs too complex or too classified for the government to handle alone. Think of it as renting expertise by the hour: the government tells you what problem it needs solved, and you send your best people to sit in its buildings and solve it.

Systems integration was the more complex and more lucrative side of the business. It meant taking responsibility for making disparate pieces of technology work together, connecting sensors to networks, networks to command centers, and command centers to the people who made life-or-death decisions. The Pentagon had an acronym for this world: C4ISR, which stood for Command, Control, Communications, Computers, Intelligence, Surveillance, and Reconnaissance. It is, in essence, the nervous system of the military. SAIC lived and breathed C4ISR.

The company's involvement in classified programs during this period was extensive. SAIC worked on elements of the Strategic Defense Initiative, the ambitious missile defense program that critics called Star Wars and that proponents believed could render nuclear weapons obsolete. The company worked on intelligence systems for agencies whose names it could not utter in public. It performed nuclear weapons testing analysis for the Department of Energy's national laboratories. And it did all of this while remaining essentially invisible to the general public, a company generating billions of dollars in revenue that almost nobody outside the defense community had ever heard of.

The employee ownership model was the engine that drove this growth. When an SAIC engineer won a major contract, the financial reward was not just a bonus check. It was an increase in the value of their ownership stake in the company. This created an alignment of incentives that was almost unheard of in the defense industry.

Engineers acted like entrepreneurs because they were entrepreneurs. They identified opportunities, pitched solutions, won contracts, and then watched as their share of the company grew alongside the revenue they generated. The system was self-reinforcing: the best engineers attracted the best contracts, which generated the best returns, which attracted more of the best engineers. By the late 1990s, the system had made hundreds of SAIC employees millionaires.

The geographic footprint expanded during this period from San Diego, where Beyster had founded the company, to the Washington DC corridor, where the customers were. SAIC established a major presence in Northern Virginia, within commuting distance of the Pentagon, the intelligence agencies in McLean, and the civilian agencies scattered across the capital region.

The move was driven by proximity economics. In government contracting, relationships are everything, and relationships require physical presence. You cannot build trust with a program manager over email. You build it by showing up at their building, day after day, year after year, until you understand their mission better than they do themselves.

By the time the company crossed two billion dollars in annual revenue, still as a private company, it had become one of the largest employee-owned enterprises in the United States.

Beyster's management philosophy remained stubbornly decentralized even as the company scaled. He resisted the centralization that most management consultants would have prescribed for a company of SAIC's size. Different groups operated almost autonomously, competing for internal resources and external contracts. The culture of secrecy was so deeply embedded that even employees in one division often had no idea what employees in another division were working on, not because of corporate politics but because the classification walls between programs made it physically impossible to share information.

This was both SAIC's greatest strength and, as it turned out, a structural vulnerability. The decentralization that made SAIC so effective at winning and executing technical work also made it difficult to impose the kind of centralized oversight that a multi-billion-dollar company needed.

IV. Going Public and Growing Pains

The end of SAIC's era as an employee-owned company did not happen overnight. It happened in stages, each one eroding a little more of what Beyster had built, until the company that emerged on the other side bore almost no structural resemblance to the one he had founded.

The pressures had been building for years. As SAIC grew past eight billion dollars in revenue and its employee base expanded into the tens of thousands, the mechanics of the internal stock market became increasingly unwieldy.

Every quarter, the board set a stock price. Employees could buy and sell shares during quarterly trading windows. But as the company grew, so did the liquidity demands. Departing employees needed to sell their shares, and the company needed cash to buy them back. At its peak, more than ninety percent of SAIC's stock was held by roughly 23,000 employees. Managing that level of distributed ownership in a private company was an administrative nightmare.

There were also practical pressures from the business itself. The company needed acquisition currency to grow, and a privately held stock with a board-set price was not the kind of currency that sellers wanted to accept. Succession planning after Beyster was complicated by the ownership structure. And new board members, particularly those with public company backgrounds, viewed the internal stock market as an anachronism that belonged to SAIC's past rather than its future.

Beyster retired as CEO in late 2003 after thirty-four years at the helm. Within eighteen months of his departure, the board was pursuing an initial public offering. Beyster later wrote about this period with unmistakable bitterness in his book The SAIC Solution, noting that some board members "were not committed to employee ownership preserving our culture" and that he "didn't figure this out until it was too late." The IPO, when it came in 2006, raised $1.1 billion and marked the definitive end of the employee-ownership era. The company initially maintained a dual-class share structure that gave employee-held shares ten times the voting power of public shares, but this too was eventually unwound as SAIC transitioned to a conventional public company governance model.

The years immediately following the IPO coincided with the most extraordinary period of defense spending in American history. The September 11 attacks had unleashed a torrent of government spending on intelligence, homeland security, and military operations that made the Reagan buildup look modest by comparison. SAIC was everywhere. Its employees provided intelligence analysis in Iraq and Afghanistan. It worked on reconstruction projects in war zones. It supported the standup of the Department of Homeland Security. Revenue surged past ten billion dollars as the War on Terror spending machine churned at full speed.

But the growth masked problems. SAIC's involvement in Abu Ghraib, where company employees had provided interrogation support at the infamous prison, created reputational challenges that forced the company to confront questions about oversight and accountability that it had never faced before.

The company pursued an acquisition strategy designed to diversify beyond pure government work, buying companies in hopes of building a commercial business. Most of these acquisitions failed to deliver. The integration was poor, the commercial ventures never gained traction, and the "growth at all costs" mentality produced expansion without value creation. It was a pattern that many government contractors have repeated over the decades: the grass always looks greener in commercial markets, until you realize that the skills required to win a Pentagon contract and the skills required to sell software to a Fortune 500 company have almost nothing in common.

The company also faced a series of smaller legal issues that, while individually manageable, suggested persistent compliance challenges. False Claims Act settlements of $11.75 million in 2014 and $5.98 million in 2020 for Army IT support contract irregularities pointed to the kind of billing practices that, while common in the industry, carry legal and reputational risk.

The worst of it came from New York City. In 2003, SAIC had won a no-bid contract valued at sixty-three million dollars to build CityTime, an electronic timekeeping and payroll system for the city's roughly 163,000 employees across more than a hundred agencies. Over the next seven years, the project's cost ballooned to approximately seven hundred twenty million dollars. The reason was fraud, and it was breathtaking in its scope.

SAIC had hired Technodyne LLC as a subcontractor to provide staffing. Technodyne was controlled by individuals who systematically kicked back millions of dollars to SAIC's CityTime program manager, Gerard Denault. The scheme involved shell companies, forged invoices, and offshore accounts.

Costs were inflated. Timelines were artificially extended. Red flags were ignored by both SAIC management and city oversight bodies for years. The fraud was not subtle, but it operated in the blind spot created by SAIC's decentralized management structure, where individual program managers had enormous autonomy and centralized oversight was thin.

In February 2011, U.S. Attorney Preet Bharara announced the indictment of five CityTime consultants, describing it as "the single largest fraud ever perpetrated against the City of New York." In 2014, Denault and two co-conspirators were each sentenced to twenty years in federal prison. SAIC settled with New York City for $500.4 million, one of the largest fraud settlements in the city's history.

The CityTime scandal was a wake-up call. It demonstrated the catastrophic risks of inadequate oversight in a decentralized organization, the very structure that had once been SAIC's competitive advantage. Combined with the failed commercial acquisitions and compressing margins in a post-sequestration budget environment, CityTime became one of the forces that pushed the company toward the most radical restructuring in its history.

V. The Split: A Radical Restructuring

By 2012, the diagnosis was becoming clear to everyone who looked at SAIC's financials: there were two fundamentally different businesses trapped inside one corporate body, and they were suffocating each other.

One business was a legacy IT services operation, the kind of work that involved managing networks, running help desks, and maintaining the sprawling information technology infrastructure of the federal government. This work was high volume but low margin, increasingly commoditized, and subject to brutal price competition through lowest-price-technically-acceptable contracting, a procurement method where the government awards the contract to the cheapest bidder that meets a minimum technical threshold.

The other business was a high-value technical services operation, the kind of work that involved building intelligence systems, performing systems engineering for weapons programs, and solving the classified problems that kept generals and spymasters awake at night. This work commanded better margins, required deeper expertise, and had stickier customer relationships.

The problem was that the two businesses had different growth profiles, different margin structures, and different customer bases. Bundling them together created an organizational conflict of interest, or OCI, that limited SAIC's ability to compete.

OCI is one of those concepts that sounds abstract until you see what it does in practice. Government rules prevent a contractor from advising the government on a program while simultaneously competing to build solutions for that same program. The logic is sound: you do not want the company advising the Air Force on what kind of software to buy also bidding to sell the Air Force that software. But for a company as sprawling as SAIC, the effect was paralyzing. The company was constantly tripping over OCI restrictions, unable to bid on work because a different division was already advising the customer.

Activist investors saw the opportunity before management did. The strategic review that followed led to a conclusion that seemed radical at the time: split the company in two.

The mechanics of the split, executed on September 27, 2013, were elegant in their financial engineering. The transaction used a Reverse Morris Trust structure, a mechanism that, in simple terms, allows a company to split into two pieces without either piece having to pay taxes on the separation. It is the corporate equivalent of dividing a house between two siblings without either sibling having to pay capital gains on their share.

The larger entity, which inherited most of the original SAIC's national security and capability development work, took the name Leidos and was led by former Air Force Chief of Staff John P. Jumper. The smaller entity, focused on direct government support and technical services, kept the SAIC name and was led by Tony Moraco, a long-tenured company executive who had been instrumental in the government services business.

Leidos emerged as the larger company, taking the lion's share of the debt. SAIC emerged as a roughly four-billion-dollar revenue company with a clean balance sheet and a focused mission: be the best pure-play government services contractor in the market. The split resolved the OCI conflicts immediately. Each company could now compete freely in its respective domain without worrying about what the other half was doing.

Wall Street's initial reaction was confusion. Analysts who had covered the old SAIC now had to figure out how to value two companies that had never existed independently. But the confusion gave way to clarity within months. The market began to recognize what the split's architects had understood: that focus creates value, and that two companies pursuing distinct strategies would be worth more than one company trying to be everything to everyone. For investors who understood the spinoff playbook, the new SAIC represented exactly the kind of hidden value that the market tends to underprice in the chaos of corporate restructurings.

VI. The Turnaround Under Tony Moraco

Tony Moraco inherited a company that was simultaneously liberated and vulnerable. The new SAIC had focus, a clean balance sheet, and freedom from OCI conflicts. It also had four billion dollars in revenue, secular headwinds from sequestration, and the challenge of defining itself as something more than the leftover piece of a corporate breakup.

The timing could not have been worse. The Budget Control Act of 2011 had triggered sequestration beginning on March 1, 2013, just months before the split. Defense accounts absorbed a 5.6 percent cut that year, with the pain falling disproportionately on contractors. Eighty percent of sequestration cuts landed on industry because the Pentagon exempted military and civilian pay, benefits, and insurance. The remaining half of the defense budget, essentially all of it contracts, bore the full weight of the reductions. Every government services contractor in America was facing revenue declines, and the newly independent SAIC was no exception.

Moraco's response was counterintuitive but strategically sound. Rather than chasing revenue growth in a shrinking market, he focused on margins and operational excellence. The company tightened its belt, improved its contract execution, and began the slow work of shifting its business mix from commodity staff augmentation toward higher-value solutions work.

The difference between staff augmentation and solutions work is crucial to understanding SAIC's transformation. Staff augmentation is essentially renting bodies: the government tells you how many engineers it needs, you send them, and you bill by the hour. Solutions work means the government tells you the problem it needs solved, and you figure out the approach, the technology, and the team needed to solve it. The margins are better because you are selling expertise, not just labor.

The transformation was codified in 2017 under the banner "Ingenuity 2025," a strategy that called for SAIC to become a mission integrator rather than a body shop. The company restructured from five business groups into three customer groups and service lines, each aligned around a specific set of government missions rather than internal organizational logic.

The acquisition strategy was disciplined in a way that the pre-split SAIC's had not been. In May 2015, SAIC acquired Scitor Corporation for approximately $790 million, a deal that gave it deep access to the intelligence community and positioned it for classified work that commanded premium margins. The Scitor integration went smoothly, a welcome contrast to the failed acquisitions of the pre-split era.

But the defining moment of Moraco's tenure was the Engility acquisition. Engility Holdings was a systems engineering and integration company with strong positions in defense, civilian agencies, intelligence, and space. The deal, announced in 2018 and closed on January 14, 2019, was valued at approximately $2.5 billion in an all-stock transaction. Engility shareholders received 0.450 SAIC shares for each Engility share, leaving SAIC shareholders with roughly seventy-two percent of the combined company.

The Engility deal was transformative. It doubled SAIC's presence in national security mission work, added capabilities in systems engineering and space that the company had lacked, and pushed combined revenue above seven billion dollars. More importantly, the integration succeeded. Unlike the pre-split acquisitions that had destroyed value through poor execution and cultural clashes, the Engility integration demonstrated that SAIC had learned from its mistakes. The two companies shared similar cultures, similar customers, and similar approaches to the work, and the combination felt more like a reunion than a forced marriage.

By the time Moraco retired on July 31, 2019, the stock had risen from the low twenties at the time of the split to above eighty dollars, more than tripling in six years. Revenue had grown from roughly $4 billion at the time of the split to more than $7 billion after the Engility integration. He had taken a company that Wall Street initially viewed as the less interesting half of a corporate breakup and turned it into a focused, disciplined government services contractor with improving margins and a growing backlog.

The baton passed to Nazzic Keene, SAIC's former Chief Operating Officer, who became the company's first female CEO. Keene had been with SAIC through the split and had played a central role in the Engility integration, making her the natural choice for continuity.

VII. COVID, Digital Transformation, and New Battlefields

Nazzic Keene took the helm just as the world was about to change in ways that nobody anticipated. The COVID-19 pandemic, when it hit in early 2020, created a paradox for government contractors. On one hand, many SAIC employees worked in classified facilities that required physical presence, which meant that pandemic lockdowns disrupted operations in ways that fully remote companies never experienced. On the other hand, the pandemic exposed just how antiquated much of the federal government's information technology infrastructure really was, and the resulting scramble to modernize created demand for exactly the kind of work SAIC did.

Keene moved quickly to capitalize on the moment. In February 2020, just weeks before the pandemic shuttered offices across the country, SAIC announced the acquisition of Unisys Federal for approximately $1.2 billion. The deal closed on March 16, 2020, in the teeth of the pandemic's first wave, and it added a portfolio of IT modernization capabilities focused on federal civilian and defense agencies. It was a bet that digital transformation would accelerate, and it proved correct.

The federal government poured money into pandemic-related contracting. Through May 2021, agencies obligated $61.4 billion in pandemic-related contract funds, much of it for the kinds of IT modernization, cloud migration, and remote work solutions that SAIC was positioned to deliver.

Revenue proved resilient. The essential nature of defense and national security work meant that most SAIC programs continued operating through the pandemic, even if the operating environment was more challenging. The pandemic had exposed a truth that the defense establishment had long understood but never prioritized: much of the federal government's technology infrastructure was decades behind the commercial world, running on legacy systems that made remote work difficult and secure collaboration nearly impossible.

But the bigger story was not the pandemic. It was the tectonic shift in American defense strategy that had been building since 2018, when the National Defense Strategy explicitly pivoted from the counterterrorism and counterinsurgency focus of the post-9/11 era to great power competition with China and Russia. This was not a subtle change. It was a wholesale reorientation of the Pentagon's priorities, away from hunting insurgents in Middle Eastern deserts and toward preparing for potential conflicts with near-peer adversaries who possessed advanced missile systems, sophisticated cyber capabilities, and anti-satellite weapons.

For SAIC, the great power competition pivot opened new markets and reinforced existing ones.

Space was becoming a warfighting domain, and the establishment of the United States Space Force in December 2019 created an entirely new customer with an expanding budget. The fiscal year 2026 defense budget request allocated roughly $40 billion to space, a more than thirty percent jump from the prior year and the fastest-growing major category in the Pentagon's budget. The centerpiece of the administration's space ambitions was "Golden Dome," a comprehensive, multi-layered, space-integrated missile defense system targeted for full operational capability by 2028.

SAIC won a $444 million DTAMM contract from the Space Force's Space Systems Command, a five-year agreement to modernize space launch range instrumentation at Cape Canaveral and Vandenberg. It won a $55 million contract from the Space Development Agency for the Proliferated Warfighter Space Architecture program. Space-related awards exceeded $515 million in fiscal year 2025 alone.

Cyber and artificial intelligence became priorities that dwarfed anything the Pentagon had previously contemplated. SAIC positioned itself as an integrator of AI and machine learning capabilities for intelligence analysis and decision support, the kind of work where human judgment and domain expertise intersected with computational power. The company won a $928 million Air Force contract supporting the Tactical Exploitation of National Capabilities program, focused on prototyping warfighting capabilities. In late 2025, it won a $1.4 billion COBRA task order applying digital engineering, rapid prototyping, and data analytics across all warfighting domains.

Russia's invasion of Ukraine in February 2022 validated the great power competition thesis in the most visceral way imaginable. The war demonstrated the centrality of electronic warfare, cyber operations, and information operations, all areas where SAIC had deep expertise. Allied interoperability systems, the kind of technology that allows NATO forces to share data and coordinate operations, became urgent priorities rather than theoretical requirements. Congress approved $113 billion in Ukraine-related aid, and while SAIC was not a weapons manufacturer, the broader defense spending uplift created a rising tide that lifted all contractors.

Keene also completed the acquisition of Halfaker and Associates in July 2021 for approximately $250 million, adding federal health IT capabilities for the VA, DoD, and HHS. But her tenure ended when she retired in October 2023, passing the CEO role to Toni Townes-Whitley.

Townes-Whitley was a different kind of leader than SAIC had ever had. A former Microsoft executive who had also served as president of CGI Federal and held leadership roles at Unisys, she brought a technology industry perspective to a company that had always been run by government services veterans. She arrived with a mandate to accelerate SAIC's transformation into a technology-forward company.

But her tenure would prove brief and turbulent, lasting barely two years before the board decided, on October 23, 2025, to move in a different direction. In a LinkedIn post after her departure, Townes-Whitley wrote that "bold enterprise-scale transformations are generally not linear" and acknowledged the challenging market conditions the company faced. The separation was characterized as "without cause," with specified severance benefits and a two-year noncompete.

VIII. The Business Model Deep Dive

To understand SAIC, you have to understand how government contracting actually works, because it is unlike almost any other business model in the American economy.

The fundamental unit of the government contracting business is the contract, and contracts come in three basic flavors.

Cost-plus contracts reimburse the contractor for allowable costs and then add a fee on top, typically a fixed fee or an award fee tied to performance. Think of cost-plus as a guaranteed margin business: you spend a dollar, you bill a dollar plus a nickel, and the government pays you the dollar five. The risk is low because the government bears the cost overrun risk, but the margins are also low, typically in the mid-single digits.

Time-and-materials contracts pay the contractor for hours worked at negotiated billing rates, plus the cost of materials. These carry moderate margins and moderate risk.

Fixed-price contracts set a ceiling price for the work, and the contractor keeps whatever is left over after costs are deducted. These offer the highest potential margins but also the highest risk, because cost overruns come out of the contractor's pocket. A fixed-price contract on a complex government IT program is a bet that you can estimate the cost of something that the customer itself may not fully understand.

SAIC's contract mix has historically skewed toward cost-plus and time-and-materials work, which reflects the nature of its government services business. The company has been deliberately shifting its mix toward more fixed-price and solutions-oriented work, which carries better margins but requires more disciplined program execution. This mix shift is one of the primary drivers of the margin expansion story. Adjusted EBITDA margins improved from the mid-single digits at the time of the 2013 split to 9.5 percent in fiscal year 2025, with guidance pointing toward 9.9 to 10.1 percent in fiscal year 2027.

The recompete challenge is what makes government contracting fundamentally different from most businesses. Every contract has a finite period of performance, typically five years with options for additional years that the government may or may not exercise. When the period of performance ends, the work goes up for rebid.

The incumbent has significant advantages: institutional knowledge, embedded teams, established relationships with program managers, and the security clearances that make switching contractors risky and expensive. SAIC maintains an average CPARS score, the government's Contractor Performance Assessment Rating System, of approximately 4.5 out of 5, which helps in recompetes.

SAIC's recompete win rate on mission-critical work has historically run between eighty-five and ninety percent, a staggering number that reflects the power of incumbency when the work is complex and the switching costs are high. But the recompete on commodity work, particularly large enterprise IT contracts where price is the primary differentiator, is far less certain.

The company's recent loss of the Army RITS recompete, worth approximately $200 million in annual revenue, and the Air Force Cloud One recompete, worth roughly $75 million annually, illustrate the risk. Both were large, cost-plus, Department of Defense enterprise IT contracts, exactly the kind of work where incumbency advantage is weakest and price competition is most intense.

The talent war is the other defining feature of the business model. SAIC's product, if you can call it that, is its people. The company employs approximately 26,000 people, most of whom hold security clearances that take an average of 243 days to process.

To put that in perspective, there are an estimated 70,000 more open cleared positions in the United States than there are available candidates. That gap is not shrinking. The cleared-talent market is projected to grow seven to ten percent annually, driven by demand for cybersecurity, AI, data analytics, and intelligence operations capabilities. Fifty-six percent of recruiters in the sector cite the limited cleared talent pool as their number one hiring challenge.

Cleared professionals command significant salary premiums, and losing a cleared engineer on an active program can degrade performance ratings, which in turn can jeopardize future contract awards. This creates a retention imperative that drives labor costs and shapes everything from benefits packages to office locations. Every government contractor is fighting for the same scarce pool of talent, and the competition is zero-sum in a way that few other industries experience.

The capital allocation story is one of the more attractive features of the business. Government services contracting is a light-capital business. SAIC's capital expenditures were just $36 million in fiscal year 2025 against revenue of $7.48 billion, a capex-to-revenue ratio of less than half a percent. Compare that to a semiconductor company spending twenty to thirty percent of revenue on capital expenditures, or an airline spending billions on aircraft. SAIC's infrastructure is its people, and people do not require depreciation schedules.

Free cash flow was $499 million in fiscal year 2025, up twenty-two percent year over year, with preliminary fiscal year 2026 results suggesting $570 to $575 million. The company has been an aggressive buyer of its own stock, repurchasing $527 million in shares in fiscal year 2025 alone, equivalent to more than ten percent of its current market capitalization. The board authorized $1.2 billion in additional buybacks in December 2024, with no expiration date.

It has paid dividends for thirteen consecutive years, currently at $0.37 per share per quarter. Total capital deployed, including buybacks and dividends, reached $638 million in fiscal year 2025.

IX. The Competitive Landscape and Industry Dynamics

The government services sector is a peculiar corner of the American economy. It is enormous, generating hundreds of billions of dollars in annual revenue, but it is also intensely competitive, populated by half a dozen companies of roughly similar scale that fight over a finite pool of government spending. Understanding where SAIC sits in this landscape requires understanding both who it competes against and how the competitive dynamics are shifting.

The most direct comparison is Leidos, which is also the most uncomfortable one. Leidos is SAIC's corporate sibling, the larger entity that emerged from the 2013 split with roughly $16 billion in current annual revenue and a broader portfolio that includes hardware alongside services. Leidos took the original SAIC's name and DNA and built something bigger, while the new SAIC had to reinvent itself from scratch. The two companies compete on many of the same contracts, but Leidos operates at a scale that allows it to prime larger programs. The relationship is something like watching siblings who grew up in the same house but chose very different careers.

Booz Allen Hamilton, with annual revenue of roughly $11 billion, is the gold standard for government consulting and analytics. Booz Allen has positioned itself as the largest AI supplier to the U.S. government, generating approximately $800 million in AI-related revenue in fiscal year 2025 and maintaining a backlog of $38 billion. It trades at a premium valuation, north of twenty times earnings, that reflects the market's belief in its AI and analytics positioning. CACI International, with revenue of approximately $8.6 billion and a backlog of $31.4 billion, is another aggressive competitor with deep roots in the intelligence community.

General Dynamics Information Technology, a division of the defense giant General Dynamics, generates roughly $8.5 billion in IT services revenue and has the backing of a parent company with deep pockets and a diversified defense portfolio. Parsons Corporation, at $5 to $6 billion in revenue, competes in defense and infrastructure digital engineering. ManTech, which Carlyle Group acquired and took private in 2022 for approximately $4.2 billion, now operates as Arcfield with approximately $2.5 billion in revenue focused on cyber and intelligence work. Peraton, also private, generates roughly $7 billion in revenue in intelligence, space, and cyber.

The competitive dynamics among these companies are both cooperative and combative. On any given day, SAIC might be priming a contract with CACI as a subcontractor, and on the next day the roles might be reversed on a different program. The industry operates on a web of teaming agreements and subcontracting relationships that makes the competitive map far more complex than a simple market share analysis would suggest.

The more interesting competitive dynamic, however, is the emergence of what the industry calls the neoprimes. Companies like Palantir Technologies and Anduril Industries, the latter valued at approximately $30.5 billion, are challenging the traditional government contracting model with software-first, product-oriented approaches. Palantir's Foundry and Maven platforms and Anduril's autonomous systems represent a fundamentally different way of selling to the government: build a product, demonstrate its value, and then scale it across agencies, rather than embedding teams of cleared engineers to provide services on a contract-by-contract basis.

The neoprimes compete most directly for new technology programs rather than the sustaining operations and maintenance work that forms the backbone of SAIC's revenue. But the threat is real and growing. Executive orders in 2025 emphasized commercially available technologies, potentially favoring product companies over traditional services integrators. Industry analysts describe a "Fifth Defense Revolution" in which faster, leaner, software-first startups challenge legacy services firms.

SAIC's response has been twofold.

First, it acquired SilverEdge Government Solutions in late 2025 for approximately $205 million, gaining a SaaS platform called SOAR and an agentic AI product called MynAI designed for secure government environments. Agentic AI, to translate from the jargon, refers to AI systems that can take autonomous actions within defined parameters rather than simply answering questions or generating text. In a government context, this might mean an AI that can independently monitor network traffic, identify anomalies, and initiate defensive protocols without waiting for a human analyst to give it permission.

Second, it has been deliberately walking away from large, commoditized enterprise IT contracts where price competition is most intense and redirecting its resources toward mission IT and engineering work where differentiation is possible. Enterprise IT exposure is expected to decline from roughly seventeen percent of revenue in fiscal year 2025 to ten percent in fiscal year 2027.

The consolidation dynamic continues to reshape the landscape. Scale matters in government contracting because it determines which contracts you can prime and how much overhead you can spread across your revenue base. But scale also brings bureaucracy and the risk of losing the agility that wins competitive bids. SAIC sits in the middle of this tension: large enough to prime major programs but not so large that it cannot partner with the primes on even bigger ones. It is a strategic positioning that creates both opportunities and vulnerabilities.

X. Porter's Five Forces and Hamilton's Seven Powers

Understanding SAIC's competitive position requires examining the structural forces that shape the government services industry.

The threat of new entrants is low. The barriers to entry in government contracting are among the highest of any industry in the American economy.

Obtaining a Facility Security Clearance requires significant infrastructure investment, including the construction of SCIFs and the implementation of secure networks that meet government specifications. Personnel clearances take an average of 243 days to process. Beyond clearances, the Federal Acquisition Regulation requires agencies to evaluate past performance when awarding contracts, creating a classic chicken-and-egg problem for new entrants: you cannot win contracts without past performance, and you cannot build past performance without contracts.

Congress has actively reinforced these barriers. The fiscal year 2017 and 2018 National Defense Authorization Acts specifically restricted the use of lowest-price-technically-acceptable contracting for IT services, cybersecurity, systems engineering, and other knowledge-based professional services. This trend toward best-value contracting favors incumbents who can demonstrate superior technical solutions, not just low prices.

SAIC's total backlog of $21.9 billion represents decades of accumulated past performance that no newcomer can replicate quickly. The neoprimes have found wedges into the market through software products that bypass some of these barriers, but for traditional services work, the moat remains deep.

The bargaining power of the buyer is high, and this is the structural challenge at the heart of the business. The United States government is SAIC's only meaningful customer, accounting for approximately ninety-seven percent of revenue. The Department of Defense alone represents roughly fifty-two percent, with the DOD and intelligence community combined accounting for about seventy-five percent.

This is a textbook monopsony: one buyer with enormous leverage over pricing, contract terms, and payment schedules. The government can unilaterally exercise termination-for-convenience clauses, freeze spending through continuing resolutions, and shut down entirely during budget disputes. SAIC lost approximately $10 million per week in revenue during the thirty-five-day government shutdown of 2018-2019. Unlike government employees, contractor employees do not receive back pay, and payment delays can persist more than thirty days after the government reopens.

The Department of Government Efficiency has introduced additional uncertainty. DOGE reviewed over 400,000 open contracts in early-to-mid 2025, terminating or adjusting 390 of them. While SAIC reported minimal direct financial impact, the operational effects were real: procurement delays pushing expected contract awards from fiscal year 2026 into fiscal year 2027, high turnover of federal procurement personnel, and elongated decision cycles across agencies.

What partially offsets this power is the government's own dependency on contractors. The cleared workforce shortage means the Pentagon cannot easily insource the work it contracts out. Government pay scales are often uncompetitive for top technical talent, and the hiring process is too slow to absorb large workforces quickly. Mission criticality also provides balance: when a contractor is running a system that affects national security, the government is reluctant to switch providers mid-stream, regardless of its theoretical leverage.

Supplier power is moderate to high, driven almost entirely by the scarcity of cleared talent. Fifty-six percent of recruiters cite the limited cleared talent pool as their top hiring challenge. Cleared professionals command significant salary premiums, and the competition for cleared cyber, AI, and software engineers is particularly intense. SAIC competes for talent against every other company in the sector, plus the intelligence agencies themselves. Labor cost inflation is a persistent headwind, though cost-plus contract structures allow some of this inflation to be passed through to the customer.

The threat of substitutes is low to moderate. The government could theoretically insource more work, and indeed the Pentagon brought roughly 17,000 contractor positions in-house in 2010 alone. But practical constraints, including uncompetitive pay, slow hiring processes, and limited management capacity, make large-scale insourcing difficult. Cloud platforms and AI automation are creating substitution risk for routine IT tasks, which is precisely why SAIC is pivoting away from enterprise IT and toward mission-critical work where human judgment and domain expertise are less easily automated.

Industry rivalry is high. Six to eight well-capitalized competitors of similar scale fight over limited budget growth. Recompete cycles ensure regular competitive pressure, and the commoditized end of the market sees particularly intense price competition. Win rates on new business typically run between thirty and fifty percent, meaning that for every contract SAIC wins, it loses one or two others.

Hamilton Helmer's Seven Powers framework offers additional insight. SAIC's strongest power is switching costs. Embedded teams with institutional knowledge, security clearances, and deep relationships with program managers create significant friction for any government customer considering a change. The company's recompete win rate of eighty-five to ninety percent on non-enterprise-IT work reflects this advantage. Process power is also strong. Decades of navigating government procurement have created organizational capabilities in program management, compliance, and risk management that are difficult for competitors to replicate.

Scale economies are moderate. Overhead spreading across a larger revenue base helps, but this is not a manufacturing business where unit economics improve dramatically with volume. There are no factories to amortize, no chip fabrication lines to fill.

Cornered resource is moderate as well: the cleared workforce with domain expertise is scarce and valuable but not truly cornered, as competitors can and do poach. The relationships that SAIC's program managers have with their government counterparts are valuable, but they are personal rather than institutional, and they walk out the door when an employee leaves.

Network economies, counter-positioning, and branding are weak to nonexistent in this context. Government buying decisions are formal, process-driven evaluations rather than brand-driven choices.

The overall assessment is that SAIC occupies a position with moderate-to-strong moats in its core domains. The company generates solid returns protected by high barriers to entry and meaningful switching costs. But the monopsony customer structure and constant recompete dynamics impose a ceiling on growth potential that more structurally advantaged businesses do not face.

XI. Bear Case, Bull Case, and the Investment Thesis

The bull case for SAIC begins with the macro environment, and the macro environment has rarely been more favorable for defense contractors.

The fiscal year 2026 defense budget request crossed one trillion dollars for the first time in American history, a thirteen percent increase over fiscal year 2025 enacted levels. Spending on space surged more than thirty percent. Cyber spending reached $15.1 billion. AI and autonomy received $13.4 billion, the first year with a dedicated, separate budget line for these capabilities.

These are exactly the domains where SAIC has been investing through acquisitions and organic capability development. The great power competition framework that drives this spending has bipartisan support and is unlikely to reverse regardless of which party controls Washington.

The margin expansion story is real and measurable. SAIC's adjusted EBITDA margin has improved from the mid-single digits at the time of the 2013 split to 9.5 percent in fiscal year 2025, with guidance pointing toward 9.9 to 10.1 percent in fiscal year 2027. The deliberate walk-away from low-margin enterprise IT work is painful in the short term, reducing revenue by an estimated two to four percent organically, but it concentrates the remaining portfolio on higher-value mission integration work that commands better economics.

Free cash flow generation is strong and improving. Preliminary fiscal year 2026 free cash flow of $570 to $575 million on a market capitalization of roughly $4.0 to $4.6 billion implies a free cash flow yield of twelve to thirteen percent. The company is using that cash to buy back shares aggressively, with a $1.2 billion authorization providing substantial support, and to pay dividends that it has maintained for thirteen consecutive years.

The valuation argument is straightforward. SAIC trades at roughly ten to eleven times forward earnings and eight to nine times EV/EBITDA, a significant discount to peers like Booz Allen Hamilton at more than twenty times earnings and CACI at eighteen to twenty times. The stock sits near its fifty-two-week low of $84.19, having fallen from an all-time high of $152.61 reached in November 2024. A $10,000 investment in SAIC in March 2015 with dividends reinvested had grown to approximately $23,115 by March 2025, a total return of 131 percent.

If the revenue trajectory stabilizes and the market gains confidence in the margin expansion story, multiple expansion could drive meaningful returns even without dramatic earnings growth.

The bear case is equally compelling.

Revenue contraction is not a theoretical risk. It is happening now. Fiscal year 2027 guidance calls for revenue of $7.0 to $7.2 billion, implying organic decline of two to four percent, driven by the recompete losses and the deliberate runoff of enterprise IT work. When the company announced these numbers on February 11, 2026, the stock fell 10.4 percent in a single day. The company is asking investors to believe that losing revenue today will create a better business tomorrow, and that is a leap of faith that the market has historically been reluctant to take.

Leadership instability is a genuine concern. SAIC has had three CEOs in roughly two years. Tony Moraco served from the 2013 split until July 2019. Nazzic Keene served from August 2019 until October 2023. Toni Townes-Whitley was removed without cause on October 23, 2025, after barely two years in the role, with the board stating that it "wanted the company to move in a different direction."

Jim Reagan served as interim CEO from that date and was appointed permanent CEO effective February 17, 2026. Reagan has been on the SAIC board since January 2023 and brings nearly forty years of government services experience, including a stint as CFO of Leidos. But any time a board cycles through leaders this quickly, it raises questions about strategic direction and organizational stability. A November 2025 organizational restructuring from five business groups into three brought what Washington Technology described as "a wave of senior executive departures," adding to the perception of disruption.

The DOGE factor introduces uncertainty that is difficult to model. While SAIC reported minimal direct profit-and-loss impact from DOGE in fiscal year 2026, the operational effects are real: procurement delays, elongated decision cycles, high turnover of federal procurement personnel, and a general atmosphere of uncertainty that makes government buyers cautious about committing to new programs. If DOGE-driven efficiency reviews lead to sustained budget pressure on government services contracting, the impact could be significant.

Technology disruption from the neoprimes is a slow-moving but potentially structural threat. Palantir and Anduril are building product-based businesses that could eventually displace services revenue in AI, analytics, and autonomy. SAIC's SilverEdge acquisition is a hedge against this risk, but a $205 million acquisition of a small AI company is not the kind of move that fundamentally changes a $7 billion company's competitive position.

The honest assessment is that SAIC is a business caught between two narratives. The optimistic narrative says it is a disciplined company trading at a discount, generating enormous free cash flow, expanding margins, and positioned in growing defense markets. The pessimistic narrative says it is a mature services business with a shrinking revenue base, an unstable leadership team, and a customer that has all the leverage. Which narrative proves correct will depend largely on whether the book-to-bill ratio, currently running at 1.3 times year-to-date in fiscal year 2026, can sustain above 1.0 and whether the margin expansion trajectory continues.

XII. Strategic Questions and Future Scenarios

The most important strategic question facing SAIC is whether it can move further up the value chain, from integrator to something closer to a platform or product company. The SilverEdge acquisition, with its MynAI agentic AI product and SOAR SaaS platform, represents a tentative step in this direction. But the history of government services companies trying to become product companies is not encouraging. The capabilities required to build and sell reusable software products are fundamentally different from the capabilities required to embed engineers in government facilities and manage complex programs. SAIC has been a services company for its entire existence, and changing that DNA is a generational challenge.

The M&A strategy ahead is another critical question. The Engility deal worked. The Unisys Federal deal appears to have worked. The SilverEdge deal is too early to evaluate. The pattern suggests that SAIC has developed a competency in acquiring and integrating companies, which in an industry undergoing consolidation is a valuable skill.

More Engility-style deals to add scale in defense and intelligence are possible. Tuck-in technology acquisitions to build capabilities in AI, cyber, and space are likely. And the possibility that SAIC itself could be an acquisition target, particularly given its depressed valuation and strong free cash flow, is not lost on the market. At a market capitalization of roughly $4 to $4.6 billion and with free cash flow exceeding $570 million annually, the company generates enough cash to pay back an acquisition premium relatively quickly. A private equity firm or a larger prime contractor looking to build its services portfolio could find SAIC attractive at current prices.

The question of commercial diversification looms again, as it does periodically for every government contractor. Past attempts failed badly, and the consensus in the industry is that the skills required to succeed in commercial markets are different enough from government contracting that diversification destroys more value than it creates. But adjacencies in critical infrastructure, energy, and health could be worth exploring if the government services market enters a prolonged downturn.

The defense tech partnership question is perhaps the most interesting strategic dilemma. Should SAIC partner with companies like Palantir and Anduril, or compete against them? The traditional primes have been partnering: Lockheed Martin works with Palantir on various programs, and Northrop Grumman has explored relationships with defense tech startups. SAIC's integration capabilities could complement the neoprimes' product capabilities in ways that create value for both parties. Alternatively, SAIC could try to build competing capabilities internally, though the track record of large services companies competing against nimble software-native startups is not inspiring.

The five-year scenarios span a wide range. The base case envisions steady three-to-five percent revenue growth once the enterprise IT runoff stabilizes, continued margin expansion toward ten percent or better, solid free cash flow generation, and an independent SAIC that compounds value through operational execution and capital returns. The bull case sees a defense upcycle driving seven-to-ten percent growth, a margin breakthrough as the portfolio shifts further toward high-value work, and a re-rating from discount to premium valuation. The bear case imagines sustained budget pressure from DOGE or fiscal austerity, technology disruption from the neoprimes, stagnant revenue, and a potential acquisition at a modest premium. The transformation case involves a major technology acquisition or partnership that fundamentally remakes the business model, though this seems least likely given the company's conservative culture.

XIII. Lessons for Founders, Operators, and Investors

The SAIC story offers several lessons that extend well beyond the defense contracting industry.

The first is about when to split. The 2013 separation of SAIC into Leidos and the new SAIC created value for both entities. Leidos went on to become a $16 billion defense and technology company. The new SAIC, despite being the smaller piece, tripled its stock price in the six years following the split. The lesson is that when two businesses with different growth profiles, different margin structures, and different customer needs are trapped inside one corporate body, the act of separation itself can unlock value by allowing each business to be managed and valued on its own terms.

The second lesson is about the focus premium. The pre-split SAIC tried to be everything to everyone: commercial and government, IT services and technical services, consulting and integration. The result was an unfocused conglomerate that tripped over its own organizational conflicts. The post-split SAIC was smaller but sharper, and the focus allowed it to build a coherent strategy around mission integration for national security customers. Trying to be everything to everyone diluted the company's competitive advantage. Refocusing restored it.

The third lesson is about M&A discipline. The pre-split SAIC's acquisition strategy destroyed value through poor integration and misguided diversification. The post-split SAIC's acquisition strategy, particularly the Engility deal, created value through disciplined target selection and effective integration. The difference was not luck. It was learning. Moraco and his team studied what had gone wrong before the split and applied those lessons to how they evaluated and integrated acquisitions afterward.

The fourth lesson is about customer concentration. Having the U.S. government as your only meaningful customer creates a unique set of challenges and protections. The challenges are obvious: budget uncertainty, political gridlock, government shutdowns, and the ever-present risk of losing a recompete. The protections are less obvious but equally real: the government is an enormously stable customer that pays its bills, the barriers to entry are extraordinarily high, and the mission criticality of the work creates switching costs that partially offset the buyer's monopsony power.

The fifth lesson is about talent as product. In a services business, the people are the product. SAIC's most valuable asset is not its technology or its contracts but the 26,000 cleared professionals who walk out the door every evening. Beyster understood this intuitively, which is why he built the employee ownership model. The modern SAIC has lost that structural alignment but still faces the same fundamental reality: recruiting and retaining cleared talent is not a support function. It is the core competency.

The operational lesson from CityTime is perhaps the most sobering. A $63 million no-bid contract became a $720 million fraud because oversight mechanisms failed at every level. SAIC's decentralized culture, which had been such an advantage in winning and executing technical work, became a liability when it came to policing a subcontractor relationship in a commercial environment. The lesson is that program execution is everything in government contracting, and that the risks of inadequate oversight compound in ways that can threaten the entire enterprise.

For investors, the SAIC story illustrates the hidden value that corporate restructurings can create. The market often underprices the complexity of splits, treating the smaller entity as a throwaway. SAIC's trajectory from the low twenties at the time of the split to above $150 at its all-time high demonstrates what can happen when a focused management team executes a coherent strategy within a favorable industry structure. It also illustrates the limits of the government contractor business model: steady, predictable cash flows that compound wealth over time but rarely produce the explosive growth that captures headlines.

XIV. Epilogue and Current State

SAIC stands today at a crossroads that feels both familiar and new.

The company generated $7.48 billion in revenue in fiscal year 2025 with adjusted EBITDA of $710 million, net income of $362 million, and free cash flow of $499 million. Adjusted diluted earnings per share were $9.13.

Preliminary fiscal year 2026 results point to revenue of approximately $7.26 billion with free cash flow improving to $570 to $575 million despite the top-line softness. Margins came in above expectations due to strong execution and operational efficiency. Adjusted EPS is expected in the range of $10.40 to $10.60. Management attributed the revenue shortfall to a government shutdown, weather disruptions, and procurement delays rather than structural demand erosion.

Total backlog stands at approximately $21.9 billion, with $20 billion in submitted bids awaiting decisions. The book-to-bill ratio, which dipped below 1.0 in fiscal year 2025, recovered to 1.3 times year-to-date in fiscal year 2026, suggesting that the pipeline is rebuilding.

The stock tells a more complicated story. From its post-split low of roughly $24 in 2013, SAIC shares rose to an all-time high of $152.61 in November 2024, a six-fold increase that rewarded patient shareholders who understood the turnaround thesis.

But from that peak, the stock has fallen roughly forty-four percent to trade near $86 to $97 as of February 2026, driven by the revenue guidance cut, the CEO transition, and DOGE-related uncertainty. The decline has been more severe than what peers like Booz Allen and CACI experienced over the same period, reflecting the market's specific concerns about SAIC's revenue trajectory and leadership stability.

The current price implies a trailing P/E of roughly ten to thirteen times and a free cash flow yield of twelve to thirteen percent, metrics that look either cheap or justified depending on your view of the revenue trajectory.

The CEO transition is the most immediate source of uncertainty. Jim Reagan, who served as interim CEO since Townes-Whitley's departure on October 23, 2025, was appointed permanent CEO effective today, February 17, 2026. Reagan brings nearly forty years of government services experience and the credibility of having served as CFO of Leidos. In November 2025, the company consolidated from five business groups into three: Army Navy, Air Force Space and Intelligence, and Civilian. The reorganization brought a wave of senior executive departures, and Bob Ritchie was named Chief Growth Officer in September 2025, merging the CTO and business development functions.

The strategic direction under Reagan appears to be a continuation and acceleration of the pivot away from commodity enterprise IT toward higher-value mission integration and technology transformation work. Enterprise IT exposure is expected to decline from seventeen percent of revenue to ten percent. Management has been careful to note that "not all enterprise IT is alike." Civilian enterprise IT work, typically structured as fixed-price or time-and-materials contracts, is being retained. It is the large DoD cost-plus enterprise IT contracts, where price competition is fiercest and margins thinnest, that SAIC is deliberately shedding.

The SilverEdge acquisition represents the company's most explicit bet on becoming more than a traditional services integrator. Recent contract wins tell a story of a company that can still compete at the highest levels: the $1.8 billion System Software Lifecycle Engineering contract, the $1.4 billion COBRA task order, a $1.8 billion PRISM multiple-award contract for DoD personnel and readiness infrastructure, and the $928 million Air Force TENCAP contract. These are not commodity IT programs. They are complex, mission-critical engagements that demand deep domain expertise.

The invisible giant paradox persists. SAIC does mission-critical work that most Americans will never hear about, in facilities they will never enter, on systems they will never see. Its engineers architect the classified cloud environments where intelligence analysts do their work. Its systems integrators connect satellites to warfighters. Its cybersecurity experts defend networks that adversaries probe around the clock. This work is essential, it is well-compensated, and it generates the kind of steady, predictable cash flows that compound over decades.

What SAIC has never been able to do, and may never be able to do, is tell its story in a way that captures the imagination of a market that rewards growth narratives over cash flow narratives. Beyster's company was built on the premise that technical excellence would speak for itself, that the work was its own advertisement. Half a century later, in a market that seems to value visibility as much as substance, that premise is being tested as never before.

XV. Further Reading and Resources

For those who want to go deeper into the SAIC story and the government contracting ecosystem, the following resources provide essential context.

J. Robert Beyster's The SAIC Solution, published in a second edition in 2014, is the founder's own account of building the employee-owned company and his analysis of what went wrong when the board pursued the IPO. It remains the most authoritative primary source on SAIC's culture and ownership model, and Beyster's reflections on governance failures are relevant to anyone studying the lifecycle of founder-led companies.

Annie Jacobsen's The Pentagon's Brain provides the broader context of the defense research and development industrial complex that gave birth to companies like SAIC. Gregg Herken's Brotherhood of the Bomb explores the nuclear weapons laboratory culture that shaped Beyster and many of his early employees.

James Bamford's Body of Secrets, a history of the National Security Agency, offers insight into one of SAIC's most important but least discussed customers. The intelligence community's relationship with contractors like SAIC is one of the most consequential and least understood dynamics in American national security.

The SEC filings surrounding the 2013 split, available through the EDGAR database for both Leidos and SAIC, provide granular detail on the transaction mechanics, strategic rationale, and financial separation. The Center for Strategic and International Studies defense budget analyses offer the macro context for understanding how federal spending cycles affect companies like SAIC. Government Accountability Office reports on defense acquisition and contracting dynamics provide the regulatory perspective.

The CityTime investigation reports and settlement documents, available through the Southern District of New York and New York City records, document the fraud that reshaped SAIC's approach to risk management. The Beyster Institute at UC San Diego's Rady School of Management continues to publish research on employee ownership models that draws on the SAIC experience.

Defense News, Washington Technology, and Federal Times archives provide the real-time record of industry consolidation, contract awards, and competitive dynamics. Washington Technology's annual Top 100 contractor rankings offer a longitudinal view of how the industry's power structure has shifted over the decades. For financial analysis, the research published by firms covering the defense services sector provides detailed competitive positioning and valuation frameworks that place SAIC in the context of its peer group.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube