Royal Bank of Canada: The Canadian Crown Jewel and the Battle for North America

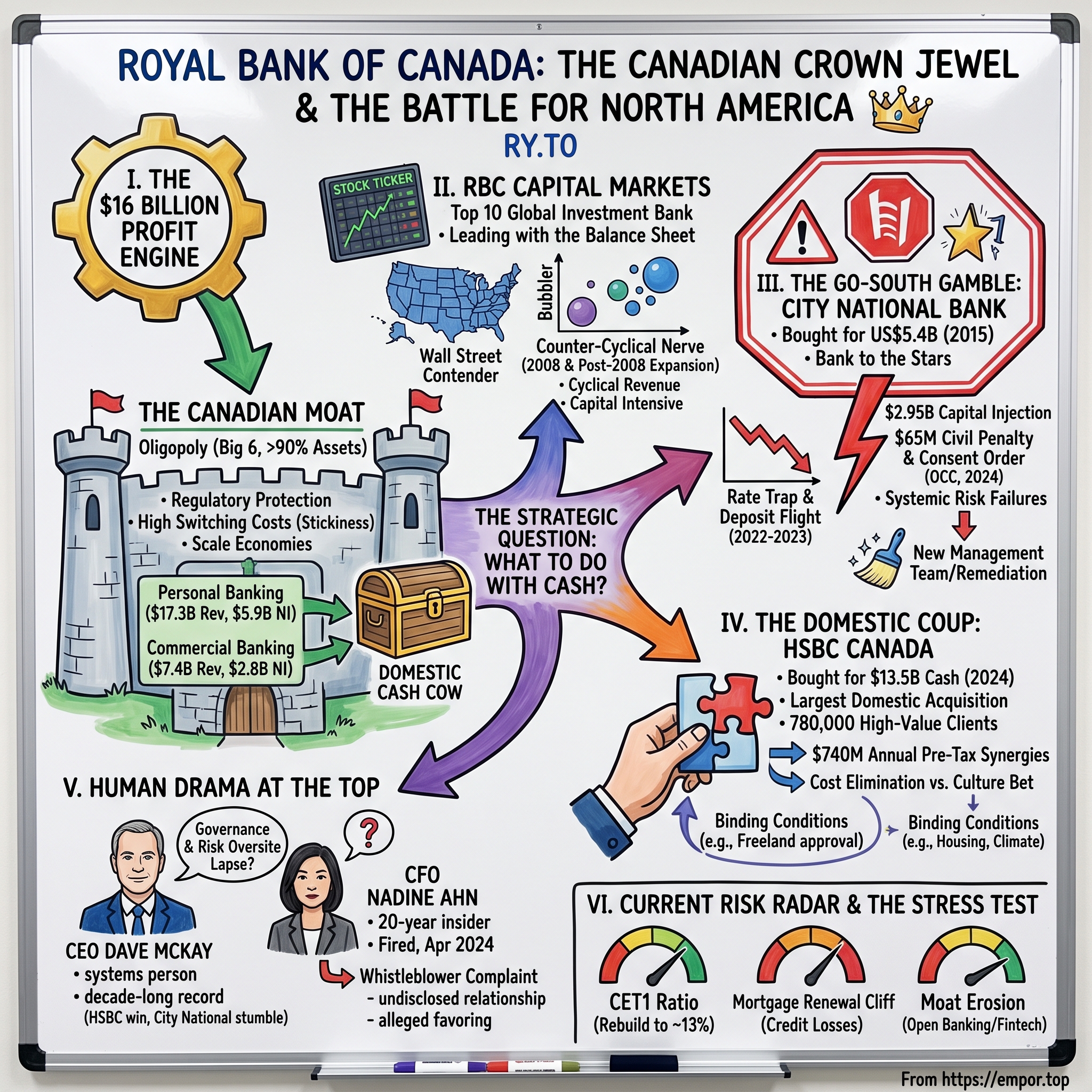

I. Introduction & The $16 Billion Profit Engine

Picture the boardroom on the 44th floor of Royal Bank Plaza in downtown Toronto, the twin gold-tinted towers that catch the winter light off Lake Ontario. Behind the glass sits an institution that most people outside Canada could not name, yet that ranks among the ten most profitable and most valuable banks on the planet. In its 2024 fiscal year, Royal Bank of Canada earned $16.2 billion in net income — a figure larger than the entire annual output of many national economies — and it did so from a home market of roughly 40 million people, fewer residents than the state of California.12

That is the paradox worth sitting with. How does a bank domiciled in a mid-sized country, in an industry that is supposed to be a low-growth utility, become a global heavyweight? The short answer is that Canada does not really have a competitive banking market at all. It has an oligopoly — a tightly held club of six large banks, protected by a century of federal law, that behaves less like a scrum of rivals and more like a cartel that everyone in Ottawa has quietly agreed is good for the country. And Royal Bank of Canada, which trades as RY on both the Toronto Stock Exchange and the New York Stock Exchange, sits at the very top of that club.

Here is the deeper mechanism, and the tension that animates this entire story. RBC runs a domestic retail and commercial bank that is, for practical purposes, a licensed printing press: high-margin, low-volatility, sheltered from foreign competition, and throwing off billions in cash every quarter with metronomic reliability. The strategic question that has consumed three decades of RBC leadership is what to do with all that cash. You cannot simply reinvest it at home — the Canadian market is saturated, and the regulator will not let you buy your neighbors. So the bank takes the winnings from its safe domestic casino and wagers them on far riskier tables abroad: a top-ten global investment bank competing with Goldman Sachs, a Los Angeles private bank that caters to Hollywood, and the occasional multi-billion-dollar acquisition.

Sometimes those bets pay off spectacularly. Sometimes they nearly blow up. This is a story about both.

Consider the roadmap for what follows. First, the Canadian fortress itself — the structural machinery of the "Big Six" and why it is one of the most durable competitive moats in global finance. Second, RBC Capital Markets, the quietly enormous Wall Street contender that most retail shareholders forget the bank even owns. Third, the "go-south" gamble embodied by City National Bank, the "bank to the stars" that turned into a multi-billion-dollar remediation headache. Fourth, the domestic coup: the $13.5 billion cash purchase of HSBC's Canadian business in 2024, the largest bank acquisition in Canadian history.3 And finally, the human drama at the top — a long-tenured CEO, a $65 million regulatory fine, and a chief financial officer marched out the door in a scandal that read like corporate pulp fiction.45

The thread connecting all of it is a single strategic engine, so let us begin where the money is actually made: inside the Canadian moat.

II. The Canadian Moat: The Big Six Oligopoly and How RBC Wins

To understand why RBC is so profitable, forget the bank for a moment and look at the country's grocery aisle. In Canada, three companies control most of the supermarkets, two railways move most of the freight, a handful of carriers dominate wireless, and — most consequentially for this story — six banks control the money. The "Big Six" — Royal Bank of Canada, Toronto-Dominion, Bank of Montreal, CIBC, Scotiabank, and National Bank — together command well over 90% of domestic banking assets. It is one of the most concentrated banking markets in the developed world, and it is concentrated by design, not by accident.

The design has a name and a history. Canadian banking is governed by the federal Bank Act, a piece of legislation that is reviewed and renewed on a roughly five-year cycle — a recurring ritual in which Parliament reconsiders the rules of the game. Two features of that law matter enormously. The first is a "widely held" rule: any bank with substantial equity must limit single-shareholder ownership, which makes a hostile takeover of a major Canadian bank effectively impossible. The second is a long-standing political consensus that the government simply will not allow the biggest banks to combine with each other or to be swallowed by foreigners.

The moment that crystallized this consensus is worth recounting, because RBC itself was at the center of it. In 1998, RBC and the Bank of Montreal announced plans to merge, and — in a rush of competitive anxiety — CIBC and Toronto-Dominion promptly announced their own tie-up in response. Two mega-deals were suddenly on the table that would have collapsed the Big Five into a Big Three. The banks argued they needed the scale to compete globally. Ottawa disagreed. Then-Finance Minister Paul Martin rejected both mergers outright, citing an unacceptable concentration of economic power and reduced competition for ordinary Canadians. It was a defining act of state, and its message echoed for a generation: the incumbents may keep their protected, profitable market, but they may not use it to consolidate into an even smaller club or sell themselves to outsiders. The garden is walled — but the gardeners do not get to merge their plots either. That single decision is why, more than a quarter-century later, there are still six large banks rather than three, and why the only permitted form of consolidation is picking off a departing foreign player like HSBC. The message to any would-be disruptor, domestic or foreign, has been consistent for a century: this club is closed, and its membership is fixed.

Reading the moat through Helmer's lens

Hamilton Helmer's "7 Powers" framework offers a useful vocabulary for what this produces, and three of his powers map onto RBC almost perfectly.

The first is what Helmer calls a Cornered Resource — control of a coveted asset that competitors cannot replicate. In RBC's case the cornered resource is not a patent or an oil field; it is the banking charter itself, and the regulatory umbrella of the Office of the Superintendent of Financial Institutions (OSFI). New charters for a scaled, deposit-taking national bank are, in practice, not being handed out. Foreign giants are hemmed in by ownership limits. The upshot is that the incumbents were handed a walled garden and told to tend it. There is a genuine analytical point here for investors: RBC's returns are not primarily a reward for cleverness, they are a reward for incumbency inside a structure the state has chosen to protect. That is both the bull case and the thing to watch, because moats granted by policy can, in principle, be modified by policy.

The second power is Switching Costs. Ask any Canadian how often they change their primary bank and the answer is: almost never. Moving a primary chequing account is not a matter of a single click. It means re-pointing your payroll direct deposit, re-establishing every pre-authorized bill payment, migrating a mortgage, untangling a line of credit, possibly moving a brokerage and a wealth-management relationship — all while trusting that nothing breaks mid-cycle. The friction is partly administrative and partly psychological: people treat their bank the way they treat their family doctor, as a relationship you inherit and rarely question. This is why Canadian banks enjoy famously low customer churn, and why RBC can hold the largest base of primary-chequing relationships in the country without constantly discounting to defend it.

The third power is Scale Economies. Banking is a business of enormous fixed costs — technology platforms, compliance departments, branch networks, cyber-security, regulatory reporting — spread across a customer base. RBC has the largest retail customer base in Canada, which means it spreads those fixed costs more thinly per customer than anyone else. The bank has invested heavily in digital tooling, including a proprietary AI-driven assistant marketed as NOMI that nudges customers about spending and savings, precisely because a dollar spent on a platform used by 17 million clients is cheaper per head than the same dollar at a smaller rival. Scale in banking is not glamorous, but it compounds quietly into the lowest cost of doing business.

The crown jewel, in numbers that actually mean something

Where does the money come from? Overwhelmingly, from Canadian households and businesses. In fiscal 2024, RBC's Personal Banking segment generated roughly $17.3 billion in revenue and $5.9 billion in net income, and its Commercial Banking segment added about $7.4 billion in revenue and $2.8 billion in net income.16 Put those two together and the domestic retail-and-commercial engine produced on the order of $8.7 billion of profit — more than half of the bank's entire $16.2 billion bottom line.1 Everything else the bank does — the global investment bank, the wealth franchise, the insurance arm, the American adventures — is, in aggregate, the minority partner to this one dominant business.

The analytical conclusion matters more than the digits. A bank that mints the majority of its profit from a protected, low-loss, high-switching-cost domestic deposit franchise is a bank that can absorb a great deal of pain elsewhere without threatening its own survival. That is the true meaning of the moat: not that RBC never makes mistakes, but that its core cash machine is insulated enough to fund the mistakes.

The scoreboard bears this out. RBC has consistently produced return on equity in the mid-teens — 14% to 16% through most of the past decade, and 17.3% as recently as the third quarter of fiscal 2025 — a level of profitability that most large American and European banks can only envy, and that reflects both the pricing power of the oligopoly and the low cost of its deposit funding.7 When your raw material (customer deposits) is cheap and sticky, and your competitors are five banks who have no particular incentive to start a price war, the economics take care of themselves.

Benchmarking the winner against the club

It is worth being precise about how RBC wins even inside a group that all enjoy the same protected market, because "everyone in the oligopoly is rich" is not the same as "everyone in the oligopoly is equal." The Big Six are not identical. Toronto-Dominion built the largest retail branch presence and pushed hardest into the United States — a strategy that, as we will see, blew up spectacularly on the compliance front. Bank of Montreal and Scotiabank pursued their own foreign bets, BMO into California and the U.S. Midwest, Scotiabank into Latin America. CIBC and National Bank stayed more domestically focused. RBC's distinction is that it built the broadest, most balanced franchise of the group — number one or number two in virtually every domestic product category, from mortgages to credit cards to mutual funds — while keeping the largest single base of primary-chequing relationships in the country.

That primary-chequing dominance is the quiet engine of everything. A primary chequing account is where a customer's paycheck lands and their bills flow out, and it is the cheapest, stickiest deposit a bank can hold — money that mostly sits there earning the bank a spread while paying the customer almost nothing. Because RBC holds more of these anchor relationships than any rival, it enjoys structurally one of the lowest costs of retail deposits in Canada, which flows straight through to its net interest margin. Layer on the largest customer base over which to spread fixed technology spend, and RBC's advantage compounds: cheapest funding, lowest cost per customer, widest product shelf. Against that, a challenger bank or a fintech trying to buy its way in has to offer higher deposit rates to attract money it cannot make sticky — the exact opposite of RBC's position.

The scale is genuinely difficult to overstate. RBC intermediates well over a trillion dollars of Canadian deposits and serves on the order of 17 million clients, and it reinvests billions annually into technology and digital platforms — including its NOMI suite of AI-driven money-management features embedded in the mobile app — precisely to keep that customer base engaged and to lower the marginal cost of serving each one.2 The strategic point for an investor is that this is a self-reinforcing loop rather than a static advantage: scale funds the technology, the technology deepens engagement, engagement lowers churn, low churn protects the cheap deposit base, and the cheap deposit base funds the next round of scale. This is what a durable moat looks like from the inside.

But a cash cow this rich creates a peculiar problem — the problem of what to do next — and to understand how RBC came to face that problem, we have to go back to a wharf in Halifax during the American Civil War.

III. Succinct History: From Halifax Gold to the Great Financial Crisis

In 1864, the port of Halifax on Canada's Atlantic coast was booming on other people's war. To the south, the United States was tearing itself apart, and the Nova Scotian merchants who traded in fish, timber, sugar, and gold needed a place to finance cargoes and hold the proceeds. A group of them founded the Merchants' Bank of Halifax to do exactly that — a small, regional, trade-financing institution with saltwater in its veins. It was, in the most literal sense, a bank built to move money across water.

For our purposes the early decades can be compressed, because what matters is the trajectory rather than every branch opening. The Merchants' Bank grew, followed the country's economic center of gravity westward and inland, and in 1901 rechristened itself the Royal Bank of Canada — a name chosen to signal ambition well beyond the Maritimes. It shifted its operational weight first toward Montreal, then the dominant financial capital, and eventually toward Toronto, which over the twentieth century became the undisputed heart of Canadian finance. Branch by branch, the bank stitched itself into the fabric of a young country expanding across a continent.

Why the boring model was the brilliant model

The single most important inheritance from this history is a philosophical one, and it explains a great deal about the modern bank. Canada chose, very early, a national branch-banking model — a handful of large banks operating branches from coast to coast under a single federal regulator. The United States chose the opposite: thousands of small "unit banks," often restricted to a single state or even a single location, fragmented and locally captive.

The consequences showed up violently in the 1930s. During the Great Depression, more than 9,000 American banks failed, wiping out savings and deepening the misery. Canada did not lose a single major bank. A diversified, nationally branched bank could offset a bad harvest in Saskatchewan with a good year in Ontario; a tiny unit bank on the American plains had nowhere to hide when its local economy cratered. Canadians drew a lesson their institutions never forgot: in banking, resilience beats fragmentation, and safety is a feature worth paying for. The regulator that eventually became OSFI institutionalized that preference, prioritizing solvency and system stability over the free-for-all dynamism of the American model.

The 2008 stress test that changed everything

Fast-forward to the event that gave modern management its swagger. When the global financial crisis detonated in 2008, the world's marquee banks — Lehman Brothers, Bear Stearns, Royal Bank of Scotland, Citigroup — either collapsed or survived only on government life support. Across the Canadian border, RBC and its Big Six peers sailed through without a single government bailout, without emergency capital injections, and without the existential terror that gripped Wall Street and the City of London. Canada's conservative capital rules, its aversion to the most toxic subprime engineering, and the diversified strength of the domestic franchise turned the country's banks into a global advertisement for prudence. The World Economic Forum spent years afterward ranking Canada's banking system the soundest in the world.

There is a myth worth puncturing here, because the "Canadian banks are simply prudent by nature" story is only half true. Canada's banks did not avoid the crisis purely through superior virtue; they avoided it because the structure they operate in removed the temptation. A concentrated oligopoly with fat, protected domestic margins has less need to reach for yield in exotic subprime products than a fragmented, hyper-competitive market where thin margins push everyone toward risk. Safety, in other words, was partly a by-product of the moat itself — profitable incumbents do not have to gamble. That distinction matters, because it means RBC's celebrated conservatism is strongest exactly where the moat is strongest (at home) and weakest where the moat disappears (abroad), a pattern that the City National chapter would later confirm in painful detail.

The importance of 2008 is nonetheless real, and not merely reputational, though the "safe-haven fortress" brand became a genuine asset. It is psychological and strategic. Emerging from the crisis stronger than nearly every peer, RBC's leadership acquired the confidence — some would later argue overconfidence — to go hunting. If the domestic franchise was this unshakeable, why not use its ballast to pursue ambitions abroad? That conviction would, within a decade, send the bank into Wall Street trading floors and Beverly Hills wealth offices. The first of those adventures was the least visible and, for a long time, the most successful: the quiet construction of a global investment bank.

IV. RBC Capital Markets: Building a Canadian Wall Street Contender

Walk into the trading floor of RBC Capital Markets in midtown Manhattan and you would be forgiven for forgetting you were dealing with a Canadian institution at all. There are no beavers on the wall, no polite apologies. There are rows of traders and bankers underwriting bonds, syndicating loans, and pitching M&A to American corporates — the full apparatus of a Wall Street investment bank, owned by a company most Americans associate, if they associate it with anything, with hockey sponsorships.

This is the most underappreciated fact about Royal Bank of Canada. While retail investors picture a sleepy domestic lender, RBC has spent three decades assembling one of the ten largest investment banks in the world. In fiscal 2024, the Capital Markets segment produced roughly $12.0 billion in revenue and $4.6 billion in net income — on the order of 28% of the entire bank's profit.16 That is not a rounding error bolted onto a retail bank; it is a top-tier global franchise hiding inside one.

How a provincial bank built a Wall Street business

The strategy is a clinic in exporting a domestic advantage, and it is worth slowing down to understand the mechanism, because it explains both the wins and the risks. Recall that RBC's Canadian deposit base is enormous, sticky, and cheap. That gives the bank something most independent investment banks lack: a low-cost, reliable pool of funding and a fortress balance sheet. RBC discovered it could use that balance sheet as a wedge. Offer a mid-sized American utility or infrastructure company a large, competitively priced credit facility or debt syndication — something that requires balance-sheet muscle — and you earn a seat at the table. Once seated, you cross-sell the high-margin work: the advisory mandate, the bond underwriting, the M&A assignment. In banker's shorthand, RBC "led with the balance sheet" and monetized the relationship on the way through.

The choice of where to compete was as important as the decision to compete at all. RBC did not try to out-Goldman Goldman Sachs or out-Morgan Morgan Stanley in the mega-cap, blue-chip, bulge-bracket arena where those franchises are nearly unassailable. Nor did it repeat the catastrophic error of the European universal banks — Deutsche Bank most infamously — who spent the 2000s trying to build sprawling global investment banks to rival the Americans and mostly succeeded in importing enormous risk and enormous losses. Instead, RBC concentrated on the middle market: mid-cap corporates, utilities, energy, and infrastructure advisory, plus a genuinely strong North American debt franchise. It picked a lane where its balance-sheet-led model was a real edge and where the bulge bracket paid less attention, and it ground out share year after year.

The build was patient and, at times, opportunistic. RBC entered U.S. investment banking in earnest with the roughly US$1.5 billion acquisition of the Minneapolis-based securities firm Dain Rauscher, announced in September 2000 and completed in January 2001, which gave it a beachhead and a distribution network in the American mid-market.18 It then did what disciplined acquirers do in a crisis: it hired aggressively while rivals retrenched. In the aftermath of 2008, when the bulge-bracket banks were shedding talent and licking their wounds, RBC — flush with the credibility of a bank that had needed no bailout — poached senior bankers, expanded its coverage teams, and pushed deeper into U.S. equities, debt capital markets, and advisory. A crisis that shrank its competitors became a recruiting event for RBC. Over the following fifteen years the franchise climbed steadily up the global league tables in debt underwriting and syndicated lending, and secured a durable place in the global top ten by fees — a remarkable outcome for an institution that most of Wall Street had once regarded as a polite Canadian afterthought.

The lesson embedded in this build is one about counter-cyclical nerve. RBC's Capital Markets ascent was not primarily a story of financial wizardry; it was a story of a bank whose safe domestic base let it lean into the market precisely when everyone else was forced to retreat. That is the moat working at one remove — the fortress at home funding aggression abroad at exactly the moment aggression was cheapest.

The catch: this engine is cyclical, and it eats capital

Here is where the neutral lens matters. Capital Markets is lucrative, but it is nothing like the placid Canadian retail business — and the contrast is the whole point. Trading and underwriting revenues swing with market conditions; a booming year for deals can be followed by a frozen one. More importantly, the business is capital-intensive: holding trading inventory, extending large credit facilities, and warehousing risk all consume the bank's regulatory capital, specifically its Common Equity Tier 1 (CET1) ratio, the core measure of how much loss-absorbing equity a bank holds against its risk-weighted assets. When Capital Markets grows aggressively, it can eat into that buffer and, in effect, compete for capital with the bank's other ambitions — including acquisitions.

So the analytical read on RBC Capital Markets is genuinely two-sided. On one hand, it is proof that RBC's management can build a world-class business from scratch and that the "cheap Canadian funding as a weapon" thesis is real. On the other, it injects earnings volatility and capital intensity into an institution whose entire valuation premium rests on stability. The market tends to pay a high multiple for the boring Canadian retail earnings and a lower one for the cyclical trading earnings — which means the more RBC leans on Capital Markets, the more it risks being re-rated toward a Wall Street multiple rather than a fortress multiple.

That tension — between the stable cash cow and the riskier growth engine — was about to play out in an even more dramatic key. Because at the same time RBC was quietly winning on Wall Street, it decided the real prize lay 4,000 kilometers to the southwest, in the wealth vaults of Los Angeles.

V. The Go-South Gamble: The "Bank to the Stars" and the City National Crisis

Russell Goldsmith liked to say that his bank did not chase clients; it earned them, one relationship at a time, and then kept them for life. For decades that pitch made City National Bank a legend in Los Angeles. Founded in 1954 and headquartered on the edge of Beverly Hills, City National had cultivated an almost mythical roster: film studios, entertainment law firms, talent agencies, and the individual movie stars, directors, and moguls who banked their fortunes there. Frank Sinatra had been a client. The bank leaned into the aura, nicknaming itself the "bank to the stars." Its business was high-touch private banking — the sort where a banker knows your accountant, your agent, and your children's names, and where the product is service and discretion rather than the best interest rate.

For a saturated Canadian bank hunting for growth, City National looked like the perfect trophy.

The 2015 purchase: a platform for the American dream

In January 2015, RBC announced it would acquire City National Corporation for approximately US$5.4 billion, a deal structured roughly half in cash and half in RBC stock, and completed it in November of that year.89 Russell Goldsmith stayed on to run what became RBC's U.S. wealth-management platform. The strategic logic was seductive and, on paper, coherent: bolt a premier American private bank onto RBC's existing U.S. wealth and capital-markets operations, and you have a growth engine aimed squarely at the wealthiest, fastest-compounding pool of clients in the world. This was the "go-south" strategy in its purest form — take the winnings from the Canadian oligopoly and buy a foothold in the American high-net-worth market that Canada could never organically supply.

For several years the story worked well enough. City National grew, expanded beyond Los Angeles, and rode the long bull market and cheap money of the late 2010s. And then interest rates did something they had not done in forty years.

The interest-rate trap, explained simply

To understand what went wrong, you need one concept: a bank makes money by borrowing short and lending long. It takes in deposits (short-term money it may have to return on demand) and uses them to hold longer-term assets like loans and bonds. The danger is a mismatch — if you fund long-dated, low-yielding assets with deposits that can flee, and then rates spike, you are trapped. This is "asset-liability management," and getting it wrong has killed banks for centuries.

City National got it wrong. During the zero-rate years it loaded its balance sheet with long-duration, low-yielding fixed-income securities — perfectly sensible when rates seemed anchored near zero. Then, in 2022 and 2023, the U.S. Federal Reserve raised rates at the fastest pace in a generation to fight inflation. Two things happened at once, and both were bad. First, the market value of those low-yield bonds collapsed, because no one wants a bond paying 1.5% when new ones pay 5%. Second — and more dangerously — City National's wealthy, financially sophisticated clients did exactly what wealthy, sophisticated clients do: they yanked their deposits out of low-paying accounts and moved them into Treasury bills and money-market funds paying far more. A bank whose entire brand was high-touch loyalty discovered that loyalty evaporates when a client can earn 5% down the street.

The deposit flight forced City National to replace that cheap, fleeing funding with expensive borrowed money, drawing heavily on the Federal Home Loan Bank system. Its net interest margin — the spread between what it earns on assets and pays on funding, the very heartbeat of bank profitability — was crushed. The "bank to the stars" had become a bank bleeding money.

The bailout from Toronto

This is where the moat earns its keep, and also where it exacts its price. When a subsidiary founders, the parent must decide whether to stand behind it. In 2023, CEO Dave McKay chose to do so decisively, injecting roughly $2.95 billion of the parent bank's capital into City National — a first tranche of about $950 million early in the year, followed by roughly $2 billion in the autumn — much of it used to buy money-losing securities off the subsidiary's books and shore up its liquidity.10 In plain terms: the Canadian cash cow was milked to plug a hole in Los Angeles. RBC could afford it precisely because the domestic franchise is such a reliable printing press. But shareholders were entitled to ask what, exactly, they had bought in 2015 — a growth platform, or a capital sink.

The regulators arrive

If the balance-sheet failures were a problem management could quantify, the regulatory failures were the ones that stung. In late January 2024, the U.S. Office of the Comptroller of the Currency (OCC) hit City National with a $65 million civil money penalty and a cease-and-desist consent order.41112 The OCC's findings were not about a single bad quarter; they described systemic, long-running deficiencies in risk management and internal controls — failures in operational risk, strategic planning, and compliance, including with the Bank Secrecy Act and anti-money-laundering rules, stretching back years.1112 The regulator was, in effect, saying that City National had grown faster than its control functions could handle and that the problems had gone unaddressed on RBC's watch. The bank had also, earlier in 2023, agreed to a separate $31 million settlement with the U.S. Department of Justice over allegations it had failed to offer mortgage lending in majority-Black and Hispanic neighborhoods of Los Angeles County — a redlining accusation that further tarnished the acquisition's shine.11

The pattern is what should concern a long-term investor. A single fine is an accident; a consent order citing systemic, multi-year control failures is an indictment of oversight. It suggests that when RBC bought the trophy, it did not adequately inspect the plumbing — and that the "high-touch relationship bank" had underinvested in the deeply unglamorous machinery of compliance.

Cleaning house

RBC's response was to import a new management team from the American regional-banking world. In late 2023 it pushed aside then-CEO Kelly Coffey and installed Howard Hammond, a former senior Fifth Third Bancorp executive, as City National's chief executive, with Greg Carmichael — the former CEO and chairman of Fifth Third — brought in as executive chairman to oversee the expensive, multi-year remediation program.13 Bringing in the top two leaders of a well-run American regional bank was a clear signal: RBC concluded that City National needed to be run less like a boutique and more like a properly controlled U.S. bank, with the compliance and risk architecture the OCC demanded.

Did RBC overpay? A comparative verdict

Step back and the balance sheet on the whole adventure is sobering. The $5.4 billion purchase price, plus the roughly $2.95 billion capital injection, plus the $65 million fine, plus the DOJ settlement, plus years of ongoing remediation costs, add up to a far more expensive bet than the sticker price suggested. And yet the comparison to peers complicates any simple verdict. Bank of Montreal paid US$16.3 billion for California's Bank of the West and then took its own lumps on credit and integration. Toronto-Dominion's attempted US$13.4 billion acquisition of First Horizon collapsed entirely in 2023 amid regulatory obstacles tied to TD's own anti-money-laundering troubles, costing TD a roughly US$1 billion breakup-related payment and, ultimately, a far larger AML penalty in the United States.

Seen against that backdrop, RBC's City National saga looks less like a unique failure and more like a chapter in a broader, cautionary Canadian pattern: banks flush with domestic profit, convinced that their fortress-Canada discipline would travel south of the border, repeatedly discovering that the U.S. market is bigger, more competitive, and more heavily policed than it looked from Toronto. RBC avoided the outright strategic collapse TD suffered. But City National remains, for now, a capital drag and a live remediation risk rather than the growth engine it was sold as.

If the American adventure taught RBC humility, the next deal would let it play to its absolute strength — at home, on its own turf, in a market it already dominated.

VI. The Domestic Coup: Buying HSBC Canada for $13.5 Billion

In late November 2022, a bombshell landed on Bay Street. HSBC, the London-headquartered global banking giant, announced it was putting its entire Canadian subsidiary up for sale. HSBC Bank Canada was not a minnow — it was the seventh-largest bank in the country, with an outsized franchise among affluent, internationally mobile customers and a strong commercial book serving importers and exporters. For any of the Big Six, it was the acquisition of a lifetime: a chance to buy a rival's entire Canadian customer base outright, something Ottawa would never permit between two of the incumbents themselves. HSBC was leaving to redeploy capital toward Asia, and in doing so it handed the Canadian oligopoly a rare opportunity to consolidate further.

RBC did not hesitate. It agreed to acquire HSBC Bank Canada for $13.5 billion in cash for the common shares — a deal it and its advisers described as a "once-in-a-generation" opportunity, and one that would become the largest domestic bank acquisition in Canadian history.314 The transaction closed on March 28, 2024, bringing roughly 780,000 clients and about 4,500 employees into RBC.3

Why this deal is everything City National was not

The contrast with the Los Angeles saga is the whole point, and it illustrates a fundamental truth about bank M&A. City National was a cross-border acquisition into an unfamiliar market with a different regulator, a different culture, and hidden control problems. HSBC Canada was the opposite in every dimension: same country, same regulator, same currency, overlapping branch footprint, and a customer base RBC already knew how to serve. That is why the economics were so much more attractive.

The magic of an in-market acquisition is cost elimination. When you buy a competitor in a market where you already operate, you do not need two head offices, two technology platforms, two compliance departments, or two overlapping branch networks. You migrate the acquired customers onto your existing infrastructure and switch off the duplicates. RBC estimated it could wring out roughly $740 million in annual pre-tax cost synergies — a figure representing about 55% of HSBC Canada's non-interest expense base — precisely by folding the operation into machinery it had already built and paid for.14 Against roughly $1.4 billion in one-time acquisition and integration costs, that is the kind of math that makes in-market deals so much safer than cross-border ones.14 The analytical lesson, which recurs throughout banking history: domestic consolidation is a cost story you largely control, while cross-border expansion is a revenue-and-culture bet you mostly do not.

The prize was not just cost savings, though; it was the specific customer base. HSBC Canada's franchise skewed toward exactly the segment RBC covets most: affluent, internationally connected households — newcomers, cross-border professionals, and business owners with money and needs on more than one continent — plus a commercial banking book weighted toward trade-oriented companies that import and export. These are high-value, multi-product relationships, the kind that generate wealth-management fees and commercial lending spreads for decades, not just a chequing account. Bolting 780,000 of them onto RBC's distribution machine, and cross-selling RBC's fuller product shelf into that base, is where the revenue upside lives beyond the pure cost math. It is also, notably, a way to acquire the internationally-mobile clientele that RBC tried and largely failed to serve profitably through its more exotic foreign ventures — buying the affluent-immigrant franchise at home rather than chasing it abroad.

The price of a monopoly discount

But there is no such thing as a free acquisition when you already dominate a market, because the same concentration that makes the deal lucrative makes it politically radioactive. RBC buying HSBC Canada meant the country's largest bank getting even larger by removing a scrappy, price-competitive challenger — exactly the kind of independent option that gives consumers an alternative. The Competition Bureau, consumer advocates, and eventually the NDP all raised alarms about reduced competition and higher fees.

To win approval, the deal had to clear Finance Minister Chrystia Freeland, who held ultimate authority, and she extracted a price. When she approved the transaction in December 2023, it came wrapped in binding conditions designed to blunt the anti-competition criticism: RBC committed to no front-line employee layoffs for a period after closing, to keeping a set of former HSBC branch locations operating, and to a large multi-billion-dollar allocation of financing directed at affordable housing and climate-related lending in Canada.[^15] These concessions were the political toll for being allowed to grow through consolidation — a reminder that the very government protection that creates RBC's moat also gives Ottawa leverage to impose obligations in return.

The capital hangover

Financing a $13.5 billion all-cash purchase is not free either, and here the deal collided with the constraint we met earlier: capital. Paying that much cash drew down RBC's loss-absorbing equity buffer sharply. The bank's CET1 ratio — the core solvency measure — fell by roughly 210 basis points to 12.8% as of the quarter ending April 30, 2024, largely reflecting the closing of the HSBC deal.15 That drop is highly consequential in practical terms, because a bank's excess capital above the regulatory minimum is the fuel for share buybacks, and buybacks are one of the primary ways Canadian banks return cash to shareholders. To fund HSBC, RBC had to throttle back its buyback engine and commit to a disciplined, quarter-by-quarter rebuild of its capital ratio.

For investors, that created a clear, trackable question: how quickly could RBC earn its way back to a comfortable capital cushion and restart returning cash? It is one thing to buy the deal of a generation; it is another to digest it without straining the fortress balance sheet that is the entire basis of the bank's premium valuation. By the third quarter of fiscal 2025, the CET1 ratio had recovered to 13.2%, suggesting the domestic profit engine was doing its job of rebuilding the buffer.7

The HSBC coup showcased RBC playing to its strengths. But even a bank executing a flawless acquisition can be undone by what happens in its own executive suite — and in 2024, RBC's C-suite delivered a scandal no one saw coming.

VII. The Executive Suite: Dave McKay, the $65M Fine, and the CFO Scandal

Dave McKay does not look like a Wall Street caricature of a bank CEO. Trained in mathematics and computer science before he earned an MBA, he came up through RBC's retail and technology ranks rather than its trading floors, and that pedigree matters to how he thinks. Where many bank chief executives are dealmakers or traders at heart, McKay is a systems person, someone who cut his teeth on the plumbing of retail banking — payments, personal lending, and the mechanics of serving millions of ordinary customers. He spent years running the personal and commercial banking engine that is the bank's crown jewel before becoming chief executive in 2014. Colleagues describe a low-key, process-driven leader more comfortable talking about digital adoption and operating efficiency than about swashbuckling M&A — which makes the risk-taking of his tenure all the more striking.

Under McKay the bank compounded its capital steadily, expanded its wealth and capital-markets franchises, pushed early and hard on digital and artificial intelligence, and — in the HSBC Canada deal — pulled off the domestic acquisition of a generation. To much of Bay Street, McKay is the steady hand who proved a Canadian bank could think globally without losing its discipline, and who read the HSBC opportunity correctly when it appeared.

The neutral assessment is more mixed, and the mix is the interesting part. The same decade that produced the HSBC coup also produced the City National debacle, a $65 million regulatory penalty at a subsidiary bought on his watch, and — in the spring of 2024 — a governance scandal that struck at the very heart of the bank's financial controls. A CEO's credibility is built not on the wins alone but on how the failures are handled, and McKay's record offers evidence for both the bulls and the skeptics.

Aligning the boss with the shareholders

On paper, RBC's compensation structure is designed to bind the CEO's fortunes to the company's long-term health rather than to a single good year. McKay is required to hold RBC shares worth a substantial multiple of his salary — a large personal stake that rises and falls with the stock — and to keep meaningful equity for a period after he eventually retires, so that he cannot cash out and walk away from decisions whose consequences arrive later. The bulk of his variable pay is deferred and tied to multi-year measures including earnings-per-share growth, return on equity, and total shareholder return relative to peers. The design is sound: it pushes a CEO to think in years, not quarters, and to care about relative performance against the other Big Six rather than merely absolute results in a rising market.

Whether the design actually disciplined the capital-allocation decisions is a fair question. Deferred, ROE-linked pay did not prevent the City National overreach or the control failures there. Incentive structures shape behavior at the margin; they do not substitute for judgment.

The more useful way to assess McKay is through behavior over time rather than pay structure. On the credit side of the ledger, his narrative has been broadly consistent across a decade of earnings calls and annual reports — a steady emphasis on premium clients, disciplined capital, and technology-driven efficiency — and when the HSBC opportunity arrived he moved decisively and, so far, on plan. On the debit side, the City National story is a case study in a strategy that was oversold on the way in and under-explained on the way out. The 2015 acquisition was pitched as a growth platform; the 2023 capital injections and 2024 fine were the quiet unwinding of that pitch, and management's public framing evolved from "premier U.S. wealth platform" to "multi-year remediation" without ever quite conceding that the original thesis had misfired. A skeptical investor is entitled to note that the same leadership that celebrated the trophy was slow to acknowledge the crack in it. That is not disqualifying — every long-tenured CEO accumulates a mixed record — but it is the kind of pattern that belongs in an honest assessment of credibility.

The scandal no one scripted

Then came April 2024, and a story that read like a corporate thriller.

Nadine Ahn was, by every account, a model of the RBC insider ideal. A two-decade veteran of the bank, she had risen through its finance ranks to become chief financial officer in 2021 — one of the most powerful and trusted positions in the institution, the person who signs off on the numbers the entire market relies upon. She was widely respected and, in a bank that prizes continuity, exactly the kind of steady internal promotion the culture celebrated.

On April 5, 2024, RBC abruptly fired her.4 The bank disclosed that an internal investigation, triggered by a whistleblower complaint, had found that Ahn was in an undisclosed "close personal relationship" with another RBC employee — Ken Mason, a senior figure in the bank's treasury and funding operations — and that she had used her position to favor him, allegedly securing him preferential compensation increases and a promotion, in violation of RBC's code of conduct.4 For a bank whose entire brand is trust and control, the optics were brutal: the person responsible for the integrity of the financials had allegedly breached the conduct rules herself.

What followed turned an embarrassing dismissal into a public legal war. Both Ahn and Mason denied any romantic relationship, characterizing their bond as a long, platonic work friendship, and both sued the bank. Ahn filed a wrongful-dismissal claim seeking roughly C$48.9 million, arguing that RBC had mischaracterized an innocent friendship, humiliated her publicly, and inflicted lasting reputational harm.516 RBC did not back down. It countersued, moving to claw back compensation and asserting that it possessed evidence — text messages, emails, and personal mementos — that it argued demonstrated a relationship the two had failed to disclose.[^18] In later filings the bank pointed to items it described as tokens of the relationship, from affectionate notes to keepsakes, while Ahn's lawyers accused RBC of selectively quoting private messages between two friends to build a salacious narrative.[^18] As of this writing the litigation remains unresolved, and the competing accounts have not been tested at trial.

Why the scandal matters beyond the tabloid appeal

It would be easy to file this away as gossip, but for an investor it carries a real signal, and it cuts in two directions. On one hand, the affair exposed a genuine risk-oversight lapse: whatever the truth of the relationship, the alleged conduct persisted long enough to require a whistleblower to surface it, which raises questions about how closely the most senior executives were being supervised. On the other hand, the bank's response was fast and firm — it removed its CFO within days of concluding the investigation, disclosed the matter, and did not let a valued 20-year insider's status buy her leniency. In governance terms, a board willing to fire its own CFO and fight her in court is demonstrating that the code of conduct binds the powerful, not just the junior staff.

RBC also managed the transition with minimal operational disruption. Katherine Gibson, herself a long-serving RBC finance executive with more than two decades at the bank, stepped in as interim CFO immediately and was confirmed as permanent chief financial officer in September 2024, restoring stability to the most sensitive seat in the building.17 The swiftness of that succession — an experienced internal hand ready to step up — is itself a mark of a deep bench, even as the episode underscored that no control culture is immune to human failure at the top.

The C-suite drama, the regulatory fine, and the two acquisitions all point to a single set of underlying lessons about how this business actually works. It is worth extracting them explicitly.

VIII. Playbook: Business, Moat, and 7 Powers Analysis

Strip away the personalities and the deals, and RBC teaches one dominant lesson, with several corollaries. The lesson is the extraordinary strategic value of a protected, high-margin domestic cash cow — and the way that cash cow both enables and disguises risk-taking elsewhere.

The power of the printing press

The core insight is almost mechanical. Because the Canadian retail-and-commercial franchise is a licensing-protected business with high switching costs and low credit losses, it generates a torrent of stable profit that is remarkably insensitive to management error in the rest of the enterprise. That is why RBC could absorb a multi-billion-dollar stumble at City National — the purchase price, the $2.95 billion capital injection, the $65 million fine, and years of remediation costs — without any threat to its own solvency or its dividend. In most industries, a mistake of that magnitude in a major division would be a corporate emergency. At RBC, it was a bad chapter funded by the good business back home.

This is the double-edged nature of the moat, and the neutral investor should hold both edges at once. The protected domestic engine is a genuine, durable competitive advantage — arguably one of the best in global banking. But precisely because it is so forgiving, it can subsidize poor discipline abroad. A cash cow that funds your mistakes can also mask them, delaying the reckoning that a less-protected company would face immediately. The very safety that makes RBC investable is the safety that let City National fester longer than it should have.

The 7 Powers, applied and interrogated

Return to Hamilton Helmer's framework, now with the full story in view, and test each power rather than merely assert it.

The Cornered Resource is the banking charter and the OSFI regulatory umbrella — a genuine, state-granted asset competitors cannot replicate. The interrogation: it is granted by policy, and policy is not immutable. Open-banking reforms, fintech entrants nibbling at payments and deposits, and periodic political pressure to increase competition are all slow-moving threats to a moat that exists because the government wants it to.

The Scale Economies power is real and measurable — RBC spreads its very large technology and distribution spend across the largest customer base in the country, producing a structurally low cost per customer. The interrogation: scale in banking is defensive, not expansionary. It protects the home market beautifully but did nothing to prevent value destruction in Los Angeles, where RBC was sub-scale and out of its element.

The Switching Costs power keeps Canadian customers glued in place through multi-product integration — chequing, mortgage, credit card, wealth, all bundled into a relationship that is painful to unwind. The interrogation: switching costs are a domestic phenomenon. They travel poorly. City National's supposedly loyal, high-touch clients demonstrated exactly how fast "sticky" wealthy depositors flee when a better rate appears.

Domestic versus international M&A: the enduring divide

The cleanest strategic takeaway from the past decade is the sharp asymmetry between the two acquisitions. HSBC Canada worked as a value proposition because it was an in-market consolidation: overlapping networks, immediate back-office elimination, roughly 55% cost synergies, and a regulator and culture RBC already understood. City National struggled because it was the reverse: a cross-border leap into an unfamiliar competitive and regulatory environment, where the promised revenue synergies had to overcome culture clash, control gaps, and a rate cycle that exposed hidden fragility.

The generalizable rule for any bank — and it is written in the graveyard of failed cross-border banking deals — is that cost synergies are far more reliable than revenue synergies, and that acquiring inside your existing footprint is a fundamentally different, safer activity than acquiring outside it. RBC has now run the controlled experiment on itself, and the results are instructive.

With the playbook clear, the final question is the one every long-term owner must answer: from here, does RBC win or stumble — and what, precisely, should be watched?

IX. The Stress Test: Bull vs. Bear and the Key KPIs

Imagine an activist investor building a position in RBC and preparing the presentation deck. What would the argument be? It would not be that RBC is a bad bank — it plainly is not. It would be that a superb domestic franchise is being partly obscured by self-inflicted complexity abroad, and that management should be forced to simplify.

The activist's stress test

The activist case would likely demand three things. First, a moratorium on further international retail and commercial banking M&A — an acknowledgment that the domestic engine is where RBC's edge lives and that its cross-border record does not justify betting more shareholder capital on foreign expansion. Second, a hard decision on City National: either complete the remediation and prove it can earn an acceptable return, or explore a strategic exit to free up the capital it consumes. Third, an accelerated return of capital to shareholders — restarting aggressive buybacks the moment the CET1 ratio is comfortably rebuilt, rather than hoarding capital for the next ambitious deal.

The strength of this critique is that it aligns with the evidence: RBC's returns are highest, safest, and most defensible at home, and its two worst chapters — City National's controls and the CFO scandal — were both failures of oversight rather than of the core business. The counterargument is that RBC's management has, in fact, been disciplined about capital and did rebuild its ratio while integrating HSBC, and that the wealth and capital-markets diversification, City National included, gives the bank growth avenues a purely domestic bank would lack.

Reading the competitive landscape: Porter and Helmer together

Through a Porter's Five Forces lens, RBC's domestic position is enviable on nearly every axis. The threat of new entrants is minimal, throttled by the Bank Act and OSFI. The bargaining power of customers is low, blunted by switching costs and the absence of a genuine price-competitive alternative — which is exactly why removing HSBC Canada was so valuable and so controversial. Rivalry among the Big Six is real but disciplined; these are rational competitors who compete on service and share far more than on ruinous pricing. The two forces that actually matter are the threat of substitutes — fintechs, open banking, and payment disruptors chipping at the edges of the franchise — and, uniquely for a bank, the "sixth force" of government, which both grants the moat and can constrain it. On the Helmer scorecard, RBC holds three of the seven powers domestically and essentially none of them in its cross-border operations, which is the entire strategic story compressed into a single sentence.

The current risk radar

Four risks deserve genuine attention because each has a clear business mechanism.

The first, and most Canadian, is the mortgage renewal cliff. Unlike the thirty-year fixed mortgages common in the United States, Canadian mortgages typically renew every few years. A wave of homeowners who locked in ultra-low rates during 2020 and 2021 have been renewing at materially higher rates, which squeezes household budgets, dampens consumer spending, and threatens to push up the bank's provision for credit losses — the money it sets aside for loans it expects to go bad. Whether this becomes a slow drag or a sharp shock depends heavily on employment and the pace of interest-rate cuts.

The second is the City National remediation drag — the ongoing risk of elevated compliance costs, higher funding expenses, and the possibility of further regulatory action if the OCC's cease-and-desist milestones are missed. This is a known, disclosed overhang rather than a hidden one, but known problems can still cost real money and management attention.

The third is the slow, structural one: the erosion of the moat's edges by technology and policy. Canada has been inching toward an open-banking regime that would give customers the right to share their financial data with third parties, and a generation of fintechs and payment apps has been chipping at the pieces of the franchise that are easiest to unbundle — foreign-exchange, everyday payments, budgeting, and low-cost investing. None of this threatens RBC's core the way a recession would; the switching costs on a primary chequing relationship remain formidable, and the bank has answered with its own digital investment. But the direction of travel is worth watching, because the entire RBC thesis rests on a moat that exists in part because regulation and inertia keep challengers out. Anything that lowers switching costs or invites new entrants — open banking most of all — nibbles at the foundation, slowly, from the edges inward. It is a decade-long risk, not a quarterly one, but it is the risk that could eventually change the character of the whole business.

The fourth is executive and integration risk — the tail of the CFO litigation, the cultural strain of absorbing HSBC's people and systems, and the ordinary execution hazards of merging two banks. Integration is where projected synergies are either realized or quietly lost.

The bull case and the bear case

The bull case is straightforward and grounded in the bank's actual strengths. The HSBC integration delivers its cost synergies on or ahead of schedule, adding a large, affluent customer base to the country's best distribution machine. City National, under its imported Fifth Third leadership, completes remediation, repairs its margins, and stops being a capital sink. Canadian rate cuts engineer a soft landing for the mortgage cliff, keeping credit losses contained. And the domestic engine keeps compounding at mid-to-high-teens returns on equity — 17.3% in the third quarter of fiscal 2025 — while the rebuilt capital ratio funds a resumption of generous buybacks.7

The bear case is equally coherent and uses the same facts read differently. The Canadian housing market, propped up for years by cheap money and high immigration, cracks under the weight of deferred mortgage stress, and provisions spike as unemployment rises. City National remains a structural drag that consumes capital and management focus without ever earning its cost of equity. HSBC integration costs run hotter than the $1.4 billion budgeted, and the promised synergies arrive late, weighing on returns. In this reading, RBC is a great domestic bank whose valuation premium is slowly eroded by the cumulative cost of its ambitions beyond the border.

The honest synthesis is that both cases are live, and that the domestic moat is strong enough to keep RBC profitable and safe under either scenario — the debate is about the magnitude of returns, not survival. That is a comfortable position for a bank and precisely why it commands a premium; it is also why the marginal dollar of shareholder value will be decided at the edges, in the foreign and acquired operations, rather than in the fortress at home.

The three KPIs that actually matter

For a long-term owner trying to cut through the noise, three metrics capture almost everything that matters about RBC's trajectory. There is no need to compute them — the bank reports them every quarter — only to watch their direction.

The first is the CET1 ratio, the measure of capital strength. It reveals how quickly RBC is rebuilding its buffer after the HSBC drawdown and, by extension, when it can resume returning meaningful capital to shareholders. Watch for it holding comfortably in the 13% range and above, as it did at 13.2% in the third quarter of fiscal 2025.7

The second is return on equity, the single best summary of whether the bank is still earning its premium. RBC's ability to sustain mid-teens or better ROE — against a backdrop of higher capital requirements and lower-return foreign operations — is the ultimate test of whether the moat is still delivering.7

The third is the provision for credit losses, the clearest early-warning gauge of stress in the loan book. Rising provisions, especially in the Canadian residential mortgage and commercial books, would be the first hard evidence that the renewal cliff or a housing downturn is turning from a risk into a reality.

Together those three numbers tell the story this article has traced: a fortress domestic bank, generating enough capital and enough return to fund its global ambitions, now being judged on whether it can rebuild its strength, defend its profitability, and hold its credit discipline while it digests the largest acquisition in its country's history. The moat is not in doubt. What remains genuinely open is whether the apex predator of Canadian banking can be as disciplined with its winnings as it has been dominant in earning them.

References

-

Royal Bank of Canada Reports Fourth Quarter and 2024 Results — Newswire (RBC), 2024-12-04 ↩↩↩↩

-

RBC Annual Report 2024 — Royal Bank of Canada, 2024-12-04 ↩↩

-

RBC Completes Acquisition of HSBC Bank Canada — Royal Bank of Canada, 2024-03-28 ↩↩↩

-

RBC Fires CFO Nadine Ahn After Probe Into Undisclosed Relationship — Bloomberg, 2024-04-05 ↩↩↩↩

-

RBC Fired CFO Nadine Ahn to Deny Her Payout, Lawsuit Claims — Reuters, 2024-06-21 ↩↩

-

Royal Bank of Canada Investor Relations — Quarterly & Annual Reports ↩↩

-

Royal Bank of Canada Reports Third Quarter 2025 Results — Newswire (RBC), 2025-08-27 ↩↩↩↩↩

-

RBC to Acquire City National Corporation, a Premier U.S. Private and Commercial Bank — PR Newswire (RBC), 2015-01-22 ↩

-

RBC Completes 'Milestone' Deal for U.S.-Based Bank City National — The Globe and Mail, 2015-11-02 ↩

-

RBC Injects $2.95 Billion of Capital Into City National Bank Subsidiary — Banking Dive, 2023-10-18 ↩

-

U.S. Banking Regulator Imposes $65-Million Fine on RBC Unit City National Bank — The Globe and Mail, 2024-01-31 ↩↩↩

-

OCC Assesses $65 Million Civil Money Penalty Against City National Bank — Office of the Comptroller of the Currency, 2024-01-31 ↩↩

-

City National Bank Appoints Howard Hammond as CEO and Greg Carmichael as Executive Chair — City National Bank, 2023-11-27 ↩

-

RBC to Strengthen Premium Canadian Business With Agreement to Acquire HSBC Canada — Newswire (RBC), 2022-11-29 ↩↩↩

-

Royal Bank of Canada Reports Second Quarter 2024 Results — Royal Bank of Canada (SEC Form 6-K), 2024-05-30 ↩

-

Former RBC Executive Nadine Ahn Files $49M Wrongful Dismissal Lawsuit Against Bank — CBC News, 2024-06-21 ↩

-

RBC Appoints Katherine Gibson as Permanent Chief Financial Officer — Royal Bank of Canada, 2024-09-12 ↩

-

Royal Bank of Canada and Dain Rauscher Corporation Announce Merger Agreement — Dain Rauscher Corp (SEC Form 8-K), 2000-09-28 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube