Revvity, Inc. (NYSE: RVTY): The Ultimate Corporate Metamorphosis

I. Introduction & Episode Roadmap

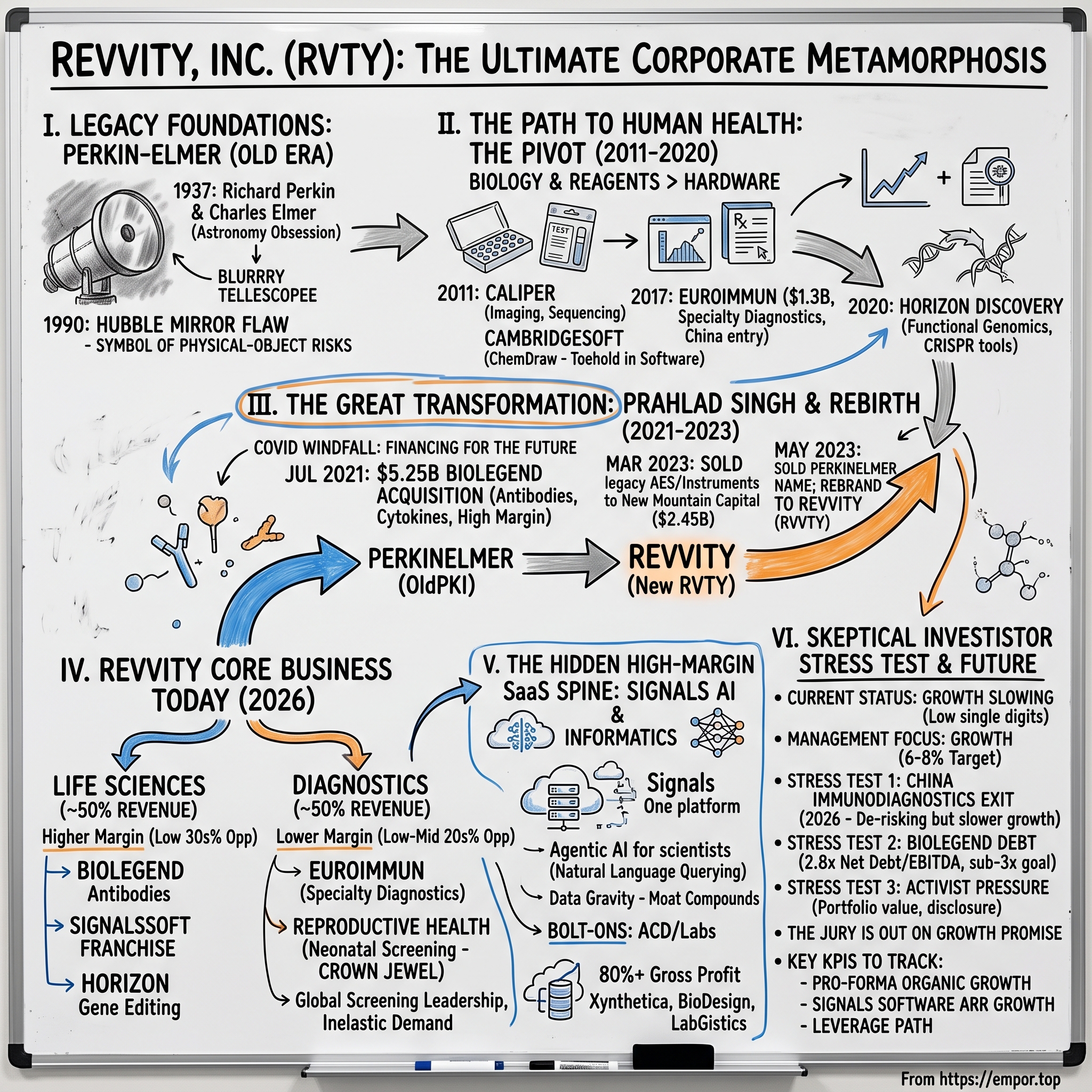

There is a strange symmetry to writing about Revvity on June 27. Exactly thirty-six years ago to the day, on June 27, 1990, NASA held the press conference that turned a company's name into a cautionary tale. The Hubble Space Telescope, launched two months earlier amid enormous fanfare, was sending back blurry images. The culprit was its primary mirror — the most precisely ground piece of glass humanity had ever attempted — and the contractor that had ground it to the wrong shape was the Perkin-Elmer Corporation.7 For a generation of engineers, "Perkin-Elmer" became shorthand for a brilliant optics house undone by the unforgiving economics of building perfect physical things.

Fast-forward to June 2026, and the company that descends from that very name did something its founders would not have recognized as belonging to the same universe. It did not unveil a sharper lens or a more sensitive sensor. Instead, Revvity announced it was embedding agentic artificial intelligence across its Signals software platform — letting a bench scientist type a plain-English question across a tangle of experiments, instruments, multi-omics datasets, and clinical records, and get back a traceable answer.[^2] No menus. No SQL. No data scientist as a middleman. Just a question and an answer, the way you might ask a colleague.

And the market shrugged. Revvity shares barely moved on the news, and the stock spent the first half of 2026 going essentially nowhere — a low-single-digit gain against a tape that was actually negative for the year.[^9] That shrug is the whole story. Here is a business sitting squarely inside one of the most fashionable themes on Earth — AI applied to the life sciences, a market estimated at roughly $2.73 billion in 2026 and compounding near 11% a year toward an estimated $6.8 billion by 2035 — and investors are not paying up for it.6 In an era when stapling "AI" to a press release can add billions of market value overnight, that indifference is a tell. Either the market is sleeping on a re-rating, or it has correctly judged that the AI layer, however clever, does not yet change the arithmetic of a company whose core growth has slowed to a crawl.

The macro backdrop sharpens the puzzle. Revvity's customers are pharmaceutical companies, biotech startups, academic labs, and public-health agencies — and for the better part of three years, the first two of those have been in a funding winter. The biotech bull market that crested in 2021 gave way to a long drought: venture funding pulled back, smaller biotechs cut their burn, and big pharma optimized R&D spending rather than expanding it. For a company whose Life Sciences segment sells the reagents and software those labs consume, that backdrop is a headwind that no amount of corporate restructuring can fully offset. Part of the bull case for Revvity is simply a bet that this winter ends — that rates ease, funding returns, and lab activity reaccelerates. That is a real, evidence-based hope, but it is also a bet on a cycle the company does not control, and it is worth being honest that a meaningful chunk of the upside case is exogenous.

Sorting between those two readings is the job of this episode, and it requires telling one of the great corporate-reinvention stories in modern industrials. The entity that issued that June press release barely resembles the company investors knew a decade ago. It ground the Hubble mirror, spent the back half of the 20th century as a sprawling instruments-and-engineering conglomerate, then methodically — almost surgically — disassembled itself. It split in two. It sold off the low-margin businesses dragging down its multiple. And then, in a move that still makes people blink, it sold its own legendary name. "PerkinElmer" now belongs to a private equity firm. What remained re-emerged in 2023 as an invented word — Revvity — a roughly $11 billion pure-play in reagents, diagnostics, and scientific software.[^6]

The central question: how does an industrial optics shop become a recurring-revenue life sciences platform — and did the team that pulled it off create durable value, or simply trade one set of problems for a more expensive set?

Here is the roadmap: 1. The Legacy Foundations — optics, bombsights, and the Hubble blunder that bookends the old era. 2. The Path to Human Health — the pre-COVID pivot from machines to biology. 3. The Great Transformation — Prahlad Singh, the $5.25 billion BioLegend bet, and the audacious decision to sell the company's own name. 4. The Core Business Today — the deceptively even split between Life Sciences and Diagnostics, and why the profit pools are anything but even. 5. The Hidden SaaS Engine — Signals, and whether software is a real moat or a rounding error. 6. Management & the Skeptical Investor Stress Test — debt, slowing organic growth, and the 2026 China exit. 7. Strategic Frameworks — 7 Powers, 5 Forces, and the bull/bear playbook for a business still proving its new identity.

Let's start where every great reinvention starts: with the thing that had to die.

II. The Legacy Foundations: From Hubble Mirrors to Analytical Instruments

Picture a precision optics fabrication facility in 1979. Inside, technicians are polishing a 2.4-meter disk of ultra-low-expansion glass to a smoothness that, if scaled up to the width of the continental United States, would not vary by more than a few inches. This was Perkin-Elmer's craft, and it was sublime. The company had been founded in 1937 by Richard Perkin, an investment banker with an astronomy obsession, and Charles Elmer, an older businessman who shared it. They built bombsights and reconnaissance optics in World War II, spy-satellite cameras in the Cold War, and the analytical instruments — spectrometers, chromatographs — that became the workhorses of 20th-century laboratories.

The Hubble mirror should have been the company's crowning achievement. Instead it became its most public humiliation. When the telescope's images came back fuzzy in 1990, the diagnosis was spherical aberration: the mirror had been ground to the wrong shape, its outer edge too flat by an amount far smaller than a human hair yet about ten times larger than the design tolerance allowed.7 The root cause was almost poetic in its banality — a testing device called a null corrector had been assembled with a tiny spacing error, so Perkin-Elmer had measured the mirror against a flawed reference and polished it, with exquisite precision, into exactly the wrong curve. The flaw was announced on June 27, 1990; it took a 1993 shuttle servicing mission and corrective optics to fix.7 The lesson that matters for investors is not the engineering. It is the business model. Perkin-Elmer made money by building physical objects of staggering complexity, one at a time, where a single sub-microscopic error could erase a decade of work. That is a brutal way to compound capital.

It is worth dwelling for a moment on the two men whose names rode this whole saga. Richard Perkin was a Wall Street financier who happened to be a serious amateur astronomer; Charles Elmer was a court stenographer turned businessman, two decades Perkin's senior, who shared the obsession with telescopes. They met, the story goes, through a shared membership in an amateur astronomy circle, and founded the firm in 1937 to design and build optical instruments at a level of precision that the United States, on the eve of war, badly needed and largely lacked. Within a few years the company was supplying the optics for aerial reconnaissance and bombsights, and the precision-optics culture it built — the obsessive measurement, the clean rooms, the tolerances measured in fractions of a wavelength of light — became its identity. That culture produced the Hubble mirror, and that same culture's blind spot produced the Hubble flaw: a team so confident in its own measuring apparatus that it trusted a miscalibrated null corrector over independent checks that hinted something was wrong. The episode is a permanent reminder that precision and correctness are not the same thing — you can be exquisitely precise about the wrong answer.

By the late 1990s, the conglomerate that had grown up around those optics was creaking, sprawling across instruments, fluid sciences, optoelectronics, and government services with no coherent center of gravity. A tidy piece of corporate surgery reset everything. In 1999, EG&G — a diversified engineering and government-services firm with roots in MIT physics and Cold War nuclear-test instrumentation, the company that had literally photographed atomic detonations — bought Perkin-Elmer's Analytical Instruments division for a reported sum of around $425 million.9 In a classic case of the acquired soul swallowing the acquirer's body, EG&G shed much of its own legacy defense work, adopted the better-known PerkinElmer name, and took the ticker PKI. The new PerkinElmer was a laboratory-instrumentation company: gas chromatography, mass spectrometry, atomic absorption, and the broad apparatus of measurement. The old Perkin-Elmer optics and defense lineage, meanwhile, was carved off and lives on elsewhere in the defense-electronics world — a reminder that "PerkinElmer" the name and PerkinElmer the company had already, once before, been pried apart. Selling the name in 2023, in other words, was not quite as unprecedented as it looked.

Here is the trap that defined the next twenty years. Instruments are wonderful businesses to talk about and difficult businesses to own. They are capital-intensive to develop, sold in lumpy capital-equipment cycles, and acutely sensitive to whether a customer's R&D budget got frozen this quarter. Much of PerkinElmer's hardware lived in "applied markets" — testing soil, food safety, environmental samples, industrial chemicals. Steady and respectable, but structurally low-margin and cyclical, the kind of revenue that the stock market capitalizes at a discount rather than a premium. To escape the gravity of the Hubble-era economics, PerkinElmer needed to migrate from selling machines once to selling the things those machines consume forever — reagents, test kits, and software. That migration is the spine of everything that follows.

III. The Path to "Human Health": The Pre-COVID Shift

The strategic insight that drove the 2010s is one every life-sciences-tools executive eventually internalizes: the razor is a worse business than the blades. A mass spectrometer sells once for a few hundred thousand dollars and then sits there for a decade. A diagnostic test kit, or a vial of antibody reagent, gets consumed and re-ordered every single week, at gross margins that would make a software company nod in approval. PerkinElmer spent the decade buying its way out of hardware and into biology.

Make the contrast concrete. Imagine two businesses with identical revenue. The first sells one analytical instrument to a customer for $300,000; once the sale closes, the relationship goes quiet for years, the next sale depends on the customer's capital-budget cycle, and a competitor can win the replacement with a better demo. The second places an instrument at modest margin and then sells that customer a stream of proprietary test kits — say a few thousand dollars a month, indefinitely, with no purchasing decision to re-litigate because the workflow is already validated around those kits. Over a decade, the second business collects far more revenue, at higher margin, with vastly more predictability, and the stock market rewards that predictability with a higher multiple on every dollar of earnings. Same headline revenue today; radically different value. That is the entire intellectual engine behind PerkinElmer's transformation, and it is why each acquisition in this era pointed in the same direction.

The pivot announced itself in 2011 with two deals that look small in hindsight but planted enormous seeds. In September 2011, PerkinElmer acquired Caliper Life Sciences for $600 million in cash, roughly $10.50 a share and a 42% premium, picking up molecular and cellular imaging, microfluidic "lab-on-a-chip" systems, and sample-prep technology for genomic sequencing.8 Around the same period it absorbed CambridgeSoft, whose flagship product, ChemDraw, was the indispensable software that every organic chemist on the planet used to draw molecular structures — the Microsoft Word of chemistry. ChemDraw was not a rounding error in disguise; it was the toehold that would eventually grow into the Signals informatics franchise. The strategic message was that PerkinElmer wanted to own not just the instruments in a lab, but the consumables they burned and the software that recorded what they found.

The truly transformative deal came in 2017. PerkinElmer agreed to acquire Euroimmun Medical Laboratory Diagnostics AG, a German leader in autoimmune, allergy, and infectious-disease testing, for roughly $1.3 billion in cash.[^4] This was the company's clearest declaration that it intended to be a diagnostics business. Euroimmun made the kind of specialty test kits — for lupus, for allergies, for esoteric infections — where roughly nine in ten dollars of revenue were recurring reagent reorders, and where the testing instruments locked customers into a razor-and-blade relationship.

On the numbers, PerkinElmer paid up but not insanely so: Euroimmun changed hands at around 6.9 times trailing revenue and roughly 19 times EBITDA on EBITDA margins in the mid-30s.[^4] For benchmark, that was broadly in line with the deal multiples flying around the tools sector in that era, and arguably reasonable for a 90%-recurring-revenue asset. But buried in the deal was a time bomb that would not detonate for years: a very large share of Euroimmun's revenue came from China. In 2017, that was sold as the bull case — exposure to the fastest-growing healthcare market on Earth. With hindsight, it was a severe geographic concentration that converted, post-COVID, from growth engine into policy trap. Hold that thought. It becomes the central drama of 2026.

There is a second piece of the pre-COVID build-out worth flagging, because it becomes load-bearing later in the story: functional genomics. Over this period PerkinElmer assembled, and then in 2020 completed the acquisition of, Horizon Discovery, a Cambridge, UK company specializing in gene editing — custom CRISPR and RNA-interference reagents and engineered cell lines that let researchers switch individual genes on or off to study what they do. In plain terms, Horizon sells the molecular scalpels and the genetically tailored "model" cells that underpin modern drug discovery and cell-and-gene therapy research. It is precisely the kind of high-value, recurring, scientifically sticky consumable that the company was hunting for, and it slotted alongside BioLegend's antibodies to give Revvity a credible position in the reagents that the next generation of biology actually runs on.

Step back and the pattern is unmistakable. Caliper bought imaging and microfluidics. CambridgeSoft bought the chemist's software. Euroimmun bought specialty diagnostics and its recurring kits. Horizon bought gene editing. Each deal moved the revenue mix a notch away from sell-it-once hardware and toward consume-it-forever biology and software. The pre-COVID PerkinElmer, then, was a company halfway through a transformation — one foot still in cyclical industrial hardware, one foot in recurring diagnostics and reagents — and visibly impatient to complete the crossing. What it needed was a leader willing to take the radical, irreversible steps. In December 2019, it got one.

IV. The Great Transformation: Prahlad Singh & Rebirth as Revvity

Prahlad Singh did not arrive as an outsider with a consultant's slide deck. He had run PerkinElmer's Diagnostics business, the very segment the company was betting its future on, and he understood viscerally that you cannot serve two masters. A company that sells both soil-testing instruments to environmental agencies and immunodiagnostic kits to hospitals is, in capital-markets terms, two companies wearing one suit — and the market pays the blended multiple of the worse one. Appointed CEO in December 2019, Singh set out to do something that most managers only talk about: voluntarily cut the company in half and throw away the slower half, even though it meant a smaller, scarier-looking business.

Then COVID hit, and for a moment it looked like the diagnostics bet had paid off beyond anyone's dreams. PerkinElmer's molecular-diagnostics and lab-automation capabilities — the very assets Singh had spent years assembling — rode the pandemic to an enormous windfall of COVID-testing revenue, at one point running into the hundreds of millions of dollars a quarter. The stock more than doubled off its pandemic lows. Suddenly the company had two things it had never had together before: a fortress balance sheet swollen with testing cash, and an equity currency trading at a rich multiple.

The danger of a windfall, of course, is mistaking it for a foundation. A weaker management team would have let COVID revenue flatter the run-rate, guided to a permanently higher base, and watched the stock implode when testing demand evaporated — which it inevitably did. Singh did something more interesting and more disciplined: he treated the windfall as a one-time financing event, a chance to fund the transformation he already wanted, and largely told investors not to capitalize the testing revenue as permanent. His defining decision was what he did with the cash and the elevated stock price the pandemic handed him — and he moved fast, while the window was open.

In July 2021, at what we can now identify as roughly the peak of the post-COVID biotech bubble, Singh announced the acquisition of BioLegend for $5.25 billion — about $3.3 billion in cash and the remainder in PerkinElmer stock.1 BioLegend, a privately held San Diego company, made research antibodies, reagents, and cytokines — the proprietary biological "tools" that academic and pharma scientists use to tag, sort, and study cells. It was high-growth, extraordinarily high-margin, and almost entirely recurring. It was also breathtakingly expensive: the deal valued BioLegend at something on the order of 14 times forward revenue, a multiple that only makes sense in the gravitational distortion of a bubble.

There is a human story underneath the price tag. BioLegend was built by Gene Lay, an immigrant scientist-entrepreneur who had earlier co-founded another antibody company and who ran BioLegend as a fast-moving, founder-led specialist obsessed with antibody quality and breadth. The appeal for PerkinElmer was not just the financials but the catalog: BioLegend's vast library of validated antibodies and its reputation among working immunologists were exactly the kind of asset that takes decades and millions of validation experiments to replicate. You cannot simply spend your way to a trusted antibody catalog overnight, which is precisely what made it worth a bubble multiple to a buyer with the cash to pay.

Did they overpay? The honest answer is "by the standards of a sober market, yes — by the standards of 2021, it was the going rate." That same year, Danaher paid roughly 19 times revenue for gene-therapy supplier Aldevron. The cleaner test came two years later, after the bubble had deflated: in August 2023, Danaher agreed to buy BioLegend's closest public comparable, the British antibody house Abcam, for about $5.7 billion — and that deal penciled out to roughly 10 times revenue.3 So Revvity bought a marginally faster-growing, arguably higher-quality asset at a meaningfully richer multiple than its giant rival paid for the comparable, just before the music stopped. Put differently: had Singh waited two years, he might have bought the same quality of asset for materially less. He did not wait, because in mid-2021 the consensus was that biotech demand would keep compounding and that prices would only rise — the same psychology, ironically, that led Oberhelman's Caterpillar to buy Bucyrus at the top of the mining cycle a decade earlier. Buying a cyclical growth asset at the top of its cycle is the recurring sin of ambitious acquirers, and the BioLegend deal will be debated for years on exactly this point. BioLegend instantly became the high-margin reagent engine at the heart of the company. Whether its growth ultimately justifies the 2021 price is, even today, an unresolved question — and we will return to it as the single largest swing factor in the investment case.

Funding a $5.25 billion deal mostly in cash meant taking on substantial debt, which made the next move both strategically elegant and financially necessary. In March 2023, PerkinElmer sold its Applied, Food, and Enterprise Services (AES) businesses — the cyclical, lower-margin industrial instrument operations that were the literal descendants of the old EG&G analytical division — to private equity firm New Mountain Capital for $2.45 billion.2 This deleveraged the balance sheet and amputated the slow-growth past in one stroke.

There is a deeper strategic elegance to the New Mountain transaction that is easy to miss. The businesses Revvity sold were not bad businesses — they generated cash, held respectable market positions in food and environmental testing, and were exactly the kind of stable cash flows a private equity firm prizes. They were simply the wrong businesses for a public-market growth multiple. By matching the slow, stable AES assets to a buyer who values stability and uses leverage to juice returns, while keeping the faster, higher-margin assets in the public vehicle, Singh was doing a kind of multiple arbitrage: putting each set of assets into the hands of the owner who would pay the most for it. The $2.45 billion of proceeds went straight at the BioLegend debt, turning the pandemic-era leverage from a liability into a manageable balance sheet. It was capital allocation as choreography — buy the growth asset with windfall cash and stock at the top, then sell the legacy assets to pay down the resulting debt, leaving a cleaner, faster company behind.

And then came the flourish that makes this a story rather than a transaction. As part of the divestiture, the public company sold the actual "PerkinElmer" brand name to New Mountain. Think about the audacity of that. The name carried eighty years of equity — and also eighty years of association with low-multiple hardware and a famous space-telescope flaw. Singh's wager was that the name had become a liability, anchoring the stock to a hardware valuation the company was trying to escape. So on May 9, 2023, the remaining Life Sciences and Diagnostics business rebranded as Revvity, Inc. and switched its ticker from PKI to RVTY.[^6] It was a clean-slate gambit: accept a period of brand confusion and a depressed multiple, and re-emerge under an invented name that carried no baggage, in the hope that the market would finally value the recurring-revenue reality rather than the industrial ghost. Three years on, the stock's flat reception suggests the re-rating Singh was reaching for has not yet arrived — which means the burden of proof now sits squarely on the underlying business.

V. The Core Business: Where the Money is Made Today

Walk into the Revvity story expecting a tidy "diagnostics company" or "reagents company," and the segment math will surprise you. In fiscal 2025, Revvity's revenue split almost exactly down the middle between its two reporting segments — Diagnostics at roughly $1.425 billion and Life Sciences at roughly $1.43 billion, a near-perfect 50/50.9 But revenue symmetry hides profit asymmetry. The two halves of this company are very different machines, and one of them is meaningfully more valuable per dollar of sales than the other.

Life Sciences is the higher-margin engine. This is BioLegend's proprietary antibodies and reagents, cellular and high-content imaging, functional genomics from the Horizon Discovery acquisition (custom CRISPR and RNAi gene-editing tools), and the Signals software franchise. Because so much of it is consumable reagents and software rather than hardware, segment operating margins run materially higher than the corporate average — on the order of the low-30s percent range, well ahead of Diagnostics.9 The way Revvity wins here is not by competing on commoditized instruments but by owning irreplaceable inputs: a specific BioLegend antibody clone validated in thousands of published papers cannot simply be swapped for a competitor's without re-validating years of work. That is a real switching cost, and it is the reason the BioLegend price tag was defensible even if it was steep.

The competitive neighborhood, however, is terrifying. Revvity is a mid-cap fish in an ocean of whales. Danaher, a $20-billion-plus revenue colossus, now owns both Abcam and Aldevron and competes with BioLegend head-on. Thermo Fisher Scientific, north of $40 billion in revenue, has distribution muscle and a hardware install base that no one can match. Agilent, around $6-7 billion, is strong in analytical instruments and cell analysis. Revvity's strategy in this company is not to out-scale the giants — it cannot — but to be the deeper specialist in narrow niches where proprietary clones and custom reagents create stickiness the scale players cannot easily replicate.

Diagnostics is the lower-margin but arguably more defensible engine, with adjusted operating margins running in the low-to-mid-20s percent range.9 It houses two very different businesses. One is the Euroimmun specialty immunodiagnostics franchise — autoimmune and allergy testing. The other, and the crown jewel of the entire company, is Reproductive Health: neonatal and newborn screening.

It is worth slowing down on newborn screening, because it is the best business Revvity owns and the least understood from the outside. Here is how it works. Within a day or two of birth, a nurse pricks a newborn's heel and blots a few drops of blood onto a special card — the "dried blood spot." That card travels to a public-health laboratory, where Revvity's instruments and reagents screen it for dozens of rare but devastating genetic and metabolic disorders — conditions like phenylketonuria, congenital hypothyroidism, sickle cell disease, and severe combined immunodeficiency. Many of these conditions are treatable if caught in the first weeks of life and catastrophic if missed. The screening is mandated by law in most developed countries and a growing list of emerging ones. Revvity is the undisputed global leader, with an estimated 60-70% global share, and it screens a large share of the millions of babies born each year into screening programs.

Why is this such a good business? Three reasons stack on top of each other. First, the demand is utterly inelastic and non-cyclical — babies are born in recessions, and the screening is legally required, so volumes do not flex with R&D budgets or hospital capital cycles. Second, it is a razor-and-blade model: Revvity places the screening instruments and then sells the consumable reagent kits in perpetuity, with the install base creating years of recurring pull-through. Third, and most powerfully, it is woven into the regulatory and operational fabric of national public-health systems. A health ministry that has built its entire newborn-screening program around Revvity's platform — trained its lab staff on it, validated its assays against it, integrated its data systems with it — does not casually re-tender the system that screens every baby born in its jurisdiction. The switching cost is not just money; it is the political and clinical risk of disrupting a program where the failure mode is a missed diagnosis in an infant. That is about as close to a monopoly as exists in regulated healthcare, and it throws off steady cash through every cycle.

In Diagnostics, the competitors are the clinical-lab titans — Roche (a $50-billion-plus diagnostics-and-pharma giant, Swiss-named, so no native script applies), Abbott Laboratories in core immunodiagnostics, and Italian specialist DiaSorin as a direct peer in autoimmune testing. Against all of them, Revvity's edge is concentration in defensible niches rather than breadth. Critically, Revvity does not try to compete in high-volume routine clinical chemistry — the blood-panel-and-cholesterol commodity testing where Roche and Abbott's scale is unbeatable. It deliberately fishes in the specialty ponds where being the validated, regulatory-integrated incumbent matters more than being the biggest.

Myth vs. Reality

A few consensus narratives deserve a fact-check. Myth: Revvity is an "AI company" now. Reality: it is a reagents-and-diagnostics company with a small, fast-growing software business that has added AI features. The AI is real and strategically important, but it is a thin, high-value layer on top of a business whose revenue still overwhelmingly comes from physical kits and instruments. Anyone buying the stock for the AI headline is buying a reagents company at a reagents company's growth rate. Myth: the 50/50 revenue split means the two segments are equally important. Reality: Life Sciences earns a meaningfully higher margin, so it contributes more profit per dollar, while Diagnostics — specifically newborn screening — contributes the most durable competitive position. The segments are equal in size and unequal in almost every way that matters. Myth: BioLegend made Revvity a growth company. Reality: BioLegend is high quality, but Revvity's blended organic growth has been stuck in the low single digits; the reagent engine has not yet been enough to lift the whole company into its target growth band.

The takeaway for investors is that Revvity is not really one business with a 50/50 split; it is a portfolio of moated micro-monopolies — newborn screening, specific antibody clones, ChemDraw — bolted together, with the profit weighted toward the Life Sciences side and the most durable competitive position sitting inside Diagnostics. That portfolio shape is what the next section's software story is quietly trying to tilt even further toward recurring, high-margin revenue.

VI. The Hidden High-Margin SaaS Spine: Signals AI & Informatics

Tucked inside the Life Sciences segment, unbroken out in the headline numbers, is the business that excites Revvity's management more than any other on its earnings calls: software. The Signals franchise — descended from that 2011 ChemDraw acquisition — is an informatics platform for R&D labs. At its simplest, it is the electronic lab notebook and data backbone where a pharmaceutical scientist records experiments, stores chemical structures, and manages the avalanche of data a modern lab generates. Think of it as the operating system that sits underneath the science.

Why does a relatively small slice of revenue command so much management attention? Two reasons. First, the economics: software carries gross margins north of 80%, so every incremental dollar of software revenue does disproportionate work on company-wide margins — a $10 million software dollar drops far more to the bottom line than a $10 million reagent dollar. Second, the stickiness. Software grows in the high teens organically, and management has pointed to recurring software revenue compounding far faster than the hardware-era core as labs convert from one-time perpetual licenses to cloud subscriptions — a transition that, as every SaaS investor knows, depresses revenue optically in the short run while building far more valuable recurring revenue underneath. Once a pharma company has loaded its proprietary chemical structures, assay results, and now its AI models into Signals, the cost, risk, and validation burden of ripping it out to move to a rival becomes prohibitive. Data gravity is a moat that compounds: the more a customer puts in, the harder it is to leave.

It is worth naming the competition honestly, because Signals does not own this market. The informatics-and-electronic-lab-notebook space is a genuine battleground. Benchling, a venture-backed Silicon Valley company valued in the billions at its peak, has won a large share of younger biotech labs with a modern, cloud-native interface. Dotmatics (owned by Insightful Science) is a direct scientific-informatics competitor with its own roll-up of lab software. And the scale giants lurk: Thermo Fisher and Danaher both have informatics ambitions, and a well-funded newcomer could always target a slice of the workflow. Revvity's defensible edge here is its incumbency in chemistry specifically — ChemDraw and the structure-handling heritage give it a foothold in the chemist's daily workflow that the biology-first newcomers do not naturally own — plus the ability to bundle software with the reagents and instruments a customer already buys. But "defensible" is not "unassailable," and the honest read is that Signals is fighting for share in a contested market, not harvesting a captured one.

What does "agentic AI" actually mean in this context, in plain terms? A traditional electronic lab notebook is a passive filing cabinet: a scientist puts data in, and to get an answer back, they — or a data scientist — must write a query, build a report, or manually hunt through records. An "agentic" layer flips that relationship. Instead of the scientist doing the work of finding and assembling the answer, an AI agent does it: the scientist asks, in ordinary language, "show me every compound we tested against this target that also passed toxicity screening," and the agent figures out which datasets to search, runs the queries, and returns a traceable answer with its sources. The word "agentic" signals that the AI does not just answer a single question but can take a sequence of actions on the scientist's behalf — querying, cross-referencing, even chaining steps together. If it works as advertised, it collapses hours of skilled data-wrangling into a conversation, and it makes the underlying data platform dramatically more valuable, because the value is no longer just in storing the data but in reasoning over it. That is the prize Revvity is reaching for.

This is the strategic logic behind the June 2026 AI push. Revvity announced an expansion of AI capabilities across the Signals business — an agentic framework on the unified Signals One platform that lets researchers query chemical, biological, and clinical datasets in natural language.[^2] On the Q1 2026 call, management was even more specific, walking through a slate of 2026 software launches: Xynthetica, described as an "AI models as a service" secure marketplace connecting computational tools to wet-lab research; BioDesign, a cloud-native design tool; and LabGistics.[^9] The ambition is to convert Signals from a passive "system of record" — a place data sits — into an active "system of understanding" that reasons over that data. If it works, it converts an electronic filing cabinet into an indispensable scientific collaborator, with the pricing power that implies.

Revvity also bolted on capability through M&A. In late 2025 it acquired ACD/Labs, integrating chemistry and analytical-workflow software into the Signals stack; management has quantified ACD/Labs as adding roughly 75 basis points to corporate revenue growth in 2026.[^9] That is a useful, honest disclosure — and also a quiet admission of how the growth math works: at this stage, the software story is real but still small enough that a single tuck-in acquisition is a measurable fraction of total growth.

Here is the neutral read. The bull narrative — high-margin, 80%-plus gross profit, sticky, AI-supercharged SaaS hiding inside a hardware-adjacent company — is genuinely attractive, and the switching costs are real, not rhetorical. But the skeptic is entitled to ask for the receipts. Revvity does not break out Signals as a standalone reportable segment, so investors cannot independently verify its ARR, its growth, or its margin contribution; they are taking management's characterization on faith. And launching three products in one year ("the biggest launches that could have happened in the software business," as management put it on the Q1 call) is exactly the kind of statement that demands follow-through.[^9] The software spine could be the lever that re-rates the whole company. It could also remain a compelling slide that never quite moves the consolidated needle. The evidence to settle that is the disclosure Revvity has so far chosen not to give — which brings us to the harder questions about management and the balance sheet.

VII. Current Management & The Skeptical Investor Stress Test

To understand whether to trust this transformation, you have to weigh the people executing it against their own track record, and then run the numbers through a skeptic's stress test. Let's do both.

The leadership. Dr. Prahlad Singh remains President and CEO, in the seat since December 2019 and the architect of every move in this story — the BioLegend bet, the New Mountain split, the rebrand, and now the China exit. His total reported compensation for 2025 was about $13.8 million, up roughly 14% year over year, with the large majority delivered as performance-vesting long-term equity rather than cash, tying his outcomes to revenue growth, adjusted EPS, and returns on capital.5 Alongside him is CFO Max Krakowiak, appointed in September 2022, who has been the financial engineer behind the divestiture, the BioLegend integration, and the deleveraging campaign. The pay structure is reasonably aligned; the more interesting question is whether the behavior matches the alignment. On the evidence of the calls, this is a management team that does not hide behind macro excuses and tends to give concrete, quantified explanations. That is a point in its favor. The stress test is whether the substance holds up.

Stress test #1: The China diagnostics trap and the 2026 exit. Recall the time bomb from 2017 — Euroimmun's heavy China exposure. Over the following years, China's healthcare system rolled out volume-based procurement and localized pricing pressure that crushed margins and demand for imported diagnostics, with a structural preference for domestic suppliers. On the Q1 2026 earnings call on May 5, management announced the resolution: Revvity would divest its immunodiagnostics business in China, a unit that represented roughly 6% of total company revenue in 2025.[^9] The company framed the Chinese diagnostics market as facing "persistent policy-induced headwinds" expected to continue over the medium term.[^9] Notably, Revvity did not disclose the financial terms or the buyer in its prepared remarks, and the value of the deal was not made public in the sources reviewed here.4

One second-layer detail deserves a flag: the fact that Revvity did not disclose the price or buyer is itself informative. Companies trumpet the headline number when a divestiture fetches a strong price and stay quiet when it does not. The absence of a proud valuation, combined with management's framing of the business as facing "persistent policy-induced headwinds," strongly suggests this was a clearing price for a structurally impaired asset rather than a premium exit.4[^9] That does not make the decision wrong — selling an impaired business at a fair clearing price to redeploy management attention is good discipline — but investors should read the silence on terms as a quiet confirmation that the China immunodiagnostics thesis, born in the 2017 Euroimmun deal, did not end the way it was sold.

So is this elegant de-risking or a quiet admission that the Euroimmun-in-China thesis broke? The honest answer is "both, and the framing is doing some work." On the one hand, exiting a structurally impaired, low-margin, cash-draining business is textbook capital discipline — and management quantified the cleanup precisely: it expects the move to improve 2026 organic growth by roughly 100 basis points and operating margins by about 30 basis points, while pro-forma China exposure drops to roughly 8-9% of revenue (about 7% of which is the more durable Life Sciences business).[^9] Most strikingly, management noted that excluding the China unit, fiscal 2025 free-cash-flow conversion would have been about 300 basis points higher than the 87% actually reported, and Q1 2026 pro-forma organic growth would have been 6% rather than the 3% reported.[^9] On the other hand, none of that changes the fact that an asset bought as a growth engine in 2017 is being shed as a problem in 2026. Cleaning up the optics of your growth rate by selling your slowest business is legitimate, but investors should recognize it for what it is: the pro-forma 6% is partly an act of subtraction, not acceleration.

Stress test #2: The BioLegend debt overhang. Funding a $5.25 billion deal mostly in cash left a balance sheet to manage. As of the first quarter of 2026, Revvity carried total debt of roughly $3.35 billion against about $860 million of cash, for net debt near $2.5 billion and a net-debt-to-adjusted-EBITDA leverage ratio of about 2.8 times.[^9] The structure itself is conservatively built — management noted 100% of the debt is fixed-rate at a weighted-average interest rate of just 2.6%, with about six years of weighted-average maturity, a genuinely enviable cost of debt in the 2026 rate environment.[^9] In mid-July 2026, Revvity plans to retire roughly $600 million of a Eurobond coming due, using cash on hand, which it expects will bring gross leverage below 3 times by year-end.[^9] The bear's nuance here is subtle but fair: paying off cheap 2.6%-ish debt with cash forfeits the interest income that cash was earning and drains the balance-sheet cushion, so the "deleveraging" is partly a reshuffling rather than pure debt reduction.

Stress test #3: Organic growth. This is the crux. Strip away the rebrands and the AI launches, and the uncomfortable core fact is that Revvity's organic growth has been stuck in the low single digits — 3% total-company organic growth in Q1 2026, with a roughly 3% currency tailwind flattering the reported figure and a 75-basis-point boost from the ACD/Labs acquisition.[^9] Management's own long-range plan calls for 6-8% organic growth and double-digit EPS growth, and its 2026 pro-forma guidance (excluding China) targets only 3-4% organic growth, a 28.4% adjusted operating margin, and adjusted EPS of $5.20-5.30.[^9] In other words, the company is currently running at roughly half the bottom of its own long-term growth target. The entire bull case rests on BioLegend reagent demand and Signals software reaccelerating into that 6-8% band as biopharma funding recovers. That has not happened yet.

Stress test #4: The activist's portfolio question. Imagine a skeptical activist building a position. What would they push on? The most obvious lever is the same one Singh has already been pulling: portfolio focus. An activist would argue that even after the China exit, Revvity is still two businesses — Life Sciences and Diagnostics — that share little operational overlap and could arguably be worth more apart, with Life Sciences commanding a reagents-and-software multiple and Diagnostics a steadier healthcare multiple. They would scrutinize whether the BioLegend goodwill — Revvity carried roughly $6.6 billion of goodwill on its balance sheet at the start of 2026, against total assets of about $12 billion — is at risk of impairment if reagent growth disappoints, since a write-down would be the accounting system's belated admission that the 2021 price was too high.9 And they would press on disclosure: a company that talks up software as its crown jewel but declines to report its ARR is inviting the question of what the number would show if revealed. None of these is a smoking gun. Collectively they describe the agenda a determined outside investor would bring — and, to management's credit, Singh has pre-empted much of it by acting like an activist on himself.

A note on the analyst exchanges. The texture of the Q1 2026 call is worth capturing, because it reveals where the pressure is. Management led with the China divestiture and the software launches — the offense. Where the prepared remarks were most insistent was on the pro-forma framing: nearly every key metric was restated to exclude China, converting a 3% reported growth quarter into a "6% pro-forma" one and an 87% cash-conversion year into a "~90% pro-forma" one.[^9] That repeated reach for the cleaner pro-forma number is itself a tell about what management knows investors are worried about. On the software questions, executives were enthusiastic but notably qualitative — describing Xynthetica, BioDesign, and LabGistics as "three of the biggest launches that could have happened in the software business" without attaching hard revenue or ARR figures to them.[^9] Enthusiasm is not evidence; the gap between the energy of the software narrative and the specificity of the software disclosure is the single cleanest illustration of the show-me posture the whole stock is stuck in.

Credibility verdict. On execution mechanics — cost discipline, cash conversion (a robust 97% in Q1 2026), and surgical capital allocation — this team has earned real marks.[^9] It set out a transformation and delivered the hard, unglamorous parts: the split closed, the leverage is coming down, the cost structure is disciplined, and the China problem is being cut out rather than nursed. Where the jury is still out is on the growth promise. Management has been consistent and concrete, which is more than many peers manage, but consistency in narrating a 3% growth rate is not the same as delivering the 6-8% it has promised. The skeptic's one-line summary: excellent surgeons, unproven physicians. They have removed what needed removing; whether the patient actually grows is the open question.

VIII. Strategic Frameworks: Porter's 5 Forces & Hamilton's 7 Powers

Strip the story down to its competitive bones, and two analytical lenses — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — tell you where Revvity's moat is real and where it is aspirational.

Hamilton's 7 Powers Applied to Revvity

Switching Costs (High, and the strongest power). This shows up in three places. In Diagnostics, a public-health agency that has validated and integrated a newborn-screening system faces multi-year cost and regulatory friction to switch — the testing is mandated, the stakes are infants' lives, and re-validation is enormous. In software, once a lab's proprietary structures and assay data live in Signals One, migration risks data loss and revalidation. In reagents, a validated antibody clone is woven into the published scientific record. Switching costs are the single most durable thing Revvity owns.

Cornered Resource (High, in pockets). BioLegend controls proprietary hybridoma cell lines and specific monoclonal antibody clones — for example, particular CD-marker antibodies — that have been cited and validated in thousands of papers. A scientist cannot substitute a different clone without potentially invalidating comparisons to decades of prior work. That citation lock-in is a genuine cornered resource, though it applies clone-by-clone rather than across the whole catalog.

Scale Economies (Moderate). Running a global regulatory machine capable of securing FDA, CE-IVD, and 国家药品监督管理局 NMPA (China's National Medical Products Administration) approvals across 190-plus countries is a real barrier to small startups. But against Danaher and Thermo Fisher, Revvity is the one lacking scale, so this power cuts against it more than for it.

The powers Revvity conspicuously lacks are network economies and branding power in the consumer sense — and arguably process power at scale. This is not a company protected by a flywheel of users or a luxury brand premium. Its moat is the unglamorous, durable kind: lock-in and irreplaceability in narrow niches.

Porter's 5 Forces Applied to Revvity

Threat of New Entrants (Very Low). Clinical-diagnostic regulation, GMP-grade reagent manufacturing, and multi-year instrument-validation cycles make greenfield entry into Revvity's core niches nearly impossible. No venture-funded startup is going to displace the global newborn-screening incumbent.

Bargaining Power of Buyers (Moderate-to-High). Large pharma purchasing departments and consolidated hospital systems push hard on price. But mandated newborn screening and validated specialty reagents have highly inelastic demand, which blunts buyer power in exactly the niches Revvity cares about most.

Threat of Substitutes (Low). There is no viable substitute for mandated dried-blood-spot newborn screening, and in life sciences, switching to an alternative antibody or gene-editing reagent carries steep validation costs that deter substitution.

Bargaining Power of Suppliers (Low). Revvity manufactures its own antibody clones, reagents, and software; it is largely vertically integrated, so it is not hostage to upstream suppliers.

Competitive Rivalry (High — the binding constraint). This is where the pressure lives. Revvity occupies defensible niches, but it defends them against scale-advantaged giants — Danaher arming Abcam, Thermo Fisher's distribution juggernaut, Roche and Abbott in diagnostics. The risk is not that a giant invents something Revvity cannot; it is that a giant bundles a "good enough" competing product into a relationship the customer already has, and slowly squeezes Revvity's pricing at the edges.

It is instructive to hold Revvity up against its larger peers through this lens, because the contrast explains the valuation. Danaher and Thermo Fisher possess the same switching-cost and cornered-resource powers Revvity has, plus enormous scale economies and plus the distribution muscle that lets them cross-sell across vast install bases. Agilent, similar in size to Revvity, competes on a broader instrument franchise. Revvity's distinctive bet is to be the deepest specialist rather than the broadest platform — to win on irreplaceability in newborn screening, specific antibody clones, and chemistry software rather than on breadth or scale. That is a coherent strategy, and in its best niches it produces monopoly-like economics. But it also means Revvity is structurally the smaller combatant in most of its fights, perpetually defending borders against opponents who can absorb a price war it cannot. The framework does not tell you Revvity loses; it tells you Revvity's wins will be narrow, defended, and hard-earned rather than sweeping.

The net framework read: Revvity has authentic, narrow moats (switching costs, cornered resources) sitting inside an industry with intense rivalry and scale disadvantages. That combination tends to produce durable but slow-growing businesses — which is exactly what the financials show. The moats explain why Revvity's margins and cash conversion are strong and stable; the rivalry and scale gaps explain why its growth rate is not. Both halves of that sentence are true at once, and holding them together is the key to thinking clearly about the stock.

IX. Playbook: Business & Investing Lessons

Three transferable lessons fall out of this story for operators and investors alike.

1. The consumables-and-software holy grail. The entire Revvity arc is one extended argument that selling machines is a worse business than selling what machines consume. Hardware revenue is transactional, lumpy, cyclical, and capitalized at a discount; reagent and software revenue is recurring, sticky, high-margin, and capitalized at a premium. Every move Singh made — Caliper, Euroimmun, BioLegend, Signals, and the divestiture of the applied-instruments legacy — pushed the revenue mix from the first category toward the second. The lesson is not "hardware bad"; it is that the durable compounders in instrumentation are the ones who own the razor's blades and the lab's software, not just the razor.

2. Sometimes the most rational asset to sell is your own name. The decision to sell "PerkinElmer" to New Mountain is the boldest illustration of a hard truth: brand equity can be a liability when the brand is synonymous with the valuation you are trying to escape. When a name anchors investors to a low-multiple, hardware-era mental model, the clean-slate rebrand — accepting a transition discount to unlock a pure-play re-rating — can be the value-maximizing move, however much it stings to give up eighty years of history. The open question, three years on, is whether the re-rating ever fully arrives; the gambit is not yet proven to have paid.

3. Geographic concentration is a growth story until it is a trap. Euroimmun's China exposure was celebrated in 2017 and divested in 2026. The lesson is not "avoid China"; it is that a single-country dependency built during a boom can invert into a policy and pricing trap when local rules shift, and that aggressive, early de-risking — taking the loss and moving on — often beats a slow, capital-draining defense of a structurally impaired position. Revvity's willingness to amputate rather than nurse the China unit is, whatever else one thinks of it, the disciplined version of this lesson.

4. Windfalls are financing events, not earnings. The most underrated piece of the whole saga is what Singh did not do with the COVID windfall. He did not let testing revenue inflate a permanently higher base, did not guide investors to capitalize it, and did not get caught flat-footed when it evaporated. He treated a once-in-a-generation cash surge as a one-time opportunity to fund a structural transformation — buying BioLegend and paying down debt — rather than as a new run-rate to defend. The contrast with companies that let pandemic demand define their cost structure and then spent years unwinding the overhang is instructive. When fortune hands a business a windfall, the disciplined move is to convert temporary cash into permanent assets, not temporary cash into permanent expectations.

5. The acquirer's recurring sin is timing, not target. The BioLegend purchase was a fine asset bought at a frightening price at the top of a cycle — the same error, in a different industry, that the best operators keep repeating. Aggressive companies tend to deploy their largest checks precisely when optimism is highest and assets are most expensive, because that is exactly when caution feels most like cowardice. The investing lesson is to watch when a management team spends its biggest dollars at least as closely as what it buys. A great asset bought at a cycle peak can take a decade to earn back its price.

X. The Bull vs. Bear Case & KPIs to Track

The bull case is a reacceleration story. If global rates ease and biotech venture funding thaws, BioLegend's high-margin reagent sales — leveraged to academic and biotech research budgets — could climb back toward mid-teens growth. Signals One, supercharged by the 2026 AI launches, could scale ARR fast enough to lift consolidated adjusted operating margins back toward the high-20s-to-30% range. The China divestiture sanitizes the growth and cash-conversion math, lifting pro-forma organic growth to a cleaner 6%-plus with reduced geopolitical risk. And the July 2026 Eurobond retirement pushes leverage safely below 2.5 times by 2027, freeing capital for buybacks or fresh tuck-in M&A. In this scenario, the market's current indifference is the opportunity: a moated, recurring-revenue compounder priced as if its 3% growth is permanent, just before it isn't.

The bear case is that the 3% is, in fact, roughly the steady state. Danaher leverages its scale to push Abcam reagents through channels BioLegend cannot match, slowly choking BioLegend's share. Biopharma keeps R&D budgets frozen and works down inventory, leaving Life Sciences flat. The China exit produces a disappointing price or reveals deeper decay in the broader Euroimmun portfolio. And Signals AI generates impressive demos but no measurable pricing power or net-new contract wins — a feature, not a franchise. In this scenario, Revvity is a fairly valued collection of slow-growing niche monopolies that overpaid for its crown jewel at the top of a bubble, and the flat stock is the market being right.

A disciplined investor will also keep a risk radar running on the mechanisms that could break either case. Demand risk is the central one: a prolonged biopharma funding winter keeps Life Sciences flat regardless of how good the products are. Concentration risk lingers even after the China exit — newborn screening, for all its quality, depends on government budgets and procurement decisions that can shift with public-health politics. Acquisition-accounting risk is real given the ~$6.6 billion of goodwill: a disappointing BioLegend trajectory could force an impairment that, while non-cash, would crystallize the "overpaid" verdict.9 Execution risk runs through the software story — three major product launches in one year is a lot of simultaneous bets, and integration of acquisitions like ACD/Labs is never free. And competitive risk is the slow grind of Danaher and Thermo Fisher leveraging scale to compress Revvity's pricing at the margins. None of these is an emergency; each is a mechanism worth watching for evidence rather than assuming away.

What would falsify each case is admirably concrete, which is part of what makes Revvity an interesting study. The bull case is falsified if, two or three years out, organic growth is still stuck at 3% despite a biopharma recovery — proof that the problem is structural, not cyclical. The bear case is falsified if organic growth climbs durably toward 6-8% and management finally breaks out software ARR to show a high-growth recurring engine underneath. The frameworks above suggest the truth sits in the uncomfortable middle: the moats are real enough to make the bear's "terminal decline" thesis unlikely, but the rivalry and scale disadvantages make the bull's "6-8% reacceleration" far from guaranteed. This is a quality business whose central debate is not survival but growth rate — and growth rate is precisely what the next several quarters will reveal.

The three KPIs that actually matter:

- Pro-forma organic revenue growth (ex-China, ex-COVID-legacy). The whole investment case turns on whether this climbs from today's ~3-4% toward management's 6-8% long-range target. Nothing else matters as much. Watch this number above all.

- Signals software ARR growth. Because management has not broken this out, any incremental disclosure is gold. Sustained high-teens-to-30% recurring software growth would be the proof that the AI/SaaS spine is real and re-rating-worthy; continued vagueness is itself a data point.

- Net-debt-to-adjusted-EBITDA leverage. Track the path from ~2.8x down toward the sub-2.5x zone. Falling leverage restores M&A and buyback optionality; stalling leverage signals that cash generation is not keeping pace with ambition.

Watch those three and the numbers will tell you the story as it actually unfolds, with or without management's narration.

XI. Epilogue

Return one last time to that June 27 press conference in 1990 — the blurry images, the flawed mirror, the symbol of a company brilliant at building physical things and exposed to their unforgiving economics. The Revvity of 2026 is, in nearly every respect, the negative image of that company. It has shed the optics, the bombsights, the industrial instruments, the food-and-soil testing, and finally even the name that carried all of it. What remains is a focused collection of moated niches — newborn screening, proprietary antibody clones, scientific software — pointed at high-margin, recurring, technology-led revenue.

There is a broader industry truth running underneath the Revvity story. Across the life-sciences-tools sector, the same migration has played out at every scale: away from the lumpy economics of selling instruments and toward the compounding economics of consumables, services, and software. Thermo Fisher built an empire on it. Danaher turned it into a religion. Revvity is the mid-cap version of the same conversion — more dramatic in its surgery because it had further to travel and less scale to cushion the journey. Studied that way, Revvity is less an idiosyncratic special situation than a clean, concentrated case study of the single most important business-model shift in its entire industry. That is what makes it worth understanding even for investors who never buy the stock.

The two events that bracket June 2026 capture the entire strategy in miniature. The expansion of agentic AI across Signals and the exit from China immunodiagnostics are two sides of one coin: a management team adding to the high-moat, high-margin assets it wants and amputating the structurally impaired ones it does not. As a piece of corporate strategy, it is coherent, disciplined, and genuinely ambitious — and it has been executed with a consistency and a willingness to take irreversible steps that is rarer than it should be.

What it is not — yet — is a proven one. The market's flat reception is the verdict that investors have heard the narrative and are waiting for the arithmetic to back it. Did Revvity overpay for BioLegend at the top of a bubble, or secure the irreplaceable reagent engine of the next decade? Did it time the China exit with foresight, or merely formalize a loss it could no longer avoid? Was selling the PerkinElmer name a stroke of valuation genius or an expensive cosmetic? The answers are not in the press releases. They are in the next several years of organic growth, software disclosure, and deleveraging — the slow, unglamorous evidence that will determine whether the ultimate corporate metamorphosis produced a butterfly, or merely a more expensive caterpillar.

References

-

PerkinElmer inks massive $5.25B deal for reagent producer BioLegend — Fierce Biotech, 2021-07-26 ↩

-

PerkinElmer Completes Divestiture of its Applied, Food, and Enterprise Services Businesses to New Mountain Capital — Business Wire, 2023-03-13 ↩

-

Danaher to Acquire Abcam for $5.7 Billion — Danaher Corporation, 2023-08-28 ↩

-

How Investors May Respond To Revvity (RVTY) Divesting Its China Immunodiagnostics Business — Sahm Capital, 2026-06-08 ↩↩

-

REVVITY, INC. ($RVTY) CEO 2025 Pay Revealed (DEF 14A filed 2026-03-16) — Quiver Quantitative, 2026 ↩

-

AI in Life Science Analytics Market Outlook 2026-2035 — Precedence Research, 2026-01-15 ↩

-

PerkinElmer Doles Out $600M to Acquire Caliper Life Sciences — GEN (Genetic Engineering & Biotechnology News), 2011-09-08 ↩

-

Revvity, Inc. Form 10-K for Fiscal Year Ended December 28, 2025 — U.S. Securities and Exchange Commission, 2026-02 ↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube