RTX Corporation: The Defense Giant's Second Act

I. Introduction & Episode Roadmap

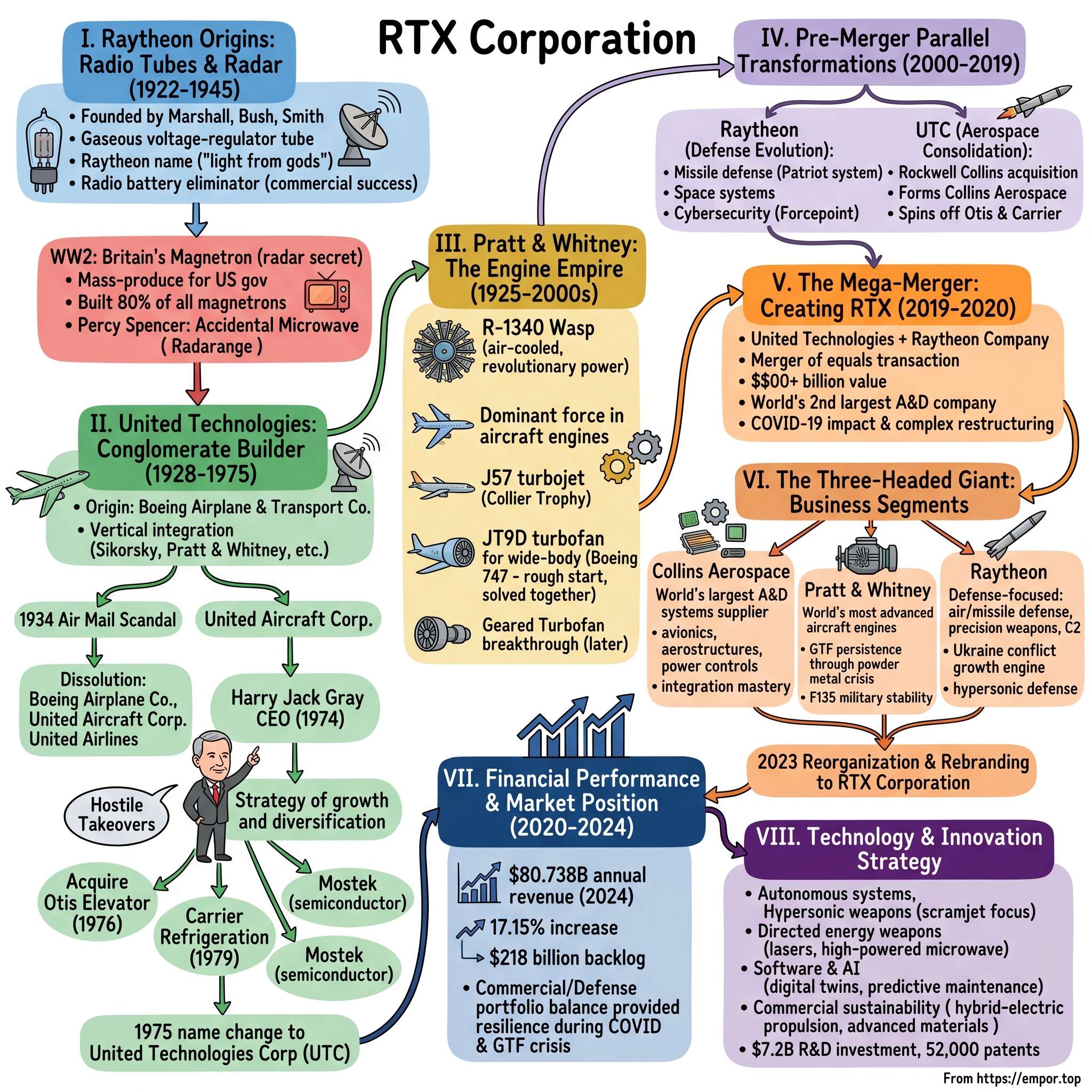

The conference room at United Technologies' Hartford headquarters hummed with tension on a June morning in 2019. Greg Hayes, UTC's CEO, sat across from Tom Kennedy, his counterpart at Raytheon. Between them lay documents that would create a $150 billion aerospace and defense colossus—a merger of equals that would reshape the industry landscape. Neither man blinked first. This wasn't a takeover; it was a marriage between two century-old industrial giants, each bringing their own dowry of technology, talent, and tradition. The successful completion of the all-stock merger of equals transaction between Raytheon Company and United Technologies Corporation came on April 3, 2020, a date that would mark the birth of one of history's most complex industrial combinations. The combined company, valued at more than $100 billion after planned spinoffs, would be the world's second-largest aerospace-and-defense company by sales behind Boeing.

This wasn't just another mega-merger in the defense consolidation wave—it was an architectural masterpiece of corporate engineering. The company was formed by a merger of equals between the aerospace subsidiaries of United Technologies Corporation (UTC) and the Raytheon Company, but the real story lies in what happened before the ink dried. UTC had to first perform corporate surgery, spinning off its Otis elevator and Carrier air conditioning businesses—a $30 billion divestiture that cleared the decks for a pure-play aerospace combination.

The key question haunting this episode: How did two companies with roots stretching back nearly a century—one born from radio tubes and radar, the other from the golden age of aviation—reinvent themselves to dominate the modern defense landscape? The answer involves wartime transformations, Cold War buildups, commercial aviation booms and busts, and ultimately, a recognition that in the 21st century aerospace and defense industry, scale isn't just an advantage—it's survival.

Headquartered in Waltham, Mass., Raytheon Technologies emerged as one of the largest aerospace and defense companies in the world with approximately $74 billion in pro forma 2019 net sales and a global team of 195,000 employees, including 60,000 engineers and scientists. Those engineers would soon be tasked with solving problems that span from hypersonic missiles to sustainable aviation fuel, from quantum computing to directed energy weapons.

Our journey through RTX's formation reveals three critical themes that define modern industrial strategy. First, the delicate dance between commercial and defense exposure—a portfolio balance that smooths the violent cycles inherent to both markets. Second, the power of vertical integration in an era where supply chain control equals competitive advantage. And third, the innovation imperative: how companies born in the mechanical age transformed themselves into software-defined, AI-enabled technology platforms.

As we unpack this story, we'll discover that RTX isn't just the sum of Raytheon and United Technologies. It's the culmination of dozens of acquisitions, thousands of patents, and countless strategic pivots—each one a bet on where aerospace and defense technology was heading next. From Percy Spencer's accidental discovery of the microwave oven to the Geared Turbofan engine that would revolutionize fuel efficiency, this is a story of American industrial innovation at its most ambitious.

II. The Raytheon Origins: From Radio Tubes to Radar (1922–1945)

The summer of 1922 in Cambridge, Massachusetts, was sweltering, and inside a small workshop near the MIT campus, three men were wrestling with a problem that would define the next century of defense technology. The Raytheon Company was founded in 1922 in Cambridge, Massachusetts, by Laurence K. Marshall, Vannevar Bush, and Charles G. Smith as the American Appliance Company. But calling it the "American Appliance Company" was almost comically mundane for what would become one of the most sophisticated defense contractors on Earth.

Vannevar Bush—yes, the same visionary who would later coordinate the entire U.S. scientific war effort and conceive the modern internet's precursor—wasn't thinking about missiles or radar in those early days. He was thinking about refrigerators. Its focus, which was originally on new refrigeration technology, soon shifted to electronics. The pivot came from an unlikely source: the stars themselves. The company's first product was a gaseous (helium) voltage-regulator tube that was based on Charles Smith's earlier astronomical research of the star Zeta Puppis. Charles Smith, the scientist of the trio, had been studying this peculiar blue supergiant star, analyzing its spectrum and radiation patterns. His astronomical work led to an unexpected breakthrough: understanding how to control electrical flow through helium gas. The electron tube was christened with the name Raytheon (a compound of Old French and Greek meaning 'light from the gods') and was used in a battery eliminator, a type of radio-receiver power supply that plugged into the power grid in place of large batteries.

This wasn't just clever engineering—it was solving a massive consumer pain point. In the 1920s, radio owners had to lug around expensive, heavy batteries that died quickly and leaked acid on their carpets. Raytheon's tube let radios plug directly into wall outlets, converting AC to DC power. The market exploded. In 1925, the company changed its name to Raytheon Manufacturing Company and began marketing its rectifier, under the Raytheon brand name, with commercial success.

But the real transformation—the pivot that would define the next century—came with World War II. Early in World War II, physicists in the United Kingdom invented the magnetron, a specialized microwave-generating electron tube that markedly improved the capability of radar to detect enemy aircraft. The magnetron was Britain's most closely guarded secret, arguably more important than the atomic bomb in winning the war. In 1940, the British Tizard Mission brought the cavity magnetron to America in what has been called "the most valuable cargo ever brought to our shores. "American companies were then sought by the US government to perfect and mass-produce the magnetron for ground-based, airborne, and shipborne radar systems, and, with support from the Massachusetts Institute of Technology's Radiation Laboratory (recently formed to investigate microwave radar), Raytheon received a contract to build the devices. Here's where the story becomes distinctly American: scale and speed. Within a few months, Raytheon began to manufacture magnetron tubes for use in radar sets, and then complete radar systems.

The numbers tell a staggering story of industrial mobilization: At war's end in 1945, the company had built about 80 percent of all magnetrons. Think about that—a company that started making battery eliminators for radios was now producing the majority of the Allied forces' most critical military technology. Raytheon ranked 71st among U.S. corporations in the value of World War II military production contracts—not bad for a company that had been making vacuum tubes just years earlier.

But the magnetron's greatest peacetime gift came from Percy Spencer, a self-taught engineer who never finished grammar school but became one of the world's leading experts on magnetron design. The legend goes that Spencer was working on magnetrons when he noticed a chocolate bar in his pocket had melted. Rather than cursing his ruined snack, Spencer had the presence of mind to investigate. He placed popcorn kernels near the magnetron—they popped. He tried an egg—it exploded. In 1945, Raytheon's Percy Spencer invented the microwave oven by discovering that the magnetron could rapidly heat food. In 1947, the company demonstrated the Radarange microwave oven for commercial use.

This accidental discovery would eventually put Raytheon technology in millions of American kitchens, but more importantly, it demonstrated something fundamental about the company's DNA: the ability to see dual-use potential in military technology. That pattern—defense innovation bleeding into commercial markets—would define not just Raytheon but the entire American aerospace industry for the next century.

The transformation from radio tubes to radar fundamentally changed Raytheon's trajectory. By war's end, this scrappy Massachusetts company had proven it could compete with giants like Western Electric, RCA, and GE. More importantly, it had forged deep relationships with the military establishment and MIT that would sustain it through the Cold War. The company that started by eliminating batteries had become essential to eliminating enemy aircraft. The stage was set for Raytheon's evolution into a permanent fixture of the military-industrial complex.

III. United Technologies: The Conglomerate Builder (1929–1975)

While Raytheon was tinkering with electron tubes in Cambridge, a very different industrial story was unfolding on the West Coast. William Boeing stood on the shore of Lake Union in Seattle in 1928, watching his seaplanes take off into the morning mist. He had built an empire—Boeing Airplane & Transport Corporation—that controlled everything from the aluminum in the aircraft skin to the passengers buying tickets. It was beautiful, integrated, efficient. Within six years, the federal government would tear it all apart. The origin of UTC lies with the company formed in 1928 by William E. Boeing as Boeing Airplane & Transport Corporation. Within a year the company was renamed United Aircraft and Transport Corporation and acquired a number of aircraft- and aircraft-component-manufacturing companies including Sikorsky Aviation, Stearman Aircraft, Avion (later Northrop Aircraft), Chance Vought (aircraft), Hamilton (propellers and aircraft), and Pratt & Whitney (engines). This wasn't just vertical integration—it was total domination of the aviation supply chain.

But the empire was too perfect to last. The 1934 Air Mail scandal erupted when Senator Hugo Black—yes, the future Supreme Court Justice—launched investigations into "spoils conferences" where lucrative airmail contracts had been divvied up among the aviation giants. President Roosevelt cancelled all airmail franchises and handed delivery to Army pilots. Ten died in two weeks, flying in planes utterly unsuited for mail delivery. The public outcry was immediate, but the damage to the conglomerates was done.

In response to legislation prohibiting the affiliation of airlines with aviation manufacturers, United Aircraft and Transport Corporation was dissolved in 1934, resulting in three separate companies. Manufacturing facilities west of the Mississippi River became Boeing Airplane Company, those east of it became United Aircraft Corporation, and all transportation services were unified as United Airlines. William Boeing, embittered by the breakup of his empire, sold all his stock and essentially walked away from the industry he'd helped create.

United Aircraft Corporation, the eastern remnant of Boeing's empire, retained Pratt & Whitney, Sikorsky, Hamilton Standard, and Chance Vought. Based in Hartford, Connecticut, it would spend the next four decades as a collection of brilliant but disparate aerospace businesses, each maintaining its own identity and culture. During World War II, United Aircraft ranked sixth among United States corporations in the value of wartime production contracts—a testament to the power of its constituent companies, particularly Pratt & Whitney's engines.

The post-war years saw United Aircraft evolve but not truly transform. It remained a federation of aerospace companies, each excellent in its domain but lacking a unifying strategic vision beyond aerospace. That changed dramatically when Harry Jack Gray arrived. In 1974, Harry Jack Gray left Litton Industries to become the CEO of United Aircraft. Gray was a character straight from central casting for 1970s corporate America—a Silver Star veteran from the Battle of the Bulge who'd changed his last name from Grusin to Gray in 1951 for, according to court records, "no reason." The Wall Street Journal would later call him "a merger artist who resented making just one deal at a time." Gray maintained a list of 50 companies he wanted to acquire, treating M&A like a personal collection rather than a strategic exercise.

He pursued a strategy of growth and diversification, changing the parent corporation's name to United Technologies Corporation (UTC) in 1975 to reflect the intent to diversify into numerous high tech fields beyond aerospace. The change became official on May 1, 1975. This wasn't just rebranding—it was a declaration of war on the traditional boundaries of the aerospace industry.

In 1976, UTC forcibly acquired Otis Elevator for $276 million. The word "forcibly" is key here—Gray pioneered the hostile takeover in industrial America, using UTC's cash flow from defense contracts to fund aggressive acquisitions. The Otis acquisition was particularly brilliant: elevators are recession-resistant (buildings still need them maintained), counter-cyclical to aerospace, and generate predictable service revenue.

In 1979, Carrier Refrigeration was acquired in another hostile takeover, along with Mostek, a semiconductor company. The Mostek acquisition would prove disastrous—UTC would later write off $424 million—but it demonstrated Gray's ambition to transform UTC into something beyond aerospace. He wanted to build the American Siemens or Hitachi, a technology conglomerate spanning every industry.

Gray's management style was as aggressive as his acquisition strategy. One former executive said, "Harry equates his corporate position with his own mortality." When potential successors emerged, Gray would systematically undermine them. His refusal to name a successor or step down at retirement age created a succession crisis that nearly tore UTC apart. When he finally retired in 1986, UTC had grown from a $2 billion aerospace company to a $16 billion conglomerate.

But here's the crucial insight: Gray's diversification strategy, while financially successful in the short term, created a fundamental strategic problem. UTC now had world-class positions in aerospace (Pratt & Whitney, Sikorsky), building systems (Otis, Carrier), and various industrial products. Each business required different capabilities, served different customers, and operated on different cycles. The synergies that justified the premium prices paid in hostile takeovers never fully materialized.

This conglomerate structure would define UTC for the next three decades—brilliant individual businesses held together by financial engineering rather than operational logic. It would take another generation of leaders, and ultimately the Raytheon merger, to finally resolve the strategic contradictions Gray had created. His legacy was both UTC's transformation into a industrial powerhouse and the strategic complexity that would eventually force its breakup and reformation as RTX.

IV. Pratt & Whitney: The Engine Empire (1925–2000s)

The story of Pratt & Whitney begins not in a boardroom but in a converted tobacco warehouse in Hartford, Connecticut, where in 1925, Frederick Rentschler was about to gamble everything on a radical new engine design. Rentschler had quit his job as president of Wright Aeronautical—walking away from the company founded by the Wright Brothers themselves—because the board wouldn't let him build the engine he envisioned. Now, with backing from the Pratt & Whitney Machine Tool Company (which had excess factory space and capital but no aviation experience), he had one shot to prove his vision. Pratt & Whitney originated as the creation of the businessman Frederick B. Rentschler. In 1925 the machine-tool maker Pratt and Whitney provided Rentschler with start-up funds, idle plant space, and a company name to create an aircraft engine manufacturer. Rentschler had quit Wright Aeronautical in frustration—the investment bankers running the company had no interest in aviation innovation. He took with him George Mead, Wright's chief engineer, and a handful of the best designers.

Their first creation would revolutionize aviation. On Christmas Eve 1925, the team completed their first engine, the R-1340 Wasp. Rentschler's wife Faye had suggested the name—a wasp was small but packed a powerful sting. The engine delivered 425 horsepower while weighing only 650 pounds, an unprecedented power-to-weight ratio. More importantly, it was air-cooled rather than liquid-cooled, eliminating the radiators, hoses, and pumps that added weight and created failure points in existing engines.

The Wasp engine revolution wasn't just technical—it was commercial. The U.S. Navy immediately ordered 200 engines for its new aircraft carriers Lexington and Saratoga. Commercial airlines quickly followed. Boeing's Model 40A, powered by the Wasp, made airmail delivery profitable for the first time. Charles Lindbergh and Amelia Earhart set records in Wasp-powered aircraft. By the 1930s, Pratt & Whitney had become the dominant force in aircraft engines.

The great demand for Pratt & Whitney piston engines during World War II—more than 360,000 engines were shipped for the wartime effort—diverted the company from early jet-engine development, allowing its competitors General Electric and Westinghouse initially to overtake it in this area. This would become a pattern: Pratt & Whitney's success in one generation of technology often delayed its transition to the next. Nevertheless, by the early 1950s Pratt & Whitney had leapfrogged the rest of the industry with its first turbojet design, the J57. First run in January 1950, it was the first 10,000-pound thrust class engine in the United States. The J57 featured a revolutionary two-spool design—essentially two engines in one, with separate low-pressure and high-pressure compressors. This allowed it to operate efficiently across a wide range of speeds and altitudes.

The prestigious Collier Trophy for 1952 was awarded to Leonard S. Hobbs, chief engineer of United Aircraft Corporation, for "designing and producing the P&W J57 turbojet engine." The engine powered everything from the B-52 bomber to the Boeing 707 and Douglas DC-8—the first successful American jetliners. Production figures reached 21,186 engines, making it one of the most successful jet engines ever built. In 1965 Pratt & Whitney launched a program to develop a more efficient engine for wide-body aircraft. The resulting JT9D turbofan, which introduced many new technologies in structures, aerodynamics, and materials to improve efficiency and reliability, opened a new era in commercial aviation with its application to new versions of Boeing and McDonnell Douglas transports, including the Boeing 747. The JT9D program was launched in September 1965 and the first engine was tested in December 1966.

But the path to success was rocky—literally. Pratt & Whitney faced difficulties with the JT9D design during the Boeing 747 test program. Engine failures during the flight test program resulted in thirty aircraft being parked outside the factory with concrete blocks hanging from the pylons, awaiting redesigned engines. The trouble was traced to ovalization, in which stresses during takeoff caused the engine casing to deform into an oval shape, resulting in rubbing of high-pressure turbine blade tips. Boeing and Pratt & Whitney worked desperately together in 1969 to solve the problem, strengthening the engine casing and adding yoke-shaped thrust links.

The JT9D crisis nearly destroyed both companies. Boeing had bet everything on the 747, and Pratt & Whitney had invested massively in the high-bypass turbofan technology. The fact that they solved it together—under enormous pressure, with the world watching—forged a partnership that would define commercial aviation for decades. Since entering service on the Boeing 747 aircraft in 1970, more than 3,200 JT9D engines were delivered, powering the 747, 767, A300, A310, and DC-10.

The Geared Turbofan breakthrough would come much later, representing Pratt & Whitney's most revolutionary innovation since the turbofan itself. But the journey from the Wasp to the GTF shows a consistent pattern: technical brilliance coupled with execution challenges, followed by eventual dominance. Pratt & Whitney's engine empire wasn't built on smooth victories but on the ability to solve seemingly impossible problems under extreme pressure—a capability that would prove essential when merging with Raytheon to create RTX.

V. The Pre-Merger Era: Parallel Transformations (2000–2019)

The morning of September 11, 2001, changed everything for both Raytheon and United Technologies. As the towers fell in New York, defense executives across America knew that their industry was about to experience a fundamental shift. For Raytheon, it would mean a surge in demand for precision weapons and missile defense systems. For UTC, it would mean both opportunity and challenge—military contracts would soar, but commercial aviation would enter its darkest period since the jet age began. Raytheon's modern defense evolution centered on three pillars: missile defense, space systems, and increasingly, cybersecurity. The Patriot missile system, which had gained fame during the 1991 Gulf War, evolved into the backbone of air defense for 19 countries. Since January 2015, Patriot had intercepted more than 150 ballistic missiles in combat operations around the world. The system's continuous upgrades—from PAC-2 to PAC-3 to the new Lower-Tier Air and Missile Defense Sensor—demonstrated Raytheon's ability to maintain technological edge through iterative improvement rather than revolutionary leaps.

In September 2009, Raytheon purchased Bolt Beranek and Newman Inc. as a wholly owned subsidiary—the company that had built ARPANET, the internet's precursor. This acquisition signaled Raytheon's recognition that future warfare would be as much about bytes as bullets. In May 2015, Raytheon acquired cybersecurity firm Websense, Inc. from Vista Equity Partners for $1.9 billion, later rebranding it as Forcepoint. The company was building a portfolio that spanned from kinetic interceptors to cyber defense, recognizing that modern threats didn't respect traditional domain boundaries.

Meanwhile, UTC was executing its own transformation, but in the opposite direction—consolidation rather than diversification. In 2017, UTC proposed to acquire Rockwell Collins in cash and stock for $23 billion, $30 billion including Rockwell Collins' net debt, for $500+ million of synergies expected by year four. The deal, completed in 2018, was one of the largest in aerospace history. It brings together Rockwell Collins and UTC Aerospace Systems to create Collins Aerospace Systems, an industry leader with a global presence of 70,000 employees in 300 sites and $23 billion in annual sales on a 2017 pro forma basis.

UTC's acquisition of Rockwell Collins represented a fundamental strategic shift. Rather than Gray's conglomerate-building of the 1970s, this was about creating aerospace scale to compete with vertically integrating OEMs. Boeing and Airbus were increasingly bringing capabilities in-house, squeezing suppliers on price through programs like "Partnering for Success," and aggressively pursuing aftermarket revenue that traditionally belonged to suppliers. UTC needed scale to push back.

But even as UTC completed the Rockwell Collins integration, CEO Greg Hayes was already planning the company's next transformation. The conglomerate structure—with Otis elevators and Carrier air conditioning alongside aerospace—no longer made strategic sense. The markets valued focused companies higher than conglomerates. Hayes began preparing for what would become the most complex corporate restructuring in American industrial history: spinning off Otis and Carrier while simultaneously merging with Raytheon.

The parallel transformations of Raytheon and UTC in the 2000s and 2010s set the stage for their eventual merger. Raytheon had evolved from a missile manufacturer into a broad defense technology company, adding cybersecurity and space capabilities to its traditional strengths. UTC had consolidated its aerospace holdings while preparing to shed its non-aerospace businesses. Both companies recognized that the future belonged to those with scale, technological breadth, and balanced exposure to commercial and defense markets. The only question was whether they would recognize that their futures lay together.

VI. The Mega-Merger: Creating RTX (2019–2020)

Tom Kennedy, Raytheon's CEO, stared at the presentation slide showing defense spending projections through 2030. It was early 2019, and while the numbers looked good, he knew the cycles too well. Defense budgets surge during conflicts, then inevitably contract. Meanwhile, on the commercial side, the Boeing 737 MAX was grounded, trade wars were escalating, and everyone was whispering about a coming recession. Raytheon needed balance—the kind only a major commercial aerospace presence could provide.

Three hundred miles south in Farmington, Connecticut, Greg Hayes was running his own calculations. UTC's soon-to-be-completed Rockwell Collins integration had created a aerospace systems powerhouse, but he lacked sufficient defense exposure to smooth the violent cycles of commercial aviation. The math was compelling: combine two companies with roughly equal commercial and defense revenue, and you create a giant that could weather any storm.

In June 2019, United Technologies announced the intention to merge with defense contractor Raytheon to form Raytheon Technologies Corporation. The combined company, valued at more than $100 billion after planned spinoffs, would be the world's second-largest aerospace-and-defense company by sales behind Boeing. But this wasn't a typical acquisition—it was structured as a true merger of equals, with UTC shareholders owning 57% and Raytheon shareholders 43% of the combined entity, reflecting their relative contributions to the merged company's value.

The strategic rationale went beyond simple diversification. Hayes and Kennedy had identified $1 billion in annual cost synergies by year four, but the real value lay in revenue synergies that Wall Street couldn't easily model. Raytheon's missiles could benefit from UTC's advanced materials. Collins Aerospace's sensors could enhance Raytheon's radar systems. Pratt & Whitney's engine expertise could accelerate Raytheon's hypersonic propulsion development. The intellectual property cross-pollination alone justified the merger premium.

But first came the surgical separation. In March 2020, United Technologies Corporation announced the separations of Carrier Global and Otis Worldwide. This wasn't just a spinoff—it was a $20 billion market cap creation event. Carrier, with its $18 billion in annual revenue, would become an independent climate technology leader. Otis, generating $13 billion annually, would stand alone as the world's largest elevator company. Both businesses were healthy, growing, and generated strong cash flows—exactly the wrong time to sell according to conventional wisdom, but exactly the right time to maximize shareholder value.

The timing couldn't have been worse—or perhaps better, depending on perspective. COVID-19 was spreading globally, commercial aviation was collapsing, and capital markets were in freefall. Yet Raytheon Technologies Corporation announced the successful completion of the all-stock merger of equals transaction between Raytheon Company and United Technologies Corporation on April 3, 2020, following the completion by United Technologies of its previously announced spin-offs of its Carrier and Otis businesses. The fact that they closed the deal amid such chaos demonstrated both management teams' conviction in the strategic logic.

Integration challenges immediately surfaced. Combining two companies with 195,000 employees across hundreds of facilities during a global pandemic required unprecedented flexibility. Virtual integration meetings replaced in-person sessions. Travel restrictions meant site visits happened through video calls. The traditional playbook for post-merger integration—bringing teams together physically to build culture and alignment—was impossible.

Cultural differences ran deeper than geography. Raytheon's Waltham headquarters embodied the Boston defense establishment—formal, hierarchical, steeped in military protocol and classification levels. UTC's Connecticut operations reflected a more commercial mindset—faster-moving, cost-conscious, focused on quarterly earnings rather than multi-year government contracts. Engineers who'd spent careers optimizing for weight in commercial aircraft now worked alongside those who optimized for survivability in combat systems.

The integration complexity extended to systems and processes. Raytheon operated on government cost-accounting standards that tracked every hour and dollar with forensic precision. UTC's commercial businesses required speed and flexibility to respond to airline customers who might change orders overnight. Harmonizing IT systems alone required an 18-month effort involving 2,000 IT professionals and $400 million in integration costs.

Yet by late 2020, the merger synergies were already materializing. Supply chain consolidation yielded immediate savings—the combined company was suddenly buying twice as much titanium, twice as many semiconductors, twice as many specialized alloys. Suppliers who'd previously played one company against the other now faced a single negotiator. The company identified over 180 facilities for consolidation, expecting $350 million in real estate savings alone.

The merger also created unexpected innovation opportunities. Raytheon's expertise in gallium nitride semiconductors for radar systems could improve Collins Aerospace's commercial avionics. Pratt & Whitney's ceramic matrix composites developed for jet engines found applications in Raytheon's hypersonic vehicles. The companies' combined patent portfolio—52,000 patents and applications—became a competitive moat that no single competitor could match.

VII. The Three-Headed Giant: Business Segments Deep Dive

Collins Aerospace emerged from the merger as the world's largest aerospace systems supplier, a title that carried both opportunity and burden. Collins Aerospace Systems specializes in aerostructures, avionics, interiors, mechanical systems, mission systems and power controls that serve customers across the commercial, regional, business aviation and military sectors. The segment is led by President Stephen Timm, headquartered in Charlotte, North Carolina, with approximately $26 billion in 2019 net sales.

The Collins story within RTX is one of integration mastery. The business combined UTC Aerospace Systems—itself a rollup of Goodrich, Hamilton Sundstrand, and dozens of smaller acquisitions—with Rockwell Collins' avionics leadership. The result: a supplier that touches virtually every aircraft flying today. On a typical Boeing 787, Collins provides 11 major systems, from the auxiliary power unit to the landing gear, from flight controls to cabin interiors. This content-per-aircraft advantage creates powerful aftermarket dynamics—when airlines need spare parts, they have one phone number to call.

Collins' commercial aerospace exposure proved both blessing and curse during COVID-19. Revenue collapsed 30% in 2020 as airlines parked aircraft and deferred maintenance. But the segment's diversity provided cushion—military programs, business jets, and helicopters partially offset commercial weakness. More importantly, Collins used the downturn to restructure, eliminating 13,000 positions and closing 20 facilities, emerging leaner as aviation recovered.

The segment's real competitive advantage lies in systems integration. While competitors might excel in individual components, Collins offers complete solutions. Their connectivity systems don't just provide Wi-Fi to passengers—they integrate with flight management systems, maintenance computers, and ground operations. This systems-level thinking, inherited from Rockwell Collins' avionics heritage, commands premium pricing and creates switching costs that lock in customers for aircraft lifecycles spanning decades.

Pratt & Whitney represents RTX's most technologically ambitious bet: the Geared Turbofan engine that promised to revolutionize commercial aviation fuel efficiency. Pratt & Whitney designs, manufactures and services the world's most advanced aircraft engines and auxiliary power systems for commercial, military and business aircraft. The segment is led by President Chris Calio, headquartered in East Hartford, Connecticut, with approximately $21 billion in 2019 net sales.

The GTF story is one of persistence through pain. The engine's revolutionary architecture—using a gear reduction system to allow the fan and turbine to rotate at optimal speeds independently—delivered 16% better fuel efficiency than previous generation engines. Airlines loved the economics. By 2023, Pratt had captured over 50% of the narrow-body engine market, breaking the Boeing 737/CFM International duopoly that had dominated for decades.

But the triumph turned to crisis when powder metal defects were discovered in 2023, requiring accelerated inspections and repairs on roughly 3,000 engines. The financial impact was staggering—$3 billion in charges, 300 aircraft grounded simultaneously, and airline customers furious about compensation. Yet Pratt's response demonstrated RTX's financial strength: the company could absorb the hit while maintaining R&D spending and dividend payments, something a standalone engine manufacturer might not have survived.

The segment's military portfolio provided crucial stability during the GTF crisis. The F135 engine powering the F-35 fighter generated steady revenue and margins, with over 1,000 engines delivered and thousands more on order. The adaptive engine technology Pratt developed for next-generation fighters—engines that can shift between high thrust and high efficiency modes—positioned them for the sixth-generation fighter competitions worth potentially $100 billion over the next decades.

Raytheon, the defense-focused segment, brought to RTX what the commercial businesses lacked: predictable, multi-year government contracts with built-in profit margins. The segment specialized in integrated air and missile defense systems, precision weapons, radars, command and control systems, and cybersecurity solutions. Its portfolio read like a catalog of American military power: Patriot air defense, Standard Missiles for Navy ships, Tomahawk cruise missiles, and classified programs that generated 15% of revenue but whose details remained hidden even from most RTX executives.

The Ukraine conflict that began in 2022 transformed Raytheon from steady performer to growth engine. The segment is rushing to boost production of Stinger missiles by refurbishing hundreds in surplus of its allies' stocks after the U.S. sent 1,400 of the weapons to Ukraine. European nations, watching Russian aggression, accelerated defense modernization. Poland alone ordered $15 billion in Raytheon systems. The Pentagon initiated multi-year procurement contracts for missiles, providing unprecedented demand visibility through 2030.

But Raytheon's real innovation lay beyond traditional weapons. The segment's work on hypersonic defense—systems to detect and intercept missiles traveling at Mach 5+—positioned RTX for the next era of strategic competition. Their directed energy weapons, including high-energy lasers for counter-drone operations, offered militaries cost-effective alternatives to expensive missiles for defeating cheap threats. The integration with Collins and Pratt enhanced these capabilities: Collins' sensors improved radar performance, while Pratt's materials expertise accelerated hypersonic vehicle development.

The 2023 reorganization reflected RTX's evolution from merger integration to operational optimization. In January 2023, Raytheon Technologies announced it would combine its missiles and defense division and intelligence and space division into a single business unit, effective July 1. The reorganization created three divisions at Raytheon Technologies: Collins Aerospace, Pratt & Whitney, and Raytheon. The reorganization was preceded by the rebranding to RTX in June 2023. In July 2023, Raytheon Technologies Corporation changed its name to RTX Corporation.

The rebranding to RTX wasn't just cosmetic—it signaled the company's transformation from a collection of heritage brands to an integrated defense and aerospace enterprise. The three-segment structure clarified reporting, simplified customer relationships, and accelerated decision-making. Each segment maintained P&L responsibility while benefiting from shared services in IT, procurement, and research. The model balanced autonomy with integration, allowing each business to serve its unique markets while capturing enterprise synergies.

VIII. Financial Performance & Market Position (2020–2024)

The numbers tell a story of resilience, recovery, and ultimately, remarkable growth. When RTX closed its merger in April 2020, commercial aviation was experiencing its worst crisis since the Wright Brothers. Global air traffic had dropped 90%. Boeing and Airbus slashed production rates. Airlines parked thousands of aircraft in desert boneyards. Yet RTX's first earnings call as a merged company projected confidence: the balanced portfolio would see them through.

The COVID impact was immediate and brutal. Commercial aerospace revenue fell 33% in 2020, with aftermarket sales—typically the most profitable segment—down 40%. RTX burned through $2 billion in free cash flow as it maintained employment and R&D spending despite the downturn. The company took $3.5 billion in charges for workforce reductions, facility closures, and asset impairments. Wall Street questioned whether the merger's timing had destroyed value rather than created it.

But defense provided the ballast. Raytheon's revenue grew 7% in 2020, with international sales particularly strong as allies accelerated modernization programs. The U.S. defense budget continued growing despite the pandemic, with particular emphasis on RTX's strengths: missile defense, space systems, and cybersecurity. By year-end 2020, RTX's defense backlog had grown to $64 billion, providing multi-year revenue visibility that commercial aerospace couldn't match.

The recovery, when it came, exceeded expectations. RTX annual revenue for 2024 was $80.738B, a 17.15% increase from 2023. RTX annual revenue for 2023 was $68.92B, a 2.75% increase from 2022. RTX annual revenue for 2022 was $67.074B, a 4.17% increase from 2021. The 2024 surge reflected three factors: commercial aviation's recovery to pre-pandemic levels, defense spending driven by geopolitical tensions, and pricing power from supply chain constraints that allowed RTX to expand margins. The backlog dynamics tell a compelling story of momentum. Company backlog of $218 billion; including $125 billion of commercial and $93 billion of defense at the end of 2024, up from Company backlog of $196 billion; including $118 billion of commercial and $78 billion of defense in 2023. The defense backlog surge—from $78 billion to $93 billion in a single year—reflects the Ukraine conflict's impact on global defense priorities.

The Arlington, Virginia-based aerospace and defense contractor's financial trajectory demonstrated the power of the balanced portfolio strategy. Defense revenues surged as NATO allies scrambled to rebuild depleted weapon stocks and modernize aging systems. Demand for Raytheon's products remains strong, with a $63 billion backlog and a 1.48 book-to-bill ratio. In the US, it's about replenishment, while in Europe, it's about integrated air and missile defense. International demand is robust, with NATO countries committing to sustained spending increases.

Commercial aviation's recovery proved equally dramatic. After the 2020 collapse, airlines discovered they'd cut too deep. The revenge travel boom of 2022-2023 caught carriers unprepared, with insufficient aircraft and maintenance capacity. RTX's aftermarket business—selling spare parts and maintenance services—exploded. Margins in aftermarket typically run 35-40%, versus 15-20% for original equipment, making this recovery particularly profitable.

Stock performance reflected this operational momentum. RTX shares rose from $60 in October 2022 to over $120 by late 2024, dramatically outperforming the broader market. The company returned $3.7 billion of capital to shareholders in 2024, contributing to over $33 billion returned since the merger, demonstrating management's confidence in cash generation despite ongoing investments in technology and capacity.

But the GTF engine crisis tested RTX's financial resilience like nothing since the merger. The powder metal issue discovered in 2023 required inspecting and potentially replacing parts in 3,000 engines—roughly 70% of the GTF fleet. Airlines grounded hundreds of aircraft during peak travel season. Compensation negotiations turned acrimonious. The financial hit was massive: $3 billion in charges, with ongoing compensation payments expected through 2026.

Yet the crisis paradoxically demonstrated RTX's strength. A standalone engine company might have faced bankruptcy or forced sale. RTX absorbed the hit while maintaining its dividend, continuing R&D investments, and even buying back stock. The defense business provided the cash flow cushion that made this possible. Collins Aerospace's aftermarket boom offset some of Pratt's weakness. The portfolio balance that seemed like financial engineering in 2019 proved its worth in crisis.

IX. Technology & Innovation Strategy

The future of warfare appeared on computer screens in Tucson, Arizona, where RTX engineers were designing missiles that could think. Not guided missiles—those had existed since World War II—but truly autonomous systems capable of identifying, prioritizing, and engaging targets without human intervention. The ethical implications were staggering. The technological challenges even more so. But this was where RTX was betting its future: the intersection of artificial intelligence, hypersonic flight, and directed energy that would define 21st-century conflict. Today, that drive is evident in the work of the researchers, engineers and other innovators who are using the company's $7.2 billion research-and-development investment and 52,000 patents to make air travel safer, more sustainable and more connected. RTX plans to invest over $7.5 billion in R&D in 2025 to advance technologies and meet customer needs. But the nature of that research has fundamentally shifted from the mechanical innovations of previous generations to software-defined, AI-enabled systems that blur the line between physical and digital warfare.

Hypersonic weapons represent RTX's most visible bet on next-generation warfare. Hypersonic weapons travel faster than five times the speed of sound — Mach 5 — covering vast distances in minutes. Hard to stop, they fly and nimbly maneuver to avoid detection and dodge defensive countermeasures. The technical challenges are staggering: at Mach 5+, air friction generates temperatures exceeding 3,000 degrees Fahrenheit, hot enough to melt most metals. Materials must withstand not just heat but the violent pressure changes and vibrations of hypersonic flight.

Raytheon, an RTX business, has successfully completed a technical review and a seamless prototype fit-check in phase one of the U.S. Navy's Hypersonic Air Launched Offensive Anti-Surface (HALO) program. HALO is a carrier-based high-speed missile that will allow the Navy to operate in and control contested battlespaces in anti-access/area denial environments and will support their long-range fires strategy. The company is also developing the Hypersonic Attack Cruise Missile (HACM) for the Air Force, with the aim to have the Hypersonic Air-breathing Weapon Concept [HACM] fully operational by 2028.

RTX's approach to hypersonics differs from competitors. While Lockheed Martin pursues boost-glide vehicles that rocket to the edge of space then glide to targets, RTX focuses on air-breathing scramjets that sustain hypersonic flight using atmospheric oxygen. We're applying our advanced weapon expertise to develop air-breathing hypersonic scramjet systems that use fast-moving air around them to provide oxygen for propulsion, relying on a single solid rocket booster with no moving parts. This design results in a lower risk, less complex and more cost-effective solution when compared to other systems.

But hypersonics are just one element of RTX's technology portfolio. Directed energy weapons—lasers and high-powered microwave systems—promise to revolutionize defense economics. A Patriot missile costs $4 million; a laser shot costs about $10 in electricity. Against drone swarms or cheap rockets, the math becomes compelling. RTX's high-energy laser systems have already demonstrated the ability to track and destroy drones, mortars, and rockets in testing.

The real revolution, however, lies in software and artificial intelligence. Modern missiles aren't just guided—they're intelligent. RTX's newest systems use machine learning to identify targets, discriminate between military and civilian objects, and adapt tactics in real-time. The ethical implications are profound: who decides when a machine can take a life? RTX has instituted AI ethics boards and red teams to stress-test systems, but the questions remain largely unanswered.

Commercial aerospace innovation follows a different trajectory, driven by sustainability imperatives and economic pressures. The aviation industry contributes 2-3% of global CO2 emissions, a figure that will grow as air travel expands unless technology intervenes. RTX's response spans multiple fronts: more efficient engines, sustainable aviation fuels, hybrid-electric propulsion, and eventually, hydrogen power.

The Geared Turbofan engine already delivers 16% better fuel efficiency than previous generations, but RTX is targeting 30% improvement by 2035. Advanced materials like ceramic matrix composites allow engines to run hotter and more efficiently. Digital twins—virtual replicas of physical engines—enable predictive maintenance that reduces fuel burn by optimizing performance before problems develop.

Electric and hybrid-electric propulsion represents a longer-term bet. Collins Aerospace is developing 1-megawatt electric motors for regional aircraft, with commercial service targeted for the 2030s. The challenges are daunting: batteries remain too heavy for long-range flight, cooling systems for high-power electronics add weight and complexity, and certification standards for electric aircraft don't yet exist.

The patent portfolio tells its own story of innovation evolution. While the technologies have evolved – focusing today on areas like avionics, cybersecurity, directed energy, electric propulsion, hypersonics and quantum physics – what hasn't changed is the company's drive for era-defining innovations. Of RTX's 52,000 patents, increasingly few cover mechanical systems. The growth areas: artificial intelligence, quantum computing, cybersecurity, and advanced materials. Each patent represents not just an invention but a competitive moat in industries where technology advantages compound over decades.

We are applying our expertise from over 50 years of missile experience and capabilities to digital engineering tools such as digital twins, modeling, and simulation, to accelerate hypersonic development. This digital transformation extends beyond design to manufacturing. RTX's factories increasingly resemble software companies: 3D printing of rocket components, automated assembly guided by computer vision, and AI-driven quality control that catches defects humans miss.

The R&D investment strategy reflects portfolio thinking. Roughly 40% goes to near-term product improvements—incremental advances in existing systems. Another 40% targets medium-term opportunities—technologies that will enter service in 5-10 years. The final 20% funds long-term research into quantum computing, artificial general intelligence, and other technologies that may not yield products for decades, if ever.

This innovation strategy creates a virtuous cycle. Defense contracts fund basic research that yields commercial applications. Commercial revenues support defense R&D during budget downturns. The cross-pollination of ideas—military AI improving commercial flight safety, airline efficiency techniques reducing weapon system costs—creates value that neither business could achieve alone. In an era where technology determines both military superiority and commercial competitiveness, RTX's innovation engine may be its most valuable asset.

X. Playbook: Business & Investing Lessons

The RTX story offers a masterclass in industrial strategy, but the lessons extend far beyond aerospace and defense. At its core, this is a story about managing complexity, creating value through integration, and building competitive advantages that compound over decades. The playbook that emerges challenges conventional wisdom about focus, disruption, and value creation in capital-intensive industries.

The Power of Scale in Aerospace & Defense operates differently than in consumer technology. While software companies achieve scale through network effects and zero marginal costs, aerospace scale comes from spreading enormous fixed costs across larger production volumes. Developing a new jet engine costs $10 billion; whether you sell 100 or 10,000 engines determines everything. RTX's scale allows it to amortize R&D across three major segments, each supporting the others during cyclical downturns.

But scale without integration is merely size. The real power comes from operational synergies that competitors can't replicate. When Collins Aerospace develops a new material for aircraft structures, Raytheon can apply it to missile casings. When Pratt & Whitney advances ceramic coatings for turbine blades, the technology migrates to hypersonic vehicles. These synergies aren't captured in financial statements but represent billions in value creation.

Managing Commercial/Defense Cycle Balance requires thinking like a portfolio manager, not an operating executive. Commercial aviation follows 7-10 year cycles driven by airline profitability, fuel prices, and global GDP growth. Defense spending cycles span 4-8 years, influenced by geopolitical events, election cycles, and budget politics. The cycles rarely align—when commercial aviation boomed in 2018-2019, defense budgets were flat. When COVID crushed commercial aerospace, defense spending surged.

RTX's roughly 50/50 commercial/defense split isn't arbitrary—it's optimized for cash flow stability. During commercial downturns, defense contracts provide steady cash flow to maintain R&D and employment. During defense budget cuts, commercial aftermarket sales generate high-margin cash. This balance allowed RTX to maintain its dividend through COVID while Boeing suspended theirs and smaller suppliers required bailouts.

The M&A Consolidation Playbook that created RTX offers lessons in industrial combination. Unlike tech acquisitions that often destroy value through culture clashes and talent exodus, industrial mergers can create lasting advantages through operational integration. The key: focus on capabilities, not just cost synergies. UTC's acquisition of Rockwell Collins wasn't about eliminating duplicate functions but combining avionics expertise with systems integration capabilities to compete with increasingly aggressive OEMs.

The merger timing—completing during COVID—seemed disastrous but proved inspired. Distressed valuations allowed aggressive cost-cutting that would face resistance in good times. The crisis provided cover for eliminating 48,000 positions and closing dozens of facilities. By the recovery, RTX had the cost structure of a company half its size with the capabilities of one twice as large.

Synergies in Complex Industrial Mergers extend beyond the typical procurement savings and headcount reductions. The real value lies in capability combinations that create new products and markets. RTX's ability to integrate Raytheon's radar technology with Collins' commercial avionics created dual-use products that neither could develop alone. Pratt & Whitney's engine expertise accelerated Raytheon's hypersonic propulsion development by years.

Supply chain leverage represents another hidden synergy. Semiconductor shortages that crippled competitors in 2021-2022 barely affected RTX—their combined purchasing power guaranteed allocation from chip manufacturers. Negotiations with titanium suppliers, specialty chemical providers, and rare earth element processors all shifted in RTX's favor post-merger.

Capital Allocation in Capital-Intensive Industries requires different thinking than asset-light businesses. RTX must balance maintenance capex (replacing worn equipment), growth capex (new production lines), R&D spending (future products), shareholder returns (dividends and buybacks), and balance sheet strength (credit ratings and liquidity). Get the balance wrong, and you either under-invest and lose competitiveness or over-invest and destroy returns.

RTX's capital allocation framework prioritizes in order: maintaining technology leadership (R&D spending), supporting existing programs (maintenance capex), funding contracted growth (growth capex), maintaining investment-grade credit ratings, and returning excess cash to shareholders. This hierarchy explains why RTX maintained R&D spending through COVID while cutting the dividend—technology leadership matters more than quarterly returns.

Managing Government Relations and Contracts requires understanding that in defense, the customer is also the regulator, the financier, and sometimes the competitor. The Pentagon doesn't just buy products; it funds development, dictates specifications, controls exports, and occasionally insources capabilities. Success requires balancing cooperation with independence, transparency with proprietary advantage.

RTX's approach emphasizes partnership over confrontation. While Lockheed Martin frequently battles the Pentagon over contract terms, RTX typically negotiates quietly, accepting lower margins for longer-term relationships. This strategy paid off during COVID when the Pentagon accelerated payments to RTX while other contractors faced delays.

The Importance of Aftermarket Services cannot be overstated in aerospace. While original equipment sales generate headlines, aftermarket services generate profits. A jet engine might sell for $15 million with a 15% margin, but generate $100 million in parts and service revenue over 30 years at 35% margins. RTX's installed base—tens of thousands of engines, millions of components—represents an annuity stream worth hundreds of billions.

The aftermarket model creates powerful competitive dynamics. Airlines can't switch engine providers without replacing entire fleets. Military customers require OEM support for decades-long programs. This lock-in effect means market share gained today generates profits for decades. RTX's focus on growing installed base, even at low initial margins, reflects this long-term value creation.

The playbook that emerges from RTX's formation and evolution challenges the conventional wisdom that focused pure-plays always outperform conglomerates. In industries with long development cycles, enormous capital requirements, and complex customer relationships, intelligent diversification can create value that focused competitors can't match. The key lies not in financial engineering but in operational excellence, technological leadership, and patient capital allocation that builds advantages over decades, not quarters.

XI. Bear vs. Bull Case & Future Outlook

The investment case for RTX splits Wall Street into two camps, each armed with compelling evidence. Bulls see a defense supercycle, commercial aerospace recovery, and unmatched technological advantages. Bears point to execution risks, geopolitical uncertainties, and structural challenges that could derail the growth story. The truth, as always, lies somewhere between the extremes.

The Bull Case starts with defense spending dynamics that haven't been this favorable since the Reagan buildup. Global defense spending exceeded $2.4 trillion in 2023, with NATO allies committing to sustained increases through 2030. The Ukraine conflict fundamentally changed European defense psychology—Germany alone increased defense spending by €100 billion. These aren't one-time purchases but multi-decade modernization programs that favor RTX's portfolio.

The backlog tells the story: $93 billion in defense orders, up from $78 billion a year ago, with international orders comprising 44% versus 35% historically. Raytheon's Patriot system has become the West's air defense standard, with orders from Poland, Germany, Switzerland, and others representing $40+ billion in future revenue. The Standard Missile family, AMRAAM upgrades, and classified programs provide additional growth vectors invisible to public markets.

Commercial aviation's recovery trajectory supports the bull case. Global passenger traffic reached 2019 levels in 2024 and continues growing at 5-7% annually. Airlines need 43,000 new aircraft over the next 20 years, split between growth and replacement. Every new aircraft needs engines, avionics, landing gear, and dozens of systems where RTX holds leading positions. The aftermarket opportunity is even larger—as fleets age, maintenance spending accelerates.

Technology leadership provides the moat. RTX's 52,000 patents, $7.5 billion annual R&D budget, and decades of expertise create barriers competitors can't quickly overcome. In hypersonics, directed energy, and AI-enabled systems, RTX's head start compounds annually. The integration of defense and commercial technologies—unique among major contractors—accelerates innovation in ways pure-play competitors can't match.

Financial flexibility enables aggressive capital deployment. With investment-grade ratings and $7+ billion in annual free cash flow by 2025, RTX can simultaneously invest in technology, expand capacity, and return cash to shareholders. The company targets $10 billion in share buybacks through 2025 while maintaining dividend growth—a combination few industrials can match.

Management quality under Chris Calio inspires confidence. Unlike predecessors who prioritized financial engineering, Calio brings operational expertise from running Pratt & Whitney through crisis and recovery. His focus on execution, customer relationships, and technology investment resonates with both customers and investors.

The Bear Case begins with the GTF engine crisis that's far from resolved. While RTX has managed the immediate financial impact, long-term consequences remain uncertain. Airlines remember the disruption, potentially affecting future engine competitions. The final bill could exceed $7 billion, and litigation risks remain as airlines seek compensation beyond current agreements.

Geopolitical risks cut both ways. While current tensions drive defense spending, they also threaten supply chains and international sales. China provides critical rare earth elements for defense electronics. Russia supplies titanium for aerospace. Export restrictions could limit RTX's addressable market, particularly in Middle East and Asia where human rights concerns affect arms sales.

Competition intensifies across all segments. In defense, new entrants like Anduril and Shield AI bring Silicon Valley innovation and Pentagon attention. Traditional competitors like Lockheed Martin and Northrop Grumman aggressively protect market share. In commercial aerospace, GE's new leadership targets RTX's engine position while Airbus pushes vertical integration that could squeeze suppliers.

Execution complexity threatens margins. RTX operates hundreds of facilities, manages thousands of suppliers, and coordinates among three massive business segments. Each integration failure, quality issue, or program delay costs billions. The company's complexity makes it vulnerable to black swan events—a single faulty component could ground fleets or compromise defense systems.

ESG pressures increasingly affect defense contractors. Institutional investors face pressure to divest defense holdings. European banks restrict financing for weapons manufacturers. Talented engineers, particularly younger ones, increasingly avoid defense work for ethical reasons. These trends could raise RTX's cost of capital and limit access to talent.

The government relations that enable RTX also constrain it. Defense contracts include onerous reporting requirements, profit limitations, and political interference. Cost-plus contracts limit upside while fixed-price development programs create massive downside risk. The Pentagon's monopsony power means RTX can't simply raise prices when costs increase.

Competition Dynamics reveal structural challenges. Boeing, despite its troubles, remains formidable in defense with $30+ billion in annual defense revenue. Lockheed Martin's F-35 program—the largest defense program in history—generates cash flows that fund aggressive R&D and pricing. General Electric's aerospace division, soon to be standalone, will focus entirely on competing with Pratt & Whitney.

International competition intensifies as well. European consortiums like MBDA challenge RTX in missiles. Chinese companies, backed by state resources, undercut Western suppliers in emerging markets. Russian systems, while sanctioned, remain attractive to price-sensitive buyers. The era of American defense industry dominance faces more challenges than any time since the 1950s.

Technology disruption represents both opportunity and threat. Quantum computing could render current encryption obsolete, requiring massive system upgrades. Autonomous systems might eliminate manned aircraft, destroying RTX's commercial engine market. Small satellites and distributed sensors could replace expensive radar systems. RTX must cannibalize its own products or watch others do it.

The Future of Warfare and Aerospace will be shaped by forces beyond RTX's control. Climate change drives sustainable aviation requirements that could obsolete current technologies. Demographic shifts in developed countries reduce military recruitment, accelerating automation. Economic nationalism threatens the global supply chains RTX depends upon. Each trend requires adaptation that large organizations struggle to achieve.

The bull-bear debate ultimately comes down to time horizons and risk tolerance. Near-term, RTX appears well-positioned with strong backlogs, improving operations, and favorable market dynamics. Long-term, structural challenges and technological disruption pose real threats. Investors must weigh whether RTX's advantages—scale, technology, portfolio balance—can overcome these challenges.

The most likely scenario splits the difference: RTX successfully navigates the next 5-10 years, generating strong returns from defense spending and commercial recovery. Beyond that, the company faces strategic choices about portfolio composition, technology investment, and market positioning that will determine whether it remains a industrial titan or becomes another former giant disrupted by change it couldn't anticipate or adapt to quickly enough.

XII. Epilogue: What Makes RTX Different

Standing in RTX's mission control center in Tucson, watching real-time feeds from missile tests, satellite reconnaissance, and cybersecurity operations, you understand what makes this company unique. It's not just the scale—though $80 billion in revenue certainly matters. It's not just the technology—though hypersonic missiles and quantum computers are impressive. What truly differentiates RTX is its position at the intersection of commercial and defense, physical and digital, American industrial might and global technological change.

The unique position as both commercial and defense leader creates advantages no competitor can replicate. When Lockheed Martin develops technology, it's trapped in the defense world by classification and export controls. When GE innovates in commercial aerospace, it lacks the defense contracts to fund basic research. RTX operates in both worlds, transferring technology, talent, and insights between them. A ceramic coating developed for fighter jet engines improves commercial fuel efficiency. A sensor designed for passenger aircraft enhances missile guidance. This cross-pollination accelerates innovation in ways that pure-play competitors simply cannot match.

The merger created something greater than the sum of its parts. United Technologies brought commercial expertise, global supply chains, and decades of airline relationships. Raytheon contributed defense technology, government relationships, and program management capabilities. Together, they formed an enterprise uniquely equipped for 21st-century aerospace and defense—where commercial technology increasingly drives military capability and defense innovation enables commercial advancement.

"Organic growth was broad based and led by strength in commercial aftermarket, which was up 21 percent year-over-year driven by continued demand for our industry leading products and solutions." This quote from CEO Chris Calio captures RTX's fundamental strength: diversified growth drivers that provide resilience regardless of market conditions. When commercial aviation struggled during COVID, defense carried the company. As defense budgets eventually moderate, commercial aerospace will provide growth. This balance isn't luck—it's strategy.

The leadership transition marks a new chapter. In December 2023, RTX announced that CEO Greg Hayes would step down the following May and be replaced by company president Christopher Calio. Unlike Hayes, who came from finance, Calio rose through operations, running Pratt & Whitney during both its GTF triumph and crisis. His appointment signals RTX's shift from financial engineering to operational excellence, from merger integration to organic growth, from portfolio assembly to technology leadership.

Calio inherits strengths and challenges in equal measure. The strengths are obvious: unmatched scale, technological leadership, balanced portfolio, strong cash generation. The challenges are equally clear: GTF remediation, supply chain constraints, talent competition, geopolitical uncertainty. How he navigates these dynamics will determine whether RTX fulfills its potential as the defining aerospace and defense company of the 21st century.

Lessons for Founders on Building Enduring Industrial Companies emerge from RTX's century-long evolution. First, technology moats in industrial companies differ from software—they require decades of accumulated expertise, billions in capital investment, and relationships that span generations. You can't disrupt Boeing or RTX with a better app; you need better metallurgy, aerodynamics, and systems integration.

Second, customer relationships in aerospace and defense transcend typical B2B dynamics. When Pratt & Whitney sells an engine to United Airlines, it's entering a 30-year relationship. When Raytheon delivers a Patriot system to Poland, it's committing to decades of support, upgrades, and partnership. These relationships, built over decades and tested through crises, create switching costs that no startup can overcome with features or pricing.

Third, portfolio construction matters more than individual business excellence. Harry Gray's UTC conglomerate failed because the pieces didn't reinforce each other—elevators and air conditioners had no synergy with jet engines. The RTX portfolio works because each element strengthens the others: commercial provides volume for suppliers that also serve defense; defense funds R&D that benefits commercial; both share technologies, talent, and infrastructure.

Fourth, timing matters enormously in industrial combinations. The RTX merger closed during COVID, allowing aggressive restructuring under crisis cover. The Rockwell Collins acquisition preceded the 737 MAX crisis, providing scale when Boeing became vulnerable. The Otis and Carrier spinoffs occurred at peak valuations, maximizing proceeds. Industrial strategy requires not just vision but patience to wait for the right moment.

Finally, culture in industrial companies must balance innovation with execution, risk-taking with reliability. RTX's culture blends Raytheon's military precision with UTC's commercial urgency, creating an organization that can both innovate and deliver. This cultural balance—harder to achieve than any technology—may be RTX's most sustainable advantage.

Final Thoughts on American Industrial Competitiveness place RTX in broader context. As America debates its industrial future, RTX represents both achievement and challenge. The achievement: building a company that leads in the most complex technologies humans create, from jet engines to hypersonic missiles to quantum computers. The challenge: maintaining that leadership as China invests hundreds of billions in aerospace, as Europe consolidates its defense industry, as new technologies disrupt traditional advantages.

RTX's success or failure matters beyond shareholders. In an era of great power competition, aerospace and defense capabilities determine national security. In a warming world, aviation technology affects climate outcomes. In a global economy, American industrial competitiveness shapes prosperity. RTX doesn't just build products—it builds the foundation of American power projection, global connectivity, and technological progress.

The story of RTX is far from over. The company stands at an inflection point where past success guarantees nothing about future performance. The technologies that defined the 20th century—jet engines, radar, missiles—are giving way to artificial intelligence, directed energy, and autonomous systems. The geopolitical stability that enabled global supply chains is fracturing. The business models that generated decades of profits face disruption.

Yet RTX's history suggests room for optimism. This is a company that transformed from radio tubes to radar, from propellers to jets, from analog to digital. Each transformation required writing off old capabilities, investing in uncertain technologies, and betting the company on unproven markets. Each time, the company not only survived but emerged stronger.

As we conclude this analysis, RTX embodies both the triumph and challenge of American industrial capitalism. The triumph: creating enterprises of staggering complexity that push the boundaries of human capability. The challenge: maintaining relevance as technological change accelerates, geopolitical tensions rise, and new competitors emerge. Whether RTX rises to these challenges will shape not just its own future but the future of American aerospace, defense, and ultimately, global security and prosperity.

The defense giant's second act has begun. The script remains unwritten. But with $218 billion in backlog, 185,000 employees, and technologies that span from the ocean floor to outer space, RTX has the resources to author its own future. The question isn't whether RTX will remain relevant—it's whether it will define what relevance means in the aerospace and defense industry of tomorrow.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube