Range Resources: The Marcellus Shale Pioneer

I. Introduction: The Unlikely Revolution Beneath Pennsylvania's Rolling Hills

In October 2004, on a crisp autumn day in Mount Pleasant Township, Pennsylvania—just 150 miles south of where Edwin Drake drilled America's first commercial oil well in 1859—a small team from Range Resources gathered around the Renz #1 well. The location was unremarkable: farmland in Washington County, about a mile and a half from where the McGugin Well had first discovered gas back in the 1880s. What happened next would fundamentally alter the global energy landscape.

"On a crisp October day, Range pumped a Barnett-style frac job into the Marcellus and changed the world's energy outlook." That single well—completed for approximately 300,000 cubic feet per day—proved something the industry had dismissed for decades: the Marcellus Shale, a 390-million-year-old rock formation buried thousands of feet beneath Appalachia, could produce commercial quantities of natural gas.

Today, Range Resources Corporation (NYSE: RRC) stands as a leading U.S. independent natural gas and NGL producer with operations focused in the Appalachian Basin, and the pioneer of the Marcellus Shale. At year-end 2024, the company's proved reserves totaled 18.1 Tcfe with positive performance revisions for the 17th consecutive year. Production averaged 2.18 Bcfe per day, approximately 68% natural gas.

The central question of this story is profound: How did a small Ohio oil and gas company, operating worn-out conventional wells and struggling for relevance in the early 2000s, become the catalyst for what many consider the most significant energy discovery of the 21st century?

The answer involves visionary geologists willing to challenge conventional wisdom, executives who bet millions on unproven ideas, a near-death experience with crushing debt, and a remarkable financial turnaround that restored the company to financial strength. This is not merely a corporate history—it is the origin story of American energy independence.

In 2004, the U.S. imported 652,015 mmcf of natural gas. Fast forward to 2023, that number was only 15,239 mmcf. In fact, last year, the U.S. exported more than 7,600 bcfe. Pennsylvania has grown to be the second largest gas-producing State, only behind Texas. If Pennsylvania was an independent country, it would now rank as the 5th largest gas producer behind the U.S, Russia, Iran, and China.

The Marcellus discovery didn't just transform Range Resources—it redefined America's role in global energy markets.

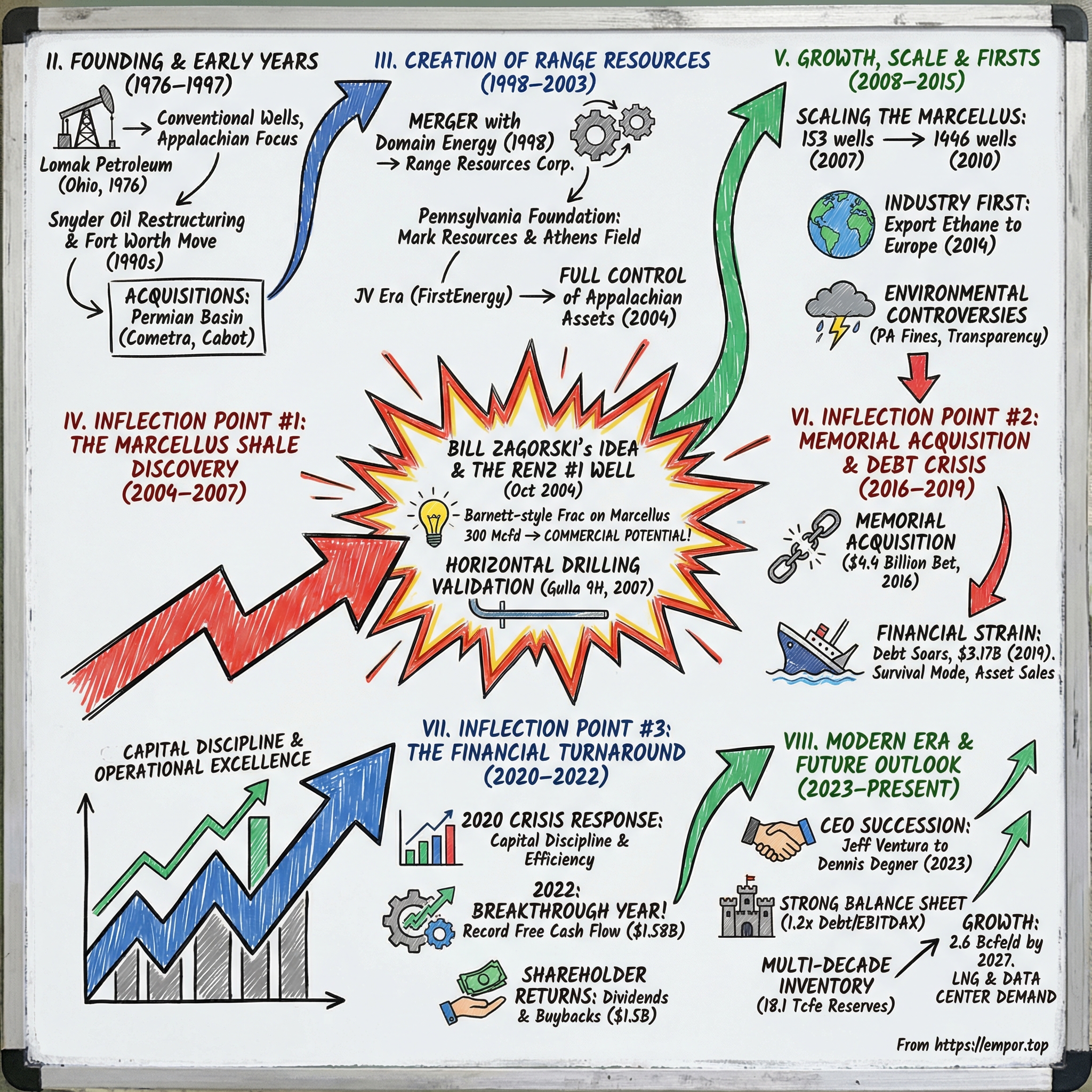

II. Founding & Early Origins: The Lomak Petroleum Era (1976–1997)

The Humble Beginnings in Ohio

In 1976, the company was founded as Lomak Petroleum, based in Hartville, Ohio. The company drilled wells in eastern Ohio. The founding circumstances were decidedly modest. It was founded and incorporated in the state of Ohio in 1976 by a group of investors led by C. Rand Michaels, who became the chief executive, and K.G. Hungerford, a certified public accountant who became secretary-treasurer of the corporation.

Courtland Rand Michaels brought an unusual background to the oil patch. He earned a Bachelor of Science from Auburn University in 1959 and a Master of Business Administration in Finance from the University of Denver in 1961. His career trajectory before founding Lomak was distinctly corporate: he worked in the marketing department at DuPont in Akron, Ohio from 1961 to 1970, then served as general manager at BASF from 1970 to 1972, and as vice president at Edge Industries from 1972 to 1976.

The early business model was straightforward but capital-efficient. Lomak, along with an affiliated partnership, acquired gas and oil-bearing properties in the Appalachian Basin and contracted outside companies to perform the actual drilling. In 1980, the company was reincorporated in Delaware and went public. The IPO netted approximately $3.4 million—a modest sum that nonetheless provided the capital needed for expansion.

In 1981, the company's first full year since its reorganization, Lomak generated almost $9 million in revenues and posted net income of $185,000. In that year the company also entered into a joint venture with a subsidiary of The Gillette Company, forming CLK Associates. Over the next two years Gillette would buy more Lomak stock, eventually owning as much as a 10.3 percent stake. This unusual partnership with a consumer products giant reflected the era's concerns about petroleum product access for manufacturing plastics and resins.

Revenues topped $17 million in both 1982 and 1983, and Lomak was profitable enough to think about expanding its activities beyond the Appalachian Basin to become a multi-regional company. It established subsidiaries in Michigan and Texas.

The Dark Days and Snyder Oil Transformation

The mid-1980s oil price collapse devastated small producers. In 1987, Lomak's stock was delisted from NASDAQ. The company's survival was in question.

In 1988, Snyder Oil Company gained control. Snyder Oil was founded by Harvard graduate John C. Snyder. Two of his executives would be assigned the task of restructuring Lomak. Michaels stepped down as chairman and CEO in favor of Thomas J. Edelman, who had served as Snyder's vice-chairman after earlier merging his company with Snyder Oil. Michaels now assumed the roles of president and COO.

Critically, also joining Lomak as a vice-president and director was John H. Pinkerton, who would eventually rise to the top of the company and continue to serve as president of Range Resources. Pinkerton earned an M.B.A. at the University of Texas, then worked with Arthur Andersen for four years before joining Snyder Oil in 1981.

As part of the Lomak restructuring, all of the directors resigned, except for Michaels, whose stake in the company was reduced from 25 percent to around 3 percent. Edelman and Pinkerton now called the shots. The new management team brought financial discipline and strategic focus that would prove crucial for the company's survival and eventual transformation.

Snyder Oil divested its Lomak holdings in 1995. The company was listed on the New York Stock Exchange in 1996. In 1992, the company moved its headquarters to Fort Worth, Texas.

Strategic Acquisitions Build the Foundation

With new management and improved financial standing, Lomak embarked on an acquisition strategy that would prove prescient. In 1997, the company acquired American Cometra for $385 million, which owned properties in the Permian Basin. It also acquired assets from Cabot Oil & Gas for $92.5 million.

These acquisitions expanded Lomak's geographic footprint beyond Appalachia into the prolific Permian Basin of West Texas. The diversification strategy seemed prudent—spreading risk across multiple basins while building production and reserves. Yet it would be the company's Pennsylvania roots that would ultimately define its future.

For investors analyzing Range's early history, the key takeaway is the importance of management transitions. The Snyder Oil restructuring brought professional management with capital markets experience—John Pinkerton and Thomas Edelman—who could navigate commodity cycles and position the company for transformative opportunities. The move to Fort Worth placed the company in the heart of the American oil patch, where it would learn about emerging shale technologies that would later revolutionize its Appalachian operations.

III. The Creation of Range Resources & Strategic Reorientation (1998–2003)

The Domain Energy Merger

In 1998, Lomak merged with Domain Energy to create Range Resources Corporation. Range Resources was created in 1998, the result of a merger between Lomak Petroleum Inc. and Domain Energy Corp. More than 70 percent of its reserves are natural gas, of which 83 percent are company-operated.

The deal was accomplished through a stock exchange, with Lomak serving as the acquiring corporation. Once the deal was completed in August 1998, Lomak changed its name to Range Resources Corporation, although it continued to operate out of its Fort Worth offices.

Domain Energy brought important attributes to the combination. Domain was very much focused on exploration, with approximately two-thirds of its properties located in the Gulf of Mexico and one-third in the Gulf Coast, as well as a 50 percent stake in a subsidiary operating in Argentina. Domain was only two years old, the result of a management buyout from Tenneco Inc. Its CEO, Michael V. Ronca, had worked for Tenneco for more than 20 years. He held a number of positions at Tenneco, then in 1992 founded an exploration and production and petroleum finance business unit called Tenneco Ventures Corp.

The merger gave Range Resources a diversified portfolio. Range Resources' primary development areas are the Appalachian Basin of eastern Ohio, western Pennsylvania, western New York, and West Virginia; the Permian Basin of west Texas; midcontinent properties of Oklahoma and the Texas Panhandle; and the Gulf Coast region.

Building the Pennsylvania Foundation

While the company was building its multi-basin portfolio, something quietly important was happening in Pennsylvania. "We drilled our first wells as an operator in Pennsylvania in 1992. We were fully involved in conventional drilling in the Appalachian basin long before the Marcellus ever came along," says Chuck Moyer, Ohio native and Director of Geology at Range.

In the 1990's, Range was operating in Pennsylvania under the banner of Lomak Petroleum. The company purchased what is known as the Athens Field in 1990, and the drill bit first hit in 1992, as part of a five-well package located in Crawford County. Less than a year later, the company made another Pennsylvania purchase, acquiring a Pittsburgh-based company called Mark Resources. That acquisition brought thousands of wells and valuable, drillable Pennsylvania acreage to the company. It also introduced the company to Pittsburgh native Bill Zagorski.

The Mark Resources acquisition would prove pivotal for reasons no one anticipated at the time. Bill Zagorski, who came with that deal, would become the key figure in one of the most important discoveries in American energy history.

The Joint Venture Era

In 1999, the company formed a 50-50 joint venture with FirstEnergy called Great Lakes Energy Partners LLC to own properties in the Appalachian Basin. In 2004, the company bought the 50% interest in the venture that it did not own for $290 million, including the assumption of debt.

This buyout of the FirstEnergy joint venture was significant. It gave Range full control of its Appalachian assets just as the Marcellus opportunity was emerging. The $290 million investment consolidated Range's position in the basin and provided the operational flexibility needed to pursue unconventional strategies.

In addition to already having a large legacy acreage position in the Appalachian Basin, Range had been leasing more land in southwestern Pennsylvania since 2000. Range now has approximately 875,000 net acres in the play, which includes a major position in what is considered the core liquids-rich portion of the Marcellus.

The strategic significance of this period cannot be overstated. While the industry was focused on conventional plays and offshore exploration, Range was quietly accumulating acreage in Pennsylvania at remarkably low costs. This early-mover advantage would generate extraordinary returns when the Marcellus boom began.

IV. INFLECTION POINT #1: The Marcellus Shale Discovery (2004–2007)

The Pre-Discovery Context

In the early 2000s, Range Resources was a modestly sized E&P company with a diversified but unremarkable portfolio. Before its major expansion into the Marcellus Shale, the company only held a small position in the Texas Barnett Shale and 9,000 "worn-out gas wells across the Appalachian basin that had been producing for 25 years".

The company was searching for growth, watching from afar as Mitchell Energy achieved breakthroughs in the Barnett Shale of North Texas. The Barnett was proving that tight shale formations, previously dismissed as source rocks rather than reservoirs, could produce commercial quantities of gas through a combination of horizontal drilling and hydraulic fracturing.

With one year under his belt as Chief Operating Officer of Range Resources (ticker: RRC), Ventura was approached by a company geologist named Bill Zagorski who had returned from a visit to Texas' Barnett shale, the birthplace of the shale revolution.

Bill Zagorski: "The Father of the Marcellus"

The year was 2003, and a little-known Range Resources geologist, Bill Zagorski, worked with the upstart producer trying to make vertical natural gas wells in southwestern Pennsylvania at depths of more than 8,000 ft, aiming for the Lower Devonian Oriskany Sandstone and the deeper Silurian Lockport Dolomite. The target formations had frustrated operators for decades.

"We already had a couple misses on here. We retired this well. They were literally ready to plug it, and then reclaim the location," said Zagorski, who, spoiler alert, is now known as the "Father of the Marcellus."

The pivotal moment came during a business trip. About that time, Zagorski traveled on business to Houston, where a geologist friend, Gary Kornegay, had a prospect he wanted Zagorski to look at in the Neal/Floyd shale in the Black Warrior basin in Alabama. "Part of the prospect pitch included a comparison of the Floyd as an analog to the Barnett shale," he said. At that time, Zagorski explained, he hardly knew what the Barnett shale was. Zagorski, whose career had focused strongly on studying the Appalachian basin, noted that characteristics of the Barnett seemed to parallel those of the Marcellus. "When he showed me all of the information on the Barnett shale," he said, "it was like, 'Oh my God.' We've got all this acreage, we've got it all right in our backyard in Washington County."

Doug Bowman, Senior Staff Geologist, had worked alongside Bill during the exploration process and remains one of the only Range employees left at the company who was on site for the Renz drilling. After a trip to Texas to visit a friend who was drilling in the Barnett Shale, which at the time was the largest natural gas field in the US, Bill came back inspired and determined. "What's that look like to you?" Bill asked Doug as he rolled out logs from the Barnett. "It looks like the Renz," Doug replied. "We need to do something with the Marcellus," Bill said.

But the proposition was risky. "Since the Renz at that point had turned out to be unsuccessful, Doug said it was a hard sell to go back and keep drilling. 'There was a common belief that the Marcellus wouldn't be successful, that it was too costly, and that the real gold was beneath it,' he said."

In 2003, geologist Bill Zagorski in Range Resources' Appalachia office had proposed a well, Renz 1, in Washington County, Pa., that had turned out to be a dry hole. Visiting with a fellow explorer in Houston in early 2004, Zagorski looked at the rock properties of the Barnett shale. It looked just like the Marcellus shale in Pennsylvania. He proposed to Range that Renz 1 be re-entered and completed in the Marcellus. "I was scared, you know," Zagorski said. "I'm the guy with the dry hole and I'm asking him for more money."

The Renz #1 Well: A Pivotal Gamble

At the meeting, Zagorski proposed to Ventura that the company go back into an unsuccessful exploration wellbore that had sucked up millions of the company's capital, thus far to no benefit. The bore, known as Renz #1, already had its surface area restored and was slated to be plugged and abandoned. Zagorski's idea was to go back into the well and specifically target the Marcellus shale layer using a hydraulically fractured well completion. "Bill presented the idea and he presented it very well," Ventura said when retelling the tale to the American Association of Petroleum Geologists as the organization's 2013 Halbouty lecturer. "The conventional wisdom was: don't test, it won't work, it's been tried before…"

Jeff Ventura made the call. After a lengthy discussion with the Range exploration team, Ventura approved Zagorski's idea and told the Range team to "put a big, Barnett style water frac on it."

On October 23, 2004, a large Barnett-style water frac consisting of 3,569,500 L (943,000 gal) of water and 167,800 kg (370,000 lb) of sand was used to treat a 27 m (90 ft) gross interval of the Marcellus organic shale in the Range Resources 1 Renz Unit. A flow test of approximately 0.400 mmcfepd was observed.

"On a crisp October day, Range pumped a Barnett-style frac job into the Marcellus and changed the world's energy outlook. The well had an initial rate of 300 mcfpd, sufficient enough to be comparable to a Barnett vertical well and providing enough results to continue the exploration of the Marcellus."

In early October 2004, high on a hill off Sabo Road, Range Resources Corp. successfully fracked a well on the Renz farm. Workers at Range extracted an estimated 300,000 cubic feet of natural gas that day. At the time, it was the largest fracking job executed east of the Mississippi River. The well site has been labeled, "The discovery well for the modern Marcellus Shale gas play."

"That single business decision resulted in the discovery of what would become the largest producing natural gas field in the U.S., estimated to be the second largest on the planet, behind only the South Pars gas field in the Persian Gulf. The Marcellus shale boom was officially born. 'Looking back, it was one of the best decisions of my life,' Ventura, now CEO of Range, said."

The Horizontal Drilling Validation (2007)

The vertical well was encouraging, but the real prize required horizontal drilling. "If you could make it vertical, you can make it a play. And if you could turn it horizontally, then you have a world class play," said Doug Bowman.

The early horizontal attempts produced mixed results. After drilling and fracturing two more vertical confirmation wells, Range began drilling horizontally in 2005. By early 2006, the team had drilled and completed its first horizontal test well. But the results were not as good as the vertical wells. The second horizontal test came up dry. "The third was twice as good as the first," said Zagorski, "but still not as good as we needed to establish commerciality."

Zagorski suggested a fourth horizontal be landed in the uppermost portion of the shale. In the meeting, he walked up with a chart. He noted that the deepest well, at about 40 feet above the bottom of the 100-foot Marcellus, made almost no gas, just 20 Mcf/d; the middle well, about 20 feet higher, came on with about 350 Mcf; the least-deep well, at about 30 feet from the top of the Marcellus, with about 600 Mcf. Ventura said, "I remember, when he put the graph up, everybody laughed and thought, 'Hey, that's hilarious, Bill.' Someone said, 'You know, if you had two points, you could get an even straighter line.'"

Despite the skepticism, they tried it. The team examined the first three horizontal wells and plotted the peak gas rate versus the height landed above the Onondaga. This led to the famous "3-point correlation," leading Range to shift their landing zone into a higher target within the Marcellus. With many trials and feeling that an economically viable well was on the horizon, the team finally drilled a successful horizontal well in the Marcellus in 2007, the Gulla 9H marking a massive leap in production and in turn, validating this generational discovery.

The drilling levels increased significantly in 2007, with 153 wells completed during that year. In 2007, the first significant horizontal completion was reported in Washington County, Pennsylvania, by Range Resources Corporation, with a reported initial potential (IP) of 3.9 mmcfepd.

By the close of 2007, Range had drilled 44 vertical and 15 horizontal wells in the Marcellus play and invested about $200 million. The Marcellus was real, although it took some in the industry another year to fully appreciate the black shale's potential.

Industry-Wide Impact

Two men who helped drive the company's approach were its president and chief executive officer, Jeffrey L. Ventura, and William A. Zagorski, Marcellus Shale Division vice president of geology. In fact, in 2009, the Pittsburgh Association of Petroleum Geologists honored Zagorski's key role by officially giving him the title "Father of the Marcellus."

"Range's pioneering of the Marcellus, now believed to be the largest natural gas field in the world, changed the global energy industry – forever."

The discovery's magnitude became clearer as academic estimates emerged. Terry Engelder at Penn State "sat down and did the calculation, and ended up saying, jeepers creepers, that's a lot of gas in there!" Engelder checked the estimate from the US Geological Survey. It was wildly different from his own number. Engelder didn't believe his own math: 50 trillion cubic feet of recoverable gas, 500 trillion cubic feet of total gas in the rock.

Zagorski projected the Marcellus as up to a 1 Tcf natural gas prospect. For context, in early 2008, Penn State University geoscientist Terry Engelder estimated the Marcellus' natural gas reserves as 50 Tcf. He later revised it way higher to 392 Tcf in late 2008, and then to as much as 489 Tcf in 2009. "There were times when we were looking at it and comparing the size of the Marcellus to the size of the Barnett and the Fayetteville [Shale], and we knew this thing was huge," Zagorski said. "But we didn't know it was going to be that big."

For investors, the Marcellus discovery illustrates the asymmetric returns possible from exploration when a company possesses both technical knowledge and local acreage. Range's early recognition and leasing strategy established it as a first-mover in the basin. The company's willingness to challenge conventional wisdom—and management's courage to back an unproven hypothesis—generated returns that would reshape the entire company.

V. Growth, Scale & Industry Firsts (2008–2015)

Scaling the Marcellus

With the Marcellus validated, Range moved aggressively to scale production. The company's early acreage position, acquired at less than $1,000 per acre on average, proved enormously valuable. In 2010, Forbes called the company "King of the Marcellus Shale". The company had spent less than $1,000 per acre on average to acquire land suitable for drilling, compared to larger traditional oil and gas players who joined the exploration rush late in the game who had paid as much as $14,000 an acre.

The price for leasing rose from $300 per acre in February to $2,100 in April, 2008. Only four Marcellus wells were drilled in Pennsylvania in 2005, but by 2010 1,446 Marcellus wells were drilled in Pennsylvania.

Leadership Transitions

Ventura joined Range in 2003 as COO after previously serving as president and COO at Matador Petroleum Co. He became Range's president effective May 2008 and CEO in January 2012.

In accordance with the plan, Range's President, Jeffrey L. Ventura, will assume the additional role of Chief Executive Officer beginning January 1, 2012. At such time, John H. Pinkerton, Range's current Chief Executive Officer, will assume the position of Executive Chairman. Mr. Pinkerton has served as Range's CEO since 1992.

The leadership transition reflected a deliberate succession plan. Pinkerton had led the company through the Snyder restructuring and the Domain merger; Ventura had made the pivotal decision to frac the Renz well and overseen the Marcellus development. Their partnership exemplified continuity amid growth.

Industry Firsts & Achievements

Range's operational achievements during this period were remarkable. The company set production records, extended horizontal lateral lengths, and pioneered new market access strategies.

"The company is currently selling ethane to INEOS, a Norwegian chemical firm, under a long-term contract. The first ethane and LPG shipments were loaded in March, making Range the first company in North America to export ethane to Europe."

"It's been a real global collaboration, and it brings such credibility and validity to Range. We'll be the first company to export ethane from the United States to Europe. Not one of 'the big guys.' It's Range. That's huge." President, Chairman and CEO of Range Resources Jeff Ventura credits a team of people, working together on an effort unlike any other.

"The United States started exporting ethane in 2014 via pipeline to petrochemical plants in Canada. In 2016, the United States began exporting ethane to countries in Europe from marine export terminals."

The Mariner East pipeline project, connecting Marcellus production to export facilities at Marcus Hook, Pennsylvania, represented a creative solution to the ethane glut that had depressed prices in the basin. Range's partnership with INEOS and Sunoco Logistics created new market access that improved realizations and demonstrated the global reach of Appalachian hydrocarbons.

Environmental Controversies

The rapid development of the Marcellus was not without controversy. This American Life and The New York Times investigated the company's operations in Amwell Township and Mount Pleasant Township, Washington County, Pennsylvania. Journalists Eliza Griswold and Sarah Koenig found allegations that gas wells owned by Range Resources caused water pollution and air pollution. Residents complained of black running water that corroded faucets and household machinery, showers smelling of "rotten eggs" (hydrogen sulfide) and diarrhea, "mysterious stomach pains", extreme fatigue or anemia.

The company paid $219,875 in fines to the Commonwealth of Pennsylvania as of May 2010. The bulk of these fines related to a fracking fluid spill that affected Brush Creek in Washington County.

In 2010, the company announced that it would list on its website the chemicals, including their volume, concentration and purpose, used in each well completed via hydraulic fracturing. Range became an early leader in transparency around fracking fluid composition, though controversies over water and air quality continued in subsequent years.

In 2020, Pennsylvania Attorney General Josh Shapiro said Friday that Range Resources has pleaded no contest to environmental crimes at two Washington County sites. The charges are the product of a two-year investigation from Shapiro's office into the fracking industry. The company will pay a fine of $150,000 for charges stemming from leaks and spills at the sites. At one of them, the Brownlee site, a storage tank leaked 2,000 gallons of fracking waste into a field and nearby creek in 2018. "Range Resources was careless — and carelessness in the fracking industry can have consequences that can last for decades," Shapiro said.

For investors, the environmental controversies represent ongoing operational and reputational risks. The industry-wide scrutiny of fracking practices has led to stricter regulations, higher compliance costs, and potential legal liabilities. Range's response—improved transparency, enhanced containment operations, and remediation investments—reflects the need to maintain its social license to operate.

VI. INFLECTION POINT #2: The Memorial Resource Acquisition & Debt Crisis (2016–2019)

The $4.4 Billion Bet

In May 2016, Range made its largest acquisition ever, one that would nearly destroy the company. Range Resources and Memorial Resource Development Corp. announced a definitive merger agreement under which Range will acquire all of the outstanding shares of common stock of MRD in an all-stock transaction valued at $4.4 billion. This valuation includes the assumption of MRD's net debt, which was $1.1 billion.

Range Resources (ticker: RRC), the legacy shale gas developer credited with discovering the Marcellus shale play, announced that it would acquire all of the outstanding shares of Memorial Resource Development Corp. The acquisition by Range of Memorial places the Terryville natural gas asset in northern Louisiana into Range's portfolio.

The strategic rationale seemed sound. Jeff Ventura, Range's chief executive, summed up the transaction as combining "two high-quality unconventional producers with large de-risked, high-return projects into one portfolio."

The acquisition of Memorial gives Range the long-lived northern Louisiana assets of Memorial—Terryville—an area that has been producing since 1954.

The Deal Structure

Under the definitive agreement, MRD shareholders will receive 0.375 shares of Range common stock for each share of MRD common stock held. Based on the Range closing price on May 13, 2016, the transaction has an implied value to MRD shareholders of $15.75 per share, representing a 17% premium to the closing price of MRD stock. Following the transaction, shareholders of MRD are expected to own approximately 31% of the outstanding shares of Range.

The completion of the merger agreement was announced in September 2016, in an all-stock transaction valued at approximately $4.2 billion, including the assumption of MRD's net debt. The transaction, which was approved by Range and Memorial shareholders at special meetings held on September 15, 2016, enhances Range's position as a premier independent natural gas, oil and NGL producer in the United States with exceptional core acreage positions in both the Appalachian Basin and Northern Louisiana.

The Debt Burden Emerges

The timing could not have been worse. Natural gas prices remained depressed through 2017-2019, and the Memorial assets—while high-quality—required substantial capital investment. Range's leverage soared.

Range Resources started the new decade off with some notable moves in an attempt to shore up their heavily indebted financial position. Suspending their dividend is sensible since it was completely debt funded, however, its absence barely moves the needle. Perhaps their further capital expenditure reductions will prove fruitful, however, given the capital intensive nature of their industry, this may only provide a short-term boost to their free cash flow. Refinancing debt with higher interest rates is only providing a short-term fix to their long-term problem.

After reviewing these ratios, it is easily apparent that their financial position is very weak, with all of the most recent results from the first nine months of 2019 indicating severe financial strain. Even though all of these metrics, barring net debt to operating cash flow and current ratio, have improved since the end of 2018, they would still need to improve significantly for their financial position to be considered strong. Their very low interest coverage of only 1.77 is especially concerning as their refinanced debt carries significantly higher interest rates of 9.25% versus the between 5.00% and 5.875% for the previous debt.

Although they have come very close during 2018 and the first nine months of 2019, they have never produced any positive free cash flow during the last seven years, which includes two years before the oil and gas price crash of 2015-2016. Since the beginning of 2013, their free cash flow has totaled negative $2.109b, despite their capital expenditure trending lower.

Financial Strain

As of December 31, 2019, Range Resources had a total of $3.172987 billion in total debt compared to $3.836861 billion at the same time last year. This gives the company a debt-to-equity ratio of 1.35.

The company sold a total of $785 million in assets over the course of 2019 and used the proceeds to reduce its debt. Range Resources reported a net loss of $1.805320 billion in the fourth quarter of 2019.

The company was in survival mode. Management suspended dividends, slashed capital expenditures, and sold non-core assets. The question was whether Range could generate sufficient cash flow to service its debt and avoid bankruptcy.

The Memorial acquisition stands as a cautionary tale about leverage and timing. The strategic logic—diversification, scale, cost synergies—was reasonable. But taking on $1.1 billion of additional debt at the bottom of a commodity cycle, funded by equity that would subsequently decline, created an existential threat to a company that had pioneered one of the most important energy discoveries in American history.

VII. INFLECTION POINT #3: The Financial Turnaround (2020–2022)

The 2020 Crisis Response

The COVID-19 pandemic and oil price collapse of March 2020 seemed to seal Range's fate. Natural gas prices plummeted alongside oil, and energy credit markets froze. Yet the crisis forced the discipline that would ultimately save the company.

Reducing their capital expenditure for 2020 by 29% below their estimated 2019 levels may finally result in free cash flow turning positive. The move to suspend their dividend payments is undoubtedly wise, however, considering these only cost a total of $15m for the first nine months of 2019, it does not really move the needle all that much.

The company executed on its deleveraging plan with remarkable focus. Range reduced outstanding debt while maintaining production levels through operational efficiencies. The $785 million in asset sales during 2019 had provided breathing room, and management continued to prioritize balance sheet repair.

Capital Discipline & Operational Excellence

The pivot from growth to capital discipline represented a fundamental shift in corporate strategy. Jeff Ventura, the Company's CEO said, "During 2021, Range generated significant free cash flow, reduced debt, refinanced near-term maturities, lowered well costs, expanded cash margins and delivered our operational plan safely and for less than budgeted. These results reflect the organization's continuing focus on capital discipline and further strengthening our financial position as we develop the most prolific natural gas and NGL play in North America."

"In 2022, we expect to build upon these achievements, generating over $1 billion of free cash flow at recent strip pricing. Range's improved financial positioning supports our plan to reinstate our dividend program with a yield that is competitive with the broader market, in addition to authorizing a share repurchase program."

The reinstatement of dividends and authorization of a $500 million share repurchase program in early 2022 signaled management's confidence in the turnaround.

2022: The Breakthrough Year

Range's sales of natural gas, NGL and oil totaled $4.91 billion in 2022, up from $3.22 billion in 2021. The company's 2022 net income was $1.18 billion, up 187% year over year from $411.78 million in 2021.

Full-Year 2022 Highlights – Generated record cash flow from operations of $1.9 billion. Jeff Ventura, the Company's CEO said, "The Company successfully managed a great market opportunity in 2022 – generating record free cash flow, materially strengthening our financial foundation and returning significant capital to shareholders. We reduced debt by over $1 billion and expanded our return of capital program with $400 million in share repurchases and an annualized dividend of $0.32 per share. As we enter 2023, the progress made during the past year both financially and operationally puts Range in the strongest position in Company history."

Jeff Ventura said, "Range delivered record free cash flow and cash flow per share in the third quarter, allowing us to reduce net debt while increasing returns of capital to shareholders. Range has unlocked a massive inventory of high-quality wells in the Marcellus, measured in decades, and translated that inventory into a business capable of generating healthy free cash flow and returns of capital through the cycles. As a result of Range's organic operational and financial performance, commitment to disciplined spending and confidence in free cash flow sustainability, we are tripling our share repurchase authorization to $1.5 billion."

The company reported free cash flow of $656 million in 2021, $1,580 million in 2022, $513 million in 2023, and $453 million in 2024.

The turnaround was complete. From near-bankruptcy to generating $1.58 billion in free cash flow in a single year, Range had executed one of the most impressive financial recoveries in the E&P sector.

VIII. The Modern Era: Leadership Transition & Future Outlook (2023–Present)

CEO Succession

Range announced that, after almost 20 years of service which included the discovery and development of the Marcellus Shale field, Jeff Ventura plans to retire from the Company effective June 2, 2023 and will not seek reelection to the Board. Range's Board of Directors has selected Dennis Degner, the Company's Executive Vice President and Chief Operating Officer to assume the role of President and Chief Executive Officer effective at the Company's annual shareholder meeting May 10, 2023.

"I have had the pleasure of working with and serving alongside Jeff for the last seven years. Jeff provided steady leadership and a consistent vision during an extremely challenging chapter for our whole industry," said Chairman Greg Maxwell. "Jeff will leave Range with the strongest balance sheet in company history, record free cash flow, and a business that is well-positioned to generate shareholder returns."

Dennis L. Degner, Chief Executive Officer and President joined Range in 2010. Mr. Degner was named Chief Executive Officer effective May 10, 2023. Mr. Degner previously served as the Company's Chief Operating Officer and has more than 20 years of oil and gas experience having worked in a variety of technical and managerial positions across the United States including Texas, Louisiana, Wyoming, Colorado and Pennsylvania. Prior to joining Range, Mr. Degner held positions with EnCana, Sierra Engineering and Halliburton.

2024-2025 Financial Performance

In 2024, Range reduced net debt by $172 million, returned $77 million in dividends, and invested $65 million in share repurchases. Production averaged 2.18 Bcfe per day, approximately 68% natural gas. Proved reserves of 18.1 Tcfe with positive performance revisions for 17th consecutive year. Debt to EBITDAX of 1.2x at year-end 2024.

In 2025, Range anticipates a capital budget of $650 to $690 million, aiming for annual production of approximately 2.2 billion cubic feet equivalent per day, while focusing on building in-process well inventory for future growth.

In 2024, Range Resources's revenue was $2.36 billion, a decrease of -7.57% compared to the previous year's $2.55 billion. Earnings were $265.04 million, a decrease of -69.04%.

"Operational excellence and environmental responsibility go hand in hand - delivering sustainable performance today, and long-term value well into the future," said Dennis Degner, the Company's CEO. Range achieved Net Zero Scope 1 and 2 GHG emissions through direct emissions reductions and verified carbon offsets for 2024 emissions, ahead of its 2025 goal.

Three-Year Growth Outlook

Range plans to significantly increase daily production to 2.6 Bcfe by 2027, leveraging its low-cost, low-emission Marcellus assets to meet the anticipated global gas demand. Range Resources aims for a daily production level of 2.6 Bcfe by 2027, signaling a growth of 400 Mmcfe per day from 2024.

The company projects production growth of approximately 20% through 2027 while generating approximately $2.5 billion in cumulative free cash flow during the same period.

IX. Competitive Landscape & Industry Analysis

The Appalachian Basin Competitive Environment

Range operates in an increasingly competitive Appalachian Basin. Understanding the competitive environment for Range Resources involves analyzing its position against other Appalachian Basin oil and gas companies. Key players in the Pennsylvania natural gas market, such as EQT Corporation and Southwestern Energy, are often considered direct competitors. The impact of commodity prices on Range Resources competition is a critical factor, influencing market share trends compared to peers.

Appalachian natural gas competes with Haynesville dry gas and Permian Basin associated gas, so in a sense, Range Resources competes with a large number of producers, especially from the Permian. However, specifically within the Marcellus field, Range Resources' competitors include Antero Resources (AR), Cabot Oil and Gas (COG), Chesapeake (CHK), Consolidated (CNX), EQT Corporation (EQT), Exxon Mobil (XOM), and Southwestern Energy (SWN).

EQT, one of the largest U.S. natural gas producers, benefited most directly from its scale, operational leverage, and exposure to expected long-term LNG export growth. Range Resources' performance over the period was supported by a relatively low-cost structure and continued progress in debt reduction. Antero's period price gain reflected balanced fundamentals but also the absence of meaningful hedge coverage, leaving it more exposed to spot market volatility. Coterra's flat performance aligned with its greater oil exposure.

Porter's Five Forces Analysis

Threat of New Entrants: LOW The Marcellus Shale is a mature basin with most quality acreage already leased. New entrants face significant capital requirements, need for technical expertise in shale drilling, and limited available acreage. Range's first-mover advantage and accumulated operational knowledge create barriers.

Bargaining Power of Suppliers: MODERATE Oilfield service companies and equipment providers have pricing power in tight markets, but the industry's consolidation has also increased E&P company bargaining power. Pipeline access remains a critical constraint in Appalachia.

Bargaining Power of Buyers: HIGH Natural gas is a commodity with pricing determined by liquid markets. Producers are price-takers. However, Range's NGL production and access to export markets provides some differentiation and premium pricing opportunities.

Threat of Substitutes: MODERATE-HIGH Renewable energy, electrification, and energy efficiency represent long-term substitution threats. However, natural gas benefits from its role in power generation reliability and industrial applications. The AI/data center buildout is creating new demand.

Competitive Rivalry: HIGH The Appalachian Basin features multiple large, well-capitalized competitors. EQT has scale advantages; Antero competes in the liquids-rich window; Coterra offers oil exposure. Consolidation pressure continues.

Hamilton Helmer's 7 Powers Framework

Process Power: Range possesses accumulated operational expertise from pioneering the Marcellus. Its understanding of optimal landing zones, completion designs, and production optimization creates sustainable cost advantages. However, this knowledge has diffused to competitors over two decades.

Scale Economies: EQT has greater scale, but Range operates efficiently at its current size. The capital intensity of shale development creates some scale benefits in drilling and completions.

Counter-Positioning: Range's pure-play Appalachian focus versus diversified competitors represents a form of counter-positioning. Competitors with multi-basin exposure may underweight Marcellus investments.

Network Effects: Limited in commodity production. Pipeline access and gathering infrastructure create some network-like dynamics but are shared across the basin.

Switching Costs: Minimal at the product level (natural gas is fungible), but contractual commitments with midstream providers and customers create some operational stickiness.

Branding: Not applicable in commodity production.

Cornered Resource: Range's 18.1 Tcfe of proved reserves and extensive Marcellus acreage represent a valuable resource position. The multi-decade drilling inventory provides visibility and optionality.

X. Investment Considerations: Bull Case, Bear Case & Key Metrics

Bull Case

Multi-Decade Inventory: In addition to proved reserves, Range has approximately 25 million lateral feet of undeveloped high-quality Marcellus inventory, which is supported by continued strong performance of existing production. This provides decades of high-quality drilling opportunities at low breakeven costs.

Low-Cost Structure: Range operates one of the lowest-cost gas production portfolios in North America. Maintenance capital has declined to approximately $530 million annually, enabling substantial free cash flow generation even at moderate gas prices.

Balance Sheet Strength: Debt to EBITDAX of 1.2x at year-end 2024 represents a dramatic improvement from the 2019 crisis. The company has flexibility for shareholder returns and opportunistic investments.

Growing Demand Drivers: The company projects significant natural gas demand growth through 2030, driven primarily by LNG exports, industrial demand, and power generation needs, particularly from data centers. Specifically in the Appalachian region, Range expects demand to grow by approximately 5-8 Bcf/d through 2030, supported by data centers.

Shareholder Returns: Management has committed to returning substantial free cash flow through dividends and buybacks. This capital efficiency is intended to support increased shareholder returns through dividends and share repurchases. In Q2 2025, Range repurchased $53 million in shares and paid $21 million in dividends.

Bear Case

Commodity Price Exposure: Natural gas prices remain volatile and subject to weather, storage levels, LNG export dynamics, and associated gas production from oil-focused basins. Range lacks the oil exposure that provides diversification for some competitors.

Takeaway Constraints: Appalachian production growth depends on pipeline infrastructure that faces permitting challenges and environmental opposition. Basis differentials can widen significantly when takeaway capacity is constrained.

Competitive Intensity: EQT's larger scale and Antero's competing liquids-rich position create competitive pressure. An activist investor is urging EQT Corp. to take a bold step and commence merger discussions with Antero Resources or Range Resources Corp. for "much needed, large-scale consolidation in the Appalachian Basin." The bold suggestion, should it ever come to fruition, could potentially reshape control of gas production in the eastern U.S.

Regulatory/ESG Risks: The fracking industry faces ongoing scrutiny from regulators and environmental groups. Pennsylvania's political environment may shift against the industry, potentially raising costs or restricting activity.

Execution Risk: The planned 20% production growth through 2027 requires disciplined execution, securing additional transportation capacity, and supportive commodity prices.

Key Metrics to Monitor

For investors tracking Range Resources, three metrics stand out as critical indicators of ongoing performance:

-

Free Cash Flow Per Share: This metric captures the company's ability to convert production into distributable cash after maintenance capital. It reflects operational efficiency, commodity prices, and capital discipline. Historical range: $(3) to $6+ per share depending on commodity environment.

-

Net Debt / EBITDAX: The leverage ratio demonstrates balance sheet health and capacity for shareholder returns or growth investment. Target range: 1.0x-1.5x under normalized conditions.

-

All-In Unit Costs ($/Mcfe): Combining direct operating expense, transportation/gathering, production taxes, G&A, and interest captures the full cost structure relative to peers. Range's competitive position depends on maintaining industry-leading unit economics.

XI. Conclusion: What Range Resources Teaches About American Energy

Range Resources' journey from a small Ohio oil and gas company to the pioneer of the Marcellus Shale offers enduring lessons about entrepreneurial risk-taking, the importance of local knowledge, and the perils of leverage.

Bill Zagorski's courage to propose drilling into a formation that "conventional wisdom" said would never work, and Jeff Ventura's willingness to approve the experiment, created hundreds of billions of dollars in value—not just for Range shareholders, but for the American economy. For the past decade the Marcellus has boosted the country's essential natural gas supplies and fueled low-carbon electricity and heat for U.S. families and businesses, led to the creation and/or support of more than 240,000 jobs in Pennsylvania alone, and delivered the foundation required to revive U.S. manufacturing—cheap, reliable energy.

Yet the Memorial acquisition nearly destroyed what the Marcellus discovery had built. The lesson is timeless: leverage can amplify returns in good times but threatens survival in bad times. Range's near-death experience and subsequent turnaround demonstrate both the fragility and resilience of well-managed companies.

Today, Range Resources stands at an interesting inflection point. Under new leadership, with a fortress balance sheet and decades of drilling inventory, the company is positioned to benefit from structural demand growth in natural gas—from LNG exports, data center proliferation, and power generation needs. The question is whether commodity prices and regulatory conditions will cooperate.

"We were—all this time—searching for [pockets of] nickels and dimes and we're sitting here with $100 bills," Zagorski reflected. "It's just amazing. Not just here; that's in the whole U.S. oil and gas industry."

That observation captures Range's enduring significance. The company didn't just discover a gas field—it helped unlock a revolution that reshaped global energy markets, restored American energy independence, and created a template for unconventional resource development worldwide. From 9,000 worn-out wells in Appalachia to one of the world's largest natural gas producers, Range Resources' story is, at its core, the story of American innovation in the energy sector.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube