RPM International: The Story of an American Specialty Coatings Empire

I. Introduction & Episode Roadmap

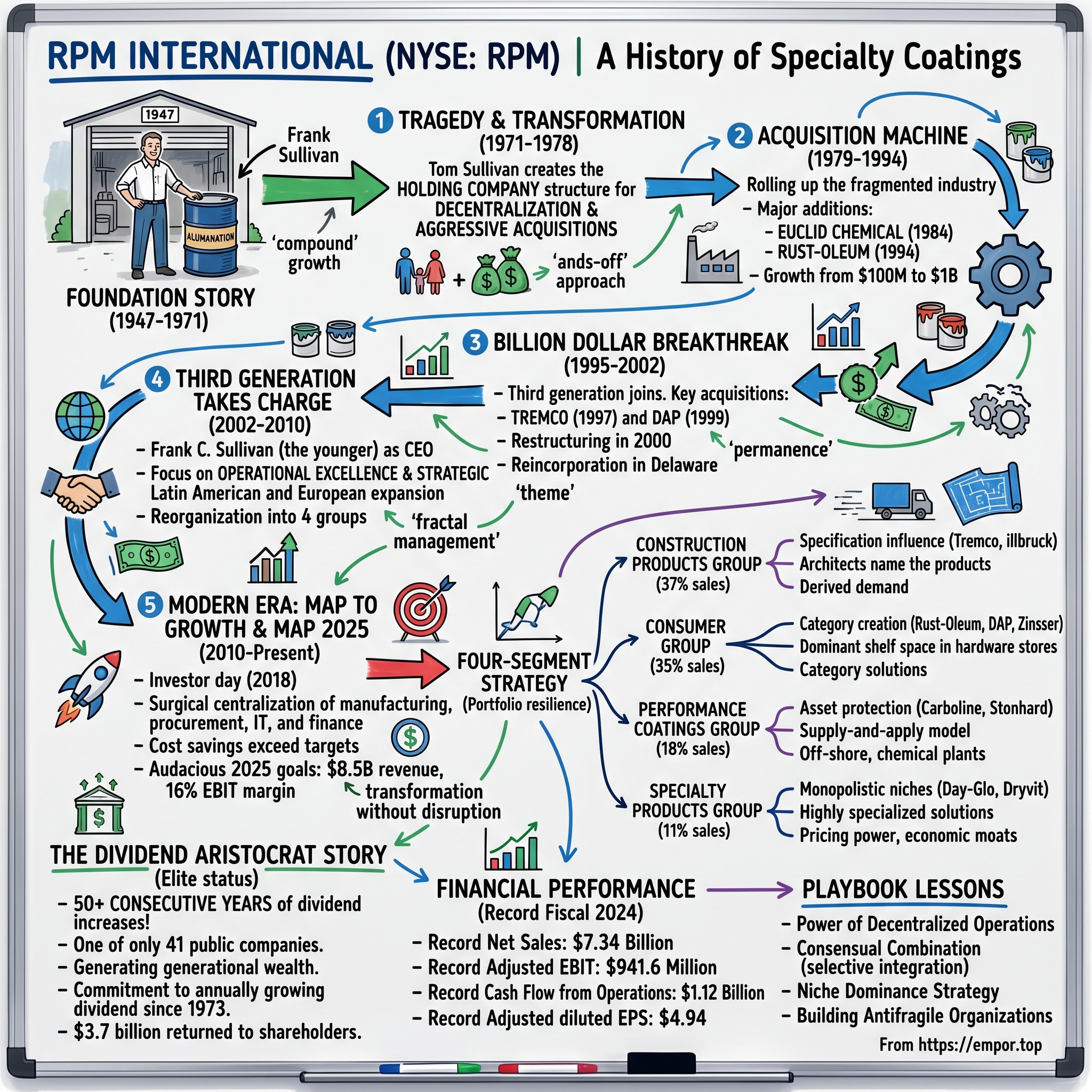

Picture this: It's 1947 in post-war Ohio. While America's industrial giants are scaling steel production and automobile manufacturing, a scrappy entrepreneur named Frank Sullivan is mixing aluminum powder with asphalt in a garage, convinced he's found a better way to protect factory roofs from the elements. That humble aluminum coating—branded "Alumanation"—would become the foundation stone of what is today RPM International, a $7.3 billion specialty chemicals empire that owns brands you've probably used without knowing it: Rust-Oleum, DAP, Zinsser, and dozens more.

This is the improbable story of how a small Ohio roof coating company transformed into the world's fifth-largest paint and coatings manufacturer through one of the most disciplined acquisition strategies in American business history. RPM International (NYSE: RPM) now operates 121 manufacturing facilities worldwide, employs 17,300 people, and has increased its dividend for 50 consecutive years—a feat achieved by only 41 other public companies in history.

What makes RPM fascinating isn't just its scale—it's the paradox at its core. While conglomerates from GE to ITT rose and spectacularly fell trying to manage diverse businesses from the center, RPM built an empire by doing the opposite: radical decentralization. They perfected the art of buying entrepreneurial companies and then leaving them alone. No synergy initiatives. No forced consolidation. No centralized purchasing. Just capital, patience, and trust.

The themes we'll explore cut against conventional wisdom: How a three-generation family dynasty maintained control while growing a public company 600-fold. Why boring products like roof coatings and garage floor paint create better businesses than sexy tech. How operational discipline can coexist with entrepreneurial chaos. And perhaps most intriguingly, how a company can roll up an entire industry while preserving the very independence that made each acquisition valuable in the first place.

This isn't just a business story—it's a masterclass in patient capital allocation, a case study in family succession done right, and a blueprint for building wealth through compound growth in unglamorous markets. From Frank Sullivan's $90,000 in first-year sales to today's global specialty chemicals conglomerate, RPM's journey offers lessons that challenge everything we think we know about corporate growth, operational excellence, and long-term value creation.

II. The Frank Sullivan Foundation Story (1947–1971)

The post-war morning of May 1947 in Medina, Ohio was thick with possibility. While Detroit's assembly lines churned out chrome-laden dreams and Pittsburgh's mills forged the skeleton of America's new prosperity, Frank C. Sullivan stood in a converted garage mixing aluminum powder into an asphalt base, convinced he could revolutionize how America protected its rooftops. The concoction—which he branded "Alumanation"—would seem an unlikely foundation for a multi-billion dollar empire. Yet Frank C. Sullivan founded Republic Powdered Metals, the forerunner to RPM International Inc. that month, launching what would become one of American industry's most enduring success stories.

The timing was exquisite. America's industrial infrastructure, pushed to its limits during wartime production, desperately needed protection from the elements. Factory roofs across the Midwest were leaking, corroding, failing. Sullivan's aluminum coating offered something revolutionary: a reflective barrier that could extend roof life by decades while reducing interior temperatures. Sales in the first year reached $90,000—modest by today's standards but enough to validate Sullivan's intuition that specialty coatings could be more than commodities.

What distinguished Sullivan from the countless other post-war entrepreneurs wasn't just his product—it was his philosophy. He believed in what he called "The Value of 168," representing the hours in a week. The figure "168" represents the number of hours in a week and serves as a reminder that each of us has a limited amount of time—and a duty to use this gift wisely and productively. This wasn't corporate platitude; it was operational doctrine. Sullivan worked those hours with methodical intensity, personally driving samples to customers, adjusting formulations based on field feedback, building relationships one handshake at a time.

The 1950s saw Republic Powdered Metals evolve from garage startup to regional player. Sullivan assembled a team of chemists and salesmen who shared his obsession with solving unglamorous problems—waterproofing, corrosion prevention, substrate adhesion. These weren't sexy challenges, but they were expensive ones for industrial America. Each solution commanded premium pricing and customer loyalty that commodity paint manufacturers couldn't match.

By the early 1960s, Sullivan faced a crossroads. The company had grown beyond his ability to self-finance expansion, yet he was reluctant to cede control to Wall Street bankers who might not understand the patient, relationship-driven nature of the specialty chemicals business. His solution was characteristically bold yet conservative: After more than 15 years of private ownership, Republic Powdered Metals sold 25,000 shares of common stock to the public in an intrastate offering in Ohio in 1963. The shares sold out in 48 hours and paved the way for a national public stock offering a few years later.

The 48-hour sellout wasn't just vindication of Sullivan's business model—it revealed something profound about investor appetite for boring, profitable, industrial companies. While the go-go 1960s celebrated conglomerates and tech pioneers, Ohio investors recognized the value in a company that made products nobody thought about but everybody needed.

International expansion came next, driven by Sullivan's recognition that American manufacturing methods were being adopted globally. The company received the prestigious "E" Award in 1964 at a personal White House presentation from U.S. President Johnson for its outstanding contributions to the country's export expansion program. Standing in the White House, receiving recognition from President Johnson himself, Sullivan must have reflected on the improbability of the journey—from mixing chemicals in a garage to exemplifying American industrial excellence on the global stage.

The company's first acquisition came in 1966, a pivotal moment that would define RPM's future strategy. Republic Powdered Metals completed its first acquisition in 1966 with the purchase of The Reardon Company of St. Louis for $2.3 million. This wasn't just a purchase—it was a template. Sullivan recognized that the specialty coatings industry was fragmented, filled with family-owned businesses possessing deep technical expertise but lacking capital and distribution. By acquiring and preserving these enterprises' entrepreneurial culture, he could build something far greater than the sum of its parts.

As the 1960s drew to a close, Frank Sullivan had transformed Republic Powdered Metals from a one-product company into a diversified specialty chemicals manufacturer with international reach. Yet he understood that sustainable success required more than business acumen—it needed institutional permanence. He began grooming his son Thomas, involving him in strategic decisions, teaching him not just the chemistry of coatings but the chemistry of relationships that made the business work.

The tragedy that would catalyze RPM's transformation into a true conglomerate came suddenly. In August 1971, Frank Sullivan died suddenly. At 58, at the height of his powers, the founder was gone. Republic Powdered Metals faced the existential crisis that destroys most founder-led companies. What happened next would determine whether Frank Sullivan had built a company or merely a personal enterprise. The answer would reshape American specialty chemicals for the next half-century.

III. The Tragedy & Transformation: Tom Sullivan Era Begins (1971–1978)

The morning after Frank Sullivan's sudden death in August 1971, Thomas C. Sullivan faced a boardroom filled with worried faces. Suppliers wondered if payment terms would change. Customers questioned whether quality standards would slip. Investors speculated about a sale. The 34-year-old Tom Sullivan, who had been president of Republic Powdered Metals, understood the moment's gravity. According to Tom, the elder Sullivan had been "the individual most closely identified with [RPM]". The company didn't just need new leadership—it needed transformation to survive its founder's absence.

Tom's first masterstroke wasn't operational but structural. Later that same year, RPM, Inc. was formed to become a holding company to develop a more aggressive acquisition program in a rapidly consolidating paint and coatings industry. This wasn't merely corporate reorganization—it was philosophical revolution. Where Frank had built a company, Tom would build a platform. Thomas C. Sullivan, who was previously president of Republic Powdered Metals, became chairman and chief executive officer of the holding company.

The holding company structure revealed Tom's sophisticated understanding of what made specialty chemical companies valuable: their entrepreneurial leadership and customer relationships. Traditional conglomerates of the era—ITT, Gulf+Western, Textron—practiced aggressive centralization, stripping acquired companies of autonomy in pursuit of "synergies." Tom Sullivan looked at this playbook and did the opposite.

To fend off such speculation RPM, Inc. was incorporated as a holding company under which Republic Powdered Metals, Bondex, and any new acquisitions would operate as wholly owned subsidiaries with a large degree of independence in their daily operations. That "hands-off" approach became a model for all RPM's acquisitions and a strategy envied by other large corporations.

The decentralization wasn't abdication—it was calculated empowerment. Each subsidiary retained its own president, sales force, and R&D team. They controlled pricing, product development, and customer relationships. RPM provided capital, back-office support, and most importantly, patience. While Wall Street pushed quarterly earnings, RPM subsidiaries could think in decades.

Going public brought new pressures and possibilities. RPM was listed on the NASDAQ stock exchange in 1971, trading under the symbol RPOW. The timing seemed inauspicious—the early 1970s brought oil shocks, stagflation, and industrial malaise. Yet Tom Sullivan saw opportunity in chaos. Smaller competitors, lacking access to capital, struggled with volatile raw material costs. Family-owned businesses faced estate tax pressures. The consolidation Frank had anticipated was accelerating.

Tom's leadership style contrasted sharply with his father's. Where Frank was hands-on, Tom was strategic. Where Frank knew every customer personally, Tom built systems. The younger Sullivan understood that RPM couldn't grow through one man's relationships—it needed institutional capabilities. He began recruiting talent from larger chemical companies, offering them something unique: entrepreneurial freedom within a public company framework.

James A. Karman, who was elected president and chief operating officer in 1978, became Tom's critical partner. The two met at Miami (of Ohio) University and worked together for 16 years before the formation of the holding company. Their partnership embodied RPM's dual nature: Sullivan focused on acquisitions and capital allocation while Karman managed operations and integration. This division of labor would become the template for RPM's next three decades of growth.

The 1970s tested the new structure immediately. The 1973 oil embargo quadrupled the price of petroleum-based raw materials. The 1974-75 recession hammered industrial production. Inflation reached double digits. Lesser companies might have retreated, but Tom Sullivan saw disruption as opportunity. While competitors cut R&D spending, RPM increased it. While others delayed acquisitions, RPM accelerated them.

The acquisition philosophy that emerged during this period was distinctive. RPM didn't buy distressed assets to strip and flip. They bought profitable niche leaders and made them more profitable through patient capital and shared expertise. Each acquisition was evaluated not on immediate synergies but on long-term market position. Could this company dominate its niche? Did its management team share RPM's values? Would customers remain loyal post-acquisition?

One early acquisition exemplified the approach: Mohawk Finishing Products, a small company that dominated furniture touch-up and repair products. It wasn't glamorous—bottles of stain and fill sticks for scratched coffee tables. But Mohawk owned its niche, commanded premium pricing, and generated consistent cash flow. More importantly, its management understood their customers intimately. RPM kept that management in place, provided capital for expansion, and watched Mohawk's profits compound.

The decentralized structure created unexpected benefits. Subsidiary presidents, freed from corporate bureaucracy, moved faster than larger competitors. They could approve customer-specific formulations without committee approval. They could enter new geographic markets without extensive studies. They could fail small and learn fast. This agility, paradoxically achieved through decentralization rather than central control, became RPM's competitive advantage.

In 1975, RPM declared a 50 percent stock dividend to its shareholders, an action that would recur over the next three years. These weren't just financial engineering—they were statements of confidence. While America questioned its industrial future, RPM was betting on it. The stock dividends made shares more accessible to retail investors, broadening the ownership base beyond Ohio and creating a constituency that would support the company's long-term approach.

Media recognition followed performance. Barron's, a weekly Wall Street publication, reported that RPM was among the top 15 paint firms in the industry and declared that the company's "Broad Mix of Protective Coatings Adds Luster to Results of RPM". The headline captured something essential: RPM wasn't really a paint company. It was a collection of specialists solving specific problems. That distinction would drive the next phase of explosive growth.

By 1978, Tom Sullivan had proven that RPM could survive and thrive without its founder. The company had evolved from a manufacturer to a manufacturing platform, from a family business to a public enterprise that retained family values. The infrastructure was in place—decentralized operations, acquisition expertise, public market access. Tom Sullivan and the board of directors decided to divide his leadership role into two positions: president/chief operating officer and chairman/chief executive, with Karman taking the president role. The stage was set for RPM to become not just a participant but an architect of industry consolidation. The acquisition machine was about to shift into high gear.

IV. The Acquisition Machine Takes Shape (1979–1994)

In 1979, just as RPM achieved the milestone of $100 million in annual sales, three of the company's outside directors recommended actions that would drive RPM's long-term growth. The boardroom conversation that day wasn't celebratory—it was confrontational. The outside directors challenged Sullivan and Karman: Why own businesses that didn't fit? Why not cooperate more between subsidiaries? Why maintain such radical decentralization? Their recommendations—divest non-core assets, implement operational planning, foster inter-company cooperation—sounded reasonable. But they threatened RPM's DNA.

Tom Sullivan's response defined the company's future. Yes, they would divest non-core assets. Yes, they would improve planning. But no, they would not force cooperation. The magic of RPM's model wasn't in synergy—it was in preserving the entrepreneurial spirit that made each acquisition valuable. Forcing collaboration would destroy the very independence that enabled innovation.

The 1980s became RPM's golden age of acquisition. While corporate America pursued hostile takeovers and leveraged buyouts, RPM practiced something different: consensual combination. They didn't raid companies; they courted them. The typical RPM acquisition began with relationship building, sometimes lasting years. Tom Sullivan would meet with owners at industry events, discussing philosophy more than price. When owners were ready—facing retirement, estate taxes, or growth capital needs—RPM was there with a unique proposition: sell us your company, keep running it.

The acquisition of Euclid Chemical Company in 1984 exemplified the approach. RPM acquired the Euclid Chemical Company, a leading manufacturer of concrete additives, masonry, waterproofing products and grouting materials, based in Cleveland. Euclid's owners had built a technical powerhouse but lacked capital for international expansion. RPM provided the capital while preserving Euclid's engineering culture. The result: Euclid's sales tripled within five years while maintaining its technical leadership.

International expansion accelerated through the 1980s, but not through traditional foreign subsidiaries. Instead, RPM acquired local champions who understood their markets intimately. RPM's exports grew, complemented by overseas licensees and joint ventures that accounted for $50 million in annual sales by 1987. Each international acquisition brought not just revenue but intelligence—about local regulations, customer preferences, and competitive dynamics that no amount of market research could provide.

The multi-segment structure emerged organically from these acquisitions. Consumer brands like Bondex and Mohawk served DIY markets. Industrial brands like Carboline and Stonhard served heavy industry. Construction brands like Tremco served commercial builders. Each segment had different customers, channels, and cycles. Traditional management theory suggested consolidation for efficiency. RPM did the opposite, preserving each segment's distinct culture and capabilities.

The stock market rewarded this unconventional approach. RPM announced an offering of 860,000 common shares in November 1977, which helped to finance the decade's many acquisitions. The stock was issued and sold out the same day. Investors understood something Wall Street analysts often missed: in specialty chemicals, intimacy beats efficiency. A Tremco salesman who had specified roofing systems for 20 years couldn't be replaced by a centralized sales force, no matter how well-trained.

But the masterstroke of the era was RPM's pursuit of Rust-Oleum, beginning with an unconventional backdoor approach. RPM opened a back door to Rust-Oleum Corporation with the strategic acquisition of its European operation in 1991. This wasn't just clever tactics—it was strategic patience. Rust-Oleum's owners could see how RPM operated, how they preserved independence, how European management thrived under RPM ownership. When RPM completed the deal in 1994 when it acquired the rest of the business, it wasn't a takeover—it was a marriage.

Rust-Oleum brought something invaluable: consumer brand recognition. While RPM's industrial brands dominated niches, they were unknown to consumers. Rust-Oleum was different—millions of Americans had used it to protect everything from lawn furniture to mailboxes. The brand's penetration in hardware stores and home centers provided a platform for RPM's other consumer brands.

The integration—or rather, non-integration—of Rust-Oleum became a Harvard Business School case study in contrarian management. RPM didn't move Rust-Oleum to Ohio. They didn't merge it with other paint brands. They didn't even change its packaging. They simply provided capital for new product development and geographic expansion. Rust-Oleum's sales doubled within five years while maintaining the highest margins in RPM's portfolio.

RPM was named to the venerable Fortune 500 list in 1994. At the time, the list was comprised of the world's largest industrial manufacturers. For a company that had been mixing chemicals in an Ohio garage just 47 years earlier, it was a remarkable achievement. But Tom Sullivan's reaction was characteristic: awards were nice, but what mattered was the next acquisition, the next product innovation, the next customer problem to solve.

The international expansion strategy of this period deserves special attention. While competitors built foreign factories, RPM bought foreign companies. This brought immediate market presence but more importantly, local knowledge. A French contractor wouldn't specify an American roofing system, but he would specify Viapol, RPM's French acquisition, without knowing it was American-owned. This stealth internationalization allowed RPM to become global while remaining local.

By 1994, RPM had assembled a portfolio of 30+ subsidiaries generating nearly $1 billion in revenue. But the real achievement wasn't size—it was system. RPM had created a replicable process for identifying, acquiring, and improving specialty chemical companies while preserving their entrepreneurial essence. The machine wasn't just operating; it was accelerating. The next phase would test whether this model could scale beyond $1 billion, whether a third generation of Sullivan leadership could emerge, and whether patient capital could survive in an increasingly impatient market.

V. The Billion Dollar Breakthrough & Major Brand Acquisitions (1995–2002)

In 1995, RPM's sales for the year surpassed $1 billion, a 25 percent increase from the previous year. Tom Sullivan marked the milestone not with celebration but with succession planning. The same year, Frank C. Sullivan, Tom Sullivan's son, was named RPM's executive vice president and was elected to the company's board of directors. The third generation's arrival signaled continuity but also evolution—Frank C. Sullivan (the younger) brought MBA training and Wall Street experience to complement the family's operational DNA.

The younger Frank's early involvement coincided with RPM's most ambitious acquisition phase. He had worked summers at RPM since age 13, starting at minimum wage—actually below what other seasonal workers earned. Around the time of his 18th birthday, Frank discovered he was making minimum wage of A$3.50, while other seasonal part-time associates were earning two dollars more. When I challenged my father, he asked me whether I was interested in making money or learning the business. The lesson stuck: RPM wasn't about quick profits but long-term value creation.

The late 1990s brought RPM's most significant strategic acquisitions. RPM made several acquisitions in 1997, the largest of which was the purchase of Tremco Inc., an industrial sealants and roofing manufacturer for $236 million. It served as the platform for the Construction Products Group, RPM's largest operating segment today. Tremco wasn't just another acquisition—it was a cornerstone. With dominant positions in commercial roofing and structural glazing, Tremco brought specification influence that money couldn't buy. When architects specified Tremco systems, contractors had no choice but to buy them.

The company's 50th anniversary in 1997 provided a moment for reflection. RPM celebrated its 50th anniversary and five consecutive decades of record sales and earnings. In recognition of this momentous achievement, the world-renowned Cleveland Orchestra performed for more than 5,000 RPM shareholders at the company's annual meeting. The classical music choice was deliberate—RPM was positioning itself as a company built for permanence, not fashion.

The DAP acquisition in 1999 expanded RPM's consumer reach dramatically. RPM added another highly regarded consumer brand to its portfolio in 1999 when it acquired DAP Products, a manufacturer and marketer of caulks, sealants, adhesives, and patch and repair products. Every hardware store in America carried DAP. Every contractor had used it. The brand's ubiquity provided distribution leverage for RPM's entire consumer portfolio.

But success bred complexity. By 2000, RPM operated dozens of subsidiaries across four continents. The decentralized model that enabled growth also created inefficiencies. Duplicate functions, incompatible systems, and missed opportunities for cooperation were becoming costly. The market was also changing—customers increasingly wanted single-source suppliers who could provide complete solutions.

The restructuring of 2000 was painful but necessary. The company took a $52 million restructuring charge during the 2000 fiscal year, which brought an end to the streak of consecutive years of increasing net income, at 52 years. For a company that prided itself on consistency, breaking the streak was agonizing. But Tom Sullivan and Jim Karman recognized that preserving the company's future required sacrificing its perfect record.

The restructuring wasn't about centralization—it was about optimization. Weak facilities were closed. Marginal product lines were discontinued. But critically, subsidiary autonomy was preserved. The cuts were surgical, not systemic. RPM proved it could adapt without abandoning its core philosophy.

International expansion accelerated through strategic acquisitions in emerging markets. European operations were strengthened through bolt-on acquisitions to existing platforms. Latin American beachheads were established through partnerships that would later become acquisitions. Asia remained challenging—the relationship-based business culture that made RPM successful in America didn't translate easily to markets where government connections mattered more than customer connections.

The transition from NASDAQ to NYSE in 1998 symbolized RPM's evolution from growth story to established institution. With nearly 7,000 employees and products in more than 130 countries, RPM switched from NASDAQ to the New York Stock Exchange and began trading under the symbol RPM. The three-letter ticker—simply RPM—was perfect. No need for explanation. The company had become synonymous with its industry.

By 2002, the pieces were in place for leadership transition. Tom Sullivan and Jim Karman had built a $2 billion enterprise from an $11 million base. During their tenure, net sales increased to $2 billion from $11 million, net income increased to $101.6 million from $0.6 million, cash dividends per share increased to $0.50 from $0.0035 (split-adjusted), and a $1,000 investment in RPM shares in 1971 would have been worth more than $100,000.

The numbers told only part of the story. Sullivan and Karman had institutionalized a paradox: entrepreneurial discipline. They proved that companies could grow through acquisition without losing their soul, that decentralization could coexist with public market accountability, that patient capital could outperform financial engineering. They had created not just a company but a system—one that could survive its creators.

VI. Leadership Transition & Third Generation Takes Charge (2002–2010)

After more than 30 years at the company's helm, Sullivan and Karman retired as executive officers of the company in 2002. The transition ceremony was deliberately understated—no grand speeches, no gold watches. Tom Sullivan simply handed his son Frank the same brass paperweight that his father had given him in 1971, engraved with "The Value of 168." Three generations, one philosophy.

Tom was succeeded by his son, Frank C. Sullivan, who became president and chief executive officer. The younger Frank faced immediate skepticism. Nepotism was the accusation whispered in analyst calls and trade publications. But Frank had credentials beyond his surname: He began his career with RPM in 1987 as regional sales manager for its joint venture AGR Company, before being elected to director of corporate development in 1989, vice president in 1991 and chief financial officer in 1993. Frank became executive vice president in 1995, president in 1999 and chief operating officer in 2001.

His first major decision surprised everyone: reorganization through reincorporation. RPM International Inc. became successor to RPM, Inc. following statutory merger effective October 15, 2002, for purpose of changing state of incorporation to Delaware. This wasn't financial engineering—it was strategic positioning. Delaware's corporate law provided better takeover protection, crucial for a company committed to long-term thinking in an increasingly short-term market.

More significantly, In connection with the 2002 reincorporation, RPM International Inc. realigned its various operating companies according to their product offerings, served end markets, customer base and operating philosophy. The new structure created four distinct groups: Construction Products, Consumer, Industrial (later Performance Coatings), and Specialty Products. Each group had its own leadership, strategy, and performance metrics. It was decentralization within decentralization—a fractal management structure.

The wisdom of this reorganization became apparent during the 2008 financial crisis. When construction markets collapsed, Consumer held steady. When industrial production plummeted, Specialty Products maintained margins. The portfolio wasn't just diversified by product—it was diversified by customer, channel, and cycle. RPM could weather any storm because it wasn't really one company but dozens of companies sharing capital and culture.

Frank Sullivan's leadership style blended his father's strategic vision with his grandfather's operational intensity. He spent weeks visiting subsidiaries, not to inspect but to listen. He learned that Rust-Oleum's R&D team had developed a revolutionary nano-coating technology. He discovered that Tremco's commercial roofing systems could be adapted for residential markets. He recognized that DAP's retail relationships could distribute other RPM consumer brands.

The international expansion under Frank's leadership was more systematic than opportunistic. RPM expanded its European presence with the strategic acquisition of illbruck Sealant Systems, which was headquartered in Cologne, Germany. Illbruck brought not just revenue but technology—advanced polymer chemistry that could be leveraged across RPM's portfolio. The acquisition also provided a platform for Eastern European expansion as those markets opened.

For the fiscal year ended May 31, 2006, the Company recorded sales of $3.0 billion. Crossing $3 billion in sales validated Frank's leadership and silenced the nepotism critics. But Frank understood that size without profitability was meaningless. He began focusing on operational excellence—not through centralization but through best practice sharing. Subsidiary presidents met quarterly to exchange ideas, voluntary collaboration replacing mandatory consolidation.

The acquisition pace continued but with more strategic focus. In 2008, RPM expanded its global footprint by acquiring nine companies with $200 million in combined annual sales. These weren't random purchases but carefully selected pieces that filled portfolio gaps or provided geographic expansion. Each acquisition was evaluated on strategic fit, not just financial metrics.

Latin American expansion accelerated during this period. Between 2007 and 2014, RPM acquired Viapol, Betumat and Cave, expanding its reach into emerging South America markets. These markets offered something North America and Europe couldn't: double-digit growth. Infrastructure spending in Brazil, industrial expansion in Mexico, and construction booms across the region provided tailwinds for RPM's products.

The 2008 financial crisis tested Frank's leadership and RPM's model. Competitors centralized operations, fired thousands, and slashed R&D. RPM took a different path. They maintained subsidiary autonomy, allowing local managers to respond to local conditions. They preserved R&D spending, believing innovation was the path out of recession. They continued acquiring, taking advantage of distressed valuations.

The crisis also revealed weaknesses in RPM's decentralized model. Some subsidiaries had excess capacity. Others had incompatible IT systems. Customer complaints about dealing with multiple RPM companies were increasing. Frank recognized that RPM needed to evolve—not abandon decentralization but optimize it. The seeds of what would become MAP to Growth were planted during these crisis years.

By 2010, Frank Sullivan had proven himself worthy of the family legacy. RPM had not just survived the worst recession since the 1930s but emerged stronger. The company was positioned for the next phase of growth, with strong brands, global presence, and financial flexibility. But Frank understood that past success guaranteed nothing. The next decade would require operational transformation without sacrificing entrepreneurial culture—perhaps the hardest challenge in RPM's history.

VII. Modern Era: MAP to Growth & Operational Excellence (2010–Present)

The October 2018 investor day at RPM's Medina headquarters felt different. Frank Sullivan, standing before analysts who had followed the company for decades, was about to announce something that seemed to contradict everything RPM stood for: centralization. At a 2018 investor day, RPM announced its operating improvement program— the MAP (Margin Acceleration Plan) to Growth.

The catalyst was uncomfortable truth. While RPM's decentralized model had built a $6 billion empire, it had also created inefficiencies that were becoming untenable. Competitors with centralized operations enjoyed 20% EBIT margins; RPM struggled to maintain 12%. The company operated 150+ manufacturing facilities, many running at 60% capacity. Dozens of subsidiaries maintained separate accounting systems, procurement contracts, and IT infrastructure. Customer complaints about dealing with multiple RPM entities were mounting.

Sullivan's solution was characteristically nuanced: operational centralization without organizational centralization. The program included initiatives to drive greater efficiency in order to accelerate growth and increase value from the unique entrepreneurial culture and leading brands that have been the foundation of RPM's success for decades. Subsidiaries would maintain their autonomy in customer relationships, product development, and market strategy. But back-office functions would consolidate.

From 2018 through 2021, RPM transformed its business into a center-led operational approach. Management implemented four center-led functional areas: manufacturing and operations, procurement and supply chain, information technology, and accounting and finance. This wasn't the heavy-handed centralization that destroyed value at other conglomerates—it was surgical optimization that preserved entrepreneurial spirit while eliminating redundancy.

The manufacturing transformation was dramatic. The MAP to Growth plan optimized RPM's manufacturing facilities, providing more efficient plant and distribution capabilities. In line with the MAP to Growth objective, RPM International completed the planned closure of 31 plants and 28 warehouses. These weren't arbitrary cuts—each closure was evaluated based on capacity utilization, customer proximity, and product overlap. Production was consolidated into modern, efficient facilities without disrupting customer relationships.

The procurement revolution was equally transformative. For decades, each RPM subsidiary negotiated its own raw material contracts. A Rust-Oleum plant in Illinois might pay 20% more for the same resin that a Tremco facility in Ohio purchased. consolidated material spending across our operating companies, negotiated improved payment terms that helped us to reduce working capital. The consolidated purchasing power of a $6 billion company replaced the fragmented negotiations of dozens of smaller entities.

Technology consolidation brought perhaps the greatest efficiency gains. consolidated 46 accounting locations, migrated 75% of our organization to one of four group-level ERP platforms. Instead of maintaining dozens of incompatible systems, RPM created shared platforms that enabled real-time visibility across the enterprise while preserving subsidiary autonomy in customer-facing systems.

The results exceeded all expectations. At year end, we brought our MAP to Growth operating improvement program to a successful conclusion. Over the course of the three-year initiative, we reduced our global manufacturing footprint by 28 facilities, created a lasting culture of manufacturing excellence and continuous improvement... These actions generated $320 million in annualized cost savings, which exceeded our original target by $30 million.

The $320 million in savings wasn't just cost-cutting—it was value creation. Margins expanded without sacrificing growth. Customer satisfaction improved as consolidated logistics reduced delivery times. Employee morale increased as investment in modern facilities replaced maintenance of obsolete ones. RPM proved that operational excellence and entrepreneurial culture weren't mutually exclusive.

The success of MAP to Growth emboldened Sullivan to think bigger. In August 2022, he announced MAP 2025, the next phase of operational transformation. RPM International Inc. (NYSE: RPM) today announced its MAP 2025 (Margin Achievement Plan) operational improvement initiative... Through MAP 2025, RPM expects to accelerate growth, maximize operational efficiencies, and build a better world to generate superior value creation for the company's customers, associates and shareholders.

The goals were audacious: By May 2025 end, RPM projects to achieve $8.5 billion of annual revenues, 42% gross margin and 16% adjusted EBIT margin. These targets would put RPM's profitability on par with the best specialty chemical companies globally while maintaining its decentralized operating model.

"MAP 2025 builds upon the successes we achieved with our previous MAP to Growth program," stated Frank C. Sullivan, RPM chairman and CEO. "These new initiatives are designed to amplify the strengths of RPM's entrepreneurial culture and accelerate our transformation into a more connected and efficient company".

The international expansion during this period was methodical rather than opportunistic. RPM expanded its European presence with the strategic acquisition of illbruck Sealant Systems, which was headquartered in Cologne, Germany. Illbruck brought advanced polymer chemistry and established relationships with European contractors—assets that would take decades to build organically.

Latin American expansion accelerated as infrastructure spending boomed across the region. Between 2007 and 2014, RPM acquired Viapol, Betumat and Cave, expanding its reach into emerging South America markets. These weren't just geographic expansions—they were platforms for capturing the infrastructure boom transforming emerging markets.

The 75th anniversary in 2022 provided perspective on the transformation. Since its founding in May 1947 by Frank C. Sullivan, Republic Powdered Metals – the forerunner to RPM International Inc. – has grown from a company with $90,000 in sales during its first year to a $7.3 billion, multinational company with subsidiaries that are world leaders in specialty coatings, sealants, building materials and related services.

Frank Sullivan (the third) had proven worthy of his inheritance. He transformed RPM from a successful but inefficient conglomerate into a world-class operator without sacrificing its entrepreneurial soul. The company that once prided itself on leaving acquisitions alone had learned when to integrate and when to preserve independence. The MAP initiatives weren't abandonment of RPM's philosophy—they were its evolution. The next phase would test whether this operational excellence could drive organic growth in an increasingly competitive global market.

VIII. The Four-Segment Strategy Deep Dive

Walking through an American hardware store in 2024 reveals RPM's strategic genius: you can't avoid their products. The caulk aisle is dominated by DAP. The spray paint section features walls of Rust-Oleum. The wood stain shelves showcase Varathane. Yet most customers have no idea these brands share a corporate parent. This anonymity is deliberate—RPM's four-segment strategy isn't about corporate branding but portfolio optimization.

About 36% of RPM's net sales are generated by the Construction Products Group, making it the company's largest segment. But CPG isn't really about size—it's about specification influence. When an architect designs a commercial building, they don't specify "roofing materials." They specify Tremco systems by name. Tremco Commercial Sealants & Waterproofing is North America's leading distributor of sealant, weatherproofing and passive fire control solutions. Its products are used by architects, engineers, home builders, contractors and building owners for a mix of commercial, residential construction and industrial applications.

The power of specification can't be overstated. Once Tremco is written into architectural plans, contractors have no choice but to purchase it. No substitutions allowed. This creates what economists call "derived demand"—the contractor isn't really the customer; the architect is. RPM understood this dynamic when it acquired Tremco for $236 million in 1997, using it as the platform for building CPG into a specification powerhouse.

The European consolidation exemplifies CPG's strategy. CPF Europe was established in the UK on 1 June 2020. It brings together RPM brands including illbruck, Flowcrete, Nullifire, Tremco, Vandex and Dryvit. Rather than force these brands under one umbrella, RPM maintained their identities while consolidating back-office functions. A German contractor still orders illbruck; he just doesn't know it shares warehouses with Tremco.

The Performance Coatings Group generates approximately 18% of RPM's total sales, but its strategic importance exceeds its revenue contribution. PCG serves the most demanding customers on earth: offshore oil platforms, chemical plants, nuclear facilities. These customers don't buy paint—they buy asset protection. When a refinery specifies Carboline coatings, they're paying for decades of corrosion resistance in environments that would destroy ordinary paint in weeks.

The supply-and-apply model sets PCG apart. Performance Coatings Group products are sold worldwide to contractors and distributors, as well as directly to end‑users with a unique supply-and-apply model serving manufacturers, public institutions and other commercial customers. RPM doesn't just sell coating; they apply it. This vertical integration captures higher margins while ensuring proper application—critical when coating failure could cost millions in downtime.

Approximately 35% of RPM's net sales are generated by the Consumer Group, but this segment punches above its weight in brand recognition. Consumer brands include Zinsser, Rust-Oleum, DAP, Varathane, Mean Green, Krud Kutter, Concrobium, Moldex and Testors. Walk into any Home Depot, Lowe's, or Ace Hardware—these brands dominate shelf space.

The Consumer Group's genius lies in category creation. Rust-Oleum didn't just make spray paint; they created reasons to use it. Chalkboard paint for kids' rooms. Metallic finishes for furniture flipping. Glow-in-the-dark paint for safety applications. Each innovation opens new markets while maintaining premium pricing. When a DIYer reaches for spray paint, they're not comparing prices—they're looking for Rust-Oleum.

DAP's acquisition in 1999 brought distribution leverage that transformed the Consumer Group. Every hardware store already carried DAP caulk. Adding other RPM consumer brands to DAP shipments reduced logistics costs while increasing shelf presence. The portfolio approach means RPM can offer retailers complete category solutions—not just products but planograms, training, and marketing support.

The Specialty Products Group generates approximately 11% of RPM's total sales, making it the smallest segment by revenue but perhaps the most profitable by margin. These aren't products you'll find at Home Depot—they're highly specialized solutions for niche industrial applications. Day-Glo fluorescent pigments for safety equipment. Stonhard seamless flooring for pharmaceutical clean rooms. Dryvit exterior insulation systems for commercial buildings.

The beauty of specialty products is pricing power. When you're the only company making fluorescent pigments that meet military specifications, price becomes secondary to performance. Customers can't substitute; they can't dual-source; they're essentially captive. This creates the economic moat Warren Buffett dreams about—sustainable competitive advantage that compounds over time.

The four-segment structure creates portfolio resilience that smooths cycles. When oil prices collapse, Performance Coatings suffers but Consumer thrives on lower raw material costs. When DIY trends fade, Construction Products picks up slack from commercial activity. When commercial construction slows, Specialty Products maintains margins through non-discretionary maintenance. The segments don't just coexist—they counterbalance.

Cross-selling between segments remains deliberately limited, preserving entrepreneurial independence. But knowledge transfer is encouraged. When Rust-Oleum developed a revolutionary nano-coating technology, the innovation spread to Performance Coatings products. When Tremco perfected cold-applied roofing systems, the technology enhanced Consumer Group repair products. Innovation flows freely even as operations remain independent.

International expansion varies by segment, reflecting different market dynamics. Construction Products expanded aggressively in Europe where building codes favor specification products. Performance Coatings grew in Asia following industrial expansion. Consumer brands remained primarily North American, where DIY culture drives demand. Specialty Products followed their niche customers globally. Each segment's geographic strategy reflects its unique market dynamics rather than corporate mandate.

The acquisition strategy differs by segment. Construction Products acquisitions focus on specification influence—buying companies architects already specify. Performance Coatings targets technical capabilities—companies with proprietary chemistry or application expertise. Consumer acquisitions prioritize shelf space—brands with established retail distribution. Specialty seeks monopolistic niches—companies dominating narrow markets.

Digital transformation affects segments differently. Consumer Group invested heavily in e-commerce and social media marketing, recognizing DIYers research online before buying in-store. Construction Products built specification software helping architects integrate products into building information modeling (BIM) systems. Performance Coatings developed IoT sensors monitoring coating performance in real-time. Specialty Products created customer portals for technical documentation. Each segment's digital strategy reflects its customer base rather than corporate diktat.

The margin profile varies dramatically across segments. Specialty Products generates 25%+ EBIT margins through monopolistic pricing. Performance Coatings achieves 18-20% through value-added services. Construction Products maintains 15-17% via specification influence. Consumer Group, despite brand strength, faces 12-14% margins due to retail pricing pressure. The portfolio approach means RPM can optimize capital allocation based on return potential rather than segment size.

By 2024, the four-segment strategy had proven its wisdom. RPM wasn't trying to be Sherwin-Williams or PPG—companies focused on architectural paint. Instead, it had become something unique: a collection of market-leading specialists united by capital and culture but operating with entrepreneurial independence. The structure that seemed unnecessarily complex to Wall Street analysts had become RPM's greatest strategic advantage.

IX. The Dividend Aristocrat Story

The October 5, 2023 annual meeting felt like a coronation. Frank Sullivan stood before shareholders to announce what many thought impossible in modern capitalism: RPM International Inc. (NYSE: RPM) today announced at its annual meeting of stockholders that its board of directors declared a regular quarterly cash dividend of $0.46 per share, marking the company's 50th consecutive year of dividend increases. RPM's 50th consecutive year of increased cash dividends paid to its stockholders places RPM in an elite category of less than half of 1 percent of all publicly traded U.S. companies.

The mathematics of this achievement stagger the mind. If you invested $1,000 in RPM stock on August 31, 1973, and reinvested dividends for the past 50 years, the total value of that investment (excluding taxes) as of August 31, 2023, would be over $1.1 million. This compares to a total value of $0.2 million for a $1,000 initial investment in the S&P 500® over the same period with dividends reinvested and taxes excluded. The compound effect of consistent dividend growth had created generational wealth for patient shareholders.

Understanding RPM's dividend philosophy requires understanding the Sullivan family's view of ownership. They didn't see shareholders as traders to be managed but as partners to be rewarded. The dividend wasn't residual cash after all other uses—it was a primary obligation, ranking alongside R&D and acquisitions in capital allocation priority. This inverted the typical corporate hierarchy where dividends come last.

Since initiating its focus on an annually growing dividend in 1973 to drive long-term value for shareholders, RPM has grown from $25 million in annual sales to more than $7.4 billion, while delivering $3.7 billion in after-tax capital through its cash dividend program. The $3.7 billion returned to shareholders represents more than half of RPM's current market capitalization—a staggering transfer of wealth from company to owners.

The commitment to dividend growth shaped every strategic decision. During the 2008 financial crisis, while competitors suspended dividends to preserve cash, RPM increased its payout. The signal was unmistakable: RPM would sacrifice almost anything before breaking its dividend streak. This commitment attracted a unique shareholder base—patient capital that valued consistency over volatility.

Only 41 other U.S. companies, besides RPM, have consecutively paid an increasing annual cash dividend for a longer period of time, according to Dividend Radar. This places RPM among companies like Coca-Cola, Johnson & Johnson, and Procter & Gamble—the royalty of American capitalism. Yet RPM achieved this while operating in cyclical, commodity-influenced markets that supposedly made consistent dividend growth impossible.

The dividend policy created operational discipline. Knowing they needed to increase the dividend annually forced management to think long-term. Short-term earnings manipulation became pointless—you can't fake cash dividends for 50 years. This aligned management incentives with shareholder interests more effectively than any compensation scheme.

The shareholder base that emerged reflected this philosophy. 202,929 Institutional and Individual Investors owned RPM shares, an unusually broad ownership for a specialty chemicals company. Many were individual investors who had owned shares for decades, treating RPM dividends as retirement income. This stable ownership provided patient capital that enabled long-term thinking.

The payout ratio remained deliberately conservative—typically 35-40% of earnings. The company's projected dividend payout ratio for 2025 is 37%. This wasn't stinginess but sustainability. RPM could maintain dividend growth through recessions because the payout never stretched the balance sheet. Conservative payout ratios also left capital for acquisitions and organic growth, ensuring the dividend could grow with the business.

The dividend reinvestment plan (DRIP) became a wealth-building machine for small investors. By automatically reinvesting dividends to purchase additional shares, investors harnessed compound growth without transaction costs. Many RPM employees enrolled in the DRIP, gradually building substantial holdings that funded retirements and college educations. The company that started in an Ohio garage had created millionaires among its rank-and-file employees.

Tax efficiency added another dimension. Qualified dividends received favorable tax treatment compared to ordinary income, making RPM attractive to high-net-worth investors. The consistent growth rate—typically 5-10% annually—outpaced inflation while remaining sustainable. Investors received real purchasing power growth, not just nominal returns.

The psychological impact of the dividend streak became self-reinforcing. As the streak lengthened, breaking it became unthinkable. Each CEO inherited not just a company but a sacred obligation. Frank Sullivan (the third) understood that ending the streak would destroy not just shareholder value but family legacy. This created extraordinary pressure for operational excellence—mediocrity might be forgiven, but dividend cuts never.

The 2020 restructuring charge that ended RPM's 52-year streak of consecutive earnings increases demonstrated the dividend's priority. Management chose to break the earnings streak to preserve the dividend streak, recognizing which metric truly mattered to long-term shareholders. Earnings could be managed; dividends required real cash.

International investors particularly valued RPM's dividend consistency. In a world of negative interest rates and currency debasement, RPM offered something precious: dollar-denominated income growth. European and Asian investors bought RPM not for capital appreciation but for reliable, growing income streams unavailable in their home markets.

The dividend philosophy influenced acquisition strategy. RPM favored cash-generative businesses that could immediately contribute to dividend coverage. Speculative technology ventures or capital-intensive expansions were avoided. Every acquisition was evaluated not just on strategic fit but on dividend sustainability. This discipline prevented the empire-building that destroyed many conglomerates.

RPM has raised its dividend for 51 consecutive years as of 2024, joining the exclusive "Dividend Kings" club. A Dividend King is a company that's grown its dividend payment for at least 50 consecutive years. The psychological barrier of 50 years created a new level of institutional permanence. RPM wasn't just a company anymore—it was an institution, like a university or museum, built to endure centuries.

The dividend commitment also shaped corporate governance. Board members were selected not for celebrity but for long-term thinking. Quarterly earnings calls spent more time discussing five-year plans than quarterly variances. Analyst questions about "returning cash to shareholders" were met with bemusement—RPM had been doing nothing but returning cash for half a century.

Modern financial engineering—buybacks, special dividends, spin-offs—held no appeal. RPM's capital allocation philosophy was boringly consistent: fund operations, make acquisitions, pay dividends, repeat. This simplicity was its genius. While competitors pursued complex financial strategies, RPM simply sent checks to shareholders every quarter, slightly larger than the previous year.

By 2024, the dividend had become RPM's defining characteristic. The company wasn't known for innovation or growth or operational excellence, though it achieved all three. It was known for reliability—the corporate equivalent of Old Faithful, erupting predictably every quarter for half a century. In a world of disruption and creative destruction, RPM offered something invaluable: consistency. For investors seeking not excitement but certainty, RPM's dividend aristocracy provided exactly what modern capitalism rarely delivered: trust.

X. Financial Performance & Current State Analysis

The July 2024 earnings call opened with Frank Sullivan's characteristic understatement: "We achieved record adjusted EBIT for the 10th consecutive quarter due to our strategic balance and our ability to leverage MAP 2025 operating improvement initiatives to increase profitability." Ten consecutive quarters of record profitability during a period of inflation, supply chain chaos, and demand volatility—this wasn't luck but operational excellence finally matching RPM's strategic positioning.

Record fiscal 2024 net sales of $7.34 billion, up 1.1% from the prior year might seem modest growth, but the composition revealed strategic transformation. Fiscal year 2024 sales were a record, driven by strength in CPG and PCG, which have positioned themselves to provide engineered solutions for infrastructure and high-performance building projects, including reshoring projects. RPM wasn't just growing—it was growing in the right places.

The margin story dominated the narrative. Record fiscal 2024 adjusted diluted EPS of $4.94 increased 14.9% over prior year and record adjusted EBIT increased 11.9% to $941.6 million. Earnings growing faster than revenue—the holy grail of operational leverage. The MAP 2025 initiatives weren't just cost-cutting; they were fundamental business transformation enabling pricing power and mix improvement.

Cash generation reached unprecedented levels. Record fiscal 2024 cash flow from operating activities of $1.12 billion, up $545.2 million over prior year. The $545 million increase—nearly doubling cash generation—reflected not just profitability but working capital excellence. RPM had learned to convert earnings into cash with unprecedented efficiency.

Segment performance revealed portfolio wisdom. CPG fourth-quarter sales were a record with broad-based strength led by turnkey roofing systems, wall systems and products serving infrastructure-related projects, including those that lower the carbon footprint of projects. Construction Products wasn't just benefiting from infrastructure spending—it was positioned at the intersection of sustainability and resilience, two megatrends reshaping construction.

Consumer generated record adjusted EBIT, despite continued DIY softness, due to its MAP 2025 initiatives and ability to win market share. This was perhaps most impressive—generating record profitability in a declining market through operational excellence and market share gains. When competitors struggled with DIY weakness, RPM's brands gained shelf space and customer loyalty.

The geographic mix showed strategic evolution. In Europe, although sales declined, a focused strategy to leverage MAP 2025 initiatives improved profitability in the region. RPM had learned that not all revenue is created equal—profitable European business beat unprofitable growth. This maturity in thinking marked RPM's evolution from growth-at-any-cost to value creation.

Partially offsetting this growth was the Consumer Group, which experienced soft DIY demand and SPG, which faced weak demand, particularly in disaster restoration and specialty residential OEM markets. The weakness wasn't hidden or explained away—RPM's transparency about challenges enhanced credibility about successes.

The balance sheet transformation was dramatic. The company also reduced its total debt by $556.7 million, bringing it down to $2.13 billion. Deleveraging while growing, returning capital to shareholders, and investing in operations—this financial flexibility provided options in an uncertain world.

Capital allocation remained disciplined. Capital expenditures were $214.0 million, and RPM returned $286.9 million to stockholders through cash dividends and share repurchases. The balance—investing enough to support growth while returning excess capital—reflected mature capital allocation philosophy.

The forward guidance revealed confidence without hubris. Fiscal full-year 2025 outlook calls for revenue growth of low single digits and adjusted EBIT growth of mid-single-digits to low-double-digits. Profit growth exceeding revenue growth—the MAP 2025 flywheel continuing to spin.

Record adjusted EBIT was driven by MAP 2025 benefits, including the commodity cycle, better mix and improved fixed-cost leverage at businesses that generated volume growth. The commodity cycle reference was crucial—RPM had learned to manage input cost volatility through pricing discipline and mix management rather than hoping for favorable markets.

Analytical depth improved dramatically. The primary driver behind last 12 months revenue was the Construction Products Group (CPG) segment contributing a total revenue of US$2.70b (37% of total revenue). CPG's dominance wasn't concerning but strategic—infrastructure spending provided multi-decade tailwinds that CPG was uniquely positioned to capture.

Cost structure evolution showed operational maturity. Notably, cost of sales worth US$4.32b amounted to 59% of total revenue thereby underscoring the impact on earnings. A 59% cost of sales ratio in a commodity-influenced business during inflationary times represented exceptional procurement and pricing discipline.

Selling, general and administrative expenses increased due to incentives to sell higher-margin products and services, investments to accelerate long-term growth, and inflation in compensation and benefits. Several MAP 2025-enabled initiatives to streamline the selling, general and administrative expense structure were implemented during the fourth quarter of fiscal 2024. Even rising SG&A was strategic—investing in growth while simultaneously streamlining operations.

The international narrative evolved from expansion to optimization. Rather than pursuing growth everywhere, RPM focused on profitable growth in strategic markets. This selectivity—anathema to traditional conglomerates—reflected confidence that organic improvement could drive returns better than geographic sprawl.

Innovation investment continued despite margin focus. New product development, particularly in sustainable building materials and high-performance coatings, positioned RPM for secular growth trends. The company wasn't mortgaging its future for current profitability—it was investing for both.

Digital transformation, though less visible than operational improvements, revolutionized customer engagement. E-commerce platforms for Consumer brands, specification software for Construction Products, and IoT monitoring for Performance Coatings created competitive advantages beyond traditional distribution.

Supply chain resilience, tested during COVID and subsequent disruptions, proved robust. Multiple sourcing strategies, regional manufacturing, and inventory management enabled RPM to serve customers when competitors couldn't. This reliability premium—customers paying more for certainty of supply—enhanced margins and relationships.

The workforce evolution reflected changing business needs. Technical sales engineers replaced traditional salespeople. Data analysts supplemented accountants. Digital marketers joined brand managers. RPM's 17,300 employees increasingly looked like a technology company that happened to make coatings.

Sustainability initiatives, once peripheral, became central to strategy. Products that reduced carbon footprints, extended asset life, or eliminated harmful chemicals commanded premium pricing. RPM's boring products suddenly seemed essential for a sustainable future.

By 2024, RPM had achieved something remarkable: transformation without disruption. The company Frank Sullivan founded in 1947 would recognize the products but not the operations. The company Tom Sullivan built through acquisitions would recognize the structure but not the efficiency. The company Frank Sullivan (the third) inherited was becoming something new—a 21st-century industrial champion built on 20th-century values. The next chapter would test whether this transformation could accelerate growth while maintaining the consistency that defined RPM for nearly eight decades.

XI. Playbook: Business & Investing Lessons

The conference room at Harvard Business School fell silent as the professor posed the question: "How does a company in commodity chemicals achieve 50 consecutive years of dividend increases while maintaining entrepreneurial culture across hundreds of acquisitions?" The case study was RPM International, and the paradoxes it presented challenged everything MBAs thought they knew about corporate strategy.

The Power of Decentralized Operations with Centralized Capital Allocation

RPM's model inverted traditional corporate structure. While most conglomerates centralize operations to achieve synergies, RPM centralized only capital allocation while radically decentralizing operations. Each subsidiary operated as if independent—own P&L, own management, own culture. But capital flowed from the center, allocated by executives who understood portfolio theory better than most hedge fund managers.

This structure solved the fundamental agency problem of conglomerates. Subsidiary presidents weren't corporate politicians managing up; they were entrepreneurs managing out to customers. They couldn't blame corporate for failures or credit headquarters for successes. This ownership mentality—psychological rather than legal—drove performance that centralized structures couldn't achieve.

The discipline came through capital allocation. Subsidiaries competed for growth capital based on returns, not politics. A small specialty products business generating 25% returns on invested capital received more investment than a large consumer brand generating 15%. This meritocracy of capital created internal competition that improved performance across the portfolio.

Building a Dividend Aristocrat: Long-term Thinking vs. Quarterly Capitalism

RPM's dividend commitment created a different temporal framework. While competitors managed quarters, RPM managed decades. The dividend streak became an organizing principle that shaped every decision. Would this acquisition support dividend growth in year 10? Would this restructuring risk the dividend in a recession? The questions themselves forced long-term thinking.

This commitment attracted a unique shareholder base. RPM shareholders weren't momentum traders or activist investors but patient capital seeking reliability. This stability allowed management to invest through cycles, knowing shareholders wouldn't panic during downturns. The dividend commitment created a virtuous cycle: patient shareholders enabled long-term thinking which enabled consistent dividends which attracted patient shareholders.

The psychological impact on management was profound. Breaking the streak would be personal failure, not just professional setback. This created extraordinary motivation for operational excellence. Managers would accept lower bonuses before cutting the dividend. They would divest underperforming assets rather than risk dividend coverage. The dividend wasn't a financial policy—it was an identity.

Roll-up Strategy Execution: When to be Hands-off vs. Hands-on

RPM perfected the art of selective integration. Unlike traditional roll-ups that immediately integrate acquisitions for synergies, RPM left customer-facing operations untouched while consolidating back-office functions. A newly acquired company kept its sales force, brand identity, and customer relationships but gained RPM's purchasing power, capital access, and operational expertise.

The decision framework was elegant: if it touches the customer, leave it alone; if it touches the spreadsheet, consolidate it. This preserved the entrepreneurial energy that made targets valuable while eliminating redundancies that destroyed value. Customers saw continuity; shareholders saw synergies.

The acquisition courtship process—often lasting years—was as important as price. RPM wanted sellers who valued legacy over maximizing price. These sellers often remained as managers, motivated by earnouts and cultural fit rather than just economics. This patient approach meant RPM paid fair prices for great businesses rather than great prices for fair businesses.

Family Business Succession Done Right: Three Generations of Leadership

The Sullivan family's three-generation leadership violated every principle of modern governance, yet succeeded spectacularly. The key wasn't nepotism but meritocracy within constraints. Each generation had to prove themselves operationally before ascending to leadership. Frank Jr. started in sales, not the executive suite. Frank III worked minimum wage (actually below) before earning promotions.

This apprenticeship model created deep operational knowledge. The Sullivans understood the business from the ground up, not just from board presentations. They could evaluate acquisitions based on operational reality, not financial projections. They could sense cultural fit because they had lived the culture.

The family ownership mentality—even with public shareholders—created different incentives. The Sullivans thought about RPM as a legacy to pass on, not a vehicle for wealth extraction. This aligned their interests with long-term shareholders in ways that professional managers with option packages never could.

Niche Dominance Strategy: Owning Boring but Essential Products

RPM's product portfolio strategy was counterintuitive: dominate niches too small for giants to care about but too essential for customers to ignore. Fluorescent pigments for safety equipment. Concrete additives for infrastructure. Roof coatings for factories. These weren't sexy products, but they were sticky products with pricing power.

Each niche had characteristics: specialized knowledge requirements that created barriers to entry; small market size that discouraged new competition; essential applications where product failure cost far more than product price; and technical sales processes that created switching costs. These niches were economically attractive precisely because they were strategically unattractive to larger competitors.

The portfolio of niches created resilience. When one market declined, others compensated. When construction slowed, maintenance increased. When commercial struggled, consumer compensated. This wasn't diversification for its own sake but thoughtful portfolio construction based on uncorrelated demand drivers.

The Entrepreneurial Holding Company Model

RPM pioneered a structure that combined entrepreneurial energy with corporate resources. Subsidiary presidents were entrepreneurs with safety nets—they could take risks knowing RPM's balance sheet backed them, but success or failure was their own. This attracted a unique talent pool: operators who wanted autonomy but not isolation.

The model created option value. Each subsidiary was essentially a call option on its market. If it succeeded, RPM captured the upside. If it struggled, the damage was contained. With dozens of subsidiaries, some would always be creating value even if others were destroying it. The portfolio approach reduced risk while maintaining upside.

Knowledge transfer happened organically, not through mandate. Subsidiary presidents met quarterly, sharing best practices voluntarily. Innovation spread through pull, not push. When one subsidiary developed breakthrough technology, others adopted it because they wanted to, not because they had to. This voluntary collaboration was more effective than mandatory integration.

Lessons from the SEC Investigation (2014-2016) and Governance Improvements

In August 2013, RPM paid $61 million to settle U.S. General Services Administration claims regarding a subsidiary's overcharging the U.S. government on roofing contracts. In June 2014, the SEC launched an investigation into the timing of RPM's disclosure and accrual of loss reserves involving the GSA settlement. On September 9, 2016, the SEC charged RPM and its general counsel, Edward W. Moore, with violating antifraud provisions of Federal securities laws by failing to disclose a material loss. According to the SEC's complaint Moore did not inform RPM's CEO, CFO, audit committee and independent auditors of material facts about the U.S. Department of Justice investigation into the GSA issue.

The SEC investigation revealed governance weaknesses in RPM's decentralized model. The extreme autonomy that enabled entrepreneurship also enabled misconduct. The resolution—On December 23, 2020, the SEC announced that the company and Moore agreed to pay more than $2 million to settle the SEC's charges without admitting or denying the allegations of the complaint—forced RPM to evolve its governance while maintaining operational independence.

The reforms were surgical: enhanced compliance monitoring without operational interference; improved information flow from subsidiaries to corporate without creating bureaucracy; and stronger financial controls without constraining commercial flexibility. RPM proved that governance and entrepreneurship weren't mutually exclusive but required thoughtful balance.

The crisis became a catalyst for improvement. RPM emerged with better systems, stronger controls, and clearer accountability. The company that had perhaps been too trusting learned appropriate skepticism without becoming cynical. The governance improvements made RPM stronger without making it slower.

The Meta-Lesson: Building Antifragile Organizations

RPM's deepest lesson wasn't about strategy or operations but about organizational design. They built an antifragile company—one that gets stronger from stress rather than just surviving it. Each crisis—founder's death, recessions, SEC investigation—made RPM better. This wasn't resilience but evolution.

The antifragility came from structure: decentralization meant problems couldn't cascade; diversity meant downturns couldn't devastate; patience meant cycles couldn't panic; and ownership mentality meant challenges created determination, not despair. RPM designed a company that thrived on disorder—the ultimate competitive advantage in a chaotic world.

For investors, RPM offered a different proposition: not growth or value but consistency. In a portfolio, RPM was ballast—the boring holding that paid dividends, grew steadily, and survived crises. While exciting stocks created returns, RPM created wealth. The distinction—returns versus wealth—embodied everything RPM represented: patience over performance, sustainability over speculation, building over trading.

XII. Bear vs. Bull Case & Future Outlook

The investment committee debate over RPM had reached its third hour. The bull was passionate, the bear skeptical, and both had compelling data. As they parsed through projections and probabilities, a fundamental question emerged: Was RPM a relic of 20th-century industrialism or a template for 21st-century resilience?

Bull Case: The Infrastructure Supercycle Thesis

"The stars have never been more aligned for RPM," the bull argued, pulling up a cascade of government spending authorizations. The Infrastructure Investment and Jobs Act's $1.2 trillion. The CHIPS Act's $280 billion. The Inflation Reduction Act's clean energy provisions. "We're not talking about a cycle—we're talking about a generational rebuilding of American infrastructure."

The numbers were staggering. America's infrastructure report card showed $2.6 trillion in needs through 2029. Every bridge repaired needed protective coatings. Every new semiconductor fab required specialized flooring. Every renewable energy installation demanded weather-resistant sealants. RPM's Construction Products and Performance Coatings groups were perfectly positioned—they didn't just participate in infrastructure spending, they were essential to it.

The reshoring/nearshoring boom added another layer. As supply chains relocated from Asia to North America, new manufacturing facilities needed construction, protection, and maintenance. Each new factory was a 30-year annuity for RPM products—initial construction, ongoing maintenance, periodic renovation. The multiplier effect was extraordinary.

The bull's ace card was RPM's proven M&A machine. With 200+ successful acquisitions and dry powder for more, RPM could consolidate the fragmented specialty chemicals market for decades. Each acquisition at 8-10x EBITDA immediately became worth 15x within RPM's multiple. This arbitrage—not synergies or integration—created shareholder value. With thousands of family-owned specialty chemical companies approaching succession, RPM's acquisition pipeline was essentially infinite.

The dividend aristocrat status had become self-reinforcing. In a world of zero interest rates and volatile equities, RPM's growing dividend attracted permanent capital. Pension funds, sovereign wealth funds, and family offices needed reliable income growth. RPM stock had become a bond substitute with equity upside—an increasingly rare combination that commanded premium valuations.

The MAP 2025 margin expansion story was just beginning. With targets of 16% adjusted EBIT margins by 2025, RPM had line of sight to best-in-class profitability. The operational improvements weren't one-time cost cuts but structural transformations—digitized supply chains, automated manufacturing, and AI-powered pricing optimization. As volumes recovered, these improvements would create explosive earnings growth.

"RPM at 20x earnings might seem expensive," the bull concluded, "but it's cheap for a company with 50 years of dividend growth entering a multi-decade infrastructure supercycle with proven margin expansion and unlimited acquisition opportunities."

Bear Case: The Mature Market Trap

The bear's response was measured but devastating. "You're describing yesterday's opportunity, not tomorrow's challenge."

The cyclical exposure was RPM's Achilles heel. Yes, infrastructure spending was massive, but it was also political. A change in administration, a budget crisis, or a recession could defer projects indefinitely. Meanwhile, 35% of revenue came from consumer DIY markets clearly past their pandemic peak. When housing turnover slowed and home improvement normalized, Consumer Group would face years of headwinds.