RenovoRx: The Precision Strike on Cancer

I. Introduction & The "Delivery Problem"

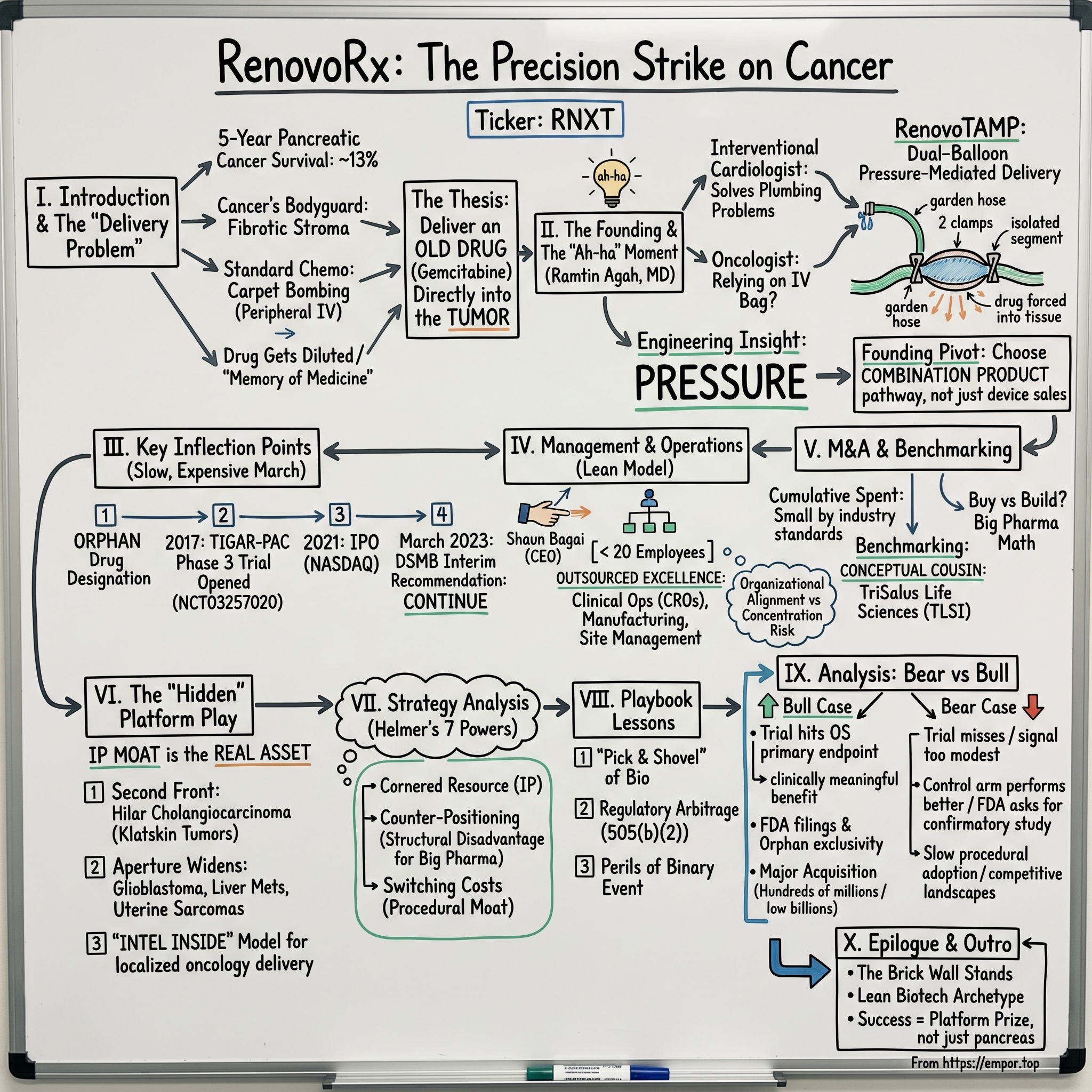

Picture a stage at the Pancreatic Cancer Action Network's annual symposium. A medical oncologist clicks to the next slide, and there it is — the chart that has haunted American medicine for fifty years. Five-year survival for pancreatic ductal adenocarcinoma sits stubbornly around 13%, a number that has crept upward by single percentage points across decades while breast, prostate, and even some lung cancers have seen their survival curves bend dramatically upward.[^1] The audience already knows the punchline. The drugs have improved. The diagnostics have improved. The surgical technique has improved. And yet the brick wall stands.

Why? The standard explanation invokes biology — pancreatic tumors hide behind a dense fibrotic stroma, the cancer's bodyguard of scar tissue that strangles its own blood supply and turns away the very molecules sent to kill it. But the more interesting question, and the one this story turns on, is not about the drug. It is about the truck that carries the drug.

Most chemotherapy is a carpet bomb. You infuse a cytotoxic agent into a peripheral vein in the patient's arm, it circulates through the entire body — bone marrow, gut lining, hair follicles, every fast-dividing cell that has the misfortune to be in the blast radius — and a tiny, tiny fraction of it actually reaches the tumor. For a hypovascular tumor like pancreatic adenocarcinoma, "tiny" is generous. By the time the gemcitabine molecule has been diluted through forty liters of total body water and dodged the liver's first-pass metabolism, what arrives at the pancreas is closer to a memory of medicine than medicine itself.

This is the delivery problem. And it is the thesis of a company called RenovoRx, Inc., trading on the NASDAQ Capital Market under the ticker RNXT, which has spent more than a decade arguing — with patents, catheters, and a Phase 3 trial called TIGAR-PAC — that the next great oncology breakthrough may not be a new molecule at all. It may be a better way to drive an old one straight into the tumor.1

This article traces the company from a Silicon Valley garage and a cardiologist's "ah-ha" moment in the cath lab, through an Orphan Drug Designation, a 2021 micro-cap IPO, a positive interim analysis that the market mostly ignored, and into the strange purgatory of a sub-$50 million market-cap biotech sitting on a Phase 3 readout that could either rerate the equity by an order of magnitude or extinguish it. Along the way we will examine the drug-device hybrid business model, the lean operating philosophy of a sub-twenty-person company running a global Phase 3 study, and the strategic question that hovers over every micro-cap in this space: is this a future acquisition target for big pharma, or is it a binary lottery ticket priced like one?

We will also look at the platform thesis — because if the RenovoTAMP catheter works in the pancreas, the same approach might work in the bile duct, the liver, the uterus, and any other solid tumor that lives at the end of a feeding artery. The bull case is not just pancreatic cancer. The bull case is the "Intel Inside" of localized oncology delivery. Whether that bull case survives contact with the data, and with the world's most demanding regulator, is the story that follows.

II. The Founding & The "Ah-ha" Moment

The origin story does not begin in a wet lab. It begins in a catheterization suite, sometime in the mid-2000s, where a young interventional cardiologist named Dr. Ramtin Agah was threading a guidewire through a patient's femoral artery and watching the contrast bloom on the fluoroscopy screen. Agah had trained in the world of stents and balloons — the discipline of solving plumbing problems inside the human body — and he had grown intimate with a particular kind of intellectual frustration. When a cardiologist needs to deliver a drug to a specific patch of heart muscle, they have tools. They have catheters, balloons, occlusions, and pressure gradients. When an oncologist needs to deliver a drug to a specific tumor, they have, essentially, an IV bag.

The "ah-ha" was simpler than most founding myths pretend. Why, Agah asked, was the most sophisticated discipline in interventional medicine — the precise, image-guided delivery of agents to a specific spot in the body — being entirely ignored by oncology? Why was the field that pioneered targeted endovascular access still relying, in the year of our lord 2010, on systemic infusion to treat tumors that were, in many cases, fed by a single identifiable artery?

There were answers to that question, of course. Some of them were technical. Hepatic artery infusion pumps had existed for decades; transarterial chemoembolization (TACE) was already standard of care for certain liver tumors. But for pancreatic cancer specifically, the geometry was forbidding. The pancreas is a small, retroperitoneal organ fed by a tangle of fine branches off the celiac trunk and the superior mesenteric artery. Pushing drug through one of those feeding vessels with a standard catheter would simply send most of the dose downstream into the duodenum and the spleen, poisoning bystander tissue without bathing the tumor.

The engineering insight was to use pressure. If you could isolate a segment of artery with two balloons — one upstream and one downstream of the tumor's feeding vessel — and then inject the drug into the sealed segment under positive pressure, you would force the molecules out through the vessel wall and into the interstitial space of the tumor itself. You would, in a sense, be "bathing" the tumor in concentrated medicine while sparing the rest of the body the toxicity. The dual-balloon, pressure-mediated delivery concept became the founding patent and the founding product. The company called the platform RenovoTAMP — Trans-Arterial Micro-Perfusion.2

In layman's terms, picture a garden hose with two clamps. Close both clamps, drill a small hole in the side of the hose between them, then turn on the faucet. Water has nowhere to go but out the hole. That is what RenovoTAMP does inside a tumor's feeding artery — except instead of water, it pushes gemcitabine, and instead of escaping into the open air, the drug is forced through the porous vessel wall and into the tumor tissue at concentrations that would be unthinkable to administer systemically.

There was a strategic choice baked into this from the start, and it would prove to be one of the most important business decisions in the company's history. RenovoRx could have been a pure medical device company — sell catheters to hospitals, let oncologists pair them with whatever drug they pleased, take a hardware margin, and call it a day. Instead, the company chose to file as what the FDA classifies as a combination product. Their lead candidate, RenovoGem, is a specific drug-device pairing: intra-arterial gemcitabine delivered via the RenovoTAMP catheter, regulated and reimbursed as a single therapy.1

This was, in retrospect, the founding pivot. By coupling an off-patent generic chemotherapy with a proprietary delivery system, the company traded the simplicity of a pure device play for the much larger economics of a branded therapeutic. The catheter on its own might command a few thousand dollars per procedure. The combination product — if approved — could be priced as a cancer therapy, which is to say in the tens of thousands of dollars per course. And because the underlying gemcitabine was already FDA-approved, the regulatory pathway could lean on the 505(b)(2) framework, which allows a sponsor to reference existing safety data for the active ingredient and focus their own clinical work on the novel delivery aspect.

That was the bet. Take a forty-year-old chemotherapy nobody wanted to defend any longer, marry it to a catheter nobody else had built, and aim the whole thing at the disease with the worst survival statistics in modern oncology. From there, the company needed something every biotech founder eventually confronts — a regulator willing to play along.

III. The Last Decade: Key Inflection Points

If the founding was a flash of insight in a cath lab, the decade that followed was a slow, expensive march through the most unforgiving terrain in American business: the FDA clinical pathway. For RenovoRx, four inflection points define the journey from idea to public-company drug developer.

The first was Orphan Drug Designation. Securing FDA Orphan Drug status for RenovoGem in pancreatic cancer was the bureaucratic equivalent of getting your name on a guest list — it does not guarantee approval, but it does grant you tax credits on clinical research, exemption from certain FDA user fees, and, most importantly, seven years of market exclusivity once you get there.[^4] For a tiny company developing a therapy for a disease that kills more than fifty thousand Americans a year, the designation was less a perk than a survival mechanism. It told prospective investors that the regulator had at least acknowledged the unmet need. In a world where most micro-cap biotechs die not from clinical failure but from running out of capital, Orphan Drug status is the kind of paperwork that keeps the lights on for another quarter.

The second inflection point arrived in 2017, when the company opened enrollment in TIGAR-PAC — the Targeted Intra-arterial Gemcitabine vs. Continuation of Standard of Care Chemotherapy in PAtients with Locally Advanced Pancreatic Cancer trial. The study was registered on ClinicalTrials.gov under the identifier NCT03257020, and from the moment it was activated it became the company's gravitational center. Everything — capital allocation, hiring, IR strategy, even the corporate slide deck — would orbit around TIGAR-PAC for the better part of a decade.3

This is the strange physics of single-asset biotech. When your entire enterprise value depends on a single Phase 3 readout, every other decision is in service of getting that trial to its primary endpoint. You do not diversify. You do not branch out. You do not, if you can avoid it, take on any operational complexity that does not directly accelerate enrollment. The trial is the company; the company is the trial. That is also why the trial is sometimes described internally — and described by us here — as "betting the company." Because that is precisely what it is.

The third inflection point was the IPO. In August 2021, RenovoRx filed its S-1 with the SEC, and shortly thereafter listed on the NASDAQ Capital Market.4 The raise was small by biotech standards — approximately $15 million in gross proceeds — and the offering hit the public markets at a moment when the broader biotech rally of 2020-2021 was already starting to wobble. But the S-1 told a story that is, in some ways, more interesting than the dollar figure. It revealed a company that had been running on what the kids in venture capital call "extreme capital efficiency": a sub-twenty-person headcount, an outsourced clinical operations model, and a balance sheet built to spend exactly enough to get the Phase 3 trial across the finish line and not a dollar more.

This was the lean model formalized. RenovoRx never tried to be Genentech. It tried to be the smallest possible organization that could legally and credibly run a global Phase 3 oncology study, and it leaned on contract research organizations, academic medical centers, and a tight investor base to do everything else. The S-1's risk factors, predictably, ran on for dozens of pages and included the usual incantations about going-concern doubt, dilution, and clinical-trial uncertainty. But the operating philosophy underneath was coherent: spend on the trial, not on the office.

The fourth inflection point was, in many ways, the most consequential — and also the most invisible. In March 2023, RenovoRx announced that the independent Data Safety Monitoring Board overseeing TIGAR-PAC had recommended that the trial continue as designed following a planned interim analysis.5 In biotech, that single sentence is worth more than most twenty-page press releases. A DSMB has three options at an interim look: stop for futility (because the experimental arm is clearly not working), stop for overwhelming efficacy (because the experimental arm is clearly working so well that it would be unethical to continue randomizing patients to control), or continue as designed (which translates to "we cannot tell yet, but we have not seen anything that makes us want to stop"). For a single-asset, micro-cap biotech, "continue as designed" is the news. The trial lives. The hypothesis remains testable. And the company gets to keep walking toward what may turn out to be the most important readout in its history.

In equity markets, this kind of news rarely produces a sharp re-rate, because the absence of failure is not the same as the presence of success. But fundamentally, the DSMB recommendation was the moment when TIGAR-PAC stopped being a hopeful science project and became a credible Phase 3 candidate. From that point forward, the conversation was not whether the trial would finish, but what the final data would say. Which brings us to the people charged with steering the company across that finish line.

IV. Current Management: The Shaun Bagai Era

There is a moment in many founder-led biotech stories where the company has to decide whether the same person who saw the original problem is also the right person to take the resulting product through Phase 3, FDA submission, and commercial launch. The skill sets are different. The first job rewards obsessive scientific curiosity and a willingness to chase technical white whales. The second rewards operational discipline, regulatory fluency, and the ability to write a board deck that does not put the audit committee to sleep. Most companies handle this transition badly. RenovoRx, by all available evidence, handled it methodically.

The handoff put Shaun Bagai in the CEO chair, with Dr. Ramtin Agah moving into a chief medical and scientific role on the founder side. Bagai's resume is, on its face, an unusual choice for a small oncology company. He is not a classic biopharma executive — he did not come up through Merck or Pfizer or one of the big specialty pharma operators. His background is in interventional medical devices, with operating experience at Hansen Medical and Abbott, two companies that lived at the intersection of catheter-based intervention and large-organization commercial execution.[^8]

That is the tell. If you believe, as the company's founding thesis does, that the future of oncology is about delivery rather than chemistry, then your CEO probably should not be a chemistry person. He should be a delivery person. He should know how to think about catheter design, procedural training, interventionalist adoption, and the operational realities of getting a device through the hands of a busy radiology suite. Bagai's hiring was, in effect, a doubling-down on the original thesis: the bottleneck in pancreatic cancer is not the drug, it is the truck, and we need someone who knows trucks.

Bagai's public style — visible in earnings calls, investor presentations, and interviews with outlets like Proactive — leans practical rather than visionary.6 He talks about enrollment cadence, site activation, training curricula for interventionalists, and the mechanics of FDA dialogue with the kind of unglamorous specificity that reassures institutional analysts and bores retail investors looking for breathless milestone hype. That tonal choice is itself a strategic signal: he is managing the company as if the trial outcome were knowable only by waiting, and the only useful work between now and then is to make sure the trial executes well.

Around Bagai, the management team has stayed small and stayed cheap. RenovoRx has consistently operated with fewer than twenty full-time employees through most of the post-IPO period. The model is what some lean-biotech observers call "outsourced excellence" — keep the medical, regulatory, and strategic functions inside; rent everything else. Clinical operations run through CROs. Manufacturing for the catheter system runs through specialty contract manufacturers. Site management runs through academic medical centers and a network of community oncology partners. The internal team's job is not to do the work directly but to make sure the work that gets done elsewhere is done correctly.

This has implications for the equity story. A twenty-person company that gets to a Phase 3 readout has burned an order of magnitude less capital than a typical biotech of similar clinical maturity. That changes the math on dilution, on the cost basis of long-term shareholders, and — crucially — on what a buyer would have to pay to get the asset. It also changes the math on what management has at stake. Insider ownership at RenovoRx has been reported in the high-single-digit to low-double-digit percentage range across recent proxy filings, with performance milestones tied to clinical and regulatory progress.7 That is not the eye-popping insider stake of a venture-backed founder still pre-IPO, but it is meaningfully higher than what you see at the average late-stage biotech, where founder dilution has typically washed out by Phase 3.

The risk of this lean model is concentration. Twenty people running a global Phase 3 trial means there are very few backup plans for any individual role. The reward of this lean model is alignment. There is no organizational fat to defend, no internal political faction lobbying to spin out a side program, and no large overhead to apologize for in the quarterly burn rate. When you read the 10-K, the company looks almost stark in its singularity of purpose.1 That is, depending on your temperament, either reassuring or terrifying. Either way, it is the company that exists. And it is the company that has to decide how to deploy what little capital it has.

V. M&A, Capital Deployment, & The Benchmarking

The temptation, when discussing a micro-cap biotech's "capital stack," is to walk through every secondary offering, every ATM facility, every warrant tranche, and to drown the reader in a sea of share-count footnotes. We will resist that temptation, mostly. The more interesting question is qualitative: how has RenovoRx survived this long on so little money, and what does that tell us about the structural economics of single-asset oncology development?

Start with the headline. From founding through the IPO and through the post-IPO follow-on capital raises, the cumulative amount of money RenovoRx has spent to get to a Phase 3 interim analysis is, by industry standards, almost embarrassingly small. The 2021 IPO brought in roughly $15 million; subsequent capital-markets activity has been measured in single-digit and low-double-digit millions of dollars per event, generally executed through registered direct offerings and standard at-the-market facilities.41 Compared to a typical pivotal-stage oncology asset, where total capital deployed often runs into the hundreds of millions before a single FDA filing, RenovoRx is operating in a different currency entirely.

How is this possible? Three reasons, all of which point back to the founding choices. First, the 505(b)(2) regulatory pathway lets the company reference existing safety and efficacy data on gemcitabine rather than re-running every preclinical and Phase 1 study from scratch. That collapses years of work and tens of millions of dollars of cost. Second, the orphan-disease focus means the trial population is smaller and the endpoint — overall survival in locally advanced pancreatic cancer — is brutally well-defined. There is no biomarker subtlety, no PRO scale, no novel imaging endpoint. People are alive, or they are not. Third, the lean operating model means the burn rate between clinical milestones is genuinely lean, in the low-eight-figure annualized range rather than the mid-eight-figure range you would expect for a comparable company.

For benchmarking, the natural comparable is TriSalus Life Sciences (NASDAQ: TLSI), another company built around pressure-mediated, catheter-based intra-arterial drug delivery for solid tumors. TriSalus came public through a SPAC merger in August 2023, with a different lead indication — primarily liver-directed therapy with their PEDD (Pressure-Enabled Drug Delivery) platform — and a meaningfully larger commercial footprint, including a marketed delivery device used in transarterial radioembolization procedures.8 The two companies are not direct competitors in the strict sense — different organs, different drugs, different reimbursement pathways — but they are conceptual cousins, and the market frequently looks at them through the same lens.

The benchmarking comparison is instructive. TriSalus monetized its delivery platform earlier, by attaching itself to existing radioembolization workflows and generating real device revenue while its own drug candidates moved through the clinic. RenovoRx took the harder path: tying its catheter to a specific drug as a combination product, betting that the larger therapeutic margin would justify the longer regulatory road. Whether that bet pays off depends, of course, on TIGAR-PAC.

The other instructive comparable is the broader set of small-cap oncology delivery and radiopharmaceutical companies. Galera Therapeutics is a useful, if cautionary, reference point — a company that took an interesting localized-oncology asset through a pivotal program, missed its primary endpoint, and saw its equity value collapse accordingly. That trajectory is exactly the bear case for any single-asset Phase 3 biotech, and any honest narrative on RenovoRx has to hold both possibilities in mind: the company that gets bought for north of a billion dollars after a positive readout, and the company whose equity round-trips to near-zero after a miss.

Which raises the build-versus-buy question from the other side of the table. To a strategic acquirer — Merck, Pfizer, AstraZeneca, or any of the specialty oncology operators with a position in pancreatic cancer — RenovoRx is not interesting as a corporate organization. It is interesting as a delivery platform that could extend the commercial life of off-patent chemotherapy assets, expand the indications of in-line oncology drugs, and provide a procedural anchor in a disease area where the standard of care has been frozen for years. The bolt-on math is straightforward: pay a clinical-stage premium, fold the catheter into your existing oncology sales force, and pair it with whatever else is on your shelf. The reason that math has not yet been executed is the same reason RenovoRx remains independent: the data are not in. Once the data are in, the math, in either direction, becomes very fast.

What that math will value most is not RenovoGem alone. It is the platform underneath it.

VI. The "Hidden" Business: The Platform Play

There is a temptation in single-asset biotech to treat the lead candidate as the entire investment thesis. RenovoGem hits its endpoint, the equity re-rates; RenovoGem misses, the equity is broken. That framing is not wrong — for a binary event, it is in fact the dominant framing. But it misses something that the company itself spends an increasing amount of its corporate-presentation real estate on: the platform.[^12]

The RenovoTAMP catheter does not know what drug is flowing through it. The dual-balloon, pressure-mediated delivery mechanism is, in principle, agnostic to the molecule. If it can force gemcitabine into pancreatic tumor tissue, it can probably force other small molecules, perhaps biologics, and conceivably even certain gene or cell therapies into other tumor types fed by accessible arteries. That is the platform thesis, and it is the reason the company's intellectual-property portfolio matters more than any single trial result.

The most concrete near-term platform expansion is intrahepatic cholangiocarcinoma — specifically extrahepatic cholangiocarcinoma involving the hilar bile ducts, sometimes called Klatskin tumors. Like locally advanced pancreatic cancer, hilar cholangiocarcinoma is a small-population, high-mortality disease with a poorly served standard of care and a tumor that lives at the end of an accessible arterial tree. The biological argument for pressure-mediated intra-arterial delivery in that setting is strong, and the regulatory path can leverage many of the same arguments that underpinned the pancreatic program. The company has publicly described cholangiocarcinoma as its second front in the war on hypovascular solid tumors.6

Beyond cholangiocarcinoma, the platform aperture widens. Glioblastoma. Uterine sarcomas. Certain liver metastases. Any solid tumor that can be reached by a selective arterial catheterization is, in theory, addressable. The company has been measured in its public communications about which of these indications it will pursue directly versus license out, which itself is a tell. Pursuing every indication directly would require capital RenovoRx does not have. Licensing the platform — or sub-licensing the catheter — to companies with deep pipelines of oncology assets is a financially attractive alternative that requires far less capital, although it caps the per-indication upside.

The closest historical analogy may be one drawn from a different domain entirely: the "Intel Inside" model of the 1990s. Intel did not build the best PC; it built the best processor, and convinced every PC vendor that the best processor was what mattered. The analog for RenovoRx is not subtle: build the best intra-arterial delivery system, get it embedded in oncology workflows for one or two anchor indications, and then license it to anybody with a payload worth delivering. The cancer-immunotherapy companies, the gene-therapy companies, the oligonucleotide companies — all of them face their own delivery problems, and many of them would, in principle, value a partner whose catheter is already FDA-cleared, payer-reimbursed, and trained into the muscle memory of interventional radiologists.

This is the "hidden" business, in the sense that it does not show up as a line item on the income statement and does not yet feature in segment reporting. The company does not, today, break out research-and-development spend by indication or by platform expansion versus lead-candidate maintenance. A careful reader of the 10-K can infer the rough allocation from headcount, trial budgets, and patent prosecution activity — and the inference is that the bulk of current spending still goes to TIGAR-PAC, with a meaningful and growing slice directed at platform-expansion intellectual property and exploratory studies in adjacent indications.1 In January 2024, the company announced the issuance of a new U.S. patent covering elements of the RenovoTAMP platform, reinforcing that the IP moat is being actively widened rather than left to the original founding filings.[^13]

For investors, the platform thesis has an important asymmetry baked in. If TIGAR-PAC hits its primary endpoint, the platform value rides on top of the pancreatic asset and a strategic acquirer is paying for both. If TIGAR-PAC misses, the platform value is the only thing the company has left to monetize, and the question becomes whether the IP and the procedural know-how are worth more outside the public-company structure than inside it. Either way, the catheter — not the drug — may turn out to be the most important asset on the balance sheet. That is a strange thing to say about a combination product. It is also the kind of statement that, when borne out, separates the multi-bagger biotechs from the also-rans.

VII. Strategy Analysis: 7 Powers & 5 Forces

It is fashionable, in some corners of fundamentals-driven investing, to wave away strategy frameworks as MBA wallpaper. But the truth is that a clinical-stage biotech is one of the rare businesses where Hamilton Helmer's 7 Powers framework and Michael Porter's Five Forces produce concrete, testable predictions. Let us walk through them with RenovoRx in mind.

Cornered Resource. The most defensible asset RenovoRx has is intellectual property — specifically, the family of patents around the dual-balloon, pressure-mediated intra-arterial delivery system, and the methods claims around their use in specific oncology indications. The 2024 patent issuance was a marker that this IP portfolio is being actively prosecuted and extended, not allowed to expire on its founding filings.[^13] Cornered Resource as a power requires that the resource be hard to replicate and economically meaningful when used. The catheter design checks both boxes: replicating it requires both the device engineering and the regulatory clearance, and the device is what unlocks the entire therapeutic concept.

Counter-Positioning. This is the most subtle of Helmer's powers, and the one most relevant to RenovoRx's competitive moat. Counter-Positioning exists when an incumbent cannot copy a challenger's business model without cannibalizing its existing business. For RenovoRx, the relevant incumbents are the large oncology drug makers whose existing business is built on systemic chemotherapy and systemic-administration biologics. To copy the RenovoRx model, a major chemotherapy supplier would have to encourage clinicians to switch from high-volume systemic infusions of their own drugs to lower-volume, intra-arterial regimens. The volume math hurts. Worse, the operational complexity of intra-arterial delivery — interventional radiology suites, catheter procedures, longer chair time per patient — is incompatible with the high-throughput, oncology-suite economics that systemic chemotherapy was optimized for. The big pharma incumbents are structurally disadvantaged, not because they cannot see the opportunity, but because seeing it requires undermining their own product economics.

Switching Costs. Once a hospital's interventional radiology team has been trained to perform the RenovoTAMP procedure, a procedural moat begins to form. The training time, the credentialing process, the integration with the hospital's tumor-board workflow, and the relationships with the oncology service line all create friction against switching to a different intra-arterial delivery platform — even if a competitor catheter were to emerge. This is the same dynamic that makes interventional cardiology so durable as a business: once you have trained a generation of interventionalists on a particular device family, that family enjoys a defensive perimeter that lasts years.

The remaining 7 Powers — Scale Economies, Network Economies, Process Power, and Branding — are largely absent at RenovoRx's current stage. That is not a knock; they are powers that accrue with commercial scale, and RenovoRx is not yet a commercial-scale company. They are also, importantly, the powers that a strategic acquirer would bring to the asset, which is part of why a successful TIGAR-PAC readout would so naturally invite a buyout conversation.

Now Porter. Bargaining Power of Buyers in oncology is bifurcated. On one hand, U.S. payers — both commercial and CMS — have considerable leverage on price for any therapy that does not demonstrate clear incremental survival benefit. On the other hand, the unmet need in locally advanced pancreatic cancer is so severe, and the existing standard of care so unsatisfactory, that a treatment with a credible survival benefit would face relatively little pricing pressure. The buyer's power, in other words, is constrained by the absence of alternatives.

Threat of Substitutes is more nuanced. The current standard of care is systemic combination chemotherapy — most commonly FOLFIRINOX or gemcitabine combined with nab-paclitaxel — and any improvement on that standard has to either outperform it on overall survival or match it with materially lower toxicity. The looming long-term substitutes are the cancer vaccine modalities, including mRNA-based personalized neoantigen vaccines that several large players are advancing in pancreatic cancer. Those vaccines, if successful, would address a fundamentally different mechanism (immune activation rather than direct cytotoxicity) and might in fact be complementary rather than substitutive — delivered systemically while RenovoTAMP delivers cytotoxic regimens locally.

Threat of New Entrants is moderated by the regulatory moat and the IP moat. Building a competing intra-arterial delivery platform is technically feasible but takes years and tens of millions of dollars before clinical proof-of-concept, and any new entrant would face the same set of patents and the same set of clinical-trial timelines.

Bargaining Power of Suppliers is largely irrelevant. Gemcitabine is a generic, multi-sourced commodity. Catheter components are sourced from established medical-device contract manufacturers. There is no single chokepoint supplier that can squeeze RenovoRx's economics.

Rivalry Among Existing Competitors is the most interesting line. TriSalus is the closest direct rival on platform philosophy, but the indication overlap is small. The dominant rivalries, instead, are between RenovoRx's combination product and the existing standard-of-care systemic regimens, and between RenovoRx and any future intra-arterial entrant that might come down the regulatory pipeline. For now, the field is sparse. That sparseness is itself a kind of opportunity — and a kind of warning, since it means the company has not had the benefit of competitors validating the category for payers and clinicians.

The net of the framework analysis is that RenovoRx, on paper, has plausible Cornered Resource and Counter-Positioning powers, a developing Switching Cost moat, and a generally favorable Porter posture in the specific niche of locally advanced pancreatic cancer. None of which matters if the trial misses. All of which matters enormously if it hits.

VIII. Playbook: Business & Investing Lessons

Step back from RenovoRx the equity and look at RenovoRx the case study. Three lessons emerge that generalize well beyond pancreatic cancer.

Lesson 1: The "Pick and Shovel" of Bio. The history of medicine is littered with new molecules that failed to reach the right place in the body. The history of medicine is also littered with companies that got rich by building better ways to get existing molecules where they needed to go. Pumps, pens, catheters, inhalers, slow-release implants — the delivery infrastructure of medicine has, over decades, generated as much shareholder value as the molecules themselves. RenovoRx is, in its essence, a pick-and-shovel play on cancer chemotherapy. It is not trying to invent a new drug. It is trying to do something that, from the outside, sounds modest — make the existing drug work better — but that, in practice, may produce more clinical value than the next generation of molecular discoveries.

The pick-and-shovel framing matters because it changes how an investor should think about competitive risk. New-drug biotechs face competition from every other new-drug biotech working on the same disease, plus the constant risk that a different mechanism of action proves superior. A delivery-platform biotech faces a narrower competitive set: other delivery platforms in the same anatomical niche, of which there are usually very few. The result is that delivery companies, when they succeed, often end up with surprisingly durable market positions — and when they are acquired, often command surprisingly large multiples relative to the capital they consumed.

Lesson 2: Regulatory Arbitrage. The 505(b)(2) pathway is one of the great underappreciated features of the FDA system. It lets a sponsor build a new therapy on top of existing approved drug data — pairing the established safety profile of an old molecule with a novel delivery, dose, or indication. For RenovoRx, this was the difference between a feasible Phase 3 program and an impossible one. They did not have to re-prove that gemcitabine is a chemotherapy. They had to prove that intra-arterial gemcitabine delivered via RenovoTAMP works better than the standard of care in a specific indication. That is still a hard problem. But it is a much narrower problem than "develop a new pancreatic cancer drug from molecule to market."

The general lesson is that regulatory pathways are not all equally expensive, and choosing the right one is a strategic decision that compounds over years. For founders, the path-selection conversation is sometimes more important than the molecule-selection conversation. For investors, the path is a signal — both about the kind of company you are buying and about the time and capital horizon to a meaningful catalyst.

Lesson 3: The Perils of the "Binary Event." Every Phase 3 single-asset biotech is, at its core, a leveraged bet on a single statistical readout. The stock lives and dies by the p-value. There is no diversification benefit, no smoothing of revenue, no operating cash flow to fall back on. This is both the appeal and the danger of micro-cap clinical-stage equity. The appeal is that, in the event of success, the re-rate can be five-fold, ten-fold, or more, often in a single trading session. The danger is that, in the event of failure, the equity can lose ninety percent of its value just as quickly.

The honest investing lesson is not "avoid binary events." It is "size them appropriately, understand them deeply, and never confuse the breadth of the platform thesis with the binary nature of the near-term catalyst." A company can have a brilliant long-term platform and still be wiped out by a single failed pivotal trial, because the platform's value depends on the credibility provided by the lead asset's approval. RenovoRx illustrates this with painful clarity: the platform is broad, the patents are real, the IP is being extended, the management is disciplined. None of it survives, in equity-market terms, an outright TIGAR-PAC miss without years of additional work and additional capital. The lesson is to enter such positions with both eyes open about which scenarios are which.

These three lessons, taken together, point toward an investing framework: prefer delivery-platform stories with regulatory arbitrage and platform optionality, but size them as binary events, because at the pivotal-trial stage that is what they are. With those lessons in hand, we can finally weigh the case.

IX. Analysis & The Bear vs. Bull Case

There is a particular type of conversation that happens, late at night, in the offices of healthcare-focused hedge funds before a major biotech readout. The portfolio manager wants to know two things from the analyst. What is the case for this trial succeeding, and what is the case for it failing — and not "what does the company say," but what does the data actually say, what does the trial design imply, and what are the things that could go wrong that are not in the press release. The exercise of articulating both cases honestly is the only way to size the position. So let us do that.

The Bull Case. TIGAR-PAC hits its primary endpoint on overall survival in locally advanced pancreatic cancer. The magnitude of the survival benefit is clinically meaningful — perhaps a several-month improvement on median overall survival, with a hazard ratio that translates into a clear story for the FDA and for treating oncologists. Following that readout, RenovoRx files for FDA approval under the 505(b)(2) pathway. Approval is not assured — it never is — but the combination of orphan-drug status, an Phase 3 trial with a credible endpoint, and a severely underserved indication makes the case favorable. Approval is followed, in this scenario, either by an aggressive commercial launch in the United States or by an acquisition.

The acquisition story is what most analysts focus on, because it is what produces the biggest delta in shareholder value. A successful Phase 3 readout in pancreatic cancer would, plausibly, draw acquisition interest from any oncology operator with an interest in expanding their pancreatic franchise or in establishing a delivery-platform position. The deal economics could comfortably reach into the high hundreds of millions or the low billions, especially if the platform extension into cholangiocarcinoma and other indications is factored in. Given that RenovoRx has lately traded at micro-cap valuations a small fraction of those numbers, the asymmetry, in the bull case, is dramatic.

There is a softer version of the bull case, too. Even without an immediate acquisition, a TIGAR-PAC win would give RenovoRx the ability to raise capital on much more favorable terms, partner the cholangiocarcinoma program with a larger oncology player, and begin generating real revenue from RenovoGem under the orphan-drug exclusivity window. The equity in this softer bull case probably does not 20x — but it does meaningfully re-rate and provide the basis for a real, growing therapeutics business.

The Bear Case. The first and most obvious bear case is that the trial misses its primary endpoint. There are many ways this can happen. The control arm — patients receiving continuation of systemic standard-of-care chemotherapy — could perform better than expected, narrowing the survival gap between treatment groups and leaving the experimental arm without a statistically significant benefit. This is, in fact, one of the more common ways oncology trials fail: not because the experimental therapy did nothing, but because the comparator did more than the historical literature suggested it would.

A second bear-case path is partial efficacy. The trial could show a statistical signal that is too modest to drive regulatory approval, or that splits awkwardly between subgroups. The FDA could ask for an additional confirmatory study. The clinical community could greet the results with the kind of skepticism that crushes commercial uptake even if the regulatory checkbox is technically met. Each of these outcomes is, in equity terms, very nearly as bad as an outright miss.

A third bear-case path is the procedural-adoption problem. Even if the data are excellent, the RenovoTAMP procedure is not a simple intravenous infusion. It requires an interventional radiology suite, a trained operator, and a reasonably willing referral pipeline from medical oncology to interventional radiology. Adoption could prove slow — particularly in community oncology settings, which is where most U.S. pancreatic cancer patients are actually treated. A scenario where the trial wins but commercial uptake disappoints is plausible, and would translate into an underwhelming acquisition multiple and a longer, more dilutive road to profitability.

A fourth bear-case path is competitive. Pancreatic cancer is a field that has frustrated drug developers for decades, but it is also a field that draws constant new investment. mRNA-based personalized vaccines, novel chemotherapy combinations, and KRAS-targeting small molecules are all advancing, and any of them could reshape the standard of care between now and RenovoGem's commercial maturity. RenovoRx's specific delivery platform might remain valuable in such a future, but its lead indication and its negotiating leverage in any acquisition could erode.

The Valuation Gap. Through much of the post-IPO period, the market has treated RenovoRx as a "broken IPO" — an equity that priced in 2021 expectations and has since spent years grinding downward despite the company actually advancing clinically. The gap between clinical progress and market capitalization is the kind of disconnect that produces both opportunity and risk. The opportunity is that, if the bull case plays out, the rerate is starting from a depressed base. The risk is that the market may be implicitly pricing not just clinical uncertainty but operational uncertainty about whether the company can complete the trial, secure the capital, and execute on approval and launch — and the market is often right about such things, even when individual investors disagree.

Myth vs. Reality. A persistent retail narrative around RenovoRx frames it as a near-certain acquisition target — "big pharma will buy this no matter what." The reality is more nuanced. Big pharma acquires companies that have either approved products with growing revenue, or pivotal-stage assets with high-quality data and a clear regulatory path. They do not typically acquire micro-cap clinical-stage biotechs out of strategic charity. The acquisition thesis is contingent on the data. The data are contingent on the trial. The trial is contingent on enrollment, retention, and execution. The story is real, but the chain of contingencies between today and the acquisition is longer than the bull case sometimes acknowledges.

A second persistent narrative — this one on the bearish side — frames RenovoRx as a "perpetual capital raise" with no real underlying asset. The reality, again, is more nuanced. The company has been disciplined in its capital deployment by micro-cap biotech standards, the trial has cleared a meaningful interim hurdle, and the IP portfolio has been actively extended. Cynicism about micro-cap biotech as a category is sometimes correctly applied here; sometimes it is lazily applied here. The honest answer is that the equity is what the trial outcome decides.

Key KPIs to Track. For an investor following this story over the next several quarters, three metrics matter most. First, TIGAR-PAC enrollment completion and event accrual — because the primary endpoint is overall survival, the trial is event-driven, and the timing of the readout depends on how many events have accrued, not just on how many patients are enrolled. Second, cash runway — quarterly cash balance disclosed in the 10-Q, combined with operating burn, tells you when the next dilutive raise is likely and on what terms. Third, platform-expansion signals — any disclosure on cholangiocarcinoma study initiation, additional patent issuances, or partnership announcements is a tell on whether the platform thesis is being executed in parallel with the lead asset.

These are the three numbers that, between now and the TIGAR-PAC readout, would actually move the equity's fundamental story. Everything else is, in the kindest reading, supporting context.

X. Epilogue & Outro

It is worth ending where we began — with the brick wall. Pancreatic cancer remains, in May 2026, one of the great unsolved problems in oncology. Survival has crept upward in tiny increments, the standard of care has barely shifted in a decade, and the disease continues to claim tens of thousands of Americans each year. Any company that proposes a meaningful improvement on that standard of care deserves to be taken seriously. Any company that proposes such an improvement at the operating scale of fewer than twenty people, with a cumulative capital deployment in the tens of millions of dollars, deserves to be taken seriously and studied carefully.

RenovoRx is, in many ways, the archetype of the modern lean-biotech model. The company has compressed an enormous amount of clinical and intellectual-property work into a tight organization, leaned on regulatory arbitrage to make a Phase 3 program economically feasible, and built a platform whose downstream optionality has yet to be priced into the equity. Whether that compression is rewarded depends on a single trial in a single indication, with a readout whose timing remains a function of event accrual rather than calendar guidance.

For long-term fundamental investors, the most interesting thing about the story is not the binary nature of the next data readout. It is the way the company has set up its business so that, in the success case, the platform is the prize, not just the pancreas. RenovoTAMP — if it works — could become the kind of asset that gets quietly licensed into a half-dozen oncology programs across as many companies, generating royalty streams and equity participation that would dwarf the revenue of any single drug. That is the long-term view, and it is the view that distinguishes RenovoRx the platform story from RenovoRx the binary-event story.

The next places to watch are well known. The TIGAR-PAC primary endpoint readout. Any update on cholangiocarcinoma study design. Continued patent prosecution activity. Analyst initiations beyond the existing small-cap coverage.[^14] Each of these will, in its own way, sharpen the picture of whether the lean-biotech bet has paid off — or whether the brick wall of pancreatic cancer remains, for now, exactly what it has always been.

Either way, the story is worth telling. And the next chapter is being written, one event, one patient, and one data point at a time.

References

-

RenovoRx 2023 Annual Report (Form 10-K) — SEC Filing, 2024-03-28 ↩↩↩↩↩

-

ClinicalTrials.gov: TIGAR-PAC Study (NCT03257020) — National Institutes of Health ↩

-

RenovoRx IPO Prospectus (Form S-1) — SEC Filing, 2021-08-26 ↩↩

-

RenovoRx Announces Positive Outcome of Planned Interim Analysis in Phase 3 TIGAR-PAC Clinical Trial — GlobeNewswire, 2023-03-14 ↩

-

RenovoRx CEO Shaun Bagai Interview on Platform Expansion — Proactive Investors, 2023-11-20 ↩↩

-

RenovoRx 2023 Annual Report (Form 10-K) — SEC Filing, 2024-03-28 ↩

-

Comparison: TriSalus Life Sciences vs RenovoRx — Seeking Alpha Analysis, 2023-12-05 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube