RingCentral: The Cloud Communications Revolution

I. Introduction and Episode Roadmap

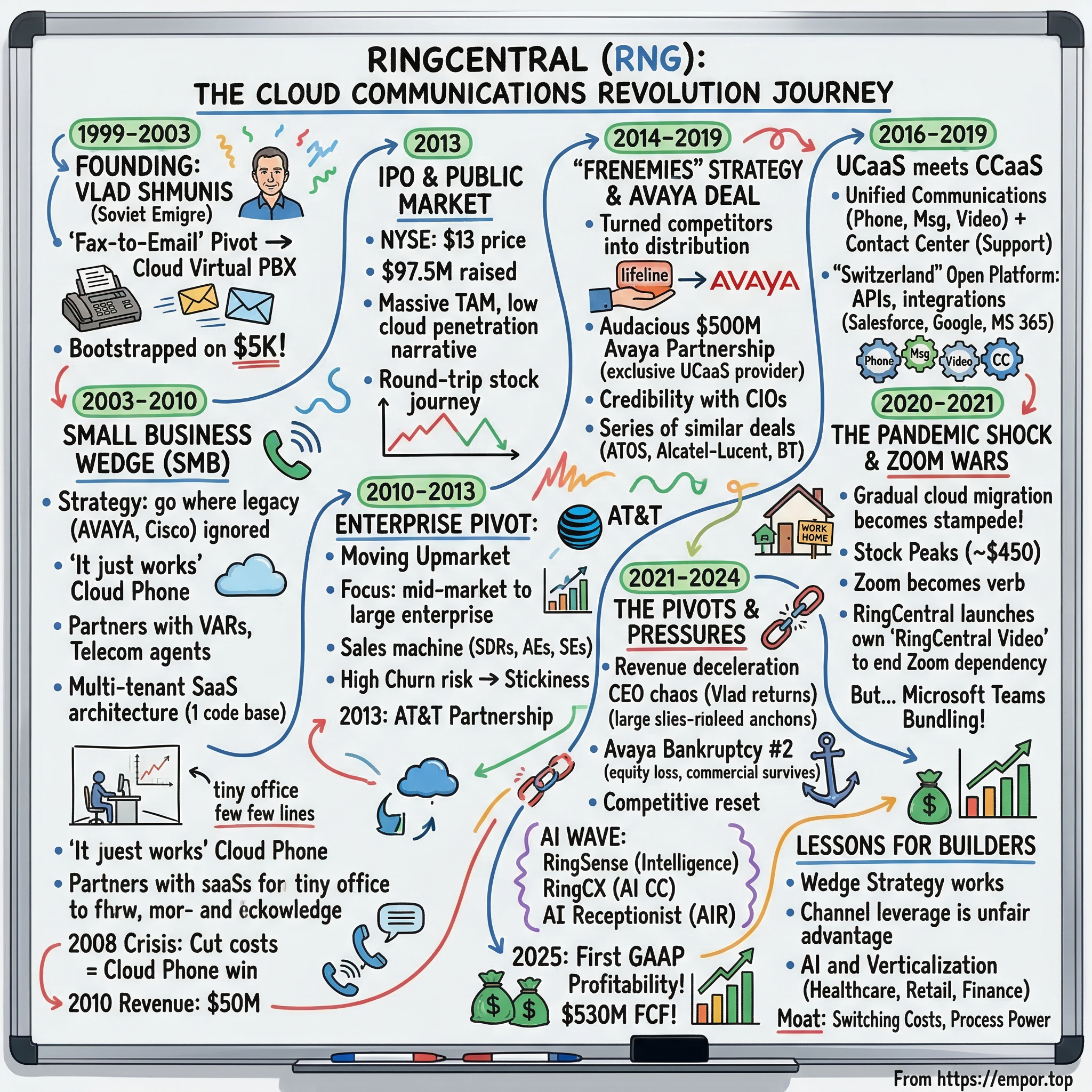

Picture this: It is 1999, the dot-com bubble is inflating to absurd proportions, and a Soviet emigre named Vlad Shmunis is sitting in a modest office in the San Francisco Bay Area, trying to sell businesses on the idea of sending faxes over the internet. Faxes. In an era when everyone was chasing portals, eyeballs, and e-commerce. The idea seemed almost quaint, like selling better typewriter ribbons while the world was discovering word processors.

Fast forward to today. That fax-to-email company became RingCentral, a cloud communications juggernaut generating over $2.5 billion in annual revenue, serving hundreds of thousands of businesses worldwide, and holding the title of pioneer in what the industry now calls Unified Communications as a Service, or UCaaS. The company trades on the NYSE under the ticker RNG, and while its stock has had one of the most dramatic round-trip journeys in all of SaaS — from a $13 IPO to nearly $450 at its pandemic peak, then back down to the mid-$30s — the underlying business has never been stronger. RingCentral achieved GAAP profitability for the first time in 2025, generating over $530 million in free cash flow.

The big question that makes this story worth telling is deceptively simple: In a world dominated by Microsoft Teams, Zoom, and Cisco, how did RingCentral carve out and defend a multi-billion dollar position in one of the most competitive markets in enterprise technology? The answer involves platform shifts, enterprise sales mastery, one of the most audacious partnership strategies in tech history, and a masterclass in what Clayton Christensen called the innovator's dilemma — except in this case, RingCentral was the innovator, and it had to keep innovating even as the ground shifted beneath it.

This story is really about four interconnected themes. First, how to exploit a platform shift — specifically, the migration from on-premise hardware to cloud software in business communications. Second, how to build an enterprise sales machine from scratch, starting with the smallest businesses and methodically moving upmarket. Third, how to turn your competitors into your distribution channels, which is one of the most counterintuitive strategic moves in modern tech. And fourth, how to survive when a company two orders of magnitude larger than you decides to bundle your product for free.

For anyone building in crowded markets, investing in enterprise software, or trying to understand what happens when an unstoppable force — Microsoft's bundling strategy — meets a movable but remarkably sticky object — RingCentral's installed base — this story has lessons that extend far beyond telecom.

There is also a deeply human thread running through this story — the journey of a Soviet emigre who arrived in America as a teenager, built and sold his first technology company, and then spent a quarter century building a second one through dot-com busts, financial crises, pandemics, and the most competitive market in enterprise software. It is a story about persistence, pragmatism, and the willingness to reinvent.

Let us start at the beginning, with a world of tangled phone cables, expensive PBX boxes, and a telecom industry that was begging to be disrupted.

II. The Telecom Industry Before the Cloud

To understand why RingCentral exists and why it mattered, you first need to understand just how terrible business phone systems were in the late 1990s and early 2000s. Not mildly inconvenient — genuinely, absurdly terrible.

The dominant paradigm was the Private Branch Exchange, or PBX. Think of a PBX as a private telephone switching system that sat in a company's server room — or more often, a dusty closet — and routed calls between employees and the outside world. The market was controlled by a handful of legacy giants: Avaya, Nortel, Cisco, Mitel, and a few others. These companies sold hardware boxes that cost tens of thousands to hundreds of thousands of dollars, required specialized technicians to install and maintain, and locked customers into multi-year contracts with proprietary equipment that could not talk to competing systems.

For a mid-sized business with, say, 200 employees, getting a new phone system installed was a capital expenditure project that could easily run $50,000 to $200,000 upfront, plus ongoing maintenance contracts, plus the cost of dedicated IT staff or outside consultants to manage it. Adding a new employee meant physical wiring. Opening a new office meant buying an entirely new PBX box. Moving to a different building was a nightmare. And heaven help you if Nortel — which controlled about a third of the market — went bankrupt. Which, as it happened, Nortel did in 2009, stranding millions of business customers on orphaned hardware.

The economics were terrible for buyers and wonderful for the incumbents. Avaya alone generated billions in annual revenue, with gross margins north of 60%, largely from maintenance contracts on installed hardware that customers could not easily rip out. It was the definition of vendor lock-in, and the telecom incumbents loved it. Think of it like the mainframe era of computing — a small priesthood of specialists controlled the technology, ordinary users had no visibility into what they were paying for, and the vendors had no incentive whatsoever to make things simpler or cheaper.

The maintenance contract racket deserves special attention because it explains why the incumbents were so slow to embrace the cloud. When Avaya or Cisco sold a PBX system, the upfront hardware sale was profitable, but the real money came from the ongoing maintenance and support contracts that customers were essentially forced to buy. These contracts typically ran 15-20% of the initial hardware cost per year, every year, for as long as the equipment was in service. For an industry with tens of millions of installed PBX lines, this represented a river of recurring revenue that flowed regardless of whether the vendor did anything to improve the product. Why would you cannibalize that annuity by offering a cloud alternative?

Then came Voice over Internet Protocol — VoIP. The basic idea was elegant: instead of routing calls over dedicated telephone circuits, why not convert voice into data packets and send them over the internet, just like email? Companies like Vonage launched in the early 2000s targeting consumers with cheap internet phone calls. Skype, founded in 2003, became a sensation by offering free computer-to-computer calling. The promise was obvious: voice was just data, data could travel over the internet, and the internet was getting faster and cheaper every year.

But here is why most VoIP 1.0 companies failed or stayed small, and why this matters for understanding RingCentral's later success: they were solving the wrong problem for the wrong customer. Vonage went after consumers with a slightly cheaper alternative to their home phone line — a product that was already dying as mobile phones proliferated. Skype was great for international calls and casual video chats, but it was not a replacement for a business phone system. It could not handle call routing, auto-attendants, voicemail management, compliance recording, or any of the hundred other features that enterprises required.

The real opportunity — the massive one hiding in plain sight — was not cheaper phone calls. It was replacing the entire PBX infrastructure with software running in the cloud. A business phone system that required no hardware, no installation, no maintenance contracts, and no specialized IT staff. One that scaled instantly when you added employees, worked identically across multiple offices, and cost a predictable monthly fee instead of a massive upfront capital expenditure.

To appreciate the scale of this opportunity, consider the numbers. By the mid-2000s, there were an estimated 500 million business phone lines worldwide. The total addressable market for business communications — including hardware, software, services, and connectivity — was measured in the hundreds of billions of dollars. And virtually all of it was running on technology architectures designed in the 1980s and 1990s, before the internet was a commercial reality.

The incumbents saw this coming and did absolutely nothing about it, because their entire business model depended on selling and maintaining expensive hardware. This was the classic innovator's dilemma, and it was about to play out in textbook fashion. Into this void stepped a company that most of the telecom industry had never heard of — and would not take seriously for another decade.

III. Founding Story: Vlad Shmunis and the Fax Pivot (1999-2003)

Vlad Shmunis was born in Odessa, Ukraine, when it was still part of the Soviet Union. His father Gregory was a mechanical engineer, his mother Svetlana an electrical engineer. The family was Jewish, and in the 1970s, with the help of Jewish family service organizations, they emigrated to the United States, arriving in San Francisco when Vlad was about fourteen years old. He attended public high school, graduated at sixteen, and went on to San Francisco State University, where he earned both a bachelor's and master's degree in computer science, graduating magna cum laude.

What happened next reveals the thread that would eventually lead to RingCentral. In 1992, Shmunis founded a company called Ring Zero Systems — note the naming pattern — which made desktop business communications software. Ring Zero shipped over 25 million copies of its phone and fax communication software through OEM partnerships with IBM, HP, Sony, and Toshiba. In 1998, Motorola acquired Ring Zero for a deal reportedly in the double-digit millions. At thirty-something years old, Shmunis had already built and sold a successful communications technology company. He understood the plumbing of how businesses communicated, and he understood that the internet was about to change everything about that plumbing.

In March 1999, Shmunis co-founded RingCentral alongside Vlad Vendrow, who had been Ring Zero's Director of Engineering. Vendrow would serve as Chief Technology Officer from day one and would go on to accumulate over 40 patents in unified communications technology. The founding team also included Dawn Adachi and Eliza Auyeung.

The initial product was a cloud-based virtual PBX service aimed at small businesses, bundling business phone numbers, auto-attendants, voicemail-to-email, and cloud fax capabilities. The fax-to-email component was a significant piece of the early value proposition. In 1999, small businesses were still sending and receiving enormous volumes of faxes, and the idea that you could receive a fax as an email attachment — without owning a fax machine — was genuinely compelling.

But here is the crucial insight that separated Shmunis from the dozens of other fax-to-email startups that launched around the same time: he recognized almost immediately that fax was a transitional product. The real prize was hosting the entire business phone system in the cloud. The fax capability got small businesses in the door, but the phone system was what would keep them and generate meaningful recurring revenue.

RingCentral launched its cloud business phone service in 2003. The technical challenges were substantial, and this is worth dwelling on because they explain why so few companies successfully made this transition. Voice traffic is fundamentally different from web or email traffic. When you load a webpage, a delay of a few hundred milliseconds is imperceptible. When you are having a phone conversation, a delay of even 150 milliseconds creates an awkward echo effect, and packet loss of more than 1% makes the conversation unintelligible. Cloud-based voice required solving what engineers call the "last mile" problem — ensuring that voice packets traveled from RingCentral's servers through the public internet to the customer's office with the same reliability that the old copper telephone network had provided for a century.

The team had to build carrier interconnects, optimize codecs — the algorithms that compress and decompress voice data — for last-mile quality, and create monitoring systems to detect and route around network congestion in real time. They built redundant paths through multiple internet service providers and deployed servers in geographically distributed data centers to minimize the distance that voice packets had to travel. It was deeply unglamorous work compared to the consumer internet companies grabbing headlines, but it was the foundation that everything else would be built on.

The timing was everything. Broadband penetration in the United States crossed the 50% threshold for households around 2004-2005, and business broadband adoption was even further ahead. SIP — the Session Initiation Protocol that standardized how voice calls were set up over the internet — was maturing. And Amazon Web Services launched in 2006, beginning the broader shift toward cloud computing that would make RingCentral's model seem less radical and more inevitable.

Perhaps the most remarkable aspect of the early years was this: RingCentral reportedly started with as little as $5,000 in initial capital. And the company operated without institutional venture capital for seven years, from 1999 through 2006. In an era of spectacular dot-com excess, when companies were burning through tens of millions in venture funding before generating a dollar of revenue, Shmunis bootstrapped his company through the bubble, the crash, the recession, and the slow recovery, building real revenue from real customers paying real monthly subscriptions. This was not a growth-at-all-costs story. This was an immigrant entrepreneur's story — methodical, frugal, and focused on building something that actually worked.

IV. The Small Business Wedge (2003-2010)

The strategic genius of RingCentral's early go-to-market approach can be summed up in one principle: go where the incumbents refuse to look. Avaya, Cisco, and Nortel were selling six-figure deals to enterprises with thousands of employees. They had sophisticated direct sales forces, complex implementation teams, and massive profit margins on hardware. A dentist's office with five phone lines? A real estate agency with twelve agents? A restaurant chain with twenty locations? These customers were invisible to the PBX giants — too small to justify the sales cost, too price-sensitive to afford the hardware, and too unsophisticated to manage the technology.

RingCentral targeted exactly these businesses. The economics were irresistible. Instead of spending $50,000 or more on a PBX system, a small business could get a fully featured cloud phone system for $20 to $40 per user per month. No hardware to buy. No installation appointments to schedule. No IT staff to hire. Sign up online, plug in some phones — or just use your computer — and you had a professional business phone system with auto-attendants, voicemail, call routing, and conference calling. For a ten-person office, that was roughly $200 to $400 per month versus a $50,000 capital outlay. The math sold itself.

The channel strategy was equally shrewd. Rather than building an expensive direct sales force to reach millions of small businesses — an approach that would have been prohibitively expensive — RingCentral partnered with telecom agents and Value-Added Resellers, or VARs. These were the same people who were already selling internet connections, phone lines, and IT services to small businesses. RingCentral gave them a recurring commission for every customer they brought in, turning thousands of independent sales agents into an extended salesforce that cost RingCentral nothing until a deal closed.

The product philosophy was relentlessly focused on simplicity. The mantra was essentially "it just works." While competitors loaded their products with complex features aimed at enterprise IT administrators, RingCentral designed its interface for a small business owner who might also be the receptionist, the IT department, and the CEO. Features that enterprise products buried in configuration menus were exposed as simple toggles. Setup that enterprise vendors quoted in weeks was measured in minutes.

Competition existed — 8x8, Vonage Business, and a constellation of regional hosted PBX providers were chasing similar customers. But RingCentral's combination of product simplicity, channel leverage, and cloud-native architecture gave it an edge.

The architecture point deserves emphasis because it had enormous long-term consequences. RingCentral was building a truly multi-tenant platform, meaning every customer — whether a five-person law firm or a 500-person retailer — ran on the same infrastructure, the same code base, the same version of the software. When the engineering team shipped an improvement or a new feature, it was available to every customer simultaneously. This is the fundamental advantage of true SaaS, and it sounds obvious in retrospect, but in the early 2000s many competitors were taking a different approach: they were running modified versions of traditional PBX software in data centers, essentially hosting on-premise systems in the cloud. This "hosted" model created per-customer complexity — different versions, different configurations, different maintenance schedules — that limited their ability to scale and made every new feature deployment a project rather than a switch flip. RingCentral's architectural bet on multi-tenancy would prove decisive as the company scaled from thousands to hundreds of thousands of customers.

The 2008 financial crisis, which devastated many startups, actually helped RingCentral. Small businesses that had been on the fence about their phone systems suddenly had intense pressure to cut costs. A cloud phone system with no upfront capital expenditure and a predictable monthly bill was exactly what a cash-strapped business needed. While competitors that depended on capital-intensive sales cycles struggled, RingCentral's subscription model generated steady monthly recurring revenue.

By 2010, the company had reached $50.2 million in annual revenue — still small by tech standards, but growing at a rate that attracted serious attention. When Sequoia Capital and Khosla Ventures invested approximately $12 million in 2006-2007, it was validation from two of Silicon Valley's most prestigious venture firms. Additional rounds followed, but the company remained remarkably capital-efficient, having built a real business on real revenue before ever taking institutional money.

The infrastructure moat was also taking shape. RingCentral was building out its own data center presence, establishing direct carrier relationships with major telecommunications providers, and investing heavily in reliability. For a business, the phone system is arguably the most mission-critical piece of technology — if email goes down for an hour, it is annoying; if the phones go down for an hour, you are losing customers and revenue in real time. RingCentral's ability to deliver carrier-grade reliability — the famous "five nines" of 99.999% uptime — from a cloud platform was a genuine technical achievement and a competitive differentiator that would become increasingly important as the company moved upmarket.

V. The Enterprise Pivot: Moving Upmarket (2010-2013)

By 2010, RingCentral faced a strategic inflection point that every successful SMB-focused company eventually confronts. The small business market was enormous in aggregate but brutally fragmented. Customer acquisition costs were high relative to the low per-customer revenue. Churn rates were elevated because small businesses failed, changed direction, or simply were not sophisticated enough to fully adopt the platform. And the market was attracting more competitors every quarter, putting pressure on pricing.

The enterprise market — companies with hundreds or thousands of employees — offered everything the SMB market did not: larger deal sizes, lower churn rates, higher willingness to pay for premium features, and the kind of logos that attracted other enterprise customers. But it also presented challenges that had defeated many companies before. Enterprise buyers demanded security certifications, compliance features, and SLA guarantees. They needed integrations with their existing technology stacks — Salesforce, Microsoft Office, SAP. They required multi-site support, global coverage, and the ability to handle complex call routing scenarios with thousands of extensions.

Most critically, selling to enterprises required an entirely different go-to-market motion. Small businesses bought phone systems the way they bought office supplies — quickly, based on price and simplicity. Enterprises bought phone systems the way they bought ERP systems — slowly, through a process involving RFPs, proof-of-concept deployments, security reviews, legal negotiations, and approval from multiple stakeholders including IT, procurement, finance, and the C-suite. A typical enterprise deal cycle could stretch six to eighteen months, and losing at any stage of the process meant starting over with a different prospect. The economics were attractive — enterprise deals could be worth hundreds of thousands or even millions in annual recurring revenue — but the sales cost and cycle time were an order of magnitude higher than SMB.

The challenge was compounded by the fact that enterprise IT departments were, understandably, deeply skeptical of entrusting their most mission-critical communication infrastructure to a cloud startup. When a hospital's phone system goes down, patients cannot reach the emergency department. When a financial trading floor loses phone connectivity, millions of dollars in trades can be lost. Enterprise buyers were not just evaluating features and price — they were evaluating existential risk.

RingCentral made the bet that it could make this transition, and the vehicle was the enhanced RingCentral Office product — an all-in-one cloud platform that combined PBX capabilities with meetings, messaging, and collaboration features. The architectural decisions that Shmunis and Vendrow had made from the very beginning — building a true multi-tenant cloud platform rather than hosting traditional PBX software — now paid enormous dividends. Adding enterprise features did not require building a separate product or platform; it meant extending the same platform with the security, compliance, and administration capabilities that large organizations required.

Revenue during this period tells the story of a company investing aggressively for growth. Revenue grew from $50 million in 2010 to $79 million in 2011 to $114.5 million in 2012 — growth rates of 57% and 45% respectively. But net losses also widened, from $7.3 million to $13.9 million to $35.4 million, as the company built out its enterprise sales organization.

A pivotal hire came in June 2013 when RingCentral brought on David Berman as President. Berman was a veteran of Cisco's WebEx division, where he had served as President. He understood the enterprise collaboration market intimately — the buyer personas, the sales cycles, the competitive dynamics — and his appointment signaled that RingCentral was serious about competing at the highest levels of enterprise technology. His immediate mandate was to either prepare the company for an IPO or position it for acquisition, and to accelerate the enterprise sales motion.

The company began hiring enterprise sales veterans from Oracle, Cisco, and Salesforce, building out the full inside-outside sales model that is standard in enterprise SaaS: Sales Development Representatives to qualify leads, Account Executives to run deal cycles, and Solutions Engineers to provide technical validation. It was expensive, it was complex, and it took years to tune — but once the machine was running, it became one of RingCentral's most durable competitive advantages.

By the time of the IPO filing, RingCentral served over 300,000 businesses and had secured a partnership with AT&T — one of the largest telecommunications companies in the world — to distribute its cloud phone service. The AT&T partnership was particularly significant because it provided instant credibility with enterprise CIOs who might have been skeptical of a relatively unknown cloud startup. If AT&T was willing to put its name on the product, it had to be enterprise-grade. The company was ready for Wall Street.

VI. The IPO and Public Markets Journey (2013)

The morning of September 27, 2013, Vlad Shmunis stood on the trading floor of the New York Stock Exchange and watched as RingCentral went public at $13 per share. The company sold 7.5 million shares, raising $97.5 million in fresh capital. The market liked what it saw — shares opened at $17.51, a roughly 35% pop above the offering price, giving the company an initial public market valuation of approximately $887 million, or about 6.9 times its trailing year revenue of $114.5 million.

The narrative to Wall Street was bold and simple: enterprise cloud communications represented one of the largest untapped markets in all of technology. The global business phone system market was measured in the hundreds of billions of dollars, the vast majority of it still running on legacy on-premise hardware. Cloud penetration was in the low single digits. RingCentral was the leader in the migration from old to new, and the migration had barely begun. It was the classic SaaS pitch — massive TAM, low penetration, land-and-expand dynamics — applied to a market that every company in the world participated in because every company needed phones.

The early years as a public company were not without turbulence. Growth stocks in general, and SaaS companies specifically, faced periodic bouts of skepticism from investors worried about the path to profitability. RingCentral was growing revenue rapidly but losing money on a GAAP basis, investing heavily in sales and marketing and R&D. Competitors were multiplying. And the specter of Microsoft — which was already beginning to integrate communications features into its Office suite — loomed as an existential question that analysts raised on virtually every earnings call.

RingCentral learned to speak Wall Street's language fluently. The company began emphasizing metrics that demonstrated the quality and durability of its revenue: net dollar retention rates above 100%, meaning existing customers were spending more each year even before accounting for new customer additions; the Rule of 40, which combines revenue growth and profitability margins to measure the health of a SaaS business; and enterprise customer counts, showing the steady march upmarket toward larger, stickier, more profitable customers.

The stock performance over the next eight years told one of the great SaaS wealth creation stories. From its $13 IPO price, RNG shares climbed steadily through the mid-2010s, then accelerated dramatically as the market recognized the scale of the enterprise cloud communications opportunity. Revenue grew from $114 million in 2012 to over $900 million in 2019 — roughly doubling every two to three years. The company crossed the 300,000-customer mark, then pushed steadily upmarket, with enterprise customers becoming an increasingly large share of the mix. Before the pandemic supercharged everything, the stock was already trading above $200 — more than fifteen times the IPO price.

There is a subtler lesson here about the relationship between SaaS companies and the public markets. Unlike traditional technology companies that sold perpetual licenses — booking a large upfront revenue number but then needing to sell again next quarter — SaaS companies like RingCentral were building a revenue base that compounded. Each new customer added to a growing stream of recurring revenue, and as long as existing customers stayed and expanded, the revenue base grew even if new customer acquisition slowed. This "snowball" dynamic made SaaS companies uniquely suited to the public markets, where investors could model future revenue with higher confidence than in traditional software.

What the public markets taught RingCentral was that in enterprise SaaS, the narrative matters almost as much as the numbers. Investors needed to believe not just in this quarter's results but in a multi-year vision of market transformation. Shmunis and his team delivered that vision consistently, quarter after quarter, year after year. The biggest test of that narrative — and the most controversial strategic bet — was about to arrive in the form of an unlikely partnership.

VII. The Avaya Partnership: Frenemies at Scale (2014-2019)

The Avaya partnership is where RingCentral's story shifts from impressive execution to genuinely brilliant strategy — the kind of move that business school professors will teach for decades.

To appreciate the audacity of the deal, you need to understand what Avaya was in the 2010s: the most important company in business telephony, and simultaneously one of the most troubled companies in all of enterprise technology.

Avaya had been spun out of Lucent Technologies — itself a descendant of the legendary AT&T Bell Labs — in 2000. At its peak, Avaya was the undisputed king of enterprise PBX systems, with an installed base of hundreds of millions of business phone users worldwide. Then, in 2007, at the worst possible moment, private equity firms Silver Lake and TPG Capital acquired Avaya in a leveraged buyout valued at approximately $8 billion, loading the company with debt just as the financial crisis was about to hit and the cloud was about to disrupt its entire business model.

The debt became a millstone. Avaya could not invest adequately in cloud technology because it was spending billions servicing interest payments. Its customers were aging out of legacy systems but had no cloud migration path from Avaya itself. The irony was excruciating: Avaya had more enterprise customer relationships than anyone in the industry, but it could not give those customers what they were increasingly demanding — a modern cloud communications platform. It was like owning the best restaurant locations in every city but being unable to afford ingredients.

In January 2017, Avaya filed for Chapter 11 bankruptcy protection to restructure its crushing debt load from the 2007 leveraged buyout. The company emerged in 2018 under CEO Jim Chirico, relisting on the NYSE with a cleaner balance sheet but still burdened by its legacy hardware business model and the fundamental inability to build competitive cloud technology in-house.

This was the backdrop when, on October 3, 2019, RingCentral and Avaya announced a bombshell partnership: Avaya Cloud Office by RingCentral. The deal made RingCentral the exclusive UCaaS provider to Avaya, creating a co-branded cloud communications solution that would be sold through Avaya's massive global sales and channel organization. In exchange, RingCentral committed $500 million — $125 million as an equity investment in Avaya's preferred stock and $375 million primarily in RingCentral stock for licensing rights and future payments.

The strategic logic was elegant. Avaya had what RingCentral needed: relationships with thousands of the world's largest enterprises, a global channel of resellers and partners, and brand credibility with CIOs who had used Avaya products for decades. RingCentral had what Avaya needed: an actual cloud communications platform that worked, because despite years of trying, Avaya had been unable to build one that could compete.

The market reaction was volcanic. RingCentral's stock surged over 28% in the first twenty-four hours after the announcement, and analyst price targets jumped from $143 to $225. The spike made Vlad Shmunis a billionaire based on his approximately 8.5% ownership stake. Wall Street understood immediately what this deal meant: RingCentral had just gained preferred access to one of the largest installed bases of enterprise phone system users in the world.

But RingCentral did not stop with Avaya. The company executed a series of similar partnerships that collectively represented one of the most innovative go-to-market strategies in enterprise software. In July 2020, Atos — a major European IT services firm — launched Unify Office by RingCentral, giving RingCentral access to Atos's 40-million-user installed base. In August 2020, Alcatel-Lucent Enterprise created Rainbow Office powered by RingCentral, with RingCentral paying $100 million in cash for exclusive access. BT, the British telecommunications giant, had been partnering with RingCentral since approximately 2014 and launched BT Cloud Work for medium and large enterprises in 2018.

The pattern was brilliant in its consistency. Each of these legacy telecom companies faced the same innovator's dilemma: their customers were demanding cloud solutions, but building a competitive cloud platform from scratch was prohibitively expensive and risky, especially for companies carrying debt, managing declining hardware revenue, or both. RingCentral offered them a lifeline — a white-label cloud platform they could sell under their own brand, preserving their customer relationships while giving those customers the cloud migration path they demanded.

In effect, RingCentral turned its competitors into its distribution channels. The companies that should have been building products to compete with RingCentral were instead reselling RingCentral's technology. Combined, these partnerships gave RingCentral preferred access to over 200 million potential users worldwide. It was, arguably, the single most important strategic decision in the company's history.

The validation extended beyond revenue. When a CIO at a Fortune 500 company saw that Avaya — the company whose PBX systems they had used for twenty years — was recommending a migration to RingCentral's cloud platform, it eliminated the biggest obstacle to enterprise adoption: trust. Enterprise buyers are fundamentally risk-averse with their communications infrastructure. A recommendation from a trusted incumbent was worth more than any marketing campaign or analyst report. The partnership strategy did not just provide distribution — it provided credibility at scale.

VIII. The Great Convergence: UCaaS Meets CCaaS (2016-2019)

While RingCentral was assembling its partnership empire, a tectonic shift was reshaping the communications industry. For decades, business communications had been organized into two separate categories: unified communications — the phone system, video meetings, and team messaging that employees used to talk to each other — and the contact center — the specialized technology that customer service agents used to interact with customers through phone, email, chat, and eventually social media.

These two worlds had different vendors, different technologies, different buyers within the organization, and different budget lines. The unified communications market was dominated by the PBX vendors and their cloud successors. The contact center market was controlled by companies like Genesys, NICE, Five9, and Avaya's contact center division.

But enterprises were starting to ask an obvious question: why do we need two separate communications platforms? If an employee could make a phone call, join a video meeting, and send a team message all from one application, why could a contact center agent not do the same things from the same application, with the added capabilities specific to customer service — queue management, skills-based routing, workforce optimization, quality monitoring?

RingCentral recognized that the convergence of UCaaS and CCaaS — Contact Center as a Service — was both an enormous opportunity and an existential necessity. If RingCentral only offered the unified communications piece, it would eventually lose enterprise deals to competitors who offered both. The complete platform would become the table stakes.

The company initially addressed this through partnerships and integrations, working with contact center vendors to ensure that RingCentral's UCaaS platform could work alongside existing contact center deployments. But the long-term vision was clear: RingCentral needed its own contact center capabilities.

Meanwhile, competition was intensifying from every direction. Zoom, which had started as a pure video conferencing company, was expanding into phone systems with Zoom Phone and eyeing the broader UCaaS market. Microsoft Teams, bundled with Office 365, was gaining rapid adoption and adding telephony features. Cisco was rebuilding its Webex platform. Each competitor brought different strengths, but they all shared one thing: ambitions to own the entire communications stack.

RingCentral's response was to double down on platform openness — what might be called the Switzerland strategy. Rather than trying to lock customers into a single ecosystem, RingCentral built integrations with everyone. The platform worked with Microsoft Office 365, Google Workspace, Salesforce, and hundreds of other enterprise applications. The company published extensive APIs, enabling developers to build custom integrations and workflows on top of the RingCentral platform. The logic was that while Microsoft Teams might be free with Office 365, it only worked well within the Microsoft ecosystem. RingCentral worked with everything.

This open platform approach created stickiness through a different mechanism than vendor lock-in. The more integrations a customer built, the more workflows that depended on RingCentral's APIs, the more painful it became to switch to a competitor. It was lock-in through value rather than lock-in through restriction — a critical distinction in a market where buyers were increasingly sophisticated and allergic to proprietary platforms.

Think of it like the app store analogy. Apple does not lock you in because its phones are technically superior — it locks you in because you have bought hundreds of apps, stored years of photos in iCloud, and synced your devices in ways that would take weeks to replicate elsewhere. RingCentral was building the same kind of ecosystem stickiness, but for business communications. A company that had built custom integrations connecting RingCentral to its CRM, its help desk, its ERP system, and its workforce management tools had effectively embedded RingCentral into its operational DNA. Ripping it out meant rebuilding all of those connections from scratch.

The convergence trend would fully materialize with RingCentral's own contact center product several years later, but the strategic groundwork — the APIs, the integrations, the platform architecture — was being laid in this period. What came next would test every strategic assumption the company had made.

IX. The Pandemic Shock and Zoom Wars (2020-2021)

When COVID-19 sent the world home in March 2020, the impact on business communications was instantaneous and seismic. Within a matter of days, companies that had never considered remote work were scrambling to set up home offices for their entire workforce. The IT departments that had been methodically planning cloud migrations over multi-year timelines suddenly received emergency mandates from their CEOs: "Everyone needs to be able to work from home by Monday."

Within weeks, what had been a gradual enterprise migration to cloud communications became a stampede. Companies that had been planning multi-year cloud transitions compressed them into multi-week emergency deployments. Video conferencing went from a nice-to-have to the primary way that hundreds of millions of knowledge workers communicated with their colleagues, customers, and partners.

For RingCentral, the pandemic was both a massive tailwind and a competitive earthquake. Companies that had resisted the cloud for years — citing security concerns, regulatory compliance, or simple institutional inertia — suddenly had no choice. Their on-premise PBX systems sat in empty offices while their employees worked from kitchen tables and spare bedrooms. The cloud was no longer a future migration path — it was an immediate survival requirement.

On the positive side, revenue accelerated dramatically. The company crossed the billion-dollar revenue threshold in 2020, reporting approximately $1.18 billion, up 31% year over year. Growth then accelerated further to approximately $1.59 billion in 2021, a 35% increase — the highest growth rate in five years. The stock surged to an all-time high of approximately $449 on February 16, 2021, representing a 34-fold gain from the IPO price of $13.

But the pandemic also elevated a competitor in a way that fundamentally altered the market landscape. Zoom Video Communications went from a well-regarded enterprise video tool to a household name overnight. "Zoom" became a verb, the way "Google" had a decade earlier. When your grandmother knew how to use a competitor's product, you had a brand awareness problem that no amount of enterprise sales execution could solve.

RingCentral had actually been using Zoom's video technology since 2013, when the two companies signed a partnership shortly after RingCentral's IPO. For over six years, Zoom's video engine powered RingCentral Meetings. The companies extended this partnership in May 2019. But as Zoom's ambitions expanded from video into phone systems and broader UCaaS — making it a direct competitor — the relationship became untenable.

In April 2020, RingCentral launched RingCentral Video, its own homegrown video conferencing technology that had been in development for years. This was not, as some initially misreported, a product powered by Zoom — it was the replacement for the Zoom-powered product. New customers and key channel partners like AT&T began using RingCentral Video instead of the Zoom-based Meetings product.

The decision to build its own video technology rather than continuing to depend on an increasingly hostile partner was one of the most important product decisions in RingCentral's history. It was also one of the most expensive and risky — building video conferencing technology that could compete with Zoom's polished product required a massive R&D investment at exactly the moment when resources were needed for enterprise sales, contact center development, and international expansion. But the alternative — remaining strategically dependent on a direct competitor — was untenable. It was a critical move to secure the company's long-term platform independence.

But the bigger competitive threat was not actually Zoom. It was Microsoft Teams. Microsoft did something devastatingly simple: it bundled Teams, including basic calling capabilities, into Microsoft 365 subscriptions that enterprises were already paying for. Overnight, hundreds of millions of enterprise users had access to a "free" communications tool that was good enough for many use cases. CIOs who had been planning to deploy standalone UCaaS platforms began asking their teams a simple question: why would we pay extra for RingCentral when Teams comes free with our Office subscription?

This was the bundling threat that every standalone software company dreads, and RingCentral faced it from the largest software company on earth. The enterprise dilemma became acute: CIOs were under pressure to consolidate vendors and reduce costs, and Microsoft's pitch — one vendor for productivity, collaboration, and communications — was compelling on a spreadsheet even if the actual product had significant limitations in telephony and contact center capabilities.

The stock peaked in February 2021, and then the reckoning began. As pandemic-era growth rates normalized, interest rates rose, and the market rotated away from high-growth technology stocks, RNG shares plunged over 75% in 2022 alone. The company's substantial debt load — approximately $1.68 billion versus $267 million in cash — amplified investor concerns. What had been a momentum darling became a value trap debate, and the narrative shifted from "massive TAM opportunity" to "can they survive Microsoft?"

The speed of the reversal was jarring even by technology stock standards. A company that the market had valued at over $40 billion at its peak was suddenly being valued at under $4 billion — a tenfold decline that wiped out years of gains for investors who had bought in during the pandemic euphoria. For employees holding stock options granted at higher prices, the decline was demoralizing. For the company's strategic positioning, it raised uncomfortable questions about whether the market was signaling something fundamental about the competitive outlook.

X. The Pivots and Pressures (2021-2024)

If the pandemic was the party, the hangover was brutal. The post-pandemic era brought a harsh reckoning for RingCentral. Revenue growth decelerated from the mid-30s percentage range to the mid-20s, then to roughly 10% in 2023 and high single digits in 2024. For a company that had been valued as a high-growth SaaS leader, the deceleration was painful. Multiple compression — the market assigning a lower price-to-revenue ratio as growth slowed — compounded the revenue deceleration, driving the stock from its $449 peak into the $30-$40 range by 2023, a decline of approximately 90%.

The leadership transition that followed was one of the more unusual episodes in recent tech history. In August 2023, Vlad Shmunis announced that he would step aside as CEO to become Executive Chairman, focusing on strategic product vision and innovation. His replacement was Tarek Robbiati, a veteran executive who had served as CFO and EVP of Finance and Strategy at Hewlett Packard Enterprise. Robbiati was expected to bring operational discipline and a financial rigor that would help RingCentral navigate its transition from growth-at-all-costs to profitable growth.

What happened next shocked the industry and raised eyebrows across Wall Street. Just four months later, in December 2023, Robbiati resigned. The company stated the departure was a mutual agreement and was not the result of any disagreement about operations, policies, or practices, but such a brief tenure inevitably raised questions about strategic direction and internal dynamics. Shmunis immediately returned to his full-time role as CEO and Chairman, where he remains today. Whatever the internal dynamics, the market interpreted the return of the founder as a stabilizing move, and the company refocused on execution.

Meanwhile, the Avaya relationship — which had been one of RingCentral's most celebrated strategic moves — became considerably more complicated. For the second time in six years, Avaya found itself unable to service its debt obligations. In February 2023, Avaya filed for Chapter 11 bankruptcy protection for the second time, burdened by $3.4 billion in total debt. The restructuring eliminated more than 75% of Avaya's debt, but it also wiped out equity holders — including RingCentral's $125 million convertible preferred stock investment, which was completely cancelled in the restructuring. However, the commercial partnership survived. In fact, Avaya expanded and extended the Avaya Cloud Office arrangement post-bankruptcy, adding a new reseller model and expanding into all markets where RingCentral operated. The loss of the equity investment was real and painful, but the preservation of the commercial relationship — the actual strategic value of the deal — demonstrated the durability of the partnership model.

On the competitive front, the landscape hardened. Microsoft Teams continued its relentless expansion, commanding roughly 27.5% of global UCaaS revenue and 53% of subscriptions by 2024. Zoom was pushing aggressively into enterprise telephony with Zoom Phone. Cisco was reorganizing around Webex. And the overall UCaaS market was maturing, with growth projections settling into the low single digits through the end of the decade.

RingCentral's response was a strategic reset that touched nearly every aspect of the business. The company doubled down on the mid-market segment — companies large enough to need sophisticated communications but not so large that they were captive to Microsoft's ecosystem. It pursued verticalization, building specialized solutions for healthcare, retail, and financial services that addressed industry-specific compliance, workflow, and integration requirements.

The AI wave provided a new vector for differentiation. RingCentral launched RingSense, a conversation intelligence platform using proprietary large language models to transcribe calls, summarize meetings, and provide real-time coaching. RingSense for Sales, launched in March 2023, applied AI to revenue intelligence. RingCX, launched in November 2023, represented RingCentral's entry into the native, AI-first contact center market — a product that had been years in the making and represented the full realization of the UCaaS-CCaaS convergence strategy. By 2025, RingCX had surpassed 1,000 customers, including a Fortune 500 win with over 1,000 seats.

Perhaps the most intriguing new product — and the one that most directly echoes the company's small business origins — was AI Receptionist, or AIR, launched in late 2025. This was an AI-powered virtual receptionist that could handle 90% of inbound call routing without human intervention, priced at $39 per user per month. The product resonated strongly with small and mid-sized businesses — the same market that had been RingCentral's original wedge — and surpassed 1,000 customers shortly after launch. Collectively, RingCentral's new products — RingCX, RingSense, Events, and AIR — generated over $50 million in ARR by the end of 2024 and were on track to exceed $100 million by the end of 2025.

The financial story also improved dramatically, reflecting a company that had internalized the post-pandemic shift in investor expectations from growth-at-all-costs to profitable growth. After years of GAAP losses, RingCentral achieved GAAP operating profitability for the first time in 2024 and reported its first year of GAAP net income in 2025 — $43 million, compared to a $58 million loss the prior year. Non-GAAP operating margins expanded to 22.5%. Free cash flow reached a record $530 million, up 32% year over year, representing a 21% free cash flow margin that would be the envy of most SaaS companies.

The transformation from a cash-burning growth company to a cash-generating profitable company was perhaps the most important strategic pivot of the Shmunis era. It did not happen by accident — it required disciplined cost management, a reduction in stock-based compensation that had been diluting shareholders, and a ruthless focus on sales efficiency. The company was no longer a growth story trying to prove it could be profitable; it was a profitable company exploring where its next phase of growth would come from. Management set a target of 20% GAAP operating margins over the next three to four years and began working toward an investment-grade credit profile — a signal that the era of leveraged growth was giving way to an era of capital discipline.

XI. The Business Model Deep Dive

To truly understand RingCentral's competitive position, you need to understand the engine room — the business model economics that determine whether the company can generate sustainable returns in a structurally challenging market. RingCentral's business model is textbook SaaS with some distinctive characteristics that reflect the unique economics of cloud communications. Understanding these economics is essential for anyone evaluating the company as a business or an investment.

At the foundation, RingCentral charges businesses a monthly subscription fee per user for access to its cloud communications platform. Pricing varies by plan and features, ranging from roughly $20 per user per month for basic phone service to significantly more for premium plans that include video conferencing, team messaging, analytics, and contact center capabilities. AI features like RingSense and AIR represent incremental monetization opportunities layered on top of the base subscription. To put the unit economics in concrete terms: a mid-sized company with 500 employees paying an average of $30 per user per month generates $180,000 in annual recurring revenue — a meaningful number that compounds across thousands of such customers.

The model benefits from what SaaS investors call "negative churn" potential — the ability for the installed base to generate more revenue over time without adding new logos. When an existing customer hires more employees, each new hire needs a phone line, which means another $30 per month flowing to RingCentral. When a customer upgrades from basic phone service to a plan that includes video and messaging, the revenue per user increases. And when a customer adds contact center seats or AI features, entirely new revenue streams open up from the same relationship.

The beauty of this model is its predictability. Unlike companies that depend on one-time sales or project-based revenue, RingCentral's annualized exit monthly recurring subscriptions stood at approximately $2.67 billion by late 2025. This revenue is contractual, recurring, and exhibits what the SaaS world calls "net dollar retention" — the percentage of revenue retained from existing customers after accounting for upgrades, downgrades, and churn. RingCentral has historically maintained net dollar retention above 100%, meaning the revenue from its existing customer base grows each year even without adding a single new customer. This metric is arguably the single most important indicator of customer satisfaction and product stickiness. When net dollar retention is above 100%, it means customers are buying more seats, upgrading to premium plans, or adding new products faster than other customers are leaving or downgrading.

Customer acquisition cost relative to lifetime value varies dramatically by segment. Small businesses are inexpensive to acquire through the channel but generate modest individual revenue and exhibit higher churn. Mid-market and enterprise customers are expensive to acquire — the sales cycles are long, the sales teams are highly compensated, and proof-of-concept deployments require significant resources — but they generate much larger revenue streams and churn far less frequently. The payback period on enterprise customer acquisition typically stretches beyond twelve months but the lifetime value is multiples higher.

One of the most distinctive aspects of RingCentral's model is its extraordinary channel leverage. Over 70% of revenue flows through partners — telecom carriers, VARs, technology distributors, and the white-label partnerships with Avaya, Atos, Alcatel-Lucent Enterprise, and BT. This channel model allows RingCentral to reach customers at a fraction of the cost of a pure direct sales motion. The partners handle customer relationships, local support, and in many cases, billing and collections. RingCentral provides the platform, handles the technology, and collects the majority of the subscription revenue. It is a remarkably capital-efficient distribution model that would take years and billions of dollars for a competitor to replicate.

Gross margins run above 70%, which is typical for enterprise SaaS but remarkable for what is essentially a telecommunications service. The multi-tenant cloud architecture means that marginal costs of serving additional users are minimal — the same platform, the same code, the same infrastructure serves a ten-person accounting firm and a ten-thousand-person enterprise. The primary cost drivers below the gross margin line are R&D, which runs in the high teens as a percentage of revenue, and sales and marketing, which remains the largest expense category as the company continues to invest in enterprise customer acquisition.

So where does this leave the competitive moat? The moat is real but narrower than bulls would like. Switching costs are substantial: businesses that migrate to RingCentral port their phone numbers, build integrations with their other enterprise applications, train their employees on new workflows, and configure complex call routing rules. For an enterprise with a contact center, the switching costs are even higher — agent scripts, queue configurations, workforce management rules, and compliance recording setups represent months of implementation work. A typical enterprise migration takes twelve to eighteen months. Nobody switches their business phone system on a whim.

But the moat has limits. Phone number portability is improving, standards-based integrations reduce the uniqueness of any single platform's connectivity, and — most significantly — Microsoft's ability to bundle communications features with an operating system and productivity suite that enterprises already own creates pricing pressure that no amount of switching costs can fully offset. The question is whether RingCentral's advantages in telephony depth, contact center capabilities, and multi-vendor flexibility are sufficient to justify a premium over "free" alternatives that are good enough for many use cases.

XII. Porter's Five Forces Analysis

Understanding the competitive forces acting on RingCentral requires looking beyond the obvious "Microsoft is bundling" narrative to examine the full structural dynamics of the industry. Michael Porter's framework, originally developed in 1979, remains the most rigorous tool for assessing whether an industry's structure is favorable or unfavorable for the companies competing in it. In RingCentral's case, the picture is sobering.

Threat of New Entrants sits at medium-high. Building a basic VoIP service has never been easier — cloud infrastructure from AWS and Azure, open-source telephony frameworks, and SIP trunking services from dozens of providers mean that a startup can launch a functional internet phone service in months. But there is an enormous gap between a functional phone service and an enterprise-grade communications platform. Carrier-grade reliability requires redundant data centers, direct carrier interconnects, and sophisticated quality-of-service engineering. Regulatory compliance — E911 emergency services, HIPAA for healthcare, PCI for payments, GDPR for European operations — adds layers of complexity. And building the enterprise sales motion, channel partnerships, and brand credibility that RingCentral has assembled over two decades is not something that can be replicated quickly regardless of funding levels. The threat comes not from new pure-play entrants but from adjacent technology giants expanding into communications.

Bargaining Power of Suppliers is low to medium. RingCentral's key inputs are telecommunications carrier connections, data center capacity, and cloud infrastructure. Multiple options exist for each, and RingCentral's scale gives it negotiating leverage. No single supplier has disproportionate power over the company's cost structure, though the Zoom partnership did create a specific dependency that RingCentral wisely eliminated by building its own video technology.

Bargaining Power of Buyers is high and getting higher. Enterprise customers have more choices than at any point in the history of business communications. Microsoft Teams, Zoom, Cisco Webex, 8x8, Vonage, Dialpad — the menu is extensive. Switching costs create friction but are declining as portability standards improve. Most concerning for RingCentral, CIOs are under intense pressure to consolidate vendors and reduce costs, and the pitch of "you already pay for Microsoft 365, Teams is included" resonates powerfully with procurement departments focused on total cost of ownership.

Threat of Substitutes is very high. Microsoft Teams bundled with Office 365 represents the most potent substitute threat. When a product that addresses most of a customer's needs comes "free" with something they are already buying, the standalone product needs to be dramatically better to justify incremental spending. Beyond Teams, a range of alternative communication tools — Zoom, Slack, Google Meet, WhatsApp Business — address specific communication needs and reduce the perceived necessity of a comprehensive UCaaS platform. Traditional telephony, while declining, still exists for use cases where cloud migration is impractical or undesirable.

Competitive Rivalry is very high and intensifying. The UCaaS market generated approximately $33.4 billion in global revenue in 2024, but the growth engine is slowing — projections call for just 1.1% annual growth through 2029. When a market stops growing, the competitive dynamics change fundamentally. Every dollar of new revenue must come from someone else's customer, and well-funded competitors have every incentive to compete on price rather than innovation. A slowing market with well-funded competitors creates a zero-sum dynamic where growth comes primarily from taking market share. Microsoft's distribution advantage is overwhelming — its installed base of Office 365 users numbers in the hundreds of millions. Zoom's brand power and engineering culture make it a formidable competitor. Cisco's networking relationships give it unique access to enterprise infrastructure decisions. And private equity-owned competitors like Mitel and Dialpad may be willing to accept lower margins to gain share, further pressuring pricing.

The net assessment from a Five Forces perspective is that RingCentral operates in a structurally challenging industry. Buyer power, substitute threats, and competitive rivalry all pressure margins and growth. The company's defenses — switching costs, channel leverage, and platform depth — are real but eroding. Survival and success require continuous differentiation, which is why the company's AI investments and vertical strategies are so strategically important.

XIII. Hamilton's Seven Powers Framework

If Porter's Five Forces tells us about the industry, Hamilton Helmer's Seven Powers framework tells us about the company's specific competitive advantages within that industry. Helmer's framework asks a different question: what powers does this company possess that create durable differential returns? Let us examine each of the seven powers as they apply to RingCentral.

Scale Economies are moderate. RingCentral's multi-tenant architecture means that the cost of serving each additional customer is marginal, and the massive R&D investment in the platform is amortized across an installed base of hundreds of thousands of businesses. Carrier agreements improve with volume — the more minutes RingCentral routes through a carrier, the lower the per-minute cost — and the company's data center and network infrastructure benefits from utilization. However, RingCentral does not have the most scale in its market — Microsoft and Zoom both serve far larger user bases — which limits the relative advantage. In Helmer's framework, scale economies are most powerful when the company is the largest player, and RingCentral is not.

Network Effects are limited but present. Within a company, more users on RingCentral makes the platform more valuable — an employee can call, message, or video conference with any colleague through a single interface. The developer ecosystem and integration marketplace create a modest cross-side network effect: more customers attract more developers building integrations, which makes the platform more valuable to more customers. But these are not the viral, cross-company network effects that power companies like social networks or marketplaces. A business does not gain significant value from other unrelated businesses using RingCentral.

Counter-Positioning was historically RingCentral's most powerful advantage, and it is largely spent. For over a decade, the legacy PBX vendors — Avaya, Nortel, Mitel — could not respond to RingCentral's cloud model without cannibalizing their own hardware and maintenance revenue streams. This was the innovator's dilemma in its purest form. RingCentral had a decade-plus head start to build its platform, customer base, and channel while the incumbents were paralyzed by their business models. But that window is now closed. Every major competitor has a cloud offering. The counter-positioning advantage against legacy vendors has been fully exploited.

Switching Costs represent RingCentral's strongest current power. Phone numbers, integrations, custom configurations, compliance setups, employee training, and business process dependencies create genuine friction for any customer contemplating a switch. Contact center deployments are particularly sticky — the configuration complexity of agent skills routing, workforce management rules, and quality monitoring setups can represent thousands of hours of implementation work. Enterprise migrations typically take twelve to eighteen months, and the operational risk of disrupting business communications is high enough that many organizations will tolerate a premium rather than undertake a switch. However, this power is under secular pressure as portability improves and standards-based integrations reduce the uniqueness of any single platform.

Branding is moderate. RingCentral has strong brand recognition within the UCaaS category, particularly among IT buyers and channel partners. The company regularly lands in the Leaders quadrant of Gartner's Magic Quadrant for UCaaS, which carries significant weight in enterprise purchase decisions. Fortune 500 customer logos provide social proof. But in the broader consciousness — among the executives and end users who actually use the product daily — Zoom and Microsoft have dramatically stronger brand pull. Zoom's pandemic-era consumer adoption created a level of brand awareness that RingCentral cannot match, and Microsoft's brand is simply ubiquitous.

Cornered Resource is weak. RingCentral does not possess unique technology or intellectual property that competitors cannot replicate given sufficient investment. The patents held by CTO Vlad Vendrow cover specific implementations rather than fundamental capabilities. Talent in cloud communications is available on the market. The infrastructure — carrier relationships, data centers, cloud resources — is accessible to well-funded competitors. Channel partner relationships are valuable but not exclusive.

Process Power is strong and arguably RingCentral's most underappreciated advantage alongside switching costs. The enterprise sales machine that has been refined over fifteen-plus years — the SDR-to-AE-to-SE pipeline, the channel partner management, the customer success playbooks, the implementation methodology, the retention and expansion motions — represents institutional knowledge that is extraordinarily difficult to replicate. Process power is invisible from the outside but manifests in consistently high net dollar retention, efficient channel leverage, and the ability to execute complex enterprise deals with predictable outcomes. It took RingCentral years to build this machine, and a new entrant cannot shortcut that organizational learning.

The overall power assessment suggests a company whose strongest defenses are switching costs and process power — powers that are real and meaningful but not the highest-order powers in Helmer's framework. Helmer argues that the most valuable powers are those that create persistent differential returns over very long time horizons, like network effects and counter-positioning. RingCentral's current powers — switching costs and process power — are more defensive than offensive. They protect the existing business but do not create the kind of compounding advantage that drives sustained value creation.

The most concerning dynamic is that RingCentral's historical advantage — counter-positioning against cloud-challenged incumbents — is exhausted, and no comparably powerful new advantage has emerged to replace it. The company must find defensible niches through verticalization, international expansion, and AI differentiation to sustain its competitive position against rivals with greater scale and distribution. The question for investors is whether process power and switching costs, combined with these new vectors, can sustain a durable competitive position — or whether they merely slow the gravitational pull of Microsoft's bundling strategy.

XIV. The Playbook: Lessons for Builders and Investors

RingCentral's twenty-seven-year journey from a fax-to-email startup to a multi-billion-dollar enterprise communications platform offers a remarkably rich set of lessons for both company builders and investors.

Every great business story contains a tension between what the company did right and what the market did to it. RingCentral's story is more instructive than most precisely because it is not a simple triumph narrative — it includes brilliant strategic moves, painful competitive challenges, and an ongoing struggle for relevance against industry titans. The lessons are nuanced because the story is nuanced.

The wedge strategy works. RingCentral's approach of starting with small businesses that the incumbents ignored and systematically moving upmarket is one of the most proven playbooks in enterprise technology. The SMB market served as a testing ground for the product, a source of early revenue, and a proof point for enterprise buyers. The key insight is that the wedge must be large enough to sustain a business while the enterprise motion is being built — and small enough that the incumbents do not feel threatened until it is too late.

Channel leverage is an unfair advantage. RingCentral's model of distributing over 70% of revenue through partners allowed it to achieve enterprise sales scale without building an army of direct salespeople. For founders, the lesson is that channel partnerships, when structured correctly, can be the difference between a company that grows linearly with headcount and one that grows exponentially through leverage. But channel partnerships require patience — they take years to build, and the initial revenue contribution is small before it compounds.

Turning competitors into distribution channels is genius when you can pull it off. The Avaya, Atos, and Alcatel-Lucent Enterprise partnerships represent a strategic pattern that is almost unique in enterprise technology. By building a platform that declining incumbents could white-label, RingCentral effectively converted the entire legacy PBX industry into its sales channel. The precondition for this strategy is a genuine innovator's dilemma — the partner must be unable to build the product themselves due to business model constraints.

Know when to build versus when to partner. RingCentral's original decision to partner with Zoom for video conferencing was pragmatic — video was not its core competency, and Zoom's product was excellent. The subsequent decision to build its own video technology when Zoom became a competitor was equally pragmatic. The lesson is that build-versus-partner decisions should be revisited continuously as competitive dynamics evolve.

Enterprise sales is a moat that takes years to build. RingCentral's process power — the refined sales machine, the channel management expertise, the customer success playbooks — represents an accumulated investment of well over a decade. A well-funded startup can build a competitive product in a year or two. It cannot build a competitive enterprise sales organization in less than five.

SaaS metrics discipline matters. RingCentral's ability to communicate its story to Wall Street through metrics like net dollar retention, the Rule of 40, and enterprise customer counts allowed it to raise capital, maintain investor confidence during growth slowdowns, and fund the strategic investments that kept it competitive. For any SaaS company, the lesson is that the right metrics, consistently reported, build credibility that survives cyclical headwinds.

The bundling threat is real and requires honest assessment. When Microsoft bundles a communications product with Office 365, the appropriate response is not denial or dismissal — it is an honest assessment of where the bundled product falls short and a relentless focus on those gaps. RingCentral's emphasis on telephony depth, contact center capabilities, and multi-vendor flexibility represents a clear-eyed response to the bundling threat.

Timing of platform shifts is everything. Shmunis recognized the cloud communications opportunity in 1999, seven years before the term "cloud computing" entered mainstream use. That early timing gave RingCentral the architectural advantages, customer base, and organizational learning that allowed it to lead the market through the critical growth years of the 2010s. For investors, the implication is that the companies best positioned to win platform shifts are those that start earliest — and that means investing in them before the shift is obvious.

Capital allocation discipline defines the transition from growth to maturity. RingCentral's journey from cash-burning growth company to $530 million free cash flow generator illustrates a transition that every high-growth SaaS company must eventually make. The timing of this transition — when to shift from investing for growth to optimizing for profitability — is one of the most consequential decisions a management team faces. Move too early and you cede market share to competitors still investing. Move too late and you burn through cash and investor patience. RingCentral arguably threaded this needle, though not without the stock market extracting a 90% toll along the way.

XV. Bear versus Bull Case

The Bear Case

The existential concern for RingCentral begins and ends with three words: Microsoft. Teams. Free.

With 27.5% of global UCaaS revenue and 53% of subscriptions, Teams is not just a competitor — it is the gravitational center of the market. Every enterprise that uses Microsoft 365 has Teams, and the incremental cost of using Teams for business communications is zero. For CIOs under pressure to reduce vendor count and technology spending, the pitch is almost impossible to resist: consolidate onto Microsoft, eliminate the standalone UCaaS contract, and redirect the savings elsewhere.

The UCaaS market itself is maturing. Growth projections of just 1.1% annually through 2029 suggest that the explosive cloud migration phase is largely over. What remains is a market-share battle among well-funded competitors, which tends to compress margins and reward scale advantages that RingCentral does not possess relative to Microsoft, Zoom, or Cisco.

Revenue growth has decelerated from 35% in 2021 to roughly 5% in 2025 — a trajectory that tells the story of a market that was pulled forward by the pandemic and is now settling into a mature growth profile. While profitability has improved dramatically, the stock market has little patience for former high-growth companies that have transitioned to low growth. The 90%-plus decline from peak reflects this re-rating, and there is no obvious catalyst for a return to the growth rates that would justify a significantly higher multiple.

The international expansion opportunity is real but expensive and competitive. Markets outside the United States present regulatory complexity, established local competitors, and the need to build carrier relationships country by country. With 70% of revenue still coming from the United States, meaningful international diversification will require years of investment.

Finally, AI presents a double-edged sword. While RingCentral is investing heavily in AI capabilities, AI could fundamentally disrupt communication workflows in ways that reduce the need for traditional phone systems altogether. If AI agents can handle the majority of customer interactions, the contact center market could shrink rather than grow. If AI-powered tools make it trivial to switch between communication platforms, switching costs — one of RingCentral's primary powers — could erode.

The Bull Case

The bull case starts with a distinction that the market often fails to make — and it is a distinction that separates casual observers from people who actually run enterprise communications infrastructure. Microsoft Teams is excellent at internal collaboration and adequate at basic telephony, but it is genuinely weak in the areas where businesses spend the most on communications — advanced telephony features, contact center capabilities, and multi-vendor environments. Teams Phone has limited call routing, weak analytics, minimal contact center functionality, and poor integration with non-Microsoft ecosystems. For businesses with complex telephony needs — healthcare systems with nurse call routing, retail chains with store-to-headquarters communications, financial services firms with compliance recording requirements — Teams is simply not sufficient.

The contact center opportunity is particularly compelling. RingCX, launched in November 2023, represents a higher-margin growth vector in a market where nearly half of companies want the same provider for unified communications and contact center. Over 50% of RingCX customers opt for paid AI capabilities, suggesting strong monetization potential. The CCaaS market is growing faster than UCaaS, and RingCentral's integrated platform — one vendor for both employee communications and customer interactions — is a genuine competitive advantage.

The mid-market remains dramatically underserved. Companies with 100 to 5,000 employees are too large for basic phone solutions and too small for the massive professional services engagements that Microsoft and Cisco prefer to sell. There are hundreds of thousands of these companies globally, and they represent the economic backbone of most developed economies. They need sophisticated communications but do not have the IT staff to manage complex deployments. This is RingCentral's sweet spot, and the channel ecosystem — with its thousands of VARs and telecom agents who have relationships with exactly these kinds of companies — is optimized to reach them efficiently.

AI is creating new monetization opportunities rather than just threats. AI Receptionist, priced at $39 per user per month, is already demonstrating strong adoption in the SMB market. RingSense adds revenue intelligence and conversation analytics on top of existing subscriptions. These are not replacement products — they are expansion products that increase the revenue per customer without requiring new customer acquisition.

The financial profile has never been stronger. Free cash flow of $530 million on $2.52 billion in revenue represents a 21% margin, and management is targeting 20% GAAP operating margins over the next three to four years. At current stock prices in the mid-$30s, the company trades at roughly 6 times free cash flow — a valuation that would be more typical of a declining business, not a company with 100%+ net dollar retention, expanding margins, and new product-driven growth vectors.