Rocket Companies: The Digital Mortgage Revolution

I. Introduction & Episode Thesis

Picture this: It's 2015, Super Bowl Sunday. Between the Denver Broncos and Carolina Panthers, a commercial airs that doesn't feature talking animals or celebrity cameos. Instead, it shows something radical—a mortgage application completed on a smartphone in eight minutes. The tagline: "Push Button, Get Mortgage." Traditional bankers watching from their suburban living rooms nearly choked on their nachos. This wasn't how mortgages worked. This wasn't how banking worked. Yet within three years, the company behind that ad would become America's largest mortgage lender.

The company was Rocket Mortgage, the flagship brand of what is now Rocket Companies—a $36 billion fintech platform that processes more mortgage applications than any other lender in America. From its headquarters in downtown Detroit (yes, Detroit), Rocket operates a vertically integrated financial services ecosystem spanning mortgages, real estate, title services, personal loans, and financial management tools. Think of it as the Amazon of home financing—except instead of books, they started with the most complex financial transaction most Americans ever make.

Here's the central question we're exploring: How did a brick-and-mortar mortgage broker founded in 1985 transform into America's mortgage technology powerhouse? The answer involves three interwoven threads: a relentless focus on technology when competitors clung to paper, a contrarian bet on Detroit when everyone else fled, and a founder who bought his company back from a tech giant because they didn't move fast enough online.

The Rocket story challenges conventional wisdom about financial services. While Wall Street banks built trading floors, Dan Gilbert built server farms. While competitors opened branches, he coded algorithms. While the industry lobbied for looser lending standards before 2008, he stuck to vanilla mortgages and invested the savings in technology. The result? A company that didn't just survive the financial crisis—it emerged as the industry's digital standard-bearer.

What makes Rocket particularly fascinating for students of business strategy is how it weaponized simplicity in a complex industry. Mortgages involve hundreds of documents, dozens of stakeholders, and regulations that vary by state, county, and municipality. Most companies accepted this complexity as immutable. Rocket asked: what if we abstracted all of that away from the customer? What if getting a mortgage felt more like ordering an Uber than visiting a bank?

This isn't just a technology story, though. It's equally about geography as strategy. When Gilbert moved Rocket's headquarters to downtown Detroit in 2010, the city was synonymous with urban decay. Crime was rampant. Buildings stood empty. The city would declare bankruptcy three years later. Yet Gilbert saw what others missed: talent arbitrage, cheap real estate, and the opportunity to build a company town in America's most unlikely location. Today, Rocket employs over 19,000 people, mostly in Detroit, making it one of the city's largest employers and a cornerstone of its revival.

The company's structure tells you everything about its ambitions. Rocket Companies isn't just Rocket Mortgage—it's an ecosystem play. Rocket Homes helps you find a house. Rocket Mortgage finances it. Amrock (formerly Title Source) handles the title. Rocket Money (acquired as Truebill) manages your finances before and after. Rocket Loans provides personal credit. Each business feeds the others, creating network effects and reducing customer acquisition costs. It's the same playbook Amazon used in e-commerce, applied to financial services.

As we dive into this story, we'll trace the company's evolution through five distinct eras: the scrappy mortgage broker years under Rock Financial, the digital pioneering after Gilbert bought it back from Intuit, the platform-building decade that created Rocket Mortgage, the pandemic-fueled IPO that made it public, and the current AI-powered consolidation phase that includes blockbuster acquisitions of Redfin and Mr. Cooper. Each phase reveals different lessons about disruption, timing, and the power of betting against conventional wisdom.

The Detroit setting matters more than you might think. This is a company shaped by Rust Belt pragmatism, not Silicon Valley idealism. When Rocket talks about democratizing home ownership, it's not abstract—they're headquartered in a city where you could buy a house for $1,000 after the financial crisis. The company culture reflects this environment: aggressive but not pretentious, innovative but not experimental, ambitious but grounded in the harsh realities of American economics.

So buckle up for a journey from 1980s mortgage brokerage to 2020s AI-powered lending, from suburban Detroit to downtown revival, from startup to $36 billion public company. It's a story about how technology eats traditional industries, but also about timing, geography, and the power of controlling your own destiny. Because sometimes the best way to predict the future is to build it yourself—even if that means buying your company back to do it.

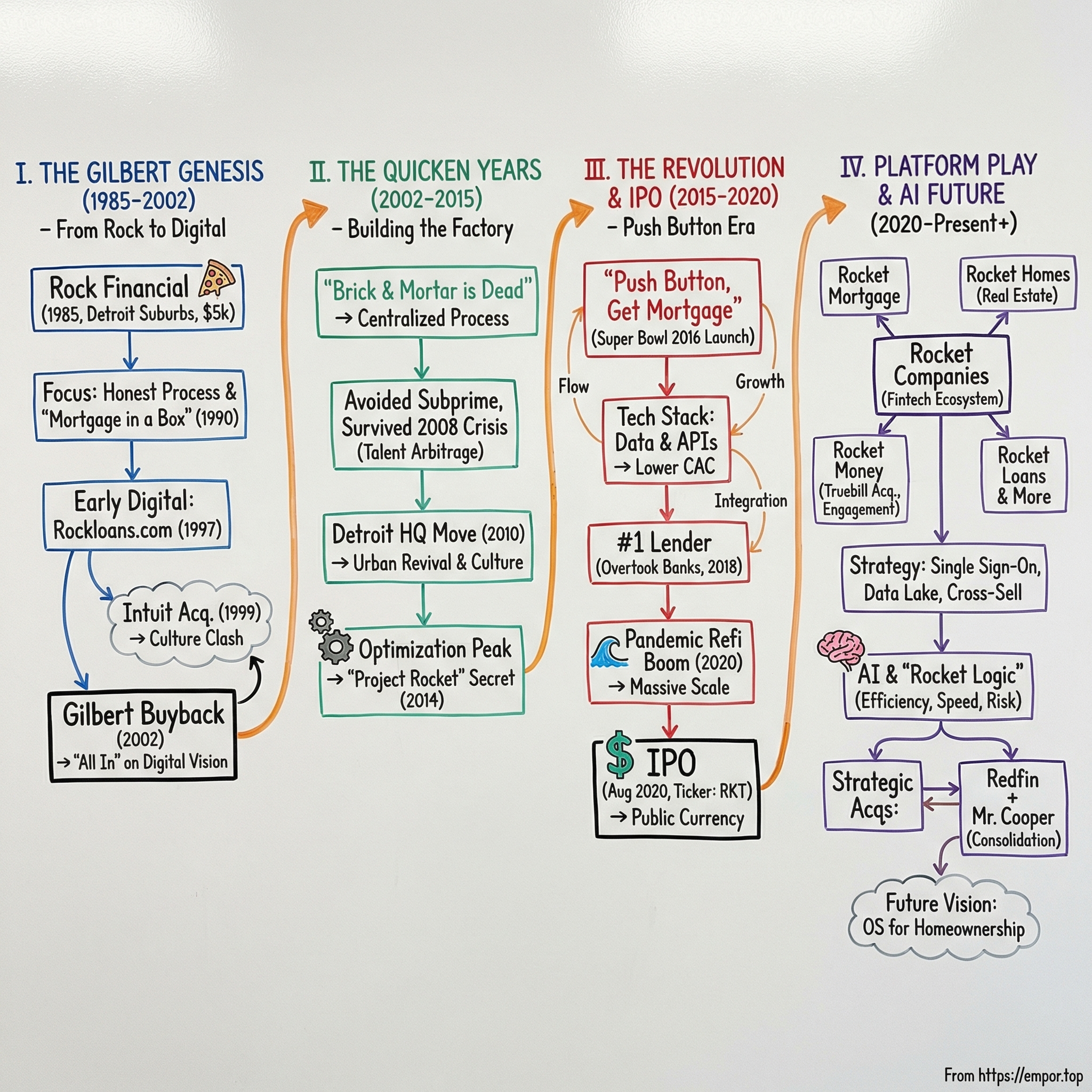

II. The Gilbert Genesis: From Rock Financial to Digital Pioneer (1985-2002)

The year was 1985. Ronald Reagan was president, "Back to the Future" dominated the box office, and in suburban Detroit, a 22-year-old Dan Gilbert was pitching pizzeria owners on a revolutionary idea: What if getting a mortgage didn't require three months and a filing cabinet worth of paperwork? The pizzeria owners weren't buying it—literally. Gilbert had been waiting tables there, trying to save money for law school, when he realized he was better at selling ideas than pizza slices. That summer, with $5,000 saved and three friends—Ron Berman, Lindsay Gross, and his brother Gary—Gilbert founded Rock Financial from a tiny office in Livonia, Michigan.

The name "Rock" wasn't some clever acronym or focus-grouped brand. It came from Rock Financial's original business model: they were the rock-solid option in a sea of sketchy mortgage brokers. This was the go-go 1980s, when mortgage brokers had roughly the same reputation as used car salesmen. The industry was fragmented, unregulated in many states, and full of operators who would promise anything to close a deal. Gilbert's insight was simple but powerful: What if a mortgage broker actually told the truth? What if they explained the process clearly, delivered on promises, and treated customers like humans rather than commission checks?

For three years, Rock Financial operated as a pure broker—matching borrowers with lenders and taking a fee. The business model was straightforward but limited. Brokers had no control over the actual lending decision, couldn't set rates, and were essentially middlemen in a process they couldn't improve. Gilbert grew increasingly frustrated watching deals fall apart because of slow, incompetent lenders. In 1988, he made the pivotal decision to become a mortgage banker—actually funding loans rather than just arranging them. This required serious capital, regulatory approvals, and taking on real credit risk. Most 25-year-olds would have balked. Gilbert saw it as the only way to control the customer experience.

The transformation from broker to lender revealed Gilbert's true innovation gene. While competitors focused on sales, Rock Financial obsessed over process. In 1990, they launched something called "Mortgage in a Box"—a physical box mailed to customers containing a simplified mortgage application, clear explanations of each step, and prepaid envelopes to return documents. Think of it as the prehistoric ancestor of today's digital applications. Customers loved it. Instead of multiple trips to a broker's office, they could complete everything from their kitchen table. The box became Rock Financial's signature, so popular that competitors tried (and failed) to copy it.

By the mid-1990s, Rock Financial was originating over $1 billion annually—serious volume for an independent lender. Gilbert had built a machine: centralized processing in Detroit, standardized procedures, and a culture of continuous improvement. But he saw the internet coming and understood its implications before most of his competitors could spell "URL." In 1997, while established banks debated whether customers would ever trust online banking, Gilbert launched Rockloans.com—one of the first online mortgage platforms in America.

The website was primitive by today's standards—basically an online version of Mortgage in a Box. But in the context of 1997, when most Americans were still using dial-up modems, it was revolutionary. Customers could research rates, calculate payments, and start applications online. More importantly, it gave Rock Financial a laboratory to test digital processes. Every online application taught them something about user behavior, dropout rates, and confusion points. They were gathering data that would prove invaluable later.

The late 1990s were rocket fuel for Rock Financial. The economy was booming, internet stocks were soaring, and everyone wanted to own a home. In May 1998, Rock Financial went public on the NASDAQ, raising capital to fund expansion. The IPO valued the company at around $150 million—not bad for a business started with $5,000 thirteen years earlier. Gilbert owned roughly 25% and was suddenly worth nearly $40 million on paper. He was 36 years old, wealthy, and running a public company. Most entrepreneurs would have been satisfied.

But Gilbert was restless. He saw how slowly public markets moved, how quarterly earnings constrained long-term thinking, and most importantly, how far behind Rock Financial remained in the digital transformation he envisioned. When Intuit came calling in 1999, offering $532 million to acquire Rock Financial, Gilbert saw an opportunity. Intuit owned Quicken, the dominant personal finance software, used by millions of Americans to manage their money. Combining Quicken's user base with Rock Financial's lending capability seemed like a perfect match. The deal closed in December 1999, and Rock Financial became Quicken Loans.

The honeymoon lasted exactly 18 months. By mid-2001, the dot-com bubble had burst, Intuit's stock had crashed, and the company was retrenching to its core tax and accounting software. The mortgage business—rechristened Quicken Loans—was a distraction. Worse, from Gilbert's perspective, Intuit moved at software speed, not internet speed. Every decision required committees, approvals, and consensus-building. Gilbert wanted to go all-in on online lending; Intuit wanted to integrate gradually. The culture clash was immediate and irreconcilable.

In June 2002, Gilbert made his move. He assembled a group of private investors and offered to buy Quicken Loans back from Intuit for $64 million—about 12% of what Intuit had paid three years earlier. Intuit, eager to shed non-core assets and raise cash, accepted immediately. On July 1, 2002, Dan Gilbert was once again the owner of the company he'd founded. But this wasn't really the same company. The Quicken brand was valuable, the technology infrastructure had improved under Intuit, and most importantly, Gilbert had learned what didn't work. He'd seen how big companies operated, understood the constraints of public markets, and crystallized his vision for what came next.

The day after closing the buyback, Gilbert sent an email to all employees. The subject line: "All In." The message was short but clear: Quicken Loans would bet everything on moving the entire mortgage process online. Not just applications, but underwriting, processing, closing—everything. No more branches. No more paper. Pure digital. Employees who couldn't adapt should leave now. Those who stayed would help build something the mortgage industry had never seen. It was July 2002. The housing bubble was just beginning to inflate. The iPhone wouldn't exist for five years. Facebook hadn't been invented. Yet Gilbert was betting his entire company on digital transformation. As we'll see in the next chapter, that bet would pay off beyond anyone's wildest imagination—but not before surviving the greatest financial crisis since the Great Depression.

III. The Quicken Years: Building an Online Empire (2002-2015)

Dan Gilbert stood before his 300 employees on a humid Detroit morning in August 2002, just weeks after buying back Quicken Loans. Behind him, a massive banner read: "Brick and mortar is dead." He wasn't talking about retail stores—he was declaring war on the traditional mortgage industry. "Every bank branch, every loan officer with a desk and a secretary, every filing cabinet full of paper applications," he said, "they're all going to be replaced by servers and code." Half the room thought he was crazy. The other half started updating their resumes. Within five years, both groups would be believers.

The transformation began with a ruthless simplification of the product line. While competitors offered exotic mortgages—negative amortization loans, option ARMs, no-documentation "liar loans"—Quicken Loans went the opposite direction. They would offer only conventional mortgages, government-backed FHA loans, and VA loans. Nothing fancy. Nothing subprime. This wasn't a moral stance initially; it was operational. Complex products required human judgment, exceptions, and manual processing. Simple products could be automated, standardized, and scaled. Gilbert was building a mortgage factory, and factories work best when they produce the same thing over and over.

The numbers from 2003 to 2007 tell the story of a company hitting escape velocity. Loan originations grew from $4 billion to $12 billion. Employee count tripled. Market share in online lending went from 15% to over 35%. But the real innovation was happening behind the scenes. Quicken Loans built something called the "Quicken Loans Mortgage Process"—a proprietary system that broke down every mortgage into discrete steps, automated what could be automated, and optimized what couldn't. Think of it as the mortgage equivalent of the Toyota Production System. Every loan followed the same path, every decision point was documented, every outcome was measured.

The system generated staggering efficiencies. By 2006, Quicken Loans could process a loan in 30 days versus the industry average of 45-60 days. Their cost per loan was $2,800 versus an industry average of $4,500. Customer satisfaction scores were in the 90s while the industry averaged in the 60s. But here's what really mattered: Because everything was digital and centralized, Quicken Loans could operate from anywhere. They didn't need branches in California to serve California customers. They didn't need loan officers in Texas to write Texas mortgages. Everything flowed through Detroit.

Then came 2007, and the first cracks in the housing market. Subprime lenders started failing. Home prices flattened, then fell. By early 2008, the mortgage industry was in free fall. Bear Stearns collapsed. Lehman Brothers filed for bankruptcy. Washington Mutual—the nation's largest savings and loan—was seized by regulators. The mortgage industry lost 500,000 jobs between 2007 and 2009. Over 400 mortgage lenders went out of business. It was an extinction-level event for the industry.

Yet Quicken Loans didn't just survive—it thrived. Revenue grew from $1.6 billion in 2008 to $2.4 billion in 2009. Market share doubled. Employee count actually increased. How? The answer reveals the genius of Gilbert's strategy. First, because Quicken Loans had avoided subprime lending, they had no toxic assets to write down. Their loan portfolio performed better than any major lender. Second, their digital infrastructure meant lower costs—critical when volumes plummeted. Third, and most importantly, when competitors failed, Quicken Loans was ready to grab their customers.

The financial crisis also created an unexpected opportunity: talent acquisition. Suddenly, thousands of experienced mortgage professionals were unemployed. Quicken Loans went on a hiring spree, but with a twist. They only wanted people willing to relocate to Detroit. This wasn't just about convenience—it was a culture filter. Anyone willing to move to Detroit in 2009 (when the city was approaching bankruptcy) was serious about transformation. They weren't looking for just another job; they were looking to build something new.

In 2010, Gilbert made his boldest move yet: relocating Quicken Loans headquarters from the suburbs to downtown Detroit. The city was in shambles. The Renaissance Center stood half-empty. Entire blocks were abandoned. Crime was rampant. Local media called Gilbert crazy. Why move 1,700 employees to a dying city center? Gilbert's answer was simple: "Suburban office parks are where innovation goes to die." He wanted his employees surrounded by energy, even if that energy came from crisis. He wanted them to feel like pioneers, not paper-pushers.

The Detroit move wasn't charity—it was strategy. Gilbert negotiated massive tax breaks. He bought buildings for pennies on the dollar. He created his own security force, his own shuttle system, his own ecosystem. Within two years, Quicken Loans employees occupied 1.2 million square feet of downtown office space. The company became Detroit's gravity well, attracting restaurants, bars, and other businesses to serve its thousands of employees. Gilbert wasn't just building a company; he was building a company town.

By 2012, Quicken Loans had become the country's largest online mortgage lender, originating $70 billion in mortgages. But "online lender" was becoming a meaningless distinction—every lender was moving online. The real differentiator was speed and simplicity. While competitors digitized their existing processes, Quicken Loans redesigned the entire experience from first principles. They introduced something called "MyQL Mobile"—an app that let customers track their loan status, upload documents, and communicate with their banker. Remember, this was 2012, when most banks didn't even have functional mobile apps for checking accounts.

The period from 2013 to 2015 marked peak optimization. Quicken Loans had mastered the existing mortgage process. They could originate loans faster, cheaper, and with higher satisfaction than anyone else. J.D. Power ranked them #1 in customer satisfaction—a position they would hold for the next decade. They were processing over $80 billion in annual volume. They had 10,000 employees, mostly in Detroit. By any measure, they were a massive success.

But Gilbert knew that optimization wasn't innovation. The mortgage process was still fundamentally the same: fill out application, provide documents, wait for underwriting, get approval, close loan. It still took weeks. It still required dozens of documents. It still felt like something from the 20th century. What if, Gilbert wondered, getting a mortgage could be as simple as buying something on Amazon? What if you could be approved in minutes, not weeks? What if the entire process could happen on your phone?

In late 2014, Gilbert gathered his top engineers and product managers for a secret project. The code name was "Project Rocket"—a reference to both speed and Detroit's aerospace history. The goal was audacious: build a completely new mortgage platform from scratch. Not an evolution of existing systems, but a revolution. Native mobile. Real-time decisions. No paper whatsoever. The team had one year to build it, and they would launch it at the biggest possible venue: Super Bowl 50.

As 2015 began, Quicken Loans was at an inflection point. They had won the old game—becoming the best traditional lender who happened to be online. But Gilbert understood that wasn't enough. The next war wouldn't be against other mortgage lenders. It would be against consumer expectations set by Uber, Amazon, and Netflix. The mortgage industry's digital moment had arrived, and Quicken Loans was about to light the fuse.

IV. The Rocket Mortgage Revolution (2015-2020)

The conference room at Quicken Loans headquarters was silent as the commercial ended. It was November 2015, and Dan Gilbert had just shown his leadership team the Super Bowl ad that would air in three months. The spot featured a couple getting approved for a mortgage on their phone while sitting on their couch, completing the entire application during a single commercial break. The tagline: "Push Button, Get Mortgage." The Chief Risk Officer finally spoke: "Dan, if this actually works, we'll be overwhelmed. If it doesn't work, we'll be a laughingstock." Gilbert's response: "Perfect. Ship it."

Rocket Mortgage launched to the public on November 7, 2015, but the real detonation came on February 7, 2016—Super Bowl 50. The ad, which cost $5 million for 30 seconds of airtime, was a declaration of war on the traditional mortgage industry. Within one minute of the commercial airing, Rocket Mortgage's servers were handling 1,000 applications per second. By halftime, they had received more applications than most lenders process in a month. The system held. Every application was processed. The revolution had begun.

What made Rocket Mortgage revolutionary wasn't just speed—it was the complete reimagination of the mortgage experience. Traditional mortgage applications asked hundreds of questions, many redundant or irrelevant. Rocket Mortgage used conditional logic to ask only what was necessary. If you were buying a single-family home, it didn't ask about condo association fees. If you were salaried, it didn't ask about business income. The average application went from 300+ fields to about 40. But here's the clever part: behind the scenes, Rocket Mortgage was pulling data from thousands of sources—credit bureaus, employment databases, asset verification systems—filling in the blanks without customer input.

The technology stack was a marvel of modern engineering. While the front-end was clean and simple, the back-end orchestrated a complex symphony of API calls, data validation, and risk assessment. When a customer entered their employer, Rocket Mortgage instantly verified employment through The Work Number database. When they entered their bank, it connected via Plaid or Yodlee to pull statements. The customer saw a simple interface; behind it ran algorithms processing thousands of data points in real-time.

In its first full year, Rocket Mortgage funded $7 billion in loans. By 2017, that number hit $25 billion. By 2018, $50 billion. The growth was exponential because Rocket Mortgage solved the industry's fundamental problem: customer acquisition cost. Traditional lenders spent $5,000-$7,000 to acquire each customer through branches, loan officers, and marketing. Rocket Mortgage's digital acquisition cost was under $2,000 and dropping. They could offer better rates, spend more on technology, and still maintain higher margins than traditional competitors.

The marketing strategy was equally revolutionary. While competitors advertised rates and terms, Rocket Mortgage sold simplicity and speed. Their 2017 Super Bowl ad featured a translation app that turned complex mortgage jargon into plain English. The 2018 ad showed Keegan-Michael Key explaining that getting a mortgage was now "so simple, you could do it right here"—in increasingly absurd locations. The message was consistent: mortgages were no longer scary, complex, or time-consuming. They were as easy as ordering pizza.

But the real validation came from J.D. Power. In 2016, Rocket Mortgage ranked #1 in customer satisfaction. In 2017, #1 again. 2018, 2019—the same. This wasn't just beating other online lenders; this was beating everyone—banks, credit unions, traditional mortgage companies. The Net Promoter Score, a measure of customer loyalty, was 75—unheard of in financial services where 30 was considered good. Customers weren't just satisfied; they were evangelical, referring friends and family at rates the industry had never seen.

January 2018 marked a historic milestone: Quicken Loans, powered by Rocket Mortgage, became the nation's largest mortgage lender, surpassing Wells Fargo. A Detroit-based online lender had defeated the nation's third-largest bank. The symbolism was perfect—the future overtaking the past, technology defeating tradition, Detroit rising while San Francisco stagnated. Gilbert celebrated by buying every employee a pair of Nikes with "PUSH BUTTON GET MORTGAGE" printed on them.

The next innovation came in 2019 when Rocket Mortgage became the first lender to perform electronic closings in all 50 states. This was harder than it sounds. Every state had different laws about notarization, witnessing, and recording. Some required wet signatures. Others mandated in-person appearance. Rocket Mortgage's legal and technology teams spent two years navigating this regulatory maze, building relationships with state regulators, and developing systems that satisfied everyone. The result: customers could close their mortgage from their couch, signing on their phone or tablet.

That same year, Rocket Mortgage doubled its origination volume to $145 billion. To put that in perspective, they were now originating more mortgages than the entire industry did online just five years earlier. The company had 19,000 employees, mostly in Detroit, making it the city's second-largest employer after the healthcare system. Downtown Detroit, once a ghost town, was now buzzing with activity, largely due to the thousands of Rocket employees flooding coffee shops, restaurants, and bars.

The platform strategy was also taking shape. In 2017, Quicken Loans launched Rocket Homes, a real estate search platform. In 2018, Rocket Loans began offering personal loans using the same simplified application process. The vision was becoming clear: Rocket wouldn't just be a mortgage company but a comprehensive financial services platform. Single sign-on across all services. Data shared between applications. A customer who got a mortgage through Rocket would naturally turn to them for personal loans, real estate searches, and eventually, wealth management.

By early 2020, Rocket Mortgage was firing on all cylinders. They had just closed their best year ever. Customer satisfaction was at an all-time high. The technology platform was mature and scaling beautifully. Plans were underway for an IPO that would value the company at $30-40 billion. Then, in March 2020, COVID-19 shut down the world. What happened next would transform Rocket Mortgage from a successful disruptor into a financial juggernaut.

The Federal Reserve slashed interest rates to near zero. Suddenly, every homeowner in America wanted to refinance. Traditional lenders, with their branch-based models and paper processes, couldn't handle the volume—especially with offices closed and employees working from home. But Rocket Mortgage was built for this moment. Their entire operation was digital. Their employees had laptops and could work from anywhere. Their customers never needed to visit an office. As traditional lenders struggled, Rocket Mortgage scaled up, processing more applications in Q2 2020 than they had in all of 2015.

The numbers were staggering. Q2 2020 production: $72 billion. Q3 2020: $89 billion. The company was on pace to originate over $300 billion in 2020—more than double their 2019 volume. Profit margins expanded as the refinance boom reduced customer acquisition costs to near zero. Everyone wanted to refinance, and Rocket Mortgage was the easiest way to do it. The company was printing money, and Gilbert knew this was the perfect time to go public. The window was open, the numbers were spectacular, and the story was compelling. In August 2020, Rocket Companies would debut on the New York Stock Exchange, marking the end of one chapter and the beginning of another.

V. The IPO Story: Going Public in a Pandemic (2020)

Jay Farner, CEO of Rocket Companies, rang the opening bell at the New York Stock Exchange on August 6, 2020—virtually. He was actually in Detroit, standing in front of a replica bell, with hundreds of Rocket employees watching on screens throughout the company's headquarters. It was a perfect metaphor for the moment: a digital company going public during a pandemic that had forced everything online. The stock, trading under the ticker "RKT," opened at $18 per share and immediately jumped to $21.50. By day's end, Rocket Companies was worth $43 billion, making it the second-largest IPO of 2020.

The road to IPO had been anything but smooth. Initial plans called for going public in March 2020, with a traditional roadshow where management would fly to major cities, wine and dine institutional investors, and build demand for the offering. Then COVID hit. Markets crashed. The IPO window slammed shut. By April, with the mortgage market in chaos and uncertainty everywhere, going public seemed impossible. But then something unexpected happened: the mortgage boom of a lifetime.

The Federal Reserve's emergency rate cuts had triggered a refinancing tsunami. Mortgage applications hit levels not seen since the 2003 refinance boom. But this time was different. In 2003, customers had to visit branches, fill out paper applications, and wait weeks for approval. In 2020, they could do everything from their couch. Rocket Mortgage was perfectly positioned—a digital platform built for exactly this moment. Q2 2020 results were eye-popping: $72.5 billion in origination volume, $3.5 billion in revenue, and $2.8 billion in net income. Yes, billion with a B in profit—in a single quarter.

The IPO prospectus, filed in July, told a compelling story. Rocket Companies wasn't just Quicken Loans anymore. It was a platform company with multiple businesses: Rocket Mortgage (mortgages), Rocket Homes (real estate), Rocket Loans (personal loans), Rocket Auto (car sales), and Amrock (title insurance). The company had originated over $1.5 trillion in mortgages since 1985. It was the #1 retail mortgage lender, #1 direct-to-consumer lender, and #1 in customer satisfaction. The numbers spoke for themselves: 2019 revenue of $5.1 billion with $893 million in profit. 2020 was tracking to potentially triple those numbers.

But the structure of the IPO raised eyebrows. Rocket Companies would go public with a dual-class share structure that gave Dan Gilbert 79% voting control despite owning only 20% of the economic interest. Class D shares, owned by Gilbert, carried 10 votes each. Class A shares, available to public investors, carried one vote each. This meant public shareholders were essentially silent partners in Gilbert's empire. Some institutional investors balked. Corporate governance experts criticized the structure. Gilbert's response was characteristically blunt: "If you don't like it, don't buy it."

The pricing drama was intense. Initial expectations called for a range of $20-22 per share. But demand was softer than expected. Large institutional investors worried about the sustainability of the refinance boom. What would happen when rates rose? How would Rocket perform in a purchase market versus a refinance market? The company's dependence on refinancing—which made up 70% of volume—was a red flag. On August 5, the night before trading, the price was cut to $18, below the initial range.

Despite the pricing disappointment, the IPO raised $1.8 billion, with an unspecified portion designated for Detroit community development. This wasn't just PR—it was central to Rocket's identity. The company's success was intertwined with Detroit's recovery. Gilbert had invested over $5.6 billion in Detroit real estate and businesses. Rocket Companies employed 19,000 people in the city. The IPO prospectus mentioned Detroit 153 times. This wasn't a Silicon Valley unicorn or a Wall Street titan—this was a Detroit company, and proud of it.

The first day of trading was volatile. The stock opened at $21.50, peaked at $22.75, and closed at $21.51—a 19.5% gain. Volume was massive: 71 million shares changed hands. Retail investors, many of them Rocket Mortgage customers, piled in through Robinhood and other trading apps. The narrative was irresistible: a technology company disrupting traditional banking, riding a massive refinance wave, led by a billionaire who rebuilt Detroit. Within weeks, the stock hit $34.

But institutional investors remained skeptical. The refinance boom wouldn't last forever. Interest rates would eventually rise. Competition was intensifying from both traditional banks investing in technology and new fintech startups. United Wholesale Mortgage, Rocket's primary competitor, was also going public via SPAC. The mortgage industry was notoriously cyclical. When rates rose and refinancing dried up, margins would compress and volumes would plummet. The bears argued Rocket was going public at peak earnings.

The Q3 2020 earnings report, released in November, seemed to vindicate the bulls. Revenue hit $4.5 billion. Net income was $2.8 billion. Origination volume was $89 billion—more than most lenders originate in a year. The company was generating cash at an unprecedented rate. But CEO Jay Farner's comments on the earnings call were telling: "We're not just benefiting from market conditions. We're taking market share." The implication was clear—even when the refinance boom ended, Rocket would emerge stronger.

The dual-class structure proved its worth almost immediately. In November 2020, activist investor Kenneth Griffin's Citadel took a significant position and began agitating for changes. With a normal share structure, this might have led to board battles and strategic disruption. But with Gilbert controlling 79% of votes, Citadel was powerless. Rocket could focus on long-term strategy rather than quarterly earnings. This would prove crucial as the company embarked on its next phase: building a comprehensive fintech ecosystem.

The IPO also triggered a cultural shift within Rocket. As a private company, equity compensation had been limited to senior executives. Now, thousands of employees received stock options. The company instituted broad-based equity grants, making every employee an owner. This wasn't just about retention—it was about alignment. Gilbert wanted employees thinking like owners, focused on long-term value creation rather than short-term bonuses.

By December 2020, Rocket Companies had originated $320 billion in mortgages for the year—double its 2019 volume and more than any lender in American history. The stock had settled into a range between $19-23, roughly where it had IPO'd. The refinance boom was showing signs of slowing, but purchase mortgages were picking up. The company was using its windfall profits to invest aggressively in technology, marketing, and new business lines.

As 2020 ended, Rocket Companies faced a classic innovator's dilemma. They had disrupted the mortgage industry with superior technology and customer experience. Now they needed to prove they were more than a one-trick pony. The next chapter would involve expanding beyond mortgages, building a true financial services ecosystem, and navigating the transition from a refinance to a purchase market. The IPO had given them capital and currency for acquisitions. The question was: could a mortgage company become a fintech platform? The answer would reshape not just Rocket, but the entire financial services industry.

VI. The Platform Play: From Mortgage to Fintech Ecosystem (2020-Present)

The email from Dan Gilbert landed in every Rocket employee's inbox at 6 AM on May 12, 2021. Subject line: "Quicken Loans is Dead. Long Live Rocket." After 36 years, the Quicken Loans brand was being retired. Everything would be unified under the Rocket brand—Rocket Mortgage, Rocket Homes, Rocket Money, Rocket Loans. "We're not a mortgage company that happens to have other businesses," Gilbert wrote. "We're a fintech platform that happens to do mortgages really well." The rebrand wasn't cosmetic. It was a declaration of strategic intent.

The vision was ambitious: create a single platform where Americans could manage their entire financial life. Find a home on Rocket Homes. Finance it with Rocket Mortgage. Close through Amrock. Manage your finances with Rocket Money. Need a personal loan? Rocket Loans. Want solar panels? Rocket Solar. The key innovation was a single sign-on across all services. One account, one login, one unified experience. Your data from one service would enhance your experience in others. It was the Amazon Prime model applied to financial services.

The first major piece of the ecosystem puzzle came in December 2021 when Rocket acquired Truebill for $1.275 billion. Truebill was a personal finance app that helped users track spending, cancel unwanted subscriptions, and negotiate bills. With 2.5 million users, it brought something Rocket desperately needed: high-frequency engagement. Mortgages are episodic—most people get one every 5-7 years. But personal finance is daily. By acquiring Truebill (quickly rebranded as Rocket Money), Rocket gained a persistent relationship with consumers.

The strategic logic was compelling. Rocket Money users provided continuous data about their financial health—income, spending patterns, savings rates. This data could be used to pre-qualify them for mortgages, identify when they were ready to buy a home, and offer relevant financial products at the perfect moment. Instead of spending thousands to acquire a mortgage customer, Rocket could nurture them from within their ecosystem. Customer acquisition costs could drop from $3,000 to essentially zero.

The integration went deeper than just cross-selling. Rocket Money's data enhanced Rocket Mortgage's underwriting. Traditional lenders looked at point-in-time snapshots—credit score, income verification, asset statements. Rocket Money provided longitudinal data—months or years of actual financial behavior. This allowed more accurate risk assessment and potentially better rates for qualified borrowers. It was a data moat that traditional lenders couldn't replicate.

Rocket Homes, launched in 2017, was evolving from a search portal to a full-service real estate platform. By 2022, it had partnerships with over 3,000 real estate agents and was generating $100 million in annual revenue. But the real innovation was the integration with Rocket Mortgage. Home shoppers could get pre-approved instantly, see exactly what they could afford, and make offers with confidence. When they found a home, their pre-approval seamlessly converted to a full mortgage application. The friction between home search and home purchase was disappearing.

The platform strategy faced a major test in 2022 when interest rates began rising rapidly. The Federal Reserve, fighting inflation, raised rates from near zero to over 5% in just 18 months. The refinance market evaporated almost overnight. Rocket's origination volume plummeted from $351 billion in 2021 to $133 billion in 2022. The stock price collapsed from a high of $45 to under $6. Critics argued the platform strategy was a distraction from a fundamentally broken mortgage business.

But the ecosystem proved its value during this stress test. While mortgage originations fell 62%, Rocket Money grew users by 50%. Rocket Homes maintained steady traffic despite the frozen housing market. Rocket Loans expanded into new products like home equity lines of credit. The platform businesses provided stability while the mortgage business weathered the storm. More importantly, they maintained customer relationships that would prove valuable when the market recovered.

The competitive landscape was also validating the platform approach. United Wholesale Mortgage, Rocket's primary competitor in wholesale lending, remained focused solely on mortgages and saw similar volume declines without offsetting growth. Traditional banks like Wells Fargo and JPMorgan had multiple business lines but couldn't integrate them into a unified experience. Fintech startups like Better.com and LoanDepot tried to copy Rocket's digital mortgage model but lacked the resources to build broader platforms.

By 2023, the platform strategy was generating measurable results. Cross-sell rates between Rocket businesses exceeded 20%. A Rocket Money user was 3x more likely to choose Rocket Mortgage when buying a home. Rocket Homes users who got pre-approved through Rocket Mortgage closed 40% faster than those using other lenders. The lifetime value of a platform customer was $15,000 versus $3,000 for a mortgage-only customer. The network effects were finally kicking in.

The technology infrastructure supporting the platform was equally impressive. Rocket had built a unified data lake containing information from all its businesses. Machine learning models analyzed patterns across millions of customers to identify opportunities, predict behavior, and personalize experiences. When a Rocket Money user's savings hit a threshold suggesting they could afford a home, they received tailored content about homebuying. When a Rocket Mortgage customer's home value increased, they were offered a home equity loan. The platform was becoming prescient.

The cultural transformation was just as significant. Rocket employees no longer thought of themselves as mortgage professionals but as platform builders. Engineers who once optimized mortgage workflows were now building connections between services. Product managers thought about customer journeys spanning years, not just transactions. Sales teams sold solutions, not products. The company hired talent from Amazon, Google, and Meta—people who understood platforms, not just financial services.

In 2024, the platform expanded into adjacent verticals. Rocket Insurance offered homeowners and auto insurance. Rocket Connect provided internet and utility connections for new homeowners. Rocket Solar financed and installed residential solar systems. Each addition made the platform stickier and more valuable. The vision was becoming reality: a single destination for all consumer financial needs.

The numbers by late 2024 told the story. Rocket Companies had 5 million active platform users, up from essentially zero in 2020. Platform businesses generated $500 million in annual revenue, growing 50% yearly. The contribution margin of platform customers was 3x that of mortgage-only customers. Most importantly, platform customers showed 80% lower churn rates. They weren't just customers; they were locked into an ecosystem.

But the biggest validation of the platform strategy would come in early 2025 with two blockbuster acquisitions that would fundamentally reshape not just Rocket, but the entire real estate and mortgage industry. The platform wasn't just growing—it was becoming the foundation for industry consolidation.

VII. AI & Technology Innovation: The Next Generation Platform

Inside Rocket's Detroit headquarters, in a room they call the "AI War Room," 50 engineers were working on a problem that had plagued the mortgage industry for decades: earnest money deposits. These deposits—typically 1-3% of a home's purchase price—require manual verification, often taking days and involving multiple phone calls. In Q2 2024, Rocket's new agentic AI system began processing these automatically. Within three months, it was handling 80% of all EMDs without human intervention, saving 20,000 hours annually. But this was just the beginning of Rocket's AI transformation.

The scale of Rocket's data advantage is staggering: 65 million call logs annually, 10 petabytes of stored data, 20 million customer interactions monthly. Every phone call is transcribed and analyzed. Every customer click is tracked. Every document is digitized and parsed. This isn't just big data—it's the largest proprietary dataset in mortgage history. While competitors were still debating whether to use AI, Rocket was already three generations deep into custom large language models trained specifically on mortgage interactions.

The breakthrough came with what Rocket calls "Rocket Logic"—an AI system that doesn't just process applications but actually understands them. When a customer uploads a pay stub, Rocket Logic doesn't just extract the income number. It understands employment patterns, identifies inconsistencies, predicts future income stability, and flags potential issues before they become problems. It can read between the lines of bank statements, identifying regular deposits that represent income even if they're not from traditional employment.

Consider the complexity Rocket Logic handles: A mortgage application involves over 500 potential documents, 2,000 data fields, and regulations that vary by state, county, and even zip code. Traditional lenders employ armies of processors to manage this complexity. Rocket Logic does it in seconds, with higher accuracy than human processors. When it encounters something it doesn't understand, it doesn't just flag it for human review—it learns from the resolution, becoming smarter with every interaction.

The customer experience transformation was even more dramatic. In 2015, Rocket Mortgage's "8-minute mortgage" was revolutionary. By 2024, with AI assistance, qualified customers could get conditional approval in under 60 seconds. The AI pre-populated applications using data from thousands of sources, asked clarifying questions in natural language, and provided instant feedback on how to improve approval odds. It wasn't just faster—it was conversational, adaptive, and surprisingly human.

The AI system's natural language processing capabilities were particularly impressive. Customers could ask questions like "What would my payment be if I put down $50K instead of $40K?" or "How much house can I afford if I pay off my car loan?" The AI understood context, remembered previous conversations, and provided personalized advice. It could explain complex mortgage concepts in simple terms, adapting its communication style to each customer's sophistication level.

Behind the scenes, Rocket's AI was revolutionizing risk assessment. Traditional underwriting relied on rigid rules—credit score above X, debt-to-income below Y. Rocket's machine learning models analyzed millions of loan outcomes to identify subtle patterns humans couldn't see. They discovered that certain combinations of factors—like consistent rent payment history plus rising bank balances—predicted loan performance better than credit scores alone. This allowed Rocket to approve loans others rejected while maintaining lower default rates.

The fraud detection capabilities were equally advanced. The AI system analyzed thousands of signals to identify potential fraud—unusual document formats, inconsistent data patterns, suspicious timing of deposits. It could detect doctored bank statements that looked perfect to human eyes. In 2024 alone, it prevented an estimated $200 million in fraudulent loans. But it did this invisibly—legitimate customers never knew they were being screened, experiencing only smooth, fast approval.

Rocket's investment in AI infrastructure was massive. They employed over 200 data scientists and ML engineers. They built custom GPU clusters for model training. They developed proprietary tools for model governance and bias detection. While competitors outsourced to generic AI providers, Rocket built everything in-house. This wasn't just about capability—it was about competitive advantage. Every model was trained on Rocket's unique data, optimized for Rocket's specific use cases.

The operational efficiency gains were transforming Rocket's unit economics. Cost per loan fell from $2,800 in 2020 to under $1,500 in 2024. Processing time dropped from days to hours. Error rates fell by 90%. But the real gain was in human productivity. Loan officers, freed from paperwork, could focus on customer relationships. Underwriters, augmented by AI, could handle 5x more volume. The same workforce that processed $320 billion in 2020 could now handle $500 billion.

The AI strategy extended beyond mortgages. Rocket Money used machine learning to identify subscription payments users had forgotten about, negotiate better rates with service providers, and predict which users were ready for mortgages. Rocket Homes used computer vision to analyze listing photos, estimate home values, and identify properties likely to sell quickly. Every Rocket business was becoming AI-powered, creating synergies across the platform.

The competitive moat was widening rapidly. Every customer interaction made Rocket's AI smarter. Every loan outcome improved its risk models. Every document processed enhanced its understanding. This was a classic data network effect—the more customers Rocket served, the better its AI became, which attracted more customers, creating a virtuous cycle competitors couldn't break. Traditional lenders, with their fragmented systems and limited data, were falling further behind.

Looking forward, Rocket's AI roadmap was even more ambitious. They were developing systems that could conduct entire mortgage consultations via natural conversation. Imagine calling Rocket, describing your situation in plain English, and having AI guide you through the entire process—from pre-qualification to closing—without ever filling out a form. They were building predictive models that could identify life events—marriage, job changes, growing families—and proactively offer relevant financial products.

The ethical considerations weren't ignored. Rocket established an AI Ethics Board to ensure models were fair and unbiased. They conducted regular audits to detect discrimination. They made their approval logic explainable—customers could understand why they were approved or denied. This transparency was both ethical and strategic. As regulators scrutinized AI in financial services, Rocket's responsible approach positioned them as industry leaders.

By late 2024, Rocket's AI capabilities had become so advanced that they were considering a new business: licensing their technology to other lenders. Rocket Logic could become the AWS of mortgage technology—a platform others built upon. This would transform Rocket from a lender who used technology into a technology company that happened to lend. The implications were profound: higher margins, recurring revenue, and a path to dominating not just mortgage origination but mortgage infrastructure.

The innovation pipeline showed no signs of slowing. Rocket was experimenting with generative AI to create personalized home-buying guides. They were using computer vision to assess property condition from photos. They were building predictive models to forecast home values and optimize pricing. Every month brought new capabilities, new efficiencies, new advantages. The gap between Rocket and traditional lenders wasn't just widening—it was becoming unbridgeable.

As one senior engineer put it: "We're not trying to digitize the mortgage process. We're trying to make it disappear. The perfect mortgage is one the customer doesn't even notice happening." With AI advancing at exponential rates and Rocket's data advantage compounding daily, that vision was closer than anyone imagined.

VIII. Strategic Moves & Market Evolution (2025)

The announcement came at 6 AM Eastern on March 3, 2025, timed to hit before market open. Rocket Companies would acquire Redfin for $1.75 billion in stock and Mr. Cooper, the nation's largest mortgage servicer, for $9.4 billion in stock. Combined, these deals would create a vertically integrated real estate and financial services giant worth over $50 billion. Dan Gilbert, speaking from Detroit, called it "the final piece of our platform puzzle." Wall Street was stunned. Competitors were terrified. The mortgage industry would never be the same.

The Redfin acquisition made immediate strategic sense. Redfin brought 2,600 real estate agents, proprietary home search technology, and most importantly, 50 million monthly active users. These weren't just browsing homes casually—they were high-intent buyers and sellers, exactly the customers Rocket wanted. The synergies were obvious: Redfin agents would naturally recommend Rocket Mortgage. Rocket's pre-approval would integrate seamlessly into Redfin's search. The combined entity would control the customer from first search to final closing.

But the Mr. Cooper deal was the real bombshell. Mr. Cooper serviced $1.1 trillion in mortgages—loans they collected payments on for other lenders. This servicing portfolio generated steady, predictable cash flow regardless of interest rates. When origination markets were hot, Rocket would make money writing loans. When markets cooled, Mr. Cooper's servicing would provide stability. It was the ultimate hedge, turning Rocket from a cyclical business into an all-weather platform.

The servicing asset was more valuable than it appeared. Every month, Mr. Cooper interacted with 5.5 million homeowners collecting payments. These touchpoints were opportunities—to offer refinancing, home equity loans, insurance, solar panels. Traditional servicers treated these interactions as cost centers. Rocket would transform them into revenue generators. Imagine getting your monthly mortgage statement with a personalized offer to refinance at a lower rate, powered by AI that knew exactly when you'd benefit.

To fund these acquisitions, Rocket issued $4 billion in senior notes—a massive debt raise that demonstrated institutional confidence. The terms were favorable: 5.5% interest in a 6% rate environment. Investors saw what Gilbert saw: these weren't risky acquisitions but strategic consolidation in a fragmenting industry. The mortgage business was undergoing its biggest transformation since the financial crisis, and Rocket was positioning itself to emerge as the dominant platform.

The corporate restructuring was equally significant. Rocket collapsed its complex "Up-C" structure, simplifying from four share classes to two. This wasn't just administrative cleanup—it was preparation for future moves. The simplified structure made Rocket more attractive to potential acquirers or merger partners. Speculation ran wild: Would Amazon buy Rocket to enter financial services? Would JPMorgan acquire them to leap forward in digital capabilities? Gilbert wasn't selling, but he was keeping options open.

The competitive response was swift but inadequate. United Wholesale Mortgage announced a partnership with various real estate brokerages—a pale imitation of owning Redfin. Wells Fargo accelerated its digital transformation—years behind Rocket's capabilities. Better.com, once a promising competitor, was laying off staff and burning cash. The industry was consolidating around two models: massive scaled platforms like Rocket, or niche specialized lenders. Everyone in between was getting crushed.

The integration plans were ambitious but achievable. Redfin's technology would be rebuilt on Rocket's platform within 18 months. Mr. Cooper's servicing operations would migrate to Rocket's systems within two years. The combined entity would operate from a single technology stack, enabling unprecedented efficiency and customer experience. This wasn't bolt-on M&A—it was fundamental transformation.

The human capital implications were profound. Rocket would add 10,000 employees from these acquisitions, making it one of America's largest financial services employers. But more importantly, they were acquiring talent—engineers who understood real estate technology, servicing experts who knew the intricacies of portfolio management, data scientists who could optimize new business lines. This was acquisition as talent strategy.

Market timing was perfect. The housing market was stabilizing after two years of chaos. Interest rates had peaked and were beginning to decline. Home prices had moderated but not crashed. Existing homeowners had massive equity—over $35 trillion nationally. The conditions were ideal for both purchase mortgages and home equity lending. Rocket was positioned to capture both sides of the market.

The regulatory approvals would take time, but Rocket was confident. They had good relationships with regulators, having operated conservatively through multiple cycles. The acquisitions didn't create antitrust issues—even combined, Rocket would have less than 15% market share. If anything, regulators welcomed consolidation in a fragmented industry with thousands of small, often undercapitalized lenders.

The financial projections were compelling. Combined 2025 revenue would exceed $15 billion. EBITDA margins would expand from 15% to 20% due to scale efficiencies. The platform would serve 10 million customers annually. Most importantly, customer lifetime value would triple as the average customer used three or more Rocket services. This wasn't just growth—it was transformation into a fundamentally different business model.

The strategic vision was becoming clear. Rocket wasn't trying to be the biggest mortgage lender—they were building the operating system for American homeownership. Every touchpoint from searching for a home to paying it off would run through Rocket's platform. They would know more about American housing than any other company. That data advantage would compound, creating an unassailable moat.

The announcement of RocketRentRewards in July 2025 showed the platform's evolution. This program offered renters up to $5,000 toward homeownership for every year they rented, funded by partnerships with property managers who paid Rocket for tenant acquisition. It was genius: capturing customers years before they bought homes, building loyalty through tangible benefits, and creating a pipeline of future buyers. Traditional lenders could never match this—they lacked the platform to engage renters.

By mid-2025, the transformation was evident in every metric. Rocket's stock had recovered to $30, up 400% from its 2022 lows. Customer satisfaction scores hit all-time highs. Employee satisfaction surged as people realized they were building something historic. Even Detroit was benefiting—the combined company would add 5,000 jobs to the city, making Rocket its largest private employer.

The bear case still existed. Integration risk was real—many M&A deals failed in execution. The mortgage industry remained cyclical. Regulatory scrutiny was increasing. Competition from both banks and tech companies was intensifying. But Gilbert had answers for everything. Integration would be methodical. Servicing provided cycle protection. Compliance was a competitive advantage. Competition validated the market opportunity.

As Q3 2025 began, Rocket Companies looked nothing like the mortgage broker Dan Gilbert had founded 40 years earlier. It was a technology platform, a data powerhouse, a real estate marketplace, a financial services ecosystem. The acquisitions of Redfin and Mr. Cooper weren't the end of transformation—they were the beginning of dominance. The next decade would determine whether Rocket became the Amazon of financial services or remained merely a very successful mortgage company. Based on the moves of 2025, betting against Gilbert seemed unwise.

IX. Detroit & Social Impact: The Hometown Story

The view from Dan Gilbert's office on the 10th floor of One Campus Martius shows a Detroit that shouldn't exist. Where abandoned buildings once stood, there are now tech offices, trendy restaurants, and bike lanes. The streetscape bustles with 30,000 Rocket employees and contractors who work downtown—a number that would have been laughable in 2010 when Gilbert first moved Quicken Loans from the suburbs. This isn't just a corporate headquarters story. It's the largest urban revitalization project by a private company in American history.

The numbers are staggering. Since 2010, Gilbert's family of companies has invested over $5.6 billion in Detroit real estate and businesses. They own or operate over 100 properties totaling 19 million square feet in downtown Detroit. But this isn't charitable giving—it's strategic capitalism. Gilbert understood something others missed: Detroit's collapse had created a once-in-a-generation arbitrage opportunity. Talent was cheap, real estate was basically free, and the city was desperate enough to offer almost anything to attract business.

The initial move in 2010 brought 1,700 employees downtown. Gilbert literally paid people to relocate—offering $20,000 forgivable loans to employees who bought homes in the city, $3,500 per year to those who rented. The suburban workforce was skeptical. Downtown Detroit had a 50% commercial vacancy rate. Crime was rampant. The city was three years from bankruptcy. Parents worried about their kids commuting to work. Gilbert's response was to buy the buildings around his headquarters, hire private security, and create a safe zone that would expand block by block.

The strategy was methodical. First, consolidate Rocket employees in a dense footprint around Campus Martius Park. Second, attract retail and restaurants to serve those employees. Third, develop residential units to house them. Fourth, incubate startups and attract other companies to create a critical mass. Fifth, expand the zone of safety and development outward. It was SimCity in real life, with Gilbert as the master planner.

By 2013, when Detroit declared bankruptcy—the largest municipal bankruptcy in U.S. history—Gilbert's commitment deepened rather than wavered. While others saw catastrophe, he saw opportunity. The bankruptcy would clear decades of debt and dysfunction. The emergency manager could make decisions politicians couldn't. The national attention would attract resources and talent. Gilbert doubled down, buying the iconic Book Tower, the historic Greektown Casino, and dozens of other properties at fire-sale prices.

The Rocket Community Fund, announced in 2021, committed $500 million over 10 years to Detroit-focused initiatives. But this wasn't traditional corporate philanthropy. The fund invested in job training programs that created Rocket's future workforce. It funded internet access initiatives that enabled remote work. It supported entrepreneurship programs that built Rocket's vendor ecosystem. Every dollar spent had both social impact and business logic.

The Connect 313 Fund, launched with IPO proceeds, aimed to provide internet access to every Detroit household. Why would a mortgage company care about broadband? Because digital literacy was essential for online mortgage applications. Because connected households were potential customers. Because Rocket's employees needed connected communities to thrive. The $20 million investment would generate both social returns and customer acquisition benefits that traditional marketing could never achieve.

The talent strategy was particularly clever. Rocket didn't just hire Detroiters—they manufactured them. The company created training programs that took people with no technical background and turned them into mortgage bankers, software developers, and data analysts. They partnered with local universities to create specialized curricula. They funded coding bootcamps and apprenticeship programs. By 2025, over 40% of Rocket's Detroit workforce had come through these programs—people who couldn't get these jobs elsewhere, creating loyalty that money couldn't buy.

The real estate empire became self-reinforcing. As Rocket grew, it needed more space, which meant buying more buildings, which meant more investment in the surrounding area, which attracted more businesses and residents, which made Detroit more attractive to talent, which helped Rocket grow. By 2025, Gilbert's Bedrock real estate company had developed over 2 million square feet of office space, 2,000 residential units, and 500,000 square feet of retail—all centered around Rocket's footprint.

The cultural impact was equally significant. Rocket didn't just bring jobs to Detroit—it brought energy, optimism, and pride. The company's success changed the narrative about Detroit from "dying city" to "comeback city." Young professionals who would never have considered Detroit were moving there for opportunities. The downtown population grew from 7,000 in 2010 to over 40,000 in 2025. Restaurants had waiting lists. Apartments had bidding wars. Detroit was becoming, improbably, cool.

But this wasn't without controversy. Critics accused Gilbert of creating a "tale of two cities"—a thriving downtown surrounded by struggling neighborhoods. Gentrification displaced long-time residents who couldn't afford rising rents. The city's tax breaks to Gilbert's companies meant less revenue for services. Some called it "Gilbertville"—a company town where one man had too much power. These criticisms had merit, but they also missed the counterfactual: without Gilbert's investment, downtown Detroit might have completely collapsed.

The symbiotic relationship between Rocket and Detroit created unique advantages. Rocket's cost structure was 30-40% lower than competitors in expensive coastal cities. A software engineer who cost $200,000 in San Francisco cost $120,000 in Detroit. Office space that cost $100 per square foot in New York cost $30 in Detroit. But employees got more for less—they could buy homes, have short commutes, and enjoy a quality of life impossible in tier-one cities.

The Detroit location also shaped company culture. This wasn't a place for entitled tech bros or Wall Street wolves. Rocket employees had Midwest work ethic—they showed up, worked hard, and didn't complain. They understood struggle and appreciated opportunity. They were builders, not financial engineers. The company's "For More Than Profit" motto wasn't just marketing—it reflected a genuine belief that business success should create community benefit.

The COVID-19 pandemic tested but ultimately validated the Detroit strategy. While San Francisco and New York saw massive exodus as remote work enabled geographic flexibility, Detroit's population remained stable. Rocket employees, many of whom owned homes and had deep community ties, didn't flee. The company's investment in the city created resilience that pure economic incentives couldn't match.

By 2025, Rocket's impact on Detroit was undeniable. The company directly employed 24,000 people in the city and indirectly supported another 50,000 jobs. It generated over $500 million in annual tax revenue. It had catalyzed over $10 billion in additional investment from other companies. Downtown occupancy rates exceeded 95%. The city's credit rating had improved from junk to investment grade. Detroit was no longer synonymous with decay—it was becoming a model for urban revival.

The next phase of Gilbert's Detroit vision was even more ambitious. Plans were underway for a massive mixed-use development on the site of the former Hudson's department store—Detroit's answer to Hudson Yards. The project would include Michigan's tallest building, 1.5 million square feet of office space, and 500 residential units. Rocket would anchor the development, but the goal was to attract other major companies—creating a true central business district rather than a Rocket company town.

The lesson from Rocket's Detroit story was profound: geography could be a competitive advantage if you were willing to create your own ecosystem. While competitors fought for expensive talent in saturated markets, Rocket built its own talent pipeline in a grateful city. While others paid premium prices for real estate, Rocket bought at the bottom and created value through development. While competitors dealt with entitled employees and difficult regulators, Rocket enjoyed loyal workers and supportive government. Detroit wasn't just where Rocket happened to be located—it was integral to what Rocket had become.

X. Business Model & Unit Economics

The math behind Rocket Companies is deceptively simple: originate mortgages at roughly 300 basis points (3%) of loan value, service them for 30 basis points annually, and cross-sell other products to maximize lifetime value. But executing this model at scale—processing over $300 billion in annual volume while maintaining industry-leading margins—requires operational excellence that competitors have proven unable to match. Let's peek under the hood at one of the most efficient money-making machines in financial services.

Rocket operates through two primary segments that account for 94% of net revenue: Direct to Consumer (D2C) and Partner Network. The D2C segment, representing about 70% of volume, is where customers come directly to Rocket through advertising, word-of-mouth, or the platform ecosystem. These loans generate the highest margins—typically 350-400 basis points—because Rocket controls the entire experience and doesn't pay referral fees. The Partner Network, the remaining 30%, involves relationships with real estate agents, financial advisors, and other referral sources who receive compensation for sending clients to Rocket.

The unit economics of a D2C mortgage are remarkable. Average loan size in 2024 was $285,000. At a 375 basis point margin, that generates $10,687 in revenue. The variable cost to process that loan—including credit checks, appraisals, and processing—is roughly $1,500 thanks to AI and automation. Sales and marketing allocation adds another $2,000. That leaves approximately $7,000 in contribution margin per loan before fixed costs. With Rocket originating over 400,000 D2C loans annually, the math becomes compelling quickly.

The Partner Network operates on thinner margins but requires minimal marketing spend. Partners typically receive 100-150 basis points for referrals, leaving Rocket with 150-200 basis points. On that same $285,000 loan, Rocket nets about $5,700 in revenue, with $1,500 in processing costs, yielding roughly $4,000 in contribution margin. Lower margins, but also lower customer acquisition costs and higher conversion rates since partners pre-qualify leads.

Customer acquisition costs (CAC) tell the real story of Rocket's competitive advantage. Traditional lenders spend $5,000-7,000 to acquire a mortgage customer through branches and loan officers. Rocket's digital CAC is under $2,000 and falling. But here's the kicker: platform customers acquired through Rocket Money or Rocket Homes have essentially zero incremental CAC. They're already in the ecosystem, already trust the brand, already have their data stored. This is the platform network effect in action.

The lifetime value (LTV) calculation extends far beyond the initial mortgage. A typical Rocket customer generates $7,000 from their first mortgage, $2,500 from servicing over seven years (the average life of a mortgage), $3,000 from a refinance, $1,500 from a home equity loan, and potentially thousands more from insurance, personal loans, and other products. Total LTV can exceed $15,000 for a fully engaged platform customer. With CAC under $2,000, the LTV/CAC ratio exceeds 7:1—exceptional for financial services.

Servicing economics deserve special attention, particularly after the Mr. Cooper acquisition. Servicing yields about 30 basis points annually on unpaid principal balance. For a $285,000 loan, that's $855 per year in gross servicing revenue. The cost to service—collecting payments, managing escrow, handling customer service—is roughly $50 per loan annually thanks to automation. The net servicing margin of $800+ per loan per year provides steady, predictable cash flow regardless of origination market conditions.

The technology leverage in Rocket's model is stunning. In 2010, it cost Rocket about $4,500 to process a mortgage. By 2020, that had fallen to $2,800. By 2024, with AI automation, it's under $1,500 and dropping toward $1,000. Every dollar saved in processing costs drops directly to the bottom line. At 500,000 loans annually, reducing processing costs by $500 adds $250 million in profit. This is why Rocket invests so heavily in technology—the returns are immediate and compounding.

Marketing efficiency has also improved dramatically. In 2016, Rocket spent $500 million on marketing to generate $25 billion in origination volume—a 2% marketing-to-volume ratio. By 2024, they spent $800 million to generate $150 billion—just 0.53%. The brand is so strong that organic traffic now represents 40% of applications. The Super Bowl ads and ubiquitous marketing created a brand moat that generates free customer acquisition worth billions.

The platform businesses layer additional economics onto the core mortgage model. Rocket Money generates $30 per user annually through premium subscriptions and financial product referrals. With 5 million users, that's $150 million in high-margin recurring revenue. Rocket Homes earns 1% referral fees on home transactions. Rocket Loans captures 5-7% origination fees on personal loans. Each business is profitable standalone but more valuable as part of the ecosystem.

The working capital dynamics are particularly favorable. Mortgages are typically sold to investors within 30 days of origination, meaning Rocket doesn't tie up capital in loans. They collect fees upfront but spread costs over time. This negative working capital model means growth actually generates cash rather than consuming it. During the 2020-2021 boom, Rocket generated over $10 billion in free cash flow—money that funded technology investment, acquisitions, and shareholder returns.

Risk management is embedded in the unit economics. Rocket retains minimal credit risk, selling 95% of loans to government-sponsored enterprises (Fannie Mae and Freddie Mac) or other investors. They might retain servicing rights, but the credit risk transfers immediately. This capital-light model enables massive scaling without proportional risk. When loan defaults spiked during COVID, Rocket was largely insulated because they'd already sold the loans.

The scalability of the model is its most impressive feature. Rocket can double origination volume with only 20-30% increase in costs. The technology platform, once built, handles additional volume with minimal marginal cost. Customer service is increasingly automated. Marketing becomes more efficient with scale. This operating leverage means margins expand as volume grows—the opposite of traditional lenders who face diseconomies of scale.

Competitive dynamics reinforce Rocket's unit economic advantages. Traditional banks carry massive fixed costs—branches, legacy technology, armies of processors. Their cost per loan is often $5,000-7,000, making it impossible to match Rocket's pricing while maintaining profitability. Digital competitors like Better.com have lower fixed costs but lack Rocket's scale advantages in marketing and technology. They're stuck in the middle—more efficient than banks but less efficient than Rocket.

The refinance versus purchase mix significantly impacts unit economics. Refinances typically generate 400+ basis point margins because customers are less price-sensitive and shopping behavior is limited. Purchase mortgages generate 300-350 basis points as customers compare multiple lenders. During refinance booms like 2020-2021, Rocket's margins expand dramatically. During purchase-heavy markets like 2023-2024, margins compress but remain healthy due to operational efficiency.

The capital allocation strategy maximizes returns on the strong unit economics. Rather than holding mortgages on balance sheet (which would require significant capital), Rocket operates asset-light, turning capital multiple times annually. The $4 billion raised for acquisitions will generate returns far exceeding the 5.5% cost of debt because it's deployed into businesses with 20%+ returns on invested capital. This financial engineering amplifies the underlying business model returns.

Looking forward, the unit economics should continue improving. AI will drive processing costs toward $500 per loan. Platform network effects will reduce CAC below $1,000. Cross-selling will push LTV above $20,000. The Mr. Cooper acquisition adds a massive servicing portfolio generating steady cash flow. The Redfin acquisition brings 50 million high-intent users with zero acquisition cost. Every trend points toward expanding margins and returns.

The key risk to the model is commoditization. If mortgages become completely undifferentiated, margins will compress toward zero economic profit. But Rocket's platform strategy, brand strength, and technology advantages create differentiation that protects margins. Customers choose Rocket not just for rates but for experience, speed, and ecosystem benefits. As long as that differentiation persists, the unit economics will remain exceptional.

XI. Playbook: Key Lessons & Strategic Insights

The Rocket Companies story offers a masterclass in industry disruption, but the lessons extend far beyond mortgages. This is ultimately a playbook for how to attack sleepy, regulated, complex industries using technology, vertical integration, and contrarian thinking. The strategies that transformed a Detroit mortgage broker into America's largest lender can be applied to any industry ripe for disruption.

Lesson 1: Technology-First in Traditional Industries Creates Asymmetric Advantages

When Gilbert declared "all in" on digital in 2002, online mortgage penetration was under 3%. His competitors thought he was abandoning 97% of the market. But Gilbert understood that being early in digital transformation meant building capabilities competitors couldn't easily replicate. By the time traditional lenders realized digital was the future, Rocket had a decade head start in data, systems, and processes. The lesson: don't wait for customer demand to drive digital transformation. Build the future, then convince customers to join you there.

Lesson 2: Vertical Integration Enables Experience Control

Most mortgage brokers accepted their role as middlemen. Rocket systematically integrated backward and forward—becoming a lender, building a servicing platform, acquiring title companies, creating real estate services. Each integration point removed friction and improved margins. But the real value was experience control. When you own the entire stack, you can optimize the whole rather than the parts. Traditional companies outsource for efficiency; disruptors integrate for control.

Lesson 3: Geographic Arbitrage Is Real and Sustainable

Moving to Detroit wasn't corporate social responsibility—it was brilliant strategy. Rocket pays 40% less for talent than coastal competitors. Real estate costs are 70% lower. The city government supports rather than constrains growth. But the real advantage is cultural: Detroit employees are builders, not optimizers. They're grateful, not entitled. They stay longer and work harder. The lesson: instead of competing for expensive resources in crowded markets, find overlooked geography and build your own ecosystem.

Lesson 4: Brand Building in Commoditized Industries