Riot Platforms: The Power Arbitrage King

I. Introduction: The $600 Million Pivot

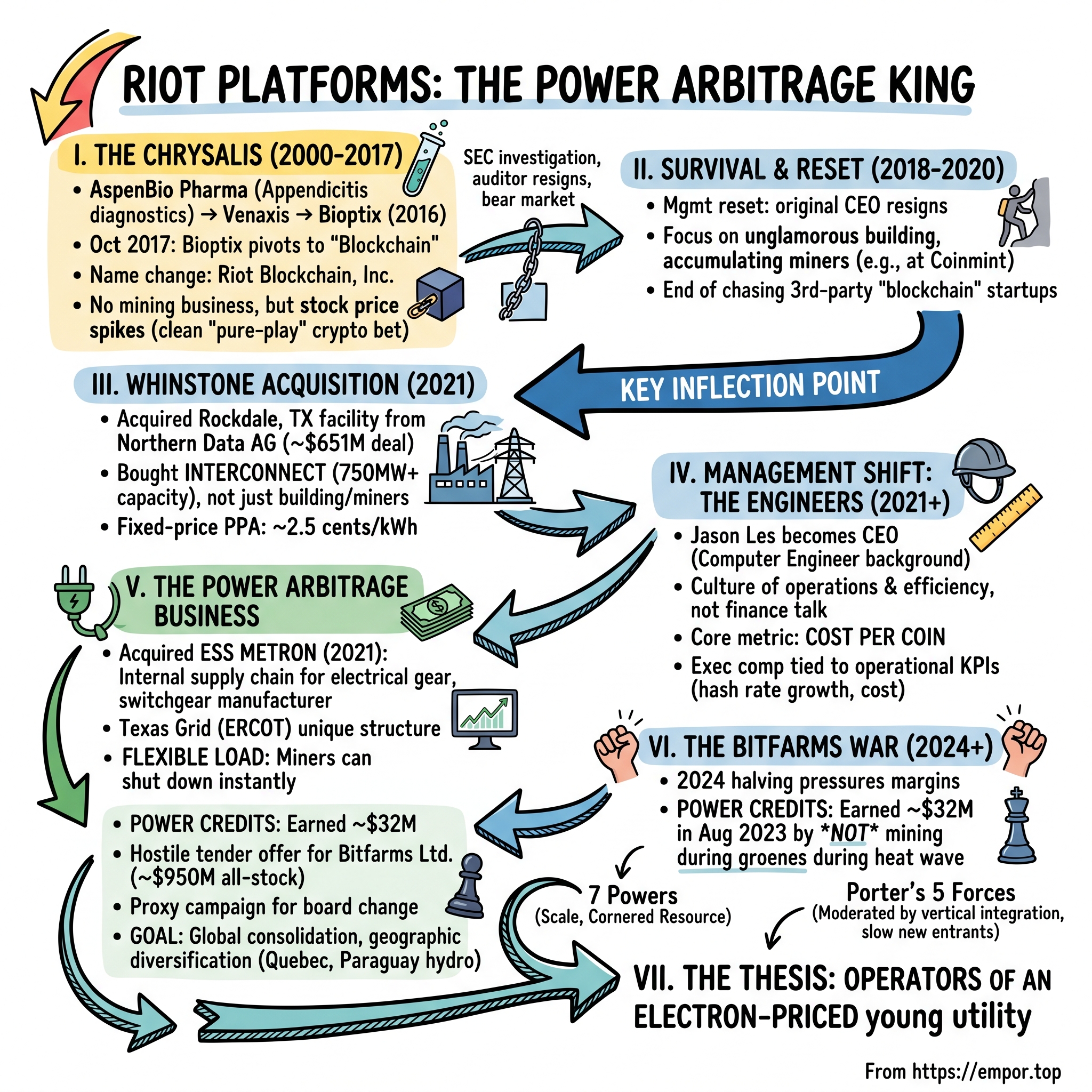

Picture the scene on October 4, 2017. A small-cap biotech company called Bioptix Inc., whose primary business had been making fluid handling systems and licensing veterinary diagnostic technology, files an 8-K with the SEC announcing it will change its corporate name. The new name is Riot Blockchain. There is no functioning blockchain product. There are no miners. There is no mining facility. There is barely a business plan. There is just a name — and on the strength of that name alone, the stock more than triples over the following weeks, peaking near $46 a share by year-end after starting October below $8.1

Bitcoin, meanwhile, was on its own moonshot, climbing from roughly $4,000 in early October 1, 2017 to nearly $20,000 by mid-December. The Riot Blockchain trade was, in the parlance of the era, the cleanest "pure-play" crypto bet you could make on a U.S. exchange. It was also, by any reasonable corporate-governance standard, a circus. Within months the SEC had opened an investigation, short sellers were circling, an annual meeting had been cancelled, and the company's auditor had quietly resigned.2 By the spring of 2018 the stock had collapsed by more than 80% from its highs. Riot Blockchain, the meme, looked finished.

Fast-forward to 2026. The same ticker — RIOT — sits at the center of one of the most consequential infrastructure stories in North America. Riot Platforms, as it is now known, controls the Rockdale, Texas campus, the largest dedicated Bitcoin mining facility in North America by developed capacity, and is building out the Corsicana facility, which the company describes as a one-gigawatt site when fully energized.3 It owns an electrical-equipment manufacturer in Denver that builds its own switchgear. It earned tens of millions of dollars in a single month from the Texas grid operator for not mining. And it just made a hostile tender offer for one of its largest publicly traded competitors.

This is the central puzzle of the company. Is Riot a levered Bitcoin proxy — a financial instrument with an industrial costume — or has it, almost by accident, assembled what Hamilton Helmer in 7 Powers would call a Cornered Resource: a physical position in the ERCOT grid that nobody else can replicate?

The roadmap for this episode tracks that question across nine years. We will move from the Wild West of 2017, through the regulatory cleanup and management purge of 2018-2020, into the Whinstone acquisition that redefined the company, and out the other side into an era where Riot increasingly looks less like a crypto-mining startup and more like an unregulated power utility that happens to monetize electricity by hashing SHA-256. Along the way we will look at the engineers in the C-suite, the manufacturing subsidiary almost nobody talks about, the demand-response payments that show up as line items in the 10-K, and the consolidation war with Bitfarms. The thesis we will keep testing: in an industry where almost everyone competes on the same Bitmain S21 ASICs from the same Shenzhen supplier, the only durable edge is the electron.

II. The Chrysalis: From Bioptix to Riot

Long before Riot was a Bitcoin story, it was a sad little biotech story. The legal entity now known as Riot Platforms was incorporated in 2000 as a Colorado company called AspenBio Pharma, focused on appendicitis diagnostics. It tried, and failed, to commercialize a blood test called AppyScore. It rebranded once already, to Venaxis, then merged in 2016 with a Dutch outfit called BiOptio B.V. to form Bioptix, hoping fluid handling and bovine reproductive hormones might keep the lights on.4 None of it worked. By mid-2017, with a market cap below $20 million and a shareholder base losing patience, Bioptix was a textbook public shell looking for a thesis.

The thesis arrived dressed in a hoodie. In October 2017, the board announced not just a name change to Riot Blockchain but a strategic pivot: the company would invest in blockchain ecosystem companies and acquire Bitcoin-mining assets. The very first move — a roughly $11 million purchase of a 92% stake in Tess Inc., a "blockchain telecom" venture, alongside a position in goNumerical Ltd., the operator of Canadian exchange Coinsquare — looked like the corporate equivalent of buying every "blockchain" sticker on the wall.5 The market did not care about the strategy. It cared about the word. Volume exploded, the share price ramped, and Riot briefly became a CNBC talking point.

What followed was the regulatory hangover. In April 2018, the SEC subpoenaed Riot as part of a broader sweep of crypto-named companies. The company cancelled its annual meeting twice, faced shareholder litigation alleging the rebrand was a pump scheme, and watched its auditor walk.2 Short reports — most famously a series from a financial-news outlet that questioned insider sales around the name change — piled up. The stock, which had touched $46, traded under $4 by the end of 2018. For most public-market investors, that was the end of the story. Just another 2017 crypto carcass.

It almost was. What saved Riot was not the price of Bitcoin, but a quiet board-level reset. The original CEO from the Bioptix era, John O'Rourke, resigned in early 2018 under regulatory pressure. An interim CEO, Christopher Ensey, ran the company for two years through the bear market, focused on accumulating ASIC miners and quietly consolidating hosting relationships at facilities like Coinmint in upstate New York.6 The company stopped chasing strategic investments in third-party "blockchain" startups and started doing the unglamorous work of building a single, focused business: Proof-of-Work mining at scale. It deregistered the meme stuff. It survived.

The transition that matters happened in 2020 and early 2021. Jason Les, a hardware-savvy former professional poker player who had been a Bitcoin advocate since the early 2010s, joined the board in mid-2017 and took over as CEO in April 2021.7 Around him, the team that would later define Riot's identity began to assemble. The mandate was simple and ruthless: stop being a holding company that owned miners, and start being an infrastructure company that owned the building. The pivot from "Bioptix" to "Riot Blockchain" had been a name change. The pivot from "Riot Blockchain" to what Riot would become was an identity change. The first transaction of the new era would be the largest the company had ever attempted, and it set everything that followed in motion.

III. The Inflection Point: The Whinstone US Acquisition

In late 2020, if you flew into Austin and drove east for about an hour, past the suburbs and into the hard scrub of Milam County, you would arrive at a place called Rockdale, Texas, population about 5,300. Rockdale's claim to fame, until very recently, had been an Alcoa aluminum smelter that closed in 2008 and took thousands of jobs with it. What Alcoa had left behind was the most valuable thing in Texas after oil: a massive, already-built 1,000-acre industrial site sitting directly on the Sandow Lakes power infrastructure, with transmission interconnections that could move hundreds of megawatts. In 2018, a German entrepreneur named Chad Harris and his team had taken over part of that footprint and started building what would become the Whinstone US data center. By 2020 it was operating around 300 megawatts of mining capacity. There was nothing else like it in North America.[^8]

On April 8, 2021, Riot announced it was acquiring Whinstone US from Northern Data AG in a transaction valued at approximately $651 million — $80 million in cash, around 11.8 million shares of Riot common stock then valued at roughly $429 million, plus an additional cash payment of up to $130 million tied to certain conditions.[^8] At the time, this looked, frankly, insane. Riot was a sub-billion-dollar company before the deal. It was paying close to its entire enterprise value for one site, denominated mostly in its own stock at prices that had been pumped by a parabolic Bitcoin rally. Critics called it the high-water mark of pandemic-era crypto froth.

History, as it usually does, looked different in hindsight. To understand why, you need to understand what was actually being purchased. It was not, fundamentally, miners. It was not even buildings, though buildings were included. The asset that mattered was the interconnect: a substation arrangement with Oncor and the ERCOT transmission backbone that effectively gave Riot the right to draw up to 750 megawatts of power at industrial rates, expandable further with infrastructure investment. In 2021, that interconnect already let Whinstone strike long-dated power purchase agreements at a fixed-price contract with a fixed component of approximately 2.5 cents per kilowatt-hour — among the lowest industrial power costs in the United States.8

To benchmark how good a deal that turned out to be, consider what happened to the data-center market between 2021 and 2026. Hyperscale demand from artificial intelligence training, combined with the cost of new transmission and the multi-year queues to interconnect with ERCOT, sent the implied value of grid-connected, energized "empty" data-center capacity skyward. By 2024, industry analysts were pricing energized capacity at roughly $7 million to $10 million per megawatt for greenfield builds, with permitting and interconnect timelines stretching to four or five years.9 A 750-megawatt position acquired in 2021 for $651 million implied a per-megawatt cost of under $1 million. Even accounting for the cost to build out the cooling and rack infrastructure on top of that grid connection, the math is hard to argue with. Riot had not overpaid for Whinstone. Riot had stolen Whinstone.

The strategic shift mattered more than the financial one. Before Whinstone, Riot's miners were largely hosted at third-party facilities — most prominently Coinmint in Massena, New York, where Riot paid a hosting rate per kilowatt-hour that included someone else's margin.6 After Whinstone, Riot became its own landlord, its own utility customer, and its own operator. The economics of mining flipped from "buy ASICs, rent power" to "own the dirt, own the wires, own the transformers, host other people's miners as a side business." That side business — the data center hosting segment — would later become a meaningful and counter-cyclical revenue stream in its own right.

The deeper lesson here is about the ERCOT grid itself. The Electric Reliability Council of Texas runs an energy-only market that is, in important ways, unlike any other in the U.S. It does not pay generators for capacity. It pays them for energy actually delivered at the moment of delivery. Demand-response participants — large industrial users who can shed load on command — get paid the same scarcity prices that generators get when the grid is stressed. This structure makes ERCOT uniquely friendly to flexible, interruptible loads. Bitcoin mining, which can be powered down within seconds, is the perfect flexible load. By owning a hyperscale, fully-interruptible asset directly inside ERCOT, Riot wasn't just buying cheap power. It was buying a seat at the table where ERCOT decides who gets paid when the grid screams.

IV. Current Management: The Engineers in the Room

The biographical legend most people know about Jason Les is the poker part. From roughly 2010 to 2015 he was a top-ranked online cash-game player and one of the four humans selected to play heads-up Texas Hold'em against Carnegie Mellon's Claudico AI in 2015 — a precursor to the later Libratus matches that ultimately solved no-limit poker.[^11] What gets lost in the poker headline is that Les was, even then, primarily an engineer. He has a degree in computer engineering from UC Irvine, taught himself Bitcoin protocol minutiae in the early 2010s, and ran a Bitcoin-focused engineering consultancy called Riot Proof before joining Riot's board in 2017.

When Les took the CEO chair in April 2021, the message he sent to the organization and to the market was deliberate and consistent: Riot is an energy infrastructure company first, and a Bitcoin company second. In a series of interviews through 2023 and 2024 he framed the strategy plainly. The Bitcoin price is exogenous and not something management controls. What management can control is the cost of each bitcoin produced, the scale of the platform, and the optionality embedded in the energy contracts.[^12] That framing — cost per coin, not coins per quarter — became the lodestar metric for the entire executive team.

Around Les, the senior team is dominated by people whose résumés are heavier on electrons than on cryptocurrency. Colin Yee, the CFO appointed in 2023, came from PIMCO and previously held leadership roles at private investment firms; his job has been to keep Riot's balance sheet, famously, debt-free at the corporate level while funding nine-figure capital expenditure programs through at-the-market equity offerings.[^13] The construction and energy operations leaders came out of industrial backgrounds at firms building substations, switchgear, and large-scale electrical infrastructure. The Chief Mining Officer's team measures itself on uptime, hash rate efficiency, and the J/TH (joules per terahash) of the fleet — the kinds of metrics you would find at a semiconductor foundry, not at a fintech.

This matters for one specific reason: incentives. Riot's executive compensation, as laid out in the proxy filings, ties performance-based restricted stock units to a basket of operational metrics rather than to share price alone. The board's compensation committee has explicitly highlighted hash rate growth, deployment of capacity, and total cost to mine a Bitcoin as the metrics that move PSU payouts.10 In an industry that has historically rewarded executives for issuing stock at Bitcoin's local highs and surviving until the next halving, Riot has tried to instill a culture more analogous to a regulated utility — where the things you can control (kilowatt-hours per terahash, megawatts energized, downtime minutes) are what compensation tracks.

Skin in the game, in absolute dollar terms, is modest. Jason Les owned roughly 0.6% of the company's outstanding shares as of the 2024 proxy, and other named executives held similarly small percentages — typical for a company that has grown its share count substantially through ATM offerings.10 But the structure of the compensation is unusual. A material portion of equity grants only vest if multi-year cost-per-Bitcoin targets are hit. If Bitcoin doubles tomorrow and Riot's operations get sloppy, executives don't automatically win. This alignment is exactly what a long-term investor in a commodity-exposed business should want. It also, frankly, is rare in this sector. Many peers still report hashrate-targets-and-Bitcoin-held as their core scorecard.

The cultural tell is in the language. Listen to a Riot earnings call from 2018 versus a Riot earnings call from 2024. The first one is full of references to "ecosystem" and "blockchain" and "tokens." The second one sounds like a SCADA-systems engineer briefing a substation upgrade. That linguistic shift, from finance talk to operations talk, is the clearest signal of who is actually running the company.

V. The Hidden Business: ESS Metron and the Power Credits

On December 1, 2021, Riot announced a transaction that, in the rush of the moment, almost nobody covered properly. It acquired a Denver-area company called ESS Metron, an electrical equipment manufacturer specializing in custom switchgear, power distribution units, and modular substation gear for data centers, mission-critical industrial users, and utilities. The headline price was about $50 million in cash plus stock, with earn-outs that could push the total to $80 million.11 In the context of the Whinstone deal, $50 million looked like a rounding error. It was, in fact, the second-most strategic thing Riot ever bought.

To understand why, you have to think about what was happening to data-center construction during 2021 and 2022. Lead times on the boring but essential pieces of an electrical build-out — transformers, switchgear, busways, MV/LV switchboards — were exploding. A standard 138 kV transformer that historically took 8 to 12 months to deliver was quoted at 24 to 36 months. Hyperscale data-center operators were finding that the bottleneck on new capacity was not chips or land or even power contracts, but the physical metal cabinets that route the electricity. Riot, by buying ESS Metron, gave itself an internal supply chain for that exact bottleneck.

The financial contribution of the engineering segment was, in pure GAAP revenue terms, smaller than the mining business — in the tens of millions per quarter through 2023 and 2024 — but the strategic contribution was outsized.12 When Riot announced its Corsicana, Texas build-out in 2022, a one-gigawatt expansion site in Navarro County, the electrical room build was substantially executed by Metron, on Metron's schedule, with Metron's gear.3 Competitors had to bid into a queue that stretched past their development windows. Riot was running an internal supplier, on its own schedule, with backlog visibility nobody else had.

But the part of Riot's business that genuinely confused traditional analysts in 2023 was something else: the power credits. In August 2023, Texas suffered a historic heat wave. ERCOT prices spiked into the thousands of dollars per megawatt-hour during the late-afternoon peak hours, and the grid sat repeatedly on the edge of emergency conditions. Riot, by virtue of being one of the largest interruptible industrial loads in ERCOT, simply curtailed its mining operations and sold the curtailment back to the grid through demand-response programs and the long-dated fixed-price power purchase agreements at Whinstone.

The number that came out of that month stunned the market. In August 2023 alone, Riot reported receiving $31.7 million in power and demand-response credits — more than it earned from mined Bitcoin in the same month.13 CNBC, Bloomberg, and the Texas Comptroller's office all picked the story up; for many readers it was the first time they had encountered the concept that a Bitcoin miner could be more profitable while not mining.14 The Texas Comptroller's fiscal-notes division published an analytical piece in August 2023 walking through the economics of mining in the state, concluding that interruptible Bitcoin loads were emerging as a meaningful new participant in ERCOT's ancillary-services and demand-response markets.[^19]

The accounting matters here. Power credits at Riot flow through cost of revenue as an offset to power expense. Demand-response participation, where Riot bids capacity into ERCOT programs, shows up in the data center hosting segment and partially as credits against self-mining costs. The net effect is that during periods of grid stress, the all-in cost to mine a Bitcoin at Whinstone falls, even as gross mining production also falls, because the avoided power cost plus the cash from curtailment more than compensates for the lost hash. This is the synthetic-battery thesis in numbers: Riot acts, economically, like a giant grid-stabilization battery that earns peak energy prices on the way in and an irregular but lucrative call option on the way out.

Compare the segment margins. Riot's self-mining segment runs on gross margins that swing violently with Bitcoin's price and the halving schedule — sometimes 70%, sometimes near zero. Data center hosting margins are smaller in absolute terms but vastly steadier; they're priced in dollars-per-kilowatt-hour against contracts. Engineering through ESS Metron is the smallest line but the most countercyclical: when crypto winters force smaller miners to suspend builds, Metron's external book of utility and industrial customers keeps revenue ticking over.12 The architecture is deliberate. The company has three businesses that, in combination, can stay cash-flow positive across most macro states.

VI. The Bitfarms War: The Consolidation Era

By the spring of 2024, the publicly listed Bitcoin mining sector had a problem. The April 2024 halving had cut block rewards in half, from 6.25 BTC to 3.125 BTC. Network hash rate, far from falling, kept climbing as larger operators deployed newer-generation ASICs. The marginal cost of producing a Bitcoin, network-wide, was creeping up against the price of Bitcoin itself. Smaller miners with weaker balance sheets, expensive hosted hash rate, and short-dated power contracts began to look, in classic Acquired language, like prey. And on April 22, 2024, Riot moved.

The target was Bitfarms Ltd., a Toronto-listed miner with operations primarily in Quebec, Argentina, and Paraguay, plus a smaller footprint in the U.S. Bitfarms operated roughly 200 megawatts of mining capacity with an additional pipeline under development, and it had a peculiarly cheap power profile thanks to Quebec's hydroelectric grid and Paraguay's Itaipu Dam exports.15 In late April Riot disclosed it had accumulated a position in Bitfarms and offered to acquire the company at $2.30 per share in an all-stock transaction valued at approximately $950 million. Bitfarms' board rejected the offer as inadequate. Riot, undeterred, raised the stakes.

What followed was one of the more publicly aggressive activist campaigns the crypto sector had ever seen. On June 24, 2024, Riot issued an open letter to Bitfarms shareholders demanding a special meeting to remove the Bitfarms chairman, Nicolas Bonta, and replace several board members.[^21] Riot, by that point holding north of 14% of Bitfarms' outstanding shares, framed the campaign as a governance crusade — pointing to Bitfarms' adoption of a shareholder rights plan (a poison pill) and the resignation of its CEO weeks earlier as evidence the board was not serving shareholders. Bitfarms fired back, accusing Riot of "creeping control" tactics designed to gain influence without paying a control premium.

The strategic logic, beneath the corporate-governance theater, was simple. The Bitcoin mining industry post-halving was — in Porter's framing — a textbook scale-economies game. The fixed costs of operating a hyperscale site are enormous. The variable cost per terahash, with modern Bitmain S21 or MicroBT M60S ASICs, is essentially defined by your power price. The biggest, lowest-cost operator wins. Period. And in a global hash-rate race, geographic diversification of cheap power matters because no single grid is friendly forever. Bitfarms' Paraguayan hydro and Quebec hydro positions were strategic assets Riot's Texas-only footprint did not have.

By the autumn of 2024, the campaign had partially achieved its aims. Bitfarms agreed to expand its board, several Riot-nominated independent directors were appointed, and a cooperation framework was eventually reached. Riot did not outright acquire Bitfarms — the full takeover stalled — but it gained meaningful influence over a competitor's strategic direction while keeping its position as a financial holding.16 The episode signaled something important to the rest of the sector: Riot was prepared to use its balance sheet and its scale as a consolidation weapon. For smaller listed miners trading at sub-scale economics with overhangs of insider control, the message was unmistakable. The roll-up era of public Bitcoin miners had begun.

The footprint that resulted is what matters. Riot's home base remained Rockdale, with Corsicana coming online through 2024 and 2025 as additional capacity. The Bitfarms position gave Riot exposure, via influence and equity, to non-Texas geographies. The pattern is familiar from every commodity industry that has matured: a handful of disciplined, well-financed operators absorb the marginal players, the industry's all-in cost curve flattens, and the survivors enjoy structurally better returns. The race to the bottom on cost only ends well for the largest player at the bottom.

VII. Playbook: 7 Powers and Porter's 5 Forces

Hamilton Helmer's 7 Powers framework is built for exactly the kind of question Riot raises. The framework asks, of any company, which of seven distinct sources of durable competitive advantage it actually possesses, and whether those sources are reinforced by the industry's structural dynamics. Applied to Riot, two powers stand out, and a third is interesting but not yet proven.

The first is Scale Economies. The Whinstone site, fully built out, draws on the order of 750 megawatts. The Corsicana site adds approximately one gigawatt of capacity when fully energized.3 Combined, Riot's owned megawatt footprint puts it among the very largest interruptible industrial loads in the United States. When Riot signs a power purchase agreement at that scale, the counterparty — Oncor, an independent generator, or a transmission cooperative — is dealing with one of the largest single offtakers in the region. The PPA prices Riot can extract reflect that buyer power. The implied cost per kilowatt-hour at Whinstone, around 2.5 cents fixed, is structurally below what smaller miners pay even when they think they're getting a great deal.8 Scale here doesn't just lower cost. It lowers the cost of the input that defines the cost structure.

The second is Cornered Resource. The Rockdale interconnect is not a thing you can build. ERCOT's interconnection queue, the time required to expand transmission, and the political-physical reality of building 345 kV lines in Texas mean that a 750-megawatt grid connection at a given substation is, for practical purposes, an asset of finite supply. Riot owns it. The Corsicana interconnect is similar. By 2025, the queue to obtain a new gigawatt-class interconnect in ERCOT stretched into the early 2030s on most realistic project schedules.17 AI hyperscalers were paying premium prices for any energized capacity they could find. Riot's interconnects had become, in the language of the framework, scarce inputs to which Riot has preferential access.

Beyond those two, the case becomes weaker but not zero. Process Power — meaning institutional know-how that's hard to replicate — is plausible in operations. Riot's mining uptime, fleet efficiency, and immersion cooling design at Building G at Rockdale are areas where the team has accumulated genuine craft. Network Economies do not apply (mining is not a network business). Switching Costs do not apply to mined Bitcoin (a fungible commodity). Counter-Positioning is not yet visible; Riot's competitors could in principle build identical businesses, they just can't build them quickly. Branding is irrelevant. So the durable case rests on the two clear powers: Scale and Cornered Resource.

Porter's Five Forces tells a complementary story. Supplier power is moderated by vertical integration: by owning ESS Metron, Riot has hedged the single most painful supplier bottleneck in the data-center industry, electrical gear, even as it remains dependent on Bitmain and MicroBT for ASICs.11 Buyer power doesn't really exist in mining; Riot sells Bitcoin into a deep, liquid market at the prevailing price. Threat of new entrants is the most underappreciated force: the entrants exist, but they take five-plus years to interconnect at gigawatt scale, so the threat is real but slow-moving. Rivalry is intense among the existing miners (Marathon Digital, CleanSpark, Core Scientific, IREN, TeraWulf), but the post-halving consolidation we just discussed is structurally rationalizing the field.

The fifth force is the interesting one: threat of substitutes. The substitution debate inside Riot is whether the company will pivot megawatts from Bitcoin mining to high-performance computing (HPC) and AI training. Several peers — Core Scientific, IREN, TeraWulf — have signed multi-hundred-million-dollar HPC hosting deals that, in some cases, value a single megawatt of energized capacity at $7-10 million in implied annual revenue, materially above what mining produces per megawatt.9 Riot management, through 2024 and 2025, was visibly disciplined about not chasing this. Switching a mining building to HPC requires different cooling, different fiber, different layout, and different uptime guarantees. The technical lift is real. But the optionality is there, and the market began, increasingly, to value Riot partly as a real-option on that pivot — particularly given the size and quality of the Corsicana site, which was designed with greater electrical robustness than legacy mining-only sites.

The seventh power that almost applies and almost doesn't is Counter-Positioning. Could Riot adopt a business model that incumbents (legacy hyperscalers) cannot copy without cannibalizing themselves? Possibly: as a flexible interruptible compute load, Riot can profit from grid scarcity events in a way that AWS or Microsoft Azure cannot, because AWS cannot tell its customers their training jobs will pause for six hours when ERCOT calls. That makes Riot, plausibly, the natural owner of "second-tier" interruptible AI workloads — a niche, but a real one.

VIII. The Bear vs. Bull Case

Walk the bear case first, because it is the more straightforward of the two.

The bear case starts with the asset. Bitcoin's price is volatile, exogenous, and not analytically forecastable on the kind of cash-flow horizon a long-term investor wants. Riot's revenue scales with Bitcoin's price (and its hash rate share of the network), so the top line is fundamentally non-stationary. Every four years a halving cuts block subsidy in half, structurally pressuring margins unless price or transaction-fee revenue compensates. The April 2024 halving was the third such event; the next is scheduled for around 2028. In each halving cycle, less-efficient operators are squeezed first, but the entire sector's economics compress.

Layered on top is the hardware obsolescence problem. ASIC miners have effective economic lives of three to five years before efficiency improvements from competing chips make them uneconomic at marginal grid prices. The capex cycle for ASIC fleet upgrades is therefore continuous and large. Riot, like every miner, is running hard to stay still. Bernstein Research and other equity-research desks have written extensively about how to think about cost-curve dynamics in mining; the consensus is that fleet J/TH efficiency is the single most important operational lever after power price.18

The regulatory bear case for Texas is real but easy to overstate. After 2023's grid stress events, the Texas legislature passed several bills aimed at clarifying and in some cases constraining the participation of cryptocurrency miners in ERCOT's ancillary-services programs. The most-discussed bill, SB 1751 from the 2023 session, sought to cap demand-response participation by miners, though it did not pass in its most restrictive form.[^19] The structural risk is that political winds in Austin could turn against the industry. Counter to that, however, ERCOT badly needs flexible interruptible load to manage a grid that is increasingly weighted with intermittent renewable generation, and Bitcoin mining is, technically, the cleanest such load that exists.

Now the bull case. It rests on three pillars.

First, balance sheet. Riot has maintained corporate-level debt at essentially zero through the entire 2022-2025 period, funding capex through cash from operations, sales of mined Bitcoin, and equity issuance via at-the-market offerings.[^13] In a sector that consumed Core Scientific (Chapter 11 in December 2022, emerged later), nearly killed Greenidge Generation, and pushed several private operators into restructuring, balance-sheet conservatism turned out to be a wildly underrated competitive advantage. When Bitcoin's price falls 60% from a cycle peak, the operator without debt does not need to sell miners at firesale prices. The operator with debt does.

Second, the "synthetic battery" optionality. Riot's interruptible footprint inside ERCOT is, in effect, a large embedded option on grid scarcity. Whenever ERCOT prices spike — driven by heat waves, cold snaps, or generator outages — Riot's curtailment economics make money. The August 2023 episode where credits substantially exceeded mining revenue is not a one-off; it is a recurring possibility whose value increases as ERCOT's renewable share grows and reserve margins tighten.13[^19] Critics call this volatility. The framework view is that it's a high-variance, positive-expected-value option that Riot owns essentially for free.

Third, optionality on the AI/HPC pivot. If a sufficiently attractive HPC hosting deal materializes for any meaningful fraction of Corsicana's energized capacity, the value uplift is potentially material. Riot is not pricing this aggressively into its narrative, which keeps expectations grounded. But the asset profile — gigawatt-scale, energized, well-located for fiber, in a low-tax state — is precisely what the AI capex cycle is bidding for.9

For long-term investors, the punch list of KPIs to actually track is small. First, cost-to-mine per Bitcoin, all-in, including power costs net of credits. Second, megawatts energized and contracted, as a leading indicator of future hash rate and HPC optionality. Third, demand-response revenue and power credits, both because they're a direct quantification of the synthetic-battery thesis and because they reveal how stressed the ERCOT grid is structurally.

A useful myth-vs-reality test. The myth is that Riot is a pure Bitcoin proxy and that owning RIOT is just a leveraged way to own BTC. The reality, visible in the segment disclosures, is that on a multi-year basis a non-trivial fraction of Riot's gross profit comes from data-center hosting, engineering through ESS Metron, and demand-response credits. Those are not Bitcoin-price-sensitive in the same way mined-coin revenue is. The correlation to BTC is high, but not one. A second myth is that Texas regulators are about to kill the business. The reality is the legislative outcomes through 2025 have been more nuanced; punitive bills have repeatedly failed, while ERCOT's operating need for interruptible load has, if anything, grown.[^19]

A short second-layer note on overhangs. The biggest sector-level qualitative risks are concentrated in two areas: ASIC supply chain (heavy dependence on Bitmain and MicroBT, both Chinese-headquartered) and ESG/political pushback (the energy-consumption narrative remains a flashpoint in some jurisdictions). The biggest company-specific risks are the standard ones for any commodity-exposed industrial: continued discipline on capital allocation as the share count grows through ATM issuance, and the operational complexity of running gigawatt-scale sites without quality erosion.[^13] None of these are easily resolved, but all are visible.

IX. Epilogue: The Future of Energy

It is worth pausing on the arc here. In October 2017, Riot was a biotech shell whose only innovation was changing its name. In May 2026, Riot is one of the largest single industrial energy users in ERCOT, a vertically integrated operator that builds its own electrical equipment, an activist investor in publicly traded competitors, and the owner of physical assets — interconnects, substations, transformers, energized data-center buildings — whose replacement cost has, since 2021, approximately tripled in market value. The journey from punchline to infrastructure titan took about seven years.

What makes the story Acquired-worthy is not that Bitcoin went up. Many companies were positioned to benefit from Bitcoin going up. What makes it interesting is that the management team, somewhere between 2020 and 2022, made a non-obvious bet: that the durable edge in mining is not the miner, not the hash rate, not the financial engineering, but the electron. The Whinstone acquisition was the expression of that bet. The ESS Metron acquisition was the hedge that made the bet executable. The disciplined balance sheet was what kept the bet alive through the 2022 crypto winter. And the demand-response monetization through ERCOT was the unexpected upside that turned the bet into a thesis.

The deeper, structural question for the next five years is the future of the energy system itself. American electricity demand, after two decades of being roughly flat, started growing again in 2024 and 2025, driven by AI training, manufacturing reshoring, and electrification. Texas in particular faces a generation-and-transmission build-out the scale of which is unprecedented in the state's modern history. In that environment, the entities that own large, flexible, dispatchable industrial loads sitting on existing high-voltage interconnects are not crypto plays. They are infrastructure assets. They look more like Linde, more like Air Products, more like Cleveland-Cliffs in the sense that physical position determines economics — except they have an additional optionality layer in that their underlying compute can be repurposed from hashing Bitcoin to training AI models.

Whether Riot has built a "great company" or merely captured a "great trade" depends largely on what you believe about that infrastructure thesis. If you believe ERCOT will continue to need interruptible flexibility, that AI capex will continue to bid for energized capacity, and that the consolidation of public miners will continue, then the assets Riot has assembled are durable. They generate cash, they hold optionality, and they sit behind regulatory and physical moats that protect them.

If, instead, you believe Bitcoin is a transient phenomenon and ERCOT will solve its flexibility problem with grid-scale batteries that don't need hash, then Riot is, ultimately, a clever financial structure stacked on top of a commodity. The argument cuts both ways and the answer is unknowable today.

What is knowable is the discipline. The management team has, repeatedly and consistently, behaved like infrastructure operators rather than crypto promoters. The metrics they emphasize are the right ones for a commodity-exposed industrial. The acquisitions they have made are the ones that vertically integrate them into the parts of the cost stack that matter. The fights they have picked — for the Bitfarms board, for ERCOT regulatory clarity, for cheap PPAs — are the right fights for an operator trying to build something durable.

The story, in a sentence: a meme stock from 2017 grew up into the boring, capital-intensive, operations-heavy, electron-priced infrastructure business that, if you squint, looks less like a Bitcoin company and more like a young Texas utility. Whether that's worth what the market thinks it's worth on any given day is a question for the trade. Whether that's a real business is no longer in dispute.

References

-

Bioptix Officially Changes Name to Riot Blockchain, Inc. — GlobeNewswire, 2017-10-04 ↩

-

Riot Blockchain says SEC investigating, postpones annual meeting again — Reuters, 2018-04-09 ↩↩

-

Riot Platforms Provides June 2024 Production and Operations Update — Riot Platforms Press Release, 2024-07-03 ↩↩↩

-

Venaxis and BiOptio Complete Combination, Company Renamed Bioptix — Bioptix Press Release, 2016-11-08 ↩

-

Riot Blockchain Announces Acquisition of Tess and Stake in goNumerical (Coinsquare) — GlobeNewswire, 2017-11-03 ↩

-

Riot Blockchain, Inc. Form 10-K for Fiscal Year 2019 — SEC, 2020-03-17 ↩↩

-

Riot Blockchain Appoints Jason Les as Chief Executive Officer — GlobeNewswire, 2021-02-08 ↩

-

Riot Platforms, Inc. Form 10-K for Fiscal Year 2023 — SEC, 2024-02-28 ↩↩

-

Bitcoin Miners Pivot to AI as Hyperscalers Bid for Energized Capacity — Bernstein Research note summarized by Reuters, 2024-06-26 ↩↩↩

-

Riot Platforms Proxy Statement (Form DEF 14A) — SEC, 2024-04-26 ↩↩

-

Riot Blockchain Acquires Electrical Equipment Leader ESS Metron — GlobeNewswire, 2021-12-01 ↩↩

-

Riot Platforms, Inc. Form 10-Q for the Period Ended March 31, 2024 — SEC, 2024-05-09 ↩↩

-

Texas Paid Bitcoin Miner Riot $31.7 Million to Shut Down During August Heat Wave — CNBC, 2023-09-06 ↩↩

-

Bitcoin Miner Riot Earned More From Power Curtailment Than Bitcoin in August — Bloomberg, 2023-09-07 ↩

-

Bitcoin Miner Riot Platforms Makes $950 Million Offer for Bitfarms — Reuters, 2024-05-28 ↩

-

Bitfarms Reaches Cooperation Agreement with Riot Platforms — Bitfarms Press Release via GlobeNewswire, 2024-10-22 ↩

-

Understanding the ERCOT Demand Response Program for Industrial Users — ERCOT.com ↩

-

Comparison of Bitcoin Miner Efficiency and Power Costs — Bernstein Research note summarized by CoinDesk, 2024-03-15 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube