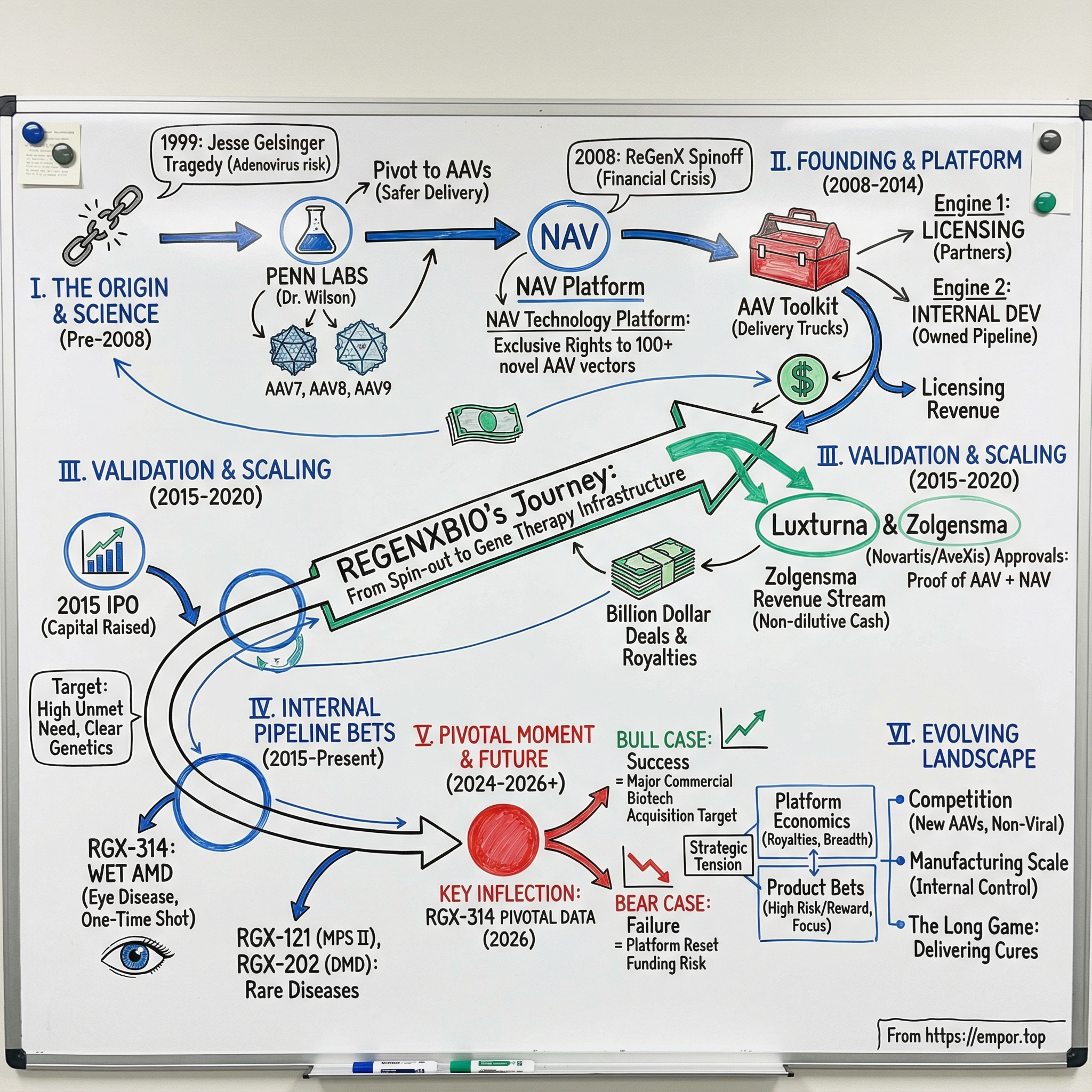

REGENXBIO: Engineering the Gene Therapy Revolution

I. Introduction & Episode Roadmap

Picture this: September 2015. A small biotech out of Rockville, Maryland is about to ring the opening bell at NASDAQ. REGENXBIO is only seven years old, a spinout from the University of Pennsylvania, and it has just priced its IPO at $22 a share. The plan had been to raise about $65 million. Instead, demand surges and the company pulls in roughly $138 million. By midday, the stock is trading north of $30.

What investors are buying isn’t one drug. It’s the possibility of a platform.

REGENXBIO is one of the cleanest examples in biotech of an “Intel Inside” model—especially in the early days of gene therapy. The company focuses on developing, commercializing, and licensing recombinant adeno-associated virus, or AAV, gene therapies. Its NAV Technology Platform is built around exclusive rights to a library of more than 100 novel AAV vectors, including AAV7, AAV8, AAV9, and AAVrh10.

Here’s the simplest way to think about it: gene therapy needs a delivery system. AAVs are the delivery trucks. REGENXBIO didn’t start by trying to sell a single finished product; it started by owning and improving the trucks, then licensing them to partners—while also building its own pipeline on top of the same foundation.

That sets up the central question of this story: how did a 2008 spin-out from Penn—born into the depths of the global financial crisis, and into a field still haunted by gene therapy’s darkest chapter—turn itself into the pick-and-shovel play of the gene therapy gold rush?

To answer it, we’ll follow a set of themes that define modern biotech: platform economics versus single-product bets; the messy art of turning academic breakthroughs into commercial IP; the audacity of trying to treat disease with a one-and-done injection; and the business model required to finance timelines that can swallow a decade or more.

We’ll also track the key moment that made REGENXBIO real: in 2009, the company secured exclusive rights to intellectual property covering novel recombinant AAV vectors discovered at the University of Pennsylvania in the lab of James Wilson, M.D., Ph.D. Over time, that technology flowed into licensed programs that went on to drive massive commercial impact—including products like Zolgensma. Meanwhile, REGENXBIO pushed forward with its own bets, particularly in ocular diseases and rare genetic conditions.

And this is where the tension comes in. A licensing platform can be an incredible engine—upfront payments, milestones, royalties, validation. But it can also become a trap. Can the cash from being the underlying technology provider actually fund a real, standalone drug company? Can you be both the arms dealer and the army? And what happens when your partners’ success doesn’t just create royalties—it also creates competition?

Today, that tension is no longer theoretical. REGENXBIO’s biggest swing is tied to ABBV-RGX-314, developed with AbbVie for wet age-related macular degeneration. Data from the ATMOSPHERE and ASCENT pivotal trials evaluating the safety and efficacy of subretinal delivery are expected in 2026. If they’re positive, the companies could be staring at a first-in-class gene therapy opportunity in one of the leading causes of blindness. If they’re not, REGENXBIO has to confront an existential version of the platform question: what, exactly, is this business without a flagship product?

So let’s start at the real beginning—not with the company, but with the science that made it possible… and the tragedy that nearly erased gene therapy as a field.

II. The Science Backstory: AAV Gene Therapy Emerges

To understand REGENXBIO, you first have to understand a deceptively simple idea: that you might cure a genetic disease with a single injection. Not manage it. Not treat it. Fix it.

The logic of gene therapy is almost too clean. A huge number of devastating diseases—from inherited blindness to muscular dystrophy to metabolic disorders—trace back to a mutation in a single gene. If you could deliver a working copy of that gene into the right cells, those cells could start doing their job again. In the best-case version of the dream, the patient’s body becomes its own medicine factory, producing the missing protein or enzyme for years, maybe for life. One treatment, potentially one cure.

And then you hit the real problem: delivery.

How do you get a piece of genetic code into the right tissue, into the right cells, in enough quantity to matter—without triggering a reaction that harms the patient?

That’s where viruses enter the story. Evolution has spent billions of years turning viruses into experts at breaking into cells and dropping off genetic payloads. Researchers realized they could hijack that machinery—remove what makes the virus dangerous, insert a therapeutic gene instead—and create what are called vectors. If gene therapy is shipping, vectors are the delivery trucks: the viral shell is the truck, and the therapeutic gene is the cargo.

In the 1990s, the field rallied around adenoviruses, the family of viruses behind many common colds. They were efficient at entering cells and relatively straightforward to manufacture. Progress felt fast. The optimism was real.

Then came September 1999.

Jesse Gelsinger (June 18, 1981 – September 17, 1999) became the first person publicly identified as having died in a gene therapy clinical trial. He was 18 years old, from Arizona, and lived with a rare metabolic disorder called ornithine transcarbamylase deficiency. His condition was managed with diet and medication. He wasn’t terminally ill. He enrolled in a safety study at the University of Pennsylvania, led by gene therapy researcher James Wilson, hoping that what researchers learned could help infants born with the severe form of the disease.

On September 13, 1999, Gelsinger received an infusion of a corrective OTC gene packaged in an attenuated cold virus—a recombinant adenoviral vector—delivered into his hepatic artery. His immune system reacted violently to the vector, and he died four days later.

The investigation that followed was bruising. It raised serious concerns, including that Gelsinger had been included as a substitute for another volunteer who dropped out, despite ammonia levels that should have excluded him; that the university failed to report serious side effects experienced by two prior patients; and that informed-consent documents did not disclose the deaths of monkeys that had received similar treatment.

The shockwave didn’t stop at Penn. For a time, gene therapy trials in the United States halted. Funding evaporated. Startups collapsed. Wilson became the focal point of multiple investigations. He was stripped of titles, his gene therapy center was disbanded, and he was barred from conducting clinical trials until 2010.

That should have been the end of this story. Instead, it was the pivot.

While the field retreated, Wilson didn’t walk away. He changed the approach. If adenoviruses could provoke the kind of immune response that killed Jesse Gelsinger, the path forward had to start with a different delivery truck.

Wilson’s lab turned to adeno-associated viruses, or AAVs.

AAVs had been known since the 1960s, but they weren’t the obvious choice. They couldn’t carry as much genetic cargo, and they were notoriously difficult to produce. But they had one feature that mattered more than everything else: they generally didn’t make people sick. Wild-type AAV infections are essentially asymptomatic in humans. That raised the possibility of a much lower immune reaction—the very thing the field now feared most.

Wilson’s team started methodically hunting for AAV variants in primates, betting that nature’s diversity would contain vectors with better properties than what scientists already had. Two early finds, AAV7 and AAV8, turned out to be dramatically more effective—on the order of ten to a hundred times better at getting genes into cells than the handful of previously known serotypes. Then came AAV9, discovered in 2003, which looked even more promising.

These weren’t just incremental improvements. Different AAV serotypes—think of them as different variants of the virus—tended to prefer different tissues. Some were better at targeting the liver. Others were stronger in muscle. AAV9, remarkably, could cross the blood-brain barrier. Suddenly, gene therapy started to look less like a single technology and more like a toolkit: match the right vector to the right disease and the right tissue.

At first, Wilson struggled to get the work published. “Gene therapy was still under the shadow of Jesse Gelsinger,” Gao says. Skepticism wasn’t just about the field; it was about Wilson himself.

But the science didn’t stay contained. Penn researchers produced thousands of AAV preparations each year, using them internally and distributing them widely. “These things were being sent out left, right, and center,” Vandenberghe says. Other labs used those vectors to power some of the most important advances that followed.

By the mid-2000s, the contours of a comeback were coming into focus. These novel AAV vectors looked safer. They were more efficient. They offered tissue targeting that earlier approaches couldn’t. The question was no longer whether gene therapy might work. The question was: who would control the commercial rights to the best delivery technology?

That question would be answered in Rockville, Maryland.

III. Founding & The Penn Spin-Out Story (2008-2009)

By the summer of 2008, the global financial system was coming apart at the seams. Bear Stearns had already been rescued. Lehman Brothers would collapse in September. Biotech was getting hit from every angle: public markets were shutting, venture firms were pulling back, and “funding a science project” was not exactly the mood.

And yet—this is when REGENXBIO was born.

The company was originally formed on July 16, 2008 as ReGenX, LLC, a Delaware limited liability company. The founding team wasn’t the stereotypical gene therapy crew, either. James Brown (COO) and Kenneth Mills (CEO) were trained as chemists. They’d worked at a diagnostics company called IGEN in the late 1990s and early 2000s, and later at Meso Scale Diagnostics.

That background mattered. Mills, in particular, brought financial and operational horsepower more than academic pedigree. Before REGENXBIO, he was Chief Financial Officer and Vice President of Business Development at Meso Scale Diagnostics. He’d spent his career living in the practical world of building and financing life-sciences businesses—which meant he could look at gene therapy with a different lens. Less “is this a beautiful scientific idea?” and more “if this works, how does value actually accrue?”

That outsider’s perspective only got sharper through FoxKiser, the biotechnology consultancy that helped catalyze the company alongside Penn and the Wilson Lab. Through that work, Mills got pulled into the gene therapy world. And because he wasn’t shaped by the field’s trauma in the same way, he could evaluate the opportunity with fresh eyes—rigorously, commercially, and without being permanently spooked by past failures.

The timing, while brutal, created its own opening. Gene therapy was still fighting its way back from the Gelsinger era, and investors were fleeing risk assets. But that also meant a rare window to secure something that would be almost impossible to replicate later: exclusive rights to Penn’s AAV gene delivery technology.

That license was the bedrock. Everything that followed—every internal program, every partnership, every royalty check—traced back to controlling those delivery trucks.

From the beginning, the vision was not “pick a disease, build a drug.” Most biotechs are product-first: choose a target, push a candidate through trials, then try to commercialize. REGENXBIO aimed to be a platform company, built around a dual-engine model.

Engine one was licensing. REGENXBIO would grant other companies rights to use the NAV Technology Platform in specific indications, collecting upfront payments, milestones, and royalties.

Engine two was internal development. Using royalty income and other funding, REGENXBIO would build its own pipeline of proprietary in vivo gene therapy programs.

That hybrid approach was an attempt to get the best of both worlds—and avoid the worst. Pure platform companies can end up as the supplier watching someone else strike gold. Pure product companies live and die on a small number of clinical bets. REGENXBIO was trying to thread the needle: a recurring licensing business to create leverage and validation, plus owned programs to capture the real upside.

REGENXBIO’s mission is to transform the lives of patients suffering from severe diseases with significant unmet medical need by developing and commercializing in vivo gene therapy products based on REGENXBIO's NAV Technology Platform. REGENXBIO seeks to accomplish this mission through a combination of internal development efforts and third‐party NAV Technology Platform licensees.

Early on, the investor thesis essentially boiled down to two questions. First: how valuable could the NAV platform become as a licensing asset? Second: could REGENXBIO use that platform advantage to build internal programs that ultimately mattered even more?

Those answers would take years. But by 2009, the foundation—exclusive rights, a platform mindset, and a business model built for a long war—was in place.

IV. Building the Platform: The NAV Technology Portfolio (2009-2014)

So what, exactly, did REGENXBIO own?

The answer is the NAV Technology Platform: exclusive rights to AAV7, AAV8, AAV9, AAVrh10, and more than 100 other novel AAV vectors discovered through research aimed at building safer, more effective gene delivery vehicles than the early AAVs that came before. Compared to earlier-generation vectors, NAV’s differentiators were straightforward but powerful: higher expression with better durability, broader and more selective tissue targeting, reduced immune response, and improved manufacturability.

A good way to picture it is keys and locks. Different AAV serotypes “fit” different tissues. AAV8 showed particularly strong tropism—its natural targeting ability—for the liver and the retina. AAV9 could cross the blood-brain barrier, opening the door to treating diseases in the central nervous system. AAVrh10 looked promising in muscle tissue. The whole NAV library came from a deliberate push to overcome the limitations of the original set of vectors, AAV1 through AAV6, which were useful but often underpowered, hard to target, or hard to translate into real-world therapies.

And NAV wasn’t just about where you could go in the body. It was also about whether you could ever get a product made at scale.

Gene therapies are notoriously hard to manufacture. These aren’t small molecules you can synthesize and bottle. They’re living, biological constructs that have to be produced in cell systems, purified, and carefully characterized batch by batch. During these years, REGENXBIO leaned into the idea that vector performance and vector manufacturability are inseparable—because a therapy that works in a lab but can’t be reliably produced isn’t a therapy at all. The NAV vectors’ favorable manufacturing characteristics would become more important as programs moved from experiments to patients, and from patients to commercial scale.

At the same time, REGENXBIO’s licensing playbook started to mature. In some indications, it granted exclusive licenses—one partner, one shot, maximum concentration of rights. In others, it chose non-exclusive licenses, letting multiple companies build on the same underlying vector technology. Each approach came with tradeoffs: exclusivity could mean bigger economics per deal, while non-exclusivity spread NAV across more programs and reduced the company’s dependence on any single partner succeeding.

The partner roster grew and, with it, the platform’s credibility. REGENXBIO enabled leading global partners including Baxter Healthcare, Fondazione Telethon, Audentes Therapeutics, Lysogene, Esteve, AveXis, AAVLife and Voyager Therapeutics to use its NAV Technology.

One partnership in particular would end up looming over the entire gene therapy industry: AveXis.

In 2014, AveXis licensed NAV AAV9 to develop a gene therapy for spinal muscular atrophy, a devastating genetic disease and the leading genetic cause of infant death. That program would eventually become Zolgensma—and even before the world knew that name, the deal signaled something important: NAV wasn’t just interesting science. It was becoming foundational infrastructure for therapies that could actually matter.

While partners took NAV into their own disease areas, REGENXBIO was quietly building its second engine: internal development. The company began leveraging the same platform to pursue gene therapy treatments for Hurler Syndrome (MPS I), Hunter Syndrome (MPS II), wet age-related macular degeneration, and X-linked retinitis pigmentosa.

By the end of this period, the blueprint was set. Licensing could bring validation and future royalties. Owned programs could capture the real upside.

The only problem was time. In biotech, “future royalties” can be another way of saying “not soon enough.” The looming question was whether either engine could generate meaningful value before REGENXBIO ran out of runway.

V. Key Inflection Point #1: The Spark Therapeutics IPO & Luxturna Approval (2014-2017)

If you had to pick the day gene therapy truly stepped out of exile, December 19, 2017 is a strong contender. That Tuesday, the FDA approved Spark Therapeutics’ Luxturna for a hereditary form of vision loss—making it the first gene therapy for an inherited disorder cleared in the U.S. for commercial use. After nearly two decades of skepticism and stop-start progress, the message was suddenly simple: this can work.

Luxturna (voretigene neparvovec) treated patients with an inherited retinal disease caused by mutations in the RPE65 gene. The arc of the disease was brutal and predictable: progressive vision loss, often ending in legal blindness by someone’s twenties. Luxturna didn’t promise perfect vision. But with a single injection into the retina, it could restore enough sight for people to navigate, recognize faces, and reclaim everyday independence.

It’s worth underscoring what made that approval feel so definitive. Yes, the FDA had already labeled two CAR-T treatments for blood cancers as gene therapies. But Luxturna was different: it was the first directly administered treatment for an inherited disease caused by a genetic mutation—the first in vivo gene therapy approved by the FDA.

For REGENXBIO, Luxturna was field-level validation with a personal connection. Spark’s roots ran through Penn’s gene therapy ecosystem. And while Luxturna used AAV2—not one of REGENXBIO’s NAV vectors—the win still mattered: it proved AAV-based gene therapies could make it all the way through the regulatory gauntlet and out the other side as an approved medicine.

Then came the capital markets stamp of approval.

In September 2015, REGENXBIO went public, selling 7,245,000 shares at $22.00 per share. It had initially planned to raise about $65 million. Instead, the deal swelled to roughly $138.6 million, and the stock quickly traded above $30. The company later announced gross IPO proceeds of approximately $159.4 million.

More important than the day-one pop was what the IPO unlocked: the ability to graduate from platform-plus-research into a clinical-stage development company—funding trials, expanding operations, and pushing its own programs forward instead of only living through partners.

At the time, REGENXBIO’s NAV Technology Platform was already being used across 23 product candidates: five developed internally, and 18 pursued by partners. The narrative around gene therapy had flipped. This wasn’t science fiction anymore. It was science fact—and REGENXBIO looked less like a single bet and more like infrastructure.

And then Big Pharma made the quiet part loud.

Roche announced it had entered into a definitive agreement to acquire Spark Therapeutics for $114.50 per share in an all-cash transaction, a premium of about 122% to Spark’s closing price on Feb. 22, 2019, valuing the deal at $4.8 billion. In December 2019, Spark was acquired by Hoffmann-La Roche for $4.3 billion and continued operating as an independent subsidiary.

The punchline was hard to miss: a gene therapy company with just $27 million in Luxturna sales had been bought for $4.3 billion. The premium wasn’t about current revenue—it was about conviction that gene therapy platforms and pipelines could be worth billions before they ever reached commercial scale. And when you paired that with Novartis’s earlier $8.7 billion acquisition of AveXis—the REGENXBIO licensee behind Zolgensma—the takeaway landed even harder.

The gold rush wasn’t coming. It was already here.

VI. Building the Internal Pipeline (2015-2019)

With IPO money in the bank and the licensing model starting to look real, REGENXBIO leaned harder into its second engine: building drugs of its own. The strategy question wasn’t “can we do gene therapy?” It was “where do we place the bets that could actually carry a company?”

Their target-selection filter was pragmatic: diseases with major unmet need, clear genetic causation, biology that fit a gene-therapy approach, and a clinical path that didn’t require a decade of guesswork before you’d know whether it worked. That pushed the pipeline toward three lanes: retinal diseases, metabolic and lysosomal storage disorders, and neurodegenerative conditions.

The program that rose to the top was in the retina: RGX-314 for wet age-related macular degeneration, or wet AMD.

This wasn’t a rare-disease niche. Wet AMD is one of the biggest markets in ophthalmology, and it runs on a brutal trade: today’s standard-of-care drugs can preserve vision, but only if patients keep coming back—again and again—for injections into the eye. Those anti-VEGF medicines, like Eylea and Lucentis, work by blocking the signals that drive abnormal blood vessel growth in the retina. They’ve changed what it means to be diagnosed with wet AMD.

But they come with a catch that’s hard to overstate. Treatment is typically ongoing, with injections commonly needed every four to eight weeks to maintain the effect. For patients, it’s a lifelong schedule built around clinic visits, needles, and the constant risk that missed doses mean lost vision.

RGX-314 was built to break that cycle. The idea was to swap repeated dosing of an anti-VEGF protein for a one-time gene therapy that delivers the gene encoding an anti-VEGF antibody fragment into retinal cells. Instead of returning for injections, the patient’s own cells would continuously produce the therapeutic protein—turning the eye into its own long-term drug factory.

RGX-314 is being investigated as a potential one-time gene therapy for the treatment of wet AMD.

If it worked, the payoff could be enormous. Wet AMD alone represented a massive commercial opportunity, far larger than anything in REGENXBIO’s rare-disease portfolio—and big enough to redefine what kind of company REGENXBIO could become.

At the same time, REGENXBIO kept pushing forward in diseases where the “one-and-done” promise of gene therapy felt even more existential. Mucopolysaccharidoses, or MPS, are rare disorders where patients lack enzymes needed to break down complex sugars, leading to progressive damage across the body. In MPS I (Hurler syndrome) and MPS II (Hunter syndrome), the tragedy is not just organ damage—it’s neurological decline.

Existing enzyme replacement therapies can help some symptoms, but they can’t cross the blood-brain barrier. That leaves the brain untouched, and patients and families with the most devastating part of the disease still ahead of them.

A gene therapy delivered directly to the central nervous system offered a different possibility: not just treating the periphery, but reaching the disease where current medicine can’t.

VII. Key Inflection Point #2: The Platform Scales (2018-2020)

From 2018 through 2020, something important happened to REGENXBIO’s story: it stopped being a clever platform thesis and started looking like a business with proof.

And the proof came from a partner.

In May 2019, the FDA approved Zolgensma, Novartis’s gene therapy for spinal muscular atrophy—an approval that also carried a quieter headline: this was the first FDA-approved gene therapy built on REGENXBIO’s NAV Technology Platform. REGENXBIO marked the moment publicly, and CEO Kenneth Mills called it “a major milestone for NAV Technology, gene therapy and patients and families facing SMA.”

SMA is as stark as genetic disease gets. Children lose motor neuron function, progressively and relentlessly. In its most severe form, most patients die before age two. Zolgensma aimed straight at the root cause, delivering a functional copy of the SMN1 gene using REGENXBIO’s NAV AAV9 vector so patients could produce the survival motor neuron protein they were missing.

The FDA approved Zolgensma as a one-time infusion for pediatric patients with SMA who were under two years old.

For REGENXBIO, the initial economics were meaningful, but they didn’t yet feel like a company-defining windfall. The approval triggered a $3.5 million milestone payment from AveXis. There was also a much larger carrot: an additional $80 million commercial milestone once Zolgensma hit $1 billion in cumulative sales, plus tiered royalties on sales up to a low double-digit percentage.

Then Zolgensma’s launch made that “someday” milestone a lot closer than anyone expected. In October 2020—just 17 months after approval—REGENXBIO announced it would receive the full $80 million milestone payment from Novartis based on Zolgensma crossing $1 billion in cumulative net sales.

By the third quarter of 2020, since the 2019 approval, REGENXBIO had earned more than $140 million in revenue from Zolgensma royalties and commercial milestone payments.

This was the platform model in its best form: REGENXBIO wasn’t selling Zolgensma, but it was getting paid because Zolgensma existed. The royalty stream was real. The idea that NAV could be “infrastructure” for the industry was no longer hypothetical.

Then the world shut down.

COVID-19 disrupted clinical trials across biotech, and REGENXBIO wasn’t spared. Enrollment slowed, site visits became difficult or impossible, and the sector’s stock prices whipsawed on sentiment more than substance.

But while timelines wobbled, REGENXBIO kept building the part of gene therapy that rarely makes headlines and almost always decides who wins: manufacturing. Gene therapy production is complex and expensive, and the companies that could reliably make their own vectors—rather than fight for time and capacity at contract manufacturers—were setting themselves up with a real advantage as programs moved closer to commercialization.

VIII. Key Inflection Point #3: RGX-314 Phase II Data & Pivotal Path (2021-2023)

With Zolgensma validating NAV and proving the royalty engine could turn on, REGENXBIO’s story narrowed to a sharper point: could it win with a drug it owned—especially RGX-314?

REGENXBIO and its partner AbbVie published two-year results from their first-in-human study in neovascular age-related macular degeneration, or wet AMD. The data, published in The Lancet, supported the safety and showed encouraging efficacy signals for subretinal injection of ABBV-RGX-314.

The takeaway was the kind of thing gene therapy companies live for: over two years, many participants maintained stable or improved vision and retinal anatomy while needing few—or in some cases no—supplemental anti-VEGF injections. In participants treated at therapeutic dose levels, the study also showed sustained levels of ABBV-RGX-314 protein, suggesting the therapy was doing what it was designed to do: turn the eye into a long-running producer of anti-VEGF treatment.

Those results helped set up the next major move: a full-scale partnership with AbbVie to develop and commercialize RGX-314 for wet AMD, diabetic retinopathy, and other chronic retinal diseases.

The deal itself was a headline. AbbVie agreed to pay REGENXBIO $370 million upfront, with the potential for up to $1.38 billion more in development, regulatory, and commercial milestones. In the U.S., the companies agreed to split profits equally. Outside the U.S., REGENXBIO would receive royalties.

The structure mattered as much as the dollars. AbbVie wasn’t buying the asset and leaving REGENXBIO with a small trailing check. REGENXBIO kept meaningful upside if RGX-314 became a real product. And AbbVie brought exactly what a mid-sized gene therapy company doesn’t have: global development and commercial muscle—especially in ophthalmology after its Allergan acquisition.

"Based on this data, we created a global strategic collaboration with AbbVie to start a 1,200-patient pivotal program. This is the largest in vivo gene therapy program ever conducted. And, with AbbVie's help, we've gone global—we're enrolling patients worldwide."

The pivotal effort centered on two Phase III trials: ATMOSPHERE and ASCENT. ASCENT is a multi-center, randomized, active-controlled trial evaluating the efficacy and safety of subretinal delivery of RGX-314 across two dose arms versus intravitreal injections of aflibercept, dosed according to the label. The primary endpoint is non-inferiority to aflibercept based on the change from baseline in Best Corrected Visual Acuity (BCVA) at one year. The trial is expected to enroll approximately 465 patients.

At the same time, REGENXBIO pushed on a second idea that could be just as important as the molecule: making delivery easier. Subretinal dosing requires surgery—a vitrectomy, then injection under the retina. Suprachoroidal delivery aims for a different target space using a specialized microinjector, with the promise of in-office administration without surgery.

Two separate routes of administration of RGX-314 to the eye are being evaluated, including a standardized subretinal delivery procedure as well as delivery to the suprachoroidal space. REGENXBIO has licensed certain exclusive rights to the SCS Microinjector® from Clearside Biomedical to deliver gene therapy treatments to the suprachoroidal space of the eye.

But by 2021 through 2023, the stakes were clear. Early studies can hint at durability; pivotal trials have to prove it. The Phase III program would decide whether RGX-314 could truly compete with the anti-VEGF standard of care—turning “one shot, potentially years” into an approved product—or whether it would join the long list of gene therapy programs that looked promising right up until the moment they had to perform at scale.

IX. The Competitive Landscape & Business Model Evolution (2020-2024)

As REGENXBIO pushed its own programs forward, the rest of gene therapy didn’t stand still. The 2020s were the era when AAV-based therapies stopped being a novelty and started becoming a category: Zolgensma for SMA, Luxturna for inherited blindness, Hemgenix for hemophilia B, BioMarin’s Roctavian for hemophilia A.

But a new reality set in: getting approved wasn’t the same thing as getting used.

Even when AAV therapies worked clinically, adoption could be slow. In 2022, the FDA approved CSL Behring’s Hemgenix as the first gene therapy for hemophilia B, followed shortly by BioMarin’s Roctavian for hemophilia A. Both offered the core promise of the whole field—a potential single-dose alternative to ongoing infusions—yet uptake for both remained limited.

A lot of that came down to a problem that gene therapy can’t outrun: sticker shock. Luxturna, Zolgensma, and Hemgenix landed among the most expensive therapies in the world, priced at roughly $850,000, $2.1 million, and $3.5 million per dose, respectively.

And that pricing isn’t just greed or ambition; it’s math. Gene therapies are designed as one-time treatments. There’s no refill business, no chronic tail of prescriptions. So the developer tries to capture, upfront, what might otherwise be years of medical value. The problem is that most healthcare systems are built to pay for costs over time, not to write a single check that pulls years of benefit into one transaction. Even when the long-term economics can make sense, the mechanics of reimbursement often don’t.

At the same time, the race in the eye got crowded. Adverum Biotechnologies, Gyroscope Therapeutics (which Novartis acquired), and others advanced competing approaches for wet AMD and adjacent retinal diseases. The competition wasn’t just about getting across the FDA finish line—it was about being first, and being good enough to replace a standard of care that already works.

The broader AAV field also started to look more brittle than it had during the boom. In September 2025, Biogen officially discontinued all gene therapy programs using AAV capsids, following similar moves by Vertex Pharmaceuticals, Pfizer, and Takeda. AAV, once treated as the default delivery truck for in vivo gene therapy, was now being evaluated in a tougher, more disciplined environment.

All of that pressure made REGENXBIO’s core strategy feel less like a nice-to-have and more like survival: breadth in its platform, and control over manufacturing. Companies relying heavily on contract manufacturers often ran into capacity limits and quality headaches. REGENXBIO’s internal manufacturing was expensive, but it offered something that’s hard to buy in a rush—control over one of the most critical bottlenecks in the entire gene therapy stack.

X. Key Inflection Point #4: Recent Developments & Current State (2024-Present)

In the present moment, REGENXBIO is trying to do the hardest thing in biotech: graduate from “promising platform” to “commercial company,” while its biggest clinical bets are still in motion.

That shift has come with a baton pass at the top.

Curran Simpson, the company’s Chief Operating Officer, was appointed President, Chief Executive Officer, and a member of the Board of Directors, effective July 1, 2024. Co-founder Kenneth T. Mills stepped down as President and CEO after 15 years, and took on an expanded role as Chairman of the Board.

Simpson had already been running much of the operational core. Since becoming COO in January 2023, he led key functions including Research and Clinical Development, Corporate Strategy, and Manufacturing and Quality—exactly the mix you’d want in charge as a gene therapy company moves from trials toward filings and, potentially, launch.

The timing wasn’t accidental. The company was approaching multiple inflection points, starting with its rare-disease pipeline. REGENXBIO initiated its BLA submission for RGX-121 and expected to complete it in the first quarter of 2025. RGX-121, for MPS II (Hunter syndrome), represents REGENXBIO’s first potential proprietary product approval. The company positioned it as potentially the first gene therapy and one-time treatment approved for MPS II, and approval could result in receipt of a Priority Review Voucher in 2025.

Meanwhile, the crown-jewel eye program stayed on a longer clock. Pivotal data evaluating the safety and efficacy of subretinal delivery of ABBV-RGX-314 in patients with wet AMD were expected in 2026. AbbVie and REGENXBIO also planned the Phase 3 clinical program of investigational ABBV-RGX-314 in diabetic retinopathy.

All of this only matters if the company can stay funded long enough to reach the readouts—and, ideally, get through a launch. Cash, cash equivalents, and marketable securities were $302.0 million as of September 30, 2025, up from $244.9 million as of December 31, 2024. The increase was primarily driven by two moves: a $110.0 million upfront payment from the Nippon Shinyaku partnership in March 2025, and $144.5 million in net proceeds from a royalty monetization with HCRx in May 2025.

REGENXBIO expected that $302.0 million balance as of September 30, 2025 to fund operations into early 2027.

And it wasn’t just eye disease and MPS. The company also kept pushing in Duchenne muscular dystrophy with RGX-202. REGENXBIO said the pivotal trial was nearly 50% enrolled, and expected to complete enrollment in 2025, share topline data in the first half of 2026, and submit a BLA under the accelerated approval pathway in mid-2026. Results to date from the ongoing Phase I/II trial showed what the company described as a favorable safety profile with no serious adverse events or adverse events of special interest, along with robust microdystrophin expression and improved functional outcomes at nine and 12 months.

XI. The Business of Gene Therapy Platforms

REGENXBIO’s story makes the core tension of platform biotech impossible to ignore: the thing that makes the model powerful is also the thing that makes it hard.

The “Intel Inside” analogy is tempting, but it breaks down the moment you look closely. Intel won because the microprocessor became a standardized component shipped at massive volume, and the economics of manufacturing scale kept compounding in its favor. Gene therapy vectors aren’t like that. They aren’t standardized, they aren’t interchangeable, and they don’t move in consumer-electronics quantities. Every program has its own biology, its own dosing, its own manufacturing and regulatory nuance. Even when a vector platform is broadly useful, each use case still behaves like a custom build.

That leads to the second tension: royalties arrive late.

A platform company can sign licensing deals early, but the meaningful money tends to show up only if a licensee actually gets a product approved and onto the market—often a decade or more after the original agreement. In the meantime, the platform company still has to pay for science, manufacturing, and clinical development. For REGENXBIO, that meant years where royalties were more idea than income, and where staying alive required raising equity capital—diluting shareholders along the way.

Zolgensma changed that. Novartis’ commercial success with a NAV-based therapy didn’t just validate the science; it validated the business model. It turned licensing from “eventual upside” into recurring, non-dilutive revenue—money that could help fund REGENXBIO’s R&D engine without constantly going back to the market.

But platform advantages also decay. Patents expire. New vector designs and novel capsids get engineered. Non-viral delivery and gene editing approaches can route around viral vectors entirely. In gene therapy, being early matters—but it doesn’t guarantee permanence.

That’s why it helps to look at the broader category of platform biotechs. Moderna and BioNTech proved how valuable an mRNA platform could be, but they spent years as cash-burning clinical-stage companies before the world handed them a once-in-a-century demand shock. Alnylam pioneered RNA interference and took two decades to reach meaningful profitability. Ionis built an antisense platform that threw off royalties while it advanced its own pipeline—a structure that looks a lot like REGENXBIO’s dual-engine approach.

The pattern is consistent: platform-based biotechs can create enormous optionality, but the platform alone is rarely enough. You need patient capital, you need multiple clinical shots on goal, and, sooner or later, you need product-level success that proves the platform isn’t just enabling other companies—it can anchor enduring value on its own.

XII. Strategic Analysis: Porter's 5 Forces

Threat of New Entrants: Medium-High

Gene therapy has real moats. The intellectual property is dense, the manufacturing is specialized, the regulatory path is unforgiving, and the capital requirements are huge. Building a program can take hundreds of millions of dollars and a decade or more before you have something that looks like a commercial product.

But the field is also unusually good at producing new contenders. Academic labs keep discovering and engineering new vectors. Big Pharma has spent the last few years building in-house gene therapy capabilities rather than relying on partners. And entirely different modalities—CRISPR-based editing and non-viral delivery, among others—create a path for newcomers to sidestep AAV platforms altogether.

Bargaining Power of Suppliers: Low-Medium

Making gene therapy vectors requires a supply chain of specialized ingredients: plasmids, cell culture reagents, and other components that don’t come from commodity vendors. The supplier base exists, but it’s not endless, and bottlenecks can appear fast.

This is where REGENXBIO’s manufacturing strategy matters. The more work it can do internally, the less it’s exposed to price pressure, capacity constraints, and scheduling risk from outside suppliers.

Bargaining Power of Buyers: High

This is the force that can make or break the entire category.

Even when gene therapies work, payers—private insurers, government programs, and hospital systems—ultimately decide whether patients can access them. They control reimbursement, they can restrict coverage, and they can push manufacturers into outcomes-based contracts that shift durability risk back onto the company.

Patients and physicians may want one-time, potentially curative treatments. But reimbursement is the gatekeeper. Zolgensma’s roughly $2.1 million price tag made gene therapy’s economic tension impossible to ignore, and it set the precedent for the scrutiny future one-and-done therapies face.

Threat of Substitutes: Medium-High

AAV gene therapy doesn’t compete in a vacuum. It competes against next-generation genetic medicines—CRISPR, base editing, prime editing—and it competes against incumbents that already work. For many diseases, standard-of-care drugs have long safety histories, predictable reimbursement, and physicians who know exactly how to use them.

Wet AMD is a perfect example. Anti-VEGF injections have decades of data and are highly effective. For RGX-314 to win, it has to deliver comparable vision outcomes while clearly outperforming on the thing gene therapy is selling: fewer treatments and durable benefit over time.

Competitive Rivalry: High

Competition is intense, and it shows up at every layer. There’s platform competition (AAV tech versus AAV tech), program competition (multiple shots at the same indications), and modality competition (AAV versus gene editing versus other approaches).

The list of serious players is long: Amgen, Artgen Biotech, BioMarin Pharmaceutical, bluebird bio, CRISPR Therapeutics, CSL Behring, Ferring Pharmaceuticals, Kolon TissueGene, Krystal Biotech, Novartis, Orchard Therapeutics, Pfizer, PTC Therapeutics, and Sarepta Therapeutics, among others.

XIII. Strategic Analysis: Hamilton's 7 Powers

1. Scale Economies: Emerging

REGENXBIO is building the kind of manufacturing base that, in theory, can create real scale advantages. As capacity grows, fixed costs can be spread across more programs, and each additional batch gets cheaper and easier to make. The catch is that gene therapy volumes are still tiny compared to traditional biologics, so the “factory flywheel” is only starting to spin. Scale economies are forming, but they’re not fully bankable yet.

2. Network Economies: Limited

There is a small network effect in the licensing model: every partner program that moves forward generates learnings—clinical, regulatory, manufacturing—that can spill over into other programs. Over time, that shared experience compounds. But this isn’t a classic network business where each new participant makes the platform dramatically more valuable for everyone else. The benefits are real, just incremental.

3. Counter-Positioning: Strong Historically, Fading

For years, REGENXBIO’s licensing-first strategy worked partly because the incumbents weren’t set up to do gene therapy themselves. NAV let Big Pharma buy access to cutting-edge vectors without building the capability in-house. That edge has narrowed. As large companies have built, partnered for, or acquired gene therapy platforms, REGENXBIO’s original “we’ll be the supplier” counter-position has become less unique.

4. Switching Costs: Not Applicable (Pre-Commercial)

Without commercial products, there’s no customer base locked in by habit, workflows, or contracts. Partner switching costs do exist—licensees invest time, data packages, and manufacturing processes around a given vector—but those moats aren’t absolute. If a better capsid shows up, or if strategy changes, companies can still pivot to alternative technologies.

5. Branding: Minimal

Inside gene therapy, REGENXBIO is a known quantity: NAV is a recognized platform, and Zolgensma put a spotlight on the company’s vectors. But among patients and physicians, the brand is essentially invisible. Brand power only starts to matter when a company is the one shipping the medicine—and when outcomes in the real world create trust and preference.

6. Cornered Resource: Moderate

NAV and the exclusive relationship with Penn are real cornered resources: difficult to recreate, historically important, and still valuable. But they’re not permanent. Patents expire, competitors can design around advantages, and talent moves. The long-term strength of this resource depends on whether REGENXBIO keeps extending the platform through innovation—and whether it translates that technology into winning products.

7. Process Power: Developing

This is the power REGENXBIO is still trying to earn. Reliable manufacturing, repeatable quality systems, clinical execution, and regulatory competence can become a quiet but durable advantage in gene therapy. The company has been investing here for years, but process power only becomes undeniable once you can deliver at commercial scale, consistently, under scrutiny.

Overall Assessment: REGENXBIO has real strategic powers, but most of them are still in the “promising” phase rather than the “durable” phase. Today, the company’s strength rests mainly on intellectual property (Cornered Resource) and its growing operational foundation (Process Power). Whether those strengths harden into something lasting depends on what biotech always comes back to: clinical results, approvals, and adoption.

XIV. Bull vs. Bear Case

The Bull Case

In the best version of this story, everything starts with the eye.

RGX-314 works in wet AMD. ATMOSPHERE and ASCENT come back showing it can match today’s anti-VEGF injections on vision outcomes while delivering what patients and doctors actually want: durability. If a one-time gene therapy can keep people off frequent injections for long stretches, it doesn’t need to replace the entire market to be meaningful. Wet AMD is already a large and growing category, and even a slice of it could be worth a lot. And unlike a typical licensing deal, REGENXBIO doesn’t just collect a small royalty here—it has a 50% U.S. profit share with AbbVie, meaning real participation if the product becomes a standard option.

At the same time, the platform engine keeps doing what it’s supposed to do. Zolgensma continues to throw off royalties, giving REGENXBIO recurring, non-dilutive cash. Other partners move their NAV-based programs closer to the market, widening the base of potential milestones and royalties.

Then the rare-disease pipeline adds a second leg to the stool. If RGX-121 wins approval for MPS II, it would mark REGENXBIO’s first potential proprietary product approval, help establish commercial infrastructure, and could generate a Priority Review Voucher—an asset that can be monetized and has historically commanded prices north of $100 million.

Finally, there’s strategic optionality. If you’re a large pharma company that wants gene therapy capabilities, manufacturing know-how, and a portfolio with real shots on goal, REGENXBIO is an obvious name on the list. An acquisition could create significant shareholder value even before REGENXBIO fully proves it can scale as a standalone commercial company.

The Bear Case

The bear case also starts with the eye—and it’s brutal.

RGX-314 disappoints in the pivotal trials. The durability isn’t there. The safety profile doesn’t hold up at scale. Or the efficacy simply can’t clear the non-inferiority bar against highly effective anti-VEGF drugs. If that happens, the wet AMD thesis breaks, and with it, the fastest path to becoming a true commercial biotech.

From there, the risk widens from company-specific to category-level. If durability proves inconsistent across AAV gene therapy programs, it doesn’t just hit REGENXBIO’s internal pipeline—it hits the value of the licensing model itself. And safety risk isn’t theoretical. In 2025, Sarepta Therapeutics reported that three patients with muscular dystrophy died of acute liver failure following treatment with AAV gene therapies, and all of Sarepta’s clinical trials for gene therapy products were put on hold.

Competition is the other slow-moving threat. If better vectors, non-viral delivery methods, or CRISPR-based approaches take the lead, NAV could start to look less like “Intel Inside” and more like an important early chapter—respected, but no longer the default foundation for the next wave of programs.

And then there’s the simplest bear argument in biotech: time and money. If major catalysts slip or fail, cash burn forces REGENXBIO back to the market at depressed valuations. More dilution arrives before meaningful commercial upside does.

Key Variables to Watch

- RGX-314 pivotal trial data (2026): The most important catalyst for the company

- Partner program advancement: Licensee success drives royalties and reinforces NAV’s relevance

- Cash position and financing needs: Runway determines leverage and strategic flexibility

- Competitive landscape evolution: Whether alternatives to AAV gain real traction

XV. Lessons for Founders & Investors

REGENXBIO’s journey offers a handful of lessons that travel well beyond gene therapy.

Platform vs. Product Strategy: The dual-engine model—platform licensing plus internal drug development—looks clean on a slide, but it’s messy in practice. Every dollar you put into your own trials is a dollar you can’t bank as high-margin platform profit. And every licensing check you cash makes it easier to rationalize staying “just” a platform. The hard part isn’t coming up with the model. It’s making disciplined, repeatable capital-allocation decisions when the payoffs show up years apart.

University Technology Transfer: The entire company rests on one foundational move: securing exclusive rights to AAV gene delivery technology from the University of Pennsylvania. Academia is where a lot of category-defining IP is born—but turning that IP into a business means living inside the friction. Negotiating licenses, keeping research relationships healthy, and defending rights over time isn’t a side quest. It is the job.

Manufacturing as Competitive Advantage: In gene therapy, manufacturing isn’t back-office plumbing—it’s part of the product. The companies that can make vectors reliably, at quality, and at scale don’t just save money; they buy speed, control, and credibility with regulators. Asset-light models can look efficient early. They can also become the bottleneck when it’s time to deliver.

The Long Game: Biotech runs on patience, whether investors like it or not. REGENXBIO was founded in 2008, and its lead internal program, RGX-314, wasn’t expected to deliver pivotal data until 2026. That’s the real timeline of building medicines. If you don’t have patient capital and a business model that can survive the waiting, the science doesn’t matter.

Optionality and Probability-Weighted Outcomes: Biotech forces probabilistic thinking. Most programs fail. The way you survive that math is with shots on goal: multiple programs, multiple indications, different risk profiles, and enough flexibility to double down when the data earns it. Optionality isn’t a buzzword here—it’s what keeps a company alive long enough to find the winners.

XVI. Epilogue: What's Next for REGENXBIO?

The next 12 to 18 months are set up to shape REGENXBIO’s next decade.

The biggest catalyst is still the eye. Data from the ATMOSPHERE® and ASCENT™ pivotal trials evaluating the safety and efficacy of subretinal delivery of ABBV-RGX-314 in patients with wet AMD are expected in 2026. Those readouts are the company’s clearest make-or-break moment: a positive outcome would cap years of platform building with a credible path to a major commercial product, and it would prove that the AbbVie partnership was the right way to take this bet to scale. A negative outcome wouldn’t just be a miss on one asset—it would force a hard reset on the whole platform-plus-products story.

And the clock is running in wet AMD. The race isn’t only against a disease that steals vision; it’s against a standard of care that keeps getting better. Anti-VEGF therapies continue to evolve through longer dosing intervals, new delivery approaches, and biosimilars that can compress costs. Gene therapy still offers something those tools can’t—a step-change in durability—but the window for disruption isn’t open forever.

That leads to the bigger question hanging over the whole category. The debate is no longer “can AAV work?” Luxturna and Zolgensma already answered that. The question now is whether AAV can remain a durable foundation for the next generation of gene therapies.

The technology stack is shifting under everyone’s feet. CRISPR-based approaches are moving deeper into clinical validation. Non-viral delivery keeps advancing. The AAV platform that felt like the obvious delivery truck in 2015 may face real pressure by 2030. For REGENXBIO, NAV’s long-term relevance depends on continued innovation—and, more than anything, on turning that innovation into approved medicines that physicians actually use.

There’s also always the strategic wildcard: M&A. Big Pharma’s appetite for gene therapy assets has persisted through the hype cycles, and REGENXBIO—with a validated platform, major commercial partnerships, and late-stage programs—will remain a plausible target. An acquisition could crystallize value for shareholders, but it would also close the book on the independent-company version of this story.

In the end, the success case is still the simplest to say and the hardest to do: one-time treatments that cure, or meaningfully transform, severe genetic diseases. That ambition—curing blindness, metabolic disorders, muscular dystrophy with a single injection—is what powered REGENXBIO from the start, and it’s what justifies the scientific, clinical, and financial risk.

The business model to fund that ambition is still being proven. But the platform is real. The bets are placed. The next chapters will be written in pivotal readouts—and, if the data holds, in the unforgiving reality of launch and adoption.

XVII. Critical KPIs for Ongoing Monitoring

If you’re tracking REGENXBIO as an investor, there are three metrics that tell you—quickly—whether the story is strengthening or getting shakier.

1. Zolgensma Royalty Revenue Trajectory

Quarterly royalties from Zolgensma are the cleanest, most “real” read on whether the NAV platform is still throwing off commercial value. This is non-dilutive cash that helps fund the pipeline and keeps the licensing model grounded in something more than promise.

If those royalties start sliding—whether from competition, pricing pressure, or market maturation—it’s an early warning that the platform’s economic engine may be weakening. If they hold steady or grow, it’s ongoing proof that NAV remains relevant in the market, not just in the lab.

2. Clinical Milestone Achievement Rate

In biotech, timelines are part science and part execution. So watch how often REGENXBIO hits what it says it will: enrollment targets, data updates, and regulatory submissions.

Companies miss timelines all the time for legitimate reasons. But a consistent pattern of slipping milestones is one of the fastest ways credibility erodes—especially when the company’s value is tied to a handful of major readouts. Consistent follow-through, on the other hand, is a strong signal that management can actually run a late-stage development and manufacturing organization.

3. Cash Runway (Months of Operations)

REGENXBIO is still in the phase where cash is oxygen. The key isn’t just how much cash sits on the balance sheet, but how many months of operations it buys relative to the next major milestones.

If the runway is shrinking faster than the catalysts are approaching, the company risks being forced into financing from a position of weakness. If runway is stable or extending—through disciplined spend, partnerships, or other non-dilutive capital—it buys flexibility: more control over strategy, better negotiating leverage, and more time to let the data speak.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube