ATRenew: Mining the Urban Gold Mine

I. Introduction & The Hook

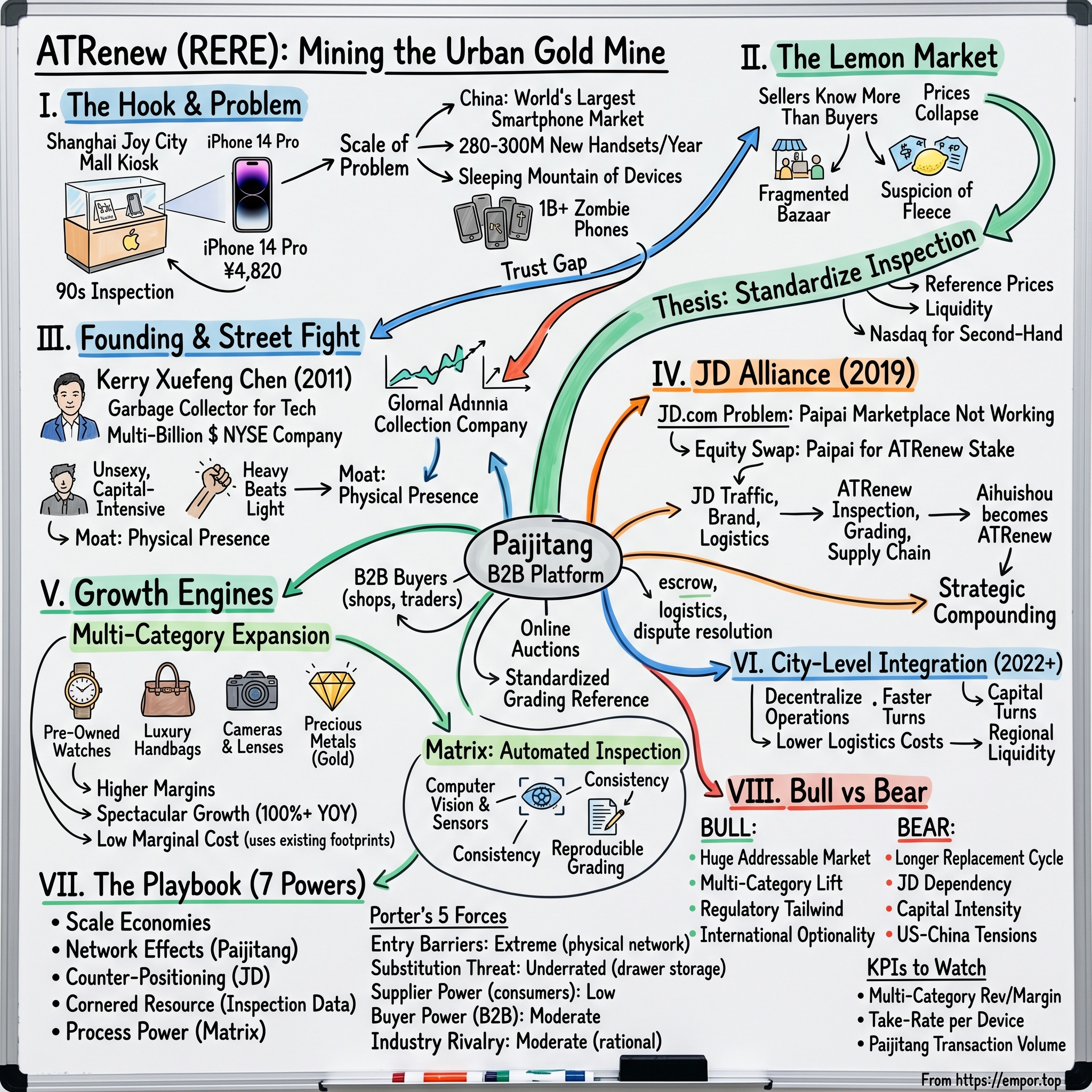

Picture a Saturday afternoon in late 2024 inside the Joy City mall in Shanghai's Jing'an district. Shoppers drift past Louis Vuitton, Apple, and a Starbucks Reserve. But tucked between a luxury watch boutique and a cosmetics counter, there is a small, brightly lit kiosk. The branding is clean, almost Apple-like in its restraint. The staff wears uniforms. There is a glass-walled inspection booth where a young technician slides a customer's iPhone 14 Pro into a black machine that looks like a cross between a CT scanner and a vending machine.

Ninety seconds later, a price flashes on the screen. ¥4,820. The customer nods. A QR code is scanned. The money lands in her Alipay account before she finishes her coffee.

This is not a pawn shop. It is not a charity recycler. It is not a flea market. It is a single physical node in what has quietly become the largest standardized pre-owned consumer electronics network in the world. The company behind that kiosk is ATRenew Inc., listed on the New York Stock Exchange under the ticker RERE.

To understand why this matters, consider the scale of the problem. China is the world's largest smartphone market. The country sells roughly 280 to 300 million new handsets every year. The country also sits on a sleeping mountain of devices estimated by industry researchers at well over a billion units, the vast majority of them stuffed into desk drawers, kitchen cupboards, and shoeboxes. These are the "zombie phones" of the Chinese consumer economy. Each one contains gold, silver, palladium, copper, rare earth elements, and roughly $50 to $400 of residual market value if anyone could be trusted to extract it honestly.

That last word is the entire game. Trust.

Before ATRenew, the second-hand electronics market in China was what economists call a lemon market, a reference to George Akerlof's famous 1970 paper on used cars. Sellers knew more than buyers. Buyers assumed the worst. Prices collapsed to the lowest common denominator. Everyone lost. The result was a fragmented bazaar of corner shops, Taobao listings of dubious provenance, and the persistent suspicion that whoever was on the other side of the transaction was about to fleece you.

ATRenew's thesis, articulated patiently across more than a decade by founder Kerry Xuefeng Chen, was simple to state and brutally hard to execute. If you could standardize the inspection of a used phone the way the Chicago Mercantile Exchange standardized the inspection of pork bellies, you could create a real market. You could create reference prices. You could create liquidity. You could create, in effect, a Nasdaq for second-hand goods.

This is the story of how a Fudan University graduate who started as a self-described "garbage collector for tech" built a multi-billion dollar NYSE-listed company by doing the unsexy, capital-intensive work that nobody else in Chinese internet wanted to touch. It is also a story about why heavy beats light, why physical beats digital, and why the most interesting companies in the world are sometimes the ones hiding behind a kiosk at the mall.

Let us begin where every great Chinese internet story begins: with a young, ambitious, slightly stubborn founder and a market that everyone else thought was beneath them.

II. The Founding & The Street Fight

In 2011, Kerry Xuefeng Chen was twenty-nine years old. He had a degree from Fudan University, one of China's most prestigious schools, and the kind of resume that should have led him to a venture-funded SaaS company or a comfortable role at Tencent or Alibaba. Instead, he started a company called Aihuishou, which translates roughly to "Love Recycle." The company did exactly what its name suggested. It bought used phones from consumers and resold them.

In 2011, this was not a respectable business. It was, frankly, the kind of thing your parents asked you not to talk about at dinner. The Chinese second-hand electronics trade was associated with shadowy figures in the Huaqiangbei electronics market in Shenzhen, with stolen phones and grey-market exports, with the unglamorous bottom rung of the consumer economy. Selling a refurbished phone in China carried a stigma comparable to selling a used mattress in the United States. The customer assumed the device was broken, stolen, or both.

Chen saw this differently. He had spent time studying the American market, particularly Gazelle, the Boston-based recycler that had raised significant venture funding to do exactly this kind of business in the United States. He noticed that Gazelle had hit a ceiling. Pure online recycling worked for a certain segment of the population, but it left the bulk of the market untouched. People wanted to see who they were dealing with. They wanted their device inspected in front of them. They wanted cash, or its mobile equivalent, immediately. They did not want to mail an iPhone to a warehouse in some faraway city and wait two weeks for an offer that might be lower than promised.

The early years of Aihuishou were a brutal education in this lesson. The company tried the pure online model first, because that was what investors wanted to fund. It built a website. It accepted mailed-in devices. It made offers. The unit economics were terrible, the conversion rates were dismal, and the customer experience was fraught with disputes. A typical interaction went like this: a customer mailed in a phone described as "like new," the inspection center found scratches and a depleted battery, the offer was revised downward, the customer accused the company of theft, and everyone was unhappy.

Chen's response, in roughly 2014 and 2015, was to do the thing that none of the venture capital playbook said to do. He went physical. He started building kiosks inside shopping malls.

To appreciate how counterintuitive this was, you have to remember the prevailing wisdom in Chinese internet at the time. Mobile was eating everything. WeChat was becoming the operating system of daily life. Alibaba and JD were demonstrating that China would skip past the brick-and-mortar phase entirely. The smart money was going into pure-play mobile applications. And here was Chen, signing five-year leases for retail space at premium rents in Joy City, IFC, and Wanda Plaza locations, building inspection booths, hiring uniformed staff, and trying to convince mall traffic to walk in with their old phones.

The math, on paper, looked terrible. The mall locations were expensive. The throughput per kiosk was modest. The capex was enormous. Competitors mocked the strategy. Several pure online players raised more money on the promise of "asset light" digital recycling.

What Chen understood, and what those competitors did not, was that the bottleneck in the second-hand market was not technology. It was trust. And trust, in a high-value transaction involving a device that contained the customer's personal photos, banking apps, and intimate digital life, was a function of physical presence. A kiosk in a Tier-1 mall said something that no website could say. It said: we are here. We are not going anywhere. If you have a problem, you can find us.

Chen also embraced what he privately called his long-termism. He has been compared to Jeff Bezos in this regard, and the comparison is not entirely unearned. Like Bezos, Chen was willing to absorb years of operating losses to build the infrastructure that would eventually become a moat. Like Bezos, he was willing to be misunderstood by public market investors and even by some private market backers. Like Bezos, he believed that the heavier and uglier the business, the more defensible it would be when it finally worked.

The pivotal years were 2016 and 2017. The kiosk network expanded to a few hundred locations. Volume started to compound. The company began collecting something that no online competitor could match: a proprietary, ground-truth dataset of millions of physical inspections. Every scratch, every battery health reading, every screen blemish, every functional test result was logged. This dataset would later become the raw material for the automated inspection systems that would define the company's technology moat.

By the late 2010s, Aihuishou had outgrown the corner shop image. It had become something stranger and more ambitious. A retail operator. A logistics company. A data company. A trust franchise. And it was about to attract the attention of the largest e-commerce empire in China.

III. Inflection Point #1 - The JD Alliance and the Paipai Deal

In 2019, JD.com had a problem. Specifically, JD had a second-hand marketplace called Paipai that nobody much loved. Paipai had a long and slightly tortured history. It had originally been built by Tencent in the mid-2000s as a competitor to Taobao. Tencent eventually sold it to JD in 2014 as part of the broader strategic alliance between the two companies. JD relaunched Paipai as a second-hand and refurbished goods platform. It did not really work.

The reason it did not work is instructive. JD was, and is, a magnificent first-hand commerce machine. It runs the most respected logistics network in Chinese e-commerce. It is famous for authentic products, fast delivery, and the kind of operational discipline that comes from founder Richard Liu's obsession with controlling the supply chain. But second-hand commerce is a fundamentally different business. It is not about predictable inventory and standardized SKUs. It is about messy, unique, single-unit transactions, each requiring inspection, grading, pricing, and trust. JD's culture and infrastructure were not built for this. The company was, in a sense, trying to fit a square peg into a round hole.

The Paipai deal, announced in mid-2019 and consummated over the subsequent months, was Acquired-podcast catnip. Here is the structure. JD did not sell Paipai for cash. Instead, JD contributed the Paipai business to Aihuishou in exchange for a substantial equity stake in the combined entity. The combined entity took the holding company name that would eventually become ATRenew. JD became a strategic partner and a major shareholder. JD's traffic, brand, and logistics became available to ATRenew. ATRenew's inspection, grading, and supply chain became the back-end engine for JD's second-hand ambitions.

Was this overpayment? In retrospect, it was the exact opposite. JD got something far more valuable than the cash they could have demanded. They got a permanent equity claim on the company that would become the dominant player in a market they themselves had failed to crack. ATRenew got something far more valuable than the Paipai brand. They got a top-of-funnel customer acquisition machine attached to one of the most trusted commerce brands in China.

This is the kind of deal structure that, in hindsight, looks obvious. Two companies, each strong where the other is weak, exchange equity rather than cash and align incentives for the long term. It is rare because it requires both parties to admit what they cannot do alone, and admitting weakness is not a common posture among Chinese founders.

The strategic logic compounded faster than anyone expected. With JD's user base now flowing into the funnel, ATRenew's monthly active user count grew rapidly. With ATRenew's offline kiosks now branded as JD partners, the kiosks themselves gained credibility. Customers who would never have walked into an unknown recycler walked confidently into a JD-affiliated booth.

But the most important consequence of the JD deal was something more subtle. It was the launch and acceleration of a B2B platform called Paijitang. Paijitang is the part of ATRenew that public market investors most often miss, and it may eventually be the most valuable part of the entire enterprise.

Here is how it works. Once a phone is collected, whether through a kiosk, a mail-in, a JD trade-in, or a partnership channel, it has to go somewhere. It cannot all be resold to consumers. The volume is too large, the grading too varied, the geographic distribution too uneven. The natural buyers are the thousands of small refurbishment shops, regional retailers, and export traders who actually run the downstream economy of used phones in China. Historically, these buyers had to source inventory through opaque channels, traveling to wholesale markets, negotiating one-on-one with sellers, accepting the risk of mislabeled or defective devices.

Paijitang turned this into an online auction marketplace. ATRenew's inspections became the standard. The grading system became the reference. Bidders bid against each other in real time. The platform handled escrow, logistics, and dispute resolution. The number of registered buyers grew into the hundreds of thousands. Transaction volume scaled into the tens of millions of devices annually.

This is the masterstroke that the JD deal enabled. Without JD's traffic, ATRenew would have struggled to source enough inventory to make Paijitang interesting to buyers. Without Paijitang, ATRenew would have been stuck reselling devices through retail channels with limited scale. With both, the company became a two-sided marketplace whose flywheel accelerated with every additional kiosk and every additional B2B buyer.

The lesson here is one of the most important in modern Chinese internet history. The companies that win are not always the ones with the best technology or the most capital. Sometimes they are the ones that figure out the right alliance at the right moment. The JD-ATRenew deal was, in this sense, a textbook example of capital-light strategic compounding through equity alignment.

By 2021, ATRenew was ready for its public market debut. The company listed on the NYSE in June of that year, raising significant capital and giving public investors their first window into a business that had been compounding largely out of view.

IV. The Hidden Growth Engines - Multi-Category and Automation

If you only follow the smartphone narrative, you will miss the most interesting thing happening at ATRenew right now. The smartphone business is a fine business. It is the founding business. It is the volume engine. But the growth and the margin expansion is happening elsewhere, in the categories that ATRenew quietly began building two and three years ago and that are now compounding at rates that dwarf the core.

Walk into a flagship ATRenew store in 2025 or 2026 and you will see what the business is becoming. There is a glass case with pre-owned Patek Philippe and Rolex watches, each accompanied by a printed authentication report. There is a luxury handbag section featuring Hermes Birkins, Chanel flap bags, and Louis Vuitton trunks, each with provenance documentation. There is a counter for cameras, lenses, and professional photography equipment. There is a precious metals desk where customers can sell gold jewelry for spot price plus a small premium, with assays performed on the spot. The inventory ranges from a slightly used Canon mirrorless to a vintage Audemars Piguet to a kilogram of investment-grade gold bullion.

This is the multi-category strategy, and it is the single most important driver of the company's margin trajectory.

Why does it matter so much? Two reasons.

First, the unit economics of luxury and precious metals are dramatically better than the unit economics of smartphones. A used iPhone might generate a few percentage points of gross margin after accounting for inspection, refurbishment, logistics, and the inevitable returns. A pre-owned Hermes Birkin can generate tens of percentage points. A gold transaction is essentially a spread business with minimal capital tied up beyond the float between purchase and resale. Every additional dollar of multi-category revenue contributes far more to gross profit than the same dollar of smartphone revenue.

Second, the marginal cost of adding multi-category to the existing footprint is astonishingly low. The kiosks already exist. The mall leases are already paid. The staff are already trained on inspection processes. The customer is already in the door. Adding a luxury authentication capability to a flagship store costs a fraction of building a new luxury authentication network from scratch. ATRenew is, in effect, monetizing the same square footage twice.

The growth rates in non-electronics categories have been spectacular. Reported growth has consistently exceeded 100 percent year-on-year for several quarters, driven by the combination of category expansion, footprint expansion, and the maturing brand permission to handle high-value goods. The percentage of total revenue contributed by multi-category remains modest, perhaps in the high single digits to low double digits, but the trajectory is what matters. Every percentage point of mix shift toward multi-category is a percentage point of margin uplift for the consolidated business.

Now let us talk about the technology, because this is the part that separates ATRenew from being just another reseller and turns it into something that looks more like a logistics technology company.

The system is internally called Matrix. It is a fleet of automated inspection machines that look something like industrial 3D printers crossed with photo light boxes. A phone is placed inside. The doors close. Cameras and sensors examine the device from every angle. Software analyzes the screen for cracks, the chassis for dents, the camera for sensor defects, the battery for capacity degradation. A diagnostic suite tests every functional component. Within roughly a minute, the system produces a grading report that, in early generations, matched human inspector accuracy and, in later generations, exceeded it.

The reason Matrix matters is not just that it is faster than a human, although it is. It is not just that it is cheaper than a human, although at scale it is. It is that it is consistent. Every phone is graded by the same algorithm. Every grading is reproducible. Every grading can be audited. This consistency is the foundation of the standardized pricing engine that makes Paijitang work. A B2B buyer in Foshan who bids on a Grade A device knows what Grade A means because the definition is enforced by software, not by the subjective judgment of a tired inspector at 9 PM.

This is, frankly, the unglamorous heart of the company. It is also the reason that competitors who try to enter this market from a pure software angle, building an app and partnering with third-party recyclers, tend to fail. The data exhaust from millions of physical inspections is not something you can replicate by writing code. It is a cumulative asset built over a decade of operating physical infrastructure. Every additional inspection makes the algorithms more accurate. Every additional inspection makes the pricing more reliable. Every additional inspection makes the moat deeper.

To put this in Acquired terms, the Matrix system is the industrial heart of ATRenew. It is the analog to Amazon's fulfillment centers, to Costco's warehouse SKU discipline, to TSMC's process node investments. It is the boring, capital-intensive, expertise-dense infrastructure that competitors cannot simply replicate by raising more venture capital.

The next thing to watch is whether this same automated inspection logic can be extended to luxury goods. Authenticating a Birkin is currently a human-intensive process requiring trained specialists. The early versions of computer vision authentication for luxury are promising but not yet at human accuracy. If ATRenew can crack that problem, the multi-category trajectory accelerates dramatically.

V. Management, Governance, and the Owner Mindset

To understand a Chinese internet company, you have to understand the founder. To understand ATRenew, you have to understand Kerry Xuefeng Chen.

Chen is, by Chinese tech standards, deliberately low-profile. He does not appear at the World Economic Forum. He does not have a million WeChat followers. He does not write open letters or stage product launches that go viral. He gives a small number of measured interviews each year, almost always focused on the operational details of the business rather than personal branding. In a country where founders like Jack Ma and Lei Jun have cultivated celebrity, Chen has cultivated focus.

His background matters. He grew up in a generation that came of age during China's economic acceleration in the 1990s and 2000s. He attended Fudan University in Shanghai, studied business and economics, and entered the workforce just as the first wave of mobile internet was breaking. Unlike many of his peers, who chose to ride the obvious wave into consumer apps and games, Chen made the deliberate choice to build in a category that everyone else dismissed. He has described the early years as lonely, in the sense that there were no peers building similar companies and no investors who understood why he would want to.

Chen's operating philosophy revolves around what he calls long-termism. In conversation he tends to refer to ten and twenty year horizons rather than quarterly results. He has spoken admiringly of Amazon's tolerance for sustained operating losses in service of long-run market position. He has, more controversially, defended the heavy capex of the kiosk strategy against repeated investor pressure to go asset-light. The general managerial posture is: we are building infrastructure that will compound for decades, and if you do not understand that, you are not the right shareholder.

Alongside Chen is Chen Yi, who serves as President. Chen Yi is the operational counterpart to Kerry Chen's strategic vision. The two men have been described internally as a complementary pair, with Kerry Chen focused on long-range strategy, capital allocation, and external relationships, and Chen Yi focused on day-to-day execution, supply chain, and the operational metrics that drive the business. This division of labor has been remarkably stable, which is not always the case in Chinese internet companies where founder turnover and political infighting are common.

The governance structure of ATRenew reflects an owner mindset. Kerry Chen retains a meaningful equity stake, well into double digits when including affiliated holdings, with voting power augmented through the dual-class share structure typical of US-listed Chinese tech companies. JD.com remains a major shareholder. The combination of founder ownership and strategic shareholder alignment means that the company is not run for short-term public market optics. It is run by people whose personal wealth is tied to the same long-term outcome they are asking public investors to underwrite.

The 2021 and 2022 share incentive plans are worth pausing on. These plans extended significant equity grants to senior management and key operational leaders, with vesting tied to multi-year performance metrics. The structure was deliberately back-loaded, meaning that the bulk of the value would only accrue to participants if the company achieved sustained growth and profitability over a multi-year period. This is a different model from the more typical Silicon Valley pattern of front-loaded option grants that vest over four years regardless of performance. It signals a culture of patience and a belief that the most important value creation is still ahead.

The cultural shift inside the company over the past five years has been notable. In the early days, the cultural challenge was rebuilding trust in a market that had none. Every internal meeting, every store opening, every customer interaction was oriented around proving that a second-hand device transaction could be honest and professional. The marketing was defensive. The operations were paranoid. Every dispute was a potential brand crisis.

By the mid-2020s, that battle is largely won. The cultural challenge has shifted from rebuilding trust to standardizing value. The question is no longer "can we be trusted?" The question is now "how do we extract the maximum economic value from every device that flows through our system?" This is a different problem with different mental models. It rewards engineers, data scientists, supply chain optimizers, and category managers rather than brand evangelists and trust ambassadors. The company's hiring profile has shifted accordingly.

One useful diligence overlay here is the matter of regulatory and ESG positioning. Chinese regulators have been broadly supportive of the circular economy thesis, viewing companies like ATRenew as aligned with the national policy goals of carbon reduction, e-waste management, and consumer protection. This is not to be taken for granted. Regulatory weather in China can shift quickly, as the platform companies of 2020 and 2021 learned the hard way. But ATRenew's positioning is unusually well-aligned with stated state priorities, which provides at least a partial tailwind in a regulatory environment that has been hostile to some other internet sectors.

VI. Inflection Point #2 - The City-Level Integration

By 2022, the ATRenew operating model had a problem that only successful companies experience. It was getting too centralized.

Here is what was happening. A phone collected at a kiosk in Chengdu would be packaged, shipped to a regional sorting hub, then potentially shipped again to a central refurbishment facility, then graded, then listed on Paijitang for B2B sale, then potentially shipped again to the buyer, who might be a refurbishment shop back in Chengdu. The device was making a multi-thousand-kilometer round trip to end up a few miles from where it started. Logistics costs were eating into margins. Capital was tied up in transit. Time-to-cash was being throttled by the centralized routing.

The strategic response was a quiet but profound architectural shift. Starting in 2022 and accelerating through 2023 and 2024, ATRenew began decentralizing its operations into city-level service centers. The vision was to create regional nodes capable of inspection, light refurbishment, and direct B2B distribution within their geographic catchment, supplementing rather than replacing the central facilities.

The economics of this shift are easy to underestimate from the outside but enormous on the inside. Three things happen.

First, logistics costs drop. A phone that no longer has to make a national round trip is a phone that costs less to process. At the volumes ATRenew handles, even a few yuan saved per device per cycle adds up to material margin uplift across millions of transactions.

Second, capital turns faster. The cycle time from collection to cash is compressed. A device that used to spend two weeks in transit and inspection now spends a few days. Faster turns mean less working capital tied up in inventory. Less working capital tied up in inventory means more capacity to grow without raising additional funding.

Third, regional liquidity in Paijitang improves. A B2B buyer who can take delivery within a day or two of winning an auction is a happier buyer than one who has to wait a week. Regional fulfillment increases buyer engagement, which increases auction prices, which increases the value captured per device.

This is the hidden reason that ATRenew's path to GAAP profitability accelerated through 2023 and 2024. It was not driven by any single hero metric. It was driven by the cumulative effect of many small operational improvements compounding through a more efficient architecture. The kind of structural improvement that does not show up in a single quarter but reveals itself in the slope of the margin curve over multiple quarters.

There is a useful analogy here to Amazon's same-day delivery infrastructure investments in the late 2010s. Amazon did not announce a single dramatic shift. It quietly built out a network of regional fulfillment centers, last-mile partnerships, and route optimization software. The result, over several years, was a step-change in delivery speed, customer satisfaction, and ultimately operating margin. ATRenew's city-level integration is structurally similar. It is the kind of unglamorous infrastructure investment that competitors find easy to dismiss and impossible to replicate without similar volume and capital.

The flip side of decentralization is operational complexity. A more distributed network requires more sophisticated management software, more local talent, more disciplined execution at the regional level. The risk is that quality control degrades as the network spreads, that local managers cut corners, that the brand promise of standardized inspection is undermined by inconsistent practice. ATRenew has so far managed this through a combination of automation, centralized algorithm management, and rigorous training. Whether this discipline holds as the network continues to spread is one of the operational questions worth watching.

The city-level model also positions the company for what comes next. As tier-3 and tier-4 cities in China continue to gain consumer purchasing power, the addressable market for second-hand goods is expanding outward from the coastal megalopolises. A decentralized operating model is far better suited to capture that geographic expansion than a centralized hub-and-spoke architecture. The company is, in effect, pre-building the infrastructure for the next decade of geographic growth.

This is what professional management looks like. Not the dramatic strategic pivot that gets covered in the financial press. The patient, methodical re-architecture of the operating model to support the next phase of scale. It is the kind of work that does not generate fawning magazine profiles but does generate compounding shareholder returns over time.

VII. The Playbook - Hamilton's 7 Powers and Porter's 5 Forces

Now let us put the company through the analytical wringers that every Acquired listener knows by heart. We will take Hamilton Helmer's 7 Powers framework first, then layer in Porter's classical five forces, and try to identify which structural advantages are real, which are nascent, and which are aspirational.

Helmer's framework asks where a company derives its sustainable advantage. Of the seven powers, ATRenew exhibits clear strength in several.

Scale economies are the most obvious. The fixed cost of building and maintaining automated inspection facilities, the data infrastructure to support standardized grading, the brand investment in consumer trust, all of these scale in a way that overwhelmingly favors the largest player. At ATRenew's volume of millions of devices processed annually, the per-unit cost of inspection, grading, and listing has dropped to a level that smaller competitors simply cannot match. A regional recycler trying to build a similar inspection capability would have to spread the same fixed cost across a fraction of the volume, resulting in per-unit economics that cannot compete on price while maintaining margin.

Network effects are emerging, particularly in the B2B marketplace. Paijitang is the canonical example of a two-sided market where the value to each side increases with the size of the other side. More sellers attract more buyers because there is more inventory variety. More buyers attract more sellers because there is more competitive bidding and faster liquidity. As Paijitang grows, the cost for a competitor to launch a rival B2B marketplace increases, because that competitor would have to seed both sides simultaneously without the benefit of network density.

Switching costs are real but not extreme on the consumer side. A consumer selling a single phone every few years has no particular reason to be loyal to one platform versus another, beyond brand familiarity. On the B2B side, however, switching costs are substantial. A small refurbishment shop that has integrated ATRenew's inspection API, that has trained its purchasing team on the Paijitang grading taxonomy, that has built its inventory planning around the rhythm of ATRenew auctions, faces real friction in moving to a competitor. Those switching costs deepen as the integration matures.

Counter-positioning, the structural advantage that comes from a business model competitors cannot copy without harming themselves, is partially present. JD's failure to make Paipai work as an internal product is a soft form of counter-positioning. JD's first-hand commerce business is so optimized for speed, authenticity, and standardized SKUs that taking on the messiness of second-hand transactions is structurally difficult. A pure-play e-commerce competitor cannot easily replicate ATRenew's approach without sacrificing the operational discipline that makes them good at first-hand commerce.

Cornered resource, in this framework, is ATRenew's accumulated dataset of physical inspection results. This dataset is genuinely unique. It cannot be replicated through capital. It can only be earned through the slow grind of operating physical infrastructure over time. Every additional year that ATRenew operates, the dataset grows in scope and accuracy, widening the gap between the company's grading reliability and what any new entrant could achieve.

Brand power is a legitimate but contested asset. The ATRenew brand is more trusted than the unbranded alternatives that dominated the market a decade ago. But the brand is still less universally recognized than, say, JD or Apple. The brand permission to handle high-value items like luxury watches and gold is something the company is actively building, and it is not yet at the level where consumers will reflexively choose ATRenew over a luxury authenticator.

Process power, the last of Helmer's powers, is arguably the strongest. The Matrix inspection system, the city-level operational model, the integration of online and offline channels, the management of B2B and B2C flows, all of this represents accumulated process knowledge that took more than a decade to build. A new entrant cannot simply copy the playbook. The playbook is encoded in software, in training programs, in supplier relationships, in regulatory filings. Reverse-engineering it is theoretically possible but practically impossible at the speed required to catch up.

Now to Porter's five forces.

Barriers to entry are extreme. Building a national network of physical kiosks in premium retail locations is a capital expenditure that no software company can simply spend its way past. ByteDance, with all its capital and talent, cannot wake up tomorrow and decide to operate 1,900 mall kiosks. Alibaba has tried adjacent moves through Xianyu, its peer-to-peer marketplace, and while Xianyu is large in transaction volume, it occupies a fundamentally different position in the market, focused on consumer-to-consumer rather than the standardized inspection-and-resale model.

Threat of substitution is the most underrated risk. The substitute is not another recycler. The substitute is the consumer choosing to keep the device in the drawer, to give it to a family member, to throw it away, or to sell it informally to a colleague. As long as the convenience and price gap between ATRenew and these alternatives is wide, ATRenew wins. If consumers ever decide that the friction of selling to ATRenew exceeds the value, the addressable market shrinks.

Bargaining power of suppliers is an interesting question because the suppliers are individual consumers selling their own devices. Individually, they have no power. Collectively, they exhibit price sensitivity, and the company has to maintain competitive recycling prices to keep volume flowing. The Apple iPhone trade-in programs run through partners are a particular constraint, since Apple's official trade-in pricing functions as a market reference.

Bargaining power of buyers, on the B2B side, is moderate. Individual refurbishment shops have limited power, but large institutional buyers, including export traders and regional chain refurbishers, can negotiate. The dynamic on the B2C side is straightforward, with consumer buyers facing essentially take-it-or-leave-it pricing on refurbished devices.

Industry rivalry is moderate but not lethal. The major direct competitors include Zhuanzhuan, which is backed by 58.com and Tencent, and various regional players. Xianyu, owned by Alibaba, competes for consumer mindshare in the broader second-hand category but is not directly comparable in the standardized recycling business. The competitive dynamic has been more rational than the consumer internet wars of the 2010s, with each major player carving out a distinct niche rather than burning capital in head-to-head subsidy battles.

The summary is that ATRenew's structural position is genuinely strong, with multiple reinforcing powers that have compounded over more than a decade. The risks are real but mostly external rather than competitive.

VIII. The Bull vs Bear Case

Every great company is also a great argument. ATRenew is no exception. There are intelligent investors on both sides of this stock, and the disagreement reveals what is actually at stake in the business.

Start with the bull case, because it is the more interesting story.

The bull thesis begins with the addressable market. China's installed base of consumer electronics is enormous and growing. Smartphones alone exceed a billion active devices, with a similar number of zombie devices sitting unused. Add tablets, laptops, smart watches, headphones, and the universe of connected devices, and the total addressable pool of equipment that could theoretically pass through the recycling system is vast. ATRenew's current market share, even in the smartphone category where the company is dominant, is a single-digit to low double-digit percentage of the total addressable flow. The runway, in other words, is enormous before market saturation becomes a constraint.

The bull thesis then layers in the multi-category expansion. If non-electronics revenue continues to grow at triple-digit rates and reaches twenty or thirty percent of total revenue, the consolidated gross margin profile of the company changes dramatically. The blended margin uplift, even with conservative assumptions about category-level economics, could be several hundred basis points over a multi-year period. That kind of mix-driven margin expansion, applied to a growing top line, generates the kind of operating leverage that produces compounding earnings growth.

The bull thesis also emphasizes the regulatory tailwind. China's national policy framework around carbon neutrality and the circular economy is genuinely supportive of companies in ATRenew's category. The State Council has issued multiple documents emphasizing the importance of resource recycling, e-waste management, and the formalization of the second-hand economy. ATRenew is, in effect, the national champion of a sector that the state wants to grow. This is not a guarantee against future regulatory friction, but it is a meaningfully better starting position than the platform companies that ran into regulatory headwinds in 2021 and 2022.

The bull thesis also notes the optionality of cross-border expansion. The model of standardized inspection plus B2B marketplace plus B2C kiosks is not specifically Chinese. It could work in any market with sufficient consumer electronics density and a similar trust deficit in the second-hand category. Markets like Southeast Asia, India, and Latin America are obvious candidates. The company has been cautious about international expansion to date, but the optionality exists.

Now the bear case.

The bear thesis starts with the smartphone replacement cycle. Chinese consumers are holding their phones longer than they used to. The cycle has lengthened from roughly two years a decade ago to closer to three or four years now, driven by the maturation of smartphone hardware, the slowing pace of meaningful innovation, and the simple reality that people's phones are good enough. A longer replacement cycle means fewer devices flowing into the recycling system per unit time. ATRenew's volume growth in the core smartphone category depends on either expanding market share or growing the total flow, and the latter is slowing.

The bear thesis then questions the JD relationship. Is ATRenew's growth genuinely organic or is it largely a function of JD's traffic gift? If JD's own commerce growth slows, or if JD decides for any reason to redirect strategic priorities, what happens to ATRenew's customer acquisition? The relationship is contractually structured for the long term, but contracts can be renegotiated, and the dependency is real.

The bear thesis also flags the capital intensity. ATRenew's business model is fundamentally heavier than a pure software company. The kiosks require ongoing rent and capex. The regional centers require investment. Working capital requirements for inventory are substantial. In a rising interest rate environment, the cost of carrying this capital intensity rises. If margins do not expand fast enough to absorb the cost of capital, the financial returns of the business compress.

There is a related concern about competitive pressure on take-rates. As the second-hand market formalizes, the spread between what ATRenew pays consumers and what it sells devices for could compress under competitive pressure. Zhuanzhuan, Xianyu, and other competitors are not standing still. If a price war develops, the take-rate of the entire industry could compress and the unit economics deteriorate.

A second-layer diligence concern is the macroeconomic sensitivity of the business. Second-hand consumer goods are a partially counter-cyclical category. In a downturn, more consumers sell their devices to raise cash and more consumers buy used rather than new. But the same downturn can also reduce overall consumer device replacement, dampening the volume flow. The net effect is ambiguous, and the company's revenue trajectory has shown some sensitivity to the broader Chinese consumption environment.

There is also the perpetual concern about US-listed Chinese ADRs. The PCAOB audit access agreement reached in 2022 reduced but did not eliminate the risk that political tensions between Beijing and Washington could disrupt the listing of Chinese companies on US exchanges. ATRenew, like its peers, carries some structural discount in its valuation reflecting this overhang. Any deterioration in the bilateral relationship could weigh on the multiple regardless of the operational performance.

The honest synthesis is that the bull case requires you to believe in the multi-category expansion, the operational leverage of the city-level model, and the broader formalization of the Chinese second-hand economy. The bear case requires you to believe that the smartphone slowdown will outpace those positive trends and that capital intensity will weigh on returns. Both cases are intellectually defensible. The investor's job is to weigh which thesis aligns with the operational data over the next several years.

The KPIs to watch, narrowed to the most important, are these. First, the growth rate and gross margin of the multi-category business as a percentage of total revenue, because this is the single largest swing factor on consolidated margin. Second, the take-rate or net revenue per transacted device, because this captures both pricing discipline and the maturation of the value-added services layer. Third, the volume and frequency of Paijitang B2B transactions, because this reflects the health of the marketplace flywheel and the depth of the buyer network. Three numbers. Track those, and you will understand most of what matters about the business.

IX. Conclusion and Final Reflections

There is a temptation, when telling the story of a company like ATRenew, to reach for the obvious analogy. Is this the Amazon of recycling? The Costco of second-hand? The eBay that actually figured it out? Every analogy captures something and misses something else.

The Amazon comparison fits in the founder's long-termism, the willingness to absorb operating losses for years to build infrastructure, the obsession with the customer experience as the foundation of trust. It misses in the absence of a dominant cloud business or any equivalent to AWS that could become the economic engine of the next decade.

The Costco comparison fits in the relentless operational discipline, the membership-like loyalty of B2B buyers, the patient compounding of small advantages. It misses in the absence of a membership model and the much greater technological intensity of ATRenew's business.

The eBay comparison fits in the marketplace structure and the network effects of two-sided liquidity. It misses in eBay's failure, in the United States and especially in China, to build the standardized inspection layer that ATRenew has built. eBay was, in retrospect, a marketplace without trust infrastructure. Mercari in the US has struggled with similar issues. ATRenew's central insight was that trust had to be built into the supply chain, not just into the rating system, and that insight required a fundamentally heavier business model than what either eBay or Mercari were willing to build.

Perhaps the most accurate comparison is none of the above. ATRenew is, more than anything, a Chinese internet company that learned from the failures of its predecessors and built the infrastructure that those predecessors refused to build. It is a counter-example to the common narrative that the best businesses are asset-light, capital-efficient, and rapidly scalable through pure software. It is, instead, an argument for the durability of asset-heavy, operationally disciplined, slowly compounding businesses in markets where trust is the binding constraint.

The lessons for founders are several. First, sometimes the right move is the one that the venture capital playbook tells you not to make. Going physical when everyone else is going digital, going heavy when everyone else is going light, going slow when everyone else is going fast. Second, alliances structured around equity rather than cash, around long-term alignment rather than short-term contracts, can create value that no single party could create alone. The JD-Paipai deal is a case study that should be taught in every business school. Third, the most defensible moats are often built out of the most boring infrastructure. Inspection booths, sorting facilities, regional warehouses, training programs. Not the kind of stuff that wins design awards, but the kind of stuff that compounds for decades.

The lessons for investors are different but related. The companies that look ugly on first inspection, that are misunderstood by public market analysts, that are classified into the wrong sector taxonomy, are often the most interesting opportunities. ATRenew has been classified at various times as a recycler, a marketplace, an e-commerce company, a logistics company, a technology company. It is, in some sense, all of these and none of them. Trying to fit it into a clean category is the analyst's failure, not the company's.

The story that began with a young Fudan graduate in 2011, in a corner of the Chinese economy that nobody respected, has become a multi-billion dollar NYSE-listed company at the heart of the largest second-hand electronics market in the world. The kiosk in the Joy City mall, where this article opened, is just one node in a network that now spans nearly two thousand locations, processes tens of millions of devices annually, and increasingly handles luxury goods, precious metals, and the long tail of consumer durables.

The Chinese expression for what ATRenew does is something like "turning waste into treasure." It is a phrase that captures both the literal economic activity of the company and the strategic insight at its core. The treasure was always there. It was just locked up in a million drawers, waiting for someone to build the trust infrastructure to set it free.

What happens next is, of course, the question that no one can answer with certainty. The smartphone replacement cycle will continue to lengthen. The multi-category expansion will continue to compound or it will hit the natural limits of consumer demand for pre-owned luxury. The regulatory environment in China will remain supportive or it will shift in ways that are difficult to anticipate. The relationship with JD will deepen or evolve as both companies pursue their own strategic agendas. The international optionality will be exercised or it will remain dormant.

What is clear is that the next decade of the Chinese consumer economy will require, more than ever, the kind of trusted, standardized, technologically enabled infrastructure that ATRenew has spent the last fifteen years building. Whether the company captures the full value of that opportunity is a story still being written. But the foundation has been laid, the moat has been dug, and the playbook has been validated. From a corner of the market that nobody wanted to a category that nobody can ignore, ATRenew is the quiet emperor of the urban gold mine.

And somewhere in a Shanghai mall this afternoon, another customer will walk up to a kiosk, hand over an old phone, and walk away with a few thousand yuan. The transaction will take less than five minutes. It will leave no obvious mark on the customer's day. But it will add one more data point to the dataset, one more device to the flow, one more brick to the wall of the moat. And that, multiplied across a country of 1.4 billion people and an economy still figuring out what to do with its abundance, is the entire business.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube