Regeneron Pharmaceuticals: The Science-Driven Biotech That Became a Giant

I. Introduction & Episode Framework

Picture this: Two scientists from Queens, New York—the sons of immigrants and public school kids—sitting in a tiny lab in 1988, dreaming of building something that had never existed before: a biotechnology company where science would come first, always. No shortcuts. No compromises. Just pure, relentless pursuit of scientific truth that could be transformed into medicines.

Leonard Schleifer was born and raised in a Jewish family in Queens, New York. George Yancopoulos and Leonard Schleifer are both from Queens, New York. These weren't your typical Silicon Valley entrepreneurs or Boston biotech aristocrats. They were scrappy outsiders with an audacious vision.

Fast forward thirty-six years: Regeneron Pharmaceuticals, Inc. is an American biotechnology company headquartered in Westchester County, New York. The company they built from scratch now boasts a market capitalization exceeding $60 billion, has created multiple blockbuster drugs generating tens of billions in annual sales, and has fundamentally transformed how the pharmaceutical industry thinks about drug discovery.

The central narrative question driving our story today is deceptively simple: How did two physician-scientists from Queens build one of the most successful biotech companies in history while refusing to play by the traditional rules of the pharmaceutical industry?

This isn't just a story about scientific breakthroughs or financial returns—though we'll have plenty of both. It's about a radical experiment in corporate structure: What happens when you actually put scientists in charge, give them decades to fail and learn, and never waver from the belief that the best business strategy is simply to do the best science?

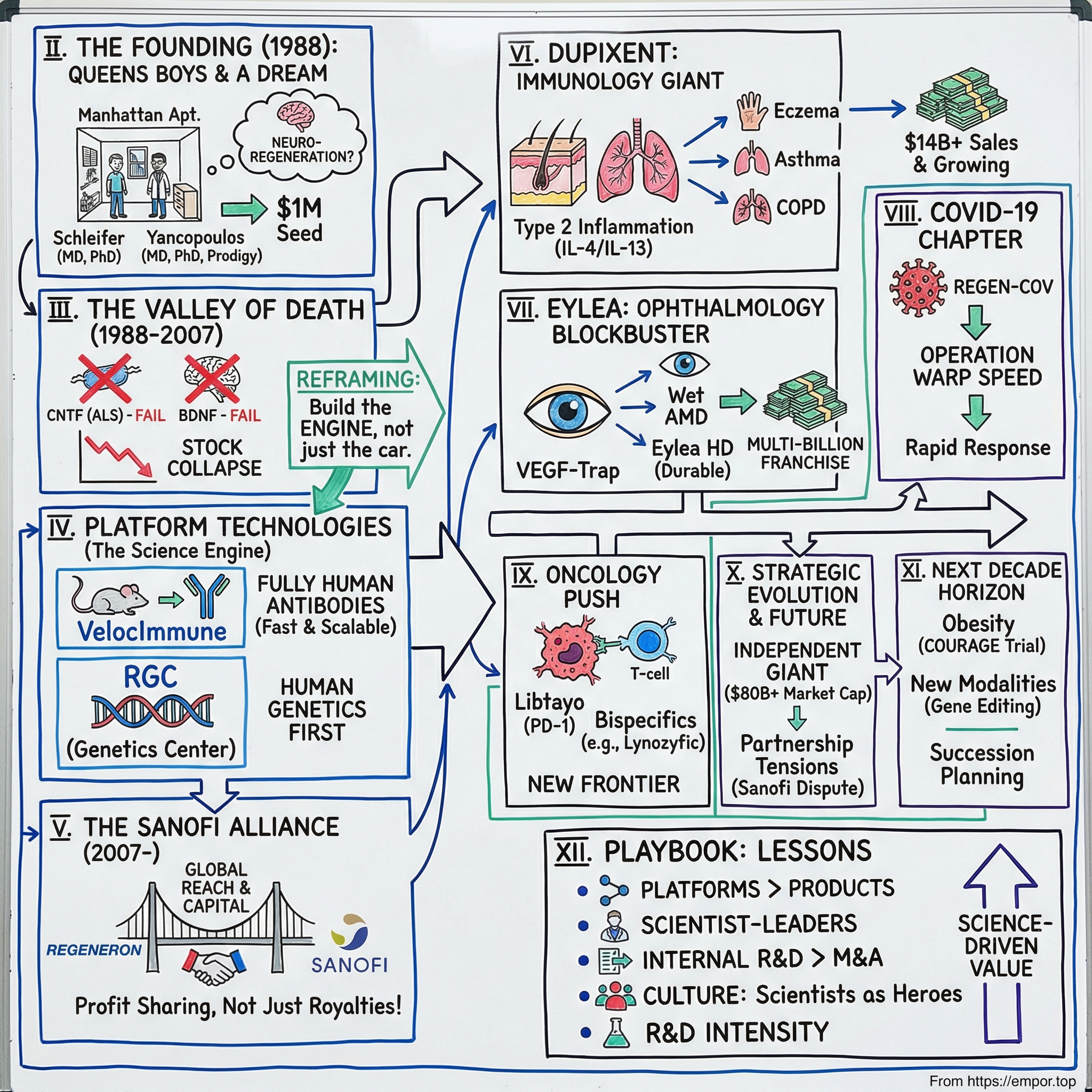

II. The Founding Story: Two Scientists from Queens

The origin story of Regeneron begins not in a boardroom or venture capital office, but in the labs and hospital wards of New York City's premier medical institutions. Len grew up in Queens, New York, with parents and teachers who sparked his passion for science and entrepreneurship from a young age. While working as a practicing neurologist and professor at Cornell Medical School, Len became frustrated with the lack of effective treatments for patients with serious neurodegenerative diseases like Parkinson's and Alzheimer's.

Leonard Schleifer wasn't your typical physician. He studied under future Nobel Laureate, Alfred G. Gilman at the University of Virginia where he earned his MD-PhD. He then worked at New York Hospital where he trained to become a neurologist and also served as a junior faculty member. But watching patients deteriorate from neurodegenerative diseases with no effective treatments available lit a fire in him. While working as a practicing neurologist and professor at Cornell Medical School, Len became frustrated with the lack of effective treatments for patients with serious neurodegenerative diseases like Parkinson's and Alzheimer's. He wondered if new biotechnologies could be harnessed to potentially make an impact for these people, their families and many others.

The pharmaceutical industry in the late 1980s was dominated by massive companies pursuing a chemical-based approach to drug discovery—essentially sophisticated trial and error with small molecules. But Schleifer saw something different emerging. Noticing that the biotechnology company Genentech was conducting state-of-the-art research but not on diseases of the nervous system, Schleifer was determined to get into the biotechnology business.

Meanwhile, across town at Columbia University, a young scientific prodigy was making waves. George is a life-long New Yorker and the son of Greek immigrants. He attended New York City public schools and graduated as valedictorian of the Bronx High School of Science. At Bronx Science, he was a top winner of the nation's premier high school science competition, then known as the Westinghouse Science Talent Search, and now known as the Regeneron Science Talent Search.

The son of Greek immigrants in New York City, George attended the Bronx High School of Science, where he wanted to be like the heroes at school and compete in the Westinghouse Science Talent Search. With the help of his teacher-mentor, Mrs. Strom, George would arrive to school at 5:30 each morning to work on his project, a top winner in the 1976 Science Talent Search. This was a life-changing experience that confirmed he would commit to a career in the sciences.

The partnership that would define both of their careers began in 1988. He also recruited George Yancopoulos, a 28-year-old scientist, to be his partner, and in 1988 they founded Regeneron Pharmaceuticals. Schleifer found a sponsor in George Sing, a venture capitalist at Merrill Lynch, and obtained $1 million in seed capital

What made their partnership special wasn't just their complementary skills—Schleifer the physician-businessman, Yancopoulos the scientific visionary—but their shared belief in a radical idea. Len founded Regeneron in 1988, with the vision of creating a company built entirely on science, where scientists are the heroes and everyone works toward the common goal of helping patients.

The name itself told the story of their ambition: Originally focused on neurotrophic factors and their regenerative capabilities, giving rise to its present name; the company has since expanded operations into the study of both cytokine and tyrosine kinase receptors, which gave rise to their first product, which is a VEGF-trap. They would regenerate neurons, cure neurological diseases, change the world.

III. Early Years: The Valley of Death (1988-2007)

Every biotech company faces what insiders call "the valley of death"—that treacherous period between founding and first product approval where capital burns fast and revenue is zero. For Regeneron, this valley would stretch nearly two decades.

The company's initial focus on neurotrophic factors seemed promising. Regeneron was founded by a neurologist with the original goal of "REGENErating neuRONs," and has been focused on neurological conditions since its early days, with our first investigational drug – a neurotrophic factor – entering clinical development in 1992. These proteins, which help neurons survive and grow, represented the cutting edge of neuroscience in the early 1990s.

Then came the crushing blow. But this initial commitment to exploring growth factors hit a snag in 1997 when our first neurotrophic factor Phase 3 trial did not achieve its primary endpoint in patients with amyotrophic lateral sclerosis, or Lou Gehrig's disease. The phase 3 trial of our first neurotrophic factor does not achieve its primary endpoint, and though the team is disappointed, we regroup to focus on new therapeutic solutions.

For most companies, this would have been the end. They'd burned through years and millions of dollars. Their lead program had failed in the most public, painful way possible—a Phase 3 trial failure in desperately ill ALS patients. But here's where Regeneron's story diverges from the typical biotech tragedy.

While disappointing, we took this failure as an opportunity enhance our understanding of growth factors. Sometimes this means revisiting hypotheses with new knowledge – like we've done with neurotrophic factors. Instead of abandoning the science, they doubled down on understanding why they'd failed.

The pivot that saved the company came from an insight: rather than trying to stimulate growth, what if they could block harmful proteins instead? This led to the development of their "Trap" technology. Regeneron's novel and patented Trap technology creates high-affinity product candidates for many types of signaling molecules, including growth factors and cytokines. The Trap technology involves fusing two distinct fully human receptor components and a fully human immunoglobulin-G constant region.

But the real game-changer was brewing in Yancopoulos's lab. Drawing on his graduate work, where VelocImmune stems from Chief Scientific Officer George D. Yancopoulos' work as a graduate student, when he was the first to envision making such a genetically humanized mouse., the team was developing something revolutionary: mice with humanized immune systems that could produce fully human antibodies.

This wasn't just an incremental improvement—it was a fundamental reimagining of how to make antibody drugs. It utilizes a proprietary mouse platform engineered with a genetically humanized immune system. VelocImmune creates a multitude of antibody drug candidates efficiently and directly from immunized mice, overcoming limitations of traditional platforms by rapidly creating fully human antibodies that tightly bind to therapeutic targets and avoid potential negative immune responses that may occur in patients receiving antibodies that contain nonhuman (typically mouse) components.

The scale of the genetic engineering required was staggering. When Regeneron's VelocImmune mice were developed, they represented the largest scale precision genetic engineering feat achieved to date. We attempted to make mice that more efficiently use human variable region segments in their humoral responses by precisely replacing 6 Mb of mouse Ig heavy and kappa light variable region germ-line gene segments with their human counterparts while leaving the mouse constant regions intact, using a unique in situ humanization approach. We reasoned the introduced human variable region gene segments would function indistinguishably in their new genetic location, whereas the retained mouse constant regions would allow for optimal interactions and selection of the resulting antibodies within the mouse environment.

By 2006, the fruits of this massive technical undertaking were becoming clear. By 2006, our first fully human antibody had entered clinical development

The transformation was complete: Regeneron had evolved from a company chasing neurotrophic factors to one possessing perhaps the most powerful antibody discovery platform in the industry. They'd survived the valley of death not by abandoning their science-first philosophy, but by embracing it even more deeply.

IV. The Sanofi Alliance: A Game-Changing Partnership (2007-2017)

On November 29, 2007, Regeneron announced a deal that would transform the company's trajectory forever. Regeneron Pharmaceuticals, Inc. (Nasdaq: REGN) and sanofi-aventis (Euronext: SAN and NYSE: SNY) announced today that they have entered into a global, strategic collaboration agreement to discover, develop, and commercialize fully-human therapeutic antibodies utilizing Regeneron's proprietary VelociSuite of technologies.

The deal structure was unlike anything the industry had seen. Sanofi-aventis will also increase its ownership of Regeneron's outstanding common stock from approximately 4 percent to approximately 19 percent by purchasing 12 million newly issued shares of Regeneron common stock at a price of $26.00 per share. Beyond the $312 million equity investment, Sanofi committed to funding Regeneron's research at unprecedented levels—initially $100 million per year.

But here's what made this partnership truly special: Regeneron maintained control. For any new product successfully developed as part of the collaboration, sanofi-aventis will take the lead in commercialization activities and will consolidate the sales. Regeneron will have the right to co-promote any and all collaboration products worldwide. In the United States, profits will be shared equally. Outside the United States, profits will be split on a pre-determined sliding scale with sanofi-aventis' share ranging from 65 percent to 55 percent.

The productivity of this partnership stunned the industry. To date, Regeneron and sanofi-aventis have advanced four therapeutic antibodies into clinical development and have filed an IND for a fifth additional antibody. Among the four antibodies in clinical development, three are antibodies to (1) the Interleukin-6 receptor (IL-6R), being developed for the treatment of rheumatoid arthritis, (2) Nerve Growth Factor, being developed for the treatment of pain, and (3) Delta-like Ligand 4 (Dll4), being developed for the treatment of advanced malignancies.

In 2009, recognizing the partnership's success, Sanofi doubled down. The antibody collaboration entered into in November 2007 was scheduled to expire at year-end 2012. As amended, the collaboration will continue at higher levels of funding through 2017. Funding increased from $100 million to $160 million annually.

The crown jewel of this collaboration would be dupilumab—later branded as Dupixent. Regeneron's collaboration with Sanofi dates back to 2007, when the partners first joined forces on the development and commercialization of the promising antibody dupilumab.

But by 2017, after a decade of extraordinary productivity, the partnership had run its course. Under a "Business Development Update" section of its financials this morning, Regeneron said quite simply: "The company's antibody discovery agreement with Sanofi will end on December 31, 2017 without any extension."

The reasons were complex—Regeneron had grown powerful enough to go it alone, while Sanofi was reorganizing its R&D priorities. But the numbers told the story of success: In addition, these mice are perhaps the most valuable ever engineered, already having brought in more than $2 billion in committed licensing fees and collaboration revenues.

V. The Dupixent Revolution: Creating a Multi-Billion Dollar Franchise

If Regeneron's platform technologies were the engine, Dupixent would be the rocket fuel that propelled the company into the pharmaceutical stratosphere. The story of Dupixent isn't just about creating a successful drug—it's about recognizing a fundamental biological insight and pursuing it relentlessly across multiple diseases.

The breakthrough came from understanding the role of interleukin-4 (IL-4) and interleukin-13 (IL-13) in driving what scientists call "type 2 inflammation." Dupixent, which was invented using Regeneron's proprietary VelocImmune® technology, is a fully human monoclonal antibody that inhibits the signaling of the interleukin-4 (IL-4) and interleukin-13 (IL-13) pathways and is not an immunosuppressant. The Dupixent development program has shown significant clinical benefit and a decrease in type 2 inflammation in Phase 3 trials, establishing that IL-4 and IL-13 are key and central drivers of the type 2 inflammation that plays a major role in multiple related and often co-morbid diseases.

March 28, 2017, marked the beginning of the Dupixent era. The U.S. Food and Drug Administration (FDA) approved DUPIXENT® (dupilumab) Injection, the first and only biologic medicine approved for the treatment of adults with moderate-to-severe atopic dermatitis (AD) whose disease is not adequately controlled with topical prescription therapies.

But Schleifer and Yancopoulos saw something bigger. If IL-4 and IL-13 drove type 2 inflammation, and type 2 inflammation underlied multiple diseases, then Dupixent could be a platform drug—one therapy for many conditions. This was pharmaceutical heresy. The industry wisdom said: one drug, one disease.

The expansion strategy was methodical and brilliant. Dupixent (dupilumab) is an interleukin-4 receptor alpha antagonist used for the treatment of atopic dermatitis, asthma, chronic rhinosinusitis with nasal polyposis, eosinophilic esophagitis, prurigo nodularis, chronic obstructive pulmonary disease (COPD), chronic spontaneous urticaria, and bullous pemphigoid.

Each new indication wasn't just a regulatory win—it was validation of the underlying scientific hypothesis. The market responded accordingly. Dupixent's trajectory has been nothing short of spectacular: The drug generated $557 million in Q2 2019, helping the Sanofi partnership turn profitable for the first time after more than a decade.

By 2024, the numbers had become astronomical. The blockbuster monoclonal antibody has seen its sales increase year-over-year amid high uptake from AD – reaching $14.9bn in sales in 2024. Full year 2024 Dupixent global net sales, recorded by Sanofi, increased 22% to $14.15 billion versus 2023.

The recent COPD approval represents perhaps the biggest opportunity yet. The FDA approved Dupixent as an add-on maintenance treatment for adults with inadequately controlled COPD and an eosinophilic phenotype—a market with millions of potential patients.

But success brought complexity. Regeneron has taken Sanofi to court over claims that its partner violated the terms of a long-standing Dupixent collaboration. Regeneron's main complaint is that Sanofi has allegedly withheld pharmacy benefit manager contracting information on Dupixent. Digging into the lawsuit, Regeneron's lawyers assert that Sanofi is required by the commercialization agreement to provide full access to Dupixent sales materials, including written and oral contracts with PBMs, payers and related organizations. The problem is, Sanofi has allegedly "stonewalled" Regeneron's "repeated requests" for full access to those PBM agreements.

VI. Eylea: The Ophthalmology Blockbuster

While Dupixent would become Regeneron's biggest success, Eylea came first and proved the company could create a blockbuster entirely on its own. The story begins with the VEGF-trap technology developed during those dark early years.

On November 18, 2011, the U.S. Food and Drug Administration (FDA) approved EYLEA (aflibercept) Injection, known in the scientific literature as VEGF Trap-Eye, for the treatment of patients with neovascular (wet) Age-related Macular Degeneration (AMD). The approval came under Priority Review, recognition that Eylea represented a major advance.

The wet AMD market was already competitive, dominated by Roche's Lucentis, which cost roughly $2,000 per injection and required monthly dosing. Eylea's advantage was elegant: equal efficacy with less frequent dosing. The recommended dose was 2 milligrams (mg) every four weeks (monthly) for the first 12 weeks, followed by 2 mg every eight weeks (2 months).

The launch exceeded all expectations. The drug was a blockbuster generating $838 million in its first full year and sales increased 55% to $1.3 billion in 2013. By 2015, Eylea grossed $1.735 billion.

The key to Eylea's success wasn't just the science—it was Regeneron's decision to maintain U.S. commercial rights while partnering with Bayer for international distribution. This gave them full control over the critical U.S. market while leveraging Bayer's global reach.

But by the early 2020s, storm clouds were gathering. Biosimilar competition was coming, and physicians were increasingly comfortable using off-label Avastin, which cost a fraction of Eylea's price. Regeneron's response was bold: rather than cut prices, they'd improve the drug.

In August 2023, the FDA approved EYLEA HD (aflibercept) Injection 8 mg for the treatment of patients with wet age-related macular degeneration (wAMD), diabetic macular edema (DME) and diabetic retinopathy (DR). The higher-dose formulation allowed for even longer intervals between injections—up to 16 weeks in some patients.

Both the PULSAR trial in wAMD (N=1,009) and PHOTON trial in DME (N=658) met their primary endpoint, with EYLEA HD demonstrating non-inferior and clinically equivalent vision gains at 48 weeks with both 12- and 16-week dosing regimens after only 3 initial monthly doses.

Fourth quarter 2024 U.S. net sales for EYLEA HD and EYLEA increased 2% versus fourth quarter 2023 to $1.50 billion, including $305 million from EYLEA HD. The transition to the higher-dose formulation was protecting the franchise, even as biosimilar competition intensified.

VII. The COVID-19 Chapter: REGEN-COV and Operation Warp Speed

No story of Regeneron would be complete without examining their remarkable—and controversial—response to the COVID-19 pandemic. When SARS-CoV-2 emerged in early 2020, Regeneron's antibody platform was perfectly positioned to respond rapidly.

On February 4, 2020, the U.S. Department of Health and Human Services, which already worked with Regeneron, announced that Regeneron would pursue monoclonal antibodies to fight COVID-19.

The speed was breathtaking. Using VelocImmune mice and antibodies from recovered patients, Regeneron's scientists identified two antibodies that could neutralize the virus. By combining them into a cocktail—REGN-COV2—they aimed to prevent viral escape mutations.

In July 2020, under Operation Warp Speed, Regeneron was awarded a $450 million government contract to manufacture and supply its experimental treatment REGN-COV2, an artificial "antibody cocktail" which was then undergoing clinical trials for its potential both to treat people with COVID-19 and to prevent SARS-CoV-2 coronavirus infection. The $450 million came from the Biomedical Advanced Research and Development Authority (BARDA), the DoD Joint Program Executive Office for Chemical, Biological, Radiological and Nuclear Defense, and Army Contracting Command.

Then came the moment that thrust Regeneron into the global spotlight. In October 2020, President Donald Trump contracted COVID-19. He received an 8-gram dose of Regeneron's investigational antibody cocktail, dubbed REGN-COV2, administered after the president's Thursday diagnosis.

Trump's rapid recovery and effusive praise—calling it a "cure"—created a publicity windfall. But it also raised ethical questions. REGN-COV2 has no emergency use approvals anywhere in the world—a fact that could underscore Trump's relationship with New York-based Regeneron and CEO Len Schleifer, who has been a guest at the White House during the pandemic. The company said late Friday that Trump's doctors had requested the therapy under its compassionate use program.

The FDA granted emergency use authorization in November 2020. The Food and Drug Administration on Saturday granted an emergency use authorization for Regeneron's Covid-19 antibody treatment, the experimental therapy given to President Donald Trump when he contracted the coronavirus in October. Regeneron submitted an emergency use application that month after preclinical studies showed that the therapy, called REGN-COV2, reduced the amount of virus and associated damage in the lungs.

But the commercial story was complicated. Unlike vaccines, antibody treatments were expensive to manufacture and required infusion centers for administration. Regeneron expects to have enough doses of REGEN-COV2 treat just 80,000 patients by the end of November, 200,000 by the first week of January and 300,000 by the end of that month.

More problematically, viral mutations eventually rendered REGEN-COV ineffective against dominant variants. By early 2022, the FDA pulled the authorization as Omicron swept the globe. The government had spent billions, but the antibodies sat unused.

In October 2017, Regeneron made a deal with the Biomedical Advanced Research and Development Authority (BARDA) that the U.S. government would fund 80% of the costs for Regeneron to develop and manufacture antibody-based medications, which subsequently, in 2020, included their COVID-19 treatments, and Regeneron would retain the right to set prices and control production.

The COVID experience taught valuable lessons: Regeneron's platform could respond with unprecedented speed to emerging threats, but commercial success in a pandemic required more than just good science.

VIII. Platform Technologies & The Science Engine

At the heart of Regeneron's success lies something that sounds deceptively simple: they build better mice. But VelocImmune represents one of the most ambitious genetic engineering projects ever undertaken in biotechnology.

Mice genetically engineered to be humanized for their Ig genes allow for human antibody responses within a mouse background (HumAb mice), providing a valuable platform for the generation of fully human therapeutic antibodies. Unfortunately, existing HumAb mice do not have fully functional immune systems, perhaps because of the manner in which their genetic humanization was carried out. Heretofore, HumAb mice have been generated by disrupting the endogenous mouse Ig genes and simultaneously introducing human Ig transgenes at a different and random location; KO-plus-transgenic humanization. We attempted to make mice that more efficiently use human variable region segments in their humoral responses by precisely replacing 6 Mb of mouse Ig heavy and kappa light variable region germ-line gene segments with their human counterparts while leaving the mouse constant regions intact, using a unique in situ humanization approach.

The results were extraordinary. These mice, termed VelocImmune mice because they were generated using VelociGene technology, efficiently produce human:mouse hybrid antibodies (that are rapidly convertible to fully human antibodies) and have fully functional humoral immune systems indistinguishable from those of WT mice.

The numbers speak for themselves. Dr. Yancopoulos and his team have used VelocImmune technology to create a substantial proportion of all original, FDA-approved fully human monoclonal antibodies. This includes Dupixent® (dupilumab), Libtayo® (cemiplimab-rwlc), Praluent® (alirocumab), Kevzara® (sarilumab), Evkeeza® (evinacumab-dgnb), Inmazeb® (atoltivimab, maftivimab and odesivimab-ebgn) and Veopoz® (pozelimab-bbfg).

But VelocImmune is just one piece of a larger technology suite. The Regeneron Genetics Center, launched in 2014, represents another massive bet on platform technology. By sequencing hundreds of thousands of patient samples and correlating genetic variants with health outcomes, Regeneron can identify and validate drug targets with unprecedented precision.

The philosophy is consistent: invest massively in platform technologies that can produce multiple drugs rather than betting everything on individual programs. It's capital-intensive and requires patience, but the payoff has been enormous.

VelociSuite includes some of the most valuable biotechnologies ever created and has enabled the development of a substantial proportion of all original, FDA-approved or authorized fully human monoclonal antibodies currently on the market. These tools ultimately allow us to help more patients around the world, faster.

IX. The Oncology Push and Pipeline Evolution

Regeneron's entry into oncology came late but with characteristic ambition. Rather than pursuing traditional chemotherapy or even conventional targeted therapy, they bet on immuno-oncology—harnessing the immune system to fight cancer.

The partnership with Sanofi evolved to encompass this new frontier. In 2015, Sanofi and Regeneron entered into a new global collaboration to discover, develop and commercialize new antibody cancer treatments in the emerging field of immuno-oncology. Sanofi committed to an initial investment of up to $2.17 billion in the exclusive collaboration, including $640 million in upfront payments to Regeneron and a potential sales milestone of $375 million.

Libtayo (cemiplimab), their PD-1 inhibitor, became the spearhead. Approved first for advanced cutaneous squamous cell carcinoma—a niche indication—it demonstrated Regeneron's strategy: start small, prove the science, then expand. Global net sales of Libtayo increased by 50% to $869 million for the full year through various reporting periods.

But the real innovation came with bispecific antibodies—engineered proteins that can bind two different targets simultaneously. The new agreement covers both monoclonal antibodies and new bi-specific antibodies, a variation of standard antibody therapeutics in which two distinct targets within the body can be bound by the same molecule, usually the cancer cell and an immune cell. Regeneron has developed a novel and flexible manufacturing platform that enables efficient production of bi-specific antibodies that are otherwise similar to natural antibodies.

The immuno-oncology collaboration with Sanofi eventually fractured, leading to a 2019 restructuring. The 2015 Agreement was scheduled to end in approximately mid-2020, and this revision provides for ongoing collaborative development of two clinical-stage bispecific antibody programs. Regeneron received $120 million in development costs for the two selected clinical-stage bispecific antibodies, plus the termination fee for the other programs under the original immuno-oncology agreement.

In 2023, Regeneron made a decisive move. The Sanofi and Regeneron global immuno-oncology license and collaboration agreement was originally executed in 2015. Under the terms of the amended and restated immuno-oncology license and collaboration agreement, Sanofi will transfer the rights to develop, commercialize, and manufacture Libtayo entirely to Regeneron, on a worldwide basis. They bought out Sanofi's rights to Libtayo for $900 million plus royalties, taking full control of their oncology future.

X. Partnership Dynamics & Strategic Evolution

The Regeneron-Sanofi relationship stands as one of the most productive—and complex—partnerships in pharmaceutical history. It began with promise, delivered extraordinary results, and ultimately ended in lawsuits and recriminations.

The initial structure was brilliant in its simplicity. Sanofi and Regeneron first joined forces way back in 2007, agreeing to split U.S. profits and losses 50-50 and ex-U.S. proceeds on a sliding scale. Regeneron got funding and global reach; Sanofi got access to VelocImmune and Regeneron's pipeline.

But success bred tension. As Regeneron grew more powerful and Dupixent became a mega-blockbuster, the relationship dynamics shifted. By 2020, Sanofi held a 20.6% stake in Regeneron—enough to be influential but not controlling.

The lawsuit over Dupixent commercialization revealed the underlying friction. In turn, Regeneron says it has lost out on its rights—as defined in the collaboration pact—to weigh in on key Dupixent commercialization decisions, a situation Regeneron's legal team calls "commercially unreasonable" given the magnitude of Dupixent sales in the U.S. The lawsuit further contends that Sanofi is being cagey about its PBM deals because they contain agreements tied to other, non-partnered drugs beyond Dupixent. Regeneron argues that it can't be certain the deals don't unfairly advantage other Sanofi products at Dupixent's expense.

In 2020, Regeneron took a dramatic step: they bought back $5 billion worth of shares from Sanofi, reducing the French company's stake and increasing their independence. The message was clear: Regeneron no longer needed a big pharma partner to succeed.

Yet the partnership model remains central to Regeneron's strategy—just more selectively applied. With Bayer on Eylea internationally. With Roche on manufacturing. With Intellia on gene editing. Each partnership carefully structured to maintain Regeneron's autonomy while accessing complementary capabilities.

XI. Playbook: Business & Scientific Lessons

After three and a half decades, what can we learn from Regeneron's playbook?

First, the power of platform technologies. While competitors chase individual drugs, Regeneron builds systems that produce multiple drugs. VelocImmune alone has generated seven FDA-approved medicines and counting. The Regeneron Genetics Center is identifying the next generation of targets. This requires massive upfront investment and patience, but the returns compound over time.

Second, the physician-scientist leadership model. Founded and led by physician-scientists, our leadership team includes Nobel Laureates and eight members of the National Academy of Sciences who guide our science-first approach. Having leaders who deeply understand both science and medicine creates a different decision-making dynamic. They can evaluate programs on scientific merit, not just commercial potential.

Third, internal R&D versus M&A. While big pharma spends billions acquiring companies, Regeneron grows from within. Nearly every drug in their portfolio was discovered in their own labs. This isn't ideological—it's practical. Internal development maintains quality control and captures full value.

Fourth, partnership structuring. Regeneron's deals are masterclasses in maintaining leverage. They keep U.S. rights when possible, share profits rather than accepting royalties, and always retain control over the science. When partnerships no longer serve them, they're willing to walk away or buy out partners.

Fifth, managing multiple blockbusters. Running a portfolio of billion-dollar drugs requires different muscles than developing them. Regeneron has built commercial capabilities while maintaining their scientific culture—a difficult balance many biotechs fail to achieve.

Sixth, long-term thinking in a short-term world. Wall Street wanted them to cut R&D during the early years. Activists pushed for a sale to big pharma. Regeneron ignored them all, maintaining R&D spending above 25% of revenue even today.

XII. Analysis & Bear vs. Bull Case

The Bull Case:

Dupixent's growth story is far from over. With new indications in COPD and potential expansion into other type 2 inflammatory diseases, peak sales could exceed $20 billion annually. The drug's patent protection extends into the early 2030s, providing nearly a decade of cash generation.

Eylea HD is successfully defending against biosimilar competition. The convenience of less frequent dosing matters to patients and physicians, supporting premium pricing even as cheaper alternatives emerge.

The pipeline runs deep. Multiple oncology programs, gene therapy initiatives through the Decibel acquisition, and new platform technologies like siRNA through the Alnylam partnership provide numerous shots on goal.

The Regeneron Genetics Center has become a competitive moat. With genetic data from over a million individuals, they can identify and validate targets competitors can't access.

The balance sheet is fortress-like, with minimal debt and substantial cash generation supporting continued R&D investment without dilution.

The Bear Case:

Eylea faces an existential threat from biosimilars. Even with HD's advantages, price pressure will intensify as multiple biosimilars launch. The ophthalmology franchise could decline from $6 billion to $3 billion by 2027.

Dupixent's patent cliff looms in the early 2030s. While still years away, the market will begin discounting this well before expiration. Finding a replacement for $15+ billion in annual sales will be nearly impossible.

Oncology remains subscale despite heavy investment. Competing against Merck, Bristol-Myers, and Roche in immuno-oncology requires resources even Regeneron might struggle to match.

The Sanofi relationship, while productive, created dependencies. Disputes over commercialization and the complex profit-sharing arrangements could limit flexibility and returns.

Valuation multiples assume continued excellence. At 25-30x earnings, any stumble—a major trial failure, manufacturing issues, safety concerns—could trigger significant multiple compression.

Financial Metrics:

In 2019, Regeneron Pharmaceuticals was announced the 7th best publicly listed company of the 2010s, with a total return of 1,457%. This performance has created high expectations.

Today, Regeneron trades at premium multiples reflecting its quality: ~25x forward P/E versus 15-18x for large-cap pharma peers. The premium is justified by superior growth, but leaves little room for error.

R&D productivity remains exceptional, with R&D spending around 25-30% of revenues consistently yielding new drug approvals—a hit rate that far exceeds industry averages.

XIII. Epilogue & "If We Were CEOs"

Standing at the crossroads of biotechnology's future, Regeneron faces fundamental questions about its next chapter. The founders, now in their 70s, have built something remarkable. But what comes next?

If we were running Regeneron, the succession planning would be priority one. The company's culture is so intertwined with Schleifer and Yancopoulos that their eventual departure poses existential risk. The solution isn't finding replacements—it's institutionalizing their approach. Create structures that ensure science-first decision-making survives leadership transitions.

Gene editing and cell therapy represent the next platform opportunity. The Intellia partnership provides access to CRISPR, but Regeneron needs to own these capabilities internally. The Decibel acquisition for gene therapy was a start. A major cell therapy acquisition or partnership should follow.

Geographic expansion remains underpenetrated. While Sanofi handles international commercialization for Dupixent, Regeneron needs direct presence in China and other emerging markets. These regions will drive pharmaceutical growth over the next decade.

The partnership philosophy needs evolution. The Sanofi experience—productive but ultimately limiting—suggests future partnerships should be more modular. Collaborate on specific programs or technologies, not entire portfolios. Maintain maximum flexibility.

On capital allocation, the temptation will be to return cash to shareholders as drugs go off patent. Resist this. The next VelocImmune—whatever form it takes—will require massive investment. Regeneron succeeded by thinking in decades, not quarters.

The biggest risk isn't biosimilars or patent cliffs—it's losing the cultural edge. As the company grows beyond 10,000 employees, maintaining the scientific hunger of a startup becomes increasingly difficult. The solution is radical: spin out new platform technologies as semi-autonomous units, recreating the entrepreneurial energy that built Regeneron.

Looking ahead, Regeneron stands as proof that in biotechnology, science-first isn't just an acceptable strategy—it might be the only sustainable one. In an industry increasingly dominated by financial engineering and M&A gymnastics, Regeneron's success building from within offers a different path.

The question isn't whether Regeneron's model can survive, but whether anyone else can replicate it. The combination of patient capital, scientific leadership, and relentless focus on platform technologies created something unique. In a world of copycats and fast followers, Regeneron remains an original.

XIV. Recent News

The latest developments continue to validate Regeneron's approach while highlighting ongoing challenges. The COPD approval for Dupixent opens a massive new market, while continued geographic expansion drives growth in existing indications. Eylea HD's launch trajectory suggests the franchise can be defended despite biosimilar entry.

Yet tensions with Sanofi over Dupixent commercialization remain unresolved, and the company faces increasing scrutiny over drug pricing as Dupixent's sales approach $15 billion annually. The pipeline advances with multiple Phase 3 programs, but none appear capable of replacing Dupixent's eventual loss of exclusivity.

XV. Links & References

The story of Regeneron draws from decades of scientific publications, SEC filings, analyst reports, and industry analyses. From the original VelocImmune papers in Science and PNAS to recent clinical trial results in The Lancet and New England Journal of Medicine, the scientific record documents an extraordinary journey from Queens startup to pharmaceutical giant. The company's own investor relations materials, particularly annual reports from 1991 onward, provide crucial financial and strategic context, while industry publications like FiercePharma, BioPharma Dive, and Endpoints News capture the real-time evolution of partnerships, competition, and market dynamics.

The journey from two scientists in a tiny lab to a $60 billion company creating medicines for millions isn't just a business success story—it's a testament to the power of patient capital, scientific excellence, and the radical idea that in biotechnology, the best business strategy might simply be to do the best science.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube