The Daily Needs Monopoly: How Regency Centers Cornered the Suburban American Grocer

I. Introduction & Episode Roadmap

Drive through almost any prosperous American suburb on a Saturday morning and you will pass one without noticing it. A low-slung row of storefronts wrapped around a parking lot, anchored by a grocery store with a familiar logo — a Publix in Florida, a Whole Foods in the Northeast, a Safeway in California. There is a dry cleaner, a nail salon, a coffee shop with a line out the door, a dentist, a taqueria, a boutique gym. You have been there a thousand times. You have almost certainly never once thought about who owns the dirt underneath it.

The answer, in a surprising number of these cases, is a Jacksonville-based real estate investment trust that most Americans could not name if their lives depended on it. As of the end of 2025, Regency Centers Corporation held interests in roughly 480 shopping centers spanning about 58 million square feet of leasable space, a portfolio touching some of the wealthiest zip codes in the country.7 It trades on the Nasdaq under the ticker REG, sits in the S&P 500, and carries an enterprise value north of $16 billion.[^4] And it does something deceptively simple for a living: it owns the corner where you buy your groceries.

For readers who do not live in the world of commercial real estate, it helps to know what kind of animal this is. Regency is a real estate investment trust — a REIT — a corporate structure Congress created in 1960 to let ordinary investors own income-producing real estate the way they own shares of a company. The bargain is simple: a REIT pays little or no corporate income tax, but in exchange it must return the vast majority of its taxable earnings to shareholders as dividends. That single rule shapes everything about how a company like Regency behaves. It cannot hoard cash and empire-build the way a tech company can; it must distribute its profits and then persuade the capital markets to fund its growth. It lives and dies on the quality of its assets, the discipline of its balance sheet, and the steady, unglamorous business of collecting rent and raising it. There are no moonshots in a REIT. There is only the compounding — or the erosion — of cash flow per share.

Here is the premise worth sitting with. For roughly a decade, the business press wrote obituary after obituary for physical retail. The "Retail Apocalypse" was going to be total — Amazon would eat the mall, the store would die, and the commercial real estate that housed it would follow. That prophecy came true for one specific kind of property: the enclosed regional mall, anchored by department stores selling discretionary fashion. Hundreds of them went dark. But a different, humbler class of retail real estate did something the headlines missed entirely. It compounded. Quietly, unglamorously, the open-air, grocery-anchored suburban shopping center turned out to be one of the most durable cash-generative business models in modern commerce.

The thesis this story will test — not assert, but test — is why. Why should owning the physical intersection where an affluent family buys organic kale, drops off dry cleaning, and takes a kid to urgent care be a high-moat business rather than a commodity? What is the actual mechanism? And, just as important, where does that mechanism run out of road? Because a business this well-run, this widely admired, and this fully priced by the market invites a harder question: if everything is already going right, what is left to go right, and what could go wrong?

The roadmap. First, the origin story — how a Jacksonville family that built a shopping mall learned to hate shopping malls, and pivoted to something more boring and more durable. Then the physics of the grocery-anchored center itself: the strange two-sided economics of the anchor tenant who pays almost nothing and the small-shop tenant who pays a fortune. Then the great consolidation wave — the $4.6 billion Equity One merger and the $1.4 billion Urstadt Biddle acquisition that reshaped the company. Then the modern era under Lisa Palmer, tested almost immediately by a pandemic. Then a deep dive into the financial machinery — the metrics that actually reveal whether the moat is real. The balance sheet and its rare A-minus credit rating. And finally the analytical spine: Helmer's 7 Powers, Porter's Five Forces, and an honest bull-versus-bear stress test. Let's begin where the company began — with a family that got rich building exactly the kind of real estate it would later spend decades avoiding.

II. The Stein Family Legacy & The Defensive Pivot (1963–1993)

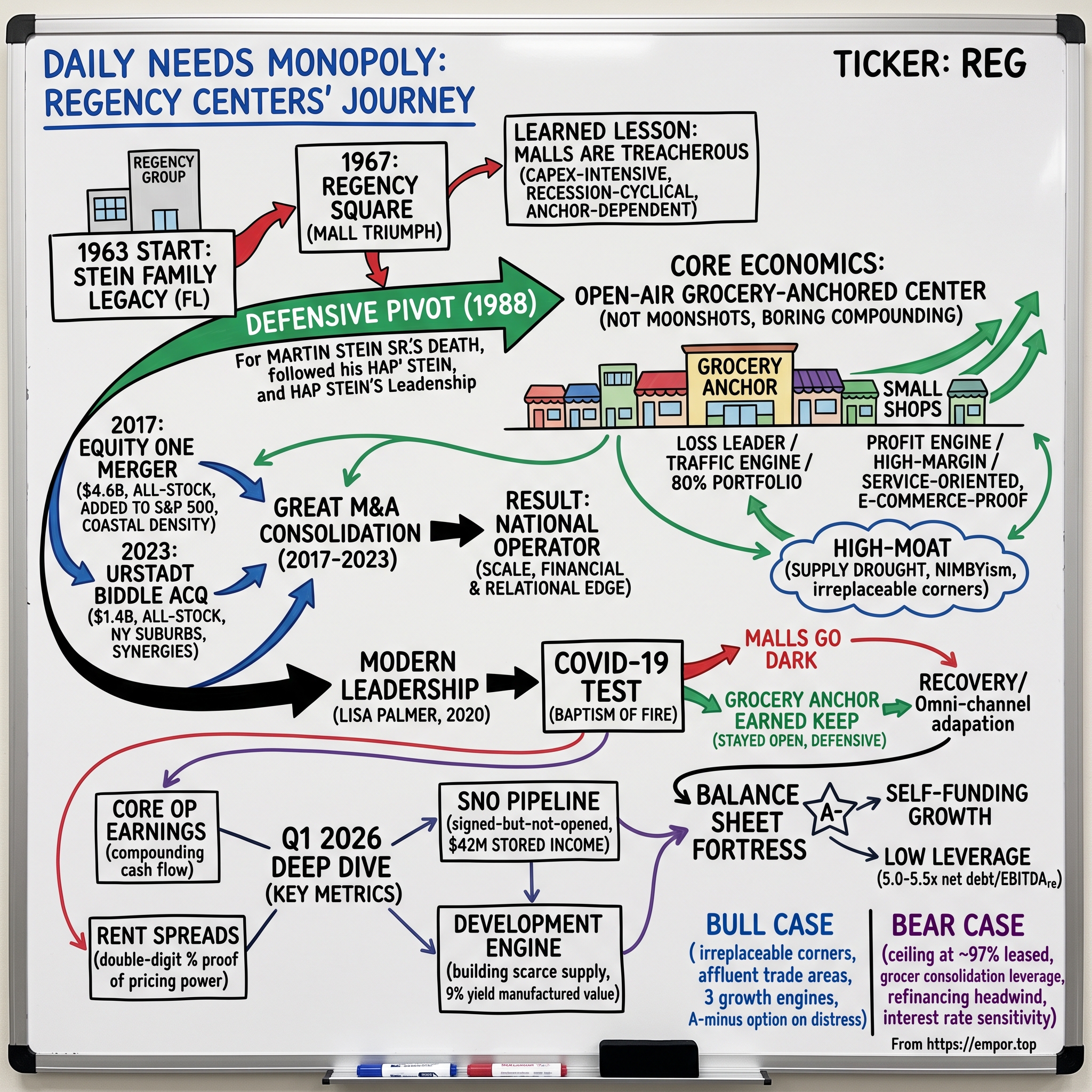

In 1963, a young Jacksonville developer named Martin E. Stein Sr. and his wife Joan Wellhouse Stein founded a modest operation called the Regency Group.3 It was, at the outset, an unremarkable Florida real estate business of its era — land plays, apartment complexes, the kind of opportunistic development that built the postwar Sun Belt. The Steins were not, in 1963, in the shopping center business. They were in the business of building whatever the growing city of Jacksonville needed next.

What it needed, they decided, was a mall. In 1967 the Regency Group opened Regency Square, billed as the first major regional shopping mall in Florida, anchored by May Department Stores and J.C. Penney.3 It was a genuine triumph — a gleaming monument to the American consumer economy, so successful that the surrounding neighborhood took its name. By 1981 the company had doubled the mall's size and was expanding across the state.3 For a regional developer, this was the top of the mountain. You built the biggest, most glamorous retail palace in the market, filled it with department stores, and collected the rent.

But the Regency Square experience taught the family a lesson that would eventually define the company — though it took years to fully absorb. Enclosed regional malls are magnificent and treacherous businesses. They are enormously capital-intensive: acres of climate-controlled common area, escalators, fountains, and parking structures that generate no rent but devour maintenance dollars. They live and die on discretionary spending, which evaporates in every recession. And they are hostage to their anchors — the fashion department stores whose fortunes rise and fall with the fickle winds of apparel retailing. When the anchor sneezes, the whole mall catches pneumonia. The mall business, in other words, was a leveraged bet on the American consumer's most volatile, least essential spending. It just didn't look that way in 1967, when the champagne was flowing.

The turning point came in tragedy. In 1988 Martin Stein Sr. died. His widow Joan stepped in as chairman, and their son, Martin E. "Hap" Stein Jr. — a graduate of Washington and Lee and Dartmouth who had run the real estate division since 1981 — took over as chief executive.3 Hap Stein inherited the company at a moment of genuine strategic reflection, and he arrived at a conviction that would sound almost heretical to the men who had built Regency Square: the future was not in the glamorous mall. It was in the grocery store.

The logic was a study in inverting everything the family had learned. If the problem with malls was that they depended on discretionary spending, then the solution was to own retail that people used whether the economy was booming or crashing. Nobody stops buying milk in a recession. Nobody defers a trip to the pharmacy because the stock market fell. Under Hap Stein's direction, Regency began concentrating on grocery-anchored neighborhood shopping centers — typically a 30,000-square-foot supermarket co-anchored by a drugstore, planted in an established residential neighborhood.3 The bet was that a grocer, precisely because it sold necessities, was recession-resistant in a way a department store could never be. The company was trading glamour for durability, and cyclicality for the boring beauty of the weekly grocery run.

To scale that vision, Regency needed permanent capital, and in 1993 it went public. Incorporated as a real estate investment trust, the company sold 5.41 million shares at $20 apiece, raising $108 million and retiring more than $80 million of debt in the process.3 The REIT structure mattered enormously: it required the company to pay out the vast majority of its taxable income as dividends, which disciplined management against empire-building and gave it a currency — publicly traded stock — with which to roll up shopping centers across the country. Through the late 1990s that is exactly what it did, absorbing Branch Properties, the Midland Group, and Pacific Retail Trust in a string of deals that by 1999 had built a portfolio of nearly 200 centers across more than 20 states.3 In 2001, the company shed its old name, Regency Realty, and rebranded as Regency Centers Corporation — a signal that it was no longer a Florida developer but a national operator of one specific, deliberately unexciting kind of real estate.3

The pivot from mall to grocery corner is the founding decision that everything else rests on. It was a bet that in retail real estate, the durable money is in necessity, not desire. Whether that bet still holds — whether necessity retail is truly as defensible as three decades of Regency marketing claims — depends entirely on the economics of the asset itself. So let's take one apart.

III. The Anatomy of Grocery-Anchored Real Estate Economics

Picture the physical structure of the thing. A regional mall is a fortress: two or three stories, fully enclosed, hundreds of thousands of square feet of interior corridor that must be heated, cooled, cleaned, and lit around the clock, all of it generating precisely zero rent. A grocery-anchored strip center is almost the opposite. It is a single-story row of storefronts, each opening directly onto the parking lot. There are no interior common areas to speak of. There is no roof over the walkways in many cases. The tenant, not the landlord, fits out and maintains most of the interior of each box. The whole thing can be built for a fraction of a mall's cost per square foot, and — crucially — it costs far less to keep running once it exists.

This is the first, most underappreciated advantage: the open-air center is a low-capital-expenditure machine. Real estate investors obsess over a metric called capital expenditure, or CapEx — the money a landlord must continually pump back into a property just to keep it competitive and occupied. Malls are CapEx sinkholes. Strip centers are CapEx-light. And because a larger share of the rent survives the trip to the bottom line, the same dollar of rent is simply worth more when it comes from an open-air center than from an enclosed mall. That structural cost advantage is baked into the concrete.

Now the traffic. Roughly 80% of Regency's centers are anchored by a grocer, and that is not an aesthetic preference — it is the entire engine.7 Consider your own behavior. You visit a shopping mall maybe a handful of times a year. You visit your grocery store two or three times a week. The grocer is a foot-traffic generator of a completely different order, dragging the same affluent households past the same storefronts fifty-two weeks a year, on a schedule dictated by the perishability of milk and produce. Anchor a center with a dominant local grocer — a Publix in the Southeast, a Kroger in the Midwest, an Albertsons or Safeway out West, a Whole Foods bankrolled by Amazon in the dense coastal markets — and you have built a reliable, recurring river of consumers.7

Here is where the economics get genuinely strange, and genuinely clever. The grocer, the very tenant generating all that traffic, pays almost nothing in rent. Because the anchor's traffic-generating power is so valuable, grocers negotiate from a position of enormous leverage. They occupy large boxes — often in the range of 30,000 to 60,000 square feet — on very long leases stretching twenty or thirty years, at strikingly low rents per square foot. In effect, the grocer is paid in cheap rent for the service of showing up and pulling the crowd. On paper, the anchor looks like a mediocre tenant: it eats up most of the square footage and contributes a modest slice of the rent.

The money is made on the edges. Wrapped around that anchor are the inline shops — the small spaces, often 1,200 to 5,000 square feet, occupied by the dry cleaner, the nail salon, the local restaurant, the urgent-care clinic, the boutique fitness studio. These tenants pay dramatically higher rents per square foot than the grocer does, on shorter leases with built-in annual rent increases. And they pay it precisely because they are desperate to sit next to that river of grocery traffic. The nail salon does not need to generate its own customers; it fishes in the stream the grocer creates. This is the core mechanism of the entire business model, and it is worth stating plainly: the anchor grocer effectively subsidizes the operating baseline of the center and generates the traffic, while the high-margin small shops surrounding it drive the growth in cash flow and the ultimate value of the asset. The grocer is the loss leader; the shops are the profit.

On Regency's own first-quarter 2026 call, the leasing math surfaced in a revealing detail: management said 90% of its new small-shop leases carried three or more embedded annual rent increases, and roughly a quarter of them carried step-ups of 4% or greater.2 That is the small-shop margin engine in action — contractual, compounding rent growth wired into the leases before a single new tenant is signed. It is a very different, and more durable, kind of pricing than a landlord hoping the market moves in its favor.

There is a second-order benefit to this structure that rarely gets its due: tenant retention. Because inline tenants are fishing in a stream they cannot recreate elsewhere, they renew. A successful nail salon or sandwich shop that has spent five years building a local clientele beside a busy Publix does not casually relocate two miles away to save a few dollars on rent — the whole value of its lease is the location. High retention means low turnover, and low turnover means the landlord avoids the single most expensive event in the business: a vacant box that must be re-marketed, re-fitted, and re-leased, often with months of lost rent and a fat tenant-improvement check to lure the next occupant. The open-air center's economics are quietly protected by the fact that its most profitable tenants have nowhere better to go.

The obvious objection — the one that haunted every retail landlord through the 2010s — is e-commerce. If Amazon can deliver anything to your door, why does the physical store survive at all? The grocery-anchored center's answer is unusually strong, and it comes in two parts. First, groceries have proved stubbornly resistant to pure e-commerce: fresh food is perishable, delivery economics are brutal, and most American households still do the bulk of their food shopping in person, often multiple times a week. Even Amazon, having spent years trying to crack the problem digitally, ultimately concluded it needed physical stores and bought Whole Foods to get them. Second, the small-shop mix has drifted decisively toward things a website cannot do to you: you cannot email someone a haircut, a restaurant meal, a workout class, a dental cleaning, or a urgent-care visit. Regency's centers have gradually re-weighted toward these service, food, and medical uses — precisely the categories that are e-commerce-proof by nature. Rather than being disrupted by the internet, the well-positioned grocery center absorbed it, becoming the pickup point, the returns depot, and the last-mile node for the very digital economy that was supposed to kill it.

Layered on top of this is a macro condition that has quietly become the sector's best friend: nobody is building new supply. Since the 2008 financial crisis, ground-up development of new shopping centers in the United States has all but stopped. Financing dried up, then construction costs soared, then land in desirable suburbs became prohibitively expensive and politically difficult to entitle. The result is a supply-demand mismatch that works entirely in the incumbent landlord's favor: tenant demand for good space is intense, while the supply of new competing space barely grows. On the Q1 2026 call, Regency's East Region chief operating officer, Alan Roth, put it bluntly — the availability of high-quality space is increasingly scarce, and "that dynamic is working in our favor."2 When you own the good corners and no one can build new ones, you set the price.

Run this through Porter's Five Forces and the picture sharpens. The threat of new entrants at any specific intersection is very low: a competitor cannot simply build a rival grocery-anchored center across the street when the land is gone, the zoning is hostile, and the neighbors — the eternal force of suburban NIMBYism — will fight it at every hearing. The bargaining power of tenants is fascinatingly asymmetric: it is high for a national grocer that any landlord would kill to have, but low for the small-shop operator who has no viable alternative to co-locating beside high grocery traffic. That asymmetry is the source of the pricing power. It also contains the seed of the bear case, which we will return to: the landlord's leverage over its most important tenants, the grocers, is not actually that strong. First, though, the strategic move that turned a good regional operator into a national one — buying up the competition.

IV. The Great M&A Consolidation Wave (2017–2023)

By the mid-2010s, Regency faced a strategic question that confronts every successful mid-cap company: how do you keep growing when you have already assembled a very good portfolio? Ground-up development is slow and lumpy. Buying centers one at a time in the open market is expensive and incremental. The answer, twice in six years, was to swallow an entire public competitor whole — and to do it without spending a dollar of cash.

The first and larger of the two deals closed on March 1, 2017, when Regency completed an all-stock merger with Equity One, a transaction that valued Equity One at roughly $4.6 billion and created a combined company with a market capitalization near $16 billion.[^4] Equity One shareholders received 0.45 of a Regency share for each of their own, and the very next day Regency was added to the S&P 500 — an inclusion that matters because it forces every index fund on earth to become a permanent, price-insensitive buyer of the stock, lowering the company's cost of capital in perpetuity.[^4]

The strategic logic ran deeper than scale for its own sake. Equity One brought Regency into exactly the markets it most wanted and could least easily build in: dense, supply-constrained, high-income coastal metros in the Northeast, South Florida, and California. These are the places where land is scarcest, entitlements are hardest, and — not coincidentally — the moat around an existing center is deepest. The merger also connected Regency to a certain institutional pedigree; Equity One had been controlled by the Israeli-listed real estate group Gazit-Globe under its chairman Chaim Katzman, and the combination knitted together two of the more sophisticated ownership cultures in the shopping-center world.

It helps to understand why scale is such a weapon in this particular industry, because the advantages are not the obvious ones. A bigger REIT does not get to charge higher rents simply for being bigger; a nail salon in Westport pays the market rent whether its landlord owns fifty centers or five hundred. The scale advantages are financial and relational. On the financial side, a larger, more diversified, more highly rated balance sheet borrows more cheaply — and in a business where growth is funded by continually issuing debt and equity, a persistent edge in the cost of capital compounds into a widening lead over smaller rivals that cannot match it. This is the flywheel: cheaper capital lets you buy and build at higher net yields, which strengthens the balance sheet, which lowers the cost of capital further. On the relational side, a national platform becomes the preferred landlord for national retailers. When a chain like TJX or Ulta or a fast-growing grocer wants to open dozens of locations, it would rather negotiate one master relationship with a landlord that owns good corners in twenty states than stitch together fifty separate deals with fifty local owners. Scale, in other words, buys you cheaper money and a fuller Rolodex — and those, not size for its own sake, are the real prizes of consolidation.

Why do all-stock deals matter so much in REIT-land? Because a REIT is a machine for converting rent into dividends, and it distributes almost all of its earnings to shareholders by law. That leaves little retained cash to fund acquisitions, so growth is financed externally — by issuing debt or equity. An all-stock merger lets a REIT expand its asset base without draining its balance sheet or piling on expensive debt, provided its own shares are richly enough valued to serve as strong currency. Regency's premium valuation — the very thing skeptics grumble about — is what makes these deals possible on favorable terms. The stock is the acquisition weapon.

The second deal, six years later, was smaller but in some ways more revealing about the philosophy. On August 18, 2023, Regency closed its acquisition of Urstadt Biddle Properties, an all-stock transaction valued at roughly $1.4 billion including assumed debt and preferred stock.4 Urstadt Biddle was a peculiar and precious target: a small, family-controlled REIT that owned a tightly concentrated collection of grocery-anchored centers in the wealthy suburban collar around New York City — Westchester County, Fairfield County in Connecticut, Bergen County in New Jersey. This is some of the most irreplaceable retail real estate in America, in trade areas where household incomes run among the highest in the country and where the odds of a competitor ever building a new center are essentially zero.

The structure of the deal exposed both the prize and its price. Urstadt Biddle carried a dual-class share structure, with the founding Urstadt family holding outsized voting control through a special class of stock — the kind of governance arrangement that lets a family run a public company as if it were still private. To get the deal done, Regency had to offer terms attractive enough to persuade the family to give up that control, and holders of roughly 68% of the voting power committed to support the merger.5 Each Urstadt Biddle share converted into 0.347 of a Regency share, worth about $20.40 based on Regency's price the day before the announcement.5

Was it worth paying up for a family-controlled collection of suburban strip malls? The case rests on two things. First, hard synergies: Regency expected to strip out roughly $9 million a year in duplicative corporate overhead — the general and administrative costs of running a separate public company, from the second stock listing to the second set of auditors and executives.5 For a business this simple, eliminating a redundant corporate layer is close to free money. Second, and less quantifiable, the assets themselves: buying an existing portfolio of trophy corners in the nation's richest suburbs, funded entirely with stock rather than high-cost debt, and folding it into an already-owned operating platform. The bet was that these were centers Regency could never assemble any other way, at any price, because they will never be built again.

This is the right place to run the honest "overpay" stress test, because acquirers routinely destroy value by paying control premiums for assets they could have assembled more cheaply. A skeptic looking at Urstadt Biddle would note that Regency did pay up — a family that controls a company through supervoting stock does not hand over the keys without a premium, and the whole point of a control premium is that the buyer pays for something (voting power) that generates no extra cash flow. The counter-argument rests on three legs, and each should be weighed rather than assumed. The overhead synergies were real and immediate, roughly $9 million a year of duplicative corporate cost that simply disappeared on close.5 The financing was non-dilutive to the balance sheet, funded in stock rather than by piling on debt at a moment of high interest rates.4 And the assets were, in the strict sense, irreplaceable — trophy corners in the wealthiest New York-collar suburbs that no amount of capital could recreate, because they will never be entitled and built again. Whether those three legs justified the specific premium paid is a judgment the numbers alone cannot settle, but the structure of the deal — synergy-rich, all-stock, aimed at scarcity assets — is textbook disciplined M&A rather than the empire-building that usually accompanies a control premium.

But an independent read has to flag what the deal also demonstrates: Regency's external growth increasingly depends on finding sellers willing to part with irreplaceable assets, and those are rare. Urstadt Biddle came available only because a founding family finally chose to cash out. There is no pipeline of such targets. That is precisely why, alongside the M&A, Regency leaned so heavily on a different growth engine — building the scarce new supply itself. To understand that engine, and how the whole machine performed under genuine stress, we need to meet the executive who inherited it at the worst possible moment.

V. Modern Leadership & The COVID-19 Baptism of Fire (2020–Today)

Lisa Palmer took over as chief executive of Regency Centers on January 1, 2020. She was not a parachuted-in outsider or a celebrity dealmaker. She had joined the company back in 1996 and spent a quarter-century climbing every rung — capital markets, then chief financial officer, then president — before finally taking the top job as Hap Stein moved up to executive chairman.2 By the time she became CEO she had lived through every cycle the modern company had weathered, a point she would later make almost offhandedly on an earnings call, noting that in her three decades at Regency she had seen same-property income decline only twice — during the 2008 financial crisis and during COVID.2

She would get to add the second of those to the list almost immediately. Palmer had been chief executive for roughly ten weeks when the pandemic arrived and governments began ordering non-essential retail to close. For a company whose entire thesis rested on the resilience of physical retail, it was the ultimate stress test, arriving before the new CEO had even settled into the chair. Regional malls went dark. Rent collection across commercial real estate collapsed. The stock market priced in something close to an existential crisis for anyone who owned stores.

And then the grocery-anchored thesis did exactly what it had been designed, over thirty years, to do. Because the overwhelming majority of Regency's centers were anchored by supermarkets and pharmacies — the definition of essential businesses — its properties largely stayed open. In the early weeks of the pandemic, the grocery store was not just open; it was one of the few places Americans were permitted and compelled to go, transformed overnight into a community lifeline and a logistics hub for a nation suddenly cooking every meal at home. The essential anchor, so grudgingly cheap on rent, earned its keep in the crisis by keeping the lights on for the entire center. This was the moment the durability argument stopped being a marketing slogan and became an observed fact.

The small shops were a different and harder story. The nail salon, the dine-in restaurant, the boutique gym — these discretionary, service-oriented tenants were exactly the ones ordered shut, and they were the high-margin tenants that drove the center's profitability. Here management's execution mattered. Rather than force struggling small operators into bankruptcy over missed rent, Palmer's team negotiated deferrals — pushing payments out rather than writing them off — preserving tenants it had spent years cultivating and betting they would survive to pay later. The team also accelerated a physical adaptation that turned out to be lasting: reconfiguring parking lots for curbside pickup, expanding outdoor dining, and leaning into the omni-channel role of the suburban center as a place you drive to, grab, and go. The recovery, when it came, was faster and more profitable than the panic had implied.

How should an independent observer weigh Palmer's record from there? The honest assessment is that the numbers have been strong and the narrative has been unusually consistent — which is itself a data point. Across earnings calls, filings, and investor presentations, the story management tells barely changes: high-quality suburban trade areas, necessity-based anchors, a differentiated development platform, and a conservative balance sheet. There have been no abrupt strategy pivots, no unexplained reversals, no history of activist investors forcing the board's hand. Guidance has generally been set conservatively and met or beaten. On the compensation side, the structure is heavily weighted toward equity and performance-based awards rather than cash salary, which aligns the executive team's outcomes with shareholders' — the arrangement one would want to see, though it is worth noting that in a sector-wide upcycle, generous equity comp rewards executives for a rising tide as much as for individual skill.

It is worth pausing on a piece of consensus mythology here, because the pandemic hardened a story that deserves a more careful telling. The myth is that grocery-anchored real estate is simply "recession-proof" — a magic asset class immune to the business cycle. The reality is more specific and more useful. Regency's income did fall during COVID, just as it fell during the 2008 crisis; Palmer said as much on the Q1 2026 call, counting exactly two declines in her three decades at the company.2 The asset is not immune to downturns. What it is, is defensive — its cash flows fall less, and recover faster, than almost any other kind of retail real estate, because the anchor keeps the lights on and the trade areas are wealthy enough to keep spending. That is a meaningfully different claim from invincibility, and the distinction matters for an investor, because a defensive asset priced as if it were invincible is a bad trade no matter how good the underlying real estate. The right lesson from COVID is not that Regency cannot be hurt; it is that when the whole world was terrified of physical retail, Regency's specific corner of it bent without breaking — and the market, having watched that happen in real time, has been willing to pay a premium for the demonstration ever since.

A second myth worth puncturing is that a company veteran promoted from the CFO's chair is, by definition, a caretaker rather than a strategist. Palmer's tenure argues the opposite. It was on her watch that the company executed the Urstadt Biddle acquisition, leaned hard into the development platform as the primary external growth engine, and won the S&P upgrade that reset its cost of capital — none of which is caretaking. Her background in capital markets shows up in how the company is run: the obsessive focus on the balance sheet, the reluctance to issue equity except at attractive prices, the framing of development in terms of yield-on-cost spreads to market cap rates. This is a CEO who thinks like a financier about a business that happens to be made of concrete. Whether that produces market-beating returns from an already-premium starting point is a separate question; that it reflects genuine strategic agency rather than passive stewardship is hard to dispute.

That is the sympathetic-but-skeptical read: a credible, aligned, disciplined management team operating in favorable conditions, whose consistency is genuine but whose tailwinds are partly not of its own making. The way to separate skill from luck is to look past the narrative and into the operating metrics — the numbers management cannot spin. That is where we go next.

VI. The Financial Machine: Demystifying the KPIs (Q1 2026 Deep Dive)

If you want to know whether a shopping-center REIT is actually good or merely riding a good market, you ignore the headline earnings and watch three numbers. Regency's first-quarter 2026 results, reported on April 29, 2026, offer a clean look at all three — and at where the skeptic should push back.

The first number is same-property net operating income growth, and it is the closest thing real estate has to an organic growth rate. It strips out the noise of acquisitions and dispositions and asks a pure question: are the centers the company already owned a year ago generating more profit today? In Q1 2026, Regency posted same-property NOI growth of 4.4% year over year, comfortably ahead of inflation, with the company guiding to full-year growth in the range of roughly 3.25% to 3.75%.1 For a portfolio of mature, already-high-occupancy shopping centers, growing property-level profit at better than 4% is a strong result — it means the assets are compounding without the company having to buy anything. On the earnings call, the CFO, Mike Mas, offered a useful caution against reading any single quarter too literally, noting that the first quarter ran hot on some lumpy "other income" and the second would run below the full-year pace on a tough expense comparison.2 That kind of pre-emptive candor about quarterly noise is, in itself, a small marker of guidance discipline.

The second number is the rent spread, and it is the single most direct measure of pricing power a landlord has. When a lease expires, what can the landlord charge the next tenant compared with the old rent? In Q1 2026, Regency generated blended cash rent spreads of 12.1% on 1.5 million square feet of comparable leasing — meaning it re-leased expiring space at rents 12% higher than before, in cash terms — with straight-line spreads, which smooth in future contractual increases, near a record at 24.3%.1 This is the hard, indisputable evidence that the underlying real estate is in genuine demand and short supply. You cannot fake a double-digit rent spread; either tenants pay up to be there or they don't. That they did, on a million and a half square feet, is the clearest proof point in the whole quarter that the moat is real and not merely asserted.

A brief detour on how to read a REIT's earnings at all, because the standard bottom line lies to you here. Under accounting rules, a company like Regency records enormous non-cash depreciation charges against its buildings every year, on the theory that the assets are wearing out — even though well-maintained commercial real estate in a good location generally appreciates over time. Those paper charges crush reported net income and make the company look far less profitable than it is in cash terms. That is why the industry reports Funds From Operations, or FFO — net income with real-estate depreciation added back — as its primary measure of earnings power. Regency reported Nareit FFO of $1.20 per share in Q1 2026, and guided to full-year FFO in the range of roughly $4.83 to $4.87 per share.1 The company also publishes a stricter figure it calls Core Operating Earnings, which additionally strips out lumpy, non-recurring items to show the clean, repeatable cash-earning power of the portfolio — the number management argues best captures how the business actually compounds. When Regency's CFO gently steered an analyst toward Core Operating Earnings over the noisier measures on the Q1 call, it was not spin so much as an argument about which yardstick tells the truth about a business whose reported net income is distorted by accounting depreciation.2 The investor's job is to know which number is which.

The third KPI is subtler and, for a forward-looking investor, arguably the most important: the gap between leased and commenced occupancy — the SNO pipeline, for "signed but not opened." In Q1 2026, Regency's same-property portfolio was 96.6% leased but only about 94.3% commenced, meaning rent-paying.1 That gap of roughly 230 basis points is not a problem; it is a stored asset. It represents tenants who have signed leases but have not yet opened their doors — a build-out contractor is still installing the kitchen, the permits are still pending — and who are therefore not yet paying rent. As they open over the following twelve to eighteen months, that pipeline converts automatically into new income with no additional leasing effort required. Management quantified it on the call as roughly $42 million of incremental base rent waiting in the wings.2 Think of it as deferred revenue that is already under contract: highly visible, low-risk future growth that is baked in but not yet showing up in the results.

There is a fourth engine worth understanding, because it is where Regency claims its most durable edge: development and redevelopment. Buying a finished, stabilized grocery center in the open market is expensive — such assets trade at capitalization rates, the ratio of income to price, of roughly 5.5% to 6.5%, meaning you pay $100 to buy about $6 of annual income. Regency's alternative is to build or substantially rebuild the center itself. At the end of Q1 2026 it carried an in-process development and redevelopment pipeline of about $635 million at a blended expected yield around 9%.1 The arithmetic of that spread is the whole point: if you can build income-producing real estate at a 9% yield in a market that values the same finished asset at a 6% cap rate, you have manufactured value out of thin air on every dollar you deploy — the classic developer's margin. On the call, management was careful to disaggregate the claim, noting that pure ground-up development yields sit "firmly in the 7% plus range," with redevelopment of existing centers pushing the blended figure toward 9%.2 That distinction matters, and it is to management's credit that it drew it rather than flashing only the headline number.

The development platform deserves a closer look, because management repeatedly frames it as Regency's single greatest differentiator, and the claim is worth examining rather than accepting. On the Q1 2026 call, the chief investment officer, Nick Wibbenmeyer, described the company as "the only national developer of high-quality grocery-anchored shopping centers at scale" in an environment of otherwise almost nonexistent new supply — and pointed to a potential of more than $1 billion of project starts over the following three years, on top of the roughly $800 million already started in the prior three.2 The proof points he offered were concrete rather than abstract: a Safeway-anchored center in the Bay Area delivered ground-up in under eighteen months, a Northern California project that was already fully leased before its anchor opened, Whole Foods openings in the Northeast, and a Long Island redevelopment being reshaped around a new Whole Foods.2 The reason this is hard to replicate is not capital — plenty of players have capital — but the combination of grocer relationships, entitlement expertise, and a track record that makes landowners and municipalities willing to deal. When a master-planned community developer wants a grocery center as an amenity for thousands of new homes, it calls the firm with the deepest grocer Rolodex and the cleanest delivery record.

There is discipline embedded in how these projects get built, and it is the part a skeptic should actually respect. Wibbenmeyer was explicit that Regency de-risks each project before breaking ground — securing entitlements, pre-leasing the anchor, and locking in construction bids before committing capital — which is why the projects tend to land on time and on budget rather than becoming the open-ended money pits that sink less careful developers.2 The company also runs the land side capital-efficiently, optioning parcels rather than hoarding a large speculative land bank that would tie up cash and expose it to falling land values.2 The honest caveat, which management itself volunteered, is that development is inherently lumpy: because Regency refuses to start a project until it is fully de-risked, start dates slip, and any given year's spend can swing on a single delayed permit.2 That lumpiness is the price of the discipline, and it means investors should judge the platform over years, not quarters.

One more metric belongs on the watch list because it is where trouble would show up first: bad debt, or in the industry's language, uncollectible lease income. It is the canary in the coal mine for tenant health. On the Q1 2026 call, management reported bad debt running near record lows, below historical averages, even as it flagged that it was still working through a handful of ongoing tenant bankruptcies.2 The company also disclosed, with unusual candor, that it had moved a single lease among more than nine thousand onto a cash-accounting basis — a conservative judgment that a particular tenant might struggle to meet its future obligations, booked as a non-cash reserve rather than hidden.2 That is exactly the kind of small, proactive disclosure that, over time, builds the case that management is not papering over deterioration. But it is also a reminder that even in a strong portfolio, individual tenants fail, and the SNO pipeline and rent spreads look their best precisely at the top of a cycle. The metrics are strong; the discipline is to keep watching whether they stay strong when the cycle turns.

What ties these metrics to the resilience story is the customer underneath them. Regency's centers sit in affluent suburban trade areas with household incomes well above the shopping-center sector average, and the Urstadt Biddle acquisition only enriched that mix by adding the wealthy New York collar counties. On the Q1 call, Roth reported that portfolio foot traffic was up 2.3% in the first quarter and, notably, up around 3% in April even as fuel prices climbed — with bad-debt levels near record lows.2 The analytical read: high-income shoppers are simply less sensitive to inflation and macro shocks, which insulates the small-shop tenants from the demand swings that would sink stores in a weaker trade area. That is the demographic moat translating into observed foot traffic, not just a line on a marketing slide.

But this section should end where a good skeptic ends it — on the ceiling. At 96.6% leased, Regency is running near a structural maximum. On the call, one analyst from Deutsche Bank pressed exactly this point: the whole industry has a good backdrop, Regency trades at a premium to peers, so what are investors underestimating?2 Palmer's answer leaned on the combination of portfolio quality, development platform, balance sheet, and team, and on a long-term record of top-of-sector NOI growth achieved with less capital than rivals.2 It was a confident, well-rehearsed answer. It was also, unavoidably, a promise about the future rather than a fact about the present — and the market's tepid reaction to a strong quarter suggested investors have already priced much of that promise in. The question of how much room is left is the crux of the bear case, and we will return to it. First, the foundation that makes the whole edifice safe: the balance sheet.

VII. Balance Sheet Fortress & The Cost of Capital Advantage

In a capital-intensive, cyclical industry like real estate, the balance sheet is not a back-office detail — it is a competitive weapon, and occasionally a survival tool. The clearest single expression of Regency's financial conservatism arrived on February 26, 2025, when S&P Global Ratings upgraded the company's credit rating to A-minus with a stable outlook, lifting it out of the BBB tier where the vast majority of REITs live.6 Moody's rates the company in the same neighborhood, in the A category.2 Only a tiny handful of American REITs carry an A-level rating; it is an elite and rarely granted status.

Why does a bond rating matter to an equity investor? Because it is a direct discount on the company's cost of borrowing, and for a business that grows by continually raising external capital, the cost of that capital is close to everything. A more highly rated borrower issues debt at lower interest rates than a weaker-rated peer for identical assets, and that spread compounds across every dollar borrowed for decades. The advantage showed up in real time in February 2026, when Regency issued $450 million of seven-year unsecured notes at a 4.5% coupon — which management described as the lowest credit spread in the company's history and among the most favorable costs of debt in the entire REIT sector.2 While more leveraged competitors were forced to borrow at expensive rates in a higher-interest-rate era, Regency could still tap the debt markets cheaply. In a downturn, that difference is the difference between playing offense and scrambling to survive.

The rating is earned by genuinely low leverage. Regency operates with net debt to a measure of cash earnings called EBITDAre in the range of roughly 5.0 to 5.5 times, finishing 2025 at about 5.1 times.7 In plain terms, its total debt is only around five years of pre-tax operating cash flow — modest for an asset class where lenders will happily finance far more. That conservatism is deliberate, and it is the mechanical reason S&P cited the company's "sustained low leverage" in the upgrade.6 The company pairs it with a well-laddered debt maturity schedule, spreading its borrowings out over many years so that no single year brings a large, dangerous wall of debt coming due at once — the kind of concentrated maturity that can force a company to refinance at the worst possible moment.

The strategic value of all this conservatism becomes clearest precisely when the industry is under stress. On the Q1 2026 call, Palmer described the balance sheet as the enabler of everything else — the capacity to fund the development pipeline out of free cash flow with, as Mas put it, no current need to issue equity or sell properties.2 Self-funding growth is a luxury most REITs do not have; it means Regency does not have to sell stock at a bad price or dump assets in a weak market to keep building. And it preserves optionality: if a broader refinancing crisis were to hit the sector — if over-levered competitors were forced to sell good centers cheaply to meet maturing debt — Regency would be one of the few players with the balance sheet to buy. The A-minus rating, in other words, is not just defense. It is a call option on other people's distress.

The self-funding point deserves emphasis because it is where the balance sheet and the growth engine meet. A REIT must distribute the great majority of its taxable income as dividends, which normally leaves it perpetually dependent on the capital markets to fund any growth — issuing stock and bonds to build and buy. That dependence is a vulnerability: when markets seize up or a company's own stock trades cheaply, the growth machine stalls precisely when opportunities are richest. Regency has engineered its way partly out of that trap. Its full-year 2025 Nareit FFO grew nearly 8% to about $4.64 per share, and its low payout relative to that cash generation, combined with modest leverage and a nearly untapped revolving credit facility, left it able to fund its entire in-process development pipeline out of retained free cash flow.7 On the Q1 2026 call, management said flatly that it had no current need to raise equity or sell properties to keep building.2 Being a forced seller of stock or assets at the wrong moment is how good real-estate companies destroy shareholder value in downturns; Regency has structured itself specifically to avoid ever having to be one.

The honest counterpoint is that this fortress carries a slow, structural cost. Much of Regency's outstanding debt was issued years ago at historically low interest rates. As those cheap bonds mature and get refinanced at today's higher market rates, the company's average interest expense will grind upward, a persistent if manageable headwind to earnings over the coming decade. It is not a crisis — the low leverage and A-minus rating ensure the transition is gradual rather than a shock — but it is a real drag that even a pristine balance sheet cannot fully escape. That tension between structural strength and structural headwind is the right frame for the final analytical question: from here, does Regency win, and what breaks the case?

VIII. Hamilton Helmer's 7 Powers & The Investment-Story Spine

Strip away the narrative and ask the cold strategic question: what, exactly, prevents someone from competing away Regency's returns? Hamilton Helmer's 7 Powers framework — a taxonomy of the durable advantages that let a business sustain profits — offers a rigorous way to test the moat rather than simply admire it. Three of the seven powers apply to Regency with real force; the honest exercise is to notice which ones do not.

The clearest is what Helmer calls a cornered resource. The primary retail intersection in a wealthy, built-out suburb is a finite, non-replicable asset. There is exactly one best corner in a given trade area, Regency often owns it, and — because the land is gone and the zoning is hostile — no one can manufacture a second one. This is the purest source of the moat, and it is why the supply drought discussed earlier is so powerful: the cornered resource is only valuable if new resources cannot be created, and in American suburbs, they largely cannot. The second power is scale economies. Regency's size lets it borrow more cheaply than smaller rivals, spread corporate overhead across a large asset base, and — importantly — serve as a one-stop national landlord for expanding retail chains like TJX or Ulta that want to open dozens of stores across many states through a single relationship. The third is switching costs, which operate most strongly on the anchor grocer. A supermarket sinks millions of its own dollars into custom refrigeration, buildout, and supply-chain fit-out for a specific store, and it spends years training the surrounding neighborhood to drive to that exact location out of pure habit. Moving across the street means abandoning all of it. That inertia is why anchor leases run for decades and why the anchor, once installed, tends to stay.

Notice what is absent. Regency has no meaningful network economies, no counter-positioning against an incumbent, no branded pricing power in the consumer's mind, and no process power of the kind that protects a manufacturer. Its moat is real but narrow: it is fundamentally a moat of location and scale, not of technology or brand. That narrowness is important, because it defines both why the company wins and where the winning stops.

Before weighing the bear case, it is only fair to state the bull case at its strongest, in the evidence it can actually point to rather than the story it tells. The proof is in the operating record: same-property income compounding above 4% off an already-full portfolio, double-digit cash rent spreads on every renewal cycle, a contracted pipeline of un-commenced rent, and a development platform manufacturing new assets at yields well above what the market charges to buy them.12 These are not projections; they are results already on the books, and they cohere into a single mechanism — a business that grows its cash flow per share several points faster than inflation, funded largely from within, behind an A-minus balance sheet. Over a full cycle, a defensively positioned asset that compounds cash flow at a mid-single-digit rate with very low risk of permanent impairment is a genuinely rare thing, and the market's willingness to pay up for Regency is, at bottom, a rational response to having watched it do exactly that for years.

The bull case, stated as its proponents would: Regency owns irreplaceable corners in the country's richest suburbs, insulated by high-income shoppers who keep spending through downturns. It has three visible, contracted growth engines — the roughly $42 million SNO pipeline converting to rent, the double-digit rent spreads on lease renewals, and the value-creating development platform earning a mid-to-high single-digit yield in a market that pays up for the finished product. And it sits behind an A-minus balance sheet that lets it self-fund that growth and pounce on distressed assets if the broader market cracks. Put together, the argument goes, this is a business engineered to compound its cash flow per share at a steady, defensible rate for a very long time, almost regardless of the macro weather.

There is also a risk that sits above the business entirely, in the valuation itself: interest rates. REITs are, in part, yield instruments, and their share prices move inversely to long-term interest rates. When the "risk-free" yield on government bonds rises, the dividend a REIT pays looks relatively less attractive, and its shares tend to de-rate; the property values underpinning the company also fall as the cap rates buyers demand drift upward. This is a market-structural risk rather than an operating one — Regency's centers can be performing beautifully while its stock falls simply because the ten-year Treasury yield rose — and it is precisely the kind of pressure the sector navigated through the higher-rate era of the mid-2020s. It cuts both ways: a sustained decline in rates would likely re-rate the whole group upward regardless of individual execution. For an investor, the uncomfortable implication is that a meaningful share of Regency's near-term return may be driven by the direction of interest rates, a variable neither management nor anyone else controls.

Now the bear case, taken seriously rather than dismissed. The first and most concrete problem is the growth ceiling. At 96.6% leased, Regency is essentially full.1 You cannot grow occupancy much past a level that is already near the physical maximum, which means future organic growth depends almost entirely on pushing rents higher and executing development flawlessly — a narrower, more demanding path than a company with vacancy to fill. Management itself effectively conceded the point on the call, noting that the remaining upside is concentrated in anchor leasing and in the slow conversion of the commenced-occupancy gap.2 The second risk is the mirror image of the switching-cost moat: tenant consolidation. The bargaining asymmetry that favors Regency over small shops runs the other way with the grocers, and the grocery industry is consolidating. When two national grocers merge, the combined entity gains leverage to rationalize overlapping stores and press for flatter rents at renewal. Regency's most important tenants are precisely the ones with the most power over it. The third risk is the refinancing headwind already discussed — the multi-year grind of rolling cheap legacy debt into pricier new debt. None of these is likely to be fatal. But together they describe a business whose easy growth is behind it and whose future returns depend on excellent execution against a rising cost of capital, all while the stock already trades at a premium that assumes exactly that excellence.

It is clarifying to place Regency against its peers, because the shopping-center REIT sector is a natural experiment in strategy. Kimco Realty is the largest of the group by property count and has pursued scale and a Sun Belt tilt, with a grocery-anchored focus of its own; Brixmor operates a value-add, higher-yielding, more middle-market portfolio; Kite Realty and others sit in adjacent niches. And then there is Federal Realty Investment Trust — the sector's aristocrat, famous for the longest streak of consecutive annual dividend increases of any REIT, built on a small collection of extraordinarily high-barrier, high-income coastal assets. Regency's identity emerges most clearly in this company. It is not the biggest, and it is not the highest-yielding. It has deliberately positioned itself at the premium, defensive, high-credit-quality end of the spectrum — closer to Federal Realty's trophy-asset philosophy than to a scale-and-yield roll-up — while running a development platform that few peers can match at national scale. The premium valuation the market assigns Regency is, in effect, the market agreeing that this positioning is real. The bear's rejoinder is that when an entire sector is enjoying the same supply drought and the same healthy fundamentals, the incremental advantage of being the best-run operator narrows, and paying a premium to own it becomes harder to justify. Both things can be true: Regency can be the highest-quality operator in the group and a fully priced one.

Run it through Porter one final time and the verdict is coherent: rivalry among landlords is muted by the supply drought, new entrants are blocked by land and zoning, and substitution — the e-commerce threat that gutted the mall — is weakest against the grocery run and the in-person services that fill the small shops. The one force that genuinely bites is supplier and tenant power, concentrated in the consolidating grocers. That is the honest shape of the moat: wide against most threats, thin against one. Whether that is enough to justify the premium is the judgment each investor has to make. What the evidence supports is narrower and more defensible than the marketing: this is a genuinely high-quality, low-risk collection of real estate run by a disciplined team, whose principal vulnerability is not collapse but the simple exhaustion of easy upside.

IX. Epilogue & Playbook Lessons

Step back from the metrics and the story resolves into a few durable lessons, each of which travels well beyond one Jacksonville REIT.

The first is the value of boring necessities. In an era defined by technological disruption, the humble grocery store — the least glamorous tenant in retail — proved to be the ultimate survivor, precisely because it sells things people cannot defer and increasingly cannot fully replace with a screen. The mall, built on desire, was disrupted. The grocery corner, built on need, became a logistics hub for the omni-channel age. The lesson for investors is that durability often hides in the unexciting places, and that the market's obsession with disruption can blind it to the assets quietly compounding because nothing about them ever changes.

The second is the discipline of merger math. Regency's two great acquisitions worked not because they were bold but because they were disciplined: geographically complementary, funded with stock rather than debt, and justified by hard, quantifiable overhead synergies rather than vague promises of strategic fit. The all-stock structure protected the balance sheet; the G&A savings were real and bankable; the acquired assets were things the company could not have built. That is a template for non-dilutive consolidation — and a reminder that the best deals are often the least dramatic ones.

The third is the moat of capital conservatism. Maintaining an A-level credit rating and low leverage in a cyclical, capital-hungry industry looks like timidity in a boom. It reveals itself as strategy in a bust, when the conservative operator is the only one still able to build, buy, and lend to itself while others are starved of capital. The balance sheet is not the boring part of the story; in real estate, it is frequently the whole game.

And the fourth, which the independent analyst should hold onto most tightly, is that a wonderful business and a wonderful investment are not the same thing. Regency has assembled genuinely irreplaceable real estate, run it with unusual discipline, and built a fortress balance sheet — all of that is real, and the evidence supports it. But it is also nearly full, facing a rising cost of capital and consolidating tenants, with much of its quality already reflected in a premium valuation. The interesting question is no longer whether Regency owns great corners. It plainly does. The question is what happens to the returns of a great business once the market has decided, in advance, that it is great — and that is a question no outline, and no management narrative, can answer for you.

References

-

Regency Centers Reports First Quarter 2026 Results — GlobeNewswire, 2026-04-29 ↩↩↩↩↩↩↩

-

Earnings call transcript: Regency Centers beats Q1 2026 expectations — Investing.com, 2026-04-30 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

History of Regency Centers Corporation — FundingUniverse ↩↩↩↩↩↩↩↩

-

Regency Centers Closes Acquisition of Urstadt Biddle Properties — Regency Centers, 2023-08-18 ↩↩

-

Regency Centers to Acquire Urstadt Biddle Properties in All-Stock Transaction — GlobeNewswire, 2023-05-18 ↩↩↩↩

-

Regency Centers Upgraded by S&P Global Ratings to an 'A-' Credit Rating — Regency Centers / GlobeNewswire, 2025-02-26 ↩↩

-

Regency Centers Reports Fourth Quarter and Full Year 2025 Results — Regency Centers, 2026-02-05 ↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube