Radian Group: From Near-Death to Bold Transformation

I. Introduction and Episode Roadmap

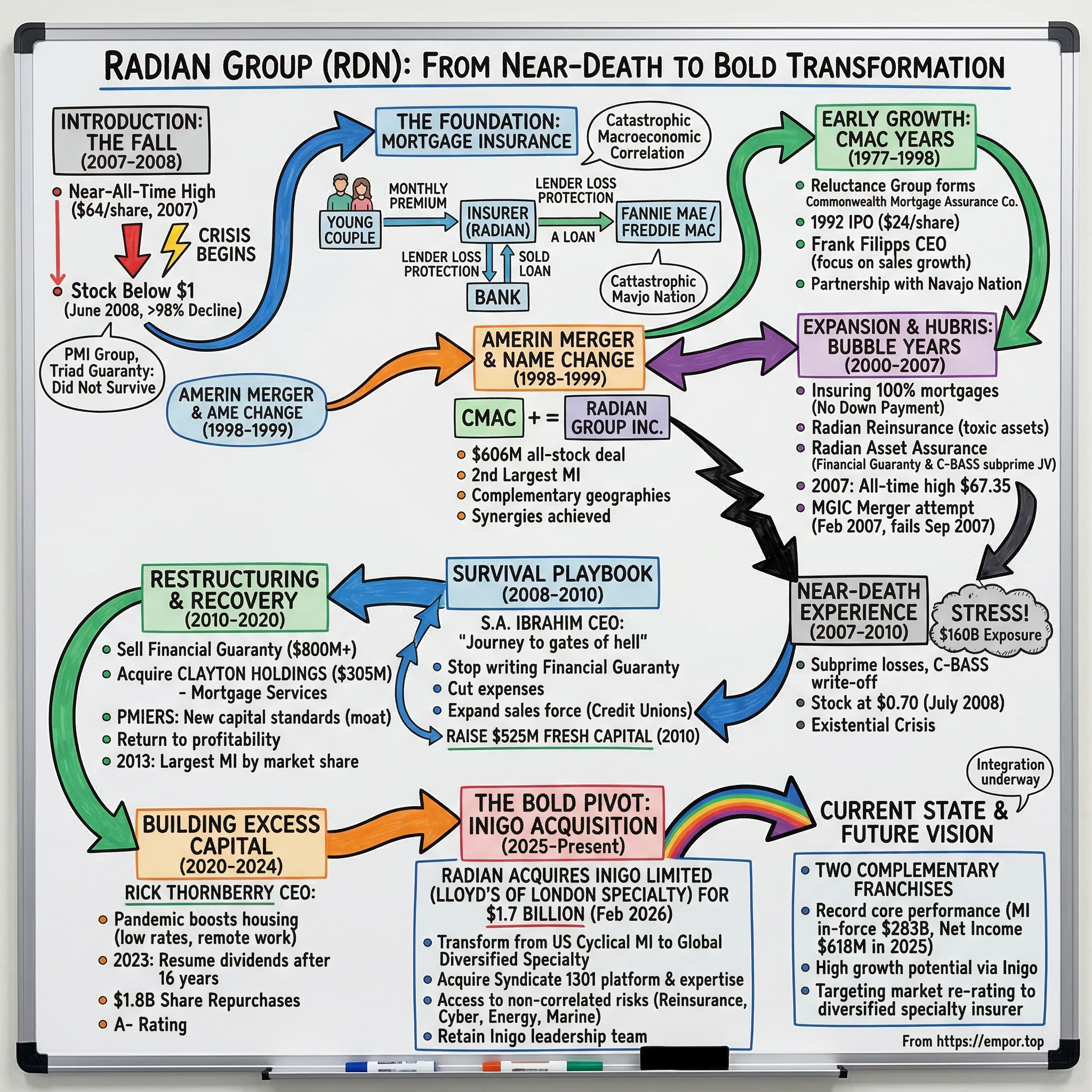

In the summer of 2007, if you had walked into the Philadelphia headquarters of Radian Group and told the employees that within twelve months their stock would lose roughly ninety-eight percent of its value, they would have thought you were insane. The company was riding high, close to its all-time high of sixty-four dollars a share, sitting at the center of the greatest housing boom in American history. Mortgage insurance was the golden goose. Homeownership rates had climbed to historic peaks. The money was flowing.

By late June 2008, Radian's stock had tumbled below one dollar.

That kind of fall does not just destroy shareholder value. It destroys organizational confidence, institutional memory, and the very idea that the people running the company know what they are doing.

Most companies that experience a ninety-eight percent stock price decline never recover. They get acquired at fire-sale prices, go through bankruptcy, or simply fade into irrelevance as a cautionary tale in business school case studies. Two of Radian's own competitors, PMI Group and Triad Guaranty, did not survive the same storm. Seven of nine financial guaranty monolines discontinued operations entirely during the crisis years.

Radian did none of those things. Instead, it survived, rebuilt, and then did something that almost nobody in the industry expected: it made a one-point-seven-billion-dollar bet to transform itself from a domestic mortgage insurer into a global, diversified specialty insurer by acquiring Inigo Limited, a Lloyd's of London specialty platform.

That transaction, which closed in February 2026, represents one of the most ambitious strategic pivots in the modern insurance industry. A company whose entire identity had been defined by a single product in a single geography for nearly five decades decided to reinvent itself entirely.

To understand why this matters, consider the numbers. As of the third quarter of 2025, Radian reported net income from continuing operations of one hundred fifty-three million dollars, its primary mortgage insurance in-force portfolio hit an all-time high of two hundred eighty-one billion dollars, and book value per share grew nine percent year-over-year to thirty-four dollars and thirty-four cents. For the full year 2025, net income reached six hundred eighteen million dollars and insurance in force climbed to two hundred eighty-three billion.

This is not a company running from weakness. This is a company pivoting from a position of extraordinary strength, which makes the strategic decision all the more fascinating.

The story of Radian Group is a story about what happens when a near-death experience fundamentally changes the DNA of an organization, and what management teams do when they accumulate more capital than their existing business can absorb. It is a story about the commodity trap in financial services, the discipline required to survive a crisis that kills your peers, and the audacity required to change the game entirely when incremental improvements are no longer enough.

This is the Radian story.

II. What Even Is Mortgage Insurance? The Foundation

Before diving into the history, it is worth spending time on a concept that most people encounter exactly once in their lives, during the most stressful financial transaction they will ever make, and then promptly forget about: private mortgage insurance.

Picture a young couple buying their first home. They have saved diligently but have only scraped together ten percent of the purchase price as a down payment. The bank wants to lend them the money, Fannie Mae or Freddie Mac will buy that loan on the secondary market, but everybody involved understands the math: with only ten percent equity, if home prices decline even modestly, the couple could owe more than the house is worth. If they stop paying, the lender takes a loss that the thin equity cushion cannot absorb.

Private mortgage insurance exists to solve this problem. The insurer, in this case Radian, promises to cover a portion of the lender's losses if the borrower defaults. In exchange, the borrower pays a monthly premium that gets added to their mortgage payment.

Think of it as a toll that the borrower pays to access homeownership without having saved up a full twenty percent down payment, which in many American housing markets today would require a decade or more of disciplined saving. Without private mortgage insurance, millions of Americans would simply be locked out of homeownership entirely.

The economics of the business are conceptually simple but deceptively complex in practice. The mortgage insurer collects premiums every month from millions of borrowers, invests that cash float, and hopes that the claims it eventually pays out on defaulting loans are significantly less than the premiums and investment income it earns.

In good times, this is one of the most profitable businesses in financial services. Premiums flow in like clockwork, claims are minimal, and the investment portfolio compounds quietly in the background. It looks like free money.

The danger is that mortgage insurance is catastrophically correlated. Unlike auto insurance, where one car accident in Ohio has nothing to do with another car accident in Texas, mortgage defaults are driven by macroeconomic factors that hit everywhere at once. When the economy tanks, unemployment rises, and housing prices fall simultaneously across the country, every single policy in the portfolio becomes riskier at exactly the same time. The diversification that makes property and casualty insurance manageable simply does not exist in the same way for mortgage insurance.

This is the fundamental structural risk that would nearly destroy Radian and every one of its competitors in 2008.

The key participants in this ecosystem form a tightly regulated chain. Lenders originate mortgages and want protection against default. Borrowers pay for the insurance but, critically, have no choice in which insurer is selected, the lender makes that decision. The government-sponsored enterprises, Fannie Mae and Freddie Mac, buy most conforming mortgages and require private mortgage insurance on loans with down payments below twenty percent.

And the insurers themselves, of which there are only six approved providers, compete for lender business within this framework.

Radian's primary competitors include Arch Capital's mortgage insurance subsidiary, Essent Guaranty, Genworth Financial's Enact Holdings, MGIC Investment Corporation, and NMI Holdings. The government also competes through the Federal Housing Administration and the Department of Veterans Affairs, which offer their own mortgage insurance programs with different cost structures and eligibility requirements.

This creates a market defined by an unusual paradox. The barriers to entry are enormous, because getting approved by Fannie and Freddie requires massive capital reserves and exhaustive regulatory compliance, but the product itself is essentially a commodity.

Lenders choose among the six providers based primarily on pricing, financial strength ratings, and service quality. No borrower has ever said, "I want my mortgage insured by Radian specifically." The brand is invisible to the end consumer.

Understanding this commodity dynamic is essential to grasping why Radian eventually felt compelled to pursue a transformational acquisition, even from a position of tremendous financial strength.

III. Origins and Early Growth: The CMAC Years (1977-1998)

The origin of Radian Group traces back to 1977, when Reliance Group established the Commonwealth Mortgage Assurance Company, known as CMAC, in Philadelphia. The late 1970s represented a period of dramatic expansion in the American housing market. Interest rates were volatile, inflation was rampant, and the traditional model of homeownership, where buyers saved diligently for years to accumulate a twenty percent down payment, was increasingly out of reach for middle-class families.

The private mortgage insurance industry existed precisely to bridge this gap, and CMAC entered the market with the backing of Reliance Group's financial resources and a simple thesis: there was an enormous, underserved population of creditworthy Americans who could afford monthly mortgage payments but could not afford the upfront capital required to avoid mortgage insurance.

For the first fifteen years of its existence, CMAC operated as a subsidiary, doing what good insurance companies do, which is to say, very little that generates headlines. It underwrote policies, collected premiums, managed reserves, and quietly built relationships with mortgage lenders across the country. The business was steady, predictable, and exactly the kind of operation that makes insurance executives sleep well at night.

The first major corporate milestone came in 1992, when CMAC Investment Corporation was spun off from Reliance Group Holdings through an initial public offering. The IPO offered nine-point-one million shares at twenty-four dollars apiece, though the stock opened trading at eighteen dollars, a discount that reflected the market's cautious assessment of a newly independent insurance company.

But the underlying business was stronger than the opening price suggested. In its first year as a public company, CMAC reported a remarkable seventy percent surge in income compared to the previous year, posting income of twenty-one-point-eight million dollars on revenues of eighty-three-point-five million. The company held over five percent market share in the private mortgage insurance market.

It was a parentage worth noting: Reliance Group Holdings, CMAC's former corporate parent, would itself collapse into bankruptcy in 2001, making the 1992 spinoff one of the most fortuitous acts of corporate separation in insurance history. Had CMAC remained a subsidiary, it might have been dragged into the parent's insolvency. Instead, it was free to grow.

The early 1990s housing market was recovering from the savings and loan crisis, and mortgage origination volumes were climbing steadily. For a private mortgage insurer, this was an ideal environment. The excesses that had caused the S&L debacle had been purged from the system. Lending standards were reasonable. Borrowers were creditworthy. And the fundamental demand for homeownership, driven by demographic growth, suburbanization, and rising incomes, was strong and getting stronger. CMAC was positioned to ride a wave that would last for the better part of fifteen years, though nobody knew at the time how large or how dangerous that wave would eventually become.

Under James C. Miller, its first CEO as a public company, the business focused on operational discipline and steady market share growth. But the real acceleration came when Frank Filipps took the helm. Filipps had joined CMAC as senior vice president and chief financial officer around the time of the IPO, was promoted to president in 1995, and became chairman and CEO shortly after.

He brought an aggressive but disciplined approach to growth. One of his early moves was to restructure the company's commission incentive system, rewarding sales personnel only for new business rather than allowing them to coast on renewal premiums from existing policies.

This seemingly mundane operational tweak had an outsized impact: it reoriented the entire sales organization toward growth rather than relationship maintenance.

Combined with innovative product introductions like the monthly premium plan, which gave borrowers more flexible payment options, Filipps' strategy nearly doubled CMAC's market share from five percent to approximately ten percent during the 1990s. He was also a visionary in terms of community impact, pioneering a partnership with the Navajo Nation to extend homeownership access to Native American communities.

By the late 1990s, CMAC was actively looking for a transformational deal that would vault it into the top tier of the industry. Filipps was not content to be a mid-sized player in a consolidating market.

IV. The Amerin Merger: Becoming Radian (1998-1999)

That transformational deal arrived in November 1998, when CMAC announced the acquisition of Amerin Corporation of Chicago in a six-hundred-six-million-dollar all-stock transaction. The merger was significant not just for its size but for what it created. The combined entity would serve approximately thirty-five hundred customers and rank as the second-largest mortgage insurer in the country, trailing only MGIC Investment Corporation, which had dominated the industry for decades.

Filipps articulated a vision that went beyond simple scale. "The merger is about creativity, breaking the mold, and a commitment to delivering the best of the best," he said at the time. This was not empty corporate rhetoric. The expected cost savings were meaningful, with projections of fifteen million dollars in synergies in the first year alone, but the real strategic rationale was about competitive positioning in an industry that was clearly consolidating.

CMAC and Amerin had complementary strengths: CMAC's East Coast lender relationships meshed well with Amerin's Midwest presence, and the combined technology platforms could be rationalized to reduce duplication while improving service levels.

In June 1999, the company formally changed its name to Radian Group Inc., with Radian Guaranty Inc. serving as its principal mortgage insurance subsidiary. The name change was more than cosmetic. It signaled a desire to leave behind the somewhat parochial identity of a Philadelphia-based insurance subsidiary and present itself as a national, and eventually international, financial services company. The word "Radian" itself evokes measurement, precision, and mathematics, qualities that an insurance company built on actuarial science would want associated with its brand.

The merger integration proceeded smoothly by the standards of financial services combinations, which are notoriously difficult to execute. The two companies' cultures were compatible, their geographic footprints were complementary, and the operational synergies materialized roughly on schedule. By the turn of the millennium, Radian had established itself as a genuine force in the mortgage insurance industry, with the scale, capital base, and market relationships to compete with anyone.

There is an important subtext to the Amerin merger that tends to get lost in the corporate narrative. By the late 1990s, the mortgage insurance industry was beginning to show the characteristics that would define it for the next two decades: a small number of well-capitalized players competing for a finite pie of business, with the GSEs serving as de facto regulators of who could play and on what terms. The Amerin deal was as much about survival in this consolidating landscape as it was about growth. Mid-sized players without the scale to invest in technology, maintain capital requirements, and service thousands of lender relationships simultaneously were going to struggle. Filipps understood this intuitively, and the merger gave Radian the scale it needed to be a permanent participant rather than an eventual acquisition target.

What the newly formed Radian Group did next, however, would plant the seeds of both extraordinary growth and near-catastrophic risk. Filipps' ambition to "break the mold" was about to be tested in ways nobody anticipated.

V. Expansion and Ambition: The Bubble Years (2000-2007)

The early 2000s were a period of extraordinary ambition for Radian, and the decisions made during this era reveal the dangerous seduction of a rising market. In 2000, Radian made the fateful announcement that it would begin insuring one hundred percent mortgages, enabling families to become homeowners with literally no down payment.

Think about what insuring a zero-down-payment mortgage actually means. The insurance company is guaranteeing a loan where the borrower has zero equity from day one. If housing prices decline even slightly, the borrower is immediately underwater. The borrower's economic incentive to keep paying drops dramatically when they can walk away and rent a comparable home for less. The insurer is essentially making a leveraged bet that housing prices will continue to rise for the life of the policy.

For context, from 1991 to 2006, national home prices had never declined on an annual basis. The idea that they could fall simultaneously across the entire country seemed to many like an impossible scenario. Risk models at every major financial institution were calibrated to a world where housing prices always went up, or at worst, flattened. The phrase "well, housing prices have never declined nationally" was repeated so often in boardrooms and risk committees that it had acquired the weight of natural law. History had a cruel lesson in store.

Radian was far from alone in this expansion. Every major mortgage insurer was writing increasingly aggressive business. The lenders wanted it. The GSEs were buying it. The rating agencies were blessing it. And consumers, who had watched their neighbors' home values double in five years, were eager to get in on the action. It was a system-wide failure of risk assessment, and Radian was both a participant and a victim.

Simultaneously, Radian expanded its product capabilities at breakneck speed. Radian Reinsurance launched in September 2000 to offer credit enhancement for home equity loans, second mortgages, and manufactured housing, products that would prove to be among the most toxic asset classes in the coming crisis. The company expanded its internet offerings to provide e-commerce options to lenders, positioning itself as a technology-forward insurer.

Perhaps the most consequential strategic decision of this era was the move into financial guaranty insurance. In 2001, Radian acquired Enhance Financial Services Group for approximately five hundred forty million dollars, creating Radian Asset Assurance, a subsidiary that provided credit enhancement for municipal bonds and structured finance transactions.

This acquisition also brought with it a joint venture called C-BASS, a subprime mortgage operation that originated and securitized subprime loans. At the time, C-BASS appeared to be a lucrative addition to the portfolio, generating attractive returns from the booming subprime market. Within a few years, it would become a ticking time bomb.

Also in 2001, Radian targeted the European market through a partnership with AGS Financial LLC, forming Asset Guaranty Insurance Company and opening a London office in May. The global ambitions were clear: Radian wanted to be more than a domestic mortgage insurer.

The hubris of the era was not unique to Radian. Every major financial institution was riding the same wave, convinced that financial engineering had fundamentally tamed credit risk.

But Radian's exposure was unusually diverse and unusually dangerous: conventional mortgage insurance on increasingly aggressive loan products, financial guaranty exposure to structured finance, a joint venture in subprime origination, and reinsurance of second mortgages and manufactured housing. The company had diversified in precisely the wrong direction, adding correlated credit risks that would all blow up simultaneously when the music stopped.

Then came the proposed merger with MGIC. On February 6, 2007, the very day Radian's stock hit its all-time high of sixty-seven dollars and thirty-five cents, the two companies announced an agreement to merge. The combined entity, to be called MGIC Radian Financial Group, would have controlled nearly fifteen billion dollars in total assets and more than two hundred ninety billion dollars of primary mortgage insurance in force. It would have been the undisputed giant of mortgage insurance.

By September 2007, the deal was dead. The two companies cited "current market conditions" that had made combining significantly more challenging. The reality was far more dramatic. MGIC had gotten cold feet as the subprime crisis accelerated. Their joint C-BASS venture had been hammered by margin calls: two hundred ninety million dollars in the first half of 2007 alone, followed by another two hundred sixty million in just the first twenty-four days of July. Each company faced a write-off of over five hundred million dollars on the C-BASS investment. MGIC actually sued Radian to force disclosure of its financial guaranty losses. The one-hundred-eighty-five-million-dollar breakup fee was eliminated entirely in the termination agreement.

The failed merger was a harbinger of something far worse. But there is a fascinating counterfactual worth noting: had the MGIC deal closed before the crisis hit, the combined entity would have been a significantly larger company with a more diversified insurance-in-force portfolio. Whether that scale would have made the combined company more or less likely to survive is debatable, but the fact that both MGIC and Radian survived independently suggests that the termination, while painful at the time, may have been one of those fortunate accidents of corporate history.

VI. The Crisis: Near-Death Experience (2007-2010)

Picture a single data point rendered on a stock chart. On February 6, 2007, Radian's stock touched sixty-seven dollars and thirty-five cents, its all-time high. On July 3, 2008, roughly seventeen months later, it hit seventy cents, its all-time low. A decline of ninety-nine percent.

Radian Group's total credit and default risk exposure stood at approximately one hundred sixty billion dollars. Of that, forty-five billion came from its mortgage insurance subsidiary, Radian Guaranty, while the rest was spread across financial guaranty and credit enhancement businesses.

To put one hundred sixty billion dollars in perspective, that was larger than the GDP of most countries. It was more than the combined market capitalization of every major U.S. airline at the time. And every single line of that exposure was bleeding simultaneously, because the one scenario the risk models had assumed was implausible, a nationwide decline in housing prices combined with a spike in unemployment and a seizure of credit markets, was happening in real time.

The losses were cascading from every direction.

Radian projected six hundred twenty-three million dollars in losses from subprime mortgages for which it had provided primary insurance. Its businesses insuring second mortgages and insuring securities linked to subprime interest payments were expected to generate an additional five hundred seventy million dollars in losses. And the C-BASS joint venture required a write-off exceeding five hundred million dollars.

Added together, the company was staring at potential losses that dwarfed its capital base. The arithmetic of survival was brutally simple: either raise enough new capital to absorb the losses while maintaining regulatory minimums, or join the growing list of financial institutions that the crisis was consuming.

At the center of this maelstrom was S.A. Ibrahim, who had been serving as Radian's CEO since May 2005. Ibrahim was a fascinating figure for this particular crisis. Educated at Osmania University in India with an engineering degree and at the Wharton School with an MBA in finance, he had spent the mid-1990s heading reengineering efforts across four continents for American Express's Travel Related Services Company. He had served as CEO and COO of Chemical Mortgage Finance, then moved to GreenPoint Financial Corporation in 1997, where he ran the mortgage business.

Ironically, GreenPoint Mortgage Funding, the subsidiary Ibrahim had led before joining Radian, itself stopped issuing new policies in August 2007 and was dissolved. Ibrahim had jumped from one ship to another, and both were sinking.

Ibrahim also served as Chairman of the Board of MERSCORP, sat on the Mortgage Bankers Association of America Residential Board of Governors, and on the Fannie Mae National Advisory Council. He was deeply embedded in the mortgage ecosystem, which gave him both the relationships and the credibility to navigate the crisis, but also meant he could not pretend he had not seen the warning signs.

In 2008, Ibrahim honored a commitment he had made a year earlier to speak at the Wharton Leadership Conference. The organizers had invited him when Radian was still flying high. By the time the conference arrived, the company was in existential crisis. "What could be more relevant than hearing about leadership from someone in the middle of a multitude of challenges?" he observed. Later, a Wharton publication described his experience as "a journey to the gates of hell and back," a phrase that captured the existential dread permeating the Philadelphia headquarters during those dark months.

Ibrahim's approach to the crisis combined brutal pragmatism with something rarer: genuine optimism about the future even as the present was crumbling. "If I am not optimistic and giving people hope, it is doomed," he said in a 2010 interview with Leaders Magazine. He kept his workforce of six hundred employees together rather than implementing massive layoffs. More counterintuitively, he actually expanded the sales force, adding twenty salespeople during the crisis and targeting credit unions as new customers.

This seemed reckless at the time but was rooted in a calculated bet: the companies still writing insurance when the crisis ended would capture enormous market share from the competitors who had retreated or failed. Ibrahim understood something that many of his peers did not: a mortgage insurance company's most valuable asset is not its capital reserves or its investment portfolio. It is its relationships with lenders and the trust those lenders place in the insurer's willingness and ability to pay claims. Those relationships, once broken, take years to rebuild. By staying in the market while competitors pulled back, Radian was buying future market share at a price that no acquisition could match.

The survival playbook was brutal and unglamorous. In 2008, Radian discontinued writing new financial guaranty business entirely, slamming the door on the structured finance operations that had compounded its losses. The company implemented aggressive capital preservation measures, cutting expenses and doing everything possible to stop the hemorrhaging while maintaining minimum capital levels.

In 2010, Radian raised five hundred twenty-five million dollars in fresh capital. This was deeply dilutive to existing shareholders, painful to execute in a market still skeptical of anything housing-related, and absolutely necessary for survival. Without it, the company would have breached capital requirements mandated by state regulators and the GSEs, which would have meant losing its ability to write new business. A death sentence.

For perspective, two of Radian's competitors, PMI Group and Triad Guaranty, could not raise sufficient capital and were forced into runoff, effectively ceasing to exist as going concerns. The difference between survival and death in the mortgage insurance industry during the crisis came down to a handful of decisions made under extreme duress: whether to raise dilutive capital or try to ride it out, whether to cut losses on non-core businesses immediately or hope for recovery, and whether to maintain lender relationships at all costs or retreat to protect capital. Radian made the painful choices. Others did not.

By 2012, Radian had not only returned to profitability but had become the number-one mortgage insurer by market share, with a twenty-two-point-two percent share of the market. Ibrahim's bet on expanding during the crisis had paid off spectacularly. The company commissioned a "Radian Rising" mural at its headquarters, symbolism that captured the organizational mood of defiant recovery.

The near-death experience was not something to be forgotten. It was something to be memorialized, studied, and used as the foundation for everything that came next. The underwriting models that emerged from the crisis were fundamentally different from those that preceded it. Pre-crisis models had relied heavily on historical data that, by definition, did not include a scenario where housing prices fell nationally. Post-crisis models incorporated stress testing, tail-risk analysis, and a deep suspicion of any assumption that "this time is different." The organizational culture shifted from one that rewarded growth and product innovation to one that rewarded disciplined risk management and capital stewardship. This cultural transformation, perhaps more than any single financial transaction, is what would enable Radian's eventual strategic pivot.

VII. Post-Crisis Restructuring and Focus (2010-2020)

The Radian that emerged from the financial crisis was a fundamentally different organization from the one that had entered it. The era of expansion into adjacent businesses, of financial guaranty, of structured finance, of zero-down-payment insurance, was definitively over. The new mandate was simple: get back to basics, build an impregnable balance sheet, and never again let diversification become a euphemism for undisciplined risk-taking.

The most significant transaction of the post-crisis restructuring came in 2014, when Radian reached an agreement to sell its financial guaranty business, Radian Asset Assurance, to Assured Guaranty. The deal, initially announced at eight hundred ten million dollars, closed in April 2015 at a final price of approximately eight hundred four-point-five million.

This was not a sale born of weakness but of strategic clarity. The financial guaranty business had been a source of enormous losses during the crisis, and even in recovery, it represented a capital-intensive, complex operation that distracted management from the core mortgage insurance franchise. The proceeds provided a crucial injection of capital that could be redeployed into the core business or returned to shareholders.

The same year, Radian completed the acquisition of Clayton Holdings for three hundred five million dollars in cash. Clayton, based in Shelton, Connecticut, was a provider of loan due diligence, surveillance, REO management, and consulting services to the mortgage industry, employing approximately seven hundred people.

The strategic logic was sound: Clayton's services were complementary to core mortgage insurance, providing loan-level analysis and quality control capabilities that could enhance underwriting and reduce risk.

Unlike the financial guaranty diversification of the previous era, this was expansion within the mortgage value chain rather than into an entirely different risk category. The theory was that if Radian could offer lenders not just insurance but also due diligence, valuation, and technology services, it would create multiple touchpoints in the mortgage process that would make lender relationships stickier and generate fee income that was not correlated to the insurance underwriting cycle.

Clayton subsequently acquired Red Bell Real Estate and ValuAmerica in 2015, adding valuation and title capabilities. In 2017, Radian acquired Mortgage Builder, a mortgage loan origination system provider. These acquisitions reflected a coherent strategy: if the core mortgage insurance product was essentially a commodity, perhaps Radian could differentiate through an ecosystem of related services that made it more valuable to lender customers. It was a reasonable theory, and one that several competitors explored in their own ways. But ultimately, as the Inigo acquisition would later demonstrate, the services diversification was not enough to break out of the commodity dynamics of the core business.

The regulatory landscape was being reshaped simultaneously. Fannie Mae and Freddie Mac established the Private Mortgage Insurer Eligibility Requirements, known as PMIERs, which set minimum capital standards for approved mortgage insurers. Think of PMIERs as the Basel III of mortgage insurance: they mandated specific levels of available assets relative to risk exposure, with granular requirements varying based on loan characteristics, vintage, and delinquency status.

For well-capitalized companies like Radian, PMIERs represented a competitive moat. The requirements were stringent enough to make new entry nearly impossible while confirming the financial strength of existing players.

No new private mortgage insurer has been approved since NMI Holdings in 2013, and the likelihood of future approvals remains negligible.

The net effect was to ossify the competitive landscape: the six survivors of the crisis would essentially be the six participants in the market for the foreseeable future. This is an important insight for investors. PMIERs created a regulated oligopoly with enormous barriers to entry, which should in theory allow participants to earn attractive returns. But the counterbalancing force is that six competitors in a commoditized product is enough to prevent any single player from exercising meaningful pricing power. You have a stable industry with predictable participants but limited ability for any one company to earn outsized returns. It is a market structure that rewards operational efficiency and penalizes ambition, which partly explains why Radian eventually looked beyond mortgage insurance for growth.

In 2013, Radian confronted another regulatory challenge, reaching a settlement with the Consumer Financial Protection Bureau over captive reinsurance arrangements. The company agreed not to enter into new captive arrangements for ten years and paid a civil penalty of three million seven hundred fifty thousand dollars. Since 2008, HUD had been investigating whether these captive arrangements constituted unlawful payments under the Real Estate Settlement Procedures Act. In these arrangements, lenders received reinsurance premiums through affiliated captive entities in exchange for directing mortgage insurance business. Regulators viewed this as potential kickbacks dressed up in insurance jargon. The settlement eliminated a material regulatory overhang.

By 2013, Radian had become the largest private mortgage insurer in the country, with one hundred sixty-one billion dollars of insurance in force. In May 2016, S.A. Ibrahim announced his intention to retire in December 2017, having guided the company from near-collapse to market leadership over more than a decade.

Ibrahim's legacy was one of crisis survival, disciplined rebuilding, and, perhaps most importantly, the institutional memory of what happens when you take on risks you do not fully understand. His successor would inherit a company that was fundamentally sound but facing a strategic question that none of the post-crisis restructuring had fully answered.

VIII. The Recovery Years: Building Excess Capital (2020-2024)

Rick Thornberry assumed the CEO role at Radian in March 2017, and his background told you something about what the board was looking for. Thornberry was not a career insurance executive in the traditional mold. He held a bachelor's degree in business administration with a concentration in accounting from Saint Louis University and started his career as a CPA at Deloitte, focusing on financial services clients.

He then moved through increasingly senior roles in the mortgage industry: executive positions at Prudential Home Mortgage Company, Citicorp Mortgage, and MBNA Home Finance. But more tellingly, Thornberry was an entrepreneur. In 1999, he co-founded Nexstar Financial Corporation, an end-to-end mortgage business process outsourcing firm that he built from scratch and sold to MBNA in 2005. He then co-founded NexSpring Group in 2006, a financial services advisory and fintech firm serving private equity firms, lenders, and mortgage investors.

This was a person who understood mortgage operations at a granular level, who had built and sold companies, and who thought about strategic positioning with an entrepreneurial lens rather than a bureaucratic one. He also brought a strong organizational focus, creating a diversity, equity, and inclusion council at Radian and earning recognition as a 2024 HousingWire Vanguard and a 2025 CEO of the Year by HR Awards.

In 2019, Radian posted net income of six hundred seventy-two million dollars, a remarkable figure for a company that had nearly ceased to exist a decade earlier. The mortgage insurance business was performing beautifully, benefiting from strong housing markets and underwriting standards hardened by the crisis experience.

Then came the pandemic. COVID-19 initially terrified the mortgage insurance industry. Memories of 2008 were fresh, and the prospect of mass unemployment leading to mass mortgage defaults was very real. In March and April of 2020, as lockdowns shuttered the economy and unemployment applications surged to levels not seen since the Great Depression, executives across the mortgage insurance industry held emergency board meetings to model scenarios that looked disturbingly similar to 2008.

But something unexpected happened. Instead of destroying the housing market, the pandemic supercharged it. Remote work enabled geographic mobility, as millions of Americans discovered they could live anywhere with a decent internet connection and suddenly wanted more space. Federal stimulus payments and enhanced unemployment benefits supported household incomes at levels that actually exceeded pre-pandemic earnings for many families. And the Federal Reserve drove interest rates to the lowest levels in recorded history, with thirty-year fixed mortgage rates briefly dipping below three percent.

The combination was explosive. Housing demand surged as remote workers fled expensive cities for suburbs and exurbs. Supply was already constrained by a decade of underbuilding following the 2008 crisis. Home prices skyrocketed, and mortgage origination volumes hit levels not seen since the mid-2000s bubble. For mortgage insurers, this was the best possible environment: high volumes of new insurance written on loans with strong credit quality, substantial borrower equity, and rock-bottom default rates.

A quietly momentous milestone arrived in 2023, when Radian Guaranty resumed paying ordinary dividends to its parent holding company for the first time since 2007. A sixteen-year gap.

That single fact encapsulates the length and severity of the post-crisis rehabilitation better than any other data point. For sixteen years, the insurance subsidiary's capital had been ringfenced by regulators who demanded that excess reserves stay within the regulated entity rather than flowing upward to the holding company. The resumption of dividends signaled that regulators were finally satisfied with the subsidiary's capital position, and that excess capital could begin migrating to the holding company for broader corporate purposes.

The result was a classic "good problem" in financial services: too much capital, not enough places to deploy it efficiently. The company became aggressive about returning capital to shareholders, repurchasing seventy-four million shares for one-point-eight billion dollars since 2020, representing more than thirty-six percent of outstanding shares. This was not a token buyback program. This was a company methodically shrinking its share count while earnings continued to grow.

In January 2024, S&P Global Ratings upgraded Radian Guaranty to A-minus, solidifying its investment-grade status across all major rating agencies. This upgrade was symbolically important: it represented an external validation that the company had fully recovered from the crisis and was now considered a strong, stable insurer by the most rigorous independent assessors.

For the full year of 2024, the company reported total revenues of one-point-three billion dollars and net income of six hundred four million dollars, with primary mortgage insurance in force at two hundred seventy-five billion and fifty-two billion in new insurance written.

By early 2024, Radian maintained approximately sixteen percent market share, positioning it as one of the top three providers alongside MGIC, which led with about twenty percent, and Essent. The gap between MGIC and Radian had been narrowing from two-point-six percentage points to just one-point-two points.

But underneath these impressive numbers, a strategic tension was building. Competition among private mortgage insurers was, and remains, largely driven by pricing, underwriting standards, and service quality. Essent had differentiated through its proprietary EssentEDGE credit engine, a machine-learning-based pricing tool. Arch Capital had been the first to introduce risk-based pricing and the first to execute a mortgage insurance-linked note, transferring risk to capital markets. Everyone was competing, but nobody was truly winning. Market shares shifted by fractions of a percentage point. The private mortgage insurance market was fundamentally homogeneous.

The question confronting Thornberry and his board was stark: what do you do when you are generating enormous amounts of cash in a mature, commoditized business with limited growth potential?

Consider the math. Radian was generating over six hundred million dollars in annual net income from a business with approximately sixteen percent market share. The total addressable market for private mortgage insurance in the United States was finite, constrained by the volume of conventional mortgage originations with down payments below twenty percent. Growing market share from sixteen to twenty percent would require either pricing concessions that would erode profitability or service improvements so dramatic that they would convince lenders to switch from longstanding insurer relationships. Neither path offered particularly attractive risk-adjusted returns.

The company could keep buying back stock, which is value-accretive in the short term but does not change the fundamental trajectory of the enterprise. It could try to gain market share through pricing, which invites a destructive race to the bottom. It could pay a special dividend, which is tax-inefficient and signals a lack of better ideas. Or it could do something bold.

IX. The Bold Pivot: The Inigo Acquisition (2025-Present)

On September 18, 2025, Radian Group made the announcement that would define the next chapter of its corporate history: a definitive agreement to acquire Inigo Limited, a Lloyd's of London specialty insurer, for one-point-seven billion dollars in a primarily all-cash transaction.

To appreciate the audacity of this move, you need to understand what Inigo actually is. Start with the name. Inigo was named after Inigo Jones, the seventeenth-century English architect who introduced Renaissance classicism to Britain. The founders chose the name deliberately: they wanted to build an insurance company the way an architect builds a building, from first principles, with attention to design, structure, and craftsmanship.

Inigo was founded in November 2020 by three former senior executives from Hiscox, one of the most respected specialty insurers in the London market. Richard Watson, who became CEO, had spent thirty-three years at Hiscox building their specialty insurance franchise. Russell Merrett, the chief underwriting officer, brought decades of underwriting expertise. Stuart Bridges, the CFO, provided the financial architecture. All three had the credibility, the relationships, and the institutional knowledge to build something meaningful from scratch.

They raised eight hundred million dollars in initial capital from a blue-chip consortium of global investors, including J.C. Flowers and Company, La Caisse de depot et placement du Quebec, Oak Hill Advisors, and the Qatar Investment Authority. Their first move was to purchase the StarStone Managing Agency and the rights to operate Lloyd's Syndicate 1301 from Enstar, giving them an immediate operational platform within Lloyd's of London.

For those unfamiliar with how Lloyd's works, a brief explanation is useful. Lloyd's of London is not an insurance company. It is a marketplace, a centuries-old ecosystem where syndicates of capital providers come together to underwrite risks that are often too complex, too large, or too unusual for the conventional insurance market. Each syndicate operates independently, managed by a managing agency, and writes business within the Lloyd's framework. Access to Lloyd's is regulated, and syndicate capacity is allocated by Lloyd's central governance. This means that owning a Lloyd's syndicate is not like starting an insurance company from scratch: it comes with an established platform, regulatory permissions, broker relationships, and access to a flow of specialty business that would take decades to replicate independently. Syndicate 1301 was Inigo's platform, and acquiring it from Enstar gave the founders an enormous head start.

By January 2021, Inigo was underwriting.

Their approach was deliberately focused. Inigo wrote seven classes of business: reinsurance, property insurance, terrorism and political violence, general liability, directors and officers, marine liability, and energy liability. They later added cyber insurance in April 2023. Each class was selected because the founders believed they could build genuine expertise and analytical edge, not because the premium volume was attractive.

This discipline was reflected in their emphasis on data science. Watson described the approach with palpable enthusiasm: "The advances in computer science and the ability to gather and analyze data offer so much potential to reinvent how risk is understood and managed. What we are able to do now is so cool."

The results were staggering for a start-up. In its first year, Inigo wrote four hundred twelve million dollars in gross written premium, making it the biggest start-up syndicate in Lloyd's history. By 2022, gross written premium had doubled to eight hundred two million, and the company posted its first profit of twenty-eight-point-seven million with a combined ratio of ninety-four-point-four percent.

In 2023, the trajectory steepened dramatically: gross written premium surged thirty-five percent to one-point-one billion, profit before tax hit one hundred forty-four-point-five million, a fivefold increase, and the combined ratio improved to an impressive eighty-five-point-five percent. By 2024, gross written premium reached one-point-three-four billion, and projections for 2025 estimated one-point-six billion. In the first half of 2025 alone, Inigo reported profit before tax of one hundred sixteen million with an eighty-six percent net combined ratio.

For Radian, the strategic rationale was multilayered. The acquisition valued Inigo at one-and-a-half times its projected tangible equity at the end of 2025. The deal was expected to deliver mid-teens percentage accretion to earnings per share and approximately two hundred basis points of accretion to return on equity in the first full year after closing. Most importantly, it would double Radian's annual revenue and expand the addressable market by a factor of twelve.

As Radian's CFO noted, the company had "deployed its excess capital into an operating business that we expect is going to earn a mid-teens return through the cycle," a vastly better use than letting it sit on the balance sheet.

Watson was equally direct about the cultural alignment: "We are delighted to have found Radian. From our first meeting there was a clear cultural match." Given that cultural misalignment is the number one killer of insurance acquisitions, this was not a throwaway comment.

The financing reflected the capital strength Radian had spent fifteen years building. By the third quarter of 2025, available liquidity had increased to nine hundred ninety-five million dollars, with expectations of approximately one-point-eight billion in holding company liquidity by early 2026. In November 2025, the company secured a new five-hundred-million-dollar unsecured revolving credit facility with a syndicate of bank lenders, maturing in November 2030, with an accordion option to increase capacity by two hundred fifty million.

Simultaneously, the board approved a divestiture plan for the Mortgage Conduit, Title, and Real Estate Services businesses, the legacy of the Clayton Holdings acquisition and subsequent bolt-ons. These operations, carried at approximately one hundred seventy million dollars, were reclassified to discontinued operations, with divestitures expected to complete by the third quarter of 2026. The company's strategic identity was being sharpened: mortgage insurance plus Lloyd's specialty insurance, nothing else.

In December 2025, all regulatory approvals were received. The transaction closed in February 2026 for a final price of one-point-six-seven billion dollars. A mortgage insurer becoming a Lloyd's specialty player is not incremental. It is a fundamentally different business. The fact that Radian retained Inigo's leadership team suggests an awareness that the acquired expertise is the entire point of the transaction.

X. Current State and Future Vision (2025-Beyond)

As of early 2026, Radian Group stands at the most consequential moment in its nearly fifty-year history. The company now operates two distinct but complementary franchises: a market-leading U.S. private mortgage insurance business performing at record levels, and a rapidly growing Lloyd's specialty insurance platform opening entirely new categories of growth.

Full-year 2025 results showed net income of six hundred eighteen million dollars and insurance in force reaching two hundred eighty-three billion. New insurance written for 2025 totaled fifty-five billion dollars.

The third quarter of 2025 demonstrated the core franchise firing on all cylinders, with fifteen-point-five billion in new insurance written, a fifteen percent year-over-year increase. Fourth quarter net income came in at one hundred fifty-nine million, or one dollar and fifteen cents per diluted share. Radian Guaranty paid a two-hundred-million-dollar ordinary dividend to the holding company during the third quarter alone, evidence of the capital generation engine operating at full capacity.

In 2025, the company returned five hundred seventy-six million dollars to shareholders through dividends and share repurchases. The board approved a new seven-hundred-fifty-million-dollar share repurchase program extending through December 2027. Combined with the existing program's remaining one hundred thirteen million, total repurchase authority reached approximately eight hundred sixty-three million, signaling confidence that the company can fund the transformation and still return substantial capital.

CEO Rick Thornberry's vision is ambitious. The articulated strategy is to transform from a cyclical U.S. mortgage specialist into a diversified global specialty insurer. The mortgage insurance business provides stable, predictable cash flows and massive domestic scale. The Inigo platform provides growth, global reach, diversification away from the U.S. housing cycle, and access to specialty markets where underwriting expertise determines profitability rather than price competition.

The company maintains a nearly three percent dividend yield with thirty-three consecutive years of dividend payments, a track record spanning the company's entire public history including the near-death experience of 2008. That continuity says something meaningful about management's commitment to shareholders even in the darkest periods. Maintaining a dividend when your stock is trading below a dollar requires either extraordinary financial strength or extraordinary stubbornness. In Radian's case, it was probably both.

The market is still digesting the implications of the transformation. Mortgage insurance stocks have historically traded at single-digit price-to-earnings multiples, reflecting their cyclical nature and commodity economics. Specialty insurers with strong Lloyd's franchises and disciplined underwriting regularly command multiples two to three times higher. The valuation gap between these two categories is one of the widest in the insurance industry.

If the market eventually re-rates Radian as a diversified specialty insurer rather than a cyclical mortgage play, the implications for valuation could be substantial. But that re-rating requires execution, specifically demonstrating that the Inigo platform can maintain its underwriting discipline under Radian's ownership, that the two businesses generate genuine synergies rather than merely coexisting, and that management can navigate the complexities of operating across two regulatory regimes, two continents, and two fundamentally different insurance cultures.

The integration is still in its earliest stages, and the coming quarters will reveal whether the combination is greater than the sum of its parts or merely more complex.

XI. Playbook: Business and Strategic Lessons

The Radian story offers several enduring lessons for investors and business leaders, each earned through real experience rather than theoretical frameworks.

The first lesson is about survival through crisis. Radian's near-death experience illustrates a counterintuitive truth: the companies that survive existential threats are not necessarily the ones with the best balance sheets going in, but the ones with management teams willing to make painful decisions quickly. Ibrahim's willingness to shut down financial guaranty entirely, raise deeply dilutive capital when the stock was in single digits, and expand the sales force while competitors retreated was the difference between survival and oblivion. PMI Group and Triad Guaranty, which could not or would not make those same painful decisions, no longer exist.

The second lesson is about the commodity trap. Private mortgage insurance is a textbook example of a market where strong competitive barriers coexist with limited pricing power. Six approved insurers, fungible products, and price-sensitive buyers create a dynamic where profitability is acceptable but extraordinary returns are difficult to sustain.

Radian's pivot into specialty insurance was an acknowledgment that you cannot outrun the commodity trap through operational excellence alone. Sometimes you have to change the game entirely.

The third lesson is about capital deployment discipline. The years between 2020 and 2025 represent a masterclass in managing excess capital. Rather than empire-building through scattered acquisitions or returning to the undisciplined diversification of the pre-crisis era, Radian was methodical.

The playbook was clear: massive share buybacks to optimize the capital structure, patient accumulation of reserves, sixteen years of waiting for the insurance subsidiary to resume ordinary dividends, and then a single transformative transaction deployed at the right moment. The discipline to wait for the right opportunity, rather than deploying capital into mediocre ones, is among the rarest qualities in corporate management.

The fourth lesson is about bold strategic pivots. When incremental improvements are insufficient, transformational action becomes necessary.

Radian's board recognized that they could spend the next twenty years as a highly competent mortgage insurer generating steady but unspectacular returns, or they could take a calculated risk to build something genuinely different. The Inigo acquisition was a bet that the combination of mortgage insurance's stable cash flows with specialty insurance's growth potential would create a more valuable, more resilient, and fundamentally more interesting company than either business could be on its own.

The fifth lesson is about regulatory navigation. PMIERs, the CFPB captive reinsurance settlement, state insurance capital requirements, GSE approval processes, and Lloyd's capital frameworks all constrain behavior but also create barriers protecting incumbents. Radian turned regulatory compliance into competitive advantage, treating capital requirements as a feature rather than a bug.

The sixth lesson is about the float game. Insurance companies collect premiums today and pay claims tomorrow, and the money sitting in between, the float, can be invested. Warren Buffett has spent decades explaining this concept at Berkshire Hathaway, and it applies equally to mortgage insurance. Radian's investment portfolio generates hundreds of millions in annual investment income, which effectively subsidizes the insurance operations and provides a floor under profitability even in years when underwriting results are mediocre. The Inigo acquisition adds a second float stream from an entirely different risk category, creating a diversified investment income base that is more stable than either business alone. This is an underappreciated aspect of the strategic rationale: it is not just about underwriting diversification, it is about float diversification.

The final lesson is about optionality. Building balance sheet strength creates strategic options that may not be visible in the moment. When Radian was building excess capital from 2020 to 2024, the Inigo acquisition was not on the horizon. But the financial flexibility that resulted from discipline made the transaction possible when the opportunity materialized. Counter-cyclical thinking, making your biggest acquisition when you have the strength to do it rather than when you are forced to, is the mark of a management team that thinks in decades rather than quarters. The contrast with the pre-crisis era is instructive: in the early 2000s, Radian deployed capital into financial guaranty and subprime exposure during a period of market euphoria, when risks were highest and prices were most inflated. In 2025, it deployed capital into a growing specialty platform from a position of financial strength and operational discipline. The difference in outcomes may prove to be equally dramatic.

XII. Competitive Analysis: Porter's Five Forces and Hamilton's Seven Powers

Understanding Radian's competitive position requires examining the company through two complementary frameworks, applied both to its legacy mortgage insurance business and to its evolving post-Inigo profile.

Starting with Porter's Five Forces, the threat of new entrants into mortgage insurance is remarkably low. PMIERs capital requirements create enormous barriers requiring hundreds of millions in minimum available assets. The GSE approval process is rigorous and time-consuming. No new private mortgage insurer has been approved since NMI Holdings in 2013, and established relationships with thousands of lenders provide an additional moat that takes decades to build.

The specialty insurance market entered through Inigo has different but equally formidable barriers: Lloyd's syndicate capacity is regulated and limited, and building the underwriting expertise and broker relationships required to compete effectively takes years of patient investment.

The bargaining power of suppliers is low. Insurance is a financial product whose primary input is capital, and Radian has demonstrated consistent access to capital and reinsurance markets.

The bargaining power of buyers presents the asymmetry that goes to the heart of Radian's strategic rationale. In mortgage insurance, buyer power is high because lenders can choose from six approved insurers in a commoditized market where switching costs are relatively low.

In specialty insurance post-Inigo, the dynamics are fundamentally different. Complex, bespoke risks like marine liability, political violence, or directors and officers coverage require deep underwriting expertise that not every insurer possesses. Buyers of these products value underwriting judgment and claims-paying certainty over minor pricing differences. Moving from a market where price is paramount to one where expertise commands premium economics is the core strategic insight driving the entire transformation.

The threat of substitutes is moderate. FHA and VA programs offer alternatives, and GSE credit risk transfer programs provide options outside private mortgage insurance. But private mortgage insurance remains the most capital-efficient solution for conventional loans with down payments below twenty percent, and GSE requirements effectively mandate its use.

Competitive rivalry in mortgage insurance is intense but structured. Six approved insurers maintain a stable yet concentrated market where MGIC leads with roughly twenty percent share, followed by Radian at sixteen percent, with Essent, Arch, Enact, and NMI filling out the field. The competitive dynamics resemble an oligopoly where participants are locked in a constant but low-intensity struggle for marginal market share gains.

What makes this rivalry particularly interesting is the absence of meaningful exit. No approved insurer would voluntarily leave the market because the barriers to re-entry would be prohibitive. This creates a dynamic where all six participants are permanently committed, which tends to moderate competitive intensity over time. Nobody wants to start a pricing war that they will have to live with for decades. But the flip side is that nobody can achieve dominant market share either, because the remaining players will always match competitive moves.

The Inigo acquisition repositions Radian against a different peer set entirely. Instead of comparing itself exclusively to MGIC and Essent, Radian can now be evaluated alongside diversified specialty insurers like RenaissanceRe, Hiscox, and Beazley. Whether this reframing changes how the market values the company remains to be seen.

Turning to Hamilton Helmer's Seven Powers, the framework reveals the strategic logic of the transformation clearly.

Scale economies provide a moderate advantage. Fixed technology and compliance costs are spread over volume, and the combined Radian-Inigo entity achieves meaningful scale across diversified insurance lines.

However, scale in mortgage insurance is not as powerful as in other financial services because the product is too standardized for scale-based differentiation. The largest mortgage insurer and the smallest approved insurer offer fundamentally the same product.

Network economies have historically been absent from Radian's business. Post-Inigo, the Lloyd's ecosystem provides valuable access to brokers, underwriters, and capital providers, but this is ecosystem participation rather than exponential network effects.

Counter-positioning is perhaps the most important power the Inigo acquisition creates, and it deserves careful examination. Traditional mortgage insurance competitors, MGIC, Essent, Enact, Arch, and NMI, are all deeply embedded in the domestic mortgage insurance paradigm. Their boards, management teams, risk frameworks, and investor bases are all oriented around U.S. housing exposure.

For any of them to follow Radian into specialty insurance via a Lloyd's platform would require a similarly transformative acquisition, a fundamental cultural overhaul, and complete management retooling. The incumbent's existing business model actually prevents them from responding, which is the classic Helmer counter-positioning dynamic. The irony is that Radian's competitors would likely view such a move as irrational, which is precisely why it creates durable competitive advantage.

Switching costs provide moderate protection. Lender servicing relationships create stickiness, loan origination system integration introduces friction, and mortgage insurance policies persist on the books for years, generating premiums long after the initial sale. This persistency creates an embedded revenue stream with high visibility.

Branding remains weak in the traditional mortgage insurance context but carries meaningful credibility within the Lloyd's ecosystem, where reputation and relationships are foundational.

Cornered resources were historically absent from Radian's competitive position, but the Inigo acquisition changes this equation materially. Lloyd's Syndicate 1301 represents regulated, limited capacity within the Lloyd's marketplace, a resource that cannot be replicated simply by spending money.

The experienced underwriting team, led by Watson with his thirty-three years at Hiscox and complemented by Merrett and Bridges, constitutes intellectual capital that cannot be easily reproduced. Specialty underwriting talent is scarce, takes decades to develop, and tends to be loyal to organizations where they can practice their craft with genuine autonomy.

Process power is where Radian's post-crisis transformation built the strongest advantage. The underwriting models refined through decades of experience, and particularly the risk management insights seared into the organization by the 2008 catastrophe, represent genuine institutional knowledge that cannot be copied overnight.

The combination of U.S. mortgage data analytics with Lloyd's specialty underwriting capabilities creates a knowledge base that no single competitor possesses.

The synthesis is revealing. Pre-Inigo, Radian possessed switching costs and process power as its primary sources of durable advantage. These were sufficient to survive and prosper within the existing market structure but insufficient to escape the commodity dynamics that capped returns and limited growth. Radian was winning the game it was playing, but the game itself had a low ceiling.

The post-Inigo strategy is explicitly designed to change the game. By building counter-positioning that traditional mortgage insurance peers cannot replicate, accessing cornered resources through the Lloyd's platform and Inigo's underwriting talent, and achieving meaningful scale across diversified insurance lines, Radian is attempting to construct a competitive position that generates both higher returns and faster growth than its legacy business alone could deliver.

The risk, from a Seven Powers perspective, is that counter-positioning only works if the new position is genuinely defensible. If other well-capitalized insurers can simply acquire their way into Lloyd's, then Radian's counter-positioning advantage is temporary at best. But the scarcity of available Lloyd's platforms with Inigo's quality, the difficulty of integrating insurance cultures across continents, and the first-mover advantage in this particular strategic niche all suggest that the barrier to replication is real, even if it is not permanent.

XIII. Bull vs. Bear Case

The investment case for Radian at this juncture is genuinely interesting because reasonable people can look at the same facts and reach opposite conclusions.

The bull case rests on several reinforcing pillars. The balance sheet is a fortress with excess capital providing both protection and strategic flexibility. The core mortgage insurance franchise continues performing at record levels with credit quality among the best in the company's history. The Inigo acquisition transforms the growth profile from a limited domestic ceiling to global specialty insurance, a market twelve times larger than the historical addressable market.

Inigo itself is not speculative: it posted an eighty-five-point-five percent combined ratio in 2023, a metric most established specialty insurers would envy, and it is led by founders with a combined century of Lloyd's experience.

The management team has demonstrated ability to survive existential crisis and allocate capital with extraordinary discipline. If the market re-rates Radian from a cyclical mortgage insurer at modest multiples to a diversified specialty insurer commanding premium valuation, the stock has meaningful room to appreciate.

The analogy worth considering is what happened when companies like Fairfax Financial or Markel Corporation were recognized as diversified specialty platforms rather than niche insurers. The re-rating in those cases was dramatic and sustained.

The nearly three percent dividend yield with thirty-three consecutive years of payments provides income while shareholders wait. And the 2025 shareholder return of five hundred seventy-six million demonstrates the flywheel remains intact even during a major acquisition.

There is also a structural argument in the bull case worth considering. The private mortgage insurance industry benefits from two powerful secular tailwinds. First, housing affordability in the United States continues to deteriorate, which means a growing share of homebuyers need to make smaller down payments, which means more loans require private mortgage insurance. Second, the regulatory framework established after 2008 has effectively locked in private mortgage insurance as a permanent feature of the conventional mortgage market. These are not cyclical tailwinds. They are structural demand drivers that will persist regardless of interest rate movements or economic cycles. The addition of Inigo provides exposure to an entirely separate set of growth drivers in the global specialty insurance market.

The bear case is equally compelling.

Execution risk on this integration is substantial, particularly when the acquiring management team has zero specialty insurance experience. The cultural gap between a Philadelphia mortgage insurer and a London Lloyd's syndicate is enormous: different regulatory frameworks, compensation structures, risk philosophies, and professional cultures.

Lloyd's underwriters operate in a bespoke, relationship-driven environment where individual judgment on complex risks determines profitability. It is a world that has almost nothing in common with the algorithmic, high-volume, data-driven world of U.S. mortgage insurance.

Paying one-and-a-half times tangible book for a company founded just five years ago raises legitimate valuation questions. Inigo has only three years of profitability and has never been tested through a major catastrophe loss or a hard market downturn.

The eighty-five percent combined ratio looks superb, but the specialty insurance pricing cycle has been historically favorable during Inigo's brief operating history. What happens when a major hurricane generates multi-billion-dollar industry losses, or when casualty reserves prove inadequate years after policies were written? These are risks that Radian's mortgage-centric risk management team has never had to manage.

Meanwhile, the core mortgage insurance business faces structural headwinds from elevated interest rates suppressing refinancing and purchase volume. If rates remain elevated for an extended period, the existing insurance-in-force portfolio will shrink through natural runoff as homeowners pay down their mortgages or reach twenty percent equity, at which point the private mortgage insurance is automatically cancelled. If new insurance written does not grow fast enough to replace the natural runoff, the in-force portfolio could decline, taking premiums and earnings with it.

There is also the question of what happens to Radian's organizational focus now that it operates two fundamentally different businesses. In the pre-crisis era, Radian's diversification into financial guaranty diluted management attention and introduced risks that the core team did not fully understand. Is the specialty insurance diversification different this time because Radian retained Inigo's experienced management team? Or will the inevitable tensions of a dual-headquarter, dual-culture organization eventually compromise performance in one or both businesses?

Bears would argue that Radian is taking a business generating steady returns and adding complexity, volatility, and execution risk in pursuit of a market re-rating that may never arrive.

The divestiture of Mortgage Conduit, Title, and Real Estate Services businesses introduces transition risk if buyers do not materialize at expected valuations. The businesses are carried at approximately one hundred seventy million dollars on the balance sheet, and management has indicated it expects no significant gain or loss. But in a sale process, expectations and outcomes do not always align, particularly when the buyer knows the seller is divesting as part of a strategic plan rather than from a position of negotiating strength.

And established specialty insurers, the Hiscoxes and Beazleys and Lancashires of the Lloyd's world, may view Radian as a well-capitalized but inexperienced newcomer, responding with aggressive pricing or talent poaching that could undermine the acquired franchise. The Lloyd's market is a small, relationship-driven ecosystem where reputations are built over decades. Earning credibility as a new participant, even one backed by a nearly fifty-year-old parent company, takes time and demonstrable underwriting skill.

For investors monitoring this transformation, three metrics matter above all.

First, the combined ratio for the Inigo specialty insurance segment. This is the single most important indicator of whether the acquired business maintains underwriting discipline under new ownership. Consistent performance below ninety percent validates the thesis. Deterioration above ninety-five percent raises serious questions.

Second, primary mortgage insurance in force for the legacy business. This metric, which hit an all-time high of two hundred eighty-three billion dollars in 2025, reflects the size and health of the existing book. Sustained growth in insurance in force combined with low default rates demonstrates that the core franchise remains healthy even as management attention divides across two fundamentally different businesses.

Third, return on equity for the consolidated entity. Radian has targeted approximately two hundred basis points of ROE accretion from Inigo in the first full year. Tracking consolidated ROE against this target and against specialty insurance peers will reveal whether the combination is creating value or merely adding complexity.

The Radian story is ultimately about whether a company that survived one of the most dramatic near-death experiences in American corporate history can channel the discipline, humility, and strategic courage forged in that crisis into a genuinely transformative reinvention. The answer will unfold over the coming years, and it will be worth watching closely.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube