Rogers Communications: The High-Stakes Financial Alchemy of Canada's Telecom and Sports Empire

I. Introduction & Episode Roadmap

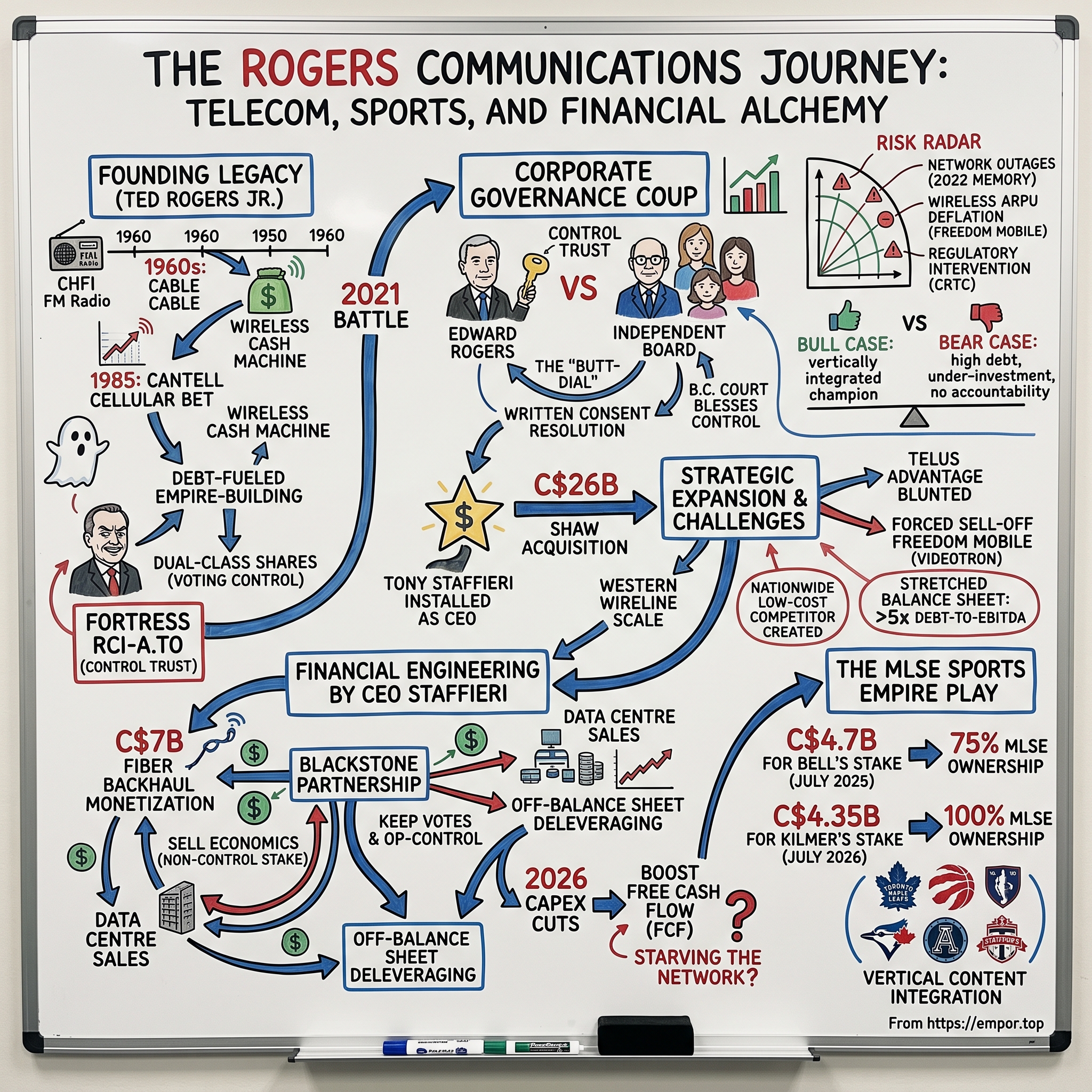

Picture the scene in a Toronto boardroom in the autumn of 2021. Canada's largest wireless carrier, a company that carries the calls, texts, and Netflix streams of tens of millions of Canadians, has effectively split into two rival governments. On one side sits a chief executive with the support of the independent board and much of the founding family. On the other sits a single man — Edward Rogers, son of the founder — armed with nothing more than a piece of paper and control of a family trust. That piece of paper, a written consent resolution, would prove more powerful than the board, the CEO, and the objections of his own mother and sisters combined. It is one of the most extraordinary demonstrations of raw corporate control in modern North American business, and it tells you almost everything you need to know about how Rogers Communications actually works.

How did a business that began with a single, money-losing FM radio station in 1960 become a company generating more than C$17 billion in annual revenue that controls both the physical pipes carrying Canada's data and the crown jewels of Canadian professional sport — the Toronto Maple Leafs, the Raptors, and the Blue Jays?1 And how did it do so while behaving less like a widely held public company and more like a private family fiefdom?

That tension — a public company traded on the TSX and NYSE that answers to one family's trust — is the spine of this story. It runs from founder Ted Rogers Jr.'s obsessive, debt-fueled empire-building, through the Shakespearean 2021 boardroom coup that a B.C. court ultimately blessed,7 and into a post-coup era of breathtaking transformation under CEO Tony Staffieri: the C$26 billion acquisition of Shaw Communications,8 the multi-stage capture of Maple Leaf Sports & Entertainment (MLSE) culminating in a July 2026 deal for 100% ownership,2 and a suite of financial-engineering maneuvers designed to keep a mountain of debt from crushing the whole edifice.

The core puzzle for any serious investor is this. Rogers is simultaneously buying the most expensive trophy assets in Canadian sport and slashing the capital it spends on the networks that generate its cash. It is monetizing its own fiber backbone, selling data centres, and manufacturing free cash flow — all while carrying leverage that would make most telecom boards flinch. Is this brilliant capital allocation, or is it financial alchemy that borrows against the future of the network to fund the present-day acquisition of hockey teams? Let us start where every empire starts: with a ghost, an obsession, and a bet nobody else would make.

II. The Founding Legacy: Ted Rogers Jr. and the Rebuilding of an Empire

Every founding myth needs a ghost, and the Rogers story has a literal one. In 1925, a young Toronto inventor named Edward "Ted" Rogers Sr. cracked a problem that had defeated the entire radio industry: he built the world's first practical alternating-current radio tube, the "Rogers Batteryless Receiving Tube." Overnight, radios could be plugged into a wall socket instead of running on messy, acid-leaking batteries. It was a genuine technological breakthrough, and it made the Rogers name synonymous with radio in Canada. Then, in 1939, Ted Sr. died of a hemorrhage at just 38 years old. The business slipped away, the family fortune evaporated, and his five-year-old son was left with an inheritance that was less financial than psychological: a burning obsession to reclaim a name that had once meant something.

That son, Ted Rogers Jr., spent his life answering the ghost. In 1960, while still a law student at the University of Toronto, he scraped together the money to buy a struggling Toronto FM station, CHFI. At the time this looked like buying a horse in the age of the automobile — FM radio was a commercial graveyard, so obscure that most radios sold in Canada could not even receive the band. Ted's insight was not that FM was good; it was that FM was early. He sold cheap FM converters door to door to build an audience before the format's fidelity advantage became obvious. It is the pattern that would define his entire career: spot the technological shift a beat before the market, then borrow aggressively to own it.

He ran the same play on cable television. Through the 1960s and 1970s, while incumbents dismissed cable as a rural curiosity for households with bad reception, Ted amassed cable franchises across Ontario and beyond, wiring up homes and turning Rogers Cable into a dominant distribution monopoly in the markets it controlled. Cable taught him the lesson that would become the company's DNA: whoever owns the physical connection into the home owns a toll booth that compounds for decades.

The biggest bet came in 1985. Ted co-founded Cantel, a national cellular carrier, to challenge the government-blessed telephone monopolies of the Stentor alliance. Mobile phones were then luxury bricks for executives, and the conventional wisdom said the market was tiny. Ted saw the opposite — a business where customers would pay every month, forever, with margins that cable could only dream of. Cellular, rebranded Rogers Wireless, became the cash machine that funded everything else. To this day, wireless remains the engine room of the entire enterprise.

Ted's final act was vertical integration — buying the content that flowed through his pipes. He acquired the publishing and broadcasting giant Maclean-Hunter in 1994, bought the Toronto Blue Jays in 2000, and launched Sportsnet to control live sports rights. The logic was that pipes are commodities but content is not; owning the thing people want to watch protects the network from becoming a dumb utility. When Ted Rogers Jr. died in December 2008, he left behind a company loaded with debt but armored with a defensive mix of network and content assets — and one more thing that would matter enormously: a dual-class share structure engineered so that the family, through a control trust, could never be outvoted, taken over, or second-guessed by public shareholders. He built the fortress. Thirteen years later, his children would go to war inside it.

III. The Corporate Governance Battle of 2021: A Shakespearean Feud

To understand the war, you first have to understand the weapon Ted left behind. Rogers Communications has two classes of stock. The Class A shares (TSX: RCI-A) carry the votes; the Class B shares (TSX: RCI-B, NYSE: RCI) carry the economics and are what the public overwhelmingly owns. The trick is that the Rogers Control Trust — the family vehicle — holds roughly 97.5% of the Class A voting shares, which means that whoever chairs the trust controls the company outright, regardless of what the public equity thinks. Since Ted's death, the chair of that trust has been his son, Edward Rogers. On paper, Edward is one director among many. In practice, he holds a skeleton key to the entire corporation.

For years the arrangement was stable. Then, in 2021, it detonated over a mundane operational disagreement that curdled into a dynastic feud. Edward had soured on CEO Joe Natale and quietly lined up the company's chief financial officer, Tony Staffieri, to replace him. The plan might have unfolded discreetly but for one of the most improbable accidents in corporate history: Staffieri, according to widely reported accounts, accidentally pocket-dialed Natale — a "butt-dial" — and the CEO overheard himself being discussed as a dead man walking.14 The scheme was exposed, and the company's polite fiction of unity collapsed.

What followed was pure Shakespeare, staged inside a telecom giant. The family split down the middle. Edward's mother, Loretta Rogers, and his sisters, Melinda Rogers-Hixon and Martha Rogers, sided with Natale and the independent board. When the board moved against Edward — firing Staffieri and stripping Edward of his chairmanship of the company board — he reached for the nuclear option written into the family's own DNA. As chair of the Rogers Control Trust, Edward executed a written shareholder consent resolution that simply fired five independent directors and installed his own hand-picked slate in their place, no meeting required.

The audacity of the move sent it straight to court, where it became a landmark test of Canadian corporate law. Could a controlling shareholder rewire a public company's board by signing a document at his kitchen table? In November 2021, the Supreme Court of British Columbia said yes. The court ruled that Edward's written consent was valid under B.C. corporate law and that no physical shareholder meeting was required to give it effect.157 Dissenting family members called it "a black eye for good governance and shareholder rights," but the law was the law.15

Edward was reinstated as chair. Natale departed with a severance package reported at roughly C$20 million, and Tony Staffieri — the very executive whose promotion had lit the fuse — was installed as CEO.15 The feud's coda came in January 2024, when Melinda Rogers-Hixon and Martha Rogers retired from the board as part of a family settlement, leaving Edward's control unchallenged and total.11 For public shareholders, the episode was a stark, real-world lesson: at Rogers, the board is not the ultimate authority, the trust is. Everything that followed — the deals, the debt, the sports empire — was the product of a company now steered by a single, unaccountable hand. And that hand was about to make the biggest bet since Ted's cellular gamble.

IV. The Shaw Acquisition: Overpaying for National Scale

Rogers had a geography problem that money could not immediately fix. For all its dominance in wireless nationally and in cable across Ontario and Atlantic Canada, it had essentially no wireline footprint in Western Canada. British Columbia and Alberta were Telus country, and Telus was pouring capital into fiber-to-the-home — the gold-standard broadband technology that runs glass all the way into the house. A Rogers with no Western wireline was a Rogers permanently boxed out of a quarter of the country's households and exposed on its flank. The answer was to buy the West outright.

In March 2021, Rogers announced a roughly C$26 billion agreement to acquire Shaw Communications, the Calgary-based cable titan that owned the Western wireline networks Rogers coveted.8 The deal was colossal in ambition and, on the numbers, expensive. Rogers paid a valuation of roughly 10.7 times Shaw's 2021 EV/EBITDA — a premium of around 70% over where Shaw had been trading before the announcement. Even crediting the full C$1 billion of promised annual cost synergies, the effective post-synergy multiple sat near 7.6 times. For context, global cable and wireline peers typically changed hands in the 7 to 8 times range. Rogers, in other words, paid a full price and then some.

Why overpay? Two reasons, and neither appears on a synergy slide. First, scale is defensive: a national wireline footprint blunts Telus's fiber advantage and lets Rogers spread the enormous fixed cost of a network over more subscribers. Second, and more quietly, paying a knockout premium discourages a rival bid and gets the target's controlling family to sign. Shaw was also a family-controlled company; a clean, rich, all-cash-and-stock offer was as much about locking up the Shaw family as about the assets. The lesson for investors is that Rogers treated the Western footprint as a strategic must-have rather than a value buy — a decision that made sense competitively but stretched the balance sheet past 5.0 times debt-to-EBITDA, a level that would shape every financial decision the company made afterward.

The price also came in a currency other than dollars: competition. Ottawa's regulators — the Competition Bureau, the CRTC, and the department of Innovation, Science and Economic Development (ISED) — would not wave through a merger that eliminated a wireless competitor. To win approval, Rogers was forced to carve out and sell Shaw's scrappy discount wireless brand, Freedom Mobile. The deal finally closed on April 3, 2023, and on that same day Quebecor's Videotron completed its purchase of Freedom Mobile on an enterprise value of about C$2.85 billion.1213 The regulatory conditions attached to Videotron were pointed: it was required to offer plans at least 20% cheaper than those of Rogers, Bell, and Telus, and to expand Freedom's network.13

Here is the irony at the heart of the transaction. Rogers got the Western wireline scale it wanted, but in the process it hand-delivered a subsidized, government-mandated, low-cost fourth national competitor to Quebecor — a company with a proven playbook for waging price war. Rogers spent C$26 billion to solve a geographic weakness and, in doing so, energized the very pricing pressure that now gnaws at its wireless margins. The bill for that trade-off would come due just as interest rates spiked — which is where the financial engineering begins.

V. Financial Alchemy & Deleveraging under Tony Staffieri

Tony Staffieri inherited a beautiful problem: a company with world-class assets and a balance sheet buckling under the weight of how it acquired them. Post-Shaw, Rogers carried one of the heaviest debt loads in Canadian corporate life, and it carried it into the most hostile interest-rate environment in a generation. A CFO by training, Staffieri responded not with a fire sale but with a series of intricate financial maneuvers designed to raise billions without triggering the two things a controlling family hates most — debt covenants and equity dilution.

The centerpiece was a deal that deserves to be studied in finance courses. In April 2025, Rogers agreed to sell a non-controlling stake in a newly formed subsidiary holding a slice of its wireless backhaul fiber — the transport network that hauls cellular traffic from towers back to the core — to a consortium led by Blackstone. The structure is the artful part. Blackstone and its co-investors put in roughly C$7 billion (about US$4.85 billion) for a 49.9% equity interest, but received only 20% of the voting rights. Rogers kept 50.1% of the equity and 80% of the votes, meaning it retained full operational and strategic control of an asset it had, in economic terms, half-sold.418 The transaction closed on June 20, 2025.3

The elegance lies in what the deal is not. It is not debt, so it does not trip Rogers' borrowing covenants or add to reported leverage in the way a bond would. It is not a public equity raise, so it does not dilute the family's carefully guarded ownership. And because the backhaul subsidiary signed a 25-year contract to remain Rogers' exclusive backhaul provider in Ontario and Alberta, Rogers did not lose the use of the network — it simply sold outside investors a claim on the cash the network throws off, then used substantially all of the proceeds to pay down debt.18 The Blackstone consortium was a who's-who of Canadian pension capital — CPP Investments, CDPQ, PSP Investments, BCI, and IMCO — patient money content to own a low-risk, cash-generating piece of essential infrastructure.18 It is off-balance-sheet deleveraging in its purest form: monetize a passive, utility-like asset, keep the votes, bank the cash.

Staffieri kept shedding non-core weight. In August 2025, Rogers agreed to sell its portfolio of nine data centres to InfraRed Capital Partners, converting another slug of capital-intensive real estate into cash for the deleveraging campaign.10 Each move followed the same logic: if an asset generates predictable cash but does not require Rogers' operational control to keep the customer, sell the economics and keep the relationship.

But the boldest financial statement was the one Rogers made about its networks themselves. In its Q1 2026 results, released in April 2026, management slashed full-year capital expenditure guidance to C$2.5–2.7 billion, down sharply from the prior C$3.3–3.5 billion range, while simultaneously raising free-cash-flow guidance to C$4.1–4.3 billion.1 Mechanically, the two moves are the same move: capex is cash out the door, so cutting it flatters free cash flow almost dollar-for-dollar. That is where the skeptics live. Free cash flow generated by spending less on your network is not the same quality of cash flow as free cash flow generated by earning more from your customers. The bull reads it as discipline after a period of heavy fiber investment; the bear reads it as starving the physical network — the fiber and 5G plant — at the precise moment Bell is touting a pure-fiber footprint and Telus is extending its own. Which reading is right will not be knowable for years, because network under-investment shows up not in the next quarter but in the churn statistics of 2029. The capital freed up, meanwhile, was already spoken for — by the most expensive trophies in Canada.

VI. Consolidating the Canadian Sports Empire: The MLSE Power Play

For decades, the most valuable collection of sports teams in Canada sat behind an awkward stalemate. Maple Leaf Sports & Entertainment — owner of the Maple Leafs, the Raptors, Toronto FC, the Argonauts, and their arena — was co-owned by two bitter telecom rivals, Rogers and Bell, each holding 37.5%, with the businessman Larry Tanenbaum's Kilmer Sports holding the remaining 25%. Two competitors sharing custody of the same prize is a recipe for paralysis, and for years neither side would let the other win. Then, in September 2024, Rogers ended the standoff with a checkbook.

Rogers agreed to buy Bell's entire 37.5% stake for C$4.7 billion in cash, a transaction that valued MLSE in its entirety at roughly C$12.5 billion and handed Rogers a 75% controlling interest.619 The deal was not purely a sports play — as part of the arrangement, Bell secured long-term broadcast rights to Leafs and Raptors games on its TSN network for two decades, meaning Rogers bought the equity while its rival kept a claim on the content.19 The transaction cleared its regulatory and league hurdles and closed on July 2, 2025, making Rogers the majority owner of the franchises.5

That might have been the end of the ambition. Instead, barely a year later, Rogers went for the whole thing. On July 6, 2026 — nine days before the writing of this article — Rogers signed a definitive agreement to purchase the final 25% from Tanenbaum's Kilmer Sports for C$4.35 billion, a deal that would give it 100% of MLSE.29 Do the arithmetic and something striking jumps out. The 37.5% Bell stake implied a C$12.5 billion valuation for the whole; the 25% Kilmer stake, at C$4.35 billion, implies a valuation of roughly C$17.4 billion.9 In roughly twelve months, the implied price of the same asset stepped up by nearly C$5 billion. Some of that is genuine appreciation in sports franchise values, which have run hot globally; some of it is the premium a buyer pays to convert control into total ownership and erase the last minority partner. Either way, Rogers paid up — again — to own something outright.

The strategic logic is the vertical-integration thesis that Ted Rogers pioneered, taken to its absolute conclusion. Combine MLSE's basketball, hockey, soccer, and football franchises with Rogers' 100% ownership of the Blue Jays, the Rogers Centre, and the Sportsnet broadcast network, and Rogers now controls what is arguably the most valuable and least replicable sports-media ecosystem in North America. In an age of cord-cutting, live sports is the one category of programming audiences will not time-shift, will not pirate en masse, and must watch live — which makes it the ultimate anchor for a distribution business.

There is, of course, the small matter of paying for it. Two MLSE tranches plus the Blue Jays sit atop a balance sheet already stretched by Shaw. Staffieri's answer, telegraphed to investors, is to package Sportsnet, the Blue Jays, and MLSE into a single consolidated sports-and-media entity and sell a minority stake to institutional or public investors in late 2026 or 2027 — crystallizing a headline valuation, raising deleveraging cash, and, in true Rogers fashion, keeping control. Whether the public will pay Rogers' price for a minority slice of Canadian sport, with the family holding the votes, is the open question that hangs over the entire strategy. To assess it, we have to look at the businesses that actually pay the bills.

VII. Core Business Deep Dive: Segments, Economics, and Market Structure

Strip away the sports pageantry and the financial wizardry, and Rogers is three businesses stacked on top of one another, operating inside one of the most protected market structures in the developed world. Canadian telecom is a "Big Three" oligopoly — Rogers, Bell, and Telus together command roughly 90% of the national market — insulated by staggering capital barriers and by foreign-ownership restrictions that legally bar the deep-pocketed American carriers from ever entering. It is a comfortable club, and Rogers is one of only three members. But comfortable does not mean static, and each of Rogers' three segments tells a different story about where the pressure is building.

The Wireless segment is the cash engine, the direct descendant of Ted's 1985 Cantel bet. It generates on the order of C$2.6 billion in quarterly revenue and roughly C$1.32 billion in adjusted EBITDA, an approximately 65% margin that is the envy of almost every other line of business Rogers touches, serving around 11.6 million subscribers.1 Those margins are what fund everything else. But the key metric to watch is not the subscriber count — it is postpaid ARPU, or average revenue per user, the monthly bill the typical contract customer pays. ARPU is under sustained downward pressure, and the culprit has a name: Videotron's Freedom Mobile, the very competitor Rogers was forced to create. When a subsidized fourth carrier is mandated to undercut you by 20%, price discipline in the industry erodes, and it erodes fastest in the discount tier. The oligopoly still holds, but its pricing power is quietly leaking.

The Cable/Broadband segment is the Shaw integration made flesh — roughly C$2.0 billion in quarterly revenue at about C$1.12 billion of adjusted EBITDA, a margin near 58%.1 The strategic project here is migrating legacy Shaw customers in the West onto a next-generation platform built around Comcast's Xfinity technology and a "10G" cable roadmap, the goal being to slow churn and hold the line against Telus's fiber. This is where the capex debate bites hardest: broadband is a technology arms race, and choosing to spend less on it than your fiber-building rivals is a bet that "good enough" cable can hold customers who are being offered glass to the door. That bet is unproven.

The Media segment is the sports powerhouse, and in Q1 2026 it did something it rarely does — it made headlines with growth rather than losses. Revenue surged 82% year over year to C$988 million, driven overwhelmingly by the consolidation of MLSE onto Rogers' financials, and the segment reached roughly adjusted-EBITDA breakeven, a swing of about C$60 million from the prior year.1 For a media business that has historically been a money-loser tolerated for its strategic value, breakeven is a meaningful marker. The caution is that much of the jump is consolidation accounting — Rogers now books all of MLSE's revenue because it owns the franchises — rather than pure organic growth, so the year-over-year comparison flatters the underlying trend. How Rogers wins here is unmatched sports-content integration and national scale; how it loses is that Bell's superior fiber footprint in the East and Telus's execution in the West keep chipping at the core connectivity businesses that the media empire is supposed to protect.

VIII. Strategic Moat Analysis: Helmer's 7 Powers & Porter's Five Forces

Set the deals aside and ask the harder question an investor must ask: what actually protects Rogers' profits from being competed away? Two frameworks help — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — and Rogers scores genuinely well on some and only rhetorically well on others.

Start with Helmer. Scale economies are real and high. A telecom network is a machine of enormous fixed costs — spectrum, towers, fiber, billing systems — that gets cheaper per customer the more customers you spread it across. Post-Shaw, Rogers has Canada's largest combined wireless-plus-cable subscriber base, and that scale genuinely lowers its unit costs relative to a hypothetical smaller entrant. This is the most durable power in the portfolio.

Cornered resource is where Rogers is arguably strongest of all. The company owns something that literally cannot be manufactured: exclusive, government-licensed low-band and mid-band spectrum (including the prized 3500 MHz and 3800 MHz bands for 5G). There is a finite quantity of usable radio spectrum, the government controls its allocation, and Rogers holds a premier slice — a legally enforced scarcity that no amount of capital can replicate. Layer on 100% ownership of MLSE and the Blue Jays, and Rogers controls two categories of genuinely unique, non-replicable assets. This is the closest thing in the business to an unbreachable wall.

Switching costs are the softest of the three, and honesty requires calling them moderate rather than high. Bundling a household's internet, TV, home monitoring, and several mobile lines onto one bill creates friction — untangling all of it to switch providers is a hassle most families avoid. But friction is not a lock. When a competitor offers a bill that is 20% cheaper, switching costs bend, and Canada's regulators are actively working to lower them further. The moat here is real but shallow.

Now Porter. The threat of new entrants is close to nil — the combination of multi-billion-dollar spectrum auctions, physical network buildout, and foreign-ownership limits makes de novo entry practically impossible, which is exactly why the oligopoly persists. The bargaining power of buyers is individually low but structurally rising, because the CRTC has been mandating wholesale access — forcing incumbents to rent their networks to smaller resellers (MVNOs) and to offer cheaper entry-tier plans — which hands consumers alternatives the market would not otherwise provide. And the intensity of rivalry is high and climbing, concentrated in the discount sub-brands where Fido, Koodo, and Virgin Plus knife-fight over price and where Freedom Mobile keeps expanding its footprint. The uncomfortable synthesis is that Rogers' structural moats — scale and spectrum — are formidable, but its pricing power, the thing that turns a moat into profit, is being eroded at the edges by regulation and by a competitor of its own creation. A wide moat around a shrinking margin is still a risk.

IX. Management Credibility & Governance Stress Test

Judge management by behavior over time, not by the polish of the latest press release. The Rogers leadership tandem is unusual: Edward Rogers, the controller who can rewire the board by signature, paired with Tony Staffieri, the execution architect who owes his job to Edward's patronage. It is a partnership with no daylight between principal and agent — which is a strength for decisiveness and a glaring weakness for accountability.

On execution, the track record since 2021 is, on its own terms, impressive. The Shaw integration proceeded faster than skeptics expected, with the company claiming synergy capture ahead of schedule. The Blackstone backhaul deal was a genuinely creative piece of off-balance-sheet financing that raised C$7 billion without a covenant breach or an equity raise.3 The MLSE consolidation was opportunistic and, in franchise-value terms, well-timed. A management team that says it will deleverage and then actually generates the cash and closes the asset sales to do it has earned a measure of credibility. Staffieri has, so far, delivered the deals he promised.

But the skeptical investor has an equally sharp counter-narrative, and it centers on the quality and motive of that cash generation. The 2026 decision to cut capex from roughly C$3.4 billion toward C$2.5–2.7 billion while raising free-cash-flow guidance is the crux.1 Manufacturing free cash flow by under-spending on the network — and then deploying the freed-up capital toward C$8-plus billion of sports acquisitions — is precisely the pattern that makes long-term owners nervous. It privileges a headline FCF number and a portfolio of prestige assets over the unglamorous, compounding work of keeping the fiber and 5G plant ahead of Bell and Telus. Management frames it as discipline following a heavy investment cycle; a critic frames it as harvesting the network to fund vanity. Both can be partly true, and the ambiguity is itself the problem — because there is no independent board with the power to force the question.

That is the deepest governance risk, and it is structural rather than personal. Because the control trust holds the votes, there is no realistic mechanism by which independent directors or public Class B shareholders can override Edward Rogers on a decision they believe is destroying value. The 2021 court ruling and the 2024 departure of the dissenting sisters removed the last internal checks.711 Public shareholders own the economics and almost none of the control — a single point of failure with no circuit breaker. For some investors the family's long-term orientation is a feature; for others, the absence of any accountability mechanism is a discount that no operating result can fully erase.

X. Risk Radar: What Keeps Management Awake at Night

Every network business lives with the knowledge that its greatest asset can become its greatest liability in a single afternoon. For Rogers, that afternoon already happened. On July 8, 2022, a botched maintenance update — the deletion of a routing filter during a phased network upgrade — cascaded into a national outage that knocked out wireless and internet service for roughly 12 million Canadians for the better part of a day.16 The failure was not cosmetic: it disabled Interac debit payments across the country, cut off some 911 emergency calls, and paralyzed government and banking services. A later independent review commissioned by the CRTC concluded the root cause was human error, compounded by systemic "deficiencies" in Rogers' network design and management.1716 The reputational damage was severe, and the episode crystallized the single largest operational risk the company carries: another systemic failure would invite punishing regulatory penalties and hand competitors a ready-made argument for every switching customer. It is also the strongest exhibit in the case against under-investing in network resilience.

The second risk is slower but more corrosive: wireless ARPU deflation. The pricing pressure from Videotron's Freedom Mobile is not a one-quarter phenomenon — it is a structural feature of a market that regulators deliberately engineered to become more competitive. As Freedom expands aggressively across Ontario, Alberta, and B.C., the entire industry's ability to raise prices weakens, and Rogers' 65% wireless margins are the prize most exposed to that erosion. The cash engine is not stalling, but the market is refusing to let it accelerate.

The third is regulatory intervention, the permanent weather system of Canadian telecom. The CRTC's ongoing push to force lower wholesale rates on both fiber and mobile networks — compelling the incumbents to rent capacity to resellers at regulated prices — directly attacks the returns on the very infrastructure Rogers is spending billions to own. Add the persistent political temptation to be seen "lowering cell phone bills," and Rogers faces a standing risk that the rules of its protected oligopoly get rewritten against it. None of these three risks is likely to be fatal in isolation. The concern is that they compound: a network stretched thin by capex cuts, in a market where regulators are lowering prices and a subsidized rival is taking share, is a more fragile machine than the balance sheet alone suggests.

XI. The Playbook: Business & Investing Lessons

Step back from the specifics, and the Rogers story yields three transferable lessons that any serious investor can carry to other companies.

Lesson one: voting control is the ultimate corporate leverage. The most important number in this entire story is not a revenue figure or a debt ratio — it is the 97.5% of Class A voting shares that the family trust holds despite owning a far smaller slice of the total economics. A dual-class structure lets a family direct a C$17-billion-plus enterprise, execute a boardroom coup, and win a court's blessing to do so, all while public investors supply most of the capital and absorb most of the risk. The lesson is double-edged: such structures can enable patient, long-horizon decisions free from quarterly tyranny, but they also strip away the accountability that protects minority owners. When you buy the Class B shares, you are buying economics without a vote — and you must price that trade honestly.

Lesson two: content is the moat that keeps the pipes from becoming dumb. Ted Rogers understood in 2000 what streaming has now proven: in a world where every other form of content can be time-shifted, pirated, or unbundled, live sports is the one thing audiences must consume in real time. Owning MLSE and the Blue Jays is not a hobby; it is a defensive wall around the broadband and wireless businesses, insurance against the day connectivity becomes a commodity sold on price alone. The lesson generalizes: distribution businesses that fear commoditization can defend themselves by owning the scarce content their customers cannot get elsewhere — provided they do not overpay so much that the insurance costs more than the house.

Lesson three: you can deleverage without selling control or diluting owners. The Blackstone backhaul deal is the cleanest illustration in recent Canadian finance of a specific technique — monetizing a passive, cash-generating, utility-like asset by selling its economics to patient capital while retaining the votes and the operational use.3 For any capital-intensive business sitting on infrastructure that generates predictable cash but does not require full ownership to control, the maneuver is a template. The caveat, always, is that selling tomorrow's cash flows to solve today's leverage is only brilliant if the underlying business keeps growing into the obligations it has created.

XII. The Investment Story Spine: Bull vs. Bear Case

So, does Rogers win from here? Lay the two cases side by side and test them.

The bull case — the "why win" — is that Rogers has become the ultimate vertically integrated telecom-and-sports champion in a legally protected market. It solved its Western geographic gap by taking Shaw, integrated it faster than doubters expected, consolidated 100% of Canada's premier sports franchises into a non-replicable media ecosystem, and demonstrated real financial creativity in raising billions without diluting shareholders or breaching covenants.823 It sits inside an oligopoly with near-impossible barriers to entry and owns cornered resources — spectrum and sports — that cannot be competed away. And it has articulated a credible path to bring leverage down toward and below 3.5 times, using more than C$4 billion of annual free cash flow plus the planned minority monetization of its sports-media entity.1 If those deleveraging plans land, an investor is left owning irreplaceable assets whose debt overhang is steadily shrinking.

The bear case — the "why not" — attacks that story at its two weakest joints: the balance sheet and the network. Rogers remains heavily leveraged, and the mechanism it is using to generate the free cash flow that funds deleveraging is, in part, a cut to network capital spending that risks leaving it technologically inferior to Bell's fiber and Telus's buildout over time.1 Meanwhile, the wireless cash engine faces genuine, regulator-engineered price competition from Freedom Mobile that is eroding the ARPU on which the whole edifice rests. And overlaying all of it is a governance structure in which public shareholders have essentially no ability to check the unilateral decisions of a single family controller.7 The bear's sharpest question is the one the bull cannot fully answer: how much of the "free cash flow" is real earning power, and how much is deferred network investment that will have to be paid back — with interest — in churn and competitive decline later this decade?

The honest verdict is that both cases rest on the same facts read through opposite lenses, and the tie-break will come from a small number of measurable outcomes over the next several years. Three KPIs sit above all others. First, postpaid wireless ARPU — the truest gauge of whether the cash engine still has pricing power or is slowly bleeding to Freedom Mobile. Second, the debt-to-EBITDA leverage ratio — the single number that tells you whether the deleveraging story is real or merely narrated. And third, free cash flow growth and its composition — not just the headline figure, but whether it is being earned from customers or manufactured from capex cuts. Watch those three, and the alchemy either resolves into gold or reveals itself as something less precious. Ted Rogers built the empire on the conviction that owning the pipe and the content beats owning either alone. His son's company is now betting that the same conviction, financed by ever more intricate engineering, can carry it through the most leveraged and most contested chapter in its history. The assets are extraordinary. The question, as always at Rogers, is who is accountable when the bet is wrong.

References

-

Rogers Announces First Quarter 2026 Results — Rogers Communications, 2026-04-22 ↩↩↩↩↩↩↩↩

-

Rogers to Acquire Remaining Interest in Maple Leaf Sports & Entertainment — Rogers Communications, 2026-07-06 ↩↩↩

-

Rogers Closes CDN$7 Billion Equity Investment Transaction — Rogers Communications, 2025-06-20 ↩↩↩↩

-

Rogers Concludes Definitive Agreement for CDN$7 Billion Equity Investment — Rogers Communications, 2025-04-04 ↩

-

Rogers Becomes Majority Owner of Maple Leaf Sports & Entertainment — Rogers Communications, 2025-07-02 ↩

-

Rogers to Become Majority Owner of Maple Leaf Sports & Entertainment — Rogers Communications, 2024-09-18 ↩

-

Edward Rogers wins court ruling in 'Shakespearean' battle for control of family-run telecom giant — CBC News, 2021-11-05 ↩↩↩↩

-

Rogers Secures Canadian Approval for $20 Billion Shaw Deal with Conditions — Reuters, 2023-03-31 ↩↩↩

-

Rogers to Buy Remaining MLSE Stake from Kilmer for $4.35 Billion — Bloomberg, 2026-07-06 ↩↩

-

Rogers Communications to Sell Data Centre Portfolio to InfraRed Capital Partners — GlobeNewswire, 2025-08-11 ↩

-

Rogers Announces Retirement of Melinda Rogers-Hixon and Martha Rogers from Board — Rogers Communications, 2024-01-17 ↩↩

-

Rogers takeover of Shaw finalized, deal now official — CBC News, 2023-04-03 ↩

-

Quebecor closes acquisition of Freedom Mobile — GlobeNewswire, 2023-04-03 ↩↩

-

The Rogers family drama: from a butt-dial to a B.C. Supreme Court case — The Globe and Mail, 2021-11-01 ↩

-

Edward Rogers' board overhaul is valid, B.C. Supreme Court decides — Global News, 2021-11-05 ↩↩↩

-

Assessment of Rogers Networks for Resiliency and Reliability Following the 8 July 2022 Outage — CRTC, 2024-07-05 ↩↩

-

Human error caused 2022 Rogers outage, system 'deficiencies' made it worse: report — CBC News, 2024-07-05 ↩

-

Blackstone Completes CDN$7 Billion Equity Investment in Rogers in Partnership with Leading Canadian Institutional Investors — Blackstone, 2025-06-20 ↩↩↩

-

Rogers to become majority owner of MLSE after buying Bell's stake for $4.7B — CBC News, 2024-09-18 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube