LiveRamp: The Identity Fabric of Digital Advertising

I. Introduction & Episode Roadmap

Somewhere in the invisible plumbing of every major digital advertising campaign running right now, there is a quiet but critical handshake happening. A consumer's email address, hashed and anonymized, is being matched to a browser identifier, a mobile device, a connected television, and perhaps a loyalty card number at a grocery chain. The company making that handshake possible, more often than not, is LiveRamp.

LiveRamp Holdings is not a household name. It does not make the apps people use or the ads they see. It does not own the data. It does not buy the media. What it does is connect things — brands to publishers, offline customer databases to online advertising platforms, first-party data owners to the sprawling, fragmented ecosystem of digital marketing. Think of it as a universal translator for the advertising industry, a Rosetta Stone that allows different parties who speak entirely different data languages to understand one another without ever seeing each other's raw information.

The company generated approximately $746 million in revenue for its fiscal year ending March 2025, employed roughly 1,400 people, and traded on the New York Stock Exchange under the ticker RAMP with a market capitalization hovering around $1.8 billion. Those numbers, on their own, do not scream "critical infrastructure." But consider this: LiveRamp's technology touches an estimated $700 billion in global digital advertising spend. Nearly every major brand, agency holding company, and media platform has some form of integration with LiveRamp's identity graph. When Google announced that third-party cookies would eventually disappear from Chrome — the browser used by roughly two-thirds of the world's internet users — the entire advertising industry scrambled for alternatives. LiveRamp was already building one.

The central question of this story is deceptively simple: How did a data append company buried inside a legacy direct-mail firm in Conway, Arkansas, become the Switzerland of ad tech — the neutral, trusted infrastructure layer that competitors, frenemies, and sworn enemies all depend on? The answer involves a bold corporate spin-off, a series of privacy regulations that turned from existential threat to strategic tailwind, and a bet that the future of advertising would be built on authenticated identity rather than surveillance cookies.

What makes this story particularly relevant right now is the collision of several massive forces: Google's long-delayed but seemingly inevitable deprecation of third-party cookies, a thicket of global privacy regulations from GDPR to state-level laws in the United States, the explosion of retail media networks and connected television advertising, and the rise of AI-powered marketing that demands ever more sophisticated data infrastructure. LiveRamp sits at the intersection of all of these trends. Whether it emerges as the indispensable middleware layer or gets squeezed between cloud platforms from above and open-source alternatives from below is one of the most consequential questions in ad tech.

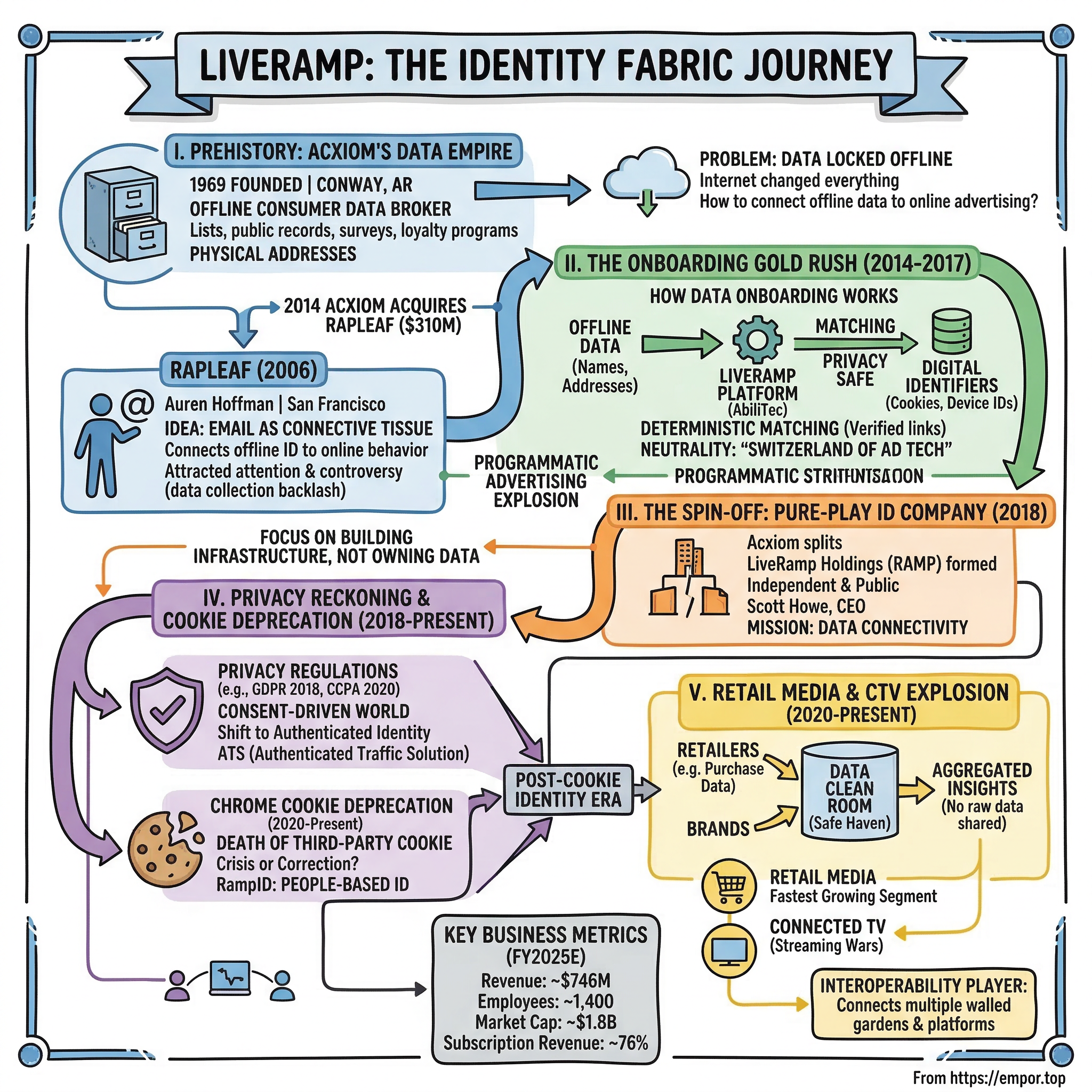

II. Prehistory: Acxiom's Data Empire & the Rapleaf Acquisition

To understand LiveRamp, you have to start in a place that could not be further from Silicon Valley — Conway, Arkansas, population roughly 67,000, home to the University of Central Arkansas and, improbably, one of the most powerful data companies in American history.

Acxiom Corporation was founded in 1969, originally as Demographics Inc., by Charles Ward, a man with a gift for understanding what could be done with lists. Not mailing lists in the quaint, junk-mail sense, but comprehensive databases of consumer information — names, addresses, purchasing histories, demographic details, financial indicators — assembled from public records, surveys, loyalty programs, and data partnerships. By the 1990s, Acxiom had become the largest consumer data broker in the United States, maintaining files on virtually every American household. The company was the invisible engine behind direct mail campaigns, insurance underwriting, political targeting, and credit card marketing. If a company wanted to know who you were, where you lived, what you bought, and what you were likely to buy next, Acxiom was the first call.

But Acxiom faced a problem that would define its next two decades: the internet was changing everything about how advertising worked, and Acxiom's treasure trove of offline data was locked in a format that the digital world could not easily use. The company knew more about American consumers than perhaps any entity outside the federal government, yet it could not connect that knowledge to the explosion of online advertising happening in real time. A brand might know from Acxiom's database that a household in suburban Dallas was in the market for a minivan, but it had no way to show that household a minivan ad when they browsed the web. The offline world and the online world operated on entirely different identity systems — physical addresses and phone numbers on one side, cookies and device IDs on the other.

Enter Rapleaf. Founded in 2006 in San Francisco by Auren Hoffman, a serial entrepreneur with an instinct for data infrastructure, Rapleaf started with a provocative idea: use email addresses as the connective tissue between offline identity and online behavior. The concept was elegant in its simplicity. Nearly everyone has an email address. That email address is used for online accounts, social media profiles, e-commerce purchases, and newsletter subscriptions. It is also typically tied to offline records — loyalty programs, credit card accounts, warranty registrations. If you could build a system that hashed email addresses into anonymous identifiers and matched them across databases, you could bridge the offline-online divide.

Rapleaf attracted attention — and controversy. In 2010, a Wall Street Journal investigation revealed that the company was collecting data from social networking profiles tied to email addresses and selling that information to political campaigns and marketers. The backlash was fierce. Privacy advocates accused Rapleaf of surveillance. Consumers were horrified to learn that their email addresses could unlock detailed profiles about their political leanings, household income, and purchasing habits. Hoffman responded by pivoting hard toward B2B enterprise services and away from consumer-facing data collection, but the episode left a mark.

Despite the controversy — or perhaps because of the underlying technology's obvious power — Acxiom saw in Rapleaf exactly the bridge it needed. In 2014, Acxiom acquired the company for $310 million, a significant bet for a firm generating around $1.1 billion in annual revenue. The acquisition brought not just Rapleaf's email-matching technology but its engineering talent and, crucially, its concept of "data onboarding" — the process of taking a company's offline customer database and making it addressable in digital advertising environments. Acxiom rebranded the acquired business as LiveRamp, and within the larger organization, it became the growth engine that the legacy direct-mail operation desperately needed.

The strategic thesis was clear even then: Acxiom's decades of offline data expertise, combined with LiveRamp's digital connectivity technology, could create something neither company could build alone — a universal identity layer that made data portable, addressable, and privacy-compliant across the entire marketing ecosystem. What nobody fully appreciated at the time was that this identity layer would become far more valuable than the data itself.

III. The Data Onboarding Gold Rush (2014-2017)

To understand what LiveRamp actually does, imagine a major retail bank. This bank has millions of customers. It knows their names, addresses, account balances, transaction histories, and credit scores. It wants to reach its best customers — say, high-net-worth individuals who might be interested in a premium credit card — with targeted digital advertising on websites, mobile apps, and social media. The problem is that the bank's customer database speaks one language (names, addresses, Social Security numbers) while the digital advertising ecosystem speaks an entirely different one (browser cookies, mobile advertising IDs, IP addresses). Data onboarding is the process of translating between these two languages.

Here is how it works in practice. The bank uploads its customer list to LiveRamp's platform. LiveRamp's system, powered by its proprietary AbiliTec identity graph, takes each customer record and matches it — through a series of deterministic and probabilistic techniques — to the corresponding digital identifiers. The bank's customer "Jane Smith at 123 Main Street" becomes a hashed, anonymized token that can be recognized when Jane visits a website, opens an app, or watches a streaming show. Crucially, LiveRamp never shares the raw data with anyone. The bank's customer information stays encrypted, and the matching happens in a privacy-safe environment. The output is simply: "show this ad to this anonymous identifier."

The timing could not have been better. Between 2014 and 2017, programmatic advertising — the automated buying and selling of digital ad inventory through real-time auctions — exploded from a niche technique into the dominant method of digital media buying. Spending on programmatic advertising in the United States roughly doubled during this period, surpassing $30 billion. Brands were desperate to make their first-party customer data actionable in this new environment, and LiveRamp offered the cleanest, most reliable way to do it.

LiveRamp's technical advantage centered on AbiliTec, an identity resolution system that Acxiom had been building and refining for decades. While competitors used probabilistic matching — statistical guesses about whether two data points referred to the same person — AbiliTec specialized in deterministic matching, meaning it relied on known, verified connections between identifiers. A deterministic match might link an email address to a physical address through a verified transaction record, while a probabilistic match might infer a connection based on patterns like shared IP addresses or browsing behavior. Deterministic matching was more accurate, more privacy-compliant, and more trusted by enterprise customers who could not afford false matches in regulated industries like financial services and healthcare.

The early customer wins were telling. Major consumer packaged goods companies, automotive manufacturers, financial institutions, and retail chains all adopted LiveRamp's platform. The value proposition was straightforward: without data onboarding, these companies were flying blind in digital advertising, spending billions on campaigns that could not leverage their most valuable asset — their own customer data. LiveRamp made that data actionable, and the results were measurable improvements in targeting accuracy, campaign performance, and return on ad spend.

Competition emerged quickly. Oracle acquired BlueKai in 2014 and Datalogix in 2014, assembling its own data onboarding and identity stack. Neustar, Experian, and Epsilon all developed competing offerings. But LiveRamp maintained a crucial advantage: neutrality. Oracle was building a walled garden around its marketing cloud. Experian and Epsilon were data owners with their own agendas. LiveRamp, by contrast, positioned itself as the neutral infrastructure layer — it did not own data, did not compete with its customers, and did not favor one advertising platform over another. This "Switzerland positioning" became the company's defining strategic choice and, arguably, its most durable competitive advantage.

The Connectivity segment within Acxiom grew from $102 million in fiscal year 2016 to $147 million in fiscal 2017 and then $211 million in fiscal 2018 — roughly doubling in two years. LiveRamp was becoming Acxiom's crown jewel, a high-growth, high-margin technology platform trapped inside a low-growth, low-margin data services conglomerate. The tension between the two businesses would soon become unsustainable.

IV. The Spin-Off: Creating a Pure-Play Identity Company (2018)

By 2017, the mismatch between Acxiom's legacy marketing services business and its fast-growing LiveRamp platform had become impossible to ignore. The marketing services division — the core of old Acxiom — generated hundreds of millions in revenue but grew slowly, competed on price, and carried the stigma of being a "data broker" in an era of rising privacy consciousness. LiveRamp, by contrast, was growing at thirty to forty percent annually, commanded premium pricing, and was building genuine technology moats. Analysts covering Acxiom increasingly valued the two businesses separately, and the sum-of-the-parts math told a clear story: LiveRamp was worth more on its own than the entire combined company.

The catalyst came from an unexpected direction. In July 2018, Interpublic Group, the advertising holding company behind agencies like McCann and FCB, announced it would acquire Acxiom's legacy marketing solutions business for $2.3 billion. The deal was transformative. IPG wanted Acxiom's data assets and marketing services capabilities to power its own agencies' offerings. What IPG explicitly did not want was LiveRamp — the technology platform that connected data across the ecosystem, including to IPG's competitors. This was precisely the point. LiveRamp's value depended on its neutrality, and being owned by a major agency holding company would have destroyed that positioning overnight.

The transaction closed on October 1, 2018, and the remaining entity — the LiveRamp platform, its engineering team, and its customer relationships — became an independent public company. The corporate entity formally changed its name from Acxiom Holdings to LiveRamp Holdings, trading under the new ticker symbol RAMP. Scott Howe, who had served as Acxiom's CEO since 2011, stayed on to lead the newly independent company.

Howe's background shaped LiveRamp's strategic direction. Before joining Acxiom, he had spent over a decade at Microsoft, including a stint running the company's advertising business. He understood both the technology and the business dynamics of digital advertising at a deep level. His articulation of LiveRamp's mission — "data connectivity" rather than "data brokerage" — was not merely semantic. It reflected a genuine strategic repositioning away from owning or selling data and toward building the infrastructure that allowed others to activate their own data safely and effectively. In an industry increasingly suspicious of companies that profited from consumer data, the distinction mattered enormously.

The market's initial reaction was mixed. LiveRamp's first fiscal year as an independent company (ending March 2019) showed revenue of $286 million — a dramatic drop from Acxiom's $917 million the prior year, reflecting the divestiture. Investors struggled to value a company that was essentially middleware — critical but invisible, deeply technical but hard to explain in an elevator pitch. The stock experienced significant volatility, trading in a wide range as the market tried to determine what multiple to assign to a high-growth identity platform that was still burning cash.

The cash position, at least, was strong. The IPG transaction had left LiveRamp with a substantial cash balance and no debt, providing runway to invest aggressively in product development, sales, and international expansion. Howe used this freedom to double down on the vision: LiveRamp would not be a data company. It would be the connective tissue of the data economy.

V. GDPR, CCPA & The Privacy Reckoning (2018-2020)

The timing of LiveRamp's independence coincided with what many in the advertising industry remember as the Great Privacy Panic. On May 25, 2018, the European Union's General Data Protection Regulation went into effect, and the shockwaves were immediate and global.

GDPR fundamentally changed the rules of digital advertising in Europe and, by extension, anywhere that European data might flow. The regulation required explicit consent for data collection, gave consumers the right to access and delete their data, mandated data protection officers, and imposed fines of up to four percent of global revenue for violations. For an industry that had grown accustomed to hoovering up consumer data with minimal oversight, it was a reckoning.

The initial reaction in ad tech circles was something close to existential dread. LiveRamp, as a company whose entire business involved matching and connecting consumer data across systems, seemed particularly exposed. Analysts openly questioned whether the business model could survive in a consent-driven world. If consumers opted out of data sharing — as many European consumers promptly did — would there be anything left for LiveRamp to connect?

What happened next was one of the most consequential strategic pivots in recent ad tech history. Rather than retreating, LiveRamp leaned in. The company invested heavily in consent management infrastructure, built tools that allowed its customers to respect consumer preferences at every point in the data supply chain, and — most importantly — began shifting its identity framework away from cookies and device IDs toward authenticated identity. The logic was elegant: if the future of privacy meant that companies could only use data from consumers who had actively chosen to share it, then the most valuable data would come from logged-in, authenticated users who had explicitly consented to a relationship with a brand or publisher. Email addresses, customer accounts, and loyalty program memberships — the very types of first-party data that LiveRamp's technology was designed to connect — would become more valuable, not less.

This insight led to the development of the Authenticated Traffic Solution, or ATS, which became one of LiveRamp's most important products. ATS allowed publishers to recognize logged-in users on their websites and apps and connect those users — with their consent — to LiveRamp's identity graph. This meant that advertisers could reach authenticated audiences across the open web without relying on third-party cookies. For publishers, ATS offered a way to monetize their authenticated audiences at premium rates, reducing their dependence on Google and Facebook's walled gardens. For advertisers, it provided a privacy-compliant alternative to the increasingly unreliable cookie-based targeting they had relied on for two decades.

The California Consumer Privacy Act, which took effect on January 1, 2020, reinforced the trend. CCPA gave California residents the right to know what data companies collected about them, to delete that data, and to opt out of its sale. While less comprehensive than GDPR, it signaled that privacy regulation was coming to the United States, the world's largest advertising market. Companies that had been slow to adapt to GDPR suddenly needed compliance infrastructure for their domestic operations.

LiveRamp positioned itself as the privacy-forward alternative in an industry still dominated by companies with questionable data practices. The contrast was deliberate and strategic. While data brokers faced Congressional hearings and FTC investigations, LiveRamp's messaging emphasized consent, transparency, and consumer control. The company joined industry bodies, published privacy frameworks, and invested in a Chief Ethics Officer role — moves that burnished its reputation with enterprise customers in regulated industries.

The competitive shakeout was severe. Several smaller data onboarding and identity companies folded or were acquired. Oracle, which had spent billions assembling an advertising data stack through acquisitions, announced in June 2022 that it would shut down its advertising business entirely — a stunning capitulation that validated LiveRamp's bet that neutrality and privacy compliance would matter more than data ownership. The companies that survived and thrived in the post-GDPR landscape shared a common trait: they helped brands and publishers use their own first-party data more effectively, rather than trafficking in third-party data of dubious provenance.

For investors tracking this period, the critical insight was counterintuitive: privacy regulations, which initially appeared to threaten LiveRamp's business model, actually strengthened it. Complexity became a moat. Every new regulation, every new consent requirement, every new data governance mandate made it harder for companies to manage their data infrastructure in-house and increased the value of a trusted intermediary like LiveRamp. The companies that understood this distinction early — and LiveRamp was among them — emerged from the privacy reckoning in a stronger competitive position than they entered it.

VI. The Chrome Cookie Deprecation Saga (2020-Present)

In January 2020, Google dropped a bombshell that would reshape the digital advertising industry for years: Chrome, the world's dominant web browser, would phase out support for third-party cookies by 2022. The announcement was, in some ways, the culmination of a trend that Apple's Safari and Mozilla's Firefox had already embraced. But Chrome's roughly sixty-five percent market share made this different. When Chrome killed cookies, the entire infrastructure of open-web advertising — the targeting, the measurement, the attribution, the frequency capping — would break.

The industry's response was a mixture of panic and entrepreneurial frenzy. Third-party cookies had been the backbone of digital advertising for over two decades. They were the mechanism that allowed an advertiser to follow a consumer from one website to another, building a behavioral profile that could be used for targeting. They enabled the real-time bidding auctions that powered programmatic advertising. They were how brands measured whether someone who saw an ad subsequently visited their website or made a purchase. Removing them was not a minor technical adjustment — it was demolishing the foundation of a multi-hundred-billion-dollar industry.

What followed was a Cambrian explosion of "identity solutions." Dozens of companies launched alternative identifiers, each claiming to be the post-cookie answer. Some were based on email addresses, others on probabilistic fingerprinting, still others on contextual signals or cohort-based approaches. Google itself proposed the Privacy Sandbox, a collection of APIs that would move targeting and measurement capabilities into the browser itself, effectively making Google the gatekeeper of advertising functionality that had previously been distributed across the ecosystem.

LiveRamp's response was to double down on authenticated identity and its proprietary RampID. The company's argument was that the cookie had always been a flawed proxy — an anonymous, ephemeral, device-specific identifier that could not reliably represent a real person across devices, browsers, or channels. RampID, by contrast, was a people-based identifier derived from authenticated data, capable of recognizing the same person on their phone, their laptop, their connected TV, and their in-store purchase. The death of the cookie, in LiveRamp's framing, was not a crisis but a correction — a shift from anonymous surveillance to consented, authenticated relationships.

The competitive dynamics became particularly interesting with the emergence of Unified ID 2.0, an open-source identity framework championed by The Trade Desk, the largest independent demand-side platform. UID 2.0 was based on hashed and encrypted email addresses, conceptually similar to LiveRamp's approach but with a critical difference: it was open source and governed by a nonprofit, Prebid.org. The Trade Desk argued that identity infrastructure should be a public good, not a proprietary toll booth. LiveRamp argued that its proprietary approach offered superior privacy protections, better match rates, and deeper integrations.

The tension between these two visions — open-source identity infrastructure versus proprietary identity platform — became one of the defining strategic debates in ad tech. In practice, the two approaches proved more complementary than competitive. LiveRamp integrated with UID 2.0, allowing its customers to use both systems. The real threat to both was Google's Privacy Sandbox, which, if adopted, could have made third-party identity solutions irrelevant by moving all targeting and measurement into Chrome itself.

Then came the delays. Google pushed back its cookie deprecation timeline from 2022 to 2023. Then to 2024. Then to early 2025. Each delay reflected the immense technical and regulatory complexity of the transition, as well as the advertising industry's lack of readiness. The UK's Competition and Markets Authority raised concerns that the Privacy Sandbox would further entrench Google's dominance. Advertisers and publishers protested that the replacement APIs were not ready. Google found itself caught between privacy advocates demanding faster action and an industry begging for more time.

For LiveRamp, the delays were paradoxically beneficial. Each postponement extended the period of uncertainty during which companies needed to invest in alternative identity infrastructure. The urgency was real even if the deadline kept moving: Apple had already eliminated third-party cookies in Safari, and its App Tracking Transparency framework had devastated the mobile advertising ecosystem. Brands and publishers that waited for Google's final decision risked being caught unprepared. LiveRamp's sales pitch essentially became: "The cookie is dying. We do not know exactly when. But you need to be ready, and we can help you get there."

The result was a sustained period of investment in LiveRamp's platform. Publisher partnerships expanded significantly, with major media companies integrating ATS to build authenticated audiences. Brand advertisers invested in first-party data strategies that relied on LiveRamp's connectivity. The chaos of the cookie transition, rather than undermining LiveRamp's business, created a persistent demand for exactly the kind of identity infrastructure the company provided.

VII. The Architecture Play: Safe Haven & Clean Rooms (2019-Present)

While the cookie wars grabbed headlines, LiveRamp was quietly building what may prove to be the more enduring part of its business: data collaboration infrastructure.

The concept is straightforward, even if the technology is not. Imagine that a major automaker wants to understand which of its customers also shop at a particular retail chain, so it can target ads more effectively and measure whether its advertising drives in-store visits. Both the automaker and the retailer have rich customer databases, but neither is willing to share raw data with the other — for competitive reasons, privacy compliance, and simple corporate paranoia. A data clean room is a secure environment where both parties can bring their data, run analyses on the combined dataset, and receive aggregated insights without either party ever seeing the other's individual records. Think of it as a sealed laboratory where two scientists can collaborate on an experiment without either one seeing the other's proprietary formula.

LiveRamp launched its Safe Haven product in 2019 to address exactly this use case. Safe Haven allowed companies to run analytics, build audience segments, and measure campaign performance across combined datasets in a privacy-safe environment. The platform handled the identity matching (connecting the automaker's customers to the retailer's shoppers), the data governance (ensuring compliance with privacy regulations and contractual restrictions), and the computation (running the actual analyses in a secure enclave).

The timing was prescient. By 2021, "data clean rooms" had become one of the hottest categories in ad tech and marketing technology. Google launched its Ads Data Hub. Amazon built its Amazon Marketing Cloud. Snowflake, the cloud data warehouse company, introduced its Data Clean Room capabilities. AWS launched AWS Clean Rooms. The proliferation of clean room offerings validated LiveRamp's strategic direction but also raised a critical question: if every major cloud platform and walled garden was building its own clean room, where did LiveRamp fit?

LiveRamp's answer was interoperability. In a world where a brand might need to collaborate with data inside Google's clean room on Monday, Amazon's on Tuesday, Snowflake's on Wednesday, and a retail media network's on Thursday, someone needed to provide the connective layer that made all of these collaborations possible with a single identity framework and a consistent set of privacy controls. LiveRamp argued that its RampID and its partnerships across the ecosystem made it the only company that could serve as this universal translation layer.

The retail media explosion made this argument particularly compelling. Between 2020 and 2025, virtually every major retailer in the United States launched an advertising network — Walmart Connect, Target's Roundel, Kroger Precision Marketing, CVS Media Exchange, and dozens of others. Each of these networks sat on valuable first-party purchase data. Each wanted to allow brands to match their own customer data against the retailer's shopper data to measure ad effectiveness. And each needed clean room infrastructure to do this in a privacy-compliant way. LiveRamp became a preferred infrastructure partner for many of these networks, providing the identity matching and data governance that made retail media collaboration possible.

The moat question loomed large, however. Snowflake's clean room was built into the data platform that many enterprises already used. Google's clean room was integrated with the world's largest advertising ecosystem. Could LiveRamp's specialized identity infrastructure compete against platforms with vastly larger distribution and deeper pockets? The company's bet was that identity — the ability to accurately and privacy-safely match records across organizations — was the hardest and most valuable part of the clean room equation, and that generic data infrastructure providers would struggle to replicate the decades of identity resolution expertise embedded in AbiliTec and RampID. Whether that bet holds remains one of the central questions of LiveRamp's investment thesis.

VIII. Retail Media & The Bezos Problem (2020-Present)

The retail media revolution deserves its own moment in this story because it represents both LiveRamp's largest near-term growth opportunity and its most complex strategic challenge.

The numbers are staggering. Retail media advertising in the United States grew from roughly $13 billion in 2019 to an estimated $55 billion by 2025, making it the fastest-growing segment of digital advertising. The logic behind the boom is simple: retailers sit on something that Google and Meta do not — actual purchase data. They know what consumers bought, when they bought it, how much they paid, and whether they came back for more. This closed-loop measurement capability makes retail media extraordinarily attractive to brand advertisers who have long struggled to connect their digital ad spending to real-world sales.

Amazon pioneered this model, building Amazon Advertising into a roughly $50 billion business that now rivals Google and Meta. But Amazon's success inspired every other major retailer to launch its own media network, and this is where the opportunity gets interesting for LiveRamp. Amazon's advertising ecosystem is largely closed — brands that advertise on Amazon cannot easily connect their Amazon campaign data to their broader marketing efforts. The rest of the retail media landscape, however, is fragmented and in need of infrastructure.

Consider the challenge facing a major consumer packaged goods company like Procter & Gamble. P&G sells products through dozens of retailers, each with its own media network, its own data format, its own measurement methodology, and its own clean room. To run effective campaigns across Walmart Connect, Target Roundel, Kroger Precision Marketing, and Instacart Ads simultaneously, P&G needs a way to manage identity, audiences, and measurement consistently across all of these platforms. This is precisely what LiveRamp offers — the connective tissue that makes the fragmented retail media landscape manageable for large advertisers.

The Walmart partnership has been particularly significant. Walmart Connect, one of the largest non-Amazon retail media networks, integrated with LiveRamp's identity infrastructure to allow brands to match their customer data against Walmart's shopper data and measure campaign effectiveness. For LiveRamp, this partnership represented validation of its retail media strategy and a template for similar deals with other major retailers.

But the challenge is real. Every retailer building a media network faces a tension between openness and control. They want to attract brand advertising dollars, which requires making their platforms accessible and interoperable. But they also want to protect their competitive advantage, which means keeping their purchase data proprietary and preventing competitors from gaining insights into their business. LiveRamp's pitch — "let us be the neutral infrastructure that connects everything" — works well with some retailers and terrifies others. Retailers that fear becoming commoditized by a universal identity layer may resist integration. Those that lack the technical resources to build their own infrastructure may embrace it.

Revenue from retail media-related use cases grew meaningfully during this period, though LiveRamp does not break out retail media as a separate segment. The growth showed up in the Marketplace & Other revenue line, which expanded from $87 million in fiscal 2021 to $177 million in fiscal 2025. While not all of this growth was attributable to retail media, the segment's rapid expansion coincided with the retail media boom and reflected LiveRamp's deepening role in the ecosystem.

IX. The Business Model Evolution & Unit Economics

LiveRamp's business model underwent a fundamental transformation between 2018 and 2025, shifting from a transactional, volume-based approach to a subscription-driven platform model that more closely resembles enterprise software.

In the early days of data onboarding, LiveRamp charged primarily on a cost-per-thousand (CPM) basis — a fee for each thousand consumer records matched and activated. This model was simple and aligned with advertising industry norms, but it created volatile, unpredictable revenue tied to campaign volumes. A major brand might onboard ten million records for a holiday campaign and then go quiet for months. Revenue fluctuated with advertising cycles rather than growing steadily.

The shift to subscription pricing changed the economics dramatically. By fiscal 2025, subscription revenue accounted for $569 million of LiveRamp's total $746 million in revenue — roughly seventy-six percent of the business. Marketplace and other revenue, which includes data distribution and more transactional elements, contributed the remaining $177 million. The subscription model provided predictable, recurring revenue, improved customer retention (it is harder to cancel a platform subscription than to simply stop running campaigns), and aligned LiveRamp's economics more closely with the SaaS companies that commanded premium valuations in public markets.

The gross margin trajectory told an encouraging story. LiveRamp's gross profit margin expanded to approximately seventy-one percent in fiscal 2025, up from roughly sixty percent in fiscal 2020. This improvement reflected the increasing proportion of high-margin subscription revenue, better infrastructure utilization, and the operational leverage that comes with scaling a platform business. For context, best-in-class SaaS companies typically operate at seventy-five to eighty-five percent gross margins, suggesting LiveRamp still had room to improve but was moving in the right direction.

The bottom line, however, remained a sticking point for investors. LiveRamp generated a net loss of approximately $800,000 in fiscal 2025 — essentially breakeven, and a dramatic improvement from the $125 million loss in fiscal 2020 and the $90 million loss in fiscal 2021. Operating income turned slightly positive at $5.4 million in fiscal 2025, following $11.4 million in fiscal 2024. The company was clearly approaching profitability, but after years of losses, investors wanted to see sustained, convincing proof that the business model could generate consistent profits while maintaining growth.

The investment in research and development remained substantial. LiveRamp spent $177 million on R&D in fiscal 2025, representing about twenty-four percent of revenue — a level more typical of a high-growth software company than a mature infrastructure provider. Sales and marketing expenses consumed another $213 million, reflecting the reality that LiveRamp's product requires significant enterprise sales effort. The company was essentially reinvesting all of its gross profit back into growth, a strategy that made sense if the market opportunity was large and the competitive position was strengthening, but one that required patience from shareholders.

Stock-based compensation remained elevated at roughly fifteen percent of revenue in fiscal 2025, reflecting the competitive market for engineering talent in ad tech and data infrastructure. This was a meaningful ongoing cost that diluted shareholders, though it was trending downward as a percentage of revenue as the company scaled.

X. The Competitive Landscape & Market Structure

LiveRamp operates in one of the more complex competitive environments in technology, where the company's partners, customers, and competitors are often the same entities. Understanding this landscape requires thinking about several distinct categories of players, each with different motivations and capabilities.

The walled gardens — Google, Meta, and Amazon — represent LiveRamp's most important partners and its most dangerous potential competitors simultaneously. Each of these companies has built proprietary identity systems within their own ecosystems. Google knows who you are through your Gmail account and Chrome browser. Meta identifies you through Facebook and Instagram logins. Amazon recognizes you through your shopping account. Within their own walls, these companies do not need LiveRamp. But when a brand wants to connect its customer data to campaigns running across multiple walled gardens and the open web — which is the norm for major advertisers — LiveRamp's translation layer becomes essential. The walled gardens tolerate LiveRamp because it drives advertising spending to their platforms. But they could, at any time, decide to build competing connectivity solutions or restrict access to their ecosystems.

The Trade Desk's Unified ID 2.0 represented a philosophically different approach to the identity problem. Rather than building a proprietary identity graph, The Trade Desk championed an open-source framework that anyone could adopt. UID 2.0 was based on encrypted, hashed email addresses and governed by Prebid.org, an independent nonprofit. The Trade Desk argued that identity infrastructure should be a shared utility, not a proprietary toll booth controlled by any single company. For LiveRamp, UID 2.0 was both a competitive threat (it offered an alternative to RampID) and a potential complement (LiveRamp integrated with UID 2.0, allowing its customers to use both systems). The strategic tension was whether open-source identity would commoditize LiveRamp's core product or whether LiveRamp's superior matching accuracy, deeper integrations, and enterprise-grade privacy controls would maintain its premium positioning.

The cloud data platforms represented perhaps the most formidable long-term threat. Snowflake, Databricks, and Google BigQuery all launched clean room capabilities between 2021 and 2023. These platforms had massive existing customer bases, deep engineering resources, and the advantage of being the data infrastructure that enterprises already used. If a company stored its customer data in Snowflake, the argument for using Snowflake's built-in clean room — rather than extracting data and sending it to LiveRamp — was compelling from a simplicity and cost perspective. LiveRamp's counter-argument was that clean rooms without identity resolution were just secure databases, and that identity was the hard part that generic platforms could not easily replicate. This debate remained unresolved and was arguably the single most important strategic question for LiveRamp's long-term value.

A wave of startups — InfoSum, Habu (acquired by LiveRamp in 2024), Optable, and others — entered the clean room space with various approaches to privacy-safe data collaboration. LiveRamp's acquisition of Habu was particularly noteworthy, as it brought in technology that strengthened LiveRamp's ability to operate across multiple cloud environments and clean rooms — essentially making LiveRamp the interoperability layer rather than a standalone clean room provider.

The independence question was crucial. Agency holding companies like WPP, Publicis, and Omnicom had all invested in proprietary data and identity capabilities. Large brands were building in-house data teams. The question for LiveRamp was whether the trend toward in-housing would reduce demand for third-party infrastructure or whether the complexity of the ecosystem would make specialized infrastructure more valuable over time. History suggested the latter — few companies could afford to build and maintain the breadth of integrations that LiveRamp offered — but the risk of disintermediation by large, well-resourced customers was real.

XI. Inflection Point: Connected TV & Streaming Wars (2021-Present)

If retail media represented LiveRamp's most immediate growth opportunity, connected television may represent its most transformative one. The shift from linear television to streaming fundamentally changed the advertising model for the largest advertising medium in history, and it created a set of identity challenges that were tailor-made for LiveRamp's capabilities.

Traditional television advertising was bought and sold on demographics — age, gender, household income — with relatively crude targeting. A car commercial aired during a football game because the audience skewed male, twenty-five to fifty-four, with above-average household income. There was no way to target individual households, no way to know whether someone who saw the ad subsequently visited a dealership, and no way to frequency-cap across networks. The measurement was based on panel-based ratings from Nielsen, a system that was accurate at scale but imprecise at the individual level.

Connected television changed all of this. When advertising arrived on Netflix in November 2022, on Disney+ around the same time, and across Amazon Prime Video in January 2024, the streaming platforms could theoretically offer the same kind of data-driven, audience-level targeting that digital display advertising had provided for years. But there was a catch: the identity infrastructure was not ready.

The complexity of TV identity was significantly greater than web or mobile advertising. Television is a household medium — multiple people watch the same screen. Unlike a phone or laptop, which is typically associated with a single user, a connected TV might be watched by parents in the evening and children in the afternoon. Identifying which household member was watching at any given time required a combination of deterministic data (who logged into the streaming app), contextual signals (what was being watched suggested the likely viewer), and probabilistic modeling. LiveRamp's identity graph, with its foundation in household-level data from Acxiom's decades of offline identity resolution, was well-suited to this challenge.

LiveRamp partnered with television manufacturers, streaming platforms, measurement companies, and multichannel video programming distributors to build identity infrastructure for the CTV ecosystem. These partnerships aimed to enable advertisers to target specific audience segments on streaming platforms, measure the effectiveness of their campaigns against real business outcomes, and manage frequency across linear and streaming TV. The vision was ambitious: a unified identity layer that allowed an advertiser to reach the same household with a coordinated message across Netflix, Hulu, live sports on YouTube TV, and traditional cable, all while respecting privacy preferences and consent requirements.

The opportunity was enormous but the execution was uncertain. CTV advertising spending in the United States was estimated at roughly $30 billion in 2025 and growing rapidly. But the streaming platforms themselves were building proprietary identity and targeting capabilities, potentially reducing the need for third-party infrastructure. Netflix, Amazon, and Disney all had strong logged-in user bases and were investing in their own advertising technology stacks. Whether they would partner with LiveRamp for interoperability or build walled gardens that excluded third-party identity providers remained an open question — one that would significantly influence LiveRamp's growth trajectory in the coming years.

XII. International Expansion & Regulatory Divergence

LiveRamp's international footprint tells a story of ambition tempered by the harsh realities of regulatory complexity and local market dynamics.

In fiscal year 2023, the most recent year with detailed geographic disclosure, the United States accounted for approximately $556 million of LiveRamp's $597 million in revenue — roughly ninety-three percent. Europe contributed about $32 million, and Asia Pacific just $7.5 million. For a company that positioned itself as global identity infrastructure, the concentration was striking.

The European challenge was fundamentally about GDPR. The regulation's strict consent requirements and aggressive enforcement created a more conservative data culture across the continent. Advertising technology that was standard practice in the United States — deterministic matching, cross-site tracking, even basic audience targeting — faced significant legal scrutiny in Europe. LiveRamp operated in Europe and had adapted its products to comply with GDPR, but the addressable market was smaller and the sales cycle was longer. European publishers and advertisers were more cautious about data partnerships, and the regulatory environment created uncertainty that chilled investment.

The Asia-Pacific region presented different challenges. China's internet operated behind regulatory and technical barriers that made Western ad tech infrastructure largely irrelevant. India, the fastest-growing major digital advertising market, had its own regulatory framework taking shape and a competitive landscape dominated by local players. Japan and Australia offered pockets of opportunity but at modest scale relative to the US market.

The international revenue numbers had actually declined significantly from the pre-divestiture Acxiom days, when European revenue alone exceeded $65 million. This reflected the fact that much of Acxiom's international business had gone to IPG in the 2018 transaction. LiveRamp was essentially rebuilding its international presence from a smaller base, with the added complexity of navigating an increasingly fragmented global regulatory landscape.

For investors, the international situation presented a classic strategic tradeoff. Expanding internationally would diversify revenue and expand the total addressable market, but it required significant investment in regulatory compliance, local partnerships, and adapted products. Staying focused on the US market — where LiveRamp had dominant market share and where the regulatory environment, while evolving, was more permissive — might generate better near-term returns but would limit long-term growth potential.

XIII. Porter's Five Forces & Market Dynamics

Understanding LiveRamp's competitive position requires looking at the structural forces shaping its industry.

The threat of new entrants into LiveRamp's market is higher than one might expect for a company with twenty-plus years of identity data. Clean room technology, at its core, is not technically exotic — it involves secure computation, data matching, and privacy controls that are well-understood by competent engineering teams. Cloud platforms like Snowflake and Databricks entered the space relatively quickly, leveraging their existing data infrastructure and customer relationships. What protects LiveRamp is not the difficulty of building a clean room but the difficulty of replicating its identity graph and its web of integrations. AbiliTec contains deterministic identity links built over decades, and LiveRamp maintains hundreds of direct integrations with advertising platforms, publishers, data providers, and technology partners. A new entrant would need years to build comparable connectivity, during which time LiveRamp's network effects would continue to compound.

The bargaining power of buyers is meaningfully high and represents a persistent pressure on LiveRamp's business. The company's customer base includes some of the largest companies in the world — agency holding companies, major brands, and technology platforms — all of which have significant negotiating leverage. The top customers likely account for a meaningful share of revenue, though the exact concentration figures are not publicly disclosed with granularity. High switching costs once integrated provide some buffer against price pressure, but the emergence of alternative solutions from cloud platforms and open-source projects gives large buyers credible alternatives to reference in negotiations.

The threat of substitutes is the force that keeps LiveRamp's investors up at night. Cloud-based clean rooms from Snowflake, Databricks, and Google BigQuery offer data collaboration capabilities that overlap significantly with LiveRamp's Safe Haven product. The Trade Desk's UID 2.0 provides an open-source alternative to RampID for identity resolution. Large enterprises with sophisticated data teams can potentially build in-house identity solutions. And the walled gardens — Google, Meta, Amazon — can bypass third-party infrastructure entirely within their own ecosystems. Each of these substitutes addresses a different piece of LiveRamp's value proposition, and their collective presence creates meaningful commoditization pressure.

Competitive rivalry within the identity and data collaboration space is intense but nuanced. The market is growing rapidly, which means the competition is not purely zero-sum — there is room for multiple winners. But the fragmentation of approaches (proprietary graphs, open-source IDs, cloud clean rooms, walled garden solutions) creates confusion for buyers and makes it difficult for any single player to establish dominance. Price pressure from free or low-cost alternatives (UID 2.0 is open source; cloud clean rooms are often bundled with existing data platform subscriptions) constrains LiveRamp's pricing power, even as its premium positioning and superior matching accuracy justify higher prices for enterprise customers.

The supplier landscape is the one area where LiveRamp faces relatively favorable dynamics. The company does not depend on unique data suppliers — its identity graph is built from publicly available records, customer-contributed data, and its own matching algorithms. Cloud computing infrastructure is widely available from multiple providers. The primary supply constraint is talent: LiveRamp competes for privacy engineers, data scientists, and ad tech specialists with companies that can offer significantly higher compensation, including Google, Meta, and well-funded startups.

XIV. Hamilton's Seven Powers & Strategic Moat Assessment

Applying Hamilton Helmer's Seven Powers framework to LiveRamp reveals a company with real but contestable advantages — a business that has built meaningful barriers to competition but faces genuine questions about whether those barriers will prove durable.

LiveRamp's scale economies are moderate. The company's infrastructure costs do scale reasonably well — adding a new customer to the identity graph does not require proportional increases in computing or storage. The identity graph itself becomes more accurate and valuable as more data flows through it, creating a form of data-driven scale advantage. However, LiveRamp is not a pure software company with near-zero marginal costs. Its gross margins of around seventy-one percent are strong but not exceptional, and the heavy investment required in sales, engineering, and compliance limits the operating leverage that pure scale would otherwise provide.

The network effects are LiveRamp's strongest power and deserve careful examination. LiveRamp operates a two-sided network: more brands using the platform make it more attractive to publishers (more advertising demand), and more publishers using the platform make it more attractive to brands (more addressable inventory). Additionally, more data flowing through the identity graph improves matching accuracy, which makes the platform more valuable for everyone. These network effects are real and measurable — LiveRamp's match rates improve as its graph expands, and its integration network creates genuine ecosystem stickiness. However, unlike a social network or marketplace where one dominant platform tends to emerge, the identity space allows multiple graphs to coexist. Brands routinely use LiveRamp alongside UID 2.0 and walled garden identity systems. The network effects are meaningful but not winner-take-all.

Counter-positioning is LiveRamp's weakest power. The concept holds that an incumbent's existing business model prevents it from adopting a challenger's approach. In LiveRamp's case, the walled gardens could theoretically build neutral identity infrastructure similar to LiveRamp's, but doing so would conflict with their incentive to keep data within their own ecosystems. This provided some protection historically. However, cloud platforms like Snowflake face no such conflict — they can add clean room and identity capabilities without cannibalizing existing revenue. As cloud platforms increasingly incorporate identity features, LiveRamp's counter-positioning advantage narrows.

Switching costs represent LiveRamp's most tangible near-term defense. Integrating LiveRamp's platform into an enterprise's data infrastructure is a significant undertaking involving technical integration with dozens of internal and external systems, training for data and marketing teams, development of custom workflows and audience strategies, and establishment of governance and compliance frameworks. Once embedded, the cost and disruption of switching to an alternative are substantial. Enterprise customers frequently report that LiveRamp is deeply woven into their day-to-day operations, creating genuine lock-in. The durability question is whether commoditization of clean rooms and identity tools could reduce these switching costs over time by standardizing interfaces and making migrations easier.

LiveRamp's brand power is moderate and context-dependent. Within the ad tech industry, LiveRamp is widely recognized as the trusted neutral party — the "Switzerland" that competitors can safely integrate with. This reputation has real commercial value, particularly with privacy-conscious enterprise customers in regulated industries. However, LiveRamp has no consumer brand, and B2B brands in technology tend to be less durable than consumer brands — they can erode quickly if product quality declines or if a competitor achieves comparable trust.

The cornered resource analysis centers on AbiliTec, LiveRamp's proprietary identity graph built over decades of data accumulation and refinement. AbiliTec contains deterministic identity links that would take years to replicate, giving LiveRamp a meaningful head start in matching accuracy. However, this advantage is slowly eroding as competitors build their own graphs using alternative data sources and as AI-powered identity resolution techniques improve. The graph's value lies not in any single data point but in the accumulated connections between identifiers — a form of institutional knowledge that is difficult but not impossible to replicate.

Process power — the ability to execute complex operations that competitors struggle to match — is moderate. LiveRamp's operational expertise in privacy compliance, data governance, and cross-platform integration represents genuine organizational capabilities built over years of experience. The company manages data flows across hundreds of partners while maintaining compliance with dozens of regulatory frameworks — an operationally complex task that requires institutional knowledge, established processes, and trained personnel. Well-resourced competitors could eventually build comparable processes, but doing so would take time and significant investment.

The overall assessment suggests that LiveRamp's moat is real but time-limited. Switching costs and network effects provide meaningful near-term defensibility, likely measured in three-to-five-year horizons. But long-term durability depends on continuous execution: maintaining the identity graph's accuracy advantage, expanding the integration network faster than competitors, and delivering enough differentiated value that customers resist the pull of cheaper or more convenient alternatives from cloud platforms.

XV. Bull vs. Bear Case

The bull case for LiveRamp rests on a simple but powerful structural argument: the digital advertising industry is undergoing a once-in-a-generation infrastructure transition, and LiveRamp owns critical middleware.

Privacy regulations are proliferating globally, with no sign of reversal. GDPR, CCPA, Virginia's VCDPA, Colorado's CPA, and similar laws in Brazil, India, and elsewhere are creating permanent demand for privacy-compliant data infrastructure. Each new regulation increases the complexity of managing consumer data across borders and platforms, making specialized intermediaries like LiveRamp more valuable. The regulatory trend is LiveRamp's friend — not because regulations help LiveRamp directly, but because they raise the cost and complexity of doing what LiveRamp does in-house.

The cookie deprecation, whenever it finally arrives in Chrome, would accelerate the shift toward authenticated identity and first-party data strategies — precisely the capabilities that LiveRamp has spent years building. Even if Google delays indefinitely, the broader trend toward privacy-first advertising is clear. Apple's moves in Safari and iOS have already demonstrated the impact, and the advertising industry is adapting regardless of Google's timeline.

Retail media and connected television represent massive total addressable market expansions. These are not incremental opportunities but fundamental restructurings of how advertising works in the two largest media channels. LiveRamp's positioning as the connective tissue for fragmented retail media networks and CTV platforms puts it at the center of multi-billion-dollar market shifts.

The bull case sees cloud platforms as partners rather than existential threats. In this view, Snowflake and Databricks provide the data infrastructure while LiveRamp provides the specialized identity and connectivity layer on top — much as Twilio provides communications infrastructure on top of cloud platforms without being displaced by them. LiveRamp's acquisition of Habu in 2024 strengthened this positioning by enabling LiveRamp to operate across multiple cloud environments rather than competing with any single one.

The path to profitability is visible. Revenue grew from $286 million in fiscal 2019 to $746 million in fiscal 2025 — a compound annual growth rate of roughly seventeen percent. Gross margins expanded from fifty-eight percent to seventy-one percent over the same period. Operating losses narrowed from $198 million to near breakeven. If revenue continues growing at low-to-mid teens while operating expenses grow more slowly, the company should achieve sustained profitability — unlocking significant operating leverage from its high-margin subscription base.

The bear case is equally compelling and centers on commoditization risk.

Open-source alternatives like UID 2.0 provide identity resolution capabilities at no cost, potentially undermining LiveRamp's pricing power for its core identity product. If identity becomes a commodity — a standard, interchangeable utility rather than a differentiated product — LiveRamp's premium positioning erodes.

Cloud clean rooms from Snowflake, Databricks, and Google BigQuery are rapidly adding capabilities that overlap with LiveRamp's Safe Haven product. These platforms have massive distribution advantages — their clean rooms are already integrated into the data infrastructure that enterprises use daily. A CISO or CTO evaluating whether to adopt LiveRamp's standalone product or simply enable clean room features in their existing Snowflake instance faces a straightforward comparison that often favors the integrated solution.

The walled gardens represent a persistent threat of vertical integration. Google, Meta, and Amazon collectively control the majority of digital advertising spending. If any of them decides to restrict access to their ecosystem for third-party identity providers, LiveRamp loses a significant portion of its value. Google's Privacy Sandbox, though delayed and modified, represents exactly this kind of vertical integration play — moving identity and targeting capabilities inside the browser and reducing the need for external infrastructure.

The company has never achieved sustained, meaningful profitability. After seven years as an independent company, LiveRamp has generated cumulative operating losses of hundreds of millions of dollars. While the trajectory has improved dramatically, the business has not yet proven it can generate consistent profits while continuing to invest in growth. This is the "investment treadmill" risk — the fear that maintaining competitive parity will require perpetual reinvestment that prevents profits from materializing.

For investors tracking LiveRamp's ongoing performance, two metrics deserve close attention above all others. First is net revenue retention — the rate at which existing customers increase their spending over time. This metric captures both the stickiness of the platform (are customers staying?) and the expansion potential of the business model (are they buying more?). A net retention rate consistently above one hundred and ten percent would indicate that the business is compounding from within its existing customer base, reducing the pressure on new customer acquisition. Second is subscription revenue growth rate, which measures the health of LiveRamp's highest-quality revenue stream and the pace of the transition from transactional to recurring economics. Sustained double-digit subscription growth with expanding margins would validate the platform thesis; deceleration would suggest competitive pressure or market saturation.

XVI. The Strategy Tax & Organizational Challenges

Every company pays a strategy tax — the hidden costs of its historical decisions, cultural inheritance, and organizational structure. For LiveRamp, that tax has several distinct components.

The Acxiom legacy cuts both ways. On the positive side, LiveRamp inherited AbiliTec, decades of identity resolution expertise, deep relationships with enterprise customers in regulated industries, and an organizational culture that understood data governance before it became fashionable. On the negative side, the Acxiom brand carried baggage. "Data broker" was a term of art in the industry but a term of suspicion in public discourse. Congressional hearings, FTC investigations, and media exposés about the data brokerage industry tarred all participants with the same brush, regardless of their actual practices. LiveRamp spent considerable effort distancing itself from the data broker label, emphasizing that it connected data rather than selling it. The rebranding was strategically necessary but could never fully erase the historical association.

Scott Howe's leadership provided strategic consistency during a period of enormous transformation. Having served as CEO since 2011 — first of Acxiom, then of the renamed LiveRamp — Howe brought continuity to a business that underwent a radical transformation from data conglomerate to identity platform. His background at Microsoft gave him credibility with both technology buyers and Wall Street, and his articulation of the "data connectivity" vision was clear and consistent. The leadership team around him, including CFO Lauren Dillard and CTO Mohsin Hussain, brought a mix of financial discipline and technical depth.

The tension between growth investment and profitability pressure was a constant theme. Public market investors, particularly after the SaaS downturn of 2022, increasingly demanded that technology companies demonstrate a path to profitability. LiveRamp responded by rationalizing spending, reducing headcount, and improving operational efficiency — moves that brought the company to near breakeven in fiscal 2025 but that also risked slowing the pace of innovation and market expansion.

Selling infrastructure rather than outcomes remained LiveRamp's most persistent go-to-market challenge. Brands and agencies understood the value of better-performing ad campaigns. They understood the value of higher conversion rates. What they often struggled to grasp was the value of a more connected identity graph or a more interoperable clean room infrastructure. LiveRamp's sales team had to translate technical infrastructure capabilities into business outcomes — showing customers not what LiveRamp did but why it mattered for their bottom line. This required sophisticated, consultative selling that was expensive and time-consuming, contributing to the company's high sales and marketing costs.

XVII. What's Next: AI, Privacy, & the Future of Identity

The emergence of generative AI as a transformative force in technology has implications for LiveRamp that are simultaneously exciting and unsettling.

On the opportunity side, AI-powered advertising is likely to increase demand for data infrastructure. Generative AI can create personalized ad creative at scale, optimize media buying in real time, and generate sophisticated audience insights from complex datasets. All of these capabilities require high-quality, well-connected data as input. If AI makes advertising more sophisticated, it should increase the value of the identity and data connectivity infrastructure that LiveRamp provides. More sophisticated advertising means more demand for precise targeting, measurement, and attribution — all of which depend on accurate identity resolution.

On the threat side, AI could potentially commoditize identity resolution itself. Machine learning techniques are increasingly capable of matching records across datasets without the carefully curated, rules-based matching that has been AbiliTec's historical advantage. If an enterprise data team can achieve comparable matching accuracy using off-the-shelf AI models running on their own data, the value of LiveRamp's proprietary graph diminishes. This is a medium-to-long-term risk rather than an immediate threat — AI-powered matching today still struggles with the edge cases and regulatory nuances that LiveRamp handles well — but it is directionally concerning.

The privacy pendulum continues to swing, and where it settles will significantly influence LiveRamp's trajectory. The maximalist position — that all consumer tracking should be eliminated and advertising should return to contextual targeting based on content rather than audience — would be devastating for LiveRamp and the entire identity infrastructure sector. The pragmatic position — that consumers should have meaningful control over their data but that consented, transparent data usage should be permitted — favors LiveRamp's model. Regulatory developments in the US, EU, and elsewhere will determine which position prevails.

First-party data strategies are maturing across the enterprise landscape. Major brands and publishers have invested heavily in collecting, organizing, and activating their own customer data. As these strategies mature, the question is whether companies will need more or less third-party infrastructure. LiveRamp's argument is "more" — that as first-party data becomes more valuable, the need to connect it across partners, platforms, and channels increases. The counterargument is that sophisticated first-party data owners may internalize capabilities they currently outsource to LiveRamp.

The question of whether LiveRamp is ultimately an acquirer or a target hangs over the company. At a market capitalization of approximately $1.8 billion, LiveRamp is large enough to be a meaningful acquisition for a strategic buyer — a cloud platform wanting to add identity capabilities, an agency holding company seeking technology infrastructure, or a private equity firm attracted to the recurring revenue base and the potential for margin expansion. The company has shown willingness to acquire, as evidenced by the Habu deal, but its relatively modest size in the context of the broader technology industry makes it a plausible target as well.

The consolidation dynamics in ad tech more broadly suggest that the middle ground where LiveRamp operates — too large to be a startup, too small to be a platform — is an uncomfortable position. Companies in this zone either need to grow into platforms themselves, find a larger home through acquisition, or demonstrate such compelling profitability and defensibility that they justify independent existence. LiveRamp's next few years will likely determine which of these paths it follows.

XVIII. Epilogue & Reflection

At the heart of the LiveRamp story is a tension that runs through much of modern technology: the challenge of building neutral infrastructure in a world that rewards vertical integration.

Every era of technology has produced companies that positioned themselves as the connective layer — the middleware, the plumbing, the picks-and-shovels provider. Some of these companies became enormously valuable and enduring. Visa and Mastercard built payment infrastructure that neither merchants nor banks wanted to build themselves. Twilio built communications infrastructure that allowed developers to add messaging and voice to their applications. Stripe built payments infrastructure for the internet economy. Others saw their middleware position eroded as platforms above and below them absorbed their functionality.

LiveRamp's bet is that identity — the ability to accurately, safely, and privacy-compliantly connect data about people across the fragmented digital ecosystem — is a problem complex enough and sensitive enough that no single platform will dominate, and that a trusted, neutral intermediary will remain essential. The evidence for this bet is compelling: the advertising ecosystem is more fragmented than ever, with dozens of walled gardens, hundreds of publishers, thousands of data providers, and millions of brands all needing to interoperate. The evidence against it is equally compelling: the cloud platforms that enterprises already depend on are adding identity and clean room capabilities that could commoditize LiveRamp's core product.

The lessons from this story are relevant far beyond ad tech. For founders: the power of positioning as neutral infrastructure is real but fragile. LiveRamp's "Switzerland" strategy gave it access to every corner of the ecosystem, but it requires constant vigilance to maintain credibility. The moment one large partner perceives LiveRamp as favoring a competitor, the entire positioning unravels. For investors: moats in middleware are real but time-bounded. Switching costs and network effects provide protection today, but they must be continuously reinforced through product innovation, partnership expansion, and demonstrated value. The commoditization risk is not theoretical — it is already visible in the proliferation of cloud-based clean rooms and open-source identity solutions.

What remains uncertain — and what makes this a story worth following — is whether the macro tailwinds that have buoyed LiveRamp over the past several years (privacy regulations, cookie deprecation, retail media, CTV) will prove powerful enough to overcome the headwinds of commoditization and platform competition. The company has navigated extraordinary change with strategic clarity and operational discipline, transforming from a division of a legacy data broker into a standalone identity platform with approaching three-quarters of a billion dollars in revenue. Whether the next chapter of the story involves continued independence, acquisition, or disruption depends on execution, timing, and the unpredictable evolution of an industry in which the rules seem to change every year.

XIX. Further Reading & Resources

Top 10 Resources:

-

Scott Howe's shareholder letters and earnings call transcripts (2018-2025) — the clearest articulation of LiveRamp's strategic evolution through the spin-off and beyond.

-

"The Attention Merchants" by Tim Wu — essential context on the history of advertising and the attention economy that LiveRamp's infrastructure supports.

-

GDPR and CCPA regulatory texts — the privacy frameworks that transformed LiveRamp's business from threatened to strengthened.

-

The Trade Desk's UID 2.0 documentation — the open-source alternative that represents both competitive threat and philosophical counterpoint to LiveRamp's proprietary approach.

-

Snowflake and Databricks clean room documentation — understanding the technical competitive threat from cloud data platforms requires familiarity with their capabilities.

-

AdExchanger and Digiday coverage of LiveRamp and the identity landscape — the ad tech trade press provides the most current and detailed coverage of competitive dynamics.

-

LiveRamp's privacy and security documentation and its Data Ethics and Privacy practices — understanding the technical architecture and governance frameworks that underpin the company's trust positioning.

-

FTC data broker reports and Congressional testimony — the regulatory risk context that every investor in identity infrastructure should understand.

-

"Subprime Attention Crisis" by Tim Hwang — a critical examination of the ad tech infrastructure that LiveRamp operates within, raising questions about the fundamental value of digital advertising.

-

Amazon, Walmart, and major retailer earnings calls discussing retail media — the growth opportunity analysis for LiveRamp's most important near-term market expansion.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube