Regional S.A.B. de C.V.: The Banking Dynasty of the Monterrey Corridor

I. Introduction & Episode Roadmap

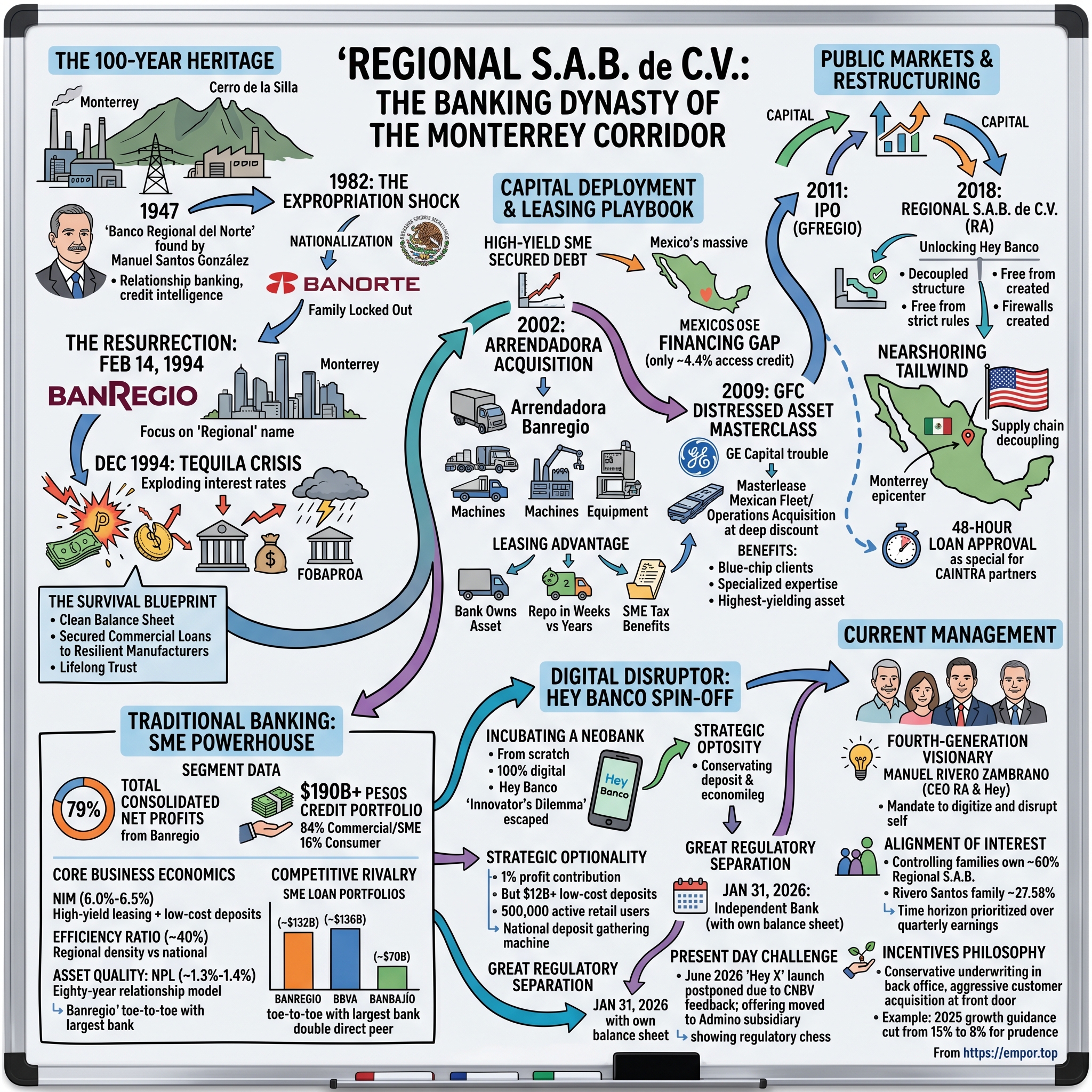

Picture the industrial valley of Monterrey at dawn. The Cerro de la Silla — that saddle-shaped mountain that every Regiomontano uses as a compass — catches the first light, and below it stretch mile after mile of factory floors, cement plants, steel mills, glass furnaces, and the loading docks of companies whose names anchor Mexico's entire industrial economy. This is the most productive square mileage in Latin America, a place where family-owned manufacturers have been forging fortunes for over a century. And quietly, threaded through nearly every one of those factories, sits a bank that most people outside northern Mexico have never heard of.

Here is the puzzle that makes Regional S.A.B. de C.V. one of the most fascinating businesses in emerging-market finance. How did a mid-sized, family-controlled regional bank — headquartered not in Mexico City but in the leafy, affluent suburb of San Pedro Garza García — build a small-and-medium-enterprise lending franchise that, in absolute peso terms, rivals the SME book of BBVA, the largest bank in the entire country? And how did it do that while throwing off a Return on Equity of 19% to 21%, year after year, in an industry where most banks would kill for a steady 15%?1

The answer is not a single trick. It is the story of Regional S.A.B. de C.V., the publicly listed holding company that today owns two very different banking children: Banregio, the century-rooted commercial bank that finances the factories of the north, and Hey Banco, one of Latin America's fastest-growing digital neobanks, which in 2026 went off and got its own banking license. It is the story of a banking dynasty that reaches back nearly eighty years, that was expropriated by the Mexican state, shut out of the institution it helped found, and then clawed its way back into existence on Valentine's Day, 1994 — only to be tested ten months later by one of the worst financial crises in modern history.

It is also a story riding one of the largest macroeconomic waves on the planet: nearshoring, the great decoupling of global supply chains from Asia, which has turned northern Mexico into the workshop of North America. Regional sits directly at the epicenter of that wave.

So here is our agenda. We will trace the family legacy from the 1947 founding through the trauma of nationalization. We will watch Banregio survive the 1994 Tequila Crisis when giants around it collapsed. We will study the genius of their leasing playbook and the GE Capital distressed-asset masterclass of 2009. We will walk through the 2011 IPO and the clever 2018 corporate restructuring that set up everything to follow. We will go deep — segment by segment — on the SME lending engine that is the real crown jewel here. We will examine the high-stakes spin-off of Hey Banco into an independent bank. We will meet the fourth-generation CEO running the whole show. And we will war-game the competition, the moat, the bull case, and the bear case. Let's get into it.

II. The Hundred-Year Heritage: From Expropriation to the Resurrection of February 14, 1994

To understand why the people of Monterrey trust this bank with a kind of loyalty that money cannot buy, you have to start in the late 1940s, in a Mexico that was just beginning to industrialize. Monterrey was already different from the rest of the country — a city of foundries and brewers and cement makers, of families who built empires out of steel and glass and beer, of a self-reliant business culture that prided itself on getting things done without waiting for Mexico City. Those families needed capital, and they preferred to get it from people who understood their world.

In 1947, a banker named Manuel Santos González — the patriarch and grandfather of the leaders who run Regional today — co-founded Banco Regional del Norte in Monterrey, built precisely to finance the region's surging base of industrial conglomerates.[^4] This was relationship banking in its purest form. The bankers knew the factory owners by name. They knew which families paid their debts and which cut corners. They knew, walking through an industrial park, whose business was about to boom and whose was quietly failing. That tacit, on-the-ground credit intelligence would become, generations later, the very heart of the franchise.

For three and a half decades, the bank grew alongside the Monterrey industrial machine. And then, on September 1, 1982, it all vanished in a single afternoon.

The Expropriation Shock

President José López Portillo, in the final months of a presidency wrecked by a debt and currency crisis, stood before the nation and nationalized the entire private banking system. Every private bank in Mexico became, overnight, property of the state. For the Santos and Rivero families, it was the confiscation of a life's work — the institution their family had built to serve their neighbors was simply taken. In the forced consolidations that followed, Banco Regional del Norte was folded together with Banco Mercantil de Monterrey to form a new entity: Banco Mercantil del Norte, which the world now knows as Banorte.[^4] The cruel irony is hard to overstate. The family helped lay the foundation of what would become one of Mexico's largest banks — and then found themselves locked out of it entirely, shareholders of nothing, watching from the sidelines.

That decade in exile from their own profession shaped everything. When you lose something to a stroke of a government pen, you learn in your bones what conservatism and a clean balance sheet are actually worth.

The Comeback

The wheel turned again under President Carlos Salinas de Gortari, who in the early 1990s re-privatized the banking system he had inherited. The door cracked open. Brothers Manuel and Jaime Rivero Santos — the third generation of the family — moved to walk back through it. They secured a banking license, and on February 14, 1994, they opened the doors of Banco Regional de Monterrey, which everyone would come to call Banregio.[^4]

The name itself was a statement of intent. They deliberately resurrected the word "Regional" — reclaiming the brand, the heritage, and the implicit promise that they were once again the trusted local partner of Monterrey's business owners, the bankers who belonged to the same community as their clients. After twelve years of being shut out, the family was back in the arena under a name that announced exactly who they were.

Baptism by Fire

They had roughly ten months to enjoy it before the world fell apart.

In December 1994, the newly inaugurated administration of President Ernesto Zedillo devalued the peso, and the currency went into freefall. What followed became known as the Crisis del Tequila — the Tequila Crisis — and it nearly destroyed the entire Mexican banking system. Interest rates exploded. Borrowers who had taken loans in a stable-peso world suddenly owed amounts they could never repay. Across the freshly privatized banking sector, loan books rotted from the inside out as bad debt metastasized.[^14] The government's eventual response, the controversial bailout vehicle FOBAPROA (Fondo Bancario de Protección al Ahorro), absorbed hundreds of billions of pesos in toxic loans and became a political scandal that haunted Mexico for years.

The titans of the industry — banks that had paid enormous prices in the privatization auctions and then lent aggressively into the consumer boom — were gutted. Many were absorbed, recapitalized by foreign buyers, or simply ceased to exist as independent institutions.

The Survival Blueprint

So how did a ten-month-old bank survive a storm that drowned giants?

The answer is almost paradoxically simple, and it reveals the entire strategic DNA of the company. First, Banregio was too new and too small to have accumulated the toxic pile of consumer credit-card and mortgage debt that destroyed its larger rivals. It had not had time to make the mistakes that killed everyone else. Second, the family — scarred by 1982 — ran a deliberately clean, conservative balance sheet. And third, and most importantly, they stuck rigidly to what they knew: secured, middle-market commercial loans to the resilient manufacturing businesses of Nuevo León, lending against hard assets to companies whose owners they personally knew.[^14]

When the dust settled, Banregio stood as one of the rare, genuinely admired survival stories of the Tequila Crisis. And that survival bought something that does not appear on any balance sheet: the lifelong trust of the local industrial families, who watched their regional bank weather a storm that took down the national champions. That trust would compound for the next thirty years — and it is the first stone in a moat we'll spend the rest of this episode mapping. But trust alone does not generate a 20% ROE. For that, the family needed a weapon. They found it in leasing.

III. Capital Deployment & The Leasing Playbook: The GE Capital Masterclass

Here is a problem that every regional bank in the world eventually confronts. You are not the biggest player. You cannot win the volume game against national giants who can fund themselves more cheaply and spread fixed costs across a hundred million customers. If you try to compete head-to-head on plain-vanilla loans, you will be ground down. So you need to be different — and specifically, you need to find a product that is high-yield, low-risk, and that the giants are structurally bad at offering. For Banregio, that product was leasing.

The Pivot to High-Yield SME Secured Debt

Start with the size of the prize. Mexico has a staggering financing gap for small and medium enterprises — the PyMEs that form the backbone of the economy. By most estimates only around 4.4% of Mexican SMEs have access to formal bank credit.[^10] Read that number again. More than 95 out of every 100 small businesses in one of the world's larger economies cannot get a normal bank loan. That is not a market failure to be lamented; for a disciplined lender, it is the single greatest pricing opportunity in Mexican finance. When supply is that scarce, the lender, not the borrower, sets the terms — and good businesses will happily pay healthy yields for fast, reliable credit.

But the obvious objection is: if these businesses are so hard to lend to, isn't that because they're risky? Yes. Which is exactly why the structure of the loan matters more than the borrower's credit score. And leasing is the most elegant structure ever devised for this problem.

The Arrendadora Acquisition

In 2002, Banregio deployed capital to acquire Arrendadora Financiera del Norte, rebranding it as Arrendadora Banregio and turning it into the high-yield engine of the entire group.[^4] Let's slow down and explain why leasing — arrendamiento in Spanish — is such a masterstroke in the Mexican context, because it is the mechanical heart of this whole business.

Think about how a normal secured loan works when it goes bad. The borrower defaults; the bank holds a lien on some collateral; and then the bank has to go to a Mexican court to actually seize and sell that collateral — a process that can take years, cost a fortune in legal fees, and often ends with the bank recovering pennies on the peso. Mexican creditor-protection law is famously slow.

Now consider leasing. The bank does not lend money to buy the truck, the CNC machine, or the factory equipment. The bank buys the equipment itself and leases it to the business. The bank is the legal owner the entire time. If the business stops paying, the bank does not need to win a lawsuit to foreclose on collateral — it already owns the asset, and it simply repossesses what is legally its property, with minimal legal friction. The recovery process collapses from years to weeks. On top of that, the SME gets a powerful tax benefit: lease payments are typically fully deductible operating expenses, which is enormously attractive to a small manufacturer trying to lower its tax bill. So the bank gets better collateral protection and the customer gets a better tax outcome — a genuinely rare win-win that lets Banregio charge a premium yield while taking less risk than a conventional lender. This is the source of the eye-popping margins we'll dissect later.

The GFC Distressed Asset Masterclass

If 2002 proved the model, 2009 proved that the family knew how to be greedy when others were fearful.

In the depths of the 2008–2009 Global Financial Crisis, GE Capital — once the most admired finance machine on earth — was in serious trouble. Its enormous balance sheet and reliance on short-term funding had turned from a strength into a liability overnight, and the parent company began aggressively shedding non-core foreign assets to raise liquidity. Among the assets on the block were GE's Mexican corporate fleet-management and leasing operations, run under the Masterlease brand.[^4]

Banregio pounced. They acquired the Masterlease Mexican leasing and fleet operations from a forced seller during the worst liquidity panic in eighty years.

Now, did they overpay? Let's benchmark it the way an M&A banker would. Historically, traditional corporate bank acquisitions in emerging markets have fetched somewhere between 1.8x and 2.2x book value — you pay a hefty premium for an established loan book and deposit franchise. Banregio, buying from a distressed seller who needed the cash, secured the Masterlease portfolio at a steep discount, at an estimated multiple well under 1.2x book value. They bought a high-quality, going-concern asset for a fraction of its through-cycle worth, precisely because the seller's problems had nothing to do with the quality of the Mexican business.

But the price was almost the least interesting part. Look at what the deal did strategically. Overnight, it diversified Banregio's client roster with the corporate fleets of top-tier multinationals — exactly the kind of blue-chip, sticky, high-volume customers a regional bank cannot easily win on its own. It imported deep institutional expertise in fleet and asset management, a genuinely specialized discipline. And it supercharged Arrendadora Banregio into the highest-yielding asset generator in the entire group, the product line that would go on to power those famous margins.

In two moves, separated by seven years, the family had built a leasing machine that converted Mexico's credit scarcity into premium yields and converted other people's crises into cheap acquisitions. The next problem was scale. To grow beyond Nuevo León, they needed to tap the public markets — and that meant inviting outside shareholders into the family's century-old project.

IV. Public Markets, Corporate Restructuring, and the Nearshoring Tailwind

There is a particular tension that runs through every family-controlled business that decides to go public. On one side sits the family's instinct for control, secrecy, and the long view. On the other sits the simple fact that growth needs capital, and capital, beyond a point, has to come from strangers. For Banregio, the resolution of that tension came in stages — first an IPO, then a clever corporate redesign — and each stage was engineered to get the capital and flexibility the family wanted without ever surrendering the control they prized.

The 2011 IPO

By the early 2010s, Banregio had outgrown its home state. The opportunity was no longer confined to Nuevo León; it stretched south into the Bajío — Guanajuato and Querétaro, the booming automotive-manufacturing belt of central Mexico — and west toward Guadalajara, the country's second city. But planting branches, hiring relationship managers, and funding a fast-growing loan book in three new regions at once requires capital the family could not supply on its own.

So in 2011, the group listed on the Bolsa Mexicana de Valores, Mexico's stock exchange, under the ticker GFREGIO.[^4] The IPO did exactly what a good growth IPO is supposed to do. It raised the equity capital needed to fund geographic expansion, and it began the transition from a localized Monterrey boutique into a genuine multi-regional financial player — all while the family retained firm control of the voting shares. This was outside capital on the family's terms.

The 2018 Restructuring into Regional S.A.B. de C.V.

The more interesting piece of financial architecture came seven years later, and to appreciate it you have to understand a quirk of Mexican banking law.

In April 2018, the family executed a strategic corporate restructuring. They dissolved the traditional Grupo Financiero — Financial Group — structure that had housed the bank, and reincorporated the whole enterprise as a modern holding company: Regional S.A.B. de C.V., trading on the BMV under the new ticker RA.1 On the surface it looked like a piece of dry corporate plumbing. In reality it was a deliberate act of legal engineering that unlocked everything that followed.

Here is the "why." Under Mexican law, a regulated Grupo Financiero is bound by extremely strict, rigid rules around capital-sharing and cross-guarantees among its subsidiaries. The legal premise of a Financial Group is that the entities inside it stand behind one another — which is prudent for a conventional bank, but a straitjacket for a company that wants to incubate, buy, and eventually spin off technology and fintech ventures. Under the old structure, an experimental, cash-burning digital bank would have been chained directly to the core bank's capital ratios, and any stumble at the startup would have dragged down the mothership.

By restructuring into a plain holding company, Regional decoupled the traditional bank from its other activities. It created clean legal and operational firewalls between the conservative, cash-generating Banregio and whatever new ventures the family chose to nurture. In other words, the 2018 restructuring was the legal prerequisite for Hey Banco — the act that made it possible to build a neobank, let it lose money for years, and ultimately hand it its own independent banking license, all without ever putting the crown jewel at risk. Few observers understood at the time just how forward-looking that piece of paperwork was.

The Epic Nearshoring Corridor

And then history handed Regional the tailwind of a generation.

As the United States and China decoupled, and as the pandemic exposed the fragility of supply chains stretched across the Pacific, global manufacturers began the largest reorganization of production since China joined the WTO. They went looking for a manufacturing base close to the American consumer, inside the USMCA free-trade zone, with cheap labor and existing industrial infrastructure. They found northern Mexico. They found, more specifically, the Monterrey corridor — and Regional S.A.B. was already sitting at the epicenter, having spent eighty years building exactly the relationships and products that an explosion of new factories would need.

The geographic concentration that a diversification purist might flag as a risk became, in the nearshoring era, the single greatest source of leverage to the theme. With nearly 50% of its loan portfolio originated in Nuevo León, and with that one state absorbing billions of dollars in new industrial investment, Banregio captured wave after wave of fresh corporate and SME demand — companies building plants, expanding capacity, buying equipment, and leasing fleets to feed the North American supply chain.[^11]

The bank pressed its hometown advantage with surgical precision. It signed an exclusive partnership with CAINTRA Nuevo León — the Cámara de la Industria de Transformación, the powerful regional manufacturing chamber — and used it to compress loan approval times for industrial SMEs to an astonishing 48 hours.[^11] In a market where a small manufacturer might wait weeks for a national bank's centralized credit committee to render a verdict, Banregio could say yes in two days. For a factory owner racing to win a contract from a newly arrived multinational, that speed is not a convenience; it is the difference between landing the order and losing it. That 48-hour promise is a competitive weapon we'll return to when we war-game the moat.

All of which raises the question we've been circling: just how good is the core business, really? It's time to open the hood.

V. Traditional Banking Segment: The SME Powerhouse

The financial press loves a neobank. Hand a journalist a sleek app, a hockey-stick user-growth chart, and a charismatic founder talking about disruption, and you'll get a thousand headlines. Hand them a regional commercial bank that finances air-conditioning manufacturers in Apodaca, and you'll get silence. But for an investor trying to understand where the money in Regional S.A.B. actually comes from, you have to ignore the noise and look at the cold, hard, segment-level numbers. And those numbers tell you, unambiguously, that the boring business is the entire story.

Materiality and Proportionality

Let's establish the proportions, because everything downstream depends on getting this right. Banregio — the traditional commercial bank, the unglamorous one financing the factories — generates roughly 79% of Regional's total consolidated net profits.1 Nearly four out of every five pesos of profit the holding company earns come from this single division. Out of Regional's total credit portfolio, which has grown to exceed $190 billion pesos, a commanding 84% is dedicated to corporate and SME commercial lending, with preferred consumer lending — mortgages and auto loans to the bank's affluent business-owner clientele — making up the remaining 16%.1[^12]

So when we talk about Regional S.A.B., we are talking, first and foremost, about a wildly profitable SME and commercial lender. The digital story is real and important, but it is the seasoning, not the steak.

The Core Business Economics

Now to the question that should be burning a hole in your mind: why is this business so profitable? Banregio posts Returns on Equity consistently near 20% — a figure that would be the envy of nearly any bank on earth.1 That kind of return doesn't come from one thing; it comes from three engines firing at once.

The first engine is the Net Interest Margin, or NIM. This is simply the spread between what a bank earns on its loans and what it pays for its funding — the fundamental profit margin of banking. Banregio runs a NIM of roughly 6.0% to 6.5%, which is exceptionally fat for commercial lending, where margins are usually thin and competitive.[^12] Where does that extra spread come from? On the asset side, from the high-yield leasing products we discussed — Arrendadora's machinery and fleet leases earn well above a plain corporate loan. And on the funding side, from a deeply loyal, low-cost regional deposit base; the business owners of Monterrey park their operating cash at Banregio, and much of it sits in low- or no-interest accounts. Cheap money in, high-yield assets out — that gap is the margin.

The second engine is efficiency. A bank's efficiency ratio measures how many cents of operating cost it takes to generate one peso of revenue, so lower is better. Banregio runs an efficiency ratio of around 40% — meaning it spends roughly 40 centavos to produce a peso of revenue.[^12] To put that in perspective, that figure rivals or beats the giant national banks, despite Banregio having a tiny fraction of their scale. How? Density. By concentrating its branches and bankers in the dense industrial corridors of Monterrey and the Bajío rather than scattering them thinly across a vast country, Banregio achieves big-bank efficiency without big-bank infrastructure. We'll come back to this as a genuine "power" in the strategic analysis.

The third engine is asset quality — and this is the one that separates a great lender from a lucky one. Anyone can post high margins for a few years by lending recklessly; the bill arrives later, in the form of defaults. Banregio's non-performing loan ratio — the share of its book that has gone bad, known locally as the IMOR — sits at a pristine 1.3% to 1.4%.[^12] The Mexican national banking average runs around 2.2%, so Banregio's borrowers default at roughly half the system rate.[^13] That is not luck. It is the eighty-year-old relationship model at work: the bankers genuinely know the businesses they lend to, walk their factory floors, and understand their cash flows in a way no centralized credit algorithm in Mexico City ever could. The same local intelligence that let them survive 1994 keeps the loan book clean today. High margin, low cost, low losses — stack those three and a 20% ROE is the arithmetic result.

The Competitive Landscape

Here is the fact that genuinely stuns people when they first encounter it. In SME lending — the specialized, high-yield niche that is Banregio's home turf — this regional bank goes toe-to-toe, in absolute peso terms, with the largest bank in the country.

Consider the field. BBVA México is the undisputed Goliath, controlling around 25.6% of the entire Mexican banking system's assets — a national colossus.[^13] In SME lending specifically, BBVA carries a portfolio of roughly $136 billion pesos, won through massive standardized digital scale and its well-known Banco de Barrio neighborhood-banking initiative.[^13] Then there is Banco del Bajío — BanBajío — the most direct peer, the sixth-largest corporate lender in Mexico with about a 3.4% share of total system assets and an SME book of roughly $70 billion pesos, which makes up around 29% of its total loans; BanBajío is the master of agribusiness lending across central Mexico.[^13]

Now place Banregio next to them. Its SME portfolio stands at approximately $132 billion pesos — virtually identical in absolute size to BBVA's, and nearly double BanBajío's.[^13] Sit with that for a moment. A bank with a fraction of BBVA's branches, deposits, and national footprint has built an SME lending book that matches the giant's, peso for peso. It did not do that by being cheaper or bigger. It did it by being faster, more local, and more deeply embedded — winning its core northern corridor through high-touch relationships, customized leasing solutions, and physical integration inside the industrial parks where its clients actually operate. On BBVA's national turf, Banregio would be crushed. On Banregio's home turf, BBVA is the one that struggles to compete. That is what a regional moat looks like in practice.

So the core business is a profit machine guarded by relationships the giants cannot replicate. Which makes the family's next move all the more surprising — because instead of simply harvesting this cash cow, they used it to fund the construction of the very thing that was supposed to disrupt them.

VI. The Digital Disruptor: The Hey Banco Spin-Off

There is a famous trap in business known as the Innovator's Dilemma. A profitable incumbent sees a disruptive technology coming, but cannot bring itself to cannibalize its own lucrative business to chase it, so it does nothing — and is eventually destroyed by a startup with nothing to lose. The history of banking is littered with conservative institutions that watched fintechs eat their lunch because building a competing product would have embarrassed their core franchise. What makes Regional genuinely unusual — almost unique among family-controlled commercial banks anywhere — is that they looked at the dilemma and chose to disrupt themselves first.

Incubating a Neobank

Around 2017, with pure-play digital banks like Nu, Mercado Pago, and Ualá beginning to swarm across Latin America, Regional did something that conservative, family-run banks almost never do. Rather than partner, acquire, or ignore, they built a 100% digital neobank from scratch, in-house, and launched it as Hey Banco.[^9] A bank whose entire identity was the factory floor and the handshake deliberately created a child whose entire identity was the smartphone screen and the algorithm. The 2018 holding-company restructuring we walked through earlier is what made this possible — it gave the family a legal structure where Hey could burn money and take risks without endangering Banregio's pristine capital ratios.

Size to its Weight

Now, a reality check, because hype is the enemy of good analysis. How much does Hey Banco actually contribute to Regional's profits today? Around 1%.[^9] One percent. After years of operation, the celebrated digital child throws off a rounding error of the holding company's earnings.

Why so little? Because Hey is doing exactly what a growth-stage neobank is supposed to do: plowing everything into technology, customer acquisition, and infrastructure rather than harvesting profit. The 1% figure is a choice, not a failure.

But here's the question that matters: if it only produces 1% of profits, why should an investor care at all? Because Hey Banco is not valued on its current earnings — it is valued on its strategic optionality, and that optionality is real and large. Hey has built a low-cost, retail-focused funding funnel, gathering over $12 billion pesos in low-cost deposits from more than 500,000 active retail customers.[^9] Think about what that means in the context of everything we've learned. Banregio's entire profit engine runs on the spread between cheap deposits and high-yield SME loans. Hey Banco is, among other things, a national deposit-gathering machine — a way to pull in low-cost retail funding from across all of Mexico and channel it into Banregio's high-yield commercial book. It is simultaneously a hedge against retail disruption and a fuel line for the core franchise. That is why a business contributing 1% of profits commands real attention.

The Great Regulatory Separation

For years, Hey Banco operated under Banregio's banking license, as a digital division riding on the parent's regulatory permissions. That changed through one of the more demanding regulatory journeys in recent Mexican banking history.

In July 2023, the CNBV — the Comisión Nacional Bancaria y de Valores, Mexico's banking and securities regulator — granted Hey Banco its own full, independent Institución de Banca Múltiple license, the authorization to operate as a standalone bank.2 But a license is only the beginning. What followed was a massive, multi-year operational migration: untangling Hey's customers, deposits, technology, and balance sheet from Banregio's and standing them up as a genuinely independent institution. On January 31, 2026, that migration crossed the finish line, and Hey Banco officially began operating on its own independent balance sheet, a separate banking subsidiary sitting alongside Banregio under the Regional S.A.B. holding company.[^5] The neobank the family built in-house had become a fully licensed, freestanding bank in its own right.

The Present Day Challenge

If you want a window into just how hard it is to run an independent bank in real time, look no further than what happened a few weeks ago. Hey Banco had been preparing to launch a highly anticipated investment platform, branded "Hey X," meant to let its retail customers invest directly through the app. In early June 2026, the company had to postpone the launch.[^6]

The reason is instructive. Following regulatory feedback from the CNBV, Regional could not have the bank itself operate the investment-referral scheme as originally designed. So the group pivoted: rather than scrap the product, it restructured the plan so that the offering would be run by Admino, another specialized subsidiary within the holding company, rather than by Hey Banco directly.[^6] This is exactly the kind of regulatory chess that modern digital banking in Mexico demands — and it is a vivid reminder that a freshly independent bank now has to fight its own regulatory battles, with its own license on the line, rather than sheltering under its parent's. The holding-company structure, once again, proved its worth: it gave Regional a spare subsidiary to route the product through. The episode is a small live drama, but it foreshadows the execution risk we'll weigh in the bear case.

Behind every one of these strategic moves — the in-house neobank, the holding-company design, the patient license journey — stands a single figure who has been quietly orchestrating the modernization of a century-old institution. It's time to meet him.

VII. Current Management: The Fourth-Generation Visionary & Executive Incentives

Walk into Regional's offices in San Pedro Garza García and you will not find the typical modern-banking CEO — the parachuted-in turnaround specialist with a five-year horizon and a one-way ticket to the next institution. You will find a member of the founding family who has spent essentially his entire career inside the bank his great-grandfather helped create, and whose personal fortune rises and falls with the stock that bears the family's legacy. That alignment — the difference between a steward and a hired hand — is the soul of how this company is run.

Current Leadership

We will skip the historical figures and focus on the man steering the ship today: Manuel Rivero Zambrano, CEO of both Regional S.A.B. and Hey Banco. He represents the fourth generation of the Rivero banking family, joined the bank nearly two decades ago, and is universally credited as the executive who dragged a traditional brick-and-mortar SME lender into the digital age.[^9] Think about the dual nature of that mandate. He runs the conservative, relationship-driven commercial bank that survived the Tequila Crisis on prudence — and he simultaneously runs the aggressive, cash-burning neobank that is supposed to reinvent retail banking. Those two jobs require almost opposite temperaments, and the fact that one person holds both, and that the digital initiative was championed from inside the founding family rather than forced on it from outside, is precisely why Hey Banco escaped the Innovator's Dilemma. The disruption had a patron at the very top with the authority and the family credibility to protect it.

Alignment of Interest

Now to the structure that makes everything else credible. The controlling families own roughly 60% of Regional S.A.B., with the Rivero Santos family alone holding a commanding 27.58% stake.1 This is not management-for-hire, where executives own a sliver of options and optimize for the next quarterly print. This is an owner-operator running a substantial portion of his family's multi-generational wealth, with all the behavioral consequences that implies.

What does that ownership actually change in practice? It changes the time horizon. A family that has already lived through expropriation in 1982 and near-death in 1994 does not manage for the applause of quarterly earnings calls. It manages for survival and steady compounding across decades, for the preservation and growth of wealth that is meant to pass to a fifth generation. The patience and conservatism that look like under-ambition to a short-term trader are, to the family, simply the lessons of their own history encoded into how they run the bank.

Executive Compensation & Incentives

Look at how the executives are paid and the philosophy comes into sharp focus, because incentives are where stated values either get backed by money or exposed as talk.

On the short-term side, performance bonuses are tied explicitly to hard operational metrics rather than vague goals or share-price moves: growth in the SME loan portfolio, holding the efficiency ratio under roughly 41%, and hitting strict Return on Assets and Return on Equity targets, with a minimum ROE threshold around 18%.1 These bonuses are calculated and paid on a rolling basis, which ties the cash reward tightly to immediate credit quality and asset performance — you do not get rewarded for booking loans that go bad next year.

On the long-term side, there is a robust share-based payment plan that grants actual shares of Regional S.A.B. to the CEO and senior officers.1 The logic is to force management to think like the owners they already are — to ensure that an executive's personal net worth is welded directly to the long-term compounding of the RA stock, not to any single year's bonus pool.

And the governing philosophy that emerges from those incentives is a study in productive contradiction: conservative credit underwriting in the back office, aggressive digital customer acquisition at the front door. The clearest evidence came in 2025. As macroeconomic uncertainty rose — trade tensions, rate volatility, questions about the durability of the nearshoring boom — management voluntarily dialed back its loan-growth guidance from 15% down to 8%, deliberately choosing slower growth to protect the balance sheet.[^12] A management team paid purely on growth and stock price would have kept the pedal down and prayed. A family that remembers what 1994 did to over-extended lenders chose prudence over Wall Street applause. That single decision tells you more about how this company will behave in the next crisis than any mission statement ever could. With the people and incentives mapped, we can now step back and ask the structural question: how durable is this advantage, really?

VIII. Strategic Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Strip away the family romance and the nearshoring excitement, and a sober investor is left with one question: is the moat real and durable, or is this just a good bank enjoying a good cycle? To answer it properly, we'll run the business through two classic frameworks — Porter's Five Forces to map the industry structure, and Hamilton Helmer's Seven Powers to isolate the genuine, persistent sources of advantage.

Porter's Five Forces Applied to Regional S.A.B.

Threat of New Entrants — Low to Moderate. Banking is one of the most heavily protected industries on earth, and Mexico is no exception. Securing a banking license from the CNBV takes years and serious money — Hey Banco's own multi-year journey from license grant in 2023 to independent operation in 2026 is the living proof. That regulatory barrier shields the core franchise. The nuance is that aggressive fintechs are entering the retail arena with relative ease, attacking deposits and consumer credit. But here is why Regional's core is insulated: a consumer fintech cannot simply replicate complex corporate credit, structured equipment leasing, and cross-border factoring for industrial SMEs. Building an app is hard; building eighty years of factory-floor underwriting judgment is much harder.

Bargaining Power of Buyers — Low. We've established that only around 4.4% of Mexican SMEs can get formal bank credit.[^10] When the product is that scarce, the buyer has almost no leverage over pricing. A factory owner who needs a 48-hour approval to win a contract is not going to haggle Banregio down by twenty basis points; he is going to take the deal and pay a healthy yield gratefully. Scarcity hands the pricing power to the lender.

Bargaining Power of Suppliers (Deposits) — Moderate. A bank's "suppliers" are its depositors, and their power rises when interest rates are high, because they can demand more for their money. With Banco de México holding rates elevated, that pressure is real. But Regional blunts it from two directions: the loyal, sticky, low-cost deposit base of Monterrey's business community, and the national retail funding funnel of Hey Banco. Together they give Regional a structurally cheaper cost of capital than the pure fintech lenders, who have no deposit franchise and must fund themselves with expensive market money.

Threat of Substitutes — Low. The obvious substitute for a bank loan is a Sofom — a non-bank financial company that lends to SMEs. But Sofomes fund themselves at a much higher cost of capital, so they must charge more, and crucially they cannot offer the surrounding ecosystem: the treasury services, payroll dispersion, and cash management that bind an SME to Banregio. A standalone loan is a substitute; an integrated banking relationship is not easily replaced.

Competitive Rivalry — High but Segmented. At the national level Regional competes with giants — BBVA, Banorte, Santander. But the actual rivalry in the high-yield SME leasing niche of the northern corridor is a far more focused contest, primarily between Banregio and BanBajío, each of which has carved out a defensible, highly profitable regional stronghold. Rivalry is intense in theory and gentle in practice, because the combatants have largely divided the territory.

Hamilton's Seven Powers Framework

Porter tells us the industry is attractive. Helmer's framework tells us which specific powers let Regional capture that attractiveness durably. Four stand out.

Counter-Positioning — the SME Relationship Model. This is the deepest and most interesting of Regional's powers. The national giants serve SMEs through heavily standardized, centralized, algorithmic credit-scoring systems — efficient at scale, but slow and blunt, frequently rejecting good local businesses or taking weeks to decide. Banregio runs the opposite model: relational, localized underwriting paired with customized leasing and that 48-hour turnaround. The magic of counter-positioning is that the incumbent cannot copy it without harming itself. For BBVA to replicate Banregio's high-touch, relationship-led model nationwide would mean dismantling the very low-cost, automated, centralized machine that makes BBVA profitable at scale. They are structurally trapped into their model, which leaves Banregio's model uncontested in its niche.

Switching Costs — High. Once an SME wires Banregio into its daily operations — business credit lines, equipment leasing, corporate fleet management, factoring, and payroll dispersion (dispersión de nómina) — the friction of leaving becomes enormous. Switching banks would mean re-plumbing the company's entire financial nervous system, re-papering every facility, and retraining staff, all to save a marginal amount on rate. Most owners simply won't do it. Integration, not loyalty alone, is what locks the customer in.

Cornered Resource — Local Family Prestige. In the tight-knit industrial culture of Monterrey, trust and heritage are scarce, non-replicable assets. Being a native Regio bank, run by a multi-generational local dynasty that survived 1982 and 1994, grants a kind of access that money cannot buy — to industrial-park developers, to CAINTRA leadership, to the manufacturing families who would rather bank with one of their own than with a foreign-controlled national chain. A competitor can hire bankers and build branches; it cannot manufacture eighty years of being a trusted member of the same community.

Scale Economies — Regional Density. Here is the counterintuitive one. Regional has no national scale, yet it enjoys scale-like economics through density. By concentrating branches, offices, and relationship managers in the dense industrial corridors of Monterrey and the Bajío rather than spreading them thin across a continent, it drives its efficiency ratio down toward 40% — rivaling BBVA, a bank perhaps ten times its size nationally.[^12] It does not need an expensive national retail network to be elite on cost, because within its chosen geography it is the dense, dominant player. Density is its own form of scale.

Put the two frameworks together and the picture is of a business protected by genuine, structural, hard-to-replicate advantages — not merely a good bank riding a good cycle. But no moat is absolute, and intellectual honesty requires us to stress-test the thesis from both directions.

IX. Bear vs. Bull Case, KPIs, and Key Risks

Every great business story contains the seeds of its own potential undoing, and Regional is no exception. So let's do the work of an honest analyst: first identify the handful of numbers that actually matter for tracking this company, then argue the bear case as forcefully as we can, and finally lay out the bull case on its own terms — leaving the judgment to you.

The KPIs That Matter Most

Resist the temptation to track everything. For Regional, three metrics capture the essence of the business, and if you watch these you understand the company.

The first is SME loan growth paired with net interest margin. The whole thesis rests on the bank's ability to keep expanding its high-yield commercial book — ideally at 8% to 10% a year — without sacrificing that premium 6.0% to 6.5% NIM. Growth that comes at the cost of margin would signal that competition is finally biting; margin held steady alongside healthy growth confirms the moat is intact. Watch them together, never separately.

The second is the efficiency ratio. The critical question over the next few years is whether the consolidated group can hold its efficiency near that elite 40% to 42% band even as it absorbs the standalone technology and marketing costs of an independent Hey Banco and the broader Hey Tech operations. A creeping efficiency ratio would be the early warning that the digital ambitions are eroding the discipline of the core.

The third is asset quality — the NPL or IMOR ratio. This is the canary in the coal mine. As long as non-performing loans stay comfortably below the 1.5% threshold, the conservative underwriting story holds. Any sustained drift above it — particularly during a macro wobble or a shift in US–Mexico trade policy — would be the first hard evidence that the credit machine is straining.

Key Risks — The Bear Case

Geographic over-concentration. The same Nuevo León concentration that makes Regional the purest play on nearshoring also makes it dangerously undiversified. With nearly half the loan book tied to a single state, the bank is exposed to anything that derails the Monterrey industrial machine.[^11] If the nearshoring trend cools, if marquee projects stall or get cancelled, or if US protectionist tariffs slam Monterrey's export manufacturers, Regional will be hit far harder than a nationally diversified bank. Its greatest strength and its greatest vulnerability are the same fact.

Hey Banco execution and capital burn. Independence cuts both ways. Now that Hey Banco carries its own banking license, it must hold its own regulatory capital and stand on its own balance sheet. If it fails to grow its higher-margin consumer products — credit cards and personal loans — fast enough to cover its substantial technology and acquisition overhead, the celebrated digital child could curdle into a persistent drag on the holding company's ROE. The optionality is genuine, but so is the possibility that the option simply expires worthless after years of investment.

The retail deposit battle. Hey Banco's value to the group rests on cheap deposits. But the Mexican retail-deposit market has become a war zone, with aggressive fintechs — Nu México foremost among them — dangling eye-catching annual yields in the low-to-mid teens to vacuum up customer cash. If that pricing pressure forces Hey to raise its own deposit rates to stay competitive, the cheap-funding advantage that justifies its existence could compress, weakening the very mechanism that makes the neobank strategically valuable.

The Investment Thesis — The Bull Case

The nearshoring super-cycle play. Flip the concentration risk on its head and Regional becomes arguably the single purest listed equity on the industrialization of northern Mexico. It is not merely exposed to the supply-chain relocation; it is one of the primary financial facilitators of it, armed with a leasing-and-factoring product suite that is almost perfectly designed for an era of factory-building and capacity expansion. If you believe the nearshoring wave has years left to run, it is hard to find a more direct way to own it.

The family dynasty premium. Run by a deeply aligned fourth-generation CEO atop a 60% family ownership block, the bank is managed with a prudence and a multi-decade horizon that public markets rarely reward in advance.1 The voluntary growth-guidance cut of 2025 is the kind of decision that costs you a quarter and saves you a cycle — and it is exactly what you want from stewards protecting their own family's wealth.

The unrivaled SME moat. Stack the powers we mapped — counter-positioning the giants cannot copy without self-harm, switching costs that weld customers in place, the cornered resource of local prestige, and density-driven efficiency — and you get a competitive moat in the SME corridor that national giants have spent decades failing to breach. That moat is the ultimate source of the 20% ROE, and it is not going anywhere quickly.

Bull and bear both flow from the same handful of facts viewed through opposite lenses. Which lens is correct is a judgment about the durability of nearshoring and the execution of a single management family — and that is precisely the judgment an investor is paid to make.

X. Epilogue & Surprises

After all of this, what is the thing that should genuinely surprise you?

It is this. A conservative, family-controlled commercial bank — born in the industrial valleys of Monterrey, hardened by expropriation and a near-fatal currency crisis, run by people whose entire instinct is caution — managed to build a pioneering, fully digital bank from scratch and carry it all the way to a historic independent banking license in 2026, without ever compromising the disciplined SME franchise that is its reason for being. The institutions most likely to fall into the Innovator's Dilemma are exactly the kind of prudent, profitable, family-run incumbents that Regional is. That it disrupted itself on purpose, and survived doing so, is the real anomaly at the center of this story.

And the takeaway reaches beyond one bank. In finance, scale is usually treated as the ultimate weapon — bigger balance sheet, cheaper funding, more branches, more data. Regional S.A.B. quietly proves that there is another way to win. Geographic density, product specialization through leasing, and a relationship moat built over generations can let a mid-sized player out-compete global giants on the only metrics that ultimately matter to an owner: profitability and efficiency. As the nearshoring wave continues to roll through northern Mexico, a banking family that has been doing this for nearly eighty years finds itself positioned, improbably, to write its most profitable chapter yet.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube