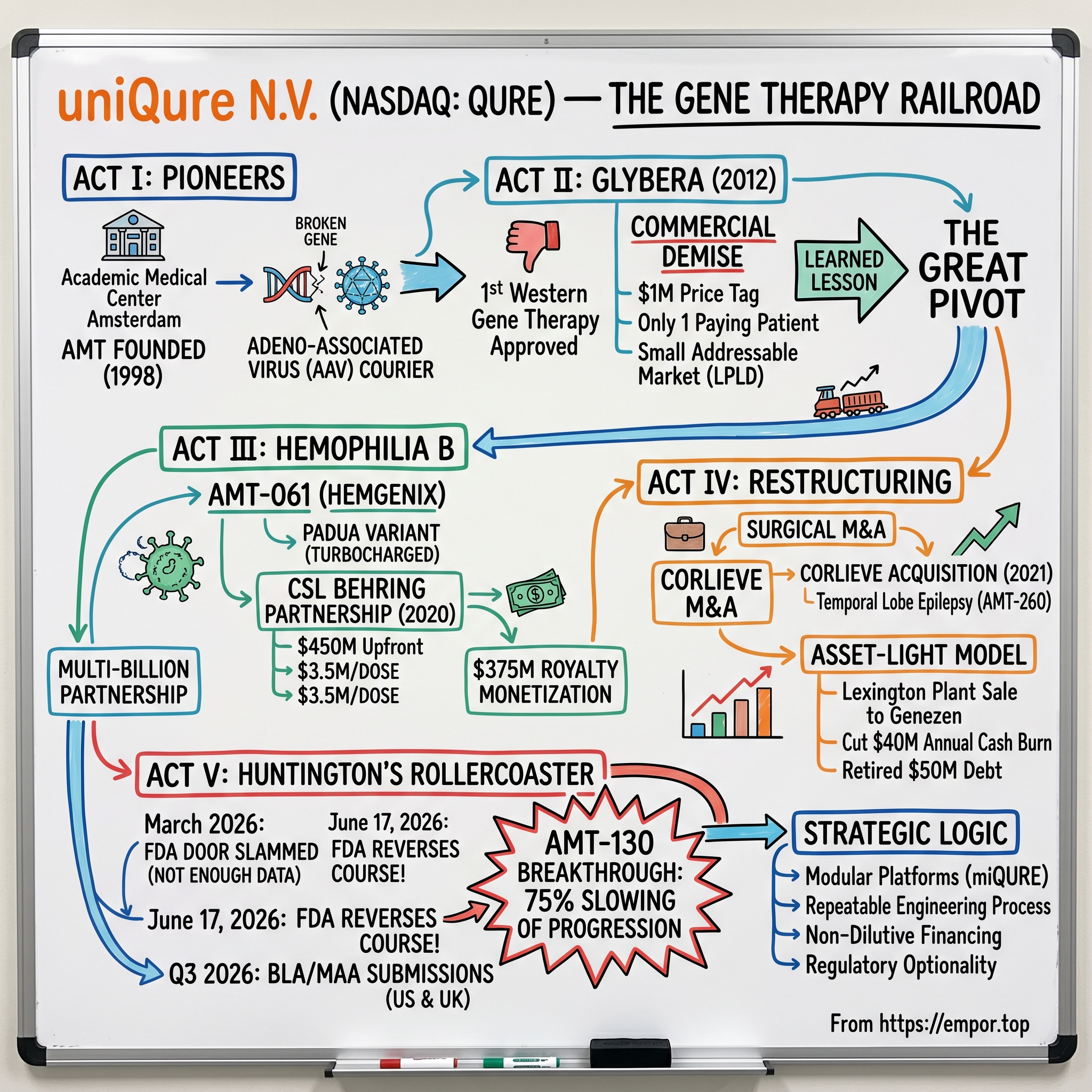

uniQure N.V. (NASDAQ: QURE) — The Gene Therapy Railroad

I. Introduction & Episode Roadmap

At 6:38 in the evening, Indian Standard Time, on Wednesday, June 17, 2026, a single sentence buried in a corporate press release detonated across the biotech trading desks of two continents. Shares of uniQure—a Dutch-American gene therapy company most retail investors had never heard of—rocketed more than 70% in pre-market trading on the NASDAQ.1 By the time the opening bell rang in New York, the stock was changing hands at its highest level in over seven months.1 The catalyst was not a buyout, not earnings, not a celebrity tweet. It was a regulator changing its mind.

The U.S. Food and Drug Administration had, just months earlier, effectively slammed the door on uniQure's most important program. In March 2026, the agency told the company that the early-stage data behind AMT-130—its experimental gene therapy for Huntington's disease—were not sufficient to support an approval, and that what was really needed was a large, randomized, multi-year confirmatory trial.1 For a small company betting its future on a single neurological cargo, that message read like a death sentence written in regulatory bureaucratese. And then, on this Wednesday in June, the FDA reversed course, agreeing it was now willing to consider three years of data from uniQure's Phase I/II study as the primary basis for an accelerated Biologics License Application.1 The company announced it would file that BLA in the third quarter of 2026.1 The market did the math on what a marketed Huntington's cure might be worth, and the result was the kind of single-day move that careers and fortunes are built on.

Here is what makes this story worth two hours of your attention. This is not a tale of an overnight biotech rocket. This is a survival story—arguably the most improbable corporate survival story in the history of genetic medicine. Because uniQure is the company that pioneered the very first gene therapy ever approved in the Western world, a drug called Glybera, and then watched that historic scientific triumph become one of the most spectacular commercial disasters in pharmaceutical history. One single paying patient. A million-dollar price tag. A quiet, embarrassed withdrawal from the market.

How does a company go from launching a product that essentially sold a grand total of one unit, to standing on the precipice of delivering the first-ever disease-modifying treatment for one of the cruelest hereditary diseases known to medicine? That is the arc we are going to trace. And the answer, as you will see, has surprisingly little to do with luck and almost everything to do with a ruthless, repeatable playbook of capital allocation, platform engineering, and regulatory chess.

Here is our roadmap. Act I takes us to the canals of Amsterdam and the wild, almost reckless science of early 2000s gene therapy. Act II is the rise and commercial collapse of Glybera. Act III is the great pivot—the move into Hemophilia B and the multi-billion-dollar partnership with CSL Behring that refilled the company's coffers. Act IV is the asset-light restructuring: surgical acquisitions like Corlieve and the transformation of a physical manufacturing plant into a liquid financial estate. And Act V brings us to today's management roster, the Huntington's rollercoaster, and the strategic logic underneath that 70% move. Let's get into it.

II. The Pioneers of Gene Therapy: Amsterdam Molecular Therapeutics

Picture the late 1990s in academic medicine. Gene therapy was, to put it gently, in disgrace. In September 1999, an eighteen-year-old named Jesse Gelsinger died in a gene therapy trial at the University of Pennsylvania, killed by a catastrophic immune reaction to the viral vector meant to save him. The entire field froze. Funding evaporated. Serious scientists distanced themselves from a modality that, just years earlier, had been heralded as the future of medicine. It was precisely into this winter—against the prevailing wind, as all the best origin stories go—that a small band of researchers at the Academic Medical Center in Amsterdam decided to keep going.

In 1998, they founded Amsterdam Molecular Therapeutics, or AMT, a company built on a deceptively simple and audacious premise.[^2] What if you could take a virus—nature's own delivery machine, evolved over millions of years specifically to insert genetic material into human cells—disarm it so it couldn't cause disease, load it with a healthy gene, and use it to permanently correct an inherited genetic error? Not treat the symptoms. Not manage the condition for life. Correct the underlying broken instruction set, one time, forever.

The vehicle they bet on was the adeno-associated virus, or AAV. To understand why this mattered, it helps to drop the jargon entirely. Think of a genetic disease as a typo in the instruction manual that every one of your cells reads to function. Your body keeps printing the same broken page over and over. A traditional drug is like hiring a translator to stand next to the reader and verbally correct the typo every single time the page is read—you need that translator there for life, and you pay for it for life. Gene therapy is different. Gene therapy hands the cell a corrected page and slips it into the binder. AAV is the courier that carries that page. The reason AAV was so attractive is that, unlike the virus that killed Jesse Gelsinger, AAV is associated with essentially no human disease, it can deliver its cargo to cells that don't divide much—like neurons and liver cells—and it tends to produce its corrected protein for years.

AMT chose for its first target a disease almost nobody outside of metabolic medicine has heard of: lipoprotein lipase deficiency, or LPLD. People with LPLD inherit two broken copies of the gene that makes lipoprotein lipase, the enzyme that clears fat from the bloodstream. Without it, fat accumulates to grotesque levels, and patients suffer repeated, agonizing, and potentially fatal attacks of pancreatitis. There was no real treatment beyond a near-impossible fat-free diet. It is an ultra-rare disease—we are talking one or two people per million—and that rarity was, in equal measure, the scientific opportunity and the commercial time bomb that would later nearly destroy the company.

The therapy AMT built was called alipogene tiparvovec, later branded Glybera, and the regulatory road it traveled was brutal. The European Medicines Agency, the EMA, did not want to approve it. The fundamental problem was statistical: when your disease afflicts only a handful of people on Earth, you cannot run a trial with thousands of patients. Glybera's clinical evidence rested on fewer than thirty patients in total.2 The EMA's scientific committee rejected the application not once but multiple times, repeatedly sending AMT's scientists back to defend a dataset that, by the conventional standards of pharmaceutical statistics, was simply too thin.2 What followed was years of trench warfare between a tiny Dutch biotech and the most powerful drug regulator in Europe—clinicians flying in to argue patient by patient, the company restructuring and very nearly running out of money. Finally, in late 2012, the EMA relented and recommended approval.2 Glybera officially became the first gene therapy ever approved anywhere in the Western world. The science had won. The business lesson was about to begin.

III. Glybera: The World's First Approved Gene Therapy and Its Commercial Demise

There is a particular kind of corporate tragedy that only happens when a company is too far ahead of its time. Glybera is the textbook case—the drug that proved everything about the science and almost nothing about the business.

On the scientific merits, Glybera was a genuine landmark. It demonstrated, in living human beings, that you could deliver a corrected gene with an AAV vector and have it produce a functional protein durably, for years, with an acceptable safety profile.2 Every gene therapy company alive today—every one of the hundreds of programs now in clinical trials for everything from blindness to muscular dystrophy—stands on the validation that Glybera provided. It was the proof of concept for an entire industry. As a piece of biology, it was a triumph that would echo for decades.

As a product, it was a catastrophe. The company priced Glybera at roughly one million dollars per treatment—at the time, the most expensive drug in the world by a wide margin.2 Now, on paper, that price was almost defensible. If a single infusion permanently spares a patient a lifetime of hospitalizations for pancreatitis, a million dollars spread over decades might pencil out. But here is the catch that nobody in 2012 had solved: the entire global apparatus of health insurance was built around the opposite model. Insurers and national health services are organized to pay small amounts continuously over time—a monthly prescription, an annual infusion. They had no mechanism, no actuarial framework, no contract template for a one-and-done, seven-figure, pay-it-all-upfront cure. Who pays when the benefit accrues over thirty years but the bill arrives on day one? What happens if the patient switches insurers? What if they move countries? The financial plumbing of modern healthcare simply had no pipe of the right shape.

And then there was the demand problem, which was even more fundamental. LPLD is so vanishingly rare that the addressable market was measured not in thousands of patients, not in hundreds, but in a few dozen across all of Europe. The grim punchline of the entire Glybera saga is this: across its commercial life, exactly one patient ever received the therapy through normal commercial reimbursement.2 One. A drug that took fifteen years and the survival of an entire company to bring to market was administered, for money, to a single human being.

By 2017, the calculus was inescapable. Maintaining a European marketing authorization is not free—there are pharmacovigilance obligations, regulatory reporting requirements, manufacturing readiness costs—and uniQure was bleeding cash to keep a product on shelves that nobody was buying. The company made the unsentimental decision not to renew Glybera's marketing authorization, and the first gene therapy in Western history quietly left the market.2

But—and this is the hinge on which the entire investment thesis turns—the company had already begun to learn the right lesson from the wrong outcome. The problem with Glybera was never the science. It was the size of the market. An ultra-orphan disease with a few dozen patients can never support the economics of a one-time cure, no matter how miraculous. So the company, which by now had rebranded from Amsterdam Molecular Therapeutics to uniQure, made a deliberate strategic turn away from ultra-orphan vanity projects and toward what you might call "large-orphan" opportunities—genetic diseases still rare enough to command premium pricing and regulatory designations, but with patient populations large enough to build a real business on. Two diseases sat at the top of that new list. One was a bleeding disorder called Hemophilia B. The other was Huntington's disease. The first would save the company. The second would, eventually, make it.

IV. The Hemophilia B Miracle & The CSL Behring Partnership

To understand the deal that rescued uniQure, you first have to understand the disease that made it possible. Hemophilia B is a hereditary bleeding disorder, almost always in men, caused by a deficiency in a single clotting protein called Factor IX. Without enough working Factor IX, the blood cannot form stable clots, and patients face a lifetime of dangerous spontaneous bleeds—into joints, into muscles, into the brain. The standard of care is grueling and astronomically expensive: regular, prophylactic intravenous infusions of clotting factor, often several times a week, for the patient's entire life. The lifetime cost of managing a single severe hemophilia patient runs into the millions of dollars. This was exactly the profile uniQure was now hunting for—a disease where a one-time genetic fix could replace decades of crushing recurring cost, and where the patient population numbered in the tens of thousands rather than the dozens.

uniQure's scientific answer was a program internally called AMT-061. And the clever bit—the part that separates a me-too gene therapy from a potential blockbuster—was a piece of biological engineering called the Padua variant. Here is the simple version. The gene that codes for Factor IX comes in different flavors in the human population. Years earlier, researchers had discovered a family near Padua, Italy, whose members carried a naturally occurring mutation in their Factor IX gene that made the protein dramatically more potent—roughly eight to nine times more active than the standard version. Instead of delivering the ordinary Factor IX gene, uniQure engineered its AAV5 vector to deliver this hyperactive Padua variant. The analogy is almost too neat: rather than installing a standard-output engine, they installed a turbocharged one. The result was that even a modest amount of gene expression in the patient's liver could produce enough clotting activity to transform the disease from severe to mild—or to functionally eliminate the need for infusions altogether.[^4]

The science was extraordinary. But uniQure now faced a problem that has killed countless clinical-stage biotechs: it had a potential global hematology blockbuster and absolutely none of the commercial infrastructure required to sell one. Launching a drug like this worldwide means building sales forces, navigating reimbursement negotiations across dozens of national health systems, managing a complex global supply chain, and educating thousands of hematologists. That costs hundreds of millions of dollars and takes years. For a company still nursing the wounds of Glybera, going it alone was not an option.

So uniQure did something that, in retrospect, looks like one of the smartest capital decisions in modern biotech. In 2020, it struck a licensing megadeal with CSL Behring, the plasma-products powerhouse, handing CSL the global commercial rights to the therapy.[^4] The terms were transformational for a company of uniQure's size: $450 million in cash upfront, up to roughly $1.6 billion in additional regulatory and commercial milestone payments, and tiered double-digit royalties climbing into the low twenties as a percentage of global net sales.[^4] In one stroke, uniQure offloaded the enormous cost and execution risk of a global launch while retaining a long, lucrative royalty stream on every dose sold for years to come. It got paid to hand the heavy lifting to a partner uniquely built for it.

The validation came in November 2022, when the FDA approved the therapy—now branded Hemgenix—as the first gene therapy for Hemophilia B in the United States.3 And the price tag rewrote the record books once more: $3.5 million per dose, making Hemgenix, at the time, the most expensive drug in the world.4 But unlike Glybera, this number sat atop a genuine market and a genuine economic argument—a one-time cost against a lifetime of multi-million-dollar factor infusions, sold by a partner with the muscle to actually collect on it.

Then uniQure ran the play one level deeper. In May 2023, rather than simply waiting for royalties to dribble in over a decade, the company sold off a portion of its future Hemgenix royalty stream to HealthCare Royalty and Sagard Healthcare in exchange for $375 million in cash upfront.5 This is financial engineering at its most elegant. Royalty monetization let uniQure convert a stream of uncertain future payments into a large, certain slug of cash today—cash that carried no interest, no repayment schedule, and, crucially, no dilution of existing shareholders. It was, in effect, borrowing against its own future success without issuing a single new share or taking on traditional debt. Between the upfront from CSL and the royalty sale, uniQure had pulled the better part of a billion dollars of non-dilutive capital out of a single asset. The question now was what to do with it. The answer was to go shopping—very, very carefully.

V. Capital Allocation & Surgical M&A: Benchmarking the Corlieve Acquisition

Here is a scenario that destroys more biotech companies than failed trials do. A small company suddenly finds itself flush with cash—hundreds of millions, non-dilutive, no strings. The temptation, the almost gravitational pull, is to spend it lavishly: a splashy acquisition at the top of the market, a trophy asset to signal ambition to investors. The graveyards of biotech are full of companies that raised a war chest and then deployed it at exactly the wrong moment, for exactly the wrong price. Watching how a management team spends a windfall tells you more about its discipline than any pipeline chart ever will. So watch what uniQure did.

In July 2021, uniQure acquired a privately held French biotech called Corlieve Therapeutics.6 The prize was a preclinical program for refractory temporal lobe epilepsy—the program that would become AMT-260—aimed at the most common and most drug-resistant form of focal epilepsy in adults. Temporal lobe epilepsy is a far larger market than the ultra-orphan diseases of uniQure's past: refractory cases number in the hundreds of thousands across the U.S. and Europe, patients who continue to seize despite every available medication and for whom the only alternative is to have a piece of their brain surgically removed. It was, in other words, exactly the kind of large-orphan central nervous system target the post-Glybera strategy demanded.

Now look at how they structured the payment, because this is the masterclass. The total potential deal value was around €250 million. But uniQure paid only €46.3 million—roughly $55 million—in cash upfront.6 The remaining €203.7 million was not money that changed hands on day one. It was structured as milestone payments—what the industry affectionately calls "bio-bucks"—contingent on the program actually hitting specific clinical and regulatory targets: completing Phase I/II, advancing through Phase III, winning regulatory approval.6 And uniQure retained the option to pay up to a quarter of those milestones in stock rather than cash.6 In plain terms: uniQure paid a small, fixed amount for the option, and agreed to pay the big money only if and when the asset proved it actually worked. The downside was capped at $55 million; the large payments were entirely earned by success.

To appreciate just how disciplined that was, you have to remember the year. 2021 was the absolute peak of the biotech bubble—a frenzy of cheap money and astronomical valuations. In that same window, Novartis paid $800 million upfront (about $1.5 billion all-in) to acquire Gyroscope Therapeutics, and Sanofi paid roughly $1.0 billion upfront (about $1.225 billion total) for Amunix, a company whose lead assets were still preclinical.7 Against that backdrop of nine- and ten-figure cash payments flying out the door for early-stage science, uniQure secured an entire neurological program addressing a market of hundreds of thousands of patients for a cash outlay smaller than what some of its peers were spending on a single financing round. It refused to participate in the bubble pricing even while sitting on bubble-era cash. That is the behavior of a management team that learned, the hard way, exactly what it costs to bet wrong. And it set up the next move, which was even more counterintuitive: the realization that some of uniQure's most valuable assets weren't drugs at all.

VI. The "Hidden" Businesses Within uniQure: Platforms & Manufacturing

Public markets are blunt instruments. They look at a clinical-stage biotech and they value the cargo—the drugs in the trials, the binary readouts, the FDA decision dates. Will AMT-130 work? Yes or no? The whole company gets priced as one giant coin flip. But if you only watch the cargo, you miss the thing that actually makes uniQure durable. You miss the rails.

Let me explain what I mean by the "gene therapy railroad." A railroad company's value isn't really the specific freight sitting in any one car on any one day. It's the track, the rolling stock, the rights-of-way—the infrastructure that can carry any cargo, over and over, at low marginal cost. uniQure built exactly that kind of infrastructure for gene therapy, and its centerpiece is a proprietary technology platform called miQURE.

Here's the elegant idea behind it, in everyday terms. The early gene therapies, like Glybera and Hemgenix, work by adding a missing gene—you're broken, so here's a working copy. But a huge number of devastating diseases are caused not by a missing instruction, but by a toxic one—a mutant gene that actively produces a poisonous protein that slowly destroys cells. For those diseases, adding a good gene doesn't help; you need to silence the bad one. miQURE is a gene-silencing platform. It uses an AAV vector to deliver a small piece of genetic material—a micro-RNA—that acts like a precisely targeted muzzle, finding the messenger from the toxic gene and shutting it down before the poisonous protein can ever be made. In Huntington's disease, that toxic gene is mutant huntingtin. In temporal lobe epilepsy, the target is the overactive receptors driving the seizures. Same muzzle technology, different target.

And that is the entire point. Because the platform is modular, uniQure can keep the delivery vehicle, the manufacturing process, and the regulatory know-how constant, and simply swap out the therapeutic "cargo"—the specific micro-RNA—to aim at a new disease. Every new program doesn't start from a blank page; it starts from a validated, de-risked, reusable chassis. That collapses the time and cost of preclinical development and turns drug discovery from a series of independent miracles into something closer to a repeatable engineering process. That is the railroad.

But uniQure's most instructive lesson in hidden value wasn't the platform—it was the factory. To make AAV gene therapies at commercial scale, the company had built an 80,000-square-foot, state-of-the-art manufacturing plant in Lexington, Massachusetts. On paper, owning your own commercial-grade manufacturing looks like strength—vertical integration, control of your destiny. In practice, for a company that had just licensed away its only commercial product, that plant was an enormous, fixed, cash-incinerating liability. It cost a fortune to run whether or not it was producing anything for uniQure's own account.

So in July 2024, uniQure sold the Lexington facility to a contract manufacturer called Genezen.[^10] And the structure of that sale is the whole education. The headline price was a modest $25 million—but not in cash. It came as $12.5 million in Genezen Series C preferred stock and a $12.5 million convertible note.8 On its face, selling a state-of-the-art plant for $25 million in paper looks underwhelming. But the cash price was never the point. The point was what the transaction eliminated and what it created. The deal immediately retired roughly $50 million in debt that had been attached to the facility, and it cut uniQure's annual operating cash burn by about $40 million—extending the company's cash runway by years, eventually out toward the end of the decade, without raising a dime from shareholders.8

And uniQure didn't lose access to manufacturing. It became a meaningful equity holder in Genezen, with CEO Matt Kapusta taking a seat on Genezen's board, and it locked in a long-term strategic supply agreement under which Genezen would continue manufacturing Hemgenix and serve as the preferred manufacturer for uniQure's clinical pipeline.[^10] Read that again: uniQure converted a high-burn physical liability into a financial asset (equity in a growing CDMO), a partnership (a board seat and supply security), and a massive reduction in cash burn—all while keeping full operational continuity over the products it actually needed made. It took a millstone and turned it into a stake. That is the asset-light playbook executed about as cleanly as it gets, and it is the kind of move that only happens when the people running the company have internalized that survival is a function of cash runway. Which brings us to those people.

VII. Current Management: Matthew Kapusta's Tenure, Shareholding, & Incentives

In December 2016, Matthew Kapusta inherited a company in slow-motion crisis. Glybera was on its way to oblivion, the commercial story was a smoking ruin, and uniQure was, by most honest assessments, a cautionary tale about being first. Kapusta had come up through finance—he'd served as the company's chief financial officer before stepping up—and that background turns out to explain almost everything about the uniQure you've been hearing about for the last hour.9 A scientist-founder might have fallen in love with the technology and chased the next ultra-orphan moonshot. A financier looked at the balance sheet and asked a colder, more useful question: how does this company not run out of money, and how does it convert its genuine scientific assets into durable cash? Nearly every defining decision of the modern era—the CSL licensing deal instead of a self-funded launch, the royalty monetization, the disciplined Corlieve structure, the Genezen plant sale—bears the fingerprints of a CFO's mind running the show.9

That orientation shows up most clearly in how Kapusta is paid, and compensation structure is one of the most underrated tells in all of investing. His base salary sits at $676,700, with an annual cash bonus target of 60% of that base.9 But here's the part that matters: that entire bonus is tied 100% to corporate milestones—clinical trial readouts, regulatory filings, preservation of cash runway—rather than to any individual or subjective performance targets.9 In other words, the CEO does not get paid a cash bonus for looking busy or managing up. He gets paid when the programs advance, the filings go in, and the company stays solvent. The incentive is welded directly to the things long-term shareholders actually care about.

The equity alignment runs deeper still. As of early 2026, Kapusta personally held a substantial stake of 604,639 ordinary shares in the company.9 And there's a revealing episode in the insider-trading record that, far from being a red flag, is actually a portrait of incentive alignment working exactly as designed. In September 2025, Kapusta exercised options to acquire 226,316 shares at strike prices of $6.22 and $7.53—strikes set years earlier when the stock was a fraction of its later value—and sold them under a pre-arranged Rule 10b5-1 plan at average prices in the range of $39.20 to $45.30, realizing about $9.38 million.10 Now, insider selling sometimes spooks investors, but pause on what this actually shows. A Rule 10b5-1 plan is a pre-scheduled, automated selling program set up far in advance precisely to remove any hint of trading on inside information. And the math tells the real story: those options were nearly worthless when granted. They became worth millions only because the stock multiplied as the clinical and strategic value Kapusta was building got recognized by the market. His personal wealth and the company's success rose on the same rope.

Kapusta does not run this alone. The clinical engine is led by Dr. Walid Abi-Saab, the chief medical officer, who carries perhaps the most delicate portfolio in the company: the design of the trials and, above all, the intricate, high-stakes negotiations with the FDA that, as we're about to see, would whipsaw the stock by tens of percentage points in a single morning. And in a tell about where management believes this is all heading, in 2025 the company hired Kylie O'Keefe as chief customer and strategy officer—a role created specifically to map the global commercial strategy for a potential Huntington's launch. You do not bring in a senior commercial strategist for a drug you expect to fail. That hire was a statement of conviction.

None of which made the ride smooth. In early 2026, uniQure was hit with a securities class action lawsuit centered on its communications with the FDA—the kind of legal overhang that can paralyze a small company's leadership and derail its clinical focus precisely when steadiness matters most. It is a genuine risk and worth flagging plainly: litigation tied to regulatory disclosure can be expensive, distracting, and reputationally corrosive. What's notable is that Kapusta and the board managed to keep the clinical programs moving through the noise and the volatility, rather than letting the legal storm dictate the science. And the reason all of this management drama matters—the comp structure, the share stakes, the lawsuit, the steady hands—is that everything was riding on a single, devastating disease and one terrifying word from a regulator. So let's finally talk about Huntington's.

VIII. The Huntington's Disease Holy Grail: The June 17, 2026 Regulatory Breakthrough

Of all the diseases medicine has failed to crack, Huntington's occupies a special circle of cruelty. It is hereditary and autosomal dominant, which means if your parent has it, you have a coin-flip chance of inheriting it, and if you inherit the mutation, you will get the disease—there is no ambiguity, no maybe. It typically strikes in the prime of adult life, somewhere in the thirties or forties, and then proceeds, relentlessly and without remission, to dismantle the person: first the involuntary movements, then the cognitive decline, then the psychiatric collapse, over ten to twenty years, until it kills them. Patients often watch a parent die of it knowing precisely what is coming for them. And here is the part that makes the science so maddening and so tantalizing—we have known the exact cause since 1993. It is a single mutant gene producing a single toxic protein, mutant huntingtin. We have known the villain's name for over thirty years. And until now, there has been not a single treatment that slows the disease. Not one. Everything on the market merely blunts symptoms while the brain continues to die.

This is the disease AMT-130 was built to attack, and it deploys exactly the gene-silencing approach we discussed earlier. It's an AAV5 vector carrying a micro-RNA designed to find and silence the mutant huntingtin gene's message inside the neurons of the brain, choking off production of the toxic protein at its source. But there's a formidable wrinkle that makes this program unlike almost any drug you've encountered: you cannot deliver it with a pill or an IV, because the therapy has to get inside the brain itself, past the blood-brain barrier. So AMT-130 is administered through specialized micro-neurosurgery—neurosurgeons using MRI guidance to infuse the therapy directly into the deep structures of the brain in a procedure lasting many hours. This is genetic medicine delivered by a surgeon's hand. That delivery complexity is both a barrier and, as we'll see in the competitive analysis, a moat.

Now the rollercoaster. Through late 2025, the stock was a war zone of volatility, because the FDA signaled that the early Phase I/II data—data from a small number of patients, without the large randomized control group regulators traditionally demand—might not be enough to support an accelerated approval. The agency's message, formalized in March 2026, was that the available data were not sufficient and that uniQure should run a large, multi-year randomized trial.1 For a Huntington's patient, a multi-year confirmatory trial isn't a delay; it's a death sentence with a timeline. For uniQure shareholders, it gutted the near-term thesis.

So uniQure executed a maneuver that is, in hindsight, a small strategic masterstroke. If the front door in Washington was closing, it would try a different door entirely. The company announced plans to file first with the United Kingdom's regulator, the MHRA, targeting a submission in the third quarter of 2026, supported by three-year trial data showing a remarkable 75% slowing of disease progression—meaning treated patients declined at roughly a quarter of the expected rate.[^14]11 Think about what that 75% figure represents in human terms: for a disease that has never been slowed at all, slowing it by three-quarters isn't an incremental win, it's the difference between a decade of accelerating decline and something approaching a held line. And filing in the UK first did two things at once. It opened a genuine, independent path to commercialization that didn't depend on the FDA. And it applied quiet but real pressure on the U.S. agency—because no regulator wants to be the reason American patients get a breakthrough years after British ones.

Then the ground shifted in Washington. A leadership reshuffle swept the FDA. Vinay Prasad—a controversial figure whose tenure had drawn sharp criticism over several high-profile drug review decisions, and whom Wells Fargo analysts had specifically flagged as an obstacle to AMT-130's prospects—departed the agency.1 In the reshuffle, Karim Mikhail was named Acting Director of the Center for Biologics Evaluation and Research, the CBER division that rules on exactly this kind of therapy.1 The regulatory weather was changing.

And so we arrive at today, June 17, 2026. The FDA reopened the door. The agency confirmed it is now willing to consider the three-year data from the Phase I/II study as the primary basis for an accelerated BLA—precisely the path it had rejected three months earlier.1 uniQure announced it will submit that BLA in the third quarter of 2026.1 It was the regulatory U-turn the entire thesis had been waiting for, and it came stacked on top of designations AMT-130 had already accumulated—Regenerative Medicine Advanced Therapy, Breakthrough Therapy, and Fast Track—each one a previous signal that the FDA itself saw the promise even as it wrestled with the data.1 The market's verdict was instantaneous and violent: up over 70% before the bell.1 On Stocktwits, retail sentiment flipped from bearish to bullish overnight; one user floated a $120 price.1 Another, more soberly, called the move an overreaction and reminded everyone of the one fact that should anchor every reader of this story: the drug has not actually been approved yet.1 Both of them are, in their own way, right. And holding both of those truths at once is exactly the discipline this situation demands.

IX. Playbook: Business & Investing Lessons

Step back from the day's fireworks, and the uniQure story resolves into a handful of repeatable, transferable lessons that apply far beyond gene therapy.

The first is the railroad model itself: build modular platforms, not bespoke products. uniQure's enduring advantage isn't any single drug—drugs fail, and uniQure's first one failed commercially about as completely as a drug can. The advantage is the validated combination of a delivery system (the AAV5 vector) and a reusable gene-silencing cassette (miQURE) that lets the company point the same proven machinery at one new disease after another. When you turn drug development from a sequence of discrete biological gambles into a repeatable engineering process, you change the entire risk profile of the enterprise. Each new program inherits the de-risking of every program before it.

The second lesson is the art of non-dilutive financing, and this is where Kapusta's CFO instincts pay the biggest dividends. The cardinal sin of clinical-stage biotech is funding your pipeline by repeatedly selling stock—every financing round dilutes your earliest believers, and a company that survives ten years of dilution can leave its founding shareholders owning a sliver of their own success. uniQure threaded the needle by pairing early licensing (the CSL upfront) with royalty monetization (the HealthCare Royalty deal) to pull roughly $825 million of non-dilutive capital into the company—money that funded the pipeline without crushing equity holders.[^4]5 The principle generalizes: if you have a genuinely valuable asset, find ways to borrow against its future without selling your ownership of the present.

The third is turning liabilities into assets. The Lexington divestiture is the cleanest example you'll find of recognizing when vertical integration has flipped from strength to drag, and then unwinding it without losing what you actually needed. uniQure shed a $40-million-a-year cash burn and $50 million of debt while keeping operational control of its manufacturing through a supply agreement and even gaining an equity stake in the counterparty.8 The lesson isn't "outsource manufacturing." It's "ruthlessly re-examine which of your owned assets are still earning their place on the balance sheet."

And the fourth is regulatory optionality. uniQure's willingness to file in the UK ahead of the U.S. was not just a fallback; it was strategy. When you face resistance in one jurisdiction, geographic diversification gives you both a genuine alternative path to revenue and negotiating leverage against the regulator that's stalling you. A company with only one regulatory door is a hostage to whoever guards it. A company with two is a negotiator. These four lessons, taken together, are what let the historic pioneer avoid becoming a historical footnote.

X. Frameworks: Hamilton's 7 Powers & Porter's Five Forces

Let's war-game uniQure's competitive position with two of the sharpest tools in strategy, because the qualitative story only becomes an investment thesis once you can locate the durable advantage.

Start with Hamilton Helmer's 7 Powers. The most striking power here is switching costs, and in gene therapy they reach an almost absolute, biological extreme that has no equivalent in ordinary business. When a patient receives an AAV5-based therapy—Hemgenix, or a future AMT-130—their immune system mounts a response and develops neutralizing antibodies against the AAV5 capsid. Those antibodies persist. The practical consequence is staggering: that patient generally cannot receive another AAV5-delivered therapy for the rest of their life, because their body will destroy the vector before it can deliver its cargo. Read what that means competitively. The first company to successfully treat a patient with an AAV5 therapy doesn't just win that sale—it potentially forecloses every AAV5 competitor from ever serving that patient again. It's a one-and-done treatment that creates a one-and-done customer relationship, locked in by the patient's own immune system. There is no churn because there is, biologically, no possibility of churn.

The second power is the cornered resource. uniQure controls, through licensing and proprietary development, two genuinely scarce inputs: rights to the hyperactive Factor IX Padua variant that makes Hemgenix so potent, and the proprietary miQURE micro-RNA constructs at the heart of its CNS pipeline. These aren't commodities a competitor can simply buy or easily design around. The third power is process power—the decades of accumulated, proprietary know-how in baculovirus, insect-cell-based manufacturing, a method that can yield AAV vector at higher concentration and purity than the transient-transfection approaches many rivals rely on. Process power is the most modest of the three here, because manufacturing edges can erode, but combined with the other two it rounds out a defensible position.

Now run Porter's Five Forces over the specific arena of neurological gene silencing, and the picture gets even more favorable—almost suspiciously so. Rivalry is strikingly low, and not because uniQure out-competed everyone, but because the field is emptying out. The big players are walking away from the modality. 武田薬品工業株式会社 Takeda Pharmaceutical Company Limited exited AAV gene therapy entirely in April 2023, terminating its Huntington's partnerships in the process.12 アステラス製薬株式会社 Astellas Pharma Inc., in an early-2026 round of pipeline pruning, deprioritized its own preclinical Huntington's program to concentrate on neuromuscular assets.12 And while エーザイ株式会社 Eisai Co., Ltd. remains a neurology powerhouse, its weapon of choice is the monoclonal antibody Leqembi, an Alzheimer's drug, not gene therapy. The competitors who could most credibly challenge uniQure have chosen, one by one, to fight somewhere else—which is both an opportunity and, honestly, a yellow flag worth sitting with: when sophisticated players all exit a modality, a prudent investor asks whether they see something about the economics that the bulls are discounting.

The threat of new entrants is about as low as it gets in any industry. To challenge uniQure in Huntington's, a newcomer would need to fund multi-hundred-million-dollar clinical trials, develop specialized neurosurgical delivery systems, and clear the same brutal regulatory gauntlet—a near-impenetrable wall of cost, complexity, and time. The one force that genuinely cuts against uniQure is the bargaining power of buyers. Payers—insurers and national health systems—hold real power, and they will demand overwhelming proof of long-term durability before they reimburse a multi-million-dollar one-time therapy. We saw with Glybera what happens when the buyer simply has no framework to pay; that risk never fully disappears for any seven-figure cure. Suppliers and substitutes round out the analysis as relatively minor forces. The net read: a strongly defended competitive position whose principal vulnerability lives not on the supply side but on the demand side, in the wallets and willingness of the payers.

The single most important thing for a long-term investor to track through all of this is narrow. Not the daily stock gyrations, not the Stocktwits sentiment. Watch two things: the AMT-130 regulatory timeline—does the Q3 2026 BLA actually get filed, accepted, and move toward a decision in both the U.S. and UK—and the cash runway, the number that nearly killed this company once and that management has spent a decade fortifying. For a clinical-stage biotech, regulatory progress and months of cash on hand are the heartbeat. Everything else is commentary.

XI. Epilogue: The Horizon of Gene Therapy

So where does the railroad run from here? The immediate horizon is the dual submission—the BLA to the FDA and the marketing authorization application to the MHRA—both targeted for the third quarter of 2026, both for AMT-130 in Huntington's disease.1[^14] If even one of those lands, uniQure will have done what no one in the history of medicine has managed: deliver a treatment that actually slows the relentless march of Huntington's. The science we've known how to name since 1993 would finally have an answer.

But remember the railroad thesis. The whole point of building modular rails is that the cargo behind the locomotive keeps coming. Behind AMT-130 sits AMT-260, the temporal lobe epilepsy program acquired in the disciplined Corlieve deal, now advancing toward the clinic and aimed at a refractory patient population far larger than Huntington's. Behind that sits AMT-191, a program for Fabry disease, another inherited metabolic disorder, moving through early Phase I/II development. Each is a different cargo riding the same validated chassis—the same vector science, the same manufacturing know-how, the same regulatory muscle memory. If the platform thesis is right, these are not three independent coin flips; they're three draws from a deck that the company has spent twenty years learning to stack in its favor.

And that, in the end, is the real story of uniQure. It is the company that proved gene therapy could work, then proved—painfully, expensively, through a million-dollar drug sold exactly once—that working isn't the same as winning. The decade since has been a sustained tutorial in everything Glybera failed to teach the rest of the industry: that the platform matters more than the product, that capital allocation is a survival skill and not an afterthought, that a manufacturing plant can be worth more sold than owned, and that regulatory resilience means always having a second door. The pioneers of any frontier usually end up as footnotes—first to arrive, first to die, remembered mainly by the settlers who learned from their bones. uniQure spent ten years refusing that ending. Whether the Huntington's filing ultimately succeeds or stumbles, the company has already demonstrated the rarer thing: how to be first, fail, and still be standing when the future you predicted finally arrives.

References

-

QURE Stock Surges Over 70% After FDA Softens Stance On Huntington's Disease Gene Therapy — Stocktwits, 2026-06-17 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

European Medicines Agency Retrospective on Glybera: Lessons from the First Approved Gene Therapy — NIH PubMed, 2018-10-12 ↩↩↩↩↩↩↩

-

CSL Behring and uniQure Announce FDA Approval of HEMGENIX — CSL, 2022-11-22 ↩

-

FDA Approves First Gene Therapy for Hemophilia B Priced at $3.5 Million — Reuters, 2022-11-23 ↩

-

uniQure Announces Royalty Monetization Agreement with HealthCare Royalty for $375 Million Upfront — SEC Form 8-K, 2023-05-15 ↩↩

-

uniQure Acquires Corlieve Therapeutics to Expand into Temporal Lobe Epilepsy — GlobeNewswire, 2021-06-22 ↩↩↩↩

-

AAV Gene Therapy Landscape Shift: Takeda and Astellas Pipeline Updates — BioPharma Dive, 2026-04-15 ↩

-

uniQure Announces Sale of Lexington Manufacturing Facility to Genezen — SEC Form 8-K, 2024-07-23 ↩↩↩

-

uniQure's AMT-130 Shows 75% Slowing of Huntington's Progression at Three Years — NeurologyLive, 2026-06-17 ↩

-

AAV Gene Therapy Landscape Shift: Takeda and Astellas Pipeline Updates — BioPharma Dive, 2026-04-15 ↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube