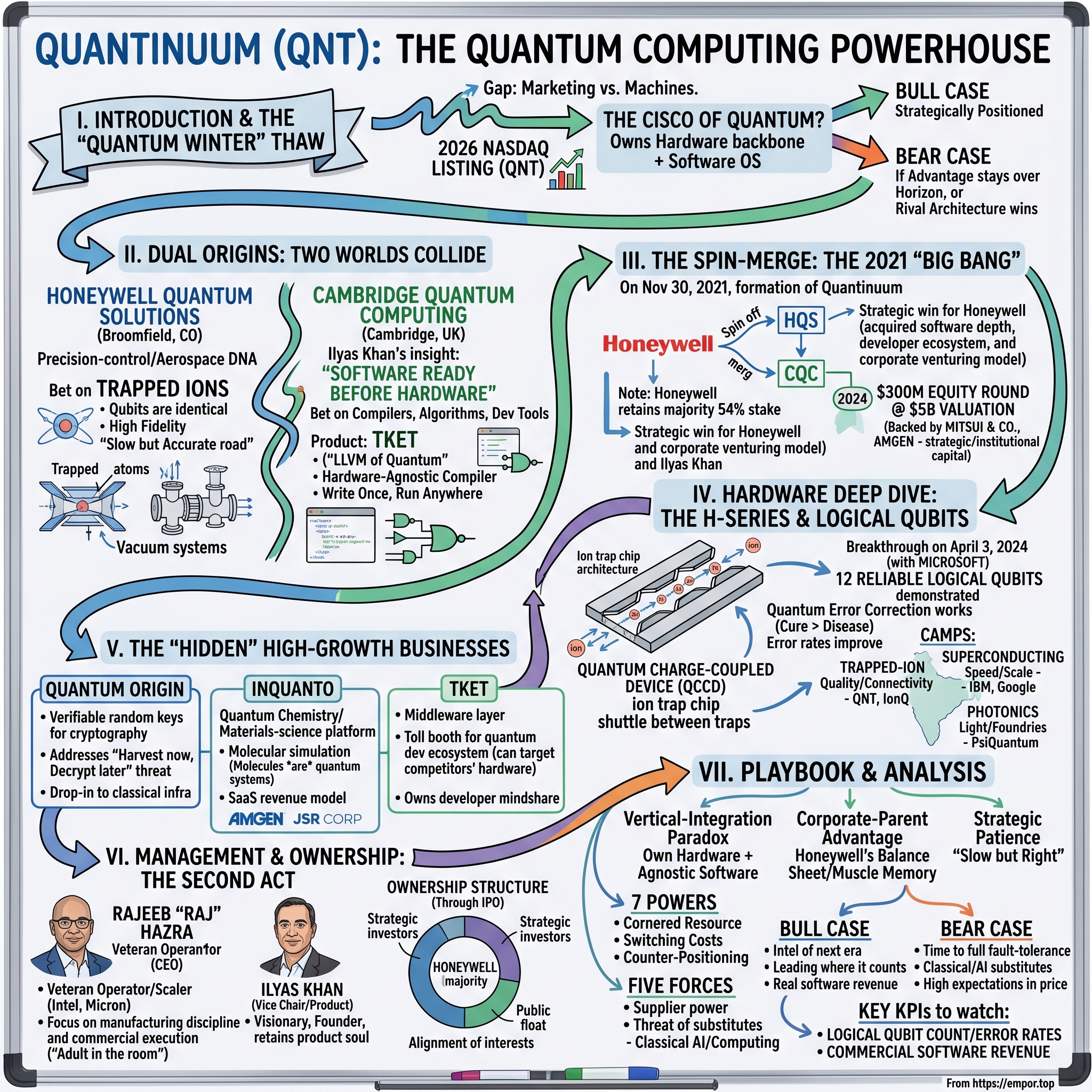

Quantinuum: The Quantum Computing Powerhouse

I. Introduction & The "Quantum Winter" Thaw

There is a particular kind of silence inside a quantum computing lab that has nothing to do with sound. It is the silence of expectation deferred. For the better part of a decade, the field had a reputation problem dressed up as a physics problem: dazzling press releases, qubit-count records that read like horsepower brochures, and a stubborn refusal of any of it to translate into a machine that did something a laptop could not. Venture capitalists who had piled into the first wave of quantum startups around 2020 and 2021 watched their public-market darlings get cut in half, then in half again. People started using a chilly little phrase—the "quantum winter"—to describe the gap between the marketing and the machines.

So when Quantinuum's shares opened for trading on the NASDAQ in 2026 under the ticker QNT, it was not merely another deep-tech listing. It was, depending on whom you asked, either the thaw that the believers had been promised, or the most expensive validation yet of a technology that has spent forty years being "ten years away." The company arrived on the public markets not as a plucky startup that had finally scraped together enough hardware to demo, but as something stranger and, frankly, more interesting: a company that was simultaneously the world's leading builder of a particular kind of quantum hardware and the owner of the software layer that a large slice of the entire industry—competitors included—used to program their machines.

That duality is the heart of the story, and it is the thesis we want to test in this episode. The most useful analogy is not to any quantum peer. It is to the early networking era. In the 1990s, Cisco won not because it built the fastest router in a vacuum, but because it sold the boxes that moved the traffic and the software—IOS—that ran on them, and it did so while the rest of the industry was still arguing about protocols. The question we keep circling is whether Quantinuum is the Cisco of quantum: the company that ends up owning both the backbone hardware and the de facto operating system of an entire computing paradigm. If that framing holds, QNT is one of the most strategically positioned deep-tech companies of its generation. If it doesn't—if quantum advantage stays perpetually over the horizon, or if a rival architecture leapfrogs trapped ions—then a great deal of the optimism baked into the listing was, to borrow a phrase, priced for a perfection that physics may not deliver on schedule.

To get there, we have to tell a genuinely unusual corporate-history story. It begins not in one garage but in two very different places at once: a sprawling industrial campus outside Denver where a company famous for thermostats and jet engines was quietly building the most precise quantum hardware on Earth, and a cluster of offices in Cambridge, England, where a former banker turned philosopher-entrepreneur bet that the software for quantum computers would be ready before the computers themselves. It runs through one of the most creative pieces of corporate financial engineering of the decade—the 2021 "spin-merge" that fused those two worlds—and into the moment in 2024 when a partnership with Microsoft turned the field's holy grail, error-corrected "logical" qubits, from a theoretical promise into a demonstrated reality.[^1][^2]

So let's rewind, all the way back to the unlikeliest of beginnings: an aerospace giant deciding, against every instinct of corporate America, to bet on the slow road.

II. Dual Origins: Two Worlds Collide

Picture the high plains north of Denver: Broomfield, Colorado, a place better known for tech office parks and big-box retail than for the frontiers of physics. Inside a Honeywell facility there, sometime in the early 2010s, a small group of engineers were doing something that, had it leaked to the company's own investors at the time, would have sounded faintly absurd. They were trapping individual electrically charged atoms in a vacuum, suspending them in mid-air with electromagnetic fields, and zapping them with precisely tuned lasers to nudge them into the fragile, ghostly states that quantum computing requires. This was a company whose brand lived on the wall of nearly every American home in the form of a round thermostat. Why on earth was it building qubits?

The answer is one of the great underappreciated facts of corporate strategy: Honeywell was never really a thermostat company. It was, and is, a precision-control and aerospace company that happened to also make thermostats. Its aerospace division had spent decades mastering exactly the disciplines that trapped-ion quantum computing demands—ultra-high vacuum systems, cryogenics, laser systems, and the kind of obsessive, milli-Kelvin environmental control that keeps a guidance system honest at forty thousand feet. The skills that let Honeywell build avionics that don't drift were uncannily close to the skills required to keep a quantum state from collapsing. Where a software startup would have had to acquire that capability at enormous cost, Honeywell already had it sitting in its industrial DNA. The quantum effort, run as Honeywell Quantum Solutions, was less a moonshot bolted onto the company than a natural extension of what the company was already extraordinarily good at: controlling physical systems with brutal precision.

And here is the decision that, in hindsight, defined everything. Around 2011 to 2014, while the loudest names in the field—the Googles and IBMs of the world—were pouring resources into superconducting qubits (tiny circuits chilled to near absolute zero, fast to operate but notoriously noisy and error-prone), Honeywell's physicists made a contrarian call. They bet on trapped ions instead. The trade-off was stark and unglamorous. Trapped-ion qubits are slower. They are harder to pack in large numbers. But they have two properties that, the Honeywell team argued, would matter far more in the long run: they are extraordinarily identical to one another—every ion of a given element is a perfect copy, where every manufactured superconducting circuit is a slightly flawed snowflake—and they hold their quantum state with far higher fidelity. In a field obsessed with qubit count, Honeywell chose to obsess over qubit quality. It was the deliberate choice of the slow, accurate road over the fast, noisy one, and it ran against the entire grain of how Silicon Valley likes to compete.

Now travel about forty-five hundred miles east, to Cambridge, England, and meet the other half of this company. In 2014, Ilyas Khan founded Cambridge Quantum Computing, and his founding insight was as counterintuitive in software as Honeywell's was in hardware. Khan was not a career physicist. He had spent years in finance, served as a fellow and stalwart supporter of mathematics at the University of Cambridge, and approached the field as someone fascinated by the commercial and intellectual architecture of what a quantum industry would need. His thesis, which sounded almost backwards at the time, was this: the software will be ready before the hardware. Everyone else assumed software was the easy part you'd write once the machines arrived. Khan bet that building the compilers, the algorithms, and the developer tools was itself a decade-long undertaking—and that whoever built that layer first would sit at the center of the entire ecosystem when the hardware finally caught up.

The concrete expression of that bet was a piece of software called TKET (pronounced "ticket"). The simplest way to understand TKET is by analogy to a thing that already quietly runs the classical computing world: LLVM, the compiler infrastructure that lets a programmer write code once and have it run efficiently on wildly different processors. TKET aimed to be the LLVM of quantum—a hardware-agnostic compiler that takes a quantum program and optimizes it to run on whatever physical machine you point it at, whether that machine uses trapped ions, superconducting circuits, or something else entirely. The strategic genius of this was subtle. By being deliberately hardware-neutral, Cambridge Quantum positioned itself to profit no matter which hardware approach eventually won. It was selling shovels to every prospector in the gold rush, and it didn't much care which claim struck gold.

Two companies, then, embodying two halves of a single radical idea. One had the world's most precise quantum hardware and no real software ecosystem to speak of. The other had a software ecosystem and developer mindshare but no hardware of its own to anchor it. Each was, in a sense, incomplete. The obvious move—obvious in retrospect, audacious at the time—was to put them together. But how do you merge a tiny British software startup with a unit buried inside a $100-billion-plus American industrial conglomerate without one simply swallowing and smothering the other? That question led to one of the most unusual transactions in recent corporate history.

III. The Spin-Merge: The 2021 "Big Bang"

Corporate marriages usually take one of two boring forms. Either a big company buys a small one outright and absorbs it, or two roughly equal companies merge as peers. What Honeywell and Cambridge Quantum did in 2021 was neither, and the structure itself tells you almost everything about how seriously Honeywell took the prize.

On November 30, 2021, the two combined to form Quantinuum, with Honeywell Quantum Solutions and Cambridge Quantum folded into a single new company.[^1] The mechanism was a "spin-merge"—Honeywell spun its internal quantum hardware division out of the mothership and simultaneously merged it with the independent Cambridge Quantum, rather than buying Cambridge Quantum and bolting it on as a subsidiary. The distinction is not legal hairsplitting. A spin-merge let Cambridge Quantum's culture, its founder, and crucially its hardware-agnostic commercial posture survive intact, while still giving Honeywell economic control. Honeywell emerged as the majority owner, holding a 54% stake in the combined entity.[^1] Ilyas Khan, the Cambridge founder, took a senior leadership role rather than being shown a polite exit, which is what usually happens to founders in a conglomerate acquisition.

Step back and look at what Honeywell actually pulled off here, because it is a masterclass in something most industrial giants are spectacularly bad at: corporate venturing. Honeywell had a world-class hardware division but lacked the software depth and the developer ecosystem to turn that hardware into a platform. Cambridge Quantum had exactly that software depth. Rather than write an enormous check to acquire it—a check that would have demanded a clean cash valuation in a market where quantum valuations were already getting frothy—Honeywell paid in kind. It contributed its hardware business and, in effect, traded roughly half the equity of that business for the software house. The conclusion we keep coming back to is that Honeywell essentially bought a leading quantum software company by trading away half of its hardware division, while still retaining majority control of the whole. It got the software ecosystem it lacked without draining its balance sheet, and it kept the steering wheel.

Was this a fire sale by Honeywell—a quiet admission that it didn't want to keep funding a speculative hardware unit alone—or a shrewd strategic carve-out? The evidence points firmly to the latter. A company conducting a fire sale does not keep 54% and install the combined entity as a long-term holding on its books.[^1][^11] What Honeywell did was convert an internal cost center, the kind of thing activist investors love to demand the spinning-off of, into a freestanding company that could raise outside capital, attract specialist talent who would never join a thermostat conglomerate, and command its own valuation—all while Honeywell retained majority economic exposure to the upside. It is corporate venturing as it is supposed to work, and almost never does.

The valuation story that followed validated the structure. In January 2024, Quantinuum raised $300 million in an equity round that valued the company at roughly $5 billion.1 To understand why that number was striking, you have to remember the carnage happening around it. The first generation of pure-play quantum companies had gone public via SPAC—the blank-check vehicles that flooded the market in 2020 and 2021—and the results had been brutal. 量子 peers like IonQ and Rigetti Computing had listed at lofty valuations on the promise of qubit-count roadmaps, then watched their shares crater as the gap between roadmap and revenue became impossible to ignore. The lesson the market took away was that quantum hardware was a money pit dressed up as a growth story. Against that backdrop, a private $5 billion mark for Quantinuum was a statement: this was a company being valued not on a SPAC-era promise but on demonstrated technical leadership and, increasingly, real commercial products.12

The investor roster reinforced the point. This was not retail-driven SPAC money chasing a ticker. The round drew in strategic and institutional capital, including a notable investment from Japan's 三井物産 Mitsui & Co., which took a stake as both a financial investor and a commercial partner with an eye on bringing quantum capabilities to its sprawling industrial network.[^6] When a 150-year-old Japanese trading house with that kind of due-diligence apparatus writes a check, it is a different quality of validation than a momentum trade.

But valuation and structure are scaffolding. The thing that actually had to be true—the thing that separated Quantinuum from every quantum company that had promised and underdelivered—was the hardware. Did the slow, accurate road actually lead somewhere the fast, noisy road couldn't? In 2024, the field got its answer.

IV. Hardware Deep Dive: The H-Series & Logical Qubits

To explain what Quantinuum's hardware actually does, let's start with the problem that has haunted quantum computing since its conception. Qubits are exquisitely, maddeningly fragile. A breath of stray heat, a flicker of electromagnetic noise, the faintest vibration—any of it can knock a qubit out of its delicate quantum state and corrupt the calculation. The deeper problem is that errors accumulate. Run a quantum program of any real length on a noisy machine and the errors pile up faster than the answer can emerge, like trying to whisper a long message down a line of people in a noisy room—by the end, the message is gibberish. For decades, this was the wall. You could build more qubits, but more noisy qubits just gave you more ways to be wrong.

Quantinuum's hardware answer is an architecture called the Quantum Charge-Coupled Device, or QCCD. The name is a mouthful, so here is the picture to hold in your head. Imagine a tiny chip with a network of microscopic channels etched into it, like a switchyard of railway tracks. Individual ions—the qubits—are the railcars, and electric fields are the switches and engines that physically shuttle those ions around the chip, parking them, bringing pairs together to perform an operation, then moving them apart again. Because the ions are physically moved to wherever they need to interact, rather than being locked in a fixed grid, the architecture achieves something rare: any qubit can be made to interact with any other qubit, with extraordinarily low error rates. This "all-to-all connectivity" plus the inherent quality of trapped ions is why Quantinuum's H-Series machines have consistently posted the highest fidelity in the industry. It is the slow, accurate road made physical: fewer qubits than the superconducting crowd, but each one of vastly higher quality.

That quality is what set up the breakthrough. On April 3, 2024, Microsoft and Quantinuum jointly announced that, running on Quantinuum's hardware with Microsoft's error-correction software, they had demonstrated 12 reliable logical qubits—and crucially, that these logical qubits had error rates dramatically better than the underlying physical qubits.[^2] This is the moment that deserves to be slowed down, because it is genuinely the most important thing that has happened in the field's commercial history.

Here is what a "logical qubit" means, in plain terms. Because individual physical qubits are unreliable, the long-standing theory of quantum error correction says you can bundle many noisy physical qubits together and use them, collectively, to encode a single logical qubit that is far more reliable than any of its parts—the same way a RAID array of imperfect hard drives can store data more reliably than any single disk. The catch, for years, was that nobody had actually made the trick work at scale. In practice the error-correction overhead tended to introduce more errors than it removed. The 2024 demonstration showed, for the first time in a convincing way, that the cure was now better than the disease: bundling physical qubits into logical ones actually made the system more reliable, not less.[^2] That is the inflection the entire industry had been waiting for. It was the moment quantum error correction stopped being a chalkboard promise and became an engineering reality.

It helps to map the competitive battlefield here, because the architecture wars define the investment case. There are, broadly, three camps. The trapped-ion camp—Quantinuum and IonQ—bets on quality and connectivity. The superconducting camp—IBM and Google—bets on speed and on the manufacturing scalability of chip fabrication, accepting higher noise in exchange for raw qubit counts and fast gate operations. And the photonics camp—most notably PsiQuantum—bets on using particles of light as qubits, with a thesis built around eventually fabricating millions of qubits in conventional semiconductor foundries. Each approach has a coherent argument. But the logical-qubit demonstration handed the trapped-ion camp, and Quantinuum specifically, a powerful talking point: when the metric that finally matters—reliable, error-corrected computation—came into focus, the high-fidelity approach was first across a line that the high-count approaches had not yet reached.

This is precisely why the enterprise customers who matter began to gravitate toward Quantinuum. When JPMorgan Chase explores quantum algorithms for portfolio optimization and risk, or when BMW investigates quantum chemistry for better battery materials, those institutions are not chasing the biggest qubit headline. They are looking for the machine that gives a trustworthy answer, because an unreliable answer in finance or materials science is worse than no answer at all. The high-fidelity approach is, in effect, an enterprise-trust strategy disguised as a physics preference. Quantinuum was selling correctness in a field that had spent a decade selling spectacle.

And yet—a hardware company that lives only on hardware in a field this early would be a cash-incinerating gamble. The most underappreciated part of the Quantinuum story is that, while the world fixated on logical qubits, the company had quietly built a set of businesses that generate revenue today, from technology that doesn't require waiting for fault-tolerant quantum computers to arrive. That is where the story gets unexpectedly commercial.

V. The "Hidden" High-Growth Businesses

Here is a riddle that captures the cleverest part of Quantinuum's strategy. How does a company sell quantum products to customers who don't have, and won't soon have, a useful quantum computer? The answer is that Quantinuum figured out how to extract value from quantum processes and quantum insights and package them for the classical world that exists right now. Three businesses embody this, and together they transform the company from a pure science bet into something with the texture of a software company.

Start with Quantum Origin, launched in December 2021 as what the company described as the world's first commercial product built using a quantum computer.[^8] The product sounds almost too elegant. Quantum Origin uses a quantum computer to generate cryptographic keys with verifiable, provable randomness—genuine quantum unpredictability rather than the pseudo-randomness that classical computers fake with algorithms. And the beautiful part is the delivery: those quantum-hardened keys can be dropped into existing classical infrastructure, today, with no quantum computer required on the customer's end. You sell the output of your quantum machine without making anyone buy a quantum machine.

Why would a customer care? Two words that keep chief information security officers awake at night: "harvest now, decrypt later," sometimes called store-now-decrypt-later, or SNDL. The threat is chillingly simple. Adversaries are already vacuuming up and storing vast quantities of encrypted data—financial records, state secrets, health information—that they cannot crack today. The bet is that a future, large-scale quantum computer will be able to break today's encryption, at which point all that hoarded data becomes readable retroactively. For any data that must stay secret for years or decades, the threat is not in the future; it is now, because the data is being stolen now. Quantum Origin sells into that fear with a product that strengthens defenses immediately. It is, in a sense, Quantinuum monetizing the very anxiety that its own industry's eventual success would create—an exquisite piece of strategic positioning.

The second hidden business is InQuanto, a quantum chemistry and materials-science platform.[^7] If you want to know where quantum computing will likely deliver its first world-changing economic value, most physicists will point to chemistry. The reason is poetic: molecules are quantum systems, so simulating them on a classical computer is like trying to model an ocean one water molecule at a time—the complexity explodes exponentially. A quantum computer, being itself a quantum system, is naturally suited to the task. InQuanto packages this capability as a platform that pharmaceutical and materials companies can use to explore molecular simulation. The partner roster signals the seriousness: the biotechnology company Amgen has worked with Quantinuum on applications in its domain, and Japan's JSR株式会社 JSR Corporation, a major materials and semiconductor-chemicals firm, partnered on materials-science applications in 2022.[^9] InQuanto matters strategically because it is, at its core, a software-as-a-service revenue model living inside a hardware-heavy company—recurring, higher-margin, and far less capital-intensive than building machines. It is the kind of revenue that public-market investors understand and reward.

The third piece brings us back to where Cambridge Quantum started: TKET, the hardware-agnostic compiler. Recall its design philosophy—write once, run on any quantum machine. The strategic consequence in 2026 is remarkable. Quantinuum owns the middleware that a large community of quantum developers uses to write programs, and because TKET is hardware-neutral, those developers use it to target competitors' hardware as well as Quantinuum's own. Think about the positioning that creates. Whether a developer ultimately runs their job on an IonQ machine, an IBM machine, or a Quantinuum machine, there is a meaningful chance the program passed through Quantinuum's compiler on the way. The company sits at a toll booth on the road that leads to all the destinations, not just its own. This is the clearest expression of the Cisco analogy we opened with: own the operating layer, and your relevance no longer depends solely on winning the hardware war.

There is a tension buried in all this that we'll return to in the analysis—being the neutral toll-collector while also running one of the destinations is a genuinely double-edged position. But commercially, the three businesses do something vital for the investment story: they give Quantinuum revenue, customer relationships, and recurring software economics while the long fault-tolerant hardware dream matures. They are the bridge across the quantum winter. The question of whether that bridge is wide enough to support a multi-billion-dollar valuation brings us to the people steering the company.

VI. Management & Ownership: The Second Act

Every deep-tech company eventually faces the same crossroads, and it usually arrives at the worst possible moment—right when the science starts working. The founders and physicists who got you there are often not the operators who can scale you into a real business. Honeywell and Quantinuum's board saw this crossroads coming, and in February 2023 they made a move that told you exactly what kind of company they intended Quantinuum to become.

They hired Rajeeb "Raj" Hazra as chief executive.[^4] Hazra was not a quantum physicist with a charismatic vision and a TED talk. He was, by background, an operator and a scaler—a veteran of Intel, where he had run the data-center and high-performance-computing business, and later a senior executive at Micron, the memory giant. In other words, the board went out and hired the "adult in the room": someone whose entire career had been about taking advanced computing technology and turning it into a manufacturable, sellable, repeatable business at industrial scale. The signal was unmistakable. Quantinuum had reached the point where the binding constraint was no longer "can we do the physics" but "can we build a company." Bringing in a Hazra over, say, another celebrated researcher was a declaration that the company's second act would be about operations, manufacturing discipline, and commercial execution—precisely the muscles that Honeywell's industrial heritage had always prized.[^4]2

Crucially, the visionary did not leave. Ilyas Khan, the Cambridge Quantum founder, transitioned into a Vice Chair and chief product role, retaining stewardship of the company's product direction and its intellectual soul while handing the operational reins to Hazra.[^1] This is the rare and healthy founder-CEO division that so many companies attempt and so few execute well: the visionary stays close to the product and the long-term technology bets, while a seasoned operator runs the machine. It works only when egos cooperate and the board enforces clarity of role, and the fact that Quantinuum structured it this way—rather than pushing the founder out or letting the founder cling to operations he was not suited for—speaks to a certain organizational maturity inherited from its industrial parent.

The ownership structure is where the alignment story gets genuinely interesting, and it is the part long-term investors should study most closely. Through the IPO, Honeywell remained the majority owner, having entered the public listing as the dominant shareholder by virtue of the original 54% stake.[^1][^10] This is unusual and consequential. Most newly public companies are controlled by founders, venture funds, or a dispersed float. Quantinuum is, in effect, a publicly traded company with a $100-billion-plus industrial conglomerate as its anchor shareholder. That brings patient, deep-pocketed capital and industrial credibility—but it also means minority public shareholders are, in a real sense, riding alongside Honeywell rather than steering. The interests are broadly aligned because Honeywell's upside is the same upside public investors are buying, but the control dynamic is one to watch.

Around that anchor sit the strategic investors who validated the private rounds—Mitsui & Co. and Amgen among them—whose presence is as much about commercial partnership as financial return.[^6] When your shareholders are also your customers and channel partners, alignment runs deeper than a quarterly stock price; Mitsui wants quantum capability for its industrial network, Amgen wants it for drug discovery, and both have an incentive to see the platform succeed commercially, not just to flip the shares. The post-IPO lock-up arrangements—the standard provisions that prevent insiders and pre-IPO holders from dumping stock immediately after listing—were structured to keep this coalition intact through the early public-market period, though the specific terms beyond the customary windows were not separately disclosed in detail.3

So the picture is of a company governed for the long haul: an industrial parent holding majority control, a seasoned operator in the CEO chair, a founder kept close to the product, and strategic investors with skin in the commercial game. Whether that alignment translates into durable competitive advantage is the question the playbook section exists to answer.

VII. Playbook: Business & Investing Lessons

Strip away the physics, and Quantinuum's story offers a set of strategic lessons that travel far beyond quantum computing. Three stand out, and each is double-edged in a way that rewards careful thought.

The first is the vertical-integration paradox. Quantinuum simultaneously owns the best hardware and sells the hardware-agnostic software layer that runs across everyone's machines. The bull reading is that this is the strongest possible position—you capture value whether the industry standardizes on your hardware or fragments across many vendors. But notice the tension. TKET's value to the broader developer community depends on its neutrality; developers trust it precisely because it is not a thinly veiled funnel to Quantinuum's own machines. The moment Quantinuum is perceived to tilt the compiler toward its own hardware, the neutrality that makes TKET valuable erodes, and rivals gain a reason to build or fund alternatives. So the company must perpetually walk a tightrope: extract strategic advantage from owning the operating layer while scrupulously preserving the openness that gives that layer its reach. It is a genuinely double-edged sword, and managing it is an ongoing test of corporate discipline, not a one-time structural win.

The second lesson is the corporate-parent advantage, and it is the cleanest contrast with the company's peers. The first wave of quantum pure-plays—the SPAC cohort—shared a structural weakness: they were startups trying to do industrial-grade hardware engineering on venture timelines and venture balance sheets. Building ultra-high-vacuum, laser-controlled, cryogenically stabilized machines is not a "move fast and break things" endeavor; it is aerospace-grade manufacturing, and it eats capital for years before it pays. Honeywell handed Quantinuum two things those startups could not buy at any speed: a balance sheet deep enough to fund the slow road without flinching at every down quarter, and decades of institutional muscle memory in precision manufacturing. The takeaway for investors and operators alike is that in capital-intensive deep tech, who your parent is can matter as much as how clever your science is. The startups had to choose between running out of money and cutting corners; Quantinuum had to do neither.

The third lesson is strategic patience, and it is the most countercultural. The entire ethos of modern technology investing rewards speed, scale, and visible momentum—qubit-count records, splashy roadmaps, the "fast and noisy" path. Honeywell's original 2011-era bet on trapped ions was a bet on "slow but right." For years that looked like a disadvantage; trapped-ion machines had fewer qubits and made for worse headlines. But the logical-qubit breakthrough revealed the wisdom of optimizing for the metric that would ultimately matter—reliability—rather than the metric that generated near-term attention.[^2] The investing lesson is uncomfortable precisely because it is so hard to act on: sometimes the technically correct path looks like falling behind for a long time before it looks like winning, and the discipline to fund "slow but right" through years of unflattering comparison is rare. It requires a shareholder base patient enough to allow it—which loops back to why the conglomerate-parent structure and the strategic investor coalition matter so much.

These three lessons—the integration tightrope, the parent's balance sheet, and the patience to be slow-but-right—are the load-bearing pillars of the bull case. But every pillar casts a shadow, and a serious investor has to war-game the ways each could fail. That is the work of the next section.

VIII. Analysis: 7 Powers & Bear vs. Bull

Let's run Quantinuum through the frameworks that disciplined investors use to separate durable advantage from temporary lead, starting with Hamilton Helmer's 7 Powers, then Porter's Five Forces, and ending with the honest bull-and-bear debate.

Cornered Resource. Helmer's idea of a cornered resource is access to a coveted asset on terms others can't match. Quantinuum's cornered resource is twofold and unusually deep: the accumulated intellectual property spanning both the QCCD hardware architecture and the TKET software stack, and—more importantly—the specialized human capital. The pool of people on Earth who can build and operate trapped-ion quantum computers at the frontier is vanishingly small, and Quantinuum assembled an outsized fraction of it by fusing Honeywell's hardware physicists with Cambridge Quantum's software and algorithms talent.[^1] You cannot simply hire this team into existence; it took two institutions a combined two decades to assemble. That is a real, defensible cornered resource—though it is worth flagging that talent walks, and in a field this hot, retention is a live risk.

Switching Costs. Once an enterprise builds its quantum workflows on TKET and integrates Quantinuum's tools into its research pipelines, migrating away becomes painful—code must be rewritten, teams retrained, validated results re-validated on new tooling. This is the classic enterprise-software moat, and it is the most underrated of Quantinuum's powers because it accrues quietly with every developer who learns the stack. The deeper TKET embeds in corporate and academic workflows, the higher the wall.

Counter-Positioning. This is the subtlest and most interesting power in the analysis. The "big tech" quantum efforts—Google and IBM—are divisions inside enormous companies with sprawling priorities, and both committed heavily and publicly to superconducting hardware. Quantinuum is counter-positioned as the focused, hardware-agnostic-at-the-software-layer specialist that can credibly serve customers regardless of which hardware wins, precisely because it is not structurally wedded to defending a single big-company architecture bet. A giant cannot easily copy this posture without implicitly conceding doubts about its own hardware program. That said, counter-positioning against players with effectively unlimited R&D budgets is a power with a shelf life; if Google or IBM's approach achieves its own fault-tolerance breakthrough at scale, the positioning advantage narrows fast.

Now Porter's Five Forces, briefly, because two of them are sharp. Bargaining power of suppliers is a real concern: trapped-ion systems depend on highly specialized lasers, ultra-high-vacuum equipment, and precision components supplied by a thin roster of vendors. A constraint or price shock in that supply chain—a single specialized laser maker raising prices or facing a backlog—could pinch the hardware roadmap, and the supplier concentration here is genuinely narrow. Threat of substitutes is the existential one, and it is not another quantum company. It is classical computing getting better. Every year, classical high-performance computing and, increasingly, AI-driven simulation chew into the problems that quantum was supposed to solve first. If a clever classical or AI method cracks a chemistry or optimization problem before quantum can, the quantum value proposition for that use case evaporates. The substitute threat is the bear case's sharpest weapon.

So let's state the bull and bear cases plainly.

The bull case: Quantinuum becomes the foundational layer of an entirely new computing era—the Intel of the next fifty years. The logical-qubit milestone proved the technology is real and that the high-fidelity approach is ahead where it counts.[^2] The hidden businesses—Quantum Origin, InQuanto, TKET—generate growing revenue today, giving the company a commercial bridge across the quantum winter that pure-play rivals lack.[^7][^8] The ownership structure provides patient industrial capital that startups can only dream of. And the switching costs and cornered-resource powers compound with time. If quantum advantage arrives even roughly on the timeline the optimists project, QNT is positioned to sit at the center of it, collecting tolls on hardware and software alike.

The bear case is equally coherent and should not be waved away. Quantum advantage has been "ten years away" for decades, and it may remain so. Demonstrating 12 logical qubits is a milestone, but the road from there to the thousands or millions of logical qubits needed for the world-changing applications is long, and nobody can credibly promise the timeline.[^2] Meanwhile, classical AI is advancing at a blistering pace and may solve the most valuable chemistry and optimization problems first, hollowing out quantum's commercial rationale before the machines are ready. The company's revenue today, while real, is modest against a multi-billion-dollar valuation—meaning the stock embeds enormous expectations about a future that physics has not yet guaranteed.12 And majority control by a single industrial parent, however patient, concentrates governance risk in ways minority shareholders cannot influence.

If you want to track which case is winning, ignore the qubit-count headlines and watch a small number of things. The first and most important KPI is logical qubit count and logical error rates over time—the genuine measure of progress toward useful, fault-tolerant computation, and the metric on which the entire thesis ultimately rests.[^2] The second is commercial revenue traction in the software businesses—Quantum Origin, InQuanto, and TKET-related revenue—because that is the proof that the company can monetize the bridge years before full fault tolerance arrives.[^7][^8] If logical qubits scale and software revenue compounds, the bull case is building. If logical-qubit progress stalls or the software revenue plateaus, the bear case gains the upper hand. Those two dials, more than any press release, will tell the story.

That tension—between a proven technical lead and an unproven commercial timeline—is exactly what the public markets had to price when QNT began trading. Which brings us to the verdict.

IX. Epilogue & Final Grading

Was QNT priced for perfection? In an honest sense, every frontier deep-tech IPO is. The market cannot value a company like Quantinuum on its current cash flows the way it might value a mature industrial; it has to value it on a probability-weighted vision of a future that may arrive in five years, in twenty-five, or—the bear's whisper—never in the form promised. The 2026 listing asked public investors to underwrite that uncertainty, and the price embedded a meaningful chunk of optimism about logical-qubit scaling and commercial adoption that remains, by definition, unproven.2[^10] What can be said with confidence is that the company arrived on the public markets with something most of its predecessors lacked: a genuine technical milestone behind it, real if modest revenue, and an industrial backbone underneath it. Whether that justified the valuation is a judgment each investor must make against their own time horizon and risk tolerance—and against the two KPIs that will keep telling the real story long after the IPO headlines fade.

The more durable lesson of this story may have nothing to do with quantum computing at all. It is about Honeywell, and about what other conglomerates can learn from the "spin-merge." For decades, the conventional wisdom held that big industrial companies are where promising technologies go to be smothered—starved of focus, drowned in bureaucracy, valued at a conglomerate discount. Honeywell did something different. It recognized that its quantum hardware division was a world-class asset trapped inside a structure that could neither properly value it nor give it the software ecosystem it needed. So instead of either keeping it buried or selling it off, Honeywell engineered a third path: it merged its hardware unit with the software house it lacked, gave the combination an independent identity and the freedom to raise its own capital and attract its own specialists, and retained majority economic exposure to the upside.[^1] It turned a hidden internal asset into a public company without losing control of it.

That playbook—identify the crown jewel buried in the conglomerate, fuse it with the complementary capability it lacks, set it free to attract capital and talent, and keep majority control—is a template that every diversified industrial giant with a promising-but-stranded technology unit should study. Whether or not Quantinuum becomes the Cisco of quantum, Honeywell has already demonstrated something rarer than a quantum breakthrough: a large, old industrial company creating, rather than destroying, frontier value. The thaw in the quantum winter, if it holds, will have begun in the unlikeliest of places—a precision-control company that understood, long before its rivals, that in quantum computing as in aerospace, the prize goes not to the fastest but to the one who is willing to be slow, and right.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube