QUALCOMM: The Story of Mobile's Most Essential Company

I. Introduction & Episode Roadmap

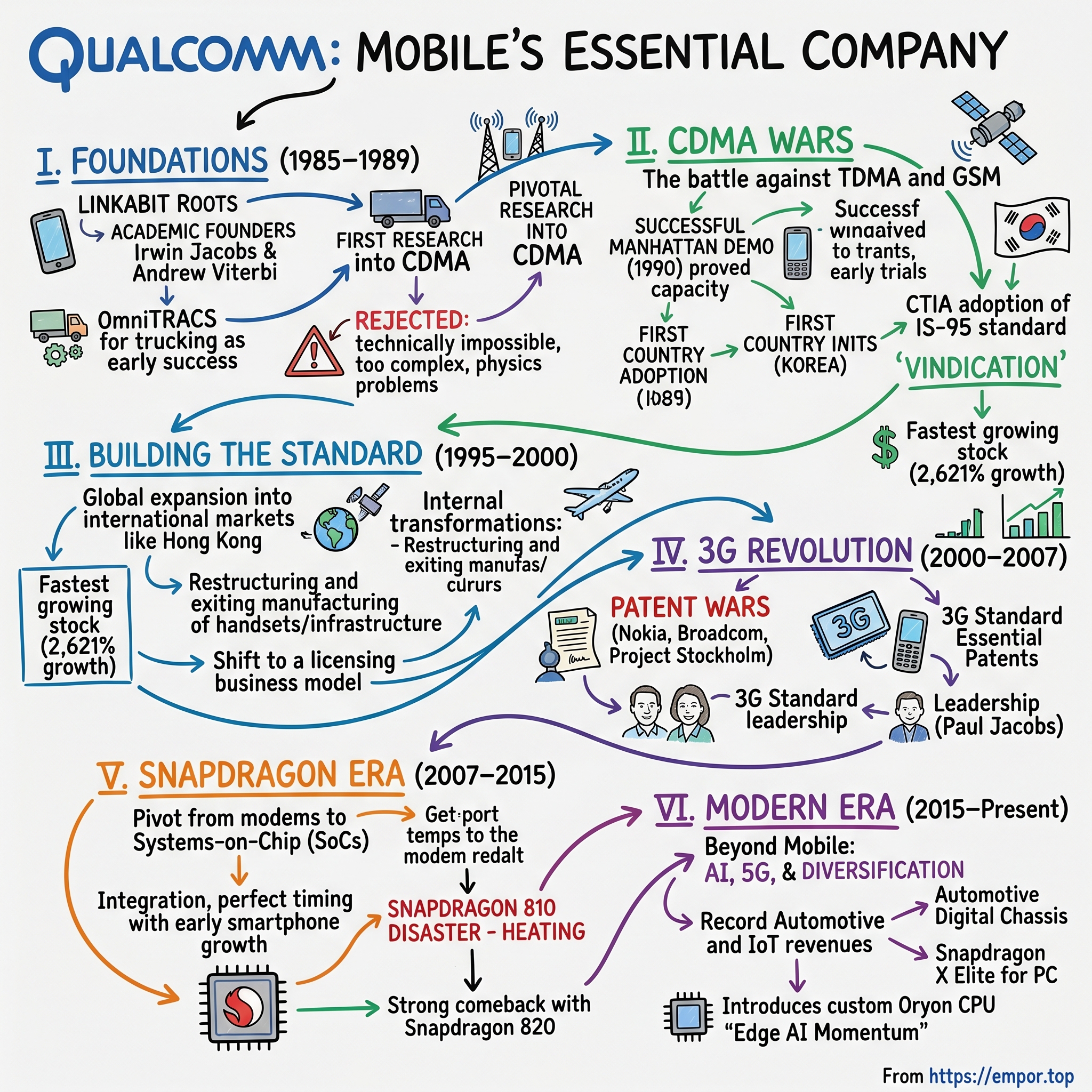

Picture this: It's 1989, and the cellular industry's biggest players—Ericsson, Nokia, Motorola—have just unanimously rejected a small San Diego company's proposal for a new wireless technology called CDMA. The Cellular Telecommunications Industry Association declares it technically impossible, too complex for commercialization, suffering from insurmountable physics problems. That company was Qualcomm, and within a decade, every single 3G network on Earth would run on their "impossible" technology.

Today, Qualcomm generates $39 billion in annual revenue, commands a market cap north of $160 billion, and collects royalties on virtually every smartphone sold globally. The company that started by helping truckers communicate via satellite has become the foundation layer of mobile computing—owning patents critical to 5G, 4G, CDMA2000, TD-SCDMA, and WCDMA standards. If you've made a phone call, sent a text, or streamed a video on a mobile device in the last two decades, you've used Qualcomm technology.

But here's the fascinating question: How did a company founded by academics with zero experience in consumer electronics build one of the most powerful patent portfolios in technology history? How did they convince an entire industry to abandon existing standards and adopt their untested approach? And perhaps most intriguingly—how did they structure a business model where competitors have no choice but to pay them billions in licensing fees, even as those same competitors desperately try to design around their patents? The numbers tell one story: $38.96 billion in fiscal year 2024 revenue, Non-GAAP EPS of $10.22, reflecting 21% growth, and a licensing business that prints money with 72% operating margins. But the real story—the one that explains how a company born from academia became the toll collector for the entire mobile industry—begins not in a corporate boardroom, but in the classrooms of MIT and the research labs of UC San Diego.

This is a tale of technical conviction against overwhelming skepticism, of patent wars that reshaped global telecommunications, and of a business model so controversial that regulators worldwide have spent decades trying to break it. It's about how seven engineers transformed an "impossible" idea into the foundation of modern connectivity, and how they built a company that has become, quite literally, unavoidable.

We'll trace Qualcomm's journey from its academic origins through the CDMA wars that nearly killed it, the 3G revolution that vindicated it, the Snapdragon era that diversified it, and into today's AI-powered future where it's attempting perhaps its most ambitious pivot yet: from enabling mobile phones to enabling all computing at the edge. Along the way, we'll unpack the strategic playbook that turned technical superiority into market dominance, examine the patent machine that generates billions with minimal marginal cost, and assess whether Qualcomm can maintain its stranglehold as the industry evolves beyond smartphones.

The structure ahead mirrors the company's own evolution—from pure research to commercial breakthrough, from infrastructure provider to chip designer, from mobile specialist to edge computing platform. Each phase reveals new layers of strategic brilliance and competitive brutality. Because understanding Qualcomm isn't just about understanding wireless technology—it's about understanding how standards get set, how technical moats get built, and how a company can position itself to tax an entire industry's innovation.

II. The Academic Founders & Linkabit Origins

The conference room at MIT's Research Laboratory of Electronics hummed with the particular energy of academic discovery. It was 1959, and Irwin Jacobs had just defended his doctoral thesis on sequential decoding—a topic so esoteric that even his advisors wondered about its practical applications. Nobody in that room could have imagined that this soft-spoken engineer from New Bedford, Massachusetts, would one day hold patents worth more than most countries' GDP.

Jacobs' path to Qualcomm began not in industry but in academia. After completing his B.S. from Cornell in electrical engineering, he'd pursued his Masters (1957) and Doctorate (1959) at MIT, immersing himself in information theory—the mathematical framework Claude Shannon had pioneered just a decade earlier. While his classmates chased jobs at Bell Labs and IBM, Jacobs became fascinated by a different question: How could you transmit information reliably over noisy channels? His doctoral work on sequential decoding would become the theoretical foundation for everything that followed.

In 1966, Jacobs accepted a professorship at the newly established University of California, San Diego. The move to La Jolla wasn't just geographical—it represented a shift from pure theory to applied research. UCSD was hungry, ambitious, willing to blur the lines between academia and industry. It was here that Jacobs met Andrew Viterbi, another professor who'd developed the Viterbi algorithm—a breakthrough in convolutional code decoding that would later become fundamental to digital communications. Together, they co-authored "Principles of Communication Engineering," a textbook that would educate a generation of wireless engineers.

But textbooks don't build industries. In 1968, frustrated by the gap between their research and real-world applications, Jacobs and Viterbi made a decision that would reshape telecommunications: they founded Linkabit, a consulting company that would bridge academia and defense contracting. The name itself was an engineer's pun—linking bits of information—but the ambition was serious. They would take the most advanced communication theories and turn them into working systems.

Linkabit became a kind of graduate school for entrepreneurial engineers. The company developed micro-coded multi-satellite terminals for the military, Very Small Aperture Terminals (VSATs) for commercial satellite communications, and the VideoCipher TV scrambler that would enable HBO and other premium channels to protect their content. The culture was unique—part university lab, part startup, part defense contractor. Engineers were encouraged to publish papers, pursue wild ideas, fail fast, and spin out their own companies if they discovered something worth commercializing.

By 1980, Linkabit had grown to 1,400 employees and attracted the attention of M/A-COM, a Massachusetts-based defense contractor that acquired it for $25 million. But corporate ownership chafed at the entrepreneurial culture Jacobs and Viterbi had cultivated. Decisions that once took hours now required months of committee meetings. Innovation slowed. The academic freedom disappeared. By 1985, Jacobs had seen enough. At age 52, when most executives eye retirement, he decided to start over.

The founding team of Qualcomm reads like a Linkabit reunion: Irwin Jacobs, Andrew Viterbi, Harvey White, Adelia Coffman, Andrew Cohen, Klein Gilhousen, and Franklin Antonio. Each brought specific expertise—Viterbi in algorithms, Gilhousen in systems engineering, Antonio in software—but they shared a common philosophy inherited from their academic roots: the best solution should win, regardless of politics or market momentum.

The name "Qualcomm" came from a brainstorming session in Jacobs' living room. They wanted something that captured their focus on excellence and communications. "QUALity COMMunications" was almost embarrassingly straightforward, but it stuck. The founders would later joke that they spent more time incorporating the company than naming it—a reflection of their engineering bias toward building over branding.

Initial funding came from the founders' own pockets—$3.5 million total, with Jacobs putting in the largest share. They leased 8,000 square feet in a Sorrento Valley office park, hired a handful of engineers, and faced a fundamental question: What problem should we solve first? Unlike most startups that begin with a product looking for a market, Qualcomm began with capabilities looking for applications. They knew how to manipulate information theory, how to squeeze signals through noisy channels, how to make the impossible possible. They just needed to figure out where to apply it.

Within six months, four distinct projects emerged, each reflecting the founders' belief that superior technology would eventually win: a portable satellite communications terminal for Kodak, consulting work for Hughes Aircraft, the OmniTRACS system for trucking, and—almost as an afterthought—some research into applying military spread-spectrum techniques to civilian cellular communications. That last project, initially funded by selling truck tracking systems, would eventually consume the company and revolutionize global communications.

The Linkabit heritage gave Qualcomm three critical advantages that would define its trajectory. First, the founders understood both the theory and practice of communications—they could prove mathematically why something would work before building it. Second, they'd learned how to navigate government contracts and standards bodies, skills that would prove invaluable in the coming CDMA wars. Third, and perhaps most importantly, they believed that technical merit could overcome entrenched interests—a conviction that would be tested when they challenged the entire cellular industry.

Looking back, the academic origins explain much about Qualcomm's culture and strategy. The company approaches problems like professors approaching research: define the theoretical limits, prove the optimal solution, then engineer toward it. They publish papers, contribute to standards, and believe that intellectual property is the highest form of competitive advantage. It's a profoundly different model from the "move fast and break things" ethos of Silicon Valley—Qualcomm moves deliberately and patents everything.

III. Early Years: Satellites, Trucking & Finding Product-Market Fit (1985–1989)

The Schneider National dispatch center in Green Bay, Wisconsin, operated like a military command post circa 1987. Walls of paper maps marked with colored pins tracked thousands of trucks across America's highways. Dispatchers shouted into radios, trying to reach drivers who might be anywhere within a 500-mile radius. A loaded truck sitting idle because dispatch couldn't find it cost $300 per day. Multiply that inefficiency across 100,000 long-haul trucks, and you had a billion-dollar problem waiting for a solution.

Klein Gilhousen saw the opportunity first. The former Linkabit engineer had been working on satellite communications for the military when he realized the same technology could solve trucking's fundamental problem: knowing where your assets were and being able to communicate with them anywhere. But there was a catch—existing satellite systems required dish antennas the size of umbrellas, hardly practical for trucks barreling down Interstate 80 at 70 miles per hour.

Qualcomm's solution was elegant: use spread-spectrum technology borrowed from military communications to create a low-power signal that could reach satellites with an antenna no bigger than a dinner plate. The system, dubbed OmniTRACS, would provide two-way messaging and position tracking using a combination of satellites and the LORAN-C terrestrial navigation system. It was, as trade publications would later declare, "one of the world's most technologically advanced two-way mobile satellite communications and tracking systems."

But building the technology was only half the battle. Trucking companies were notorious for their conservatism—if something worked, you didn't change it. Qualcomm needed a demonstration that would shatter their skepticism. In late 1987, they outfitted a Schneider truck with a prototype OmniTRACS unit and invited executives to watch from headquarters as the truck drove from Green Bay to Los Angeles. Every fifteen minutes, a position update appeared on the screen. Messages typed in Wisconsin appeared instantly on the driver's dashboard terminal. When the truck broke down outside Amarillo—an unplanned but fortuitous demonstration—dispatch knew immediately and vectored another truck to pick up the load.

Schneider signed up for 5,000 units on the spot, at $3,000 per installation plus monthly service fees. Within eighteen months, Qualcomm had contracts with major carriers representing 40,000 trucks. Revenue jumped from essentially zero to $32 million annually. More importantly, OmniTRACS generated something even more valuable than revenue: cash flow to fund research.

Because here's what the trucking industry didn't know: Qualcomm's leadership was already looking beyond satellites. In parallel with OmniTRACS development, Jacobs had tasked a small team with investigating whether spread-spectrum techniques could work in terrestrial cellular networks. The conventional wisdom said no—cellular systems needed narrow, defined channels to avoid interference. Spread-spectrum did the opposite, spreading signals across wide frequency bands like butter on toast. It seemed crazy for cellular.

The research was bootlegged, funded by OmniTRACS profits and conducted by engineers who were supposed to be working on satellite projects. Andrew Viterbi would later describe this period as "venture capital by other means"—using revenue from one business to fund research in another. The board, filled with patient capital from San Diego's tight-knit tech community, understood the game. OmniTRACS was the cash cow that would fund the moon shot.

By early 1989, the cellular research had progressed enough to require a decision. The team had solved three fundamental problems that made CDMA (Code Division Multiple Access) viable for cellular: the near-far problem (where strong signals drown out weak ones), the soft handoff challenge (seamlessly transferring calls between cell towers), and variable rate encoding (adjusting data rates based on actual speech patterns). Each solution was elegant, patentable, and completely theoretical. Nobody had built a working CDMA cellular system.

The company faced a classic innovator's dilemma. OmniTRACS was generating reliable revenue and had clear growth potential—the trucking market alone could support a billion-dollar business. But cellular represented a market 100 times larger, albeit with entrenched competitors who had no interest in new technology. Ericsson, Nokia, and Motorola had spent billions developing TDMA (Time Division Multiple Access) systems. The entire industry had aligned around this standard. Qualcomm would be picking a fight with giants.

The decision came down to a simple calculation that only academics-turned-entrepreneurs could love: CDMA was theoretically superior to TDMA by a factor of 20 in spectral efficiency. That meant a CDMA network could handle 20 times more calls using the same spectrum. In a world where spectrum was the scarcest resource, that advantage would eventually prove decisive. Theory said they should win. Reality said they were insane.

The board meeting where they decided to bet the company on CDMA has become Silicon Valley legend, though it actually took place in a nondescript conference room in Sorrento Valley. Jacobs presented the technical case with characteristic understatement. Viterbi laid out the patent strategy. Franklin Antonio demonstrated a crude prototype that could barely complete a call across the parking lot. Harvey White, ever the pragmatist, asked the key question: "What happens if the industry tells us to go to hell?"

Jacobs' answer revealed the strategic genius that would define Qualcomm's next decade: "Then we build it ourselves and prove them wrong." They wouldn't just develop CDMA technology—they would build phones, base stations, even operate networks if necessary. They would create irrefutable proof that CDMA worked, then license the technology to the very companies that were fighting them.

The pivot from satellites to cellular marked more than a technology shift—it represented a fundamental change in business model. OmniTRACS was a traditional product business: build hardware, sell it, provide services. CDMA would be about intellectual property: create standards, own patents, collect royalties. The margin structure was completely different. The competitive dynamics were completely different. The skills required were completely different.

But Qualcomm had advantages that wouldn't become apparent until later. Their academic backgrounds meant they could engage in standards bodies as technical contributors, not just commercial participants. Their defense contracting experience taught them how to navigate complex, political environments. Their OmniTRACS revenue gave them independence—they didn't need venture capital that might push for quick exits. Most importantly, they had conviction born from mathematical proof. They knew CDMA was superior. They just had to convince everyone else.

IV. The CDMA Wars: Taking on the Industry (1989–1995)

The Cellular Telecommunications Industry Association meeting in Washington D.C., March 1989, should have been a coronation. After years of committee meetings and technical evaluations, the industry was ready to anoint TDMA as the second-generation digital standard for North America. Ericsson executives had prepared champagne. Motorola's engineers were already designing handsets. Then Irwin Jacobs stood up and politely destroyed their consensus.

"We believe CDMA can deliver twenty times the capacity of TDMA," he stated matter-of-factly, as if mentioning the weather. The room erupted. Engineers from Nokia called it "downright impossible." Ericsson's representative declared it would never work at commercial scale. The CTIA's technical committee chair would later tell the Wall Street Journal it was "the worst-case possibility: that CDMA doesn't work on the massive scale required."

The physics problem that everyone cited was real: the near-far field effect. Imagine you're trying to have a conversation in a crowded restaurant. If someone at the next table starts shouting, you can't hear your dinner companion. In CDMA, where all users share the same frequency band, a phone close to a cell tower would theoretically drown out phones farther away. It was, the critics said, an insurmountable flaw.

But Qualcomm had already solved it. Three patents filed in 1989 would become the foundation of their empire. The first described a power management system that could adjust transmission strength 800 times per second, ensuring that all signals arrived at the base station with equal power. The second detailed a "soft handoff" methodology where phones could communicate with multiple towers simultaneously, eliminating dropped calls during transitions. The third introduced variable rate encoding that could reduce data transmission by 85% during silent periods in conversation.

Each patent was a masterpiece of engineering elegance, but papers don't change industries. Qualcomm needed a demonstration that would silence the skeptics. The San Diego test in November 1989 was their first attempt—a single base station communicating with modified phones within a two-mile radius. It worked, barely, but critics dismissed it as a laboratory curiosity. "Anyone can make something work in perfect conditions," an Ericsson executive told Communications Week. "Try it in New York City."

So they did. The November 1990 Manhattan demonstration was theater as much as technology. Qualcomm rented space in the Times Square Marriott Marquis and invited 200 industry executives and journalists. They installed base stations on the hotel roof and another building blocks away. Then, in full view of skeptics, they made calls while walking through Times Square, riding in taxis, even from inside the subway entrance. The system handled 10 simultaneous calls in one of the most challenging radio environments on Earth.

But even successful demonstrations weren't enough. The industry had billions invested in TDMA. Switching to CDMA would require new base stations, new handsets, new engineering expertise. The cellular carriers, led by McCaw Cellular and Bell Atlantic, were skeptical of being locked into a single company's technology. "What happens if Qualcomm gets hit by a bus?" one executive asked at an industry conference, not entirely metaphorically.

Qualcomm's response was strategic brilliance disguised as necessity. They would give away the kingdom to create the empire. In July 1990, they announced agreements with Nynex and Ameritech to conduct large-scale field trials. But here was the key: Qualcomm would also license their CDMA patents to any manufacturer who wanted them. They would help competitors build CDMA equipment. They would even sell them chips and software. The only catch? Everyone would pay royalties on every device and base station that used CDMA technology.

The field trials in 1991 would determine CDMA's fate. The tests weren't just technical evaluations—they were public trials with the entire industry watching. In San Diego, they built a 36-cell network covering 1,000 square miles. Real customers made real calls. Drive tests measured actual capacity. The results were undeniable: CDMA delivered 10 to 20 times the capacity of analog systems and 3 to 6 times that of TDMA. Moreover, call quality was superior, battery life was longer, and the soft handoff eliminated the dropped calls that plagued other systems.

The November 1991 CTIA meeting in Nashville became CDMA's vindication. The same committee that had rejected it two years earlier now had to acknowledge the results. But the victory wasn't unanimous—it was bitter and contested. Ericsson's representative stood up and delivered what one attendee called "the most hostile technical presentation I've ever witnessed," arguing that Qualcomm's tests were rigged, that real-world performance would never match trials, that the whole thing was an elaborate confidence game.

The political maneuvering that followed was vicious. European companies, having invested heavily in GSM technology, saw CDMA as an American attempt to dominate global standards. They lobbied their governments to mandate GSM. They spread fear, uncertainty, and doubt about CDMA's viability. An Ericsson executive told the Financial Times that adopting CDMA would "set the mobile industry back five years."

But Qualcomm had an ace: the Pacific Rim. While Europe circled its wagons around GSM, Asian carriers faced different pressures. Dense populations meant capacity was everything. Korea, in particular, needed a solution immediately. In 1993, after extensive testing, Korea adopted CDMA as its national standard—the first country to do so. It was a massive bet on unproven technology from a company with no track record in cellular.

The July 1993 CTIA adoption of CDMA as the IS-95 standard (later branded cdmaOne) triggered what the Wall Street Journal called "widespread criticism" from businesses invested in competing technologies. Motorola hedged its bets, developing both TDMA and CDMA phones. Nokia and Ericsson continued fighting, funding studies that showed TDMA's supposed advantages. AT&T Wireless, having already committed to TDMA, found itself on the wrong side of technical history.

The business model battles were as fierce as the technical ones. Qualcomm wanted 5% royalties on every CDMA device. Manufacturers called it highway robbery. The negotiations were brutal. In one legendary meeting, a Motorola executive allegedly threw a phone (a Motorola phone, naturally) at the wall and declared they'd rather exit the business than pay Qualcomm's "tax." But they had no choice. The patents were bulletproof, the technology was essential, and Qualcomm owned it all.

By 1995, the war was effectively over. Primeco announced a 15-state CDMA rollout. Sprint PCS committed to building a nationwide CDMA network. Even skeptics were converting. The same Wall Street Journal that had warned about CDMA's "worst-case possibility" now wrote about its "remarkable vindication." Qualcomm's stock price increased 20-fold from its 1991 IPO.

But victory came with complications. The company had promised to be both partner and competitor—licensing technology while also building phones and infrastructure. This schizophrenic structure created constant tension. Customers resented buying from a supplier who was also a rival. The solution would take years to implement: gradually exit manufacturing, focus on chips and patents, let others build the products while Qualcomm collected the tolls.

V. Building the Standard: Global Expansion & Infrastructure (1995–2000)

The conference room at Hutchison Telecom's Hong Kong headquarters, September 1994, felt like a casino's high-stakes poker room. On one side sat Qualcomm's deployment team, jet-lagged engineers who'd been living on instant noodles and sleeping in the equipment rooms. On the other, Hutchison executives who'd bet their company's future on an unproven American technology. Between them lay maps of Hong Kong—one of the most challenging cellular environments on Earth, with its dense towers, underground metros, and 6 million people crammed into 426 square miles. In ninety days, they would either launch the world's first commercial CDMA network or become history's most expensive technology failure.

The Hong Kong launch on January 28, 1995, wasn't just a network deployment—it was a proof point for the entire industry. Every major carrier in the world sent engineers to observe. If CDMA could work in Hong Kong's urban canyon, it could work anywhere. The first commercial call, placed from a ferry in Victoria Harbor to demonstrate mobility and in-building penetration, connected flawlessly. Within six months, Hutchison was reporting 40% fewer dropped calls than their GSM competitors and needed 50% fewer cell sites to cover the same area.

But the real prize was Korea. The country's decision to adopt CDMA as its national standard in 1993 had been strategic, not technical. Korea wanted to leapfrog Japan in mobile technology, and betting on CDMA offered a chance to reset the game. The partnership between Qualcomm and the Electronics and Telecommunications Research Institute (ETRI), initiated in 1991, was more than technology transfer—it was industrial policy in action. Qualcomm would provide core technology; Korea would build an entire ecosystem around it.

By April 1996, when SK Telecom and Korea Telecom launched commercial CDMA services, the transformation was remarkable. Samsung, LG, and Hyundai had all become CDMA manufacturers. Korean engineers had filed hundreds of their own CDMA patents. The country that had been a technology follower was suddenly a leader. Within two years, Korea had the highest mobile penetration rate in the world, and Korean manufacturers were exporting CDMA equipment globally. The American market numbers validated the strategy: By 1997 CDMA had 57 percent of the US market, whereas 14 percent of the market was on TDMA. Sprint PCS and Primeco were building coast-to-coast CDMA networks. But the real action was international. Qualcomm teams were simultaneously deploying networks in Argentina, Brazil, Mexico, India, and Venezuela. Each deployment was a masterclass in technical diplomacy—convincing local regulators, training local engineers, navigating import restrictions, and managing currency fluctuations.

The business model evolution during this period was painful but necessary. The company had $383 million in annual revenue in 1995 and $814 million by 1996. But growth came with contradictions. Qualcomm was simultaneously partner and competitor—licensing technology to Nokia while competing with Nokia phones, selling chips to Motorola while Motorola sued them for allegedly copying the StarTAC design. The Q Phone controversy in March 1997 epitomized the tension. Motorola claimed patent infringement; Qualcomm countered that form followed function. The real issue wasn't design—it was that Qualcomm's vertical integration threatened everyone.

The infrastructure division was bleeding money—$400 million annually by some accounts. Building base stations required massive capital investment, long sales cycles, and competed directly with their licensees. The handset business faced similar challenges: fierce price competition, channel conflicts, and the awkwardness of competing with customers. By 1998, something had to give.

The restructuring of 1998-1999 was Silicon Valley surgery performed with a chainsaw. Seven hundred employees were laid off. The infrastructure division was sold to Ericsson—the same company that had fought CDMA most viciously—as part of a patent settlement. In December 1999, Qualcomm sold its manufacturing interests to Kyocera Corporation, a Japanese CDMA manufacturer and Qualcomm licensee. Qualcomm's infrastructure division was sold to competitor Ericsson in 1999 as part of an out-of-court agreement for a CDMA patent dispute that started in 1996.

These weren't retreats—they were strategic brilliance. By exiting manufacturing, Qualcomm transformed from a company with massive capital requirements and modest margins to one with minimal capital needs and extraordinary margins. The licensing model that emerged was elegant: Qualcomm would innovate, patent, and collect royalties while others did the messy work of manufacturing and distribution. Qualcomm was the fastest growing stock on the market with a 2,621 percent growth over one year.

The employee exodus was traumatic. Engineers who'd built the company's products suddenly found themselves working for competitors or unemployed. Stock option disputes festered—by 2005, Qualcomm reached $74 million in settlements regarding a protracted legal dispute over employee stock options, following the sale of its infrastructure division in 1999. The culture changed from "we build everything" to "we enable everything"—a psychological shift that many original employees couldn't accept.

But the numbers vindicated the strategy. Without manufacturing overhead, Qualcomm's R&D could focus on next-generation technology. Without channel conflicts, relationships with licensees improved (slightly). Without capital requirements, cash flow exploded. The company that had struggled to fund CDMA development from trucking revenues now had billions to invest in 3G research.

The global footprint by 2000 was staggering. By 2005, there were 143 CDMA carriers in 67 countries. Each represented not just a customer but a dependency—carriers who'd bet their networks on Qualcomm technology and now had no choice but to continue paying royalties. The initial resistance in markets like China and India had transformed into eager adoption as those countries realized CDMA's capacity advantages were perfect for their dense populations.

The lesson from this period was counterintuitive: sometimes the best way to dominate an industry is to stop competing in it. By transitioning from manufacturer to enabler, Qualcomm positioned itself as the toll collector for the entire mobile industry—a position far more profitable and defensible than making phones or base stations. As one former executive put it: "We realized we didn't need to own the roads if we owned all the bridges."

VI. The 3G Revolution & Patent Wars (2000–2007)

The mahogany conference table at Nokia's Espoo headquarters could have been a negotiating platform. Instead, on a gray February morning in 2000, it became a war council. Nokia's executives had just received Qualcomm's licensing terms for 3G technology: 5% royalties on every WCDMA phone, regardless of how much Nokia technology it contained. The head of Nokia's legal department allegedly threw the contract across the table and declared, "We'll see you in court for the next decade." He was optimistic—it would take longer.

The 3G standards battle was supposed to be different. The International Telecommunication Union had learned from the 2G fragmentation—CDMA, GSM, TDMA all competing—and mandated that 3G would have harmonized global standards. What they got instead was a knife fight disguised as a standards process. Every proposal, whether WCDMA from Europe, CDMA2000 from North America, or TD-SCDMA from China, relied on Qualcomm's fundamental CDMA patents. The revolution they'd started in San Diego had become inescapable.

The European strategy was breathtaking in its audacity. Unable to avoid CDMA entirely, they would create WCDMA (Wideband CDMA)—different enough to claim independence, similar enough to actually work. Ericsson and Nokia poured billions into developing workarounds for Qualcomm patents. They funded academic research to find alternative approaches. They lobbied the European Commission to investigate Qualcomm for antitrust violations. They did everything except acknowledge the obvious: all third generation cellular technical standards ("3G") were based on the CDMA technology pioneered by Qualcomm.

The technical challenge Europe faced was fundamental. CDMA's core innovations—power control, soft handoff, rake receivers—weren't just features you could engineer around. They were mathematical solutions to physics problems. Every attempt to avoid them either didn't work or infringed different Qualcomm patents. One Ericsson engineer would later admit privately: "We spent five years and a billion dollars to avoid paying Qualcomm five percent. We should have just paid."

Paul Jacobs' succession as CEO in 2005 marked a generational transition. Where Irwin had been the professorial founder explaining why CDMA was superior, Paul was the strategist who understood that technical superiority meant nothing without market power. His first major decision revealed his approach: rather than fight every patent battle in court, selectively license technologies that would accelerate 3G adoption. More users meant more devices meant more royalties. Let competitors win battles while Qualcomm won the war.

The Nokia war was epic in scope and pettiness. Between 2005 and 2008, the companies filed over 40 lawsuits across 11 countries. Nokia claimed Qualcomm was charging excessive royalties; Qualcomm countered that Nokia was using its patents without paying. The legal bills exceeded $100 million annually for each company. At one point, the companies were simultaneously suing and countersuing each other in the United States, United Kingdom, Germany, Netherlands, France, Italy, China, and Japan.

The October 2005 complaint to the European Commission, filed by Nokia, Ericsson, Broadcom, NEC, Panasonic, and Texas Instruments, alleged something remarkable: six large telecommunications companies led by Nokia filed a complaint against Qualcomm with the European Commission's antitrust division, alleging Qualcomm was abusing its market position to charge unreasonable rates for its patents. Qualcomm alleged the six companies were colluding together under the code name Project Stockholm in a legal strategy to negotiate lower rates.

"Project Stockholm" revealed the desperation. Internal emails later disclosed in discovery showed competitors coordinating legal strategies, sharing intelligence about Qualcomm negotiations, and agreeing not to settle individually. It was cartel behavior aimed at breaking a patent monopoly—legally gray, ethically questionable, strategically understandable.

The Broadcom battle took a different approach: attack the patents themselves. Broadcom argued that Qualcomm's patents were either invalid, unenforceable, or that Broadcom's chips didn't infringe. The case went to trial in 2007, with Broadcom seeking $8.3 billion in damages. The courtroom drama included Qualcomm being sanctioned for withholding emails, accusations of evidence tampering, and technical testimony so complex that jurors later admitted they understood perhaps 10% of it.

But while lawyers fought, engineers innovated. Qualcomm's 3G chipsets were simply better—more power efficient, more integrated, more capable. The MSM6000 series, launched in 2004, could handle CDMA2000 and WCDMA on a single chip. Competitors needed two chips, doubling power consumption and cost. By 2006, even companies suing Qualcomm were buying Qualcomm chips because their own solutions couldn't compete.

The patent portfolio expansion during this period was relentless. Qualcomm filed over 1,000 patents annually, covering everything from antenna design to video compression. In 2021, Qualcomm ranked 5th globally for patent applications by the World Intellectual Property Organization, reflecting its vast portfolio in CDMA and other wireless technologies. They hired the best wireless engineers from universities worldwide, gave them unlimited budgets, and told them to invent the future. The R&D spending exceeded $2 billion annually—more than most competitors' total revenue.

China presented a unique challenge. The government mandated TD-SCDMA as the national 3G standard, partly to avoid foreign patent royalties. But TD-SCDMA still used CDMA technology, still required Qualcomm patents, and performed poorly compared to WCDMA or CDMA2000. China Mobile, forced to deploy TD-SCDMA, watched its competitors using WCDMA gain market share. By 2009, even Chinese officials privately admitted the TD-SCDMA strategy had failed.

The resolution of the Nokia war in July 2008 set the template for future settlements. Nokia agreed to pay $2.29 billion in past royalties and ongoing licensing fees. But the key provision was less publicized: Nokia acknowledged Qualcomm's patents were valid, essential, and fairly licensed. It was complete capitulation dressed as compromise. Every other holdout understood the message: resistance was expensive and futile.

Paul Jacobs' strategy had worked perfectly. In 2005, Paul E. Jacobs, son of Qualcomm founder Irwin Jacobs, was appointed as Qualcomm's new CEO, inheriting the patent wars but transforming them into validations of Qualcomm's licensing model. By 2007, Qualcomm was collecting royalties from every major handset manufacturer, generating over $3 billion annually in licensing revenue with 85% operating margins.

The 3G revolution validated everything Qualcomm had argued during the CDMA wars. Capacity mattered more than politics. Physics trumped nationalism. And owning the fundamental patents for wireless communication was the best business model in technology. As one industry analyst observed: "Qualcomm doesn't win patent wars. They win patent sieges. Eventually, everyone pays."

VII. The Snapdragon Era: From Modems to Systems-on-Chip (2007–2015)

The Qualcomm engineering lab in San Diego, November 2006, looked like a silicon graveyard. Prototype chips that had cost millions to develop sat in anti-static bags, most would never see production. But one project, code-named "Scorpion," was different. The engineers working on it weren't just designing another mobile processor—they were reimagining what a phone could be. When they finally unveiled Snapdragon a year later, the name itself was a statement: In November 2005, Qualcomm announced that it was developing the Scorpion central processing unit (CPU) for mobile devices. "Snap" for responsiveness, "Dragon" for power—together, they promised to transform smartphones from communication devices into pocket computers.

The first Snapdragon chip, released in November 2007, was a marvel of integration. While competitors cobbled together separate chips for processing, graphics, GPS, and cellular, Snapdragon combined everything on a single piece of silicon. The 1 GHz clock speed was unprecedented—competitors' chips ran at 500 MHz, when they ran at all. Battery life, the perpetual smartphone constraint, improved by 40%. But the real innovation was invisible: the first custom Hexagon DSP (Digital Signal Processor), designed specifically for mobile multimedia processing.

The timing was perfect and accidental. Apple had just launched the iPhone in June 2007, creating a market for powerful mobile processors that didn't exist six months earlier. Google's Android was still in development, desperately seeking hardware that could match iPhone's smoothness. The entire industry was scrambling to respond to Apple's disruption, and Qualcomm had accidentally built exactly what everyone needed.

HTC's HD2, launched in 2009 with the Snapdragon QSD8250, became the proof point. Reviews called it "impossibly fast" and "laptop-like." Users could actually browse desktop websites without wanting to throw their phones against walls. YouTube videos played without stuttering. Games that had been PlayStation exclusive three years earlier ran smoothly. The HD2 became legendary in hacking communities—enthusiasts installed everything from Ubuntu to Windows 95 on it, just because Snapdragon made it possible.

By 2011, Qualcomm had captured 50% market share of the $7.9 billion smartphone processor market. The Snapdragon S4 series, featuring the custom Krait CPU architecture, didn't just compete with ARM's reference designs—it demolished them. Krait could process two instructions per clock cycle when ARM's Cortex-A9 could barely manage one. Power consumption dropped 40% while performance doubled. Samsung, despite designing their own Exynos processors, used Snapdragon in their US flagship phones because Qualcomm's integrated LTE was superior.

The competition responded predictably: they quit. Nvidia's Tegra, despite strong graphics performance, couldn't match Snapdragon's integration. Texas Instruments, one of the semiconductor industry's giants, exited mobile processors entirely in 2012. Intel spent billions trying to enter the market with x86-based Atom processors, subsidizing manufacturers to use their chips, and still failed. The graveyard of "Snapdragon killers" grew so large that industry analysts stopped predicting new challengers.

But then Apple did something unexpected. The September 2013 launch of the iPhone 5S featuring the A7 processor changed everything. It wasn't just fast—it was 64-bit, a full year before anyone expected mobile processors to make that transition. Android manufacturers panicked. Google scrambled to add 64-bit support to Android. And Qualcomm, caught completely off-guard, had to respond immediately.

The Snapdragon 810 disaster of 2015 became Silicon Valley legend for all the wrong reasons. Rushed to market to match Apple's 64-bit challenge, the 810 used ARM's reference Cortex-A57 cores instead of Qualcomm's custom architecture. The chip ran so hot that phones throttled performance within minutes. The LG G Flex 2 literally bent from heat. Samsung publicly rejected the 810 for the Galaxy S6, choosing their own Exynos processor globally—a humiliation for Qualcomm. Sony's Xperia Z3+ warned users about potential overheating during camera use.

Internal emails leaked during later lawsuits revealed the chaos. Engineers warned executives that the 810 wasn't ready. Thermal testing showed problems that would take months to fix. But with design wins at stake and Apple pulling ahead, Qualcomm shipped anyway. One engineer's email summarized the situation: "We're shipping a space heater that occasionally makes phone calls."

The financial impact was severe but not fatal. Qualcomm's stock dropped 30% through 2015. Major customers like Samsung and LG diversified away from Snapdragon. MediaTek, a Taiwanese competitor previously dismissed as "good enough for cheap phones," gained share in the premium segment. Industry consensus was that Qualcomm had lost its edge, that vertical integration was dead, that Apple's approach of designing custom silicon would dominate.

They were wrong. The 810 disaster forced Qualcomm to confront uncomfortable truths. They'd become complacent, assuming integration alone would win. They'd stopped pushing custom architectures, relying on ARM's designs. They'd prioritized time-to-market over excellence. The fix required both technical and cultural changes.

The Snapdragon 820, released in 2016, was redemption through engineering. Qualcomm returned to custom Kryo cores, delivering 40% better performance than the 810 while using less power. The integrated X12 LTE modem supported gigabit speeds when most carriers barely offered 100 Mbps. The Hexagon 680 DSP could process neural networks, enabling on-device AI before anyone knew they wanted it. Reviews called it "the comeback chip" and "Qualcomm's return to form."

But the real strategic shift was broader. Whereas Irwin Jacobs focused on CDMA patents, Paul Jacobs refocused much of Qualcomm's new research and development on projects related to the Internet of things. Snapdragon wasn't just for phones anymore. Qualcomm created variants for tablets, smartwatches, cars, and laptops. The Snapdragon brand, once associated with mobile processors, became a platform for connected computing.

The lesson from the Snapdragon era was profound: technical leadership was necessary but not sufficient. Success required predicting where the market would be, not where it was. The 810 failed because Qualcomm reacted to Apple instead of anticipating them. The 820 succeeded because it delivered capabilities—AI processing, gigabit LTE, 4K video—that wouldn't become mainstream for years. As one executive reflected: "We learned that being first means nothing if you're not also best."

VIII. Modern Era: 5G, AI & Beyond Mobile (2015–Today)

Cristiano Amon stood before a packed auditorium at Qualcomm's San Diego headquarters in December 2020, about to make an announcement that would have seemed insane five years earlier. "We're not a wireless company anymore," the newly appointed CEO declared. "We're becoming the connected computing company for the age of AI." Behind him, slides showed Snapdragon chips running in Mercedes-Benz dashboards, Samsung laptops, and Meta's VR headsets. The transformation from mobile-first to everything-connected was complete.

The foundation for this shift had been laid carefully. During Q4 in fiscal '24, we continue to make progress on our growth and diversification strategy, with Android maintaining devices over $400 increasing from 21% to 30% of the market. While Apple captured premium margins, Android's 84.6% market share by July 2014 meant Qualcomm powered the vast majority of global smartphones. But Amon saw what others missed: the smartphone market was saturating, and future growth required new frontiers.

The automotive transformation was stunning in its speed. record automotive revenue wasn't just about adding cellular modems to cars. Qualcomm reimagined the entire vehicle as a computing platform. The Snapdragon Digital Chassis integrated everything—infotainment, driver assistance, connectivity—onto unified silicon. General Motors committed to using Snapdragon across its entire fleet by 2026. Mercedes-Benz, BMW, and Stellantis followed. The automotive pipeline ballooned to billions in contracted revenue. The crown jewel of this transformation was Oryon. Developed by the team Qualcomm acquired from Nuvia—founded by ex-Apple engineers who'd designed the A-series processors—Oryon represented Qualcomm's first truly custom CPU architecture since 2016. The Snapdragon 8 Elite marks a groundbreaking milestone as the first Snapdragon Mobile Platform to feature Qualcomm's next-generation, custom Qualcomm Oryon™ CPU. The 3nm chip featured 2 Prime (4.32 GHz) and six Performance (3.53 GHz) cores, with both sets of cores custom designed, abandoning efficiency cores entirely—a bold bet that performance cores could handle everything efficiently.

The PC ambition with Snapdragon X Elite was even more audacious. For decades, x86 had monopolized personal computing. Intel and AMD's duopoly seemed unbreakable. But Apple's M1 chip proved ARM architecture could match or exceed x86 performance while using a fraction of the power. Qualcomm saw opportunity where others saw impossibility. The Snapdragon X Elite promised "multi-day battery life" and AI processing capabilities that x86 couldn't match.

Microsoft became an unlikely ally. Desperate to compete with Apple's MacBooks and seeing AI as the future of computing, they committed to optimizing Windows for ARM. The partnership went beyond software—Microsoft's Surface devices would showcase Snapdragon's capabilities. When the first X Elite laptops launched in 2024, reviews were cautiously optimistic. Battery life genuinely lasted 20+ hours. Performance matched mid-range x86 chips. But software compatibility remained challenging—a problem that would take years to fully solve.

The 5G story was different from 3G or 4G. This time, Qualcomm wasn't fighting for standard adoption—everyone agreed on the technology. Instead, the battle was about implementation and integration. The Snapdragon X80 modem didn't just support 5G; it aggregated six downlink carriers simultaneously, achieving theoretical speeds of 10 Gbps. But the real innovation was power efficiency—5G that didn't destroy battery life.

Apple's modem ambitions cast a shadow over everything. Since acquiring Intel's modem business in 2019, Apple had been developing their own 5G chips. Industry consensus was that Apple modems would debut by 2025, potentially ending Qualcomm's most profitable relationship. But technical challenges kept pushing Apple's timeline back. Designing modems that worked globally, across hundreds of carrier configurations, while maintaining Apple's power efficiency standards, proved harder than designing processors.

The AI pivot was both opportunistic and essential. Qualcomm's differentiated technology and product road maps lead in every industry in which we now participate, and we are very optimistic about the edge AI momentum across our business. The Hexagon NPU (Neural Processing Unit) could run large language models locally, enabling ChatGPT-like experiences without cloud connectivity. While Nvidia dominated datacenter AI, Qualcomm positioned itself for edge AI—processing that happened on devices, not servers. The automotive numbers tell the story: QCT Automotive Revenue: $899 million, with 11% sequential growth and 68% year-over-year growth, marking its fifth consecutive record quarter. But the ambition extends far beyond current results. Specifically, the chip maker has set out to achieve a combined $22 billion in annual revenue from its automative and IoT segments by its FY29, with $8 billion of that coming from automotive and $14 billion from IoT. Qualcomm CEO Cristiano Amon, also speaking during the Investor Day 2024 event, was particularly proud of the company's Automotive business, whose success, he said is "reflected in five consecutive quarters of record revenue in automotive, and a $45 billion design win pipeline that will be translating into revenue as we have new cars launched".

The IoT expansion was equally aggressive but more fragmented. Industrial automation, smart cities, retail analytics, healthcare devices—each required different capabilities but all needed edge computing. Qualcomm's approach was platform-based: create reference designs that partners could customize rather than building everything themselves. The strategy worked— QCT IoT Revenue: $1.7 billion, marking a 24% increase from the prior quarter.

But success brought new challenges. The company that had fought patent wars over telecommunications now faced different battles: software ecosystems, developer tools, customer support at scale. Supporting a Mercedes-Benz infotainment system required different capabilities than selling chips to Samsung. The organization had to transform from component supplier to solution provider—a cultural shift as significant as the technology transitions.

The strategic reset under Amon was working. Total Revenue: $39.0 billion. Non-GAAP EPS: $10.22, a 21% increase year-over-year. Free Cash Flow: A record $11.2 billion. But the real transformation was philosophical. Qualcomm was no longer defining itself by what it made—modems, processors, radios—but by what it enabled: connectivity, intelligence, experience. The company that Irwin Jacobs founded to solve communications problems was becoming what Cristiano Amon envisioned: the nervous system for an AI-powered, connected world.

IX. Business Model & The Patent Machine

The glass-walled conference room on the 30th floor of Qualcomm's headquarters offers a panoramic view of San Diego Bay, but the real empire isn't visible—it exists in filing cabinets at the U.S. Patent Office, in licensing agreements locked in legal departments worldwide, and in the mathematical certainty that anyone building a modern communication device will eventually write Qualcomm a check. The three-segment structure—QCT (chips), QTL (licensing), QSI (strategic investments)—looks simple on paper. The reality is a financial engineering masterpiece that would make Wall Street jealous.

On the licensing front, Qualcomm Technology Licensing (QTL) generated $5.57 billion, up 5% from the previous year. The segment's earnings before tax (EBT) margins rose from 68% to 72%, indicating increased profitability due to attractive licensing agreements and a strong patent portfolio. Think about those margins for a moment. For every dollar of licensing revenue, seventy-two cents is profit. No factories. No inventory. No supply chains. Just intellectual property converting into cash flow at margins that make software companies envious.

The "Qualcomm tax," as critics call it, works like this: Qualcomm charges about 5% or $30 per device in royalties—significantly higher than most patent holders—arguing the critical role its patents play in the industry's infrastructure. But here's the genius—the royalty isn't based on the chip price but on the wholesale price of the entire device. Build a $1,000 phone? Qualcomm wants $50, regardless of whether their chip costs $30 or $300. Use a competitor's chip? Still pay Qualcomm because the patents cover the system, not just the component.

The patent portfolio itself is a work of art. In 2021, Qualcomm ranked 5th globally for patent applications by the World Intellectual Property Organization, reflecting its vast portfolio in CDMA and other wireless technologies that the company has pioneered for decades. These aren't frivolous patents for rounded corners or slide-to-unlock. They're fundamental: how to manage power in a multi-user system, how to hand off calls between towers, how to compress voice without losing quality. Remove any one, and modern cellular doesn't work.

The controversy is predictable and permanent. This stance has led to frequent disputes with competitors, clients, and regulators, who accuse Qualcomm of charging excessive rates and engaging in anti-competitive practices. Every major market has investigated Qualcomm for antitrust violations. China fined them $975 million in 2015. Korea extracted $854 million in 2016. The European Commission demanded $1.2 billion in 2018. The FTC sued them in 2017. Each settlement is essentially a cost of doing business—painful but not fatal, and never requiring fundamental changes to the model.

The legal arguments against Qualcomm are consistent: they bundle standard-essential patents (which must be licensed on FRAND—fair, reasonable, and non-discriminatory—terms) with implementation patents (which don't have such restrictions). They refuse to license chips to competitors, forcing everyone to pay device-level royalties. They use their chip market power to enforce their licensing terms. All true. All profitable. All sustainable because the alternative—building a modern communication system without Qualcomm patents—is essentially impossible.

QCT, the chip business, generated revenues of $33.2 billion, up from $30.4 billion in fiscal year 2023. But this isn't just a chip business—it's a patent enforcement mechanism. Every Snapdragon sale reinforces Qualcomm's technology leadership. Every design win validates their royalty rates. The chips and licenses create a virtuous cycle: better chips justify higher royalties, which fund better chips.

The strategic investments through QSI seem minor—less than 1% of revenue—but they're strategic chess moves. Investments in Chinese companies create political cover. Stakes in emerging technology companies provide early visibility into new markets. The $1.4 billion investment in RF360 Holdings (later acquired fully) gave Qualcomm control over the entire phone RF chain. Each investment either extends the patent portfolio, creates new licensing opportunities, or blocks potential competitive threats.

But here's what critics miss: Qualcomm's model incentivizes innovation in a way that pure product businesses don't. Qualcomm also provides licenses to use its patents, many of which are critical to the CDMA2000, TD-SCDMA and WCDMA wireless standards. When your revenue comes from everyone in an industry using your technology, you're motivated to make that technology as broadly applicable as possible. Qualcomm doesn't care if Samsung or Apple wins the smartphone wars—they profit from both. They don't care if 5G enables smartphones or smart cities—they collect royalties either way.

The regulatory battles reveal the model's resilience. After China's antitrust action, Qualcomm adjusted royalty rates for Chinese manufacturers—but still collected billions. After Korea's fine, they modified some practices—but maintained the essential structure. After the FTC case (ultimately won on appeal), they made minor concessions—but the patent machine kept printing money. Each regulatory action is like a stress test that proves the model's durability.

The numbers tell the story of a business model perfected over decades. The QTL segment's success demonstrates Qualcomm's substantial intellectual property portfolio, particularly in 5G and advanced connectivity solutions. When 5G deployment accelerates, licensing revenue grows. When new device categories emerge—watches, cars, industrial IoT—each one needs Qualcomm patents. The model scales infinitely with minimal marginal cost.

Consider the strategic brilliance: most technology companies fear commoditization, where products become interchangeable and margins collapse. Qualcomm inverted this—they commoditized the manufacturing while maintaining pricing power on the intellectual property. Let others fight over who can build chips most cheaply. Qualcomm will collect royalties from whoever wins.

The criticism that Qualcomm stifles innovation by taxing it misses a crucial point: they also fund it. The $6+ billion annual R&D budget, sustained by licensing revenue, produces the next generation of communications technology. Would carriers or device manufacturers invest similarly if they could capture all the value? History suggests not. The "Qualcomm tax" is also a "Qualcomm subsidy" for fundamental research.

The future challenges to the model are real but manageable. Standard-essential patent pools might reduce individual company leverage. Open-source alternatives might emerge for some functions. Geopolitical tensions might fragment global standards. But Qualcomm has survived every previous challenge by adapting the model, not abandoning it. They've shown that owning the tollbridge is more profitable than operating the transportation.

X. Playbook: Strategy & Investing Lessons

The wood-paneled boardroom at Kleiner Perkins in 1991 witnessed a masterclass in venture capital rejection. John Doerr, already a legend for backing Compaq and Sun Microsystems, listened to Irwin Jacobs pitch CDMA's potential, then politely declined. "Too technical, too capital intensive, too many entrenched competitors," he reportedly said. Thirty years later, that decision cost Kleiner Perkins roughly $100 billion in returns. The Qualcomm playbook isn't just about building a successful company—it's about recognizing and executing strategies that seem impossible until they become inevitable.

The Power of Standards and Network Effects

Qualcomm understood something fundamental: in network industries, standards are destiny. But they went further—they didn't just participate in standards, they created them. The genius wasn't inventing CDMA; it was making CDMA indispensable. Every carrier that adopted it made it more valuable for others to adopt. Every device that supported it increased the ecosystem's value. Network effects compounded on network effects until resistance became irrational.

The lesson for founders and investors: identify industries where standards are emerging and position yourself as essential to those standards. Don't just build products that use standards—own patents that define them. The initial investment is massive, the timeline is long, but the terminal value is extraordinary. Qualcomm spent a decade and billions of dollars establishing CDMA. They've spent the next three decades collecting rent on that investment.

Investing Ahead of the Market (10+ Year Bets)

When Qualcomm began CDMA research in 1989, commercial deployment wasn't expected until 1995 at the earliest. When they started 5G development in 2006, commercial networks weren't anticipated until 2020. This isn't quarterly thinking or even five-year planning—it's generational strategy. They invest in technologies that won't generate revenue for a decade, knowing that when they do, the returns will be monopolistic.

The practical application: map out technology development curves and invest at the research phase, not the commercialization phase. By the time a technology is obviously valuable, it's too late to capture fundamental IP. Qualcomm's current investments in 6G, quantum communications, and neuromorphic computing seem premature. That's precisely why they might be brilliant.

Vertical Integration vs Licensing Debates

Qualcomm's journey from full vertical integration to pure licensing wasn't planned—it was discovered through expensive experimentation. They tried being Samsung (making everything), they tried being Intel (making chips), and they finally realized they should be ARM (licensing IP). But unlike ARM, they maintained enough vertical capability to prove their technology worked and to capture value at multiple points in the stack.

The strategic insight: vertical integration is a means, not an end. Use it to prove technology, establish standards, and create reference implementations. Then gradually retreat to the highest-margin, most defensible position—usually intellectual property. The companies that try to do everything end up defending nothing. The companies that own the critical chokepoint defend everything while doing almost nothing.

Managing Technical Risk vs Market Risk

Qualcomm consistently chose technical risk over market risk. They bet that they could solve the near-far problem (technical risk) rather than betting that carriers would adopt an inferior solution (market risk). They bet they could design better processors (technical risk) rather than betting that manufacturers would pay premium prices for commodity chips (market risk).

This preference shapes everything from hiring to capital allocation. When you're taking technical risk, you hire PhDs and fund R&D. When you're taking market risk, you hire MBAs and fund marketing. Qualcomm's employee base—overwhelmingly engineers and scientists—reflects this choice. Their R&D spending—consistently 20% of revenue—finances it.

Building Moats Through Complexity

Qualcomm's moat isn't just patents—it's the complexity of implementing those patents. Building a CDMA system requires understanding thousands of interdependent patents, many of which are Qualcomm's. Even if you could design around some patents, the system-level integration is so complex that it's easier to license than to recreate.

The broader principle: complexity can be a feature, not a bug. If your solution is so sophisticated that competitors need years to understand it, let alone replicate it, you've built a temporal moat that compounds into a permanent advantage. Simplicity might win in consumer products, but complexity wins in fundamental technology.

Navigating Regulatory Capture vs Innovation

Qualcomm walks a tightrope between being seen as an innovation enabler and a market manipulator. They've been investigated by every major regulatory body, fined billions, and forced to modify practices. Yet the core model remains intact. How? By making themselves essential to national competitiveness. Countries might fine Qualcomm, but they won't destroy a company that enables their 5G leadership.

The tactical lesson: if you're building a monopolistic business model, ensure you're creating positive externalities that governments value. Qualcomm enables domestic manufacturers, funds university research, and advances national technological capabilities. The fines are a tax on monopoly profits, but they're less than those profits, making them sustainable.

The Demonstration Effect

Every major Qualcomm breakthrough followed the same pattern: academic paper, internal prototype, public demonstration, industry skepticism, irrefutable proof, mass adoption. The 1989 San Diego demonstration, the 1991 field trials, the Hong Kong launch—each was theater designed to make the impossible undeniable.

Modern founders often skip the demonstration phase, assuming that theoretical superiority will win. Qualcomm knew better. They understood that industries don't adopt better technologies—they adopt proven technologies. The cost of demonstrations—millions in equipment, months of preparation—was marketing disguised as engineering.

Strategic Patience and Conviction

Perhaps the most underappreciated aspect of Qualcomm's playbook is patience. They endured five years of industry rejection for CDMA. They spent a decade transitioning from products to licensing. They're currently in year six of their automotive strategy with breakeven still years away. This isn't patience born from indecision—it's patience backed by conviction.

The investment implication: in fundamental technology, time horizons should be measured in decades, not quarters. The companies that change industries don't iterate quickly—they invest deeply, build deliberately, and compound slowly. Qualcomm's stock was essentially flat from 2000 to 2016, then quintupled as 5G and diversification paid off. Investors who understood the strategy got rich. Those who focused on quarterly earnings missed one of the great technology investments of the generation.

XI. Analysis & Bear vs. Bull Case

Standing at Qualcomm's Sorrento Valley campus, you can see the Pacific Ocean to the west and the mountains to the east—a fitting metaphor for a company caught between massive opportunities and existential threats. The fiscal year 2024 numbers—$38.96 billion revenue, $10.22 non-GAAP EPS (21% YoY increase)—paint a picture of strength. But numbers tell what happened, not what will happen. The real question facing investors: Is Qualcomm a toll collector on the future of computing, or a legacy player about to be disrupted by the very customers it serves?

Bull Case: The Inevitable Infrastructure

The optimistic thesis rests on mathematical certainty: connected devices need Qualcomm technology. Start with the patent portfolio—14,000+ patents covering everything from basic cellular communication to advanced AI processing. These aren't optional nice-to-haves; they're mandatory must-haves. It owns patents critical to the 5G, 4G, CDMA2000, TD-SCDMA and WCDMA mobile communications standards. Even Apple, with unlimited resources and exceptional engineering talent, pays Qualcomm billions because avoiding their patents is essentially impossible.

The cash generation is staggering. Free Cash Flow: A record $11.2 billion in fiscal 2024, with minimal capital requirements for growth. The licensing business operates at 72% operating margins—every new 5G device, whether phone, car, or industrial sensor, generates pure profit. This isn't a business that needs to be managed; it's an annuity that manages itself.

The diversification strategy is working ahead of schedule. Record automotive revenues with 68% year-over-year growth proves that Qualcomm can replicate its mobile success in new verticals. The automotive pipeline—$45 billion in design wins—provides visible revenue growth through 2030. Unlike smartphones where replacement cycles are lengthening, cars are becoming rolling computers requiring ever-more sophisticated processing.

The Snapdragon 8 Elite with custom Oryon cores represents a technical renaissance. The 3nm (TSMC) Snapdragon 8 Elite has a second-generation Oryon CPU that has been optimized for mobile. There are 2 Prime (4.32 GHz) and six Performance (3.53 GHz) cores, with both sets of cores custom designed. After years of using ARM reference designs, Qualcomm is innovating again, suggesting the company's best engineering days might be ahead, not behind.

AI at the edge is Qualcomm's opportunity to define another generation of computing. While Nvidia dominates datacenter AI, Qualcomm's NPUs enable AI processing on devices—more private, more responsive, more power-efficient. As AI moves from cloud to edge, Qualcomm's integrated platforms become more valuable, not less.

The financial flexibility is enormous. With $11.2 billion in free cash flow and modest capital needs, Qualcomm can simultaneously invest in R&D (maintaining technical leadership), return cash to shareholders (the new $15 billion buyback authorization), and pursue strategic acquisitions. They have the balance sheet to weather any storm and the cash flow to capitalize on any opportunity.

Bear Case: The Empire's Vulnerabilities

The pessimistic thesis starts with customer concentration risk crystallizing. Apple represents roughly 20% of Qualcomm's revenue through both chip sales and licensing. Apple has spent billions developing internal modems, acquiring Intel's modem business, and hiring Qualcomm's engineers. When—not if—Apple succeeds, Qualcomm loses both a customer and gains a competitor. The contract through 2026 isn't a partnership; it's a stay of execution.

Regulatory pressure is intensifying globally. Every major market has fined Qualcomm for anti-competitive practices, and the scrutiny is increasing, not decreasing. The licensing model that generates 72% margins does so because it's essentially a monopoly tax. Governments worldwide are becoming less tolerant of such arrangements, especially when they involve critical infrastructure. One successful regulatory action that forces patent licensing at chip-level rather than device-level would devastate the business model.

Chinese competition is real and accelerating. MediaTek has already captured significant share in mid-range smartphones. HiSilicon, despite U.S. sanctions, continues advancing. Chinese companies are explicitly targeting technological independence in semiconductors. Qualcomm's 46% revenue exposure to China isn't just a trade war risk—it's an existential threat if China achieves semiconductor self-sufficiency.

The patent portfolio, while valuable, is depreciating. The foundational CDMA patents are expiring or becoming less relevant. Each new generation of wireless technology sees more contributors, diluting Qualcomm's share of essential patents. 6G development involves more companies, more countries, and more alternative approaches. The monopolistic positioning in 3G/4G won't be replicated in future generations.

Technical competition is intensifying. Google's Tensor chips, Samsung's Exynos processors, and MediaTek's Dimensity line all challenge Snapdragon's supremacy. In PCs, x86 isn't surrendering to ARM without a fight—Intel and AMD are responding with better power efficiency and AI acceleration. Qualcomm must now compete on multiple fronts with competitors who have deeper pockets or strategic advantages.

The growth narrative requires flawless execution across multiple new markets simultaneously. Automotive success isn't guaranteed—the industry is notoriously difficult, margins are lower than mobile, and design cycles are 5-7 years. PC success requires solving software compatibility issues that have plagued ARM computers for a decade. IoT is fragmented across thousands of use cases, each requiring different support. Succeeding in all three while defending mobile share seems optimistic.

The Verdict: Asymmetric Risk-Reward

The truth lies between extremes. Qualcomm isn't going to zero—the patent portfolio and licensing model ensure cash generation for years. But it's also not going to maintain monopolistic margins forever—competition, regulation, and customer dynamics will compress returns. The question is timing and magnitude.

The bull case requires belief that Qualcomm can transition from a mobile monopolist to a diversified technology platform—possible but unproven. The bear case requires belief that multiple competitors will simultaneously succeed where others have failed for decades—also possible but historically unlikely.

For fundamental investors, Qualcomm presents a classic value-with-optionality scenario. The current business generates enormous cash flow at reasonable multiples. The growth initiatives provide free options on massive markets. The risks are real but manageable with the current balance sheet strength.

The key monitorables are clear: Apple modem development progress, Chinese semiconductor advancement, automotive design win conversion to revenue, and regulatory actions globally. Each quarterly report provides updates on these vectors. Smart investors will watch the data, not the narrative.

XII. Epilogue & Power Analysis

The San Diego sunset paints Qualcomm's headquarters in golden light, the kind of California scene that makes you forget this company was born from military technology and academic theories. Forty years after seven engineers gathered in Irwin Jacobs' living room to name their startup, Qualcomm has achieved something remarkable: they've become both inevitable and invisible. Every call you make, every video you stream, every car that parks itself—somewhere in that transaction, Qualcomm collects a toll. The fiscal year 2024 results—$38.96 billion revenue, $10.22 non-GAAP EPS reflecting 21% growth—are just numbers. The real achievement is structural: they've positioned themselves where technology must flow through their patents.

What would the mobile industry look like without Qualcomm? It's a counterfactual worth contemplating. Without CDMA, would we still be using TDMA networks with 1/20th the capacity? Would smartphones exist in their current form without efficient cellular compression? Would 5G have emerged without the technical foundation Qualcomm laid? The answer isn't clear, but the timing certainly would have been different. Innovation might have happened, but it would have been slower, more fragmented, less elegant.

The biggest surprises from researching Qualcomm's history aren't the technical achievements—those were predictable given the founders' backgrounds. The surprises are the roads not taken. Qualcomm could have become a defense contractor like Raytheon. They could have remained a satellite communications company. They could have stayed in manufacturing like Motorola. Each pivot point—from satellites to cellular, from products to licensing, from mobile to everything—required abandoning successful businesses for uncertain opportunities. Most companies can't do that once. Qualcomm has done it repeatedly.

The power analysis reveals something profound about technology markets. Qualcomm possesses what Hamilton Helmer would call "cornered resource" power—their patents—combined with "switching costs" power—the impossibility of building modern communications without their IP. But they've added a third dimension: "process power." The complexity of their technology portfolio, the interdependencies between patents, the system-level integration required—these create a maze that competitors can enter but never exit.

The lessons for founders are uncomfortable because they contradict Silicon Valley orthodoxy. Move fast and break things? Qualcomm spent five years proving CDMA worked. Fail fast? They endured a decade of industry rejection. Pivot quickly? They've been executing the same fundamental strategy—own the standards—for thirty-five years. The company is a monument to patience, conviction, and compound returns to technical excellence.

But perhaps the most important lesson is about the nature of fundamental innovation. Qualcomm didn't disrupt the cellular industry in the Clayton Christensen sense—starting with a worse product for overlooked customers. They offered a radically better solution that required rewiring the entire industry. It wasn't disruption; it was revolution. And revolutions, unlike disruptions, require overwhelming technical superiority, not just good-enough solutions.

The transition from Irwin Jacobs' academic approach to Paul Jacobs' strategic expansion to Cristiano Amon's platform vision shows how leadership must evolve with company lifecycle. Irwin was the professor who could prove why CDMA was superior. Paul was the strategist who understood how to monetize that superiority. Amon is the operator who sees how to extend that superiority beyond mobile. Each era required different skills, but all built on the same foundation: technical excellence creates business value.

Looking forward, Qualcomm faces an existential question: Can a company built on mobile monopoly transform into a diversified technology platform? The early evidence is promising. The chip maker has set out to achieve a combined $22 billion in annual revenue from its automative and IoT segments by its FY29, with $8 billion of that coming from automotive and $14 billion from IoT. But history is littered with dominant companies that couldn't navigate platform shifts—IBM in PCs, Intel in mobile, Nokia in smartphones.

The $15 billion additional share buyback authorization signals confidence, but also raises questions about capital allocation. Should Qualcomm be returning cash or investing more aggressively in new markets? The answer depends on whether you believe their core business is a melting ice cube or a cash-generating fortress. Management clearly believes the latter.

What's undeniable is Qualcomm's transformation of entire industries. They didn't just enable mobile phones; they enabled mobile computing. They didn't just improve cellular networks; they made them the foundation for IoT, automotive, and edge AI. Every connected device, from smart watches to industrial sensors, builds on protocols Qualcomm pioneered. They're not just a company; they're infrastructure.

The final judgment on Qualcomm won't be written for another decade. Will they successfully navigate the transition from mobile to ubiquitous computing? Will their automotive and IoT bets pay off? Will they maintain pricing power as patents expire and competition intensifies? These questions remain open. But what's closed is the historical verdict: Qualcomm took an academic theory, turned it into commercial reality, and in the process, connected the world.