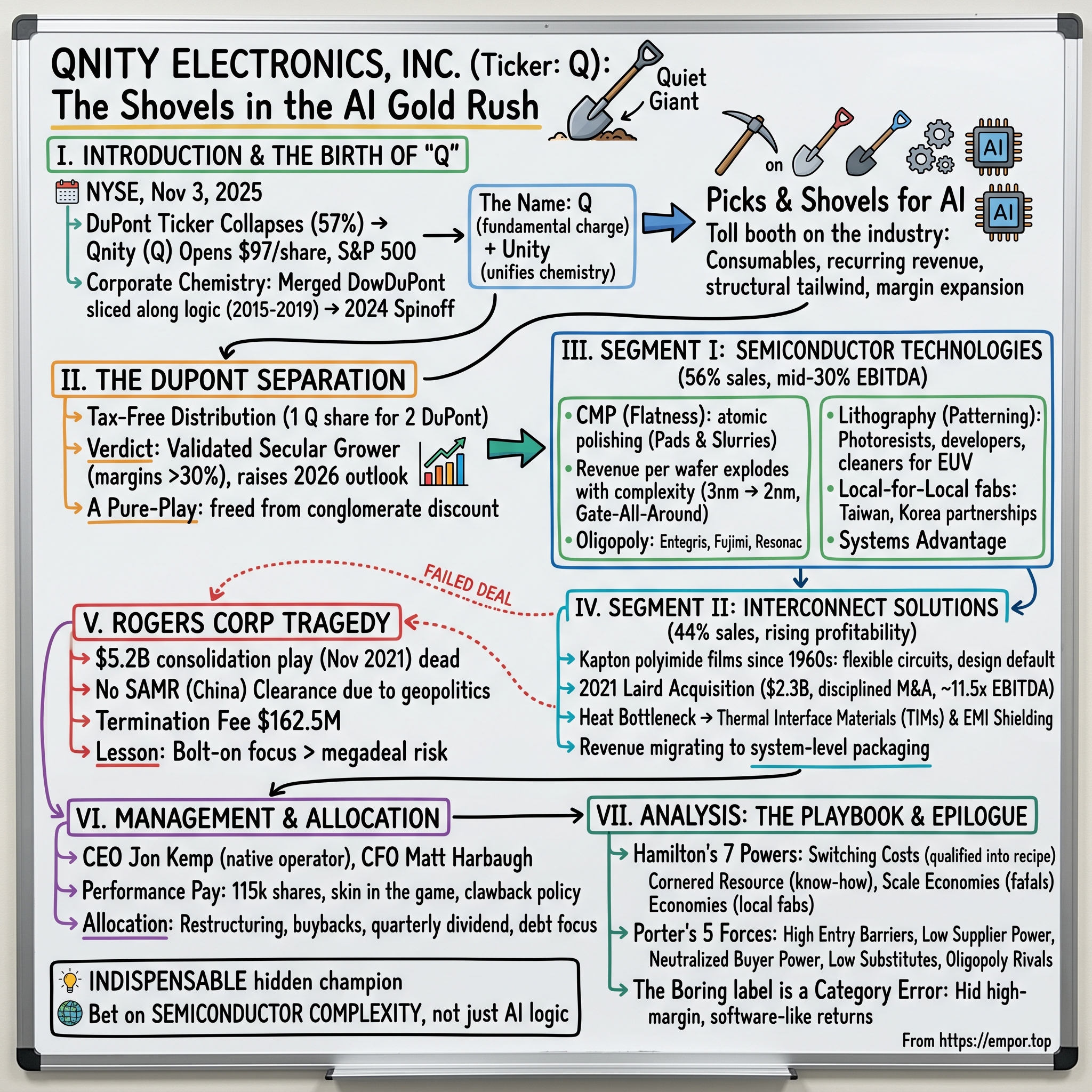

Qnity Electronics: The Shovels in the AI Gold Rush

I. Introduction & The "Quiet Giant" of AI Hardware

Picture the scene on the floor of the New York Stock Exchange on the morning of November 3, 2025. Traders are watching a curious double event unfold on their screens. One ticker — DuPont, a name as old as American industry itself, a company that made the gunpowder for the Mexican-American War and the nylon for parachutes in World War II — is collapsing by more than 57% in a single session. Another ticker, a single, lonely letter — Q — is flickering to life for the very first time, opening near $97 a share and instantly taking its place inside the S&P 500.12

To the untrained eye, it looked like a catastrophe. DuPont shareholders woke up to find more than half their company's market value gone overnight. But this was not destruction; it was a magic trick of corporate chemistry. The 57% that vanished from DuPont had not evaporated — it had simply moved next door, into that single-letter ticker. The "Q" was Qnity Electronics, Inc., and it was carrying with it the crown jewel of the old conglomerate: the chemicals and materials business that quietly sits at the very heart of every advanced semiconductor on Earth.1

Here is the thing that makes Qnity worth two hours of your attention. This is a company that, in its first reported quarter as an independent business, generated $1.3 billion in net sales and $411 million in Adjusted Operating EBITDA — margins north of 30% — yet which almost nobody outside the semiconductor supply chain had ever heard of.3 For two centuries, this business was buried inside other companies, treated as a sleepy "specialty materials" line item, its true economics obscured by the lower-growth industrial and agricultural businesses surrounding it.

The name itself is a small piece of poetry from the marketing department. Qnity is a portmanteau — "Q," the fundamental physics symbol for electrical charge, fused with "unity." It is the sort of name that only makes sense once you understand what the company actually does: it unifies the chemistry of charge — the materials that let electrons move, switch, and stay cool — across the entire semiconductor value chain.

And the power dynamic here is genuinely startling. You cannot build a modern AI accelerator — not an NVIDIA Blackwell GPU, not a custom hyperscaler ASIC, not a high-bandwidth memory stack — without Qnity's materials touching the wafer at multiple points. The company's slurries, pads, photoresists, and films are qualified — a word we will return to many times, because it is the entire moat — inside the most sophisticated fabrication plants on the planet, including 台灣積體電路製造公司 TSMC in Taiwan and 삼성전자 Samsung Electronics in South Korea. When a chip shrinks from one process node to the next, the number of times a Qnity product gets used per wafer tends to increase. This is the rare company that gets paid more, per chip, as Moore's Law gets harder.

This is the classic "picks-and-shovels" investment case, updated for the age of artificial intelligence. In the 1849 California gold rush, the people who reliably got rich were not the prospectors panning for nuggets — it was the merchants selling them the picks, the shovels, and the blue denim trousers. Today, the world is in a frenzied gold rush for AI compute, with hundreds of billions of dollars flowing toward Santa Clara and Hsinchu. Qnity sells the shovels. It does not care which AI chip wins. It cares only that more chips, and more advanced chips, get built.

It's worth pausing on why the picks-and-shovels framing is more than a cute analogy here. The chip designers — NVIDIA, AMD, the hyperscalers building custom silicon — fight a brutal, winner-take-most war where today's champion can be dethroned by next year's architecture. The foundries that physically build the chips, like TSMC, sit one layer below that war, agnostic to which design wins as long as someone keeps ordering wafers. And below even the foundry sits the materials supplier — Qnity — which gets paid no matter whose chip is being fabricated, on whichever foundry's line, using whichever design won this cycle. Each layer down the stack is a step further from the fashion risk of the end product and a step closer to a toll booth on the entire industry. Qnity occupies one of the deepest, most defensible layers in the whole pyramid.

And the toll booth is widening. The global semiconductor industry is marching toward a trillion-dollar annual size, and the capital expenditure required to build the next generation of fabs runs to tens of billions of dollars per facility. Every one of those fabs, once built, becomes a perpetual consumer of consumable materials — the slurries get used up, the pads wear out, the photoresists get washed away with every wafer. Qnity is not selling a one-time piece of equipment; it is selling the chemical "razor blades" that a fab burns through continuously for its entire operating life. That recurring-consumption model is the quiet reason this business throws off so much cash relative to the capital it employs.

Over the next two hours, we are going to trace how this quiet giant came to be: the 200-year corporate lineage and the financial engineering that finally set it free; the two business segments that print money in very different ways; the $5.2 billion acquisition that blew up on the launchpad and, in failing, may have created the company we see today; the operator now running it and how he gets paid; and finally, the bull and bear cases for a business that is simultaneously one of the highest-quality franchises in technology and one of the most geographically concentrated. Let's dig in.

One framing to carry with you throughout: the most interesting thing about Qnity is not any single product but the position it occupies. It is simultaneously close enough to the cutting edge to benefit from every advance in chipmaking, yet diversified enough across the industry to avoid being hostage to any one customer's product cycle. It sells consumables, not capital equipment, so its revenue recurs rather than lumping into boom-and-bust order cycles. And it has been refined — through a merger, two rounds of separation, one triumphant acquisition, and one catastrophic failed one — into a shape that may be close to optimal for the moment it now finds itself in. The question this episode keeps returning to is whether that position is as durable as it looks, or whether its very strengths — concentration in the right customers, in the right geography, at the right moment — are also its deepest vulnerabilities.

II. The DuPont Separation & The Birth of "Q"

To understand how Qnity was born, you have to understand that it was assembled, like a great alloy, from the molten remains of two of the largest chemical companies in American history. And the story of that assembly is one of the most ambitious — and ultimately self-cancelling — pieces of corporate strategy of the last decade.

Rewind to December 2015. Two titans of the old economy, Dow Chemical and DuPont, stunned Wall Street by announcing a "merger of equals" — a roughly $130 billion combination that created, for a brief moment, the largest chemical company on the planet, DowDuPont. But the merger was never the point. The point was the divorce that would follow. The entire logic, championed by activist investors who had circled both companies, was to merge the two behemoths and then immediately slice the combined entity along cleaner lines than either company could have achieved alone. By 2019, DowDuPont had split itself into three: Dow (commodity chemicals), Corteva (agriculture), and a "new" DuPont (specialty products).

This deserves a beat of appreciation as financial choreography, because it is genuinely audacious. You do not normally merge two of the largest companies in an industry in order to break them apart — the transaction costs alone are staggering, and antitrust regulators rarely wave through a combination of direct rivals. But the architects understood something subtle: the most valuable pieces of Dow and DuPont were not the pieces that overlapped, but the pieces that, recombined across the two companies, would form cleaner, more focused industry leaders than either firm contained on its own. Merge, then carve along the seams of logic rather than the seams of legacy corporate boundaries. It was, in effect, a giant deck of cards shuffled together and then re-dealt into better hands. The electronics materials business was one of those better hands, even if it would take another six years and a second round of separations before it was finally played as its own card.

Buried inside that reshuffling was a quiet act of consolidation that mattered enormously for our story. DuPont brought to the table its heritage electronics business — most famously, the polyimide films it had been making since the 1960s, materials with almost magical heat-resistance that NASA used on the Apollo lunar modules. Dow brought its premium electronic chemicals portfolio — the chemical-mechanical planarization slurries and lithography chemistries that had become essential to chipmaking. When the dust settled, "new" DuPont held both halves under one roof: the films-and-laminates heritage of DuPont and the wet-chemistry sophistication of Dow. For the first time, the full stack of electronic materials sat in a single company. The raw ore of Qnity was now in one place; it just needed someone to refine it out.

For five years, it sat there — a high-growth, high-margin business generating envious returns, but trapped inside a conglomerate whose other divisions (water filtration, industrial diversified products) marched to entirely different drummers. Investors who wanted exposure to the semiconductor boom had to swallow the cyclicality of construction-end-market plastics to get it. The conglomerate discount was real and stubborn.

What exactly is a "conglomerate discount," and why does it matter so much to this story? It is the well-documented tendency of the stock market to value a collection of unrelated businesses at less than the sum of those businesses would fetch as standalone companies. The logic is partly about clarity and partly about capital. A semiconductor-materials analyst at a hedge fund cannot easily build a model for a company that is one-third chipmaking chemistry, one-third water purification, and one-third industrial diversified products — each with different growth rates, customers, and economics. So the market applies a blended, cautious multiple to the whole, and the crown jewel never gets the premium valuation it would command alone. Worse, capital allocation inside a conglomerate is often a tug-of-war: cash thrown off by the high-return electronics business can get diverted to prop up slower-growing divisions, starving the jewel of investment. Spinoffs exist precisely to break this dynamic — to let each business be valued, capitalized, and run on its own terms. The entire Qnity thesis begins with the recognition that this business was worth far more on its own than the market would ever credit while it was buried.

The decisive break came on May 22, 2024. DuPont's board announced its intention to separate the company into three independent, publicly traded businesses: a water company, an industrial company (which would retain the DuPont name), and — the prize — an electronics company, then known only by the placeholder of its legal shell, Novus SpinCo 1.[^4] The strategic message was blunt: the electronics business was a different animal — faster-growing, more capital-intensive in R&D, deserving of a "pure-play" valuation that the market would never grant it while it was wrapped in industrial packaging. (DuPont would later refine this plan, ultimately deciding to keep the water business and spin off only electronics — but the electronics separation was always the centerpiece.)

Then came the mechanics, and the mechanics are elegant. On November 1, 2025, DuPont completed the tax-free distribution of the electronics business to its shareholders. The math was simple: for every two shares of DuPont a holder owned as of the October 22, 2025 record date, they received one share of the newly christened Qnity Electronics, Inc.1 Roughly 209 million Qnity shares were distributed into the market in one stroke.1 "Tax-free" is the crucial phrase here — structured properly under U.S. tax law, a spinoff like this hands shareholders stock in the new entity without triggering a taxable event, which is precisely why spinoffs are such a beloved tool for unlocking trapped value.

There's a subtle but important point in the timing that rewards a second look. The separation legally completed on November 1, but "regular-way" trading — the normal market in the new shares — began on November 3, with a brief "when-issued" trading period bridging the two. This is standard spinoff plumbing, but it matters for anyone trying to read the early price action: the first clean print of Qnity as an independent company, and DuPont's corresponding drop, both crystallized on November 3. The market needed only that one session to render its judgment on whether the separation had created or destroyed value.

When regular-way trading opened on November 3, the verdict was immediate and emphatic.1 Qnity debuted around $97 per share and stepped straight into the S&P 500, a rare privilege for a company on its first day of independent life — and a reflection of the fact that it was large enough, profitable enough, and liquid enough to belong among America's 500 most valuable companies from minute one.12 DuPont's own stock fell more than 57% that day not because the company had been wounded, but because that 57% had simply walked out the door wearing a new name.2

The early scorecard suggests the market's enthusiasm was not misplaced. In its first reported quarter as an independent company, Qnity delivered net sales of roughly $1.3 billion, up about 18% year-over-year, with organic growth — stripping out currency and portfolio effects — of around 17%, and it raised its full-year 2026 outlook in the same breath.3 For a "boring" materials company, those are eye-catching growth rates, the kind usually reserved for software, and they validated the core premise of the spinoff: that freed from the conglomerate, this business would be revealed as a genuine secular grower rather than a sleepy chemical division. Management guided full-year net sales toward the $5.2-to-$5.4 billion range with Adjusted Operating EBITDA of roughly $1.5-to-$1.6 billion, implying the kind of high-20s-to-30% margin that anchors the entire investment case.3

What emerged blinking into the daylight was substantial: a business with more than 10,000 employees, operations in over 80 countries, 39 manufacturing sites, and 17 R&D facilities worldwide, addressing a total market the company pegs at over $30 billion — with roughly two-thirds of its portfolio tied directly to semiconductors.4 To run it, the board installed Jon Kemp, who had led DuPont's Electronics & Industrial division, with Matt Harbaugh as CFO.4 After two centuries of being someone else's division, the shovel-maker finally had its own storefront. Now let's go inside and see what's on the shelves — starting with the segment that does the most delicate work in all of manufacturing.

III. Segment I: Semiconductor Technologies—The Flat-Maker & Advanced Patterning

Here is a fact that sounds like a riddle: the single most important physical property of a modern computer chip, the thing that determines whether a $10 billion fabrication plant produces working silicon or expensive gravel, is flatness. Not speed, not heat, not exotic materials — flatness. And the global champion of flatness is Qnity's largest segment, Semiconductor Technologies, which contributes roughly 56% of company net sales and carries the richest margins in the business, with Operating EBITDA in the mid-30% range.5

Let's start with the physics, because it's genuinely awe-inspiring and you cannot appreciate the moat without it. A leading-edge logic chip — the kind that powers an AI server — is built up in layers, like a microscopic city constructed floor by floor. Each layer holds billions of transistors and the copper "wiring" that connects them. The industry is now ramping the 3-nanometer generation at TSMC and Samsung and pushing toward 2-nanometer volume production.4 To put "nanometer" in perspective: a single human hair is about 80,000 to 100,000 nanometers wide. The features Qnity's chemicals help carve are smaller than many viruses. At this scale, individual atoms are no longer a rounding error — they are the engineering tolerance.

Chemical-Mechanical Planarization: the art of atomic polishing

Now, the problem. As you build each new floor of the chip-city, the surface you just laid down is never perfectly smooth — there are tiny hills and valleys where the copper and insulation sit at slightly different heights. If you try to build the next layer on top of an uneven surface, the lithography that prints the next pattern will be out of focus, and your chip dies. So before every new layer, the wafer must be polished back to a mirror-flat surface, accurate to within a few atoms across a disc the size of a dinner plate.

This is chemical-mechanical planarization, or CMP, and it is exactly what it sounds like: a combination of chemical dissolution and mechanical grinding, performed simultaneously. The wafer is pressed against a specialized polyurethane polishing pad — Qnity sells these under brands like Ikonic™ and Visionpad™ — while a liquid "slurry" full of precisely-sized abrasive nanoparticles and reactive chemistry flows across it.4 The chemistry softens the surface; the abrasive shears it away; the pad controls the pressure. Get the recipe wrong by a hair, and you either polish too much (scrapping the wafer) or too little (defocusing the next layer). Imagine sanding a hardwood floor flat to the thickness of a single molecule, across the whole floor, every time, with zero scratches. That is CMP.

The reason this is such a wonderful business is that the number of CMP steps explodes as chips get more advanced. An older chip might require a handful of polishing steps. A leading-edge AI logic chip can require dozens. Every new architectural trick — more metal layers, new transistor structures like gate-all-around — adds polishing steps, and every polishing step needs Qnity's pads and slurries. This is the secret engine of the segment: Qnity's revenue per wafer climbs structurally as the industry advances, independent of how many wafers get made.

To make that concrete, consider what "gate-all-around" — the transistor architecture now entering production at the leading edge — actually demands. Older transistors were essentially flat switches; the industry then went vertical with "FinFET" structures, and is now wrapping the conducting channel entirely in gate material on all four sides for finer control. Each of these leaps adds layers, adds materials, and adds steps where the wafer must be polished flat before the next stage can proceed. The same is true of the relentless increase in interconnect layers — the microscopic copper "wiring" stacked above the transistors, which on a leading chip can run to more than a dozen distinct levels, each one requiring its own planarization. So even in a year where the number of chips the world buys is flat, the intensity of CMP consumption per chip ratchets upward. This is why a CMP franchise can grow through a volume downturn that would crush a simpler components supplier: complexity, not just volume, is the growth driver.

There's a second, subtler reason CMP is such a beautiful business: the pad and the slurry are co-dependent consumables tuned to each other. The pad's surface texture, hardness, and grooving interact with the slurry's particle size and chemistry to determine the polishing result. A supplier who makes both — as Qnity does — can engineer the pad-slurry system as a matched pair, optimizing the whole rather than one half. That systems advantage is hard for a single-product competitor to match, and it deepens the qualification lock-in, because the customer is qualifying not one material but an integrated recipe.

The competitive landscape in CMP is a tight oligopoly of disciplined players. Qnity's most formidable rival is Entegris, which built enormous scale — roughly $3.5 billion-plus in sales — partly by acquiring CMC Materials (formerly Cabot Microelectronics) for about $6.5 billion in 2022, a price north of 20 times EBITDA that signaled just how strategic these materials had become.6 Beyond Entegris, Qnity contends with Japanese chemical specialists, including Fujimi Incorporated and 株式会社レゾナック Resonac (the company formed from Showa Denko's chemicals empire). This is not a fragmented commodity market; it is a club of a few elite formulators, and entry is effectively closed.

Notice what that 20-times-plus multiple Entegris paid for CMC tells you about the whole category. When a sophisticated, deal-disciplined acquirer pays north of twenty times earnings for a CMP materials business in an arm's-length, competitive process, the market is revealing its belief that these are not commodity chemicals at all — they are mission-critical, hard-to-displace franchises with long runways. That transaction effectively re-rated the entire peer group, Qnity's CMP business included, and it explains why management has been so reluctant to dilute the franchise with overpriced empire-building of its own. When your own assets are implicitly worth twenty-plus times earnings, buying someone else's at the same price creates no value — a discipline that will matter when we get to capital allocation.

Photolithography and advanced patterning: printing with light at the edge of physics

If CMP is about making the floor flat, photolithography is about printing the blueprint onto it — and Qnity plays here too, supplying the photoresists and cleaning chemistries that make the printing possible.4 A photoresist is a light-sensitive chemical coating: you shine patterned light through a mask onto the resist, and where the light hits, the chemistry changes, allowing you to wash away either the exposed or unexposed regions and etch the pattern beneath. The most advanced chips now use Extreme Ultraviolet (EUV) light, with a wavelength so short it would be absorbed by ordinary air and must be generated by vaporizing droplets of tin with a laser inside a vacuum. At those wavelengths, the photoresist chemistry is brutally unforgiving — a few stray molecules can ruin a pattern.

Here Qnity squares off against the Japanese masters of the craft: 東京応化工業 Tokyo Ohka Kogyo (TOK) and JSR Corporation, firms that have refined resist chemistry over decades. Qnity's edge is less about any single molecule and more about proximity and partnership. The company runs what the industry calls "local-for-local" facilities — R&D and manufacturing sites placed physically near the great fabs, in Hsinchu, Taiwan, and Cheonan, South Korea. This lets engineers co-develop recipes with the customer's process team in real time, iterating on the actual production line. That collaborative intimacy spreads R&D overhead across the industry's highest-volume producers and makes Qnity a partner rather than a vendor.

It is worth dwelling on just how much of the supply chain "leverage" sits in this segment beyond resists. Photoresists grab the headlines, but the unglamorous adjacent chemistries — the developers that wash away the exposed resist, the post-etch cleaning solutions that strip away residue without damaging delicate structures, the specialty gases and ancillary formulations — are equally indispensable and equally sticky. A fab does not buy a photoresist; it buys an entire wet-chemistry ecosystem qualified to work together. By offering breadth across that ecosystem, Qnity becomes harder to dislodge with every adjacent product it qualifies, because each addition raises the switching cost of the whole bundle. This is the quiet compounding mechanism behind the segment's durability: not one moat, but a lattice of overlapping qualifications that grows thicker over time.

There is also a geopolitical wrinkle that, counterintuitively, works in Qnity's favor. As governments push to "de-risk" and regionalize semiconductor supply chains — with new fabs rising in Arizona, Japan, and Germany alongside the established hubs in Taiwan and Korea — every new fab is a fresh greenfield qualification opportunity. A supplier with global, local-for-local manufacturing is positioned to serve these new nodes wherever they appear, while a regional specialist may struggle to follow its customers abroad. The very fragmentation of the geopolitical map creates more places that need Qnity's chemistry close at hand.

Why nobody ever switches

And this brings us to the punchline of the whole segment, the reason its margins are so durable. Inside a fab, a chemical supplier is never just a supplier — it is a co-author of the recipe. When Qnity's slurry or photoresist gets "qualified" into a customer's process, it has been validated across months of testing, tuned to that fab's exact equipment, and woven into a recipe that reliably produces working chips at high yield. Now consider the asymmetry: a single bad batch of slurry can destroy a wafer worth tens of thousands of dollars, and a contamination event can halt a multi-billion-dollar fab for days. Against that downside, what does a customer gain by switching to a competitor's chemically-similar product to save a few percent on price? Essentially nothing — and they risk everything. So they don't switch. The qualification process that takes years to win takes years to lose. It is one of the stickiest customer relationships in all of manufacturing, and it is why this segment can compound quietly for a very long time. Now let's cross the floor to the other half of the business — where the story shifts from the chip itself to the heat it produces.

IV. Segment II: Interconnect Solutions & The AI Thermal Interface Boom

In the summer of 1969, when the Apollo 11 lunar module descended toward the Sea of Tranquility, parts of its skin were wrapped in a gold-colored film that could survive the brutal swing between the searing sun and the deep cold of space. That film was DuPont's Kapton® polyimide — and more than half a century later, a direct descendant of that same material is one of the foundational products of Qnity's second segment, Interconnect Solutions, which accounts for roughly 44% of company net sales.5

Interconnect Solutions is the business of connection and survival — getting signals to move at near-light speed between chips, and getting the punishing heat those chips generate safely out of the system. Its backbone is a family of materials that has defined flexible electronics for generations: Kapton® polyimide films and Pyralux® flexible copper-clad laminates. To understand why these matter, picture the inside of any modern device. A rigid green circuit board is fine for a desktop computer, but try folding one into a smartphone hinge, a foldable display, or the impossibly tight confines of a laptop — it cracks. Flexible printed circuits, built on Kapton, can bend, fold, and flex millions of times without failing. They are the nervous system that lets electronics be thin, light, and shaped like the products we actually want.

There's a reason these films command durable pricing rather than commodity economics. Polyimide is fiendishly difficult to make well at scale — the polymer chemistry, the casting process, the purity control all require know-how accumulated over decades. Kapton has been a category-defining brand since the 1960s, the kind of product so dominant that engineers use its name generically, the way people say "Velcro" or "Xerox." When a brand becomes the default specification in datasheets and design guides across an entire industry, displacing it requires not just matching the product but rewriting thousands of engineers' habits. That is a cornered resource hiding in plain sight.

But the heritage materials are not the headline. The headline is heat — and how Qnity got into the heat business.

The 2021 Laird acquisition: a masterclass in disciplined M&A

To see how, we rewind to early 2021. The semiconductor world was roaring back from pandemic shortages, and DuPont's electronics leadership made a move that, in hindsight, looks prescient. On March 8, 2021, DuPont announced it would acquire Laird Performance Materials from the private equity firm Advent International for $2.3 billion in cash, with the deal closing that July.78 Laird was a specialist in two things that were about to become extraordinarily valuable: electromagnetic interference (EMI) shielding — keeping the radio noise from one component from corrupting its neighbor — and thermal management, the science of moving heat away from hot chips.8

Now, the question every disciplined investor asks: did they overpay? Let's run the numbers, because the answer reveals the character of the management team. Laird generated about $465 million in revenue in 2020 at roughly a 30% adjusted EBITDA margin, which puts its standalone EBITDA near $140 million.8 Paying $2.3 billion for $140 million of EBITDA works out to roughly 15.3 times — a full price on its face. But the deal came with about $60 million in expected pre-tax cost synergies, and once you fold those in, the effective multiple drops to around 11.5 times. Set that against the comparable transaction of the era — Entegris paying north of 20 times for CMC Materials the following year — and DuPont's Laird purchase looks not just reasonable but shrewd.6

There's a tell in the deal's history that's worth lingering on. Advent had bought this same business — then called Laird Technologies — for just under $1.4 billion in July 2018.7 Selling it three years later for $2.3 billion handed the private equity firm a handsome return. When you buy an asset that just made its previous owner a fortune, you have to be confident you can do something the prior owner couldn't. DuPont's bet was that Laird's shielding and thermal capabilities, plugged into DuPont's deep fab relationships, would compound far faster inside the larger electronics platform than as a standalone PE portfolio company. That bet is now paying off in a way few could have modeled in 2021.

The hidden gem: when heat became the bottleneck

Because here is what changed everything. For most of computing history, the limiting factor on performance was processing power — how many transistors you could cram on and how fast you could clock them. But in the AI era, with racks of GPUs like NVIDIA's H100 and Blackwell-class accelerators packed together drawing kilowatts each, the binding constraint flipped. It is no longer just can you compute fast enough — it is can you get the heat out fast enough and the power in densely enough before the silicon cooks itself.4

This is where Laird's quiet little thermal business turned into a rocket. Thermal interface materials — TIMs — are the unglamorous but critical compounds that sit between a hot chip and its heatsink, filling the microscopic air gaps (air is a terrible conductor of heat) so that heat can flow out efficiently. Here's the intuition: place even a beautifully machined metal heatsink directly on a chip, and at the microscopic level the two surfaces touch only at a few high points, leaving tiny pockets of air in between that act as insulation — exactly what you don't want. A thermal interface material is the engineered paste, pad, or gel that fills those gaps with something far more conductive than air, creating a continuous thermal highway from silicon to sink. In a phone, getting this slightly wrong means a warm device. In an AI server rack drawing tens of kilowatts, getting it wrong means thermal throttling, lost performance, and ultimately failed hardware — which is why hyperscalers will pay real money for materials that perform consistently at the bleeding edge.

As AI chips got hotter and denser, demand for high-performance TIMs and EMI shielding surged. The effect on Qnity's numbers has been dramatic: the Interconnect Solutions segment posted explosive profitability growth, with EBITDA in the segment rising sharply year-over-year on the back of AI-driven demand for thermal and shielding materials.3 The beauty of it, from an investor's standpoint, is that these are consumable, design-in components — once a server platform is engineered around a specific thermal material, every unit of that platform built carries the material with it, and the next generation of even hotter chips only raises the performance bar that favors the specialist.

There is a deeper structural shift worth naming here, because it reframes how to think about Qnity's growth. For decades, the value in a computer concentrated relentlessly into the chip — Moore's Law made the transistor cheaper and the silicon king, while everything around it (the board, the package, the connectors) was treated as low-value commodity plumbing. The AI era is partially reversing that. As it gets harder and more expensive to cram more performance onto a single die, the industry is increasingly chasing performance at the level of the system — stitching multiple chips together in advanced packages, stacking memory vertically, and moving data optically between them. That means more and more of the engineering difficulty, and the value, is migrating out of the chip and into the packaging, interconnect, and thermal layers. Qnity happens to sit on both sides of that shift: it sells into the chip via Semiconductor Technologies and into the package-and-system via Interconnect Solutions. Whichever way the value migrates, it migrates toward Qnity's shelf.

And the optionality from here is real. As AI architectures move toward co-packaged optics — putting the optical components that move data between chips right next to the processors — the thermal and signal-integrity challenges multiply. More heat in tighter spaces, more sensitive components that cannot tolerate interference. Every one of those trends plays directly to the materials Qnity acquired in 2021 and the films it has made for half a century. The Apollo-era heat shield, it turns out, found its second act inside the AI data center. But not every acquisition the company's predecessor attempted ended in triumph — and the one that failed may have been even more important than the one that worked.

V. The Rogers Corporation Tragedy: A Masterclass in Regulatory Risk

Every great company has a deal that got away, and in the lore of what became Qnity, that deal is Rogers Corporation. It is a story about ambition meeting geopolitics — and about how a $5.2 billion dream died not in a boardroom or a courtroom, but in the silence of a regulator that simply never said yes.

In November 2021, with the Laird integration underway and the electronics business feeling its strength, DuPont swung for the fences. It announced an agreement to acquire Rogers Corporation for $5.2 billion. The strategic logic was seductive. Rogers was a premier maker of high-performance laminates and engineered materials for exactly the markets everyone believed would define the next decade: electric vehicles, 5G wireless infrastructure, and advanced circuit boards. Bolting Rogers onto the existing Interconnect portfolio would have created a colossus in high-frequency, high-reliability materials — a genuine consolidation play to dominate the laminate world. This was meant to be the deal that vaulted the electronics business into a different weight class.

Then the deal ran into a wall that no amount of money or strategic logic could move: 国家市场监督管理总局 SAMR, China's State Administration for Market Regulation.

Here is the geopolitical reality that the deal exposed. Major global mergers, even between two American companies, typically require antitrust clearance from regulators in every significant market where the combined firm operates — and China, as the world's largest market for electronics and a manufacturing superpower, is one of those gatekeepers. Under normal conditions, SAMR clearance is a formality. But 2021 and 2022 were not normal conditions. U.S.-China technology tensions were escalating sharply, with Washington tightening semiconductor export controls and Beijing looking for points of leverage. American tech mergers became hostage to the broader rivalry, and SAMR developed a pattern of letting strategically sensitive deals simply languish — neither approved nor formally rejected, just held in limbo until the clock ran out.10

That is exactly what happened to Rogers. Month after month passed with no clearance. The merger agreement contained an outside date — a deadline of November 1, 2022, after which either party could walk away if the deal hadn't closed.9 As that date approached and SAMR remained silent, the outcome became inevitable. On November 1, 2022, DuPont announced it was terminating the agreement, unable to obtain timely regulatory clearance.9 Under the terms of the deal, DuPont paid Rogers a regulatory termination fee of $162.5 million — a painful nine-figure check for a deal that produced nothing.9

Think about the cruelty of that structure for a moment, because it captures the modern reality of cross-border M&A. DuPont did nothing wrong operationally — no financing fell through, no due-diligence skeleton emerged, no change of heart. The deal died purely because a foreign regulator chose inaction as a weapon, letting the clock run out rather than issuing a "no" that could be appealed or negotiated. And the penalty for that geopolitical bad luck fell entirely on the acquirer: $162.5 million paid to the target for the privilege of being unable to complete a purchase that both companies wanted. The break fee, designed to protect Rogers from a flaky buyer, ended up compensating Rogers for being collateral damage in a trade war. It is a vivid illustration that in today's environment, the biggest risk to a megadeal is not the boardroom or the bankers — it is the map.

For Rogers shareholders, it was a bloodbath. The stock, which had been trading up near the deal price in anticipation of the buyout, collapsed roughly 44% as the acquisition premium evaporated overnight. A company that had spent a year preparing to be absorbed suddenly had to stand on its own again, its strategic future thrown back into question.

But here is where the story turns from tragedy to something more interesting — because the Rogers failure may have been the most important non-event in Qnity's creation. Think about the counterfactual. Had the Rogers deal closed, DuPont's electronics business would have been larger, more leveraged, and far more entangled in the slow, capital-heavy work of integrating a massive acquisition. Instead, management was forced to confront a humbling lesson: in an era of geopolitical fragmentation, betting the company on a single mega-merger that requires the blessing of an adversarial regulator is a fragile strategy.

The strategic response was a pivot. Rather than chase transformational consolidation, the electronics business shifted toward organic development and disciplined, mid-sized, bolt-on acquisitions — deals small enough to clear regulatory review easily and integrate cleanly, like the Spectrum Plastics and Donatelle additions that expanded its capabilities without betting the franchise.[^12] The contrast with Rogers is the whole lesson. A $5.2 billion megadeal requires the assent of regulators on three continents, takes more than a year to close, and concentrates enormous risk in a single bet. A few-hundred-million-dollar bolt-on can close in a quarter, sails under the regulatory radar, and — if it disappoints — costs a rounding error rather than the franchise. In a fragmented geopolitical world, the option value of being able to actually complete your deals turns out to be worth a great deal. The post-Rogers playbook traded the thrill of the transformational acquisition for the reliability of the small, swallowable one, and that temperament now defines how Qnity approaches capital deployment as an independent company. And it pushed leadership toward a more profound conclusion: this business did not need to be the biggest. It needed to be focused, nimble, and independent — a pure-play that could move at the speed of its customers without a conglomerate parent slowing it down. In that sense, the regulator in Beijing that killed the Rogers deal helped midwife the Qnity spinoff. The dream of consolidation died so that the dream of independence could be born. And independence required a new kind of leader — one cut from operator's cloth rather than the generalist mold of the conglomerate era.

VI. Current Management & Capital Deployment

When you spin a business out of a 200-year-old conglomerate, the single most important question is: who's driving? A pure-play semiconductor materials company lives or dies on the credibility of its leadership with a handful of the most demanding customers on Earth. Hand the wheel to a generalist conglomerate executive who rotates through divisions every few years, and the fab engineers in Hsinchu will smell it immediately. Qnity's board chose differently.

The operator at the helm

Meet Jon D. Kemp, Qnity's Chief Executive Officer. Kemp is not a parachuted-in turnaround artist or a finance-track CEO — he is a native of this world. He led DuPont's Electronics & Industrial business as its president, the very division that became Qnity, and before that spent years inside the semiconductor supply chain learning how fabs actually buy, qualify, and trust their materials partners.14 When Kemp talks to TSMC or Samsung, he is speaking as a peer who understands their yield anxieties at a molecular level. That continuity matters enormously: the spinoff didn't hand the company to a stranger; it handed an established business to the person who had already been running it. Alongside him sits CFO Matt Harbaugh, completing a leadership team that knows where every body is buried in the old DuPont electronics portfolio.4

Skin in the game

The most revealing thing about any management team is how they get paid and how much they personally stand to win or lose. Kemp's incentive structure is built, on paper, to align him tightly with shareholders. His direct equity holdings — which grew to roughly 115,762 shares after a stock award vested in February 2026 — represent a meaningful personal stake, on the order of tens of millions of dollars at prevailing prices, anchoring his net worth to Qnity's share performance.11 When the stock moves, Kemp feels it in his own portfolio, which is precisely the alignment long-term owners want to see.

A skeptic might note that a CEO's percentage ownership of a company this size is necessarily small — a fraction of one percent — and wonder whether that is really enough "skin in the game" to matter. The honest answer is that in a company worth many billions, no professional manager will ever own a founder-sized slice, so the question is not the percentage but the absolute dollar exposure relative to the executive's own wealth. By that test, a stake worth tens of millions, concentrated in a single stock, is a powerful motivator: it is the bulk of Kemp's personal fortune riding on Qnity specifically rather than diversified away. The more important alignment lever, though, is not the static holding but the flow of future pay, which is where the design gets interesting.

The architecture of his pay is heavily weighted toward performance rather than guaranteed cash. The bulk of the package sits in long-term incentives, split between Performance Share Units — which only pay out if the company hits multi-year targets on metrics like return on invested capital and cumulative free cash flow — and Restricted Stock Units that vest over time. The design philosophy is straightforward: pay modestly in salary, pay heavily in equity that only becomes valuable if Kemp actually creates durable value and generates cash. Shareholders ratified this approach decisively at the company's first annual meeting in May 2026, with the advisory "say-on-pay" vote passing overwhelmingly — roughly 136 million shares in favor against about 6 million opposed.12 Layered on top is an SEC-compliant clawback policy that allows the company to recover incentive compensation in the event of a financial restatement or serious misconduct — a governance backstop that has become standard for newly public companies but is no less important for it.

The capital allocation philosophy

Now, what is Kemp actually doing with the company's cash? Here the post-spinoff playbook reveals a deliberate contrast with the old conglomerate's swing-for-the-fences M&A. The first priority is internal: a multi-year operational restructuring aimed at stripping out the overhead that inevitably comes with separating from a parent — duplicate corporate functions, redundant systems, the cost of standing up an independent public company. Management has targeted meaningful run-rate EBITDA savings from this program over the next several years, the kind of self-help margin expansion that doesn't depend on the market cooperating.

The second priority is returning cash to owners. Rather than hoarding capital for another transformational acquisition — the strategy that produced the Rogers debacle — Qnity came out of the gate with a shareholder-friendly posture, authorizing share repurchases and initiating a regular quarterly dividend.3 For a company generating Adjusted Free Cash Flow guided at $500 to $600 million for 2026, this signals confidence: management believes it can fund its growth, pay down separation costs, and hand cash back to shareholders simultaneously.3 It is the behavior of a team that has decided discipline, not empire-building, is the path to a premium valuation.

A word of second-layer diligence is warranted on the balance sheet, because newly spun-off companies often carry a hidden inheritance: debt. When a parent separates a division, it frequently loads the new entity with borrowings — sometimes to fund a cash payment back to the parent, sometimes simply to "right-size" the capital structure. The amount of leverage Qnity carries out of the gate, and how quickly it can be paid down with that free cash flow, will shape how much room management actually has to fund buybacks, dividends, and growth investment at the same time. A pristine income statement can coexist with a demanding debt schedule, and investors should read the cash-flow statement, not just the earnings headline, to see how much of that $500-to-$600 million is truly discretionary. This is the kind of detail that separates a genuinely shareholder-friendly capital plan from one that only looks generous until the next refinancing.

Whether that discipline holds when the next shiny acquisition target appears is one of the things long-term owners will watch most closely. To judge whether it's working, though, you need a framework for what actually makes this business defensible — so let's war-game the competitive position.

VII. The Playbook: Hamilton's 7 Powers & Porter's 5 Forces

Strip away the chemistry and the geopolitics, and the question every investor ultimately wants answered is simple: is this business defensible, and for how long? Let's run Qnity through two classic frameworks — Hamilton Helmer's 7 Powers and Michael Porter's Five Forces — and then zero in on the handful of numbers that actually tell you whether the thesis is intact.

Hamilton's 7 Powers

The dominant power here, the one that does most of the work, is switching costs. We touched on this in the semiconductor segment, but it bears stating as the central pillar of the entire investment case: once Qnity's CMP slurries or EUV photoresists are qualified into a customer's production recipe, ripping them out means months of requalification and the risk of multi-million-dollar yield losses on wafers that cannot be redone. The customer's downside from switching dwarfs any plausible savings. This is the anchor that lets margins persist.

The second power is a cornered resource — assets a competitor simply cannot replicate at any price. For Qnity, this is the accumulated intellectual property and, more importantly, the tacit know-how: decades of patents on polyimide molecular formulations and slurry particle engineering, layered over institutional knowledge of how to actually synthesize these compounds at scale with consistent purity. You cannot hire this overnight or reverse-engineer it from a data sheet. It lives in the heads of chemists and the muscle memory of manufacturing lines refined over generations.

The third power is scale economies, expressed through that "local-for-local" manufacturing footprint near the great fabs of Taiwan and Korea. Because Qnity sells to the highest-volume producers in the industry, it can spread its substantial R&D budget across an enormous denominator of output, out-investing smaller rivals in the next generation of chemistry while charging competitive prices. A subscale competitor faces the same R&D bill with a fraction of the volume to absorb it — a losing position that tends to compound over time.

Porter's Five Forces

Run the same business through Porter's lens and the picture is strikingly favorable:

Barriers to entry are extreme. The capital, the multi-year R&D cycles, and — above all — the customer qualification loops required to formulate sub-10nm chipmaking chemicals are astronomical. A new entrant would need years and a fortune just to get a first product tested, with no guarantee of qualification. This is about as closed a market as exists in industrial technology.

Supplier power is low. Qnity's raw inputs are largely commodity chemical feedstocks available from many sources. The value Qnity adds is in the formulation, not the ingredients, so it is not held hostage by any upstream supplier.

Buyer power is moderate — and beautifully balanced. On one hand, customers like TSMC and Samsung have colossal scale and could in theory squeeze any vendor. On the other, their obsessive focus on yield makes them deeply reluctant to disrupt a qualified material to save money. The buyers are powerful, but their own risk-aversion neutralizes much of that power.

The threat of substitutes is very low. There is no alternative physics that eliminates the need to planarize a wafer or to route high-frequency signals through specialized substrates. As long as chips are built in layers, someone has to make them flat, and as long as signals must travel, someone has to carry them. The functions Qnity performs are not going away.

Rivalry is a structured oligopoly. The field consolidated around a few disciplined, elite players — Qnity, Entegris, Resonac, Tokyo Ohka Kogyo — who compete fiercely on technology but rarely on destructive price wars, because everyone understands that qualification stickiness makes share gains slow and price-cutting mostly destroys industry profit without moving share.

The combined picture is unusual. It is rare to find a business where four of the five Porter forces point decisively in the incumbent's favor and the fifth — buyer power — is largely neutralized by the buyers' own behavior. Most "great" businesses have one or two strong moats and a couple of vulnerabilities. Qnity's profile is more like a fortress with multiple, mutually reinforcing walls: high switching costs make customers reluctant to leave, cornered chemical know-how makes the products hard to copy, scale economies make it hard to compete on cost, and extreme entry barriers mean no fresh challengers are coming. The honest caveat is that fortresses can still fall — not to a frontal assault, but to a change in the underlying terrain. For Qnity, the terrain risk is not a competitor; it is geopolitics and concentration, which is exactly why those, rather than rivalry, dominate the bear case we are about to lay out.

The 3 KPIs that matter most

For all the frameworks, an investor really only needs to keep an eye on three numbers to know whether this story is on track:

First, segment EBITDA margins. The whole thesis rests on Semiconductor Technologies holding its mid-30% margin and Interconnect Solutions expanding toward the high-20s. If those margins erode, it would be the first sign that switching costs are weakening or that competition is finally biting.5

Second, organic net sales growth relative to wafer starts. Because Qnity's content-per-wafer should rise as nodes advance, its organic growth ought to consistently outpace the growth in global wafer volumes. If sales merely track wafer starts, the "more content per chip" thesis is failing; if they outrun it, the thesis is working.

Third, customer concentration. With its largest customers — historically Samsung and TSMC at roughly 11% and 7% of sales respectively — Qnity's fate is tied to a small number of giants. Watching whether that concentration creeps higher or moderates tells you how much single-customer risk is building under the surface.

These three numbers are the dashboard. Now let's close by weighing what could go gloriously right against what could go badly wrong.

VIII. Analysis: The Bull vs. Bear Case & Epilogue

Every great franchise is a tension between an irresistible tailwind and a concentrated risk, and Qnity is a near-perfect specimen of that tension. Let's lay out both sides honestly.

The bull case

The bull case starts with a piece of physics that functions like a built-in growth engine. The transition to the 2-nanometer transistor node — already ramping at the leading fabs — does not just make chips a little faster; it materially increases the number of manufacturing steps each wafer must pass through. Industry estimates suggest the move to advanced nodes can lift the number of required CMP polishing steps by 30 to 40%.4 Read that again: as the world's chipmakers march down the node roadmap, they don't just buy more of Qnity's products — they need proportionally more per wafer. Qnity's revenue can grow even if the unit volume of chips stays flat, simply because each chip consumes more of its materials. That is the rare structural tailwind that compounds without requiring the company to win new customers.

Layer on top of that the AI thermal boom. The explosion in high-density AI server racks has turned heat dissipation into the gating constraint on data-center performance, and the thermal interface materials and EMI shielding from the Laird acquisition sit precisely in that bottleneck. This is no longer a niche line item; it is a core growth driver with optionality stretching into co-packaged optics and next-generation packaging.

And finally, the bull case rests on the company itself being clean. Freed from the conglomerate, Qnity now runs a focused capital allocation strategy — internal cost-out, buybacks, and a growing dividend — with management incentives tied to return on invested capital and free cash flow. It is a high-margin, cash-generative pure-play in the single most important industrial trend of the decade, finally valued on its own merits.

The bear case

Now turn the card over, because the risks are just as concentrated as the opportunities. The single largest is geography. Roughly four-fifths of Qnity's revenue comes from the Asia-Pacific region, with the crown jewels of its customer base concentrated in Taiwan and South Korea. This is the flip side of "local-for-local": the company is magnificently positioned to serve the world's leading fabs precisely because it is wedded to two of the most geopolitically sensitive locations on the planet. Any serious disruption in the Taiwan Strait — military, political, or even a severe trade rupture — would strike at the very heart of Qnity's revenue base. The same SAMR dynamic that killed the Rogers deal is a standing reminder that this company operates on a geopolitical fault line, and no amount of operational excellence can fully hedge a conflict in the strait.

The second risk is the mirror image of the customer-stickiness moat. Concentration cuts both ways. With Samsung and TSMC representing a meaningful slice of sales, the loss of share at even one major foundry — say, losing a qualification battle at the 2nm node — would be disproportionately painful. The same dynamic that makes wins durable makes losses durable too.

The third risk is cyclicality. While the semiconductor business enjoys secular tailwinds, the Interconnect segment carries exposure to consumer electronics — PCs, smartphones, and other end markets that swing with the broader economy. In a cyclical chip downturn, that exposure can compress earnings and remind investors that even a picks-and-shovels business is not immune to the gold rush going cold for a season.

A fourth, quieter risk deserves a mention precisely because it runs against the grain of the bull case: the possibility that the current AI-driven demand surge is partly a cyclical bubble dressed as a secular trend. The thermal and shielding boom that has lifted Interconnect profitability is real, but a meaningful slice of it rests on a historically aggressive wave of data-center construction by a handful of hyperscalers. If that capital expenditure cycle cools — whether because AI monetization disappoints, because the hyperscalers digest what they have built, or simply because every boom eventually pauses — the steepest part of Qnity's recent growth could flatten faster than the secular story implies. The company's broad exposure across the entire chip industry cushions this, but it does not eliminate it. Distinguishing the durable demand from the cyclical spike is the single hardest judgment an investor in this name has to make.

There is also a governance and execution dimension that newly independent companies always carry. Standing up the systems, controls, and corporate functions that a parent used to provide is genuinely hard, and the multi-year restructuring program is both an opportunity and an execution risk: hit the targets and margins expand nicely; stumble on the separation, and the promised savings get eaten by one-time costs and disruption. The first few years of any spinoff are when these wrinkles surface, and Qnity is only months into that journey.

Myth vs. reality

It is worth puncturing one comfortable narrative before we close. The myth is that Qnity is a pure, uncomplicated "AI play" — a clean way to ride the data-center boom. The reality is more nuanced. A large share of its semiconductor materials demand still flows from the entire chip industry — memory, mature-node logic, automotive, and consumer silicon — not just bleeding-edge AI accelerators. That is actually a strength: it diversifies the company away from a single AI-capex cycle. But investors who buy Qnity expecting a leveraged bet purely on AI training chips are misunderstanding the business. It is a bet on semiconductor complexity rising across the board, of which AI is the loudest but not the only driver.

Final takeaway

There is one more piece of the myth worth dismantling: the idea that a "boring chemicals company" must therefore be a slow, low-return business. The Qnity story is the opposite. Because its products are consumable, mission-critical, and qualification-locked, it earns software-like stickiness on industrial-economy assets — and because that demand scales with the complexity of chips rather than merely their volume, it has a structural growth engine bolted onto a fortress balance of competitive forces. The boring label was always a category error inherited from the conglomerate years, when these economics were averaged together with genuinely commoditized chemistry. Strip that camouflage away, and what remains looks far more like a toll road on the digital age than a cyclical chemical maker.

Qnity Electronics is the quintessential hidden champion. It does not design the dazzling AI chips that capture headlines and stock-market mania. It does something quieter and, arguably, more durable: it makes the chemical and material architecture without which those chips cannot exist — the slurries that make wafers atomically flat, the resists that let light carve transistors smaller than viruses, the films that carry signals at the speed of light, and the materials that pull the heat away before it all melts down. For two centuries this work was hidden inside other companies' balance sheets. Now, under a single-letter ticker, the shovel-maker stands alone in the daylight, selling its tools to every prospector in the greatest computing gold rush in history — indifferent to which one strikes it rich, so long as they all keep digging.

References

-

Qnity Electronics Completes Separation from DuPont, Joins S&P 500 and NYSE Under Ticker "Q" — Qnity Electronics, 2025-11-03 ↩↩↩↩↩↩↩

-

DuPont's 57.5% Plunge After Spinoff as Qnity Debuts in S&P 500 — AInvest, 2025-11-03 ↩↩↩

-

Qnity Electronics reports Q1 2026 revenue $1.315B, raises full-year guidance — TradingView/StockTitan, 2026-05-07 ↩↩↩↩↩↩

-

Qnity Electronics, Inc. to Join S&P 500 on Nov. 3 — Businesswire, 2025-10-28 ↩↩↩↩↩↩↩↩↩

-

Qnity Electronics Q1 2026 Earnings Call Transcript — Benzinga, 2026-05-07 ↩↩↩

-

Entegris Completes Acquisition of CMC Materials — Reuters / industry coverage, 2022-07-06 ↩↩

-

DuPont to acquire Laird Performance Materials for $2.3bn — PE Hub, 2021-03-08 ↩↩

-

DuPont to Acquire Laird Performance Materials from Advent International — PR Newswire, 2021-03-08 ↩↩↩

-

Rogers Announces Termination of Merger Agreement with DuPont — Rogers Corporation, 2022-11-01 ↩↩↩

-

How Chinese Antitrust Regulators are Blocking U.S. Tech Mergers — Wall Street Journal, 2023-03-22 ↩

-

CEO of Qnity Electronics (Q) receives 32,957-share stock award — StockTitan Form 4 coverage, 2026-02-27 ↩

-

Shareholders approve pay, directors and auditor at Qnity Electronics (NYSE: Q) — StockTitan, 2026-05 ↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube