PayPal: The Digital Payments Revolution

I. Introduction & Episode Roadmap

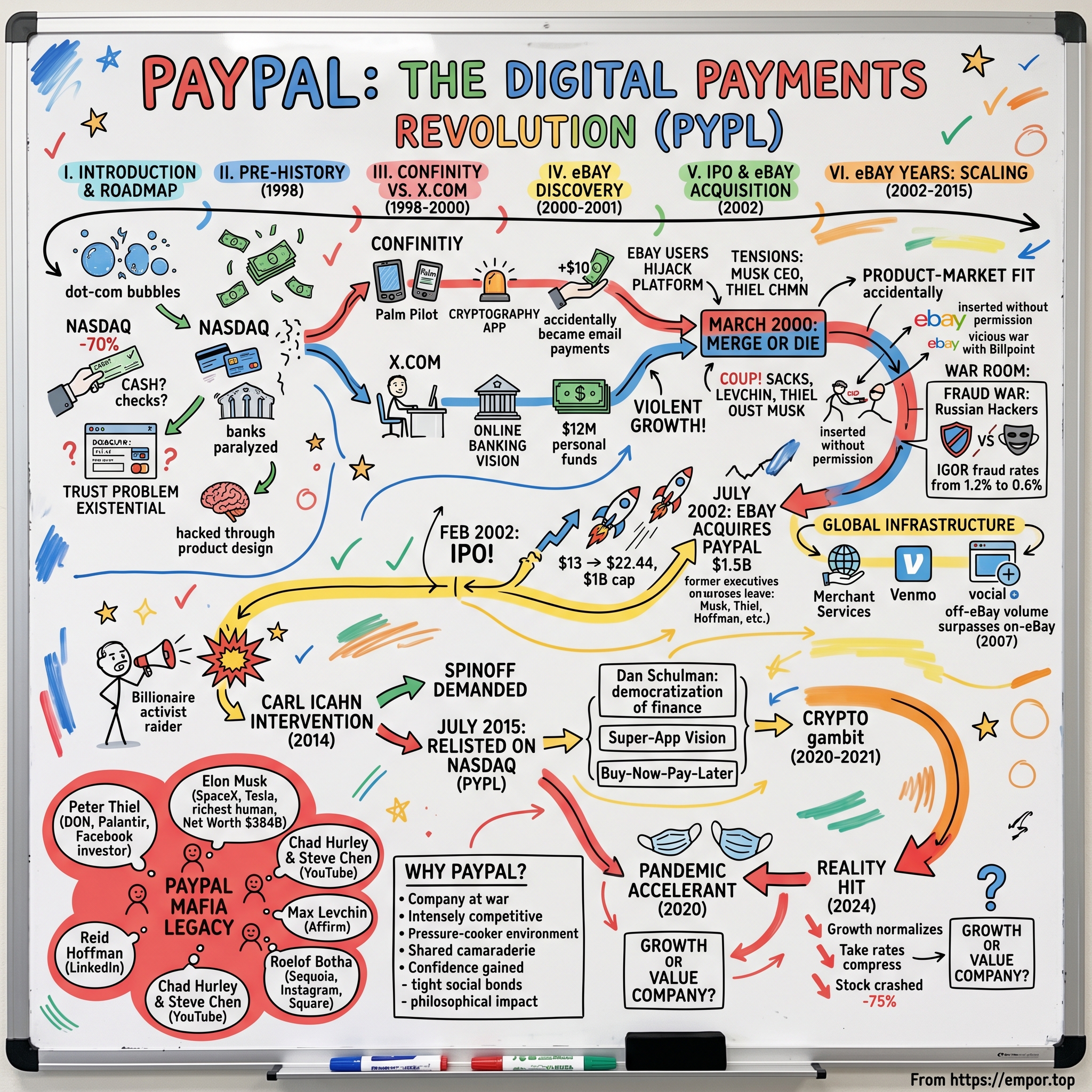

Picture this: It's February 2002, and the NASDAQ has lost 70% of its value from its dot-com peak. IPO windows are welded shut. Internet companies are radioactive. Yet in this nuclear winter, a scrappy payments startup that burns $10 million monthly and loses money on every transaction decides to go public. The bankers think they're insane. The press calls it a death march.

That company was PayPal—and within six months, it would sell for $1.5 billion to eBay, minting a generation of entrepreneurs who would reshape Silicon Valley forever.

Today, PayPal processes over $1.5 trillion in payment volume annually, serves 426 million active accounts across 200+ markets, and commands a market cap north of $70 billion. But the real story isn't the numbers—it's how a cryptography app for Palm Pilots accidentally became the financial operating system for global e-commerce, survived multiple near-death experiences, and spawned what venture capitalists reverentially call "The PayPal Mafia."

The central paradox we'll unpack: How did a company that stumbled into product-market fit, was forced to merge with its rival, got coup'd by its own board, and sold itself to avoid bankruptcy become one of the most influential companies in tech history? And perhaps more intriguingly—why did letting it go create more value than keeping it ever could have?

This is a story of accidental discoveries, brutal competition, regulatory nightmares, and the power of network effects at planetary scale. It's about how solving trust between strangers on the internet created a business moat that even Apple and Google struggle to cross. And ultimately, it's about why sometimes the best companies are built not through grand strategic planning, but through desperate adaptation to survive.

II. The Pre-History: Internet Banking's Early Days

The year is 1998. Amazon is four years old and hemorrhaging cash. Google doesn't exist yet. Broadband penetration sits at 2%. And if you want to buy something online—assuming you're brave enough to type your credit card into a website—here's what happens: You enter your 16-digit number on an unsecured form, the merchant stores it in plain text on a server running Windows NT, and you pray that neither hackers nor the merchant themselves steal your money.

The trust problem was existential. Surveys showed 70% of consumers abandoned online shopping carts because they didn't trust the payment process. The solutions were prehistoric: Some sites accepted checks by mail (yes, physical mail). Others used escrow services that took weeks. Western Union did brisk business in money orders for $20 eBay purchases.

Here's what made the problem fascinating: It wasn't technical. Cryptography existed. Secure protocols existed. The challenge was behavioral—how do you convince millions of people to trust invisible money moving through copper wires?

The banks, theoretically positioned to solve this, were paralyzed by their own success. Why cannibalize profitable credit card interchange fees? Why risk regulatory scrutiny? Why invest millions in infrastructure for a market that might not exist? Wells Fargo's early online banking required you to use Quicken software and dial in through a modem. Bank of America's first web portal looked like it was designed by accountants—because it was.

The regulatory landscape was a minefield of state money transmitter licenses, federal banking regulations, and international compliance requirements that hadn't been updated since the telegraph era. The Gramm-Leach-Bliley Act had just passed, adding new privacy requirements. State regulators couldn't even agree if email constituted "transmission" of money.

But the real insight—the one that two separate teams in Palo Alto would simultaneously discover—was that the problem wasn't about moving money at all. It was about moving trust. And trust, unlike money, could be hacked through product design, network effects, and most importantly, through solving one very specific use case that nobody else wanted to touch: person-to-person payments between strangers who would never meet.

The stage was set for one of Silicon Valley's most brutal startup battles, fought not in boardrooms but in the cramped offices of University Avenue, where two companies burning venture capital at unprecedented rates would race toward the same solution—and discover that sometimes, the only way to win is to stop fighting each other.

III. Two Companies, One Vision: Confinity vs X.com (1998-2000)

Confinity's Story: The Accidental Pivot

Max Levchin arrived in Silicon Valley in 1998 with a simple observation: Palm Pilots were everywhere, but their infrared ports were useless. His idea? Build cryptography software that would let you beam secure data between devices. He pitched it to hedge fund manager Peter Thiel at a Stanford lecture, and within weeks, they'd incorporated Confinity with Luke Nosek.

The product was elegant—hold two Palm Pilots together, beam encrypted data, complete secure transactions. The market reaction was brutal. Nobody cared. After six months of demos where Levchin literally begged people to try the product, they had dozens of users. Not thousands. Dozens.

But during one demo, someone asked: "Can you just email me the money instead?"

That question changed everything. By late 1999, Confinity had pivoted to email payments—type in an email address, enter an amount, hit send. No account numbers. No routing codes. Just email. The simplicity was radical.

The growth hack that followed became Silicon Valley legend: Give every new user $10 for signing up. Give them another $10 for each referral. Economists called it unsustainable. Levchin called it customer acquisition cost. By March 2000, they were adding 12,000 users daily—and bleeding $100,000 in bonuses every 24 hours.

X.com's Story: The Musk Machine

Three blocks away on University Avenue, Elon Musk was building something bigger. Fresh off selling Zip2 for $307 million, he poured $12 million of his own money into X.com—his vision for replacing the entire banking system. Checking accounts. Savings. Credit cards. Mortgages. Everything, online, with no physical branches.

Musk's approach was pure ambition. While Confinity was hacking growth with $10 bonuses, X.com offered no-fee, no-minimum balance accounts with interest rates that beat traditional banks. He hired engineers from the Canadian Imperial Bank of Commerce and built industrial-grade financial infrastructure from scratch.

The contrast in founders was stark. Thiel, the libertarian philosopher-lawyer who read Nietzsche between board meetings. Musk, the physicist-entrepreneur who slept under his desk and answered customer service emails at 3 AM. Levchin, the Ukrainian cryptography genius who treated fraud like a personal insult. They were about to collide.

The Merger Drama: Mutually Assured Destruction

By January 2000, both companies had discovered the same truth: eBay users were hijacking their platforms for auction payments. Neither company had planned for this—it just happened. PowerSellers started adding "PayPal accepted" or "X.com payments only" to their listings. The viral growth was intoxicating.

But the competition was murderous. Confinity and X.com were burning through $4 million monthly each, poaching each other's employees, and racing to sign up the same eBay sellers. Reid Hoffman, who knew both teams, brokered a meeting. The logic was inescapable: merge or die.

The March 2000 merger valued the combined entity at $500 million—50/50 split, with Musk as CEO and Thiel as chairman. The honeymoon lasted exactly five months. The tensions exploded in September 2000. A nascent coup began to brew when Levchin vented his frustrations to some colleagues who shared his concerns about Musk's leadership style. Things came to a head when Musk's frustrated colleagues went behind his back to pull together a study that showed PayPal's brand was more valuable than X.com's. The technical disputes were philosophical: Musk wanted to rebuild on Microsoft's Windows infrastructure for scalability; Levchin's team preferred Unix. Musk wanted to phase out the PayPal brand; everyone else knew it was their golden goose.

In September 2000, as Musk boarded a flight for a delayed honeymoon in Australia, X.com executives staged a coup. Thiel, Levchin, and David O. Sacks staged a boardroom coup, ousting him as CEO and installing Thiel. The irony was perfect: While Musk was finally taking his first vacation in two years, his own team executed a corporate assassination with surgical precision.

Musk's reaction became Silicon Valley legend. "I was pretty angry at first," Musk told biographer Walter Isaacson. "I had thoughts of assassination running through my head. But eventually I realized that it was good I got cooped". He remained the largest shareholder, kept his board seat, and watched as Thiel renamed the company PayPal—the brand Musk had tried to kill.

The coup's aftermath revealed something profound about Silicon Valley culture: Sometimes the best founders aren't the best operators. And sometimes, losing control of your company is the best thing that can happen to you. Musk would walk away with $180 million when eBay acquired PayPal, funding his next ventures. The team that ousted him would become his closest allies in the PayPal Mafia. The merger that almost destroyed both companies had accidentally created something neither could have built alone.

IV. Finding Product-Market Fit: The eBay Discovery (2000-2001)

Here's the dirty secret of PayPal's success: They never meant to become eBay's payment system. It just happened. And when it did, they almost killed it trying to pivot away.

The discovery came through customer service emails. Users weren't sending money to friends for dinner bills—they were paying strangers for Beanie Babies. By October 2000, eBay auctions drove 70% of PayPal's payment volume. The company had stumbled backwards into product-market fit.

The numbers were staggering: 10% weekly growth, compounding. At that rate, you double every two months. Triple in three. The growth was so violent that PayPal's servers crashed repeatedly. They were adding 20,000 users daily by March 2001—more than most startups see in a year.

But eBay wasn't happy. They had their own payment system, Billpoint, acquired in 1999. PayPal was a parasite on their platform, inserting itself into transactions without permission. The war that followed was vicious. eBay buried Billpoint buttons at checkout. PayPal created browser plugins that auto-inserted their logos. eBay banned PayPal links in listings. PayPal bought Google ads for "eBay payments."

The platform combat taught PayPal a crucial lesson: When you're growing 10% weekly, you can survive almost anything. Even when eBay made Billpoint free—zero fees, compared to PayPal's 2.9%—sellers stuck with PayPal. Why? Because buyers had already linked their bank accounts. The network effect had flipped: PayPal wasn't serving eBay anymore. eBay needed PayPal.

But growth without revenue is death, and PayPal was bleeding catastrophically. The fraud problem alone was existential. Russian hackers had discovered they could create fake accounts, "buy" laptops on eBay with stolen credit cards, then withdraw the money before chargebacks hit. PayPal was losing $10 million monthly to fraud alone.

Max Levchin turned PayPal's offices into a war room. Engineers slept under desks, living on Red Bull and competitive fury. They built IGOR—a fraud detection system that analyzed hundreds of signals in real-time. IP addresses, typing patterns, transaction velocities. One engineer discovered that fraudsters always rounded to even dollar amounts. Another noticed they never bought from sellers with pets in their profile photos. These tiny insights, stacked together, dropped fraud rates from 1.2% to 0.6% of payment volume. In the payments business, that 0.6% difference is the margin between death and dominance.

The burn rate, meanwhile, defied comprehension. PayPal was spending $10 million monthly on customer acquisition, another $10 million on fraud, plus operational costs. By late 2001, they had six months of runway left. The company needed to go public or die.

The IPO window had been welded shut since April 2000. No consumer internet company had gone public successfully in almost two years. PayPal would either break the streak or become the final casualty of the dot-com massacre. What happened next would determine not just PayPal's fate, but the entire trajectory of internet commerce.

V. IPO & The eBay Acquisition (2002)

On February 15, 2002, PayPal did the impossible. It became the first technology public offering in almost a year, with the stock surging 55 percent from its initial price. PayPal went public at $13 per share, giving the company a market cap of less than $1 billion, with shares shooting up over 50% in its first day of trading. Trading began at $15.41, and the stock sold for as much as $22.44 during a session in which 9 million shares changed hands.

The timing was either brilliant or insane. PayPal had accumulated $264.7 million in losses over the past three years, drew scrutiny from banking regulators and faced lawsuits that threatened to shutter the firm. Louisiana had just banned them from operating without a banking license. CertCo was suing for patent infringement, threatening an injunction that could shut down the entire business.

But the numbers told a different story. Revenue had exploded from $14.5 million in 2000 to $64.4 million in the first nine months of 2001. The company was adding 28,000 users daily at a customer acquisition cost of just $0.47. The path to profitability was clear—if they could survive long enough to reach it. Five months later, the inevitable happened. On July 8, 2002, eBay announced it would acquire PayPal for $1.5 billion in stock—0.39 shares of eBay for each PayPal share. Based on eBay's stock price on July 5, 2002, the acquisition is valued at $1.5 billion. The deal closed October 3, 2002.

The strategic logic was undeniable. Approximately 60% of PayPal's business takes place on eBay, making it the most preferred electronic payment method among eBay users. At the time of the sale, 70% of all eBay auctions accepted PayPal payments, and roughly 1 in 4 closed auction listings were transacted using the payment service. The remaining 40% of PayPal's business occurred primarily among small merchants who constituted a potential new audience for eBay.

But the real driver was fear. eBay was in talks with Wells Fargo to make their joint venture Billpoint free to all eBay auctioneers. While Billpoint had failed to gain much traction, this subsidy would have undercut PayPal in its core market. For PayPal, selling meant survival. For eBay, buying meant eliminating their most successful competitor.

The acquisition marked the end of PayPal's startup era. Peter Thiel stayed on briefly as head of the PayPal division, but the cultural mismatch was immediate. eBay's 5,000-person organization operated like a traditional corporation—process-driven, consensus-oriented, risk-averse. PayPal's 750 employees were used to shipping code daily and making decisions in hallway conversations.

Within 18 months, virtually the entire PayPal leadership team had left. Thiel departed to found Clarium Capital. Levchin started Slide. Reid Hoffman founded LinkedIn. David Sacks launched Geni. Chad Hurley and Steve Chen began plotting what would become YouTube. Elon Musk, who netted $180 million from his PayPal shares, founded SpaceX.

The diaspora wasn't bitter—it was strategic. They'd learned how to build at scale, how to fight fraud, how to create network effects. More importantly, they'd learned that sometimes the best outcome isn't staying independent—it's cashing out when the timing is perfect, then using those resources to build something even bigger. The PayPal Mafia was about to be born.

VI. The eBay Years: Scaling a Giant (2002-2015)

The first order of business was murder. eBay said it will phase out its Billpoint pay system when the PayPal acquisition becomes final. After years of bitter platform warfare, PayPal had won so decisively that eBay paid $1.5 billion to surrender. Billpoint's shutdown wasn't just a business decision—it was an admission that internal innovation couldn't compete with entrepreneurial fury.

Under eBay's ownership, PayPal transformed from scrappy startup to global infrastructure. The numbers tell the story: Revenue grew from $200 million in 2002 to $7.9 billion by 2014. Active accounts exploded from 20 million to 162 million. Total payment volume reached $228 billion annually—larger than the GDP of Portugal.

The international expansion playbook was methodical. Each new market required navigating unique regulatory mazes, banking relationships, and consumer behaviors. In Japan, they discovered users preferred bank transfers over cards. In Germany, direct debit ruled. Brazil demanded installment payments. PayPal didn't impose a one-size-fits-all solution—they localized obsessively, eventually operating in 203 markets and 100 currencies.

But the real innovation was moving beyond eBay. In 2005, PayPal launched Merchant Services, allowing any website to accept payments. This was the moment PayPal evolved from eBay's checkout system to the internet's payment layer. By 2007, off-eBay volume surpassed on-eBay for the first time. Home Depot, Barnes & Noble, and thousands of smaller merchants integrated PayPal. The company had successfully escaped its original platform dependency.

Competition emerged from every angle. Google launched Checkout in 2006 with lower fees and AdWords integration. Amazon rolled out Payments in 2007, leveraging their massive customer base. Apple introduced iTunes payments. Each tech giant saw the strategic value of owning the transaction layer. But PayPal had something they didn't: trust earned through processing billions in payments between strangers who would never meet.

The mobile revolution nearly caught them flat-footed. When the iPhone launched in 2007, PayPal's mobile experience was abysmal. The wake-up call came when Square launched in 2009, turning phones into credit card readers. PayPal scrambled to respond, eventually building native apps, one-touch checkout, and mobile SDKs. By 2012, mobile payment volume hit $14 billion—from essentially zero three years earlier.

The acquisition spree that followed reshaped PayPal's capabilities. Bill Me Later in 2008 for $945 million brought credit offerings. Zong in 2011 added carrier billing. But the masterstroke was Braintree in 2013 for $800 million. Braintree didn't just process payments—it owned the developer relationships with the next generation of commerce companies: Uber, Airbnb, GitHub. Hidden inside Braintree was an even bigger prize: Venmo.

Venmo was everything PayPal wasn't—social, mobile-first, beloved by millennials. While PayPal charged fees and felt corporate, Venmo was free and felt like texting. Users didn't "PayPal" friends for dinner; they "Venmo'd" them. The verb itself signaled a generational shift in payment behavior. By 2014, Venmo was processing $700 million quarterly, growing 100% year-over-year. But eBay's walls were closing in. It was announced on September 30, 2014, that eBay would spin off PayPal into a separate publicly traded company, a move demanded in 2013 by activist hedge fund magnate Carl Icahn. The battle had been brewing since January 2014, when Icahn revealed he owned 0.82% of eBay and launched a public campaign for separation.

VII. The Icahn Intervention & Spinoff (2013-2015)

Carl Icahn is at it again. The billionaire corporate raider turned activist investor wants eBay to spin off its PayPal unit, the giant online marketplace disclosed on Wednesday. The January 2014 announcement sent shockwaves through Silicon Valley. Icahn didn't just want a spinoff—he wanted blood.

His argument was devastatingly simple: "I think the multiple would go up dramatically, and the health of the company would be better." "There's no reason they should be together at this point, in our opinion," Icahn said. The numbers backed him up. In 2013, revenue at eBay's payments division, which includes PayPal, increased by 19%, while the company's marketplaces-division revenue increased by 12% and its enterprise-division revenue increased by 3%. In 2013, PayPal, which now has 143 million users worldwide, handled a whopping $180 billion worth of payments.

eBay's initial resistance was fierce. CEO John Donahoe argued that "PayPal and eBay make sense together for many reasons." Among them: "eBay accelerates PayPal's success," "eBay data makes PayPal smarter," and "eBay funds PayPal's growth." The board rallied behind management, with Pierre Omidyar tweeting that they were "fully aligned" on keeping the companies together.

But Icahn wasn't fighting alone. The deeper issue was that PayPal's potential partners—Amazon, Alibaba, other major retailers—were reluctant to work with a payment system owned by a competitor. PayPal's ties to the online retailer were impeding close relationships with huge platforms like Amazon and slowing its adoption of new technology. Even departed co-founder Elon Musk weighed in, warning that if PayPal didn't act quickly it would be "screwed."

The war escalated through 2014. Icahn accused board members of conflicts of interest, called eBay "the worst-run company" he'd ever seen, and threatened a proxy fight. In April, he briefly backed down, accepting a board seat compromise. But the damage was done. The strategic review that followed revealed an uncomfortable truth.

John Donahoe, eBay's chief executive, told Reuters that the decision was based on the feeling that "the pace of change in this competitive environment … is accelerating and will continue to over the next three to five years." Translation: Apple Pay had just launched. Square was going public. Stripe was eating their lunch with developers. The payments world was evolving faster than a corporate subsidiary could adapt.

On September 30, 2014, eBay capitulated. "However, a thorough strategic review with our board shows that keeping eBay and PayPal together beyond 2015 clearly becomes less advantageous to each business strategically and competitively," the company announced. The industry landscape had changed, and each business faced different competitive opportunities and challenges.

The spin-off was completed on July 18, 2015. On July 20, the company was relisted on Nasdaq under the same ticker symbol it used shortly before it was acquired by eBay, PYPL. The market's verdict was instant and brutal: Within months, PayPal's market cap exceeded eBay's. The child had outgrown the parent.

Dan Schulman, a veteran of American Express and Virgin Mobile, took the helm as CEO of the independent PayPal. His mandate was clear: transform PayPal from a checkout button into a financial operating system. The Icahn intervention hadn't just freed PayPal—it had forced a reckoning with what the company could become when it stopped being eBay's cash cow and started being its own destiny.

VIII. Independence & The Platform Wars (2015-Present)

Freedom came with a price tag: survival. Dan Schulman inherited a $45 billion company that was simultaneously dominant and vulnerable. PayPal processed $282 billion in payment volume annually, but Apple Pay had launched nine months earlier. Square was weeks from going public. Stripe was signing up every hot startup. The payment wars had begun, and PayPal's thirteen-year head start was evaporating.

Schulman's strategy was counterintuitive: Instead of defending the core business, he would attack everywhere else. "We need to democratize financial services," he declared, unveiling a vision that went far beyond payments. Mobile-first. Social commerce. Cryptocurrency. Buy-now-pay-later. PayPal would become a super-app for money—or die trying.

The Venmo phenomenon became PayPal's secret weapon. What started as a quirky peer-to-peer app had evolved into a social network where twenty-somethings publicly performed their financial lives. By 2017, Venmo was processing $35 billion annually, growing 80% year-over-year. More importantly, it owned an entire generation's payment behavior. You didn't "pay" your roommate for utilities—you "Venmo'd" them. The verb itself was worth billions.

But monetizing Venmo proved treacherous. Users loved it because it was free. Adding fees risked killing the golden goose. PayPal's solution was elegant: instant transfers for a fee, debit cards with cashback, and most cleverly, business profiles that let merchants accept Venmo. By 2021, Venmo was generating $850 million in revenue—still a fraction of its potential, but proof that free services could eventually print money.

The Buy Now, Pay Later gold rush showcased PayPal's newfound agility. When Afterpay and Klarna started eating into e-commerce checkout, PayPal didn't acquire—they built. "Pay in 4" launched in 2020, offering interest-free installments. Within 18 months, it had 7 million users and $3.5 billion in volume. The speed from concept to scale would have been impossible under eBay's bureaucracy. The cryptocurrency gambit of 2020-2021 exemplified PayPal's new risk appetite. PayPal Holdings, Inc. (NASDAQ: PYPL) today announced the launch of a new service enabling its customers to buy, hold and sell cryptocurrency directly from their PayPal account, and signaled its plans to significantly increase cryptocurrency's utility by making it available as a funding source for purchases at its 26 million merchants worldwide. The service launched with Bitcoin, Ethereum, Bitcoin Cash and Litecoin.

The timing was perfect. Bitcoin was surging toward all-time highs, institutional adoption was accelerating, and PayPal needed a narrative beyond traditional payments. The size of the waiting list for access to crypto, which is now available to 10% of PayPal customers, was two or three times as great as what the company anticipated. By early 2021, PayPal customers were able to use their cryptocurrency holdings as a funding source to pay at PayPal's 26 million merchants around the globe. Consumers were able to instantly convert their selected cryptocurrency balance to fiat currency, with certainty of value and no incremental fees.

But competition was everywhere and nowhere simultaneously. Apple Pay leveraged the iPhone's ubiquity but couldn't crack e-commerce. Square built beautiful hardware but struggled internationally. Stripe owned developers but had no consumer brand. Amazon Pay had infinite resources but merchants feared feeding the beast. Each competitor was formidable in isolation, limited in scope.

The pandemic became PayPal's unexpected accelerant. Digital payment volume exploded 40% in 2020 as lockdowns forced even technophobes online. Total payment volume surged past $900 billion. Revenue hit $21.5 billion. The stock price tripled. For a brief moment in 2021, PayPal's market cap touched $360 billion—larger than Bank of America.

Then reality hit. Growth rates normalized. Competition intensified. The stock crashed 75% from its peak. Buy-now-pay-later competitors like Affirm and Klarna ate into margins. Apple's tap-to-pay threatened Venmo. Crypto prices collapsed, taking PayPal's narrative with them.

By 2024, PayPal faced an existential question: Was it a growth company trading at value multiples, or a value company with growth aspirations? The answer would determine whether PayPal's independence was its greatest achievement—or its biggest mistake.

IX. The PayPal Mafia Legacy

The PayPal Mafia is a group of former PayPal employees and founders who have since founded and/or developed additional technology companies based in Silicon Valley, such as LinkedIn, Palantir Technologies, SpaceX, Affirm, Slide, Kiva, YouTube, Yelp, and Yammer. The term itself sounds like mythology, but the reality exceeds the legend.

Start with the numbers: PayPal alumni have founded or co-founded companies worth over $1 trillion combined. Seven became billionaires. Dozens more became hundred-millionaires. They've funded thousands of startups. They've reshaped industries from space travel to social media. No other company—not even Google or Facebook—has produced a diaspora this influential.

The roster reads like a Silicon Valley hall of fame. Peter Thiel, PayPal founder and former CEO who is sometimes referred to as the "don" of the PayPal Mafia. He serves as Chairman of the Palantir board, was a founder of Founders Fund, and was the first outside investor in Facebook. His $500,000 Facebook investment returned $1 billion. Elon Musk, co-founder of Zip2, and founder of X.com (which merged with Confinity to form PayPal), SpaceX, OpenAI, Neuralink, and The Boring Company. He bought a controlling share in Tesla Motors and purchased Twitter (rebranded as X). He is the wealthiest person on Earth, with a net worth of $384 billion.

Reid Hoffman founded LinkedIn, sold it to Microsoft for $26 billion, and became Silicon Valley's super-connector. Chad Hurley, former PayPal web designer who co-founded YouTube, which sold to Google for $1.65 billion. Jawed Karim, former PayPal engineer who co-founded YouTube, posted the first YouTube video, then returned to academia. Max Levchin, founder and chief technology officer at PayPal. Current CEO of Affirm, which went public at a $10 billion valuation.

David Sacks turned a $25 million Yammer into a $1.2 billion Microsoft acquisition. Keith Rabois, former executive at PayPal who later worked at LinkedIn, Square, Khosla Ventures, and Founders Fund, became the operator venture capitalists call when companies need fixing. Jeremy Stoppelman co-founded Yelp. Russel Simmons co-founded Yelp with him. Steve Chen co-founded YouTube. Roelof Botha became Sequoia Capital's managing partner, backing Instagram, WhatsApp, Square, and Stripe.

But why PayPal? Why not Amazon or eBay or Yahoo alumni? The answer lies in what PayPal was: a company at war. An intensely competitive environment and a shared struggle to keep the company solvent despite many setbacks also contributed to a strong and lasting camaraderie among former employees.

The PayPal environment was Darwinian. Fraud attacks came daily. Competition was existential. Regulators threatened shutdown. The burn rate demanded perfection. You either performed or perished. This pressure-cooker created a specific type of entrepreneur: paranoid, aggressive, technically brilliant, and completely comfortable with chaos.

According to Lacy, the selection process and technical learning at PayPal played a role, but the main factor behind their future success was the confidence they gained there. They'd survived the impossible—taking on banks, beating eBay at its own game, going public in a depression. After PayPal, every other startup challenge seemed manageable.

The network effect amplified everything. PayPal's founders encouraged tight social bonds among its employees, and many of them continued to trust and support one another after leaving PayPal. When Hoffman needed funding for LinkedIn, Thiel wrote a check. When Chen and Hurley started YouTube, Botha at Sequoia backed them. When Levchin launched Slide, everybody invested. The Mafia didn't just share capital—they shared intelligence, talent, and deal flow.

The philosophical impact may be deepest. PayPal proved that small teams could destroy industries. That regulation was a puzzle to solve, not a barrier to respect. That moving fast and breaking things wasn't just acceptable—it was mandatory. Every successful Silicon Valley company since has internalized these lessons.

After the 2024 United States presidential election, The Economist wrote that the PayPal Mafia would "take over America's government" with the reelection of Donald Trump. Thiel protégé JD Vance became Trump's Vice President, Musk became head of the new Department of Government Efficiency (DOGE), and Sacks became Trump's advisor on AI and cryptocurrencies.

The PayPal Mafia's legacy isn't just the companies they built or the wealth they created. It's the proof that a single company, at the right moment, with the right people, can alter the trajectory of an entire industry—and that sometimes, the best thing a successful company can do is die young and scatter its seeds to the wind.

X. Playbook: Business & Investing Lessons

Network Effects in Payments: The Winner-Take-Most Reality

PayPal's moat isn't technology—it's behavioral lock-in at planetary scale. Once consumers link bank accounts and merchants integrate payment flows, switching costs become prohibitive. The lesson: In payments, being first matters less than being embedded. PayPal wasn't the first online payment system, but it was the first to achieve two-sided network density. Every new user makes the network more valuable for merchants; every new merchant makes it more valuable for users. This recursive loop, once established, becomes nearly impossible to break.

The key insight for investors: Look for the tipping point where convenience overwhelms competition. PayPal hit this around 30 million users. Below that threshold, competitors can poach users with promotions. Above it, the network becomes self-reinforcing. The corollary: Payment networks without both sides—consumer-only apps or merchant-only processors—are fundamentally vulnerable.

Solving Fraud at Scale: The Hidden Competency

Every PayPal competitor learns the same brutal lesson: Fraud scales faster than revenue. PayPal's true innovation wasn't moving money—it was learning to lose less of it. Their fraud detection systems, built through years of hand-to-hand combat with Russian hackers and Nigerian princes, became an insurmountable competitive advantage.

The investor takeaway: In financial services, risk management IS the business model. Companies that treat fraud as a cost center rather than a core competency will inevitably fail or sell. PayPal survived because Levchin treated fraud like a personal enemy. That organizational obsession with security created capabilities competitors couldn't buy or build quickly.

Platform Dependency: Dancing with Giants

PayPal's eBay relationship exemplifies the platform paradox: Your biggest customer can become your biggest threat. 70% concentration with eBay gave PayPal scale but also existential risk. The lesson isn't to avoid platform dependency—it's to use it as a launching pad, not a destination.

Smart companies follow PayPal's playbook: Dominate a platform niche, use that cashflow to diversify, then achieve escape velocity before the platform realizes you're a threat. The timing is crucial. Leave too early and you lack scale. Leave too late and you get crushed or acquired. PayPal's 2002 exit to eBay was perfectly timed—they maximized value while competitive threats loomed.

When to Sell vs. Stay Independent

PayPal's $1.5 billion sale looks cheap in hindsight, but it was the right decision at the right time. They were burning cash, facing regulatory threats, and competing against an angry platform partner with infinite leverage. Selling to eBay removed existential risk and gave the team capital to build bigger things.

The framework for founders: Sell when you have leverage, not when you need to. PayPal sold from a position of relative strength (post-IPO, growing rapidly) rather than weakness. This maximized price and terms. The mistake most founders make is waiting until they have no choice, then accepting whatever's offered.

Building in Regulatory Grey Zones

PayPal operated for years in regulatory limbo—not quite a bank, not quite not a bank. Rather than waiting for permission, they built first and negotiated later. This "ask forgiveness, not permission" approach became Silicon Valley orthodoxy, but PayPal shows both its power and peril.

The key was moving fast enough to become systemically important before regulators could shut them down. By the time states started requiring money transmitter licenses, PayPal had millions of users who would complain to politicians if the service disappeared. Regulatory capture through consumer dependency—a playbook Uber, Airbnb, and every crypto company would later copy.

The Power of Diaspora Networks

PayPal's greatest return on investment wasn't its eBay acquisition price—it was the network effects of its alumni. The PayPal Mafia didn't just start companies; they funded each other, hired each other, and shared intelligence. This created compound returns that no single company could have achieved.

For investors, the lesson is to track talent clusters, not just companies. When a successful company breaks apart, follow where the pieces land. The next generation of unicorns often emerges from the previous generation's alumni. For founders, it means your early employees aren't just building your company—they're your future co-investors, advisors, and partners. Hire accordingly.

The meta-lesson from PayPal's playbook: The best businesses are built on paradoxes. Global scale with local network effects. Move fast but build trust. Compete fiercely but know when to sell. Break rules but become indispensable. These contradictions aren't bugs—they're features of transformational companies.

XI. Analysis & Bear vs. Bull Case

Bull Case: The Incumbent's Advantage

PayPal's bulls see a misunderstood giant trading at distressed valuations. Start with the fundamentals: 426 million active accounts processing $1.5 trillion in total payment volume annually. That's not a business—it's economic infrastructure. The company generates $7+ billion in free cash flow annually, trades at 15x P/E, and returns massive capital through buybacks. In any other industry, these metrics would signal a screaming buy.

The two-sided network moat remains formidable. Consumers have linked bank accounts, saved payment methods, and established years of transaction history. Merchants have integrated APIs, trained customer service teams, and built PayPal into their checkout flows. This embedded infrastructure creates switching costs measured not in dollars but in organizational trauma.

Venmo's dominance among millennials and Gen-Z represents optionality worth tens of billions. With 90 million users and growing, Venmo owns the social graph of money for an entire generation. As these users age into peak earning years, their payment relationships become increasingly valuable. The monetization has barely begun—business profiles, credit products, and investment services could transform Venmo from a cost center into PayPal's growth engine.

International expansion remains nascent. While PayPal operates in 200+ markets, penetration outside the U.S. remains shallow. Cross-border payment volume is growing 20%+ annually. As global e-commerce accelerates and emerging markets digitize, PayPal's existing infrastructure positions it to capture disproportionate value. The company doesn't need to win everywhere—just maintaining share in a growing pie drives substantial returns.

The financial services expansion opportunity dwarfs the current business. PayPal Credit, savings accounts, bill pay, cryptocurrency, stock trading—each vertical represents billions in potential revenue. Unlike startups attacking these markets individually, PayPal can cross-sell to 400+ million users with near-zero customer acquisition cost. The transformation from payment processor to financial super-app is plausible, valuable, and already underway.

Bear Case: Death by a Thousand Cuts

PayPal's bears see a melting ice cube masquerading as a growth stock. The core business faces existential threats from every direction, and the company's responses feel desperate rather than strategic.

Big Tech competition is suffocating. Apple Pay's tap-to-pay elegance makes PayPal feel antiquated. Google Pay leverages Android's 3 billion users. Amazon Pay converts one-click shoppers. Meta's WhatsApp Pay threatens international remittances. Each tech giant has more resources, better data, and stronger ecosystem lock-in. PayPal is fighting platform wars with checkout buttons.

Take rates are compressing everywhere. Competition has driven payment processing toward commodity pricing. PayPal's average take rate has declined from 2.9% to 2.4% over five years. Cryptocurrencies promise near-zero transaction costs. Real-time payment networks eliminate intermediaries entirely. PayPal's margin structure assumes premium pricing that markets no longer support.

The innovation deficit is glaring. While PayPal acquired Venmo, competitors built Cash App. While PayPal partnered with Paxos for crypto, Coinbase built native infrastructure. While PayPal added buy-now-pay-later, Affirm and Klarna defined the category. PayPal consistently arrives late to trends it should be setting. The company spends $6 billion annually on technology and development but produces incremental features, not breakthrough products.

Regulatory challenges are mounting globally. Europe's PSD2 directive forces open banking that commoditizes payment processing. U.S. regulators scrutinize buy-now-pay-later products. Cryptocurrency regulations remain uncertain. Data privacy laws restrict PayPal's ability to monetize transaction information. The regulatory environment is becoming more hostile, not less.

The Venmo monetization struggle exemplifies broader challenges. Despite 90 million users, Venmo barely breaks even. Users revolt at fees. Competition from Cash App and Zelle limits pricing power. The "social" aspect that makes Venmo valuable also makes monetization toxic—nobody wants to pay fees for splitting dinner bills with friends.

The Verdict: Transitional Reality

The truth lies between extremes. PayPal isn't dying, but it's not thriving either. It's a profitable, cash-generative business facing structural headwinds in a rapidly evolving industry. The company's response—trying to become everything to everyone—feels more reactive than strategic.

The bull case requires successful execution across multiple fronts simultaneously: Venmo monetization, international expansion, financial services cross-sell, and maintaining share against Big Tech. Possible, but improbable.

The bear case requires complete disruption: crypto eliminating intermediaries, Big Tech achieving payment ubiquity, or real-time networks obsoleting processors. Also possible, but not imminent.

The most likely scenario is gradual decline in relevance but not revenues. PayPal becomes the IBM of payments—profitable, persistent, but no longer pivotal. The stock will trade like a value trap: cheap for a reason, occasional rallies on quarterly beats, but structurally capped upside.

For investors, PayPal represents a fascinating study in lifecycle dynamics. It's too established to fail quickly, too challenged to grow dramatically, too profitable to ignore, and too threatened to love. The investment case depends entirely on time horizon and risk tolerance. Short-term traders can play volatility. Value investors can clip dividends and buybacks. Growth investors should look elsewhere.

The strategic lesson is more sobering: Even dominant network effects businesses face eventual commoditization. PayPal built one of the strongest moats in technology, but moats don't matter when the entire landscape shifts beneath you.

XII. Epilogue & "If We Were CEOs"

If we inherited Dan Schulman's office tomorrow, the strategic prescription would be radical simplification through decisive choices. PayPal's current strategy of being marginally competitive in everything guarantees excellence in nothing.

First decision: Choose between consumer and merchant. PayPal tries serving both masters equally, resulting in a compromised product that fully satisfies neither. The optimal strategy would be to become the merchant's champion—the Shopify of payments. Let Apple and Google own consumer wallets. PayPal should own the complexity of accepting those wallets. Build the infrastructure layer that makes every payment method work everywhere. The margin structure is better, the competition is less intense, and the technical moat is deeper.

Second decision: Divest Venmo or go all-in. The current middle ground—Venmo as a subscale social network with payment features—destroys value. Either sell Venmo to a company that can properly monetize social graphs (Meta, Twitter/X), or transform it into a full neobank for Gen-Z. Half-measures guarantee Cash App and Zelle will continue gaining share while Venmo burns cash pursuing conflicting objectives.

Third decision: Abandon the super-app fantasy. PayPal will never out-execute Ant Financial in China or beat Apple in the U.S. Instead, become the payment infrastructure that enables everyone else's super-app dreams. Build the APIs, not the apps. Own the rails, not the retail experience. This isn't retreat—it's focus.

The cryptocurrency strategy needs complete overhaul. PayPal's current approach—high fees on retail crypto trading—is precisely wrong. The opportunity isn't competing with Coinbase for speculation revenues. It's building the bridge between traditional finance and digital assets. Become the trusted custodian for institutional crypto transactions. Enable central bank digital currencies. Build the compliance layer that lets banks touch crypto without fear.

On capital allocation: Stop the scatter-shot M&A. PayPal has spent $15+ billion on acquisitions with minimal return. Instead, execute a massive tender offer at current depressed valuations. Buying back 30% of shares outstanding would signal confidence, boost EPS, and concentrate ownership among believers. Use remaining capital for strategic partnerships, not acquisitions. PayPal doesn't need to own everything—it needs to connect everything.

The organizational transformation would be equally dramatic. PayPal has 30,000 employees generating $25 billion in revenue—less than $1 million per employee. Stripe generates similar metrics with 8,000 people. The bloat isn't just expensive—it's strategically crippling. A 40% workforce reduction focused on eliminating middle management would be painful but necessary. Redeploy savings into engineering talent and developer relations.

Finally, embrace the inevitable unbundling. PayPal succeeded by bundling payment methods, currencies, and use cases into one checkout button. But bundling only works when switching costs exceed convenience gains. Today's consumers want native experiences, not universal ones. The strategic response isn't fighting unbundling—it's orchestrating it. Become the protocol layer that lets thousand payment methods bloom while capturing value from the underlying infrastructure.

The hardest decision would be cultural: Accepting that PayPal's heroic age is over. The company that fought eBay, survived the dot-com crash, and created the PayPal Mafia no longer exists. Trying to recapture that entrepreneurial energy within a 30,000-person bureaucracy is futile. Better to acknowledge reality and optimize for what PayPal has become: critical financial infrastructure that should be boring, reliable, and profitable.

The future of payments won't be winner-take-all. It will be a complex ecosystem of specialized providers, each excellent at specific use cases. PayPal's opportunity isn't to dominate that ecosystem—it's to enable it. The company that started by helping strangers trust each other on eBay could end by helping every payment provider trust each other in an interconnected financial future.

This isn't a story of decline—it's a story of evolution. PayPal changed commerce forever. The question now isn't whether PayPal remains relevant, but how it chooses to exercise the relevance it's earned. The answer will determine whether PayPal's next chapter is gradual obsolescence or graceful transformation into something the founders never imagined: the boring, profitable, indispensable plumbing of global digital commerce.

XIII. Recent News

PayPal Holdings, Inc. (NASDAQ: PYPL) announced its fourth quarter and full year 2024 results for the period ended December 31, 2024. The company has shown significant momentum under CEO Alex Chriss's leadership, with shares up 39% in 2024, according to data provided by S&P Global Market Intelligence, compared to just a 23.3% return for the S&P 500—marking PayPal's first outperformance of the broader market in three years.

The turnaround story is gaining traction. In 2024, PayPal is forecasting free cash flow of $6 billion, exceeding the previous high watermark of $5.4 billion achieved in 2021. PayPal expects 2024 adjusted profit to increase by "mid-to-high single-digit percentage", compared with its earlier forecast of it remaining flat. This dramatic improvement in profitability comes despite modest top-line growth, reflecting successful operational improvements.

Key product initiatives are showing early success. Monthly active accounts for the Venmo debit card grew more than 30% in 2024, and Pay with Venmo monthly actives increased more than 20%. The company's PayPal Everywhere initiative, launched in September 2024, offers 5% cash back for using a PayPal debit card within the mobile app, driving engagement and transaction frequency.

Strategic partnerships are expanding PayPal's reach. PayPal has partnered with Amazon to bring its checkout option to SMBs that offer Buy with Prime. The company will expand on this in 2025, giving Prime members a chance to link their Amazon and PayPal accounts. This represents a significant breakthrough in merchant acceptance and could drive material volume growth.

Looking ahead to 2025, PayPal is making substantive changes to its user agreements. Effective July 16, 2025: The PayPal user agreement is being updated to further clarify the differences between PayPal business accounts and PayPal personal accounts. We are also clarifying the actions PayPal may take if the activity associated with your account is not consistent with your account type.

The investment community remains cautiously optimistic. PayPal stock trades at a downright cheap valuation at 12 times its free cash flow. With a cheap valuation and a rapidly dropping share count, PayPal stock could have more upside in 2025. Analysts note that while the turnaround will take time, early indicators suggest new leadership's initiatives are delivering improving results.

XIV. Links & References

Key Books and Resources

- "The PayPal Wars" by Eric M. Jackson - Insider account of PayPal's early battles

- "Zero to One" by Peter Thiel - PayPal co-founder's philosophy on building monopolies

- "The Founders" by Jimmy Soni - Comprehensive history of PayPal's founding team

- "Elon Musk" by Walter Isaacson - Details the X.com merger and Musk's ouster

Regulatory Filings and Investor Materials

- PayPal Investor Relations: https://investor.pypl.com

- SEC Edgar Database - PayPal Holdings (PYPL): All 10-K, 10-Q, and 8-K filings

- Original S-1 Registration Statement (2002): Details of initial public offering

- eBay-PayPal Merger Documents (2002): Transaction terms and strategic rationale

- Spinoff Registration Statement (2015): Separation agreement and financial details

Related Analysis and Commentary

- Stratechery - Ben Thompson's analysis of payment platform dynamics

- a16z Fintech Newsletter - Insights on payment innovation

- The Information - Enterprise reporting on PayPal strategy

- Acquired Podcast episodes on PayPal, Visa, and Square for payment industry context

The PayPal story continues to evolve, but its place in technology history is secure. From a Palm Pilot app that nobody wanted to a $70+ billion financial infrastructure company, PayPal proved that solving trust between strangers could create one of the internet's most enduring businesses. Whether its next chapter brings renewed growth or gradual decline, PayPal's legacy—the companies it spawned, the entrepreneurs it trained, the commerce it enabled—has already changed the world. The question now isn't whether PayPal mattered, but what its successors will build on the foundation it created.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube