PVH Corp: From Shirtmakers to Global Fashion Power — The Calvin Klein & Tommy Hilfiger Story

I. Introduction & Episode Roadmap

Picture this: it is March 2010, and the global economy is still nursing wounds from the worst financial crisis in eighty years. Credit markets remain skittish. Department stores are closing locations by the dozen. And a company best known for making dress shirts — a firm most consumers had never heard of, called Phillips-Van Heusen — announces it is paying three billion dollars to buy Tommy Hilfiger, one of the most recognizable fashion brands on the planet.

Wall Street responded with a mix of admiration and bewilderment. A shirt manufacturer buying a global lifestyle brand? With that kind of leverage, in that kind of market? The deal looked audacious, even reckless. But it was only the latest chapter in one of the most improbable corporate metamorphoses in American business history.

Today, that company operates as PVH Corp, the parent of both Calvin Klein and Tommy Hilfiger. Together, those two brands generated over ninety percent of PVH's roughly $8.7 billion in fiscal 2024 revenue. The company employs approximately 28,000 people, operates in more than forty countries, and draws over seventy percent of its revenue from international markets. It is, by any measure, a global fashion conglomerate.

But rewind 145 years and the story begins in the anthracite coal country of eastern Pennsylvania, with immigrant hands sewing shirts and selling them off pushcarts. The central question of this episode is a simple one, yet the answer spans nearly a century and a half of American enterprise: How did immigrants sewing shirts for coal miners build a company that would buy two of the world's most iconic fashion brands?

This is a story about brand equity versus manufacturing muscle, about the strategic courage to repeatedly bet the company on acquisitions, and about the brutal economics of staying relevant in an industry where taste is fickle and loyalty is fleeting. It is the ultimate case study in radical business model transformation — from factory floor to brand platform, from Pennsylvania pushcarts to Parisian runways.

The narrative arc is sweeping: origins in the Gilded Age, a collar innovation that changed how American men dressed, decades of acquisitive diversification, two company-defining mega-deals, a painful but deliberate pruning of the portfolio, and a modern digital transformation plan that is still playing out in real time. Along the way, we will meet the key architects — the founders, the dealmakers, the turnaround operators — and pressure-test whether this company's competitive position is as strong as its brand names suggest.

Here is the essential tension at the heart of PVH's story: the company has spent 145 years evolving, shedding old identities and acquiring new ones, always moving up the value chain from manufacturing to branding. But the fashion industry does not reward history. It rewards relevance. And relevance, in an era of Shein, TikTok, and algorithmic trend cycles, is harder to maintain than ever before.

PVH's stock price — down nearly forty percent over the past year, even as the company beats earnings guidance — suggests that the market has deep questions about the durability of this story. Whether those doubts are warranted is what this deep dive aims to explore.

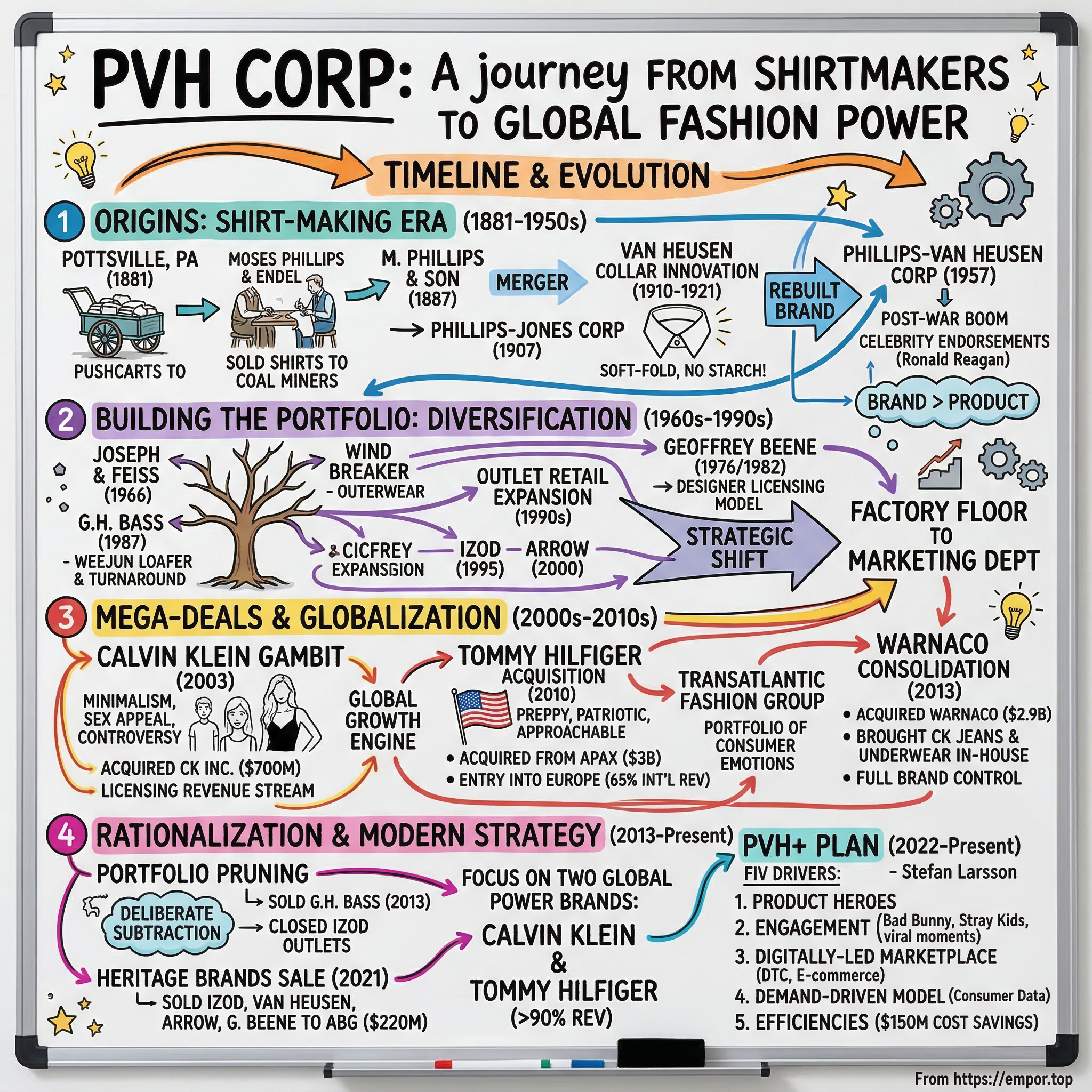

II. Origins & The Shirt-Making Era (1881–1950s)

In 1881, in the gritty coal mining town of Pottsville, Pennsylvania, a man named Moses Phillips and his wife Endel began hand-sewing shirts in their home. Their customers were anthracite coal miners — men who descended into the earth each day and needed sturdy, affordable clothing. The Phillips family sold these shirts from pushcarts, working the streets of Pottsville and surrounding mining communities. It was unglamorous work, rooted in the most basic commercial instinct: make something useful, sell it to people who need it.

Pottsville in the 1880s was the epicenter of Pennsylvania's anthracite coal industry — a rough, industrializing corner of America where immigrant families poured in from Eastern Europe seeking opportunity. The Phillips family were part of that wave. The coal miners they served were not fashion-conscious; they needed work shirts that could withstand the grime and physical demands of the mines. But Moses Phillips had an instinct for commerce that transcended the immediate transaction. He understood that even the most utilitarian product could be improved, marketed, and scaled.

The business grew slowly and steadily. By 1887, it had formalized as M. Phillips & Son, and the family relocated operations to New York City, where the garment trade was centralizing. The Phillips family placed one of the earliest shirt advertisements in the Saturday Evening Post, a move that reflected an emerging understanding that even commodity products could benefit from marketing.

In 1907, M. Phillips & Sons merged with D. Jones & Sons — the latter founded by Dramin Jones, who had died in 1903 — to form Phillips-Jones Corporation. The company was now a meaningful player in the American shirt business, but it was still fundamentally a manufacturing operation.

Then came the innovation that would define the company for the next half century. John Manning Van Heusen, a Dutch immigrant and textile engineer, invented a process in 1910 to fuse cloth on a curve. To understand why this mattered, you have to understand the state of men's fashion at the time. In the early twentieth century, men's dress shirts came with stiff, detachable collars — uncomfortable, high-maintenance contraptions that had to be starched, attached separately, and replaced frequently. They were a daily nuisance for millions of American office workers.

Phillips-Jones saw the commercial potential immediately. The company secured a patent for a self-folding collar in 1919 and released the product to the public in 1921 under the Van Heusen name. By 1929, the company introduced the first collar-attached shirt — a product so obviously superior that it rendered the old detachable collar obsolete within a decade.

By the 1930s, the soft-fold collar had become the industry standard. Van Heusen had not just improved a product; it had changed how American men dressed.

The partnership between the Phillips family and John Van Heusen proved so successful that it became the company's identity. In 1957, Phillips-Jones Corporation officially renamed itself Phillips-Van Heusen Corporation, honoring the brand that had become its crown jewel. This was more than a cosmetic change. It signaled that the company understood its future lay not just in manufacturing shirts, but in the power of a trusted brand name.

Through the post-World War II boom, Van Heusen rode the wave of American prosperity. As the white-collar workforce expanded and suburban life demanded a new kind of professional wardrobe, the Van Heusen brand became synonymous with affordable, comfortable dress shirts. The company built a manufacturing base, established distribution relationships with department stores across the country, and invested in advertising that positioned Van Heusen as the choice of the modern American businessman.

Van Heusen's advertising was notably ahead of its time. The brand enlisted celebrity endorsements — Ronald Reagan, before his political career, appeared in Van Heusen ads — and invested in the Saturday Evening Post and other mass-market publications to build national name recognition.

The company understood, decades before the concept was formalized in business literature, that a brand is a promise: a shortcut that allows consumers to make purchasing decisions without evaluating every product from scratch. When a man walked into a department store and reached for a Van Heusen shirt, he was not just buying fabric and buttons. He was buying trust — the assurance that this shirt would fit well, look professional, and hold up after repeated washings.

That simple insight — that the brand promise could be more valuable than the physical product — would eventually drive PVH's entire strategic evolution.

It was a solid, profitable business — but it was still, at its core, a shirt company. The transformation into something far more ambitious was still decades away. What mattered was that the seed had been planted: the recognition that a brand could be more valuable than the product it was stamped on.

III. Building the Portfolio: Acquisitions & Diversification (1960s–1990s)

By the 1960s, Phillips-Van Heusen had mastered the dress shirt business, but the company's leadership recognized a fundamental problem: shirts alone were a narrow, cyclical market. If you only make one thing, you are hostage to a single product cycle, a single consumer mood, a single retail channel. The solution was diversification — and PVH pursued it with the enthusiasm of a conglomerate-builder in the go-go years of American capitalism.

The first major move came in 1966, when PVH acquired Joseph & Feiss Co. of Cleveland, entering the tailored-clothing business for the first time. The idea was straightforward: if you were already selling shirts to department stores, why not sell suits and sport coats too? The same buyer, the same rack, the same consumer. Around the same time, the company moved into outerwear through Wind Breaker Inc., further broadening the product offering. These were sensible, adjacent-market acquisitions — nothing revolutionary, but each one expanded the company's footprint in the menswear ecosystem.

The real strategic evolution came in 1982, when PVH launched a Geoffrey Beene shirt line. The Joseph & Feiss operation had already added a Geoffrey Beene division under license in 1976, but this formalized the company's entry into designer licensing — a business model that would eventually become PVH's entire raison d'être.

The concept was elegant: rather than building your own designer brand from scratch (an enormously expensive and risky proposition), you license a famous name and apply it to products you already know how to make. You pay the designer a royalty; they lend you their cachet. The consumer gets an affordable designer product; the manufacturer gets higher margins than a commodity shirt would ever command.

PVH would not fully acquire the Geoffrey Beene brand outright until 2018, but the licensing relationship planted a crucial strategic idea.

In 1987, PVH made a splashier bet, acquiring G.H. Bass & Co. — the iconic New England footwear brand famous for the Weejun loafer, a preppy staple since the 1930s. Bass was struggling when PVH bought it, but the company turned the brand around by liquidating obsolete inventory, upgrading the product line, narrowing the size range, raising prices, and boosting advertising. It was a textbook brand turnaround — and it taught PVH leadership something valuable about the power of repositioning a faded brand.

The company also made a prescient bet on retail distribution. By the early 1990s, PVH was operating over six hundred outlet stores across the United States. The outlet mall revolution was transforming American retail, and PVH rode the wave hard.

According to company accounts, the outlet business was the key to PVH's financial turnaround in the early 1990s, generating cash flow that kept the company healthy during a difficult period for the broader apparel industry. Outlet stores offered a way to move excess inventory, reach price-sensitive consumers, and build brand awareness — all while generating healthy margins on products that would otherwise be marked down at department stores.

The acquisition pace continued: Izod in 1995, Arrow in 2000. Each addition brought another recognizable brand name under the PVH umbrella. Izod, in particular, was an interesting acquisition. The brand had been a 1980s preppy icon — the Izod Lacoste polo shirt, with its distinctive alligator logo, was as much a symbol of Reagan-era country club culture as the polo shirt bearing Ralph Lauren's name. By the time PVH acquired it, Izod had separated from Lacoste and was a mid-tier sportswear brand, but it still carried meaningful consumer recognition and provided PVH with another entry point into the casual apparel market. Arrow, meanwhile, was one of America's oldest dress shirt brands, further consolidating PVH's dominance in the category that had built the company.

But step back and the pattern is clear. Through the 1980s and 1990s, PVH was quietly shifting its identity. It was no longer just a manufacturer that happened to own some brands. It was becoming a brand management company that happened to manufacture some products. The strategic center of gravity was migrating from the factory floor to the marketing department.

There is an important lesson here for investors who study corporate transformation. PVH did not execute one dramatic pivot. Instead, it evolved through a series of incremental moves — each acquisition, each licensing deal, each retail experiment — that collectively changed the company's DNA. The Joseph & Feiss deal taught PVH about adjacent categories. The Geoffrey Beene license taught it about the economics of designer branding. The G.H. Bass turnaround taught it about brand repositioning. The outlet expansion taught it about direct retail economics. And each lesson laid the groundwork for the breathtaking bet that would come next.

IV. The Calvin Klein Gambit: A Company-Defining Bet (2003)

To understand what happened in 2003, you have to understand what Calvin Klein meant to American culture. Calvin Klein was not just a fashion label. It was a cultural phenomenon — a brand that had defined American minimalism, redefined sex appeal in advertising, and generated more controversy per square inch of billboard than perhaps any other name in fashion history. From the notorious Brooke Shields jeans ads of the early 1980s ("You want to know what comes between me and my Calvins? Nothing.") to the iconic Mark Wahlberg underwear campaigns of the 1990s, Calvin Klein had turned provocation into profit and minimalism into mainstream desire.

But by the early 2000s, the brand was in a complicated position. Calvin Klein the man — the Bronx-born designer who had co-founded the company with his childhood friend Barry K. Schwartz in 1968 — was looking to step away. Klein was in his sixties, and the business, while still culturally powerful, lacked the scale and operational infrastructure to compete with the emerging global luxury conglomerates.

The brand's most lucrative product categories — underwear, jeans, sportswear — were licensed to the Warnaco Group, meaning Calvin Klein Inc. collected royalties but did not control the products that generated the most consumer demand. It was a brand with enormous equity and limited operational leverage.

Enter Phillips-Van Heusen. In 2003, the shirt company outbid VF Corporation (the maker of Lee and Wrangler jeans) and acquired Calvin Klein Inc. for approximately $430 million in cash, with additional payouts of up to $270 million in subsequent years, bringing the total deal value to roughly $700 million. Calvin Klein and Schwartz each pocketed approximately $215 million in cash and stock. Klein stepped down as chief designer and became a consulting creative director. Schwartz departed to pursue his passion for horse racing, serving as chairman of the New York Racing Association.

The financing was creative by necessity. Apax Partners, a private equity firm, provided a $250 million equity investment in PVH convertible preferred stock, along with a $125 million two-year secured note. Apax received board seats in return. It was a leveraged bet by a mid-sized apparel company on one of the most storied names in fashion — and the industry took notice.

Why was this radical? Because Phillips-Van Heusen was, to the outside world, a dress shirt company. The idea that a firm known for Van Heusen and Izod could credibly own Calvin Klein seemed almost absurd. It was like a regional fast-food chain acquiring a Michelin-starred restaurant.

But PVH's leadership, led by CEO Bruce Klatsky and his protégé Emanuel Chirico (who would soon take the helm), saw something that the skeptics missed. They recognized that brand equity was the real asset — not the factory floor, not the distribution network, not the manufacturing know-how. Calvin Klein's name, its cultural resonance, its aspirational positioning — those were worth far more than the physical operations that produced the clothes.

The acquisition transformed PVH's business model overnight. Instead of relying on the modest margins of commodity dress shirts, the company now had a platform to collect licensing royalties from a globally recognized brand. Calvin Klein's licensing network generated revenue from fragrances, eyewear, watches, home goods, and dozens of other categories — all without PVH having to invest capital in manufacturing those products. The economics were compelling: licensing is essentially a royalty stream with minimal capital requirements and high margins.

The integration was not without challenges. PVH had to learn how to manage a fashion brand with global ambitions, navigate complex licensing relationships, and maintain the creative integrity that made Calvin Klein valuable in the first place.

Managing a creative brand is fundamentally different from running a shirt factory. The talent is different — designers, creative directors, and marketing executives who think in terms of cultural moments rather than production schedules. The decision-making cadence is different — fashion moves in seasons, and a misjudged collection can take years to recover from. And the economics are different — brand licensing generates high margins but requires constant investment in marketing and creative talent to maintain the brand's cultural temperature.

But the strategic logic proved sound. Calvin Klein became PVH's growth engine, re-platforming the entire company toward higher-margin designer licensing and away from the commodity shirt business that had been its foundation for over a century. The timing also proved fortunate: the early 2000s were the beginning of the global luxury boom, driven by rising wealth in emerging markets and the democratization of fashion through media and the internet. Calvin Klein, with its universal aesthetic of sexy minimalism, was perfectly positioned to ride that wave.

Emanuel Chirico, who had served as PVH's CFO since 1999, was elevated to CEO in 2006, three years after the Calvin Klein acquisition. A Fordham University graduate who had spent fourteen years as a partner at Ernst & Young specializing in the apparel industry before joining PVH in 1992, Chirico was the quintessential financially disciplined operator. He understood both the numbers and the industry, and he would go on to architect the next two transformative deals. Under his leadership, the Calvin Klein acquisition was not an endpoint but a proof of concept — demonstrating that PVH could successfully acquire and operate a premium fashion brand. The question was: could the company do it again, at even larger scale?

For investors, the 2003 deal was the true inflection point — the moment PVH stopped being a shirt company and started becoming a brand platform. Every major move that followed was a consequence of this fundamental strategic insight.

V. Going Global: The Tommy Hilfiger Acquisition (2010)

On March 15, 2010, PVH announced it was acquiring Tommy Hilfiger for approximately three billion dollars — €2.2 billion, to be precise, consisting of €1.924 billion in cash, €276 million in PVH common stock, and the assumption of roughly €100 million in liabilities. The seller was Apax Partners, the same private equity firm that had helped finance the Calvin Klein deal seven years earlier. Apax had taken Tommy Hilfiger private in 2006 and reportedly earned a 4.5x return on its investment — a spectacular outcome that validated both the brand's enduring value and PVH's willingness to pay up for premier assets.

The timing was both bold and contrarian. The financial crisis had hammered the apparel industry, and many retailers were still in survival mode. Credit was expensive and scarce.

The financing package that PVH assembled reflected the difficulty of the moment: approximately $385 million in cash on hand, $2.45 billion of senior secured debt (including an undrawn $450 million revolver), $600 million of senior unsecured notes, and $200 million in perpetual convertible preferred stock, plus a planned common stock offering of approximately $200 million. It was an aggressive capital structure by any measure — the kind of deal that works brilliantly if the brand performs and disastrously if it does not.

The strategic rationale was compelling on several dimensions. Tommy Hilfiger was one of the world's leading premium lifestyle brands, with particular strength in Europe — a market where PVH had virtually no presence. At the time of the acquisition, Tommy Hilfiger drew approximately sixty-five percent of its revenue from outside the United States, compared to PVH, which generated roughly ninety percent domestically.

The deal instantly transformed PVH from an American dress shirt company into a transatlantic fashion group. Fred Gehring, who had built Tommy Hilfiger's European business into a powerhouse, continued as CEO of the brand — a signal that PVH intended to preserve the brand's distinct identity and management culture rather than impose a one-size-fits-all corporate overlay.

The contrast between the two brands was itself an asset. Calvin Klein was minimalist, provocative, urban, and aspirational — think black and white photography, chiseled models, and spare geometric lines. Tommy Hilfiger was preppy, patriotic, colorful, and approachable — think red, white, and blue logos, varsity jackets, and a celebration of classic American leisure.

Where Calvin Klein leaned into controversy, Tommy embraced Americana. Calvin Klein targeted the fashion-forward consumer who wanted to project sophistication; Tommy Hilfiger appealed to the consumer who wanted to project casual confidence.

Owning both gave PVH a diversified portfolio of consumer emotions — covering different demographics, different price points, different occasions. The risk of owning two brands in the same segment was real (brand cannibalization is a perpetual worry in the fashion industry), but the aesthetic and cultural gap between Calvin Klein and Tommy Hilfiger was wide enough to make the pairing work.

There is a useful analogy here to the luxury conglomerates that PVH admires. LVMH owns both Louis Vuitton and Dior — two brands that compete in some categories but serve different consumer identities. Kering owns both Gucci and Saint Laurent. The principle is the same: a portfolio of brands with distinct DNA, managed independently but supported by shared back-office infrastructure. PVH was building a similar model, just at a different price tier.

The integration was not without friction. In the same year as the acquisition, PVH pulled the Van Heusen brand out of all European markets due to losses — a tacit admission that the heritage brand could not compete on the same continent where Tommy Hilfiger and Calvin Klein had genuine consumer pull. The decision to retreat with Van Heusen while investing billions in Tommy Hilfiger revealed the strategic hierarchy within PVH: the designer brands were the future; the heritage brands were legacy.

In 2011, the company made the symbolism official by renaming itself from Phillips-Van Heusen Corporation to PVH Corp. The three-letter ticker was more than a rebranding exercise. It was a declaration that the company had transcended its shirt-making origins. PVH Corp was now a multi-brand, multi-geography fashion conglomerate — and it was about to get bigger. The combined entity was projected to generate over $4.8 billion in revenue and $755 million of EBITDA on a full-year pro forma basis, numbers that would have seemed fantastical to the Phillips family sewing shirts in Pottsville just a few generations earlier.

VI. Consolidation Play: The Warnaco Acquisition (2013)

If the Calvin Klein deal in 2003 was the strategic turning point and the Tommy Hilfiger deal in 2010 was the globalization leap, then the Warnaco acquisition in 2013 was the consolidation play that completed the puzzle. And it revolved around a specific, nagging problem: PVH owned the Calvin Klein brand, but it did not control the products most consumers actually associated with Calvin Klein.

When PVH bought Calvin Klein Inc. a decade earlier, the brand's most visible and profitable product categories — underwear, jeans, and sportswear — were licensed to the Warnaco Group, a publicly traded company that manufactured and sold those products under the Calvin Klein name. This meant that PVH collected licensing royalties from Warnaco but had limited control over product design, pricing, distribution, and marketing for the categories where Calvin Klein mattered most.

It was, to use a real estate analogy, like owning the building but leasing out the penthouse.

In February 2013, PVH completed the acquisition of Warnaco for approximately $2.9 billion. Warnaco shareholders received $51.75 in cash and approximately 0.18 of a share of PVH common stock per share held.

The deal brought Calvin Klein's jeans and underwear businesses — the brand's two biggest profit centers — under PVH's direct control for the first time. It also added direct operations in Asia and Latin America, markets where Warnaco had built significant Calvin Klein businesses. As a bonus, PVH picked up the Warner's and Olga intimate apparel brands, as well as the North American license for Speedo swimwear.

The strategic significance was profound. Full ownership of Calvin Klein's denim and underwear lines meant PVH could now control every aspect of the brand experience — from design to pricing to the store experience to the advertising campaign. In fashion, brand coherence matters enormously. A single off-brand product in the wrong channel can dilute years of carefully curated positioning. By consolidating ownership, PVH eliminated the risk that a licensee's short-term profit motive might conflict with the brand's long-term health.

The deal also gave PVH the scale to be taken seriously as a global player. The combined company expected to generate approximately $100 million in annual run-rate synergies, fully realized over three years, with one-time integration costs of roughly $175 million. Pro forma revenue for the combined entity approached $8 billion — a number that would have been inconceivable for a dress shirt company just a decade earlier.

To understand why the Warnaco deal mattered so much, consider the licensing dynamic it eliminated. When Warnaco manufactured Calvin Klein underwear as a licensee, its incentives were not perfectly aligned with the brand's long-term health. Warnaco wanted to maximize unit sales and minimize costs — which sometimes meant putting Calvin Klein products in lower-end retail channels, using cheaper materials, or over-distributing the brand in ways that diluted its premium positioning.

PVH, as the brand owner, wanted to protect Calvin Klein's aspirational image — which sometimes meant restricting distribution, investing in higher-quality materials, and accepting lower volumes in exchange for higher perceived value.

This tension between licensee economics and brand health is endemic to the fashion industry, and it is one of the primary reasons that luxury companies tend to bring production in-house. The Warnaco acquisition resolved this tension for Calvin Klein's most important categories.

The combined company's size also warranted inclusion in the most tracked equity index in the world: PVH was added to the S&P 500 on June 29, 2018, replacing Big Lots. (The company would later be removed from the index in March 2023, a reflection of its declining market capitalization — a sobering reminder that index inclusion is a lagging indicator of success, not a guarantee of permanence.) For investors, the Warnaco deal closed the loop on a decade-long strategy. PVH had gone from licensing Calvin Klein's name to owning the brand, to finally controlling the products that made the brand valuable. The company was now a vertically integrated brand platform with global reach — and the next question was whether the heritage brands that had funded this transformation still had a role to play.

VII. Portfolio Rationalization: Betting Everything on Two Brands (2013–2023)

The decade following the Warnaco acquisition was defined by subtraction, not addition. Having assembled a sprawling portfolio of brands through fifty years of acquisitive growth, PVH's leadership made the deliberate — and risky — decision to strip the company down to its two most valuable assets: Calvin Klein and Tommy Hilfiger. Everything else had to go.

The pruning began almost immediately. In October 2013, PVH sold G.H. Bass & Co. to G-III Apparel Group for approximately $50 million in cash — a modest sum for a brand that had been a turnaround success story in the 1990s but no longer fit the company's elevated ambitions. Then, in January 2015, PVH announced it would close all 120 Izod retail outlets, citing an increasingly competitive outlet retail environment driven by more premium brands. The Izod wholesale business continued, but the writing was on the wall.

The COVID-19 pandemic, which devastated physical retail in 2020, actually accelerated the rationalization. PVH permanently closed 162 Heritage Brands outlet stores by mid-2021, cutting approximately 450 jobs. The pandemic exposed a truth that had been building for years: the heritage brands were capital sinks, consuming management attention and retail real estate that could be better deployed against Calvin Klein and Tommy Hilfiger. COVID did not cause the divestiture strategy — it was already underway — but it compressed the timeline and made the decision easier.

The most decisive move came in June 2021, when PVH announced the sale of its entire Heritage Brands business — Izod, Van Heusen, Arrow, and Geoffrey Beene — to Authentic Brands Group for approximately $220 million in cash. The transaction was completed in August 2021. Think about that for a moment: PVH sold the Van Heusen brand, the very name that had defined the company for over sixty years, the innovation that had changed how American men dressed. It was the corporate equivalent of selling your childhood home — painful, perhaps, but necessary if you've outgrown it and need the capital for a different life.

There is a myth versus reality dynamic worth addressing here. The consensus narrative is that PVH "gave away" its heritage brands too cheaply — $220 million for four recognizable American brand names seems like a fire sale. The reality is more nuanced. These brands were generating declining revenue, operating at thin margins, and requiring significant capital to maintain their retail footprint. Authentic Brands Group, which specializes in acquiring faded brands and licensing them aggressively, was arguably a better owner for these assets than PVH, which needed to focus its limited management bandwidth on its two marquee labels. The $220 million was not a valuation of what the brands were worth in their prime; it was a valuation of what they were worth to a company that no longer wanted to operate them. Sometimes the best deal is the one that lets you walk away.

The Heritage Brands sale was a clarifying act. In a single stroke, PVH eliminated the managerial distraction, the capital allocation tension, and the brand positioning confusion that came with operating mid-market labels alongside two global premium brands. As management put it at the time, "This transaction is an important next step to build our core brands, Calvin Klein and Tommy Hilfiger, into the most desirable lifestyle brands in the world."

The rationalization continued in 2023, when PVH sold the Warner's, Olga, and True&Co intimate apparel businesses to Basic Resources for an all-cash purchase price of $160 million, subject to adjustments, plus an additional earnout of up to $10 million based on 2024 net sales. These were brands that had come to PVH through the Warnaco acquisition and were perfectly respectable businesses, but they did not fit the streamlined, two-brand strategy.

The result was radical concentration. By 2024, Calvin Klein and Tommy Hilfiger together generated over ninety percent of PVH's revenue. The company had no fallback, no hedge, no diversified portfolio to cushion a brand-specific downturn.

This was a high-conviction bet that two brands, managed with focus and scale, would outperform a collection of five or ten brands managed with divided attention. In the fashion industry, where brand heat can cool without warning and consumer preferences shift with dizzying speed, this level of concentration is either brilliant discipline or dangerous hubris.

The answer depends entirely on execution — and on forces, like macroeconomic cycles and geopolitical shocks, that no management team can fully control.

For investors, the key question is whether the premium that focused management brings to Calvin Klein and Tommy Hilfiger outweighs the diversification benefit of having other brands to lean on when one of the two stumbles. History suggests that focused brand companies — think Hermès, think Nike in its most disciplined eras — tend to outperform conglomerates in fashion. But the comparison only holds if your brands have genuine, durable demand. That is the bet PVH has made.

VIII. The PVH+ Plan: Digital Transformation & Modern Strategy (2022–Present)

In February 2021, PVH installed a new CEO: Stefan Larsson, a Swedish executive with a resume tailor-made for the challenges ahead. Larsson had spent nearly fifteen years at H&M, rising to Head of Global Sales with responsibility for approximately 2,300 stores and nearly $17 billion in annual revenue. He then served as Global President of Old Navy at Gap Inc., where he delivered twelve consecutive quarters of profitable growth and positioned the brand among millennials' top preferences. In 2015, he became CEO of Ralph Lauren, where he focused on refocusing the brand around its iconic core positioning before departing in 2017. He joined PVH as President in 2019 and succeeded the long-tenured Emanuel Chirico — the dealmaking architect who had engineered the Calvin Klein, Tommy Hilfiger, and Warnaco acquisitions — as CEO in 2021.

Larsson's background was significant because it combined two things PVH desperately needed: deep experience in fast-fashion operational discipline (H&M is a masterclass in supply chain efficiency) and an understanding of how to elevate and protect a premium brand's positioning (his Ralph Lauren tenure, however brief, demonstrated that sensibility). Chirico had been the dealmaker who assembled the portfolio. Larsson was the operator tasked with making the portfolio perform.

In April 2022, Larsson unveiled the PVH+ Plan, a multi-year strategic growth framework built around five growth drivers.

The first driver, "Win with Product," focused on developing hero products across key growth categories where Calvin Klein and Tommy Hilfiger resonate most with consumers — think Calvin Klein underwear, Tommy Hilfiger polos, and signature denim.

The second driver, "Win with Consumer Engagement," emphasized digital-first, 360-degree marketing campaigns built around brand moments and cultural partnerships.

The third, "Win in the Digitally-Led Marketplace," aimed to accelerate direct-to-consumer and e-commerce growth while rationalizing wholesale partnerships.

The fourth driver, "Develop a Demand- and Data-Driven Operating Model," sought to build a product creation engine that puts consumer data at the center of design and assortment decisions.

And the fifth, "Drive Efficiencies and Invest in Growth," targeted cost savings to be reinvested in the first four drivers.

The marketing execution under Larsson has produced some notable wins. Calvin Klein's partnership with Bad Bunny for the Icon Cotton Stretch launch generated viral cultural moments and genuine consumer excitement — the kind of earned media that no advertising budget can buy. The campaign was not just a celebrity endorsement; it was a carefully orchestrated cultural event that leveraged Bad Bunny's massive Latin American and global fanbase to position Calvin Klein's core underwear product as both aspirational and accessible. The campaign drove a measurable spike in search interest and social media engagement, demonstrating that cultural relevance — not just advertising spend — drives brand heat in the modern fashion landscape.

Tommy Hilfiger leaned into equally unexpected collaborations, partnering with the F1 movie and K-Pop group Stray Kids to reach younger, global audiences. The Stray Kids partnership was particularly strategic: K-Pop's global reach, especially in Asia-Pacific markets where PVH sees significant growth potential, made it a perfect vehicle for introducing Tommy Hilfiger to a generation of consumers who might not have natural affinity with the brand's traditional American preppy DNA. These campaigns reflected a deliberate strategy to keep both brands culturally relevant with Gen Z and millennial consumers, demographics that will drive fashion spending for the next two decades.

The fourth growth driver — the demand- and data-driven operating model — deserves particular attention because it represents the most technically ambitious element of the PVH+ Plan.

In plain terms, what PVH is trying to build is a system where consumer data — what people are searching for, what they are buying, what they are returning, what is trending on social media — feeds directly into product design and inventory decisions. Instead of designing a collection months in advance based on a designer's intuition and then hoping consumers buy it, PVH wants to design collections that are informed by actual consumer demand signals.

This is not a trivial undertaking. It requires integrating data systems across retail, e-commerce, wholesale, and social media; building analytical capabilities that translate raw data into actionable design insights; and changing the organizational culture from one where creative instinct leads to one where data and creativity work in concert.

H&M and Zara have been leaders in data-driven fashion for years — Larsson's H&M background gives him credibility in this domain — but building these capabilities at PVH, across two brands and dozens of markets, is a multi-year effort with uncertain outcomes.

One of the most consequential elements of the PVH+ Plan is the decision to bring previously licensed product categories back in-house, particularly women's apparel. Between 2025 and 2027, PVH plans to transition core women's product categories from licensed operations to owned-and-operated wholesale. The logic is the same as the Warnaco rationale: control the product, control the brand experience, capture more of the economics. But it comes with execution risk and near-term disruption, as licensing revenue declines before wholesale revenue from the same categories ramps up.

On the digital front, PVH reported that over a third of its total revenues were generated through digital channels as of 2022, and the company set an ambitious target to triple European e-commerce. Direct-to-consumer channels, encompassing owned stores and e-commerce, represent approximately forty percent of total revenue, with wholesale accounting for the remaining sixty percent.

For a company that built its business on wholesale relationships with department stores, this shift toward DTC is both strategically necessary and culturally transformative. It requires different skills — different technology, different talent, different metrics — and it changes the economic model fundamentally by trading wholesale margins for retail margins (higher per unit, but with higher fixed costs).

The question for investors is whether the PVH+ Plan represents genuine strategic transformation or merely the latest iteration of management buzzwords. The early returns are mixed but encouraging: revenue has come in above guidance in multiple quarters, gross margins hit record levels in 2024, and brand heat indicators suggest that Calvin Klein and Tommy Hilfiger remain culturally relevant. But the real test will play out over the next several years, as PVH navigates tariff headwinds, geopolitical tensions, and the relentless competitive pressure of an industry that punishes complacency with terrifying speed.

IX. Operational Realities: Challenges & Restructuring (2024–2025)

The glossy brand campaigns and strategic frameworks tell one story. The income statement tells another — one that is more complicated and, for investors, more important.

Fiscal year 2024 (ending February 2025) delivered revenue of approximately $8.65 billion, a decline of roughly six percent from the prior year. Net income fell to approximately $598 million, down nearly ten percent.

The headline numbers masked some genuine operational achievements — record gross margins, driven by a favorable shift in channel mix and lower product costs, and EBIT margins that remained in double-digit territory on a non-GAAP basis. But the top-line shrinkage reflected deliberate choices (exiting unprofitable channels, rationalizing wholesale accounts) as well as headwinds beyond management's control.

The fifth growth driver of the PVH+ Plan — "Drive Efficiencies and Invest in Growth" — became the story of 2025. PVH embarked on significant restructuring actions aimed at simplifying its operating model by centralizing processes and eliminating redundancies. The company incurred approximately $80 million in restructuring costs, with a target of achieving $150 million in annual cost savings by 2026.

These are the unsexy but necessary operational improvements — consolidating regional offices, streamlining supply chain management, reducing headcount — that free up capital for brand investment. The tradeoff is painful in the short term: restructuring charges hit reported earnings, employee morale suffers, and organizational disruption can slow decision-making just when speed matters most.

The first quarter of fiscal 2025 delivered a particularly jarring surprise: approximately $480 million in pre-tax noncash goodwill impairment charges. This included $426 million to fully write off goodwill in the Americas and Asia-Pacific segments, plus $53.5 million in impairment on reacquired license rights in Australia.

The impairments were triggered primarily by a significant increase in discount rates — a technical accounting adjustment driven by rising interest rates and country risk premiums. In plain English, the future cash flows that PVH expected from these regions became less valuable in present-dollar terms, forcing a write-down.

It is worth noting that goodwill impairments are noncash charges — they do not affect the company's actual cash flow or operations — but they do signal that the price PVH paid for past acquisitions may have been optimistic relative to current conditions. This is an important accounting judgment that investors should flag: goodwill sitting on a balance sheet represents management's belief that future cash flows will justify the premium paid in past acquisitions. When that belief is revised downward, it serves as a reality check on the original deal economics.

Two external shocks compounded the challenges. First, tariffs: the escalating U.S. trade war imposed an estimated $65 million drag on EBIT in fiscal 2025, translating to roughly $1.05 per share in negative earnings impact. PVH sources from approximately thirty-seven countries, with about sixty percent of suppliers in Asia, twenty percent in Europe, and fifteen percent in North America. The diversified supply chain provides some buffer, but tariffs on Chinese goods hit margins directly and necessitated pricing adjustments that risked alienating cost-conscious consumers.

Second, and more troublingly, China's Ministry of Commerce placed PVH on its "Unreliable Entities List" in February 2025, alleging that the company had improperly boycotted cotton sourced from the Xinjiang region. To understand why this matters, some context is necessary. The Xinjiang cotton controversy sits at the intersection of global human rights concerns and Chinese domestic politics. Western governments and human rights organizations have alleged that cotton production in China's Xinjiang region involves forced labor of Uyghur minorities. In response, the United States passed the Uyghur Forced Labor Prevention Act in 2021, which effectively barred imports of goods made with Xinjiang cotton. Many Western brands, including PVH, adjusted their supply chains accordingly. China views these actions as politically motivated attacks on its internal affairs and has retaliated against companies it perceives as participating in the boycott.

PVH's placement on the Unreliable Entities List was a geopolitical flashpoint with real commercial consequences: potential monetary fines, restrictions on imports and exports related to China, and constraints on investment in the Chinese market. Asia-Pacific revenue declined thirteen percent in the first quarter following the designation. For a company that had invested heavily in building its Asia-Pacific business — and counted on the region as a key growth driver — the Chinese government's action represented a significant and largely uncontrollable risk factor. It is worth flagging this as a material legal and regulatory overhang: the outcome of the investigation remains uncertain, and the range of potential consequences — from a symbolic slap on the wrist to meaningful commercial restrictions — is wide. Investors should monitor this situation closely, as it could materially affect PVH's Asia-Pacific growth trajectory.

Calvin Klein's operating margin compressed to approximately fourteen percent in 2024, down from eighteen percent in 2021 — a meaningful decline that reflected both the challenging macro environment and the costs of the brand repositioning effort. For context, a fourteen percent operating margin is respectable by apparel industry standards — Gap Inc. and Hanesbrands typically operate at lower margins — but it falls well short of the twenty-plus percent margins that true luxury brands command. The four-point compression over three years raises a legitimate question: is PVH investing heavily in brand elevation and accepting temporarily lower margins as the cost of long-term brand building, or is the margin decline a structural reflection of the brands' competitive position?

Management argues the former — that the elevated marketing spend and product investment required by the PVH+ Plan will eventually translate into higher margins as the brands' pricing power increases. Skeptics argue the latter — that Calvin Klein and Tommy Hilfiger simply do not have the pricing power to sustain luxury-like margins, and that the gap between investment and returns may never close. The truth is likely somewhere in between, but the margin trajectory over the next two to three years will be a crucial tell.

The balancing act between investing in brand heat (marketing, product innovation, talent) and delivering near-term profitability is the central operational tension at PVH today. Spend too little, and the brands lose relevance. Spend too much, and margins erode. There is no formula for getting this balance right — only judgment, and the market's verdict on that judgment is delivered quarterly. What makes PVH's position particularly challenging is that it is attempting this balancing act while simultaneously absorbing tariff costs, managing geopolitical risk in China, executing a major restructuring, and bringing licensed categories in-house. Any one of these would be a full-time management challenge; executing all of them simultaneously requires exceptional organizational bandwidth.

X. The Business Model Deep Dive

PVH's business model rests on three revenue pillars: wholesale, direct-to-consumer, and licensing. Understanding the economics of each is essential to understanding the investment case.

Wholesale remains the largest channel, accounting for approximately sixty percent of total revenue. PVH sells Calvin Klein and Tommy Hilfiger products to department stores, specialty retailers, and off-price chains worldwide.

The advantage of wholesale is reach and volume: department stores provide access to millions of consumers without the capital cost of operating your own stores. The disadvantage is control. When Macy's or Kohl's puts your product on a clearance rack, your brand takes the hit.

And wholesale partners have enormous bargaining power — they decide how much shelf space you get, how prominently your products are displayed, and how deeply they are discounted. The structural decline of the American department store has added a secular headwind to this channel, though European wholesale, particularly in the premium and specialty segments, has proven more resilient.

Direct-to-consumer — encompassing owned retail stores and e-commerce — accounts for approximately forty percent of revenue and is the fastest-growing channel. PVH operates over 1,200 retail stores globally, including full-price stores, outlet stores, and concession shops within department stores.

The DTC channel offers higher margins per unit, full control over the brand experience, and access to first-party consumer data that informs product development and marketing decisions. The tradeoff is higher fixed costs: every store you operate comes with rent, staff, inventory, and overhead.

Digital commerce represented over a third of total revenue as of 2022, and the company invested approximately $200 million in capital expenditures in 2025, directed largely toward IT infrastructure and distribution capabilities to support the digital business.

Licensing is the third pillar and, in many ways, the most elegant. To understand licensing economics, think of it as renting out your brand name. PVH licenses the Calvin Klein and Tommy Hilfiger trademarks to third-party manufacturers across categories like fragrances, eyewear, watches, jewelry, and home goods. In exchange, PVH receives royalties — typically a percentage of the licensee's net sales — with minimal capital investment. PVH does not have to build a fragrance factory, hire perfumers, or manage eyewear distribution. It simply collects a check for allowing someone else to use its brand name. The margins on licensing revenue are extraordinarily high — essentially pure profit minus the cost of brand management and quality oversight — which is why licensing has historically been a profit center that far exceeds its share of total revenue.

Calvin Klein's fragrance license, held by Coty, is a prime example. Calvin Klein fragrances generate billions in retail sales globally, and PVH collects a royalty stream on every bottle sold. PVH did not invest in developing those fragrances, building the supply chain, or managing retail distribution. It simply owns the name. This is the purest expression of brand equity as an economic asset.

Licensing revenue has been declining recently, in part because PVH is deliberately bringing previously licensed categories (particularly women's apparel) back in-house. This is a strategic choice to sacrifice near-term licensing income for the higher-margin, higher-control economics of owned operations. The transition is messy in the short term — licensing revenue drops immediately when a license is not renewed, while the replacement wholesale revenue takes time to ramp up — but the long-term logic mirrors the Warnaco rationale: own the product, control the brand. The risk is execution: bringing a category in-house requires building or acquiring the design, sourcing, and distribution capabilities that the licensee previously provided.

The geographic mix is heavily international. Over seventy percent of PVH's revenue comes from outside the United States, with Europe — particularly the Tommy Hilfiger business — as the largest international market. This global footprint provides diversification benefits but also exposes PVH to currency fluctuations, geopolitical risks (as the China situation illustrates), and regulatory complexity across dozens of jurisdictions.

On the cost side, PVH's supply chain spans thirty-seven countries, with over sixty-two percent of manufacturing done in facilities with fewer than five hundred workers. Marketing expenditures totaled approximately $456 million in fiscal 2022, representing about 5.7 percent of total revenue — a meaningful investment that reflects the centrality of brand building to PVH's strategy.

Manufacturing and sourcing costs were approximately $1.8 billion in the same year. The company's gross margin — the spread between revenue and the cost of making and sourcing its products — reached record levels in 2024, driven by better channel mix and lower input costs.

But gross margins in the high-fifties (the fourth quarter of 2024 came in at 58.2 percent) are healthy by apparel standards, though well below the seventy-plus percent margins commanded by true luxury houses like Hermès or LVMH's fashion division.

That gap tells you something important about where PVH sits in the market hierarchy: premium, not luxury. Accessible, not exclusive. The economics reflect the positioning.

XI. Competitive Landscape & Market Position

PVH operates in one of the most crowded, competitive industries on earth. To understand the company's position, it helps to think about the apparel market as a series of concentric rings.

At the center are the luxury conglomerates — LVMH, Kering, Hermès — companies with staggering pricing power, massive margins, and brand equity measured in centuries, not decades. LVMH alone generated over €86 billion in revenue in 2024. PVH does not compete directly with these players on product, but it competes for the same consumer's wallet and the same cultural mindshare. When a consumer splurges on a Louis Vuitton bag, that might be the dollar that would otherwise have gone to a Calvin Klein jacket.

In the accessible luxury and premium lifestyle ring, PVH's direct competitors are companies like Ralph Lauren (market capitalization of approximately $20 billion as of early 2026, roughly six times PVH's $3.2 billion), Tapestry (the Coach parent, at approximately $31 billion), and Hugo Boss (approximately $3 billion, similar in size to PVH). The comparison with Ralph Lauren is particularly instructive: Ralph Lauren has a single dominant brand with enormous equity, higher average prices, and a more clearly defined luxury positioning. PVH has two brands with broader accessibility but less pricing power. Ralph Lauren's market cap premium reflects the market's assessment that one strong luxury-adjacent brand may be worth more than two strong premium brands.

Further out, PVH competes with mid-market players like Gap Inc. (approximately $10 billion market cap) and Hanesbrands (approximately $2.3 billion) in various product segments. The fast-fashion ring — dominated by Inditex (Zara's parent, with a staggering $201 billion market cap and nearly €40 billion in revenue) and H&M (approximately $21 billion in revenue) — represents an existential competitive challenge. Fast fashion offers trend-responsive products at a fraction of PVH's prices, with supply chains engineered to go from design to store shelf in weeks rather than months.

The Inditex comparison is particularly instructive — and humbling. Inditex, with a market capitalization of over $200 billion, is worth more than sixty times PVH. Zara's parent reported a record profit of €6.22 billion for fiscal year 2024. Its supply chain is legendary: Zara can take a trend from the runway and have it in stores within two to three weeks, compared to the six-to-nine-month lead times typical of traditional brands like Calvin Klein and Tommy Hilfiger. This speed advantage means Zara can offer consumers "the look" of premium brands at a fraction of the price, updated constantly to reflect the latest trends. For PVH, which relies on seasonal collections and brand heritage to justify its price premium, Zara's speed-to-market represents a structural challenge that no amount of marketing can fully offset.

And then there is Shein, the ultra-fast digital disruptor that has compressed those timelines even further while offering prices that make even Zara look expensive. Shein's model — algorithmically driven, digitally native, with a supply chain capable of producing new styles in as little as three days — represents a fundamentally different approach to fashion retail. While Shein competes primarily at the low end of the market, its cultural influence extends upward: Gen Z consumers who discover trends on Shein's platform develop aesthetic expectations that pressure every brand in the market, including Calvin Klein and Tommy Hilfiger.

Where does this leave PVH? Morningstar's assessment is blunt: the firm assigns PVH a "no moat" rating, stating that "we do not believe that either of PVH's major brands has the pricing power or competitiveness to provide an economic moat."

This is a harsh judgment, but it reflects a real vulnerability. Calvin Klein and Tommy Hilfiger are famous, but fame does not equal pricing power. Consumers love these brands, but they are not willing to pay luxury premiums for them.

The brands compete in a segment where substitution is easy, switching costs are low, and consumer attention is constantly contested by newer, trendier alternatives.

PVH's defensive advantages are real but limited: global scale across forty-plus countries, decades of brand heritage, deep wholesale relationships, and the operational efficiency that comes from managing two large brands on a shared platform.

In China, both brands have built meaningful businesses — Calvin Klein and Tommy Hilfiger ranked among Tmall's top international fashion brands. But the Unreliable Entity List designation exposed how quickly geopolitical forces can undermine years of market-building investment.

XII. Analysis: Porter's Five Forces & Hamilton's Seven Powers

A rigorous framework analysis reveals the structural realities behind PVH's competitive position.

Starting with Porter's Five Forces: the threat of new entrants is a paradox in fashion. The barriers to manufacturing apparel are almost nonexistent — anyone with a sewing machine and a Shopify account can launch a clothing brand tomorrow. But the barriers to building a brand with the global recognition of Calvin Klein or Tommy Hilfiger are enormous.

Decades of cultural embedding, billions in cumulative marketing spend, and deep wholesale relationships create advantages that no startup can replicate quickly. However, digital channels have lowered the distribution barriers dramatically, enabling DTC brands to reach consumers without the traditional gatekeepers of department store buyers and fashion editors.

Supplier bargaining power is relatively low, which works in PVH's favor. The company sources from a highly diversified base across thirty-seven countries, and the apparel manufacturing market is fragmented, competitive, and largely commoditized. No single supplier has meaningful leverage over PVH. The one exception may be specialized premium materials — certain high-quality fabrics and sustainable inputs — where supply may be more constrained.

Buyer bargaining power is high, and this is one of PVH's most significant structural challenges. On the wholesale side, major department store chains like Macy's and Kohl's wield enormous leverage. They can demand favorable pricing, return allowances, and markdown support.

On the consumer side, fashion shoppers have essentially infinite choice — a Calvin Klein shirt competes not just with Ralph Lauren but with Zara, H&M, Uniqlo, Amazon Essentials, and thousands of DTC brands. Price sensitivity in the wholesale channel is particularly acute, as department stores increasingly lean on promotions and clearance events to drive foot traffic.

The threat of substitutes is very high. Fast fashion offers trend-responsive alternatives at a fraction of PVH's prices. Department stores' own private labels compete directly on the same shelves. And luxury brands compete for the premium portion of the consumer's wardrobe budget. When a consumer decides between a $75 Calvin Klein T-shirt and a $15 Zara T-shirt that looks almost identical, the value proposition of the brand name is tested in its most naked form.

Competitive rivalry is intense across every dimension — product, price, geography, and channel. The premium apparel market is saturated, fashion cycles create constant disruption, and international competition spans every price point. There are no quiet corners in this industry.

Turning to Hamilton Helmer's Seven Powers framework, the picture becomes clearer.

PVH's primary competitive power is Branding — and it is a meaningful one. Calvin Klein and Tommy Hilfiger represent decades of accumulated brand equity, cultural relevance, and consumer trust. This is the asset that justifies PVH's existence as a standalone company rather than a licensing business. The brands are recognized globally, carry aspirational associations, and command price premiums over unbranded alternatives. Branding is PVH's core asset and the reason anyone would own this stock.

Scale Economies provide moderate power. Operating two global brands across forty-plus countries with approximately 28,000 employees allows PVH to spread marketing costs, share supply chain infrastructure, and negotiate better terms with suppliers and retail partners. But PVH's scale is dwarfed by the luxury conglomerates: LVMH's fashion division alone is many times PVH's size.

Switching Costs are modest. Brand loyalty creates some stickiness — Calvin Klein's rewards program claims approximately 4.7 million members, and Tommy Hilfiger's membership program has around 3.2 million. But in fashion, switching costs are inherently low. Consumers do not face contractual lock-in, data migration costs, or retraining requirements. They simply buy a different brand next time.

Network Effects are weak to nonexistent. Fashion has some social-proof dynamics (wearing a recognizable brand signals something about the wearer), but these fall far short of true network effects where each additional user makes the product more valuable for all other users.

Counter-Positioning is weak. PVH's heritage positioning offers some differentiation versus ultra-fast fashion, but the company is vulnerable to new DTC brands that can offer similar aesthetics at lower prices through more efficient business models.

Cornered Resource is limited but worth noting. PVH owns the Calvin Klein and Tommy Hilfiger trademarks outright — genuinely valuable intellectual property that cannot be replicated. No competitor can launch a "Calvin Klein" brand. But trademark ownership alone does not constitute a cornered resource in the Helmer sense, because PVH does not control unique materials, exclusive technologies, or irreplaceable distribution channels.

Process Power is weak to moderate. The operational improvements under the PVH+ Plan, including the targeted $150 million in annual cost savings by 2026, represent real efficiency gains. But operational efficiency is a necessary condition for competitiveness, not a sustainable moat. Competitors can and do replicate supply chain and cost-management innovations.

The synthesis is clear: PVH's competitive position rests almost entirely on the strength of its two brands. If those brands maintain cultural relevance and consumer demand, the company can generate attractive returns. If brand heat fades — as it does for most fashion names eventually — there is no secondary moat to fall back on.

This is a crucial insight for long-term investors. PVH is, at its core, a bet on the durability of brand equity in the premium fashion segment. Execution is not just important; it is existential.

XIII. Bull vs. Bear Case

The bull case for PVH begins with the obvious: Calvin Klein and Tommy Hilfiger are two of the most recognizable fashion brands on the planet, with global awareness that very few competitors can match.

The PVH+ Plan has shown early traction, with revenue consistently coming in above guidance and gross margins reaching record levels. The marketing machine is firing — campaigns like the Bad Bunny partnership for Calvin Klein and Tommy Hilfiger's K-Pop collaborations have generated cultural moments that translate into genuine consumer engagement.

Management's target of $150 million in annual cost savings by 2026 provides a clear path to margin improvement, and the company's aggressive capital return program — approximately $500 million in stock repurchases each in 2024 and 2025 — signals management's confidence in the business's cash generation.

In Asia-Pacific, both brands ranked among Tmall's top five international fashion labels, suggesting meaningful demand in the world's most important growth market for consumer goods. And the valuation, at a price-to-earnings ratio in the single digits, implies that the market is pricing in significant pessimism — creating potential upside if execution proves better than expected.

The bear case is equally compelling and, in some ways, more structurally grounded. The Morningstar "no moat" assessment captures the essential vulnerability: neither Calvin Klein nor Tommy Hilfiger commands the pricing power or brand exclusivity that would constitute a durable competitive advantage. This is not a subjective opinion — it is backed by the data. When department stores run promotions, Calvin Klein and Tommy Hilfiger products are routinely discounted by thirty to fifty percent, a pattern that would be unthinkable for a true luxury brand. Hermès does not go on sale. Louis Vuitton does not have clearance racks. The fact that PVH's brands participate in the promotional cycle tells you everything about their positioning relative to the luxury tier.

Net income declined approximately ten percent in fiscal 2024, and Calvin Klein's operating margin compressed from eighteen percent to fourteen percent — a worrying trajectory for a brand that is supposed to be in elevation mode. The tariff headwind of roughly a dollar per share in fiscal 2025 is a real drag on earnings, and the geopolitical situation with China introduces a risk factor that no amount of operational excellence can mitigate.

The concentration risk is stark: with over ninety percent of revenue coming from two brands, a sustained downturn in either Calvin Klein or Tommy Hilfiger would hit PVH with full force and no offset. Consider the contrast with LVMH, which operates over seventy brands across fashion, wine, spirits, perfumes, watches, and retail. If one brand stumbles, dozens of others provide ballast. PVH has no such cushion.

And the department store channel, which remains the majority of PVH's wholesale business, faces structural headwinds that show no sign of abating. The recent bankruptcy of Saks Global — the parent of Saks Fifth Avenue — sent ripples through the wholesale fashion industry. G-III Apparel, a major PVH licensee partner, took a significant earnings hit from exposure to the Saks bankruptcy. While PVH's direct exposure was more contained, the episode underscored the fragility of the wholesale channel. The question is not whether department stores will continue to decline, but how fast, and whether PVH's DTC shift can compensate quickly enough.

Key risks to monitor include tariff policy volatility and PVH's ability to mitigate cost impacts through sourcing diversification and pricing; consumer spending trends in the three critical markets of the United States, China, and Europe; the execution risk of bringing licensed categories back in-house; and the ever-present risk of brand fatigue — the possibility that consumers simply get bored and move on to the next cultural moment.

For investors tracking this company, three KPIs deserve particular attention.

First, direct-to-consumer comparable sales growth — this is the best real-time signal of brand health and consumer demand, stripped of the noise from wholesale dynamics and channel shifts. When consumers are voting with their wallets in PVH's own stores and websites, that is the purest measure of how the brands are performing.

Second, gross margin trajectory — the spread between revenue and cost of goods reflects PVH's ability to maintain pricing power, manage input costs, and shift the channel mix toward higher-margin DTC. An expanding gross margin means the brands are commanding premium pricing and the supply chain is efficient; a compressing margin signals competitive pressure or rising costs.

Third, Calvin Klein and Tommy Hilfiger brand-specific operating margins — since PVH is a pure-play two-brand company, the operating margin of each brand captures the net result of everything from marketing spend to product innovation to supply chain efficiency.

Watching these three metrics over time will tell you more about PVH's trajectory than any management presentation.

XIV. Epilogue: What's Next for PVH?

PVH stands at an interesting inflection point. The company's most recent quarterly results — Q3 fiscal 2025, reported in December 2025 — showed revenue of $2.294 billion, representing modest year-over-year growth, with earnings of $2.83 per share that beat consensus estimates by a comfortable margin.

Management narrowed full-year guidance to the high end of previous ranges, signaling confidence in the trajectory. The stock, however, tells a different story: PVH's market capitalization of approximately $3.2 billion as of early March 2026 represents a nearly forty percent decline over the past year, a dramatic divergence from competitors like Ralph Lauren, whose market cap has grown by over twenty percent in the same period.

This disconnect between operational execution and market valuation raises a question that every PVH investor must grapple with: Is the market wrong, or does it see something that the quarterly numbers do not yet reflect?

The bears would point to the structural vulnerabilities — the lack of a durable moat, the geopolitical risks, the concentration in two brands, the secular headwinds facing wholesale distribution.

The bulls would counter that the market is over-discounting near-term tariff and China-related uncertainty while under-appreciating the long-term value of two globally recognized brands managed with increasing operational discipline.

The sustainability question looms large. Can marketing-driven momentum — viral campaigns, celebrity partnerships, cultural relevance — become a sustainable competitive advantage, or is it inherently ephemeral?

In fashion, the answer is usually the latter. Brands that are culturally hot today can be culturally irrelevant tomorrow. The history of fashion is littered with once-dominant names that lost their way: think of how quickly brands like Abercrombie & Fitch, J. Crew, or even parts of the Ralph Lauren empire have cycled between relevance and irrelevance.

PVH's challenge is to break that cycle — to build the operational and creative infrastructure that keeps Calvin Klein and Tommy Hilfiger perpetually fresh rather than riding a single cultural wave until it crashes.

The generational challenge is real. Gen Z and Gen Alpha consumers — the demographics that will drive fashion spending for the next two decades — have different expectations, different values, and different consumption patterns than their predecessors. They care about sustainability, authenticity, and social signaling in ways that require brands to do more than slap a logo on a T-shirt. PVH has invested in sustainability initiatives and digital-first marketing, but whether these efforts are sufficient to win the loyalty of a generation that grew up with Shein and TikTok remains an open question.

There is an interesting tension in PVH's approach to sustainability. The company publishes comprehensive corporate responsibility reports and has made commitments around supply chain transparency, worker welfare, and environmental impact. These are meaningful initiatives. But the fashion industry as a whole faces a fundamental contradiction: it is built on the premise of constant newness — new collections, new trends, new reasons to buy — which is inherently at odds with sustainability's core message of consuming less. How PVH navigates this tension — whether it can credibly position Calvin Klein and Tommy Hilfiger as sustainable brands without fundamentally altering the consumption model that drives revenue — will be an important factor in maintaining relevance with younger consumers who are increasingly skeptical of corporate greenwashing.

Emerging trends in digital fashion — including metaverse fashion, NFTs, and virtual try-on experiences — represent potential opportunities but also potential distractions. PVH has dabbled in these areas, as have most major fashion companies, but the commercial viability of digital fashion remains unproven. The more immediate and consequential trend is the continued growth of social commerce — buying directly through platforms like Instagram, TikTok, and WeChat — which is changing how consumers discover and purchase fashion. PVH's ability to build effective social commerce capabilities will be as important as its traditional retail and e-commerce investments.

Finally, there is the ever-present M&A question. With a market capitalization below $3.5 billion and two globally recognized brands, PVH could be an attractive acquisition target for a larger luxury conglomerate seeking to expand its accessible premium portfolio. LVMH, Kering, or Tapestry could theoretically absorb PVH's brands and bring their own operational scale and distribution networks to bear.

Whether management would entertain such an approach, and at what price, is speculative — but it is a scenario that investors cannot ignore. At current valuations, PVH's two brands may be worth more to a strategic acquirer than the market is currently pricing into the stock. The entire company is valued at roughly $3.2 billion — less than Tapestry paid for Kate Spade alone back in 2017.

From the coal fields of Pottsville to the runways of Milan, PVH's 145-year journey is a testament to the power of reinvention. Moses Phillips selling shirts from a pushcart could never have imagined that his family's business would one day own Calvin Klein and Tommy Hilfiger.

But the thread connecting pushcart to global conglomerate is consistent: a belief, refined across generations, that the brand is the business. The question now is whether that belief is enough in a world where brands can be built in months, destroyed in weeks, and where the consumer has never had more choice or less loyalty.

XV. Recommended Reading

- PVH Corp Annual Reports (2020–2024) — Investor Relations section of pvh.com

- "The End of Fashion" by Teri Agins — Essential context on the fashion industry's transformation from couture to commerce

- "Deluxe: How Luxury Lost Its Luster" by Dana Thomas — A sharp examination of how premium brands navigate the tension between accessibility and exclusivity

- PVH+ Plan Investor Presentation (April 2022) — The strategic blueprint for the company's current direction

- Calvin Klein: A Brand in Crisis? — Harvard Business School case study on the brand's evolution and challenges

- "American Dreamer: My Life in Fashion & Business" by Tommy Hilfiger — The founder's own account of building one of America's most recognizable brands

- PVH Corporate Responsibility Reports — ESG strategy, supply chain transparency, and sustainability commitments

- Morningstar PVH Equity Research Reports — Independent analysis including the "no moat" rating and fair value estimates

- Business of Fashion PVH Coverage — Industry context, executive interviews, and critical analysis of brand strategy

- PVH Earnings Call Transcripts (2022–2025) — Management commentary on strategy execution, competitive dynamics, and forward guidance

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube