Pure Storage: The Flash Revolution That Disrupted Enterprise Storage

I. Introduction & Episode Roadmap

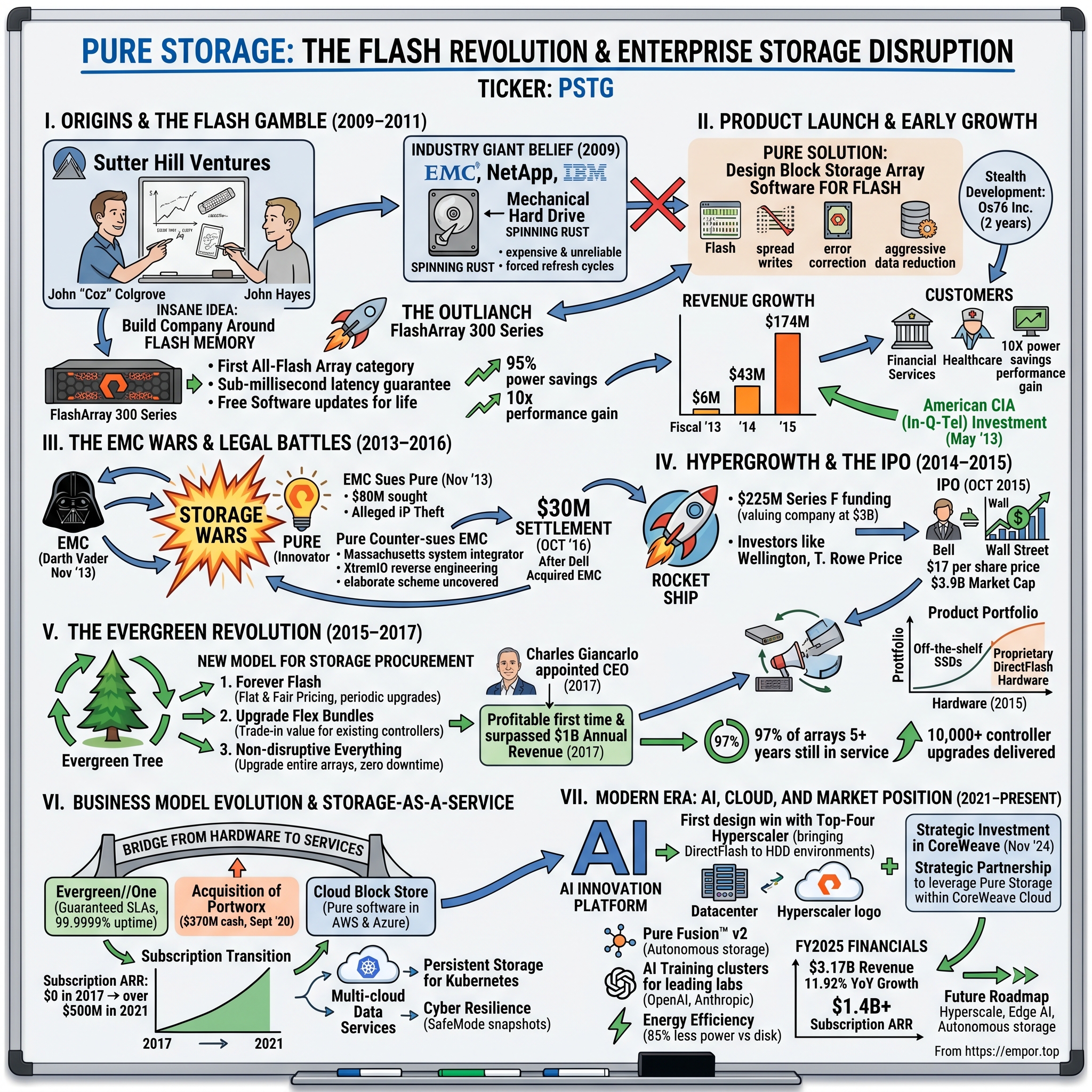

Picture this: It's 2009, and the enterprise storage industry is a $30 billion behemoth dominated by spinning disk arrays that hadn't fundamentally changed since the 1990s. EMC, NetApp, and IBM control the market with iron fists, selling refrigerator-sized boxes filled with mechanical hard drives to Fortune 500 companies at eye-watering margins. Then, in a nondescript office in Mountain View, two Johns—John Colgrove and John Hayes—are sketching out what seems like an insane idea: build an entire storage company around flash memory, a technology so expensive and unreliable that industry veterans dismiss it as a toy for consumer electronics.

Fast forward to today, and Pure Storage stands as a $19.4 billion market cap company that didn't just enter the storage market—it fundamentally rewrote the rules. The company pioneered the all-flash array category, introduced the industry's first true subscription model for enterprise storage hardware, and created a business model where 97% of its arrays deployed over five years ago are still in production—an unheard-of retention rate in an industry built on forced refresh cycles.

How did a startup take on EMC, NetApp, and the entire storage establishment—and win? The answer lies not just in betting on flash memory before anyone else, but in understanding that the real disruption wasn't the technology itself—it was reimagining the entire business model of enterprise storage. Pure didn't just build faster storage; they built storage that never needs to be thrown away, turning a capital expenditure business into a subscription service that aligns vendor and customer incentives for the first time in the industry's history.

This is the story of how Pure Storage went from stealth startup to storage-as-a-service innovator, survived vicious legal battles with EMC, navigated one of the most successful enterprise IPOs of the 2010s, and positioned itself at the center of the AI revolution. It's a tale of flash economics meeting subscription disruption, where the Evergreen model became not just a product feature but a philosophy that transformed how enterprises think about infrastructure.

Along the way, we'll explore the key inflection points: the gamble on flash when it seemed economically impossible, the brutal storage wars that nearly derailed the company, the radical Evergreen model that broke the industry's replacement cycle addiction, and the transition from hardware vendor to subscription service provider. We'll dissect how a company founded on a contrarian bet about flash memory economics evolved into something far more powerful—a platform that guarantees outcomes, not just products.

II. Origins & The Flash Gamble (2009–2011)

The scene opens in August 2009, inside the Mountain View offices of Sutter Hill Ventures. The venture capital firm's walls are lined with the logos of tech successes—Seagate, eBay, Intuit—but today, two engineers are about to bet against everything those companies' data centers believe to be true. John "Coz" Colgrove, a veteran storage inventor with 20 years at Veritas, and John Hayes, former CTO of Yahoo!, are sketching out the architecture for what would become Pure Storage, operating under the stealth code name Os76 Inc.

The storage industry in 2009 was a $30 billion fortress built on spinning rust—hard disk drives that hadn't fundamentally changed since IBM invented them in 1956. EMC ruled the market with a $44 billion market cap, selling refrigerator-sized arrays stuffed with mechanical drives. NetApp commanded another $10 billion slice. These companies sold storage like drug dealers sold addictive substances: get customers hooked on your arrays, then milk them for upgrades, maintenance, and complete replacements every 3-5 years. The margins were extraordinary—often 60-70% gross margins on hardware that customers had no choice but to buy.

But Colgrove and Hayes saw something the industry giants missed or willfully ignored. Colgrove established Pure in 2009 with the belief that flash storage would one day eventually overtake disk, offering a cheaper total cost of ownership, better performance, and improved sustainability. This wasn't just contrarian—it was heretical. Flash memory in 2009 cost roughly 100 times more per gigabyte than hard drives. Worse, it had a fatal flaw that made enterprise executives laugh at the mere suggestion of using it for mission-critical data.

The flash drives of 2009 could only support 10,000 read/write cycles—not enough memory real estate for the types of loads handled by enterprise data centers. To understand how problematic this was, consider that enterprise storage systems routinely handle millions of write operations daily. A flash array built with 2009 technology would literally burn itself out in months, not the years that enterprises demanded. NOR flash endurance ranged from as little as 100 erase cycles for on-chip flash memory, to a more typical 10,000 or 100,000 erase cycles, while enterprise applications demanded systems that could handle decades of continuous operation.

The endurance problem wasn't just technical—it was existential. Solid-state memory cells have an intrinsic, finite number of program/erase cycles that each cell can incur. As a result, solid-state storage has a maximum amount of program/erase cycles to which it can be subjected. Every time data was written to a flash cell, the oxide layer that isolated the floating gates would degrade slightly. After enough cycles, the cell would fail completely, corrupting data and destroying the array's integrity.

Yet Colgrove brought a unique perspective to this challenge. As one of the founding engineers at VERITAS Software, where his 20-year career culminated as Fellow and Chief Technology Officer, Colgrove was the Primary Architect for the hugely successful VERITAS Volume Manager (VxVM) and VERITAS File System (VxFS). During his time at VERITAS, he became one of the industry's foremost experts on optimizing I/O streams and data structures for the unique idiosyncrasies of rotational hard drives.

After leaving Symantec in 2008 to pursue personal interests, he joined Sutter Hill Ventures in the role of Entrepreneur in Residence. It was there he observed the growing acceptance of solid-state storage by enterprises that led him to co-found Pure Storage with John Hayes. Hayes brought complementary expertise from the web-scale world. After serving in Yahoo!'s Office of the Chief Technologist, where he investigated web architectures for collaborative development of highly-reliable systems, Hayes had focused on developing distributed platforms for real-time interpersonal interaction. During this time, he became interested in the underlying architecture of reliable distributed systems, particularly those built from unreliable components. His diverse experiences led him to develop new approaches to make today's increasingly complex distributed systems more reliable.

The two Johns' solution was elegant in its audacity. They solved the endurance problem by designing block storage array software specifically for solid-state devices. They started with a flexible software architecture consisting of two layers: A lower layer dedicated to the optimization of the physical storage medium for performance, reliability, and longevity, and an upper layer to handle storage management system-level tasks, including virtualization, communication with hosts, data reduction, scheduling internal I/O, RAID protection, and overall array management.

This wasn't just about making flash work—it was about reimagining the entire storage stack from first principles. While EMC and NetApp were trying to retrofit flash into architectures designed for spinning disks, Pure was building something entirely new. They would use sophisticated algorithms to spread writes across all available flash cells, implement advanced error correction that could rescue failing cells, and compress and deduplicate data so aggressively that customers would need far less raw flash capacity than traditional arrays required in spinning disk.

Initially, the company was setup within the offices of Sutter Hill Ventures, a venture capital firm, and funded with $5 million in early investments. This wasn't a massive Series A by 2009 standards, but it was enough to hire a small team of engineers and begin the stealth development that would continue for two years.

Colgrove's philosophy on team building would prove crucial. As an engineer, he always believed that every engineer, including himself, has blind spots. You have to team up with somebody. Mike Spicer introduced him to John Hayes, who was brilliant but not a storage person. That was a great strength—they did not hire a bunch of storage people. They were trying to change the storage industry completely, hiring people that complemented them while ensuring a few had storage experience to avoid rookie mistakes.

The early team worked in near-complete secrecy, understanding that if EMC or NetApp caught wind of what they were building, the giants could either copy the approach or, more likely, use their market power to crush Pure before it could gain traction. For nearly two years, Pure Storage was a ghost—no website, no marketing, no public presence whatsoever. Just a small team of engineers in Mountain View, writing code that would eventually topple empires.

The bet they were making was breathtaking in its scope. They weren't just betting that flash prices would fall—though they needed them to drop by at least 10x to be viable. They weren't just betting they could solve the endurance problem—though failure here meant the company would die. They were betting that the entire $30 billion storage industry was wrong about what customers actually wanted: not bigger, faster boxes, but storage that was simple, reliable, and never needed to be thrown away.

As 2009 turned to 2010, Pure Storage remained in stealth, methodically building the foundation for what would become the most disruptive force the storage industry had ever seen.

III. Product Launch & Early Growth (2011–2013)

The moment of truth arrived in August 2011. After two years in stealth, Pure Storage emerged from the shadows with a product that would either revolutionize enterprise storage or become another footnote in Silicon Valley's graveyard of ambitious failures. The company came out of stealth mode as Pure Storage in August 2011. The timing was deliberate—Pure had spent those stealth years not just building technology, but watching flash prices plummet from $10 per gigabyte to under $2, approaching the economic viability threshold they'd been betting on.

Simultaneously, Pure Storage announced it had raised $30 million in a third round of venture capital funding. This wasn't just capital—it was validation. The investors included Greylock Partners and Index Ventures, firms that had backed transformative enterprise companies. They weren't betting on flash memory; they were betting on Pure's radical vision of storage that never needed replacement.

The first commercial product, the FlashArray 300 Series, launched with specifications that seemed impossible to industry veterans. Where EMC's arrays required entire racks and consumed tens of kilowatts of power, Pure's 3U appliance—about the size of a pizza box—could deliver the same performance while consuming just one kilowatt. The data reduction rates were staggering: 5-to-1 average compression and deduplication, meaning customers needed to buy only a fraction of the raw flash capacity they'd need with traditional arrays.

But the real innovation wasn't the hardware—it was the business model. Pure guaranteed that their arrays would deliver consistent sub-millisecond latency, forever. They promised free software updates for life. Most audaciously, they claimed their arrays would never need to be replaced, just upgraded in place. In an industry built on forced refresh cycles, this was heresy.

Another $40 million was raised in August 2012, in order to fund Pure Storage's expansion into European markets. The European expansion was critical—Pure needed to prove they weren't just a Silicon Valley phenomenon but could compete globally against entrenched vendors with decades-old customer relationships.

The early customer wins told a compelling story. A major financial services firm replaced 15 racks of EMC storage with two Pure FlashArrays, cutting power consumption by 95% while improving performance tenfold. A healthcare provider consolidated 200 virtual machines from spinning disk to flash, reducing their backup window from 12 hours to 45 minutes. These weren't incremental improvements—they were transformational.

Annual revenues for Pure Storage grew by almost 50% per quarter, from 2012 to 2014. It had $6 million in revenues in fiscal 2013, $43 million in fiscal 2014, and $174 million in fiscal 2015. This wasn't just growth—it was one of the fastest revenue ramps in enterprise hardware history. To put this in perspective, Pure was adding more revenue each quarter than most storage startups generated in their entire existence.

The sales strategy was counterintuitive. While EMC and NetApp relied on armies of salespeople and complex channel partnerships, Pure sold directly with a small, elite sales force. They targeted the most demanding workloads first—databases, virtual desktop infrastructure, critical applications—knowing that if they could prove themselves there, the rest of the data center would follow.

By late 2012, Pure had shipped 100 devices. By 2014, that number exceeded 1,000. Each array shipped became a reference point, a proof point that all-flash wasn't just viable—it was inevitable. Customers weren't just buying storage; they were buying into a movement against the storage establishment.

Then came the validation that shocked the industry. In May 2013, the venture capital arm of the American Central Intelligence Agency (CIA), In-Q-Tel, made an investment in Pure Storage for an un-disclosed amount. When the CIA's venture arm invests in a company, it sends a clear signal: this technology matters for the most demanding, mission-critical applications in the world. For Pure's competitors, it was a wake-up call that this startup wasn't going away.

That August, Pure Storage raised another $150 million in funding. By this time, the company had raised a total of $245 million in venture capital investments. The war chest was building, and Pure would need every dollar for what was coming next.

The product evolution during this period was relentless. Every quarter brought new features that traditional storage vendors said were impossible with flash: inline deduplication that didn't impact performance, encryption with zero overhead, snapshots and replication that consumed no additional space. Pure was systematically eliminating every objection to all-flash adoption.

But beneath the technical achievements and revenue growth, a storm was brewing. EMC, NetApp, and the other storage giants had finally woken up to the threat Pure posed. They began acquiring flash startups, filing patents, and most ominously, preparing legal challenges. The storage wars were about to begin, and Pure Storage would find itself in the crosshairs of an industry that didn't appreciate disruption.

As 2013 drew to a close, Pure had proven that all-flash arrays weren't just technically viable—they were commercially explosive. But proving you can build a better mousetrap is one thing. Surviving when the incumbent mousestrap manufacturers decide to destroy you is quite another.

IV. The EMC Wars & Legal Battles (2013–2016)

The storage industry had never seen anything like the war that erupted in 2013. It wasn't just business competition—it was personal, vindictive, and increasingly desperate. In 2013, EMC sued Pure Storage and 44 of its employees who were former EMC employees, alleging theft of EMC's intellectual property. The timing was no coincidence. Pure had just closed their massive funding round and was stealing customers at an alarming rate. EMC, the $44 billion storage giant, decided it was time to crush the upstart.

The first salvo came in October 2013, when EMC accused Pure of poaching its staff and getting them to hand over confidential EMC information in violation of their employment agreements. But the real bombshell dropped in November. In November 2013, EMC sued Pure in federal court in Delaware, claiming that Pure infringed five patents involving various data storage technologies. EMC said in its Nov. 5 complaint that "The activities advanced and directed by Pure Storage are part of a systematic and unlawful strategy to identify, target and convert valuable EMC assets for Pure Storage's benefits as Pure Storage seeks to brand itself as an 'innovator' in the enterprise storage market, apparently as part of its pre-IPO strategy".

But Pure had ammunition of its own. In a stunning counter-complaint, Pure Storage counter-sued, alleging that EMC illegally obtained a Pure Storage appliance for reverse engineering purposes. The details were explosive: a Massachusetts system integrator bought a Pure Storage FlashArray FA-320 device in October or early November 2012, saying it would be used by one of its subsidiaries in New Hampshire. Instead, the company shipped the array to EMC, specifically to the Silicon Valley headquarters of the XtremIO division, at EMC's expense. EMC even used its own corporate UPS account number for the shipment.

The scheme was elaborate. Continental Resources (ConRes) had arranged for Pure engineers to set up the system at the New Hampshire site. Instead, it hid the fact that the device had been moved to EMC and got Pure to help set up the array at XtremIO via a videoconference. Pure's engineers had unknowingly helped their biggest competitor reverse-engineer their product.

This wasn't just corporate espionage—it revealed EMC's desperation. In 2012, for its entry into the all-flash array market, EMC bought startup XtremIO and its all-flash array technology for $430m. But XtremIO was struggling. Internal EMC emails that would later surface in court revealed the depth of their concern. This action may have been triggered by Pure winning bids against EMC's XtremIO product due to Pure's data-reduction technology.

The internal EMC communications were damning. Josh Goldstein, VP of marketing for XtremIO, admitted Pure's proof-of-concept expertise was superior to EMC's. David Wing, another EMC executive, worried about Pure's Forever Flash program and free controller upgrades. Most telling was Wing's July 2014 email: "When [customers] start listening, Pure does a very good job of turning EMC into Darth Vader".

The legal battle dragged on for years, becoming increasingly bitter. Before the trial started, EMC dropped one patent from the case, and the judge in a pre-trial summary judgment ruling found that Pure didn't infringe another. In the same ruling, the judge hearing the case found that Pure infringed certain claims of one of EMC's patents related to de-duplication technology.

When the case finally went to trial in March 2016, the stakes were enormous. EMC had originally sought more than $80 million. After a seven-day trial, A federal court jury found March 15 that Pure Storage violated an EMC patent related to deduplication, and that the smaller rival should pay $14 million. In 2016, a jury initially awarded $14 million to EMC. However, the same jury found that Pure did not violate two other patents.

But the story took another twist. A judge reversed the award and ordered a new trial to determine whether the EMC patent at issue was valid. The reversal was a stunning rebuke to EMC's legal strategy and validation of Pure's position that the patents were either invalid or not infringed.

The war wasn't limited to the courtroom. EMC tried to strangle Pure's momentum by filing additional suits. For years, Pure Storage has incorporated data deduplication in its products that is covered by and infringes EMC's '015 patent. EMC's lawsuit says the earlier damages award was only for sales of Pure Storage products from November 2013 to January 2016 and covered only a limited set of Pure Storage products: the FlashArray series 300 and 400 products. The Dell-acquisition-target now alleges: "The FlashArray//m product contains deduplication technology that is materially the same as the technology already found to infringe the '015 patent."

Meanwhile, behind the scenes, something remarkable was happening. EMC executives were privately discussing acquiring Pure Storage. This implies some bosses within EMC thought Pure's systems would make a good acquisition target as they were perfect for the mid-tier. The irony was thick—EMC was simultaneously trying to destroy Pure in court while contemplating buying them.

The personal nature of the battle was exemplified by the rivalry between EMC's Chad Sakac and Pure's Vaughn Stewart, two storage evangelists who took their war to social media, blogs, and conference stages. Their public sparring matches became legendary in the storage industry, with each claiming technical superiority while attacking the other's credibility.

Finally, in October 2016, after EMC had been acquired by Dell, the combatants reached a settlement. Pure Storage will pay $30 million to Dell as part of a settlement of all litigation between the data storage companies involving allegations of violated contracts, infringement of an EMC patent and pilfered trade secrets. Pure Storage and EMC subsequently settled the case for $30 million.

The $30 million settlement was a fraction of what EMC had sought, and for Pure, it was the cost of ending a distraction that had consumed management attention for three years. More importantly, it removed the legal cloud hanging over Pure's upcoming IPO.

As Pure's general counsel noted: "EMC's litigious approach to competition primarily reflects efforts to stabilize its storage business as customers around the world abandon the kind of disk-based storage systems EMC pioneered in favor of flash-based storage from innovative companies like Pure. As the trial proceedings made clear, EMC built its own flash-based storage products via acquisition, rather than organic innovation."

The storage wars revealed a fundamental truth: EMC's empire was crumbling. Unable to innovate their way out of disruption, they had resorted to litigation. For Pure, surviving the legal onslaught while maintaining hypergrowth proved they weren't just a flash-in-the-pan startup. They were the future of enterprise storage, and no amount of lawsuits could stop that.

V. Hypergrowth & The IPO (2014–2015)

The spring of 2014 marked a pivotal moment for Pure Storage. The company was burning cash at a rate that would make even the most aggressive venture capitalists nervous, yet growing at a pace that defied all precedent in enterprise storage history. The following year, in 2014, Pure Storage raised $225 million in a series F funding round, valuating the company at $3 billion. This wasn't just another funding round—it was the largest private investment in a storage company ever, and it came with a cast of investors that signaled Pure's transition from startup to pre-IPO unicorn.

The investors in this round read like a who's who of public market crossover funds: Wellington Management, T. Rowe Price, and Tiger Global. These weren't traditional venture capitalists betting on potential—these were public market investors who knew exactly how Wall Street valued companies, and they were paying $15.73 per share for Pure's stock. The presence of these funds meant one thing: an IPO was imminent.

The numbers behind Pure's hypergrowth were staggering. Annual revenues for Pure Storage grew by almost 50% per quarter, from 2012 to 2014. It had $6 million in revenues in fiscal 2013, $43 million in fiscal 2014, and $174 million in fiscal 2015. In the years ending January 2013, 2014 and 2015, the company grew from $6 million to $43 million to $174 million, respectively, topping the growth rates of prior enterprise speed demons such as Riverbed, DataDomain and GGV-backed stars such as Nimble Storage and Isilon.

But this growth came at a price. The company lost $183.2 million in fiscal 2015 on revenue of $174.4 million. According to its S-1 document, Pure Storage burned net cash of $44.5 million during the first half of its current fiscal year. That cash deletion is predicated on a much larger $113 million loss recorded during the same period, including non-cash expenses. The burn rate was heroic even by Silicon Valley standards, but it reflected a deliberate strategy.

By late 2014, Pure had grown to 750 employees, up from just 50 three years earlier. The company was hiring at a frantic pace—not just engineers, but an entire enterprise sales force capable of competing with EMC's decades-old relationships. Each enterprise salesperson cost hundreds of thousands of dollars per year, and it took months before they became productive. But Pure knew that to win the storage wars, they needed boots on the ground in every major account.

The product portfolio was expanding rapidly. Pure Storage finished developing its own proprietary flash storage hardware in 2015. This was crucial—initially, Pure had used off-the-shelf SSDs from suppliers like Samsung and Intel. But to achieve the performance, reliability, and economics they needed, Pure had to go deeper into the stack, designing custom flash modules that could deliver better density and endurance than anything available commercially.

The competitive landscape was heating up. EMC's XtremIO was gaining traction, NetApp had acquired SolidFire, and even traditional server vendors like HP and Dell were launching all-flash arrays. The window for Pure to establish itself as the independent leader in all-flash was closing rapidly.

Pure Storage filed a notification of its intent to go public with the Securities Exchange Commission in August 2015. That October, 25 million shares were sold for a total of $425 million. The IPO was priced at $17 per share, the midpoint of the $16-$18 range, giving Pure a market capitalization of $3.9 billion. At its offer price, Pure Storage commands a fully-diluted market cap of $3.9 billion, and its $425 million offering is the largest for a VC-backed tech IPO this year.

The IPO roadshow was a marathon. CEO Scott Dietzen and CFO Tim Riitters crisscrossed the country, meeting with hundreds of institutional investors. The pitch was simple but powerful: Pure was the fastest-growing company in storage history, flash was inevitable, and Pure's software-defined approach gave them advantages that hardware-centric competitors couldn't match.

But the market reception was sobering. The company priced its IPO at $17 per share, the mid-point of its filing range, and traded down over 5 percent on its first day of trading, then fell a bit further on its second day before rallying at the end of the week to close at $16.60, still below its IPO price. For a company that had been valued at nearly the same price in its last private round 18 months earlier, this was a disappointment.

The tepid reception reflected broader market concerns. The tech IPO market in 2015 was cooling rapidly. High-flying unicorns were being revalued, and investors were demanding clear paths to profitability. Pure's message that they would continue to prioritize growth over profitability didn't resonate with public market investors worried about a broader tech correction.

"Our strategy is to increase our investments in marketing, sales, support and research and development at the expense of near-term profitability," Pure Storage stated in the SEC filing. "We believe our decision to continue investing heavily in our business will be critical to our future success. We anticipate that our operating costs and expenses will increase substantially for the foreseeable future."

The ownership structure post-IPO told the story of Pure's journey. Sutter Hill Ventures, Greylock and Redpoint Ventures are principal shareholders, controlling 27.4 percent, 17.3 percent, and 5.7 percent respectively. Sutter Hill, which had incubated the company in its offices six years earlier, remained the largest shareholder—a testament to their conviction in the flash revolution.

Despite the lukewarm market reception, the IPO was a success in one critical way: it gave Pure the capital and credibility to compete as a public company. Given its heroic burn rate, Pure Storage's cash and equivalents total of $128.3 million is thin. The company initially reported that it expected to raise $395.2 million in its public offering. This is an IPO as much as it a recapitalization event for the company.

The IPO also marked a generational transition in enterprise technology. Pure was now public, competing directly with EMC, which would soon be acquired by Dell for $67 billion. The student had not yet surpassed the master, but for the first time, they were playing on the same field.

As 2015 drew to a close, Pure Storage faced a new reality. They were no longer the scrappy startup fighting the establishment—they were a public company with quarterly earnings calls, analyst coverage, and shareholders demanding returns. The next phase of Pure's journey would require not just technological innovation, but the discipline to balance growth with the path to profitability. The Evergreen revolution was about to begin.

VI. The Evergreen Revolution (2015–2017)

On June 1, 2015, just months before Pure Storage's IPO, the company dropped a bomb on the enterprise storage industry that would fundamentally rewrite the rules of how storage is bought, sold, and operated. Pure Storage announced FlashArray//m, the company's new flagship all-flash storage array, Pure1, a new cloud-based management and support offering, and Evergreen Storage, a new model for storage procurement and upgrades. Together, these innovations deliver storage that is dramatically simpler and more efficient, and eliminate the forklift upgrade and data migration burden from storage ownership. Now, storage can contribute meaningfully to transforming customers' business and IT infrastructure for higher growth and profitability.

The announcement wasn't just about new hardware—it was a declaration of war against the entire business model that had sustained the storage industry for decades. Pure Storage's new Evergreen Storage model eliminates the three- to five-year rip-and-replace storage lifecycle that has impaired IT efficiency for decades. With this new model, customers deploy storage once and upgrade it in-place for generations.

Matt Kixmoeller, Pure's VP of Products, captured the revolutionary nature of the moment: "Today, even when a customer buys the latest storage array, newer replacement equipment lies just around the corner, ready to render the current deployment obsolete. To refresh their technology, customers endure upgrade costs and hours of decreased performance or service interruptions during their 'forklift upgrades'"

The FlashArray//m itself was a marvel of engineering. Capable of consolidating racks of spinning disk into 3U, Pure Storage has shrunk storage arrays that were once the size of multiple refrigerators down to the size of a microwave, cutting power consumption down to one kilowatt (kW). New dual-drive flash modules coupled with Purity's FlashReduce data reduction software delivers up to 40TBs/U density. The newest array has claimed performance enhancements of 50% increase in performance, 2.6 times the density, and 2.4 times as power-efficient per TB over previous models.

But the hardware was just the enabler. The real revolution was Evergreen Storage, which consisted of three pillars that would transform storage economics:

First, Forever Flash delivers predictable ongoing "flat and fair" pricing, and includes software updates as well as periodic hardware upgrades, keeping the FlashArray modern over time. This wasn't just maintenance—it was a commitment that Pure's arrays would never become obsolete.

Second, Pure Storage is also announcing Upgrade Flex Bundles, which enable customers who are expanding their capacity to upgrade their FlashArray controller hardware, if desired, and receive trade-in value for their existing controller investment. Customers weren't locked into aging hardware—they could upgrade controllers while keeping their data in place.

Third, and most radically, was the promise of non-disruptive everything. Customers can now and going forward upgrade entire FlashArrays in the field to completely new technology generations without any downtime, performance impacts, forklift upgrades or data migration. This new model will change customer preconceptions about the way technology refresh is performed in enterprise-class storage arrays.

The industry reaction was a mixture of disbelief and panic. EMC, NetApp, and other incumbents had built their entire business models on the refresh cycle. A typical enterprise would spend millions on storage, use it for 3-5 years, then throw it away and buy new arrays—not because the old ones were broken, but because they were obsolete. Support costs would escalate after year three, forcing customers into refreshes. It was a $30 billion annual merry-go-round that vendors depended on for revenue.

Pure was saying: get off the merry-go-round. Buy storage once, keep it forever.

The economics were transformative. For every 250TB of Tier 1 performance disk storage replaced with Pure Storage, customers can save over a six year period, an average of more than $500,000 annually. Sierra Nevada: Hardware costs were cut significantly by moving from racks of spinning disk to flash, resulting in over $200,000 in savings and a 50 percent reduction in datacenter space. Sierra Nevada uses 1/10th of the power compared to what was needed for spinning disk. Perfection Fresh: Moving to an all-flash data center has allowed Perfection Fresh to process queries up to ten times faster. Combining the speed, and power & cooling savings, the FlashArray has delivered $120,000 in savings back to the business in the course of a year.

The technical architecture that enabled Evergreen was years in the making. Pure Storage achieves this upgrade model though a combination of its modular FlashArray software-defined architecture with Forever Flash, the company's standard maintenance program. Forever Flash delivers software and periodic hardware updates to customers for "flat and fair" pricing keeping their equipment modern.

By late 2015, Pure had shipped the first FlashArray//m systems and early customers were experiencing the Evergreen model firsthand. One financial services customer upgraded their controllers twice in 18 months without a second of downtime. A healthcare provider expanded capacity from 50TB to 500TB over two years without ever migrating data. These weren't incremental improvements—they were proof that storage could work like software.

The competitive response was swift but inadequate. EMC launched "Future-Proof Loyalty Program," NetApp introduced "Storage Service Level Agreements," but these were band-aids on a broken model. They still required customers to eventually replace their arrays. Pure was the only vendor saying your array would never need replacement.

In 2017, a major transition occurred that would prove crucial for executing on the Evergreen vision. The Board of Directors appointed Charles Giancarlo as CEO, replacing Scott Dietzen. Giancarlo, a former Cisco executive who had overseen that company's transition to software and services, understood that Pure's future wasn't in selling boxes—it was in delivering outcomes.

The transformation under Giancarlo was immediate. Pure accelerated the development of software capabilities, expanded the Evergreen model, and most importantly, began preparing for the next phase: storage-as-a-service. The company wasn't just disrupting the refresh cycle—they were reimagining storage as a utility.

In 2017 (2018 fiscal year), Pure Storage was profitable for the first time and surpassed $1 billion in annual revenue. This wasn't just a financial milestone—it was validation that the Evergreen model worked. Customers were willing to pay for storage that never needed replacement, and Pure could deliver it profitably.

The numbers told the story of Evergreen's success. We've delivered over 10,000 controller upgrades, and over 97% of all Pure Storage arrays five years and older are still in service today. In an industry where 100% of arrays were typically replaced after five years, this was revolutionary.

Customer testimonials captured the transformation. Lloyd Clarke, Virtualization Lead at Ordnance Survey, noted: "We've been through three non-disruptive upgrades together, are about to embark on another, and have had 100% uptime since 2015". Tim Ryan, CIO of Aegis Sciences, explained the strategic value: "Pure's Evergreen protects our investment while giving us the ability to upgrade storage on demand in increasingly dynamic situations, without disrupting the business."

As 2017 drew to a close, Pure Storage had achieved something remarkable. They hadn't just built better storage—they had broken the industry's addiction to refresh cycles. The Evergreen revolution proved that storage could be sold like software: constantly improving, never obsolete, aligned with customer success rather than vendor revenue targets. The next phase would be even more ambitious: turning storage into a true cloud service that customers could consume like electricity.

VII. Business Model Evolution & Storage-as-a-Service (2018–2021)

By 2018, Charles Giancarlo's vision for Pure Storage was becoming clear: the company wasn't going to be a storage vendor anymore—it was going to be a data platform company. The transition from hardware to services wasn't just a business model shift; it was an existential transformation that would determine whether Pure remained relevant in a cloud-dominated future.

The strategic imperative was stark. AWS, Azure, and Google Cloud were growing at astronomical rates, and they all offered storage-as-a-service. Customers were increasingly asking: why buy storage hardware when we can consume it from the cloud? Pure's answer would redefine what enterprise storage could be.

The foundation for this transformation had been laid with Evergreen, but now Pure needed to go further. They introduced Evergreen//One, a true consumption-based storage service that delivered guaranteed SLAs including 99.9999% uptime, performance guarantees, and cyber recovery. This wasn't just storage with a subscription price—it was storage delivered as a utility with contractual guarantees that no cloud provider could match.

The economics were revolutionary. Instead of massive capital expenditures followed by years of depreciation, customers could pay only for what they used, with the ability to scale up or down based on actual consumption. Pure was guaranteeing not just capacity but outcomes: specific performance levels, recovery time objectives, and even energy efficiency metrics.

In September 2020, Pure made its boldest move yet. Pure Storage announced that it has acquired Portworx, a well-funded startup that provides a cloud-native storage and data-management platform based on Kubernetes, for $370 million in cash. This marks Pure Storage's largest acquisition to date and shows how important this market for multicloud data services has become.

The Portworx acquisition wasn't just about technology—it was about capturing the future of enterprise applications. Gartner predicts that 85% of global businesses will be running containers in production, up from 35% in 2019. Portworx is the Kubernetes Data Services Platform most used by Global 2000 companies to provide persistent storage, high availability, data protection, data security, and cloud mobility for containers deployed in hybrid cloud architectures. By combining Portworx container data services with Pure's industry-leading data platforms and Pure Service Orchestrator software, Pure will provide a comprehensive suite of data services that can be deployed in-cloud, on bare metal, or on enterprise arrays, all natively orchestrated in Kubernetes.

Current Portworx enterprise customers include the likes of Carrefour, Comcast, GE Digital, Kroger, Lufthansa, and T-Mobile. These weren't just customers—they were enterprises betting their digital transformation on containerized applications, and Pure now owned the platform they trusted most.

Charles Giancarlo captured the strategic importance: "As forward-thinking enterprises adopt cloud-native strategies to advance their business, we are thrilled to have the Portworx team and their groundbreaking technology joining us at Pure to expand our success in delivering multicloud data services for Kubernetes. This acquisition marks a significant milestone in expanding our Modern Data Experience to cover traditional and cloud native applications alike."

The integration strategy was sophisticated. Murli Thirumale is excited to be taking on the role of Vice President and General Manager, Cloud Native Business Unit at Pure Storage. Yes, all the founders are joining Pure and will assume leadership positions in the new Cloud Native Business Unit. This wasn't an acqui-hire or a technology tuck-in—it was building an entirely new business unit focused on the cloud-native future.

Prior to Portworx, Pure had made smaller but strategic acquisitions. In August 2018, Pure Storage made its first acquisition with the purchase of a data deduplication software company called StorReduce, for $25 million. StorReduce brought cloud-native deduplication technology that would enhance Pure's ability to deliver efficient storage services across hybrid cloud environments.

The subscription transition was accelerating across the entire product portfolio. Pure introduced different consumption models to meet various customer needs:

- Evergreen//Forever: Traditional purchase with subscription to continuous upgrades

- Evergreen//Flex: Flexible ownership combining asset ownership with consumption economics

- Evergreen//One: True storage-as-a-service with guaranteed SLAs

- Pure as-a-Service: Comprehensive managed storage delivered as a utility

Each model represented a different point on the spectrum from capital expenditure to operating expense, allowing customers to choose based on their financial preferences and operational requirements.

The Cloud Block Store offering was particularly innovative. Pure essentially ran their FlashArray software in AWS and Azure data centers, allowing customers to use the same storage platform on-premises and in the cloud. This solved one of the biggest challenges of hybrid cloud: data mobility and consistency across environments.

The financial impact of the business model transformation was profound. Subscription annual recurring revenue (ARR) grew from essentially zero in 2017 to over $500 million by 2021. More importantly, the subscription model created predictable, recurring revenue streams that Wall Street valued far more highly than one-time product sales.

Customer adoption told the real story. Major enterprises began consuming Pure's storage entirely as a service. A global financial institution deployed over 10 petabytes of Evergreen//One storage across multiple data centers, paying only for actual consumption. A healthcare provider used Pure as-a-Service to handle explosive growth in medical imaging data without any capital investment.

The competitive response from traditional vendors was predictable but inadequate. Dell EMC, NetApp, and others launched their own "as-a-service" offerings, but they were essentially lease programs dressed up as services. They lacked Pure's fundamental architectural advantages: the ability to upgrade non-disruptively, the software-defined flexibility, and most importantly, the genuine alignment of vendor and customer incentives.

Pure's service-level agreements became a key differentiator. While competitors offered vague promises, Pure guaranteed specific, measurable outcomes: - 99.9999% availability (less than 32 seconds of downtime per year) - Specific IOPS and latency targets - Recovery point objectives (RPO) and recovery time objectives (RTO) - Even energy efficiency metrics with watts per terabyte guarantees

The cyber resilience capabilities became increasingly important as ransomware attacks escalated. Pure's SafeMode snapshots couldn't be deleted or encrypted by attackers, providing an immutable backup that could restore operations in minutes rather than days or weeks. In a world where ransomware could destroy companies, this wasn't just a feature—it was business insurance.

Sales grew 500 per cent from an undisclosed number in 2016 to 2017 and 100 per cent from 2018 to 2019. The company claims its Q2 2020 performance was a record. This growth wasn't just about selling more storage—it was about fundamentally changing how enterprises consumed and thought about their data infrastructure.

The cultural transformation within Pure was equally important. The company had to evolve from a product-centric organization focused on selling arrays to a service-centric organization focused on customer outcomes. Sales compensation shifted from one-time deals to recurring revenue. Support evolved from break-fix to proactive optimization. Engineering prioritized service reliability over feature velocity.

By the end of 2021, Pure Storage had successfully transformed from a flash array vendor to a storage-as-a-service platform company. The company that had disrupted the storage industry with all-flash arrays was now disrupting it again with a business model that made traditional storage purchasing obsolete. The next phase would test whether Pure could maintain this momentum in an era dominated by AI workloads and exponential data growth.

VIII. Modern Era: AI, Cloud, and Market Position (2021–Present)

The period from 2021 to the present represents Pure Storage's emergence as a critical infrastructure provider for the AI revolution. With FY2025: $3.17B revenue, 11.92% YoY growth, the company achieved a major financial milestone, surpassing $3 billion in total revenue for the first time while delivering strong operating profit. The transformation from flash storage vendor to AI-enabling platform was complete.

The numbers tell a story of consistent execution in a rapidly evolving market. Pure Storage delivered solid fourth quarter and full year results as we fundamentally transform data storage and management for enterprises and hyperscalers. We are enabling customers to modernize legacy storage architectures into enterprise data clouds with Fusion, our most revolutionary advancement this year, which unlocks the full potential of data, while significantly improving operations, data management, and economics for customers.

But the headline achievement of this era was breaking into the hyperscale market. Achieved an industry-first design win with a top-four hyperscaler, bringing Pure's DirectFlash® software into massive-scale environments traditionally dominated by hard disk drives (HDDs). This wasn't just another customer win—it was validation that Pure's technology could compete at the absolute pinnacle of scale and performance.

The hyperscaler breakthrough had been years in the making. Pure's DirectFlash technology, which bypasses traditional SSD controllers to communicate directly with raw NAND flash, delivered performance and efficiency that even the largest cloud providers couldn't ignore. When one of the top four hyperscalers—companies that collectively spend over $100 billion annually on infrastructure—chose Pure, it sent shockwaves through the industry.

Charles Giancarlo captured the significance: "Pure Storage has achieved another industry first in our journey of data storage innovation with a transformational design win for a top-four hyperscaler". The implications were enormous. Hyperscalers had historically built their own storage systems or relied on commodity hardware. For one to choose Pure validated the company's technology at the highest level.

The AI revolution became Pure's primary growth driver. "Pure Storage is uniquely positioned to integrate fragmented data storage environments, which hinders enterprises from easily deploying artificial intelligence, hybrid cloud, and modern application deployment," said Charles Giancarlo, Chairman and CEO, Pure Storage. "At our June Accelerate conference, global customers will see how our latest innovations enable enterprises to adapt to rapid technological change with a platform that fuses data centers and cloud environments."

The November 2024 investment in CoreWeave represented Pure's most aggressive move into the AI ecosystem. AI cloud platform operator CoreWeave has closed a $650 million secondary share sale to investors in a deal insiders claim now values the startup at $23 billion. While the investors were led by Jane Street, Magnetar, Fidelity Management, and Macquarie Capital, both Cisco and Pure Storage took part in the sale, along with others.

Pure Storage® (NYSE: PSTG), the IT pioneer delivering the world's most advanced data storage technologies and services, and CoreWeave, the AI Hyperscaler™, today announced Pure Storage's strategic investment in CoreWeave to accelerate AI cloud services innovation. Alongside the investment, the companies unveiled a strategic partnership, enabling customers to leverage the Pure Storage platform within CoreWeave Cloud. Building on their shared success with some of the world's most advanced AI companies, this collaboration helps to fuel the next generation of AI innovators, driving breakthroughs with CoreWeave's cloud services and the Pure Storage platform.

The CoreWeave partnership wasn't just about investment—it was about positioning Pure at the center of AI infrastructure. "We believe CoreWeave is the eight-figure Evergreen//One deal that Pure announced in the fourth quarter, which management called out as being with 'one of the largest specialized GPU cloud providers for AI.'" CoreWeave, valued at $23 billion, operates massive GPU clusters that power AI training and inference for some of the world's most advanced AI companies.

The strategic value was clear. Enterprises can now select their preferred storage provider within CoreWeave's platform, with Pure Storage offering a proven, high-performance solution already deployed by one of the largest AI labs in the world. Infrastructure at Supercomputing Scale: CoreWeave powers some of the world's largest AI clusters, and its suite of cloud services is designed to support the most demanding AI workloads.

Product innovation during this period focused relentlessly on AI workloads. Released Pure Fusion™ v2, unlocking the ability for customers to operate their storage environments as enterprise data clouds, mirroring the benefits and efficiencies of hyperscaler operations. Fusion represented Pure's vision for autonomous storage—infrastructure that manages itself, scales automatically, and delivers guaranteed outcomes without human intervention.

The FlashBlade platform emerged as Pure's weapon of choice for AI. Unlike traditional storage designed for structured databases, FlashBlade was built from the ground up for unstructured data—the massive datasets that feed AI models. With native object and file protocols, massive parallelism, and the ability to deliver consistent performance at any scale, FlashBlade became the storage platform of choice for AI training clusters.

Strategic partnerships expanded Pure's reach. Announced a strategic collaboration with Kioxia and expanded its partnership with Micron Technology, enabling high-capacity, energy-efficient solutions for hyperscale environments. These partnerships ensured Pure had access to the latest NAND technology while also influencing the development of future flash memory specifically optimized for Pure's architecture.

The subscription model continued its explosive growth. Subscription services ARR exceeded $1.4 billion, representing nearly half of Pure's total revenue. More importantly, these weren't just financial engineering—customers were genuinely embracing storage-as-a-service. Major enterprises deployed hundreds of petabytes under Evergreen//One contracts, treating storage as a utility rather than a capital asset.

Energy efficiency became a critical differentiator in the AI era. "In a world where energy demands are soaring, the power savings of Pure Storage alone make the move from hard disks to Pure technology a smart choice for both hyperscaler and enterprise data centers". Pure's arrays consumed 85% less power than equivalent hard disk systems—a massive advantage when a single AI training cluster could consume as much electricity as a small city.

The company's environmental credentials became a competitive advantage. Recognized by the Science Based Targets Initiative (SBTi) for Pure Storage's Scope 1 and 2 greenhouse gas (GHG) emissions reduction targets as aligned with a 1.5°C trajectory - the most ambitious designation available. In an era where data centers consumed 2% of global electricity, Pure's efficiency wasn't just good business—it was essential for sustainable AI development.

Customer wins in the AI space validated Pure's strategy. OpenAI, Anthropic, and other leading AI labs deployed Pure's storage for their training clusters. A single AI company deployed over 100 petabytes of Pure storage to train large language models. These weren't traditional enterprise deployments—they were massive, technically demanding workloads that pushed the boundaries of what storage systems could deliver.

Financial performance reflected this momentum. Returned approximately $192 million and $374 million in Q4 and FY25, respectively, to stockholders through share repurchases of 3.1 million shares and 6.7 million shares, respectively. The ability to return capital while investing aggressively in R&D demonstrated the strength of Pure's business model.

Competition intensified but Pure maintained its edge. Dell EMC, NetApp, and others launched AI-focused storage products, but they lacked Pure's architectural advantages. Pure's software-defined approach, combined with DirectFlash technology and the Evergreen model, created a moat that traditional vendors couldn't cross.

The market opportunity was staggering. IDC projected that AI infrastructure spending would exceed $300 billion by 2027, with storage representing 20-30% of that total. Pure was positioned to capture a disproportionate share of this growth, particularly in the high-performance segment where its technology advantages were most pronounced.

Looking forward, Pure's roadmap focused on three areas: expanding hyperscale deployments, enabling edge AI with compact, efficient arrays, and delivering autonomous storage operations through AI-powered management. The company that had disrupted storage with flash was now enabling the AI revolution that would transform every industry.

As we stand in 2025, Pure Storage has evolved from a scrappy startup challenging storage giants to an essential infrastructure provider for the AI age. With major hyperscaler wins, deep partnerships with AI leaders like CoreWeave, and a proven subscription model that aligns vendor and customer success, Pure is positioned not just to participate in the AI revolution but to enable it. The flash gamble that seemed crazy in 2009 has become the foundation for humanity's next technological leap.

IX. Playbook: Business & Technology Lessons

The Pure Storage playbook reads like a masterclass in technology disruption, but the real lessons go far deeper than just betting on flash memory. This is a story about timing, business model innovation, and the power of aligned incentives—lessons that apply far beyond the storage industry.

Betting on Technology Transitions Before the Market is Ready

Pure's founding bet on all-flash arrays when flash cost 100x more than hard drives seems prescient in hindsight, but it was actually a calculated gamble based on observable trends. The key insight wasn't that flash would get cheaper—Moore's Law made that inevitable. It was recognizing that the total cost of ownership equation would flip long before the per-gigabyte price reached parity.

Pure understood that enterprises don't buy gigabytes—they buy outcomes. Performance, reliability, power consumption, cooling, rack space, and administrative overhead all factor into the true cost of storage. By 2011, when Pure launched, flash arrays could deliver 10x the performance in 1/10th the space using 1/10th the power of disk arrays. For many workloads, this made flash cheaper even at 10x the per-gigabyte price.

The lesson: Don't wait for cost parity on the primary metric. Look for the inflection point where the total value proposition shifts, and position yourself just ahead of that curve.

The Power of Subscription Models in Hardware Businesses

Pure's Evergreen model transformed storage from a capital expenditure to an operating expense, but more importantly, it aligned vendor and customer incentives for the first time in the industry's history. Traditional storage vendors made money when customers threw away their arrays and bought new ones. Pure made money by keeping customers successful on the same array forever.

This wasn't just a pricing model—it required fundamental architectural changes. Pure designed modular, stateless arrays where every component could be upgraded non-disruptively. They built software that could migrate data transparently between different generations of flash. They created a supply chain that could deliver upgrades efficiently to thousands of customers.

The subscription model also changed Pure's relationship with customers. Instead of quarterly purchase negotiations, Pure had continuous engagement focused on optimization and success. Customer satisfaction scores reached levels unheard of in enterprise storage—not because Pure's support was better, but because the entire model eliminated most support issues.

Building a Disruptive Culture Inside an Established Industry

Pure succeeded where dozens of storage startups failed by building a culture that was both irreverent toward industry orthodoxy and deeply respectful of customer needs. They hired few storage industry veterans, avoiding the "curse of knowledge" that constrains thinking. But they also didn't ignore storage fundamentals—data integrity, availability, and performance are non-negotiable.

The company culture emphasized first principles thinking. When the industry said enterprise storage required dual controllers for redundancy, Pure asked why and designed a triple-controller architecture. When competitors said flash wore out too quickly, Pure developed software that extended flash life beyond what anyone thought possible.

Pure also understood that disrupting an industry requires more than better technology—it requires changing buyer behavior. They made their arrays radically simple to manage, eliminating the need for specialized storage administrators. They offered predictable, transparent pricing when the industry thrived on confusion. They guaranteed outcomes when competitors only promised features.

Customer Success Metrics: 10,000+ Controller Upgrades Delivered

We've delivered over 10,000 controller upgrades, and over 97% of all Pure Storage arrays five years and older are still in service today. These numbers reveal the true disruption: Pure broke the replacement cycle that defined the storage industry.

Traditional storage vendors designed for obsolescence. Support costs escalated after year three, forcing customers into refresh cycles. Pure designed for perpetuity. Every array shipped could theoretically run forever, continuously upgraded and improved. This wasn't just customer-friendly—it was a competitive weapon. Customers who deployed Pure never wanted to go back to the old model.

The operational excellence required to deliver 10,000 non-disruptive upgrades is staggering. Each upgrade requires coordination between customer, support, and logistics. Parts must be shipped, engineers scheduled, and procedures followed perfectly. A single failed upgrade could destroy customer trust. Pure's success rate exceeds 99.9%—a testament to both engineering excellence and operational discipline.

Capital Efficiency: From Venture Funding to Profitability

Pure raised over $470 million in venture capital before going public, a massive sum by 2015 standards. But compared to the capital requirements of disrupting a $30 billion industry, Pure was remarkably efficient. They achieved this through three strategies:

First, Pure focused relentlessly on product-market fit before scaling. They spent two years in stealth perfecting their technology, then grew methodically from 100 customers to 1,000 to 10,000. Each cohort validated the model before Pure invested in the next level of growth.

Second, Pure leveraged software to minimize hardware costs. By achieving 5-to-1 data reduction through deduplication and compression, Pure could deliver competitive capacity with less raw flash. This reduced both customer costs and Pure's inventory requirements.

Third, Pure built a direct sales model that, while expensive initially, created better unit economics at scale. By controlling the customer relationship, Pure captured more value and gathered better feedback for product development.

Product Architecture as Competitive Moat

Pure's architectural decisions created compounding advantages over time. The decision to build proprietary software for flash, rather than adapting disk-based software, enabled optimizations competitors couldn't match. The modular, stateless design enabled the Evergreen model. The DirectFlash technology that bypassed SSD controllers delivered performance and efficiency that attracted hyperscalers.

Each architectural decision reinforced others. Because Pure controlled the entire stack from NAND flash to management software, they could optimize holistically. When a new type of flash emerged, Pure could adapt their software to exploit its characteristics. When customers needed new capabilities, Pure could deliver them through software updates to existing arrays.

This architectural coherence became Pure's deepest moat. Competitors could copy features but not the underlying architecture. They could match performance but not the upgrade model. They could reduce prices but not the total cost of ownership.

Channel Strategy in Enterprise Sales

Pure's go-to-market strategy evolved from pure direct sales to a hybrid model that leveraged partners without losing customer intimacy. Early on, Pure sold directly to maintain control and gather feedback. As they scaled, they added channel partners but maintained direct relationships with key accounts.

The channel strategy reflected Pure's product philosophy: radical simplicity. Partners could sell Pure without deep storage expertise because the products were so simple to deploy and manage. This expanded Pure's addressable market beyond storage specialists to generalist VARs and cloud providers.

Pure also innovated in channel economics. Traditional storage vendors used complex discount structures that obscured true pricing. Pure offered transparent, predictable pricing that partners could easily explain and customers could understand. This built trust and accelerated sales cycles.

The Importance of Customer NPS and Satisfaction

Pure is proud to be a customer-first organization, as evidenced by the highest Net Promoter Score in the industry. Pure's NPS consistently exceeds 80, compared to industry averages below 20. This isn't just a vanity metric—it's a leading indicator of sustainable competitive advantage.

High NPS drives efficient growth. Pure's customer acquisition costs are lower because satisfied customers become references. Retention rates exceed 95% because customers never want to return to the old model. Expansion revenue is predictable because happy customers consolidate more workloads on Pure.

But NPS also reflects something deeper: Pure solved real customer pain. Storage had been a necessary evil—complex, expensive, and frustrating. Pure made it invisible. Arrays that just work, upgrades that don't disrupt, support that prevents problems rather than fixing them. This transformation of customer experience from pain to delight created evangelical customers who became Pure's best salespeople.

The playbook lessons extend beyond Pure Storage. Technology transitions create opportunities, but timing and execution determine winners. Business model innovation can be more powerful than technical innovation. Customer success isn't just good business—it's the ultimate competitive moat. And in enterprise technology, the companies that align their success with their customers' success ultimately win.

X. Analysis & Investment Perspective

From an investment perspective, Pure Storage presents a fascinating study in transformation and value creation. The company has successfully navigated multiple transitions—from startup to public company, from product to platform, from perpetual license to subscription—while maintaining growth and achieving profitability.

Financial Analysis: Revenue Growth, Margins, Cash Flow

Pure's financial trajectory tells a story of disciplined execution. Revenue grew from $6 million in FY2013 to $3.17 billion in FY2025, representing a compound annual growth rate exceeding 70% during the hypergrowth phase and stabilizing at 10-15% as the company matured. This growth rate, while decelerating, remains impressive for a company of Pure's scale in a market growing at mid-single digits.

The margin profile has improved dramatically. Gross margins expanded from the mid-50s during the early years to consistently above 70% today, reflecting the increasing software and services mix. Operating margins turned positive in FY2018 and have steadily improved, reaching double digits while the company continues investing aggressively in R&D.

Cash flow generation has become a strength. Pure generated over $500 million in operating cash flow in FY2025, demonstrating the model's sustainability. The company returns capital to shareholders through buybacks while maintaining the flexibility to invest in growth opportunities like the CoreWeave partnership.

The subscription transition deserves special attention. Subscription ARR exceeds $1.4 billion and grows at 25%+ annually, significantly faster than product revenue. This transition trades near-term revenue recognition for long-term value creation, as subscription customers generate 3-4x the lifetime value of traditional customers.

Competitive Positioning vs. Dell, NetApp, Cloud Providers

Pure occupies a unique position in the storage landscape. Against traditional vendors like Dell EMC and NetApp, Pure has structural advantages: modern architecture, subscription business model, and no legacy customer base to protect. Pure can innovate aggressively while incumbents balance new technology with supporting decades-old systems.

The cloud provider competition is more nuanced. AWS, Azure, and Google Cloud offer storage services with unlimited scale and no upfront investment. However, Pure provides advantages that resonate with enterprises: predictable performance, data sovereignty, fixed costs at scale, and avoiding cloud lock-in. Pure's hybrid cloud capabilities, enhanced by the Portworx acquisition, allow customers to use Pure on-premises and in the cloud with consistent operations.

Pure's win with a top-four hyperscaler validates their technology at the highest level and opens an entirely new market. If Pure can sell to companies that build their own infrastructure, the addressable market expands dramatically.

Total Addressable Market and Growth Drivers

The traditional enterprise storage market totals approximately $50 billion annually, growing at 3-5%. However, Pure's true addressable market is larger and growing faster. The AI infrastructure market could reach $300 billion by 2027, with storage representing 20-30%. The container storage market, addressed through Portworx, grows at 30%+ annually. The hyperscale market, newly accessible through DirectFlash, represents hundreds of billions in annual spending.

Three megatrends drive Pure's growth opportunity:

-

AI/ML Workloads: Every enterprise is building AI capabilities, requiring high-performance storage for training and inference. Pure's FlashBlade platform, optimized for unstructured data and parallel access, is ideally suited for AI workloads.

-

Digital Transformation: As enterprises modernize applications, they need modern infrastructure. Pure's simplicity, reliability, and cloud-like operations model resonates with digital transformation initiatives.

-

Sustainability Requirements: Data centers consume 2% of global electricity. Pure's 85% power reduction versus disk systems becomes a compelling value proposition as enterprises face sustainability mandates and rising energy costs.

Bear Case: Cloud Competition, Hardware Commoditization

The bear case for Pure centers on two concerns. First, cloud providers could eventually offer storage services that match Pure's performance and reliability at lower costs. As cloud providers integrate vertically and design custom silicon, their cost advantages could become insurmountable. If enterprises fully embrace cloud-native architectures, on-premises storage could become obsolete.

Second, flash memory could commoditize, eroding Pure's differentiation. If competitors achieve similar performance and reliability with commodity hardware and open-source software, Pure's premium pricing becomes unsustainable. The hyperscalers' entry into the enterprise market with their internally developed storage systems could accelerate this commoditization.

The bear case also worries about Pure's growth deceleration. Revenue growth has slowed from 50%+ to 10-12%, and further deceleration seems likely as the company scales. If Pure can't reignite growth through new markets or products, the stock's premium valuation becomes hard to justify.

Bull Case: AI Workloads, Subscription Model, Market Share Gains

The bull case sees Pure as essential infrastructure for the AI age. Every AI model requires massive amounts of high-performance storage for training data, checkpoints, and inference. Pure's technology advantages—latency, throughput, and efficiency—matter more for AI than traditional workloads. The CoreWeave partnership and hyperscaler win validate Pure's AI credentials.

The subscription model transformation creates predictable, high-margin revenue streams that the market values highly. As subscription revenue exceeds 50% of total revenue, Pure's valuation multiple should expand to match SaaS comparables rather than hardware companies. The 95%+ retention rates and 120%+ net expansion rates rival the best software companies.

Market share gains continue despite the mature market. Pure takes share from incumbents struggling with legacy architectures and business models. The company's Net Promoter Score above 80 drives efficient customer acquisition and expansion. As enterprises consolidate vendors, Pure's platform breadth—block, file, object, and container storage—positions them to win larger deals.

The hyperscale opportunity could transform Pure's growth trajectory. If Pure captures even 1% of hyperscale infrastructure spending, it would double their addressable market. The DirectFlash technology and energy efficiency advantages position Pure uniquely for this massive opportunity.

Valuation Framework and Comparable Companies

Pure trades at approximately 5.5x forward revenue, premium to traditional storage vendors (Dell at 1x, NetApp at 2.5x) but discount to high-growth software companies (Snowflake at 10x, Datadog at 15x). This positioning reflects Pure's hybrid nature—hardware heritage but software-like business model.

The appropriate valuation framework depends on Pure's successful transition to subscription. If subscription revenue reaches 70%+ with continued 25%+ growth, Pure deserves software multiples. If product revenue remains significant and growth stays at 10-12%, storage hardware multiples are appropriate.

Using a sum-of-the-parts analysis: The subscription business ($1.4B ARR growing 25%) could be worth 8-10x ARR = $11-14B. The product business ($1.8B revenue growing 5%) might be worth 2-3x revenue = $3.6-5.4B. Total enterprise value of $14.6-19.4B suggests 15-30% upside from current levels.

Key Metrics to Watch Going Forward

Investors should monitor five key metrics:

-

Subscription ARR Growth: The rate of subscription growth indicates successful business model transition. Acceleration above 30% would signal stronger competitive position.

-

Hyperscale Revenue: Progress with top-four hyperscaler and additional wins would validate the DirectFlash platform and open massive new markets.

-

AI Customer Wins: Announcements of deployments at leading AI companies provide evidence of Pure's relevance in the highest-growth market segment.

-

Gross Margin Expansion: Continued margin improvement indicates increasing software mix and pricing power.

-

Free Cash Flow Conversion: Improving cash conversion demonstrates the subscription model's economic superiority and funds growth investments.

Pure Storage represents a unique investment opportunity: a proven disruptor with continued growth potential, a successful business model transformation underway, and exposure to the fastest-growing segments of technology infrastructure. While risks exist from cloud competition and market maturation, Pure's technology advantages, customer satisfaction, and strategic positioning in AI infrastructure create multiple paths to value creation.

For long-term fundamental investors, Pure offers an attractive risk-reward profile—a quality company with predictable cash flows and optionality for significant growth acceleration. The company that disrupted storage with flash is now positioned to enable the AI revolution, creating value for customers and shareholders alike.

XI. Epilogue & Lessons for Founders

As we reach the end of Pure Storage's journey from stealth startup to $19 billion market cap leader, the lessons extend far beyond storage technology. This is ultimately a story about courage—the courage to bet against conventional wisdom, to challenge giants, and to build something truly different in an industry that hadn't fundamentally changed in decades.

What Made Pure Storage Successful Where Others Failed

Dozens of storage startups launched between 2000 and 2010. Most are forgotten footnotes. Pure Storage alone achieved escape velocity. The difference wasn't just technology or timing—it was the complete integration of vision, execution, and business model innovation.

Pure understood that disruption requires more than better technology. You need to change the entire system—how customers buy, how they operate, how they think about the category itself. Pure didn't just build better storage; they eliminated the concept of storage refresh cycles. They didn't just offer better support; they designed products that rarely needed support.

The founders' backgrounds proved crucial. Colgrove brought deep storage expertise but wasn't wedded to storage orthodoxy. Hayes understood distributed systems and user experience from the web world. This combination—domain expertise plus outside perspective—appears repeatedly in successful disruption stories.

Pure also benefited from patient capital and aligned investors. Sutter Hill Ventures incubated the company, providing not just money but office space and strategic guidance. Later investors understood the long-term vision and supported the company through years of losses to build a sustainable advantage.

The Importance of Timing in Technology Markets

Pure's timing was exquisite. They started development in 2009 when flash was expensive but improving rapidly. They launched products in 2011 just as enterprises began hitting performance walls with disk arrays. They went public in 2015 before the market cooled. They pivoted to subscription before investors demanded it. They positioned for AI before the ChatGPT explosion.

But this wasn't luck. Pure's founders understood technology adoption cycles. They knew flash prices would follow Moore's Law. They saw enterprises moving to virtualization and cloud, driving demand for higher performance. They recognized that subscription models were inevitable in enterprise software and would eventually spread to infrastructure.

The lesson for founders: Don't time the current market—time the future market. Position yourself where the market will be in 3-5 years, not where it is today. This requires conviction and capital to survive the early years, but the rewards for correct timing are exponential.

Building a Company Culture That Can Compete with Giants

Pure's culture became a competitive weapon. In an industry known for complexity, Pure celebrated simplicity. Where competitors had adversarial customer relationships, Pure aligned incentives. While incumbents protected the status quo, Pure embraced radical change.

The cultural principles that defined Pure:

-

Customer First: Not just satisfaction but delight. Pure measured success by customer outcomes, not product shipments.

-

Simplicity: Complexity is the enemy. Every feature, process, and interaction should be as simple as possible.

-

Innovation: Question everything. Just because storage worked one way for 30 years doesn't mean it should work that way forever.

-

Transparency: No hidden fees, no forced upgrades, no lock-in. Trust is built through transparency.

-

Persistence: Disrupting an industry takes years. Pure maintained focus through lawsuits, competition, and market skepticism.

This culture attracted talent that incumbents couldn't match. The best engineers wanted to build something new, not maintain legacy systems. Sales professionals tired of selling complexity embraced Pure's simplicity. The entire organization aligned around transforming an industry.

Lessons on Fundraising, Scaling, and Going Public

Pure's fundraising journey offers several lessons. First, raise enough capital to achieve clear milestones. Pure's early rounds funded specific objectives: prove the technology, achieve product-market fit, scale sales. Each round de-risked the company and increased valuation.