Prudential Financial: The Rock of American Insurance

I. Introduction & Opening Narrative

The September morning of 2008 felt like watching dominoes fall in slow motion. Lehman Brothers had just collapsed. Merrill Lynch was being swallowed by Bank of America. And then came AIG—the insurance titan that insured everything from airlines to investment banks—teetering on the edge of oblivion. The Federal Reserve and Treasury scrambled to arrange an unprecedented $182 billion bailout package. Without it, AIG's failure would have triggered a cascade of defaults that could have brought down the entire global financial system.

But 240 miles northeast of Washington, in Newark, New Jersey, something remarkable was happening. Inside Prudential Financial's headquarters—a building locals still call "The Rock"—executives were fielding calls from regulators, not for rescue packages, but for reassurance. While AIG's stock plummeted 95% and MetLife scrambled for TARP funds, Prudential stood firm. No bailout needed. No emergency capital raise. Just the quiet confidence of a company that had survived the Civil War, two World Wars, the Spanish Flu, and the Great Depression.

The Rock of Gibraltar—that iconic symbol discovered by a traveling ad agent in the 1890s while his train passed through the Secaucus marshlands—had never seemed more apt. "The Prudential has the strength of Gibraltar" wasn't just a marketing slogan anymore. It was a 133-year-old promise being kept in real-time.

How did this happen? How did a company that began in a Newark basement in 1875, selling burial insurance to immigrants for three cents a week, become the financial fortress that weathered 2008's perfect storm? The answer isn't just about risk management or capital ratios. It's about a series of transformative decisions, near-death experiences, and reinventions that turned The Widows and Orphans Friendly Society into a $1.5 trillion asset management colossus.

This is the story of Prudential Financial—a company that democratized insurance for the American working class, pioneered the demutualization revolution, built one of the world's largest asset managers hiding in plain sight, and somehow emerged from every crisis stronger than before. It's also a cautionary tale about the perils of transformation, featuring billion-dollar acquisition disasters, regulatory battles, and the eternal challenge of disrupting yourself before someone else does.

The journey from John F. Dryden's radical vision of insurance for the masses to today's global financial services giant reveals fundamental truths about American capitalism, the nature of trust at scale, and what it really means to be "rock solid" when everyone else is crumbling.

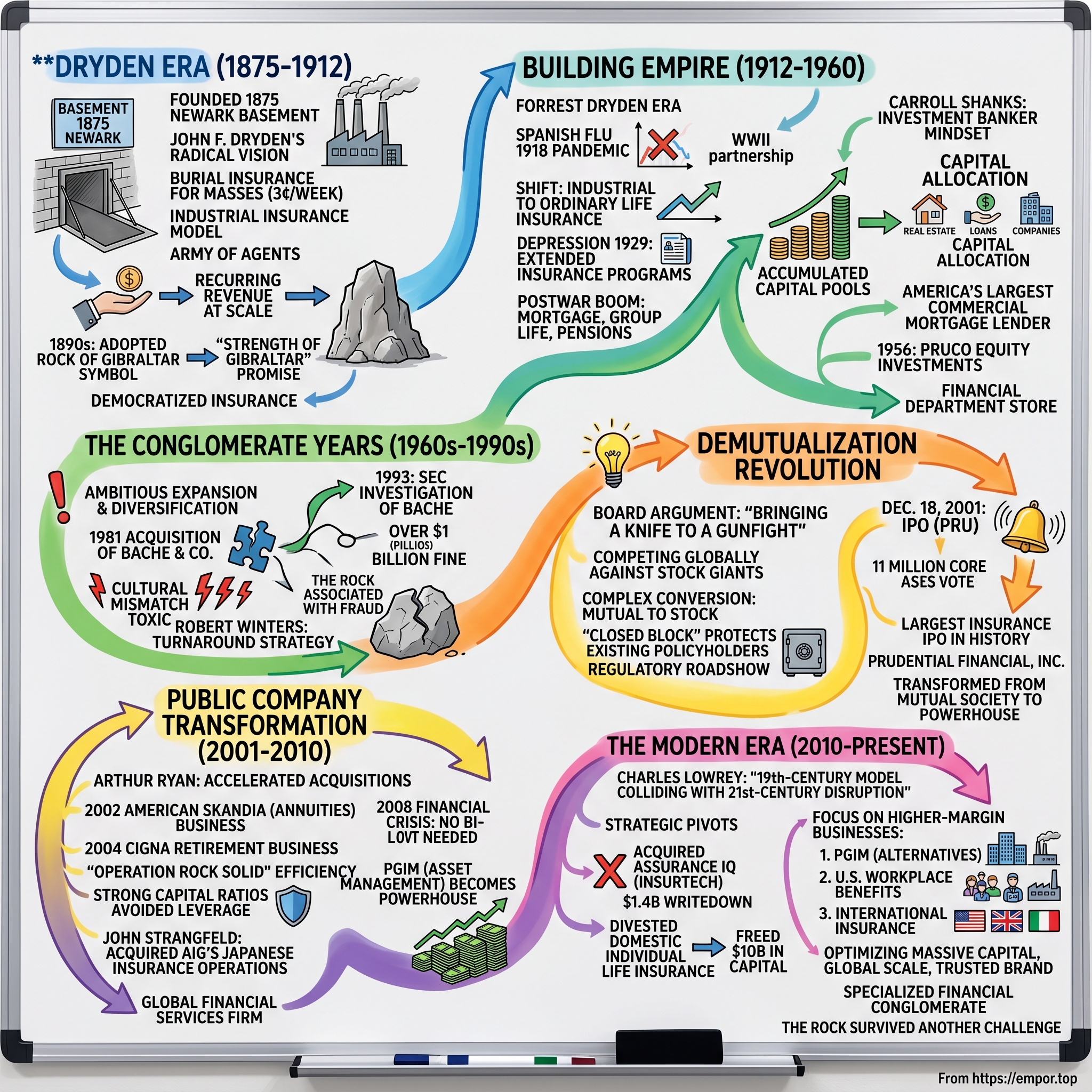

II. The Dryden Era: Industrial Insurance & The American Dream (1875-1912)

The Newark of 1875 was a city of smokestacks and sweat. German and Irish immigrants poured off ships at Ellis Island and headed straight for the factories—leather works, breweries, ironworks—that lined the Passaic River. Death came often and suddenly in this world. A factory accident. Tuberculosis. Childbirth complications. And when it did, families faced a cruel arithmetic: the cost of a decent burial often exceeded a month's wages.

John Fairfield Dryden saw opportunity in this tragedy. Not the vulgar opportunity of exploitation, but something more profound—the chance to provide dignity in death to those who had little in life. The 36-year-old Yale dropout had already failed at several ventures, including a stint selling sewing machines. But his latest obsession, sparked by reading about burial societies in England, would reshape American finance.

With $25,000 in capital—raised mostly from local physicians and clergymen who shared his reformist zeal—Dryden founded The Widows and Orphans Friendly Society in a basement office on Broad Street. The name itself was a statement of purpose. This wasn't about profit; it was about protection for society's most vulnerable.

The product was revolutionary in its simplicity: industrial life insurance, sold in tiny increments, collected weekly at the policyholder's door. Three cents a week bought a $100 death benefit—enough for a coffin, a plot, and a modest service. Five cents got you $165. For context, the average industrial worker earned about $9 weekly. Traditional life insurance companies wouldn't even talk to you unless you could afford annual premiums of $50 or more.

But the real innovation wasn't the product—it was the distribution. Dryden built an army of agents who became fixtures in immigrant neighborhoods. Every Friday, they'd walk their routes, collecting nickels and dimes, marking payment books with rubber stamps. These weren't just salesmen; they were counselors, translators, and sometimes the only financial advisors these families would ever meet. By 1880, Prudential had 500 agents. By 1890, over 2,000.

The agent system created something unprecedented: recurring revenue at massive scale from customers traditional finance ignored. While established insurers like Mutual of New York chased wealthy merchants, Prudential was building relationships with longshoremen, seamstresses, and factory workers. The company processed over 400,000 policies by 1885—each requiring weekly collections, record-keeping, and claims processing without computers, without telephones, often without literate customers.

The operational complexity was staggering. Imagine tracking millions of three-cent payments across dozens of cities, in multiple languages, with 1890s technology. Prudential pioneered industrial-scale record-keeping, developing filing systems and actuarial models that would later influence everything from Social Security to modern database design. They even created their own printing presses to produce the millions of payment books and promotional materials needed.

It was around 1896 when Mortimer Remington, a junior copywriter, was staring out the train window as it crawled through the Secaucus meadows. Through the marsh grass, he glimpsed the massive rock formation rising from the wetlands—a geological anomaly that locals called "Snake Hill" but maps labeled as the Palisades' southern terminus. Something about its solidity, its permanence amidst the swamp, struck him. Back at the office, he pitched it to management: "The Prudential has the strength of Gibraltar."

The Rock of Gibraltar became more than a logo—it was a promise rendered in stone. In an era of frequent bank failures and insurance company collapses, Prudential plastered the image everywhere: payment books, calendars, even dinner plates given as policyholder gifts. Immigrants who couldn't read English could recognize The Rock. It meant their three cents were safe.

By 1900, Prudential had become the largest life insurance company in America by number of policies—over 2 million active contracts. The basement startup now occupied a massive Renaissance Revival headquarters in Newark, complete with marble columns and bronze doors. Dryden himself had transformed from failed entrepreneur to industrial statesman, eventually serving as U.S. Senator from New Jersey while still running Prudential.

But Dryden's most lasting innovation might have been cultural. He insisted Prudential agents dress professionally—jacket and tie, always—even when collecting in tenements. He published annual reports in multiple languages. He opened Prudential's headquarters to public tours, letting immigrant families see the vaults where their money was kept. This wasn't noblesse oblige; it was strategic trust-building at unprecedented scale.

The numbers by 1911, Dryden's final year, were staggering: 10 million policies in force, $3 billion of insurance (roughly $95 billion in today's dollars), agents in every major American city. But more importantly, Prudential had fundamentally changed what insurance meant in America. It was no longer a luxury for the wealthy but a necessity for the working class—the first rung on the ladder to middle-class security.

When Dryden died in November 1911, over 10,000 people attended his funeral in Newark. Many were policyholders who'd never met him but understood what he'd built. His son Forrest would take the reins, inheriting not just a company but a social institution. The question was: could The Rock survive without its founder? The Spanish Flu pandemic and World War I would soon provide brutal tests.

III. Building an Empire: Wars, Depression & Expansion (1912-1960)

Forrest Dryden inherited more than his father's company in 1912—he inherited a social experiment in the midst of transformation. The younger Dryden, educated at Princeton and groomed from birth for leadership, faced an immediate crisis that would define Prudential's next chapter: the industrial insurance model that built the company was already showing cracks.

The problem was mathematical but deeply human. As Prudential's customer base aged, death claims accelerated. Meanwhile, the weekly collection system—sending agents door-to-door for pennies—was becoming economically untenable as cities sprawled and labor costs rose. The average agent visited 400 homes weekly, collecting an average of 15 cents per stop. After salaries, transportation, and administrative costs, margins were evaporating.

Then came 1918. The Spanish Flu didn't just kill people—it killed them in precisely Prudential's demographic: working-age adults in densely packed urban neighborhoods. In Philadelphia alone, Prudential paid out more death claims in October 1918 than in any previous entire year. The company's mortality tables, carefully calibrated over decades, were suddenly useless. Claims exceeded premiums by $3.7 million in 1918—a staggering sum when the entire company's assets were barely $400 million.

Forrest Dryden's response revealed a different leadership style than his father's idealism. Where John Dryden spoke of social mission, Forrest focused on financial engineering. He rapidly raised premiums on new policies, tightened underwriting standards, and most controversially, began aggressively pushing "ordinary" life insurance—larger policies paid monthly or annually rather than weekly.

This shift from industrial to ordinary insurance was Prudential's first great transformation. By 1925, ordinary insurance premiums exceeded industrial for the first time. The company was moving upmarket, following its original immigrant customers as they became middle-class Americans. The Polish factory worker who bought burial insurance in 1900 was now a foreman buying a whole life policy to protect his mortgage.

The 1929 crash tested this evolution. As unemployment hit 25%, millions of Americans stopped paying insurance premiums. Prudential faced a devil's choice: strictly enforce policy lapses and protect capital, or show forbearance and risk insolvency. The company chose a middle path that proved genius—they created "extended insurance" programs, essentially letting policies go dormant rather than canceled, preserving coverage with reduced benefits until policyholders could resume payments.

This wasn't charity—it was brilliant customer retention. When the economy recovered, Prudential had maintained relationships that competitors had severed. By 1935, the company had not only survived but grown, crossing $5 billion in assets while dozens of insurers failed.

World War II accelerated everything. Prudential became the exclusive provider of National Service Life Insurance, administering 4.5 million policies for servicemembers. This government partnership provided steady revenue but more importantly, introduced Prudential to millions of young Americans who would form the backbone of the postwar middle class. When Private Johnson from Iowa came home in 1945, he already had a relationship with The Rock.

The postwar boom transformed American life—and Prudential capitalized on every trend. Suburbanization meant mortgage insurance. Corporate expansion meant group life and pension plans. The GI Bill meant education savings products. Prudential wasn't just selling insurance anymore; it was selling the American Dream, packaged in financial products.

By 1955, Prudential had become something unprecedented: a financial department store. You could buy life insurance, health insurance, annuities, even mortgage loans, all from the same agent who knew your family for generations. The company's advertising evolved from somber reminders of mortality to aspirational lifestyle marketing—happy families in front of colonial homes, always with The Rock subtly visible.

The numbers were extraordinary. Assets grew from $5 billion in 1945 to $12 billion by 1960. The company now employed 60,000 people, operated in every state, and had begun international expansion into Canada and Europe. But the most important change was invisible: Prudential had accumulated enormous pools of capital that needed investment.

This is where Carroll Shanks, who became president in 1946, made his mark. Unlike previous leaders who were insurance men, Shanks thought like an investment banker. He pushed Prudential aggressively into real estate, financing entire planned communities like Los Angeles' Baldwin Hills. The company became America's largest commercial mortgage lender, funding shopping centers, office towers, and apartment complexes that defined postwar suburbia.

But Shanks' boldest move came in 1956: launching PRUCO, a subsidiary specifically designed to invest in equities and private companies. Insurance regulations strictly limited stock investments, but Shanks found loopholes, arguing Prudential needed equity exposure to match its long-term liabilities. Within three years, PRUCO had deployed $500 million into everything from aerospace companies to restaurant chains.

The transformation was complete. The company John Dryden founded to bury the poor had become one of America's largest institutional investors, controlling capital flows that shaped the national economy. When Louis Menagh Jr. took over in 1960, Prudential managed $15 billion in assets and generated investment returns of 4.4%—well above the industry average of 3.8%.

Yet success bred complexity. Prudential now operated dozens of subsidiaries, sold hundreds of products, and faced regulatory oversight from every state plus federal agencies. The simple clarity of The Rock—solid, dependable, unchanging—was harder to maintain when the company itself was shapeshifting into a financial conglomerate. The stage was set for an era of ambitious expansion that would nearly destroy everything previous generations had built.

IV. The Conglomerate Years: Diversification & Near-Death (1960s-1990s)

The executive dining room atop Prudential's Newark headquarters offered a commanding view of Manhattan's skyline in 1964. From this perch, CEO Louis Menagh Jr. could see the future of American finance, and he didn't like Prudential's place in it. While Merrill Lynch was revolutionizing stock trading and Chase Manhattan was pioneering international banking, Prudential remained what one Wall Street analyst dismissively called "your grandfather's insurance company."

Menagh's response would transform Prudential from insurance company to financial conglomerate—and nearly kill it in the process. The journey began innocuously enough with a single product launch in 1964: the first group variable annuity policy, sold to Florida Power & Light's pension plan. Unlike traditional fixed annuities that guaranteed returns, variable annuities invested in stocks and bonds, with returns fluctuating with markets. It was Prudential's first step into the securities business, requiring new licenses, new expertise, and critically, a new appetite for risk.

By 1967, the transformation was accelerating. Prudential surpassed Metropolitan Life as the world's largest insurer with $23.6 billion in assets. But size alone wasn't the goal—Menagh wanted diversification. "Insurance is just one way to manage financial risk," he told the board. "We should be in all of them."

The shopping spree that followed was breathtaking. Prudential acquired a Canadian life insurer, a British property company, Italian and Spanish insurance operations. They launched Prudential Realty Group, developing entire office complexes and shopping centers. They created PruCapital, a investment banking subsidiary. By 1975, Prudential operated in 23 countries, managed $40 billion in assets, and generated more revenue from investments than insurance premiums.

But the deal that defined—and nearly destroyed—this era was the 1981 acquisition of Bache & Co., one of Wall Street's oldest brokerage houses. The price tag of $385 million seemed reasonable for a firm with 3,000 brokers and a century of history. The strategic logic was compelling: combine Prudential's insurance products with Bache's distribution, creating a financial supermarket to rival Merrill Lynch or American Express.

The cultural mismatch was immediate and toxic. Prudential's insurance agents, who built careers on trust and long-term relationships, suddenly found themselves sharing company meetings with Bache brokers who celebrated monthly commission records. The Newark headquarters, where executives ate in the company cafeteria, clashed with Bache's Wall Street culture of expense accounts and Hamptons parties.

George Ball, the former E.F. Hutton president brought in to run the merged operation, embodied the dysfunction. He spent $100 million renovating Bache's offices while Prudential was laying off insurance staff. He hired aggressively from competitors, offering guaranteed bonuses that exceeded what senior Prudential executives earned. Most damningly, he pushed Bache brokers to sell complex limited partnerships in real estate and energy—products that generated huge commissions but would later prove disastrous for investors.

The numbers told the story. Bache lost $48 million in 1989 alone. By 1990, Prudential was forced to cut the investment banking division by two-thirds, essentially admitting defeat. But the real disaster was still unfolding. Those limited partnerships Bache had aggressively sold? They were imploding. Hotels in overbuilt markets. Oil wells that never produced. Real estate developments in savings-and-loan wastelands.

By 1993, the Securities and Exchange Commission had launched a massive investigation into Bache's sales practices. The findings were damning: systematic fraud, forged documents, and a culture that prioritized commissions over client welfare. Prudential agreed to pay a $35 million fine—then the largest in SEC history—plus restitution to 10.7 million policyholders estimated at over $1 billion.

The scandal's impact went beyond money. The Rock—that symbol of stability and trust—was now associated with fraud and greed. State regulators threatened to revoke licenses. Corporate clients canceled group policies. Morale inside Prudential collapsed; employees removed company logos from their cars to avoid confrontation at gas stations.

Robert Winters, who became CEO in 1987, inherited a company in existential crisis. A Harvard MBA who'd spent his entire career at Prudential, Winters understood both the company's traditional strengths and how far it had strayed. His turnaround strategy was radical simplification: sell non-core assets, exit investment banking, and return to insurance and asset management.

The asset sales were brutal but necessary. Prudential's Canadian operations went for $625 million. The European insurance businesses were sold piecemeal. Most symbolically, Prudential Securities—the renamed Bache—was dramatically downsized, focusing solely on retail brokerage rather than investment banking fantasies.

But Winters' most important insight was that Prudential's mutual ownership structure—where policyholders technically owned the company—had become an anachronism that prevented necessary changes. Mutual companies couldn't raise equity capital, couldn't use stock for acquisitions, and couldn't properly incentivize management. While Prudential was stuck with its 19th-century structure, nimbler competitors like AIG and MetLife (which had already demutualized) were eating market share.

The path to demutualization would take seven years and require navigating regulatory mazes in all 50 states. But Winters understood this was Prudential's only path to survival. The conglomerate era had nearly destroyed the company by losing focus. The next chapter would require something even more difficult: fundamentally restructuring a 125-year-old institution while maintaining policyholder trust.

The lessons from this period were seared into Prudential's institutional memory. Diversification without expertise is dangerous. Cultural integration matters more than strategic logic. And most importantly, trust—once broken—takes generations to rebuild. As Prudential prepared for its transformation into a public company, these hard-won insights would prove invaluable.

V. The Demutualization Revolution (1995-2001)

The boardroom argument in March 1998 was getting heated. Around Prudential's polished conference table, directors were grappling with a question that would have seemed heretical to John Dryden: Should policyholders continue to own the company they'd built with their premiums for 123 years?

Richard Simmons, a board member and former president of The Washington Post Company, cut through the rhetoric: "The mutual structure made sense when we were protecting widows and orphans from burial costs. But we're now competing globally against publicly-traded giants with access to unlimited capital. We're bringing a knife to a gunfight."

The numbers backed his frustration. While Prudential struggled to fund growth from retained earnings, publicly-traded competitors were raising billions in capital markets. AIG had used stock to finance acquisitions across Asia. MetLife, which demutualized in 2000, saw its market cap soar to $25 billion. Meanwhile, Prudential couldn't even grant stock options to retain talent—its best executives were being poached with equity packages the mutual company couldn't match.

Robert Winters and his team had been quietly studying demutualization since 1995, hiring McKinsey consultants and forensic accountants to unravel a Gordian knot: How do you convert policyholder ownership rights, accumulated over a century, into shareholder equity? Who gets what? And how do you do it without triggering a policyholder revolt or regulatory backlash?

The complexity was mind-numbing. Prudential had 11 million policyholders, many holding multiple policies purchased across decades. Some had inherited policies from parents or grandparents. Others had let policies lapse but might still have ownership claims. The company estimated it would need to contact 40 million individuals to identify eligible participants.

The solution involved creating something called a "Closed Block"—essentially a financial fortress protecting existing policyholders. The Closed Block would contain $5.6 billion in assets, segregated solely to pay benefits on participating policies issued before demutualization. These policyholders would continue receiving dividends as if nothing had changed. It was financial engineering at its most complex: creating a mutual company inside a stock company.

But the real battle was political. Every state insurance commissioner needed to approve the plan, and many were skeptical. New Jersey's commissioner initially opposed it, arguing policyholders were being shortchanged. Massachusetts threatened to block the conversion unless Prudential guaranteed job levels in Boston. California demanded detailed projections proving policyholders wouldn't be harmed.

The roadshow to convince regulators was exhausting. Arthur Ryan, who succeeded Winters as CEO in 1994, personally visited 47 state capitals, often multiple times. His pitch was consistent: "Demutualization isn't about abandoning our mission—it's about having the tools to fulfill it in the 21st century."

The policyholder vote was another hurdle. Prudential needed approval from two-thirds of voting policyholders—not just a majority. The company spent $100 million on communications, sending personalized packages to every eligible voter explaining their compensation: a mix of cash, stock, and enhanced policy benefits worth an average of $500 per policyholder.

Opposition was fierce but scattered. A group calling itself "Policyholders Against Prudential Demutualization" filed lawsuits claiming the conversion undervalued ownership rights. Consumer advocates argued vulnerable elderly policyholders were being manipulated. Some long-term policyholders felt betrayed—they'd chosen Prudential specifically because it was mutual, prioritizing their interests over Wall Street's.

The breakthrough came in November 2000 when New Jersey finally approved the plan after Prudential agreed to maintain employment levels and contribute $100 million to state health programs. Other states quickly followed. By March 2001, all regulatory approvals were secured.

The policyholder vote was overwhelming: 89% in favor, with over 2 million ballots cast. Many policyholders, particularly younger ones, were excited about receiving stock in a company they'd only known through premium payments. The average policyholder received shares worth $450 plus $150 in cash—not life-changing money, but tangible value from an ownership stake they'd never really understood.

December 18, 2001, was chosen for the conversion—a date that would live in Prudential history. At 12:01 AM, the mutual company ceased to exist. In its place stood Prudential Financial, Inc., a Delaware corporation with publicly traded stock. The IPO that morning raised $3.1 billion, pricing at $27.50 per share—the largest insurance IPO in history.

The stock structure was innovative: regular common stock (PRU) for the core business, and Class B shares linked to the Closed Block, ensuring transparency for legacy policyholders. This dual structure was Prudential's way of maintaining trust—showing policyholders their interests remained protected even as shareholders entered the picture.

Trading opened with fanfare at the New York Stock Exchange. Arthur Ryan rang the opening bell, surrounded by employees and policyholders who'd received stock. By day's end, PRU had risen to $29.40, creating $12 billion in market value. Prudential was suddenly worth more than Ford Motor Company.

But the real test came three months later when Prudential reported its first earnings as a public company. The results were strong: $315 million in net income, beating analyst estimates. More importantly, the company announced its first acquisition as a public entity—American Skandia for $1.2 billion, a deal only possible with public stock as currency.

The demutualization's success went beyond financial metrics. Employee morale surged as stock options finally provided competitive compensation. The company could now recruit top talent from Goldman Sachs and JPMorgan. International expansion accelerated with access to capital markets. The Rock had evolved from a mutual protection society into a modern financial services powerhouse.

Yet something intangible was lost. The mutual structure, for all its limitations, had provided a clear mission: serve policyholders. Now Prudential had to balance policyholder protection, shareholder returns, and employee interests. Every quarterly earnings call would bring new pressures, new trade-offs.

As 2002 began, Prudential faced the future as a fundamentally different institution. The question was whether it could maintain the trust and stability of The Rock while delivering the growth and returns public markets demanded.

VI. Public Company Transformation (2001-2010)

Arthur Ryan stood before Wall Street analysts in February 2002, nine weeks after Prudential's IPO, and made a bold declaration: "We didn't go public to be average. We're going to build the premier financial services franchise in America." The room was skeptical. Prudential's stock had already fallen 15% from its IPO price as investors questioned whether a 127-year-old former mutual could compete with hungry public companies.

Ryan's response was immediate and aggressive. Within six months, he'd deployed $1.2 billion to acquire American Skandia, instantly making Prudential a major player in variable annuities—the fast-growing retirement products that let customers invest in markets while deferring taxes. The deal brought $40 billion in assets and a coveted distribution network of independent financial advisors who'd previously avoided Prudential's stodgy insurance products.

The integration was a masterclass in post-merger execution. Unlike the Bache disaster, Ryan insisted on cultural compatibility from day one. American Skandia employees were offered retention bonuses tied to multi-year performance. Its salesforce was gradually introduced to Prudential products rather than force-fed them. Most importantly, the company maintained Skandia's innovative product development team, which would prove crucial as baby boomers approached retirement.

The acquisition spree continued. In 2004, Prudential bought CIGNA's retirement business for $2.1 billion, adding 2.3 million participants and $43 billion in assets. The strategic logic was compelling: combine CIGNA's corporate relationships with Prudential's product suite to dominate the employer-sponsored retirement market. By 2005, Prudential managed more 401(k) assets than Vanguard.

But Ryan understood that being a public company meant more than just acquisitions. It required operational excellence that quarterly earnings would ruthlessly expose. He launched "Operation Rock Solid," a three-year efficiency program targeting $250 million in annual savings. Back-office functions were consolidated in lower-cost locations. Legacy IT systems, some dating to the 1970s, were finally replaced. The agent force, bloated from the mutual era, was trimmed by 30% while productivity metrics improved.

The results were dramatic. Return on equity rose from 8% in 2002 to 14% by 2006. The stock price doubled to $90. Prudential was suddenly a Wall Street darling, praised for successfully navigating the mutual-to-public transition that had tripped up competitors like John Hancock.

Then came 2008. The financial crisis would test whether Prudential's transformation was real or cosmetic. As Lehman collapsed and AIG imploded, investors assumed all financial institutions were toxic. Prudential's stock crashed from $95 to $15 in six weeks. Credit default swaps on Prudential debt—essentially the cost to insure against bankruptcy—spiked to levels suggesting imminent failure.

But inside Prudential's Newark headquarters, there was quiet confidence rather than panic. The company had learned from past crises. Unlike AIG, Prudential hadn't gorged on subprime mortgage securities or written credit default swaps. Its investment portfolio, while damaged, was conservatively positioned with 85% in investment-grade bonds. Most critically, the company had maintained strong capital ratios, avoiding the leverage that destroyed competitors.

John Strangfeld, who succeeded Ryan as CEO in 2007, faced his trial by fire just months into the job. A Prudential lifer who'd run the investment management division, Strangfeld understood both risk management and market psychology. His response to the crisis was counterintuitive: while competitors hoarded cash, Prudential went shopping.

The crown jewel opportunity came in 2011 when AIG, desperate to repay its government bailout, put its Japanese insurance operations up for sale. The businesses—Star Life and Edison Life—were pristine assets with 2 million customers in the world's second-largest insurance market. The problem was price: AIG wanted $4.8 billion in cash, and credit markets were still frozen.

Strangfeld's solution showcased public company advantages. Prudential issued $1.5 billion in senior notes at attractive rates (investors now viewed Prudential as a safe haven), borrowed $1 billion from banks eager to lend to survivors, and funded the rest from internal cash. The deal closed in February 2011, instantly making Prudential Japan's seventh-largest life insurer.

The acquisition's success validated Prudential's evolution. Integration was smooth—Japanese operations were kept autonomous with local management. The businesses generated $400 million in annual earnings, exceeding projections. Most importantly, it gave Prudential exposure to Japan's massive retirement market just as demographics made annuities essential.

Meanwhile, a quieter transformation was occurring in Prudential's asset management division. PGIM (Prudential Global Investment Management), formed from various investment subsidiaries, was becoming a powerhouse. By 2010, it managed $600 billion—not just Prudential's insurance assets but increasingly third-party money from pension funds and sovereign wealth funds.

The key was expertise in alternative investments. While Vanguard and BlackRock dominated passive indexing, PGIM specialized in complex, high-margin strategies: private credit, real estate equity, emerging market debt. The division's 2010 operating earnings of $800 million exceeded many standalone asset managers. Yet it remained largely invisible, overshadowed by the insurance operations.

Strangfeld recognized PGIM's potential and gave it unprecedented autonomy. The division could hire from Goldman Sachs and Blackstone, paying competitive packages tied to performance. It could launch new strategies without corporate approval if risk parameters were met. This entrepreneurial freedom within a large corporation was unusual but effective—PGIM's assets grew 15% annually, double the industry average.

By 2010's end, Prudential had definitively answered whether a former mutual could thrive as a public company. The stock had recovered to $65. The company generated $3.5 billion in operating earnings. International operations contributed 40% of profits versus 15% pre-demutualization. The Rock had successfully transformed from American insurance company to global financial services firm.

But transformation is never complete. As Prudential entered the 2010s, new challenges emerged: persistently low interest rates that crushed insurance margins, fintech startups attacking distribution models, and regulators designating Prudential a "systemically important financial institution" subject to bank-like oversight. The next decade would require another reinvention.

VII. The Modern Era: Digital Disruption & Strategic Pivots (2010-Present)

The PowerPoint slide on the boardroom screen in August 2019 was stark: a graph showing Prudential's stock price essentially flat since 2014 while the S&P 500 had risen 70%. Charles Lowrey, who'd just become CEO, let the silence linger before speaking: "We're a 19th-century business model colliding with 21st-century disruption. Incremental change isn't enough anymore."

Lowrey, a Mississippi native who'd joined Prudential straight from college, represented a new generation of leadership. Unlike predecessors who'd climbed through insurance operations, he'd built his career in international markets and digital initiatives. His diagnosis was blunt: Prudential was too complex, too U.S.-centric, and too reliant on traditional distribution while InsurTech startups and tech giants circled the industry.

His first major decision would haunt Prudential for years. In September 2019, the company announced it was acquiring Assurance IQ for $2.35 billion—a Seattle-based startup that sold insurance online through a lead-generation model. The price was stunning: 50 times Assurance's revenues for a company that had never turned a profit.

The strategic rationale seemed compelling. Assurance reached 3 million consumers monthly, primarily millennials who'd never speak to traditional insurance agents. Its data analytics could identify customers likely to need life insurance based on web browsing patterns. The platform could theoretically distribute Prudential products to demographics the company had failed to penetrate for decades.

But the cultural collision was immediate and catastrophic. Assurance's employees—engineers in hoodies working from WeWork spaces—couldn't comprehend Prudential's bureaucracy. Simple product integrations that should have taken weeks required months of compliance reviews. Assurance's freewheeling sales culture, where agents made promises the technology couldn't keep, horrified Prudential's legal team.

The pandemic initially masked these problems. As COVID drove insurance demand, Assurance's sales spiked. Lowrey touted early results: "We're reaching 10 million consumers monthly who never would have considered Prudential." But behind the headlines, integration was failing. Assurance's technology couldn't handle Prudential's complex underwriting. Customer acquisition costs were triple projections. Worst of all, the quality of business was terrible—policies lapsed at rates that destroyed profitability.

By 2022, reality was undeniable. Prudential took a $1.4 billion writedown on Assurance. In 2024, the company essentially shut down the operation, absorbing another $900 million loss. The total destruction of value exceeded $2.3 billion—making it Prudential's worst acquisition ever, surpassing even the Bache debacle.

Yet while Assurance grabbed headlines, Lowrey was quietly executing more successful transformations. The decision to split off the domestic individual life insurance business—Prudential's original operation—was revolutionary. This wasn't just divesting a slow-growth unit; it was severing the company's historical core.

The logic was financial engineering at its most sophisticated. Individual life insurance required enormous capital reserves but generated minimal returns in a low-rate environment. By spinning it off, Prudential could free $10 billion in capital for higher-return businesses while removing earnings volatility that public markets despised.

The execution was complex. The separated business needed its own systems, management, and capital structure. Prudential essentially had to create a new insurance company from scratch while maintaining service for 4 million existing policyholders. The 2022 completion freed Prudential to focus on higher-margin businesses: workplace benefits, asset management, and international insurance.

Meanwhile, PGIM was emerging as Prudential's crown jewel. Under David Hunt's leadership, assets under management crossed $1.5 trillion by 2023. The business was generating $3 billion in annual revenue with operating margins exceeding 30%—metrics that standalone asset managers like T. Rowe Price envied.

PGIM's success came from zagging while competitors zigged. As Vanguard and BlackRock drove fees toward zero in passive investing, PGIM doubled down on alternatives: private credit, real estate, infrastructure. These strategies required expertise that couldn't be replicated by algorithms. A $10 billion private credit fund could charge 2% management fees versus 0.05% for an S&P 500 index fund.

The international expansion strategy was also bearing fruit, particularly in emerging markets. Prudential's joint venture in China, launched in 2000, had grown to serve 2 million customers in 100 cities. The Brazilian operation, acquired in 2011, dominated corporate life insurance. By 2023, international operations generated 45% of earnings versus 20% a decade earlier.

But digital transformation remained elusive. Prudential launched countless initiatives—a blockchain experiment for claims processing, an AI chatbot for customer service, partnerships with Amazon for distribution. Most failed to scale. The company's core challenge was unchangeable: insurance is inherently complex, regulated, and relationship-based. You can't disrupt yourself when your business model depends on trust accumulated over decades.

The pandemic accelerated some digital adoption. Virtual sales meetings became standard. Claims processing went paperless. But these were efficiency improvements, not transformation. Prudential still looked fundamentally similar to its pre-digital self, just with better tools.

Lowrey's current strategy acknowledges this reality. Rather than chase disruption, Prudential is optimizing its existing advantages: massive capital, global scale, trusted brand. The company is essentially becoming a specialized financial conglomerate—workplace benefits for U.S. corporations, life insurance for emerging market middle classes, alternative investments for institutional investors.

The numbers suggest it's working. Despite the Assurance disaster, Prudential's stock reached all-time highs in 2024. The company generated $6 billion in operating income. Return on equity exceeded 12%. The Rock had survived another existential challenge, though questions remained about its next century.

VIII. Business Model Deep Dive

To understand Prudential's $1.5 trillion empire, imagine a massive turbine with three distinct engines, each spinning at different speeds but all connected by a central shaft of capital allocation. This isn't the diversified conglomerate chaos of the 1980s—it's a deliberately constructed machine where each component amplifies the others.

The first engine—PGIM—is deceptively simple yet devastatingly effective. While BlackRock and Vanguard fight over basis points in passive indexing, PGIM operates in markets where expertise commands premium pricing. Consider their private credit operation: lending $100 million to a mid-market chemical company at 10% interest, with equity warrants attached. No algorithm can evaluate whether that company's specialized polymers will remain competitive. It requires teams who understand both chemistry and supply chains, who can structure covenants that protect capital while enabling growth.

PGIM manages $1.5 trillion across 40 strategies, but the magic is in the mix. Public fixed income—boring government and corporate bonds—provides scale at $800 billion. But the real profits come from the $300 billion in alternatives: real estate, private credit, infrastructure. A typical pension fund might pay 5 basis points for Treasury management but 200 basis points for private equity. Same dollar managed, 40 times the revenue.

The institutional knowledge moat is extraordinary. PGIM's real estate team has owned the same Manhattan office building through three cycles, understanding how tenant mix affects valuations better than any competitor. Their emerging market debt team has relationships with finance ministers across Africa dating back decades. This isn't replicable by hiring from Goldman Sachs—it's accumulated expertise that compounds over time.

The second engine—U.S. Workplace Benefits—is a distribution masterwork. Prudential provides life, disability, and retirement benefits to 25 million American workers through 100,000 employer relationships. But the genius isn't the products—it's the economics of embedded distribution.

When IBM offers employees life insurance through Prudential, several beautiful things happen. First, underwriting becomes statistical rather than individual—you're insuring IBM's entire workforce, not evaluating each employee. Second, distribution cost approaches zero—no agents, no marketing, just payroll deduction. Third, retention is spectacular—employees rarely switch coverage even when changing jobs, creating decades-long customer relationships.

The numbers are compelling: 60% operating margins on group life insurance versus 15% on individual policies. Customer acquisition cost of $50 per employee versus $2,000 for individual insurance. Lapse rates of 5% annually versus 20% for individual products. It's the insurance equivalent of software-as-a-service: recurring revenue with minimal marginal cost.

The third engine—International Insurance—is a geographic arbitrage play. In Japan, where Prudential is the seventh-largest life insurer, the population is aging rapidly with insufficient retirement savings. Japanese government pensions replace only 40% of working income versus 70% in Europe. This creates massive demand for annuities and supplemental insurance.

But here's what's brilliant: Prudential can manufacture these products using global capital markets while distributing through local partnerships. A Japanese annuity might be backed by U.S. corporate bonds, European real estate, and emerging market debt—diversification impossible for domestic Japanese insurers. Yet it's sold through Japan Post offices, leveraging trust relationships dating centuries.

The margins are exceptional. Japanese customers accept 2% returns on products Prudential funds at 4%, creating 200 basis points of spread with minimal risk. Multiply that across $100 billion in Japanese reserves and you're generating $2 billion in annual spread income before any fees.

These three engines are connected by Prudential's capital allocation framework—perhaps the most sophisticated in insurance. Every dollar of capital is assigned a required return based on risk: 10% for stable workplace benefits, 12% for volatile annuities, 15% for emerging markets. Businesses that consistently miss targets face capital starvation while outperformers get fed.

The framework drives behavior throughout the organization. The annuity team knows that writing too much guaranteed income business will trigger capital charges that destroy returns. The real estate team understands exactly how much leverage they can apply before hitting risk limits. This isn't bureaucracy—it's institutionalized discipline that prevents the excesses that destroyed AIG.

Risk management is equally sophisticated. Prudential runs 10,000 Monte Carlo simulations daily, modeling everything from pandemic mortality to commercial real estate collapse. The company maintains capital ratios assuming 1-in-200-year events occur simultaneously. This conservatism costs returns—Prudential could easily boost ROE by 300 basis points with more leverage—but it's why the company survived 2008 without bailouts.

The regulatory framework adds complexity but also competitive advantage. As a Systemically Important Financial Institution (SIFI), Prudential faces Federal Reserve oversight beyond state insurance regulation. This requires maintaining extra capital, submitting to stress tests, and accepting limitations on dividends and buybacks. Compliance costs exceed $100 million annually.

But SIFI designation is also a moat. Smaller competitors can't afford the regulatory infrastructure. International counterparties prefer dealing with SIFI-designated firms, knowing they're essentially too big to fail. The extra capital requirements that constrain returns also provide stability that attracts conservative institutional clients.

The distribution evolution tells its own story. Prudential still employs 5,000 financial advisors, descendants of those original agents collecting three cents weekly. But they now focus on high-net-worth clients, managing $150 billion in assets. The mass market is served through workplace benefits and digital partnerships. It's segmentation by economics: human touch for profitable complexity, automation for commodity products.

What makes this model resilient is optionality. If interest rates rise, insurance spreads expand. If markets boom, asset management fees surge. If recession hits, workplace benefits become more valuable. Geographic diversity provides similar hedging—Japanese demographics offset U.S. market volatility, emerging markets growth balances developed market saturation.

The challenge is complexity. Prudential is essentially three different companies—asset manager, benefits administrator, global insurer—held together by shared capital and brand. Each requires different skills, metrics, and management. The temptation to simplify through breakup is constant. Activists regularly argue PGIM alone would trade at 15x earnings versus Prudential's conglomerate discount of 8x.

But the synergies are real, if subtle. PGIM manages Prudential's insurance assets at cost, providing stable AUM. Workplace benefits create relationships that feed retail product sales. International operations provide diversification that lowers overall capital requirements. Destroy these connections and you lose competitive advantages that took decades to build.

IX. Playbook: Lessons from The Rock

The conference room in Prudential's Newark headquarters contains a oil painting most visitors ignore—a portrait of John Dryden from 1880, five years after founding the company. Look closely and you'll notice something unusual: his eyes aren't focused on the viewer but somewhere beyond, as if seeing something others couldn't yet perceive. That forward gaze captures something essential about Prudential's survival playbook—the ability to see around corners while others stare at quarterly earnings.

The first lesson is about resilience through diversification, but not the reckless conglomerate-building of the 1980s. Prudential's modern structure is deliberately anti-fragile. When COVID crushed group life insurance claims, PGIM's assets surged from market recovery. When low interest rates destroyed insurance margins, alternative investments generated 15% returns. This isn't luck—it's architected resilience, building businesses with negative correlations.

Consider how Prudential navigated 2008 versus peers. AIG concentrated risk in financial products, creating single-point failure. Prudential spread risk across geographies, products, and time horizons. The company lost money in commercial real estate but made it back in Japanese annuities. This portfolio approach—borrowed from modern finance theory but applied to business units—transforms volatility from enemy to opportunity.

The demutualization playbook deserves its own Harvard Business School case. The key insight wasn't that mutual structure was wrong—it was that ownership structure must match competitive reality. When insurance was local and simple, mutual ownership aligned incentives perfectly. When competition became global and capital-intensive, public ownership became essential. The lesson: sacred cows make the best hamburger.

But execution mattered more than strategy. Prudential spent six years preparing for demutualization, modeling every scenario, negotiating with every stakeholder. Compare that to rushed demutualizations like John Hancock's, which left billions on the table through poor timing and structure. Prudential's patience—waiting until 2001 when markets were receptive—generated $3 billion more in value than rushing would have achieved.

The M&A track record teaches through both success and failure. The American Skandia acquisition worked because Prudential preserved what made the target valuable—its innovation culture and distribution relationships—while providing what it lacked: capital and scale. The Assurance IQ disaster failed because Prudential tried to force integration between incompatible cultures, destroying the startup's agility without capturing its innovation.

The pattern is consistent: successful acquisitions (Japanese insurers, CIGNA retirement) involved buying established businesses in familiar markets. Failures (Bache, Assurance) involved buying into new capabilities or cultures. The playbook lesson: acquire for scale and geography, build for capability. When Prudential needed digital expertise, buying Assurance was lazy strategy. Building internal digital teams would have been slower but sustainable.

Capital discipline separates survivors from casualties in insurance. Prudential's framework—assigning specific return targets to every dollar deployed—seems obvious but is rarely implemented with such rigor. Most insurers manage capital at the corporate level, creating cross-subsidies where bad businesses hide behind good ones. Prudential's granular approach exposes underperformance immediately, forcing hard decisions before problems metastasize.

The 2019 decision to divest domestic individual life insurance exemplifies this discipline. The business wasn't failing—it generated steady profits. But returns were structurally inadequate given capital requirements. Rather than hope for improvement, Prudential surgically removed the unit, redeploying capital to businesses earning twice the returns. This willingness to abandon even core franchises when economics deteriorate is rare but essential.

Building trust at scale might be Prudential's greatest achievement. The Rock of Gibraltar wasn't just marketing—it was promise architecture. Every decision, from agent dress codes to claims processing, reinforced reliability. This trust compounds over generations. A Filipino worker who bought Prudential insurance in 1950 told his son, who told his daughter, who now manages her 401(k) with PGIM. These relationship chains, invisible on financial statements, are Prudential's true moat.

But trust is asymmetric—decades to build, moments to destroy. The Bache scandal nearly shattered The Rock's reputation overnight. Recovery required not just financial restitution but operational transformation: new sales practices, enhanced compliance, cultural change. The playbook lesson: trust must be actively managed like any asset, with investment in systems and culture that prevent erosion.

The regulatory navigation capability is underappreciated. Prudential operates under 50 state insurance regulators, federal oversight as a SIFI, and international supervision in 40 countries. Each regulator has different requirements, political pressures, and interpretation styles. Prudential's ability to satisfy this regulatory matrix while maintaining operational flexibility is masterful.

The key is proactive engagement. Prudential doesn't wait for regulatory problems—it anticipates them. The company maintains full-time staff in every major regulatory center, building relationships during calm periods that prove invaluable during crises. When COVID hit, Prudential could call regulators directly, explaining liquidity positions and getting flexibility on capital requirements. Competitors without these relationships faced harsh restrictions.

The challenge of disruption reveals both strength and weakness. Prudential's response to InsurTech has been schizophrenic—simultaneously dismissive and panicked. The Assurance acquisition showed dangerous FOMO, overpaying for capabilities that weren't truly disruptive. Yet the company's core advantages—capital, trust, regulatory expertise—remain defensible against digital attackers.

The playbook suggests a different approach: embrace disruption at the edges while protecting the core. Use technology to enhance existing advantages rather than chase new business models. PGIM's use of machine learning for credit analysis amplifies human expertise rather than replacing it. Workplace benefits' digital enrollment reduces costs without changing fundamental value proposition. This incremental innovation lacks Silicon Valley glamour but generates real returns.

Finally, leadership succession shows institutional maturity. Prudential has avoided the founder syndrome that cripples many financial institutions. Each CEO brought different capabilities needed for their era: Dryden's vision, Ryan's transformation expertise, Strangfeld's risk management, Lowrey's international perspective. The company develops internal talent over decades, ensuring deep institutional knowledge while bringing fresh perspective.

X. Bear vs. Bull Case & Future Analysis

The Excel model on the analyst's screen at Wellington Management showed two starkly different futures for Prudential. In the bull case, the stock reached $150 by 2027—a double from current levels. The bear case showed $40, implying the market was already overvaluing a melting ice cube. The difference came down to five critical variables that would determine whether The Rock crumbles or continues building for another century.

The Bull Case: The Retirement Crisis Creates a Golden Age

The demographic math is undeniable and terrifying. By 2030, 73 million Baby Boomers will be retired with average 401(k) balances of just $289,000—enough for maybe 10 years of retirement when life expectancy exceeds 85. The retirement savings gap in America alone approaches $7 trillion. This isn't a market opportunity; it's a societal crisis that demands Prudential's exact capabilities.

The company is uniquely positioned to capture this tsunami of demand. Workplace benefits already touch 25 million Americans who trust Prudential with their financial futures. As these workers approach retirement, they need annuities, long-term care insurance, and investment management—all high-margin products Prudential dominates. A mere 10% conversion rate from workplace benefits to retail products would add $50 billion in AUM.

PGIM's growth trajectory could be even more explosive. The alternative investment market is projected to reach $24 trillion by 2028, growing at 15% annually. PGIM's expertise in private credit, real estate, and infrastructure positions it perfectly for this shift. As pension funds and sovereign wealth funds desperately seek yield in a low-return world, PGIM's specialized strategies command premium fees that passive managers can't touch.

The math is compelling: if PGIM grows AUM at 10% annually while maintaining 30 basis point fees, revenue doubles by 2030. Apply a 30% operating margin and 15x multiple (standard for alternative asset managers), and PGIM alone could be worth $150 billion—more than Prudential's entire current market cap.

Asia represents another massive growth vector. The Chinese middle class will expand by 500 million people by 2035, all needing insurance products their government doesn't provide. Prudential's joint venture is already profitable and growing 20% annually. Japan's aging population creates inexhaustible demand for annuities. Southeast Asian markets are just beginning to develop insurance penetration. International operations could generate $5 billion in annual earnings by 2030, up from $2 billion today.

Capital return is the hidden catalyst. With the individual life business divested, Prudential has excess capital approaching $15 billion. The company could buy back 15% of shares annually while maintaining AA credit ratings. This financial engineering alone could drive 10% annual stock returns before any business growth.

The valuation disconnect is glaring. Prudential trades at 8x earnings while pure-play asset managers trade at 15x and specialty insurers at 12x. Simply achieving peer multiples implies 50% upside. If markets finally recognize PGIM's value and award a sum-of-the-parts premium, the stock could double without any fundamental improvement.

The Bear Case: Structural Decline Accelerates

But the bear case is equally compelling. Start with interest rates—the oxygen of insurance profitability. If rates remain below 4%, Prudential faces a slow-motion catastrophe. The company has $300 billion in insurance liabilities with embedded guarantees averaging 4.5%. Every year rates stay low, Prudential must use shareholder capital to fund these promises. The math is brutal: 50 basis points of spread compression costs $1.5 billion annually.

The competitive landscape is deteriorating rapidly. Vanguard entered the annuity market in 2023 with fees 75% below Prudential's. Employer benefits are being commoditized by technology companies like Gusto and Rippling that bundle insurance with payroll. Even PGIM faces pressure as sovereign wealth funds build internal investment capabilities rather than paying external managers.

Digital disruption is accelerating beyond Prudential's ability to respond. Lemonade may be losing money, but it's acquiring customers at 10% of Prudential's cost. Younger consumers don't want human advisors—they want algorithms and apps. Prudential's attempted digital transformation through Assurance IQ proved the company can't buy its way into the future. Building capabilities internally seems equally doomed given cultural antibodies against innovation.

Regulatory overhand could trigger sudden crisis. The Biden administration is reconsidering SIFI designations, potentially subjecting Prudential to bank-like capital requirements that would destroy ROE. Climate change regulations could force massive writedowns on real estate and energy investments. A single catastrophic event—pandemic, financial crisis, cyber attack—could trigger regulatory response that permanently impairs the business model.

The bear math is sobering. If margins compress 200 basis points from competition and regulation, earnings fall to $3 billion. Apply a 6x multiple reflecting secular decline, and the stock is worth $40. The dividend would be cut, triggering further selling from income investors who comprise 60% of the shareholder base.

China could become a trap rather than opportunity. Geopolitical tensions might force Prudential to exit, crystallizing billions in losses. Domestic Chinese insurers are gaining share with government support. The joint venture structure limits control just when Prudential needs to pivot strategies. What looks like growth could become a capital sinkhole.

Even PGIM faces existential threats. The private credit bubble is showing signs of stress, with default rates rising and spreads compressing. When the cycle turns—and it always does—PGIM's alternatives could face massive markdowns. The 2008 playbook of buying distressed assets won't work when Prudential is the distressed seller.

The Verdict: Cautious Optimism with Clear Triggers

The truth likely lies between extremes. Prudential will probably muddle through, generating high single-digit returns for patient investors while disappointing growth seekers. The company's advantages—capital, trust, expertise—remain formidable but eroding. The challenges—disruption, regulation, competition—are real but manageable.

The key variables to watch are specific and measurable. If 10-year Treasury yields stay above 4.5%, the bull case strengthens. If PGIM's flows turn negative for two consecutive quarters, the bear case accelerates. If China operations maintain 15% growth, international expansion validates. If workplace benefits loses major clients to tech competitors, disruption risk crystallizes.

For investors, Prudential represents a classic value-versus-growth dilemma. The stock is statistically cheap with strong capital returns, but the business faces structural headwinds. It's a widow-and-orphan stock in a market that rewards disruptors. The Rock remains solid, but in finance, as in geology, even rocks eventually erode.

XI. Recent News

The recent months have brought a mix of transformation and continuity for Prudential Financial, with the company navigating leadership changes, strategic partnerships, and evolving market dynamics as it enters 2025.

Financial Performance and Market Reception

Prudential's 2024 results demonstrated solid operational performance with net income attributable to Prudential Financial of $2.727 billion or $7.50 per share, up from $2.488 billion or $6.74 per share in 2023. After-tax adjusted operating income reached $4.588 billion or $12.62 per share versus $4.380 billion or $11.88 per share for 2023. The results reflected the company's strategic focus on higher-margin businesses and continued capital efficiency improvements.

The market has responded favorably to Prudential's strategic direction. The stock reached an all-time high closing price of $124.75 on November 27, 2024, reflecting investor confidence in the company's transformation strategy and capital return program. This performance represents a significant recovery from the challenges of previous years and validates management's strategic pivots.

Leadership Transition: The Sullivan Era Begins

In a carefully orchestrated succession, Andrew Sullivan will succeed Charles Lowrey as CEO of Prudential Financial, effective March 31, 2025. Sullivan currently serves as executive vice president and head of international businesses and global investment management. The transition represents continuity rather than disruption, with Lowrey remaining as executive chairman of the board for 18 months to ensure smooth leadership transition.

Sullivan brings deep institutional knowledge and operational expertise to the role. He currently oversees both the company's International Insurance segment and PGIM, the firm's $1.4 trillion global investment management business. Since joining the company in 2011, he has held successive leadership positions, including heading all of the firm's U.S.-based businesses. His background—including service as a Naval Academy graduate and five years in the Navy—brings a disciplined, strategic approach to Prudential's next chapter.

The board's confidence in Sullivan reflects his track record of execution. Michael Todman, Prudential's lead independent director, noted that "Charlie was the principal architect of a complex strategic transformation that has positioned Prudential to be a nimble, dynamic, and high-growth company for years to come." Sullivan inherits a company that has successfully pivoted from its traditional insurance roots toward higher-growth, capital-light businesses.

Strategic Partnerships and Global Expansion

A significant development in early 2025 was Prudential's announcement of a strategic partnership with Dai-ichi Life Holdings focused on product distribution and asset management capabilities. The partnership includes a product distribution agreement in Japan, where PFI would select Dai-ichi's wholly owned subsidiary, The Neo First Life Insurance Company, Ltd., as an exclusive product partner, distributing certain Neo First life products through PFI's Life Planner sales channel.

This partnership exemplifies Prudential's strategy of leveraging existing strengths rather than building from scratch. PGIM would provide asset management services to subsidiaries of Dai-ichi Life Holdings through its PGIM Multi-Asset Solutions business, including management of asset classes such as structured products and private credit. The collaboration allows Prudential to expand its Asian footprint without the capital intensity of organic growth.

Digital Innovation and Distribution Evolution

Prudential continues to evolve its distribution strategy following the Assurance IQ failure. The company is expanding its digital footprint on industry-leading financial planning digital platforms, designed to provide retail advisors with multi-solution modeling and other tech-forward tools. This approach represents a more measured digital transformation—enhancing existing channels rather than attempting wholesale disruption.

The focus has shifted to meeting advisors and customers where they already operate, rather than forcing adoption of proprietary platforms. This pragmatic approach acknowledges the lessons from Assurance IQ while still pursuing necessary modernization.

Organizational Changes and Operational Excellence

Supporting the CEO transition, Caroline Feeney will expand her role to become global head of insurance and retirement, a newly created position overseeing Prudential's market-leading domestic and international insurance and retirement businesses, effective March 31. This organizational restructuring reflects Prudential's continued focus on operational efficiency and clearer business unit accountability.

The company has also seen the retirement of long-serving executives, including Vice Chair Robert Falzon after 42 years with the firm, marking a generational transition in leadership while maintaining institutional continuity through promoted internal talent.

Market Positioning and Investor Sentiment

Analysts remain cautiously optimistic about Prudential's trajectory. The company's focus on capital-light businesses, international expansion, and the massive PGIM asset management platform provides multiple growth vectors. The successful execution of the $11 billion Guaranteed Universal Life reinsurance transaction in 2024 further demonstrates management's commitment to optimizing the business mix.

However, challenges remain. Persistent questions about interest rate sensitivity, competitive pressures in workplace benefits, and the need for continued digital transformation keep some investors wary. The stock's valuation—still trading at a discount to sum-of-the-parts value—suggests the market hasn't fully embraced the transformation story.

Looking Ahead

As Sullivan prepares to take the helm, Prudential stands at an inflection point. The company has successfully navigated its transformation from mutual insurer to public company, survived the 2008 crisis, and pivoted toward higher-growth businesses. The next challenge will be executing on the growth potential while maintaining the operational discipline that has defined The Rock for 150 years.

XII. Links & Resources

Key SEC Filings and Investor Materials - Prudential Financial Investor Relations: investor.prudential.com - 2024 Annual Report (Form 10-K): Available at SEC EDGAR database - Quarterly Earnings Supplements: investor.prudential.com/financials - Proxy Statements and Corporate Governance: investor.prudential.com/governance

Historical Documents and Archives - Prudential Historical Society Archives (Newark, NJ) - "A History of The Prudential Insurance Company of America" by William Carr (1975) - Demutualization Documents (2001): New Jersey Department of Banking and Insurance Archives - Rock of Gibraltar trademark history: U.S. Patent and Trademark Office

Industry Reports and Analysis - A.M. Best Insurance Industry Reports - NAIC Statistical Reports on Life Insurance - Federal Reserve SIFI Designation Documents - McKinsey Global Insurance Reports - Oliver Wyman Insurance Industry Analysis

Books and Long-form Articles - "The Prudential: A Century of Service" by Earl Chapin May and Will Oursler - "From Mutual to Stock: The Demutualization Wave" - Journal of Risk and Insurance - "Industrial Insurance in the United States" by Charles Richmond Henderson - "The Rise of Financial Services Conglomerates" - Harvard Business Review

Regulatory Resources - National Association of Insurance Commissioners (NAIC): naic.org - Federal Reserve Board - Prudential SIFI Materials - New Jersey Department of Banking and Insurance - SEC EDGAR Database - Prudential Filings

Academic Papers - "The Demutualization of Life Insurance Companies" - Wharton Financial Institutions Center - "Industrial Life Insurance and the Cost of Dying Poor" - Journal of Economic History - "Systemic Risk in Insurance: An Analysis of Insurance and Financial Stability" - Geneva Association

Podcast Episodes and Interviews - Masters in Business: Interview with Charles Lowrey (Bloomberg) - Insurance Speak Podcast: Prudential's Digital Transformation - The McKinsey Podcast: Purpose-Driven Transformation at Prudential

PGIM Research and Insights - PGIM Megatrends Series: pgim.com/megatrends - Real Estate Market Outlook: pgim.com/real-estate - Private Credit Perspectives: pgim.com/private-credit

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube