Perimeter Solutions: The Monopoly That Fights Fire With Fire

I. Introduction & Episode Roadmap

Picture this: a massive C-130 Hercules aircraft, engines roaring, banks hard over a California ridgeline engulfed in flames. Its belly doors open and a cascade of vivid red slurry blankets the hillside below, coating trees and brush in a phosphate-based chemical barrier that will not burn. That red powder, the stuff you have seen on every wildfire news broadcast for the past sixty years, comes from one company. Just one. And most people have never heard of it.

Perimeter Solutions, trading on the New York Stock Exchange under the ticker PRM, is a roughly two-billion-dollar public company that holds what is arguably one of the most extraordinary monopoly positions in American industry. It supplies one hundred percent of the long-term fire retardant used by the United States Forest Service, the state of California, and dozens of other agencies around the world. When a wildfire threatens homes in Los Angeles, when crews scramble to protect Yellowstone's ancient forests, when Greek firefighters battle blazes across the Mediterranean, the red chemical line drawn from the sky almost certainly bears the PHOS-CHEK brand name. Perimeter made it, mixed it, loaded it onto the aircraft, and in many cases staffed the base where the plane took off.

What makes this story irresistible from an investor's perspective is not just the monopoly itself, but the cast of characters who recognized its value and brought it to public markets. The company's co-chairmen are Nick Howley, the legendary founder of TransDigm who compounded shareholder returns at roughly thirty percent annually for three decades, and William Thorndike, the author of "The Outsiders," the cult-classic book on capital-allocation genius that Warren Buffett himself endorsed. Rounding out the leadership triumvirate was Tracy Britt Cool, who spent a decade as Buffett's right hand at Berkshire Hathaway before co-founding her own investment firm, Kanbrick. These are not people who stumble into mediocre businesses.

They looked at over two hundred acquisition targets before settling on this one. They chose Perimeter because it checked every box on a five-point framework they had spent years developing: recurring revenue, secular growth tailwinds, a product that costs the customer almost nothing relative to the value it provides, enormous free cash flow generation, and significant opportunity for bolt-on acquisitions. When Nick Howley, a man who turned a collection of unglamorous aerospace parts businesses into a 1,750-times return on equity over three decades, tells you he has found the next TransDigm, that alone is worth paying attention to.

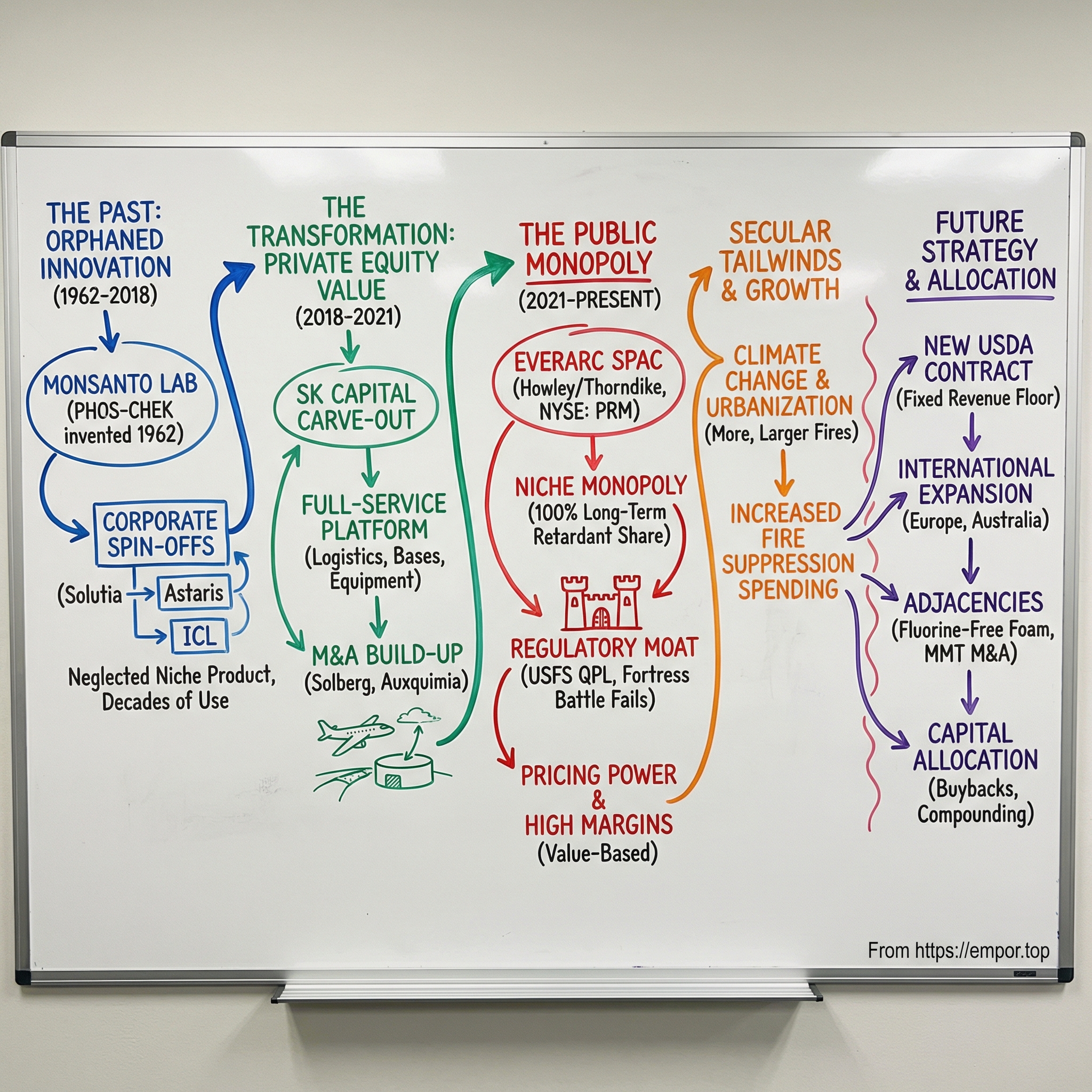

The themes running through this deep dive are ones that any serious long-term investor will find fascinating. We will trace how a niche chemical product invented in a Monsanto laboratory in 1962 drifted through a series of bankrupt companies and corporate spin-offs for four decades, neglected and underloved, until a sharp-eyed private equity firm carved it out and a dream team of capital allocators took it public. We will examine the regulatory moat created by the Forest Service's Qualified Product List, a government-mandated approval process so grueling that no competitor has successfully navigated it at commercial scale. We will wrestle with the uncomfortable question of whether Perimeter's dominance reflects genuine product superiority or something closer to regulatory capture, a question brought into sharp relief by a New York Times investigation and the dramatic rise-and-fall story of Fortress, the only competitor to briefly crack the market in twenty years.

And we will ask why this matters right now. The Los Angeles fires of January 2025 served as a brutal reminder that wildfire risk is not a rural, distant problem anymore. Climate change, drought, and the expansion of communities into the wildland-urban interface have created a structural demand curve for fire suppression that is steep and accelerating. Federal fire suppression spending has compounded at seven percent annually since 1985. California's spending has compounded at ten percent. The five-year trailing average of acres burned in the United States has increased at every five-year measurement interval between 1995 and 2020. Perimeter Solutions sits at the center of this trend with pricing power that would make a pharmaceutical company envious.

This is the story of how a hidden gem became a public-market fortress, and what that means for investors today.

II. The 60-Year Journey: From Monsanto to Monopoly

In 1962, inside a Monsanto laboratory, chemists cracked a problem that had vexed the Forest Service for years. Wildfires had always been fought primarily with water, but water evaporates, and once it is gone the vegetation is just as flammable as before. What the Forest Service needed was something that would stick to trees and brush and chemically prevent combustion even after the moisture had dried. Monsanto's answer was a phosphate-based formulation they branded PHOS-CHEK, a name that would become synonymous with aerial firefighting for the next six decades.

The science is elegant in its simplicity, and worth dwelling on for a moment because it explains why this product has been so difficult to replicate. When ammonium polyphosphate is heated, it decomposes and releases water and ammonia, which are both non-flammable gases. Simultaneously, the phosphate residue forms a char layer on the cellulosic material, essentially coating the wood and plant fibers in a glassy, fire-resistant shell. Think of it like painting every tree and bush with invisible fireproofing that activates precisely when heat arrives.

But the formulation is far more nuanced than that description suggests. The retardant must be viscous enough to cling to vegetation when dropped from thousands of feet, thin enough to flow through aircraft delivery systems without clogging, environmentally compatible enough to avoid poisoning watersheds and aquatic ecosystems, visible enough from the air so that pilots can see where previous drops have landed, and stable enough in storage to last an entire fire season without degrading.

Getting all of these properties right simultaneously, while maintaining consistent performance across wildly different temperatures, altitudes, and vegetation types, is a genuine chemical engineering achievement.

The product was the first phosphate-based fire retardant approved by the United States Forest Service, and that first-mover advantage would prove to be one of the most durable competitive edges in American industry. By 1963, PHOS-CHEK had been qualified for the USDA Forest Service's Qualified Products List, establishing a relationship between product and agency that has now survived for over six decades.

For the next thirty-five years, PHOS-CHEK lived as a small but profitable product line inside Monsanto's sprawling chemical empire. It was never going to move the needle for a company generating billions in agricultural chemicals and, later, genetically modified seeds. But for the fire agencies that depended on it, the product was irreplaceable. The Forest Service built its entire aerial firefighting infrastructure around PHOS-CHEK's specifications: the air tanker bases, the mixing equipment, the loading systems, the deployment protocols. Every base was configured to handle PHOS-CHEK's specific viscosity, mixing ratios, and storage requirements. A quiet but profound lock-in was taking shape, one that nobody in Monsanto's corner offices was paying much attention to.

Then began one of the most convoluted corporate ownership journeys in modern business history. In 1997, as Monsanto pivoted hard toward its agricultural biotechnology future, the company spun off its chemical operations into Solutia Inc., and the PHOS-CHEK brand went along for the ride. This was not a strategic decision about fire retardant; it was a corporate housecleaning exercise. Monsanto wanted to be a life sciences company and needed to shed its legacy chemicals portfolio. In 2000, Astaris LLC, a joint venture focused on phosphorus chemistry, acquired the product line from Solutia. Then in November 2005, Astaris was itself acquired by Israel Chemicals Ltd., or ICL, a Tel Aviv-headquartered conglomerate with operations spanning potash mining in the Negev Desert, bromine extraction from the Dead Sea, and specialty chemicals.

Each transition was messier than the last. Solutia filed for bankruptcy protection in 2003 under the weight of legacy liabilities inherited from Monsanto. Astaris was never a standalone company of consequence; it was a joint venture between two larger chemical companies that treated it as a convenient parking lot for phosphorus-related businesses.

ICL, while financially stable, was a massive global operation where a small American fire retardant business generating perhaps fifty or sixty million dollars in annual revenue was about as far from the corporate center of gravity as it could possibly be. The PHOS-CHEK team in St. Louis found themselves reporting up through layer after layer of management in a company whose CEO was focused on potash pricing in India and bromine demand in China.

There is a particular kind of corporate neglect that is, paradoxically, the best thing that can happen to a niche monopoly. Nobody at ICL's Tel Aviv headquarters was interested in investing in new PHOS-CHEK formulations or expanding the logistics network. But nobody was interested in disrupting it either. The product kept working. The Forest Service kept buying it. The air tanker bases kept mixing it. The approval on the Qualified Product List remained active, uncontested year after year. The brand accumulated sixty years of operational data, safety records, and institutional trust.

Meanwhile, the competitive dynamics were being shaped by this very neglect. No one at any of Perimeter's successive parent companies ever invested in building a sales force to aggressively market the product internationally or develop adjacent product lines. But equally, no competitor could muster the resources to challenge a product that had been the industry standard for decades, was manufactured at scale, and had the full regulatory blessing of the U.S. government.

The product that no corporate parent wanted to invest in was, paradoxically, the product that no customer could live without. Every year that passed without a competitor entering the market, every fire season that ended with PHOS-CHEK performing as expected, added another layer of institutional trust that would be nearly impossible for an upstart to replicate.

It would take a specialty chemicals private equity firm with a very specific playbook to finally see what everyone else had missed.

III. The SK Capital Carve-Out & Build-Up (2018-2021)

SK Capital Partners operates in a niche that most people on Wall Street have never heard of. Founded in New York, the firm specializes exclusively in carving underperforming divisions out of large chemical and specialty materials companies and turning them into standalone growth platforms. They have done this dozens of times: finding the orphaned business unit inside a conglomerate, the one that never gets capital allocation attention, never gets its own sales force, never gets to invest in R&D because the parent company has bigger priorities elsewhere. SK Capital buys these businesses, installs focused management, and lets them run.

On December 8, 2017, SK Capital announced a definitive agreement to acquire ICL's Fire Safety and Oil Additives businesses for approximately one billion dollars. The deal closed on March 28, 2018, and the newly independent company was christened Perimeter Solutions, headquartered in Clayton, Missouri, a suburb of St. Louis.

The investment thesis was straightforward but powerful. SK Capital saw a mission-critical product with no meaningful competition, sold to government customers who could not switch suppliers without risking lives, generating cash flow that was virtually recession-proof because wildfires do not check the economic calendar before igniting.

The product accounted for just two to three percent of total fire suppression costs, a ratio so small that even aggressive price increases barely registered on the customer's overall budget. And the business had been starved of investment for years, meaning there was significant low-hanging fruit in operations, logistics, and product development.

Eddie Goldberg, who had run ICL's fire safety division for nearly two decades, took the helm as CEO. A Cornell-trained chemical engineer, Goldberg had spent his career as a lifer in this business. He knew every air tanker base, every Forest Service procurement officer, every detail of the mixing protocols and deployment logistics. What he had lacked at ICL was autonomy and capital. SK Capital gave him both.

The transformation from orphaned division to focused platform happened rapidly. Between 2019 and 2021, Perimeter executed a series of acquisitions that reshaped the company from a chemical supplier into a full-service fire management operation.

In 2019, the company acquired a group of Idaho-based companies including First Response Fire Rescue, River City Fabrication, and H&S Transport. These were not chemical businesses; they were equipment manufacturers, logistics providers, and service companies that built and maintained the infrastructure at air tanker bases.

This was the strategic insight that separated Perimeter from a simple chemical manufacturer. Instead of just selling retardant and shipping it to a base where government employees would handle the mixing and loading, Perimeter began offering a "full-service" model. The company would staff the base, maintain the equipment, mix the retardant, load the aircraft, and manage the entire supply chain from factory to firebombing run.

Think of it as the difference between selling tires to a NASCAR team and being the entire pit crew. Once you are embedded that deeply in the customer's operation, displacement becomes nearly unthinkable.

The acquisition spree continued with the purchase of Spain-based AUXQUIMIA, a manufacturer of firefighting foams and retardants, and the global SOLBERG foam concentrate business. The SOLBERG deal was particularly strategic because it established Perimeter as the global leader in fluorine-free fire suppressant foam technology, positioning the company ahead of an impending regulatory shift away from PFAS-based foams, the so-called "forever chemicals" that had become an environmental liability for firefighting agencies worldwide.

The international expansion was particularly revealing of SK Capital's ambitions. Under ICL, the fire safety business had been predominantly a North American operation. SK Capital recognized that wildfires are a global phenomenon and that many countries were decades behind the U.S. in aerial firefighting capabilities.

Southern Europe, with its increasingly brutal summer fire seasons in Spain, Portugal, Italy, and Greece, represented a natural expansion market. Australia, which had just endured the catastrophic 2019-2020 Black Summer bushfire season that burned over forty-six million acres and killed over a billion animals, was another obvious target. Each new geography diversified revenue and built the kind of operational knowledge that would be impossible for a newcomer to replicate quickly.

By 2021, Perimeter was no longer the neglected chemical product line that Monsanto had invented and forgotten. It was a vertically integrated fire management platform: chemicals, equipment, logistics, and base operations, all wrapped into a single provider with a brand that had six decades of trust behind it.

The transformation under SK Capital had been remarkable. In just three years, the business had gone from a carve-out of a carve-out of a carve-out to a standalone company with clear strategic focus, expanding margins, a growing international footprint, and a growth trajectory that was entirely organic except for the bolt-on acquisitions that were strengthening the platform.

Now it needed a public-market home and a long-term owner who understood how to allocate capital in a business like this. SK Capital's typical holding period was five to seven years, and by 2021 they had created enough value to attract buyers who would pay a premium for the platform. As it happened, three of the most accomplished capital allocators in America were looking for exactly this kind of opportunity.

IV. The EverArc SPAC: Howley & Thorndike Go Public (2021)

To understand why Perimeter Solutions ended up in the hands of Nick Howley and William Thorndike, you first need to understand EverArc Holdings and the investment philosophy that created it.

Nick Howley is, by any reasonable measure, one of the greatest value creators in the history of American public markets. In 1993, at roughly forty years old, he uprooted his family and three children to Cleveland, Ohio, to take over a collection of unglamorous aerospace component businesses acquired from Imo Industries with backing from private equity firm Kelso & Company. His wife agreed to the move on the condition that they would eventually return to the East Coast. They never did. That business became TransDigm Group, and over the next three decades Howley turned it into one of the most extraordinary compounding machines ever built. The numbers are staggering: a 1,750-times return on original equity invested, a thirty-seven percent compound annual return during the private years from 1993 to 2003, and a thirty-five percent compound return after the 2006 IPO through 2021. As Howley himself observed, those returns were "remarkably evenly distributed" across both periods, proof that the strategy worked at any scale.

Howley's philosophy was deceptively simple, which is precisely what made it so powerful. He focused relentlessly on three value drivers: pricing, cost reduction, and new business development. "You can't fix the market," Howley once explained in an interview. "But what you can do is work on your value drivers in up and down markets."

He sought out businesses that made small, mission-critical components, parts that represented a tiny fraction of the customer's total cost but were absolutely essential to the customer's operations. He then applied what the industry calls "value-based pricing," pricing not based on the cost to manufacture the widget, but on the cost to the customer of not having the widget. In aerospace aftermarkets, where a fifty-dollar part could ground a hundred-million-dollar aircraft, the math was overwhelmingly in TransDigm's favor.

Howley discovered early on that "niche engineered product type businesses underpriced their product" because management teams did not fully appreciate the strength of their own franchises.

Howley was equally distinctive in how he built his management team. He had a "religious belief" in decentralization, keeping corporate headquarters intentionally skeletal, initially just himself, co-founder Doug Peacock, a CFO, and administrative staff, while granting operating units significant autonomy. He deliberately hired people younger than industry norms for senior roles, believing that "people overemphasize experience at the expense of smart, young, and energetic." And he was ruthless about cultural fit: "You got to be quick to fire when somebody doesn't fit in culturally," he said, particularly those he called "politicians" or people who were "not truthful."

William Thorndike came at the same problem from a different angle but arrived at remarkably similar conclusions. A Harvard College and Stanford Business School graduate, Thorndike founded Housatonic Partners in Boston in 1994, a middle-market private equity firm focused on recurring-revenue service businesses. Over more than two decades, he built a strong track record investing across diverse sectors. But Thorndike became famous for something else entirely: his 2012 book "The Outsiders," which profiled eight unconventional CEOs, from Henry Singleton at Teledyne to John Malone at TCI, who dramatically outperformed their peers through disciplined capital allocation rather than operational flashiness. The book originated from a conference presentation Thorndike prepared on Singleton's remarkable tenure, which evolved into a multi-year research project conducted with Harvard Business School students. One striking finding was that half of the Outsider CEOs had engineering degrees, but only two had MBAs, a pattern that suggested technical minds brought a different, more rational approach to capital allocation than traditional business school training. Warren Buffett called it "an outstanding book about CEOs who excel at capital allocation." Forbes described it as "one of the most important business books in America."

The third member of the EverArc founding team was Tracy Britt Cool, who had spent a decade as one of Buffett's most trusted lieutenants at Berkshire Hathaway. During her years at Berkshire, Britt Cool served as a "financial assistant" to Buffett, a deliberately vague title that belied the scope of her responsibilities. She was dispatched to oversee struggling Berkshire subsidiaries, sitting on boards and working directly with management teams to improve operations. In 2020, she co-founded Kanbrick, a long-term investment partnership modeled on the Berkshire approach of acquiring and building great companies in the consumer and industrial sectors. Her involvement in EverArc brought not just capital allocation sophistication but operational turnaround experience.

Together, in 2020, they formed EverArc Holdings as a permanent capital vehicle designed to acquire a single exceptional business and then compound its value over decades. This was not a traditional SPAC designed to flip a deal and move on. The structure was deliberately designed to avoid the conflicts of interest endemic to the SPAC boom: there was no promote, no warrants diluting public shareholders, and the founders committed their own capital alongside investors.

Howley and Thorndike explicitly stated that they aimed to deliver "private equity returns in the public market," which they defined as high-teens annual returns sustained over long periods.

They established five criteria for their target, criteria that reflected the combined wisdom of Howley's TransDigm experience, Thorndike's study of outsider CEOs, and Britt Cool's Berkshire schooling. The business needed recurring and predictable revenue streams. It needed long-term secular growth tailwinds. Its product had to account for a small portion of the customer's overall costs while providing enormous value, the classic Howley formula. It needed to generate significant free cash flow with high returns on tangible capital. And it needed to operate in an industry with significant M&A consolidation opportunity.

EverArc's team evaluated over two hundred potential acquisition targets before landing on Perimeter Solutions. The fit was almost uncanny. On June 16, 2021, they announced the acquisition, and on November 9, 2021, the combined company began trading on the New York Stock Exchange under the symbol PRM at a valuation of approximately two billion dollars.

The business they acquired was generating total revenues of $362 million in 2021, up seven percent year-over-year, with adjusted EBITDA of $141 million. The Fire Safety segment, which Howley and Thorndike saw as the crown jewel, contributed seventy-two percent of revenues and eighty-three percent of EBITDA.

Margins were in the forty percent range at the EBITDA line, and capital expenditures consumed just two percent of revenue, an almost absurdly low reinvestment rate for a business throwing off this much cash.

The return-on-tangible-capital math was extraordinary. The business was generating roughly sixty million dollars of free cash flow on approximately one hundred ten million dollars of tangible capital, translating to a return on tangible capital above fifty percent.

For context, even the best consumer brands in the world rarely sustain returns on tangible capital this high. Perimeter achieved it because the business needed almost no physical capital to operate: the manufacturing was relatively simple, the air tanker base infrastructure was largely owned by the government, and the company's primary assets were its regulatory approvals, its brand, and its institutional knowledge.

Consider the parallel to TransDigm. There, Howley found small aerospace parts that cost a few dollars but were mission-critical for aircraft worth hundreds of millions. Here, fire retardant costs two to three percent of total suppression spending but is literally the difference between a wildfire being contained and an entire community burning to the ground. Both businesses feature captive government customers with high switching costs. Both generate exceptional margins on modest capital bases. And both benefit from pricing power that compounds quietly year after year.

Howley recognized in Perimeter the dynamics that had made TransDigm a compounding machine. The playbook was familiar. The question was whether anyone could challenge it.

V. The Fortress Battle: Defending The Moat (2021-2024)

For nearly two decades, Perimeter Solutions had operated in a competitive vacuum. The Forest Service's Qualified Product List, the regulatory gateway that any company must pass through to sell long-term fire retardant to federal agencies, had functioned as an almost impenetrable barrier. Products submitted for QPL approval must undergo extensive performance, safety, and environmental testing, a process that takes a minimum of two to three years and costs millions of dollars with no guarantee of success. Perimeter's CEO Eddie Goldberg once noted that "hardly a day has passed over the last fifteen years without someone trying to qualify and sell a competing retardant product," yet the company had never faced a commercially viable rival.

Then, in December 2022, a startup called Fortress Fire Retardant Systems achieved what no one else had managed in over twenty years: it got its product added to the QPL.

This was the moment that Perimeter's investors had quietly feared and that short sellers had been waiting for.

Fortress was not a garage operation staffed by dreamers. It was backed by Compass Minerals, a publicly traded company with nearly two billion dollars in annual revenue, deep pockets, and a strategic interest in diversifying beyond road salt and agricultural nutrients. Compass Minerals had an abundance of magnesium chloride from its Great Salt Lake operations in Utah and saw an opportunity to enter a market dominated by a single supplier with aggressive pricing.

Fortress's product was fundamentally different from PHOS-CHEK. Instead of a phosphate-based chemistry, it used a magnesium chloride formulation, a completely different scientific approach to preventing combustion. The chemistry was novel, the raw material supply was abundant and cheap, and the Forest Service, which had been quietly uncomfortable with sole-source dependence on Perimeter for years, was eager to have a qualified alternative.

The QPL approval sent a tremor through Perimeter's investor base. For the first time in the modern era, there was an alternative on the qualified list. Government procurement officials, who had long expressed a desire for competitive bidding to keep costs in check, suddenly had options. Perimeter's monopoly, the very foundation of the investment thesis that Howley and Thorndike had built the entire EverArc acquisition around, appeared to be cracking.

What happened next became one of the most closely watched and, depending on your perspective, one of the most instructive or one of the most troubling competitive battles in the specialty chemicals industry.

Perimeter responded with a multi-pronged counteroffensive that was swift, coordinated, and relentless.

On the public relations front, the company launched a dedicated website arguing that magnesium chloride, Fortress's key ingredient, was a substance better suited for de-icing highways than dropping from aircraft onto burning forests. The messaging was pointed and personal. Perimeter's then-CEO Eddie Goldberg authored a feature article in an industry magazine raising pointed questions about the safety profile and environmental impact of the competing product. The company also filed suit against Compass Minerals' unit, alleging theft of fire-suppression trade secrets, adding a legal dimension to the battle.

Most controversially, Perimeter was instrumental in forming the United Aerial Firefighting Association, or UAFA, a trade group that lobbied federal officials on aerial firefighting standards and safety requirements. The UAFA hired an executive director and a senior policy director in April 2023, and critics questioned whether the association functioned primarily as a lobbying vehicle for Perimeter's competitive interests rather than as a genuine industry body. Perimeter's supporters countered that the UAFA represented a legitimate effort to advocate for safety standards in an industry where product failure could be catastrophic.

Perimeter's technical arguments were not without substance. The company raised legitimate questions about how a magnesium chloride product would interact with the aluminum airframes of the aging air tanker fleet. Chloride compounds are notorious for accelerating corrosion in metals, and the question of whether Fortress's retardant was slowly eating away at the aircraft that deployed it was a genuinely important safety concern, not just competitive mudslinging.

Those concerns proved prescient, or self-fulfilling, depending on one's interpretation. In March 2024, the U.S. Forest Service found significant corrosion in air tankers that had flown with Fortress's magnesium chloride-based retardant. Corrosion in aircraft is not a minor maintenance concern; it is a safety-of-flight issue that can compromise structural integrity.

The Forest Service announced it would not be entering into a new contract with Fortress and effectively removed the product from operational use.

But Perimeter was not finished. When the Forest Service subsequently awarded Fortress a thirteen-million-dollar deal to supply testing materials, Perimeter filed a formal protest with the Government Accountability Office, arguing that the agency had failed to consider Perimeter as an alternative supplier and that the sole-source award to Fortress created an unfair competitive advantage. The protest was ultimately dismissed by the GAO, but the message was unmistakable: Perimeter was willing to fight on every front, regulatory, legal, public relations, and procurement, to ensure that no competitor could establish even a toehold.

The economics of the battle proved decisive. Entering a market with a single, deeply entrenched incumbent is expensive under the best of circumstances. Doing it while simultaneously fending off lawsuits, regulatory challenges, a PR campaign, and now a product safety issue was financially unsustainable.

Though Fortress survived the initial onslaught, Compass Minerals was grappling with its own financial pressures, including debt from previous acquisitions and a declining stock price. The parent company ultimately shuttered the fire retardant arm, citing the need to "improve profitability." It could no longer afford the fight. Fortress had burned through years of investment, endured a bruising regulatory and lobbying battle, and in the end had nothing commercially viable to show for it.

By late 2024, Perimeter was back to one hundred percent market share in long-term fire retardant. As of early 2026, not a single one of Perimeter's historical would-be competitors remains active in the market. Eddie Goldberg's assessment had proven accurate: "Hardly a day has passed over the last fifteen years without someone trying to qualify and sell a competing retardant product. What has remained consistent is that no one other than Perimeter has sold a commercially significant amount of retardant."

The Fortress episode raises a legitimate and uncomfortable question that investors must wrestle with honestly. Did Perimeter's monopoly survive because its product was genuinely superior and safer, or because the company used its incumbent position, its lobbying muscle, its legal resources, and the inherent difficulty of the QPL process to crush a competitor that posed a credible threat?

The answer, as with most things in business, is probably some combination of both. The corrosion issues with Fortress's product were real and documented by the Forest Service itself, not fabricated by Perimeter. But Perimeter's aggressive campaign to discredit the challenger had begun well before the corrosion data emerged, and the speed with which the company mobilized PR, legal, and lobbying resources suggests a playbook that had been prepared long in advance.

For long-term investors, the more important question is forward-looking: what does this episode tell us about the durability of Perimeter's moat? The answer is that the moat may actually be deeper than it appeared before Fortress entered the market. Here was a challenger with real corporate backing, real chemistry, real QPL approval, and genuine government desire for competition. It still could not survive.

The QPL process, the infrastructure requirements, the institutional inertia of government agencies that prioritize reliability over marginal cost savings in life-safety applications, and the incumbent's willingness to fight ferociously, all of these forces conspire to make Perimeter's position extraordinarily difficult to dislodge. The Fortress saga was not evidence of a fragile monopoly; it was, ironically, a stress test that proved just how strong the moat really is.

VI. The Modern Business Model: More Than Just Chemicals

If you think of Perimeter Solutions as a chemical company, you are missing the point. The evolution from chemical supplier to full-service fire management platform is the key strategic insight that makes this business far more defensible than a simple commodity producer.

The Fire Safety segment, which generates the lion's share of revenue and an even larger share of profit, operates what management calls a proprietary "never-fail" service network supporting over one hundred fifty air tanker bases across North America. When a wildfire erupts and the call goes out for aerial retardant drops, there is no time for supply chain negotiations, competitive bidding, or equipment troubleshooting. The retardant needs to be mixed, loaded, and airborne within minutes. Perimeter's full-service model means that at many bases, it is Perimeter employees who are on the ground, maintaining the mixing equipment, managing the chemical inventory, loading the aircraft, and coordinating with pilots and fire management teams.

Consider what this means for competitive dynamics. A would-be competitor does not merely need to develop a qualified fire retardant and get it onto the QPL. It also needs to build or acquire mixing stations, hire and train crews at over one hundred fifty locations, establish a nationwide logistics network for raw material delivery, and convince government agencies to entrust their life-safety operations to an unproven service provider. The full-service model transforms what might be a contestable chemical supply contract into something much closer to an outsourced critical infrastructure operation.

Internationally, Perimeter has been expanding this model into Europe and Australia. The company supplies retardant to firefighting agencies in Italy, Greece, and other Mediterranean countries where wildfire seasons have been growing longer and more severe. Australia, with its devastating bushfire seasons, represents another significant market. Each international expansion deepens the company's institutional knowledge and creates new recurring revenue streams.

Beyond the core retardant business, Perimeter has been building out its product portfolio in several strategic directions. The company acquired the global SOLBERG foam business, making it the leader in fluorine-free fire suppressant technology. This matters enormously because regulatory agencies worldwide are moving aggressively to ban PFAS-based firefighting foams, the per- and polyfluoroalkyl substances that persist indefinitely in the environment and have been linked to health concerns. Perimeter's fourth-generation fluorine-free formulations position the company to capture the transition as military bases, airports, and industrial facilities replace their existing PFAS foam inventories.

The company has also developed Fortify, a fire-resistant gel designed for prevention rather than suppression. While retardant is dropped during active firefighting, Fortify can be applied proactively to structures and vegetation before a fire arrives, creating a protective barrier. This moves Perimeter from the reactive suppression market into the much larger and faster-growing prevention market, particularly relevant as more communities in the wildland-urban interface invest in defensive measures.

Then there is the Specialty Products segment, which produces phosphorus pentasulfide, known as P2S5, at facilities in Sauget, Illinois, and Hürth, Germany. P2S5 is a critical ingredient in the production of ZDDP, or zinc dialkyldithiophosphate, the primary anti-wear additive used in virtually every automotive and industrial lubricant on the planet. This is a stable, no-growth cash cow, the kind of business that will never generate headlines but reliably converts raw materials into cash quarter after quarter. It also offers potential upside from emerging applications in lithium-ion battery technology, where phosphorus compounds are being explored as electrolyte additives.

However, the Specialty Products segment has faced meaningful challenges. The company's tolling facility in Sauget, Illinois, operated by Flexsys Chemical Company, has experienced significant operational and safety events since One Rock Partners purchased the Flexsys assets in 2021. Substantial unplanned downtime has weighed on financial results, and ongoing litigation with Flexsys poses legal and financial risks that investors should monitor.

The combined business model, mission-critical fire management services backed by a regulatory monopoly in retardant plus a stable industrial chemicals cash cow, creates a financial profile that is unusual in the chemicals sector and more closely resembles a high-quality government services contractor or a defense prime. It is a business model built not on technology or brand alone, but on the slow, quiet accumulation of trust in an application where trust is everything.

VII. Secular Tailwinds: Climate, Urbanization & Policy

There is a grim arithmetic at work in the wildfire business. Between 2009 and 2020, Perimeter Solutions' fire retardant volume grew at a ten percent compounded annual growth rate. That number was not driven by market share gains since the company already had all the market share. It was driven by a fundamental increase in the demand for aerial firefighting.

The underlying trends are unmistakable and, from Perimeter's perspective, structurally favorable. The five-year trailing average of acres burned in the United States has increased at every five-year measurement interval between 1995 and 2020.

While the annual number of fire ignitions actually declined by approximately ten percent between 1990 and 2024, the annual area burned increased by nearly sixty percent during the same period. In other words, there are fewer fires, but the fires that do occur are dramatically larger and more destructive.

The reasons are well understood by climate scientists, though the implications are far more dramatic than most investors appreciate. Fire seasons have grown longer by an average of seventy-eight days since the 1970s. Rising temperatures increase evapotranspiration, drying out vegetation and soil faster.

A century of fire suppression policy, well-intentioned but ecologically misguided, allowed fuel loads to accumulate in forests that historically experienced regular, low-intensity burns. And the massive expansion of the wildland-urban interface, where suburban development pushes deeper into fire-prone landscapes, means that fires that once burned harmlessly through uninhabited forests now threaten billions of dollars in property and millions of lives.

The January 2025 Los Angeles fires were a visceral and terrifying demonstration of this convergence. Fires swept through neighborhoods in Pacific Palisades and other communities, destroying thousands of structures and forcing the evacuation of tens of thousands of residents. For most Americans, wildfire had been an abstract problem, something that happened in remote forests. The LA fires brought the reality home: this is not a rural problem anymore. It is an urban and suburban crisis. And when fire arrives at the doorstep of one of America's largest and wealthiest cities, the political and financial response is massive, immediate, and sustained.

The spending data tells the story clearly. Federal fire suppression expenditures have compounded at seven percent annually since 1985, a full four decades of consistent growth through Republican and Democratic administrations, through recessions and booms, through budget battles and government shutdowns. California's fire suppression spending has compounded at an even faster ten percent annually over the same period. Fire suppression spending in California has increased over one hundred fold in four decades.

These are Perimeter's two largest customers, the USDA Forest Service and the state of California, which together accounted for fifty-eight percent of total sales in 2020. From 2013 to 2022, there were an average of 61,410 wildfires annually, impacting an average of 7.2 million acres per year.

In September 2025, Perimeter signed what may prove to be the most significant contract in the company's history: a landmark five-year agreement with the USDA Forest Service. The contract, which was announced by Agriculture Secretary Brooke Rollins, represented a structural shift in the business model.

Under the prior arrangement, Perimeter's revenue was heavily tied to retardant volume, meaning that in years with fewer wildfires, revenue could decline meaningfully. The new contract shifts the revenue mix toward fixed services, essentially paying Perimeter for maintaining its base operations, staffing, and readiness capabilities regardless of fire season severity. The USDA estimated the contract would save taxpayers one hundred fifty-three million dollars over five years while also expanding Perimeter's full-service operations across most or all federal tanker bases.

For investors, this is a critical development. The new contract provides a predictable revenue floor that partially decouples Perimeter's financial results from the inherent volatility of fire seasons.

In 2024, federal agencies dropped 48.6 million gallons of fire retardant. In a quiet year, that figure can drop significantly. The fixed-services component of the new contract dampens that oscillation and gives management more predictable cash flows to work with.

The pricing dynamics are equally compelling and equally controversial. Reporting by The New York Times revealed that as California's firefighting agency sought to protect Los Angeles during the January 2025 fires, the long-term fire retardant being used cost twenty to thirty percent more than it had just four years earlier, substantially outpacing inflation. The U.S. government spent double the amount on fire retardant between 2021 and 2024, resulting in over $250 million paid to Perimeter in the latter year. Part of that increase reflects higher volumes in heavy fire years, but a meaningful portion reflects pricing power.

This is the TransDigm value-based pricing playbook applied to wildfire suppression. Fire retardant accounts for just two to three percent of total suppression costs. When communities are burning and lives are at stake, no government official is going to haggle over the price of retardant that represents a rounding error in the overall firefighting budget. This dynamic allows Perimeter to price its products based on the value they deliver to the customer, not the cost of manufacturing them.

The total addressable market continues to expand. As wildfires increasingly threaten populated areas, investments in aerial firefighting capacity are accelerating. More air tankers require more mobile bases for reloading, and those bases require Perimeter's services. CalFire alone has announced plans to add twenty-one thousand gallons of aerial firefighting capacity over the next four to five years, roughly doubling its current fleet capabilities.

International markets in Europe, Australia, and South America are following similar trajectories. The secular tailwinds behind this business are not cyclical, they are structural, and they are measured in decades, not quarters.

VIII. Financial Performance & Capital Allocation

The financial profile of Perimeter Solutions tells the story of a business firing on all cylinders. The company's trailing twelve-month revenue reached approximately $630 million by the end of 2025, representing a roughly thirteen percent increase over the prior year.

For the nine months ended September 30, 2025, net sales increased sixteen percent to $550.1 million, and adjusted EBITDA grew twenty percent to $295.7 million. The Fire Safety segment delivered a Q3 2025 adjusted EBITDA margin of sixty-five percent, a number that stops most investors in their tracks when they first encounter it.

To put that margin in context: most specialty chemical companies operate with EBITDA margins in the teens to low twenties. Even the best consumer staples businesses, companies like Coca-Cola or Procter & Gamble, operate in the low thirties.

A sixty-five percent segment EBITDA margin is the kind of number you see in software companies or luxury goods brands, not in a business that manufactures chemical products. It reflects the extraordinary pricing power of a monopoly supplier selling a mission-critical product to customers with no alternatives.

The capital efficiency is equally remarkable. Capital expenditures consume just two percent of revenue. The business generates roughly sixty million dollars of free cash flow on approximately one hundred ten million dollars of tangible capital, translating to a return on tangible capital above fifty percent.

This means Perimeter does not need to reinvest heavily to maintain its competitive position. The manufacturing is relatively straightforward, the air tanker base infrastructure is largely government-owned, and the company's true assets, its regulatory approvals, operational knowledge, and customer relationships, require almost no physical capital to sustain.

The balance sheet reflects conservative financial management with dry powder for opportunistic action. As of Q3 2025, the company held $340.6 million in cash and cash equivalents, with a fully undrawn $100 million revolving credit facility.

Net leverage stood at just 1.0 times adjusted EBITDA, down from 1.7 times at the end of 2024. This deleveraging reflects the strong cash generation of the business and gives management significant flexibility for capital deployment.

On capital allocation, management has articulated a clear and distinctly TransDigm-flavored framework: deploy excess cash flow and incremental leverage capacity toward the highest expected internal rate of return combination of M&A, share repurchases, and special dividends. The company evaluates every potential use of capital, whether it is an acquisition, a buyback, or simply sitting on cash, through the lens of expected returns to shareholders.

The company invested seventeen million dollars in acquisitions and capital expenditures in Q3 2025 alone and continues to pursue tuck-in acquisitions in the fire safety space. Share buybacks totaled $14.4 million during fiscal year 2024, representing a smaller but consistent allocation to returning capital to shareholders. Notably, management was buying back shares aggressively during 2022 and 2023 at average prices of $7.65 and $4.21 per share, respectively, prices that look extraordinarily prescient given the stock's subsequent move above twenty-six dollars.

Importantly, management has signaled its willingness to use leverage as a tool for amplifying equity returns. The stated approach is to maintain moderate leverage that "amplifies equity returns" as part of the overall capital strategy. With net leverage having dropped to just 1.0 times EBITDA, there is meaningful capacity to take on additional debt to fund acquisitions or accelerate returns to shareholders. For Howley, this is familiar territory: TransDigm routinely operated at higher leverage ratios and used the resulting cash flow to fund special dividends and acquisitions.

The Specialty Products segment remains the one area of financial friction. Year-to-date adjusted EBITDA for the segment decreased eleven percent to $30.8 million through September 30, 2025, reflecting the operational challenges at the Sauget, Illinois facility and ongoing legal disputes with Flexsys. The Specialty Products business has been the market leader in phosphorus pentasulfide production for more than seventy years, with manufacturing facilities in both the U.S. and Germany, and it continues to generate meaningful cash flow. But the operational issues at Sauget are a genuine overhang that management has not yet fully resolved.

The growth algorithm that management has laid out targets approximately ten to twelve percent annual revenue growth, composed of high-single-digit volume growth in fire retardant plus mid-single-digit pricing gains. Combined with modest margin expansion and disciplined capital allocation, this translates to the "high-teens annual returns" that Howley and Thorndike promised at the time of the EverArc acquisition.

In June 2025, Perimeter opened one of the world's most advanced fire retardant production facilities, a state-of-the-art PHOS-CHEK manufacturing plant at McClellan Park in Sacramento, California, a direct investment in expanding production capacity to meet growing demand from the company's largest customer base. So far, the financial results are tracking broadly in line with the growth framework, and the new USDA contract provides an even stronger foundation for the years ahead.

IX. Porter's Five Forces & Hamilton's Seven Powers

Perimeter Solutions is one of those rare businesses where nearly every element of competitive analysis points in the same direction: overwhelmingly favorable for the incumbent.

Start with the threat of new entrants, which is as close to zero as any industry in public markets. To sell long-term fire retardant to the U.S. government, a company must pass extensive performance, safety, and environmental testing to be added to the Forest Service's Qualified Product List. Perimeter is the only long-term retardant manufacturer to have passed both the laboratory and field tests required for QPL certification. The testing process takes a minimum of two to three years, costs millions of dollars, and there is no guarantee of approval at the end.

But QPL approval is only the beginning. A new entrant would then need to build or acquire mixing infrastructure at over one hundred fifty air tanker bases, hire and train field personnel, establish raw material supply chains, and convince risk-averse government agencies to trust an unproven supplier with life-safety operations. The Fortress episode demonstrated that even with a well-funded corporate parent, a qualified product, and genuine government interest in competition, the practical barriers to sustained market entry are overwhelming.

Supplier bargaining power is moderate. Perimeter depends on phosphate raw materials, but sources from multiple suppliers and does not anticipate supply constraints. The Specialty Products segment involves more complex supply chain relationships, particularly at the Sauget facility, but the Fire Safety business has robust procurement optionality.

Buyer bargaining power is remarkably low despite the fact that Perimeter's largest customers are government agencies, which typically wield significant procurement leverage. The USDA Forest Service and California together account for the majority of sales. Normally, such customer concentration would represent a risk. But in this case, the customers have no viable alternative supplier, and the product they are buying represents just two to three percent of total fire suppression costs. When lives and property are at stake, the switching costs are amplified by many multiples. As one analyst put it, "the risk-reward for the government of switching from a known, effective product to a new supplier just to save a few dollars is just not something that is going to happen."

The threat of substitutes is virtually nonexistent. There is no alternative technology for long-term aerial fire retardant. Water provides temporary suppression but offers no lasting protection. Foam products serve different use cases, primarily structural firefighting and hazardous materials. The phosphate-based retardant technology has over sixty years of proven effectiveness and is deeply integrated into every aspect of aerial firefighting doctrine and infrastructure.

Competitive rivalry, as of early 2026, is literally zero. Perimeter holds one hundred percent market share in long-term fire retardant with no active competitors anywhere in the world at commercial scale.

Turning to Hamilton Helmer's Seven Powers framework, the picture is equally compelling.

Perimeter benefits from strong scale economies through its one-hundred-fifty-plus base network, which creates unit cost advantages that no small-scale entrant could match. Switching costs are the company's most powerful protection: the combination of regulatory certification, infrastructure integration, trained personnel, and the catastrophic risk of failure in a life-safety application makes switching suppliers functionally impossible.

The company possesses a very strong cornered resource in the form of QPL approval, which functions as the ultimate scarce regulatory asset. Branding power is significant since PHOS-CHEK has been synonymous with aerial fire retardant for six decades, representing an institutional reputation that cannot be replicated. And process power, the accumulated operational knowledge of mixing, logistics, and deployment under crisis conditions, represents decades of learning that a new entrant would need to duplicate from scratch.

One of the least discussed moats in investing is simply "doing truly difficult and important things really well." Most investors focus on patents, network effects, or brand equity. But there is an underappreciated category of competitive advantage that comes from mastering a complex, mission-critical operation where failure is unacceptable. Perimeter Solutions is a textbook example. The company does not have a flashy technology moat or a viral network effect. It has something arguably more durable: the accumulated trust of doing an incredibly important job, without fail, for sixty consecutive years.

X. Bull Case vs. Bear Case

The Bull Case

The optimistic thesis for Perimeter Solutions begins with arithmetic that is difficult to argue with. Wildfire severity is a function of climate change, fuel load accumulation, and wildland-urban interface expansion, three trends that are measured in decades and centuries, not business cycles. Volume for fire retardant has compounded at roughly ten percent annually since 2010, and there is no credible scenario in which this trend reverses.

When combined with mid-single-digit pricing gains, which the company has consistently demonstrated, overall revenue growth should average ten to twelve percent annually. This would be consistent with historical performance and management's stated targets.

The new five-year USDA contract adds a predictable revenue floor that dampens fire-season volatility, one of the few legitimate concerns investors had about the business. International expansion in Europe, Australia, and potentially South America represents a large addressable market that Perimeter has barely begun to penetrate. The fluorine-free foam transition and the Fortify prevention gel open adjacent markets worth potentially billions of dollars globally.

The capital-light model generating fifty-percent-plus returns on tangible capital means that incremental growth requires almost no reinvestment, and excess cash flow can be redeployed into acquisitions, buybacks, or special dividends. The management pedigree, Howley, Thorndike, and now CEO Haitham Khouri, a Harvard MBA and former investor at JP Morgan, Oak Hill Capital, and Hound Partners who was appointed in March 2023, provides confidence in disciplined capital allocation.

And crucially, the business is recession-resistant. Wildfires do not care about GDP growth, consumer confidence, or Federal Reserve policy. When the economy contracts, most companies see demand evaporate. Perimeter's demand is driven by physics and climate, not economics.

The Bear Case

The bearish thesis centers on several risks that are real and should not be dismissed, even by the most enthusiastic bulls.

First, and most prominently, is antitrust and political risk. The New York Times published a major investigation examining how Perimeter maintained its monopoly position, detailing the company's aggressive lobbying against Fortress, its formation of the UAFA to influence federal officials, and pricing that has substantially outpaced inflation over the past four years.

The article drew attention from policymakers and the public alike, and its publication coincided with a period of heightened scrutiny of monopoly power across both political parties. Government officials at the USFS and in Congress have expressed concern about sole-source dependence on a single supplier for a critical public safety product. While no formal antitrust action has been initiated, the risk is not zero. A Congressional investigation, a GAO audit of procurement practices, or even sustained media pressure could lead to policy changes designed to encourage competition, such as modified QPL testing requirements or mandated multi-sourcing provisions in future contracts.

Second, regulatory and environmental risk. A 2025 investigation by LAist revealed that Perimeter's fire retardant contains heavy metals including lead, arsenic, cadmium, and chromium, which the company allegedly failed to disclose in public safety documents.

The environmental footprint of dropping tens of millions of gallons of chemical retardant on forests and watersheds every year is under increasing scrutiny from both environmental groups and state regulators. While the Forest Service has historically granted exemptions for retardant use during emergencies, a significant adverse finding on environmental or health impacts could force product reformulation, create liability exposure, or lead to restrictions on aerial retardant deployment in sensitive ecosystems.

Third, fire season volatility, while dampened by the new USDA contract, has not been eliminated. The year 2023 saw just 2.7 million acres burned, down nearly sixty percent from 2022 and the lowest level since 1998. A run of mild fire seasons, which is entirely possible given the year-to-year variability in weather patterns, would still impact the volume-dependent portion of revenue and EBITDA. The new fixed-services component of the USDA contract provides a floor, but it does not eliminate cyclicality entirely.

Fourth, valuation risk. The market has increasingly recognized Perimeter's quality, and the stock has rerated accordingly. UBS upgraded the stock to Buy in early 2025 with a $14 price target, later raising it to $25 as the thesis played out. The premium embedded in the current price assumes continued monopoly-level margins, uninterrupted secular growth, and flawless capital allocation. Any disruption to these assumptions, whether from a successful new competitor, a regulatory intervention, or simply a stretch of quiet fire seasons, could create meaningful downside from elevated multiples. As UBS itself acknowledged in a later downgrade, the stock may face "limited 2026 upside" after a strong run, suggesting that even analysts who believe in the long-term thesis see near-term valuation as full.

The Specialty Products segment, while small relative to Fire Safety, also adds noise and risk to the investment case. The Sauget plant issues and Flexsys litigation are manageable but represent an ongoing operational distraction and a modest drag on earnings that management has yet to fully resolve.

The KPIs That Matter

For investors tracking Perimeter Solutions over time, two metrics matter above all others.

The first is Fire Safety segment adjusted EBITDA margin. This is the single best indicator of pricing power, competitive position, and operational efficiency. At sixty-five percent in Q3 2025, this margin reflects the full economic strength of the monopoly. Any sustained compression would signal either competitive encroachment, regulatory pricing pressure, or cost inflation that the company cannot pass through. As long as this margin holds in the upper fifties to sixties, the franchise is intact.

The second is annual fire retardant volume growth. This captures the secular demand trend independent of pricing. A sustained rate in the high single digits to low double digits confirms that the structural tailwinds of climate change, urbanization, and government spending are continuing to drive adoption. A material and sustained decline below mid-single digits would suggest that either the demand thesis is weakening or that some form of alternative technology is gaining traction.

Together, these two metrics, margin and volume, tell you everything you need to know about whether the Perimeter Solutions investment thesis is playing out as expected.

Perimeter Solutions is a business that inspires strong reactions. Bulls see one of the most defensible franchises in public markets: a government-created monopoly with pricing power, secular growth, and world-class management. Bears see a company that has used its dominant position to crush competitors and gouge taxpayers while facing growing political and environmental scrutiny. The truth, as always, sits somewhere in the complexity between these narratives, and that complexity is what makes PRM one of the most intellectually fascinating companies trading on the New York Stock Exchange today.

XI. The MMT Acquisition: A TransDigm Pivot

In December 2025, Perimeter Solutions announced what was arguably its most surprising and strategically consequential move since going public: the acquisition of Medical Manufacturing Technologies, known as MMT, for $685 million in cash. MMT is a designer, engineer, and manufacturer of custom machinery and aftermarket consumables used in the production of minimally invasive medical devices. In other words, Perimeter Solutions, a fire retardant monopoly, was buying a company that makes equipment for medical device manufacturers.

The deal initially baffled many observers. What does firefighting chemistry have to do with medical device manufacturing? The answer lies not in product synergy but in business model synergy, and specifically in the TransDigm playbook that Nick Howley has spent three decades perfecting.

MMT generates approximately $140 million in annual revenue and roughly $50 million in adjusted EBITDA. The business has several characteristics that mirror Perimeter's core franchise. Its products are mission-critical to its customers, who are major medical device companies that cannot afford production downtime. The equipment is custom-designed for each customer's specific manufacturing process, creating high switching costs.

And the aftermarket consumables, the replacement parts and materials that the machinery requires on an ongoing basis, generate recurring revenue with attractive margins. This is the same razor-and-blade dynamic that makes TransDigm's aerospace aftermarket business so compelling: sell the original equipment at a reasonable price, then capture decades of high-margin aftermarket revenue on proprietary replacement parts.

Perimeter funded the acquisition with $550 million in new senior secured notes due 2034, carrying a coupon of 6.250 percent, plus approximately $185 million in cash on hand. The transaction closed on January 2, 2026, adding the existing senior secured notes due 2029 to a total gross debt load of approximately $1.22 billion. Net leverage on a pro forma basis increased to an estimated 2.5 to 3.0 times combined adjusted EBITDA, a meaningfully higher leverage profile than the 1.0 times where Perimeter stood before the deal.

The strategic logic becomes clearer when you listen to how management describes the acquisition framework. Howley, Thorndike, and CEO Haitham Khouri have stated that they evaluate every use of capital through the lens of expected internal rate of return.

The MMT acquisition is a bet that Perimeter's management team can apply the same value-based pricing, cost optimization, and decentralized operating model to a medical device manufacturing business that they have successfully applied to fire retardant. If they can expand MMT's margins from roughly thirty-five percent to something closer to Perimeter's consolidated fifty percent over time, the deal math works extremely well on a leveraged basis.

The acquisition also introduces meaningful diversification. Fire retardant demand is inherently seasonal, concentrated in the May-through-October wildfire season, and subject to year-to-year variability in fire severity. MMT's medical device manufacturing revenue is not seasonal and is driven by procedure volumes that are largely non-cyclical. Adding a stable, non-seasonal revenue stream could reduce the volatility that has historically made some investors nervous about Perimeter's quarterly results.

Critics of the deal point out that diversification for its own sake is rarely value-creating, and that Perimeter's management team has no demonstrated expertise in medical device manufacturing. The risk of a fire retardant company trying to run a medical equipment business is real, and the history of conglomerate diversification is littered with cautionary tales.

But Howley's track record at TransDigm, where he successfully integrated over one hundred acquisitions across wildly different aerospace product categories, provides at least some basis for confidence. The key question is whether the MMT business model is genuinely analogous to the types of niche monopoly franchises that Howley excels at optimizing, or whether the apparent similarities mask important differences that will only become visible once the integration is underway.

XII. Strategic Questions & Lessons

Every great business story raises questions that extend beyond the specific company under examination. Perimeter Solutions is no exception. Here are the questions that this deep dive leaves us wrestling with.

How should society value monopoly in life-safety applications?

The traditional economic argument against monopoly is that it leads to higher prices, lower quality, and reduced innovation. Perimeter Solutions challenges this framework in uncomfortable ways. The company charges prices that have outpaced inflation by a significant margin. But the product works, consistently, in conditions where failure means people die. There has never been a documented case of PHOS-CHEK failing to perform as specified when properly applied. For sixty years, the product has done exactly what it is supposed to do. Is a monopoly that charges premium prices but delivers flawless performance in life-safety applications actually bad for consumers? Or is the attempt to introduce competition, which inevitably involves testing unproven products in conditions where failure is catastrophic, the greater risk?

This is not an easy question, and reasonable people disagree. The Fortress episode illustrates the tension perfectly. The government genuinely wanted competition and actively supported a challenger. The challenger's product turned out to have a serious safety issue.

Perimeter's defenders point to this as vindication. Perimeter's critics point out that the incumbent had every incentive to ensure the challenger failed and deployed considerable resources to that end. The truth probably lies in the middle, and the policy implications are genuinely difficult.

What does Perimeter tell us about the limits of disruption?

Silicon Valley has spent two decades promising that every industry can be disrupted by a startup with a better mousetrap and a pitch deck. Perimeter Solutions is a powerful counterexample. This is a business where the incumbent advantage is so deeply embedded in regulatory structures, operational infrastructure, institutional trust, and sixty years of accumulated knowledge that disruption in the conventional sense is nearly impossible. The barriers are not technological, they are systemic. A new entrant needs not just a better product but the willingness and resources to fight a multi-year war across regulatory, legal, political, and commercial fronts simultaneously, all while spending tens of millions of dollars with no revenue to show for it.

There are more businesses like this than most people realize. Water treatment chemicals, aviation maintenance compounds, military specification lubricants, pharmaceutical excipients, all of these are industries where regulatory qualification, institutional trust, and the catastrophic cost of failure create moats that are nearly impossible to cross.

Investors who focus exclusively on technology moats and network effects are missing an entire category of durable competitive advantage.

What is the right framework for pricing a product that saves lives?

Perimeter's pricing strategy is the application of value-based pricing to a government-purchased, life-safety product. The company charges what the product is worth to the customer, not what it costs to produce. Given that fire retardant represents just two to three percent of total suppression costs and that the alternative to effective retardant is homes, forests, and potentially lives destroyed, the "value" is almost infinitely large relative to the price charged.

This creates genuine ethical tension. On one hand, Perimeter is a for-profit company with a fiduciary obligation to its shareholders, and its pricing strategy is rational, legal, and widely practiced across industries. On the other hand, the U.S. government is spending taxpayer dollars on a product where it has no meaningful negotiating leverage because there is only one supplier.

The New York Times investigation highlighted this tension, and it is unlikely to go away. As wildfire costs escalate and public scrutiny of government spending intensifies, Perimeter's pricing practices will remain a lightning rod.

What does the stock price journey tell us about market efficiency?

Perimeter Solutions traded on the NYSE for over two years, from November 2021 to late 2023, during which the stock declined from roughly twelve dollars to under five dollars. During that period, everything that makes the company valuable today was already true: the monopoly position, the regulatory moat, the secular growth tailwinds, the management pedigree, the TransDigm playbook.

Nothing fundamental had changed. What changed was sentiment: SPACs were out of fashion, a light fire season in 2023 spooked volume-sensitive investors, and the stock languished in relative obscurity.

Then the LA fires hit in January 2025, and suddenly everyone noticed. The stock re-rated from under ten dollars to over twenty-six dollars in roughly twelve months. The company was buying back shares aggressively at four and five dollars, management was purchasing at seven and eight dollars, and the public market did not figure it out until dramatic headline events made the thesis impossible to ignore.

For students of market efficiency, this is a fascinating case study. The information was entirely public. The management team was not subtle about their strategy. The competitive dynamics were well-documented. And yet the market needed a burning city on live television to recognize what was hiding in plain sight.

What are the lessons for capital allocation?

The Perimeter Solutions story offers several lessons that transcend the specific company.

First, look for neglected assets inside conglomerates. The PHOS-CHEK brand spent four decades being passed from one corporate parent to another, each of which treated it as a rounding error. SK Capital recognized that corporate neglect had preserved the franchise while starving it of the investment needed to unlock its full potential.

Some of the best investments in history have been the orphaned divisions of large companies, businesses that are too small to matter to the parent but too good to be mediocre once they have focused ownership.

Second, understand the difference between a chemical company and a service platform. Perimeter's transformation from retardant supplier to full-service fire management provider is a masterclass in vertical integration. By embedding itself in the customer's operations, the company made displacement orders of magnitude harder than simply beating the chemical formulation. The pit crew analogy that management uses is apt: once you are the entire pit crew, the conversation is no longer about who makes the best tires.

Third, regulatory moats are underappreciated and undervalued. Investors spend enormous energy analyzing technology moats, brand moats, and network effects. They spend far less time studying regulatory moats, which in many cases are more durable than any of these. The QPL approval process, the government's institutional preference for proven suppliers in life-safety applications, and the multi-year, multi-million-dollar cost of challenging an incumbent's regulatory position create barriers that are arguably harder to overcome than any patent or proprietary algorithm.

And fourth, management quality matters enormously in monopoly businesses. A monopoly is a powerful but fragile thing. Managed well, it compounds value for decades. Managed poorly, it invites regulatory intervention, competitive challenge, and public backlash. Perimeter's management team, with its deep roots in the TransDigm and Berkshire Hathaway traditions of disciplined capital allocation, has so far navigated this balance with considerable skill. Whether they continue to do so, particularly as public scrutiny intensifies and the MMT acquisition tests their ability to operate outside their core expertise, remains the central question for long-term investors.

XIII. Further Reading

For listeners and readers who want to go deeper on the topics covered in this episode, here are some recommended resources.

On Perimeter Solutions specifically, the company's investor relations page at ir.perimeter-solutions.com contains all SEC filings, earnings transcripts, and press releases. The Q3 2025 earnings call transcript is particularly valuable for understanding management's strategic framework and the USDA contract details. The New York Times investigation into fire retardant pricing and the competitive landscape provides the most comprehensive critical examination of Perimeter's monopoly position published to date. The LAist investigation into heavy metals in fire retardant offers an important counterpoint on environmental and safety concerns.

On the SPAC and EverArc structure, the original EverArc prospectus filed with the SEC contains detailed descriptions of the investment criteria and management team background. Nick Howley's interviews and presentations on TransDigm's strategy are essential reading for understanding the value-based pricing and capital allocation frameworks that Perimeter's leadership applies to this business.

On the broader wildfire landscape, the National Interagency Fire Center at nifc.gov maintains comprehensive data on acres burned, suppression costs, and fire statistics. The Congressional Research Service has published multiple reports on federal wildfire policy and spending trends. CalFire's annual reports document the acceleration in California-specific firefighting expenditures that represent a significant portion of Perimeter's revenue.

On the competitive dynamics and regulatory framework, the Forest Service's Qualified Products List documentation explains the testing and approval process that creates Perimeter's regulatory moat. The Reason Foundation published an analysis in August 2025 examining how regulatory structures in the fire retardant industry may have contributed to the lack of competition. Bloomberg Law covered the USDA contract award in detail, including the estimated $1.3 billion total value and the political dynamics surrounding the procurement.

On the management team and investment philosophy, William Thorndike's "The Outsiders" remains the definitive text on the capital allocation approach that informs Perimeter's strategy. Howley's various industry presentations on TransDigm's operating philosophy, particularly his discussions of value-based pricing, decentralization, and the "three value drivers" framework, provide the intellectual foundation for understanding how Perimeter's leadership thinks about value creation.

Tracy Britt Cool's public discussions of the Kanbrick investment philosophy offer additional perspective on the long-term ownership approach that EverArc was designed to embody.

The Perimeter Solutions story is still being written. The company's Q4 and full-year 2025 earnings are scheduled for February 26, 2026, just days from the date of this article. Those results will provide the first look at how the new USDA contract is flowing through the financials and whether the company's growth algorithm is tracking as management has projected. The MMT acquisition, which closed just weeks ago, will begin appearing in financial results in the coming quarters, offering the first real-world data on whether the TransDigm playbook can be successfully applied to a medical device manufacturing business. And the broader wildfire landscape continues to evolve in ways that are impossible to predict with precision but directionally favorable for the company at the center of it all.

RSS Feed