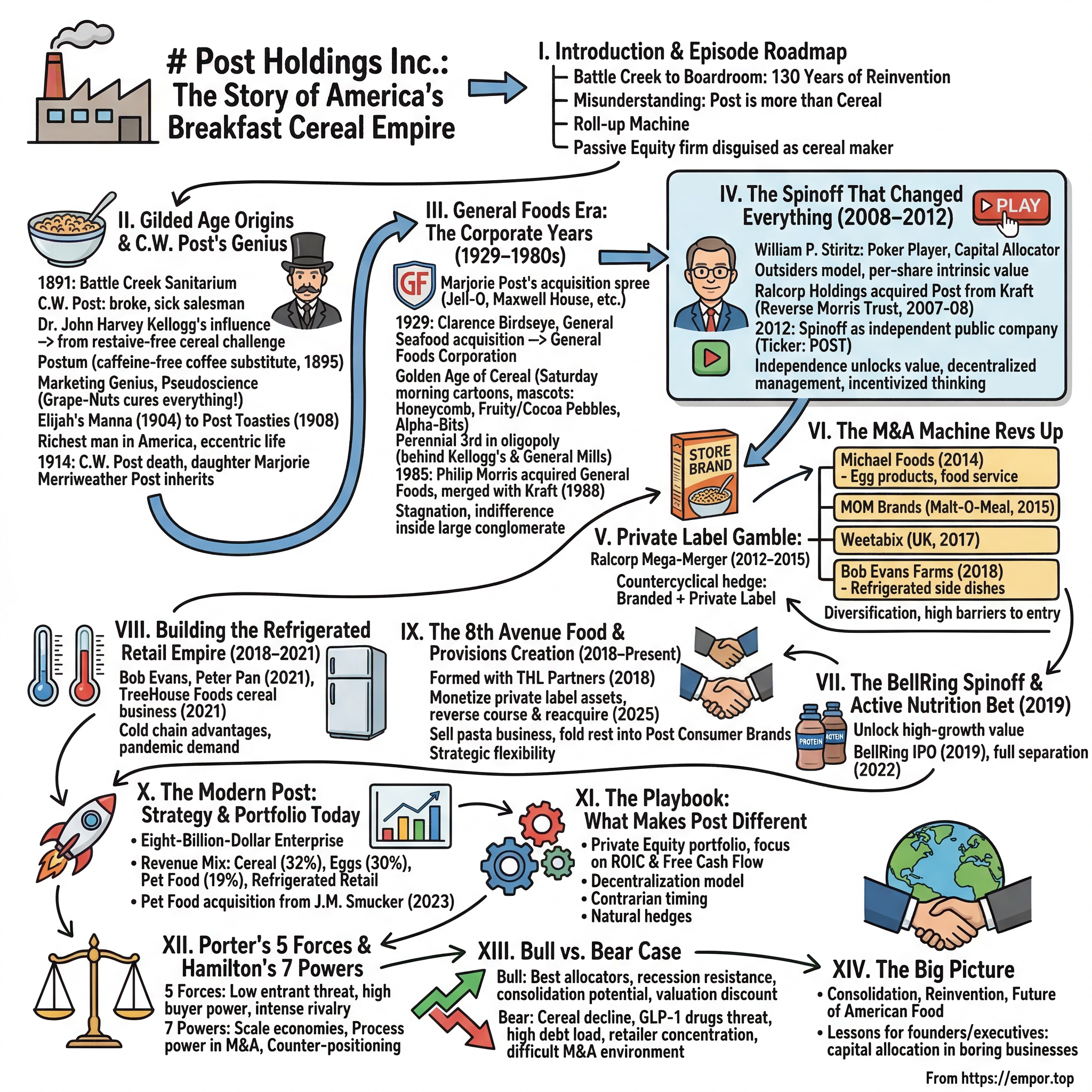

Post Holdings Inc.: The Story of America's Breakfast Cereal Empire

I. Introduction & Episode Roadmap

From Battle Creek to Boardroom: 130 Years of Reinvention

Somewhere in the cereal aisle of your local grocery store, between the cartoon-covered boxes of Fruity Pebbles and the austere brown sack of Grape-Nuts, sits a quiet empire most investors have never bothered to understand. Post Holdings generates more than eight billion dollars in annual revenue. It owns some of America's most recognizable breakfast brands — Honey Bunches of Oats, Pebbles, Great Grains — and operates one of the largest private label food manufacturing platforms in the country. It processes billions of eggs a year, makes refrigerated side dishes under the Bob Evans brand, dominates the United Kingdom's breakfast market through Weetabix, and recently muscled its way into pet food. It has spun off multiple public companies, including the fast-growing protein shake maker BellRing Brands, and generated total shareholder returns of nearly 480% since becoming an independent company in 2012.

And yet, when most people hear "Post," they think of cereal. Cereal and nothing else.

That misunderstanding is the central tension of this story. Post Holdings is not a cereal company. It is one of the most aggressive, disciplined, and surprisingly sophisticated roll-up machines in American food — a private equity firm disguised as a cereal maker, run by capital allocators who think more like Warren Buffett than like the typical consumer packaged goods executive. The company's playbook involves buying underappreciated food assets at reasonable prices, running them with lean decentralized management, generating prodigious free cash flow, and then redeploying that cash into the next acquisition. It is the kind of strategy that sounds boring until you look at the returns.

The story of Post is also the story of American food itself — from the patent medicine hucksterism of the 1890s to the Mad Men advertising wars of the 1960s, from the conglomerate mania of the 1980s to the private equity-style financial engineering of the 2010s. It spans three centuries, multiple corporate parents, at least five major reinventions, and one of the most consequential spinoffs in food industry history. Along the way, it raises questions that matter for every investor in consumer staples: What happens when a legacy brand gets separated from a bloated parent? How do you build a moat in a commodity business? And why do boring companies so often generate extraordinary returns?

Let's start at the very beginning — in a sanitarium kitchen in Battle Creek, Michigan, where a broke, sick, middle-aged salesman was about to steal an idea that would change the American breakfast forever.

II. The Gilded Age Origins & C.W. Post's Genius

Battle Creek, Michigan, 1891

In the winter of 1891, a gaunt man arrived at the Battle Creek Sanitarium in a wheelchair. Charles William Post was thirty-six years old, broken in health and in fortune, with a string of failed business ventures behind him and no clear path forward. He had tried selling agricultural equipment in Springfield, Illinois. He had patented a plow, a harrow, and a hay-stacking machine. He had dabbled in real estate in Texas. None of it had worked. Two severe nervous breakdowns — the first in 1885, the second in 1891 — had left him physically debilitated and financially ruined. His wife Ella had to borrow money to pay for his care.

The sanitarium was run by Dr. John Harvey Kellogg, a brilliant and eccentric physician who preached the gospel of vegetarianism, hydrotherapy, and grain-based health foods. Kellogg's patients ate a carefully designed diet of whole grains and cereals, drank a roasted grain beverage as a substitute for coffee, and submitted to elaborate treatments involving everything from electrical stimulation to yogurt enemas. The San, as it was known, was part hospital, part resort, part religious experiment — a temple of Progressive Era wellness culture, attracting the likes of Henry Ford, Thomas Edison, and Amelia Earhart.

Post spent nine months there. The treatments did not cure him — he later credited a Christian Science practitioner for his recovery — but they taught him something far more valuable. In the sanitarium kitchen, where Post worked to pay off his room and board because he could not afford the fees, he observed the grain-based foods and beverages being prepared for patients. He tasted the cereal coffee substitute. He watched how the affluent guests responded to the health claims and the sense of moral superiority that came with eating "scientific" food. And he saw a business opportunity of staggering proportions.

After leaving the sanitarium, Post stayed in Battle Creek and opened a small health establishment called La Vita Inn, which attempted to heal patients through mental suggestion. It never amounted to much. But in 1895, Post introduced his first commercial product: Postum, a caffeine-free coffee substitute made from roasted wheat bran and molasses. The recipe bore a striking resemblance to the cereal beverage served at Kellogg's sanitarium — so striking that accusations of recipe theft would follow Post for the rest of his life. Whether he literally copied Kellogg's formula or simply adapted the concept remains debated. What is not debated is what happened next.

Post did something the Kellogg brothers never managed to do in those early years: he marketed the product with ferocious, relentless genius. He wrote his own advertising copy and launched a nationwide campaign against coffee itself, claiming the beverage caused "coffee nerves," blindness, heart disease, and nervous breakdowns. Postum, he promised, would strengthen "red blood" and put consumers on the "Road to Wellville." The health claims were pure pseudoscience. They were also devastatingly effective. By 1900, just five years after launch, the Postum Cereal Company was netting three million dollars a year, and Post was one of the five largest advertisers in the entire United States, spending over a million dollars annually on newspaper and magazine placements.

In 1897, Post followed up with Grape-Nuts, a dense, crunchy cereal made from wheat and barley flour that was baked into rigid sheets and then ground into small nuggets. The name was a masterpiece of creative misdirection — the product contained neither grapes nor nuts — but the advertising was even more audacious. Post claimed Grape-Nuts could cure appendicitis, tuberculosis, malaria, and loose teeth. When Collier's Weekly challenged these claims in a 1907 exposé, Post responded with advertisements attacking the author's intelligence. Collier's sued for libel, and Post was eventually fined fifty thousand dollars. He never apologized.

Post's corn flakes product, launched in 1904, demonstrated both his audacity and his occasional blindness. He named it "Elijah's Manna," slapped an image of the biblical prophet being fed by a raven on the box, and waited for America to buy. Instead, clergy across the country denounced the product from their pulpits as sacrilege. Britain banned its importation. Post stubbornly held on to the name for four years before financial reality forced him to relent, renaming it Post Toasties in 1908.

By the time Will Keith Kellogg finally launched his own cereal company in 1906, Post — the sanitarium patient who could not pay his bill — was already one of the richest men in America. He owned a 225,000-acre ranch in Texas where he built an entire town called Post City. He conducted bizarre weather modification experiments, detonating dynamite along cliff edges in an attempt to force clouds to produce rain. He was a millionaire many times over, a self-made titan who had built his fortune on a combination of genuine marketing genius and brazen pseudoscience.

The irony at the heart of the Battle Creek cereal wars was this: John Harvey Kellogg viewed health food as a medical mission and was slow to commercialize his innovations. His brother Will Keith Kellogg did not launch his own cereal company until 1906. C.W. Post — the patient who arrived in a wheelchair and worked off his bill in the kitchen — beat them both to commercial success by over a decade. He understood something the Kellogg brothers did not: in consumer products, the product matters far less than the story you tell about it. Postum was not meaningfully better than other grain beverages. Grape-Nuts was not nutritionally superior to other cereals. But Post's relentless advertising created the perception of superiority, and in consumer goods, perception is reality.

Post's personal life reflected the contradictions of his public persona. In 1904, he divorced his wife Ella — who had supported him through years of failure and illness — and married his twenty-seven-year-old secretary, Leila Young, less than two weeks later. His daughter Marjorie later said her mother died of "a broken heart." The man who sold America on the "Road to Wellville" was himself chronically ill throughout his adult life, plagued by the same nervous ailments that had first brought him to Battle Creek.

On May 9, 1914, at the age of fifty-nine, C.W. Post died by suicide at his estate in Santa Barbara. He had undergone emergency appendectomy surgery at the Mayo Clinic weeks earlier and had grown despondent over his continuing decline. His twenty-seven-year-old daughter, Marjorie Merriweather Post, inherited the company and most of his approximately twenty-million-dollar fortune. She would transform it into something far larger — but the DNA of the company, that peculiar blend of marketing savvy, contrarian thinking, and willingness to make audacious bets, was already set. It would take a century to fully express itself.

III. General Foods Era: The Corporate Years (1929–1980s)

The Rise and Stagnation of an American Food Empire

Marjorie Merriweather Post was not a passive heiress. Her father had deliberately trained her in business, taking her to board meetings as a teenager and teaching her to read financial statements. By the time she inherited the Postum Cereal Company, she understood every corner of the operation. And she had ambitions that dwarfed anything her father had imagined.

Between 1925 and 1929, Marjorie orchestrated an acquisition spree that transformed Postum from a cereal maker into America's largest diversified food company. She bought Jell-O in 1925. Maxwell House coffee in 1928. Log Cabin syrup. Walter Baker chocolate. And then, in 1929, came the deal that changed everything: the acquisition of Clarence Birdseye's General Seafood Corporation for twenty-two million dollars. Legend holds that Marjorie, dining aboard her yacht the Hussar, tasted a flash-frozen turkey that had been preserved using Birdseye's revolutionary technology and immediately grasped its potential. She pushed through the purchase over the objections of skeptical board members, pioneered the distribution of commercial freezers to retailers, and essentially created the frozen food industry.

In June 1929, the Postum Cereal Company changed its name to General Foods Corporation. The cereal business that C.W. Post had built became just one division of an enormous conglomerate whose brands — Jell-O, Maxwell House, Kool-Aid, Tang, Cool Whip, Stove Top Stuffing, Birds Eye — would define the American kitchen for half a century. By the early 1930s, General Foods was generating over nine billion dollars in annual revenue and employing tens of thousands of workers across manufacturing plants, distribution centers, and corporate offices. It was, by any measure, the most important food company in America.

The mid-century decades brought the cereal industry its golden age — and its most intense competitive battles. The rise of television transformed breakfast cereal marketing from a newspaper-and-magazine affair into a full-blown cultural phenomenon. Saturday morning cartoons became the primary battlefield, with cereal companies sponsoring shows and embedding their products into children's consciousness through mascots, jingles, and toy prizes buried inside boxes. General Foods introduced a parade of sugar-coated innovations: Honeycomb in 1965, Fruity Pebbles and Cocoa Pebbles in 1971 (licensed from Hanna-Barbera's The Flintstones), and Alpha-Bits, which turned the alphabet itself into a breakfast food. These products turned the cereal aisle into the most fiercely contested real estate in the grocery store.

The General Foods era was the age of television advertising, and the company became one of the most prolific sponsors in broadcast history. Maxwell House backed popular radio shows in the 1930s and 1940s. Jell-O ran campaigns featuring Jack Benny and later Bill Cosby. By the late 1970s, General Foods was the second-largest advertiser in America, trailing only Procter & Gamble. The company's cereal brands — Post Grape-Nuts, Honeycomb, Alpha-Bits, Fruity Pebbles — competed in the great three-way cereal war with Kellogg's and General Mills. Post typically finished third, consistently outspent and out-innovated by its two larger rivals, but protected by General Foods' massive distribution infrastructure and advertising budgets.

The problem with being a division inside a massive conglomerate is that nobody pays attention to you. Post cereals received investment when it suited the parent company's priorities and starved when it did not. Brand innovation slowed. Market share eroded gradually. The cereal business became what it would remain for decades: a steady, modestly profitable cash generator that nobody thought much about.

The competitive dynamic in cereal during these decades is worth understanding because it shaped everything that followed. Kellogg's was the undisputed market leader, with a share that frequently exceeded thirty-five percent. General Mills held a strong second position with brands like Cheerios, Wheaties, and Lucky Charms. Post was a perennial third, typically holding twelve to fifteen percent of the market. The gap was not about product quality — blind taste tests often showed no meaningful difference — but about advertising spend, distribution muscle, and the relentless cadence of new product introductions. Being number three in a three-player oligopoly is actually a comfortable position: you are large enough to command shelf space and negotiate reasonable terms with retailers, but small enough that the industry leaders focus their competitive firepower on each other rather than on you. Post learned to live in this position, generating solid margins without the massive marketing expenditure required to challenge for leadership.

In 1985, tobacco giant Philip Morris acquired General Foods for 5.8 billion dollars — then the most expensive non-oil acquisition in American history. Three years later, Philip Morris bought Kraft for 12.9 billion dollars and merged the two operations into Kraft General Foods. The Post cereal brands were now buried two layers deep inside a corporate structure dominated by tobacco executives, cheese marketers, and international snack food strategists. It was the kind of corporate home where brands go to collect dust.

The problem was not that Kraft-General Foods mistreated the Post brands. The problem was indifference. When you are a mid-single-digit-billions-in-revenue cereal portfolio inside a hundred-billion-dollar conglomerate, you simply do not get the management attention, capital investment, or strategic focus needed to compete aggressively. Every capital allocation decision was filtered through layers of corporate bureaucracy, evaluated against dozens of competing priorities across hundreds of brands and dozens of countries. The talented managers who might have reinvigorated Post's competitive position had no incentive to stay — they could make faster progress in divisions that the parent company actually cared about. Post would spend the next quarter century there, quietly generating cash, slowly losing relevance, waiting for someone to notice that it might be worth more on its own.

IV. The Spinoff That Changed Everything (2008–2012)

Enter William Stiritz: The Poker Player Who Built an Empire

The story of how Post Holdings became an independent company is really the story of one man: William P. Stiritz. And to understand Stiritz, you need to understand why he is one of the most important and least famous CEOs in American business history.

Born in 1934, Stiritz joined Ralston Purina in 1964 at the age of thirty, assigned to the company's grocery products division. He was not a classic corporate climber. He was a poker player — literally and figuratively — who believed that capital allocation was the most important skill a CEO could possess. "The key skills," he once said, "were an ability to calculate odds, read personalities, and make large bets when the odds were overwhelmingly in your favor." Under his leadership, Ralston Purina's grocery division saw operating profits increase fiftyfold through relentless product launches, including Purina Puppy Chow and Cat Chow, two of the most successful introductions in pet food history.

As chairman and CEO of Ralston Purina from 1981 to 1997, Stiritz compiled one of the most impressive track records in American corporate history. Pretax margins grew from nine percent to fifteen percent. Return on equity more than doubled from fifteen percent to thirty-seven percent. He produced a twenty percent annualized return for shareholders over a forty-year career. He was featured in William Thorndike's "The Outsiders," a book about the eight greatest capital-allocating CEOs in history, alongside the likes of Henry Singleton and John Malone.

Stiritz was also deeply influenced by the writings of Benjamin Graham and Warren Buffett, viewing per-share intrinsic value — not revenue growth, not market share, not empire size — as the only metric that ultimately mattered. He once told an interviewer that the most important question a CEO could ask was not "How do we grow?" but "What is the highest-return use of our next dollar?" This philosophy would define Post Holdings from the moment it became independent.

The path to Post's independence wound through a series of corporate restructurings. In November 2007, Kraft Foods announced it would sell its Post cereals business to Ralcorp Holdings, a St. Louis-based private label food manufacturer, in a transaction valued at approximately 2.6 billion dollars. The deal was structured as a Reverse Morris Trust — a tax-efficient maneuver in which Kraft first separated Post from its portfolio, and then merged it into Ralcorp. The transaction closed in August 2008.

But Ralcorp's interest in Post cereals was always secondary to its private label operations. The combination had never quite fit — Ralcorp's DNA was in manufacturing efficiency and cost management, while Post's branded cereal business required marketing investment, brand stewardship, and consumer innovation. The two businesses attracted different investors, required different management skills, and operated according to different strategic logic. Within Ralcorp, Post was a square peg in a round hole.

In January 2012, Ralcorp's board approved spinning off the Post cereals business as a standalone public company. The distribution was structured so that eighty percent of Post stock went to Ralcorp shareholders, with Ralcorp retaining a twenty percent stake. Post Holdings began trading on the New York Stock Exchange under the ticker POST on February 6, 2012, with Stiritz installed as chairman and CEO.

At the moment of its birth as a public company, Post Holdings was a modest enterprise. It had expected annual sales of roughly one billion dollars and held barely ten percent of the branded U.S. cereal market as the third-place competitor behind Kellogg's and General Mills. Its market capitalization hovered around two billion dollars. By conventional CPG standards, it was a sleepy, single-category business with limited growth prospects in a mature market. Wall Street analysts assigned it a polite but unenthusiastic coverage initiation. The sell-side consensus was that Post would be a quiet dividend payer — a company that would harvest its cereal brands for cash and gradually fade into irrelevance.

They could not have been more wrong.

Stiritz had no intention of running a sleepy cereal company. From his very first communications with investors, he made one thing perfectly clear: Post would be acquisitive. He had spent forty years studying capital allocation, identifying undervalued assets, and making bold bets when the odds were favorable. Now, with an independent public company, a clean balance sheet, and a stable cash-generating cereal business as his foundation, he intended to build something much larger. The poker player had his chips. He was ready to bet.

The strategic logic of the spinoff itself was textbook value creation — and it is worth pausing to understand why spinoffs so frequently unlock value, because this mechanism is central to Post's entire story. Inside a conglomerate, business units compete for capital against each other rather than against their actual market competitors. A cereal division inside Kraft does not get to reinvest its cash flow into cereal-related opportunities; that cash gets pooled centrally and distributed according to the parent's priorities. Management incentives are diluted — the CEO of Post cereals inside Kraft is evaluated on how Post contributes to Kraft's overall results, not on Post's standalone performance. And the stock market, unable to separately value the individual businesses inside a conglomerate, typically applies a "conglomerate discount" that punishes all the businesses for the complexity of the parent structure.

Independence reverses all of these dynamics. Every dollar of cash flow could now be directed by management that owned substantial equity and thought like owners. The stock market could value Post on its own merits. And the management team had direct, undiluted incentives to maximize the performance of the business they actually controlled. Stiritz put his money where his convictions were: SEC filings show he never sold a single share of POST stock throughout his tenure. By the time he retired from the board in December 2025, his stake of roughly 3.2 million shares represented about five percent of the company — a level of personal conviction almost unheard of among public company executives.

V. The Private Label Gamble: Ralcorp Mega-Merger (2012–2015)

The Branded-Plus-Private-Label Thesis Takes Shape

In November 2012 — just nine months after Post Holdings began trading as an independent company — ConAgra Foods acquired Ralcorp Holdings for approximately five billion dollars, creating the largest private label food company in the United States. Post Holdings, having already been separated from Ralcorp, was not directly involved in this transaction.

But the ConAgra-Ralcorp deal illuminated something important about the strategic landscape. Private label food manufacturing — the business of making store-brand products for grocery chains — was consolidating rapidly. The companies that controlled manufacturing capacity, distribution networks, and retailer relationships in private label would hold enormous power in a world where consumers increasingly viewed store brands as equivalent in quality to national brands.

To understand why private label matters so much to Post's story, it helps to understand what private label manufacturing actually is. When you walk into a Walmart or Kroger and pick up a box of "Great Value" cereal or a jar of store-brand peanut butter, that product was not made by the retailer. It was made by a contract manufacturer — a company with the factory, the food safety certifications, the ingredient sourcing relationships, and the logistics infrastructure to produce products at scale and deliver them to distribution centers on time. The retailer contributes the brand (its store brand label), the shelf space, and the customer relationship. The manufacturer contributes everything else.

This is a fundamentally different business than selling branded products. Branded companies invest heavily in advertising, product innovation, and brand equity to command premium prices. Private label manufacturers compete on cost efficiency, manufacturing reliability, and the ability to meet retailer specifications consistently. The margins are thinner, but the volumes can be enormous — store brands now account for more than twenty-one percent of all grocery sales — and the customer relationships tend to be sticky because switching manufacturers involves significant qualification, testing, and transition costs.

Post's own engagement with private label came through a different vector. When Stiritz and his team looked at the food industry landscape in those early years of independence, they saw an opportunity that most branded food companies missed entirely. Rather than viewing private label as the enemy — the cheap knockoff eroding brand premiums — they saw it as a complementary business that could provide countercyclical balance. In good economic times, consumers pay up for branded products and margins are fat. In recessions, consumers trade down to private label, and the manufacturer of those store brands captures the volume. Owning both sides of that equation was a natural hedge.

This insight would shape Post's strategic direction for the next decade. While the company did not directly acquire Ralcorp's private label operations, its subsequent acquisitions — particularly MOM Brands and later 8th Avenue Food & Provisions — would build substantial private label capabilities alongside its branded portfolio. The logic was counterintuitive but powerful: the same manufacturing lines that produced Honey Bunches of Oats could also produce the store-brand equivalent sitting right next to it on the shelf. Instead of fighting the private label trend, Post would profit from it.

The financing of Post's early acquisitive strategy required managing leverage carefully in a business that generated steady but unspectacular cash flows. Wall Street was skeptical. Cereal was a declining category. Post was the number three player. Loading up on debt to buy more food assets seemed like a recipe for value destruction. But Stiritz understood something that most analysts did not: in stable cash flow businesses with low capital expenditure requirements, debt is not a burden — it is a tool. The predictability of cereal demand made it possible to service higher leverage ratios than growth-oriented businesses could support. Every dollar of free cash flow that was not needed to maintain the existing business could be deployed into the next acquisition.

This insight — that debt is a tool for value creation in predictable cash flow businesses, not a sign of financial distress — separated Stiritz and his team from the majority of food industry executives who viewed leverage as inherently dangerous. In a growth business with unpredictable revenues, high leverage is genuinely risky. But cereal is not a growth business. People have been eating cereal for breakfast for over a century, and while volumes may slowly decline, they do not collapse. This predictability is what makes cereal a surprisingly good foundation for an acquisitive strategy: the cash flows are reliable enough to service the debt, and the debt enables acquisitions that would be impossible with equity alone.

The early results validated the approach. Post demonstrated that a focused management team with aligned incentives could extract more value from the same cereal brands that had languished inside Kraft's sprawling portfolio. Margins improved. Operating efficiency increased. The stock price responded. And the management team began scanning the landscape for transformative deals.

VI. The M&A Machine Revs Up: Becoming a Food Conglomerate (2015–2018)

From Cereal Company to Diversified Food Powerhouse

Picture a Post Holdings board meeting in late 2013. The company has been public for less than two years. It generates roughly a billion dollars in revenue from cereal — a category growing at approximately zero percent. The stock has performed well, but the market views Post as a pure-play cereal company with limited upside. William Stiritz, the chairman and CEO, has spent forty years studying capital allocation at Ralston Purina. He knows that the greatest returns come not from optimizing existing businesses, but from deploying excess cash flow into undervalued acquisitions that expand the company's competitive footprint. The question is: what do you buy?

The answer surprised everyone: eggs.

The acquisition of Michael Foods in 2014 for 2.45 billion dollars was the moment Post Holdings stopped being a cereal company and started being something else entirely. Michael Foods was the dominant player in value-added egg products — the company that processed, pasteurized, and distributed eggs to food service operators, restaurants, and food manufacturers across the country. It also had significant businesses in refrigerated potato products, cheese, and pasta. The deal was roughly the same size as Post's entire market capitalization at the time.

The strategic logic was diversification away from cereal into a category with very different dynamics. Egg products are a business-to-business operation with high barriers to entry, significant scale advantages, and demand driven by the food service industry rather than consumer whims. You do not need to spend hundreds of millions on television advertising to sell processed eggs to restaurant chains. You need manufacturing capacity, food safety expertise, and distribution relationships that take years to build. Michael Foods had all three.

Think of it this way: when a restaurant chain like Denny's needs liquid eggs for its omelets, or when a food manufacturer needs pasteurized egg products for its baked goods, they do not shop around for the cheapest supplier. They need a partner with USDA-certified facilities, rigorous food safety protocols, reliable cold-chain logistics, and the capacity to deliver millions of pounds of product on a consistent schedule. Switching egg suppliers involves food safety audits, product reformulation testing, and supply chain reconfiguration that can take months. This creates a stickiness in customer relationships that branded cereal — where a grocery store can swap one box for another overnight — simply does not have.

The Michael Foods acquisition also revealed something important about Stiritz's successor. Robert Vitale, who had taken over as CEO in 2014, was not merely continuing Stiritz's playbook — he was expanding it. While Stiritz would have been comfortable buying more cereal assets, Vitale pushed the team to think across the entire food value chain, looking for businesses with structural advantages regardless of what they manufactured. Eggs had nothing to do with cereal, but they had everything to do with the kind of business Post wanted to own: dominant market positions, high barriers to entry, stable demand, and cash flows that could service debt and fund the next deal.

In 2015, Post followed up with the acquisition of MOM Brands — formerly Malt-O-Meal — for approximately 1.15 billion dollars. This deal was cereal, but a very different kind of cereal. MOM Brands was the fourth-largest U.S. cereal maker, with an eight percent market share built largely on value-priced cereals sold in bags rather than boxes. Combined with Post's roughly ten percent share, the merged entity held approximately eighteen percent of the U.S. cereal market. The combined cereal business was renamed Post Consumer Brands and headquartered at MOM Brands' offices in Lakeville, Minnesota. Crucially, Post put MOM Brands' CEO Chris Neugent and his team in charge of the combined operation — a signal that Post valued operational talent over corporate hierarchy.

Then came the international expansion. In April 2017, Post entered into an agreement to acquire Weetabix Food Company, the United Kingdom's dominant breakfast cereal brand, for approximately 1.77 billion dollars. Weetabix held a commanding market share in the UK breakfast category through its flagship wheat biscuit cereal and related brands including Alpen and Oatibix. The deal closed in July 2017, giving Post its first significant international beachhead and a cash-generative business with strong brand loyalty in a market where breakfast cereal consumption remained healthier than in the United States.

Before the ink on the Weetabix deal was dry, Post announced its next move. In September 2017, the company agreed to acquire Bob Evans Farms for approximately 1.5 billion dollars. The Bob Evans name carried deep recognition across the Midwest and Southeast — the brand had started as a restaurant chain in the 1940s before the restaurant and food manufacturing businesses were separated. Post was buying the food manufacturing side: refrigerated side dishes — mashed potatoes, macaroni and cheese, pasta — along with pork sausage and other convenience foods. These were the kinds of products that Americans brought home for family dinners, holiday meals, and weeknight shortcuts. The acquisition, which closed in January 2018, added another leg to Post's diversification strategy: refrigerated retail, a category characterized by regional distribution moats, steady demand, and barriers to entry that discouraged new competitors.

The pace was breathtaking. In barely three years, Post had completed four major acquisitions totaling roughly seven billion dollars — transforming itself from a one-billion-dollar cereal company into a diversified food conglomerate generating more than five billion in annual revenue. Each deal was structured to preserve management autonomy, minimize cultural disruption, and extract synergies through purchasing power and distribution efficiency rather than headcount reductions.

A clear playbook had emerged. Post was not buying randomly. It was targeting the number one or number two player in niche food categories with stable demand, high barriers to entry, and strong cash generation. Each acquisition expanded the portfolio into a different part of the food ecosystem — branded cereal, private label cereal, egg products, refrigerated sides, international breakfast — creating a diversified holding company that could weather category-specific downturns without catastrophic impact on the whole.

The management structure reflected this philosophy. Rather than centralizing operations and imposing a single corporate culture — the approach that had destroyed value at conglomerates like Kraft Heinz — Post ran each business unit as an autonomous division with its own leadership team, its own P&L, and its own operating priorities. The corporate center in St. Louis remained lean, focused on capital allocation, financial reporting, and strategic oversight rather than day-to-day operational interference. It was the Berkshire Hathaway model applied to food: buy good businesses, install or retain good managers, and stay out of their way.

The contrast with the Kraft Heinz approach is instructive. When 3G Capital and Berkshire Hathaway merged Kraft and Heinz in 2015, they applied a centralized, cost-cutting playbook that slashed overhead, eliminated management layers, and imposed zero-based budgeting across the entire organization. The initial financial results were impressive — margins soared. But the long-term consequences were devastating. Brand investment dried up. Innovation pipelines emptied. Customer relationships deteriorated. Market share eroded across virtually every category. Kraft Heinz eventually wrote down more than fifteen billion dollars in goodwill — an admission that the aggressive cost-cutting had destroyed the very value it was supposed to unlock.

Post took the opposite approach. This decentralized structure was not just a management philosophy — it was a competitive advantage. When Post acquired Bob Evans, it did not try to merge the refrigerated side dish business with the egg processing business or the cereal operations. Each unit maintained its own identity, its own customer relationships, and its own operational expertise. The corporate center added value through capital allocation — deciding where to invest, what to acquire next, and when to return cash to shareholders — rather than through operational meddling that typically destroys the entrepreneurial cultures that make acquired businesses valuable in the first place.

VII. The BellRing Spinoff & Active Nutrition Bet (2019)

Knowing When to Let Go

By 2019, Post's management team faced a problem that most conglomerates would envy. One of its business units — the active nutrition segment anchored by Premier Protein — was growing at more than twenty percent annually, a rate that dwarfed the low-single-digit growth (or outright decline) of the cereal and egg businesses. Premier Protein's ready-to-drink protein shakes had become a phenomenon in convenience stores, gyms, and grocery aisles, riding the secular trend toward high-protein diets and on-the-go nutrition. The brand was a darling among health-conscious consumers, a category with premium margins and massive runway for growth.

The issue was valuation — and understanding this requires a brief detour into how Wall Street values food companies. Mature packaged food businesses typically trade at eight to twelve times EBITDA (earnings before interest, taxes, depreciation, and amortization), reflecting their slow growth and predictable cash flows. High-growth consumer brands in attractive categories can trade at fifteen to twenty-five times EBITDA, reflecting the market's willingness to pay more today for faster future earnings growth. When a fast-growing brand is buried inside a slow-growing conglomerate, the market applies the lower multiple to the entire entity — effectively valuing the growth brand as if it were a cereal company. Wall Street valued Post as a food conglomerate — applying the mid-single-digit multiple typical of the sector. But buried inside that conglomerate was a high-growth consumer brand that, if valued independently, would command a multiple two or three times higher. Every day that Premier Protein remained inside Post Holdings, its value was being obscured by the weight of slower-growing businesses. The stock market was effectively paying cereal prices for a protein shake business.

Post's solution demonstrated a level of corporate finance sophistication rare in the food industry. The company created a new entity called BellRing Brands, housing Premier Protein, Dymatize sports nutrition supplements, and PowerBar. In October 2019, BellRing completed an initial public offering, selling more than thirty-nine million shares at fourteen dollars each. Post retained a substantial majority stake, signaling continued confidence in the business while allowing the market to assign BellRing its own valuation.

The strategy played out in stages. Post first used a tracking stock structure to establish BellRing's independent identity, then executed a full separation. In March 2022, Post distributed 80.1 percent of its remaining BellRing shares to Post shareholders. By November 2022, Post had divested its entire remaining stake, completing the separation.

The result validated the thesis spectacularly. As a standalone company, BellRing could pursue growth investments that might have seemed too small or too niche inside the Post conglomerate. It could recruit management talent with equity packages tied directly to active nutrition performance rather than diluted across a portfolio of cereal and egg businesses. And it could attract growth-oriented investors who would never have bought Post stock because of the cereal drag. BellRing Brands, trading independently on the NYSE under the ticker BRBR, grew revenue from roughly one billion dollars at the time of the IPO to over two billion by fiscal 2025. The company established a long-term algorithm of seven to nine percent annual sales growth with adjusted EBITDA margins of eighteen to twenty percent. It became one of the most successful CPG spinoffs in recent memory. And the act of separating it unlocked value not just for BellRing shareholders, but for Post shareholders as well — by removing a fast-growing business from the conglomerate, Post clarified the investment thesis for its remaining portfolio and demonstrated management's willingness to sacrifice empire for shareholder value.

For Post shareholders, the BellRing separation created a "have your cake and eat it too" outcome. They received shares in a fast-growing active nutrition company valued at a premium multiple, while retaining their stake in the remaining Post Holdings business, which was now easier for the market to understand and value. The sum of the parts, as the corporate finance textbooks predicted, was worth more than the whole.

The BellRing spinoff also carried a subtler lesson. Post's management had shown they understood not just when to acquire, but when to separate. In a world where most corporate executives instinctively hoard assets and build empires, the willingness to make a business independent — to say "this is worth more without us than with us" — is exceptionally rare. It revealed a management team that thought like investors rather than operators, prioritizing value creation over revenue growth.

VIII. Building the Refrigerated Retail Empire (2018–2021)

The Cold Chain Advantage

While the BellRing story captured headlines and investor attention, Post was quietly building another pillar of its empire in a far less glamorous corner of the grocery store: the refrigerated case.

The refrigerated retail business, anchored by the Bob Evans acquisition, represents one of the most underappreciated parts of Post's portfolio. Refrigerated side dishes — mashed potatoes, mac and cheese, pasta — occupy a peculiar competitive niche. They are not shelf-stable products that can be shipped across the country in ambient trucks. They require cold chain logistics, regional manufacturing, and freshness-dating systems that create natural barriers to entry. A competitor cannot simply build a factory in one location and distribute nationally the way a cereal company can. Geography matters. Relationships with regional distributors matter. The capital requirements to build cold chain infrastructure from scratch are substantial.

Post expanded this footprint methodically. The Bob Evans integration brought refrigerated side dishes and sausage products. Michael Foods already contributed egg products — both retail and food service — that traveled through the same cold supply chain. In January 2021, Post added Peter Pan peanut butter by acquiring the brand from Conagra Brands. Peter Pan was a century-old brand with national recognition, sold in eleven varieties, and critically, all its products were already being co-manufactured by 8th Avenue Food & Provisions — a Post-affiliated entity. Bringing the brand in-house alongside its existing manufacturing was a textbook tuck-in acquisition.

In 2021, Post also acquired TreeHouse Foods' ready-to-eat cereal business, further consolidating its private label cereal manufacturing position. The deal was smaller than the headline-grabbing acquisitions that preceded it, but strategically significant: it added manufacturing capacity specifically designed for private label cereal production, strengthening Post's position as the go-to supplier for store-brand cereals at America's largest retailers.

The COVID-19 pandemic temporarily supercharged these businesses. With Americans eating at home in unprecedented numbers, demand for refrigerated side dishes, egg products, and shelf-stable staples surged. Post's supply chain, built for scale and reliability, proved a competitive advantage when smaller competitors struggled with disruptions. The pandemic also demonstrated the resilience of Post's diversified model: when food service demand collapsed (hurting the egg business's restaurant customers), retail demand surged to compensate.

The private label dimension added another layer of strategic depth. Through its various manufacturing operations, Post served as a critical supplier to major grocery chains — producing store-brand cereals, nut butters, and other products that sat on shelves alongside Post's own branded offerings. This dual role as both branded competitor and private label supplier created a complex but advantageous position. Post profited regardless of whether consumers chose the branded box or the store-brand bag. In an industry where the biggest risk was losing shelf space to private label, Post had neutralized that threat by being the company making the private label products.

The relationship with major retailers like Walmart and Costco became central to this strategy. These retailers wielded enormous buyer power — they could dictate pricing, demand promotional support, and threaten to switch suppliers. But Post's scale and reliability made it a difficult partner to replace. When you are the company that manufactures both the branded cereal and the private label version, and you also supply the retailer's egg products and refrigerated side dishes, you become deeply embedded in the supply chain. Switching costs, while not insurmountable, are real.

The private label trend has only accelerated. U.S. store brand sales reached a record 282.8 billion dollars in 2025, with dollar share hitting an all-time high of 21.2 percent. Private label unit volumes grew while national brand volumes declined. More than sixty percent of shoppers now trust store brands, and seventy-one percent rate them equal or better in quality compared to national brands. For Post, this secular shift is not a threat — it is a tailwind. Every percentage point of market share that private label gains from branded competitors is a potential revenue opportunity for the company that manufactures many of those store-brand products.

IX. The 8th Avenue Food & Provisions Creation (2018–Present)

Corporate Structure as Strategy

In August 2018, Post announced one of its most creative financial maneuvers: the formation of 8th Avenue Food & Provisions, a standalone entity housing Post's private label businesses in nut butter, pasta, granola, and dried fruit and nut products. Post partnered with Thomas H. Lee Partners, a prominent private equity firm, to capitalize the new entity. THL contributed 250 million dollars, and 8th Avenue assumed 625 million in debt. Post received total proceeds of approximately 875 million dollars, effectively monetizing its net investment in the private label business while retaining a minority stake.

The logic was elegant — and it provided Post with nearly 875 million dollars in immediate liquidity that could be redeployed into other acquisitions. In effect, Post had monetized its private label assets at a fair valuation, freed up capital for higher-return opportunities, and retained optionality to reacquire the business later if circumstances warranted. It was corporate finance as martial art — using the opponent's weight (in this case, private equity's appetite for stable cash flow businesses) against them.

Private label food manufacturing and branded consumer goods attract fundamentally different investor bases. Private label investors care about manufacturing efficiency, contract stability, and volume growth. Branded investors care about marketing innovation, premium pricing power, and brand equity. By separating the two, Post allowed each business to be valued on its own merits and managed with its own capital structure.

But the 8th Avenue experiment also demonstrated Post's willingness to reverse course when circumstances changed. In early 2025, Post announced it would reacquire all of 8th Avenue Food & Provisions, completing the deal on July 1, 2025 for a net payment of approximately 880 million dollars, including the extinguishment of 8th Avenue's debt. Within two months, Post sold 8th Avenue's pasta business — including the Ronzoni brand and three production facilities — to Richardson Holdings for 375 million dollars in cash plus approximately eighty million in assumed leaseback liabilities. The retained nut butter, granola, and fruit and nut businesses were folded into the Post Consumer Brands segment.

The net math told a story of disciplined capital recycling. Post spent roughly 880 million dollars to reacquire 8th Avenue, then immediately recovered 375 million by selling the pasta business it did not want to keep. The approximately 505 million in net cost brought back the nut butter manufacturing (including the production lines for Peter Pan, which Post had acquired the brand for in 2021), granola, and fruit and nut operations — businesses expected to contribute forty-five to fifty million in adjusted EBITDA before synergies. It also internalized Peter Pan's manufacturing, eliminating the co-manufacturing arrangement that had been in place since the brand acquisition.

The 8th Avenue saga illustrates a broader principle about corporate structure in the food industry. There is no permanently correct answer to the question of whether businesses should be combined or separated. The right structure depends on capital market conditions, management bandwidth, competitive dynamics, and the relative advantages of shared versus independent operations. What distinguished Post was not that it always made the right structural call on the first try — 8th Avenue's round trip suggests they did not — but that it was willing to revisit and reverse decisions when circumstances changed. Most companies, having publicly announced a separation, would stubbornly stick with it rather than admit the thesis had evolved. Post's willingness to reacquire demonstrated intellectual honesty and strategic flexibility.

Post had now demonstrated the full repertoire of corporate structure as strategy: spinning off BellRing to unlock growth-company valuation, creating 8th Avenue to monetize private label assets and attract private equity capital, reacquiring 8th Avenue when the strategic calculus shifted, and divesting the pieces that did not fit. Three public companies had been created from one. Value had been created and recaptured at multiple stages. The corporate treasury had been replenished through each transaction. It was the kind of financial engineering that most food companies lack the sophistication — or the courage — to attempt.

X. The Modern Post: Strategy & Portfolio Today

An Eight-Billion-Dollar Enterprise That Started With Cereal

As of early 2026, Post Holdings operates four reportable business segments, each serving different customers, channels, and competitive dynamics.

Post Consumer Brands is the largest segment, generating roughly four billion dollars in annual revenue — nearly half the company's total. This segment includes the legacy cereal brands (Honey Bunches of Oats, Pebbles, Great Grains, Grape-Nuts, Honeycomb), the value and private label cereals inherited from MOM Brands, and — following the April 2023 acquisition of pet food brands from J.M. Smucker for approximately 1.2 billion dollars — a substantial pet food portfolio including Rachael Ray Nutrish, 9Lives, Kibbles 'n Bits, and Nature's Recipe. The Smucker pet food deal added 1.4 billion in annual net sales, three manufacturing facilities, a distribution center, and more than a thousand employees. Post's entry into pet food reflected the same diversification logic that had driven earlier acquisitions: pet food is a resilient, growing category with different demand drivers than cereal or eggs.

The Foodservice segment, built on Michael Foods, generates roughly 2.6 billion in annual revenue, making it Post's second-largest business. This segment processes and distributes egg products, cheese, and refrigerated potato products to food service operators, restaurant chains, and food manufacturers. Fiscal 2025 was a strong year for the segment, with revenue growing over fourteen percent and segment profit surging nearly thirty percent, driven in part by elevated egg prices during avian influenza outbreaks that disrupted supply. The egg business is inherently cyclical — supply disruptions from bird flu can reduce volume but simultaneously push prices higher, creating a natural hedge that management has learned to navigate.

Refrigerated Retail, the third segment, generates just under a billion in annual revenue through Bob Evans side dishes, egg products sold at retail, and related refrigerated foods. This business earns attractive margins through regional distribution advantages and brand loyalty in the refrigerated case.

Weetabix, the fourth and smallest segment at roughly 540 million dollars in annual revenue, provides international diversification and a dominant market position in UK breakfast cereals. Weetabix is to the British breakfast what Cheerios is to the American one — a cultural institution, consumed by millions of households, with brand recognition that approaches one hundred percent among UK consumers. The business generates steady cash flow and provides a platform for potential expansion into other international markets, though Post has been cautious about pushing the brand beyond its established stronghold in Britain and select export markets.

The revenue mix tells a story that would astonish anyone who thinks of Post as a cereal company. Cereal and granola products (including Weetabix) now account for roughly thirty-two percent of total revenue. Egg and egg products represent about thirty percent. Pet food contributes approximately nineteen percent. Refrigerated retail adds the remainder. The cereal business that once defined the entire company is now barely a third of revenue — still important as a cash generator, but no longer the engine of the enterprise. The real growth drivers are the food service egg business and the pet food portfolio, categories that did not even exist in Post's portfolio a decade ago.

The management transition from the Stiritz era has been remarkably smooth. Robert V. Vitale, who served as Post's CFO from 2011 before being named president and CEO in 2014, has led the company through the majority of its transformative acquisitions. Vitale's background is in finance and private equity rather than consumer marketing — a distinction that shapes Post's entire strategic orientation. In December 2025, following William Stiritz's retirement from the board at age ninety-one, Vitale added the chairman title to his roles. The veteran COO Jeff Zadoks retired in January 2026, with Nicolas Catoggio — previously the head of Post Consumer Brands — expanding his role to serve as enterprise-wide COO.

The pet food acquisition deserves its own discussion because it reveals how Post's M&A machine adapts to new categories. When J.M. Smucker decided to exit pet food in 2023 to focus on its coffee and snacking businesses, Post saw an opportunity to acquire established brands — Rachael Ray Nutrish, 9Lives, Kibbles 'n Bits, Nature's Recipe, and Gravy Train — at a price that reflected Smucker's urgency to sell rather than the brands' long-term value. The 1.2-billion-dollar deal (700 million in cash plus roughly 5.4 million Post shares) came with three manufacturing facilities, a distribution center, and more than a thousand employees. The pet food category offered secular growth — Americans spent more on their pets every year regardless of economic conditions — and resilience through economic cycles. Early integration has faced challenges, with pet food volumes declining 6.2 percent in the most recent quarter due to distribution losses, but the long-term thesis rests on Post's ability to stabilize and gradually grow these brands using its manufacturing and distribution infrastructure.

The current Post Holdings is lean, focused, and still hungry. In fiscal 2025, the company generated 1.54 billion dollars in adjusted EBITDA on 8.16 billion in revenue. It repurchased 6.4 million shares for 708 million dollars — more than eleven percent of its float — and in February 2026 authorized a new 500-million-dollar buyback program. The company refinanced 1.3 billion in debt in late 2025, extending maturities to 2036 and giving itself additional financial flexibility. Net leverage stood at roughly 4.3 times EBITDA — elevated by most standards, but manageable given the predictability of Post's cash flows.

XI. The Playbook: What Makes Post Different

The Outsiders Model Applied to Food

Step back from the individual acquisitions, spinoffs, and financial maneuvers, and a larger pattern emerges. Post Holdings is not really managed like a food company. It is managed like a private equity portfolio — a collection of distinct businesses unified by a common capital allocation philosophy rather than a common operating model.

This distinction matters enormously. Most consumer packaged goods companies are run by marketing executives who think in terms of brand equity, consumer insights, and market share. They measure success by volume growth, household penetration, and brand awareness scores. These are important metrics, but they are not the metrics that drive shareholder value. Post is run by financial executives who think in terms of return on invested capital, free cash flow yield, and per-share intrinsic value. They measure success by whether each dollar they deploy — into an acquisition, a share repurchase, or debt reduction — generates more than a dollar of value in return. This is a fundamentally different operating philosophy, and it explains why Post has generated returns that are so dramatically different from its food industry peers.

This approach, sometimes called the "Outsiders" model after William Thorndike's influential book, rests on a simple insight: in mature industries with stable cash flows, the CEO's most important job is not managing operations but allocating capital. Where does each dollar of free cash flow go? Into acquisitions? Share buybacks? Debt reduction? Dividends? The answers to these questions, compounded over years and decades, determine shareholder returns far more than any individual product launch or marketing campaign.

Post's track record on capital allocation has been exceptional. Since the 2012 spinoff, the company has spent more than ten billion dollars on acquisitions with impairment charges of less than 300 million — an extraordinarily low failure rate in an industry littered with destroyed value from overpriced deals and botched integrations. Total shareholder returns of 479 percent through late 2025 dwarfed peers like General Mills at 138 percent, Conagra, Kellanova, and Campbell Soup.

The decentralization model is central to this success. Post runs more than twenty brands across four segments without a bloated corporate center trying to harmonize everything. Each division operates with its own management team, its own culture, and its own operating priorities. The corporate office adds value through capital allocation, financial discipline, and strategic oversight — deciding what to buy, what to sell, and what to spin off — rather than through operational micromanagement. This structure avoids the "one-size-fits-all" mentality that destroyed value at conglomerates like Kraft Heinz, where 3G Capital's aggressive cost-cutting gutted brands and alienated customers.

The contrarian timing of Post's acquisitions also deserves attention. The company's most important deals were made when others were scared. The early acquisition spree in 2014-2015 came when legacy food companies were under pressure from changing consumer preferences and investors were fleeing the sector. Buying Bob Evans in 2017 at a time when refrigerated foods attracted little Wall Street excitement proved prescient. The Smucker pet food deal in 2023 acquired a portfolio of brands at a price that reflected Smucker's eagerness to exit the category rather than their long-term value.

The natural hedge embedded in Post's portfolio is worth dwelling on because it is one of the most underappreciated aspects of Post's strategy. Think of it like an investment portfolio with built-in rebalancing. Branded products — Honey Bunches of Oats, Pebbles, Bob Evans — perform well in good economic times when consumers are willing to pay premium prices for names they trust. Private label products — the store-brand cereals and nut butters that Post manufactures for grocery chains — gain share when consumers trade down during recessions. Egg products are essential regardless of economic conditions. Pet food is recession-proof because pet owners view their animals as family members, not discretionary expenses. The result is a portfolio that provides a degree of resilience few food companies can match. This is not theoretical. During the 2020 pandemic disruption and the subsequent inflationary environment, Post's diversified model proved its worth, with different segments taking turns driving growth depending on which macro tailwind was blowing.

Management ownership reinforces the alignment between executives and shareholders. Stiritz's refusal to sell a single share during his tenure set a cultural standard. Vitale and the current management team hold significant equity positions, and the incentive structure rewards long-term value creation rather than short-term earnings manipulation. The average tenure of the management team is approximately seven years, and the board's average tenure is roughly eight years — suggesting stability and institutional knowledge rather than revolving-door governance.

What has not worked? Post's track record is not unblemished. Some categories have proven more challenging than expected. Cereal volumes continue their secular decline, with Post Consumer Brands reporting a 5.1 percent volume decline in the most recent quarter. The pet food acquisition, while strategically sound, has faced distribution losses and volume declines of 6.2 percent as Post works to stabilize the brands it acquired from Smucker. And 8th Avenue's journey — created, separated, reacquired, and partially divested — suggests that even sophisticated operators sometimes need multiple attempts to find the right corporate home for an asset.

XII. Porter's 5 Forces & Hamilton's 7 Powers Analysis

No deep dive into Post Holdings would be complete without applying the two most widely used frameworks for analyzing competitive advantage: Michael Porter's Five Forces and Hamilton Helmer's Seven Powers. Together, they reveal where Post is structurally advantaged, where it is vulnerable, and what ultimately determines the durability of its returns.

Understanding Post Holdings' competitive position requires examining the structural forces that shape its industry and the specific powers that give it durable advantages.

Starting with the threat of new entrants: the barriers are substantial. Building a cereal manufacturing plant requires tens of millions in capital investment. Establishing distribution relationships with major grocery chains takes years. Building consumer brand awareness in a market dominated by General Mills, Kellogg's, and Post requires advertising budgets that few startups can afford. In egg processing and refrigerated foods, the barriers are even higher — food safety certifications, cold chain logistics infrastructure, and long-standing relationships with food service operators create a multi-year gauntlet for any would-be competitor. Small craft cereal brands and direct-to-consumer startups occasionally make noise, but they struggle to achieve the scale economics needed for national distribution. The threat of new entrants is low.

Supplier bargaining power is moderate. Post's primary inputs — wheat, corn, oats, eggs, packaging materials — are commodities with multiple sourcing options. The company's scale provides purchasing leverage, and commodity price fluctuations tend to be passed through to customers with a modest lag. The one notable exception is the egg supply chain, where avian influenza outbreaks can dramatically reduce supply and spike prices. Post experienced this directly in fiscal 2025, when bird flu at contracted facilities knocked out roughly fourteen percent of its egg supply. Paradoxically, the resulting price increases partially offset the volume losses, demonstrating the complex dynamics of commodity-dependent businesses.

Buyer bargaining power is the most significant competitive threat Post faces. The grocery retail industry is heavily concentrated — Walmart alone accounts for a substantial share of Post's revenue across multiple categories. Costco, Kroger, and Amazon wield similar power. These retailers can demand promotional funding, squeeze pricing, threaten to reduce shelf space, or develop their own private label alternatives. Post's defense against this pressure is scale and indispensability: when you are one of a handful of companies that can reliably supply both branded and private label products across multiple categories, the switching costs for retailers become meaningful. But the power imbalance remains real and permanent.

The threat of substitutes is moderate and evolving. Traditional breakfast cereal faces substitution from protein bars, yogurt, breakfast sandwiches, smoothies, and the simple reality that many consumers — particularly younger ones — skip breakfast entirely. The rise of GLP-1 weight loss drugs like Ozempic and Wegovy represents a newer and potentially significant headwind: research suggests that GLP-1 households reduce grocery spending by roughly six percent, and projections indicate that GLP-1 households could account for more than a third of food and beverage sales within five years. Cereal, as a calorie-dense processed food, is particularly vulnerable to this trend. However, the protein trend that GLP-1 drugs accelerate actually benefits Post's egg products business and its former subsidiary BellRing Brands.

Industry rivalry is intense. In cereal, Post competes with General Mills (Cheerios, Lucky Charms) and the recently split Kellogg entities — Kellanova for snacks and WK Kellogg for cereal. In eggs, Cal-Maine Foods is the largest shell egg producer. In pet food, Post faces Mars Petcare, Nestle Purina, General Mills (Blue Buffalo), and Colgate-Palmolive (Hill's). In refrigerated foods, Conagra and Hormel are significant competitors. The rivalry is sharpened by the maturity of most of these categories — when the pie is not growing, every dollar of market share must be taken from someone else.

Turning to Hamilton Helmer's 7 Powers framework, which identifies the sources of persistent competitive advantage: Post's moat derives primarily from three of the seven powers.

Scale economies are Post's strongest structural advantage. The company's manufacturing, distribution, and purchasing operations operate at a scale that smaller competitors cannot match. This is most visible in private label cereal manufacturing, where Post's MOM Brands heritage and the 2021 acquisition of TreeHouse Foods' ready-to-eat cereal business created a platform with unmatched cost efficiency. In egg processing, Michael Foods' scale provides similar advantages. Scale does not prevent competition, but it creates a persistent cost advantage that erodes the profitability of anyone trying to compete at smaller volumes.

Process power — the institutional capability to repeatedly execute complex tasks better than competitors — is Post's second major advantage. The company's M&A machine, built over more than a decade and more than twenty acquisitions, represents a genuine organizational capability. Identifying targets, structuring transactions, integrating acquired businesses without destroying their cultures, and extracting synergies without over-cutting — these are skills that take years to develop and cannot be easily replicated. Post's track record of minimal impairment charges on more than ten billion dollars in deals is the evidence that this capability is real, not just claimed.

Counter-positioning — the adoption of a business model that incumbents cannot easily replicate because doing so would damage their existing businesses — applies moderately to Post's hybrid branded-plus-private-label strategy. Traditional branded food companies like General Mills and Kellogg's have historically resisted private label manufacturing because it could undermine their premium pricing. Post's willingness to compete on both sides of the aisle gives it a structural advantage that pure branded competitors would find difficult to adopt.

Network effects, cornered resources, and switching costs are weak or absent. Food manufacturing does not benefit from network effects. Post has no unique ingredients or intellectual property that competitors cannot access. And while brand loyalty exists in categories like cereal and peanut butter, it is modest compared to the switching costs that exist in technology or enterprise software.

Branding power exists at a moderate level. Honey Bunches of Oats, Pebbles, and Weetabix are genuinely strong brands within their categories, commanding consumer loyalty and premium shelf space. But they are not transcendent brands — they do not command the kind of pricing power or emotional connection that brands like Coca-Cola or Nike enjoy. Post's branding advantage is real but category-specific and incremental rather than transformational.

The verdict: Post's moat comes from the combination of scale economies, process power in M&A and integration, and the strategic optionality created by its hybrid branded-plus-private-label portfolio. These are durable advantages, but they require continuous execution to maintain. The moat is wide enough to generate attractive returns, but not so wide that management can coast.

Compared to its primary competitors, Post occupies a distinctive strategic position. General Mills, with roughly twenty billion in revenue, has greater scale but carries the burden of managing a massive portfolio including Cheerios, Häagen-Dazs, Blue Buffalo, and numerous international brands. Kellogg's recent split into Kellanova (snacks) and WK Kellogg (cereal) reflected the same insight that drove Post's own spinoff — that cereal assets perform better when separated from faster-growing categories. Conagra Brands, with a portfolio spanning frozen foods, snacks, and staples, competes with Post in refrigerated retail but lacks Post's egg and private label capabilities. TreeHouse Foods, the largest pure-play private label food company, competes with Post in store brands but without the branded portfolio that provides a countercyclical hedge. In eggs, Cal-Maine Foods is the largest shell egg producer, but Post's focus on value-added processed egg products gives it different margin dynamics and customer relationships. None of Post's competitors replicate its specific combination of branded cereal, private label manufacturing, egg processing, refrigerated retail, international breakfast, and pet food — a complexity that is simultaneously its analytical challenge and its strategic strength.

XIII. Bull vs. Bear Case

Every investment thesis is a bet on the future, and Post Holdings presents an unusually stark contrast between its bull and bear narratives. Both are credible. Both are supported by evidence. The challenge for investors is weighing which set of forces will prove more powerful over the next decade.

The bullish case rests on four pillars.

First, the company is led by some of the best capital allocators in the food industry. Vitale and his team have demonstrated over twelve years that they can identify undervalued assets, acquire them at reasonable prices, integrate them without destroying value, and sometimes separate them to unlock additional returns. The 479 percent total shareholder return since the 2012 spinoff is not the result of luck or a rising tide — it reflects a repeatable process of disciplined capital deployment. The recent 500-million-dollar share repurchase authorization signals that management believes the stock is undervalued even after years of compounding.

Second, Post's diversified portfolio provides genuine recession resistance. Private label products gain share when consumers trade down — and with private label now holding more than twenty-one percent of grocery dollar share and still growing, the structural trend favors manufacturers with private label capabilities. Egg products are essential regardless of economic conditions; restaurants do not stop serving omelets in a recession. Refrigerated side dishes are comfort food — affordable indulgences that consumers reach for when they cut back on dining out. Pet food is famously recession-proof — Americans will cut their own food budgets before they switch their dog's kibble. This portfolio construction means Post can generate stable cash flows across economic cycles, funding continued M&A without equity dilution.

Third, the food industry remains highly fragmented, with hundreds of small and mid-sized companies ripe for consolidation. Post's process power in M&A — the institutional knowledge of how to identify, acquire, and integrate food businesses — gives it a persistent advantage in this consolidation race. Each acquisition adds scale, purchasing power, and distribution capabilities that make the next deal easier and more accretive.

Fourth, the stock trades at a meaningful discount to food industry peers, partly because the company's complexity makes it harder for generalist investors to model. This complexity — four segments across different categories, geographies, and channels — creates an analytical barrier that depresses the multiple. For patient investors willing to do the work, this complexity discount represents an opportunity rather than a risk.

The bearish case is equally substantive.

The structural decline in cereal consumption shows no signs of reversing. Younger consumers are abandoning traditional breakfast in favor of convenience options, protein-forward alternatives, or no breakfast at all. GLP-1 drugs amplify this trend by reducing overall caloric intake, with cereal — as a calorie-dense processed food — particularly exposed. Post Consumer Brands reported cereal volume declines of 5.1 percent in the most recent quarter, continuing a pattern that has persisted for years. The cereal business generates substantial cash flow today, but the long-term trajectory is unmistakably negative.

Post's debt load, at roughly 7.4 billion dollars with a net leverage ratio of approximately 4.3 times EBITDA, limits flexibility. To put that in perspective, most investment-grade food companies operate with leverage ratios between one and three times EBITDA. Post's higher leverage reflects the residual borrowing from its acquisitive strategy — each major deal added debt that takes years to pay down through free cash flow. In a benign interest rate environment with stable cash flows, this leverage is manageable and even value-enhancing. But in a scenario where multiple business units face simultaneous headwinds — a sustained egg supply disruption from avian influenza, accelerating cereal declines, and pet food distribution losses — the debt burden could constrain management's options precisely when flexibility is most needed.

Retailer concentration poses a structural risk that is unlikely to diminish. Walmart, Costco, and Amazon will continue to gain share of grocery distribution, and their bargaining power will only increase. Post's private label business partially addresses this risk — you are more valuable to a retailer when you make their store brands — but it does not eliminate it. Margin pressure from powerful buyers is a permanent feature of the food industry landscape.

The M&A pipeline raises its own questions. Post has demonstrated extraordinary skill in acquiring and integrating food businesses. But the easy deals have been done. The most attractive targets have either been acquired, taken private, or become too expensive. Finding the next Michael Foods or Bob Evans — a dominant niche player available at a reasonable price — becomes harder as the industry consolidates and competition for deals intensifies. Private equity firms, flush with capital, now compete aggressively for the same food assets that Post targets. Strategic buyers like Conagra, General Mills, and even international food companies have become more acquisitive. The arbitrage that Post exploited so successfully — buying unloved food assets at low multiples when Wall Street was fixated on high-growth technology and health food brands — may be harder to replicate in a world where every investor has read "The Outsiders" and understands the roll-up playbook.

A note on accounting: Post's financial statements are more complex than most food companies because of its frequent M&A activity, corporate restructurings, and the resulting goodwill and intangible assets on the balance sheet. As of late 2025, the company carried approximately ten billion dollars in goodwill and intangible assets — a figure that reflects the cumulative premium paid above book value for all its acquisitions. This is typical for serial acquirers but means that a significant write-down (triggered by underperformance in any acquired business) could materially impact reported earnings. The less-than-300-million in total impairment charges since 2012 is remarkably low relative to the total goodwill, but it is a risk that warrants monitoring, particularly for the more recently acquired pet food brands and the reacquired 8th Avenue operations.

Three KPIs warrant close monitoring for anyone tracking Post Holdings' ongoing performance. First, organic volume trends by segment — particularly cereal and pet food volumes, which reveal whether the underlying businesses are stable or deteriorating beneath the M&A-driven revenue growth. Second, free cash flow conversion — the ratio of free cash flow to adjusted EBITDA, which measures whether the company's reported profitability is translating into actual cash that can fund acquisitions, buybacks, and debt reduction. Third, return on invested capital on recent acquisitions — particularly the Smucker pet food brands and the reacquired 8th Avenue operations — which will determine whether Post's M&A machine continues to create value or has begun to show diminishing returns.

XIV. The Big Picture: What Post Tells Us About American Food

Consolidation, Reinvention, and the Future of How We Eat

The story of Post Holdings is, in miniature, the story of how Americans eat — and how the business of feeding America has evolved over 130 years.