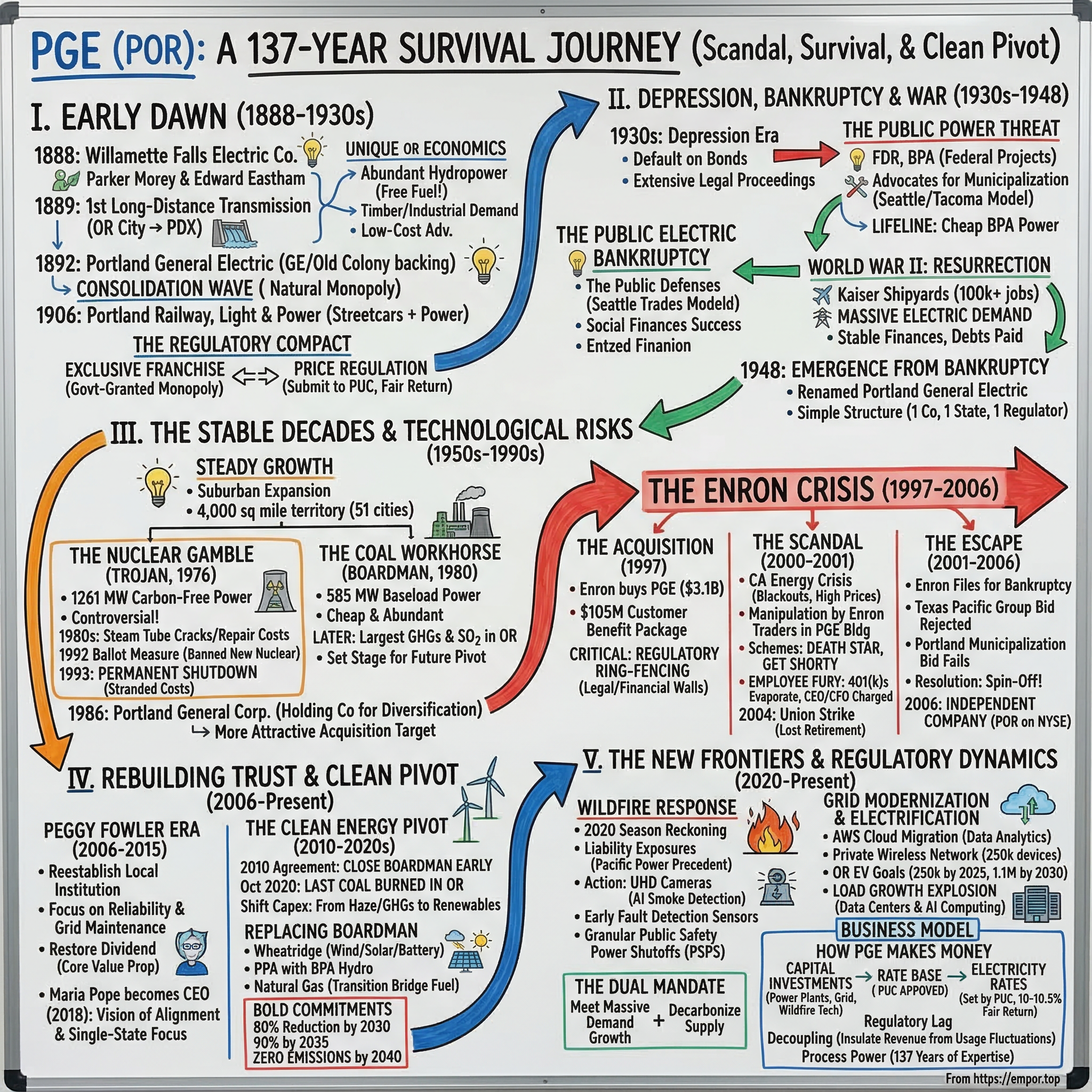

Portland General Electric: Survival, Scandal, and the Clean Energy Pivot

I. Introduction & Episode Roadmap

Picture downtown Portland, Oregon, in the winter of 2001. Inside a nondescript office building on Southwest Salmon Street, two very different companies shared the same address. On some floors, Portland General Electric employees kept the lights on for nearly a million Oregonians, dispatching linemen into ice storms and managing hydroelectric dams on the Clackamas River. On other floors, Enron energy traders invented schemes with names like "Death Star" and "Get Shorty," manipulating California's electricity markets in what would become one of the greatest corporate frauds in American history.

The same building. The same parent company. Two utterly different missions.

That surreal cohabitation captures everything that makes Portland General Electric one of the most fascinating utility stories in American business. PGE is Oregon's largest electric utility, serving roughly 950,000 customers across 51 cities and powering almost two-thirds of the state's commercial and industrial activity. But the numbers only hint at the drama. This is a company that pioneered long-distance electricity transmission in 1889, went bankrupt during the Great Depression, got swallowed by Enron, survived the largest corporate scandal of the early 2000s, and then emerged as one of the nation's most aggressive clean energy utilities.

It is the ultimate survivor story.

The central question driving this deep dive is deceptively simple: How does a company founded 137 years ago survive bankruptcy, scandal, and the most fundamental transformation the energy industry has ever faced? The answer reveals something profound about regulated utility economics, about the power of local governance, and about what happens when an industry built on burning things must learn to harness the wind and sun instead.

PGE's story touches on themes that matter far beyond Oregon. The regulated utility model itself, where a company gets a government-granted monopoly in exchange for accepting price controls, is one of the oldest social contracts in American capitalism. The Enron debacle tested whether that contract could survive corporate predation. And now, the clean energy transition is testing whether it can survive the most capital-intensive infrastructure buildout since rural electrification.

Along the way, there are labor strikes, nuclear plant shutdowns, wildfire crises, and the perpetual tension between keeping electricity affordable and keeping the planet habitable.

What makes PGE's story uniquely compelling for business analysis is its scale. This is not a giant multi-state holding company like NextEra or Duke Energy. PGE serves one state, one region, one community. That intimacy means every decision, from closing a coal plant to raising rates to fighting a wildfire, plays out under intense local scrutiny. It also means that PGE's story is, in many ways, the story of Oregon itself: progressive, environmentally conscious, fiercely independent, and perpetually wrestling with the tension between idealism and pragmatism.

The journey begins in 1888, at the base of a waterfall in Oregon City, where two entrepreneurs had an idea that would change the Pacific Northwest forever.

II. The Dawn of Electric Power in the Pacific Northwest (1888-1930s)

Stand at the edge of Willamette Falls in Oregon City today and you see a 1,500-foot-wide curtain of water plunging forty feet into a churning basin of basalt. In 1888, this was one of the most powerful natural features in the American West, and two men—Parker F. Morey and Edward L. Eastham—looked at all that kinetic energy and saw something nobody else had figured out how to capture: electricity, transmitted over distance, to power a city fourteen miles away.

The Willamette Falls Electric Company, as they named their venture, was not the first power company in America. Thomas Edison had already lit up parts of Manhattan. But what Morey and Eastham accomplished was genuinely revolutionary. On June 3, 1889, they sent power from a generator at the base of Willamette Falls across fourteen miles of wire to downtown Portland—among the first long-distance transmissions of electricity for commercial use in the United States.

The achievement was not just technical; it was conceptual. Edison's model required a power plant on every city block. The Willamette Falls model proved that you could generate power where nature provided it and deliver it where people needed it. That insight—generation separated from consumption by a transmission network—remains the fundamental architecture of the electric grid 137 years later.

Why Oregon?

The Pacific Northwest was uniquely suited for hydroelectric development. The Cascade Range funneled enormous volumes of snowmelt through steep river valleys, creating natural "head"—the vertical drop that spins turbines—at dozens of sites. To understand why this matters, think of hydroelectricity as the original renewable energy source. Coal required constant extraction, transportation, and combustion. Oil required drilling and refining. But a waterfall just keeps falling, year after year, converting gravity into kilowatts with no fuel cost whatsoever. Oregon's rivers offered something that coal-dependent Eastern utilities could not match: fuel that literally fell from the sky, for free.

The region was also industrializing rapidly. Portland was becoming a major lumber and shipping hub, and sawmills, grain elevators, and streetcar lines all needed power. The Pacific Northwest's timber industry was voracious: sawmills ran around the clock, and the electric motor was replacing steam in factory after factory. The combination of cheap, abundant hydroelectricity and growing industrial demand made Oregon a natural laboratory for the electric utility business.

The economics were remarkable. While Edison's coal-fired plants in New York charged premium rates and served a few square blocks, the Willamette Falls operation could generate power at a fraction of the cost and deliver it across a wide area. This cost advantage would become a defining characteristic of the Pacific Northwest economy for the next century, attracting energy-intensive industries—aluminum smelting, paper mills, and eventually, in the twenty-first century, data centers—that were drawn to the region's cheap electricity like moths to a flame.

By 1892, the enterprise had reorganized and expanded. General Electric, the industrial colossus founded by Edison and J.P. Morgan, partnered with Old Colony Trust of Boston to inject $4.25 million in capital and reincorporate the company as Portland General Electric. The name was no accident. Attaching "General Electric" lent credibility and signaled ambition. PGE was no longer a scrappy startup running a single transmission line; it was a properly capitalized utility with Eastern financial backing and the imprimatur of the most powerful name in the electricity business.

The Consolidation Wave

What followed was a period of aggressive consolidation that would look familiar to anyone who has studied the rollup strategies of cable companies or pharmacy chains a century later. PGE bought competitors, absorbed municipal utilities, and expanded its service territory across the Portland metropolitan area.

The logic was straightforward: electricity distribution is a natural monopoly. The cost of stringing wires to every home and business is so enormous that it only makes sense for one company to do it in any given area. Duplicating the infrastructure would be ruinous for everyone. So the race was on to claim territory before someone else did.

The consolidation wave crested in 1906 with a mega-merger that created the Portland Railway, Light and Power Company, combining streetcar operations, electric service, and water utilities into a single entity. This was the era of the "utility empire," when companies like Samuel Insull's Commonwealth Edison in Chicago were building vast holding company structures that controlled everything from generation to distribution to the streetcar you rode to work.

The Regulatory Compact

This era also saw the emergence of the regulated utility model that still governs PGE today. The basic bargain was elegant: the state grants a utility an exclusive franchise to serve a territory, eliminating wasteful competition. In exchange, the utility submits to price regulation—a government commission reviews its costs and sets rates that allow a "fair" return on invested capital, but no more.

The utility gets a guaranteed market; customers get protection from monopoly pricing. It was one of the earliest examples of what economists now call a "regulatory compact," and understanding it is essential to understanding everything that follows in PGE's story. Every strategic decision—from building a nuclear plant to closing a coal plant to investing in wildfire cameras—ultimately flows through this compact. The utility proposes, the regulator disposes, and shareholders get their return only if the commission agrees the spending was prudent.

By the late 1920s, PGE's predecessor was a mature, profitable operation serving a growing city. Portland was booming, powered by timber, shipping, and cheap hydroelectricity. But the good times were about to end, and the same leverage that had fueled expansion would nearly destroy the company when the economy collapsed.

III. Depression, Bankruptcy, and WWII Resurrection (1930s-1948)

The Great Depression did not arrive in Portland with a single dramatic crash. It crept in through falling lumber prices, declining shipping volumes, and a slow erosion of the industrial demand that kept the generators spinning. By 1939, Portland Railway, Light and Power defaulted on its bonds, triggering what historians later described as "one of the most prolonged and complicated series of legal proceedings in Portland's history."

The bankruptcy was not just a financial event; it was an existential crisis for the concept of private utility ownership in Oregon.

The Public Power Threat

To understand why, you need to appreciate the political context. The 1930s were the heyday of the public power movement—a nationwide campaign to replace private utilities with government-owned systems. President Franklin Roosevelt championed the Tennessee Valley Authority and the Bonneville Power Administration, massive federal projects that delivered cheap hydroelectricity and, not coincidentally, undercut the business model of private utilities.

In Oregon, the BPA began selling power from the newly completed Bonneville Dam on the Columbia River in 1938, and public power advocates argued that Portland should follow the example of cities like Seattle and Tacoma, which had already municipalized their electric systems. The bankruptcy of Portland's private utility seemed to validate everything the public power advocates were saying. Here was a private company, leveraged to the hilt by out-of-state holding company owners, failing to serve the public interest. Why not let the government take over?

The answer, ironically, came from the same federal government that was building the dams. The Bonneville Power Administration offered wholesale electricity at rates so low that even a struggling private utility could buy BPA power and resell it at a profit. The arrangement kept the lights on and gave the company a lifeline during the worst years of the Depression.

The War Changes Everything

Then came Pearl Harbor, and everything changed.

World War II transformed the Portland economy almost overnight. The Kaiser Shipyards, the largest shipbuilding operation in American history, set up shop along the Willamette and Columbia rivers, employing over 100,000 workers at peak production. The shipyards devoured electricity, and Portland's utility was suddenly running at full capacity, generating nearly $400,000 in revenue from Kaiser alone—serious money in the early 1940s, enough to stabilize the company's finances and begin paying down the debts that had triggered bankruptcy.

The war years demonstrated a principle that has saved PGE more than once in its history: infrastructure monopolies are extraordinarily resilient. As long as people need electricity—and they always do—the company generating and delivering it has a floor under its revenue that almost no other business enjoys. A restaurant can lose all its customers. A manufacturer can be undercut by imports. But an electric utility, even one in bankruptcy, continues to collect revenue from every home and business in its territory, every month, rain or shine.

The Fresh Start

In 1948, the company emerged from bankruptcy reorganized and renamed as Portland General Electric. The restructuring eliminated the old holding company layers, wrote down excessive debt, and established PGE as a standalone Oregon utility. The new corporate structure was deliberately simple: one company, one state, one regulatory jurisdiction. No more byzantine holding company layers where profits could be siphoned upstream and risks could be hidden in opaque subsidiary structures.

The timing could not have been better. Post-war America was about to experience the greatest period of suburban expansion in history, and every new house in every new subdivision needed electricity. Oregon's population would grow by more than fifty percent between 1940 and 1960, driven by the war workers who had moved west for Kaiser Shipyards jobs and decided to stay. Every one of those new Oregonians needed lights, refrigerators, televisions, and eventually air conditioning. PGE was positioned to serve them all.

The lesson for investors is worth pausing on: PGE's first bankruptcy was caused by excessive leverage and holding company mismanagement, not by any failure of the underlying utility business. The wires, the dams, the customer relationships—all survived intact. The equity holders got wiped out, but the essential enterprise endured. It is a pattern that would repeat, with eerie precision, sixty years later. And it reveals something fundamental about utilities as a business: the physical assets and customer relationships are nearly indestructible, but the financial structures layered on top of them can be dangerously fragile.

IV. The Stable Decades: Building the Modern Grid (1950s-1990s)

The three decades following PGE's 1948 reorganization were, by the standards of this story, almost boring—and that was exactly the point. The company settled into the steady, predictable rhythm that defines a well-run regulated utility: build infrastructure, grow the rate base, earn your allowed return, pay dividends, repeat.

Portland's suburbs sprawled outward into Washington County, Clackamas County, and the Willamette Valley. Every new housing development meant new substations, new distribution lines, and new customers. PGE's service territory expanded to cover 4,000 square miles across 51 cities—a patchwork of dense urban neighborhoods, suburban cul-de-sacs, and rural farmland stretching from the Columbia River to the Cascade foothills.

The Nuclear Gamble

The most consequential decision of this era was also the most controversial: the Trojan Nuclear Plant. Authorized in the late 1960s during a period of boundless nuclear optimism, Trojan was Oregon's only commercial nuclear power station—a 1,261-megawatt behemoth located on the Columbia River about forty miles northwest of Portland.

Think of a megawatt as roughly enough power for 750 to 1,000 homes. Trojan alone could have powered a city the size of Eugene. The plant began commercial operation in 1976 and, for a time, delivered exactly what its proponents promised: enormous amounts of carbon-free baseload power at relatively low marginal cost.

But nuclear power is a business of extremes. The upfront capital costs are staggering, the regulatory burden is immense, and when things go wrong, they go very wrong. By the late 1980s, inspectors discovered cracks in Trojan's steam generator tubes—the same type of degradation that had plagued nuclear plants across the country. The repair costs were enormous, and public opposition to nuclear power, amplified by the Chernobyl disaster in 1986, made the political environment toxic.

In 1993, PGE shut down Trojan permanently, just seventeen years into what was supposed to be a forty-year operating life. The closure left PGE with a massive stranded investment and a hole in its generation portfolio that would take decades to fill. Oregon voters then passed a ballot measure in 1992 that effectively banned new nuclear plants in the state, ensuring that PGE's nuclear chapter was closed for good.

The Trojan saga offers a timeless lesson about technology risk in regulated industries. PGE had made a rational bet given the information available in the 1960s: nuclear power appeared to be the future of cheap, clean electricity. But the economics shifted, the technology proved more fragile than expected, and public opinion turned hostile. Regulators ultimately allowed PGE to recover most of the stranded costs from customers, but the experience left scars—both on PGE's balance sheet and on the institutional memory of a company that had learned the hard way what happens when a massive capital bet goes wrong.

The Coal Workhorse

The other major asset from this era was the Boardman Coal Plant, authorized in 1975 and operational by 1980. Boardman was a conventional 585-megawatt coal-fired station in eastern Oregon that produced roughly fifteen percent of PGE's total electricity. Coal was cheap and abundant, and Boardman provided the kind of reliable baseload power that utilities craved.

But it came with a cost that would not be fully reckoned for decades: Boardman accounted for approximately sixty-five percent of Oregon's stationary sulfur dioxide emissions and was by far the largest single source of greenhouse gases in the state. In the 1970s, nobody worried about carbon dioxide. By the 2000s, everyone was.

Setting the Stage for Enron

In 1986, PGE underwent a corporate restructuring that created a holding company, Portland General Corporation, to house both the regulated utility and a portfolio of non-utility businesses. This was a common playbook in the 1980s: utilities created holding companies to diversify into unregulated ventures, hoping to earn higher returns than regulators allowed on the core utility business.

The strategy rarely worked well, and at PGE, it had an unintended consequence. The holding company structure made PGE a more attractive acquisition target, because a buyer could purchase the holding company and gain control of the regulated utility without navigating the same level of regulatory scrutiny that a direct utility acquisition would require.

That vulnerability would prove fateful. By the mid-1990s, the electric utility industry was swept up in a wave of deregulation enthusiasm. States like California were experimenting with competitive electricity markets, and energy trading companies were emerging as the new titans of the power business. The biggest and most aggressive of them was a Houston-based company called Enron, and it had its eye on Portland.

V. The Enron Era: Acquisition and Crisis (1997-2006)

The Deal

On July 1, 1997, Enron completed its acquisition of Portland General Electric in a deal valued at approximately $3.1 billion: $2 billion in Enron stock plus $1.1 billion in assumed debt. For PGE shareholders, it was a windfall—a nearly fifty percent premium over the pre-deal stock price. For Enron, it was a strategic chess move. The company was building the world's largest energy trading operation, and owning an actual utility with physical generation assets and real-time market data gave Enron something its purely paper-based trading business lacked: credibility, infrastructure, and a window into how electricity actually flowed through the Western grid.

Oregon regulators approved the deal, but not without conditions. Enron agreed to a $105 million customer benefit package—essentially a payment to Oregonians to accept out-of-state corporate ownership. The package included rate credits, economic development funds, and commitments to maintain PGE's headquarters and workforce in Portland.

Regulators also insisted on "ring-fencing" provisions—legal and financial walls designed to prevent Enron from draining PGE's assets or commingling its finances with the parent company's increasingly exotic operations. Those ring-fencing provisions, bureaucratic and unglamorous as they were, would later prove to be the single most important decision in PGE's modern history.

The Scandal Unfolds

The Enron years began with promises of synergy and innovation. Enron relocated its West Coast energy trading operations into PGE's downtown Portland offices, and for a brief moment, the marriage seemed productive. PGE employees gained access to Enron's sophisticated risk management systems, and Enron's traders gained proximity to the physical assets and grid knowledge they needed to trade Western electricity markets.

Then the California energy crisis hit.

In 2000 and 2001, California experienced rolling blackouts, skyrocketing wholesale electricity prices, and a cascading failure of its newly deregulated electricity market. It later emerged that Enron traders, operating from PGE's Portland offices, had been central to the manipulation. Timothy Belden and John Forney, working from trading desks in the same building where PGE dispatchers managed the utility's generation fleet, invented strategies with darkly playful names.

"Death Star" involved scheduling phantom power flows on congested transmission lines to collect congestion payments. "Get Shorty" involved selling power California did not need, then buying it back at inflated prices. These were not abstract financial maneuvers; they caused real suffering, contributing to blackouts that shut down businesses and endangered lives.

The human toll inside PGE was devastating. PGE's own CEO, Joseph Hirko, and CFO were charged with federal felonies related to Enron Broadband—a separate Enron subsidiary that had nothing to do with PGE's utility operations but whose executives overlapped with PGE's leadership. Meanwhile, PGE employees watched their retirement savings evaporate. Like thousands of Enron employees nationwide, many PGE workers had loaded their 401(k) plans with Enron stock, which collapsed from over ninety dollars per share to less than a dollar during 2001.

In March 2004, nine hundred PGE union workers walked off the job, striking over lost retirement benefits and demanding that the company make them whole. It was the first utility strike in Portland in decades, underscoring the fury that Oregonians felt toward a company that had plundered their community.

The Tax Scandal

Perhaps the most galling detail emerged years later in regulatory proceedings. From 1997 through 2005—the entire period of Enron's ownership—neither PGE nor Enron paid any state income taxes in Oregon. In fact, PGE received a net refund of approximately $34,000 from the state.

This was despite the fact that PGE had been collecting income tax payments from its customers through their electricity bills, a standard practice where utilities include an allowance for taxes in their rates. The money that customers thought was paying PGE's tax obligations was instead flowing up to Enron's corporate structure, where a labyrinth of offshore entities and tax shelters ensured that none of it reached the Oregon treasury. When this came to light, it became a rallying cry for public power advocates and consumer groups who argued that private utility ownership was inherently corrupt.

The Escape

Enron filed for bankruptcy on December 2, 2001, and PGE became one of the most valuable assets in the bankruptcy estate. What followed was a four-year chess match over who would control Oregon's largest utility.

In November 2003, Texas Pacific Group, the private equity firm, offered $2.35 billion to acquire PGE from the bankruptcy estate. Oregon's Public Utility Commission spent over a year scrutinizing the deal before rejecting it in March 2005, concluding that private equity ownership would not serve the public interest.

Meanwhile, the City of Portland launched an ambitious bid to municipalize PGE, proposing to issue $3 billion in bonds to buy the utility and convert it to public ownership. The plan was modeled on successful municipal utilities in cities like Sacramento and Los Angeles, but it ultimately collapsed when Enron's bankruptcy CEO, Stephen Cooper, broke off negotiations after the city refused to put up a $50 million good-faith deposit.

The resolution, when it finally came, was elegant in its simplicity. On April 3, 2006, PGE became an independent company once more. Enron's bankruptcy court ordered the distribution of 62.5 million PGE shares directly to Enron's creditors, who could then sell them on the open market. PGE listed on the New York Stock Exchange under the ticker "POR," and for the first time in nearly a decade, the company's future was in the hands of its own management and shareholders.

Playbook Insights

The Enron era taught several enduring lessons. First, regulatory ring-fencing works. The legal walls that Oregon regulators insisted on in 1997 prevented Enron from using PGE's assets as collateral for its own debts, shielded PGE's customer rates from Enron's financial engineering, and ultimately preserved the utility's operational integrity through the worst corporate bankruptcy in American history.

Second, utility assets are almost indestructible. PGE's wires, substations, dams, and customer relationships survived Enron's collapse completely intact. The financial ownership changed hands multiple times, but the physical business never missed a beat.

Third, communities will fight ferociously to maintain local control over essential infrastructure. Portland's attempted municipalization, Oregon's rejection of the TPG deal, and the eventual return to independence all reflected a deep conviction that electricity should not be a pawn in someone else's financial game.

The company that emerged from the Enron wreckage was battered, embarrassed, and deeply mistrusted. Rebuilding would require more than new management—it would require a fundamental reimagining of what PGE stood for.

VI. Rebuilding Trust & Identity (2006-2015)

When PGE's new board of directors held its first meeting as an independent company in April 2006, five of its members were Oregonians. That was not a coincidence. It was a deliberate signal. After nearly a decade of being owned by an out-of-state energy conglomerate synonymous with corporate fraud, PGE needed to re-establish itself as a local institution, accountable to Oregon and governed by people who lived in the communities it served.

The Peggy Fowler Era

CEO Peggy Fowler, who had been running PGE through the final years of the Enron ordeal, understood that rebuilding trust was not primarily a communications challenge. It was an operational one. Customers did not need to be told that PGE was different from Enron; they needed to experience it through reliable service, responsive customer support, and transparent decision-making.

Fowler focused on the fundamentals: reducing outage times, investing in grid maintenance, and restoring the dividend that shareholders had gone without during the bankruptcy years. For a utility, the dividend is not a nice-to-have; it is the core value proposition for investors. Utilities are essentially bond substitutes with modest growth potential, and a consistent, growing dividend signals that management is executing the regulatory compact properly.

Financial Stabilization

The financial stabilization was methodical. PGE re-established credit ratings, refinanced debt on favorable terms, and resumed regular dividend payments. The company also had to rebuild relationships with Wall Street analysts and institutional investors who had spent years associating the PGE name with Enron's collapse. Fowler and her team hit the road, meeting with investors, explaining PGE's standalone financials, and making the case that this was now a clean, well-run Oregon utility with no Enron baggage attached.

PGE's ability to restore the regulatory compact after the chaos of the Enron years was a meaningful accomplishment—not flashy, but exactly the kind of disciplined execution that income-oriented investors prize. The stock, which had traded around twenty dollars in the months after the Enron spinoff, began a steady climb as investors recognized that PGE's underlying business was sound and that the Enron stigma was fading.

The Independence Question

The deeper strategic challenge was existential: What should PGE be in a consolidating utility industry? Across the country, utilities were merging into massive multi-state holding companies. Exelon, Duke Energy, Southern Company, and NextEra were assembling portfolios of utilities spanning dozens of states and serving tens of millions of customers. The logic was compelling: scale brings procurement efficiencies, regulatory diversification, and access to cheaper capital.

PGE, with its single state, single regulatory jurisdiction, and roughly one million customers, was tiny by comparison. Every few years, speculation surfaced that PGE would be acquired by a larger utility—a prospect that generated equal parts excitement among shareholders hoping for a premium and anxiety among Oregonians worried about losing local control again.

PGE's leadership chose independence. Maria Pope, who succeeded Fowler and became CEO in 2018, brought a distinctive background to the role. A Stanford-educated executive who had served as PGE's CFO and Senior Vice President of Power Supply, Pope understood both the financial engineering of utility regulation and the operational complexity of running a generation fleet. She articulated a vision that leaned into PGE's smallness as a strategic advantage.

Her argument was compelling: a single-state utility answering to a single regulatory commission could move faster, build deeper community relationships, and align more naturally with local priorities than a sprawling conglomerate managing competing regulatory agendas across a dozen jurisdictions. Consider the contrast with PacifiCorp, PGE's neighbor, which serves customers in six Western states and must navigate six different regulatory commissions with six different sets of priorities. When Oregon wanted aggressive coal retirement, PacifiCorp had to balance that against the interests of customers in Wyoming and Utah, where coal was still an economic engine. PGE faced no such tension. Oregon wanted clean energy, and PGE could deliver it without compromise.

Oregon was becoming one of the most environmentally progressive states in the country, passing landmark legislation including House Bill 2021 in 2021, which mandated one hundred percent clean electricity by 2040. PGE positioned itself to lead, rather than follow, on clean energy—and its single-state focus made that alignment seamless.

The Payoff

The results spoke for themselves. By 2024, PGE had earned the top ranking in the Forrester U.S. Customer Experience Index for utilities—a distinction that mattered far more than it might seem. In a regulated industry, customer satisfaction is not just a feel-good metric; it is a regulatory asset. A utility that customers trust and respect has an easier time winning rate cases, gaining approval for capital investments, and navigating contentious decisions like plant closures or rate increases.

PGE's journey from Enron's most embarrassing subsidiary to the most trusted utility in America was, in its quiet way, one of the more impressive corporate turnarounds of the 2000s. The company's value lay not in scale but in alignment: alignment with Oregon's political priorities, alignment with customer expectations, and alignment with a regulatory commission that could either be PGE's greatest ally or its most formidable obstacle.

That alignment was about to be tested in the most ambitious undertaking in PGE's history.

VII. The Clean Energy Pivot: Coal Retirement & Renewables (2010-2020)

The Boardman Decision

In 2010, representatives from PGE, the Oregon Department of Environmental Quality, the U.S. Forest Service, and several environmental groups sat down at a negotiating table to discuss the future of the Boardman Coal Plant. Under its existing permits, Boardman could have continued burning coal until 2040. But the environmental costs were mounting. Boardman was the largest single source of haze-causing pollution affecting the Columbia River Gorge, one of Oregon's most treasured natural landscapes.

The question was straightforward: invest half a billion dollars in pollution controls to keep Boardman running for another thirty years, or shut it down early and replace it with something cleaner.

PGE chose the latter.

The 2010 agreement to close Boardman twenty years ahead of schedule was a watershed moment—not just for PGE, but for the entire Pacific Northwest. It was one of the earliest voluntary coal retirement commitments by a major U.S. utility, establishing PGE as a first mover in a trend that would sweep across the industry over the following decade.

The decision was economically rational, not just environmentally virtuous. The $500 million that pollution controls would have required was capital that PGE could instead invest in new renewable generation, which would earn the same regulated return but position the company for a decarbonizing future rather than anchoring it to a depreciating past. In utility economics, this is the fundamental insight: a regulated utility earns its return on whatever it builds, so the question is never whether to invest but what to invest in.

Boardman burned its last lump of coal in October 2020, ending coal-fired power generation in Oregon permanently. The smokestack, a visible landmark of eastern Oregon for forty years, was demolished in September 2022.

The Replacement Strategy

Replacing Boardman's output required a diverse portfolio of new resources. The flagship project was the Wheatridge Renewable Energy Facility in eastern Oregon—a first-of-its-kind installation combining 300 megawatts of wind capacity, 50 megawatts of solar, and 30 megawatts of battery storage at a single site.

Think of Wheatridge as a power plant that works in shifts: wind turbines generate at night and during storms, solar panels take over on clear days, and batteries smooth out the gaps. When Wheatridge came online in 2020 and 2021, it was one of the largest co-located wind, solar, and storage facilities in North America.

But Wheatridge alone could not fill the gap. PGE assembled a portfolio approach: securing five-year power purchase agreements with the Bonneville Power Administration for hydroelectric output, contracting with Douglas County PUD and independent suppliers, and building out its own natural gas fleet as a transitional bridge fuel.

The company's gas portfolio—including the Beaver plant at 508 megawatts, Port Westward at 636 megawatts, and the Carty Generating Station at 437 megawatts—provided the dispatchable capacity that wind and solar could not guarantee. PGE also expanded its wind holdings through the Biglow Canyon Wind Farm at 450 megawatts and the Tucannon River Wind Farm at 267 megawatts. Simultaneously, the company worked to exit its remaining coal exposure through the Colstrip plant in Montana, targeting a departure by the end of 2025.

Bold Commitments

The strategic commitment that emerged from this period was breathtaking in its ambition. PGE set targets to reduce greenhouse gas emissions by eighty percent by 2030, ninety percent by 2035, and to achieve zero emissions by 2040. Most U.S. utilities were targeting net-zero by 2050 at the earliest. PGE was pledging to get there a full decade sooner.

Achieving those targets requires enormous capital investment. PGE's integrated resource plan calls for adding 1,500 to 2,000 megawatts of new clean energy resources plus approximately 800 megawatts of non-emitting dispatchable capacity by 2030. That means nearly tripling the company's clean energy portfolio in less than a decade.

For context, 2,000 megawatts is roughly the equivalent of two large nuclear power plants or approximately 600 to 800 modern wind turbines. The capital required runs into the billions.

Why Move Faster Than Required?

Part of it was Oregon's political environment—the state's renewable portfolio standard created a regulatory expectation that utilities would lead on clean energy. Part of it was customer demand; PGE runs the largest voluntary renewable energy program in the country, with customers actively paying more for green power. And part of it was simple utility economics: every dollar invested in new generation earns a regulated return, and clean energy projects, with their federal tax credits and declining costs, offered attractive economics even before factoring in the policy tailwinds.

For investors, the clean energy pivot transformed PGE's investment thesis. The company was no longer a slow-growth, dividend-focused utility clinging to legacy assets. It was a capital-deployment story with a multi-decade runway, all earning regulated returns in a supportive political environment. But could PGE build all of this fast enough, affordably enough, and reliably enough?

That question became even more urgent as a new set of challenges emerged.

VIII. The New Frontiers: Wildfires, Grid Modernization & Electrification (2020-Present)

The 2020 Fire Season

September 2020 was unlike anything Oregon had experienced in living memory. A convergence of extreme east winds and bone-dry conditions sent wildfires racing across the state, burning over a million acres in a single week. The skies over Portland turned an apocalyptic orange, air quality reached levels worse than Beijing's on its worst days, and hundreds of thousands of Oregonians fled their homes. PGE's infrastructure was directly in the path of several fires, and the company scrambled to de-energize lines, reroute power, and keep critical facilities operational while its own equipment was threatened.

The 2020 fire season was a reckoning for every utility in the Western United States. In California, Pacific Gas & Electric had already been driven into bankruptcy by wildfire liabilities exceeding $30 billion. Closer to home, PGE's neighbor Pacific Power faced a $1.6 billion lawsuit over the 2020 Beachie Creek Fire, which destroyed hundreds of homes in the Santiam Canyon. The precedent was terrifying: a single fire, started by or attributed to utility equipment, could wipe out years of earnings and threaten the company's solvency.

PGE's Wildfire Response

PGE responded by investing aggressively in wildfire prevention and detection, treating it not as a cost center but as an existential priority. The company deployed a network of ultra-high-definition mountaintop cameras—starting with 33 and growing to 35—each equipped with AI-powered image analysis capable of detecting smoke plumes up to ten miles away.

These are not ordinary security cameras. They capture panoramic views every few seconds and feed the imagery to machine learning algorithms trained to distinguish wildfire smoke from clouds, dust, and fog. When the system flags a potential fire, it alerts PGE operators and local fire agencies simultaneously, shaving critical minutes off response times. In wildfire, minutes matter enormously; a fire contained at ten acres is manageable, while one that grows to a thousand acres before detection can become catastrophic.

Beyond detection, PGE installed smart grid devices in high fire risk zones that can automatically de-energize power lines when conditions become dangerous. These Public Safety Power Shutoffs, or PSPS events as the industry calls them, are the utility's equivalent of a controlled demolition: deliberately cutting power to prevent equipment from starting a fire. It is a blunt tool—inconvenient for customers who suddenly lose electricity for hours or even days—but far preferable to the alternative of a billion-dollar wildfire lawsuit.

The key innovation in PGE's approach was granularity. Rather than shutting down power to entire counties, as California utilities had done to widespread public fury, PGE's smart grid devices enabled more targeted shutoffs, cutting power to specific circuits in specific high-risk areas while keeping the rest of the grid running. This required enormous investment in grid sectionalization—essentially adding more switches and sensors so the utility could isolate smaller portions of the network.

PGE also deployed early fault detection technology: sensors that monitor power lines and equipment in real time, identifying degradation before it causes a failure. A cracked insulator, a sagging wire, a tree branch growing too close to a line—these are the ignition sources that start utility-caused wildfires, and catching them early is far cheaper than litigating them later. The investment in wildfire technology also carries a regulatory benefit: a utility that can demonstrate proactive risk management is in a far stronger position if a fire does occur than one that is perceived to have been negligent.

Grid Modernization

The wildfire threat accelerated PGE's broader grid modernization program. In March 2019, PGE had begun migrating its data infrastructure to Amazon Web Services, enabling advanced data analytics and machine learning capabilities impractical on legacy systems. The cloud migration was about processing the torrent of data streaming from hundreds of thousands of grid sensors, weather stations, and wildfire cameras in real time.

One of the most innovative investments was PGE's deployment of a private wireless network covering its entire 4,000-square-mile service territory. This network connects roughly 250,000 devices—from smart meters to distribution automation equipment to wildfire cameras—at approximately one-tenth the cost of building out traditional communications infrastructure. For a utility, reliable communications with field equipment is not a luxury; it is the difference between knowing what is happening on the grid in real time and flying blind.

PGE's Distribution System Plan envisions a fourfold increase in distributed solar and storage by 2030, reaching approximately 500 megawatts. Distributed energy—solar panels on rooftops and batteries in garages—creates both opportunities and challenges. It reduces the need for centralized generation but complicates grid management enormously, as the utility must now balance power flowing in two directions instead of one.

The Electrification Wave

The demand growth hitting PGE's territory adds urgency to all of this. Oregon set ambitious goals for electric vehicle adoption—250,000 EVs by 2025 and 1.1 million by 2030. Every EV is essentially a new appliance drawing power from the grid, and a million of them represents a massive increase in electricity demand, particularly during evening hours when drivers plug in at home.

Add the growth of data centers and AI computing facilities—some of the most electricity-intensive industrial operations ever built—and PGE faces a demand growth trajectory that would have been unimaginable a decade ago. A single large AI training facility can consume as much electricity as a small city, and the Pacific Northwest's combination of cheap hydropower, cool climate (which reduces cooling costs), and abundant fiber optic connectivity has made Oregon a magnet for data center development. PGE has seen significant interest from hyperscale data center operators, and the load growth projections have repeatedly been revised upward.

This creates what utility planners call the "dual mandate" problem: PGE must simultaneously build for massive demand growth and decarbonize its supply. Building more gas plants would solve the capacity problem but undermine the emissions targets. Building only renewables would advance decarbonization but might not provide enough reliable capacity for a grid that data centers demand be available 99.999 percent of the time.

Federal tax credit uncertainty, trade policy impacts on solar panel and battery imports, transmission constraints, and workforce shortages in skilled electrical trades all threaten to slow the buildout. The Inflation Reduction Act's generous clean energy tax credits made the math work for many renewable projects, but those credits face political headwinds, and any reduction would increase PGE's costs and, ultimately, customer rates. Trade tariffs on Chinese solar panels and batteries, which have been imposed and modified multiple times in recent years, add another layer of cost uncertainty to every procurement decision.

IX. Business Model & Regulatory Dynamics

How PGE Makes Money

To understand PGE as a business, start with a simple mental model: PGE is a government-sanctioned monopoly that earns money by investing in physical infrastructure. The more it invests, with regulatory approval, the more it earns. This is the "rate base" model, and it drives virtually every strategic decision in the regulated utility industry.

Here is how it works in plain terms. PGE builds a physical asset—say a new substation costing $50 million. That investment goes into PGE's "rate base," the total pool of assets on which the company is allowed to earn a return. The Oregon Public Utility Commission then sets electricity rates at a level that allows PGE to recover its operating costs plus a "fair" return on the rate base. If the authorized return on equity is roughly ten to ten and a half percent, PGE earns approximately $5 million per year on that $50 million substation. The customer's monthly bill reflects this return, along with fuel costs, operating expenses, depreciation, and taxes.

This model creates a powerful, almost irresistible incentive to invest in capital projects. Every new dollar of rate base generates new earnings, which is why utilities love building things: power plants, transmission lines, substations, smart meters, wildfire cameras. Conversely, utilities are less enthusiastic about purchased power, because buying electricity from someone else does not expand the rate base and therefore does not generate returns for shareholders. This "capex bias" is one of the most important dynamics in utility investing.

The Regulatory Referee

The Oregon Public Utility Commission sits at the center of this system, serving as both referee and protector. The PUC approves PGE's capital spending plans, sets the authorized return on equity, and establishes customer rates. If the PUC concludes that PGE has been imprudent—investing in projects that were unnecessary or excessively costly—it can deny cost recovery, meaning shareholders eat the loss rather than customers.

This "prudency review" is the primary check on the utility's incentive to over-invest, and it is why regulatory relationships matter so much. A utility with a constructive, trusting relationship with its regulator will generally be allowed to invest more aggressively and recover costs more reliably than one viewed with suspicion. Think of it like a credit score for utilities: the better your regulatory reputation, the more flexibility you get.

There is also the concept of "regulatory lag"—the gap between when a utility spends money and when it is allowed to start earning a return on that spending. In a traditional rate case process, a utility might invest in a new substation, operate it for a year or two, then file a rate case asking the PUC to include it in the rate base. During the lag period, the utility is spending real money but not yet earning a return. Utilities hate regulatory lag because it suppresses actual returns below authorized returns. Oregon has implemented mechanisms to reduce this lag, including forward-looking test years and automatic adjustment clauses for certain costs, which helps PGE earn closer to its authorized return.

PGE also benefits from "decoupling" mechanisms that insulate its revenue from fluctuations in customer usage. Here is the problem decoupling solves: imagine a mild winter where Oregonians use less heating. In a traditional model, PGE's revenue would drop because it sells fewer kilowatt-hours, even though its fixed costs—wires, substations, employees—remain the same. Decoupling breaks that link, adjusting rates periodically to ensure PGE recovers its authorized revenue regardless of consumption. This is particularly important in a state like Oregon, where aggressive energy efficiency programs are actively reducing per-customer usage. Without decoupling, every successful conservation program would punish the utility's bottom line—a perverse incentive that decoupling eliminates.

Strategic Positioning

One frequently misunderstood aspect of PGE's business is its competitive landscape. PGE does not serve all of Portland. Its service territory is interleaved with that of Pacific Power, a subsidiary of PacifiCorp owned by Berkshire Hathaway Energy. Drive ten miles in any direction from Portland's city center, and you might cross from PGE territory into Pacific Power territory and back again. The two companies do not compete for the same customers; each has an exclusive franchise in its designated area. But they serve as natural comparisons for regulators and customers alike.

PGE's independence—operating in a single state with a single regulatory commission—offers distinct advantages. Management can focus entirely on Oregon's priorities rather than balancing competing agendas across multiple states. Decision-making is faster, stakeholder relationships are deeper, and strategy can be precisely aligned with Oregon's political and environmental goals.

The downside is concentration risk: no geographic diversification, no regulatory arbitrage, and no ability to spread catastrophic events across a broader portfolio. Whether this trade-off favors independence or acquisition depends on how well Oregon's regulatory compact continues to function.

X. Competitive Analysis: Porter's Five Forces and Hamilton's Seven Powers

To assess PGE's durable competitive position, it helps to apply two of the most rigorous frameworks in business strategy: Michael Porter's Five Forces and Hamilton Helmer's Seven Powers. Together, they reveal that PGE's business is structurally protected but faces an evolving set of risks.

Porter's Five Forces

The threat of new entrants into PGE's core business is essentially zero. Electric utility service is a natural monopoly backed by exclusive franchise rights. Building a competing set of wires, substations, and power plants in PGE's territory would require billions of dollars, decades of construction, and regulatory approval that would never be granted. This is perhaps the strongest barrier to entry in all of business.

Supplier bargaining power is moderate and shifting. Historically, PGE purchased coal and natural gas on commodity markets with no individual supplier holding significant leverage. As PGE transitions to renewables, its supply chain shifts toward wind turbine manufacturers, solar panel producers, and battery suppliers—a more concentrated vendor base with greater pricing power, particularly during supply chain disruptions. The Bonneville Power Administration sets federal rates that PGE must accept, but BPA power remains among the cheapest in the country.

Buyer bargaining power presents an interesting paradox. Individual customers cannot switch providers and have no direct negotiating leverage. But collectively, customers wield enormous power through the Oregon PUC, which can deny rate increases, mandate cost cuts, and impose performance requirements. The 2003-2005 public power fight demonstrated that customers can even threaten to replace PGE entirely with a municipal utility. This collective bargaining power, channeled through the regulatory process, is a check on PGE's monopoly that most monopolies in other industries do not face.

The threat of substitutes is low today but rising. Distributed solar paired with battery storage gives customers the ability to generate and store their own electricity. If grid electricity becomes too expensive relative to self-generation—the "death spiral" scenario—customers may begin defecting, reducing the customer base over which PGE spreads its fixed costs. The grid, however, remains essential for reliability. PGE's strategy is to position itself as the orchestrator of a hybrid grid that integrates distributed resources, rather than competing with them.

Competitive rivalry within PGE's territory is nonexistent by design. No other utility can serve PGE's customers. The only competitive dynamics are indirect: PGE competes for renewable energy projects against other utilities, and its performance is benchmarked against peers in regulatory proceedings.

Hamilton's Seven Powers

Turning to Helmer's framework, PGE's position reveals layers of subtle strength.

Scale economies are present but constrained. Spreading the fixed costs of transmission and distribution across 950,000 customers creates meaningful unit cost advantages, but PGE cannot expand geographically to capture additional scale. It is a moderate power, structurally capped by regulation.

Network economies are emerging. As the grid evolves to accommodate two-way power flows, electric vehicles, distributed solar, and smart devices, PGE's role is shifting from commodity supplier to platform operator. The more devices and energy resources that connect to PGE's grid, the more valuable the grid becomes as a coordination platform. This is an early-stage network effect that could strengthen significantly over the next decade.

Switching costs are extreme—the highest of any industry. Customers literally cannot change their electricity provider without physically relocating. This monopoly-level lock-in eliminates churn and guarantees a stable revenue base regardless of competitive dynamics.

Branding matters more at PGE than at most utilities, and this surprises people. PGE's reputation directly affects regulatory outcomes: a utility that is trusted by its community has more latitude to invest, more credibility to raise rates, and more political capital to navigate contentious decisions. PGE's Forrester ranking and voluntary renewable energy programs are strategic assets that translate into regulatory goodwill.

Cornered resource is where PGE's advantages are most tangible. The company's hydroelectric sites on the Clackamas, Willamette, and Deschutes rivers are irreplaceable. Transmission corridors that connect generation to load centers are physical resources built over a century that would be practically impossible to duplicate. And the exclusive franchise rights represent the ultimate cornered resource: a legal entitlement that no competitor can acquire.

Process power is the most underrated competitive strength. Operating an electric utility for 137 years builds institutional knowledge that is extraordinarily difficult to replicate: how to navigate Oregon's regulatory process, manage stakeholder relationships, respond to ice storms and wildfires, and operate complex grid systems. This accumulated expertise is invisible on the balance sheet but critical to consistent execution.

Synthesized Assessment

PGE's competitive position is structurally sound but transforming. The company's power has historically derived from regulated monopoly status, which eliminates competition and guarantees revenue. Going forward, its power will increasingly depend on managing a complex, decentralized energy system—requiring technological sophistication, stakeholder trust, and regulatory expertise that not all utilities possess.

The key risk is straightforward but profound: if the cost of the energy transition rises faster than customers can absorb, the regulatory compact that underpins the entire business model could come under strain. The regulatory compact works because both sides perceive it as fair. If customers start feeling that they are paying too much for an energy transition they did not ask for, the compact frays—and history shows that when the compact frays, utilities lose.

Understanding these competitive dynamics is essential for evaluating PGE's prospects in the years ahead.

XI. Bull vs. Bear Case & Investment Considerations

The Bull Case

The bull case for Portland General Electric rests on a structural tailwind without precedent in the company's history: massive, sustained growth in electricity demand driven by electrification, data centers, and the broader energy transition.

For most of the past fifty years, U.S. electricity demand was essentially flat, growing at roughly one percent annually. That era appears to be over. The convergence of electric vehicles, AI-powered computing, building electrification, and industrial reshoring is creating demand growth that some analysts project at three to five percent annually for the next decade or more. For a utility like PGE, which earns returns on capital deployed to serve demand, this is the equivalent of a retailer suddenly seeing foot traffic double.

PGE's management has guided for long-term earnings growth of five to seven percent per share, above average for the utility sector. The growth is funded by rate base expansion: every new wind farm, battery installation, transmission upgrade, and grid modernization project adds to the asset pool earning authorized returns. With billions in planned investment, the capital deployment runway is long and visible.

The company's execution track record lends credibility. PGE successfully navigated the Enron crisis, executed the early retirement of Boardman, built the Wheatridge facility, and deployed advanced wildfire mitigation—all while earning high marks for customer satisfaction and maintaining constructive regulatory relationships. In the utility industry, execution is not glamorous, but it is everything.

Oregon's progressive political environment creates a favorable policy backdrop. The state's clean energy mandates, EV incentives, and building electrification programs all drive demand. The customer base is relatively affluent and educated, with greater tolerance for rate increases tied to environmental goals. PGE's strong hydro base provides low-cost, flexible generation that complements intermittent renewables.

The dividend—fifty cents per share per quarter as of early 2025—provides stable income. Utilities typically maintain sixty to seventy percent payout ratios, balancing shareholder returns with retained earnings for reinvestment. For income-oriented investors, the combination of a stable dividend and mid-single-digit earnings growth is the classic regulated utility value proposition—essentially a bond with a growing coupon.

There is also a "hidden" bull case worth noting: PGE's wildfire mitigation investments could become a source of competitive advantage. If Oregon follows California in implementing strict wildfire safety standards, PGE's early investments in cameras, sensors, and grid sectionalization will have been made at lower cost and earlier in the curve than competitors who waited. Being early to wildfire safety is like buying insurance before the premium spikes.

The Bear Case

The bear case centers on cost. PGE needs to add 1,500 to 2,000 megawatts of new clean energy resources and approximately 800 megawatts of non-emitting dispatchable capacity by 2030. That is an enormous buildout, and the capital required will inevitably flow through to customer rates.

If rates rise too fast relative to customer incomes, political pressure could force the PUC to deny cost recovery or slow investment. Oregon is a progressive state, but affordability concerns do not respect political boundaries. Even environmentally supportive customers have limits on what they will pay.

Stranded asset risk is a legitimate concern. PGE's natural gas fleet, which today provides critical dispatchable capacity, could become economically unrecoverable if carbon regulations tighten faster than expected or if battery storage costs decline enough to make gas plants unnecessary. The company is investing billions in assets that must earn returns over twenty to forty year lifetimes, and the landscape could shift dramatically.

Federal policy uncertainty is another headwind. The Inflation Reduction Act's clean energy tax credits have been significant drivers of renewable economics, but face political risk with each administration change. Trade policy, including tariffs on imported solar panels and batteries, could spike procurement costs. Transmission constraints could slow renewable development regardless of capital availability.

The wildfire liability overhang is perhaps the most existential risk. The Pacific Power lawsuit over the 2020 Beachie Creek Fire established a precedent that Oregon utilities can face catastrophic financial exposure from wildfire events. PGE's investment in prevention mitigates this risk, but no amount of cameras and sensors eliminates it entirely. A single catastrophic fire attributed to PGE's equipment could generate liability exceeding insurance coverage.

The distributed energy "death spiral" scenario, while often overstated, deserves consideration. As rooftop solar and battery costs decline, the economics of self-generation improve. If enough customers reduce grid purchases, PGE must spread fixed costs over a smaller sales base, driving rates higher and accelerating defection. PGE's approach of embracing distributed resources as grid assets rather than competitors is strategically sound, but the transition from commodity supplier to platform manager involves uncertain margins.

PGE's single-state exposure concentrates risk. An Oregon-specific recession, a major earthquake along the Cascadia Subduction Zone, or an adverse regulatory shift would hit PGE with no geographic cushion. The company's relatively small size also limits institutional investor interest and can result in less favorable capital market access.

There is also a myth-versus-reality element worth addressing. The consensus narrative on PGE is often "small Oregon utility, nice clean energy story, but limited growth." The reality is more nuanced. PGE's load growth from data centers and electrification could rival the growth rates of Sun Belt utilities that are benefiting from population migration. The difference is that PGE's growth is demand-driven (more electricity needed per customer) rather than customer-driven (more customers moving to the area). Both types of growth expand the rate base, but demand-driven growth can actually be more capital-efficient because it leverages existing distribution infrastructure.

Comparing PGE against faster-growing utilities like NextEra or AES, the risk-reward profile differs meaningfully. Sun Belt utilities benefit from population migration tailwinds but face their own risks from extreme heat, water scarcity, and hurricane exposure. NextEra, for instance, faces enormous hurricane risk in Florida that PGE simply does not have. PGE offers a different value proposition: a smaller, focused utility with strong local alignment and a potentially underappreciated demand growth story, versus sprawling conglomerates with higher headline growth but more complexity and geographic risk.

KPIs That Matter

The two key performance indicators investors should track most closely are rate base growth and the spread between authorized return on equity and earned return on equity.

Rate base growth—the annual increase in the pool of assets earning regulated returns—is the single most direct driver of long-term earnings power. It captures the pace of capital deployment across clean energy, grid modernization, and wildfire mitigation in one number.

The authorized-versus-earned ROE spread reveals execution quality. A utility that consistently earns close to its authorized ROE is managing costs effectively and maintaining healthy regulatory relationships. A persistent gap suggests operational inefficiency or regulatory friction. Together, these two metrics capture the essential dynamics of PGE's business in a way no other statistics can match.

XII. The Next Chapter

The story of Portland General Electric is, at its core, a story about adaptation. Founded in the age of Edison, reorganized during the Depression, owned by the most notorious corporate fraud in American history, and now leading one of the most ambitious clean energy transitions in the utility industry, PGE has proven again and again that the regulated utility model—for all its unglamorous predictability—is one of the most resilient business structures ever devised.

The challenges ahead are real and immediate. Unprecedented load growth from AI data centers and electrification is straining a grid designed for a different era. The pace of decarbonization must be balanced against affordability for customers already feeling the pressure of rising costs. And the physical threats—wildfires, extreme weather, and the ever-present seismic risk of the Pacific Northwest—demand infrastructure investments that go far beyond historical planning models.

Technology wildcards could reshape the landscape in ways that are impossible to predict with confidence. Long-duration energy storage—technologies that can hold electricity for days or weeks rather than the four hours that today's lithium-ion batteries typically provide—could solve the intermittency problem that currently limits renewable penetration and requires gas-fired backup. Companies like Form Energy are developing iron-air batteries that promise hundred-hour storage at a fraction of lithium-ion costs. If this technology works at scale, it could render PGE's gas fleet obsolete far sooner than current plans assume—a double-edged sword that would accelerate decarbonization but potentially strand billions in gas plant investments.

Green hydrogen, produced by splitting water molecules using renewable electricity, could replace natural gas for generating electricity on calm, cloudy days when wind and solar output drops. And small modular nuclear reactors, which NuScale Power (another Oregon company) has been developing, could provide zero-carbon baseload power at a fraction of the cost and construction time of traditional nuclear plants. PGE has not committed to any of these technologies, but each could fundamentally alter the path to the company's 2040 zero-emissions target.

The strategic question that hangs over PGE most heavily is whether the company can maintain its independence. In an industry where scale matters increasingly for capital access, procurement power, and risk diversification, PGE's position as a standalone single-state utility is both its greatest strength and its greatest vulnerability. A larger acquirer could bring resources and diversification that PGE cannot achieve alone; but an acquisition would risk losing the local focus, regulatory alignment, and community trust that PGE has spent two decades rebuilding.

The deeper question is whether the regulatory compact itself can withstand the pressures being placed on it. The bargain—monopoly in exchange for price controls—has worked for over a century because costs grew slowly and predictably. The energy transition is neither slow nor predictable. If PGE must invest tens of billions over the next two decades to rebuild its generation fleet, harden its grid, and accommodate exploding demand, customer rates will rise substantially. The question is whether Oregonians—even progressive, environmentally conscious Oregonians—will accept those increases year after year. If they do, PGE's future is bright. If they do not, the same public power movement that nearly took over the company in 2003 could return.

PGE has been here before. Bankrupt in 1939, it emerged stronger. Swallowed by Enron in 1997, it regained its independence. Each crisis forged a more resilient institution. The company that sent electricity fourteen miles from Willamette Falls to Portland in 1889 is now attempting something far more ambitious: transforming the way an entire state generates, distributes, and consumes energy—while keeping the lights on, the rates affordable, and the shareholders whole. Whether PGE succeeds in this latest reinvention will depend on the same qualities that have sustained it for 137 years: regulatory acumen, community trust, and the stubborn conviction that infrastructure built to last can outlive any crisis that comes its way.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube