Pinnacle West: Powering the Silicon Desert

I. Introduction & The Spark

Drive forty minutes north of downtown Phoenix, past the last strip malls and into the raw Sonoran scrubland, and you arrive at a place that did not exist on any economic map a decade ago. Cranes stand in rows against a sky that is cloudless roughly three hundred days a year. Convoys of trucks kick up desert dust hauling in cleanroom modules and chip-fabrication tools. This is the Arizona campus of 台積電 TSMC, the Taiwan Semiconductor Manufacturing Company — the contract manufacturer that prints the logic chips inside Apple iPhones, NVIDIA's AI accelerators, and most of the advanced silicon that runs the modern world. What began as a roughly $65 billion commitment for three fabrication plants has ballooned, after a March 2025 expansion, into a planned $165 billion investment spanning six fabs, two advanced-packaging facilities, and a research center — the largest single foreign direct investment in United States history.2

Here is the detail that turns a semiconductor story into a utility story. A leading-edge fab is one of the most power-hungry structures humans build. The first phase of the TSMC campus was projected to draw roughly 200 megawatts; industry and grid analysts expect the full build-out to consume well over a gigawatt of continuous, uninterruptible electricity — the appetite of a small, permanently air-conditioned industrial city that never sleeps and cannot tolerate so much as a flicker.1 Someone has to generate that power, wire it across the desert, and keep it flowing through 115-degree July afternoons. That someone is a company most investors would struggle to pick out of a lineup.

Pinnacle West Capital Corporation, which trades on the New York Stock Exchange under the ticker PNW, is the holding company for Arizona Public Service — APS — the largest and oldest electric utility in Arizona, serving roughly 1.3 million customer accounts across eleven of the state's fifteen counties.4 In the mental model of most investors, a regulated investor-owned utility is the closest thing the stock market offers to a government bond with a logo: slow, defensive, low-beta (PNW's beta sits around 0.4), a vehicle you buy for a dividend and forget. And yet this particular sleepy monopoly finds itself sitting directly on top of the two most violent secular demand shocks to hit the American grid in a generation — the onshoring of advanced semiconductor manufacturing, and the AI-driven data-center land rush.

That is the paradox worth an entire episode. The defensive, bond-like security is suddenly a leveraged bet on the physical infrastructure of the computing age. But this is not a fairy tale, and Pinnacle West is not a company management can simply will to greatness by pointing at TSMC. A regulated utility does not capture a demand boom the way a chipmaker does; it must spend billions of dollars of shareholder capital up front to serve that load and then persuade a panel of elected politicians to let it earn that money back. Whether the boom becomes value creation or value destruction depends entirely on a regulatory relationship this company spent the last decade nearly incinerating.

Because to understand Pinnacle West, you have to sit with three uncomfortable questions. How did a company that flirted with financial ruin in 1990 — not from running power plants, but from buying a savings-and-loan at the worst possible moment — reinvent itself into the operator of the largest nuclear power station in the United States, improbably located in a waterless desert? How did the death of a 72-year-old grandmother over a $51 balance metastasize, three years later, into one of the harshest rate rulings in modern American utility history, erasing roughly a fifth of the company's earnings? And can a young, largely untested executive team rebuild enough regulatory trust to finance the grid the Silicon Desert demands — without detonating the electricity bills of ordinary Arizona families along the way?

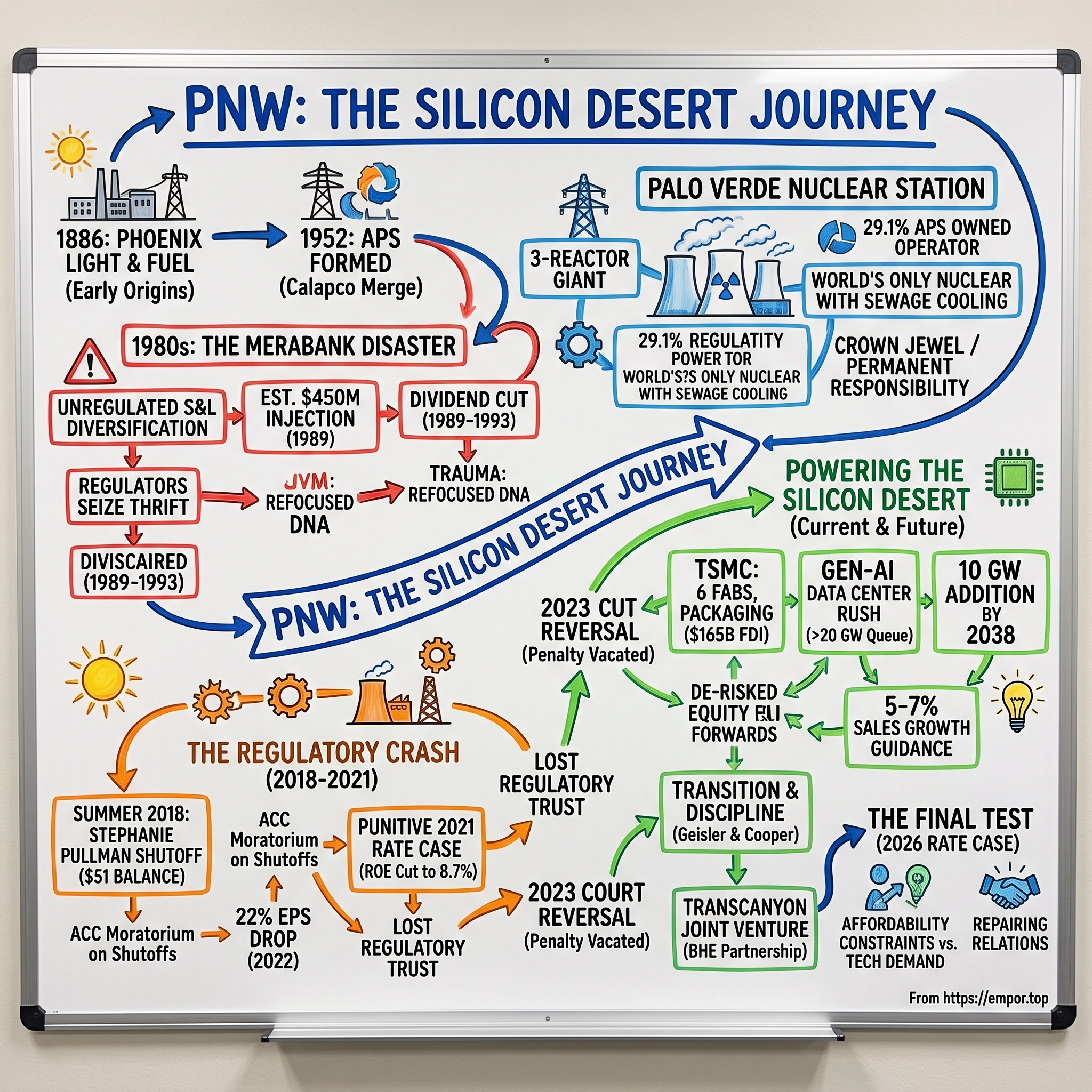

To answer any of that, we have to go back to a desert town of a few thousand people, lit by gas lamps, deciding it wanted electric light.

II. The Phoenix Rises: Founding Context & The Rise of the Desert Grid

In 1886, Phoenix was three years incorporated and barely a town — a grid of dusty streets baking in the Salt River Valley, its handful of residents relying on the sun to set their schedule because there was little to do after dark. That year, a venture called the Phoenix Light and Fuel Company was formed to bring gas lighting and, soon, electricity to the settlement.5 It is worth pausing on how audacious that was. This was a community with no railroad-scale industry, no dense population, and a climate that for half the year was actively hostile to human comfort. Building an energy business here was a bet not on what Phoenix was, but on what someone imagined it could become.

The corporate lineage from that first gas company to today's APS runs through a series of mergers and renamings that mostly matter as a single theme: consolidation of a fragmented frontier utility patchwork into one coherent desert grid. The enterprise passed through a spell as a local Pacific Gas and Electric operation before emerging, in 1920, as the Central Arizona Light and Power Company — universally shortened to "Calapco," the name under which it began paying the continuous common dividend that would run, remarkably, for the next seven decades.5 Along the way the company built genuinely pioneering assets. The Childs-Irving hydroelectric plants on Fossil Creek began generating power in 1909, harnessing a desert stream to feed the mines and towns of central Arizona at a time when long-distance electricity transmission was itself frontier technology.5

The pivotal corporate moment arrived in 1952, when Central Arizona Light and Power merged with the Arizona Edison Company and rechristened itself Arizona Public Service Company.5 APS was now the dominant electric provider for a state on the cusp of transformation — and the agent of that transformation was sitting, unremarked, in appliance-store windows across the country.

Air conditioning is the hinge on which all of Arizona history turns. Before affordable refrigerated cooling, Phoenix was a seasonal agrarian outpost; the wealthy fled the summer and the rest simply endured it. Once air conditioning became a mass-market household technology in the postwar decades, the calculus flipped entirely. Phoenix became habitable — even pleasant — twelve months a year, and the population detonated. Retirees, manufacturers, and eventually semiconductor and technology firms poured into the Valley of the Sun. But every one of those newcomers arrived with an absolute, non-negotiable dependence on electricity. In a Phoenix July, power is not a convenience that improves quality of life; it is the physical precondition of life itself. APS was no longer merely selling a service. It had become the load-bearing wall of Arizona's entire existence — a fact that would later cut in two directions, conferring an almost unassailable economic franchise while also loading the company with a moral and political responsibility no ordinary business carries.

By the mid-1980s, that franchise looked, from the inside, like a cage. Utility returns were capped by regulators; a well-run monopoly could earn its authorized return and no more. Across the United States, ambitious utility executives eyed the deregulated, high-growth businesses booming around them and asked why they should be content with a regulated single-digit return when fortunes were being made elsewhere. In February 1985, APS reorganized itself under a new holding company, AZP Group Inc., a structure explicitly designed to let capital flow out of the regulated utility and into unregulated ventures that promised to escape the rate-making ceiling.6 Two years later, in 1987, AZP Group adopted a more aspirational name — Pinnacle West Capital Corporation — signaling that this was to be a diversified capital-allocation platform, not merely a power company.5

The name promised a summit. What followed was very nearly a cliff.

III. The MeraBank Disaster: The Ultimate Lesson in Unregulated Diversification

To feel the full weight of what happened next, you have to inhabit the intoxication of Arizona in the mid-1980s. Land was the local religion. The desert around Phoenix was being subdivided, flipped, and financed at a frenzy; savings-and-loan thrifts — the S&Ls at the center of what would become a national financial catastrophe — were the fuel-injection system of that boom, pumping cheap deposits into real-estate loans as fast as developers could break ground. To a utility holding company hunting for growth beyond its regulated ceiling, a thrift looked less like a risk than a passport into the hottest economy in America.

So, in a transaction agreed in the 1985–1986 window, AZP Group paid roughly $426 million — reportedly about twice book value — for MeraBank, one of Arizona's largest savings-and-loan institutions, an enterprise that would swell to some $6.5 billion in assets.6 The logic was seductive and, in hindsight, catastrophically circular: a Phoenix utility whose fortunes already rose and fell with Arizona real estate chose to double down by buying a lender whose entire balance sheet was a leveraged bet on that same real estate. There was no diversification here at all. There was concentration wearing a diversification costume.

The desert boom broke at the end of the decade, and it broke hard. Arizona property values cratered, MeraBank's loan book rotted, and the thrift began hemorrhaging capital. Under mounting pressure from the Office of Thrift Supervision, Pinnacle West agreed in 1989 to inject roughly $450 million into the failing bank — a capital-maintenance commitment structured as approximately $300 million in cash plus a $150 million note, not, as it is sometimes misremembered, a fine.6 It did not matter. The hole was bottomless. In January 1990, federal regulators seized MeraBank and placed it into the receivership of the Resolution Trust Corporation, the government entity created to bury the corpses of the S&L crisis.6

The blast radius reached straight into the heart of the parent company. Pinnacle West wrote off its entire investment in the thrift, and — in the single most telling act of the whole saga — suspended its common stock dividend in October 1989, ending a payout streak that had run unbroken since the Calapco days of 1920.6 For a utility, cutting the dividend is the financial equivalent of a hospital losing power in the ICU; it is the signal of last resort, the admission that survival now trumps every promise made to shareholders. The company spent the early 1990s in survival mode, methodically liquidating the non-utility empire it had assembled with such confidence, and did not reinstate the dividend until 1993.

Why dwell on a thirty-five-year-old banking failure in a story about powering AI data centers? Because the MeraBank disaster is the trauma that rewired this company's institutional DNA, and understanding it is the key to understanding every capital-allocation decision Pinnacle West has made since. The lesson management took away was brutal and permanent: a regulated utility's entire competitive advantage is its localized, legally protected monopoly and its relationship with the territory it serves. That advantage is not portable. The moment you deploy utility-generated capital into a cyclical, highly leveraged, unregulated business you do not truly understand, you are not diversifying risk — you are trading a durable moat for a lottery ticket, and betting the whole enterprise on it.

That scar tissue explains a great deal about the disciplined, almost boringly focused Pinnacle West that exists today — a company that, as we will see, refuses to chase splashy unregulated M&A even when activists and empire-builders might cheer it on. For a long-term investor, the MeraBank episode is not ancient history; it is the origin of a capital-allocation philosophy still visible on every earnings call. The company nearly died learning that its job was to run the grid. Which brings us to the single most audacious thing it ever built on that grid: a nuclear power station in a place with no water.

IV. Palo Verde: Operating a Nuclear Giant in the Desert

Every nuclear power plant on Earth needs a vast, reliable supply of water to carry away the enormous heat its reactors produce. That is why they cluster along coastlines, on the shores of the Great Lakes, and beside major rivers. So consider the sheer contrarian nerve of the decision APS and its partners made in the 1970s: to build a three-reactor nuclear station in the Sonoran Desert, roughly 45 miles west of Phoenix near the tiny community of Tonopah, in a spot with no lake, no river, and no ocean for a hundred miles in any direction.7

The engineering answer to "where does the water come from?" is the detail that makes Palo Verde one of the genuinely singular industrial facilities on the planet. The Palo Verde Generating Station is the only large nuclear plant in the world not sited next to a significant body of surface water. Instead, it drinks sewage. Every day, treated municipal wastewater — the effluent from the toilets, showers, and drains of Phoenix and its surrounding cities — is piped dozens of miles out to the desert, where Palo Verde recycles more than 20 billion gallons of it a year as reactor cooling water.7 A metropolis's waste stream becomes the coolant for a fleet of reactors generating carbon-free electricity for four states. There is no more elegant illustration of the desert's central discipline: nothing is wasted, because nothing can be.

The plant's three pressurized-water reactors give it a technical nameplate capacity of roughly 3,900 megawatts, which APS markets in round numbers as the capacity to produce about 4,200 MW of carbon-free power — enough, on its own, to anchor the electricity supply of the entire region.7 Palo Verde has for years ranked as the largest power producer of any type in the United States by annual generation, precisely because a nuclear plant, unlike solar panels or gas turbines, simply runs — around the clock, in any weather, at very high capacity factors. On the Q1 2026 earnings call, with summer looming, management's tell was that it flagged the return of Palo Verde's Unit 2 from a refueling outage as central to its confidence in meeting peak demand; when the mercury hits 115 degrees and air conditioners across the Valley scream for power, this is the asset that does not blink.30

It is worth appreciating what building this actually required, because it explains why nothing like it will be built again soon. The construction program that ran through the late 1970s and 1980s was a multi-billion-dollar undertaking at a time when Pinnacle West was a fraction of its current size — a genuine bet-the-company gamble that arrived, from a financing standpoint, at nearly the same moment as the MeraBank misadventure. The difference is instructive: one enormous, capital-intensive, decades-long project was inside the company's circle of competence and became its most valuable asset; the other was outside it and nearly destroyed the firm. Same era, same balance sheet, opposite outcomes — a natural experiment in the value of sticking to what you know. A nuclear station also front-loads its pain: the capital is spent up front, the regulatory scrutiny is unrelenting, and the reward is decades of cheap, clean baseload on the back end. That shape — spend now, earn later — is the same shape the Silicon Desert build-out will take, which is one reason the company's operating experience here is more than a trophy; it is a template.

The consortium structure was itself a response to that scale. In the 1970s, no single Southwest utility could absorb the cost or the risk of a three-reactor plant, so a coalition pooled capital and split the output — a pragmatic acknowledgment that some infrastructure is simply too large for one balance sheet. That same logic echoes forward into the TransCanyon transmission joint venture and into management's insistence, on recent calls, that new nuclear would only be built if large customers helped shoulder the financing. The lesson APS internalized from Palo Verde is not just how to run a reactor; it is that the biggest assets require shared risk. And every one of those reactors carries an obligation most investors never see on the income statement: the decommissioning liability, funded through trusts today against the cost of safely dismantling the plant generations from now — a reminder that a nuclear utility is signing a contract not with this decade's customers but with the next century's.

Palo Verde is not owned by APS alone. It is a consortium, built in an era when no single Southwest utility could shoulder the cost or risk of a multi-reactor nuclear project by itself. APS serves as operator and holds a 29.1% stake — about 1.2 gigawatts of the output. The remainder is divided among a who's-who of Western power: the Salt River Project at 20.2%, El Paso Electric and Southern California Edison at 15.8% each, PNM Resources at 7.5%, and two Southern California public-power entities, the Southern California Public Power Authority (5.9%) and the Los Angeles Department of Water and Power (5.7%).7 APS runs the plant; a coalition of its regional peers and rivals shares the economics.

In the language of Hamilton Helmer's 7 Powers framework, Palo Verde is close to a textbook Cornered Resource — a unique, hard-to-replicate asset that throws off durable advantage. No competitor can conjure a second four-gigawatt desert nuclear station; the licensing alone would take decades. But the honest investor holds that advantage alongside its liabilities. A nuclear plant carries extreme fixed costs, a permanent and expensive security and regulatory overhead, low-probability but catastrophic tail risk, and decommissioning obligations that stretch generations into the future and must be funded today. Palo Verde is simultaneously Pinnacle West's crown jewel and its heaviest permanent responsibility — a source of clean, cheap baseload that is also a standing reminder that this business is measured in decades, not quarters. Management's own words on that January 2026 investor call are revealing: asked about building new nuclear to serve the data-center boom, CEO Ted Geisler said flatly that the company is "not in a position to put the utility balance sheet at risk," and would only pursue new reactors if large customers helped finance them.30 That is the voice of a company that remembers 1990.

Operating a nuclear giant flawlessly for decades earns a utility enormous technical credibility. But credibility, it turns out, is not fungible. You can run the most complex machine in the state to perfection and still torch your reputation over a single unpaid electric bill.

V. The Summer of 2018 & The Regulatory Crash of 2021

Stephanie Pullman was 72 years old and lived alone in Sun City West, a retirement community northwest of Phoenix. In the late summer of 2018, she was behind on her electric bill. An APS letter that August put her past-due balance at $176.84; in early September her family made a partial payment of $125, leaving roughly $51 outstanding.8 On September 7, 2018, on a day when the temperature reached at least 105 degrees, APS disconnected her power. Days later she was found dead inside her home. The Maricopa County medical examiner ruled the cause as environmental heat exposure, in the setting of cardiovascular disease.8 A woman had died, in her own house, in the Arizona summer, over a balance smaller than a utility executive's dinner.

It is impossible to overstate how completely this single event reframed the politics of electricity in Arizona. For most businesses, an unpaid invoice is a routine collections matter. But in a desert where losing power in July can be a death sentence, an electricity shutoff is not a commercial act — it is closer to a public-safety decision, and APS had made it algorithmically, at scale. When reporting later surfaced that APS had executed disconnections more than 110,000 times in 2018, tens of thousands of them during the deadly summer months, the Stephanie Pullman story stopped being a tragedy and became an indictment.8 The company's defense — that it had followed the disconnection rules then on the books — was technically true and politically radioactive. It amounted to arguing that the rules permitted a grandmother to die over $51.

The Arizona Corporation Commission, the elected five-member body that regulates APS, responded first with outrage and then with policy. In June 2019 the commissioners voted an emergency halt to residential summer disconnections, and the moratorium — barring shutoffs from June 1 through October 15 — was later made permanent.8 Overnight, a core lever of the utility's collections process was gone, and, more importantly, the reservoir of political goodwill APS had drawn on for decades was not just drained but poisoned. In the theater of a rate case, where a utility must persuade regulators that it deserves to earn a fair return, the company now walked on stage as the villain.

The bill came due in November 2021. Ruling on the rate case that APS had filed seeking a roughly 10.15% authorized return on equity — the regulated profit margin on the capital a utility invests in its system — the Corporation Commission instead delivered what stands as one of the most punitive utility decisions in modern American history. In a 3–2 vote, the commission slashed APS's authorized return on equity to 8.70%, built as an 8.9% base return minus an extraordinary 20-basis-point penalty explicitly imposed for poor customer service and damaged public trust.910 To grasp how unusual that is: regulators almost never dock a utility's return as an overt punishment for how it treats customers. This was the Pullman tragedy converted directly into basis points.

The ROE cut was only the headline. Rather than the rate increase APS had requested, the commission ordered a net revenue decrease of roughly $119 million — the utility was told to charge its customers less, not more.10 And in a pointed rejection of the company's investment judgment, the commission disallowed cost recovery on about $215.5 million of the roughly $450 million APS had spent on selective catalytic reduction equipment — pollution-control retrofits — at the coal-fired Four Corners Power Plant in New Mexico, effectively telling shareholders to eat the cost of environmental gear the company had already bolted onto its plant.9

The financial reset was swift and unforgiving. Ratings agencies moved against the company: Fitch cut Pinnacle West to BBB+ following the decision, and Moody's downgraded the parent to Baa1, each notch raising the cost of the debt a capital-intensive utility must constantly roll over.1112 Earnings buckled — Pinnacle West's diluted earnings per share fell from $5.47 in 2021 to $4.26 in 2022, a decline of roughly 22%.12 A "bond-like" utility had just handed shareholders an equity-like drawdown, and it had done so not because a power plant failed, but because the company had forgotten that its license to operate is ultimately social, not just legal.

Pause on the mechanism, because it is the single most important thing to understand about owning a regulated utility. A utility's earnings are, at their core, its rate base — the depreciated value of the poles, wires, plants, and meters it has invested in — multiplied by its authorized return on equity. Cut the authorized return from roughly 10% to 8.7%, and you have permanently reduced the profit the company earns on every dollar of that vast asset base, not for a quarter but for years, until the next rate case can reset it. That is why a 130-basis-point ROE cut is not a rounding error; on a rate base measured in the tens of billions, it is a structural haircut to the earnings power of the entire enterprise. The 2021 decision did not merely dent a year's profits; it re-rated the company's baseline. Investors who thought they owned a defensive bond substitute discovered they owned a bond whose coupon the issuer's regulators could slash by fiat.

There is a second-order lesson here that the eventual court reversal underscores rather than erases. Even though APS ultimately clawed back the customer-service penalty and the coal-cost disallowance through the appeals process, the damage to earnings, credit ratings, and — most durably — investor trust in the predictability of Arizona regulation had already been done during the eighteen months the case wound through the courts. A win on appeal restores the numbers; it does not restore the years of compounding lost, nor does it un-teach the market that this particular regulator is capable of turning a rate case into a punitive exercise. For a company whose valuation depends on investors believing its cash flows are stable and its regulator is rational, the mere demonstration that both assumptions could fail was itself a lasting cost.

APS did not accept the verdict quietly. It took the decision to the Arizona Court of Appeals, and in March 2023 won a genuine, if partial, vindication. The court affirmed the commission's discretion to set the 8.9% base return, but it vacated the 20-basis-point customer-service penalty — ruling that the commission had overstepped its ratemaking authority by wielding service metrics as a financial cudgel — and it vacated and remanded the Four Corners disallowance, finding that regulators had improperly judged the coal investment with the benefit of hindsight.13 The practical epilogue came in June 2023, when the commission approved a settlement, restoring the 8.9% return and allowing APS to recover the full $215.5 million it had spent on the coal retrofits.14

The saga is a masterclass in what utility investors call the regulatory compact — the implicit deal in which a monopoly accepts price controls and public-service obligations in exchange for a reasonable, reliably recoverable return. The lesson is that the compact is not a contract enforced only in courtrooms; it is a relationship, and relationships can be poisoned by a single act of institutional callousness and only slowly, expensively repaired. As APS entered the second half of this decade, the central question was whether it had repaired that relationship enough — because it was about to ask Arizona's regulators, and Arizona's ratepayers, for the largest sums in its history.

VI. Powering the Silicon Desert: TSMC, AI Data Centers, and the Capital Squeeze

For most of its existence, APS grew the way desert utilities are supposed to grow: steadily, with the population, at a percent or two a year. Then, sometime around the pandemic, the ground shifted. The Phoenix metropolitan area — with its cheap land, near-total absence of hurricanes and earthquakes, business-friendly politics, and proximity to power-constrained California — became the primary industrial and technology growth engine of the American Southwest. The Silicon Desert stopped being a booster's slogan and started being a load-forecasting problem.

The anchor tenant is TSMC, whose North Phoenix campus we opened with. But the more important point for Pinnacle West is that TSMC is not a single customer; it is the keystone of an entire ecosystem. On the Q1 2026 call, management ticked through the second-order boom: TSMC's second fab complete and preparing to volume-produce 3-nanometer chips, a third fab under construction, a fourth fab and a first advanced-packaging plant now breaking ground and targeted for 2029 — and, radiating outward, a supply chain of chemical, cleanroom, and equipment firms buying land and staffing up across the Valley.30 Each of those facilities is a new electricity account, many of them enormous.

Layered on top of the fabs is the data-center land rush. The generative-AI boom turned computing capacity into the scarcest resource in the economy, and hyperscalers went hunting for places to build the warehouse-sized server farms that train and run large models. Arizona, again, checked every box. The scale of the resulting interest is difficult to overstate: as of late 2024, APS disclosed that it was holding more than 10 gigawatts of pending data-center interconnection requests it could not simply agree to serve without jeopardizing reliability for existing customers.3 By early 2026, on the Q1 call, management put the uncommitted queue at just under 20 gigawatts — against a total system peak that has historically run around 8 gigawatts.30 Read that again: the speculative pipeline of new demand is more than double the entire grid APS built over 140 years.

Not all of that queue is real — some of it is duplicative, some is tire-kicking, and management is careful to distinguish it from committed load. But the committed load alone is staggering. APS now has roughly 4.5 gigawatts of what it calls "extra-high load factor" customers — the fabs and data centers — under firm commitment and in various stages of ramp-up.30 That is why the company projects its system peak demand will climb by roughly 40% by 2031 and about 60% by 2038, and why it raised its long-term weather-normalized sales-growth guidance to 5% to 7% a year through 2030.1530 For context, the average American electric utility grows retail sales at roughly 1% a year. In the first quarter of 2026, APS posted weather-normalized sales growth of 9.4% — over 7% even after stripping out a prior-year adjustment — driven by 14.6% growth in the commercial and industrial segment.30 These are not utility numbers. They are technology-company numbers, showing up on a regulated monopoly's income statement.

Here is where the outline's cheerful framing needs an independent counterweight, because for a regulated utility, explosive demand is not an unalloyed good — it is a capital-allocation trap wearing a party hat. To serve TSMC and the hyperscalers, APS must build generation, transmission, and distribution years ahead of the revenue, financing that construction with expensive debt and dilutive equity, and then wait for regulators to let it recover the cost. The gap between spending the money and earning it back is called regulatory lag, and it is the exact mechanism that punished shareholders in 2021. Growth that outruns cost recovery destroys value even as reported sales soar. That tension is the whole ballgame.

The scale of the required spend is enormous and rising. What was a $9.65 billion capital plan for 2025–2027 — already a 24% jump over the prior version — has been lifted to roughly $10.35 billion across 2025–2028, aimed at grid modernization, transmission capacity, and wildfire mitigation.16 To fund it, CFO Andrew Cooper told investors the company had already locked in nearly $850 million of forward-sold equity and completed all of its 2026 equity needs, part of a deliberate effort to "de-risk" the financing plan and avoid issuing stock into a weak price.30 Management's proposed antidote to regulatory lag is structural: a formula rate that adjusts more contemporaneously with spending, plus "subscription" contracts under which the giant new customers help pre-fund the infrastructure built to serve them, so that, in the company's phrase, "growth pays for growth."30 Whether elected regulators grant those mechanisms is, as of mid-2026, an open and consequential question — not a settled fact.

The subscription model deserves a closer look, because it is management's most creative answer to the central problem and its most unproven one. The idea is straightforward in principle: rather than build billions in generation and transmission on the utility's balance sheet and hope to recover it later, APS offers large-load customers a "subscription" in which they help fund the infrastructure up front — contributing to financing or even helping source scarce equipment — in exchange for accelerated, guaranteed capacity. On recent calls the company described an initial Phase 2 offering sized at roughly 1.0 to 1.2 gigawatts, tied largely to its Desert Sun generation project and the transmission to match, and said it was in active negotiations with counterparties with the goal of filing the first such special-rate contracts with the commission before the end of 2026.30 If it works, it front-loads customer cash into the build, shrinks the external funding APS must raise, and converts the fearsome regulatory-lag problem into a contractual one. The honest caveat is that, as of this writing, not a single such contract has yet been signed and approved; it is a promising design, not a demonstrated capability, and its ultimate value depends on both hyperscaler willingness to pay and commission willingness to bless bespoke deals.

Transmission, less glamorous than data centers, is quietly becoming the earnings workhorse. Because APS's transmission business operates under a federal formula rate that trues up and recovers investment on a near-contemporaneous basis — sidestepping the regulatory lag that plagues its state-regulated distribution and generation — every dollar of transmission capital converts to earnings far faster and more predictably. On the Q1 2026 call, Cooper noted the company had "doubled and then doubled again" its annual transmission capital spending over five years, and that transmission revenue contributed 16 cents per share of benefit in the quarter alone, with a further step-up expected as new rates took effect.30 For investors hunting the cleanest read on whether the growth story is translating into actual returns rather than just capital outlays, the transmission line item — with its rapid, low-lag recovery — is one of the more honest signals on the income statement.

The financing choreography behind all this reveals a management team scarred into discipline. Rather than issue a slug of dilutive equity when needed, Cooper described a program of equity forwards — pricing shares in advance and drawing on them opportunistically — that had already secured nearly $850 million against a three-year base equity need of roughly $1.0 to $1.2 billion through 2028, chipping away at the requirement before it came due.30 The subtext is unmistakable and, for once, aligns management's stated philosophy with its behavior: after a career-defining lesson in what over-reaching capital allocation can do, this is a company that would rather bore investors with careful, pre-funded, de-risked financing than thrill them with anything bolder.

There is also a political dimension to the generation debate that investors should weigh. In mid-2026, Arizona's Governor convened an energy task force whose report, management noted on the Q1 call, endorsed new natural-gas pipeline infrastructure and — strikingly — signaled openness to new nuclear generation over the longer term.30 As the operator of the country's largest nuclear plant, APS is the natural candidate to build any future reactors, and Geisler said the company would be "very open" to that discussion if large customers helped finance it. That is optionality worth noting, but it is also a tell about the constraints: even a state desperate for firm, clean power, and even a utility that runs a nuclear giant flawlessly, will not put the utility's balance sheet at risk for new reactors without someone else sharing the bill. The affordability constraint governs everything, including the clean-energy dream.

The generation side of the equation exposes the same collision between ambition and reality. In March 2025, APS retired the final coal units at its Cholla Power Plant, part of a broad move away from coal. Yet barely a year later, confronting a wall of new peak demand and the physics of AI loads that run 24/7, the company announced in early July 2026 that it would repurpose the Cholla site by converting two units to natural gas — adding roughly 380 megawatts, with construction beginning in 2028 and commercial operation targeted for 2029.1718 Meanwhile, on the Q1 2026 call, management described the Red Hawk expansion already under construction — eight combustion turbines, about 400 MW of gas capacity — plus the Desert Sun project and an all-source procurement for resources arriving in 2029–2031.30 This is a utility reaching for firm, dispatchable gas because solar panels do not run at 2 a.m. and a chip fab cannot pause.

That pivot sits awkwardly against the company's climate messaging, and here the record deserves scrutiny rather than applause. APS made headlines in January 2020 by pledging to deliver 100% carbon-free electricity by 2050, with an interim target of 65% clean energy by 2030.20 By August 2025, quietly, that changed: APS softened the language to an "aspirational" carbon-neutral-by-2050 goal and dropped the binding interim 2030 targets altogether.19 The reason is not mysterious — the surge in always-on industrial load made a hard near-term decarbonization schedule incompatible with keeping the lights on — but investors should note the pattern: a bold public commitment, made in calmer times, walked back when it collided with operational reality. It is a data point on management credibility, and an honest analyst files it as such.

Not every strategic move here is defensive. Through a 50/50 joint venture called TransCanyon — partnered with BHE U.S. Transmission, a subsidiary of Berkshire Hathaway Energy — Pinnacle West is developing the Cross-Tie Transmission Line, a roughly 214-mile, 500-kilovolt link connecting central Utah to eastern Nevada with about 1,500 MW of capacity.2122 The significance is strategic optionality: independent transmission lets Pinnacle West participate in the build-out of the Western grid, tap distant wind and solar, and earn returns on high-voltage infrastructure — all tightly adjacent to its core competence, and pointedly not the kind of unregulated adventure that once nearly sank it. It is the anti-MeraBank: growth that stays inside the circle of competence.

All of which raises the question every investor should be asking. This capital-allocation gauntlet — spend tens of billions, manage regulatory lag, keep affordability from exploding, decarbonize without going dark — will be run by a leadership team that only recently took the wheel.

VII. The Geisler-Cooper Guard: Leadership, Incentives, and Credibility

On April 1, 2025, Ted Geisler became Chairman, President, and Chief Executive Officer of Pinnacle West, succeeding Jeff Guldner, who retired after guiding the company through the wreckage of the 2021 rate case.23 Geisler is, in the most literal sense, an APS lifer: he joined the company in 2001, starting in the generation business, and worked his way through a striking breadth of the enterprise — serving at various points as Chief Information Officer, Chief Financial Officer, and, most recently, President of APS before ascending to the top job.23 There is a logic to elevating an operator who has personally run the grid's technology, its balance sheet, and its operations at the precise moment the company's central challenge is a physical and financial engineering problem: building an enormous amount of infrastructure without breaking the finances or the customer.

It is worth crediting the transition itself, because leadership handoffs are where utilities often stumble. Jeff Guldner inherited the CEO seat as the Pullman scandal was cresting and steered the company through the worst regulatory decision in its modern history, the ratings downgrades, and the multi-year appeal that ultimately reversed the harshest elements of the 2021 ruling. Handing the wheel to a long-groomed internal successor in April 2025 — with Guldner staying on in a non-executive advisory capacity through early 2026 to smooth the transition — is the kind of orderly, telegraphed succession that signals a functioning board rather than a palace intrigue.23 For a business whose entire value rests on multi-decade capital commitments and long-cycle regulatory relationships, continuity of institutional memory is not a soft virtue; it is risk management. The flip side, which a skeptic would press, is that an all-internal, APS-lifer leadership team can be prone to institutional blind spots — the same insular culture that once concluded it was acceptable to disconnect a customer in lethal heat because "the rules allowed it." Whether the post-2021 emphasis on customer experience represents genuine cultural change or merely a chastened compliance posture is something only the next crisis will reveal.

His financial counterpart is Andrew Cooper, who became Senior Vice President and Chief Financial Officer in May 2022, having previously served as Treasurer.24 Cooper's background is a deliberate contrast to Geisler's operational, grown-in-the-desert profile. He arrived from the outside world of high finance — earlier roles at Consolidated Edison in New York and more than a decade as an investment banker at Barclays covering the power and utilities sector — and he holds a law degree from Harvard.2425 In a business whose fate now turns on threading equity issuance, debt laddering, credit-rating maintenance, and regulatory finance, a CFO who has sat on the banker's side of the table is a pointed hire. The pairing — a lifelong operator as CEO, a Wall Street–trained financier as CFO — is well matched to a moment defined by capital intensity.

The natural question for any independent observer is whether management's wealth is genuinely tied to the outcomes shareholders care about. The proxy paints a nuanced picture. Executive stock ownership is modest in absolute terms — Geisler beneficially owned 19,907 shares as of early 2025, a stake the proxy marks simply as less than 1% of the company; the notion, floated in some summaries, that he owns some precise fraction like 0.041% is not supported by the filing, and the true figure is closer to a rounding error of the shares outstanding.23 In other words, this is not a founder-owner with a life-defining equity position; it is professional management, and investors should weigh incentives accordingly.

Where the alignment is more real is in the structure of pay. Roughly 79% of the named executives' targeted compensation is "at risk" — contingent on performance rather than guaranteed salary — with the sitting CEO's at-risk proportion running even higher, around 87%.23 The annual cash bonus is split evenly, 50% on financial results (Pinnacle West and APS earnings) and 50% on operational metrics spanning safety, customer experience, and operational quality — a design clearly reverse-engineered from the 2018–2021 debacle, when customer-service failures proved to be financial failures in disguise.23 The long-term incentive, which is where real wealth is made, is 70% performance shares and 30% restricted units; the performance shares vest over three years against a weighted scorecard of 40% relative total shareholder return (measured against the Edison Electric Institute index of utility peers), 40% earnings-per-share performance, and 20% "clean megawatts installed."23

That scorecard is worth pausing on, because incentive design reveals priorities more honestly than any mission statement. Tying 40% of long-term pay to performance relative to utility peers is standard and sensible — it rewards management for outrunning the sector rather than for a rising-tide interest-rate environment it does not control. Weighting 20% to clean energy keeps decarbonization in the pay formula even as the public 2030 target was dropped, a small but real tension between what the company promises the market and what it pays its executives to do. What the structure does not prominently do is directly reward affordability or bill impact — a notable omission for a company whose existential risk is precisely a ratepayer and regulatory backlash over cost. An activist reading this proxy would ask why customer affordability, the very thing that detonated the 2021 rate case, is not a hard-wired, top-weighted metric in executive pay.

On the question of capital-allocation credibility, the behavioral record since 2021 is the strongest part of the bull case. Guldner's and now Geisler's teams have done the unglamorous things right: they controlled operating costs, kept the balance sheet intact enough to hold investment-grade ratings through a period of ballooning capital spending, timed equity issuance to avoid dumping stock at the bottom, and — crucially — refused to reach for splashy, overpriced, unregulated M&A. The corporate structure today is disciplined and legible: APS as the wholly owned regulated core; TransCanyon and other transmission interests held under a new subsidiary, PNW Power; a small legacy investment arm in El Dorado Investment Company; and a clean exit from the unregulated Bright Canyon Energy business, whose sale closed in January 2024.2627 After MeraBank, this is a company that has visibly chosen to color inside the lines. Whether that discipline survives the temptation of a once-in-a-generation demand boom is the test now underway.

VIII. Playbook: Business & Investing Lessons

Step back from the desert and the reactors and the rate cases, and Pinnacle West offers a compact set of lessons that generalize far beyond one Arizona utility.

The first is the trap of conglomerate diversification, written in the company's own blood. The MeraBank catastrophe is the archetype of a regulated monopoly convincing itself that the grass is greener outside the regulatory fence. The seductive logic — "our returns are capped here, so let us deploy capital into a higher-growth, unregulated business" — ignores that the utility's advantages are almost entirely non-transferable. Its moat is a legal franchise and a physical network rooted in one specific territory; carry that capital across the fence into a cyclical, leveraged business you do not understand, and you arrive naked. The corollary, visible in Pinnacle West's post-2021 discipline, is that the highest-return move for most utilities is not diversification at all but the patient expansion of the regulated rate base they already dominate. The TransCanyon transmission venture succeeds precisely because it stays inside the circle of competence; MeraBank failed because it leapt outside it.

The second lesson is that for a monopoly, the regulatory compact is a reputation game, and social trust is a hard financial asset. It is tempting for engineers and financiers to treat customer sentiment as soft, unquantifiable PR. Pinnacle West's own history refutes that decisively: a single catastrophic failure of empathy — disconnecting a vulnerable customer in lethal heat — resurfaced three years later as a 20-basis-point penalty on authorized return and a nine-figure revenue cut. In a regulated business, goodwill is not a nicety; it is working capital, and it can be spent down to zero. The mechanism runs directly from a customer's kitchen to the return on equity, and any investor modeling a utility's future returns without weighting its standing with regulators and ratepayers is modeling only half the machine.

The third lesson reframes the entire Silicon Desert thesis: for a regulated utility, massive load growth is a double-edged sword, not a windfall. In an ordinary business, a flood of new demand is pure upside — you sell more at a good margin and bank the profit. A utility cannot do that. It must sink billions of up-front capital into serving the new load, finance that capital with debt and equity at prevailing (and lately elevated) costs, and then depend on regulators to let it recover the money over decades. If cost recovery lags the spending — the regulatory-lag problem — the growth can dilute returns and strain the balance sheet even while the top line booms. The difference between the Silicon Desert making Pinnacle West and breaking it is not the size of the demand; it is the terms of recovery. This is why the seemingly dry mechanics of formula rates and subscription contracts are, in fact, the whole investment case.

Taken together, these lessons explain why a utility that looks defensive on the surface is anything but simple underneath. The next section stress-tests the business through the standard analytical frameworks — and then argues both sides.

IX. The Analysis: 5 Forces, 7 Powers, and Bull vs. Bear Case

Begin with the structural analysis, because for a regulated monopoly the frameworks behave in unusual, almost inverted ways.

Through Hamilton Helmer's 7 Powers lens, Pinnacle West's dominant advantage is a fusion of Cornered Resource and what is effectively a government-conferred monopoly. The State of Arizona grants APS an exclusive franchise to build and operate distribution wires within its service territory. No competitor may string a rival power line to a TSMC fab, a data center, or a suburban cul-de-sac inside that footprint. This is the deepest moat in capitalism — a legally enforced absence of competition — but it comes with the defining catch that the same government which grants the monopoly also sets the price, which is why regulatory relationship management is not a side task but the core competency. Layered on top are genuine Scale Economies: the high-voltage transmission network and the generation fleet, above all Palo Verde, constitute a capital barrier no private entrant could rationally attempt to replicate. And there are high switching costs in the most literal sense — grid electricity has no substitute for an industrial customer, and even a solar-covered home remains umbilically tied to the grid for reliability and nighttime power.

Running Porter's Five Forces confirms the picture while sharpening the risks. Competitive rivalry within the franchise is essentially nil; the neighboring Salt River Project operates adjacent territory in metro Phoenix, but the boundaries are strictly drawn, so the two do not fight over customers. The threat of new entrants is trivially low, given the capital and regulatory ramparts. The threat of substitutes is moderate and worth respecting: rooftop solar is a real secular headwind in the sunniest large metro in America, chipping at residential kilowatt-hour sales, though utility-scale storage and revised net-metering rate designs have blunted its economic bite. The most analytically interesting forces are the two flavors of buyer power. For a residential ratepayer, buyer power is near zero — you cannot shop for another grid. But for a hyperscaler or a chipmaker weighing where to place a multibillion-dollar facility, buyer power is enormous: these customers wield real political leverage with state officials, negotiate bespoke rates, and can, in principle, take their load to another state entirely. Supplier power, finally, is moderate-to-high and macro-driven — the prices of natural gas, turbines, transformers, and, crucially, the cost of capital itself flow straight into the utility's economics, and in a period of supply-chain-strained equipment and higher-for-longer interest rates, that pressure is live.

So, why does Pinnacle West win from here — and what could break the case?

The bull argument is that this is a rare utility with a genuine, multi-year, structural growth engine bolted onto an unbreakable monopoly. Sales growth guided at 5% to 7% a year through 2030 is extraordinary for the sector, and it is anchored not by speculation but by roughly 4.5 gigawatts of already-committed marquee industrial load, with a vast queue behind it.30 The regulatory climate, poisonous in 2021, has demonstrably thawed — the courts restored the company's return and coal recovery, and management reports constructive engagement with all three rating agencies and a stable outlook.30 And the shares still pay a growing dividend — an indicated annual rate of $3.64 for 2025 — that provides a return floor while the growth story plays out.4 The core bull thesis is simple: rate base is about to compound faster than it has in the company's modern history, and rate base growth is, over time, the engine of a regulated utility's earnings.

The bear argument attacks the same facts from underneath. First and foremost is capital intensity: a plan north of $10 billion must be financed largely with external capital, and every dollar of dilutive equity and expensive debt is a drag that only pays off if — a very large if — regulators grant timely recovery. Second is the political fragility of the regulator itself: the Arizona Corporation Commission is elected, which means the body setting Pinnacle West's returns is subject to the swings of ballot-box politics, populist affordability campaigns, and personnel turnover no company can control. The 2021 decision proved that this risk is not theoretical. Third is the affordability collision at the heart of the whole story: asking residential customers to help underwrite billions in infrastructure built for the world's richest technology companies, in a state where summer power is a matter of survival, is politically combustible — and the current rate request already drew hours of public protest over a proposed double-digit bill increase.29 Fourth, always, is Palo Verde: decades of flawless operation cannot fully retire the low-probability, high-severity risk that attends any nuclear fleet, along with its permanent decommissioning overhang.

It helps to situate Pinnacle West against its peers, because "utility with a data-center growth story" has become a crowded pitch. Across the sector, names from Dominion in Virginia's data-center alley to the Texas and mid-Atlantic utilities are selling investors some version of the same narrative: load growth is back after two decades of stagnation, and rate base will compound accordingly. What distinguishes Pinnacle West is not the theme but the concentration and the regulator. Its growth is unusually anchored in a small number of gigawatt-scale industrial tenants — the fabs and hyperscalers — rather than diffuse population growth, which makes the story both higher-beta and more dependent on a handful of counterparties honoring long-dated commitments. And it is uniquely exposed to an elected commission, whereas many peer utilities answer to appointed regulators whose decisions, while still political, are at least one step removed from the ballot box. Arizona pairs one of the best demand backdrops in the country with one of the more volatile regulatory frameworks — a combination that can amplify returns in a constructive cycle and punish them in a populist one. That is the trade the market is pricing.

An activist or short-seller pressing on this business would zero in on precisely these seams: the widening gap between soaring reported sales growth and the actual cash returns those sales generate after lag; the concentration of the growth story in a handful of enormous customers with outsized negotiating leverage; the walk-back of the public decarbonization commitment; and the conspicuous absence of a hard affordability metric in executive pay at a company whose defining historical failure was an affordability scandal. None of these is disqualifying. All of them are real. The counter that a long-term bull would offer is equally fair: the demand is not speculative vaporware but poured concrete and signed interconnection agreements; the regulator has, since 2021, moved demonstrably back toward the center; and a utility trading at the top of its historical range while growing rate base at a mid-to-high single-digit clip is not obviously mispriced if that growth proves durable and recoverable. The debate, in the end, is not about whether the demand is real. It is about the terms on which Pinnacle West gets to serve it.

Which is why, for tracking this company over the years ahead, an investor can ignore most of the noise and watch a very small number of things. The first is the spread between authorized and actually earned return on equity — the concrete, quarter-by-quarter measure of whether the company is closing the regulatory-lag gap or losing to it; management has stated a goal of earning within roughly 50 basis points of its authorized return by 2029, and that convergence is the entire operational thesis.30 The second is weather-normalized commercial and industrial sales growth, the truest live signal of whether the Silicon Desert demand is actually showing up on the meter. And the third is the conversion rate of that enormous uncommitted interconnection queue into firm, contracted load — the number that tells you how much of the boom is real and how much is a mirage shimmering off the desert floor. Everything else is commentary.

X. Epilogue & The Active Rate Case Climax

Every thread of this story — the MeraBank scar, the Palo Verde crown jewel, the Pullman tragedy, the 2021 punishment, the Silicon Desert boom, the new leadership — converges on a single proceeding now unfolding inside a government building in downtown Phoenix.

On June 13, 2025, APS filed its latest general rate case with the Arizona Corporation Commission, requesting an authorized return on equity of 10.7% based on a 2024 test year, and seeking a base-rate revenue increase of roughly $662 million — an average customer bill impact in the mid-teens percent.28 This is the moment the entire recovery strategy has been building toward: the formal ask for the returns and cost-recovery mechanisms needed to finance the grid the fabs and data centers require. The hearing phase began on May 18, 2026, and it opened, tellingly, with hours of public testimony from customers protesting the proposed increase — a vivid reminder that in Arizona, every dollar of rate base ultimately lands on a household electric bill in a place where that bill can be a matter of life and death.29

A decision is expected in the second half of 2026 — an administrative law judge's recommended order likely in the autumn, with a commission vote to follow.28 As of this writing in July 2026, the outcome is genuinely unknown, and it is difficult to overstate what rides on it. A constructive decision — a fair return, and the formula-rate and cost-recovery tools management has requested — would validate the entire post-2021 rehabilitation, narrow the regulatory lag that stands between Pinnacle West and the earnings its growth implies, and confirm that the company can finance the Silicon Desert without breaking its own balance sheet. A punitive decision would reopen every wound of 2021 and cast doubt on whether a monopoly serving trillion-dollar tech tenants can ever extract fair terms from an elected commission answerable to angry ratepayers.

That is the balancing act, stated plainly and without a bow on top: Ted Geisler and Andrew Cooper must persuade five elected politicians to approve the rates that global technology giants' infrastructure demands, without loading a politically explosive burden onto the air-conditioning bills of ordinary Arizona families — the very failure that nearly destroyed the company's regulatory standing once already. The dividend yield that draws income investors sits near 3.4% at recent prices, materially below the 4.5%–5% a casual glance at the sector might assume, because the market has already bid the shares up toward the top of their multi-year range on the growth story — which means a great deal of optimism is already in the price.4

Pinnacle West is no longer the sleepy, bond-like utility of the investor imagination. It has become something stranger and more consequential: a defensive monopoly transformed, almost against its own institutional temperament, into a leveraged play on the physical infrastructure of the computing age. Whether that transformation compounds shareholder wealth or merely shareholder risk will be decided not by the brilliance of a chip designer in Taiwan, but by the far less glamorous verdict of a regulatory commission in the Arizona desert — the same desert where, nearly a century and a half ago, a few thousand people decided they wanted electric light.

References

-

Energy Considerations at the Dawn of Strategic Manufacturing — CSIS, 2024-04-19 ↩

-

TSMC Announces $100 Billion Investment for New Arizona Facilities — Greater Phoenix Economic Council, 2025-03-03 ↩

-

Rising data center loads pose grid reliability, residential cost risks: APS executive — Utility Dive, 2024-11-11 ↩

-

Pinnacle West Capital Corp. FY2025 Form 10-K — SEC / Pinnacle West, 2026-02-25 ↩↩↩

-

History of Pinnacle West Capital Corporation — FundingUniverse ↩↩↩↩↩

-

Nuclear Generation / Palo Verde Generating Station — Arizona Public Service (aps.com) ↩↩↩↩

-

On 107-Degree Day, APS Cut Power to Stephanie Pullman's Home. She Didn't Live — Phoenix New Times, 2019-06-14 ↩↩↩↩

-

APS vows legal action after Arizona regulators deny cost recovery for $215.5M coal plant upgrades — Utility Dive, 2021-11-03 ↩↩

-

Arizona's Utility Regulatory Environment: Improving or False Dawn? — FactSet Insight ↩↩

-

Fitch Downgrades Pinnacle West Capital Corp. to 'BBB+' Following ACC Rate Decision — Fitch Ratings, 2021-11-09 ↩

-

Pinnacle West Capital Corp. FY2021 Form 10-K — SEC / Pinnacle West, 2022-02-25 ↩↩

-

Arizona Public Service Company v. Sierra Club and RUCO (No. 1 CA-CC 21-0002) — Arizona Court of Appeals / FindLaw, 2023-03-07 ↩

-

Arizona Public Service reaches settlement with ACC to recover Four Corners investment — Utility Dive, 2023-06 ↩

-

Looking Ahead: New APS Plan Addresses Growing Customer Energy Needs — Arizona Public Service Newsroom ↩

-

Pinnacle West maps EPS growth, $10B+ APS capex and 2025 rate case — StockTitan, 2026-05-06 ↩

-

APS to convert retired coal units, adding 380 MW of natural gas — Utility Dive, 2026-07-06 ↩

-

Cholla Power Plant Conversion Project — Arizona Public Service ↩

-

APS Voluntarily Commits to 100% Carbon-Free Electricity by 2050, 45% Renewables by 2030 — Sierra Club, 2020-01 ↩

-

Major Western Transmission Project Connecting Utah and Nevada Advances — American Public Power Association ↩

-

Pinnacle West Capital Corp. 2025 Proxy Statement (DEF 14A) — SEC / Pinnacle West, 2025-04-08 ↩↩↩↩↩↩↩

-

Form 8-K — Appointment of Andrew D. Cooper as CFO — SEC / Pinnacle West, 2022-05-11 ↩↩

-

Pinnacle West Announces Executive Management Changes — Arizona Public Service Newsroom, 2022-05-12 ↩

-

Pinnacle West Capital Corp. FY2024 Form 10-K — SEC / Pinnacle West, 2025-02-25 ↩

-

Pinnacle West Capital Corp. FY2024 Form 10-K, Exhibit 21.1 (Subsidiaries) — SEC / Pinnacle West, 2025-02-25 ↩

-

APS rate case kicks off with hours of protest over 14% rate increase — Arizona Capitol Times, 2026-05-19 ↩↩

-

Pinnacle West Capital Corporation Q1 2026 Earnings Conference Call — Pinnacle West Investor Relations, 2026-05-04 ↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube