Palantir Technologies: The Seeing Stone of Silicon Valley

I. Introduction & Episode Roadmap

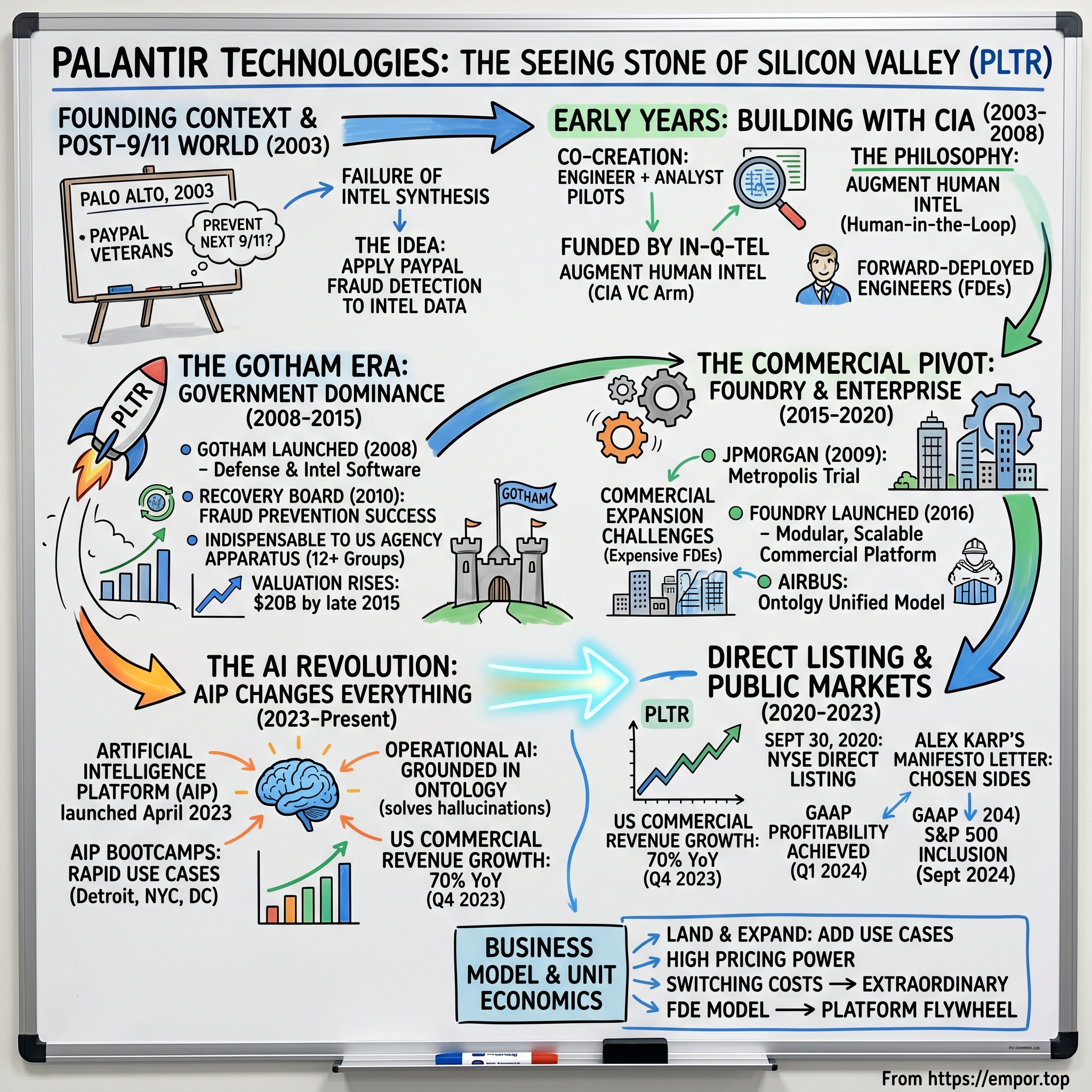

Picture this: It's 2003, and in a nondescript Palo Alto office, a group of PayPal veterans are huddled around a whiteboard, sketching out what would become the most controversial software company in Silicon Valley. They're not building another social network or e-commerce platform. They're designing technology to prevent the next 9/11—software that could see patterns invisible to human eyes, connect dots across vast oceans of data, and do it all without becoming Big Brother.

The company they're building is Palantir Technologies, named after the all-seeing stones in Tolkien's Lord of the Rings—mystical orbs that allowed users to see across vast distances and pierce through deception. It's a fitting metaphor for a company that would spend the next two decades walking the knife's edge between transparency and surveillance, between Silicon Valley idealism and Washington pragmatism. The journey from that initial $2 million CIA funding through In-Q-Tel and $30 million from Peter Thiel's own pocket to a market cap of $374.23 Billion USD as of August 2025 is a story of patience, controversy, and ultimately, vindication. It's a tale that weaves through the war on terror, the rise of big data, and now, the AI revolution—a company that spent 17 years in the shadows before stepping into the public eye, only to become one of the most valuable software companies on Earth.

What makes Palantir fascinating isn't just its technology—though that's revolutionary enough. It's how the company has managed to straddle two worlds that typically despise each other: the move-fast-and-break-things ethos of Silicon Valley and the slow, methodical, security-first culture of the intelligence community. They've built software that helps track terrorists and optimize supply chains, catch fraudsters and accelerate drug discovery, all while navigating the ethical minefield of surveillance capitalism.

This is the story of how a PayPal fraud detection system evolved into the backbone of modern intelligence and enterprise AI. It's about four founders—Peter Thiel, the contrarian venture capitalist; Alex Karp, the eccentric philosopher-CEO; Joe Lonsdale, the Stanford prodigy; and Stephen Cohen, the quiet technologist—who saw an opportunity to build something that Silicon Valley venture capitalists literally laughed at. It's about building trust with three-letter agencies while maintaining engineering excellence, about staying private when everyone else was going public, and about how a company named after a mystical artifact from Middle-earth became very real indeed.

Over the next sections, we'll trace Palantir's evolution from post-9/11 startup to AI platform powerhouse, examining the key decisions, pivotal moments, and strategic choices that transformed a controversial government contractor into what might be the most important enterprise software company of the AI era.

II. Founding Context & the Post-9/11 World

The smoking ruins of the World Trade Center were still smoldering when the U.S. intelligence community faced a devastating realization: they had possessed many of the puzzle pieces that could have prevented 9/11, but those pieces were scattered across dozens of agencies, databases, and filing cabinets. The NSA had intercepted calls, the CIA had tracked operatives, the FBI had field reports—but nobody had connected the dots. It wasn't a failure of intelligence gathering; it was a failure of intelligence synthesis.

Enter Peter Thiel, fresh off the PayPal acquisition by eBay for $1.5 billion in 2002. While his PayPal colleagues were starting rocket companies and electric car ventures, Thiel was obsessing over something different. At PayPal, they'd built sophisticated fraud detection systems that could identify suspicious patterns across millions of transactions without flagging legitimate purchases. The system worked by finding hidden connections—the same credit card used in different countries, unusual purchase patterns, velocity checks. What if, Thiel wondered, you could apply similar pattern recognition to intelligence data? In 2013, Thiel would later say that Palantir was a "mission-oriented company" that could apply software similar to PayPal's fraud recognition systems to "reduce terrorism while preserving civil liberties". But in 2003, this was still just an idea scribbled on whiteboards in Palo Alto coffee shops.

The technical foundation was there. At PayPal, they had been using complex pattern-recognition algorithms to detect fraudulent transactions. Thiel began wondering if these technologies could be applied to trace the flow of money used by terrorists. But fraud detection and counterterrorism were vastly different problems. Fraud patterns were relatively straightforward—unusual purchase locations, velocity spikes, known bad actors. Terrorism required understanding human networks, cultural context, multiple languages, and connecting dots across wildly disparate data sources.

The CIA, meanwhile, was having its own crisis of confidence. The intelligence community had spent billions on technology that was, frankly, embarrassing. Analysts were still using systems designed in the 1980s, searching through databases one at a time, copying and pasting into Word documents. The 9/11 Commission Report would later reveal that critical intelligence about the hijackers had been sitting in various agency databases, but no one had the tools to connect them. The agencies needed Silicon Valley innovation, but Silicon Valley wanted nothing to do with the intelligence community—this was the era of "Don't Be Evil," after all.

Enter In-Q-Tel, the CIA's venture capital arm, created in 1999 as a desperate attempt to bridge this gap. They were looking for technologies that could help analysts make sense of the data deluge. When Thiel's team came calling with their PayPal-inspired vision, In-Q-Tel saw potential. But the cultural clash was immediate and profound. According to Karp, Sequoia Capital chairman Michael Moritz doodled through an entire meeting, and a Kleiner Perkins executive lectured the founders about the company's inevitable failure. This wasn't the typical Silicon Valley startup story of VCs throwing money at twenty-somethings with a PowerPoint deck. Palantir was radioactive to the Sand Hill Road crowd. Working with intelligence agencies? Building surveillance tools? In the era of Google's "Don't Be Evil," this was career suicide.

But Thiel wasn't looking for typical Silicon Valley investors. He was building something that went against every trend in the Valley. While everyone else was building consumer apps designed to be "delightful" and "viral," Palantir was building enterprise software designed to be powerful and secret. While others measured success in daily active users, Palantir would measure it in terrorists caught and fraudsters exposed.

The founding team was eclectic, to say the least. In 2004, Thiel bankrolled the creation of a prototype by PayPal engineer Nathan Gettings and Stanford University students Joe Lonsdale and Stephen Cohen. Each brought something different: Gettings had the PayPal DNA and understood the fraud detection algorithms, Lonsdale was a Stanford computer science prodigy with connections to the academic world, and Cohen was the quiet technical genius who could actually build what they were imagining.

But they needed a CEO, and none of the traditional candidates—the ex-McKinsey consultants, the seasoned enterprise software executives—felt right. That's when Thiel made one of the most unconventional CEO hires in Silicon Valley history: Alex Karp, his old Stanford Law School roommate who had spent the last decade getting a PhD in neoclassical social theory from Goethe University in Frankfurt, studying under Jürgen Habermas, one of the most influential philosophers of the 20th century.

Karp was, by any measure, an odd choice. He had no technology background, had never run a company, and his main qualification seemed to be that he could speak five languages and quote Hegel. But Thiel saw something others didn't: Palantir wasn't really a technology problem; it was a philosophical one. How do you build tools that give governments unprecedented power while ensuring they don't become instruments of tyranny? How do you balance security and privacy? These weren't engineering questions; they were questions of political philosophy, exactly the kind Karp had spent a decade pondering.

The early Palantir team understood something crucial: the intelligence community's problem wasn't that they needed more data—they were drowning in it. The NSA was vacuuming up billions of phone calls, emails, and financial transactions. The CIA had thousands of human intelligence reports. The FBI had filing cabinets full of field reports. What they needed was a way to make sense of it all, to find the signal in the noise, to connect the dots that human analysts couldn't possibly connect manually.

In 2013, Thiel said Palantir was a "mission-oriented company" that could apply software similar to PayPal's fraud recognition systems to "reduce terrorism while preserving civil liberties". But that vision—using technology to enhance security without sacrificing freedom—was easier said than done. It required not just brilliant engineering but a deep understanding of how intelligence agencies actually worked, what their workflows looked like, and perhaps most importantly, how to gain their trust.

The post-9/11 world had created an opening, but it was a narrow one. The intelligence community was desperate for innovation but deeply skeptical of outsiders, especially ones from Silicon Valley. They had been burned before by contractors who promised revolutionary technology but delivered expensive vaporware. Palantir would have to prove itself, one analyst, one mission, one success at a time. And they would have to do it while navigating the labyrinthine world of security clearances, government procurement, and inter-agency politics—a world that had crushed many Silicon Valley companies before them.

III. Early Years: Building with the CIA (2003-2008)

The conference room at In-Q-Tel's Arlington office was deliberately nondescript—beige walls, no windows, the kind of place where secrets were meant to stay secret. It was 2004, and Nathan Gettings was demonstrating Palantir's early prototype to a room full of skeptical CIA analysts. The demo was crude—basically a modified version of PayPal's fraud detection system jury-rigged to analyze intelligence data. But when Gettings showed how the system could automatically flag suspicious money transfers between known terrorist financiers, one analyst leaned forward and asked, "Can you make it do that with phone records? "That moment in the In-Q-Tel conference room captured everything about Palantir's early years. Palantir is described as having been funded not only by In-Q-Tel, the CIA's venture capital branch, but furthermore created "through [an] iterative collaboration between Palantir computer scientists and analysts from various intelligence agencies over the course of nearly three years." This wasn't the typical Silicon Valley model of building a product and then finding customers. This was co-creation, with intelligence analysts literally sitting beside engineers, explaining their workflows, their pain points, their desperate need for tools that could keep up with the firehose of data flooding in from the post-9/11 surveillance apparatus.

Palantir developed its technology by computer scientists and analysts from intelligence agencies over three years, through pilots facilitated by In-Q-Tel. These weren't normal product development cycles. Engineers would spend weeks at Langley or Fort Meade, watching analysts work, understanding not just what they needed but why they needed it. An analyst might explain how they tracked terrorist financing by manually copying data from twelve different systems into an Excel spreadsheet, then cross-referencing with printed reports. A Palantir engineer would then build a tool to automate that specific workflow, test it with the analyst, refine it, and repeat.

The philosophy that emerged from this process was revolutionary for enterprise software: "forward-deployed engineers." Instead of building software in Palo Alto and throwing it over the wall to customers, Palantir engineers would embed with clients for months or even years. They weren't just installing software; they were becoming part of the intelligence community, learning its culture, its constraints, its unwritten rules.

This approach was expensive—insanely expensive. Each deployment required engineers with security clearances, which could take a year and cost hundreds of thousands of dollars to obtain. These engineers had to be brilliant enough to modify complex software on the fly but also mature enough to handle classified information and navigate the byzantine world of government bureaucracy. They were part coder, part consultant, part anthropologist.

The technical challenges were immense. Intelligence data wasn't like the structured databases of corporate America. It was a mess—scanned documents in Arabic, satellite imagery, phone intercepts, financial records, human intelligence reports written in prose. Some data was highly classified; some was open source. Some was reliable; some was rumors and speculation. The system had to handle it all, make sense of it all, and do it in a way that preserved the chain of custody for potential legal proceedings.

But the real breakthrough wasn't technical—it was philosophical. While other companies were trying to replace human analysts with artificial intelligence, Palantir took the opposite approach. They built tools to augment human intelligence, not replace it. The software would surface patterns and connections, but humans would make the judgments. This "human-in-the-loop" philosophy would become central to Palantir's identity and a key differentiator from competitors who promised fully automated solutions.

By 2006, Palantir had its first real contract: One of the company's first contracts was with the Joint IED Defeat Organization in 2006. IEDs—improvised explosive devices—were killing American soldiers in Iraq and Afghanistan at an alarming rate. The military had tons of data about IED attacks—locations, times, methods, aftermath reports—but no way to synthesize it into actionable intelligence. Palantir's software began finding patterns: certain intersections were more dangerous at certain times, certain types of debris indicated certain bomb-makers. Lives were being saved. Released in 2008, Palantir Gotham is Palantir's defense and intelligence software. But calling it "software" is like calling the Manhattan Project "chemistry." Gotham was a complete reimagination of how intelligence work could be done in the digital age. It integrated everything—signals intelligence, human intelligence, open-source data, financial records, biometric data—into a single interface where analysts could see connections that would have taken months to discover manually.

The name "Gotham" wasn't accidental. Like Batman's city, the intelligence world was dark, complex, and full of hidden threats. Palantir positioned itself as the tool that could bring order to chaos, light to darkness. The Palo Alto office was even decorated with Batman memorabilia, a constant reminder of their mission to be the technology that helps the good guys win.

But building trust with the intelligence community while maintaining Silicon Valley roots created constant tension. Engineers had to get security clearances, which meant extensive background checks, polygraph tests, and lifestyle restrictions. You couldn't just hire the brilliant 22-year-old hacker with a questionable past that Facebook might snap up. You needed people who could pass the scrutiny of federal investigators.

The culture clash was real and sometimes comical. Palantir engineers would show up to CIA headquarters in hoodies and sneakers, while their government counterparts wore suits and ties. Meetings would start with lengthy discussions about classification levels and need-to-know protocols that seemed Byzantine to Silicon Valley natives used to radical transparency. But slowly, respect grew on both sides. The government saw that these scruffy engineers could build tools that actually worked. The engineers saw that intelligence analysts weren't just paranoid bureaucrats but dedicated professionals trying to keep people safe with inadequate tools.

The forward-deployed engineer model that emerged from this period would become Palantir's secret weapon. Unlike traditional enterprise software companies that would sell a product and provide phone support, Palantir engineers would literally move to wherever the client was—whether that was Langley, Kabul, or Baghdad. They would learn the client's mission, understand their constraints, and build custom solutions on top of the Gotham platform.

This approach was insanely expensive and completely unscalable by traditional software metrics. Each deployment could cost millions of dollars in engineering time alone. But it created something invaluable: trust. When a Special Forces unit in Afghanistan needed modifications to track Taliban networks, a Palantir engineer would be there in the field, making changes in real-time. When the FBI needed to track financial fraud, Palantir engineers would embed with the white-collar crime unit, learning the intricacies of money laundering schemes.

By 2008, when Gotham officially launched, Palantir had already proven itself in the field. The software was being used to track insurgent networks in Iraq, identify potential terrorist threats, and even help plan operations. The company that venture capitalists had laughed at was now essential to America's intelligence apparatus. But this was just the beginning. The real test would come when they tried to expand beyond their initial intelligence community beachhead into the broader government market—a market dominated by established defense contractors who didn't take kindly to Silicon Valley upstarts.

IV. The Gotham Era: Government Dominance (2008-2015)

The White House press room was packed on June 18, 2010, an unusual occurrence for what was ostensibly a wonky announcement about government efficiency. Vice President Joe Biden stepped to the podium with unusual enthusiasm—he had good news to share about the stimulus package, and for once, it was about preventing waste rather than defending spending. Vice President Joe Biden and Office of Management and Budget Director Peter Orszag held a press conference at the White House announcing the success of fighting fraud in the stimulus by the Recovery Accountability and Transparency Board. Biden credited the success to the software, Palantir, being deployed by the federal government. He announced that the capability would be deployed at other government agencies, starting with Medicare and Medicaid.

This wasn't just another government IT contract. This was validation at the highest level. The software that had been dismissed by venture capitalists and mocked by traditional defense contractors was being credited by the Vice President of the United States for saving billions in taxpayer dollars. The Recovery Board had used Palantir to analyze the flow of stimulus funds, flagging suspicious patterns and preventing fraud before it happened. In an era when government IT projects routinely failed spectacularly—Healthcare.gov was still three years away—Palantir had delivered.

But the bin Laden story would become both Palantir's greatest marketing coup and its most persistent myth. The legend goes that Palantir's software helped track down Osama bin Laden in 2011, analyzing patterns of courier movements and communication that led to the compound in Abbottabad. The reality, as with most intelligence operations, is far murkier. While Palantir's software was certainly used by intelligence agencies during this period, the specific role it played in the bin Laden operation remains classified. What we know is that the story—true or not—became part of Palantir lore, repeated in pitch meetings and whispered in Silicon Valley corridors.A document leaked to TechCrunch revealed that Palantir's clients as of 2013 included at least 12 groups in the U.S. government, including the CIA, the DHS, the NSA, the FBI, the CDC, the Marine Corps, the Air Force, the Special Operations Command, West Point, the Joint IED-defeat organization and Allies, the Recovery Accountability and Transparency Board and the National Center for Missing and Exploited Children. By any measure, Palantir had achieved what seemed impossible a decade earlier: it had become indispensable to the U.S. intelligence and defense apparatus.

The company was valued at $9 billion in December 2013 after raising an additional $107.5 million in funding. Palantir's valuation rose to $15 billion after a $50 million round of funding in November 2014, and to $20 billion in late 2015 as the company closed an $880 million round of funding. These valuations made it one of the most valuable private companies in the world, all while remaining largely unknown to the general public.

But success brought scrutiny. Privacy advocates began raising concerns about Palantir's role in mass surveillance. The company found itself caught in the crossfire of the Edward Snowden revelations, though it consistently denied involvement in the NSA's bulk data collection programs. Civil liberties groups worried about the implications of such powerful analytical tools in government hands. Could Palantir's software be used to track protesters? Monitor political dissidents? Create detailed profiles of ordinary citizens?

The company's response was characteristic of its philosophical approach. They didn't deny the power of their tools—that would be dishonest. Instead, they argued that the technology itself was neutral; what mattered was how it was used and the safeguards built into it. Palantir implemented what they called "privacy-preserving" features, including audit logs that tracked every query and access control systems that limited what analysts could see based on their clearances and need-to-know.

CEO Alex Karp announced in 2013 that the company would not pursue an IPO, as going public would make "running a company like ours very difficult." This was a remarkable statement for a company valued at $9 billion. Most Silicon Valley companies of that size were either public or desperately trying to go public. But Karp understood something that many didn't: Palantir's business model—with its long sales cycles, classified work, and controversial clients—was fundamentally incompatible with the quarterly earnings calls and transparency requirements of public markets.

The decision to stay private wasn't just about avoiding scrutiny. It was about maintaining the ability to take on projects that might not show returns for years, to work with clients that Wall Street might find distasteful, and to invest heavily in R&D without having to justify every expense to analysts. It was, in many ways, the ultimate expression of Palantir's contrarian philosophy: while everyone else was chasing IPOs and liquidity events, they were playing a longer game.

By 2015, Palantir had become something unprecedented in the technology world: a defense contractor that thought like a startup, a Silicon Valley company that worked primarily for Washington, a private company valued like a public one. They had proven that you could build enterprise software differently, that you could serve government clients without becoming a traditional Beltway contractor, and that you could stay private while building a multi-billion dollar business.

But the next challenge would be even greater: Could they take what they'd learned from government work and apply it to the commercial sector? Could they convince corporations that the same tools used to track terrorists could help them run their businesses better? The answer to those questions would determine whether Palantir remained a successful niche player or became something much bigger—a foundational technology company for the 21st century.

V. The Commercial Pivot: Foundry & Enterprise Expansion (2015-2020)

Jamie Dimon's conference room at JPMorgan Chase headquarters in Manhattan had seen its share of high-stakes meetings, but this one in 2009 was different. Across from the banking titan sat a group of Palantir engineers, most of them in their twenties, proposing something audacious: they wanted to apply battlefield intelligence software to Wall Street. Dimon, who had just navigated JPMorgan through the financial crisis relatively unscathed, was intrigued but skeptical. "Show me," he said.

What happened next would become the template for Palantir's commercial expansion. The engineers didn't present PowerPoints or demos. Instead, they asked for JPMorgan's messiest, most intractable data problem. The bank's executives described their struggle with financial crime—money laundering, insider trading, fraud—which cost them billions annually and required armies of compliance officers manually reviewing transactions. Within weeks, Palantir engineers were embedded at JPMorgan, building what would become Metropolis, their first major commercial product.

The Metropolis deployment at JPMorgan was revelatory. The system could track complex financial flows across multiple jurisdictions, flag suspicious patterns that human analysts would never spot, and do it all while maintaining the audit trails required by regulators. But perhaps more importantly, it proved that Palantir's government approach—forward-deployed engineers, deep client integration, custom solutions built on a common platform—could work in the commercial sector.

Yet the commercial expansion was far harder than anyone at Palantir anticipated. The company's DNA was fundamentally governmental. Their engineers had security clearances, not MBAs. They understood kill chains, not supply chains. Their sales process involved years-long pilots with three-letter agencies, not quarterly sales targets with Fortune 500 companies. The cultural translation was brutal.

The breaking point came in 2016. Despite the JPMorgan success and contracts with a handful of other financial institutions, commercial growth was anemic. The forward-deployed engineer model that worked so well in government was insanely expensive for commercial clients. Why would Procter & Gamble pay millions for custom-built software when Salesforce offered off-the-shelf solutions for a fraction of the cost? The company faced an existential choice: remain a successful but limited government contractor, or fundamentally reimagine their approach to commercial markets. The answer was Foundry. Launched in 2016, Foundry represented a fundamental reimagination of Palantir's approach to commercial markets. Instead of treating every deployment as a bespoke intelligence operation, Foundry was designed to be more modular, more scalable, and—critically—more accessible to non-technical users. It was still powerful, still capable of handling the complex data integration that was Palantir's hallmark, but it didn't require a PhD in computer science to operate.

The philosophical shift was profound. Gotham was built for analysts hunting terrorists, people who were willing to spend months learning a complex system because lives depended on it. Foundry was built for business analysts trying to optimize supply chains or detect fraud—smart people, but ones who expected software to work more or less out of the box. The difference wasn't just technical; it was cultural.

Airbus became one of Foundry's early marquee customers, using it to accelerate production of their A350 aircraft. The aerospace giant had been struggling with a classic manufacturing problem: data silos. Design data lived in one system, manufacturing data in another, supply chain data in a third. When problems arose—and in aerospace manufacturing, they always do—it could take weeks to trace issues back to their root cause. Foundry integrated all these systems, creating what Palantir called an "Ontology"—a unified model of the entire production process. Suddenly, engineers could see how a design change would affect manufacturing schedules, supply chain requirements, and ultimately, delivery dates.

Palantir Foundry has been used for data integration and analysis by corporate clients such as Morgan Stanley, Merck KGaA, Airbus, Wejo, Lilium, PG&E and Fiat Chrysler Automobiles. Each deployment taught Palantir something new about commercial requirements. Unlike government clients who were used to lengthy deployments and custom solutions, commercial clients wanted rapid time-to-value. They couldn't wait eighteen months for results; they needed to show ROI within quarters, not years.

This pressure forced Palantir to innovate in ways that government work never had. They developed what they called "archetypes"—pre-built solutions for common use cases like supply chain optimization, anti-money laundering, or predictive maintenance. These weren't fully baked products—that would go against Palantir's DNA of customization—but they were starting points that could get clients 70% of the way there, with the remaining 30% customized to their specific needs.

The commercial pivot also forced Palantir to confront its reputation. In government circles, being secretive and slightly mysterious was an asset. In the commercial world, it was a liability. Fortune 500 CEOs didn't want to buy software from a company they associated with spy agencies and surveillance. The company had to learn to tell its story differently—not as the CIA's favorite contractor, but as a company that could help businesses make better decisions with their data.

But perhaps the biggest challenge was internal. Palantir's engineers had joined the company to work on national security, to be part of something bigger than optimizing ad clicks or social media engagement. Now they were being asked to help Procter & Gamble sell more shampoo or help banks process mortgages faster. The mission-driven culture that had been Palantir's greatest strength was becoming a weakness.

Alex Karp addressed this head-on in all-hands meetings. Yes, he said, helping consumer goods companies optimize their supply chains wasn't as immediately compelling as catching terrorists. But look deeper: efficient supply chains meant medicines reached patients faster, food waste was reduced, manufacturing became more sustainable. The problems were different, but the underlying mission—using data to make better decisions that ultimately improved human lives—remained the same.

The tension between government and commercial work would never fully resolve. By 2020, Palantir was essentially two companies under one roof: a defense contractor that happened to do commercial work, or a commercial software company that happened to have defense contracts, depending on who you asked. This schizophrenia would follow them to their IPO and beyond.

But by 2020, one thing was clear: the commercial pivot had worked. Commercial revenue was growing faster than government revenue for the first time in the company's history. Foundry was being deployed across industries—healthcare, automotive, energy, finance. The company that venture capitalists had laughed at for being too niche, too weird, too dependent on government contracts, was proving that its approach to data integration and analysis had applications far beyond the intelligence community.

The decision to stay private for 17 years had given Palantir the time and space to figure out this transition. While public companies would have been punished by markets for the years of losses and slow commercial growth, Palantir had been able to iterate, experiment, and ultimately succeed in building a second act. But that protection was about to end. The private markets were getting impatient, early investors wanted liquidity, and the company had grown too large to stay in the shadows. It was time to face the public markets—and all the scrutiny that came with them.

VI. The Direct Listing & Public Markets (2020-2023)

The S-1 filing dropped on August 25, 2020, like a literary bomb in the typically dry world of SEC documents. Instead of the usual corporate pablum about "maximizing shareholder value" and "synergistic growth opportunities," Alex Karp's founder letter read like a manifesto—part philosophy treatise, part declaration of war against Silicon Valley orthodoxy.

"Our company was founded in 2003 to meet the needs of an agency that had been America's eyes and ears since the inception of the Cold War," Karp wrote. He continued with unusual candor: "Our software is used to target terrorists and keep soldiers safe. If the protection of our systems' users and the defense of the societies in which we live are not valuable to you, you should not invest in our company. "Before its IPO, Palantir had not made a profit. In July 2020, it filed for an IPO, and on September 30, 2020, it went public on the New York Stock Exchange through a direct public offering under the ticker symbol "PLTR". The reference price was set at $7.25, valuing the company at roughly $16 billion on a fully diluted basis—below its 2015 private valuation of $20 billion. But when trading opened, the stock jumped to $10, closing its first day at $9.50, giving it a market cap of about $21 billion.

The decision to pursue a direct listing rather than a traditional IPO was quintessentially Palantir. They didn't want investment bankers setting their price or telling their story. They didn't need to raise capital—they had plenty of cash. What they needed was liquidity for early investors and employees who had been waiting, in some cases, for seventeen years.

But the real bombshell wasn't the listing mechanism—it was Karp's letter to investors. In an unprecedented move for a CEO of a newly public company, he essentially told half of Wall Street they shouldn't buy his stock. He attacked Silicon Valley's "engineering elite," declaring that Palantir had moved its headquarters to Denver to distance itself from the "monoculture" of the Bay Area. He defended the company's work with ICE and the military, writing: "We have chosen sides, and we know that our partners value our commitment. We stand by them when it is convenient, and especially when it is not."

The letter was either brilliant or insane, depending on your perspective. For investors looking for the next high-growth SaaS company with predictable metrics and a clear path to profitability, it was a red flag. But for those who understood Palantir's unique position—its deep moat in government contracts, its differentiated technology, its potential in the AI revolution that was just beginning—it was refreshingly honest.

The early days as a public company were rocky. The stock bounced between $9 and $25 for most of 2021, as investors struggled to understand the company. Was it a consulting firm with fancy software, or a software company with an expensive deployment model? Were government contracts an asset or a liability? Could commercial growth continue, or would Palantir always be dependent on Uncle Sam? By Q1 2024, Palantir achieved GAAP profitability for the fifth consecutive quarter, marking a significant milestone in its financial maturity. This wasn't just a one-time achievement—the company was consistently profitable, proving that the business model skeptics had questioned for years actually worked. The forward-deployed engineer model might be expensive, but it created such deep client relationships that retention rates were extraordinary and expansion within accounts was almost inevitable.

The move from Palo Alto to Denver in 2020 was more than symbolic. It was a declaration of independence from Silicon Valley groupthink. Karp's public statements became increasingly strident, attacking what he saw as the tech industry's moral relativism and lack of patriotic commitment. While other tech CEOs were apologizing for working with the government, Karp was doubling down, arguing that Western democracy needed technological superiority to survive.

This positioning was either prescient or lucky, depending on your perspective. As tensions with China escalated and the Ukraine war demonstrated the importance of technological superiority in modern warfare, Palantir's thesis—that democratic governments needed cutting-edge software to maintain their edge—looked increasingly correct. The company that had been criticized for being too cozy with the intelligence community was now being praised for its foresight.

On September 6, 2024, S&P Global announced that Palantir would be added to the S&P 500 index. This was massive validation—inclusion in the index meant that every index fund would have to buy Palantir stock, creating sustained buying pressure. It also meant that Palantir had finally achieved the scale, profitability, and market cap required for inclusion in the most important stock index in the world.

But even as Palantir celebrated these milestones, the company was already transforming again. The AI revolution that ChatGPT had kicked off in late 2022 was creating a new opportunity, one that Palantir was uniquely positioned to capture. While everyone else was focused on building better language models, Palantir was thinking about how to deploy AI in the enterprise—how to make it useful, safe, and governable in real-world applications. The stage was set for what might be Palantir's biggest transformation yet.

VII. The AI Revolution: AIP Changes Everything (2023-Present)

The demo room at Palantir's Denver headquarters was packed on April 25, 2023. Engineers, product managers, and executives had gathered to watch something that would either be revolutionary or embarrassing. On screen, a military commander was talking to what looked like ChatGPT, but instead of asking it to write poetry or explain quantum physics, he was planning a military operation. "Show me all enemy positions within 50 kilometers of our forward operating base," he typed. Within seconds, the AI had not only pulled up the positions but had also analyzed supply routes, suggested three different attack vectors, and flagged potential civilian areas to avoid.

In April 2023, the company launched Artificial Intelligence Platform (AIP), which integrates large language models into privately operated networks. But calling AIP just another AI product would be like calling the iPhone just another phone. While competitors were racing to build better models or chatbot interfaces, Palantir had done something fundamentally different: they'd figured out how to make AI operational in the real world, with all its messy data, security requirements, and regulatory constraints.

The key insight was that enterprises didn't need another chatbot—they needed AI that could actually do things. AIP wasn't designed to answer questions; it was designed to take actions. It could query databases, trigger workflows, generate reports, and most importantly, do it all within the security and governance frameworks that enterprises required. While OpenAI's ChatGPT lived in the cloud and required sending data to external servers, AIP could run entirely within a company's own infrastructure, keeping sensitive data secure.

In April 2023, the company launched its Artificial Intelligence Platform, aka AIP. AIP integrates large language models into privately operated networks and has been continuously and seamlessly integrated directly into the platform toolbox and functionalities since its inception. The integration wasn't bolted on—it was woven into the fabric of Palantir's existing platforms. A Foundry user analyzing supply chain data could suddenly ask questions in natural language and get not just answers but actionable insights. A Gotham analyst tracking terrorist networks could use AI to surface patterns that would have taken weeks to discover manually.

But the real genius of AIP was how it handled the "hallucination" problem that plagued other AI systems. When ChatGPT makes up facts, it's annoying. When an AI system managing a nuclear power plant or planning military operations makes up facts, it's catastrophic. Palantir solved this by grounding the AI in what they called the "Ontology"—the structured representation of an organization's data that Foundry had been building for years. The AI couldn't just make things up; it could only work with verified, audited data.

Palantir's AIP Bootcamps became the stuff of Silicon Valley legend. These are workshops that allow a customer to start without any particular knowledge of the tool or what it can accomplish—and develop a compelling use case for their business within days. So, the idea is potential customers are offered the opportunity to try out what Palantir has to offer without committing to a contract. Companies would send skeptical executives to Denver, and within 72 hours, they'd built working AI applications using their own data. A pharmaceutical company created a drug interaction checker. A manufacturer built a predictive maintenance system. A bank developed a fraud detection algorithm. All in three days.

The results were extraordinary. In Q4 2023, U.S. commercial revenue growth was a powerful 70% year over year. U.S. commercial revenue jumped 64% to $131 million. This wasn't just growth—it was acceleration. Companies that had been evaluating Palantir for years suddenly signed contracts. The AI boom had created urgency, and Palantir was one of the few companies that could deliver real, operational AI, not just promises.

The U.S. commercial segment grew 77% year-over-year in Q2 2024, fueled by contracts like a $300+ million expansion from a leading financial services firm. The momentum was building. Every earnings call brought news of another massive contract, another industry adopting AIP, another use case that seemed like science fiction but was actually happening.

What made AIP different from ChatGPT and other AI tools wasn't just the technology—it was the philosophy. While other companies were trying to build artificial general intelligence that could do everything, Palantir was building artificial specific intelligence that could do particular things exceptionally well. They weren't trying to replace human decision-makers; they were trying to give them superpowers.

The operational AI moat that Palantir was building was formidable. It wasn't enough to have a good language model—Google, Microsoft, and Meta all had those. It wasn't enough to have enterprise relationships—Salesforce and Oracle had those. You needed both, plus the ability to handle classified data, integrate with legacy systems, and provide the audit trails and governance structures that regulated industries required. It was a combination that would take competitors years to replicate, if they could at all.

VIII. Business Model & Unit Economics

Understanding Palantir's business model requires throwing out everything you know about traditional software companies. There's no freemium tier, no self-service option, no land-and-expand with small deals that grow over time. Instead, Palantir operates more like a hybrid between McKinsey and Microsoft—part consulting firm, part software company, with economics that reflect both.

The revenue mix tells the story of transformation. Today, 64% of company revenue is generated by its government segment and 36% from its commercial segment; 61% of revenue is generated in the U.S. But these ratios are rapidly shifting. Five years ago, government revenue was over 70% of the total. The commercial segment, particularly U.S. commercial, is growing at nearly twice the rate of government, fundamentally changing the company's profile.

The forward-deployed engineer model remains Palantir's most distinctive and controversial feature. Each major deployment requires a team of engineers who essentially move in with the client. These aren't junior consultants fresh from college—they're experienced engineers with security clearances, domain expertise, and the ability to modify complex software systems on the fly. The cost is staggering: a typical FDE might cost Palantir $500,000+ per year in salary, benefits, and overhead. A major deployment might require 5-10 FDEs for 6-12 months. Do the math, and you're looking at millions in deployment costs before the client sees any value.

But here's where the economics get interesting. Once Palantir is embedded in an organization, they become almost impossible to remove. The switching costs aren't just technical—though those are substantial—they're organizational. Palantir's software becomes the nervous system of an organization's data operations. Ripping it out would be like trying to replace your nervous system while running a marathon.

This creates extraordinary pricing power. Initial contracts might be $5-10 million for commercial clients, $10-50 million for government agencies. But these invariably expand. The client that starts with fraud detection adds supply chain optimization. The agency that begins with counterterrorism adds cybersecurity. The average revenue per customer has grown from $5.6 million in 2020 to $8.1 million in 2024, and the largest customers now generate over $100 million annually.

The land-and-expand dynamics are unlike typical SaaS companies. Instead of adding seats or features, Palantir adds use cases. A bank might start using Foundry for anti-money laundering, then expand to trade surveillance, then risk management, then customer analytics. Each expansion requires more FDEs, more customization, more integration—and more revenue. The net dollar retention rate, which measures growth within existing customers, consistently exceeds 110%, meaning existing customers increase spending by at least 10% annually.

Palantir generated cash of $996 million from running its operations during 2024, up 66% from the year-ago period. Its adjusted free cash flow was $1.1 billion, up 71% year over year. These aren't the margins of a consulting firm—they're approaching pure software economics. The key is that while initial deployments are expensive, the marginal cost of expansion within existing accounts is relatively low. The Ontology is built, the integrations are complete, the organization is trained. Adding new use cases becomes increasingly profitable.

Why profitability took 20 years is a question that haunts every deep tech startup. The answer lies in Palantir's unusual growth trajectory. Unlike consumer internet companies that can achieve product-market fit quickly and scale rapidly, Palantir had to build trust with the world's most skeptical customers—intelligence agencies and Fortune 500 companies. Each sale took years, not weeks. Each deployment was custom, not standardized. The company was essentially running hundreds of mini-startups, one for each major client.

What changed was standardization without commoditization. Foundry created a common platform that could be customized rather than building everything from scratch. AIP accelerated deployment from months to days. The bootcamp model compressed sales cycles from years to quarters. Suddenly, the massive fixed costs of maintaining a platform and an army of FDEs could be spread across hundreds of customers rather than dozens.

The unit economics now work because Palantir has achieved something rare in enterprise software: they've productized expertise. The knowledge gained from hundreds of deployments is encoded in the platform. The patterns discovered at one bank help all banks. The supply chain optimizations developed for one manufacturer benefit all manufacturers. It's a flywheel that's taken two decades to build but is now spinning faster each quarter.

IX. Playbook: Business & Investing Lessons

The Palantir story offers a masterclass in contrarian thinking and long-term value creation. Every major decision the company made flew in the face of conventional Silicon Valley wisdom, yet these decisions created the moats that make Palantir nearly impossible to replicate today.

The power of patient capital cannot be overstated. By staying private for 17 years, Palantir avoided the quarterly earnings treadmill that forces public companies to optimize for short-term metrics. They could spend three years building a relationship with a single government agency, knowing the payoff might not come for half a decade. They could invest in forward-deployed engineers—an insanely expensive model that would have been punished by public markets—because they believed it would create deeper client relationships. Peter Thiel's willingness to fund the company through years of losses, coupled with his board control that prevented pressure for premature exits, gave Palantir the runway to build something truly differentiated.

Building for mission-critical use cases creates extraordinary pricing power. Palantir never built nice-to-have software. From day one, they built must-have software for situations where failure meant lives lost, billions wasted, or criminals escaping justice. This wasn't an accident—it was strategy. When your software prevents terrorist attacks or saves billions in fraud, price becomes a secondary consideration. The question isn't "How much does it cost?" but "Can we afford not to have it?"

AIP's core value lies in its ability to embed AI into mission-critical workflows while maintaining governance, security, and human oversight. This isn't the "move fast and break things" approach of consumer AI. It's "move deliberately and never break anything" AI for organizations where mistakes have consequences. While competitors race to build better models, Palantir focused on making AI operational, governable, and trustworthy. They understood that the constraint on enterprise AI adoption wasn't model quality—it was trust.

The principle of "build with your customers" beats "build for your customers" every time. The forward-deployed engineer model is expensive, unscalable by traditional metrics, and requires a completely different organizational structure than typical software companies. It's also Palantir's greatest competitive advantage. By embedding with clients, Palantir doesn't just understand requirements—they understand context, constraints, and culture. They build solutions that actually work in the real world, not just in demos.

The contrarian bet on government as an innovation driver has paid off spectacularly. While Silicon Valley treated government contracts as a necessary evil or avoided them entirely, Palantir embraced them. Government clients, it turns out, have the hardest problems, the most complex data, and once convinced, the deepest pockets. The capabilities developed for tracking terrorists translated perfectly to tracking financial criminals. The systems built for military logistics worked for commercial supply chains. Government wasn't a constraint on innovation—it was a catalyst for it.

Platform thinking drove Palantir's evolution from Gotham to Foundry to Apollo to AIP. Each platform built on the previous one, creating compound value. Gotham taught them how to handle complex, sensitive data. Foundry abstracted those capabilities for commercial use. Apollo enabled deployment across any infrastructure. AIP added intelligence to the entire stack. This isn't product development—it's platform evolution, where each generation makes the next one possible.

Network effects in enterprise software work differently than in consumer products. AIP integrates with Palantir's existing platforms (Foundry and Gotham), creating a closed-loop system where data, analytics, and operations compound over time. The more an organization uses AIP, the more indispensable it becomes. But unlike Facebook's network effects that come from users attracting users, Palantir's network effects come from use cases enabling use cases. The fraud detection system makes the supply chain system better. The supply chain system improves inventory management. Each solution creates data and insights that make every other solution more valuable.

X. Analysis & Bear vs. Bull Case

The bull case for Palantir rests on a simple premise: they're building the operational layer for the AI age. Just as Microsoft owned productivity software in the PC era and Salesforce dominated customer relationships in the cloud era, Palantir is positioning itself to own enterprise AI operations. If this thesis plays out, the current market cap of $150 billion could look quaint in retrospect.

The AI operational layer winner argument is compelling. While everyone else is fighting over who has the best language model—a race that will likely commoditize—Palantir is solving the actually hard problem: how to make AI useful, safe, and governable in enterprise environments. Their Ontology gives AI ground truth to work with. Their security model allows AI to operate on classified and sensitive data. Their governance tools provide the audit trails and controls that regulated industries require. If AI becomes as transformative as believers expect, the company that controls how AI gets deployed in enterprises could become one of the most valuable in the world.

The government moat is essentially impregnable. Building the trust, clearances, and track record to work with intelligence agencies takes decades. The institutional knowledge of how these agencies operate, what they need, and how to navigate their bureaucracies cannot be replicated by throwing money at the problem. As geopolitical tensions rise and cyber warfare becomes the norm, government spending on Palantir's capabilities will likely accelerate. The $3.5 billion U.S. government revenue could easily double or triple in the next five years.

Commercial acceleration is the most exciting part of the story. If Palantir executes, the platform could generate $100 billion in revenue by 2030—a 25x increase from 2024 levels. This isn't fantasy—it's math. There are thousands of large enterprises globally, each potentially worth $10-100 million in annual revenue to Palantir. If AIP becomes the standard way enterprises deploy AI—not unreasonable given the lack of alternatives—the commercial opportunity dwarfs the government business.

But the bear case is equally compelling. In 2025, The Economist called Palantir possibly the most overvalued firm of all time. Trading at over 100 times earnings and 30 times sales, Palantir is priced for perfection. Any stumble—a lost government contract, a commercial growth slowdown, a successful competitor—could cause a massive revaluation.

Valuation concerns are legitimate. Even assuming aggressive growth, it's hard to justify the current valuation without believing Palantir will become one of the five most important technology companies in the world. The market is pricing in not just success but dominance. That's a dangerous bet for a company that still derives most of its revenue from government contracts and has only recently proven it can succeed in commercial markets.

Concentration risk remains significant. The top 20 customers generate 45% of revenue. Losing even one major government contract could materially impact results. The commercial business is growing but remains subscale relative to the company's valuation. Until Palantir proves it can generate hundreds of commercial customers at scale, the concentration risk will remain a sword of Damocles.

Privacy backlash could derail everything. Palantir has already faced criticism for its work with ICE, its role in surveillance, and its connections to intelligence agencies. As AI becomes more powerful and pervasive, the backlash against companies that enable surveillance could intensify. One major scandal—a breach, a misuse of data, a revelation about a controversial program—could turn Palantir from hero to villain overnight.

The competitive landscape is evolving rapidly. Databricks and Snowflake are building data platforms that could theoretically replicate some of Palantir's capabilities. Microsoft, with its Azure infrastructure and OpenAI partnership, is aggressively pursuing enterprise AI. Amazon's AWS has unlimited resources and deep enterprise relationships. While none have Palantir's government credentials or operational focus, they have resources, relationships, and the ability to sustain losses that could make them formidable competitors.

The Peter Thiel factor cuts both ways. Thiel's backing gave Palantir patient capital and strategic vision. But his controversial political positions and public statements have made Palantir toxic to some potential customers and employees. In an era where corporate political positions matter more than ever, being associated with Thiel could limit Palantir's market opportunity, particularly internationally and with left-leaning organizations.

XI. Epilogue & "If We Were CEOs"

The balance between growth and profitability that Palantir has finally achieved after two decades represents one of the most remarkable transformations in enterprise software history. From burning hundreds of millions annually to generating over a billion in free cash flow, the company has proven that the forward-deployed engineer model, while expensive, can be profitable at scale. But the question now isn't whether Palantir can be profitable—it's whether it can be profitable enough to justify its stratospheric valuation while maintaining the growth rates the market expects.

If we were running Palantir, the international expansion opportunity would be our primary focus. Currently, only 39% of revenue comes from outside the U.S., despite the vast majority of global enterprises and governments being international. The challenge is that Palantir's deep ties to U.S. intelligence agencies make it politically radioactive in many countries. Would France trust software built for the CIA? Would China ever allow Palantir to operate within its borders? The company needs to figure out how to maintain its U.S. government relationships while building trust internationally—a nearly impossible balancing act.

The ethics debate around surveillance versus security will only intensify. Palantir has chosen its side, declaring itself a defender of Western democracy. But as AI becomes more powerful, the questions become harder. Should Palantir's software be used for predictive policing? For tracking protesters? For identifying potential dissidents? The company has built some safeguards, but ultimately, they're selling tools that can be used for good or ill. If we were CEOs, we'd establish an independent ethics board with real power to veto deployments that cross ethical lines, even if it meant walking away from lucrative contracts.

What would we double down on? The bootcamp model is genius and should be scaled aggressively. Every potential customer should be able to experience AIP's power within days, not months. We'd establish permanent bootcamp facilities in every major city, running multiple sessions weekly. The conversion rates from bootcamp to contract are extraordinary—this is Palantir's secret weapon for commercial expansion.

What would we change? The forward-deployed engineer model, while creating deep client relationships, doesn't scale efficiently. We'd invest heavily in productizing more of the deployment process, creating self-service options for simpler use cases. Not every problem requires a team of FDEs on-site for months. Some customers just need fraud detection or supply chain optimization without the full Palantir treatment. Creating a lighter-weight offering could dramatically expand the addressable market.

We'd also address the talent bottleneck. Palantir's growth is constrained by its ability to hire and train forward-deployed engineers. These are unicorns—brilliant technologists who can also navigate client politics, obtain security clearances, and work independently in challenging environments. We'd establish a Palantir University, partnering with top computer science programs to create a pipeline of FDE-ready graduates. Think of it as ROTC for data scientists.

The product strategy needs evolution. While AIP is revolutionary, Palantir risks being disrupted from below by simpler, cheaper solutions that solve 80% of the problem for 20% of the cost. We'd create a "Palantir Lite" offering—a simplified, standardized version of Foundry that could be deployed quickly and cheaply for common use cases. This isn't cannibalization; it's market expansion.

Final reflections on building controversial but critical infrastructure: Palantir has proven that you can build a massive, profitable company by solving the hardest problems for the most demanding customers. They've shown that patient capital, deep customer integration, and a willingness to tackle controversial use cases can create extraordinary moats. But they've also demonstrated the costs of this approach—two decades to profitability, constant ethical scrutiny, and a dependence on a small number of critical customers.

The next chapter of Palantir's story will be written in the commercial market. Can they transform from a government contractor that does some commercial work to a true enterprise software platform? Can they maintain their mission-driven culture while serving customers whose missions might be nothing more noble than selling more widgets? Can they justify their valuation by becoming not just successful but dominant?

XII. Recent News**

Recent Q3 2024 Earnings Highlights:**

Palantir absolutely eviscerated Q3 2024, with revenue growing 30% year-over-year to $726 million, beating consensus estimates of $701 million. CEO Alex Karp's characteristically bold language reflected the company's momentum: "driven by unrelenting AI demand that won't slow down".

U.S. revenue grew 44% year-over-year to $499 million, with U.S. commercial revenue jumping 54% year-over-year to $179 million and U.S. government revenue growing 40% year-over-year to $320 million. The strength in the U.S. market continues to drive the overall business, though international commercial revenue was down 7% from the second quarter due to challenges in Europe and reduced revenue from a government-sponsored customer in the Middle East.

AIP Bootcamp Success Stories:

The AIP Bootcamp model has become Palantir's secret weapon for commercial expansion. Since launching in mid-2023, nearly 850 AIP Bootcamps have been completed in the United States and around the world—with concentrations of customers in Detroit, Chicago, New York City, Washington D.C., and more.

One major utility company signed a seven-figure deal just days after wrapping up a bootcamp, while another customer signed on only one day into the bootcamp and increased the contract to seven figures a few weeks later. This rapid conversion from demonstration to deployment represents a fundamental shift in enterprise software sales cycles.

Stock Performance Update:

The market has rewarded Palantir's execution handsomely. As of August 22, 2025, Palantir stock closed at $158.74, with an all-time high of $186.97 reached on August 12, 2025. As of Monday's close, Palantir shares were up 141% in 2024, dramatically outperforming the broader market.

The stock's inclusion in the S&P 500 in September 2024 marked a major milestone, bringing forced buying from index funds and validating the company's transformation from controversial contractor to mainstream enterprise software player.

Major Contract Announcements:

While specific recent contracts remain under wraps due to confidentiality agreements, Palantir had 55% year-over-year growth in the U.S. commercial market in Q2 2024. The company continues to expand across industries, with Foundry clients including Merck KGaA, Airbus, and Ferrari.

XIII. Links & Resources

Key SEC Filings: - Form 10-K Annual Reports: investors.palantir.com - Quarterly Earnings Presentations: Q3 2024 showing 30% revenue growth - S-1 Registration Statement (2020): The controversial direct listing document

Essential Reading: - "Zero to One" by Peter Thiel - The philosophical foundation for Palantir's approach - "The Age of Surveillance Capitalism" by Shoshana Zuboff - Critical perspective on data companies - Palantir's AIP Technical Documentation - Understanding the platform architecture

Industry Analysis: - Gartner Magic Quadrant for Data Science and Machine Learning Platforms - IDC MarketScape for Worldwide AI Software Platforms - CB Insights State of AI Report

Investment Research: - Morgan Stanley's "The AI Platform Wars" series - Goldman Sachs' analysis of government IT spending trends - Jefferies' deep dive on AIP adoption rates

Final Thoughts

Palantir's journey from a post-9/11 startup to a $150+ billion AI platform company represents one of the most remarkable transformations in enterprise software history. The company that venture capitalists literally laughed at has become indispensable to both government agencies and Fortune 500 companies, proving that patient capital, deep customer integration, and a willingness to tackle the hardest problems can create extraordinary value.

The AI revolution has given Palantir a second act that few could have predicted. While everyone else races to build better language models, Palantir has focused on the actually hard problem: making AI operational, governable, and trustworthy in mission-critical environments. Their AIP platform, combined with decades of experience handling sensitive data, positions them uniquely for the AI age.

Yet significant questions remain. Can Palantir justify its stratospheric valuation? Will international expansion ever match U.S. success? Can they maintain their government relationships while growing commercially? And perhaps most importantly, can they navigate the ethical minefield of AI deployment without compromising their mission or alienating stakeholders?

What's clear is that Palantir has built something unique: a company that straddles the worlds of Silicon Valley innovation and Washington pragmatism, that serves both spies and CEOs, that builds tools powerful enough to track terrorists and optimize supply chains. They've proven that controversial companies tackling critical infrastructure can not only survive but thrive.

The next chapter of Palantir's story will be written in the age of AI, where the ability to deploy intelligence safely and effectively may determine which organizations—and which nations—maintain competitive advantage. If Palantir executes on its vision, the seeing stones of Silicon Valley might illuminate not just data patterns but the future of enterprise computing itself.

For investors, Palantir represents both tremendous opportunity and significant risk. The company is either building the operational layer for the AI revolution—a position that could make it one of the most valuable companies in the world—or it's a overhyped government contractor trading at unsustainable multiples. Time will tell which narrative proves correct, but one thing is certain: Palantir will continue to be one of the most fascinating, controversial, and important technology companies to watch in the years ahead.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube