Planet Fitness: Building the Judgment Free Zone Empire

I. Introduction and Episode Roadmap

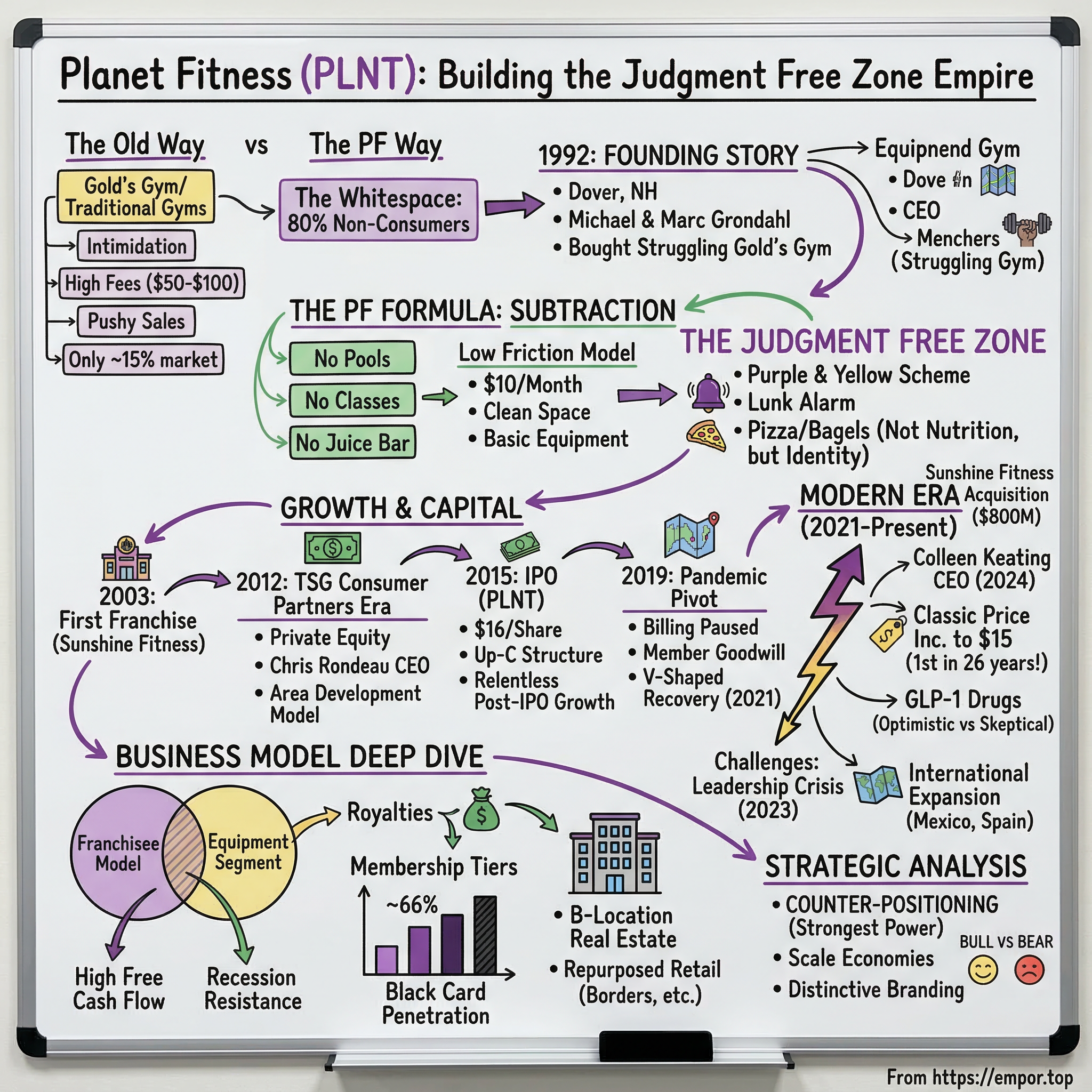

Here is a question that should not make sense: How did a gym chain become worth more than five billion dollars by actively discouraging serious exercise? By serving pizza on Mondays and bagels on Tuesdays? By installing a loud siren—called the "Lunk Alarm"—designed to publicly shame anyone who grunts while lifting? And by charging just ten dollars a month when competitors were asking ten times that?

Planet Fitness is one of the most counterintuitive success stories in American business. In an industry built on aspiration, intimidation, and the promise of transformation, Planet Fitness chose a radically different path. It chose subtraction. No pools. No group classes. No juice bar. No personal trainers pushing upsells. Instead, it offered a clean, well-lit space full of basic cardio and strength equipment, wrapped in a purple-and-yellow color scheme that screamed approachability over intensity. And for that stripped-down experience, it charged so little that canceling the membership felt like more hassle than it was worth.

The result is a business that has grown from a single struggling gym in Dover, New Hampshire, to nearly 2,900 locations across the United States, Canada, Mexico, Panama, Australia, and Spain. As of year-end 2025, Planet Fitness claimed 20.8 million members—making it the largest gym chain in America by membership count. Revenue topped 1.3 billion dollars. The franchise model generates enormous free cash flow. And the stock, which debuted at sixteen dollars per share in August 2015, has traded as high as one hundred fourteen dollars.

But here is the deeper question, and the one that makes this story worth a full episode: Is Planet Fitness actually a fitness company? Or is it something else entirely—a franchise operation, a real estate play, a consumer psychology experiment dressed up in workout clothes? The answer, as with most great businesses, is that it is all of those things simultaneously. And understanding how each layer fits together is what separates the surface-level narrative from the real story.

The journey from Dover to global franchise empire runs through private equity transformations, a recession that supercharged growth, a pandemic that nearly killed the business, a CEO firing that shocked the market, and a pricing decision in 2024 that may have permanently altered the company's identity.

Along the way, the founders, operators, and investors who built Planet Fitness made a series of bets that looked crazy at the time and brilliant in hindsight—almost all of them rooted in a single insight about human psychology that the rest of the fitness industry had been ignoring for decades.

This is the story of how serving the customer nobody wanted created one of the most profitable franchise systems in America.

II. The Fitness Industry Before Planet Fitness

To understand why Planet Fitness worked, you first need to understand the world it was born into. And that world was, frankly, hostile to most Americans.

Picture a typical American gym in 1990. Walk through the front door and the first thing you notice is the smell—a cocktail of rubber flooring, sweat, and disinfectant that signals this is a place of serious physical effort. The walls are lined with mirrors, not for aesthetics but for form-checking, and every mirror reflects bodies that have been sculpted through years of dedicated training. The free weight area—always the center of gravity in these places—is dominated by large men in tank tops, headphones on, moving through choreographed routines with the focused intensity of surgeons. The clanking of plates, the rhythmic grunting, the occasional crash of a barbell being dropped from shoulder height—these are the ambient sounds. For the person who already exercises, this environment is motivating. For everyone else, it is a minefield of self-consciousness.

Gold's Gym, the iconic chain that grew out of Venice Beach bodybuilding culture in the 1960s, set the aesthetic template that most gyms followed for decades. Arnold Schwarzenegger trained at the original Gold's. So did Lou Ferrigno, Franco Columbu, and the cast of characters who turned Venice Beach into the "Mecca of Bodybuilding." When Gold's began franchising in the 1980s, it brought that culture—ambitious, intense, and implicitly exclusive—to strip malls across America. Other chains followed the same playbook. 24 Hour Fitness, Bally Total Fitness, and a constellation of regional operators all built their businesses around the same core assumption: gym members are people who want to get serious about fitness.

The business model matched the culture. Membership fees at traditional gyms typically ran fifty to one hundred dollars per month, sometimes more. Contracts locked members in for twelve to twenty-four months with steep early termination penalties. The real money, though, came from personal training upsells—sessions that could cost sixty to one hundred dollars an hour—and from ancillary revenue like juice bars, supplement sales, and branded merchandise. The sales process itself was notoriously aggressive. High-pressure tactics, limited-time offers, and emotional manipulation were standard operating procedure. Walking into a gym to "just look around" was like walking into a car dealership: you were not leaving without a pitch. Sales staff were trained to use urgency and scarcity: "This rate is only available today." "We only have two memberships left at this price." The entire experience, from the moment you walked in the door to the moment you signed a contract, was designed to maximize the operator's revenue per member.

This model worked well enough for the operators who ran it. But it had a fundamental problem that almost nobody in the industry was thinking about. Roughly eighty to eighty-five percent of Americans did not belong to a gym. Industry data from the late 1990s and early 2000s showed total gym memberships hovering around thirty to forty million in a country of nearly three hundred million people. The fitness industry had, in effect, built itself to serve a small minority of the population and was fighting viciously over that same slice of the pie. It was as if the restaurant industry had decided to only serve people who already knew how to cook.

Why did the vast majority opt out? The reasons were layered. Cost was the obvious barrier—fifty to one hundred dollars a month was real money for middle-income families, especially when the value proposition was uncertain. If you were not sure whether you would actually use the gym, committing to eighty dollars a month felt like a gamble. But research consistently showed that cost was not the primary obstacle. Intimidation was. Survey after survey found that the culture of traditional gyms made casual exercisers, first-timers, and people who were out of shape feel unwelcome. The jargon, the posturing, the implicit judgment of not knowing how to use a machine or not lifting enough weight—these psychological barriers were more powerful than the financial ones. People would rather sit on their couch than walk into a room where they felt like the least fit person present.

There was also a deeper sociological dynamic at work. The fitness boom of the 1980s, driven by Jane Fonda aerobics videos and the rise of gym culture, had created a binary: you were either a "gym person" or you were not. If you were a gym person, you had the wardrobe, the water bottle, the knowledge of muscle groups and rep counts. If you were not, the gym was foreign territory—a place with unwritten rules you did not know, equipment you could not operate, and social dynamics you could not navigate. The industry did nothing to bridge this gap because it did not see a gap. It saw a well-served market of fitness enthusiasts and assumed that everyone else simply did not want to exercise.

This was the whitespace. The eighty percent. The non-consumers, in Clayton Christensen's language. They were not choosing between Gold's Gym and 24 Hour Fitness. They were choosing between the gym and the couch. And nobody was building a gym specifically for them. Nobody was asking the question that would eventually make two brothers from New Hampshire very wealthy: What if we built a gym for people who do not like gyms?

III. The Founding Story: From Bankruptcy to Breakthrough (1992-2002)

In 1992, Michael and Marc Grondahl were not fitness visionaries. They were two brothers from New Hampshire looking for a business opportunity. Michael, a Bryant University graduate, was the more entrepreneurial of the pair—restless, idea-driven, and willing to take risks that more cautious operators would avoid. Marc was steadier, more operationally minded. Together, they scraped together enough capital to buy a struggling Gold's Gym franchise in Dover, a small city of about thirty thousand people near the state's short stretch of Atlantic coastline. The gym was failing, and the Grondahls bought it on the cheap—the kind of deal that looked like either a bargain or a mistake depending on your perspective. Michael had what he later described as "an unfathomable dream" of someday growing to one hundred franchise locations. At the time, with a single underperforming gym in a town most Americans could not find on a map, that dream was audacious to the point of absurdity.

The early years were a grind of trial and error. The brothers operated the gym under the Gold's Gym banner initially, but they began experimenting almost immediately with the formula. They watched their members closely—not just who came in, but who did not come back. And the pattern was unmistakable: the people who signed up and disappeared were not the serious lifters. They were the regular people. The woman who tried the treadmill once and never returned. The middle-aged man who bought a membership in January and stopped coming by February. They were leaving not because the equipment was wrong or the hours were inconvenient. They were leaving because of how the gym made them feel. The heavy lifters grunting and slamming weights. The mirrors everywhere reflecting bodies that did not match the posters on the wall. The sales staff pushing personal training packages. Every element of the traditional gym experience seemed designed to remind casual exercisers that they did not belong.

The Grondahls started stripping things away. They lowered prices. They softened the atmosphere. They stopped pushing personal training. They asked a question that would become the foundation of everything that followed: Why does eighty to eighty-five percent of the population not belong to a gym? The answer was not about equipment or location or hours. It was about psychology. People stayed away from gyms because gyms made them feel bad about themselves.

Enter Chris Rondeau. In 1993, the Grondahls hired a local kid—eighteen years old, fresh out of high school—to work the front desk. Rondeau had no particular background in fitness or business. He was not a bodybuilder or an athlete. He was a kid from New Hampshire who needed a job, and a gym front desk was hiring. But Rondeau turned out to be extraordinarily good at the thing that mattered most in this particular business: talking to regular people about exercise without making them feel inadequate. He was approachable, unpretentious, and genuinely enthusiastic. He understood instinctively what the Grondahls were learning through experimentation—that the biggest barrier to gym membership was not price or convenience but feelings. He worked his way up from the front desk to management, eventually becoming the company's chief financial officer and, ultimately, its CEO. Rondeau's trajectory from minimum-wage front desk employee to the corner office of a publicly traded company is one of the great bootstrap stories in American franchising, and it gave him an invaluable perspective: he understood the member experience from the ground level in a way that no MBA hire ever could. He had swiped cards, wiped down equipment, fielded cancellation calls, and watched thousands of people walk through the door—some never to return. He knew exactly which moments mattered.

By the time the Grondahls had expanded to their third location in Concord, New Hampshire, around 1998, the core concept had crystallized. They were building what they called a "Judgment Free Zone"—a gym where the cardinal sin was not weakness or inexperience but intimidation. They installed the Lunk Alarm, a loud siren that staff could trigger when someone grunted excessively, dropped weights, or otherwise exhibited the kind of behavior that made casual exercisers uncomfortable. It was part tongue-in-cheek, part dead serious. And it sent an unmistakable signal: this gym is not for serious lifters. This gym is for everyone else.

The pricing matched the positioning. Memberships started at ten dollars a month—a price so low that it seemed almost irrational. To understand how radical this was, consider the context: the average gym membership in the late 1990s cost between fifty and one hundred dollars per month. Planet Fitness was pricing at eighty to ninety percent below the industry average. At ten dollars, the barrier to entry essentially disappeared. You could join Planet Fitness for less than the cost of two lattes at Starbucks. Less than a single movie ticket. Less than a medium pizza. And at that price, you could also forget about it entirely and never bother to cancel. The effort required to pick up the phone and cancel—or, as Planet Fitness required for years, to send a certified letter or visit in person—far exceeded the ten dollars per month you would save. Both dynamics—the low barrier to entry and the low barrier to remaining a member—were features, not bugs. They were the engine of the entire business model.

In 2002, the Grondahls purchased the rights to the name "Planet Fitness" from Rick Berks, who had started his own gym under that name in Sunrise, Florida, in 1993 and expanded to three clubs. The name change was more than cosmetic. It gave the brand an identity that was fun, accessible, and untethered from the serious-lifter culture that dominated the industry. Planet Fitness sounded like a place where you could show up in jeans and nobody would care.

The first franchise agreement came in 2003, when Eric Dore and Shane McGuiness opened a Planet Fitness in Altamonte Springs, Florida, under the Sunshine Fitness banner. That partnership would prove enormously consequential—Sunshine Fitness eventually became one of the largest franchisees in the system and, two decades later, the subject of an eight-hundred-million-dollar corporate acquisition. But in 2003, it was simply proof of concept: someone outside the Grondahl family believed in the model enough to bet their own money on it. The franchise era had begun.

IV. The TSG Consumer Partners Era: Private Equity Transformation (2003-2012)

The decade between the first franchise opening in 2003 and the private equity recapitalization in 2012 was when Planet Fitness transformed from a regional curiosity into a national franchise system. But the catalyst that turned a handful of New Hampshire gyms into a scalable machine was not a brilliant marketing campaign or a technological breakthrough. It was money—specifically, the kind of disciplined, growth-oriented capital that private equity firms specialize in deploying.

In November 2012, TSG Consumer Partners acquired a majority stake in Planet Fitness. TSG, a San Francisco-based private equity firm, had a track record of identifying and scaling consumer brands—its portfolio had included investments in Starbucks, Vitamin Water, and Pabst Blue Ribbon, among others.

TSG was not buying a gym. It was buying a franchise system with extraordinary unit economics, a massive addressable market, and a brand identity that was both distinctive and defensible. The firm's playbook was well-established: professionalize the operations, standardize the franchise model, accelerate unit growth, and position the company for an eventual public offering or secondary sale.

The professionalization effort was immediate and comprehensive. Michael Grondahl stepped down as CEO in 2013, and Chris Rondeau—the former front desk kid who had risen through the ranks—took the helm.

The choice was deliberate. Rondeau understood the culture, the franchisees, and the operations in a way that an outside hire could not. But he now had the backing of a sophisticated financial partner that could provide the systems, processes, and capital that a founder-led operation typically lacks.

One of TSG's most important contributions was refining the franchise structure, and this is worth dwelling on because it explains how Planet Fitness scaled so rapidly with so little corporate capital. Most people think of franchising as selling individual restaurant or store licenses one at a time—the way a McDonald's franchise might work, where a single operator buys the right to operate a single location. Planet Fitness did something different. It adopted an Area Development model that sold development rights for entire geographic territories. A franchisee would sign an Area Development Agreement committing to open a specified number of locations within a defined territory over a set timeline. The Area Development Fee was ten thousand dollars per planned location, paid upfront. This approach had several profound advantages: it attracted well-capitalized, sophisticated operators—often private equity-backed groups—rather than small-time entrepreneurs running a single gym; it created contractual growth commitments that the company could count on and plan around; and it gave management visibility into its expansion pipeline years in advance. Think of it like selling a developer the right to build an entire subdivision, rather than selling individual house lots one by one.

The real estate strategy was equally deliberate. Planet Fitness targeted what the industry calls "B-locations"—strip malls, suburban retail plazas, and second-generation retail spaces. These were not the gleaming downtown addresses that Equinox or Life Time Fitness pursued. They were the kind of spaces anchored by a grocery store or a big-box retailer, located on busy suburban roads with ample parking.

The typical Planet Fitness occupied twenty to twenty-five thousand square feet of repurposed retail space—often the kind of space that a defunct Circuit City or Borders bookstore had left behind. This approach kept build-out costs and rents dramatically lower than premium locations while still providing the visibility and foot traffic that a consumer-facing business needs.

Everything about the physical experience was standardized with the precision of a fast-food franchise. The purple-and-yellow color scheme became sacrosanct—every wall, every piece of equipment, every staff shirt adhered to the palette. Equipment layouts followed corporate templates, ensuring that a member walking into a Planet Fitness in Phoenix would have the same experience as one walking into a location in Philadelphia. The Lunk Alarm was not just a quirky local tradition from the New Hampshire days—it was installed in every single location as a physical manifestation of the brand promise.

The pizza and bagels deserve their own moment, because nothing captures the Planet Fitness philosophy more perfectly. Pizza Monday started informally in the late 1990s and was formalized into a system-wide event: free pizza on the first Monday of every month, free bagels on the second Tuesday. Tootsie Rolls sat in bowls at the front desk, available to every member on every visit. Critics have mocked this for years—a gym that serves junk food?—but that reaction is precisely the point. The pizza is not about nutrition. It is about identity. It says: we are not the gym that judges what you eat. We are not the gym that measures your body fat percentage or lectures you about your macros. We are the gym where you can grab a slice of pizza after walking on the treadmill for twenty minutes, and nobody will look at you funny. For the target customer—the person who has spent their entire life feeling judged about their body and their habits—that message is profoundly liberating.

The membership structure was equally refined into two tiers that would become the backbone of the revenue model. The base membership remained at ten dollars a month, providing access to a single home location. The Black Card membership, priced at roughly twenty to twenty-five dollars a month, added meaningful perks: access to any Planet Fitness location nationwide, the ability to bring a guest on every visit, and access to the "PF Black Card Spa."

The "spa" was not a spa in any traditional sense. It was a few massage chairs, HydroMassage beds, and tanning booths tucked into a corner of the gym. But the perception mattered more than the reality. The Black Card was a masterstroke of consumer psychology. For an extra ten to fifteen dollars a month, members got perks that felt premium without costing the company much to deliver. And it effectively doubled the revenue per member.

Then came the recession—and this is where the Planet Fitness story shifts from interesting to remarkable. The financial crisis of 2007 to 2009 devastated the American economy. Lehman Brothers collapsed. Housing prices cratered. Unemployment spiked above ten percent. Consumer spending contracted sharply, and discretionary expenses were the first to go. For premium gyms, the impact was devastating. Members who had been paying fifty or eighty dollars a month suddenly could not or would not justify the expense. Gym chains that had expanded aggressively during the boom years found themselves with too many locations, too few members, and too much debt.

Planet Fitness experienced the opposite effect. The recession created a perfect storm of demand for exactly what it offered. Consumers who had been paying premium prices traded down to the ten-dollar option—they still wanted to exercise, they just could not afford what they had been paying. First-time gym-goers who might have been intimidated by the financial commitment of a traditional membership found the ten-dollar entry point irresistible. And people who had lost jobs and were suddenly home during the day, looking for affordable activities and structure, discovered that a gym membership cheaper than a single restaurant meal was one of the few indulgences they could still afford. During the recession, Planet Fitness added 1.1 million members, grew same-store sales by double digits, and nearly doubled its store count. The broader fitness industry saw total memberships decline from 42.7 million in 2006 to 41.5 million in 2007. Planet Fitness was growing against the tide.

The recession proved something crucial about the business model: it was not just viable in good times. It was counter-cyclical. When the economy contracted, Planet Fitness got stronger. This is an extraordinarily rare quality in a consumer business. Most companies that serve discretionary needs suffer during recessions. Planet Fitness thrived because its price point is so low that it functions almost like a non-discretionary expense—cheaper than most alternatives for spending an hour outside the house, and psychologically valuable as a symbol of self-improvement during difficult times. That insight would inform the investment thesis for years to come and would prove prophetic again when the next crisis hit.

By 2012, when TSG recapitalized the business, Planet Fitness had grown to over five hundred locations. The franchise system was humming. The unit economics were proven. And the brand had demonstrated that it could thrive in exactly the economic environment that destroyed its competitors. The stage was set for the next transformation.

V. The Big Inflection: Going Public and Explosive Growth (2012-2015)

The years between the TSG recapitalization and the initial public offering were a masterclass in preparing a franchise business for the public markets. And the central challenge was not growing faster—Planet Fitness was already adding locations at a rapid clip—but engineering the corporate structure and financial architecture to maximize the value that public market investors would assign to the business.

Planet Fitness chose an "Up-C" corporate structure for its IPO, and while the details are arcane, understanding the structure is important because it affects how the company generates and distributes cash to this day. Here is the simplified version: Planet Fitness, Inc.—the publicly traded entity whose stock you can buy—does not actually operate any gyms. It is a holding company. Its sole material asset is an equity interest in Pla-Fit Holdings, LLC, which conducts all actual business operations. Think of it like a shell sitting on top of the real business.

The structure created two classes of common stock. Class A shares were what the public bought and traded on the stock exchange. Class B shares were issued to "Continuing LLC Owners"—the pre-IPO investors and operators, including TSG and the founders—on a one-for-one basis with their Holdings Units. These Class B shares carried voting rights but no economic rights; their economic interest flowed through the LLC rather than through the stock. When a pre-IPO owner wanted to cash out, they could exchange their Holdings Units for Class A shares—but that exchange triggered a tax event for the company.

Here is where it gets interesting: the company entered into Tax Receivable Agreements that entitled those pre-IPO owners to eighty-five percent of certain future tax savings generated by these exchanges. In plain English, when insiders converted their shares, the company got a tax benefit—but it had to pay eighty-five cents of every dollar of that benefit back to the insiders. Only fifteen cents stayed with the company.

If this sounds like financial engineering designed to maximize value for pre-IPO owners at the expense of public shareholders, that is a reasonable interpretation. The Up-C structure is perfectly legal and increasingly common among private equity-backed IPOs, but it creates a complex ownership web that can confuse investors and analysts. The key point for understanding Planet Fitness's post-IPO economics is this: the company's reported earnings and its actual cash generation are two different animals, and the Tax Receivable Agreements represent a real ongoing liability that reduces the cash available for reinvestment or shareholder returns. Investors who look only at earnings per share without understanding the TRA obligations are getting an incomplete picture.

On August 6, 2015, Planet Fitness priced its IPO at sixteen dollars per share—the top end of the fourteen-to-sixteen-dollar range—and began trading on the New York Stock Exchange under the ticker PLNT. The offering raised approximately 216 million dollars. At the time, the system had 976 stores and approximately 7.1 million members. The market capitalization at IPO was roughly 1.58 billion dollars.

For a chain of budget gyms that had existed in relative obscurity just a few years earlier, it was a remarkable debut. Wall Street was initially skeptical—a ten-dollar gym? How much can you really grow that?—but the skeptics were quickly silenced by the numbers. The franchise model's economics were unlike anything most gym industry analysts had seen. High margins, low capital intensity, recurring revenue, and a massive growth runway. It looked less like a gym company and more like a consumer franchise juggernaut in the mold of McDonald's or Subway.

The post-IPO growth trajectory was relentless. Revenue climbed steadily: 330 million in 2015, 378 million in 2016, 429 million in 2017, then a notable acceleration to 572 million in 2018 and 688 million in 2019. The company was opening more than two hundred new locations per year, and same-store sales were consistently positive.

By 2019, the system had crossed 2,000 locations and 14.4 million members. The stock, which had debuted at sixteen dollars, was trading above seventy dollars. In four years, Planet Fitness had more than quadrupled investor capital. An investor who bought at the IPO and held through 2019 would have been sitting on returns that rivaled the best-performing consumer franchises of the decade.

The geographic expansion followed a clustering strategy borrowed from Starbucks and other successful franchise operators. Rather than spreading locations thinly across the country, Planet Fitness saturated individual markets with multiple locations before moving to the next. Consider a metro area like Dallas-Fort Worth. Rather than open one Planet Fitness and then move on to Houston, the company would open five, then ten, then fifteen locations across the DFW metro—each one in a different strip mall, each one drawing from a different neighborhood, but all of them reinforcing the same brand message. This approach had several advantages: it created local brand awareness that made the marketing spend vastly more efficient, it allowed franchisees (often the same operator holding multiple locations in the market) to achieve operating efficiencies in staffing, management, and supply chain, and it made the national advertising spend more productive because campaigns reached a higher density of existing and potential customers in each market. The clustering strategy also created a competitive barrier: once Planet Fitness had fifteen locations in a metro area, a new entrant would need to match that density to compete effectively, a capital commitment that few were willing to make.

The split between corporate-owned and franchised locations remained heavily tilted toward franchisees—roughly ninety percent franchised, ten percent corporate-owned. This asset-light model was central to the investment thesis. Franchise royalties and fees flow to the corporate parent with minimal capital requirements. The franchisees bear the real estate risk, the staffing costs, and the operational complexity.

Corporate collects revenue from multiple streams: a seven-percent royalty on gross monthly membership fees, a two-percent national advertising fund contribution (capped at three percent), and initial franchise fees of twenty thousand dollars per location. But the most distinctive revenue stream—and the one that sets Planet Fitness apart from most franchise systems—is equipment placement fees.

That last revenue stream is worth pausing on because it is often misunderstood. Planet Fitness acts as a mandatory intermediary for all equipment purchases. It negotiates bulk pricing with manufacturers like Life Fitness and Hammer Strength, buys the equipment at volume-discounted prices, and resells it to franchisees at a markup. Franchisees are contractually required to purchase all equipment through corporate—they cannot shop around or negotiate their own deals. And they must refresh their equipment every five to seven years. This creates a captive, recurring revenue stream that is essentially toll-booth economics: every piece of equipment that enters a Planet Fitness location generates a margin for the parent company. Franchisees have no choice but to pay it.

Technology investments during this period were modest but strategic. The Planet Fitness mobile app allowed members to check in, find locations, and manage their accounts. The company invested in data systems to track member behavior and utilization patterns. But Planet Fitness never tried to become a technology company. The app was a utility, not a platform. The real product was the physical space—and the psychological permission it granted to people who had never felt welcome in a gym before.

VI. The Anti-Gym Gym: Business Model Deep Dive

The genius of the Planet Fitness business model is not any single element. It is the way every element reinforces every other element, creating a system that is extraordinarily difficult for competitors to replicate even though each individual component looks simple.

Start with the membership economics. At ten dollars a month—now fifteen dollars following the 2024 price increase—the Planet Fitness membership is priced below the threshold of financial attention for most American consumers. It costs less than a single lunch at a fast-casual restaurant. Less than a Netflix subscription. Less than two gallons of gas.

At this price point, something remarkable happens to consumer psychology. The traditional cost-benefit analysis that a person performs when deciding whether to renew a gym membership simply does not apply. Nobody calls to cancel a ten-dollar membership because they are not using it. The friction of cancellation—finding the number, waiting on hold, potentially being talked out of it—exceeds the financial reward of saving ten dollars. This is sometimes called the "sunk cost" model, but it is really the opposite: the cost is so low that it never feels sunk. It feels irrelevant.

Think of it this way: most Americans spend more on a single impulsive purchase at a convenience store than they spend on an entire month of Planet Fitness membership. The gym membership exists in the same mental category as a streaming subscription you rarely use—technically optional, practically invisible on the credit card statement, and not worth the five minutes it would take to cancel.

This pricing creates a utilization dynamic that is central to understanding why the model works—and why it is so different from traditional gym economics.

Traditional gyms need their members to show up. Their business model depends on selling things to people who are physically present: personal training sessions, smoothies, supplements, classes, spa services. An empty gym is a gym that is not generating ancillary revenue.

Planet Fitness's business model works best when members do not show up. Industry data suggest that roughly twenty to twenty-five percent of Planet Fitness members use their memberships with any regularity. The other seventy-five to eighty percent are paying ten to twenty-five dollars a month for the option to exercise, the psychological comfort of having a gym membership, and the vague intention of going "next week."

This is not cynical. It is economically rational on both sides. The member gets a low-cost option that makes them feel responsible about their health—a form of aspirational self-care that costs less than a single therapy session. And the gym gets to serve far more members per square foot than a facility where everyone actually shows up. A twenty-thousand-square-foot Planet Fitness might have fifteen thousand or more members on its rolls, knowing that on any given day, only a fraction will walk through the door. If every member showed up at once, the building would be a fire hazard. But they do not show up at once. Most do not show up at all. And that is the math that makes everything else possible.

The Black Card tier, priced at roughly twenty-five dollars per month, is where the real margin expansion happens. Black Card penetration has climbed steadily and reached approximately sixty-six percent of total membership by mid-2025. That number is remarkable—two out of every three Planet Fitness members voluntarily pay more than double the base price.

The perks that justify the upgrade cost the company relatively little to provide. Massage chairs and HydroMassage beds are capital expenditures that require no staff to operate—members use them self-service. Tanning beds have low variable costs. Access to any location is valuable to members but costs the company nothing incrementally. And the ability to bring a guest is actually a customer acquisition tool disguised as a perk—every guest who walks through the door is a potential new member.

The Black Card effectively doubles the revenue per member while adding only marginal cost. It is the most profitable feature of the entire business model.

The equipment segment deserves special attention because it is the most misunderstood part of the revenue model—and the one that most clearly reveals Planet Fitness's leverage over its franchise system.

Planet Fitness is not just collecting royalties from franchisees. It is acting as a mandatory equipment supplier. The company negotiates bulk purchasing agreements with major equipment manufacturers, buys the equipment at volume-discounted prices, and resells it to franchisees at a markup. Since franchisees are contractually required to purchase all equipment through corporate and must refresh their equipment on a five-to-seven-year cycle, this creates a captive, recurring revenue stream.

Equipment segment revenue reached 256 million dollars in 2024 and surged nearly fifty percent in the fourth quarter alone, driven by a wave of equipment refreshes across the system. This segment is inherently lumpy—it depends on the timing of franchise openings and refresh cycles—but over a multi-year period, it provides a meaningful and predictable contribution. For investors, the equipment revenue line is worth watching closely because it serves as a leading indicator of franchisee investment confidence and system health.

The deliberate absence of amenities is not a limitation. It is the strategy. Planet Fitness does not offer group exercise classes, pools, basketball courts, childcare, or saunas. This baffles industry observers who view amenities as essential to member retention. But each of those amenities carries significant cost.

Group exercise classes require dedicated studio space (reducing the floor area available for equipment), certified instructors (who command premium wages), and scheduling systems. Pools require enormous capital investment, specialized maintenance, lifeguards, and chemical treatment. Childcare requires dedicated rooms, background-checked staff, and liability insurance. Saunas require ventilation systems and constant monitoring.

By eliminating all of these, Planet Fitness keeps its operating cost per square foot dramatically below that of a full-service gym. A typical Planet Fitness can operate with a lean staff of around ten to fifteen employees per location, compared to fifty or more at a full-service facility. This cost structure is what makes the ten-to-fifteen-dollar membership mathematically viable. The amenities that competitors offer as differentiators are the same amenities that force them to charge five to ten times as much.

The real estate strategy amplifies the cost advantage. Second-generation retail spaces—the empty husks of retailers that have closed or downsized—offer Planet Fitness two advantages. First, the basic infrastructure (HVAC, plumbing, parking, visibility) already exists, reducing build-out costs. Second, landlords with vacant anchor or inline space are motivated to negotiate favorable lease terms. A landlord with a twenty-thousand-square-foot empty space in a strip mall would rather have Planet Fitness paying below-market rent and driving foot traffic than stare at a vacant storefront. Planet Fitness has been a direct beneficiary of the retail apocalypse—every closed bookstore, electronics shop, or department store is a potential new location.

Marketing reinforces the entire system. Planet Fitness spends heavily on national advertising—funded by the two-percent contribution from all franchisees—that consistently hammers two messages: this gym is not intimidating, and this gym is cheap. The campaigns are deliberately playful, often poking fun at the "serious gym" culture that Planet Fitness defines itself against. The "Judgment Free Zone" tagline has become culturally embedded in a way that few fitness brands can match. And the marketing works not just to acquire members but to reassure existing members that they made the right choice, reinforcing the psychological contract that keeps them paying even when they do not show up.

The alignment between corporate and franchisee incentives is strong but not perfect. Corporate benefits from franchise fees, royalties, equipment sales, and brand strength. Franchisees benefit from a proven model, national advertising support, purchasing power, and a brand that drives foot traffic. The tension arises primarily around equipment costs—franchisees have no choice but to buy through corporate at corporate's markup—and around the balance between new unit growth and cannibalization of existing locations. As the system has matured and territories have filled in, the risk that a new location steals members from an existing one has grown. Managing that tension is one of the central challenges of the next decade.

The franchisee economics, viewed in totality, help explain why the system has attracted and retained sophisticated, well-capitalized operators. The total initial investment to open a Planet Fitness ranges from approximately 1.5 million to 5.1 million dollars, depending on market and build-out complexity. The net worth requirement is three million dollars, with 1.5 million in liquid cash. These are not casual investors. They are serious operators, many of them backed by private equity firms, who have run the numbers and concluded that a Planet Fitness franchise offers among the best risk-adjusted returns in the franchise industry. Average gross revenue per location runs approximately 1.3 to 1.8 million dollars. Estimated annual earnings per mature location fall in the range of 215,000 to 269,000 dollars, and franchisees have historically earned cash-on-cash returns greater than twenty-five percent after royalties and advertising in their second year. Those are compelling numbers—compelling enough that the company is no longer offering new franchise opportunities in the United States because virtually every viable territory has been spoken for. The franchise system has essentially sold out domestically, which is both a testament to its economics and a constraint on future U.S. growth.

One additional nuance worth understanding: the franchise term is twelve years, meaning that the earliest franchise agreements are now approaching renewal. How the company manages those renewals—and whether it uses them as an opportunity to extract more favorable terms from franchisees or to reinvest in the relationship—will be an important signal about the long-term health of the system.

VII. Competition Heats Up: The Budget Gym Wars (2015-2019)

Planet Fitness did not invent the budget gym concept in a vacuum, and by the mid-2010s, a crowd of competitors had noticed the same whitespace. The question was whether anyone could replicate the formula—or whether Planet Fitness had built advantages that were more durable than they appeared.

Crunch Fitness, with its "No Judgments" philosophy, was the most direct competitor. Founded in New York City in 1989, Crunch had repositioned itself from a boutique urban gym into a multi-tiered franchise operation that included budget-friendly options. By the late 2010s, Crunch was growing aggressively, reaching over five hundred U.S. locations and planning approximately one hundred new openings per year. Among certain demographics—particularly young singles in urban markets—Crunch and Planet Fitness were polling at nearly identical popularity levels. Crunch offered something Planet Fitness did not: group fitness classes at its higher tiers. This gave it an edge with members who wanted a social workout experience without paying boutique prices.

Anytime Fitness pursued a different model entirely. With over 2,300 U.S. locations and 5,000 worldwide, Anytime Fitness was the largest gym franchise by location count globally. Its clubs were small—typically around five thousand square feet, compared to Planet Fitness's twenty-thousand-plus—and operated on a 24/7 unstaffed model with key-fob access. The membership price was higher, typically thirty to fifty dollars per month, but the convenience of a small, always-open gym within walking distance was compelling for a different segment of the market. Anytime Fitness was not really competing with Planet Fitness on price; it was competing on proximity and convenience.

Then there were the premium players attempting to move downmarket. Equinox launched Blink Fitness in 2011 as its entry into the budget segment. Blink offered clean, well-designed spaces with memberships starting around fifteen to twenty-five dollars per month. The concept seemed promising on paper: take Equinox's design sensibility and operational expertise and apply it to a high-volume, low-price format. But Blink never achieved the scale needed to compete with Planet Fitness's national footprint and advertising budget. By August 2024, Blink's parent entity filed for bankruptcy with roughly 280 million dollars in debt, and its hundred-plus locations were sold to PureGym for 121 million dollars. Planet Fitness had actually submitted an eleventh-hour bid to acquire Blink's assets, but a Delaware bankruptcy court rejected the offer, partly on antitrust grounds given Planet Fitness's dominant position. The episode was telling: Planet Fitness was so large that regulators worried about it acquiring a struggling competitor with barely a hundred locations.

The more existential competitive threat during this period came not from other gyms but from technology.

Peloton, which launched its connected bike in 2014, represented a fundamentally different value proposition: premium at-home fitness with instructor-led classes and a social community, all delivered through a screen. By 2019, Peloton had over half a million subscribers and was growing rapidly. Its pitch was seductive: never leave your house, never feel judged, get a better workout than any gym can offer, and join a community of like-minded people—all for the price of a high-end bike and a monthly subscription.

ClassPass offered a different kind of disruption—an app-based model that gave users access to classes at multiple boutique studios for a single monthly fee, unbundling the gym membership into a flexible marketplace. These digital competitors threatened to make the physical gym itself feel obsolete, particularly among younger, tech-savvy consumers who valued flexibility over commitment.

Planet Fitness's response to all of this competition was characteristically understated: it doubled down on what it already did. The company did not launch a streaming service. It did not add group classes. It did not introduce connected equipment. It did not raise prices. Instead, it opened more locations, spent more on national advertising, and continued to refine the execution of its existing model. The implicit bet was that the vast majority of Americans who wanted to exercise would always prefer an affordable, convenient, physical space over a two-thousand-dollar bike in their living room. And for the eighty percent of the population that did not belong to any gym at all, the relevant competition was not Peloton or SoulCycle. It was the couch.

International expansion also began during this period, though modestly. The first international location opened in Toronto, Canada, in December 2014. Latin American markets, starting with Mexico and Panama, followed. Australia came next. But international growth was deliberately slow. The company understood that its brand identity was deeply American—the pizza, the Lunk Alarm, the entire cultural positioning—and that translating it to other markets would require careful adaptation. By 2019, international locations still represented a tiny fraction of the total system.

What Planet Fitness did not do during this period was as revealing as what it did. It did not add group classes, even as competitors used them as a differentiator. It did not introduce personal training, even as the margins beckoned. It did not build a connected fitness platform, even as Peloton's valuation soared. It did not offer childcare, even as competitors used it to attract parents. Each of these decisions represented a temptation to expand the model—and each was resisted. The discipline of subtraction, which had defined the brand from the beginning, held firm even as the competitive landscape evolved around it. In a world obsessed with feature creep and product expansion, Planet Fitness's most important strategic decisions were the things it chose not to do.

The competitive landscape heading into 2020 was clear: Planet Fitness had established a commanding position in the high-volume, low-price segment of the U.S. fitness market. Its brand recognition, scale advantages, and proven unit economics gave it structural advantages that no competitor had been able to match. But the real test of those advantages was about to arrive in the most dramatic fashion imaginable.

VIII. COVID-19: The Existential Crisis (2020-2021)

On a Friday in mid-March 2020, gyms across America locked their doors. Not gradually, not partially—overnight. State governors issued emergency orders, health departments posted closure notices, and within the span of roughly seventy-two hours, every gym in the country went from open to dark. For an industry built on physical presence—people showing up to a building and using equipment that cannot be digitized, streamed, or shipped to their homes—the shutdown was not just a setback. It was an existential event. Revenue did not decline. It stopped. Completely. The treadmills kept their factory settings. The lights went off. The pizza ovens cooled.

Planet Fitness's stock, which had been trading near seventy-five dollars at the start of the year, cratered to under twenty-four dollars in the March panic—a decline of more than sixty percent. The financial logic was brutal and inescapable: a business whose entire value proposition required people to walk into a physical building was now legally prohibited from letting anyone through the door. Every fixed cost—rent, equipment leases, insurance, minimum staffing—kept running while every revenue dollar vanished. For franchisees who had taken on debt to build out their locations, the math was terrifying. For the corporate parent that depended on royalty streams from those franchisees, the cascade of risk was clear.

CEO Chris Rondeau faced a defining decision early in the crisis: what to do about membership billing.

Some gym chains continued charging members even though facilities were closed, betting that the combination of contract terms and consumer inertia would sustain revenue through the shutdown. The logic was coldly rational: most members will not bother to cancel, and the revenue keeps the lights on until reopening.

Rondeau chose the opposite approach. Planet Fitness paused membership billing entirely, forgoing revenue in exchange for member goodwill. It was an expensive decision—membership revenue is the company's lifeblood—but it preserved something more valuable: the relationship with millions of people who had trusted the brand with their credit card information. In an era of social media outrage, continuing to charge for a service you could not provide would have been a reputational catastrophe for a brand built on trust and fairness.

The strategic response to at-home fitness was revealing. While Peloton's stock was soaring and every gym chain in America was rushing to launch streaming workouts and virtual classes, Planet Fitness kept its digital response minimal. The company offered some free workout content through its app and social media channels, but it did not invest heavily in building a digital fitness platform. This was not laziness or denial. It was strategic clarity. Planet Fitness knew that its members were not paying for content or instruction. They were paying for access to a physical space. Building a streaming platform would not serve those members and would distract from the core business. The bet, again, was on the enduring value of the physical gym.

The financial impact was severe but not fatal. Full-year 2020 revenue fell to approximately 407 million dollars, down forty-one percent from 2019. Net income declined by over seventy-five percent.

Membership dropped roughly seven percent to approximately 13.5 million by year-end. Some members who had not been billed during the closure chose not to reactivate when billing resumed. The absence of walk-in traffic for months meant no new sign-ups to offset the attrition. For a business model built on volume, the combination of lost members and lost acquisition was a double hit.

But the reopening story was more encouraging than almost anyone expected. By the third quarter of 2020, ninety-five percent of Planet Fitness locations had reopened, and usage rates at open locations were approximately in line with pre-COVID levels. The company invested heavily in marketing during the reopening phase—advertising spending jumped fifty-nine percent year-over-year in Q3 2020—to communicate safety protocols and welcome members back. The message was calibrated: this is still the Judgment Free Zone, and it is safe.

By May 2021, Planet Fitness posted three consecutive months of positive net membership growth for the first time since the pandemic began. The recovery was not just a trickle—it was a wave. The company gained 1.7 million new members over the course of 2021, pushing total membership to approximately 15.2 million and surpassing pre-pandemic levels. The stock recovered to new all-time highs, trading above eighty dollars by the end of 2021.

The speed of the recovery surprised even the company's biggest advocates. The bear thesis during COVID had been that people would discover home fitness and never return to the gym. What actually happened was almost the opposite. After months of isolation, people craved the physical act of going somewhere—anywhere—outside their homes. The gym, even a no-frills one with fluorescent lighting and purple equipment, represented normalcy, routine, and a small assertion of control over one's life. For Planet Fitness members, many of whom had continued paying ten dollars a month throughout the closure, walking back through the door felt less like restarting a habit and more like coming home.

The pandemic validated several aspects of the Planet Fitness thesis that had been theoretical before. First, the low membership price created remarkable retention—members who were paying ten dollars a month simply did not bother to cancel, even during months of closure. Second, the demand for affordable, physical gym space proved far more durable than the tech optimists predicted. Peloton, which had seemed poised to replace the gym entirely, would soon enter a devastating downturn as consumers returned to in-person exercise. Third, Planet Fitness's franchisee network demonstrated resilience. Corporate supported operators through the crisis with deferred fees and operational guidance, and the vast majority of franchisees survived. The franchise model's distributed risk—where individual operators bear local economic exposure while corporate maintains the brand and system—proved its worth under the most extreme stress test imaginable.

The pandemic also clarified something about Planet Fitness's competitive moat. The connected fitness boom that had terrified gym operators in 2020 turned out to be a bubble inflated by stay-at-home orders, not a permanent shift in consumer behavior. Peloton's stock, which had peaked above 160 dollars in late 2020, would eventually collapse below ten dollars. The company lost CEO Barry McCarthy in 2024 and underwent multiple rounds of layoffs. Xponential Fitness, the largest franchisor of boutique fitness brands, dismissed its founder and CEO Anthony Geisler in May 2024 amid allegations of misconduct. The entire connected and boutique fitness ecosystem, which had seemed poised to replace the traditional gym, entered a period of painful contraction. When the choice between a two-thousand-dollar Peloton bike and a ten-dollar gym membership became available again, millions of Americans chose the gym. The post-pandemic world did not look like the futurists had predicted. It looked a lot more like 2019—with people wanting to leave their homes, go to a physical place, and move their bodies in the company of other humans. And for the budget-conscious majority, Planet Fitness was the most natural destination.

IX. The Modern Era: Maturity and New Challenges (2021-Present)

The post-pandemic Planet Fitness that emerged in 2021 and 2022 was financially stronger than ever—but it was also entering a new phase. The easy growth of the previous decade, when the company was expanding into vast stretches of underpenetrated geography, was giving way to the harder work of driving performance in a maturing system.

The numbers told the growth story clearly. Revenue recovered to approximately 587 million in 2021. Then in 2022, it surged to 937 million—a dramatic jump driven significantly by the landmark 800-million-dollar acquisition of Sunshine Fitness Management. This acquisition deserves a moment of attention because it fundamentally changed the corporate/franchise balance.

Sunshine Fitness was Planet Fitness's original franchisee—the same operator that Eric Dore and Shane McGuiness had built starting with that first location in Altamonte Springs, Florida, in 2003. Over two decades, Sunshine had grown into the system's largest franchisee, operating 114 locations. By acquiring Sunshine for 800 million dollars, Planet Fitness brought those locations onto the corporate balance sheet, shifting from roughly ninety percent franchised to a more blended model. The acquisition gave corporate direct operational control over a significant cluster of locations and provided a test bed for new initiatives—but it also added capital intensity and operational complexity to what had been an extraordinarily asset-light business.

Revenue crossed one billion dollars in 2023 and reached 1.2 billion in 2024. By year-end 2025, the company reported revenue of 1.3 billion dollars, adjusted EBITDA of 551.6 million, net income of 219.1 million, and earnings per share of $2.62. Membership reached 20.8 million across 2,896 clubs. The system had opened 181 new clubs in 2025 alone.

But beneath the headline numbers, challenges were accumulating—and in September 2023, the company experienced the most dramatic leadership crisis in its history.

On September 15, 2023, the board of directors fired Chris Rondeau as CEO. The man who had started at the front desk at age eighteen, who had built the company from a handful of New Hampshire gyms to nearly three thousand locations, who had been the face of Planet Fitness for a decade—was out. Rondeau himself described being "seriously blindsided" by the decision.

The stock dropped nearly twenty percent on the news, erasing billions in market value. Subsequent reporting in outlets like Fortune and Athletech News revealed allegations of a toxic workplace culture under Rondeau's leadership. The accounts were jarring: on-the-job drinking events nicknamed "Fireball Fridays" and "Beers with Peers," unprofessional weekend getaways, and a 2018 workplace lawsuit that had been filed against Rondeau and others. The picture that emerged was of a founder-era culture that had failed to evolve as the company grew from a small New Hampshire operation to a publicly traded corporation with billions in market capitalization.

Craig Benson, a former Governor of New Hampshire and long-serving Planet Fitness board member, stepped in as interim CEO while the company searched for a permanent replacement. Rondeau subsequently resigned from the board as well, severing his last formal ties to the company he had spent three decades building.

The search landed on Colleen Keating, who was announced in April 2024 and officially took the CEO role on June 10. Keating's background was in franchise operations and hospitality, not fitness. She had served as CEO of FirstKey Homes, the fourth-largest single-family rental property management company in the United States, from 2020 to 2024. Before that, she spent two years as COO of the Americas for InterContinental Hotels Group, overseeing more than four thousand hotels. And before IHG, she spent sixteen years at Starwood Hotels and Resorts, rising to Senior Vice President of Franchise Operations.

The hire signaled that the board viewed Planet Fitness's next chapter as primarily a franchise management and operational execution challenge, not a fitness industry challenge. Keating did not come from the gym world. She came from the world of managing thousands of properties across multiple markets and countries through franchise relationships. She knew how to optimize real estate portfolios, drive operational consistency across vast networks, and navigate the delicate politics of franchisor-franchisee relationships. Those were exactly the skills the company needed as it transitioned from high-growth domestic expansion to mature franchise optimization and international scaling.

Keating moved quickly to restructure the leadership team, elevating Bill Bode—formerly the Division President of U.S. Franchise operations—to a newly created Chief Operating Officer role, and moving Jennifer Simmons, who had led the Corporate Clubs division, into a new Chief Strategy position. The restructuring signaled a shift toward more formal operational hierarchy and strategic planning, the kind of infrastructure that a nearly three-thousand-location global franchise system requires but that a founder-led organization often resists.

In March 2026, CFO Jay Stasz departed, adding another layer of transition. Tom Fitzgerald was appointed interim CFO at a compensation of 250,000 dollars per month—a significant sum that reflected both the urgency of the role and the complexity of the company's financial structure. The company initiated a search for a permanent replacement. The leadership churn created uncertainty among investors—three different people in the CEO chair and now a CFO vacancy, all within thirty months—but it also represented a deliberate transformation from a founder-era management team to a professionally managed franchise organization. Whether the transformation produces better results or disrupts the culture that drove the first thirty years of success remains the central open question.

The most consequential decision of the modern era—and perhaps the most important strategic call since the original positioning decision three decades earlier—came in June 2024, when Planet Fitness raised the Classic Card membership price from ten dollars to fifteen dollars per month. This was the first price increase in over twenty-six years. To put that in perspective: when Planet Fitness set its ten-dollar price point, Bill Clinton was president, Google did not yet exist, and the average price of gasoline was about a dollar twenty. The fact that the membership price had not changed in twenty-six years was itself a remarkable feat of cost discipline and a testament to the power of the low-price identity.

The ten-dollar price point had been more than a pricing strategy; it was the brand's identity, its calling card, its one-sentence elevator pitch. "Ten bucks a month" was Planet Fitness's version of Walmart's "Everyday Low Prices"—not just a number but a promise, a psychological anchor that defined how millions of consumers understood the brand. Raising it by fifty percent—from ten to fifteen dollars—was a calculated risk that touched the very core of what made Planet Fitness different. The internal debate must have been intense: would the higher price deter the price-sensitive, first-time gym-goers who were the brand's core customer? Would it blur the line between Planet Fitness and competitors like Crunch or Blink that charged similar amounts? Would it break the magic spell of a price so low that nobody bothered to think about it?

Early data suggested the concerns were, at least for now, overblown. Same-club sales grew five percent in 2024 and accelerated to 6.7 percent in 2025, suggesting that the higher price was flowing through to revenue without meaningfully reducing traffic or sign-ups. Membership continued to climb, adding a million new members in 2024 alone. And the company announced plans to raise the Black Card price from $24.99 to $29.99 in 2026, testing whether the pricing power extended to the premium tier as well. The price increase had the effect of adding approximately five dollars per month per Classic Card member to the revenue base—which, across millions of members, represented hundreds of millions of dollars in incremental annual revenue with zero additional cost.

The GLP-1 question loomed over the entire fitness industry, and it deserves careful examination because it represents the most novel competitive threat Planet Fitness has ever faced. Drugs like Ozempic, Wegovy, and Mounjaro have demonstrated remarkable efficacy in helping patients lose significant weight—often twenty percent or more of body weight—without the diet and exercise regimen that has traditionally been the only reliable path. As these drugs moved from niche diabetes treatments to mainstream weight-loss prescriptions, analysts began asking an uncomfortable question: if people can lose weight with a weekly injection, why would they need a gym?

Planet Fitness positioned itself on the optimistic side of this debate, and the logic is not unreasonable. GLP-1 users are advised by their doctors to exercise to prevent muscle loss—a known side effect of rapid pharmaceutical weight loss. Without resistance training, patients on GLP-1 drugs risk losing not just fat but significant muscle mass, which can lead to weakness, metabolic problems, and the "skinny fat" physique that physicians increasingly warn about. Planet Fitness, with its non-intimidating environment and low price, is the natural destination for GLP-1 patients who have never exercised before and need to start. Forty percent of Planet Fitness members each year are first-time gym-goers—exactly the profile of someone beginning an exercise regimen alongside a GLP-1 prescription. By November 2025, the company's Chief Marketing Officer publicly stated that Planet Fitness was "in conversations with several GLP-1 providers" to explore marketing alignment. The bull case on GLP-1 is that it expands the funnel of potential gym members by creating a medically motivated reason to exercise for millions of people who previously had none.

The bear case is simpler: some percentage of people who might have joined a gym to lose weight will now take a pill instead. The net effect is genuinely uncertain, and investors should be wary of anyone claiming to know the answer with confidence.

International expansion accelerated under Keating's leadership, and the early results were genuinely encouraging. Spain received its first club in July 2024, and the company reported that the ramp curve—how quickly a new location reaches mature membership levels—was as good as or better than comparable openings in the U.S. and Mexico. That data point, while early, is important because it suggests that the Planet Fitness concept may have broader international appeal than skeptics assumed.

Mexico grew to 47 locations across 14 states by year-end 2025, making it the largest international market by location count. A new franchise agreement was signed in February 2026 with Impulso Gym for expansion into Tijuana and Mexicali, border cities where cultural proximity to the U.S. may give the brand a natural advantage. The company also operates in Canada, Panama, and Australia, though these markets remain small relative to the domestic system.

At the November 2025 Investor Day, management laid out long-term targets for 2026 through 2028 that painted a picture of steady, profitable growth rather than explosive expansion: low-double-digit revenue CAGR, six to seven percent annual growth in new club openings, mid-single-digit same-club sales growth, and mid-teens adjusted EBITDA growth. The company targeted 180 to 190 new club openings in 2026. These are not startup growth rates. They are the targets of a mature franchise system that is optimizing for profitability and capital returns alongside unit growth.

The stock, which had reached an all-time high of $114.47 on July 23, 2025, pulled back to approximately seventy-eight dollars by mid-March 2026—reflecting both the CFO transition and broader market uncertainty. For investors, the central question had shifted. Planet Fitness was no longer a high-growth startup story. It was a mature franchise system with strong economics and an uncertain growth trajectory. Whether the market would reward it as a growth company or value it as a cash-generating machine would depend on whether international expansion, pricing power, and continued U.S. market penetration could keep the top line growing at double digits.

X. Strategic Analysis: Porter's Five Forces and Hamilton's Seven Powers

Understanding Planet Fitness's competitive position requires looking beyond the financial statements to the structural forces that determine whether its advantages are durable or temporary.

Porter's Five Forces frame the external competitive environment. The threat of new entrants into the gym business is paradoxically both high and low. Opening a gym requires relatively modest capital—a lease, equipment, and insurance will get you started. There are no patents, no proprietary technology, no regulatory licenses. But competing with Planet Fitness at scale is a fundamentally different proposition. The national advertising budget, amortized across nearly three thousand locations, creates awareness that a local gym cannot match. The bulk equipment purchasing power drives costs below what a single-location operator could achieve. The brand recognition, built over three decades, attracts first-time gym-goers in a way that a new entrant cannot replicate overnight. Blink Fitness's failure is instructive: even with Equinox's backing, operational expertise, and design sensibility, it could not build enough scale fast enough to compete.

The bargaining power of suppliers is low. Fitness equipment is manufactured by multiple vendors—Life Fitness, Hammer Strength, Matrix, Precor—and none has sufficient market power to dictate terms to a buyer as large as Planet Fitness. Real estate is similarly fragmented, with thousands of landlords competing for tenants in the post-retail-apocalypse landscape. Labor, while tightening in the post-pandemic economy, is largely low-skill at the club level, reducing dependence on any particular talent pool.

The bargaining power of buyers—gym members—is theoretically high. Switching costs are minimal: you can cancel one gym membership and sign up at another with trivial effort. But Planet Fitness has effectively neutralized this force through pricing psychology. At ten to fifteen dollars per month, the membership is below the threshold where most consumers actively comparison shop. You do not switch gyms to save five dollars a month. And the habits, social connections, and physical familiarity that develop around a specific location create psychological switching costs even when economic ones are absent.

The threat of substitutes is the most significant force. Home fitness equipment, outdoor exercise, boutique studios, running clubs, yoga apps, and now GLP-1 drugs all compete for the same consumer intention: "I should do something about my health." The connected fitness wave of 2020-2021 demonstrated that substitution risk is real, even if that particular threat has receded. The structural defense is that Planet Fitness competes not on the quality of the fitness experience—a Peloton class is objectively better exercise than wandering around a Planet Fitness—but on the accessibility and price. For the vast majority of the population, the relevant substitute is not Peloton. It is doing nothing.

Competitive rivalry in the budget segment is intense and growing. Crunch Fitness is expanding aggressively, planning roughly one hundred new openings in 2026 alone. Anytime Fitness has a larger global footprint with over five thousand locations worldwide. LA Fitness, with the highest revenue among Planet Fitness competitors at approximately 2.1 billion dollars, occupies the mid-market but faces strategic pressure as high-value, low-price brands add amenities that blur the tier boundaries. Regional operators in specific markets can be formidable. But Planet Fitness's scale advantages—in advertising, purchasing, brand recognition, and franchisee economics—give it a structural edge that no single competitor currently threatens. The budget gym segment is not winner-take-all, but it has a clear leader, and that leader's advantages compound with every new location opened.

Hamilton Helmer's Seven Powers framework asks a deeper question: not just whether Planet Fitness has advantages today, but whether those advantages can persist over time.

Scale Economies are real and significant. The national advertising fund, supported by contributions from nearly three thousand locations, generates marketing firepower that competitors with a few hundred locations simply cannot match. Equipment purchasing leverage grows with every new location. Corporate overhead—technology, legal, brand management—is spread across an enormous system.

These economies of scale create a widening gap between Planet Fitness and smaller competitors. The bigger Planet Fitness gets, the harder it becomes for anyone else to catch up.

Network Effects are weak to nonexistent. A Planet Fitness member's experience is not improved by the addition of more members—in fact, it is degraded by crowding. There is no social network, no community platform, no user-generated content that becomes more valuable as the network grows. This is a meaningful limitation: businesses with strong network effects tend to have the most durable competitive positions.

Counter-Positioning is arguably Planet Fitness's strongest power. Premium gym chains—Equinox, Life Time, even mid-market players like LA Fitness—cannot copy the Planet Fitness model without cannibalizing their existing business.

Imagine an Equinox executive walking into a board meeting and proposing to open a stripped-down, fifteen-dollar-a-month gym with pizza, Tootsie Rolls, and a Lunk Alarm. The organizational identity, the employee base, the member expectations, and the margin structure all rebel against the idea. Every dollar of revenue at the budget tier would come at the expense of the premium brand that generates far higher margins.

Equinox tried exactly this with Blink Fitness—and Blink ended up in bankruptcy. This is the classic counter-positioning dynamic described by Hamilton Helmer: the incumbent's existing business model makes it irrational to adopt the challenger's approach, even when the challenger's approach is clearly working.

Switching Costs are moderate. The economic switching cost is near zero—you can join or quit any gym at any time. But the psychological and habitual switching costs are real. Members build routines around specific locations. They develop familiarity with the equipment layout, the staff, the parking situation. At ten to fifteen dollars per month, the cost of maintaining the membership is so low that inertia overwhelmingly favors staying rather than going through the effort of change.

Branding is strong and distinctive. The "Judgment Free Zone" is not just a tagline; it is a cultural identity that resonates with a specific, massive audience. Planet Fitness has invested decades in building this brand, and it communicates a clear promise that no competitor has successfully replicated. The purple-and-yellow color scheme, the Lunk Alarm, the pizza—these are not random. They are brand signals that, taken together, make Planet Fitness instantly recognizable and emotionally distinct from every other gym chain.

Cornered Resource takes the form of franchise territory rights. As Planet Fitness has grown, it has sold development rights to nearly every viable territory in the United States. A new competitor entering a market faces not just Planet Fitness's brand and scale but the reality that the best available real estate locations within those territories are already spoken for or under development. This territorial lock-up is a meaningful, if not absolute, barrier to entry.

Process Power is moderate. Planet Fitness has developed a highly refined franchise playbook—site selection, build-out, equipment installation, staffing, marketing—that enables consistent execution across thousands of locations. The playbook is detailed enough that a new franchisee can go from signed agreement to open doors in a predictable timeline with predictable costs. That operational consistency is valuable. But unlike a semiconductor manufacturer's fabrication process or a pharmaceutical company's R&D pipeline, this operational knowledge is fundamentally replicable by well-resourced competitors given enough time and investment. There is no secret sauce in the operations that could not be reverse-engineered.

The verdict across both frameworks is clear: Planet Fitness's primary competitive advantages are Counter-Positioning, Scale Economies, and Branding. The model works because premium competitors cannot copy it without destroying their own businesses, the cost structure improves with every new location, and the brand occupies a unique and defensible position in consumer psychology. The weaknesses—limited network effects, low economic switching costs, and replicable operational processes—are real but are offset by the extraordinary power of the pricing and positioning combination.

XI. The Investment Thesis: Bull vs. Bear

The Bull Case rests on a simple but powerful observation: even with nearly three thousand locations and twenty-one million members, Planet Fitness has barely scratched the surface of its addressable market. The math is straightforward. The United States has roughly 330 million people. Approximately seventy to seventy-five million belong to a health club of any kind. That means more than 250 million Americans—roughly three-quarters of the population—do not belong to any gym. Planet Fitness's twenty-one million members represent roughly six percent of the total population. The company's target customer—the person who has never had a gym membership or who dropped out of a more expensive gym—represents hundreds of millions of potential members. Every economic downturn, every New Year's resolution, every doctor's recommendation to "get more exercise" pushes people toward the lowest-friction option available. That option is Planet Fitness.