Palomar Holdings: The Story of a Data-Driven Insurgent in Specialty Insurance

I. Introduction and Episode Roadmap

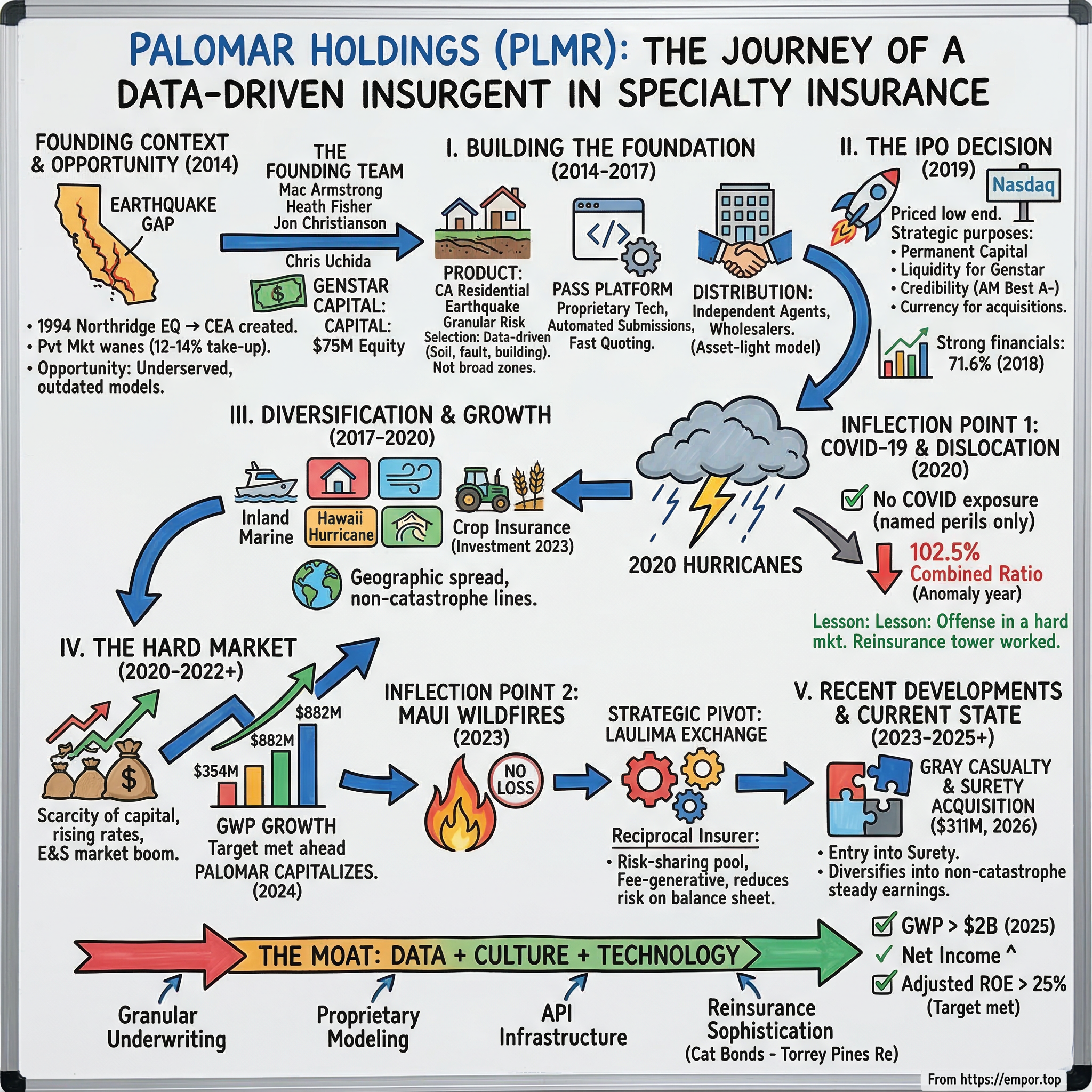

Picture a seismologist staring at a fault line map of California. The San Andreas, the Hayward, the Newport-Inglewood — hundreds of known fault lines crisscrossing the most valuable real estate in America. Now imagine that only about twelve percent of California homeowners carry earthquake insurance. That gap between catastrophic risk and actual coverage is not a market failure. It is a market opportunity. And it is exactly the gap that three insurance veterans decided to build a company around in 2014.

Palomar Holdings, trading under the ticker PLMR on the NASDAQ, is a specialty insurer that has grown from a standing start to over three billion dollars in market capitalization in barely a decade. The company writes earthquake coverage, hurricane policies, inland marine, casualty, crop insurance, and surety bonds. It operates a fronting platform that allows other capital providers to access insurance markets through Palomar's licensed, rated infrastructure. It issues catastrophe bonds through the capital markets — essentially securitizing earthquake risk into tradable instruments that diversify its reinsurance away from traditional reinsurers. And it does all of this with roughly three hundred employees out of a single office in La Jolla, California — a town better known for its surf breaks than its underwriting desks.

The question at the heart of this story is deceptively simple: how did three insurance veterans build a multi-billion dollar company in under a decade by betting on data, underwriting discipline, and market inefficiencies? The answer touches on everything from the 1994 Northridge earthquake to the rise of catastrophe bonds, from the COVID-19 pandemic to the Maui wildfires, and from the hard insurance market of the early 2020s to the January 2025 Los Angeles firestorms that caused the largest wildfire insurance losses in history.

This is a story about technology meeting insurance, about timing market dislocations with precision, and about building durable competitive advantages in what many investors dismiss as a commoditized industry. It is also a story about what happens when experienced operators — not Silicon Valley disruptors, not InsurTech evangelists — apply modern tools to an ancient business with genuine expertise and hard-won discipline.

The themes that run through every chapter of the Palomar story will be familiar to anyone who studies great businesses: founder-market fit, counter-cyclical boldness, the compounding power of disciplined underwriting, and the difference between technology as a gimmick and technology as a genuine enabler of better decision-making. Palomar did not set out to "disrupt" insurance. It set out to do insurance better than the incumbents, in the specific niches where those incumbents were either asleep or retreating. That distinction matters enormously — and it explains why Palomar is profitable and growing while a generation of InsurTech darlings burned through billions trying to reinvent a wheel that did not need reinventing.

II. Founding Context: The Specialty Insurance Opportunity (2014)

To understand why Palomar exists, rewind to 1994. On January 17 of that year, a magnitude 6.7 earthquake struck Northridge, a neighborhood in the San Fernando Valley of Los Angeles. The damage was staggering — roughly twenty billion dollars in residential losses, with only half covered by insurance. The event shattered the California insurance industry's assumptions about earthquake risk. Insurers had vastly underpriced the peril, and many of them tried to flee the market entirely.

The California legislature responded by creating the California Earthquake Authority in 1996, a not-for-profit entity designed to stabilize the market and ensure that residential earthquake coverage remained available. The CEA worked — it currently holds about sixty-two percent of the residential earthquake market in California — but its creation had an unintended consequence. It convinced private insurers that earthquake was someone else's problem. Over the following two decades, private-market earthquake coverage withered. The take-up rate — the percentage of homeowners who actually carry earthquake insurance — collapsed from about thirty-three percent when the CEA was founded to roughly twelve to fourteen percent by the mid-2010s.

This was the landscape that Mac Armstrong surveyed as he wrote a business plan during evening hours in late 2013 and early 2014. Armstrong, a Princeton graduate who grew up in La Jolla, had taken an unusual path to insurance entrepreneurship. He started in investment banking at Alex. Brown & Sons, then moved to Spectrum Equity Investors, a private equity firm in the Bay Area, where he led the insurance investing practice. That experience gave him a rare dual perspective: he understood both the financial engineering side of insurance and the operational realities of running a carrier.

In 2009, Armstrong joined Arrowhead General Insurance Agency, a managing general agency, and rose quickly from CFO to COO to President. He led the sale of Arrowhead to Brown & Brown in 2012. But by then, the itch to build something from scratch had taken hold. As he later told interviewers, "I wanted to shift my career from being an investor to being a hands-on entrepreneur." He saw a market that was underserved, mispriced, and ripe for a new entrant with better technology and tighter underwriting discipline.

Armstrong was not alone. He recruited Heath Fisher, a managing director at Guy Carpenter, one of the world's premier reinsurance brokerages. Fisher understood the reinsurance markets cold — he knew who had capacity, what it cost, and how to structure programs that would protect a young insurer from catastrophic losses.

Jon Christianson, who had worked at John B. Collins Associates servicing both casualty and property accounts and then at Holborn Corporation, another reinsurance intermediary, came aboard as the third employee. A Brown University graduate, Christianson brought deep reinsurance structuring expertise that would prove critical as Palomar built its catastrophe bond program.

Chris Uchida, who had worked alongside Armstrong at Arrowhead as chief accounting officer (and before that spent seven years at PricewaterhouseCoopers as a tax manager), joined in 2015 as CFO. The Arrowhead connection between Armstrong and Uchida was not coincidental — they had built trust working together under pressure, and Armstrong valued Uchida's combination of accounting rigor and operational pragmatism.

The founding team's thesis was precise. California earthquake insurance was severely underserved. Legacy insurers had pulled back. Underwriting models were antiquated. And the technology platforms that existing carriers used were decades old — in some cases literally running on mainframe systems from the 1980s.

There was margin to be captured by a new entrant willing to use modern data analytics, maintain rigorous underwriting standards, and focus narrowly on specialty catastrophe lines where pricing power was strong.

Genstar Capital, a San Francisco-based private equity firm, provided seventy-five million dollars of initial equity capital. That number is worth pausing on. In an era when InsurTech startups would burn through hundreds of millions before writing a single profitable policy, Armstrong and his team raised enough to capitalize a genuine insurance company — one that would need to meet state regulatory requirements, secure reinsurance, and build from a real balance sheet. Palomar was incorporated in February 2014, and the founders set to work.

Why was 2014 the right moment? Several forces converged. Post-financial-crisis capital was abundant and searching for yield in specialty markets. The technology stack required to build a modern underwriting platform — cloud computing, data analytics, API integrations — had matured to the point where a small team could build what would have required a hundred-person IT department a decade earlier. And the regulatory environment, while demanding, was navigable for experienced operators who understood the California Department of Insurance and the surplus lines market. Armstrong's team knew the playbook because they had lived it at other carriers and intermediaries. They were not learning on the job. They were applying decades of accumulated knowledge to a greenfield opportunity.

III. Building the Foundation: Strategy and Early Products (2014–2017)

The first product Palomar wrote was California residential earthquake insurance, and the choice was anything but random. Earthquake is what insurers call a "peak peril" — low frequency, high severity. A major earthquake might not happen for decades, but when it does, the losses can be catastrophic. This characteristic makes earthquake insurance uniquely challenging and uniquely profitable for carriers that price it correctly.

Think of it this way. In most lines of insurance, claims arrive in a steady drip — a car accident here, a slip-and-fall there, a kitchen fire next week. An insurer writing auto or homeowners coverage can predict with reasonable accuracy how much it will pay out each quarter. Earthquake is fundamentally different. An earthquake insurer might go years collecting premiums and paying virtually nothing in claims. Then one day the ground shakes, and the bill comes due all at once. The insurer that survives is the one that priced the risk correctly, purchased enough reinsurance to absorb the shock, and maintained enough capital to stay solvent while paying claims.

Palomar's underwriting philosophy from day one centered on what the industry calls "granular risk selection." Rather than writing earthquake policies across broad geographies using crude pricing models — the approach that had gotten legacy carriers into trouble — Armstrong's team built pricing models that evaluated risk at the individual property level. Soil type, proximity to fault lines, building construction, foundation design, occupancy — all of these factors fed into Palomar's pricing engine. The goal was to avoid the "Swiss cheese" problem: writing a book of business full of holes where the worst risks are overrepresented because they are the ones most eager to buy coverage.

This is where technology entered the picture, not as a marketing buzzword but as an operational necessity. Palomar built its underwriting platform from scratch. While legacy carriers ran on policy administration systems designed in the 1990s — or earlier — Palomar's engineers built what they called the Palomar Automated Submission System, or PASS. The system integrated quoting, underwriting, policy issuance, billing, and portfolio analytics into a single platform. It connected directly to the retail agents and wholesale brokers who distributed Palomar's products, enabling rapid automated quoting and binding.

The distribution strategy itself reflected deep industry knowledge. Rather than trying to sell directly to consumers — the approach that would prove so expensive and unprofitable for InsurTech startups — Palomar worked through independent agents and managing general agents. These intermediaries already had relationships with the property owners and commercial clients who needed earthquake coverage. Palomar provided the product, the pricing, and the paper. The agents provided the distribution. It was an asset-light model that kept Palomar's expense ratio low while leveraging existing infrastructure.

To understand why this mattered, consider the economics. A direct-to-consumer insurer might spend thirty to forty cents of every premium dollar on marketing, customer acquisition, and servicing. An insurer working through independent agents pays a commission — typically fifteen to twenty percent of premium — but avoids the massive overhead of brand advertising, call centers, and consumer-facing technology. For a young company with limited capital, the agency model was not just strategically sound — it was the only model that allowed profitable growth from year one.

The early years were a grind. Palomar wrote just $16.6 million of gross written premiums in its first year of operations. Building credibility as a startup insurer is not easy — agents need to trust that a carrier will pay claims, reinsurers need to trust that a carrier will price risk correctly, and regulators need to trust that a carrier is adequately capitalized. Armstrong's team spent countless hours in meetings with reinsurance brokers, attending industry conferences, and demonstrating their underwriting models to skeptical counterparties.

The capital structure helped. Genstar's seventy-five million dollars gave Palomar a real balance sheet, and the private equity backing provided credibility that a purely bootstrapped startup would have struggled to establish. But the true differentiator was the team's track record. Armstrong, Fisher, Christianson, and Uchida had collectively spent decades in the industry. They were not asking the market to take a chance on an unproven concept. They were asking the market to back experienced operators with a better mousetrap.

By 2016, Palomar had achieved profitability. By 2018, gross written premiums had grown to $154.9 million — nearly a tenfold increase from the first year. The combined ratio, the single most important metric in insurance (we will return to this concept repeatedly), was a stellar 71.6 percent. For context, a combined ratio below one hundred means the insurer is making money on its underwriting alone, before investment income. The industry average for property and casualty insurers hovers around ninety-seven percent. Palomar was not just profitable — it was printing money on its underwriting book, and doing so while growing at extraordinary rates.

The disciplined growth mantra was not just rhetoric. Armstrong and his team made deliberate choices about which risks to write and which to decline. They walked away from business where the pricing did not meet their return thresholds, even when it meant slower top-line growth. In an industry where the temptation to chase premium volume is perpetual, this discipline would prove to be Palomar's most durable competitive advantage — though the full evidence of that would not become apparent until catastrophe struck and the company's reinsurance program was tested under fire.

IV. The IPO Decision: Going Public at Scale (2019)

On the morning of April 17, 2019, Palomar Holdings began trading on the NASDAQ Global Select Market under the ticker PLMR. The IPO priced at fifteen dollars per share — the low end of the fifteen-to-seventeen dollar range the underwriters had marketed — and raised approximately eighty-four million dollars. Barclays, J.P. Morgan, and Keefe Bruyette & Woods served as joint book-running managers.

The pricing at the bottom of the range told a story of cautious institutional interest. Public market investors were not sure what to make of Palomar. On one hand, the company had an impressive track record — four years of operation, rapid premium growth, elite combined ratios, and a focused strategy in an underserved market. On the other hand, earthquake insurance carried a perceived binary risk that made generalist investors uncomfortable. The S-1 filing listed "catastrophic events" as the first risk factor — hardly reassuring for generalist portfolio managers accustomed to companies with more predictable earnings streams. What if the Big One hits? Would Palomar survive?

The market provided its own answer on day one. Shares closed at $18.99, up nearly twenty-seven percent from the offering price, reaching a high of $19.96 on volume of 3.3 million shares. The investors who did their homework recognized what the skeptics missed: Palomar's reinsurance program was designed precisely to handle catastrophic losses. The company did not retain earthquake risk on its own balance sheet in massive concentrations. It transferred the peak risk to reinsurers and, increasingly, to the capital markets through catastrophe bonds.

Going public was a calculated decision, not a desperate one. Palomar was already profitable and growing rapidly. The IPO served three strategic purposes.

First, it provided access to permanent capital — equity that does not need to be returned to private equity investors on a fixed timeline. In insurance, where policyholder obligations can stretch for years, permanent capital is a structural advantage. Private equity funds typically have seven-to-ten-year investment horizons, which creates pressure to exit just when the business may be entering its most productive phase.

Second, the IPO provided liquidity for Genstar Capital, which had been Palomar's primary backer since founding. Genstar would fully exit its remaining stake through secondary offerings by June 2020.

Third, and perhaps most importantly, the public listing gave Palomar a currency for acquisitions and enhanced its credibility with agents, reinsurers, and rating agencies.

That credibility point deserves emphasis. Insurance is a relationship-driven industry. Agents recommend carriers based on financial strength, claims-paying reputation, and long-term stability. An AM Best rating — the industry's gold standard for financial strength — matters enormously. A NASDAQ listing, audited financials, and the discipline of quarterly earnings reporting all contributed to Palomar's institutional credibility in ways that private ownership could not.

The challenge of quarterly earnings in a catastrophe-exposed business would become apparent soon enough. Public market investors demand predictable earnings, and earthquake insurance is inherently unpredictable. A single catastrophic event can swing a quarter from record profits to significant losses. Armstrong and his team would need to educate investors about the nature of catastrophe insurance economics — that lumpy earnings are a feature, not a bug, of a well-managed catastrophe book, and that the real measure of value creation is the long-term combined ratio and return on equity, not any single quarter's results.

The board that Palomar assembled around the IPO reflected the seriousness of the enterprise. Richard Taketa, CEO of York Risk Services Group and a Stanford Law graduate, joined as lead independent director. Catriona Fallon, a Harvard MBA and former Olympic rower for the United States who had served as CFO at multiple technology companies, brought financial rigor and governance experience. Daryl Bradley, an executive vice president at Everest Reinsurance for over two decades, contributed deep reinsurance expertise. These were not advisory-board-for-equity-type appointments. They were seasoned executives with genuine operational insight in the industries that mattered most to Palomar.

With the IPO behind them, Armstrong had the capital and the platform to accelerate Palomar's next chapter: expanding beyond earthquake into a diversified specialty insurance franchise.

V. Product Expansion and Geographic Diversification (2017–2020)

Even before the IPO, the seeds of diversification were being planted. Palomar's leadership understood a fundamental truth about catastrophe insurance: concentration kills. A company that writes only California earthquake insurance is making a single, massive bet on one peril in one geography. No matter how good the underwriting, the tail risk of a catastrophic earthquake along the San Andreas Fault is existential if the company has not diversified its exposure.

The expansion strategy was deliberate and sequenced. Palomar moved into inland marine and commercial property, two lines that share some of the analytical complexity of earthquake insurance but carry different risk profiles. Inland marine — which, despite its nautical name, covers a wide range of property-in-transit, specialized equipment, and items that do not fit neatly into standard property categories (think construction equipment on a job site, fine art in transit, or telecommunications towers) — rewards the same kind of granular underwriting that Palomar had honed in earthquake. Each risk is unique, requiring individual evaluation rather than the cookie-cutter approach used in personal lines. Commercial property brought exposure to fire, wind, and other perils, but also diversified away from the pure seismic concentration.

Hawaii became a critical market. Palomar had entered the Hawaiian market as early as 2015, writing hurricane coverage for residential and commercial properties. Hawaii presents a fascinating insurance puzzle. Standard homeowners insurance on the islands does not cover hurricane damage, earthquake damage, flood, or volcanic activity. Each of those perils requires a separate, specialized policy. Between three hundred seventy-five and three hundred ninety condominium buildings in Hawaii were underinsured for hurricane risk, and premium increases of up to one thousand percent had been reported for some condo associations. Palomar saw an underserved market with enormous demand and limited competition — the same dynamics that had drawn them to California earthquake.

The fronting business, launched in September 2021 as PLMR-FRONT, represented a strategic evolution. Fronting is worth explaining because it is one of the insurance industry's most misunderstood business models. Think of it this way: many organizations want to underwrite insurance risk — hedge funds, reinsurers, specialized managing general agents — but they do not have insurance licenses or AM Best ratings. A fronting carrier like Palomar provides the "paper" — the licensed, rated entity that actually issues the insurance policy — while the risk is transferred to the capital provider behind it. Palomar earns a fee, typically five to eight percent of gross premiums, for providing its balance sheet, regulatory compliance, and policy administration capabilities. The beauty of fronting is that it generates fee income with minimal catastrophe risk on Palomar's own balance sheet. It is essentially an asset-light, fee-generative complement to the risk-bearing underwriting business.

The crop insurance entry came in 2023 through a strategic investment in Advanced AgProtection, a Texas-based specialized crop managing general agent. Palomar simultaneously became the fourteenth approved insurance provider by the Federal Crop Insurance Corporation. Crop insurance is federally subsidized, actuarially predictable, and generates steady premium flows — characteristics that make it an excellent diversifier for a catastrophe-exposed portfolio. Following two years of successful collaboration, Palomar moved to acquire AAP outright, with the transaction expected to close during the second quarter of 2025.

Through all of this expansion, the reinsurance strategy evolved in sophistication. Palomar's Torrey Pines Re catastrophe bond program — named, fittingly, after the iconic cliffs near the company's La Jolla headquarters — became one of the most active cat bond programs among specialty insurers. The first issuance in 2017 placed $166 million of multi-peril coverage. By 2025, the program had grown to include a $525 million issuance covering California earthquake risk alone, with approximately $1.15 billion — about thirty-three percent — of Palomar's $3.53 billion earthquake reinsurance tower sourced from the capital markets.

Think of a reinsurance tower as a layer cake of protection. At the bottom sits Palomar's retention — the amount of loss the company absorbs before any reinsurance kicks in. Above that sit successive layers of reinsurance, each covering a range of losses. If an earthquake causes losses that exceed Palomar's retention, the first reinsurance layer pays. If losses exceed that layer, the next one kicks in, and so on up the tower. The cat bonds sit within this structure, providing coverage at specified attachment points. The entire tower is designed so that even in a worst-case scenario — a major earthquake along a primary California fault — Palomar's own balance sheet absorbs only a manageable portion of the total loss.

Each product expansion brought new hiring needs. Palomar recruited specialized underwriters for each vertical — professionals with deep expertise in marine, casualty, crop, and surety lines. The company remained remarkably lean, operating with roughly two hundred seventy employees as of early 2025, but each hire was selected for domain expertise rather than general insurance background. This specialist model kept the expense ratio low while maintaining underwriting quality across an increasingly diverse product portfolio.

The speed-to-market advantage that technology enabled was tangible. When Palomar identified an opportunity in a new geography or product line, it could build the underwriting model, configure the platform, test pricing assumptions, and begin writing policies within months — not the years that a legacy carrier might require to navigate internal approval processes, upgrade mainframe systems, and train staff. This operational velocity allowed Palomar to be opportunistic: when a competitor exited a market or when pricing improved in a specific line, Palomar could move into the vacuum before slower-footed rivals recognized the opportunity.

VI. Key Inflection Point: COVID-19 and Market Dislocation (2020)

When COVID-19 shut down the global economy in March 2020, the insurance industry faced its most chaotic period in decades. Businesses across every sector filed claims for lost revenue, and the question of whether commercial property policies covered losses from a pandemic became one of the most litigated issues in insurance history. Business interruption claims flooded carriers that had written commercial property policies with ambiguous pandemic exclusions. Billions of dollars hung in the balance as courts across the country rendered conflicting decisions.

Palomar watched this chaos from a position of remarkable calm. The company's product mix — earthquake, hurricane, inland marine, specialty property — carried virtually no exposure to pandemic-related business interruption losses. While competitors scrambled to estimate their COVID-19 claims liability and bolster reserves, Palomar's loss experience was largely unaffected. This was not luck. It was the consequence of deliberate product design. By focusing on named perils — earthquake, wind, flood — rather than broad "all-risk" commercial property coverage, Palomar had constructed a portfolio that was naturally immune to pandemic-driven claims.

The pandemic also accelerated a broader market dislocation that would prove enormously beneficial to Palomar. Competitors across the specialty insurance landscape began retreating from catastrophe-exposed lines. Carriers that had suffered COVID-related losses tightened their appetites. Rating agencies put several insurers on negative watch. Reinsurers, already stung by years of elevated catastrophe losses, raised prices and reduced capacity.

For a well-capitalized, disciplined underwriter with room to grow, this was the equivalent of a department store going-out-of-business sale. Palomar accelerated growth in select lines where pricing had improved and competitors had pulled back. The company maintained its underwriting standards — it did not chase unprofitable business simply because it was available — but it leaned into opportunities where the risk-reward equation had shifted in its favor.

The financial results for 2020 told a more nuanced story, however. Palomar reported a combined ratio of 102.5 percent for the full year — the only year in its history where the combined ratio exceeded one hundred. The culprit was not COVID. It was hurricanes. Storms Laura, Hanna, Isaias, and Sally hit during the hyperactive 2020 Atlantic hurricane season, generating pre-tax catastrophe losses of roughly thirty-four to thirty-eight million dollars for Palomar. This was a painful reminder that diversification into hurricane-exposed markets carried its own risks.

Net income dropped to just $6.3 million, down from $10.6 million the prior year (though 2019 had been depressed by IPO-related expenses). The stock experienced significant volatility. But investors who looked past the headline numbers recognized that the underlying business was sound. The hurricane losses were within the company's catastrophe budget, the reinsurance program functioned as designed, and the premium base was growing rapidly. By the end of 2020, gross written premiums had reached $354.4 million — up more than forty percent from the prior year. For perspective, Palomar's full-year 2020 net income of $6.3 million on a book that was rapidly approaching $400 million in gross premiums was disappointing but not catastrophic. The adjusted combined ratio of 100.4 percent meant the company essentially broke even on underwriting — losing the margin it normally earned, but not bleeding capital. Compare that to competitors who faced existential questions about solvency after COVID-related business interruption claims.

The real lesson from 2020 was about the value of a fortress balance sheet in a crisis. Companies with strong capital positions can play offense when weaker competitors are playing defense. Armstrong captured this philosophy in his approach to adversity: "For us, our greatest lessons have come from when there have been catastrophes, and the importance not just of having good products but excellent, responsive service." The 2020 hurricane losses were not a failure — they were tuition. They informed Palomar's subsequent decisions about how much non-earthquake catastrophe risk to retain, how to structure reinsurance for multi-peril exposure, and ultimately led to the Laulima Exchange restructuring of the Hawaii book.

Palomar emerged from the pandemic year with its franchise intact, its growth accelerating, and the hard insurance market that was taking shape across the industry providing a powerful tailwind for the years ahead.

VII. Key Inflection Point: The Hard Market and Pricing Power (2020–2022)

Insurance operates in cycles, and understanding these cycles is essential to understanding Palomar's trajectory. The concept is straightforward even if the dynamics are complex. In a "soft market," there is too much capital chasing too little premium. Insurers compete aggressively, cutting prices, broadening coverage terms, and accepting risks they might otherwise decline. Underwriting profitability deteriorates because premiums are inadequate to cover losses. Eventually, losses mount, capital is depleted, and the market "hardens."

In a "hard market," the dynamics reverse. Capital is scarce. Insurers raise prices, tighten coverage terms, and become more selective about which risks they accept. Underwriting profitability improves — sometimes dramatically — because premiums now exceed losses by a comfortable margin. The hard market persists until the attractive profitability draws new capital into the industry, competition intensifies, and the cycle starts over. The typical cycle lasts five to ten years, though each cycle has its own character. The hard market that began in late 2018 has proven distinctive — less steep in its pricing increases than some prior hard markets, but more protracted. As of early 2026, it has lasted over seven years, making it one of the longest hard markets on record in certain specialty lines.

The property and casualty insurance industry entered a hard market beginning in late 2018, and the hardening accelerated through 2020, 2021, and into 2022. Multiple forces drove the transition. Years of underpricing had left reserves inadequate across the industry. Climate change was increasing the severity and frequency of natural catastrophes — global insured losses exceeded one hundred billion dollars for six consecutive years starting in 2020. Social inflation — the trend of rising jury verdicts and litigation costs — was driving up casualty losses. And the reinsurance market was hardening aggressively, with reinsurers repricing risk, elevating attachment points, and in some cases simply withdrawing capacity.

The Excess and Surplus lines market — the segment where Palomar operates much of its business — experienced explosive growth. E&S premiums surpassed $104 billion in 2023 and grew to $135 billion by 2024, with seven consecutive years of double-digit growth. E&S market share of total property and casualty premiums expanded from about five percent in 2018 to over twelve percent by 2024. Business was flooding into the E&S market as the admitted market (standard insurance carriers) retreated from complex and catastrophe-exposed risks.

Palomar capitalized on this environment with precision. Gross written premiums grew from $354 million in 2020 to $535 million in 2021 (up fifty-one percent) and then to $882 million in 2022 (up sixty-five percent). These are extraordinary growth rates for an insurance company, and they were achieved while the combined ratio was improving — from the loss-year anomaly of 2020 to eighty percent in 2021 and 80.4 percent in 2022. The company was writing significantly more business and doing it more profitably.

The hard market also provided an opening for Palomar to expand into new product lines where pricing had improved. Casualty insurance, which had been soft for years, was finally seeing meaningful rate increases. The fronting business, launched in 2021, attracted managing general agents that were seeking AM Best-rated paper in a market where capacity was shrinking. Each new line of business added premium volume, diversified the risk profile, and spread fixed costs over a larger base.

Meanwhile, the Federal Reserve's aggressive interest rate increases beginning in March 2022 created a second tailwind. Insurance companies invest their premium float — the money they collect from policyholders before paying claims — in bonds and other fixed-income securities. When interest rates rise, the yield on new investments increases, boosting investment income. Palomar's net investment income grew from $9.1 million in 2021 to $13.9 million in 2022 and then to $23.7 million in 2023, eventually reaching $56 million in 2025. This was essentially free incremental income driven by macroeconomic conditions rather than any additional risk-taking.

The compounding effect of writing profitable business at scale, in a rising-rate environment, with improving pricing across specialty lines, transformed Palomar's financial profile. The company introduced its "Palomar 2X" strategic plan in 2022, targeting a doubling of adjusted underwriting income over three to five years while maintaining adjusted return on equity above twenty percent. The plan was anchored by the earthquake franchise, supported by non-attritional-loss businesses, with limited exposure to non-earthquake property catastrophe. It called for entry into new markets via replicable, analytics-driven processes — essentially a formula for disciplined diversification.

Palomar achieved the 2X goal in just three years — by 2024 — ahead of schedule. Adjusted underwriting income more than doubled from 2021 levels, validating the thesis that Palomar could grow rapidly without sacrificing profitability. The hard market was a tailwind, but execution mattered: many specialty carriers had access to the same favorable pricing conditions, and not all of them produced comparable results. The difference was in the quality of risk selection and the discipline of the underwriting process.

VIII. The Maui Wildfire Test: When Catastrophe Strikes (August 2023)

On August 8, 2023, wind-driven wildfires engulfed Lahaina, a historic town on the west coast of Maui. The fires killed over a hundred people and destroyed more than two thousand structures, making it the deadliest wildfire in the United States in over a century. Insured losses were estimated at $5.6 billion.

For investors tracking Palomar, the immediate question was obvious: how exposed was the company? Palomar had been writing insurance in Hawaii since 2015 and had built a significant presence in the state's catastrophe insurance market, with approximately forty million dollars of direct written premium in Hawaii as of 2022. The stock market braced for impact.

The answer, when it came, was surprising: zero. Palomar incurred no losses from the Lahaina wildfires.

The reason was specific and instructive. Palomar's Hawaiian product line was focused on hurricane coverage — wind damage from tropical cyclones. Wildfires, while devastating, are a different peril entirely. The policies Palomar had written in Hawaii simply did not cover wildfire losses. This was not some clever retroactive rationalization. It was the straightforward consequence of writing named-peril policies rather than broad all-risk coverage. Once again, deliberate product design protected the company from a catastrophe that devastated competitors.

But the Maui disaster prompted a deeper strategic rethinking of Palomar's Hawaii exposure. Even though the wildfires did not trigger claims, they highlighted the concentration risk of having a significant presence in a geographically isolated, catastrophe-prone market. Hurricane season in Hawaii runs from June through November, and a direct hit from a major hurricane could generate losses far larger than the Lahaina fires.

Armstrong and his team responded with one of their most creative structural moves. They formed Laulima Exchange, a fully licensed Hawaii-domiciled reciprocal insurer. A reciprocal insurer is essentially a risk-sharing pool where policyholders insure each other, managed by an attorney-in-fact. Palomar serves as that attorney-in-fact through a subsidiary called Palomar Underwriters Exchange Organization, or PUEO (the Hawaiian word for the endemic short-eared owl). The structure transitioned Palomar's Hawaiian hurricane business from risk-bearing — where catastrophic losses would hit Palomar's own balance sheet — to fee-generative, where Palomar earns management fees while the risk is borne by the reciprocal exchange and its own reinsurance program.

Laulima secured an excess-of-loss reinsurance program providing coverage up to $735 million with a $1.5 million retention. The structure meant that Palomar could continue serving its Hawaiian clients and agents, maintain its market position, and earn fee income — all without retaining significant hurricane risk on its own balance sheet. It was an elegant solution to a real strategic vulnerability, and it demonstrated the kind of financial engineering sophistication that separates Palomar from simpler specialty carriers.

The stock market's reaction to the Maui event was telling. Because Palomar had no direct losses, the stock was not materially impacted. But the episode served as a stress test of the company's risk management philosophy. Investors who had worried about Palomar's catastrophe exposure saw the reinsurance program and product design function exactly as intended. The Laulima Exchange formation showed management's willingness to proactively address concentration risks before they became balance-sheet problems.

IX. Recent Developments and Current State (2023–2025)

The period from 2023 through 2025 represented Palomar's emergence as a genuine mid-cap specialty insurance franchise. The numbers tell a remarkable story of acceleration. Gross written premiums grew from $1.14 billion in 2023 to $1.54 billion in 2024 and then to $2.03 billion in 2025 — crossing the two-billion-dollar threshold for the first time. Net income climbed from $79 million to $118 million to $197 million over the same period. Adjusted return on equity improved from 21.9 percent to 22.2 percent to 25.9 percent.

These are not the numbers of a company simply riding market conditions. The combined ratio — that crucial measure of underwriting profitability — improved from 76.6 percent in 2023 to 76.9 percent in 2025 (with 2024 at 78.1 percent). To appreciate what these numbers mean, consider that the overall property and casualty industry averages a combined ratio of about ninety-seven percent. Palomar was generating roughly twenty-three cents of underwriting profit for every dollar of premium, compared to the industry's three cents. That spread is the difference between a good insurance company and an excellent one.

The product diversification strategy bore fruit across multiple verticals. The earthquake franchise remained the foundation, with Palomar now operating the largest earthquake reinsurance tower among specialty carriers at $3.53 billion. But earthquake was increasingly complemented by inland marine, fronting fees, crop insurance, and the emerging casualty business.

On the competitive landscape, Palomar watched the InsurTech boom and bust with the detachment of a veteran boxer observing a bar fight. Lemonade, Root, and Hippo — the poster children of the InsurTech wave — had collectively burned through billions in venture capital trying to reinvent personal lines insurance with chatbots, AI, and slick mobile apps. By 2024-2025, the results were sobering. Lemonade was still reporting significant losses despite reaching $526 million in revenue. Root had finally achieved its first profitable year in 2024 with $31 million of net income — after years of cumulative losses exceeding a billion dollars. Hippo reported $58 million of net income in 2025, but that was boosted by a one-time gain from selling its homebuilder distribution network.

What did Palomar do differently? The answer is disarmingly simple: profitability first, technology as enabler rather than gimmick, and domain expertise over disruption narrative. Palomar's founders came from the insurance industry. They understood loss ratios, reserve adequacy, reinsurance structures, and agency relationships. They used technology to do underwriting better — faster quotes, more granular risk selection, lower expense ratios — but they never confused technology with the business itself. The business was always insurance, and the measure of success was always the combined ratio.

AM Best upgraded Palomar's financial strength rating to "A (Excellent)" in July 2024 and revised the outlook to Positive in September 2025 — positioning the company for a potential further upgrade. This trajectory from the initial A-minus rating at founding to A with Positive outlook represented a remarkable ascent in the eyes of the industry's most important arbiter of insurance company quality.

The most significant strategic moves of recent years came in the casualty and surety space — signaling Palomar's evolution from a pure catastrophe specialist to a diversified specialty platform.

In September 2024, Palomar hired David Sapia as Executive Vice President to lead a new E&S casualty division. On January 1, 2025, the company completed the acquisition of First Indemnity of America Insurance Company, providing initial entry into the surety market with a team of industry veterans who had delivered loss ratios outperforming the broader surety market. Then, on January 31, 2026, Palomar closed the acquisition of The Gray Casualty & Surety Company for approximately $311 million in cash — by far its largest acquisition to date and a clear statement of strategic intent.

Gray Surety was a Treasury-listed, Top 50 surety carrier specializing in contract bonds for midsized and emerging contractors, licensed in all fifty states with thirteen regional offices. Founded in 1996 as a subsidiary of The Gray Insurance Company in Louisiana, Gray had built a thirty-year track record in surety — a line that involves guaranteeing that contractors will complete construction projects as agreed. Surety bonds are fundamentally different from catastrophe insurance: losses are driven by contractor defaults rather than natural disasters, claims frequency is low and predictable, and the business generates steady, non-volatile earnings. The acquisition was financed through a $450 million unsecured credit facility consisting of a $150 million revolver and a $300 million term loan maturing in 2031.

This represented a major strategic bet that Palomar could apply its underwriting discipline and technology platform to a line of business with completely different risk characteristics — one that generates steady, non-catastrophe-exposed earnings and diversifies the company's risk profile away from natural disaster perils. If successful, the Gray acquisition could transform Palomar from a catastrophe-focused specialty insurer into a broader specialty platform with multiple earnings engines.

The January 2025 Los Angeles wildfires — the Palisades and Eaton fires that destroyed over sixteen thousand structures and generated estimated insured losses of twenty-five to forty-five billion dollars — tested the broader California insurance market but did not significantly impact Palomar. Once again, the company's focus on earthquake rather than fire-exposed homeowners coverage insulated it from the catastrophe that devastated the California FAIR Plan and forced a one-billion-dollar assessment on California insurance companies. The wildfire crisis did, however, accelerate the flight of business from the admitted market into the E&S market where Palomar operates — expanding the addressable market for specialty carriers.

Looking ahead, Palomar guided for 2026 adjusted net income of $260 million to $275 million, implying roughly twenty-four percent growth at the midpoint. The catastrophe loss budget was set at $8 million to $12 million. The company committed to maintaining adjusted return on equity above twenty percent. With the stock trading around $123 per share and a market capitalization of approximately $3.3 billion as of early March 2026, the market assigns a price-to-earnings ratio of roughly seventeen — a reflection of both the quality of the franchise and the inherent uncertainty of catastrophe-exposed earnings.

X. The Technology and Data Moat

Strip away the marketing language and ask the hard question: is Palomar's technology genuinely differentiated, or is it table stakes dressed up as a moat?

The honest answer lies somewhere in between. Palomar's technology platform — built from scratch beginning in 2014 — provides real operational advantages over legacy carriers running on systems designed in the 1990s. The Palomar Automated Submission System processes policy submissions from agents and brokers, runs them through underwriting algorithms, and returns quotes in a fraction of the time that traditional carriers require. When an independent agent has a client who needs earthquake coverage and wants a quote by end of day, the carrier that can respond in minutes rather than days wins the business. Speed-to-quote is a genuine competitive advantage in specialty insurance distribution.

The proprietary catastrophe modeling is more nuanced. Palomar uses both third-party catastrophe models — from vendors like RMS and AIR Worldwide — and proprietary analytics that overlay additional data on top of those models. The third-party models provide the foundation: they simulate thousands of potential earthquake scenarios and estimate the losses from each. Palomar's proprietary layer adds granularity — individual property characteristics, soil conditions, construction details, local building code compliance — that the broad third-party models may not capture at sufficient resolution. Think of it as the difference between Google Maps and a hand-drawn map of your own neighborhood. Both are useful, but the hand-drawn map captures details that the satellite view misses.

The API infrastructure deserves attention because it addresses a real distribution bottleneck. Palomar's software developers build application programming interfaces that integrate Palomar's underwriting platform directly into the point-of-sale systems used by agents and partner carriers. When an agent is sitting across the desk from a commercial property owner who needs earthquake coverage, the agent can generate a Palomar quote from within the same system they use for everything else. This reduces friction, increases submission volume, and makes it easy for agents to include Palomar in their quoting process.

But here is the reality check. Palomar is not the only specialty insurer investing in technology. Kinsale Capital, widely regarded as the gold standard among E&S insurers, has built its own proprietary technology platform that contributes to industry-leading combined ratios in the mid-seventies. Large incumbents like Chubb, AIG, and Travelers have the resources to invest hundreds of millions in technology modernization. The specific advantage Palomar holds today — a modern platform purpose-built for specialty catastrophe underwriting — is real but not permanent. The question is whether the institutional knowledge, underwriting culture, and data accumulated on that platform create switching costs and learning-curve advantages that outlast any individual technology edge.

The most defensible element of Palomar's technology moat may not be the technology itself but the underwriting culture it enables. When every submission is evaluated through a consistent analytical framework, when pricing decisions are driven by data rather than gut instinct, and when the platform captures and learns from every policy written and every claim filed, the result is a compounding institutional knowledge base. New underwriters hired into Palomar inherit not just a technology platform but a decision-making framework built on a decade of proprietary data. That combination of technology and culture is harder to replicate than either element alone.

XI. Business Model Deep Dive

An insurance company makes money in two ways, and understanding both is essential to evaluating Palomar.

The first is underwriting profit. When an insurer collects more in premiums than it pays out in claims and operating expenses, the difference is underwriting profit. The combined ratio measures this: it is the sum of the loss ratio (claims divided by premiums) and the expense ratio (operating costs divided by premiums). A combined ratio below one hundred means the company is making money on underwriting. Palomar's 2025 combined ratio of 76.9 percent means that for every dollar of premium collected, the company spent about seventy-seven cents on claims and expenses, keeping twenty-three cents as underwriting profit.

The second is investment income. Insurance companies collect premiums up front and pay claims later — sometimes much later, in the case of long-tail liability lines. The money sitting between premium collection and claims payment is called "float." The insurer invests this float in bonds, stocks, and other securities, earning a return. Warren Buffett famously built Berkshire Hathaway on the insight that if you can generate float at low cost — meaning your underwriting is at least breakeven — the investment income on that float is essentially free money. Palomar's net investment income reached $56 million in 2025, up from just $3.2 million in 2018.

Palomar's product mix strategy is designed to balance two competing objectives. On one side, the company wants exposure to catastrophe-prone lines like earthquake and hurricane, where pricing power is strongest and barriers to entry are highest. On the other side, it wants non-catastrophe lines — fronting fees, crop insurance, surety bonds, inland marine — that generate steady earnings regardless of whether the earth shakes or the wind blows. The Gray Surety acquisition significantly increased the weight of non-catastrophe business in the portfolio.

The reinsurance strategy is central to the business model and worth dwelling on because it defines how much risk Palomar actually retains. Palomar cedes — or transfers — a significant portion of its premium to reinsurers. The ceding ratio (the percentage of gross premiums passed to reinsurers) is a key determinant of how much net premium Palomar retains and how much catastrophe exposure sits on its own balance sheet. The company's reinsurance program is structured so that even in a severe earthquake scenario, Palomar's net losses are bounded and manageable.

The fronting model adds an asset-light fee stream. When Palomar serves as a fronting carrier, it issues policies on behalf of managing general agents or capital providers and then cedes substantially all of the risk to those partners. Palomar earns a fronting fee — typically five to eight percent of gross written premium — for providing its AM Best-rated balance sheet, licenses, and regulatory compliance infrastructure. This is high-return-on-equity business because it requires minimal capital commitment. The U.S. fronting market grew from roughly four billion dollars in premiums in 2018 to over twelve billion dollars by the mid-2020s, driven by the proliferation of managing general agents and the desire of alternative capital providers to access insurance markets without building their own licensed carriers. Palomar entered this market at an opportune moment and brought the advantage of its established technology platform and operational infrastructure.

The distribution model relies on managing general agents, wholesale brokers, and retail agents rather than direct-to-consumer sales. This keeps Palomar's acquisition costs lower than companies that spend heavily on consumer marketing, and it leverages existing distribution relationships rather than requiring Palomar to build its own sales force. The trade-off is that Palomar depends on intermediaries for customer access — if an agent stops recommending Palomar, that business walks out the door. But in specialty lines where coverage is complex and requires professional guidance, the agency model is the industry standard for good reason.

What makes specialty insurance fundamentally different from personal lines is pricing power. When a homeowner shops for auto insurance, they compare quotes from Geico, Progressive, State Farm, and a dozen other carriers. The product is essentially identical — mandated coverage, standardized terms — and the only differentiator is price. Specialty insurance is not like that. A commercial property owner who needs earthquake coverage for a high-rise building in downtown San Francisco has a limited number of carriers willing to write that risk. The coverage terms, deductible structures, and pricing vary significantly between carriers. The underwriter who can evaluate and price the risk most accurately has a genuine advantage — not just in winning the business, but in generating profitable returns on the business it writes.

XII. Competitive Landscape and Strategic Analysis

Palomar operates in a competitive arena populated by several formidable specialty insurers, each with distinct strengths and vulnerabilities. Understanding where Palomar fits requires benchmarking against the most relevant peers.

Kinsale Capital stands as the industry benchmark for E&S specialty underwriting. With a market capitalization approaching ten billion dollars and combined ratios consistently in the mid-seventies — reaching 71.7 percent in the fourth quarter of 2025 — Kinsale has demonstrated that disciplined E&S underwriting at scale generates extraordinary returns. The comparison with Palomar is instructive: both companies emphasize technology-driven underwriting, both maintain elite combined ratios, and both trade at premium valuations reflecting superior profitability. The key difference is breadth — Kinsale operates across a wide range of E&S lines focused on small and medium commercial accounts, while Palomar concentrates in catastrophe-exposed specialty lines.

RLI Corp provides a different benchmark — the long-track-record, diversified specialty model. RLI has achieved an extraordinary thirty consecutive years of underwriting profitability, and AM Best upgraded its financial strength rating to the coveted "A++ (Superior)" in February 2026. RLI's combined ratio was 83.6 percent for 2025. Palomar grows faster and produces lower combined ratios, but RLI's three-decade streak of underwriting profitability represents the gold standard of consistency that Palomar aspires to match over time.

James River Group serves as a cautionary tale. The company reported a net loss of $92.7 million in 2024, discovered accounting errors in its reinstatement premium recognition, identified material weaknesses in internal controls, and saw its stock decline approximately sixty percent in a single year. The contrast with Palomar could not be starker. James River illustrates what happens when underwriting discipline breaks down and internal controls fail — even in the same specialty insurance market where Palomar thrives.

Heritage Insurance Holdings, a catastrophe-exposed homeowners insurer concentrated in Florida, highlights the risks of geographic concentration in hurricane-prone markets. Heritage absorbed roughly $88 million in catastrophe losses from Hurricanes Debbie, Helene, and Milton in 2024 alone. Palomar's own 2020 hurricane losses — its worst year — taught a similar lesson, and the subsequent diversification into non-catastrophe lines and the Laulima Exchange restructuring were direct responses to that vulnerability.

The InsurTech comparison is perhaps the most illuminating for understanding Palomar's strategic positioning. Lemonade, Root, and Hippo entered insurance with the premise that technology could fundamentally transform the industry. They were right about the premise but wrong about the execution. All three prioritized growth over profitability, spent lavishly on customer acquisition, and entered commoditized personal lines markets — renters insurance, auto insurance, homeowners insurance — where margins are thin and competition from well-capitalized incumbents is fierce. Palomar, by contrast, entered complex specialty lines where pricing power is strong, barriers to entry are high, and incumbents were retreating rather than competing aggressively.

The difference in outcomes is stark. Palomar achieved profitability within two years of founding. Lemonade, after nine years of operation, still reports significant net losses. Root finally turned profitable in 2024 after cumulative losses exceeding a billion dollars. The lesson is not that technology in insurance is useless — it is that technology without underwriting expertise, risk management discipline, and market focus is worse than useless. It is a way to lose money faster.

There is an important myth-versus-reality distinction to make here. The consensus narrative in financial media often positions Palomar as an "InsurTech" company — a technology-first disruptor. The reality is more nuanced and more interesting. Palomar is an insurance company that uses technology well. Its founders are insurance professionals, not technologists. Its competitive advantage derives primarily from underwriting judgment and risk selection, not from algorithms or apps. The technology stack matters — it enables faster, more granular, more consistent underwriting — but it is a means to an end, not the end itself. Investors who evaluate Palomar through an InsurTech lens may be asking the wrong questions. The right questions are about combined ratios, reserve adequacy, reinsurance structures, and management discipline — the traditional metrics of insurance quality.

XIII. Analytical Framework: Porter's Five Forces and Hamilton's Seven Powers

To evaluate the durability of Palomar's competitive position, it is useful to apply two complementary analytical frameworks.

Starting with Porter's Five Forces, competitive rivalry in specialty insurance is high. Palomar faces numerous capable competitors — Kinsale, RLI, Everest Re, and others — that bring deep expertise and strong balance sheets. However, rivalry is moderated by the industry's cyclical pricing discipline. In hard markets, competitors maintain pricing floors rather than cutting each other's margins. The real risk comes during soft markets, when excess capital drives irrational pricing.

The threat of new entrants is medium-high. Regulatory barriers exist — insurance companies need state licenses, AM Best ratings, and substantial capital — but they are not insurmountable. The InsurTech wave demonstrated that new entrants can raise capital and enter the market. However, most failed to achieve profitability, suggesting that the real barrier to entry is not capital or licenses but underwriting expertise and distribution relationships, which take years to build.

Supplier power is elevated in Palomar's world. Reinsurers — the companies that provide the catastrophe protection Palomar relies on — hold significant leverage, particularly during hard reinsurance markets. When reinsurance costs rise, Palomar's margins compress unless it can pass those costs through to policyholders. The Torrey Pines Re cat bond program is partly a response to this dynamic — by accessing the capital markets directly, Palomar reduces its dependence on traditional reinsurers.

Buyer power is moderate. Agents and brokers have negotiating leverage over commission rates and placement decisions. But end customers in specialty lines often have limited alternatives — if you need earthquake coverage for a commercial building in California, your options are constrained — which supports pricing power. The important nuance is that in specialty insurance, the buyer is often the agent or broker, not the end customer. Agents control placement decisions and can steer business toward preferred carriers. Palomar must maintain competitive commissions, responsive service, and broad product offerings to keep agents engaged. Losing a productive agency relationship can mean losing an entire book of business.

The threat of substitutes is low to moderate. Government programs like the California Earthquake Authority and the FAIR Plan provide some coverage, and large commercial clients can self-insure or form captives. But for most buyers of specialty catastrophe coverage, there are few genuine substitutes for private-market insurance. The CEA, while dominant in residential earthquake, does not compete in commercial earthquake — a key market for Palomar. And self-insurance, while theoretically possible for large corporations, is impractical for most property owners who need to satisfy lender requirements and protect against catastrophic loss.

Turning to Hamilton Helmer's Seven Powers framework, the analysis reveals both strengths and limitations. Scale economies are moderate — Palomar's fixed costs in technology and infrastructure spread over a growing premium base, producing improving expense ratios. But reinsurance costs and loss ratios do not scale infinitely; catastrophe risk does not get cheaper just because the company gets bigger.

Network effects are limited in insurance. There is no direct benefit to a policyholder from other policyholders buying Palomar coverage. Agent relationships provide some ecosystem benefits, but these fall short of true network effects.

Counter-positioning was historically one of Palomar's strongest powers. The original thesis — that legacy carriers were too slow, too technology-backward, and too unfocused to compete effectively in specialty catastrophe lines — was powerful in 2014. A decade later, incumbents have adapted, investing in technology and returning to some of the markets they had abandoned. This advantage is fading.

Switching costs are low to moderate. Commercial clients can switch carriers at renewal based on price and coverage terms. Agent relationships provide some stickiness, and multi-year policies create temporary lock-in, but there is no structural barrier to switching in most specialty lines.

Branding power is limited by Palomar's B2B2C distribution model — most policyholders do not know or care which carrier is behind their policy. Reputation among agents and brokers matters significantly, however, and AM Best ratings serve as critical brand proxies. The upgrade to "A (Excellent)" with Positive outlook enhances this form of brand equity.

Cornered resources include Palomar's specialized underwriting talent, proprietary data accumulated over a decade, and reinsurance relationships — particularly the Torrey Pines Re cat bond program, which has been built through six issuances over eight years and provides access to capital markets risk transfer that newer competitors would need years to replicate. Whether these constitute truly cornered resources or merely advantages that competitors can replicate over time is debatable — but the time required to replicate them provides a meaningful head start.

Process power is arguably Palomar's strongest competitive advantage. The underwriting discipline and risk selection culture that Armstrong and his team built from founding — where every submission is evaluated through consistent analytical frameworks, where profitable underwriting is prioritized over premium growth, and where the combined ratio is the north star metric — represents organizational capability that is genuinely difficult to replicate.

Process power compounds over time as institutional knowledge deepens and underwriting algorithms improve with more data. Each year of writing earthquake policies generates proprietary loss experience that feeds back into pricing models. Each catastrophe event — whether it produces losses or not — provides calibration data. This is the power that Kinsale also possesses, and it explains why both companies produce combined ratios twenty-plus points better than industry averages. It is also why the best specialty insurers tend to stay the best — the compounding nature of process power creates widening advantages over time.

XIV. Bull versus Bear Case

The bull case rests on several reinforcing pillars.

Palomar's management team has demonstrated disciplined underwriting across a decade that included a pandemic, record hurricane seasons, historic wildfires, and volatile capital markets. The combined ratio has remained in the mid-to-high seventies while premiums have grown from seventeen million to two billion dollars. The Palomar 2X strategic plan was achieved ahead of schedule. Return on equity has climbed to nearly twenty-six percent on an adjusted basis, comfortably exceeding the company's own twenty percent target.

The runway for continued growth appears long. Earthquake insurance take-up rates in California remain below fifteen percent — meaning more than eighty-five percent of homeowners in the most seismically active state in the country do not carry earthquake coverage. Each major earthquake event could drive take-up rates higher, expanding Palomar's addressable market. The surety market, entered through the Gray acquisition, adds a large, stable, non-catastrophe revenue stream. Crop insurance provides federally backed premium flows. Casualty lines offer expansion opportunities in a market experiencing favorable pricing.

Rising interest rates have transformed the investment income profile. From $3.2 million in 2018 to $56 million in 2025, investment income has become a meaningful profit contributor without any additional risk-taking on the underwriting side. Climate change, paradoxically, may drive demand for catastrophe coverage higher while supporting pricing power for carriers that can model and price the risk accurately.

The bear case is equally substantive and deserves serious consideration.

Insurance is ultimately cyclical, and the current hard market will eventually soften. When it does, Palomar will face a choice between maintaining underwriting discipline (accepting slower growth) and chasing premium volume (accepting lower margins). Every insurance company's management team promises discipline during hard markets. The real test comes when the market turns.

Catastrophe exposure is inherent to the business model. Despite the sophisticated reinsurance tower, a major earthquake along the San Andreas or Hayward faults could test Palomar's capital and reinsurance structure in ways that modeling exercises cannot fully simulate. The company has never experienced a truly catastrophic earthquake event — the ultimate test of its risk management remains theoretical.

The technology moat may be overstated. Kinsale, RLI, and large incumbents all invest in technology, and the specific advantages that Palomar holds today may erode as competitors modernize their own platforms. Regulatory risk is real and specific to Palomar's core market. The California Department of Insurance operates under Proposition 103, a 1988 ballot initiative that rolled back insurance rates by twenty percent, required prior approval for all rate changes, and made the insurance commissioner an elected position — effectively politicizing the rate-setting process. Average rate approval processing times have stretched from 157 days to nearly 300 days in recent years. While Palomar's earthquake business is somewhat insulated from the homeowners and wildfire regulatory battles (the CEA handles most residential earthquake coverage), any insurer operating in California faces the risk that regulatory interference could prevent actuarially justified rate increases.

Reinsurance costs can squeeze margins during hard reinsurance markets, and Palomar's dependence on its reinsurance tower means that any disruption to reinsurance access would be deeply problematic.

Perhaps most importantly, can underwriting discipline survive rapid growth? Palomar has grown premiums at a compound annual growth rate exceeding forty percent since founding. Every new product line, every new geography, every new underwriter introduces the risk that standards will slip. The acquisition of Gray Surety — a three-hundred-million-dollar bet on a new line of business — brings integration risk and the challenge of maintaining Palomar's culture across a significantly larger and more diverse organization. History is littered with specialty insurers that produced excellent results during rapid growth, only to reveal adverse reserve development and underwriting deterioration years later.

The three KPIs that matter most for tracking Palomar's ongoing performance are:

First, the adjusted combined ratio — this is the single best measure of underwriting quality and the clearest signal of whether the company is maintaining discipline as it scales. Sustained combined ratios in the mid-to-high seventies indicate that growth is profitable; any sustained drift above eighty-five percent would be a warning sign.

Second, gross written premium growth rate — but specifically in the context of market pricing. Premium growth driven by rate increases in a hard market is very different from premium growth driven by market share gains in a soft market. The quality of growth matters as much as the quantity.

Third, adjusted return on equity — this integrates underwriting profitability, investment income, capital efficiency, and leverage into a single metric that captures the value being created for shareholders. Palomar targets twenty percent; sustained performance above that threshold validates the business model.

XV. Lessons for Founders and Investors

The Palomar story offers several lessons that extend well beyond insurance.

Timing dislocations is a repeatable playbook. Armstrong and his team did not invent earthquake insurance. They entered the market at a moment when legacy carriers had retreated, pricing was attractive, and the technology to build a better underwriting platform was available. The same pattern — identifying markets where incumbents have pulled back, entering with better tools and tighter discipline, and capturing margin during the recovery — has created value across industries from banking to energy to healthcare. The key is not predicting the future but recognizing the present accurately: seeing what is, rather than what was.

Discipline over growth is the hardest mantra to maintain. Every insurance CEO talks about underwriting discipline during earnings calls. Few sustain it when the market rewards growth. Armstrong's team has walked away from business repeatedly when pricing did not meet their thresholds. The 2020 hurricane season tested this discipline — losses were painful, but they were within budget because the company had not overextended in pursuit of premium volume. The Gray Surety acquisition represents the next test: can Palomar maintain its standards across a significantly larger and more diverse portfolio?

Technology as enabler, not savior. The graveyard of InsurTech startups is full of companies that believed technology alone could disrupt insurance. Palomar's approach — using technology to make experienced underwriters more accurate and efficient, rather than trying to replace them — has proven far more effective. The lesson generalizes: in complex, relationship-driven industries, technology creates the most value when it amplifies domain expertise rather than attempting to substitute for it.

Capital structure matters more than most founders realize. Insurance is a balance sheet business. Palomar's initial capitalization of seventy-five million dollars from Genstar, followed by the IPO and subsequent access to public capital markets, gave the company the financial resilience to play offense during downturns. The Torrey Pines Re cat bond program demonstrated capital markets sophistication that most specialty carriers lack. The $450 million credit facility for the Gray acquisition showed that capital markets trust Palomar's balance sheet. These capabilities are not incidental — they are strategic assets that enable counter-cyclical moves and opportunistic acquisitions.

Culture eats strategy. Palomar's underwriting culture — where the combined ratio is the north star, where profitable underwriting is celebrated over premium growth, and where every submission receives rigorous analytical scrutiny — is arguably its most durable competitive advantage. This culture was established by the founders, reinforced through hiring decisions, and embedded in the technology platform. It cannot be replicated by purchasing a software license.

Specialization creates options. Palomar started with a narrow focus on California earthquake insurance. That specialization allowed the company to build deep expertise, establish credibility, and generate the profits needed to fund expansion. The diversification into other lines followed naturally from the capabilities developed in the core business. Starting narrow and expanding from strength is a more reliable path than trying to be everything from day one.

Public market scrutiny cuts both ways. Quarterly reporting forces discipline — management teams cannot hide deteriorating fundamentals behind private-company opacity. But it also creates pressure to deliver short-term results that can conflict with long-term value creation. Armstrong has navigated this tension reasonably well, maintaining focus on the combined ratio and return on equity rather than chasing premium growth to meet quarterly expectations. The 2020 hurricane year was the ultimate test: a disappointing quarter for earnings, but the right quarter for demonstrating that the reinsurance program worked and the business model was sound.

Stay paranoid when things are going well. The best time to strengthen a business is during periods of success, not crisis. Palomar's formation of Laulima Exchange to de-risk Hawaii, its aggressive cat bond issuance to diversify reinsurance sources, and its expansion into non-catastrophe lines all occurred during periods of strong performance. These moves were defensive in nature but taken from a position of strength — exactly the kind of proactive risk management that compounds over time.

XVI. What the Future Holds

Climate change presents both Palomar's greatest opportunity and its most profound challenge.

Global insured losses from natural catastrophes have exceeded one hundred billion dollars for six consecutive years. The January 2025 Los Angeles wildfires alone generated estimated insured losses of twenty-five to forty-five billion dollars — the largest wildfire insurance event in history. Swiss Re has projected that hurricanes and earthquakes could drive insured losses to three hundred billion dollars or more in a peak year. The insurance protection gap — the difference between total economic losses and insured losses — stands at roughly sixty percent globally.

As climate-driven catastrophes become more frequent and severe, demand for sophisticated catastrophe coverage will grow. But so will the challenge of pricing that coverage accurately. Catastrophe models carry broad uncertainty ranges, and the historical data that underlies them is becoming less predictive as climate patterns shift. An important distinction for Palomar: earthquakes are not climate-driven (tectonic activity is independent of atmospheric conditions), so the core earthquake franchise is somewhat insulated from climate modeling uncertainty. However, Palomar's broader product portfolio — hurricane, flood, crop — is directly exposed to climate trends.

Artificial intelligence and machine learning are reshaping underwriting across the industry. Over ninety percent of insurance companies have adopted some form of AI, and nearly half use AI-driven pricing models in real time. The concept of "continuous underwriting" — where pricing adjusts dynamically based on real-time data rather than annual policy renewals — is gaining traction as an industry trend. For Palomar, AI represents an opportunity to refine risk selection further — analyzing satellite imagery, IoT sensor data, demographic patterns, and claims history at granularities that human underwriters alone cannot achieve. Imagine an underwriting system that can look at a satellite photo of a building, assess its roof condition, identify nearby wildfire fuel loads, cross-reference soil liquefaction maps, and generate a risk score — all before a human underwriter opens the file. That capability is moving from theoretical to operational across the industry. But AI also represents a competitive leveling — as these tools become more widely available, the specific technology advantages that Palomar holds today may commoditize.