Prologis: Building the Global Logistics Infrastructure

I. Introduction & Episode Roadmap

Picture this: Every single day, products worth $37 billion flow through a network of warehouses so vast it could cover the entire island of Singapore. This is Prologis—a company that owns 1.3 billion square feet of logistics real estate across 20 countries, quietly orchestrating the movement of goods that represent 2.8% of global GDP. From the iPhone in your pocket to the groceries delivered to your door, there's a good chance your purchases passed through a Prologis facility.

Yet for all its scale—a $100 billion market cap that dwarfs most industrial companies—Prologis remains curiously under the radar. It's not a household name like Amazon or FedEx, despite being the invisible backbone that makes their businesses possible. How did two competing warehouse REITs, born in different eras with different philosophies, merge to create what is essentially the AWS of physical logistics?

This is a story that spans four decades, from the savings and loan crisis of the 1980s to today's AI-powered supply chains. It's about two visionary leaders—Hamid Moghadam and Bill Sanders—who saw value where others saw parking lots with roofs. It's about surviving near-death experiences, making billion-dollar bets on e-commerce before "e-commerce" was even a buzzword, and transforming industrial real estate from a sleepy asset class into critical global infrastructure.

We'll trace the parallel journeys of AMB Property Corporation and ProLogis Trust, explore how they built competing empires, weathered the 2008 financial crisis in dramatically different ways, and ultimately joined forces in 2011 to create something neither could have achieved alone. We'll examine how they rode the e-commerce wave, navigated the pandemic surge, and positioned themselves at the intersection of three massive trends: globalization, digitalization, and urbanization.

The key themes we'll explore: How real estate becomes infrastructure when you reach sufficient scale. How private capital innovation can transform a capital-intensive business. And perhaps most importantly, how betting on secular trends—even when they take decades to play out—can create extraordinary value.

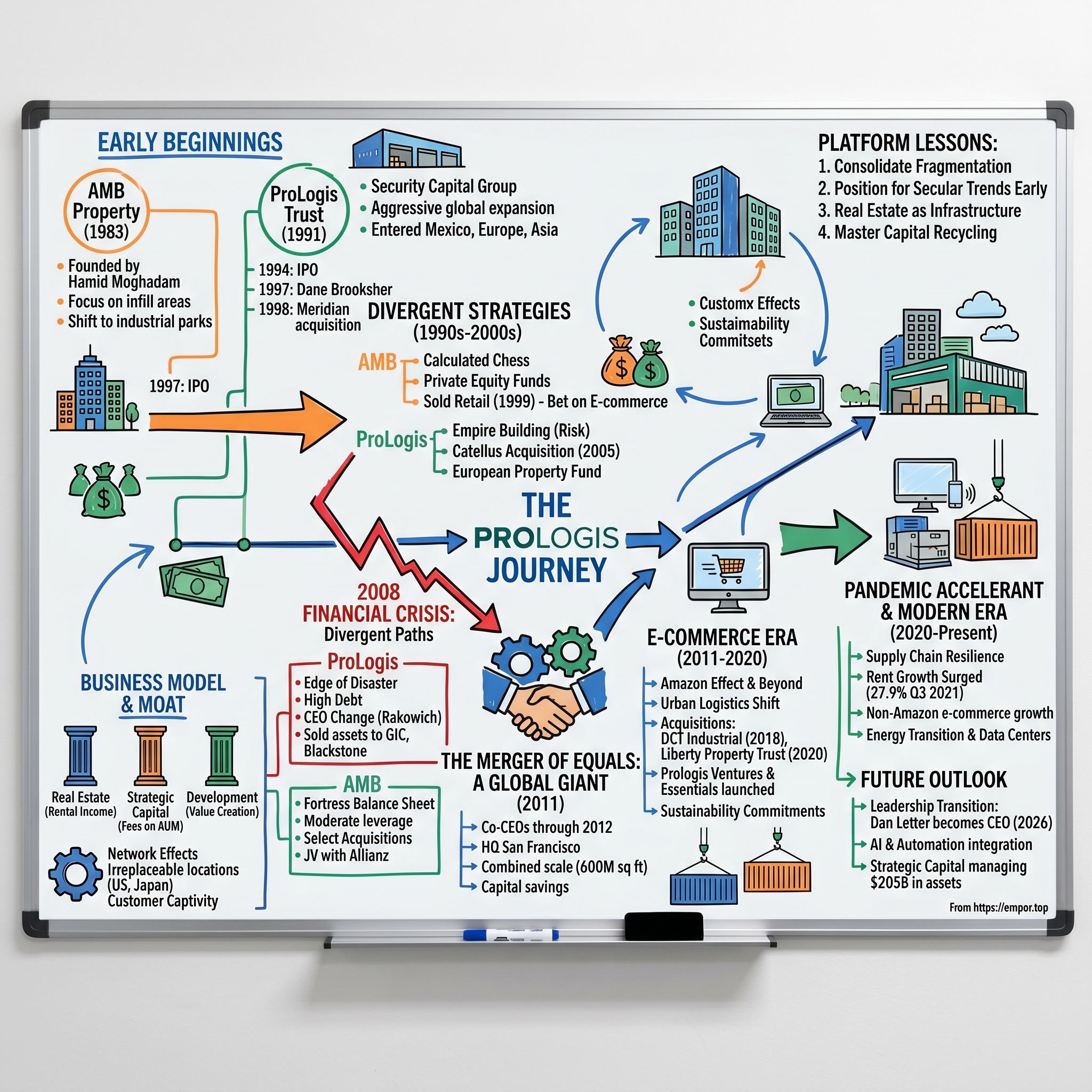

II. The Parallel Origin Stories: AMB and ProLogis Foundations### 1983: A Tehran Teenager's American Dream

In San Francisco's financial district, Hamid Moghadam stared at rejection letter number 80. The year was 1982, and the young MIT-educated engineer with a Stanford MBA couldn't land a permanent job in real estate. He received 80 rejection letters, and years later he quipped, "I actually got more rejections than interviews." The Iranian revolution had made his last name toxic in Reagan's America. His father—a successful Tehran developer who ran construction, banking, and oil exploration businesses—had died when Hamid was just 16, leaving him as the only son expected to inherit the family empire. His father died when he graduated at the age of 16. Instead, the revolution swept it all away.

But rejection letters couldn't kill the vision forming in Moghadam's mind. After a temporary stint at Homestake Mining and a job with his Stanford professor John McMahan, Moghadam was hired by John McMahan to do real estate advisory work. McMahan described Moghadam as "one of the brightest people I've ever known." In 1983, he partnered with Douglas Abbey, a colleague from McMahan's office, to form Abbey, Moghadam & Company. In 1983, he and Douglas Abbey founded Abbey, Moghadam & Company in San Francisco, California. Their plan seemed modest: provide investment advisory services to institutional investors. Although they planned to provide investment advisory services, they soon became known for "helping investors revive underperforming assets."

T. Robert Burke joined them in 1984, creating AMB Institutional Realty Advisors. They were joined by T. Robert Burke in 1984 and established AMB Institutional Realty Advisors, with initial investments in office, industrial and community shopping centers. The three men shared a contrarian insight: while everyone chased glamorous office towers and retail centers, industrial real estate—warehouses, essentially—was deeply undervalued. Moghadam would later explain the philosophy with characteristic simplicity: Warehouses are very stable; the demand for them is fairly constant. No matter what happens to the economy, you have to distribute tires, toilet paper and cereal.

1991: The Security Capital Revolution

Eight years later and 1,500 miles away in Santa Fe, New Mexico, another visionary was plotting a different path to the same destination. William Sanders—already a legend for founding LaSalle Partners in 1968 and building it into a real estate powerhouse—believed the industry was ripe for consolidation. William Sanders believed in the power of leverage through size. Through his Santa Fe-based Security Capital Group Inc., Sanders formed Security Capital Industrial Trust (SCI) in 1991.

Sanders' philosophy was simple but radical for the time: bigger companies could achieve better borrowing terms and command higher rents through scale. He envisioned not just a real estate company but a platform—a way to institutionalize an asset class that had been fragmented among thousands of local operators.

Security Capital Industrial Trust went public in 1994, raising capital on the New York Stock Exchange. SCI makes its initial public offering on the New York Stock Exchange. The company immediately began expanding beyond U.S. borders, making acquisitions in Mexico that same year. But the real transformation came in 1997 when K. Dane Brooksher, a former KPMG senior executive who had spent 32 years with the accounting giant, took the helm. In 1993, Dane joined Security Capital Industrial Trust, first as Chief Operating Officer and then as Co-Chairman and CEO. In 1994, he was successful in taking the company public on the NYSE. In 1997, the company changed its name to Prologis, and in 1998, Dane became Chairman and CEO.

Under Brooksher's leadership, the company was incorporated as ProLogis, Inc. on November 24, 1997, and by July 1998 had officially changed its name from Security Capital Industrial Trust to ProLogis Trust. SCI officially changed its name to ProLogis Trust in July 1998, then active in 84 markets in 12 countries, with a market capitalization of nearly $5 billion. The timing was perfect—or so it seemed. Global trade was exploding, supply chains were going international, and companies desperately needed sophisticated logistics partners.

The contrast between the two companies was striking. AMB, born from rejection and adversity, took a conservative, methodical approach—building trust with pension funds, focusing on gateway markets, maintaining a fortress balance sheet. ProLogis, backed by Sanders' Security Capital empire and Brooksher's operational expertise, pursued aggressive expansion—84 markets across 12 countries by 1998, a $5 billion market cap, and an appetite for transformative deals that would reshape the industry.

Both companies saw the same future: a world where logistics real estate wasn't just about storing goods but about enabling global commerce. They just had very different ideas about how to get there.

III. Divergent Growth Strategies: Building Two Empires (1990s–2000s)

AMB's Calculated Chess Moves

While ProLogis was painting the global map red with acquisitions, Hamid Moghadam was playing three-dimensional chess in San Francisco. The late 1980s savings and loan crisis had taught him a lesson that would define AMB's entire strategy: when everyone else zigs, you zag. In the late 1980s, AMB changed its investment strategy to focus on industrial parks and shopping centers in infill trade areas, with the company beginning to exit the office market in 1987. During the collapse of the office building market in the late 1980s, this shift in assets helped the company avoid significant financial repercussions.

The pivot was prescient. While office buildings hemorrhaged value during the S&L crisis, AMB's industrial properties held steady. Moghadam launched the company's first private equity fund in 1989, pioneering a model that would become central to modern real estate: use other people's money to scale, but maintain control through management. AMB launched its first private equity fund in 1989, which focused on industrial and retail properties.

By 1997, AMB was ready for its public debut. The IPO raised capital at a $2.8 billion valuation, giving Moghadam the currency he needed for his next move. In late 1997, AMB became a public company via an initial public offering, with more than US$2.8 billion under management. But what he did next shocked Wall Street. In 1999, at the height of the retail boom, AMB sold its entire retail portfolio—nearly $1 billion in assets. Moghadam's reasoning? Throughout 1999, Moghadam "made a series of moves that pared the company of most of its retail holdings, following the notion that e-commerce would become the high-margin road of the future." Starting that year AMB sold nearly $1 billion in retail assets to institutional investors and reallocated funds into warehouses in and around major consumption areas.

This wasn't just portfolio rebalancing—it was a bet on the future of commerce itself. Moghadam had met Louis Borders, founder of Webvan, and seen their pioneering online grocery fulfillment centers. "Louis Borders' vision was an internet grocer on steroids, and when I saw their first warehouse I knew the world was going to change," Moghadam told analysts. While Webvan would famously implode, Moghadam saw past the company to the revolution it represented.

By the end of 1999, AMB had transformed into the second-largest industrial REIT in the United States with a $3.5 billion market cap. By the end of 1999, AMB was the second-largest industrially focused REIT in the United States, with a total market capitalization of $3.5 billion. The company's "High Throughput Distribution" strategy focused on what Moghadam called "infill trade areas"—locations close to population centers where last-mile delivery would matter most.

AMB's international expansion began cautiously in 2002 with a single facility for Procter & Gamble in Mexico City. AMB made its first overseas investment in 2002, developing a facility for Procter & Gamble in Mexico City. But this toe in the water quickly became a full dive. In 2002, AMB initiated an international expansion program focused on buying and developing distribution facilities near global trade hubs, particularly in growth markets such as Latin America, Asia, and Europe. The strategy was surgical: focus on global trade hubs, follow the customers, build where the barriers to entry were highest.

ProLogis' Empire Building

If AMB was playing chess, ProLogis under Brooksher was playing Risk—grabbing territory with breathtaking speed. The 1998 Meridian Industrial Trust acquisition for $862.5 million made ProLogis the largest owner of industrial properties in the United States overnight. In November 1998, ProLogis Trust acquired Meridian Industrial Trust for $862.5 million in stock, and was the largest owner of industrial and warehouse properties in the U.S.

Brooksher's vision was global from day one. Throughout his tenure as CEO, Prologis expanded rapidly throughout the world through a series of acquisitions and organic growth. In 1997, Dane led the company's expansion into Mexico, in 1998 into Europe, and in 2001 into Asia. The company entered Japan in 2001, just as that country's notorious resistance to foreign real estate investment was beginning to crack. China followed in 2003, with ProLogis forming joint ventures with local partners to navigate the regulatory maze. In 2003, ProLogis was added to the S&P 500 Index and entered the Chinese market, forming its first joint venture in China with Suzhou Logistics Center Co. Ltd.

The company's European expansion was particularly audacious. ProLogis established a $1 billion European Property Fund in 1999, becoming the largest warehouse developer in the Netherlands. ProLogis had built more than 600,000 square feet of warehouse space in The Netherlands, making it the country's largest developer. To fund continued development in Europe amid rising property prices, ProLogis established a $1 billion European Property Fund in September 1999. They pushed into Eastern Europe, building facilities in Warsaw for multinationals like TDK, Kodak, and Novartis—companies that needed Western-standard logistics in emerging markets.

But ProLogis' most transformative deal came in 2005: the $3.6 billion acquisition of Catellus Development Corporation. In 2005, Prologis acquired Catellus Development Corporation for $3.6 billion. Catellus wasn't just any developer—it was the former real estate arm of Southern Pacific Railroad, sitting on vast land banks in California's most constrained markets. The deal gave ProLogis irreplaceable assets in markets where new supply was virtually impossible.

Under Brooksher's leadership, ProLogis also pioneered financial innovation in real estate. In 1999, under Dane's leadership, the company innovated its capital structure by becoming one of the first public real estate companies to create a private equity model for investing. The company created multiple property funds, essentially running a real estate private equity business inside a public REIT—a model that generated fees while allowing ProLogis to control far more real estate than its balance sheet alone could support.

By 2004, when Brooksher retired, ProLogis had become a Fortune 1000 company and joined the S&P 500. In 2003, the company was placed into the S&P 500 as among the most widely followed public companies in the world. Dane retired from Prologis in 2004. The company managed over $10 billion in assets across North America, Europe, and Asia—a global platform unmatched in industrial real estate.

Two Philosophies, One Destiny

The differences between AMB and ProLogis in this era weren't just about size or geography—they were philosophical. AMB under Moghadam believed in patient capital, conservative leverage, and strategic focus. Every move was calculated, every market entry deliberate. The company maintained close relationships with a small group of blue-chip tenants and institutional investors.

ProLogis under Brooksher and later CEOs believed in first-mover advantage, global scale, and financial engineering. They would enter markets early, often at premium prices, betting that scale would eventually deliver superior returns. The company's relationship with William Sanders' Security Capital network gave it access to capital that AMB couldn't match.

Yet both companies were building toward the same insight: industrial real estate was transforming from a sleepy, fragmented asset class into critical infrastructure for the global economy. The question wasn't whether consolidation would happen—it was who would lead it.

As the 2000s progressed, that question would be answered in ways neither company anticipated. The financial crisis looming on the horizon would test both models to their breaking point, setting the stage for an unlikely union.

IV. The 2008 Financial Crisis: Divergent Paths

ProLogis: Dancing on the Edge of Disaster

In late 2007, ProLogis CEO Jeffrey Schwartz stood before investors at a Goldman Sachs conference, projecting confidence. The company had just reported record earnings, its global footprint stretched across 118 markets, and its development pipeline bulged with $9 billion in projects. ProLogis was the undisputed king of industrial real estate. Within 18 months, it would be fighting for survival.

The warning signs had been there. ProLogis had funded its empire through aggressive borrowing—by 2008, the company carried $11.2 billion in debt. Worse, much of its growth came from development, not acquisition. The company was essentially a massive bet that global trade would keep expanding forever, that tenants would keep absorbing new space, that capital markets would stay liquid.

When Lehman Brothers collapsed in September 2008, those assumptions shattered overnight. Global trade volumes plummeted 12% in 2009—the first decline since World War II. Tenants stopped expanding. Some stopped paying rent altogether. ProLogis' stock price, which had touched $70 in 2007, crashed below $3 by March 2009.

The board acted decisively, perhaps desperately. Following aggressive expansion and heavy borrowing, ProLogis' CEO Jeffrey Schwartz was replaced by Walter Rakowich in 2008, who implemented cost-cutting efforts, raising capital and selling assets. Walter Rakowich, a ProLogis veteran who understood the company's operations intimately, took the helm with a simple mandate: survive.

Rakowich's rescue plan was brutal in its efficiency. The company slashed its dividend by 50%. Development spending dropped from $3.5 billion to near zero. Most dramatically, ProLogis began selling its crown jewels. In December 2008, ProLogis sold a portfolio of assets to the Government of Singapore Investment Corporation, with which it formed Global Logistic Properties. The company sold its China operations and some of its Japanese interests to GIC Private Limited for $1.3 billion in 2009. The Singapore GIC deals were particularly painful—ProLogis sold its China and Japan portfolios for $1.3 billion, a fraction of what it had invested to build them.

The company that had pioneered global industrial real estate was retreating to its home market, selling assets at distressed prices to whoever would buy them. By late 2010, Blackstone acquired another portfolio for $1 billion—assets ProLogis had valued at nearly twice that amount just three years earlier. The Blackstone Group acquired a portfolio of assets from the company in late 2010 for $1 billion.

AMB: The Fortress Balance Sheet Philosophy

Across San Francisco Bay, Hamid Moghadam watched ProLogis' near-death experience with a mixture of sympathy and vindication. AMB had faced the same temptations during the boom years—aggressive leverage, speculative development, growth at any cost. Moghadam had resisted them all.

When the crisis hit, AMB's balance sheet was a thing of beauty: moderate leverage, minimal development exposure, long-term leases with credit-worthy tenants. Moghadam told the San Francisco Business Times, "Our strategy is tied to global trade, and this forces us to look at international markets and redeploy cash overseas. Our customers are pushing us to help them with their global problems. There are few reliable warehouse sources that are up to international standards and companies want to simplify the business relying on a few vendors."

But Moghadam knew that in a crisis, perception matters as much as reality. In 2009, AMB completed an equity offering that would "fortify the balance sheet and secure projected capital needs through 2012." AMB completes its equity offering, fortifying the balance sheet and securing projected capital needs through 2012. The move diluted existing shareholders but sent a clear message: AMB would emerge from the crisis stronger, not weaker.

While ProLogis was selling assets in fire sales, AMB was selectively acquiring. The company formed new joint ventures, including a €470 million partnership with Allianz Real Estate—at the time, Allianz's largest real estate joint venture ever. In March 2011, before the merger with ProLogis, AMB Property formed a €470 million joint venture with Allianz Real Estate.

The Stage Is Set

By late 2010, the industrial real estate landscape had fundamentally changed. The financial crisis had winnowed the field of competitors. Dozens of smaller players had gone bankrupt or been absorbed. Capital was returning to the market, but cautiously, favoring established platforms with proven management.

ProLogis had survived, but at enormous cost. The company that once commanded a premium valuation now traded at a discount to book value. Its development pipeline was dormant. Its international expansion had been partially reversed. Walter Rakowich had saved the company, but ProLogis needed a new vision for growth.

AMB had navigated the crisis brilliantly, but Moghadam saw a problem: the company was subscale for the consolidation wave he knew was coming. E-commerce was beginning to transform logistics. Amazon alone was absorbing millions of square feet annually. The winners in industrial real estate would be those with true global platforms, able to serve multinational customers everywhere they operated.

Two proud companies. Two proven management teams. Two complementary strengths. The logic for combination was compelling, but logic alone doesn't make mergers. It would take something more: mutual respect between former rivals, shared vision for the future, and perhaps most importantly, the humility to recognize that neither company could achieve its ambitions alone.

The stage was set for one of real estate's most transformative deals.

V. The Merger of Equals: Creating a Global Giant (2011)

The Secret Meetings

The first conversation happened in December 2010, in a neutral conference room at a San Francisco law firm. Hamid Moghadam and Walter Rakowich sat across from each other—two CEOs who had competed for the same assets, the same tenants, the same investors for over a decade. The facilitator was an investment banker who knew both men well and saw what they initially couldn't: their companies needed each other.

Moghadam came prepared with analysis. AMB's portfolio was concentrated in global gateway markets—the expensive, supply-constrained locations near ports and population centers. ProLogis had scale, with facilities in secondary and tertiary markets that AMB had never entered. Together, they would control 600 million square feet across 22 countries. No customer would be too large. No market too complex.

Rakowich had his own math. ProLogis was trading at 0.7 times book value, despite having stabilized its balance sheet. The market didn't trust the ProLogis story anymore—investors remembered the near-bankruptcy, the dividend cuts, the asset sales. A merger with AMB, with its premium valuation and Moghadam's credibility, could unlock billions in shareholder value.

But the real breakthrough came when they stopped talking about numbers and started talking about vision. Both men saw the same future: e-commerce would drive demand for decades. Supply chains were becoming more complex, not simpler. Customers wanted global partners, not regional landlords. The winner in industrial real estate wouldn't be the biggest owner—it would be the best operator, the most trusted partner, the platform that could solve complex logistics problems.

Engineering the Deal

Agreed to in January 2011, AMB Property Corporation contracted to buy the larger ProLogis for $8.7 billion, with the new entity named Prologis. The structure was elegant in its simplicity: ProLogis shareholders would receive 0.4464 AMB shares for each ProLogis share they owned. Despite ProLogis being the larger company by square footage, AMB shareholders would own 60% of the combined company—a reflection of AMB's superior valuation and balance sheet.

The headquarters decision was symbolic but important. Prologis would then be based in San Francisco, AMB's hometown, and maintain an office in Denver, Colorado, where ProLogis was based. San Francisco, AMB's home, would be the global headquarters. Denver, ProLogis' base, would maintain a significant presence. The message was clear: this was a merger of equals in spirit, even if the ownership math suggested otherwise.

The governance structure was perhaps the deal's most innovative element. ProLogis CEO Walter Rakowich and Moghadam were appointed as the new company's co-CEOs, with Moghadam becoming the sole CEO at the start of 2013. Both Moghadam and Rakowich would serve as co-CEOs through 2012, with clearly delineated responsibilities. Moghadam would handle strategy, capital markets, and investor relations—the external face of the company. Rakowich would manage operations, integration, and customer relationships—ensuring the merger delivered its promised synergies.

The Vision Articulated

When the deal was announced on January 31, 2011, Moghadam and Rakowich presented a compelling vision to skeptical investors. The combined company would generate $80 million in annual cost savings through eliminated redundancies. But the real value, they argued, wasn't in cost cutting—it was in revenue growth.

With a market cap of approximately $24 billion and corporate headquarters remaining in California, the new Prologis had around $46 billion in assets under management and clients such as DHL, Home Depot Inc., Unilever, and FedEx. The new Prologis would serve 4,500 customers globally, including the world's largest logistics companies, retailers, and manufacturers. No other industrial REIT could offer space in Yokohama and New Jersey, Birmingham and Beijing, all under one roof, with consistent standards and a single point of contact.

The private capital business was particularly exciting. Combined, the companies managed $32 billion for third-party investors—pension funds, sovereign wealth funds, insurance companies. This fee-generating business would provide stable income even during real estate downturns, while allowing Prologis to control far more real estate than its balance sheet alone could support.

Integration: The Delicate Dance

Completed in June 2011, the merger was one of the biggest real estate deals since the Great Recession, and created the largest industrial real estate company in the world. The summer of 2011 was controlled chaos at Prologis. Two corporate cultures had to become one. Duplicate positions had to be eliminated—delicately, given that both companies needed their best people to stay. Systems had to be integrated. Most challengingly, overlapping assets in the same markets had to be rationalized.

Moghadam and Rakowich modeled collaboration from the top. They held joint town halls, made decisions together, and publicly supported each other even when private disagreements arose. When the time came in late 2012 for Rakowich to step aside as planned, he did so gracefully, having delivered on the integration promises.

The numbers validated the strategy. By the end of 2011, Prologis had already achieved $40 million in cost synergies—half the ultimate target in just six months. Occupancy rates increased. The stock price, which had languished for both companies pre-merger, began a steady climb.

The Platform Advantage Emerges

But the real success of the merger became apparent in customer wins. Amazon, which had been splitting its business among multiple industrial REITs, began consolidating with Prologis. The reason was simple: only Prologis could provide facilities in every market Amazon needed, with consistent quality and terms.

FedEx, UPS, and DHL—the backbone of global logistics—similarly expanded their relationships. For these companies, having a single landlord across multiple markets simplified operations, reduced transaction costs, and provided leverage in negotiations.

The merger also unlocked international expansion opportunities neither company could have pursued alone. In Japan, Prologis leveraged AMB's relationships to expand ProLogis' existing platform. He oversaw IPOs in Japan in 2013 and Mexico in 2014. The company completed an IPO of Nippon Prologis REIT in 2013, raising capital locally while maintaining control of the platform.

By every measure, the merger exceeded expectations. Cost synergies ultimately reached $120 million annually—50% above initial targets. Revenue growth accelerated as customers consolidated with the global leader. The stock price more than doubled within three years.

The new Prologis wasn't just bigger than its predecessor companies—it was fundamentally different. It had achieved something rare in business: true platform economics, where the value of the network exceeded the sum of individual assets. The merger hadn't just created the world's largest industrial REIT; it had created the essential infrastructure provider for global commerce.

VI. The E-Commerce Transformation Era (2011–2020)

The Amazon Effect—and Beyond

In 2013, something strange started happening in Southern California's Inland Empire. Warehouse rents, historically stable and predictable, began climbing at rates that defied logic. The culprit wasn't hard to identify: Amazon had arrived, and it was hungry.

The e-commerce giant leased 5 million square feet from Prologis that year. Then 10 million in 2014. By 2015, the pace was approaching 20 million square feet annually. The strategy led Prologis to pursue fulfillment center development projects for Amazon; the e-commerce firm became its largest tenant with 46 million square feet occupied as of the end of 2024. But here's what most observers missed: Amazon was just the tip of the iceberg.

Moghadam saw the deeper trend. Every traditional retailer was scrambling to build e-commerce capabilities. Walmart, Target, Home Depot—companies that had been Prologis customers for decades—suddenly needed different types of facilities in different locations. Not just bulk storage in remote areas, but last-mile facilities close to population centers. Not just standard 32-foot clear heights, but 40-foot giants that could accommodate multi-level fulfillment systems.

"We're not in the warehouse business anymore," Moghadam told his team in 2014. "We're in the time business. Every hour we can shave off delivery time is worth millions to our customers."

The Urban Logistics Revolution

This insight drove Prologis' most important strategic shift of the decade: the move into urban infill markets. These weren't traditional industrial locations. They were former shopping malls in Los Angeles, obsolete manufacturing plants in New Jersey, even abandoned automotive facilities in Chicago. The acquisition prices were eye-watering—sometimes $200 per square foot in markets where traditional industrial traded at $50.

Wall Street analysts were skeptical. Why pay premium prices for complicated redevelopment projects? The answer became clear during the 2018 holiday season, when same-day delivery became table stakes for e-commerce competition. A facility in downtown Los Angeles, no matter how expensive, could reach 10 million consumers within two hours. A cheaper facility in the desert might as well be on the moon.

The Acquisition Spree

With the platform advantage established, Prologis went shopping for portfolios that would cement its dominance. The 2015 KTR Capital Partners acquisition for $5.9 billion added 60 million square feet of prime assets. That June, Prologis partnered with Norges Bank Investment Management to buy KTR Capital Partners for $5.9 billion. But this was just the appetizer.

The 2018 DCT Industrial acquisition for $8.5 billion was transformative. Prologis completes an all-stock acquisition of DCT Industrial Trust for $8.5 billion. DCT had built a portfolio focused on exactly the markets Prologis needed: high-barrier coastal markets where Amazon and its competitors were desperate for space. The deal added 71 million square feet and eliminated Prologis' most serious competitor in one stroke.

Then came the masterstroke: Liberty Property Trust for $13 billion in January 2020. In 2020, acquisitions of Liberty Property Trust for $13 billion and Industrial Property Trust for $4 billion. The timing seemed terrible—the deal closed just as COVID-19 was shutting down the global economy. Within months, it would look like genius.

Innovation Beyond Bricks and Mortar

But Moghadam's vision extended beyond simply rolling up competitors. In 2016, Prologis launched Prologis Ventures with a radical premise: the company needed to invest in technologies that would transform how warehouses operated. Prologis formed Prologis Ventures, its venture capital arm, in March 2016, making 20 investments by late 2019.

The venture portfolio read like a who's who of logistics innovation. Autonomous forklifts. Warehouse robotics. Last-mile delivery platforms. By 2019, Prologis Ventures had invested in 40 companies, deploying $180 million. These weren't passive investments—Prologis provided its portfolio companies with something money couldn't buy: access to 6,600 customers and 1.3 billion square feet of space to test and scale their innovations.

The 2018 launch of Essentials took this strategy further. Prologis began to expand its non-real estate business, Essentials, in 2018, offering customers solar power, racking systems, forklifts, generators, EV charging infrastructure, and other logistics tech equipment for purchase. Instead of just leasing space, Prologis would provide everything a customer needed to operate: solar panels for power, racking systems for storage, even forklifts for moving goods. The message to customers was clear: Prologis wasn't just your landlord—it was your logistics partner.

The Sustainability Imperative

As the decade progressed, another force began reshaping industrial real estate: environmental consciousness. Amazon pledged to be carbon neutral by 2040. Walmart committed to zero emissions by 2040. Every major Prologis customer suddenly had aggressive sustainability targets.

Prologis responded by becoming the first logistics REIT to set science-based carbon targets, committing to net-zero emissions by 2040. But this wasn't just virtue signaling. Solar panels on warehouse roofs generated revenue. LED lighting reduced operating costs. LEED-certified buildings commanded premium rents.

By 2019, Prologis had 280 megawatts of solar capacity across its portfolio—enough to power 56,000 homes. The company's sustainability report became required reading for institutional investors, who increasingly viewed environmental performance as a proxy for management quality.

The Numbers Tell the Story

The transformation of Prologis during this decade was staggering. Assets under management grew from $46 billion at the merger to over $150 billion by 2020. The company's market capitalization quadrupled. But the most telling statistic was this: by 2020, Prologis facilities handled goods worth $2.7 trillion annually—roughly 2.8% of global GDP.

The e-commerce transformation that Moghadam had anticipated in 1999 when he sold AMB's retail portfolio had arrived in full force. But it wasn't just about e-commerce. It was about the complete reimagination of supply chains, from globalized just-in-time systems to resilient, flexible networks capable of handling anything from two-day delivery to global pandemics.

As 2020 dawned, Prologis stood at the apex of industrial real estate. It had the best portfolio, the strongest balance sheet, the deepest customer relationships. What it couldn't have anticipated was that its greatest test—and opportunity—was just weeks away.

VII. The Pandemic Accelerant & Modern Era (2020–Present)

March 2020: When Everything Changed

Hamid Moghadam was in his San Francisco office on March 16, 2020, when California announced the nation's first lockdown. The Liberty Property acquisition had closed just six weeks earlier. Prologis now owned 1 billion square feet of logistics space, carried $13 billion in fresh acquisition debt, and faced the complete shutdown of the global economy.

The initial weeks were chaos. Some tenants—airlines, automotive suppliers, traditional retailers—immediately requested rent relief. Others—Amazon, Instacart, medical suppliers—needed space yesterday. Prologis' operations team fielded thousands of calls daily, triaging requests, negotiating payment plans, and somehow keeping goods flowing through a paralyzed supply chain.

Then something remarkable happened. As Americans sheltered at home, e-commerce exploded. Online grocery shopping, which had struggled for adoption for two decades, grew 300% in three months. Amazon hired 175,000 workers in March and April alone. Every consumer brand scrambled to build direct-to-consumer capabilities.

By May 2020, Prologis' properties weren't just full—they were overflowing. Parking lots became temporary storage areas. Tenants begged for any available space. Prologis completes an acquisition of the wholly owned real estate assets of Industrial Property Trust for approximately $4 billion in cash. The Industrial Property Trust acquisition for $4 billion, initially seen as aggressive, now looked prescient.

The Great Supply Chain Stress Test

The Suez Canal blockage in March 2021 created a natural experiment in supply chain resilience. The Ever Given, stuck sideways for six days, backed up $60 billion in global trade. When the ship finally moved, the cargo tsunami hit U.S. ports all at once. The ports of Los Angeles and Long Beach had 100+ ships waiting to unload. Containers stacked up like skyscrapers.

For Prologis, this chaos was opportunity. The company's facilities near ports commanded unprecedented premiums. Tenants signed leases at any price just to secure space. In Q3 2021, Prologis reported something unprecedented: 27.9% increase in Q3 2021 net effective rental prices. Nearly 28% rental growth in a single quarter—in an industry where 3% annual growth was historically considered strong.

But Moghadam saw beyond the temporary surge. The pandemic had exposed the fragility of globalized just-in-time supply chains. Companies were reshoring production, building buffer stock, creating redundancy. McKinsey estimated that companies would need 300-400 million square feet of additional warehouse space just to carry safety stock. Prologis owned the land and expertise to build it.

The Democratization of E-Commerce

Perhaps the most significant shift was who was driving demand. For years, Amazon had been the boogeyman of industrial real estate—the tenant with outsized power, the price setter, the gorilla in the room. By 2022, that dynamic had fundamentally changed. Non-Amazon customers accounting for 85% of new e-commerce leases in 2022, up from 66% in 2020.

Every retailer had become an e-commerce company. Kroger needed fulfillment centers for grocery delivery. Nike was going direct-to-consumer. Even B2B distributors were building e-commerce capabilities. The diversification of demand gave Prologis pricing power it had never enjoyed before.

The Technology Revolution Accelerates

The labor shortages of 2021-2022 catalyzed a warehouse automation revolution. Suddenly, every Prologis customer wanted to discuss robotics. Not in five years—now. The company's Essentials platform, initially seen as a nice-to-have service offering, became central to customer conversations.

Prologis partnered with robotics companies to offer "Automation as a Service." Instead of customers making massive capital investments in unproven technology, Prologis would install and maintain automated systems, charging on a usage basis. The model de-risked automation for customers while giving Prologis another revenue stream and deeper customer relationships.

The company projected that automation could improve warehouse productivity by 10-20% over the next three years—crucial for customers facing persistent labor shortages and rising wages. But automation also meant warehouses needed different specifications: perfectly flat floors for robots, increased power capacity, different ceiling heights. Prologis' modern portfolio was ideally suited for these requirements.

The Energy Transition Opportunity

As 2024 progressed, a new opportunity emerged: the energy transition. Data centers, EV charging infrastructure, battery storage—all needed land near power infrastructure and population centers. Exactly the kind of land Prologis had been accumulating for decades.

The company began selectively developing data centers on excess land parcels, partnering with hyperscale cloud providers desperate for sites. EV charging stations appeared in Prologis parking lots, serving both tenant fleets and public vehicles. Solar installations expanded from rooftops to ground-mounted systems, with Prologis becoming one of the largest private solar operators in the world.

The New Logistics Landscape

By 2024, the statistics told a remarkable story. E-commerce accounting for 56% of retail goods growth. E-commerce was driving 56% of all retail goods growth. Total U.S. logistics space had grown 12% since the pandemic, while retail space had actually shrunk 2.4%. The economy had fundamentally restructured around logistics.

Prologis emerged from the pandemic not just larger but transformed. The company now operated as three integrated businesses: a real estate owner generating rental income, a capital manager earning fees on $60+ billion of third-party money, and a services provider offering everything from solar power to warehouse robotics.

The market recognized this transformation. Prologis' stock price, which had bottomed at $75 during the March 2020 panic, touched $140 by late 2021. The company's market cap exceeded $100 billion, making it one of the most valuable REITs in the world.

Looking Forward: The AI and Automation Era

As 2025 unfolds, Moghadam—now 69 and planning his succession—sees the next transformation already beginning. Artificial intelligence is optimizing supply chains in ways humans never could. Autonomous vehicles promise to revolutionize goods movement. Climate change is forcing companies to build resilience into their logistics networks.

The company expects continued strong demand, projecting a 140 million square foot supply deficit over the next five years even as construction ramps up. Urban land constraints, environmental regulations, and NIMBY resistance make new supply increasingly difficult, particularly in the coastal markets where Prologis dominates.

But perhaps the most important legacy of the pandemic era is philosophical. Logistics real estate is no longer seen as a commodity—interchangeable boxes in industrial parks. It's recognized as critical infrastructure, as essential to modern life as power grids or telecommunications networks. And Prologis, through vision, execution, and a bit of pandemic luck, has positioned itself as the irreplaceable provider of that infrastructure.

VIII. The Business Model & Competitive Moat

The Three-Legged Stool

Chris Caton, Prologis' head of strategy, likes to draw the business model as a three-legged stool. Most real estate companies, he explains, have one leg: they own buildings and collect rent. "That's a perfectly fine business," he says, "but it's furniture that tips over in a storm."

The first leg—owned and operated real estate—is indeed massive. Prologis owns 1.3 billion square feet across 20 countries, generating over $5 billion in annual rental income. But this is table stakes in industrial real estate. What matters is the quality: 95% occupancy, average remaining lease terms of 5+ years, and locations that would be impossible to replicate today.

The second leg transforms the model: Strategic Capital. The company also has a strategic capital business segment that has around $60 billion of third-party AUM. Prologis manages $60+ billion for institutional investors through various fund structures. The genius isn't just the $400+ million in annual management fees. It's that Prologis controls twice as much real estate as it owns, giving it market intelligence and customer relationships that no competitor can match.

The third leg—Development—is where Prologis creates value. The company's land bank, accumulated over decades, sits in markets where new supply is virtually impossible. When Amazon needs a facility in Northern California or FedEx requires expansion in Tokyo, Prologis doesn't compete for sites—it already owns them. Development yields stabilized returns of 7-9% in an environment where existing assets trade at 4-5% cap rates.

Network Effects at Scale

But the real moat isn't any single advantage—it's how they compound. Consider a typical customer interaction: Target needs to expand its e-commerce fulfillment network. It could work with dozens of local developers, negotiating separately in each market. Or it could call Prologis.

Prologis doesn't just offer space. It provides a complete solution: sites in every major market, consistent lease terms, sustainability features that help Target meet its ESG goals, and increasingly, the automation and energy infrastructure to operate efficiently. The conversation shifts from "how much per square foot?" to "how can we help you serve your customers better?"

This dynamic creates powerful network effects. It serves about 6,600 tenants. The more customers Prologis serves (currently 6,600), the more data it collects on logistics patterns. This data informs where to develop next, what specifications to build, which technologies to invest in through Prologis Ventures. Better decisions attract more customers, creating a virtuous cycle.

The numbers validate the strategy. Prologis' rent growth consistently exceeds market averages by 100-200 basis points. Customer retention exceeds 95%. The company's share of new leasing in its markets approaches 30%—remarkable for a company that owns "only" 3% of global logistics space.

The Capital Light Revolution

The Strategic Capital business deserves special attention because it fundamentally changed Prologis' economics. Traditional REITs are capital-intensive: to grow, they must raise equity or debt, diluting returns. Prologis flipped this model.

Here's how it works: Prologis develops a portfolio of assets using its balance sheet. Once stabilized and leased, it sells 80-90% of the portfolio to one of its funds, keeping 10-20% and earning management fees on the whole. The capital recycled from the sale funds new development. Prologis maintains control through its position as manager and co-investor.

The math is compelling. On a typical $1 billion portfolio: - Prologis invests $150 million (15% co-investment) - Earns $10 million annually in management fees (1% of total value) - Generates 6.7% return on its $150 million equity - Combined return on invested capital: ~13-15%

This model allows Prologis to grow without constantly tapping capital markets. It aligns interests with institutional investors who want exposure to logistics real estate but lack the platform to execute directly. And it generates stable fee income that supports the stock's premium valuation.

The Irreplaceable Portfolio

Real estate is ultimately about location, and Prologis owns locations that cannot be replicated. Consider Southern California's Inland Empire, the largest logistics market in America. Environmental regulations, water scarcity, and community opposition make new development nearly impossible. Prologis owns 100+ million square feet there, accumulated over decades.

Or consider Tokyo Bay, where Prologis operates massive multi-story fulfillment centers serving 40 million consumers. Japan's mountainous geography means flat, developable land near population centers essentially doesn't exist. Every Prologis facility there is irreplaceable.

According to The Economist, its business strategy is focused on warehouses that are located close to huge urban areas where land is scarce. The Economist captured this dynamic perfectly: Prologis focuses on "warehouses located close to huge urban areas where land is scarce." In an e-commerce world where delivery speed determines competitive advantage, these locations are gold.

Customer Captivity Through Complexity

Moving a warehouse operation is extraordinarily disruptive. Systems must be reconfigured. Workers retrained. Customer delivery promises adjusted. For modern e-commerce operations with automation infrastructure, moving is almost impossible—the robotics are built into the building itself.

This creates powerful customer captivity. Prologis' lease renewal rate exceeds 95% in most quarters. When leases do expire, tenants typically renew at rates 30-50% above prior levels—and consider it a bargain versus the cost of relocation.

The Essentials platform deepens this captivity. When Prologis provides not just the building but the solar panels, racking systems, and automation infrastructure, the switching costs become prohibitive. The landlord-tenant relationship evolves into a partnership.

The Platform Premium

All these advantages compound into what analysts call the "platform premium"—the reason Prologis trades at valuations 20-30% above other industrial REITs. It's not just about owning more buildings. It's about owning the right buildings, in the right places, with the right services, for the right customers.

The moat is widening. Each acquisition makes Prologis more essential to customers. Each development in a supply-constrained market increases the replacement cost of the portfolio. Each innovation through Prologis Ventures or Essentials adds another layer of differentiation.

Competitors face an impossible challenge. To match Prologis' scale would require $50+ billion in acquisitions—in a market where Prologis is usually the highest bidder. To match its development capability would require decades of land accumulation—in markets where land is no longer available. To match its customer relationships would require serving thousands of tenants across hundreds of markets—when most tenants are already consolidating with Prologis.

This isn't just a competitive advantage. It's a complete transformation of industrial real estate from a fragmented, commoditized industry into a platform business with winner-take-most dynamics. And Prologis has already won.

IX. Playbook: Lessons in Platform Building

Lesson 1: Consolidate Fragmented Industries Through Patient Capital

In 2003, industrial real estate was radically fragmented. The top 10 owners controlled less than 5% of total space. Local developers dominated individual markets. Institutional capital avoided the sector, viewing warehouses as commodity assets with limited growth potential.

Moghadam and his predecessors at ProLogis saw opportunity in this fragmentation. Small operators couldn't serve multinational customers. Local developers couldn't access institutional capital. Regional players couldn't achieve economies of scale. The industry was ripe for consolidation—it just needed patient capital and operational excellence to execute.

The rollup strategy wasn't about financial engineering. It was about creating value through standardization and scale. Every acquired portfolio was upgraded to institutional standards. Lease agreements were standardized across markets. Property management was centralized. What had been thousands of local businesses became one global platform.

The lesson extends beyond real estate: fragmented industries with diverse customer needs, complex operations, and high switching costs are ideal for platform consolidation. But success requires patience. It took Prologis three decades to achieve decisive scale. Quick flips and financial engineering don't build lasting platforms.

Lesson 2: Position for Secular Trends Before They're Obvious

Moghadam's 1999 decision to sell AMB's retail portfolio to focus on industrial looked insane at the time. In 1999, years before e-commerce took off, he decided to sell off AMB's retail centers to double down on logistics. E-commerce was 0.5% of retail sales. Amazon was losing money. The dot-com bubble was about to burst. Yet Moghadam saw the inevitable: goods would increasingly flow directly from warehouses to consumers, bypassing stores entirely.

Similarly, ProLogis' expansion into Asia in the early 2000s preceded the China manufacturing boom. The push into urban infill markets happened before same-day delivery became competitive necessity. Investments in cold storage preceded the grocery e-commerce revolution.

Each bet required conviction to maintain when returns lagged. Urban infill properties took years to generate acceptable yields. Asian expansion required enormous upfront investment. But positioning for secular trends before they're consensus is how platforms achieve insurmountable leads.

The key insight: look for trends that are directionally certain even if timing is uncertain. E-commerce growth was inevitable—the only question was pace. Global trade expansion was unstoppable—the only uncertainty was which markets would boom first. When you identify these trends, move decisively and be prepared to look foolish for years.

Lesson 3: Transform Real Estate into Infrastructure

Traditional real estate companies are landlords. They lease space, collect rent, maintain properties. It's a simple business model that hasn't fundamentally changed in centuries. Prologis broke this model by recognizing that modern logistics requires infrastructure, not just buildings.

Infrastructure means providing power—hence the massive solar program. It means offering technology—hence Essentials and automation partnerships. It means ensuring reliability—hence the focus on operational excellence and 24/7 customer service. When customers view you as infrastructure rather than a landlord, pricing power follows.

The transformation required cultural change. Property managers became "customer experience officers." Leasing agents became "solutions consultants." Maintenance became "asset optimization." These weren't just title changes—they reflected fundamental shifts in how Prologis viewed its role.

The broader lesson: in industries being disrupted by technology, moving up the value chain from product provider to solution enabler creates defensibility. But it requires genuine capability building, not just marketing rhetoric.

Lesson 4: Master Capital Recycling to Accelerate Growth

Most capital-intensive businesses face a cruel dilemma: growth requires capital, but raising capital dilutes returns. Prologis solved this through innovative capital recycling that turned the balance sheet into a revolving credit facility.

The model is elegant: develop with balance sheet capital, sell stabilized assets to funds while maintaining control, redeploy proceeds into new development. Each dollar of equity generates multiple dollars of development over time. The fund investors get stable, yielding assets. Prologis gets development profits plus recurring management fees.

But execution is everything. This model only works with world-class operating capabilities—fund investors must trust you to manage their assets. It requires disciplined capital allocation—the temptation to overdevelop is strong. And it demands aligned incentives—Prologis co-invests significantly in every fund, ensuring skin in the game.

The lesson applies broadly: businesses that can separate asset ownership from asset control can achieve non-linear growth. But the separation must create genuine value for capital partners, not just financial engineering.

The Meta-Lesson: Compound Advantages

Each lesson reinforces the others. Consolidation creates scale for secular positioning. Infrastructure transformation justifies premium pricing that funds growth. Capital recycling accelerates consolidation. It's a flywheel that, once spinning, becomes nearly impossible to stop.

This is perhaps the most important lesson: sustainable competitive advantages rarely come from single innovations. They emerge from systems of reinforcing advantages that compound over time. Prologis didn't just build a bigger warehouse company—it built an entirely different business model where each element strengthens the others.

The playbook isn't easily copied. Competitors can't cherry-pick individual strategies—they need the entire system. And building that system requires decades of patient execution, billions in capital, and perhaps most importantly, the vision to see where an industry is heading long before it arrives there.

X. Bear vs. Bull Case & Future Outlook

The Bear Case: Storm Clouds Gathering

The skeptics have compelling arguments. E-commerce penetration in the U.S. has plateaued around 15-16% of retail sales after the pandemic surge. The explosive growth of 2020-2021, when companies would sign leases at any price, has normalized. Amazon, once desperate for space, is now subletting excess capacity. The fear: Prologis is a pandemic winner facing structural headwinds.

Interest rates pose another challenge. Prologis thrived in the zero-rate environment of 2010-2021, when 4% cap rates looked attractive versus 1% Treasury yields. With 10-year Treasuries now above 4%, the math has changed. Why accept 4.5% returns from industrial real estate when you can get 5% from risk-free government bonds? The sector's valuation premium has evaporated.

Oversupply concerns are mounting in certain markets. The development pipeline for U.S. industrial real estate reached 650 million square feet in 2023—the highest in history. Markets like Phoenix, Dallas, and Atlanta are seeing vacancy rates rise for the first time in years. The bear case: we're building for yesterday's demand surge, setting up a painful correction.

Technology disruption looms larger than most realize. 3D printing could eliminate entire categories of inventory. Autonomous delivery vehicles might make urban fulfillment centers obsolete—why pay premium rents when robots can deliver from cheap rural facilities? Artificial intelligence is already optimizing supply chains to require less physical space. Prologis' irreplaceable portfolio might become very replaceable.

The geopolitical environment adds another layer of risk. Reshoring and friend-shoring sound positive for U.S. industrial demand, but they really mean supply chain fragmentation. Instead of efficient global networks, we're building redundant regional systems. That's inflationary, inefficient, and ultimately negative for logistics demand.

Environmental regulations are tightening everywhere. California's warehouse moratoriums. European emissions restrictions. Community opposition to industrial development. The markets where Prologis has the strongest positions are precisely where new restrictions are most severe. Premium locations become liabilities when you can't develop or expand.

Finally, there's valuation. At $100+ billion market cap, Prologis trades at a significant premium to net asset value. The market is pricing in continued growth that might not materialize. One disappointment—a major tenant bankruptcy, a development project failure, a guidance miss—could trigger a painful revaluation.

The Bull Case: Structural Tailwinds Accelerating

The optimists see the e-commerce plateau as a pause, not a peak. E-commerce projected to reach 30% of goods sold by 2030. Prologis projects e-commerce reaching 30% of goods sold by 2030, implying massive future demand for logistics space. Every percentage point of e-commerce penetration requires 30-40 million square feet of additional warehouse space. The math is inexorable.

But the real demand driver isn't e-commerce—it's supply chain restructuring. Companies are maintaining higher inventory levels after pandemic shortages. Manufacturing is reshoring, requiring new distribution networks. B2B commerce is digitizing, demanding modern fulfillment infrastructure. These trends are in early innings.

The supply picture is far brighter than bears acknowledge. 140 million square feet supply deficit expected over next 5 years. Yes, 650 million square feet is under construction, but demand is absorbing space even faster. Prologis expects a 140 million square foot deficit over the next five years. More importantly, new supply is concentrated in secondary markets. In Prologis' core coastal markets, development remains nearly impossible.

The technology disruption argument misunderstands logistics reality. Automation doesn't eliminate warehouses—it makes them more essential. Modern fulfillment centers are really distributed manufacturing facilities, with customization, packaging, and value-added services. 3D printing and autonomous vehicles, if anything, increase logistics complexity.

Prologis' balance sheet has never been stronger. Leverage is at historic lows. Debt maturities are termed out. The company has $5+ billion in liquidity. While competitors struggle with refinancing, Prologis can play offense—acquiring distressed assets, funding development, investing in innovation.

The platform advantages are widening, not narrowing. Customer retention remains above 95%. Rent growth continues outpacing market averages. The Essentials business is scaling rapidly, deepening customer relationships and generating high-margin revenue. No competitor is even attempting to replicate Prologis' integrated model.

Sustainability is becoming a competitive advantage, not a burden. Prologis' solar capacity generates significant revenue. Green buildings command premium rents. ESG-focused institutional capital increasingly views Prologis as the only acceptable industrial investment. Environmental regulations that constrain supply benefit incumbents with irreplaceable portfolios.

The Next Chapter: Platform Evolution

The future likely lies between these extremes. E-commerce growth will continue but at sustainable rates. Supply and demand will rebalance through normal market mechanisms. Technology will transform operations without eliminating the need for physical infrastructure.

But the real story is Prologis' evolution beyond traditional real estate. The company is becoming a logistics technology platform that happens to own buildings. 10-20% productivity improvements from automation in next 3 years. Automation partnerships promise 10-20% productivity improvements over three years. Data analytics optimize customer operations. Energy infrastructure supports the electric vehicle transition.

The expansion into adjacent sectors is particularly intriguing. Data centers on excess land parcels. EV charging networks in parking lots. Urban logistics hubs that blur the line between warehouse and retail. Each expansion leverages Prologis' core advantage: irreplaceable locations near population centers and power infrastructure.

The succession planning adds another dimension. Moghadam, at 69, is preparing the next generation of leadership. The challenge: maintaining entrepreneurial culture while managing institutional scale. The opportunity: fresh perspective on technology integration and sustainability.

International expansion remains underpenetrated. Prologis has minimal presence in India, Southeast Asia, and Africa—markets where e-commerce and modern logistics are just beginning. The company's proven playbook for entering new markets could drive decades of growth.

The venture capital arm is quietly building option value. Prologis Ventures' portfolio includes potential unicorns in warehouse automation, last-mile delivery, and supply chain software. One breakout success could be worth billions while providing technology to enhance the core platform.

The Verdict: Irreplaceable Infrastructure

Step back from quarterly earnings and cap rate spreads. The fundamental question is: Can the modern economy function without Prologis' platform? The answer is increasingly no. 2.8% of world's GDP passing through Prologis warehouses. With 2.8% of global GDP flowing through its facilities, Prologis has become systemically important infrastructure.

The bear case requires multiple structural breaks: e-commerce reversal, supply chain simplification, technology disruption, and competitor emergence. Possible, but improbable. The bull case requires continuation of existing trends: digitization, urbanization, and supply chain evolution. Likely, if not certain.

The most probable outcome: Prologis continues compounding at high single-digit rates for years, with occasional volatility during economic cycles. Not the explosive growth of 2020-2021, but steady value creation from an irreplaceable platform. In a world of uncertainty, owning critical infrastructure with pricing power, diversified demand, and multiple growth vectors is a reasonable bet.

The transformation from warehouse landlord to logistics platform is complete. The question now is what Prologis becomes next: technology company, energy provider, or something entirely new. That evolution, more than any near-term market dynamics, will determine whether today's $100 billion valuation looks cheap or expensive in hindsight.

XI. Epilogue: Reflections & Legacy

The AWS of Physical Logistics

In Silicon Valley, entrepreneurs often describe their startups as "the Uber of X" or "the Amazon of Y." But perhaps the highest compliment in modern business is being called the "AWS of" your industry—Amazon Web Services being the gold standard for platforms that become essential infrastructure. Prologis has earned that distinction in physical logistics.

Like AWS, Prologis started by solving its own problem—managing real estate efficiently—then realized others would pay for that solution. Like AWS, it benefits from massive scale economies that make competition almost impossible. Like AWS, it generates predictable, recurring revenue from customers who can't easily leave. And like AWS, it enables entire industries while remaining largely invisible to end consumers.

The parallel extends to business model innovation. AWS transformed Amazon from a retailer into a technology platform. Prologis transformed from a landlord into a logistics enabler. Both generate extraordinary returns on invested capital by monetizing infrastructure in multiple ways: usage fees, service charges, and value-added offerings.

The Power of Patient Capital

If there's one thread connecting Prologis' four-decade journey, it's the power of patient capital combined with secular vision. Moghadam held his urban infill properties for years before they generated acceptable returns. The Asia expansion took a decade to prove profitable. The sustainability investments seemed like costly virtue signaling before becoming competitive advantages.

This patience wasn't passive waiting—it was active preparation for inevitable futures. Every cycle, competitors would leverage up, chase growth, then flame out when markets turned. Prologis would acquire their assets at distressed prices, emerging from each crisis stronger. The company played a different game with different time horizons.

The lesson challenges modern capitalism's quarterly obsession. True value creation—building irreplaceable infrastructure, developing new capabilities, transforming industries—takes decades, not quarters. Prologis succeeded because it had leaders with vision, investors with patience, and a culture that valued long-term positioning over short-term optimization.

Building Irreplaceable Assets in the Digital Economy

The great irony of Prologis is that the digital revolution made physical infrastructure more, not less, valuable. Every iPhone ordered online, every grocery delivery, every B2B transaction creates demand for logistics space. The virtual economy requires a vast physical substrate, and Prologis owns the chokepoints of that substrate.

But "irreplaceable" doesn't mean just scarce locations. It means embedded customer relationships where switching costs exceed switching benefits. It means operational excellence that competitors can't replicate. It means network effects where each additional customer makes the platform more valuable for all customers.

Prologis built irreplaceability through accumulation of advantages: the best locations, deepest customer relationships, most sophisticated operations, strongest balance sheet, and broadest capabilities. No single advantage was insurmountable, but their combination created a moat that widened with time.

What This Means for Cities and Commerce

Prologis' footprint reveals how fundamentally cities are restructuring around logistics. Former manufacturing districts become fulfillment centers. Abandoned malls transform into last-mile delivery hubs. Even underground parking garages are being converted to urban logistics nodes.

This transformation isn't just about e-commerce. It's about cities functioning as integrated logistics systems where goods flow continuously from ports to warehouses to homes. Prologis facilities are the arteries of this system, as essential as roads or power grids. The company doesn't just respond to urban evolution—it shapes it.

The implications extend globally. As developing nations build modern logistics infrastructure, they're essentially building the Prologis model: institutional-quality facilities, strategic locations, integrated technology. The template developed in California is being replicated in Cairo, Chennai, and Chengdu.

The Hamid Moghadam Legacy

When Hamid Moghadam retires—likely within the next few years—he'll leave behind more than a $100 billion company. He'll leave a transformed industry and a new model for how real estate companies create value. The MIT engineer who couldn't get hired in 1982 built one of the most successful real estate platforms in history.

But Moghadam's greatest contribution might be philosophical. He proved that real estate, often seen as a slow, stable, yield-focused sector, could be dynamic, innovative, and growth-oriented. He showed that operational excellence matters more than financial engineering. He demonstrated that betting on secular trends, even when they take decades to materialize, creates extraordinary value.

His approach—analytical yet intuitive, patient yet aggressive, global yet detailed—became the Prologis culture. The company recruits engineers and data scientists alongside traditional real estate professionals. It measures success in decades, not quarters. It views customers as partners, not tenants.

The Future of Commerce and Logistics

Prologis' evolution from warehouse owner to logistics platform to infrastructure provider suggests where commerce itself is heading. The boundaries between physical and digital, retail and industrial, real estate and technology are dissolving. Future winners will be platforms that seamlessly integrate across these traditional boundaries.

Consider what Prologis might become: A company that not only houses goods but tracks them through the supply chain. That not only provides space but optimizes its usage through AI. That not only enables commerce but shapes how commerce evolves. The warehouses are just the beginning—the data, relationships, and capabilities matter more.

The next decade will bring new challenges. Climate change will disrupt supply chains and force infrastructure adaptation. Automation will transform labor markets and facility requirements. Geopolitical tensions will reshape global trade patterns. But each challenge is also an opportunity for a platform with Prologis' scale, capabilities, and ambition.

Final Reflections

The Prologis story is ultimately about transformation—of an industry, a business model, and our understanding of what creates value in the modern economy. Two competing warehouse REITs merged to create something neither could have imagined: essential infrastructure for global commerce.

The company that emerged from rejection letters and near-bankruptcy now facilitates $2.7 trillion in annual commerce. The warehouses once seen as commodity assets now command premium valuations. The industry once ignored by institutional capital now attracts the world's most sophisticated investors.

For investors, Prologis offers a lesson in compound value creation. For entrepreneurs, it demonstrates the power of patient platform building. For society, it shows how invisible infrastructure enables visible prosperity. And for anyone who's ever received 80 rejection letters, it proves that persistence, vision, and a bit of luck can transform industries and build legacies.

The boxes might be boring, but the business model is beautiful. In an economy increasingly defined by speed, complexity, and change, Prologis built the stable foundation that makes it all possible. That's not just a business success—it's a fundamental contribution to how the modern world works.

XII. Recent News### **

Latest Quarterly Earnings and Performance**

Prologis reported strong Q4 2024 results on January 21, 2025, with net earnings per diluted share of $1.37, up 101.5% year-over-year. Core funds from operations per share reached $1.50, increasing 19.0%, while Core FFO excluding net promote income per share was $1.42, up 10.1%. For the full year 2024, net earnings per diluted share was $4.01, up 21.9%, though Core FFO per share of $5.56 decreased 0.9% year-over-year. Core FFO excluding net promote income per share was $5.53, up 8.4%.

The company demonstrated robust operational metrics in Q3 2024, with period-ending occupancy at 96.2%, net effective rent change of 68%, and cash rent change of 44%. Lease mark-to-market stood at 34%, representing $1.6 billion of potential NOI, highlighting significant embedded growth potential in the portfolio.

Leadership Transition Announcement

In a carefully orchestrated transition, Prologis announced on February 19, 2025, the retirement of co-founder Hamid R. Moghadam from his CEO role, effective January 1, 2026. After more than four decades of visionary leadership, Moghadam will continue as executive chairman. Dan Letter, currently president, will succeed Moghadam as CEO.

Letter, who has been with Prologis since 2004, is well prepared to lead the company with deep industry experience and a leadership style rooted in collaboration and innovation. Letter joined the company's Board of Directors effective immediately upon the announcement. Moghadam noted that Letter currently oversees the majority of Prologis' business lines, including global real estate operations, capital deployment, strategic capital and Prologis Essentials, having played a key role in the company's tremendous growth.

Development and Capital Markets Activity

The company maintained disciplined capital deployment in 2024, with development projects started exceeding $0.5 billion and third-party acquisitions surpassing $1.4 billion in Q3 alone. Prologis raised $4.6 billion in new debt at a weighted average rate of 4.6%, demonstrating continued access to attractive financing despite higher interest rates.

A significant highlight was the sale of the Elk Grove data center—a turnkey facility under development—that led to significant value creation and demonstrated the end-to-end capabilities of Prologis' platform expansion beyond traditional logistics.

Market Dynamics and Outlook

The company provided measured guidance for 2025, with average occupancy expected between 96% to 96.5%, cash same-store growth of 6.5% to 7%, and net effective same-store growth of 5.5% to 6%. Management acknowledged near-term headwinds, particularly in Southern California markets, but remained confident in long-term fundamentals.

Strategic Initiatives and Innovation

The company started 54 megawatts of new energy systems in Q3, accelerating its sustainability initiatives and creating additional revenue streams. Prologis Ventures had a successful exit from an investment in Timee, realizing a 65% IRR, validating the venture capital strategy launched in 2016.

Industry Recognition and Market Position

As of June 30, 2025, Prologis manages $205 billion in assets, generates $6.4 billion in revenue, operates 1.3 billion square feet across 5,895 properties in 20 countries, serving 6,500 customers. The company maintains A/A2 credit ratings and ranks #106 on the S&P 500 with 96.0% occupancy.

The leadership transition represents a watershed moment for Prologis, marking the end of Moghadam's extraordinary 42-year journey from struggling immigrant to CEO of one of the world's most valuable real estate companies. Letter's appointment ensures continuity while bringing fresh perspective to navigate evolving logistics landscapes, technological disruption, and sustainability imperatives.

XIII. Links & Resources

Key SEC Filings and Investor Materials

- Prologis Investor Relations Portal

- Q4 2024 Earnings Release and Supplemental

- 2024 Annual Report (10-K)

- Proxy Statement and Executive Compensation

Industry Reports and Research

- CBRE Global Industrial & Logistics Market Outlook

- JLL Global Logistics Report Series

- Cushman & Wakefield Industrial Market Beat Reports

- Green Street Industrial REIT Sector Analysis

- Morgan Stanley "The Future of Logistics Real Estate" Research Series

Books on Real Estate and Logistics Transformation

- "The Box: How the Shipping Container Made the World Smaller" by Marc Levinson

- "Real Estate Investment Trusts: Structure, Performance, and Investment Opportunities" by Su Han Chan

- "The Everything Store: Jeff Bezos and the Age of Amazon" by Brad Stone (for e-commerce context)

- "Supply Chain Revolution" by Joseph Fratocchi

- "The Warehouse: Workers and Robots at Amazon" by Alessandro Delfanti

Academic Studies and White Papers

- MIT Center for Transportation & Logistics Research Papers

- Stanford Graduate School of Business Case Studies on Prologis

- Harvard Business Review: "The Rise of Logistics Real Estate as Infrastructure"

- Wharton Real Estate Review: "REITs and the Institutionalization of Real Estate"

- Urban Land Institute: "E-Commerce and Industrial Real Estate Demand"

Podcasts and Media

- Walker Webcast episodes featuring Hamid Moghadam

- REIT Report Podcast industrial sector coverage

- The Real Estate Guys Radio Show REIT episodes

- Nareit Podcast Network industrial REIT discussions

- Bloomberg Odd Lots episodes on supply chain and logistics

Industry Organizations and Data Sources

- National Association of Real Estate Investment Trusts (Nareit)

- Industrial Asset Management Council

- Supply Chain Management Review

- Council of Supply Chain Management Professionals

- Urban Land Institute Industrial Development Council

Prologis Corporate Resources

- Prologis Research Reports

- Prologis Essentials Platform

- Prologis Ventures Portfolio

- Sustainability Reports and ESG Data

- Company History Timeline

Competitor Analysis Resources

- Company filings for key competitors: Blackstone (BX), Clarion Partners, GLP

- Industrial REIT comparisons: Duke Realty (acquired), DCT Industrial (acquired), First Industrial (FR)

- CoStar Analytics industrial market reports

- Real Capital Analytics transaction databases

Technology and Innovation Resources

- Prologis Labs innovation reports

- McKinsey Global Institute: "Automation in Logistics"