Packaging Corporation of America: From Post-War Consolidation to Corrugated Dominance

I. Introduction & Episode Setup

Picture this: Every single day, 95% of all products in America touch corrugated cardboard. That Amazon package on your doorstep? The boxes stacked in every Costco aisle? The protective packaging around your new iPhone? Behind this ubiquitous brown material sits an industry giant most investors have never heard of—Packaging Corporation of America, a $17 billion market cap company that generated $8.38 billion in revenue in 2024.

Here's what's fascinating: PKG isn't sexy. It doesn't have the brand recognition of Apple or the growth story of Tesla. It makes boxes. Brown, corrugated boxes. Yet since its modern reincarnation in 2000, the stock has delivered a staggering 1,785% return, crushing the S&P 500. How did a 1959 roll-up of regional box makers transform into one of North America's packaging behemoths?

The answer involves a cast of characters straight out of industrial America's playbook: post-war consolidators betting on suburban expansion, conglomerate builders of the go-go 1960s, private equity operators who saw gold in an unloved asset, and modern executives who recognized that e-commerce would fundamentally reshape demand for their product. It's a story about finding extraordinary value in the most ordinary of businesses.

In an era where investors chase the latest AI startup or biotech moonshot, PKG represents something different—the relentless compounding machine hiding in plain sight. This is the story of how three Depression-era box companies became the supplier powering the e-commerce revolution, and why the most boring businesses often make the best investments.

II. The Origins: Three Companies Become One (1903-1959)

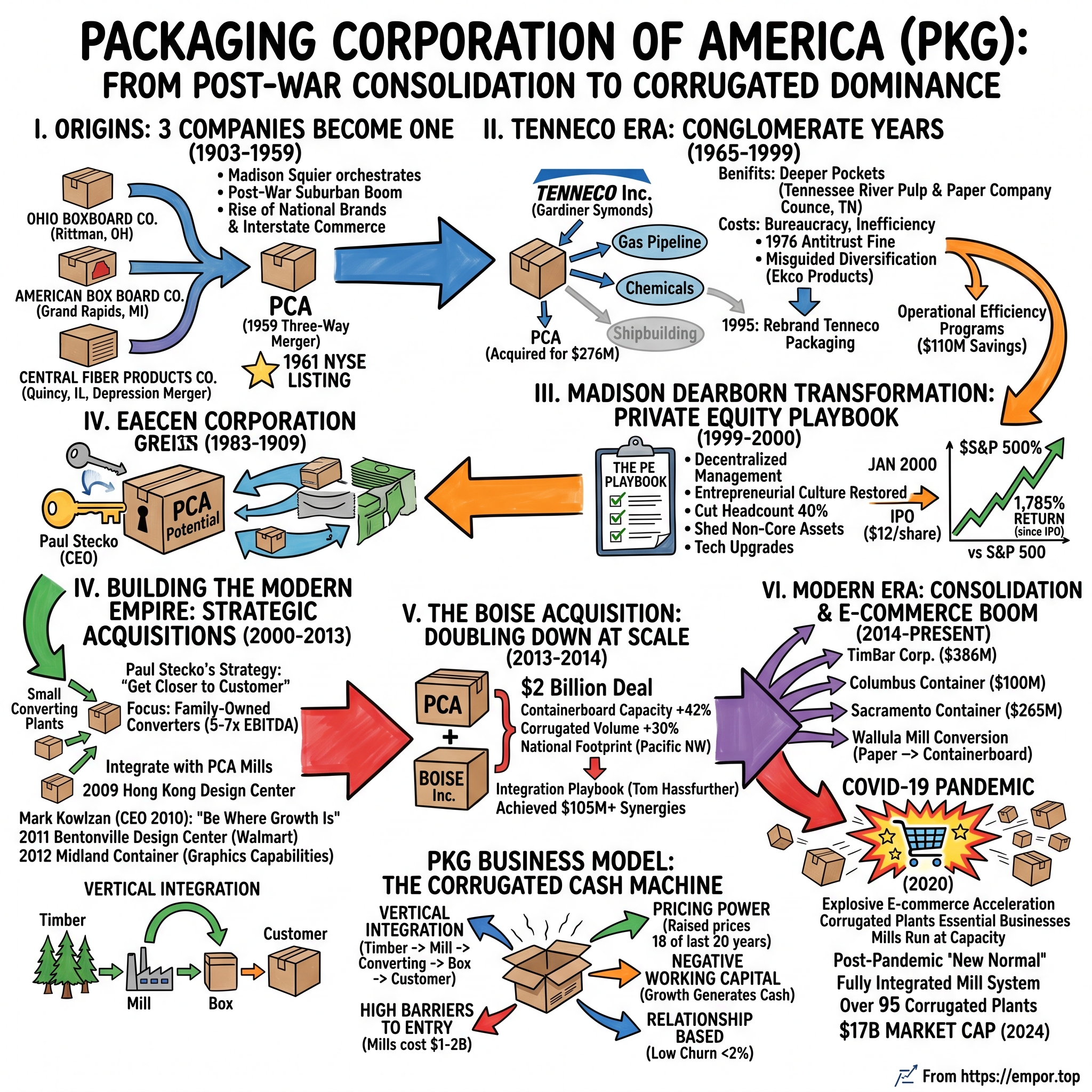

The year was 1903. Theodore Roosevelt occupied the White House, the Wright Brothers achieved first flight at Kitty Hawk, and in the industrial heartland of America, two entrepreneurs simultaneously recognized that the country's booming manufacturing sector needed something basic: boxes. In Rittman, Ohio, the Ohio Boxboard Company opened its doors, while 500 miles away in Grand Rapids, Michigan, the American Paper Box Company (later renamed American Box Board Company) began operations.

These weren't glamorous businesses. Workers fed recycled paper and straw into massive machines that pressed, heated, and formed the materials into rigid boxboard. The air hung thick with paper dust and the acrid smell of adhesives. Profit margins were thin, competition brutal. But both companies possessed something critical: they understood their regional markets intimately. Ohio Boxboard dominated shipments to Cleveland's steel mills and Akron's tire factories. American Box Board captured the furniture manufacturers of Grand Rapids, earning the nickname "Furniture City's packaging partner."

The third piece of the puzzle emerged during the depths of the Great Depression. In 1931, as banks failed and unemployment soared past 15%, a group of Illinois businessmen saw opportunity in chaos. They merged five struggling packaging firms—North Star Mill, North Star Egg Case Company, Carey Straw Mill, H.T. Cherry Company, and Indiana Board and Filler Company—into Central Fiber Products Company, based in Quincy, Illinois. The logic was simple: combine to survive. Share equipment, eliminate duplicate routes, pool customer relationships. It was financial engineering before the term existed.

By the 1950s, these three companies had survived two world wars, the Depression, and countless economic cycles. But they faced a new challenge: the rise of national brands and interstate commerce demanded scale they couldn't achieve alone. Procter & Gamble didn't want to negotiate with dozens of regional box suppliers. The new supermarket chains needed consistent packaging specifications across hundreds of stores.

Enter Madison Squier, a Wall Street dealmaker who recognized that American industry was ripe for consolidation. In 1959, he orchestrated the three-way merger that created Packaging Corporation of America. The combined entity instantly commanded significant market share in containerboard and corrugated products, with 39 plants across 16 states. Wall Street took notice—by 1961, PCA listed on the New York Stock Exchange, sporting a market cap that made it one of the 500 largest public companies in America.

But the real genius of the merger wasn't just scale—it was timing. The post-war suburban boom was accelerating. Every new Levittown house needed appliances, and every appliance needed packaging. Consumer goods companies were launching new products at unprecedented rates. The interstate highway system, still under construction, would soon make national distribution networks possible. PCA wasn't just consolidating the past; it was positioning for a future where packaging would become critical infrastructure for the American economy.

III. The Tenneco Era: Corporate Conglomerate Years (1965-1999)

In 1965, Gardiner Symonds, the legendary CEO of Tennessee Gas Transmission Corporation (later Tenneco Inc.), sat in his Houston office studying acquisition targets. Symonds had built Tenneco from a simple pipeline company into a sprawling conglomerate through relentless deal-making. His philosophy was simple: buy cash-flowing industrial businesses, leverage Tenneco's AAA credit rating to fund expansion, and create a diversified empire immune to sector-specific downturns. When PCA appeared on his radar—steady cash flows, dominant market position, unsexy enough to avoid bidding wars—he pounced, acquiring the company for $276 million.

Life inside the Tenneco empire was a study in corporate contradiction. On one hand, PCA benefited enormously from its parent's deep pockets. Production began at the Tennessee River Pulp & Paper Company in Counce, Tennessee, with PCA holding a majority interest—a $150 million investment that would have been impossible as a standalone company. By 1970, PCA gained full ownership of this critical asset, vertically integrating into virgin fiber production and reducing dependence on recycled materials.

Yet the conglomerate structure also bred inefficiency. Decisions that should have taken days required months of corporate approval. PCA executives found themselves in endless Houston meetings defending capital expenditures to Tenneco brass who knew oil and chemicals but not containerboard. The company's entrepreneurial spirit, forged in those scrappy Ohio and Michigan mills, slowly calcified under layers of corporate bureaucracy.

The 1970s brought a stark reminder that size doesn't guarantee immunity from legal scrutiny. In 1976, a federal grand jury found PCA guilty of violating antitrust laws, part of a broader price-fixing investigation that ensnared multiple packaging companies. The resulting fines and reputation damage forced a cultural reckoning—PCA needed to compete on operational excellence, not market manipulation.

The 1980s diversification wave swept up PCA like everyone else. In 1984, the company acquired Ekco Products Inc., a housewares manufacturer, in a bizarre attempt to become a "total consumer products packaging and products company." The logic—we make boxes, why not make what goes in them?—proved laughably flawed. By decade's end, Ekco was quietly divested at a loss.

Real change came in 1995 when Tenneco, facing its own pressures, renamed PCA as Tenneco Packaging and brought in new leadership obsessed with operational efficiency. They launched a "cost of quality" program that sounds mundane but revolutionized the business. Between 1997 and 1999, the initiative slashed $80 million from mill operations and $30 million from converting costs. They attacked everything: reducing paper breaks through better maintenance, optimizing truck routes with early GPS systems, eliminating quality defects that required costly rework.

By 1999, Tenneco itself was unraveling, planning to split into multiple companies. PCA's fate hung in the balance. Industry observers assumed Georgia-Pacific, the forest products giant, would swoop in to buy Tenneco's containerboard assets. Instead, something unexpected happened—a Chicago private equity firm nobody in the packaging industry had heard of emerged with a $2.2 billion offer that would resurrect the Packaging Corporation of America name and set the stage for one of industrial America's great second acts.

IV. The Madison Dearborn Transformation: Private Equity Playbook (1999-2000)

The announcement hit the packaging industry like a thunderbolt. On April 12, 1999, Madison Dearborn Partners—a Chicago private equity firm better known for buying Cintas uniforms and PayPal's predecessor—agreed to acquire Tenneco's containerboard and corrugated packaging business for $2.2 billion. Industry executives were stunned. "Who the hell is Madison Dearborn?" became the question echoing through converting plants from Wisconsin to Tennessee.

John Canning Jr., Madison Dearborn's managing director, saw what others missed. While Wall Street obsessed over dot-coms, Canning recognized that e-commerce would require massive amounts of corrugated packaging. Every online order meant a box. Every box meant containerboard. The math was simple, the opportunity enormous. But first, they needed to execute one of private equity's most ambitious operational turnarounds.

The key to Madison Dearborn's strategy was Paul Stecko, a Tenneco packaging veteran who understood the business's potential better than anyone. Stecko wasn't a financial engineer—he was an operations guy who'd spent decades in mills, understanding the rhythm of paper machines and the economics of converting plants. Madison Dearborn made him CEO and gave him unprecedented autonomy. His mandate: strip away Tenneco's bureaucracy, restore entrepreneurial culture, and prepare for an IPO within 18 months.

Stecko moved fast. The new entity, formally reestablished as Packaging Corporation of America in August 1999, immediately shed non-core assets. Unprofitable plants were closed. Headquarters staff was slashed by 40%. The savings were reinvested into technology upgrades at core facilities. Most critically, Stecko implemented a decentralized management structure where plant managers could make decisions without corporate approval for investments under $500,000—revolutionary after decades of Tenneco's command-and-control culture.

The transformation's speed was breathtaking. In January 2000, just five months after closing the acquisition, PCA went public on the NYSE at $12 per share, raising $445 million. The IPO valued the company at $1.14 billion—Madison Dearborn had already nearly recouped its entire investment while maintaining majority control. Wall Street analysts who'd dismissed the deal as "private equity trying to flip a commodity business" suddenly recognized the genius: Madison Dearborn had bought a cash-flowing industrial asset at a conglomerate discount, cleaned it up, and sold it into a market hungry for "picks and shovels" plays on the internet boom.

The numbers tell the story. Since that January 28, 2000 IPO, PKG's market cap has exploded from $1.14 billion to $21.40 billion—an increase of 1,785%. Madison Dearborn's remaining stake, gradually sold over the following years, generated returns exceeding 10x. But the real winner was Stecko's vision: PCA was now a focused, efficient, publicly-traded pure-play on containerboard with the flexibility to pursue growth. The stage was set for empire building.

V. Building the Modern Empire: Strategic Acquisitions (2000-2013)

Paul Stecko stood before PCA's board in 2003 with an unusual proposal. While competitors chased mega-mergers, he wanted to buy small converting plants—facilities that took PCA's containerboard and transformed it into custom boxes for local customers. "We're not going to win by being biggest," he argued. "We'll win by being closest to the customer." The board approved, launching a thirteen-year acquisition spree that would fundamentally reshape PCA's competitive position.

The strategy was deceptively simple. Target family-owned converting operations with strong local relationships but lacking capital for expansion. Pay fair prices—typically 5-7x EBITDA. Integrate them into PCA's supply chain, providing cheaper containerboard from PCA's mills. Keep local management in place, maintaining customer relationships while upgrading equipment. Rinse and repeat.

By 2009, as the financial crisis crushed demand and competitors retrenched, PCA zagged internationally. The company opened a design center in Hong Kong operating as Packaging Corporation of Asia Limited—not to manufacture, but to help American customers manage Asian supply chains. The insight was brilliant: American companies importing from China needed packaging expertise at the source. PCA's Hong Kong team designed packaging solutions that minimized damage during trans-Pacific shipping while reducing costs. Within two years, the operation was managing packaging for over $2 billion in imported goods.

The real acceleration came in 2010 when Mark Kowlzan replaced the retiring Stecko as CEO. Kowlzan, a chemical engineer who'd run PCA's mill operations, brought a different philosophy: "We need to be where the growth is." That meant two things: e-commerce and the American South.

In 2011, PCA opened a creative design center in Bentonville, Arkansas—Walmart's backyard. The message was clear: PCA wanted to be the retail giant's primary packaging innovation partner. That same year, they acquired Acorn Corrugated Box Company in Bedford Park, Illinois, adding crucial capacity in the Chicago logistics hub. The Acorn deal showcased PCA's integration playbook: within six months, Acorn's operating margins improved by 400 basis points as PCA's containerboard replaced expensive third-party supplies.

The 2012 acquisition of Midland Container Corporation represented a strategic evolution. Midland brought two facilities: a full-line corrugated plant in Pearl, Mississippi, and a graphics packaging facility in Olive Branch. The graphics capability was crucial—e-commerce companies wanted boxes that doubled as marketing vehicles. Amazon's smile boxes, subscription services' unboxing experiences—these required sophisticated printing capabilities PCA historically lacked.

Throughout this period, PCA's financial performance validated the strategy. EBITDA margins expanded from 14% in 2000 to over 20% by 2013. Return on invested capital consistently exceeded 15%. The stock price tripled. Yet Kowlzan wasn't satisfied. In late 2013, he began negotiations for PCA's largest acquisition ever—a deal that would either establish PCA as an industry titan or saddle it with dangerous leverage just as e-commerce competition intensified.

VI. The Boise Acquisition: Doubling Down at Scale (2013-2014)

Mark Kowlzan's phone rang at 6 AM on a October morning in 2013. On the line was Alex Toeldte, Boise Inc.'s CEO, with a simple message: "We're ready to talk." For three years, Kowlzan had courted Boise, a $2 billion revenue packaging company struggling with debt from its own 2008 leveraged buyout. Now, with Boise's private equity owners seeking an exit and debt markets finally receptive, the window was open.

The stakes were enormous. PCA would pay $2 billion—$12.55 per share in cash plus assumption of $714 million in debt—for a company nearly its own size. The acquisition would increase PCA's containerboard capacity by 42% to 3.7 million tons and expand corrugated products volume by 30%. More critically, it would give PCA a major presence in the Pacific Northwest through Boise's mills in Washington and Oregon, completing PCA's national footprint.

Wall Street was skeptical. "They're betting the company on a commodity cycle," warned one analyst. The containerboard market was notoriously cyclical, and PCA was leveraging up just as new capacity threatened to flood the market. The debt-to-EBITDA ratio would spike from 1.2x to 3.5x. If containerboard prices collapsed, PCA could face distress.

Kowlzan's response revealed deep strategic thinking. "This isn't about commodity speculation," he told investors. "It's about cost position and integration." He laid out the math: Boise's mills were running at 85% capacity. PCA could push that to 95% through its superior sales network. Boise was buying 30% of its containerboard needs from third parties at premium prices. PCA would internalize that volume. Transportation costs would plummet as PCA could now serve West Coast customers from local mills instead of shipping from the Midwest.

The projected synergies were eye-popping: $105 million in annual pre-tax benefits within three years. But execution would be everything. PCA assembled a 100-person integration team led by Tom Hassfurther, who'd run the successful Acorn integration. They developed a minute-by-minute playbook for the first 100 days post-close. Every Boise plant would be visited within 48 hours. Every customer would receive a call within a week. Every employee would know their role within a month.

The October 2013 closing revealed immediate challenges. Boise's IT systems were a decade old. Several mills needed emergency maintenance that Boise had deferred. Customer contracts were a mess of handshake deals and informal arrangements. But there were pleasant surprises too. Boise's Pacific Northwest mill network was more efficient than PCA expected. The employees, relieved to escape private equity ownership, embraced PCA's operational culture.

By mid-2014, the integration was ahead of schedule. Synergies reached $40 million in year one, with line of sight to exceeding the $105 million target. The debt markets, impressed by execution, allowed PCA to refinance at lower rates. The stock price, which had dropped 8% on the acquisition announcement, surged to new highs. Kowlzan's bet had paid off spectacularly—PCA was now the third-largest containerboard producer in North America, with the scale to compete with International Paper and WestRock while maintaining the operational discipline of a much smaller company.

VII. Modern Era: Consolidation & E-Commerce Boom (2014-Present)

The year 2016 marked an inflection point in Mark Kowlzan's strategy for PCA. Within months, the company announced two major acquisitions: TimBar Corporation for $386 million and Columbus Container for $100 million. The TimBar deal was particularly transformative. With sales of $324 million in 2015, TimBar brought expertise in higher-margin retail, industrial packaging, and display markets with a focus on multi-color graphics and technical innovation. The acquisition included five corrugated products plants, two fulfillment centers, and four design centers located primarily in the eastern and southeastern U.S.

Tom Hassfurther, who'd orchestrated the Boise integration, saw the strategic logic immediately. "The highly-skilled employees, culture and customer base of TimBar complements PCA extremely well and allows us to apply our operating and sales expertise across a larger system providing significant growth potential", he explained. The Columbus Container acquisition, though smaller, filled critical gaps in the Midwest, adding a full-line corrugated products facility in Columbus, Indiana, and five warehousing facilities in Illinois.

The 2017 Sacramento Container acquisition represented another evolution in PCA's thinking. For $265 million in cash, PCA acquired operations that would include full-line plants in McClellan and Kingsburg, California. But Kowlzan coupled this with a bold manufacturing play: discontinuing production of uncoated freesheet and coated one-side grades at the Wallula, Washington mill to begin converting its 200,000 ton-per-year No. 3 paper machine to a 400,000 ton-per-year virgin kraft linerboard machine.

The strategy was surgical: exit the declining paper business while doubling down on containerboard to feed the acquired converting operations. "At our current containerboard integration rate of 95%, the low-cost conversion of the No. 3 paper machine at our Wallula Mill provides us with much needed linerboard capacity, allows us to integrate over 200,000 tons of containerboard to our Sacramento Container acquisition", Kowlzan explained.

By 2018, the acquisition machine kept rolling with the purchase of Englander dZignPak, bringing sheet plants in Texas and additional design capabilities. The company acquired sheet plants located in Carrollton and Waco, Texas, and a design center in Bentonville, Arkansas. Each deal followed the same playbook: buy regional converters with strong customer relationships, integrate them with PCA's low-cost containerboard, capture immediate margin expansion.

Then came COVID-19 in March 2020—and everything changed. Overnight, e-commerce shifted from steady growth to explosive acceleration. E-commerce sales increased by $244.2 billion or 43% in 2020, rising from $571.2 billion in 2019 to $815.4 billion. As lockdowns became the new normal, e-commerce's share of global retail trade jumped from 14% in 2019 to about 17% in 2020.

For PCA, this wasn't a crisis—it was the moment they'd been preparing for. Every Amazon order needed a box. Every grocery delivery required packaging. Every work-from-home setup meant monitors, keyboards, and office supplies shipped in corrugated containers. The company's mills ran at capacity. Pricing power, always cyclical in containerboard, suddenly became structural as demand outstripped supply.

The numbers were staggering. From March 2020 through February 2022, U.S. consumers spent $1.7 trillion online, $609 billion more than the two preceding years combined. While other industries struggled with lockdowns and restrictions, PCA's corrugated plants operated as essential businesses, churning out the infrastructure of the pandemic economy.

But Kowlzan recognized that COVID acceleration would eventually moderate. The online share of total spending rose from 10.3% in 2019 to 14.9% at the pandemic peak, but fell to 12.2% by 2021. The key was positioning for the new normal—elevated but not explosive e-commerce penetration, combined with continued growth in industrial production and food packaging.

The modern PCA that emerged from the pandemic was a different animal than the company Madison Dearborn had carved out of Tenneco two decades earlier. With over 95 corrugated products plants and a fully integrated mill system, PCA had become the backbone of American commerce—unglamorous, essential, and enormously profitable. The company that started as three Depression-era box makers had evolved into a $17 billion market cap giant, proof that in business, boring can be beautiful.

VIII. Business Model Deep Dive: The Corrugated Cash Machine

Inside PCA's Valdosta, Georgia mill, a massive paper machine—longer than a football field and three stories tall—transforms wood chips and recycled cardboard into containerboard at 60 miles per hour. The machine runs 24/7, stopping only for scheduled maintenance every few weeks. Each ton of containerboard costs roughly $350 to produce. By the time it's converted into boxes and delivered to customers, that ton generates $800 in revenue. This is the engine of PCA's cash machine: turning trees and trash into the infrastructure of commerce at 40% gross margins.

The brilliance of PCA's business model lies in its vertical integration. The company controls the entire value chain from timber procurement through box delivery. Start with the mills: PCA operates six containerboard mills strategically located near both fiber sources and major logistics hubs. These aren't just factories; they're fortresses. Building a new containerboard mill costs $1-2 billion and takes 3-4 years. Environmental permits alone can take a decade. Once operational, a mill becomes nearly impossible to replicate—the ultimate barrier to entry.

The economics are compelling. Containerboard manufacturing is a high-fixed-cost, low-variable-cost business. Once a mill covers its overhead—roughly 85% capacity utilization—every additional ton drops almost directly to the bottom line. PCA runs its mills at 95%+ utilization, squeezing maximum profitability from every machine. During strong markets, the company can push prices up 10-15% annually. During downturns, volume might drop 5%, but the integrated model provides cushion.

Here's what most investors miss: containerboard isn't really a commodity. Yes, the physical product is standardized, but the business is about relationships and reliability. When Walmart needs 50 million boxes for Black Friday, they can't risk a supplier failing. When a food processor ships perishables across country, box failure means destroyed inventory and angry customers. PCA has supplied many of its largest customers for decades. Switching costs aren't just economic—they're existential.

The converting operations amplify this stickiness. PCA's 95+ box plants sit within 150 miles of most major U.S. businesses. Each plant is a custom shop, designing boxes for specific products, printing graphics, managing just-in-time inventory. A typical plant serves 100-200 local customers with 500+ unique box specifications. The plant manager knows every customer's loading dock supervisor by name. This isn't a commodity transaction—it's embedded infrastructure.

The capital allocation philosophy reflects operational discipline. PCA spends roughly $400 million annually on capital expenditures, mostly on maintenance and incremental capacity expansion. No moonshots, no transformational technology bets. Just steady reinvestment at 20%+ returns. The company targets 15%+ ROIC and has exceeded it for 15 consecutive years. Free cash flow conversion runs at 60-70% of EBITDA, funding both growth investments and shareholder returns.

Pricing power is the secret weapon. Unlike most industrial companies, PCA can push through price increases even during recessions. The reason is simple math: packaging represents 1-2% of most products' total cost but prevents 100% loss if the product is damaged. No purchasing manager gets fired for paying 5% more for boxes. They absolutely get fired if production stops because boxes don't arrive. This dynamic gives PCA unusual pricing leverage—the company has raised prices in 18 of the last 20 years.

The cycle management is masterful. Containerboard is cyclical, but PCA has learned to surf the waves rather than fight them. During upturns, the company maximizes price over volume, pushing increases aggressively. During downturns, it focuses on cost reduction and market share gains from subscale competitors. The integrated model provides natural hedging—when containerboard prices fall, input costs for the converting plants decrease, protecting overall margins.

Working capital management adds another lever. PCA turns inventory every 30 days and collects receivables in 45 days while stretching payables to 60 days. This negative working capital cycle means growth actually generates cash rather than consuming it. During the e-commerce boom, PCA funded massive volume increases without external capital, a self-financing growth machine.

The customer concentration is surprisingly balanced. The largest customer represents less than 10% of revenue. The top 10 customers combined are under 35%. This diversification provides stability—losing any single customer won't crater the business. Yet relationships are so embedded that customer churn runs under 2% annually, providing predictable, recurring revenue streams.

Operating leverage multiplies returns during growth periods. When volume increases 5%, revenue might grow 8% (including price), but EBITDA can surge 15%. The fixed-cost base—mills, converting plants, logistics networks—scales beautifully. Incremental margins approach 50%. This leverage explains why PCA's stock price is so sensitive to volume expectations. A 2% beat on volume can drive 10% earnings surprise.

The return on incrementally invested capital tells the real story. For every dollar PCA invests in new converting capacity or mill upgrades, it generates $0.25-0.30 in additional EBITDA—a 3-4 year payback. But here's the kicker: that asset lasts 20-30 years. The long-term returns on capital approach 30%, though accounting depreciation obscures this reality. PCA is essentially a collection of 20-30% ROI projects wrapped in a boring brown box.

IX. Playbook: Lessons from PKG's Journey

The art of industry consolidation, as executed by PCA, reads like a masterclass in strategic patience. While competitors pursued splashy mega-mergers, PCA methodically acquired small, family-owned converting operations at 5-7x EBITDA. The genius wasn't in any single deal but in the cumulative effect. Each acquisition added 50-100 basis points of market share, deepened customer relationships, and immediately benefited from PCA's low-cost containerboard. Over 20 years, these tuck-ins transformed PCA from a regional player to a national powerhouse without the integration nightmares that plagued larger deals.

Madison Dearborn's 1999-2000 transformation of PCA remains a private equity case study in operational value creation. They didn't financially engineer their way to returns through leverage and multiple expansion. Instead, they installed an operator CEO, stripped away bureaucracy, and created a performance culture. The playbook was straightforward: buy an underloved industrial asset trapped in a conglomerate, give management autonomy and incentives, clean up operations, and sell into public markets hungry for pure-plays. The 10x return wasn't luck—it was execution.

Timing commodity cycles requires a contrarian mindset, and PCA has mastered this dark art. The company's biggest capacity additions—the Boise acquisition, the Wallula conversion—came when containerboard markets were soft and competitors retreated. By the time demand recovered, PCA had the low-cost capacity to capture outsized profits. The key insight: in commodity businesses, you make money by investing at the bottom, not the top. Most managers can't stomach buying when prices are falling. PCA's leadership has trained themselves to see downturns as opportunities.

Building a moat in an "unsexy" industry might be PCA's greatest achievement. Corrugated boxes are the antithesis of Silicon Valley disruption—no network effects, no software margins, no viral growth. Yet PCA has created defensibility through density. With 95+ plants within trucking distance of most U.S. businesses, competitors can't economically serve PCA's customers without massive infrastructure investment. The moat isn't technology or brand—it's physical presence and relationship capital accumulated over decades.

The power of being a supplier to e-commerce winners became obvious during COVID, but PCA positioned for this trend years earlier. The company didn't need to predict which e-commerce players would win. Whether Amazon, Walmart, or Shopify dominated, they all needed boxes. PCA's strategy was to be the arms dealer in the e-commerce wars—selling to all sides while avoiding the brutal competition of retail itself. This strategic positioning explains why PCA captured e-commerce upside without technology risk.

Managing through multiple ownership structures—public company, conglomerate subsidiary, private equity portfolio company, public company again—taught PCA organizational resilience. Each structure brought different pressures and opportunities. Tenneco provided capital but stifled innovation. Private equity demanded performance but enabled autonomy. Public markets require transparency but provide permanent capital. PCA learned to extract value from each model while maintaining operational continuity. The company's culture survived and strengthened through each transition.

The discipline of saying no might be PCA's most underappreciated skill. The company has avoided diversification temptations that destroyed competitors. No plastics venture when oil was cheap. No international expansion when emerging markets boomed. No technology moonshots during the dot-com bubble. PCA stuck to its circle of competence: making and converting containerboard in North America. This focus enabled deep expertise and operational excellence that diversified competitors couldn't match.

Capital allocation patience separates PCA from typical industrial companies. While others chase growth through expensive acquisitions, PCA waits for distressed sellers. While competitors build greenfield capacity during booms, PCA expands during busts. The company thinks in decades, not quarters. This patience shows in the returns: PCA's stock has compounded at 15% annually since 2000, crushing both the S&P 500 and industrial peers.

The integration playbook PCA developed through dozens of acquisitions became a competitive advantage itself. Within 48 hours of closing, PCA teams arrive at acquired facilities with detailed plans. Week one: convert to PCA's containerboard, eliminate redundant costs. Month one: integrate sales forces, standardize pricing. Quarter one: optimize production schedules, cross-sell to existing customers. Year one: achieve full synergies, usually exceeding initial targets. This machine-like integration capability allows PCA to confidently pursue deals others avoid.

Operational excellence in a commodity business requires fanatical attention to detail. PCA measures everything: machine speeds, fiber yields, truck utilization, customer profitability. Plant managers compete on operational metrics published weekly. The company's "cost of quality" program, launched in the Tenneco days, still drives continuous improvement. Small optimizations—reducing paper breaks by 1%, improving truck routing by 2%—compound into structural advantages. In a business where 100 basis points of margin can double profits, these details matter enormously.

The cultural transformation from conglomerate subsidiary to entrepreneurial competitor took years but proved crucial. PCA pushed decision-making to plant managers, tied compensation to performance, and celebrated operational wins. The company cultivated an underdog mentality despite growing market share. Employees who'd spent careers being ignored by Tenneco headquarters suddenly found themselves empowered to drive results. This cultural shift, more than any financial engineering, explains PCA's outperformance.

X. Analysis & Investment Case

The bull case for PKG starts with a simple observation: e-commerce isn't going away, and every online order needs a box. While the pandemic-driven surge has moderated, structural shift toward online retail continues. Even if e-commerce penetration plateaus at 15% of retail sales—below pandemic peaks but above pre-COVID levels—that represents millions of additional boxes annually. PCA's integrated model and national footprint position it to capture disproportionate share of this secular growth.

Consolidation benefits extend beyond just market share gains. As PCA has proven through two decades of acquisitions, the corrugated industry offers endless opportunities to buy subscale operators at reasonable multiples and immediately improve their economics through integration. With thousands of small converting operations still independent, PCA can continue its rollup strategy for years. Each deal might be small, but the cumulative effect compounds powerfully.

Operational excellence provides another pillar of the bull case. PCA's mills run at higher utilization, its converting plants operate more efficiently, and its logistics network moves product at lower cost than competitors. These aren't temporary advantages—they're the result of decades of continuous improvement and billions in invested capital. As inflation pressures the industry, PCA's cost position allows it to maintain margins while competitors struggle.

The bear case starts with commodity exposure. Despite PCA's operational excellence, containerboard prices ultimately drive profitability. A 10% decline in containerboard pricing can erase 20% of earnings. While PCA has navigated cycles successfully, the next downturn could be different. New capacity additions from competitors, particularly in the Southeast, could pressure pricing for years. The commodity nature of the product means PCA can't fully control its destiny.

Recycling disruption presents a long-term threat that bulls might underestimate. Amazon and other large shippers are experimenting with reusable packaging systems. Regulatory pressure to reduce packaging waste is intensifying. While corrugated is recyclable, the push toward circular economy models could reduce overall packaging demand. PCA's enormous fixed cost base would struggle to adjust to a structural decline in volumes.

Amazon in-housing risk looms larger than most investors appreciate. Amazon already operates its own packaging facilities and continues expanding capacity. While they're currently a customer, Amazon's history shows they eventually compete with successful suppliers. If Amazon backward-integrates into containerboard production—not inconceivable given their scale—PCA loses its largest customer and gains a formidable competitor simultaneously.

Valuation presents a nuanced picture. At 12x forward EBITDA and 18x earnings, PKG trades at a premium to historical averages but a discount to quality industrials. The premium seems justified given PCA's returns on capital, but leaves little room for error. Any disappointment in volume or pricing could trigger multiple compression. The stock's 40% gain over the past year has priced in significant continued execution.

Comparison to peers reveals PCA's strengths and vulnerabilities. International Paper trades at 8x EBITDA but generates lower returns and faces European exposure. WestRock's merger with Smurfit Kappa creates a global giant but with integration risk. Smaller players like Sonoco offer higher growth but lack PCA's scale advantages. PCA sits in the sweet spot: large enough for scale, focused enough for operational excellence, disciplined enough to avoid value-destroying diversification.

Historical multiple analysis suggests the market understands PCA's quality. The company has traded at an average 10x EBITDA over the past decade, with ranges from 7x in downturns to 14x at peaks. Current valuation at 12x implies expectations for continued strong performance. The market is pricing in successful navigation of the next cycle, continued consolidation success, and sustained e-commerce growth.

Key metrics to watch going forward include containerboard pricing (published weekly), mill utilization rates, and integration levels. PCA provides excellent disclosure, but the real tells come from industry publications tracking capacity additions and operating rates. Watch for PCA's acquisition announcements—small deals signal continued rollup execution. Monitor customer concentration, particularly Amazon's percentage of revenue.

The investment case ultimately depends on time horizon. Short-term investors face commodity price volatility and economic sensitivity. A recession would hurt volumes and pressure pricing, likely driving 30%+ stock decline. But long-term investors can look through cycles to the structural story: consolidation of a fragmented industry, secular growth from e-commerce, and operational excellence driving superior returns. PCA won't excite growth investors or provide tech-like multiples, but for patient capital seeking industrial compounders, it offers a compelling proposition.

XI. Epilogue & Future Outlook

The future of packaging in a circular economy presents both opportunity and existential questions for PCA. Environmental pressures are intensifying—European regulations on single-use packaging, California's recycling mandates, corporate sustainability commitments from major customers. Yet corrugated packaging, made from renewable resources and boasting 90%+ recycling rates, stands better positioned than plastic alternatives. PCA's challenge is to lead this transition, investing in next-generation recycling technology and bio-based coatings that enhance performance while maintaining environmental credentials. The company that made brown boxes for a century must now make them greener.

Technology disruption in packaging sounds like an oxymoron, but change is coming faster than most expect. Smart packaging with RFID tags and sensors, enabling real-time tracking and condition monitoring. Automation in converting plants, reducing labor costs and improving customization capabilities. AI-driven demand forecasting and production optimization. Digital printing allowing mass customization of graphics and messaging. PCA has been notably quiet about technology investments—a strategic error or disciplined focus? The next decade will reveal whether operational excellence alone suffices or if digital transformation becomes mandatory.

Next acquisition targets are hiding in plain sight. The Southwest remains underpenetrated, with independent converters in Phoenix, Las Vegas, and Albuquerque ripe for consolidation. Food packaging specialists offer higher margins and recession resistance. The real prize might be a medium-sized integrated producer—someone like Cascades' U.S. operations or Greif's corrugated business—providing scale and synergies that move the needle. With $2 billion in debt capacity and strong cash generation, PCA has the firepower for a transformative deal.

"If we were running PKG," the thought experiment beloved by business school students, several moves seem obvious. First, accelerate the sustainability narrative—PCA's environmental story is strong but poorly told. Second, expand into Mexico, following customers' nearshoring moves. Third, develop technology partnerships rather than internal R&D—let startups innovate, then acquire proven solutions. Fourth, consider strategic alternatives for the white paper business—it's declining, distracts management, and confuses the equity story. Finally, increase transparency on customer concentration and Amazon exposure—the mystery creates unnecessary risk perception.

Final reflections on building value in industrial America reveal timeless truths. PCA's journey from Depression-era box makers to e-commerce infrastructure demonstrates that boring businesses often create extraordinary value. The company succeeded not through disruption or innovation but through relentless execution, strategic patience, and operational discipline. In an era obsessed with software margins and network effects, PCA proves that physical infrastructure, customer relationships, and manufacturing excellence still matter.

The broader lesson transcends packaging. Industrial America isn't dying—it's transforming. Companies that embrace operational excellence, consolidate fragmented markets, and serve growing end markets can generate exceptional returns. The key is choosing the right pond. PCA found its pond in corrugated packaging, then systematically became the biggest fish. No glamour, no headlines, just steadily compound returns.

Looking ahead, PCA faces a fascinating paradox. The business has never been stronger—record margins, dominant market position, secular tailwinds from e-commerce. Yet disruption risks have never been higher—sustainability pressures, technology threats, customer concentration. The next chapter of PCA's story will be written by management's ability to navigate these contradictions. Can a company built on brown boxes evolve for a digital, sustainable future? Can operational excellence overcome technological disruption? Can industrial consolidation continue creating value in an age of asset-light business models?

The answer matters beyond PCA's shareholders. If PCA succeeds, it validates a model for industrial value creation in 21st century America. If it fails, it suggests that even the best-run industrial companies can't escape commoditization and disruption. The stakes are significant, the outcome uncertain. But if history is any guide, betting against PCA's ability to adapt, evolve, and prosper would be foolish. The company that survived the Depression, thrived through conglomeration, and surfed the e-commerce wave isn't done yet.

The boxes keep moving, the mills keep running, and somewhere in Lake Forest, Illinois, Mark Kowlzan is probably studying acquisition targets and planning the next move in PCA's endless game of industrial chess. For investors seeking to understand American business, PCA offers a masterclass. Not in disruption or innovation, but in something rarer and more valuable: the art of building lasting value in the physical economy, one brown box at a time.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube