Polaris: The Adrenaline Machine

I. Introduction: The Roseau Miracle

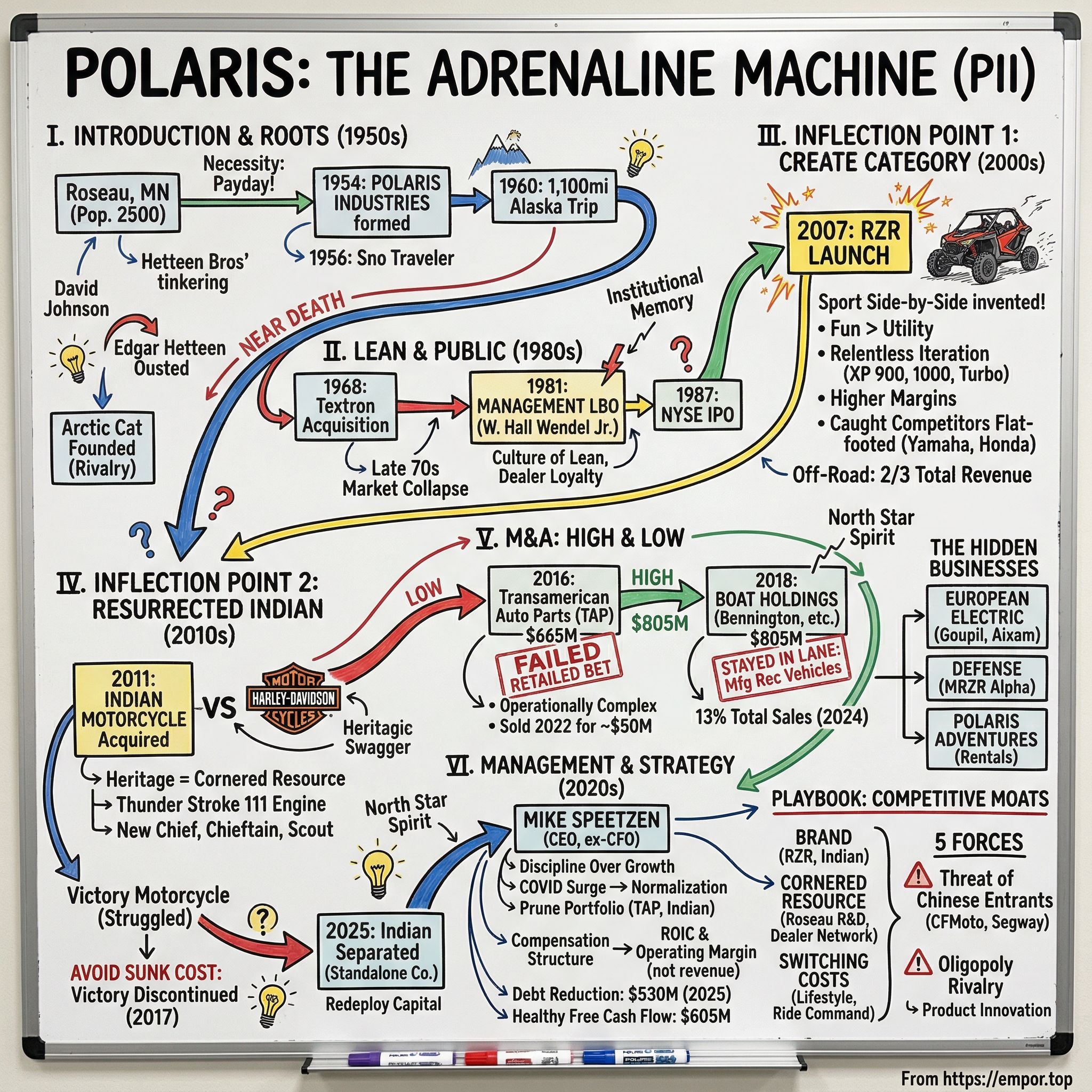

Pull up Google Maps and drop a pin on Roseau, Minnesota. Population roughly 2,500. Ten miles south of the Canadian border. The kind of place where winter lasts six months and the nearest major airport is a three-hour drive through flat, frozen prairie. It is, by any conventional Silicon Valley metric, the last place on Earth you would expect to find the headquarters of a five-billion-dollar global powersports empire.

And yet, here sits Polaris Inc., a company that has spent seven decades turning snow, mud, and open water into an extraordinarily profitable business. At its peak in 2023, Polaris generated nearly nine billion dollars in revenue, commanding the largest share of the North American off-road vehicle market and operating through more than 3,000 dealers across forty-plus countries. The company employs roughly 15,000 people. Its stock trades on the New York Stock Exchange under the ticker PII.

But the Polaris story is not a story about vehicles. Not really. It is a story about "Share of Garage"—the strategic insight that a household's garage is finite real estate, and the company that fills it with the most machines wins the most lifetime value. Snowmobiles in winter. Side-by-sides in summer. A pontoon boat for the lake. Maybe an Indian Motorcycle for the open road. Polaris does not want to sell you one product. It wants to own your recreational identity.

The arc of this company traces a remarkable evolution: from a seasonal snowmobile maker that nearly died in the 1980s, to the inventor of an entirely new vehicle category in the 2000s, to an acquisitive conglomerate that stumbled badly on a $665 million retail bet, to today's leaner, more disciplined operator under CEO Mike Speetzen. Along the way, Polaris resurrected one of America's oldest motorcycle brands, quietly built a European electric vehicle business most investors have never heard of, and supplied the U.S. Special Operations Command with lightweight tactical vehicles that fit inside an Osprey helicopter.

This is a company that has been written off more than once. Each time, it came back meaner. To understand why, we need to start where it all began—in a machine shop where three men from the frozen north built something that was never supposed to work.

II. Succinct Roots: The Iron Dog

In 1954, in a corrugated-metal shop that serviced farm equipment and built grain elevators, a man named David Johnson did something his boss would have killed him for.

Edgar Hetteen, who co-owned the shop with his brother Allan, was away on a business trip. Johnson, Edgar's brother-in-law, had been tinkering with an idea: a machine that could travel over snow. He and several shop workers cobbled together a contraption using a grain elevator conveyor belt as a track, a small Briggs & Stratton engine for power, and a repurposed Chevrolet bumper bent into crude skis. When Edgar returned and saw what his employees had built on company time with company materials, he was furious.

But then a local lumberyard owner named "Silver Pete" Peterson walked in and offered to buy the thing. The price was $465—just enough to cover the payroll Edgar had been worrying about. Necessity, as it often does, overruled anger. The company pivoted. On July 21, 1954, Hetteen Hoist & Derrick was reincorporated as Polaris Industries, named after the North Star—a fitting choice for a company born at the edge of the Arctic.

Allan Hetteen refined the design into what became the Polaris Sno Traveler, the company's first real production model, which rolled off the line in 1956. The machine was primitive by modern standards, but it solved a genuine problem for farmers, trappers, and utility workers who needed to move across snow-covered terrain. This was not recreation. This was survival.

Edgar Hetteen, restless and evangelical about the snowmobile's potential, embarked on a legendary publicity stunt in March 1960: an 1,100-mile snowmobile trek from Bethel to Fairbanks, Alaska, taking eighteen grueling days. The journey generated national press coverage, but it also generated a crisis. Edgar's prolonged absence spooked the banks financing Polaris. They demanded his removal. The board complied. Edgar Hetteen—the co-founder of Polaris—was pushed out of his own company.

What happened next is the powersports industry's original "traitorous eight" moment. Edgar moved sixty miles south to Thief River Falls, Minnesota, and founded what would become Arctic Cat, Polaris's fiercest rival for the next half-century. One small town's loss became another small town's gain, and the two companies—separated by an hour's drive through the Minnesota tundra—would define the snowmobile industry for generations.

But the pivotal moment in Polaris history came two decades later. In 1968, the company had been acquired by Textron, the sprawling industrial conglomerate. By the late 1970s, the snowmobile market had collapsed—fuel crises, warm winters, and oversupply had gutted demand. Textron's president, Beverly Dolan, told Polaris president W. Hall Wendel Jr. to find a buyer. A deal with Bombardier fell through when the U.S. Department of Justice raised antitrust concerns. So Wendel did something audacious: in July 1981, he led a management leveraged buyout, structured as a limited partnership. The company restarted with just 100 workers and barely 5,000 machines in production.

This near-death experience became the founding myth of modern Polaris. The LBO instilled a culture of lean operations, dealer loyalty, and paranoid cost discipline that persists to this day. Every dollar mattered. Every dealer relationship was sacred. The company clawed its way back, reaching $40 million in sales with 450 employees within five years. On September 16, 1987, Polaris went public on the New York Stock Exchange.

For investors, the LBO chapter matters because it explains why Polaris, even at its most acquisitive, always maintained a manufacturing-first mentality. The company never forgot what it felt like to nearly cease to exist. That institutional memory would serve it well in the decades ahead—and would make its eventual stumble into retail all the more jarring.

III. Inflection Point 1: Creating the Sport Side-by-Side

Picture a county fair in rural Iowa, circa 2005. The parking lot is a sea of dusty ATVs—Honda FourTrax, Yamaha Grizzly, Polaris Sportsman. These are work machines. Farmers use them to check fence lines. Hunters use them to haul deer carcasses out of the timber. They are about as glamorous as a wheelbarrow.

Now fast forward two years. In 2007, Polaris launched the RZR—initially branded as the Ranger RZR, a sub-model of its workhorse Ranger utility vehicle lineup. On paper, it looked like a minor product extension. In reality, it was one of the most consequential product launches in the history of recreational vehicles.

The RZR was purpose-built for one thing: fun. At just fifty inches wide, it could fit on ATV trails. At 945 pounds, it was remarkably light. Its 800cc twin-cylinder engine was mounted behind the seats, giving it a low center of gravity that made it feel like a go-kart on steroids. The suspension was tuned for aggressive terrain—rocks, jumps, whoops, desert washes. This was not a utility vehicle with a sport package bolted on. It was a sport vehicle from the ground up.

What Polaris had done, whether fully intentionally or not, was create an entirely new vehicle category: the sport side-by-side. Think about that for a moment. In an industry dominated by incremental improvements—a few more horsepower here, slightly better suspension travel there—Polaris had invented a new thing. It is the equivalent of someone in the auto industry creating the SUV category. Before the RZR, if you wanted off-road thrills, you rode an ATV or a dirt bike. After the RZR, there was a third option—one that was safer than a dirt bike, more exciting than an ATV, and could carry a passenger.

The market response was explosive. Within a year, Polaris dropped the "Ranger" prefix and gave the RZR its own standalone lineup. The company iterated relentlessly: the RZR XP 900 in 2011, the RZR XP 1000 in 2013, turbocharged models, four-seat variants, desert racing editions. Each generation pushed the performance envelope further—more horsepower, more suspension travel, wider track widths—while the price climbed from around $10,000 for the original to north of $30,000 for the flagship models.

The strategic brilliance of the RZR was threefold. First, it moved Polaris from the "utility" buyer—farmers, ranchers, hunters—to the "recreation" buyer—weekend warriors, adrenaline seekers, families looking for outdoor adventure. The recreation buyer is less price-sensitive, more brand-loyal, and far more likely to purchase accessories: doors, roofs, light bars, suspension upgrades, custom wraps. Second, the SxS business carried significantly higher margins than traditional ATVs. A fully loaded RZR Turbo with accessories could generate margins that made the old Sportsman ATV look like a loss leader. Third, Polaris had a multi-year head start. Yamaha and Honda, the two Japanese giants that had dominated the ATV market for decades, were caught completely flat-footed. Their corporate cultures—conservative, consensus-driven, optimized for reliability over excitement—were structurally incapable of responding quickly to a category that was defined by raw performance and annual model-year excitement.

Can-Am, owned by BRP (the same Bombardier Recreational Products that traces back to the company that nearly bought Polaris in 1981), was the first credible competitor, launching the Maverick in 2012. But by then, Polaris had five years of brand equity, dealer shelf space, and aftermarket ecosystem baked in. The RZR became synonymous with the sport SxS category the way Kleenex is synonymous with tissues.

By the mid-2010s, the Off-Road segment—powered primarily by the RZR franchise—had become the largest and most profitable segment of Polaris, generating roughly two-thirds of total company revenue. The RZR did not just change Polaris's product mix; it fundamentally altered the company's return on invested capital, its valuation multiple, and its strategic ambition. A company that had once been a seasonal snowmobile maker with a modest ATV business was now a year-round powersports platform with a category-defining franchise.

And it was that confidence—the swagger that comes from having invented a category—that emboldened Polaris to make its next big bet: resurrecting a motorcycle brand that had been dead for decades.

IV. Inflection Point 2: The Indian Motorcycle Resurrection

The story of Indian Motorcycle is one of the great tragedies of American manufacturing. Founded in 1901 in Springfield, Massachusetts, Indian was America's first motorcycle company—predating Harley-Davidson by two years. For the first half of the twentieth century, Indian and Harley were co-equal rivals, the Coke and Pepsi of American motorcycling. Indian's Chief, with its iconic skirted fenders, was as recognizable on American roads as a Cadillac fin.

Then Indian died. The original company ceased production in 1953, and for the next six decades, the brand passed through a parade of owners, each promising a revival, each failing. By the time Polaris came calling in 2011, Indian Motorcycle was what brand strategists call a "zombie brand"—famous, beloved, and completely inert. It had enormous emotional equity and zero commercial viability.

Polaris acquired Indian on April 19, 2011, from a group of investors advised by UK private equity firms Stellican Limited and Novator Partners. The purchase price was reportedly around $20 million—a figure so modest it barely registered on Polaris's income statement. But the real cost of the Indian bet was not the acquisition price. It was the hundreds of millions in R&D, tooling, manufacturing, and marketing required to build an entirely new motorcycle lineup from scratch.

This is where the analysis gets interesting. Polaris already had a motorcycle brand: Victory, launched in 1998 as its first foray into heavyweight cruisers. Victory had struggled for years, never capturing more than a sliver of the market dominated by Harley-Davidson. The bikes were competent but lacked soul. Victory was a brand that existed because Polaris engineers wanted to build motorcycles, not because consumers were clamoring for them.

Indian was different. Indian had something Victory could never manufacture: heritage. In Hamilton Helmer's "7 Powers" framework, Indian possessed a "Cornered Resource"—a brand with 110 years of American motorcycling history that no competitor could replicate. You cannot engineer heritage. You cannot marketing-spend your way into it. Harley-Davidson has it. Indian has it. Victory did not.

Polaris invested heavily. The company built a dedicated engineering team, designed an entirely new engine platform (the Thunder Stroke 111, a 1,811cc V-twin), and launched the all-new Indian Chief and Chieftain in 2013 to widespread critical acclaim. The Indian Scout followed in 2014, targeting younger riders with a smaller, more accessible platform. The bikes were gorgeous, powerful, and—critically—competitive on price with comparable Harley-Davidson models.

The David versus Goliath battle against Harley was fought with a weapon Polaris had honed in the off-road business: modular engineering. By sharing platforms, components, and manufacturing processes across its vehicle lines, Polaris could develop motorcycles at a fraction of the cost a standalone motorcycle company would incur. This allowed Indian to under-price Harley on an apples-to-apples basis while delivering comparable or superior performance.

Then came the hardest decision. In January 2017, Polaris announced it was discontinuing Victory Motorcycles. Victory had peaked in 2012 and sales had declined steadily. The brand represented barely three percent of Polaris's total revenue and had been profitable in only two of its previous five years. Dealers averaged just twenty Victory units per year—nowhere near enough to justify dedicated floor space and trained technicians.

Shutting down Victory was a masterclass in avoiding the sunk cost fallacy. Polaris had invested hundreds of millions in Victory over nearly two decades. Emotionally, killing it felt like admitting failure. Strategically, it was the only rational move. Every dollar spent propping up Victory was a dollar not invested in Indian, which had the brand power to actually compete with Harley-Davidson. Polaris chose the brand with the cornered resource and walked away from the brand without one.

The Indian story took another dramatic turn in October 2025, when Polaris announced it would separate Indian Motorcycle into a standalone company, selling a majority stake to Carolwood LP, a Los Angeles-based private equity firm. Indian had contributed approximately $478 million in annual revenue—about seven percent of Polaris's total. The deal, expected to close in early 2026, was projected to be accretive to Polaris's adjusted EBITDA by roughly $50 million and adjusted EPS by approximately a dollar per share, with around 900 employees transitioning to the new entity.

The Indian separation signals something important about the current Polaris strategy: the company is willing to part with even a beloved asset if the capital can be redeployed more efficiently into its core off-road franchise. Whether Carolwood can take Indian to the next level as an independent brand—or whether this proves to be a case of selling low in a cyclical trough—remains one of the most interesting open questions in powersports.

V. M&A and Capital Deployment: The Highs and Lows

Every great acquirer eventually makes a deal that makes everyone wince. For Berkshire Hathaway, it was Dexter Shoe. For Cisco, it was Flip Video. For Polaris, it was Transamerican Auto Parts.

In November 2016, Polaris completed its acquisition of TAP for $665 million. TAP was the leading manufacturer, distributor, and retailer of aftermarket accessories for Jeeps and trucks, operating 101 brick-and-mortar retail locations under the 4 Wheel Parts banner. The thesis was intoxicating: Jeep and truck enthusiasts were basically the same customer as Polaris's off-road buyer. If Polaris could capture those customers' aftermarket spending—lift kits, bumpers, wheels, lighting—it would dramatically expand its total addressable market without building new vehicles.

The price was rich. At roughly nine times EBITDA, Polaris was paying a premium multiple for a retail business with fundamentally different economics than manufacturing. Retail requires managing real estate leases, store-level labor, inventory across thousands of SKUs, and foot traffic patterns. Polaris had no institutional expertise in any of these areas.

The problems surfaced quickly. TAP's retail operations were operationally complex, margin-thin, and culturally alien to Polaris's manufacturing DNA. The company found itself managing a chain of specialty retail stores—a business that required a completely different management playbook than designing and building vehicles. Same-store sales were volatile. The integration consumed disproportionate management attention. And the strategic synergies—the idea that a Jeep customer browsing 4 Wheel Parts would naturally migrate to a Polaris RZR—never materialized in any meaningful way.

In June 2022, Polaris sold TAP to Wheel Pros, backed by Clearlake Capital Group, for a net price of approximately $50 million. Including tax benefits and other cash inflows, total proceeds to Polaris were estimated at roughly $135 million in the second half of 2022. Against the original $665 million purchase price, this represented a loss of over half a billion dollars—one of the most value-destructive acquisitions in the company's history.

The TAP debacle teaches a clear lesson about the limits of the "Share of Garage" thesis. Polaris is superb at designing, manufacturing, and distributing vehicles and their associated parts, garments, and accessories through its dealer network. It is not a retailer. The competency does not transfer. Vertical integration into retail failed where product manufacturing succeeded because the two businesses require fundamentally different organizational capabilities.

Now contrast TAP with the Boat Holdings acquisition. On July 2, 2018, Polaris completed its purchase of Boat Holdings for approximately $805 million in an all-cash transaction—the largest deal in company history. Boat Holdings was the largest manufacturer of pontoon boats in the United States, with roughly $560 million in 2017 sales. The key brands were Bennington, Godfrey, Hurricane, and Rinker.

This deal fit the "Share of Garage" thesis far better than TAP. A pontoon boat is a recreational vehicle purchased by exactly the same demographic that buys a Polaris RZR or a Polaris Ranger. The customer likely lives in the Sunbelt or Upper Midwest, owns lakefront or near-lake property, and spends weekends on the water. Critically, boat manufacturing is operationally similar to what Polaris already does: design a platform, build it in a factory, ship it to a dealer, and sell accessories alongside the unit. Polaris did not need to learn a new business model. It was applying its existing competency—manufacturing recreational vehicles and distributing them through independent dealers—to an adjacent category.

Bennington, in particular, was the crown jewel. It held the number-one market share position in pontoon boats, a category that had been growing steadily as baby boomers aged into lake-house retirement. Pontoons are the "gateway boat"—easy to operate, family-friendly, and less intimidating than a center-console fishing boat or a wakeboard tower. The demographic tailwinds were favorable.

The Marine segment, which consisted primarily of the Boat Holdings brands, generated $907 million in revenue in fiscal 2024, representing about thirteen percent of Polaris's total sales. While the segment has faced cyclical headwinds alongside the broader powersports market, it has functioned as a stabilizing diversifier—marine demand does not correlate perfectly with off-road vehicle demand, and the seasonal buying patterns are complementary.

The contrast between TAP and Boat Holdings is instructive for any investor evaluating Polaris's capital allocation track record. When Polaris stays in its lane—designing and manufacturing recreational vehicles—it allocates capital well. When it strays into adjacent but operationally dissimilar businesses, it destroys value. The current management team, led by Mike Speetzen, appears to have internalized this lesson fully.

VI. Current Management: The Speetzen Era

Mike Speetzen never planned to be CEO of Polaris. His path to the top job was as unconventional as it was abrupt.

Speetzen joined Polaris in August 2015 as Executive Vice President of Finance and Chief Financial Officer. His background was pure industrial-company finance: he had been CFO of Xylem, the water technology company spun out of ITT Corporation, and before that held senior finance roles at StandardAero, Honeywell, and General Electric. He holds an MBA from the Thunderbird School of Global Management at Arizona State and an undergraduate degree in management from Purdue. He is, by training and temperament, a numbers guy—methodical, process-oriented, and allergic to the kind of aspirational empire-building that had characterized the prior era.

When predecessor Scott Wine departed in late 2020 to become CEO of CNH Industrial, Speetzen was named interim CEO on January 1, 2021—right in the middle of the COVID-era demand surge that was flooding powersports dealers with backorders. He was confirmed as permanent CEO on April 30, 2021, with Bob Mack stepping into the CFO role simultaneously.

The timing was brutal. Speetzen inherited a company riding a sugar high. During 2020 and 2021, the outdoor recreation boom—fueled by stimulus checks, work-from-home flexibility, and a desperate desire to escape lockdown monotony—had sent powersports demand to record levels. Polaris revenue peaked at nearly $8.9 billion in 2023. Dealer lots were empty. Lead times stretched to months. Everything Polaris built, it sold.

Then the hangover arrived. As interest rates climbed, stimulus savings evaporated, and consumers returned to pre-pandemic spending patterns, powersports demand normalized sharply. Revenue fell to $7.2 billion in 2024 and was essentially flat at $7.15 billion in 2025. The net income trajectory was even more dramatic: from $503 million in 2023 to $111 million in 2024 to a net loss of $466 million in 2025, driven in part by impairment charges related to the Indian Motorcycle separation.

Speetzen's response has been textbook CFO-turned-CEO: discipline over growth. The management philosophy shifted from "conglomerate"—buying anything with an engine—back to "powersports core." The TAP divestiture was completed. The Indian separation was announced. Debt reduction became a priority, with roughly $530 million paid down in 2025. Free cash flow remained healthy at approximately $605 million despite the top-line pressure.

The compensation structure tells an important story about management incentives. A deep dive into the proxy statement reveals that Speetzen's pay is heavily weighted toward two metrics: Return on Invested Capital and Operating Margin. Not revenue growth. Not market share. Not the vanity metrics that incentivize empire-building. ROIC and operating margin are the metrics of a management team focused on earning the right to grow, rather than growing for growth's sake.

This matters enormously for long-term investors. The prior era's capital allocation mistakes—TAP being the most egregious—were driven by a growth-at-all-costs mentality. Speetzen's incentive structure is designed to prevent exactly those mistakes. When your bonus depends on generating returns above your cost of capital, you think very carefully before writing a $665 million check for a retail chain you do not understand.

The share repurchase program tells a more nuanced story. In October 2023, Polaris authorized a $1 billion buyback with no expiration date. However, execution has been minimal—the company repurchased zero shares in the third quarter of 2024, for example. The prioritization of debt reduction over buybacks during a cyclical downturn suggests a management team that, while confident in the long-term business, is unwilling to lever up the balance sheet to buy back stock at what may or may not be a trough. Given that roughly eighty percent of powersports purchases are financed—making demand highly sensitive to interest rates—this conservatism seems prudent.

Polaris currently trades at roughly $54 per share, giving it a market capitalization of approximately $3.1 billion. The dividend yields about five percent at $2.69 per share annualized. For a company that generated nearly $9 billion in revenue just two years ago, the current valuation implies deep skepticism about the durability of the post-COVID normalization.

VII. The "Hidden" Businesses

There is a version of Polaris that most American investors never think about. It is small, quiet, electric, and very European.

In 2011, the same year Polaris acquired Indian Motorcycle, the company also bought Goupil Industrie, a French manufacturer of electric commercial utility vehicles based in Bourran, France. Goupil makes small, fully electric trucks designed for urban delivery, municipal services, and campus logistics—the kind of vehicles you see in European pedestrian zones collecting trash or delivering packages where full-size trucks cannot go. At the time of acquisition, Goupil had roughly $25 million in annual sales across eighteen European countries.

Two years later, in 2013, Polaris acquired Aixam Mega, based in Aix-les-Bains, France. Aixam manufactures "voitures sans permis"—literally "cars without licenses"—lightweight, low-speed quadricycles that can be driven without a full automobile license in many European countries. These vehicles are enormously popular with older Europeans who never obtained a traditional driving license, teenagers in rural areas, and urban commuters who want something more enclosed and weather-resistant than a scooter. Aixam had approximately $110 million in 2012 sales through over 400 European dealers and offered both diesel and electric models.

Together, Goupil and Aixam represent a fascinating optionality play. The European regulatory environment is pushing aggressively toward electrification of urban transport and last-mile delivery. Goupil's electric utility vehicles are already compliant with the tightest European emissions zones. Aixam's quadricycles offer a micro-mobility solution that sits between e-bikes and traditional cars—a category that is growing as European cities restrict car access to urban centers.

Neither business moves the needle on Polaris's current income statement in a material way. But they represent a hedge against a world where electrification and urbanization reshape the global vehicle market in ways that are hostile to traditional powersports. If the future of personal transportation in European cities is small, electric, and license-free, Polaris already has a seat at the table.

Then there is the defense business. Polaris Government & Defense sells the MRZR—Military RZR—a purpose-built lightweight tactical vehicle derived from the commercial RZR platform. The MRZR Alpha, the current model, features a 1.5-liter four-cylinder turbo diesel engine producing 118 horsepower, an eight-speed automatic transmission, and a top speed of roughly sixty miles per hour with a range of over 220 miles. The key differentiator: it fits inside a V-22 Osprey tiltrotor aircraft, making it air-transportable for special operations forces who need to move fast once they hit the ground.

The MRZR is on contract with U.S. Special Operations Command as the Light Tactical All-Terrain Vehicle and with the U.S. Marine Corps as the Ultra Light Tactical Vehicle. A GSA contract valued at up to $109 million underscores the military's commitment to the platform. International sales to allied forces add another layer of demand. The defense business is high-margin, low-volume, and carries the kind of multi-year contract visibility that commercial powersports cannot offer.

The defense business also functions as a "halo" product for the broader brand. When Special Operations operators choose Polaris for the most demanding tactical environments on Earth, it validates the engineering credibility of the entire product line. It is the powersports equivalent of a Formula 1 racing program—the technology developed for the extreme trickles down to the consumer products, and the brand association with military excellence reinforces consumer perception.

Finally, there is Polaris Adventures. Launched in 2017, Adventures is a network of over 250 independent "Adventure Outfitter" locations across the United States, Canada, Mexico, and New Zealand. These outfitters partner with Polaris to offer rental experiences on side-by-sides, ATVs, snowmobiles, Slingshots, and boats. Consumers book through the Polaris Adventures platform, show up at a scenic location, and spend a few hours or a full day riding Polaris vehicles through curated trail systems.

The genius of Adventures is that it converts prospective buyers into actual buyers. Someone who has never sat in a RZR can rent one for an afternoon in Moab, Utah, or the Hatfield-McCoy Trails in West Virginia, experience the thrill firsthand, and walk into a dealer six months later ready to purchase. It is an experiential marketing funnel disguised as a rental business. In 2024, Polaris launched Adventures Elite, offering purpose-built business tools for recreation rental operators, along with a membership subscription program that allows monthly credit accrual redeemable at any location—a recurring revenue model layered on top of an experiential acquisition channel.

These three businesses—European electric vehicles, military defense, and adventure rentals—are individually small relative to the core Off-Road segment. But collectively, they represent strategic diversification that insulates Polaris from pure dependence on the cyclical North American consumer.

VIII. The Playbook: Competitive Moats and Strategic Powers

To understand where Polaris sits competitively, it helps to apply structured frameworks to what can feel like a messy, cyclical business.

Start with Hamilton Helmer's 7 Powers. The primary power Polaris possesses is Brand. Two brands, specifically: RZR and Indian. The RZR name is synonymous with sport side-by-sides in the same way that Jeep is synonymous with off-road SUVs. When someone says "Let's go RZRing this weekend," they may well be riding a Can-Am Maverick, but the generic verb belongs to Polaris. Indian Motorcycle, though now being separated, carried over a century of American motorcycling heritage—a brand asset that no amount of marketing spend could replicate from scratch. Brand power translates directly into pricing power: Polaris can charge a premium over generic competitors, and its aftermarket accessories ecosystem—which generates over $1.8 billion in annual PG&A (Parts, Garments, and Accessories) revenue—is a direct monetization of that brand loyalty.

The second power is Cornered Resource, and here the resource is not a patent or a technology but an ecosystem. The Roseau R&D complex, where Polaris still develops its core off-road platforms, represents decades of accumulated engineering knowledge in a highly specific domain. The engineers who design snowmobiles, side-by-sides, and ATVs in Roseau are not interchangeable with automotive engineers in Detroit. They understand terrain, vibration, rider ergonomics, and extreme-weather performance in ways that cannot be replicated by hiring a few dozen engineers and putting them in a new building. Alongside the R&D ecosystem sits the dealer network—over 3,000 strong globally. Dealer relationships in powersports are deeply personal, often multi-generational, and extremely difficult for new entrants to replicate. A dealer who has sold Polaris products for thirty years, whose service technicians are trained on Polaris platforms, and whose floor plan financing is structured around Polaris shipment schedules is not switching to CFMoto because the Chinese manufacturer offers a slightly better margin on paper.

The third relevant power is Switching Costs—though these operate at a different level than in, say, enterprise software. The switching cost on the vehicle itself is low. If a Polaris owner wants to buy a Can-Am next time, there is no technical barrier. But the switching cost on the lifestyle is substantial. A devoted RZR owner has invested in Polaris-specific accessories, joined Polaris-affiliated riding clubs, uses the Polaris Ride Command app for GPS navigation and trail mapping, and has relationships with a Polaris dealer's service department. The total cost of switching—financial, social, and informational—is much higher than the sticker price differential between competing vehicles.

Now apply Porter's Five Forces. The most important force in the powersports industry is the Threat of New Entrants, and here the news is both good and concerning. On the positive side, barriers to entry are massive. EPA emissions certification, CPSC safety compliance, dealer network development, warranty infrastructure, and parts supply chain logistics create a formidable gauntlet that keeps casual entrants out. It took decades and billions of dollars for the existing competitors to build their current positions.

The concerning development is the emergence of well-funded Chinese competitors, principally CFMoto and Segway Powersports (a subsidiary of Ninebot). These companies benefit from Chinese manufacturing cost advantages, state-backed financing, and a willingness to sell at aggressive price points to gain market share. CFMoto, in particular, has been rapidly expanding its North American dealer network and moving upmarket with vehicles that increasingly rival the fit, finish, and performance of Polaris and Can-Am products. The looming specter of Chinese electric powersports vehicles—manufactured at scale with vertically integrated battery supply chains—is perhaps the single most significant competitive threat to the North American powersports oligopoly over the next decade.

Supplier Power is moderate. Polaris manufactures most of its vehicles in-house but sources engines, electronics, and raw materials from global supply chains. The Buyer Power dynamic is bifurcated: individual consumers have relatively low bargaining power, but the dealer network—which is the actual customer in Polaris's wholesale model—has meaningful leverage, particularly during downturns when dealer inventories bloat and manufacturers face pressure to offer incentives.

Rivalry among existing competitors is intense but rational. The North American powersports market is effectively an oligopoly: Polaris, BRP (Can-Am), Yamaha, Honda, and Kawasaki control the vast majority of ATV and SxS sales. In motorcycles, the heavyweight cruiser market is dominated by Harley-Davidson with Indian as the challenger. In marine, Brunswick is the principal competitor. Price wars are rare because the market leaders understand that destroying margins benefits no one, and the primary competitive battleground is product innovation and model-year freshness rather than discounting.

For investors tracking Polaris on an ongoing basis, two key performance indicators matter above all else. The first is Off-Road segment operating margin. This is the core of the business, generating roughly two-thirds of revenue, and the margin on this segment reflects both pricing power and manufacturing efficiency. Compression in Off-Road margin—whether from promotional activity, input cost inflation, or competitive pressure—is the canary in the coal mine. The second KPI is dealer inventory levels, measured in weeks of supply. When dealer lots are lean, Polaris has pricing power and can ship fresh product at full margin. When dealer lots are bloated—as they became during the 2024-2025 normalization—the company faces pressure to offer rebates, extend payment terms, and slow production, all of which compress returns.

IX. Bear vs. Bull Case and Conclusion

Start with the bear case, because it is the one that has been winning lately.

Polaris is, at its core, a manufacturer of expensive discretionary toys. A new RZR costs anywhere from $15,000 to $35,000. A Bennington pontoon boat runs $30,000 to $100,000 or more. An Indian motorcycle is $10,000 to $40,000 depending on the model. These are not essential purchases. They are financed, leisure-oriented, weather-dependent luxuries that compete for the same household budget as vacations, home renovations, and pickup truck upgrades.

Roughly eighty percent of powersports vehicles are purchased with financing. That makes Polaris's demand curve a near-direct function of interest rates and consumer credit availability. When rates rose sharply from 2022 through 2025, the impact was immediate and severe: monthly payments on a financed RZR jumped by hundreds of dollars, pushing marginal buyers out of the market. Revenue dropped from $8.9 billion to $7.15 billion in just two years. Net income went from $503 million to a loss of $466 million. The stock fell from its post-COVID highs above $130 to trade around $54 at the time of this writing—a decline of nearly sixty percent.

The interest rate sensitivity is structural, not cyclical. Even if rates moderate, the fundamental reality is that powersports demand will always be among the first casualties of monetary tightening and the last beneficiary of easing. Investors in Polaris are, whether they realize it or not, making a bet on the direction of the rate cycle.

Then there is the Chinese competitive threat. CFMoto and Segway Powersports are not garage startups. They are backed by substantial Chinese industrial capital and are rapidly improving product quality while maintaining a significant cost advantage. CFMoto's UTVs are now competitive in performance testing with Polaris and Can-Am products at price points twenty to thirty percent lower. If Chinese manufacturers can crack the dealer network challenge—either by building their own or by converting existing multi-brand dealers—they could structurally compress margins across the entire North American powersports industry. This is the Honda-in-the-1970s playbook applied to off-road vehicles, and incumbent market leaders should not be complacent.

The "lumpy" nature of discretionary spending creates forecasting challenges that are inherently frustrating for public-market investors. Powersports demand is influenced by weather (warm winters kill snowmobile sales), housing markets (people who buy lake houses buy boats), fuel prices (high gas prices discourage weekend trail rides), and consumer sentiment (pessimism defers large purchases). The interaction of these variables makes Polaris's quarterly earnings inherently volatile, which depresses the stock's valuation multiple relative to steadier industrial businesses.

Now the bull case.

The post-COVID normalization is just that—a normalization. The industry pulled forward demand during 2020-2022, and the correction that followed was predictable and temporary. The installed base of powersports vehicles is aging. The average age of an ATV in operation has been climbing for years. At some point, the replacement cycle kicks in, and pent-up demand creates a tailwind. Polaris, as the market share leader with the broadest product portfolio, is best positioned to capture that recovery.

The Marine segment, acquired through the Boat Holdings deal, provides genuine diversification. Pontoon boats appeal to an aging-into-retirement demographic with high disposable income and time to spend on the water. The Marine business does not correlate perfectly with off-road demand, providing some counter-cyclical ballast. If Bennington can maintain its market share leadership in pontoons—a category with secular tailwinds from lakefront property development—the segment could become a meaningful stabilizer for the overall business.

The partnership with Zero Motorcycles, signed in September 2020 as a ten-year exclusive deal, positions Polaris at the forefront of powersports electrification. The first product, the Ranger XP Kinetic—an all-electric utility vehicle—launched in December 2021 and sold out within hours. While EV adoption in powersports remains early-stage, the Zero partnership gives Polaris access to powertrain technology, hardware, and software without bearing the full cost and risk of internal development. If battery costs continue to decline and off-road EV performance improves, Polaris has a ready-made pathway to electrify its lineup.

The current management team is, arguably, the best positioned in Polaris's history to navigate a cyclical downturn. Speetzen's CFO background makes him constitutionally averse to the kind of hubristic acquisitions that destroyed value under prior leadership. The compensation structure aligns management incentives with ROIC and margin, not revenue growth. The TAP divestiture and Indian separation demonstrate a willingness to prune the portfolio rather than defend past mistakes. Debt reduction of $530 million in 2025, even as the top line was flat, shows capital discipline. Free cash flow of $605 million demonstrates that the underlying business generates real cash even in a tough environment.

There is also a quiet efficiency play underway. Polaris has been investing in manufacturing automation, platform consolidation, and supply chain optimization. Warranty expenses declined $25 million in 2025, suggesting product quality improvements. These are the kinds of incremental operational gains that do not generate headlines but compound over time into meaningful margin expansion when demand recovers.

The question for investors ultimately comes down to cycle timing and competitive positioning. If you believe that North American powersports demand will recover as interest rates moderate and the replacement cycle accelerates, Polaris at $54 per share—with a five percent dividend yield, a clean balance sheet getting cleaner, and a management team focused on returns rather than growth—is a compelling setup. If you believe that Chinese competition will structurally compress industry margins, or that the post-COVID normalization represents a permanent downshift in demand, then the current valuation may be fair or even generous.

What is not in dispute is the quality of the underlying franchise. Polaris invented the sport side-by-side category. It operates the largest dealer network in powersports. It generates nearly $1.9 billion in annual PG&A revenue—a high-margin, recurring revenue stream that persists regardless of new vehicle sales. It has demonstrated, through the LBO survival, the RZR creation, the Victory shutdown, and the TAP divestiture, a capacity for institutional learning that is rare in any industry.

X. Epilogue: The Roseau Spirit

Drive through Roseau, Minnesota, on a winter evening and you will see the Polaris plant glowing against the snow. It is not a glamorous facility. There are no glass-walled atriums or artisanal coffee bars. It is a working factory in a working town, staffed by people whose grandparents may have worked alongside the Hetteen brothers.

There is something deeply American about the Polaris story—the kind of American story that does not get told often enough. Not a tale of venture capital and disruption, but of practical engineering, hard weather, and the stubborn refusal to die. The company was born because a man built something his boss did not want. It survived because a manager bought it back from a conglomerate that did not care. It thrived because it was willing to invent new categories, kill sacred cows, and admit its mistakes.

Jerry Bassett's The Polaris Story chronicles the early decades in rich detail, and the company's own financial filings from the TAP era offer a candid case study in capital misallocation and correction. For those interested in the deeper mechanics, the 2022 10-K's treatment of the TAP impairment and the 2025 proxy statement's discussion of executive compensation metrics reward careful reading.

What endures in Roseau is not nostalgia. It is a culture forged in the particular hardship of building things in a place where nothing comes easy—not the weather, not the logistics, not the recruiting. That culture produced the Sno Traveler, the RZR, and the MRZR. It absorbed the TAP failure and emerged leaner. It is now navigating a cyclical downturn with the discipline of a company that remembers what it feels like to have only 100 workers and 5,000 machines.

The North Star still shines over Roseau. And Polaris, for all its scars, still follows it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube