PHINIA Inc.: Betting on the Long Goodbye to Combustion

Introduction and Episode Roadmap

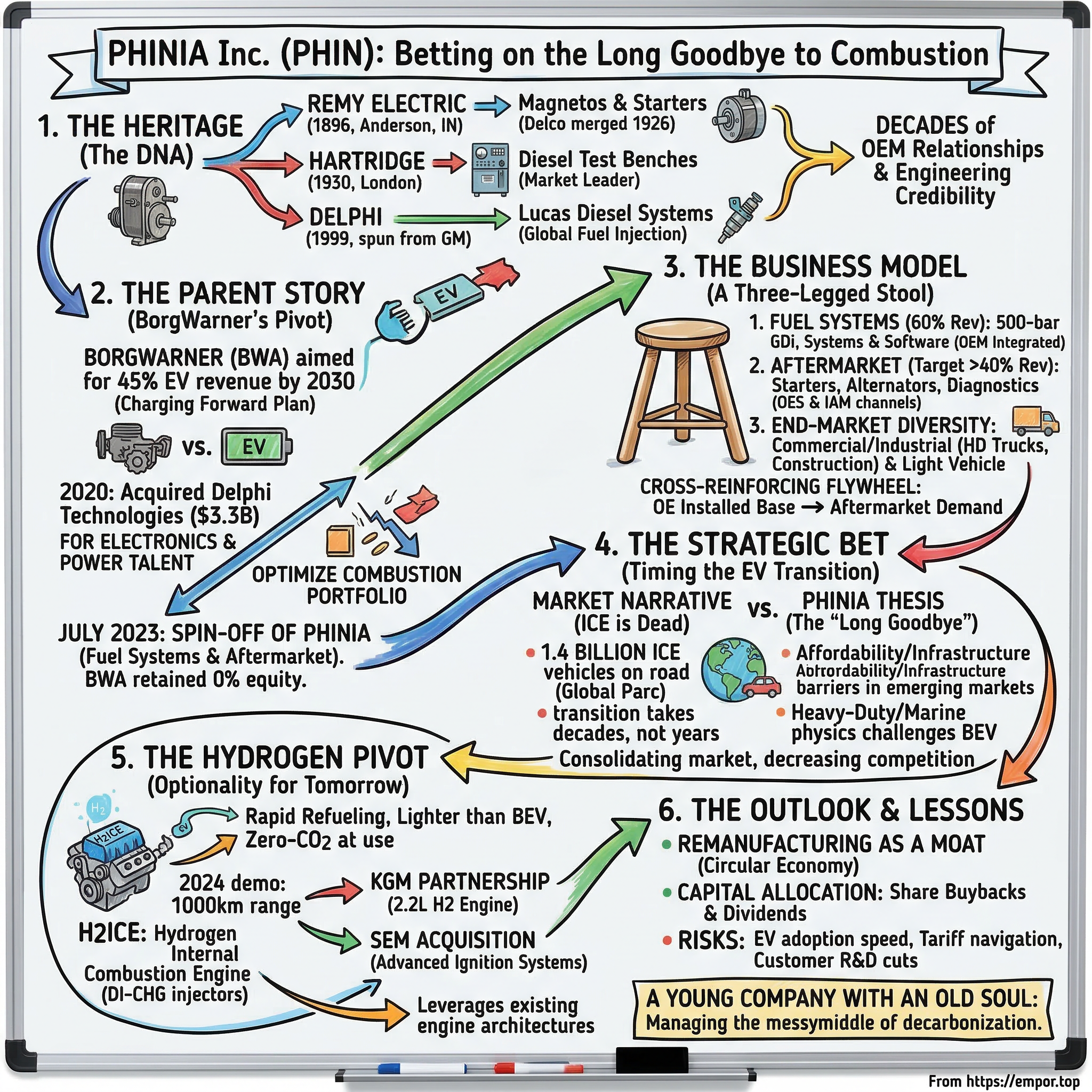

Here is a riddle for you: How does a company celebrate its hundredth birthday and its third birthday at the same time?

The answer walked onto the New York Stock Exchange trading floor on July 5, 2023, wearing an unfamiliar ticker symbol—PHIN—but carrying the accumulated wisdom of brands that had been building fuel injectors, starters, and test benches since before the Great Depression. PHINIA Inc. was, by every legal measure, a newborn corporation. Its Delaware certificate of incorporation was barely dry. Yet its portfolio of globally recognized brands—Delphi, Delco Remy, and Hartridge—carried engineering lineages stretching back more than a century.

The paradox gets richer. PHINIA did not emerge from a garage with venture capital and a dream. It was surgically extracted from BorgWarner, one of the world's premier powertrain companies, at the precise historical moment when Wall Street had decided that anything touching internal combustion engines was toxic waste to be jettisoned as quickly as possible. The electric vehicle revolution was coming, the narrative went, and companies still making fuel injectors and diesel pump test stands were relics of a dying age.

And yet, someone at BorgWarner—and more importantly, the leadership team that would run the new company—saw the situation differently. The central question animating PHINIA's existence is deceptively simple: Can a company built entirely on internal combustion engine technology thrive in what everyone assumes will be an EV-dominated future? Or is betting against the pace of electrification actually the smartest contrarian play available in the automotive sector?

This story touches on several themes that matter far beyond a single company. It is about the mechanics and market dynamics of strategic spin-offs, about how the timing debate around EV adoption creates both risk and opportunity, and about the art of building optionality when the future refuses to announce itself clearly. What makes PHINIA's story uniquely compelling is that it was born at the exact moment Wall Street most wanted to shed ICE assets—which means it entered the world carrying both the stigma and the potential bargain pricing that comes with being on the wrong side of a consensus narrative.

To understand where PHINIA is going, we first need to understand what it is made of—and that means going back more than a century, to a home wiring business in Anderson, Indiana.

The Heritage: Understanding the DNA

In 1896, two brothers named Frank and Perry Remy opened a modest home wiring business in Anderson, Indiana—a small city about forty miles northeast of Indianapolis that would become, improbably, one of the epicenters of American automotive electrical innovation. Perry Remy had a tinkerer's obsession with magnetos, the electromagnetic devices that generated sparks for early gasoline engines. By 1901, the operation had grown serious enough to incorporate as the Remy Electric Company. By 1910, the factory was shipping fifty thousand magnetos a year.

Their fiercest competitor operated out of Dayton, Ohio: the Dayton Engineering Laboratories Company—Delco—led by Charles F. Kettering, one of the most prolific inventors in automotive history. Kettering would go on to develop the electric self-starter that eliminated the dangerous hand-crank, a breakthrough that opened automobile ownership to women and older drivers and fundamentally expanded the car market. In 1916, the United States Motor Company acquired both Remy and Delco. Two years later, General Motors swallowed them both. C.E. Wilson—who would later rise to lead all of GM—engineered the formal merger of the two divisions into "Delco Remy" in 1926. For the next seven decades, Delco Remy operated as a GM division, manufacturing starters, alternators, and electrical components for everything from passenger sedans to military vehicles.

Across the Atlantic, a different origin story unfolded. In 1930, Leslie Hartridge assembled a small team of engineers in London and began building test benches for the fuel injection technology then emerging in diesel engines. Five years later, Hartridge's team adapted a magneto test stand to create one of the world's first diesel fuel pump test stands—a device that could precisely measure and calibrate the performance of fuel injection equipment. When World War II began, the organization relocated from London to the relative safety of Buckingham, England, where it remains headquartered to this day. Over the following decades, Hartridge became synonymous with diesel fuel injection testing, building the largest market share in field service test equipment worldwide. No other company competes across a comparable range of common rail test benches, injector testers, and pump test equipment.

The third thread in PHINIA's DNA is Delphi itself—the name that would eventually become the company's flagship brand. Delphi Automotive was spun off from General Motors in 1999 as the largest automotive parts company in the world. Along the way, Delphi acquired Lucas Diesel Systems from TRW for $871 million, bringing deep European fuel injection expertise into the fold. When Delphi Automotive split again in 2017—renaming the parent as Aptiv and spinning off the powertrain business as Delphi Technologies—the fuel systems heritage traveled with the spinoff.

The corporate journey of these brands through the late twentieth and early twenty-first centuries reads like a map of the automotive industry's consolidation era. Delco Remy was carved out of General Motors in 1994, when a group of private investors purchased the heavy-duty and automotive divisions. The independent company, eventually renamed Remy International and headquartered in Pendleton, Indiana, operated for two decades before BorgWarner acquired it in November 2015 for approximately $1.2 billion. BorgWarner subsequently sold the light vehicle aftermarket portion to Torque Capital in 2016, keeping the commercial vehicle Delco Remy business that is now the backbone of PHINIA's heavy-duty electrical offerings.

Hartridge traveled a different but equally winding path. As part of the Lucas Industries supply chain, Hartridge became entangled in the Lucas Diesel Systems business. When Delphi acquired Lucas Diesel from TRW in 1999, Hartridge came along. The brand then passed through Delphi Automotive, survived the 2017 split into Aptiv and Delphi Technologies, rode through BorgWarner's 2020 acquisition of Delphi Technologies, and finally landed in PHINIA. Through all of these ownership changes, Hartridge maintained its operational base in Buckingham and its market-leading position in diesel test equipment—a testament to the durability of niche industrial expertise.

These three brands share a common thread that explains why they ended up together: mastery of precision fuel delivery and electrical systems for internal combustion powertrains. Delco Remy understood how to start engines and keep them charged. Hartridge understood how to measure whether fuel injection systems worked correctly. Delphi understood how to design and manufacture those fuel injection systems at global scale. Together, they represent over a century of accumulated engineering credibility, thousands of OEM relationships validated through decades of collaboration, and a global distribution network that reaches into repair shops on every inhabited continent. These assets do not appear on a balance sheet, but they may be the most valuable things PHINIA owns. For investors, the heritage brands represent something that cannot be built from scratch—they are earned through decades of field performance and would take a generation to replicate.

The Parent Story: BorgWarner's Strategic Evolution

To understand why PHINIA exists as an independent company, you need to understand the moment of existential clarity that gripped BorgWarner's boardroom in 2020 and 2021.

BorgWarner had spent decades as one of the automotive industry's most respected powertrain suppliers—a company whose turbochargers, transmission components, and drivetrain systems powered vehicles from dozens of manufacturers worldwide. But as the EV narrative intensified, BorgWarner's leadership recognized a strategic imperative: the company needed to be seen—by investors, customers, and talent—as an electrification leader, not as a combustion-era holdover.

The first bold move came on January 28, 2020, when BorgWarner announced an all-stock agreement to acquire Delphi Technologies at an enterprise value of approximately $3.3 billion. On the surface, this was puzzling—Delphi Technologies was a fuel systems and powertrain electronics company, precisely the kind of combustion-era business that the market was beginning to discount. But BorgWarner was not buying fuel injectors. It was buying electronics capabilities, power electronics expertise, and software and calibration talent that could be redirected toward electrified propulsion. The deal closed on October 2, 2020, after overwhelming shareholder approval, with former Delphi Technologies shareholders receiving roughly 16 percent of the combined company.

Then came the pivot. On March 23, 2021, BorgWarner unveiled "Charging Forward"—a comprehensive strategy to transform the company into an electrification leader. The numbers were ambitious: grow EV revenues from less than three percent of total sales to approximately 45 percent by 2030. Target 25 percent EV revenue by 2025. Generate approximately $4.5 billion in cumulative free cash flow between 2021 and 2025 to fund the transition.

But Charging Forward had a third pillar that mattered enormously for the assets that would become PHINIA: optimize the combustion portfolio by disposing of three to four billion dollars in combustion-related revenue. This was not a vague aspiration. BorgWarner was explicitly telling Wall Street that it intended to shed its ICE businesses to achieve the pure-play EV multiple that investors were rewarding.

The logic was straightforward financial engineering, but no less powerful for being obvious. In 2021, pure-play EV companies traded at astronomical multiples. Traditional powertrain companies traded at depressed valuations, weighed down by the assumption that their core businesses were in terminal decline. If BorgWarner could separate its combustion assets and present itself as an electrification company, the remaining business would likely receive a higher valuation multiple—even if the underlying cash flows did not change.

On December 6, 2022, BorgWarner made it official: the company announced its intent to spin off its Fuel Systems and Aftermarket segments, consistent with the Charging Forward strategy. The separation would be structured as a tax-free distribution—shareholders would receive one share of the new company for every five shares of BorgWarner they held, with no need to surrender their existing shares or pay any consideration. On February 14, 2023, BorgWarner revealed the new company's name—PHINIA—and its leadership team, with Brady Ericson as CEO and Chris Gropp as CFO.

One month before the spin-off completed, BorgWarner held a pivotal investor day on June 6, 2023, unveiling the next phase of its strategy. The presentation made clear that PHINIA's departure completed the combustion portfolio optimization pillar. BorgWarner was moving on, and PHINIA would need to tell its own story to a market that was, at best, indifferent to ICE-focused businesses.

The spin-off closed at 5:00 p.m. Eastern Daylight Time on July 3, 2023. PHINIA shares began trading on the NYSE two days later. BorgWarner retained zero equity in the new company—a clean break that left PHINIA entirely on its own, for better or worse.

There is a deeper irony in the Delphi Technologies acquisition that deserves attention. BorgWarner paid $3.3 billion in 2020 to acquire a company whose fuel systems and aftermarket assets—the very assets it would spin off as PHINIA three years later—initially traded at a market capitalization well below that acquisition price. BorgWarner effectively bought Delphi Technologies for its electronics and power electronics talent, extracted those capabilities for its electrification strategy, and then distributed the remaining fuel systems and aftermarket assets to shareholders as a separate company. It was a masterclass in corporate portfolio management—acquiring for the pieces, keeping what you need, and spinning off the rest. Whether the shareholders who received PHINIA shares in the distribution appreciated the elegance of the maneuver is another question entirely.

The Spin-Off Decision: Creating Two Focused Companies

The theory behind the PHINIA spin-off was elegant: create two industry-leading companies, each with a clear strategic identity. BorgWarner would become a focused electrification leader with a retained combustion portfolio optimized for cash generation. PHINIA would become a product leader in fuel systems and aftermarket distribution, free to invest in its core businesses without competing for capital against electrification initiatives.

The numbers justified the separation. In 2022, the businesses that would become PHINIA generated $3.6 billion in revenue—roughly 21 percent of total BorgWarner revenue—with an adjusted operating profit margin of 14.5 percent. These were not distressed assets being dumped. They were profitable, cash-generative businesses with strong market positions. The problem was not performance; it was narrative. Inside BorgWarner, combustion-related businesses competed for capital and management attention against electrification programs that Wall Street was desperate to reward. Outside BorgWarner, investors looking for EV exposure did not want combustion assets dragging down their multiple.

PHINIA's founding rationale rested on a specific, data-driven thesis about the global vehicle parc—the total population of vehicles on the road worldwide. Management's view, backed by industry forecasts from IHS Markit and others, was that the global vehicle fleet would remain predominantly combustion-based through at least 2040. Even in the most aggressive EV adoption scenarios, billions of ICE vehicles would need fuel systems, replacement parts, starters, alternators, and diagnostic equipment for decades to come. PHINIA was being built to serve that installed base.

But the market did not see it that way. When PHINIA shares began trading, the stock experienced what industry observers describe as epic indiscriminate selling. The dynamics were mechanical and predictable but brutal nonetheless. BorgWarner shareholders who had bought in for the electrification story suddenly found themselves holding shares in a pure-play ICE company they never asked for. Index funds that tracked benchmarks where PHINIA did not qualify had to sell. ESG-focused funds with fossil fuel exclusion policies had to sell. Momentum traders who saw the selling stampede joined in. The result was a stock that entered the public markets under enormous technical selling pressure, completely disconnected from its underlying business fundamentals.

Into this maelstrom stepped Brady Ericson, who brought a rare combination of institutional knowledge and strategic conviction. Ericson held a mechanical engineering degree from Kettering University and an MBA from Duke. He had joined BorgWarner in 2000 and spent 23 years rising through the organization, holding roles across operations, manufacturing strategy, engineering, and sales, with overseas assignments in four countries across Europe and Asia. He served as an officer of BorgWarner from 2011 to 2023 and led three separate business units as President and General Manager. Most recently—and crucially—he had served as the executive responsible for the exact Fuel Systems and Aftermarket segments that became PHINIA. Before BorgWarner, Ericson held positions at Ford Motor Company, at Remy International (the Delco Remy business that would eventually find its way into PHINIA), and at Honeywell. He knew these businesses intimately, not as an outsider parachuting in, but as someone who had helped build them.

Ericson's public conviction was unambiguous: internal combustion engine technologies would remain a key pathway to carbon neutrality for decades, and the transition to full electrification would take longer and prove more complex than consensus expected. This was not a defensive posture. It was the founding thesis of the company—and the willingness to stand behind it, publicly and repeatedly, at a moment when the entire investment community was moving in the opposite direction, was either courageous or foolish, depending on whom you asked.

The founding challenge was immense: establish corporate independence—IT systems, HR functions, treasury operations, investor relations, board governance—while simultaneously maintaining the operational excellence that had produced those 14.5 percent margins. Spin-offs often stumble in the early quarters as standalone costs emerge and management attention is divided between running the business and building the corporate infrastructure. PHINIA would need to avoid those traps while simultaneously telling a persuasive story to a skeptical market.

Business Model: The Three-Legged Stool

Walk into a modern engine test facility—the kind of place where technicians in white coats monitor screens displaying combustion chamber pressure curves and exhaust gas composition in real time—and you will encounter PHINIA's products at nearly every stage of the fuel delivery process. The fuel pump that pressurizes gasoline to extraordinary levels. The fuel rail that distributes it. The injectors that spray precisely metered quantities into combustion chambers thousands of times per minute. The engine control module that orchestrates the entire symphony. The software and calibration data that ensure the engine meets emissions standards in Shenzhen and Stuttgart and São Paulo.

PHINIA's Fuel Systems segment is the larger of its two reporting segments, accounting for roughly sixty percent of total revenue. The business provides advanced fuel injection systems encompassing pumps, injectors, fuel rail assemblies, engine control modules, and—critically—complete systems with software and calibration services. This last point deserves emphasis. PHINIA does not merely sell components. It sells integrated solutions that reduce emissions and enhance fuel economy, which means its engineering teams work intimately with OEM customers during the multi-year development cycle for new engine platforms.

The crown jewel of the Fuel Systems portfolio is the company's gasoline direct injection technology, particularly the 500-bar GDi system. To understand why this matters, consider the basic physics: in a direct injection engine, fuel must be sprayed directly into the combustion chamber at extremely high pressure to achieve the fine atomization needed for clean, efficient combustion. Five hundred bar is roughly 7,250 pounds per square inch—imagine the pressure at the bottom of a column of water over eleven thousand feet deep. At these pressures, PHINIA's M16 injector family can deliver full static flow rates of ten to forty grams per second with shot-to-shot precision, reducing exhaust particulate emissions and lowering fuel consumption without costly engine redesigns. Think of it as the difference between a garden hose and a surgical instrument: the higher the precision of fuel delivery, the cleaner and more efficient the combustion.

The Aftermarket segment is the second leg of the stool and, in many ways, the more strategically interesting one. This business sells starters, alternators, remanufactured products, maintenance items, test equipment, and vehicle diagnostics solutions through two channels: OES (Original Equipment Supplier/Service, meaning parts sold back through OEM dealer networks) and IAM (Independent Aftermarket, meaning parts distributed through wholesale distributors and independent repair shops globally). PHINIA targets aftermarket revenue at over forty percent of total sales—a goal that reflects management's understanding that aftermarket parts are less cyclical than OE production, carry higher margins, and benefit from the enormous global installed base of ICE vehicles.

Remanufacturing deserves its own moment. Approximately ten percent of PHINIA's revenue comes from taking used cores—returned starters, alternators, and other components—and restoring them to meet original quality standards. This is not simply refurbishment. It is a sophisticated manufacturing process that involves disassembly, inspection, cleaning, replacement of worn components, reassembly, and testing to ensure the remanufactured product meets or exceeds original specifications. The economics are compelling: lower material costs than new production, higher margins, and a sustainable positioning that resonates with both customers and ESG-conscious stakeholders.

The third leg is end-market diversification. PHINIA serves commercial vehicles and industrial applications—medium-duty and heavy-duty trucks, buses, off-highway construction equipment, marine vessels, agricultural machinery, and industrial applications—as well as light commercial vehicles and light passenger vehicles. The strategic direction is clear: reduce exposure to light passenger vehicles, where EV substitution will arrive first, and increase exposure to commercial vehicles and industrial applications, where electrification faces far steeper physics and economics challenges. Management has targeted a light vehicle mix of approximately thirty percent by 2030, down from roughly a third of revenue at the time of the spin-off.

The revenue mix at the spin-off told the story: 44 percent commercial vehicles and other OE, 32 percent light vehicle OE, and 24 percent OES and independent aftermarket. Geographically, the Americas contributed 41 percent, Europe 39 percent, and Asia-Pacific 20 percent. This is a genuinely global business—43 manufacturing and distribution facilities across 20 countries, over 12,500 employees, and customer relationships reaching into repair shops on every major continent.

What makes the three-legged stool strategically elegant is how the pieces reinforce each other. OE fuel systems business creates the installed base. The installed base creates aftermarket demand. Aftermarket distribution creates brand visibility and customer relationships. Remanufacturing creates a circular revenue stream from previously sold OE parts while providing environmentally sustainable products at lower price points. And the engineering expertise required for OE fuel injection development feeds directly into alternative fuel technology—the same engineers who optimize gasoline direct injection at 500 bar can adapt those skills to hydrogen direct injection. It is a flywheel, not a collection of unrelated businesses, and that interconnection is what management means when they describe PHINIA as a "product leader" rather than a "component supplier."

The company also launched the Delphi Training Academy in 2024, previewing it at the AAPEX trade show—North America's largest automotive aftermarket event. The academy provides technician training on fuel injection diagnosis and repair, creating yet another connection between the OE engineering knowledge and the aftermarket service ecosystem. When an independent mechanic learns to diagnose fuel injection issues using PHINIA's curriculum and Hartridge's test equipment, the likelihood of that mechanic specifying Delphi replacement parts increases substantially. It is a subtle but effective form of demand creation that competitors without the full OE-to-aftermarket chain cannot replicate.

The Existential Question: Timing the EV Transition

Every investor who looks at PHINIA sees the same headline risk immediately: electric vehicles are coming, internal combustion is dying, and this company is yesterday's technology wrapped in a new corporate structure. It is the obvious bear case, and it deserves serious engagement rather than dismissal.

But the bear case contains an assumption that is doing enormous load-bearing work: the word "timing." The question is not whether EVs will eventually capture a significant share of new vehicle sales—they will. The question is how quickly, how completely, and how uniformly across geographies and vehicle segments. The gap between "EVs are the future" and "EVs will dominate global vehicle sales by 2030" is a chasm measured in trillions of dollars of investment, hundreds of millions of vehicles, and decades of transition.

PHINIA's management has been refreshingly direct about their positioning. The company has stated plainly that it is not participating in battery electric vehicles on the OE side. Instead, it focuses on making combustion engines more efficient today while helping transition to carbon-free and carbon-neutral fuels tomorrow. This is not a hedge or a hedge-the-hedge. It is a clear strategic choice that accepts the long-term direction of travel while betting that the journey will be far longer and more complex than consensus expects.

The evidence increasingly supports this view. Since 2022, the EV adoption timeline has been recalibrated repeatedly. Major automakers including Ford, General Motors, Mercedes-Benz, and Volkswagen have scaled back or delayed their electrification targets. Battery costs, which had been declining steadily, plateaued and in some cases increased. Charging infrastructure deployment has lagged projections, particularly outside of China and Northern Europe. Consumer adoption in the United States stalled at roughly eight to ten percent of new vehicle sales, well below the penetration rates that aggressive forecasts had projected for the mid-2020s.

The global vehicle parc tells an even more compelling story. There are approximately 1.4 billion internal combustion engine vehicles on the road worldwide. Even in the most optimistic EV adoption scenarios, the vast majority of these vehicles will continue operating for ten to twenty years, and every one of them needs fuel system components, replacement parts, starters, alternators, and periodic maintenance. The parc does not disappear when the last ICE vehicle rolls off an assembly line—it lingers for decades, and the companies that serve it have a long runway of demand.

Regional variation adds another layer of complexity. In Western Europe and parts of China, EV adoption has progressed rapidly, aided by generous subsidies, dense charging networks, and regulatory mandates. But in much of Asia, Africa, South America, and even large swaths of North America, ICE vehicles remain critical because affordability and infrastructure constraints make electric alternatives impractical for most buyers. A farmer in sub-Saharan Africa, a long-haul trucker in Brazil, or a construction equipment operator in Indonesia is not switching to battery electric in the foreseeable future.

The commercial vehicle segment presents the starkest physics challenge for electrification. A Class 8 long-haul truck covering 500 miles per day would require a battery pack so large and heavy that it would consume a significant portion of the payload capacity that makes trucking economically viable. Marine vessels, construction equipment, and agricultural machinery face similar constraints—high energy density requirements, demanding duty cycles, remote operating environments, and economic models that depend on maximum uptime and rapid refueling.

There is a myth-versus-reality dimension to this discussion that deserves unpacking. The myth, prevalent in mainstream financial media, is that the ICE-to-EV transition is a binary switch—one day combustion, the next day electric, and companies on the wrong side of that switch are doomed. The reality is far messier. Hybrid vehicles—which use both ICE and electric powertrains and still require fuel injection systems—are experiencing a resurgence as consumers and automakers acknowledge the limitations of pure battery electric vehicles in certain applications. Plug-in hybrids, which PHINIA's fuel systems also serve, represent a growing middle ground. And the emerging category of range-extended electric vehicles—which use a small ICE generator to charge the battery, extending range without requiring charging infrastructure—creates entirely new demand for compact, efficient fuel injection systems.

Consider the math another way. Global new vehicle production runs at approximately 85 to 90 million units per year. Even if EVs capture thirty percent of that by 2030—an aggressive assumption—that still leaves sixty million new ICE and hybrid vehicles rolling off assembly lines annually, each one needing fuel injection systems, engine management electronics, and electrical components. And every one of those vehicles will eventually need replacement parts for the fifteen to twenty years it operates on the road.

PHINIA's strategic positioning amounts to a calculated bet that the transition to full electrification will take longer than initially anticipated, and that the growing recognition of continued importance of efficient ICE technologies in the medium term creates a substantial business opportunity. If the bet is right, PHINIA operates in a consolidating market with declining competition and increasing pricing power. If the bet is wrong—if EV adoption accelerates dramatically and battery technology breakthroughs eliminate the physics constraints in commercial vehicles—PHINIA's core business enters terminal decline faster than expected. The entire investment thesis hangs on this timing question.

The Hydrogen Pivot: Building Tomorrow's Technology Today

In a testing facility somewhere in northern Europe during the first quarter of 2024, a light commercial vehicle loaded to capacity pulled away from a hydrogen refueling station and began a journey designed to answer a simple but consequential question: Could a hydrogen-powered internal combustion engine deliver the real-world performance that commercial operators demand?

Over the next twelve hours, the vehicle covered more than 1,000 kilometers in challenging winter conditions, with temperatures dropping to minus four degrees Celsius. It demonstrated a driving range of over 500 kilometers per fill, performance on par with its diesel counterpart, and significantly reduced NOx emissions. And when it needed to refuel, it did so in minutes—not the hours required by battery electric alternatives.

This was PHINIA's coming-out party for hydrogen internal combustion engine technology, and it matters enormously for the company's long-term narrative. The H2ICE concept is elegantly practical: take existing internal combustion engine architectures—the same basic engine blocks, cylinder heads, and drivetrain components that manufacturers have spent decades optimizing—and modify the fuel delivery system to run on hydrogen instead of gasoline or diesel. The combustion of hydrogen produces water vapor instead of carbon dioxide, making it a zero-carbon fuel at the point of use. And because the engine architecture remains familiar, manufacturers can adapt existing production lines and supply chains rather than starting from scratch with entirely new battery electric platforms.

PHINIA has developed a family of direct injection hydrogen fuel injectors under the DI-CHG brand name. The DI-CHG10, designed for power ranges up to 60 kilowatts per cylinder, is package-compatible with current 7.5-millimeter tip gasoline direct injectors—meaning it can fit into engine designs originally intended for gasoline with minimal modification. The larger DI-CHG15, with a 9.8-millimeter tip, extends the potential power range to 90 kilowatts per cylinder, suitable for larger commercial vehicle applications. The materials are specifically engineered to prevent hydrogen embrittlement—the phenomenon where hydrogen atoms diffuse into metals and cause them to become brittle and crack, a critical challenge in hydrogen applications that requires specialized metallurgy.

The KGM partnership, announced on April 16, 2025, brought the hydrogen strategy into sharper focus. KG Mobility—formerly SsangYong Motor Company, the South Korean OEM known for SUVs and light commercial vehicles—signed a Technical Cooperation Agreement with PHINIA to develop a 2.2-liter hydrogen internal combustion engine for light commercial vehicles. The concept is strategically brilliant: take KGM's existing diesel LCV engine architecture and adapt it to run on hydrogen using PHINIA's fuel injection, engine control unit, and fuel rail technology. The roadmap extends through multi-purpose engine and vehicle design, performance development, and eventually the base design of an Extended Range Electric Vehicle variant.

The advantages of H2ICE over battery electric are particularly compelling for commercial applications. Rapid refueling measured in minutes rather than hours is critical for vehicles that need to maximize uptime and revenue-generating miles. The powertrain is lighter than a battery electric equivalent—the innovative rail, injector, and control systems allow efficient use of hydrogen without the bulky battery packs that add thousands of pounds to BEV commercial vehicles. For the transport and haulage industry, where payload capacity directly determines profitability, this weight advantage translates directly to competitive advantage.

PHINIA's R&D spending tells the story of where management sees the future. In 2024, 89 percent of R&D was dedicated to fuel efficiency and alternative fuel technologies, with approximately thirty percent of that allocated to zero- and low-carbon fuel systems including hydrogen. The SEM acquisition, completed on August 1, 2025, for $47 million added another critical piece: SEM, a Gothenburg-based company founded in 1915, brought advanced ignition systems for natural gas, hydrogen, and other alternative fuels. This made PHINIA a full-system provider for hydrogen ICE powertrains—fuel injection, engine management, and now ignition, all from one supplier.

The broader alternative fuels portfolio extends well beyond hydrogen. PHINIA has systems for compressed natural gas, liquefied natural gas, ethanol, methanol, and various bio-fuels. This multi-fuel capability is not a marketing exercise—it reflects the engineering reality that different regions and applications will adopt different alternative fuels based on local energy resources, infrastructure, and economics. A bus fleet in New Delhi might run on compressed natural gas. A fishing fleet in Scandinavia might use liquefied natural gas. Sugar cane trucks in Brazil might run on ethanol. PHINIA's engineering platform can serve all of these use cases, creating diversified exposure to the alternative fuel transition regardless of which specific pathway wins in each market.

The hydrogen thesis does carry real risk, and it would be dishonest to minimize it. Hydrogen infrastructure is nascent at best. Production of green hydrogen—made from renewable electricity via electrolysis—remains expensive, typically two to three times the cost of gray hydrogen produced from natural gas. Storage and distribution present engineering and economic challenges—hydrogen is the smallest molecule in the universe and notoriously difficult to contain. The chicken-and-egg problem is real: vehicle manufacturers hesitate to produce H2ICE vehicles without refueling infrastructure, while infrastructure investors hesitate to build stations without a vehicle fleet to serve.

But for PHINIA, hydrogen is not a bet-the-company gamble. It is an option—a relatively low-cost investment that leverages existing engineering capabilities and manufacturing infrastructure to create exposure to what could become a significant growth market. The R&D spending on zero- and low-carbon fuel systems represents roughly thirty percent of an R&D budget that is itself a modest percentage of revenue. If hydrogen takes off, PHINIA has a first-mover advantage and a full-system capability that no competitor can match. If it does not, the investment has still produced improved conventional fuel injection technology, deepened engineering relationships with OEM customers, and created intellectual property that has applications beyond hydrogen alone.

The Circular Economy Play: Remanufacturing as Moat

There is something deeply satisfying about the economics of remanufacturing, and PHINIA leans into it with the enthusiasm of a company that has discovered the rare business model that is simultaneously more profitable, more sustainable, and more strategically defensible than its alternative.

The company has saved an estimated 10,000 tons of auto parts from landfills through its remanufactured parts programs—taking used starters, alternators, and other components, disassembling them down to their constituent parts, inspecting and cleaning each element, replacing worn components, reassembling to original specifications, and testing to ensure the finished product meets or exceeds new-product performance standards. This is not a side business or a corporate social responsibility talking point. It is embedded in the company's operational DNA, representing roughly ten percent of total revenue and contributing margins that exceed those of new-part manufacturing.

The economic logic is compelling at every level. Raw material costs are lower because the core—the basic casting or housing—is reused rather than manufactured from scratch. Energy consumption is lower because smelting, casting, and primary machining are avoided. And the customer gets a product that performs identically to new at a lower price point, creating value on both sides of the transaction.

But the strategic dimension is what makes remanufacturing a genuine moat rather than merely a profitable business line. As the global vehicle fleet ages—which it inevitably will as OEMs shift production capacity toward electric vehicles and reduce investment in new ICE platforms—the demand for replacement parts will persist and in many segments actually grow. Cars in emerging markets are kept on the road far longer than in developed economies. Commercial trucks operate for fifteen to twenty years or more. Off-highway equipment in mining and construction runs for decades. As people transition toward EVs in their next vehicle purchase, the existing ICE vehicles on the road do not disappear—they need maintenance, repairs, and replacement components. Remanufacturing becomes the critical link in keeping that installed base running.

There is a structural advantage here that deserves emphasis. As OEMs reduce their investment in ICE technology and wind down production of combustion-engine components, the availability of new replacement parts will gradually decline. Independent aftermarket suppliers who depend on OEM-sourced components will face supply constraints. But a company with an established remanufacturing ecosystem—collection networks, reverse logistics, skilled labor, testing infrastructure—can continue supplying parts from the existing pool of cores long after new production ceases. This is the parc management business model in its purest form: making money from keeping existing vehicles running, and becoming more valuable precisely because others are exiting the market.

The brand dimension amplifies this advantage. In commercial and industrial markets, where a failed starter or alternator can mean thousands of dollars in downtime for a fleet operator, reliability and quality consistency are worth paying a premium for. Delco Remy starters on a Class 8 Peterbilt, Delphi fuel injectors on a Caterpillar excavator, Hartridge test equipment in a service shop—these are trusted names backed by decades of field performance data. That trust does not transfer easily to newcomers, and it creates the kind of quiet, compounding competitive advantage that rarely shows up in analyst models.

There is also a workforce dimension to remanufacturing that creates a subtle moat. The skilled technicians who can disassemble, diagnose, and rebuild complex electromechanical components like starters and alternators are increasingly scarce. The automotive industry faces a widening skills gap from an aging workforce and declining vocational training enrollment. A company with an established remanufacturing workforce, training programs, and institutional knowledge has a human capital advantage that cannot be acquired overnight. PHINIA's remanufacturing operations in South America—including the multi-year contract signed in 2024 with a major commercial vehicle OEM—demonstrate that this capability can be deployed globally, serving markets where the economics of remanufacturing are even more compelling because new-part costs are higher relative to local purchasing power.

For investors, the remanufacturing business answers a critical question: What happens to PHINIA's revenue when new ICE vehicle production eventually declines? The answer is that the aftermarket and remanufacturing businesses become proportionally larger, more important, and potentially more profitable. It is a natural hedge built into the business model—the longer ICE vehicles stay on the road without new models being produced, the more valuable the company that can keep them running becomes.

Navigating Headwinds and Strategic Moves

PHINIA's first years as an independent company have not been a smooth ride, and the honesty about that is part of what makes the story credible.

The commercial vehicle market, which represents the largest single end-market exposure for PHINIA, experienced significant weakness in 2024 and into 2025. In Europe, new registrations of heavy-duty trucks fell for the first time since the pandemic year of 2020. North American trucking struggled under the weight of depressed freight rates, causing transport companies to postpone fleet investment. China, the world's largest truck market, also softened. The direct impact showed up in PHINIA's numbers: the Fuel Systems segment saw net sales decline seven percent in 2024, with lower commercial vehicle sales across all major regions as the primary driver.

Management's response was characteristic of a team that had spent decades in cyclical industrial businesses: lean into what you can control, protect margins, and use the downturn to strengthen competitive positioning. The aftermarket business, with its higher margins and lower cyclicality, partially offset the OE weakness—exactly the portfolio balance that the company's strategic design intended. Full-year 2024 adjusted operating income held flat year-over-year at $346 million despite the revenue decline, demonstrating cost discipline and mix improvement.

The tariff landscape added another layer of complexity. When the U.S. administration imposed 25 percent tariffs on automobiles and auto parts not meeting USMCA origin criteria, PHINIA faced direct exposure. However, the company's positioning proved more resilient than feared. The majority of PHINIA's North American business was already USMCA compliant, and over half of revenues from North American operations stayed within the country of manufacture—products made in the U.S. sold to U.S. customers, products made in Mexico sold to Mexican customers. For the cross-border exposure that did exist, PHINIA moved quickly: the company absorbed approximately $4 million in tariff costs in the first quarter of 2025 while negotiating customer pass-throughs, then implemented tariff tracking in invoices and IT systems to enable seamless auditing. By the second half of 2025, tariff recoveries were flowing through as a revenue line item, and management stated at the fourth-quarter earnings call that they expected tariffs to "come out even" going forward. The USMCA itself faces a scheduled review in 2026, adding a layer of policy uncertainty that the company continues to monitor.

On the acquisition front, PHINIA has been disciplined but active. The SEM acquisition in mid-2025 was purchased at roughly 4.7 times EBITDA—a multiple that highlights the kind of undervalued opportunities available in niche ICE technology markets where sellers face strategic pressure to exit and buyers are scarce. SEM's $50 million in expected annual revenue and $10 million in expected EBITDA added meaningful capability at a modest price. Beyond SEM, management has articulated a three-pronged acquisition framework: organic development where PHINIA already has the capabilities, acquiring OE businesses that carry significant aftermarket revenue streams, or acquiring pure aftermarket manufacturing businesses to fill portfolio gaps. The strategy is opportunistic rather than transformational—tuck-ins that strengthen the existing platform rather than bold bets that change the company's character.

PHINIA has also published an industry-leading Global Emission Regulations guide—a comprehensive reference document tracking emissions standards across every major market worldwide. This might seem like a mundane corporate publication, but it serves a strategic purpose: it positions PHINIA as the authoritative knowledge source on the regulatory landscape that drives demand for its products. Every tightening of emissions standards creates demand for more precise fuel injection, more sophisticated engine management, and more advanced calibration—all of which are PHINIA's core competencies. By helping OEM customers navigate the regulatory maze, PHINIA deepens its role as an indispensable engineering partner.

The company also expanded its geographic reach in 2024 and 2025, developing new distributor relationships in Southeast Asia—a region where the vehicle parc is growing rapidly, infrastructure for EVs is minimal, and the demand for affordable, efficient ICE powertrain components and replacement parts is substantial. This geographic expansion into emerging markets aligns perfectly with the thesis that ICE vehicles will remain the dominant transportation technology in developing economies for decades.

The 2025 full-year results showed a company finding its footing. Revenue recovered to $3.48 billion, up 2.4 percent from 2024. Net earnings improved meaningfully to $130 million, a $51 million increase year-over-year. The fourth quarter was particularly encouraging, with revenue of $889 million—up nearly seven percent year-over-year—and net earnings of $45 million, a dramatic improvement from the prior year's fourth quarter. The 2026 guidance range of $3.52 billion to $3.72 billion in net sales and $485 million to $525 million in adjusted EBITDA implies management sees the commercial vehicle market stabilizing and aftermarket growth continuing, with margins returning toward the 14 percent-plus levels that the business generated before the commercial vehicle downturn.

Competitive Positioning and Market Dynamics

Here is the counterintuitive competitive dynamic at the heart of PHINIA's thesis: its most important competitors are not Tesla or Rivian or any other EV manufacturer. They are the other ICE component suppliers—the companies that are actively divesting their combustion businesses while PHINIA is investing in them.

The automotive supply chain is experiencing an unprecedented strategic divergence. On one side, major suppliers like Continental, ZF, and others are redirecting capital from combustion to electrification, reducing R&D budgets for ICE platforms, and in some cases actively seeking buyers for their combustion-related divisions. On the other side, PHINIA is doubling down—investing in next-generation fuel injection technology, developing hydrogen ICE systems, expanding aftermarket distribution, and acquiring niche ICE technology companies at attractive multiples.

This divergence creates what may be PHINIA's most powerful competitive advantage. When a major OEM needs a partner to develop a new fuel injection system for a next-generation diesel truck engine, the list of suppliers willing and able to commit the engineering resources, manufacturing capacity, and multi-year development effort is shrinking. PHINIA, as a company whose entire strategic identity is built around fuel systems and aftermarket excellence, can offer the commitment and focus that a diversified supplier in the middle of an electrification pivot cannot. Every competitor that exits ICE development creates a potential market share opportunity for PHINIA.

The customer relationships compound this advantage. PHINIA's key OEM customers include names like PACCAR, Volvo Trucks, Daimler Trucks, Hyundai, Volkswagen, Caterpillar, Ford, BMW, Dongfeng Motor, General Motors, Stellantis, and CNH Industrial. These relationships, built over decades of engineering collaboration, involve deep technical integration—calibration data shared between PHINIA's engine control modules and OEM engine management systems, co-developed fuel injection strategies optimized for specific combustion chamber geometries, quality validation programs that take years to complete. Switching costs are real and significant, and they increase rather than decrease as other suppliers exit the market and the pool of qualified alternatives shrinks.

The distribution network provides a third layer of advantage. PHINIA's global footprint—43 facilities across 20 countries, distribution relationships reaching into independent repair shops on every major continent—represents decades of accumulated commercial infrastructure. In the aftermarket business, where the ability to deliver the right part to the right shop in the right country within days matters enormously, this network is a genuine barrier to entry.

Technology leadership in specific niches reinforces the position. The 500-bar GDi system, the hydrogen direct injection technology, the precision calibration capabilities, Hartridge's unmatched test equipment portfolio—these are not commodity products. They represent the frontier of what is possible in internal combustion engine efficiency, and the engineering expertise behind them cannot be replicated quickly by a new entrant.

The consolidation opportunity ties the competitive picture together. PHINIA can be the buyer when others are selling—picking up niche technology companies like SEM at distressed multiples, acquiring market share from competitors who are reducing their ICE commitment, and potentially absorbing larger divested business units from companies executing electrification pivots. Being willing to buy what others want to sell, at prices that reflect the sellers' urgency rather than the assets' intrinsic value, is a powerful strategy in a dislocating market.

Porter's Five Forces and Hamilton's Seven Powers Analysis

Understanding PHINIA's competitive position requires examining the structural forces shaping its industry and the strategic powers the company possesses—or lacks.

Starting with the threat of new entrants: the barriers to entering PHINIA's core markets are substantial. Designing a fuel injection system that meets modern emissions standards requires years of engineering development. Validating that system with a major OEM involves exhaustive testing cycles that typically span three to five years. Building the manufacturing capability to produce components at the required precision tolerances—we are talking about injector nozzle holes measured in microns—demands significant capital investment and deep process expertise. And establishing the global distribution network needed to serve aftermarket customers requires decades of relationship building. However, there is a countervailing force: as major OEMs reduce their own ICE investment, the traditional barriers created by long-term OEM partnerships may weaken, potentially opening doors to new suppliers in niche segments.

Supplier bargaining power is moderate. PHINIA operates a global supply base, but the precision manufacturing components at the heart of fuel injection systems—specialty alloys, micro-machined orifice plates, high-performance electromagnetic materials—have limited sources. PHINIA's approximately $3.5 billion in annual revenue provides meaningful negotiating leverage, but the company remains dependent on specialized suppliers for critical inputs.

Buyer bargaining power is the most nuanced force. On the OE side, PHINIA's customers are large, concentrated, and technically sophisticated—PACCAR, Daimler Trucks, Caterpillar, BMW. These buyers have significant leverage in negotiations, particularly on pricing. But the switching costs created by years of engineering co-development, validated calibration data, and production tooling create meaningful countervailing power for PHINIA. The aftermarket side is more favorable: distributors and independent repair shops are far more fragmented, brand loyalty matters more, and PHINIA's diagnostic equipment ecosystem creates additional stickiness.

The threat of substitutes is, of course, the defining strategic question. Electric vehicle powertrains are the ultimate substitute for everything PHINIA makes. But the timing uncertainty is the crucial variable. In light passenger vehicles, the substitution threat is real and growing. In heavy-duty commercial vehicles, marine, construction, and agricultural applications, the substitution timeline is measured in decades rather than years. And alternative fuels—hydrogen, biofuels, synthetic fuels—create a potential pathway where PHINIA's products evolve rather than become obsolete, converting the substitution threat into a growth opportunity.

Competitive rivalry is moderate and moderating. As suppliers exit ICE, the industry is consolidating, and the remaining players face less direct competition. Price competition remains a factor, particularly in light vehicle applications, but technology differentiation—GDi systems, alternative fuel capability, systems integration expertise—allows PHINIA to compete on value rather than purely on cost. The commercial vehicle and aftermarket segments, where PHINIA is deliberately concentrating, are structurally less competitive than the light vehicle OE space.

Turning to Hamilton Helmer's Seven Powers framework, PHINIA's strategic position reveals interesting patterns. The company's strongest power is counter-positioning—the willingness to invest aggressively in ICE technology while the rest of the industry pivots to electrification. Pure-play EV suppliers cannot and will not invest in the technologies PHINIA is developing. OEMs that have publicly committed to electrification timelines cannot easily reverse course without damaging their credibility with investors and regulators. PHINIA's willingness to be the "last man standing" in ICE technology development is directly counter to the prevailing industry narrative, and if the EV transition proves slower than consensus expects, this counter-positioning becomes enormously valuable.

Branding power is strong in specific segments. Delphi, Delco Remy, and Hartridge are premium brands with century-long reputations in markets where reliability is worth paying for. A fleet operator choosing starters for a hundred-truck fleet is not gambling on an unknown brand to save a few dollars per unit. The commercial and industrial markets value proven reliability over cost optimization, and aftermarket professionals—the mechanics and technicians who specify replacement parts—develop brand loyalties that persist for careers.

Process power is moderate to high. Decades of manufacturing optimization in precision fuel injection, remanufacturing operational excellence, and calibration and systems integration capabilities represent accumulated institutional knowledge that is difficult to replicate. These are not patented technologies that a competitor can license—they are embedded in organizational routines, supplier relationships, and workforce skills built over generations.

Switching costs provide moderate to high protection. The engineering validation, calibration integration, and quality certification required to qualify a new fuel injection supplier for an OEM platform take years to complete. But this power diminishes as OEMs wind down ICE platforms—there are fewer new platforms to win, which means fewer opportunities for switching costs to compound.

Scale economies are present but not dominant. PHINIA's roughly $3.5 billion in revenue provides procurement leverage and fixed cost absorption, and the remanufacturing network benefits from scale in core collection and reverse logistics. But this is not a winner-take-all market, and scale advantages are moderate rather than decisive.

Network effects are limited. The Hartridge diagnostic equipment ecosystem has some network properties—shops that invest in Hartridge test benches prefer Hartridge-compatible components—and the aftermarket distribution network benefits modestly from breadth. But these are not the self-reinforcing feedback loops that characterize true network effect businesses.

The summary view: PHINIA's strongest powers are counter-positioning, branding, and emerging cornered resource status in hydrogen ICE technology. The central risk is timing. If EV adoption accelerates faster than expected, these powers erode rapidly—counter-positioning becomes stubbornness, brand equity in ICE components loses relevance, and hydrogen technology arrives too late to matter. If the transition proves slower and more complex than consensus assumes, PHINIA's position strengthens with each passing year.

Bull vs. Bear: The Investment Debate

The investment debate around PHINIA is as polarized as any in the automotive sector, and both sides have arguments worth taking seriously.

The bull case begins with valuation. PHINIA traded at approximately six times EV/EBITDA through much of its independent life—a meaningful discount to peers like BorgWarner at seven to eight times and Tenneco at six to seven times. That discount reflects investor skepticism about the ICE-centric business model, but bulls argue it overcompensates for a risk that is far more distant and uncertain than the market implies. The stock has appreciated significantly from its post-spin-off lows, rising from a 52-week low of $36.25 to a range around $75 by early 2026, suggesting the market is beginning to recalibrate—but bulls see further upside as the EV timeline continues to slip.

The aftermarket business is the bull's anchor. Replacement parts demand is tied to the installed base of vehicles, not new vehicle production—making it inherently less cyclical and more predictable than OE revenue. As the global ICE parc ages and OEMs reduce their own aftermarket parts production, PHINIA's position as a reliable supplier of high-quality replacement components becomes more valuable, not less. This is a business that can generate attractive cash flows for fifteen to twenty years even in a scenario where ICE new vehicle production declines steadily.

Capital allocation adds fuel to the bull case. Since the spin-off, PHINIA repurchased approximately 21 percent of its outstanding shares—an aggressive buyback pace that signals management's conviction that the stock is undervalued. Total share repurchase authorizations reached $750 million by early 2026. The dividend has been increased twice—from $0.25 per quarter to $0.27, then to $0.30—an eleven percent increase in the most recent bump. Strong free cash flow generation provides the fuel for both shareholder returns and opportunistic M&A.

The hydrogen option provides the bull's growth narrative. If hydrogen infrastructure develops and H2ICE gains traction as a decarbonization pathway for commercial vehicles, PHINIA's early investment in hydrogen fuel injection technology could unlock a growth market that the current valuation assigns zero value to. The SEM acquisition and KGM partnership demonstrate that real commercial activity is developing around H2ICE, not merely theoretical research.

The bear case starts with the macro trend. Fighting the EV mega-trend is a losing battle in the long run, bears argue, drawing parallels to coal companies that generated impressive cash flows for years while their industry entered terminal decline. Heavy reliance on ICE technologies makes PHINIA vulnerable to rapid shifts in adoption curves—and technology transitions, once they reach a tipping point, can accelerate faster than anyone expects.

Technology risk compounds the concern. Hydrogen infrastructure may never materialize at the scale needed to make H2ICE commercially significant. The chicken-and-egg problem—vehicles need refueling stations, but stations need vehicles—has stalled other alternative fuel technologies before. If battery technology continues improving and costs continue declining, the window for hydrogen ICE may close before it fully opens.

OEM customer dynamics present another bear concern. As automakers cut ICE R&D budgets and wind down combustion platforms, the opportunities for PHINIA to win new OE programs diminish. Each platform that transitions from ICE to BEV is a revenue stream that PHINIA permanently loses. The aftermarket can sustain revenue for years, but without new OE programs feeding the pipeline, the aftermarket eventually starves too.

The valuation discount may be entirely justified by terminal value concerns. Traditional discounted cash flow models struggle with a company whose revenue base may be in structural decline within a decade. What discount rate do you apply to a business whose terminal value might be zero? How do you model aftermarket revenue for vehicle platforms that will eventually age out of the operating fleet? These are genuinely difficult analytical questions, and the market's hesitation to pay a premium multiple for PHINIA reflects the intellectual honesty of acknowledging that ICE technology has a finite commercial lifespan, even if the exact expiration date is unknown.

There is also an ESG headwind that bears emphasize. As ESG-focused investing has grown, funds with fossil fuel exclusion policies have excluded ICE-focused companies like PHINIA from their investable universes. This reduces the buyer pool for PHINIA shares and may create a structural valuation discount that persists regardless of fundamental performance. The company's relatively small market capitalization—roughly $3 billion—further limits institutional investor interest, as many large funds have minimum market cap thresholds that PHINIA barely clears.

Competition from low-cost manufacturers in markets perceived as declining is another risk. As the ICE supply chain contracts, Chinese and other Asian manufacturers may aggressively price into remaining demand, particularly in light vehicle applications where PHINIA's technology differentiation is less pronounced than in commercial vehicles. Price wars in a declining market would compress margins and accelerate the timeline to obsolescence.

The realistic case—the one most sophisticated investors likely hold—sits between these extremes. The "stronger for longer" theme for ICE vehicles appears validated, particularly in the United States and in commercial vehicle applications globally. Multiple transition pathways—hybrid, plug-in hybrid, hydrogen ICE, biofuels—extend PHINIA's relevance well beyond a simple ICE-versus-BEV binary. Success depends heavily on capital allocation discipline: making smart acquisitions at attractive prices, right-sizing manufacturing capacity as light vehicle OE volumes decline, and returning excess cash to shareholders rather than reinvesting in a business with a finite horizon. The company likely has a five-to-seven-year window to harvest cash flows aggressively before structural decline accelerates meaningfully. The hydrogen option adds genuine upside potential if that pathway gains traction, but it should be valued as an option, not a certainty.

For investors tracking PHINIA's progress, two key performance indicators matter most. First, aftermarket revenue as a percentage of total sales—management's target of over forty percent reflects the strategic shift toward the more resilient, higher-margin installed-base business. Progress toward this target indicates successful execution of the portfolio transformation. Second, adjusted EBITDA margin—the fourteen to fifteen percent range that management has targeted represents the operational discipline needed to maximize cash generation from a business with a potentially finite growth horizon. If margins slip below this range, it signals either competitive pressure or execution issues that would undermine the entire investment thesis.

Recent Developments and Current State

PHINIA held its 2026 Investor Day on February 25 at the New York Stock Exchange—a symbolically resonant venue for a company still establishing its identity in the investment community. Brady Ericson led the presentation alongside CFO Chris Gropp, Chief Technology Officer Todd Anderson, Global Aftermarket VP Neil Fryer, and Chief Strategy Officer Pedro Abreu. The themes—"Expanding in the right places," disciplined financial performance, shareholder returns, and "a portfolio built to last"—emphasized stability and strategic optionality over transformation or dramatic pivots.

The financial trajectory tells a story of a company finding its operational rhythm. After the commercial vehicle downturn pressured 2024 results, the 2025 recovery—revenues up to $3.48 billion, net earnings improving to $130 million, adjusted EBITDA holding at $478 million—demonstrated resilience. The 2026 guidance range of $3.52 billion to $3.72 billion in revenue and $485 million to $525 million in adjusted EBITDA implies management sees the commercial vehicle market stabilizing and aftermarket growth continuing.

The stock's journey from its post-spin-off doldrums tells its own story. From a 52-week low of $36.25 to a recent range around $75, the market has begun to reassess the indiscriminate selling that greeted PHINIA's birth. The market capitalization of roughly $3 billion still reflects meaningful skepticism about long-term prospects—but far less than the near-total dismissal that characterized the first months of trading.

Tariff navigation continues as a live issue, with the USMCA review in 2026 adding a layer of policy uncertainty. Management's demonstrated ability to implement cost pass-throughs and maintain margin discipline through the initial tariff disruption provides some confidence, but the risk of further escalation remains real.

The leadership team continues building out independent corporate functions—a process that is less dramatic than strategic pivots but no less critical for long-term success. Every spin-off faces the same challenge: the mundane but essential work of establishing IT infrastructure, treasury management, legal and compliance functions, investor relations capabilities, and corporate governance that were previously shared with the parent company. Doing this while maintaining operational performance is the blocking and tackling that separates successful spin-offs from those that stumble.

PHINIA published its inaugural Annual Sustainability Report in August 2024 and its second in August 2025—a signal that the company takes ESG reporting seriously despite being an ICE-focused business. The reports emphasize the environmental benefits of remanufacturing, the emissions-reducing properties of advanced fuel injection systems, and the pathway to zero-carbon fuels through hydrogen and alternative fuel technologies. Whether this narrative resonates with ESG-focused investors remains to be seen, but the effort to frame PHINIA as part of the decarbonization solution rather than the carbon problem is strategically important.

The company's balance sheet deserves attention as well. With a debt-to-equity ratio of 0.64 and a current ratio of 1.86, PHINIA operates with moderate leverage and comfortable liquidity—important attributes for a company whose strategy requires financial flexibility for acquisitions and shareholder returns. The return on invested capital of roughly eight percent is adequate but not exceptional, reflecting both the capital-intensive nature of precision manufacturing and the margin headwinds from the commercial vehicle downturn. As margins recover toward the 14-15 percent EBITDA range, ROIC should improve correspondingly—making it a useful indicator of whether the company is successfully executing its margin expansion plan.

Lessons for Founders and Investors

PHINIA's story, still in its early chapters, already offers several lessons that extend well beyond the automotive sector.

The first is about timing versus direction. The market can be absolutely right about the direction of a trend—electric vehicles will capture an increasing share of the global vehicle fleet—while being significantly wrong about the timing and the pathway. That gap between direction and timing is where opportunity lives. Investors who confuse "this is happening eventually" with "this is happening now" systematically misprice assets on both sides of a transition.

The second lesson concerns counter-positioning as deliberate strategy. Sometimes the most powerful strategic move is zagging when the entire industry zigs. PHINIA's willingness to invest in ICE technology at the precise moment when competitors are fleeing creates a competitive dynamic that classical strategy frameworks predict but that is remarkably rare in practice. The critical requirement is conviction backed by analysis, not mere contrarianism for its own sake.

Third, building optionality in uncertainty. PHINIA's hydrogen investment is a textbook example of strategic option creation—a relatively modest investment that leverages existing capabilities to create exposure to a potentially transformative outcome. If hydrogen infrastructure develops, PHINIA has a first-mover advantage. If it does not, the investment has still improved conventional fuel injection technology. The option costs little relative to its potential payoff.

Fourth, brand equity endures in industrial markets. In consumer technology, brands can rise and fall in years. In industrial and commercial markets, where purchasing decisions involve engineering validation, operational reliability, and long-term service relationships, brand equity compounds over decades. Delphi, Delco Remy, and Hartridge carry trust that no startup can purchase or replicate quickly.

Fifth, the parc versus production arbitrage. Investors instinctively focus on new vehicle production as the indicator of industry health. But the installed base—the vehicles already on the road—often represents a larger and more stable revenue opportunity than new production. PHINIA is built around this insight: the 1.4 billion ICE vehicles currently operating worldwide will need parts, service, and maintenance for decades, regardless of what happens to new vehicle production.

Sixth, spin-off dynamics create mechanical opportunity. When a large company spins off a division, the resulting selling pressure from index funds, ESG-mandated sellers, and investors who did not want the spun-off asset creates temporary dislocations between price and value. These are among the most well-documented sources of excess returns in public equity markets, and PHINIA's post-spin-off price action followed the textbook pattern.

Seventh, the circular economy is not just an ESG talking point—it is a business model. Remanufacturing is simultaneously more profitable than new production, more sustainable, and more strategically defensible. Businesses that discover this trifecta deserve attention.

Eighth, capital allocation in secular decline requires a specific discipline: harvest cash flows intelligently, acquire assets cheaply from motivated sellers, return excess capital to shareholders, and never fight gravity by over-investing in a business with a finite horizon. PHINIA's aggressive share repurchase program suggests management understands this framework.

Ninth, the "last man standing" strategy can work—but only if you have the staying power to outlast competitors and the discipline to manage a declining market rather than pretending decline is not happening. The companies that do this well generate extraordinary returns for shareholders even as their industries contract, because they capture market share, optimize costs, and return capital rather than chasing growth that no longer exists. The historical parallel is instructive: companies that dominated vacuum tube manufacturing in the 1960s, or typewriter production in the 1980s, generated strong returns for shareholders well after the direction of technological change was clear—provided they managed costs, returned capital, and did not over-invest in a shrinking market. PHINIA's management, with its aggressive buyback program and disciplined acquisition strategy, appears to understand this playbook.

The final lesson is perhaps the most broadly applicable: never underestimate the staying power of an installed base. Technology companies fixate on new device sales, but the real money is often in serving the installed base—the billions of devices already in use. Apple makes more money from services to its existing users than it does from selling new iPhones to first-time buyers. Microsoft's most valuable business is not selling new Windows licenses but serving the massive installed base of enterprise customers through Azure, Office 365, and support services. PHINIA is applying the same principle to the automotive world: the 1.4 billion ICE vehicles on the road represent an installed base that will generate parts, service, and maintenance demand for decades, regardless of what happens to new vehicle production. The company that owns the relationship with that installed base—through trusted brands, aftermarket distribution, remanufacturing, and diagnostic equipment—has a far more durable business than the headline "ICE is dying" narrative suggests.

The Verdict: What Happens Next

PHINIA's future unfolds along multiple plausible pathways, and the honest answer is that nobody—not management, not analysts, not the most sophisticated investors—knows which one will materialize.

In a fast EV transition scenario, where battery costs drop dramatically, charging infrastructure proliferates rapidly, and regulatory mandates force ICE phase-outs ahead of schedule, PHINIA becomes a cash cow to harvest and eventually wind down over five to seven years. In this scenario, the right strategy is exactly what management is executing: maximize cash generation, return capital to shareholders, and manage the decline gracefully. Even in this scenario, the aftermarket business provides years of cash flow, and the returns to shareholders who bought at the post-spin-off discount could be attractive.

In a slow EV transition scenario—which increasingly appears to be the base case for most independent forecasters—PHINIA thrives for ten to fifteen years, potentially re-rating upward as the market recognizes the durability of its cash flows and the strategic value of its market position. Commercial vehicle electrification faces far steeper challenges than light vehicles, and PHINIA's deliberate shift toward commercial, industrial, and aftermarket exposure positions it well for this scenario.

In a hydrogen breakthrough scenario, where policy support, infrastructure investment, and technology maturation converge to make H2ICE a viable commercial pathway, PHINIA repositions as an alternative fuel technology leader. The current investment in hydrogen fuel injection, the KGM partnership, and the SEM acquisition would look prescient, and the market multiple could expand significantly.

And there is a fourth scenario that is perhaps the most likely near-term catalyst: PHINIA as an acquisition target. A company generating nearly $500 million in annual EBITDA with strong brands, global distribution, and a defensible market position—trading at a discount to peers because of narrative rather than fundamentals—is precisely the kind of asset that private equity firms and larger aftermarket consolidators find attractive.

What investors should watch: EV adoption rates by region and segment, with particular attention to commercial vehicles and emerging markets. Hydrogen infrastructure investment and policy support, especially in Europe and Asia where government commitment is strongest. OEM decisions about extending ICE platform lifecycles, which directly affect PHINIA's new program pipeline. Execution of the M&A strategy and the discipline of capital returns. And the commercial vehicle electrification economics—if battery costs fall enough to make electric Class 8 trucks economically viable, the calculus changes fundamentally.

The company's diversification strategy—targeting light vehicle mix of approximately thirty percent by 2030 while expanding commercial vehicle, industrial, and aftermarket exposure—is the clearest expression of management's view about where the defensible long-term position lies. Progress toward these targets deserves close monitoring.

The ultimate question is whether PHINIA is a cigar butt—a declining asset with a few good puffs left—or a misunderstood compounder whose market position, cash generation, and strategic optionality are significantly undervalued by a market that cannot see past the EV narrative. For now, this remains a "show me" story: management must prove, quarter by quarter, that operational excellence and strategic optionality are translating into shareholder value.

Perhaps the most surprising insight in PHINIA's story is the irony at its core. A company born from the EV-transition spin-off—created specifically because its parent wanted to shed combustion assets to chase an electrification multiple—may ultimately prove to be the company best positioned to serve the messy, multi-pathway, decades-long reality of automotive decarbonization. The future of transportation is not a single technology; it is a portfolio of solutions adapted to different regions, use cases, and economic realities. And a company with century-old brands, precision fuel delivery expertise, hydrogen injection technology, a global remanufacturing network, and the commercial vehicle relationships to deploy all of it may be exactly what that future requires.

Epilogue

PHINIA represents something profound about technological transitions: they are never as linear, as clean, or as fast as the narrative demands.

Every great transition in industrial history—from horse to automobile, from steam to diesel, from analog to digital—has featured a messy middle period where the old technology improved, the new technology disappointed, hybrid solutions emerged, and the companies that navigated the ambiguity with clear eyes and steady hands captured extraordinary value. The transition from internal combustion to electric propulsion will be no different. It will take longer than optimists promise, arrive faster than skeptics expect, and unfold along pathways that nobody is currently predicting.