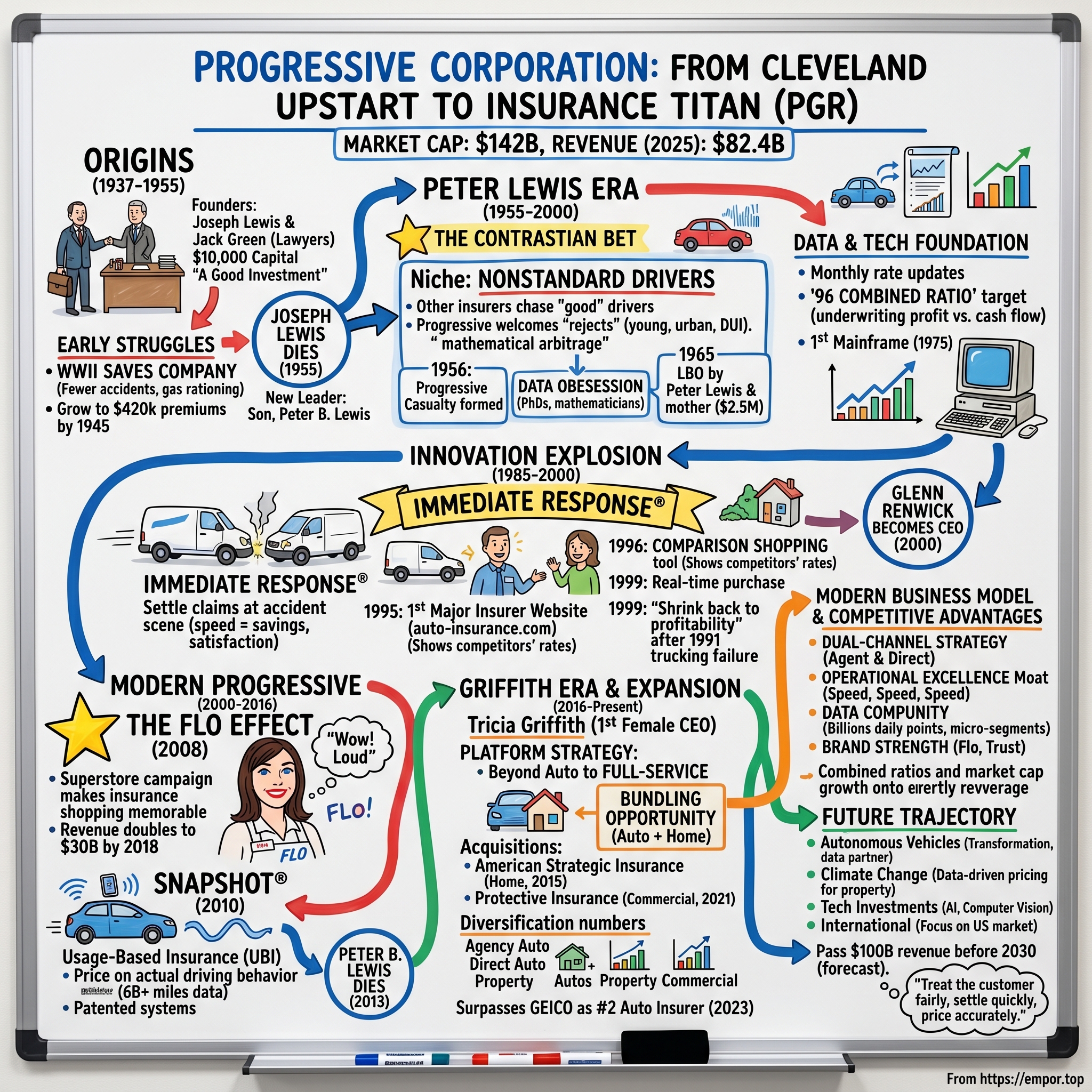

Progressive Corporation: From Cleveland Upstart to Insurance Titan

I. Cold Open & Episode Roadmap

Picture this: It's 2008, the financial crisis is ravaging American businesses, and most insurance companies are desperately trying to survive. Meanwhile, in a gleaming office tower in Mayfield Village, Ohio, a quirky insurance company with a perky spokesperson named Flo is quietly plotting world domination. Progressive Corporation, with $13.6 billion in revenue, seems like a mid-sized player in the massive auto insurance market. Fast forward to 2018—that number has more than doubled to nearly $30 billion. By mid-2025? An astounding $82.4 billion in revenue, making Progressive the second-largest auto insurer in America, breathing down State Farm's neck.

How did two Cleveland lawyers with less than $10,000 and a borrowed desk build what would become a $142 billion market cap behemoth? How did a company that nearly went bankrupt in 1939—with less than $1,500 to its name—transform into the insurance industry's most consistent innovator? And perhaps most importantly, how did they turn the most commoditized, boring product imaginable—car insurance—into a growth machine that has outperformed the S&P 500 for decades?

This is a story about contrarian thinking at its finest. While established insurers chased the "good" drivers, Progressive built an empire on the backs of the rejects. When competitors clung to paper and fax machines, Progressive bet the company on technology before "digital transformation" was even a phrase. When the industry said insurance had to be sold through agents, Progressive said "why not both?" and built a dual-channel monster.

But here's what makes this story truly remarkable: Progressive didn't disrupt insurance by being an outsider. They did it by understanding insurance better than anyone else. They turned actuarial science into an art form. They made claims processing—yes, claims processing—a competitive advantage. They proved that in a commodity business, the only sustainable moat is operational excellence married to relentless innovation.

What you're about to learn isn't just the history of an insurance company. It's a masterclass in finding gold in markets others ignore, in building culture that survives founder transitions, and in the compounding power of doing the basics better than anyone else for 88 years straight. It's about how two lawyers' "good investment" became the blueprint for building category-defining companies in the most unlikely places.

II. Origins: Two Lawyers and a Crazy Idea (1937-1955)

March 10, 1937. The Great Depression still grips America. In a modest Cleveland law office, Joseph Lewis and Jack Green are poring over documents from a state-sponsored investigation they've been conducting. Their assignment: investigate insurance companies suspected of fraudulent practices. But instead of just collecting their legal fees and moving on, the two lawyers spot something extraordinary—not in the fraudsters they're investigating, but in the legitimate corners of the insurance business. They see opportunity where others see only spreadsheets and actuarial tables.

With characteristic lawyer caution mixed with entrepreneurial ambition, Lewis and Green decide that starting an insurance company would be "a good investment for a couple of lawyers who were just getting started." They scrape together less than $10,000, borrow a desk, and found Progressive Mutual Insurance Company. Their stated goal is beautifully simple: provide vehicle owners with security and protection. No mention of disruption, no talk of revolution—just two lawyers who thought they could run an insurance company better than the crooks they'd been investigating.

The early years nearly killed the company before it could walk. By 1939—just two years after founding—Progressive's original capital had dwindled to less than $1,500. A Chicago consultant, brought in to assess the company's prospects, delivered a brutal verdict: get out of insurance while you still can. The math was simple and unforgiving. Progressive had written less than $10,000 in premiums in its first year. Administrative costs alone were eating them alive. Joseph Lewis and Jack Green were staring at bankruptcy.

Then came an unlikely savior: Adolf Hitler. As Peter B. Lewis would later observe with characteristic bluntness, "World War II saved Progressive." The war economy transformed everything. Suddenly, Americans had jobs. They had money. They could afford cars and, crucially, car insurance. But here's the beautiful irony—gas rationing meant they couldn't actually drive much. Fewer miles driven meant fewer accidents. Fewer accidents meant fewer claims. For a tiny insurance company with no reserves to speak of, it was the perfect storm of profitability.

The numbers tell the story of survival through serendipity. In 1940, Progressive wrote $65,000 in premiums. By 1945, that number had grown to $420,000. Not explosive growth by any measure, but enough to keep the lights on and build a small reserve. The company expanded cautiously from its Cleveland base, adding a handful of agents in Ohio, then tentatively reaching into neighboring states.

Through the late 1940s and early 1950s, Progressive remained what it had always been—a small, regional insurance company indistinguishable from dozens of others scattered across the Midwest. They sold standard auto insurance to standard customers through standard agents using standard pricing. Joseph Lewis ran the company with the conservative prudence of a lawyer who'd seen too many businesses fail. Jack Green focused on the legal and regulatory side, navigating the maze of state insurance regulations that made expansion costly and complex.

By 1955, Progressive Mutual Insurance Company had survived eighteen years—longer than most startups, but with little to show for it beyond survival itself. They had maybe $2 million in annual premiums, a few dozen employees, and a reputation for being reliable if unremarkable. Joseph Lewis had built a decent small business, but certainly not an empire.

Then, in the summer of 1955, Joseph Lewis died suddenly. The company he'd nursed through the Depression and war years needed new leadership. His son Peter, fresh out of Princeton with a degree in American history, had been working at the company for just a few months. At age 22, Peter B. Lewis was about to inherit not just his father's stake in a small insurance company, but the chance to transform an industry. The safe, lawyer-built Progressive was about to meet a very different kind of leader—one who would spend the next 45 years proving that the best opportunities hide in the places no one else wants to look.

III. The Peter Lewis Era Begins: Finding the Niche (1955-1965)

Peter B. Lewis didn't look like an insurance executive. Fresh from Princeton with tousled hair and an irreverent sense of humor, he'd joined Progressive just months before his father's death, mostly to appease family expectations. Now, at 22, he found himself holding significant ownership in a company he barely understood, in an industry that bored him senseless. His mother controlled the other major stake. Together, they faced a choice: sell to a larger insurer and walk away with a modest profit, or figure out how to make this sleepy Cleveland company matter.

The insurance industry of 1956 was undergoing a quiet revolution that would create Progressive's opportunity. Major insurers like State Farm and Allstate had discovered the power of actuarial segmentation. Using new statistical methods and early computers the size of entire rooms, they could now slice and dice their customer base with unprecedented precision. Age, driving record, ZIP code, marital status—every variable was fed into the models. The result? These insurers would only write policies for "standard risks"—the statistically safest drivers who promised the highest profits with the lowest claims.

Peter Lewis watched this trend with fascination. "Everyone was running toward the same customers," he'd later recall. "It was like watching every fisherman in town crowd around the same fishing hole while entire lakes sat empty." The major insurers were creating an enormous pool of orphaned customers—drivers they deemed too risky, too young, too urban, or simply too different from their ideal profile. These "nonstandard" drivers were being quoted astronomical rates or rejected outright.

Where others saw rejects, Lewis saw opportunity. But this wasn't charitable thinking—it was mathematical. Lewis realized that "nonstandard" was a lazy category that lumped together genuinely dangerous drivers with those who were merely statistically different. A 23-year-old male might be classified as high-risk simply due to age, even with a perfect driving record. A driver with one accident might be pooled with chronic drunk drivers. The pricing was crude, leaving massive arbitrage opportunities for anyone willing to do the work of proper segmentation.

In 1956, Progressive created Progressive Casualty Insurance Company specifically to serve this nonstandard market. It was a separate entity from the original Progressive Mutual, allowing them to experiment with different pricing models and underwriting standards without risking the core business. This structural innovation—using separate companies for different risk pools—would become a Progressive hallmark.

The early results were promising but not spectacular. Progressive Casualty wrote $587,000 in premiums in its first year, focusing initially on Ohio drivers who'd been rejected by standard insurers. But Lewis wasn't satisfied with simply being the insurer of last resort. He pushed his small team of actuaries to go deeper, to find the patterns within the patterns. One breakthrough came when they discovered that among drivers arrested for DUI, those with children were far less likely to repeat the offense. These customers were still charged higher-than-normal rates, but Progressive's premiums were significantly lower than competitors who treated all DUI offenders identically.

By 1960, Progressive had expanded beyond Ohio into Michigan, Florida, Tennessee, Kentucky, Georgia, and Mississippi—states chosen not randomly but through careful analysis of regulatory environments and competitive dynamics. Each state had different rules about rate-setting, different requirements for reserves, different definitions of "nonstandard." Lewis became obsessed with these variations, seeing each state as a unique puzzle to be solved.

The company culture during this period was equal parts insurance company and math department. Progressive had just over 100 employees by the early 1960s, with annual revenues reaching $6 million. But what distinguished them wasn't size—it was intensity. Lewis demanded that every underwriting decision be backed by data. He hired mathematicians and statisticians when other insurers were hiring sales managers. The company's offices in downtown Cleveland hummed with the sound of adding machines and slide rules as actuaries refined their models.

In 1965, Peter Lewis made his boldest move yet. He and his mother approached banks with an audacious proposal: lend them $2.5 million to buy out the other shareholders. They pledged their majority stake as collateral, essentially betting everything on Progressive's future. It was a leveraged buyout before the term existed, engineered by a 30-year-old with fewer than ten years of insurance experience.

The bankers were skeptical. Progressive was profitable but small, competing against giants with hundred times their resources. Lewis's pitch was simple: "We don't need to beat State Farm. We just need to be the best at serving the customers State Farm doesn't want." The loans were approved, barely. By year's end, Peter Lewis had complete control of Progressive, 40 employees reporting to him, and a vision that the nonstandard market wasn't a temporary niche—it was the future of auto insurance.

IV. Building the Machine: Data, Technology & Culture (1965-1985)

Peter Lewis stood before his 40 employees in Progressive's modest Cleveland headquarters in late 1965, now their sole leader at age 30. "We're going to do three things," he announced. "We're going to know more about risk than anyone else. We're going to process that knowledge faster than anyone else. And we're going to build a culture that outlasts all of us." His employees—mostly Ohio locals who'd joined a small insurance company for job security—had no idea they were about to become foot soldiers in a data revolution.

The transformation started with an almost manic focus on actuarial excellence. While competitors in the 1960s might update their rating models annually, Progressive updated theirs monthly. Lewis hired PhDs in mathematics and statistics, paying them more than senior executives at other insurers. He gave them a simple mandate: find profitable segments within the nonstandard market that everyone else is mispricing.

The breakthrough insights came from obsessive data collection. Progressive's actuaries didn't just track accidents—they tracked everything. Time of day, weather conditions, specific intersections, types of vehicles involved, even the day of the week. They discovered that Sunday morning accidents were fundamentally different from Friday night accidents, even if the damage looked identical. A fender-bender in a church parking lot indicated a very different risk profile than one outside a bar.

By 1970, Progressive had assembled what was likely the most sophisticated actuarial database in auto insurance. But data without application is just expensive storage. Lewis pushed for something radical: actual underwriting profit, not just premium growth. While the industry operated on the "cash flow underwriting" model—lose money on insurance but make it up by investing premiums—Progressive decided to make money on the insurance itself.

This philosophy crystallized into Progressive's famous "96 combined ratio" target, introduced after their 1971 IPO. The combined ratio measures losses and expenses against premiums—a ratio under 100 means underwriting profit. The industry average hovered around 105, meaning companies lost $5 for every $100 in premiums, hoping investment returns would cover the gap. Progressive's 96 target meant they'd make $4 on every $100, before investing a penny.

"We prefer underwriting profit to growth" became the company mantra, a heretical position in an industry obsessed with market share. Lewis would actually shrink the company in states where they couldn't hit their target margins, pulling out entirely rather than writing unprofitable business. In 1973, when inflation drove claims costs skyward, Progressive's premiums actually declined as they refused to chase unprofitable growth. Competitors mocked them as "Progressive Regressive."

But the discipline paid off spectacularly. From 1970 to 1985, Progressive averaged a 3% annual profit margin on underwriting, while competitors averaged a 7% annual loss. The company's stock price reflected this outperformance, rising from $6 at the 1971 IPO to over $45 by 1985, adjusted for splits.

The technological infrastructure supporting this growth was revolutionary for insurance. In 1975, Progressive installed one of the industry's first mainframe computers dedicated entirely to actuarial analysis. By 1980, they had terminals in every office connected to centralized databases—while competitors still shuffled paper between offices. Claims adjusters carried early portable computers by 1983, entering data directly at accident scenes while other insurers' adjusters still used carbon-copy forms.

Culture was the third leg of Lewis's trinity, and here he was most unconventional. In 1978, Progressive introduced its Core Values: Integrity, Golden Rule, Objectives, Excellence, and Profit. Note that profit came last, not first. Lewis believed that profit was the outcome of doing everything else right, not the primary goal. These weren't just poster platitudes—they were embedded in every process. The Golden Rule meant claims adjusters were evaluated not just on cost control but on customer satisfaction. Integrity meant admitting mistakes publicly, even when it hurt the stock price.

The company's physical space reflected its culture. Progressive's new headquarters, opened in 1982 in the Cleveland suburb of Mayfield Village, looked more like a college campus than an insurance office. Open floor plans, art-filled walls (Lewis was becoming a serious contemporary art collector), and casual dress codes created an environment radically different from the suited formality of Hartford or Bloomington.

By 1985, the transformation was complete. Progressive had grown from $6 million in revenue in 1965 to $456.5 million, with net income of $35.6 million. They ranked 55th among U.S. property-casualty insurers—not huge, but highly profitable and growing fast. More importantly, they'd built something unique: an insurance company that made money on insurance, that knew more about risk than anyone else, and that had a culture strong enough to survive its founder.

The next phase would test whether Progressive could scale its contrarian model into the mainstream market, but the foundation was set: superior data, superior technology, and a superior culture. The insurance industry was about to learn that the company they'd dismissed as a niche player for bad drivers was actually building the future of insurance.

V. The Innovation Explosion: Redefining Insurance (1985-2000)

The call came at 2:47 AM on a freezing January night in 1988. A Progressive customer had just been in an accident on I-271 outside Cleveland—car totaled, family shaken but unhurt, standing on the highway shoulder in 15-degree weather. In most insurance companies, this call would route to an answering service that would take a message for Monday morning. At Progressive, it triggered something unprecedented: within 20 minutes, a Progressive claims adjuster pulled up in a specially equipped van, complete with hot coffee, blankets, and a check-writing machine. By 3:30 AM, the customer had a rental car arranged and a settlement check in hand.

This was Immediate Response®, and it would revolutionize insurance. But Peter Lewis didn't start with the van—he started with a simple observation: "The moment of truth in insurance isn't when you buy the policy, it's when you have a claim." While competitors made customers wait days or weeks for adjusters, navigate phone trees, and fight for fair settlements, Progressive decided to show up immediately, settle generously, and turn the worst moment of a customer's year into a demonstration of why they chose the right insurer.

The logistics were staggering. By 1994, Progressive operated a fleet of 2,600 Immediate Response vehicles, each equipped with laptop computers, wireless modems (revolutionary for the time), digital cameras, and portable printers. Claims adjusters became roving offices, able to inspect damage, calculate settlements, cut checks, and arrange repairs all from the accident scene. The technology alone cost tens of millions—each van's equipment cost more than many people's annual salaries.

But Lewis understood something his bean-counting competitors missed: speed has value beyond customer satisfaction. The faster you settle a claim, the less it costs. No rental car bills piling up, no attorney letters, no angry customers calling repeatedly. Progressive's average claim settlement time dropped from weeks to hours. Their customer retention rates soared. Word-of-mouth became their most powerful marketing tool.

The year 1987 marked a symbolic milestone: Progressive crossed $1 billion in revenue and listed on the NYSE. But 1991 nearly ended everything. The company had expanded too fast into commercial trucking insurance, a business they didn't fully understand. Losses mounted. They'd also overstaffed, believing their own growth projections. Net income plummeted from $86 million to $3 million. The stock crashed. Analysts who'd praised Progressive's innovation now questioned whether Lewis had lost his edge.

Lewis's response revealed his true character. Instead of blaming market conditions or doubling down on bad bets, he admitted failure publicly. Progressive exited trucking insurance almost entirely, taking massive write-offs. They laid off 1,400 employees—a quarter of their workforce. But crucially, they didn't cut technology investment or claims service. "We're going to shrink back to profitability," Lewis announced, "then grow the right way."

The recovery was swift and spectacular. By 1993, Progressive was solidly profitable again. 1994 saw premium growth of 37.7% to $2.4 billion, as the company's superior service began attracting not just nonstandard customers but increasingly mainstream drivers who valued responsiveness over brand tradition.

Then came the internet, and Progressive pounced with startup-like agility. In 1995, they launched auto-insurance.com, becoming the first major insurer with a real website—not just a digital brochure but a functional platform where customers could get quotes. This might seem obvious now, but in 1995, most insurance executives thought the internet was a fad. State Farm didn't launch a comparable site until 1999.

But Progressive's boldest digital move was heretical: comparison shopping. In 1996, they began showing competitors' rates alongside their own. If GEICO was cheaper for a particular customer, Progressive would say so. The board thought Lewis had lost his mind. Why help customers leave? Lewis's logic was counterintuitive but brilliant: "If we're not competitive on price, the customer will find out anyway. By showing them upfront, we build trust. And if we can't compete on price, maybe we shouldn't have that customer."

The comparison tool had an unexpected benefit: it became a massive data collection engine. Progressive could see exactly where competitors were pricing aggressively, which segments they were avoiding, and how their rates changed over time. It was competitive intelligence handed to them by customers themselves.

By 1998, Progressive wasn't just selling insurance online—they were settling claims online. Customers could report accidents, upload photos, track claim status, and even approve repair estimates through their browsers. In 1999, they introduced the industry's first truly real-time purchase capability: enter your information, get a quote, buy a policy, print your cards—all in under 10 minutes. No agent, no phone call, no waiting.

The numbers from this period are staggering. Premium growth averaged 15% annually through the 1990s. The combined ratio stayed consistently below 96. The stock price rose from $8 in 1991's trough to over $70 by 2000. Progressive had gone from the 55th largest auto insurer to the 4th. They'd proven that insurance—boring, commoditized insurance—could be a growth business if you reimagined every assumption.

As the millennium approached, Peter Lewis was 66 years old and had been running Progressive for 35 years. He'd taken his father's tiny mutual insurance company and built it into a $6 billion innovation machine. But he knew the next phase required fresh leadership. In 2000, he stepped down as CEO, remaining as chairman but handing operational control to Glenn Renwick, a technology expert who'd been instrumental in Progressive's digital transformation. The Lewis era was ending, but the innovation explosion he'd ignited was just beginning.

VI. The Modern Progressive: Scale, Marketing & Leadership Transition (2000-2016)

Glenn Renwick didn't look like a typical insurance CEO when he took Progressive's helm in 2000. The Scottish-born mathematician and computer scientist had joined Progressive in 1986 to build pricing models, not glad-hand agents or schmooze regulators. But Peter Lewis saw in Renwick exactly what Progressive needed: someone who understood that insurance was becoming a technology business disguised as a financial service.

The handoff was remarkably smooth—Lewis remained chairman, providing strategic guidance while letting Renwick run operations. Their first major decision together would transform Progressive from a respected innovator into a household name. In 2003, the company was spending hundreds of millions on advertising with modest brand recognition to show for it. They needed something different, something that would make people actually remember an insurance company.

Enter Flo.

In 2008, a comedian named Stephanie Courtney walked into an audition for Progressive wearing a retro-styled white uniform, bright red lipstick, and an aggressively perky attitude. The script called for an enthusiastic insurance store employee. Courtney delivered the line that would launch a thousand commercials: "Wow! I say it louder." The Progressive Superstore campaign was born, and with it, the most recognizable character in insurance history.

The genius of Flo wasn't just her quirky charm—it was what she represented. The fictional Progressive Superstore where Flo worked was a physical manifestation of Progressive's comparison-shopping ethos. Customers could see all their options, compare prices transparently, and make informed decisions. Flo made insurance shopping feel less like a necessary evil and more like, well, shopping.

The numbers tell the Flo effect story. When she debuted in 2008, Progressive had $13.6 billion in premiums. By 2018, that number had more than doubled to nearly $30 billion. Flo became so popular that Progressive created an entire universe around her—her family, her colleagues (notably Jamie), her increasingly absurd situations. She had Halloween costumes, Twitter accounts, and fan conventions. An insurance mascot had become a pop culture phenomenon.

But while Flo was charming America, Renwick was revolutionizing how Progressive understood risk. In 2004, the company quietly launched a pilot program called TripSense in Minnesota. Customers installed a small device in their cars that tracked when, how far, and how they drove. The data was revolutionary—Progressive could now price based on actual driving behavior, not just demographics.

This evolved into Snapshot, launched nationally in 2010. The program was voluntary—customers could try it for six months and potentially earn discounts up to 30%. The real brilliance was the psychological effect. Good drivers loved proving they deserved lower rates. Bad drivers self-selected out. Progressive got incredible data on actual risk while customers felt empowered rather than surveilled. The technology advantages were significant. Progressive had been awarded a series of patents on the methods and systems used in Snapshot, creating a competitive moat. Progressive had tested and refined its UBI program for more than 15 years and had collected more than six billion miles of driving data by 2013. This wasn't just a product—it was a data goldmine that grew more valuable with every mile tracked.

By 2003, Progressive had become the third largest insurance company in the United States, with $11.9 billion in written premiums and 12 million customers. The company was firing on all cylinders—superior service, breakthrough technology, and now a marketing icon that made insurance memorable. But the real test of Progressive's model would come with leadership transition.

November 23, 2013. Peter B. Lewis dies at age 80 at his home in Coconut Grove, Florida. The man who'd transformed his father's tiny mutual company into a $25 billion innovation machine was gone. Lewis left behind more than just a company—he left a culture so strong it could survive without him. His stake, valued at about $1.2 billion, made him Progressive's largest shareholder, but he'd spent the last decade systematically reducing his control, ensuring no single person could derail what he'd built.

Glenn Renwick's tenure as CEO from 2000 to 2016 proved that Progressive's success wasn't dependent on its charismatic founder. Under Renwick, revenues grew from $6 billion to over $23 billion. The combined ratio stayed consistently below 96. The company climbed from the 4th to the 3rd largest auto insurer. More importantly, Renwick institutionalized innovation, making it a process rather than a personality.

But by 2016, the insurance landscape was shifting again. InsurTech startups with names like Lemonade and Root were promising to disrupt insurance with AI and apps. Amazon was rumored to be entering insurance. Autonomous vehicles threatened to eliminate accidents altogether. Progressive needed leadership that understood not just insurance or technology, but how to build platforms in the digital age. They found it in an unlikely place: their own customer service department.

VII. The Griffith Era: Platform Expansion & Market Leadership (2016-Present)

Tricia Griffith's path to the CEO suite was unlike any insurance executive before her. She'd started at Progressive in 1988 as a claims adjuster, literally inspecting damaged cars in body shops. Over 28 years, she'd run almost every major division—claims, customer service, sales, and most recently, personal lines. When the board named her CEO in July 2016, she became the first woman to lead Progressive and one of the few Fortune 500 CEOs who'd started in an entry-level position.

Griffith inherited a company at an inflection point. Progressive was immensely successful in auto insurance—the #3 player with $20 billion in premiums. But auto insurance was becoming a mature market. Growth rates were slowing. Price competition was intensifying. The real opportunity lay elsewhere: the $300 billion home insurance market where Progressive had virtually no presence.

"Auto insurance gets you in the door," Griffith explained to investors in 2017, "but the relationship deepens with home." The math was compelling. Customers who bundled auto and home stayed twice as long. They filed fewer claims. They referred more friends. But Progressive had spent 80 years perfecting auto insurance—they knew nothing about homes.

Rather than build from scratch, Griffith engineered a series of strategic acquisitions that would transform Progressive from an auto specialist to a full-service insurer. The first major move came in 2015, just before Griffith became CEO, when Progressive acquired a controlling interest in American Strategic Insurance (ASI), a Florida-based home insurer. ASI wasn't huge—about $900 million in premiums—but it gave Progressive instant expertise in property insurance, particularly in catastrophe-prone markets.

The integration revealed Griffith's operational genius. Instead of forcing ASI to adopt Progressive's systems, she had Progressive learn from ASI's property expertise while sharing Progressive's customer service and technology capabilities. Within two years, ASI's combined ratio improved by 10 points while customer satisfaction scores rose to Progressive levels.

In 2021, Griffith made an even bolder move, acquiring Protective Insurance Corporation for $338 million. Protective specialized in fleet trucking and workers' compensation—commercial lines that Progressive had largely abandoned after the 1991 crisis. But Griffith saw what others missed: the same data and technology advantages that worked in personal auto could transform commercial insurance.

The platform strategy was working. Customers who started with just auto insurance increasingly added home, renters, boat, and RV coverage. The "bundle discount" became Progressive's most powerful retention tool. By 2023, Progressive achieved what seemed impossible just a decade earlier: they surpassed GEICO to become the #2 personal auto insurer in America, behind only State Farm. The numbers under Griffith's leadership tell a story of unprecedented growth. As of August 2025, Progressive's trailing twelve-month revenue stands at $82.37 billion—more than quadruple what it was when she became CEO. Progressive reported net premiums written of $5.96 billion for December 2024, a 22% increase compared to $4.88 billion in December 2023. For the fourth quarter, net premiums written rose 20% year-over-year to $18.11 billion.

But the most impressive metric is market diversification. At year-end 2024, Progressive reported growth across its policy segments, with company-wide policies in force increasing by 18% to 34.95 million. Personal lines reached 33.81 million policies in force, an 18% increase year-over-year. Agency auto policies grew 17% to 9.78 million, while direct auto policies increased by 25% to 14 million. Special lines policies rose 9% to 6.52 million. Property policies in force increased by 14% to 3.52 million, and commercial lines policies grew by 4% to 1.14 million.

The dual-channel strategy that Peter Lewis pioneered has become even more sophisticated under Griffith. Progressive now seamlessly serves customers whether they prefer buying through agents or directly online, with pricing and service optimized for each channel. The technology infrastructure supporting 35 million policies would have been unimaginable in Lewis's era—real-time pricing across 50 states, instant claims processing via mobile apps, and AI-powered customer service that handles millions of interactions daily. Progressive's market cap has reached $143.55 billion as of August 12, 2025, with 586 million shares outstanding, making it the world's 120th most valuable company. The transformation from the $1.2 billion company Peter Lewis left behind in 2013 to today's insurance titan represents more than 100x growth in market value—a testament to the power of consistent execution and strategic expansion.

VIII. Modern Business Model & Competitive Advantages

Walk into any Progressive claims center today and you'll see something remarkable: a technology operation that would rival Silicon Valley startups, housed within an 88-year-old insurance company. Screens display real-time metrics on claims processing times. AI algorithms route cases to adjusters based on complexity and expertise. Mobile apps allow customers to photograph damage and receive instant estimates. This isn't just digitization for its own sake—it's the physical manifestation of Progressive's core insight: in a commodity business, operational excellence is the only sustainable moat.

Progressive markets its policies through independent insurance agencies in the US and Canada and directly via the internet and telephone. Its premiums are split roughly equally between the agent and the direct channel. This dual-channel strategy, pioneered under Peter Lewis and perfected under subsequent leadership, gives Progressive unique flexibility. When competitors like GEICO went all-in on direct sales, or State Farm doubled down on agents, Progressive said "why choose?" They built separate but integrated systems for each channel, optimizing pricing and service for the specific needs of agent customers versus direct buyers.

The technology moat runs deeper than distribution. Progressive has been awarded a series of patents on the methods and systems used in Snapshot, their usage-based insurance program. Think about what this means: Progressive has legal protection for insurance innovation. While competitors scramble to copy their telematics programs, Progressive has already moved on to the next innovation, always staying one step ahead.

But perhaps the most underappreciated competitive advantage is Progressive's actuarial sophistication. Remember, this is a company that in the 1950s began investing far more heavily than competitors in collecting and analyzing accident data. That culture of data obsession has compounded over seven decades. Today, Progressive processes billions of data points daily, from weather patterns to traffic flows to individual driving behaviors. Each quote, each claim, each customer interaction adds to their knowledge base.

The profitability numbers tell the story of this operational excellence. From 1970 to 1992, Progressive averaged a 3% annual profit margin on underwriting insurance, while competitors averaged a 7% annual loss. In the more profitable 1990s, Progressive's underwriting profit margin increased to 8.4%. Even in 2024, a challenging year for the industry with inflation and catastrophe losses, Progressive's combined ratio stood at 84.1 for December, a 0.7-percentage-point increase from 83.4 in the prior-year period. For the fourth quarter, the combined ratio improved by 0.8 percentage points to 87.9, compared to 88.7 in 2023.

The scale economics are staggering. Progressive can spread its technology investments across 34.95 million policies. A $100 million investment in AI capabilities costs them less than $3 per policy, while a smaller competitor with 1 million policies would pay $100 per policy for the same capability. This creates a virtuous cycle: more policies enable more investment, which improves service and pricing, which attracts more customers.

Consider their claims operation alone. Progressive processes millions of claims annually, but their average settlement time is measured in hours, not days. They've turned what most insurers consider a cost center into a competitive weapon. Fast claims processing doesn't just please customers—it reduces costs. No mounting rental car bills, fewer attorney interventions, less fraud opportunity. Progressive has proven that in insurance, speed equals savings.

The pricing sophistication goes beyond traditional factors. While competitors might use 20-30 variables to price a policy, Progressive uses hundreds. They know that a 35-year-old accountant who drives a Honda Accord 5 miles to work at 8 AM is fundamentally different risk than a 35-year-old accountant who drives the same car 5 miles to a bar at 11 PM. These micro-segments, invisible to competitors, allow Progressive to cherry-pick the best risks while properly pricing the worst.

Their brand strength, amplified by Flo and creative marketing, provides pricing power in a commodity market. Customers will pay a small premium for Progressive because they trust the brand, know the service is superior, and value the technology tools. This brand equity, built over decades, can't be replicated with venture capital or acquired through mergers.

The bundling opportunity represents the next phase of competitive advantage. As Progressive expands into home, commercial, and specialty lines, they gain more data about customers, more touchpoints for retention, and more opportunities for cross-selling. A customer with auto, home, and umbrella policies is far less likely to switch than one with just auto. The lifetime value of these bundled customers can be 5-10x higher than single-line customers.

Finally, there's the cultural moat—perhaps the most important and least replicable advantage. Progressive's Core Values, introduced in the 1970s and maintained through multiple leadership transitions, create an organization that thinks differently. The emphasis on integrity means they'll admit mistakes publicly. The golden rule means they treat customers fairly even when legally they don't have to. The focus on objectives means everyone knows the 96 combined ratio target. This culture attracts a certain type of employee—data-driven, customer-focused, innovative—and repels those who won't fit.

IX. Current State & Future Trajectory

The numbers coming out of Progressive's Mayfield Village headquarters in 2024 would make any CEO jealous. Revenue of $75.3 billion, up 21% from 2023. Net income of $8.46 billion, up 119% from the prior year. Profit margin of 11%, up from 6.2% in 2023. But Tricia Griffith isn't celebrating—she's worried about what comes next.

The insurance industry stands at an inflection point. Autonomous vehicles, once science fiction, are becoming reality. Tesla's Full Self-Driving, Waymo's robotaxis, GM's Cruise—they all promise a future with fewer accidents. For an auto insurer, even one as innovative as Progressive, this represents an existential question: what happens to car insurance when cars don't crash?

Griffith's answer is transformation, not resistance. Progressive is already working with autonomous vehicle manufacturers, collecting data on semi-autonomous features, understanding how liability shifts from driver to manufacturer. They're positioning themselves as the insurance partner for the autonomous age, not its victim. The Snapshot program, which tracks driving behavior, could easily evolve to track vehicle software performance, maintenance patterns, and usage profiles in an autonomous world.

Climate change presents another massive challenge. The home insurance business Progressive entered through acquisitions is increasingly exposed to catastrophic weather events. Hurricanes, wildfires, floods—they're becoming more frequent and severe. State Farm and Allstate have pulled out of entire states. But Progressive sees opportunity in crisis. Their data capabilities allow them to price risk more accurately than competitors. Their technology enables faster claims processing after disasters. Their financial strength lets them stay when others flee.

The competitive landscape is evolving rapidly. Traditional competitors like State Farm (still #1 in auto insurance) and GEICO (now #3 after Progressive passed them) are investing heavily to catch up technologically. New entrants like Root and Lemonade promise AI-driven insurance that's faster and cheaper. Tesla has even hinted at offering insurance directly, leveraging their vehicle data.

Yet Progressive's position has never been stronger. S&P Global Market Intelligence expects Progressive to be among the biggest underwriting profit contributors for 2024, with Berkshire Hathaway Group recording $12.2 billion of net underwriting profits and Progressive entities showing some of the largest individual company profits. The company is hiring aggressively—they announced plans to add 12,000 employees, betting on continued growth.

The technology investments continue at a breathtaking pace. Progressive is experimenting with computer vision for claims assessment, natural language processing for customer service, and machine learning for fraud detection. They're building APIs to integrate with smart home devices, connected cars, and health wearables. The insurance company of 2030 will look more like a technology platform that happens to underwrite risk.

Regulatory dynamics add complexity but also opportunity. Insurance remains a state-by-state business in America, with 50 different regulators, rules, and market dynamics. This regulatory maze is a barrier to new entrants and rewards companies like Progressive with decades of experience navigating it. While InsurTech startups struggle to get licensed in multiple states, Progressive can launch new products nationwide within months.

The bundling strategy is accelerating. Progressive now offers auto, home, renters, condo, boat, RV, motorcycle, commercial auto, general liability, professional liability, and workers' compensation. They're becoming a one-stop insurance shop, competing directly with State Farm and Allstate's agent-based models but with superior technology and pricing. The goal is simple: own the customer relationship entirely.

International expansion remains notably absent from Progressive's strategy, and deliberately so. While competitors chase growth in emerging markets, Progressive focuses on dominating the US market. With personal auto insurance penetration still growing, home insurance dramatically underserved, and commercial lines ripe for disruption, Progressive sees decades of growth opportunity without leaving American soil.

Looking ahead, the trajectory seems clear. Revenue growth is forecast to continue at 11% annually over the next three years, well above the 4.5% forecast for the overall insurance industry. The company is on track to pass $100 billion in revenue before 2030. Market cap could reach $200 billion if current multiples hold. The question isn't whether Progressive will grow, but how fast and in which directions.

X. Playbook: Lessons for Founders & Investors

Sitting in a venture capital office in San Francisco, you'd never hear someone say "let's build the next Progressive." The pitch would be laughed out of the room. Insurance? Boring. Cleveland? Not exactly Silicon Valley. Focusing on bad drivers? Sounds like a terrible TAM. Yet Progressive has created more value than 99% of venture-backed startups ever will. The lessons from their 88-year journey are profound, counterintuitive, and surprisingly applicable to any business.

Lesson 1: Find Gold in the Segments Others Abandon

When major insurers used new technology to identify and cherry-pick the best customers, they inadvertently created Progressive's opportunity. The "nonstandard" drivers everyone rejected became a multi-billion dollar market. The key insight: when industries segment customers, the abandoned segments don't disappear—they become underserved markets ripe for focused competitors. Today's equivalent might be the consumers rejected by AI-driven credit models or the patients avoided by concierge medicine.

Lesson 2: Operational Excellence Beats Disruption

Progressive never tried to "disrupt" insurance. They didn't eliminate agents (they embraced them). They didn't introduce a radical new business model (they sold the same insurance policies as everyone else). Instead, they did insurance better—better data, better service, better technology, better pricing. In commodity businesses, a 10% operational advantage compounded over decades creates an insurmountable moat.

Lesson 3: Culture Survives Founders

Peter Lewis ran Progressive for 35 years, but the company thrived after his departure because he'd embedded values, not just personality. The Core Values introduced in the 1970s still guide decisions today. The 96 combined ratio target remains sacred. The focus on data and technology continues. Building culture that transcends founders requires codifying principles, creating systems that reinforce them, and hiring leaders who embody them.

Lesson 4: Technology as Enabler, Not Product

Progressive has always been a technology leader, but they never sold technology—they sold insurance. The technology made them better at insurance. This distinction matters. Companies that fetishize technology often forget what problem they're solving. Progressive never forgot: help customers protect their assets at a fair price. Technology was just the means to that end.

Lesson 5: Patient Capital Compounds

Progressive went public in 1971 at $6 per share. Adjusted for splits, an investment then would be worth over 400x today, not counting dividends. But the journey wasn't smooth—multiple recessions, the 1991 near-bankruptcy, the 2008 financial crisis. Patient investors who understood the business model and competitive advantages were rewarded. Impatient traders who sold during downturns missed one of the great compounding stories in American business.

Lesson 6: Brand Building in Commodity Markets

Insurance is the ultimate commodity—state-regulated, standardized products that are functionally identical across providers. Yet Progressive built one of the most recognizable brands in America with Flo. The lesson: even in commodities, brand matters if it represents genuine differentiation. Flo works because she embodies Progressive's actual advantages—transparency, technology, and customer focus.

Lesson 7: Embrace Cannibalization

When Progressive launched direct sales online, they knew it would cannibalize their agent channel. When they introduced comparison shopping, they knew some customers would choose competitors. When they launched Snapshot, they knew some profitable customers would discover they deserved lower rates. Each decision sacrificed short-term profits for long-term positioning. Companies that won't cannibalize themselves will be cannibalized by competitors.

Lesson 8: Data Moats Compound

Progressive's 70-year head start in data collection can't be replicated with money or talent. Every claim, every quote, every customer interaction adds to their knowledge base. In industries where prediction drives profits, historical data becomes increasingly valuable. The lesson for startups: choose markets where data advantages compound and start collecting immediately.

Lesson 9: Boring Markets Hide Great Businesses

Insurance, logistics, waste management, industrial supplies—the unsexy industries that venture capitalists ignore often harbor the best businesses. Less competition, rational customers, predictable demand, and opportunities for operational excellence create environments where focused execution beats flashy innovation. Progressive proved that boring can be beautiful if you do it better than anyone else.

Lesson 10: Crisis Creates Opportunity

World War II saved Progressive from bankruptcy. The 1991 crisis forced strategic focus. The 2008 financial crisis weakened competitors. COVID-19 accelerated digital adoption. Each crisis that should have killed Progressive made it stronger because they were prepared to adapt. Companies that survive crises don't just endure—they use disruption to accelerate transformation.

XI. Bear & Bull Cases

Bear Case: The Disruption Scenario

The autonomous vehicle revolution could devastate Progressive's core business. If self-driving cars reduce accidents by 90%, the personal auto insurance market could shrink from $300 billion to $30 billion. Progressive's beautiful growth story becomes a melting ice cube. Tesla Insurance, leveraging real-time vehicle data, could offer insurance at 50% lower cost. Apple or Google could bundle insurance with their autonomous vehicle platforms. Progressive becomes the Kodak of insurance—a once-great company disrupted by technology change.

Climate change makes home insurance unprofitable everywhere, not just Florida and California. Catastrophe losses that were once "hundred-year events" happen annually. Reinsurance costs skyrocket. Regulators prevent adequate price increases. Progressive's expansion into property insurance, meant to diversify revenue, becomes an anchor dragging down profitability. They're forced to exit state after state, destroying the bundling strategy.

InsurTech competitors, funded by billions in venture capital, finally crack the code. They use AI to price risk better than Progressive's actuaries. They offer customer experience that makes Progressive look antiquated. They operate at 70 combined ratios while Progressive struggles to maintain 96. The young consumers who should be Progressive's future choose Lemonade or Root instead. Progressive's brand, strong with Boomers and Gen X, means nothing to Gen Z.

Regulatory pressure intensifies as insurance becomes politically toxic. States cap rate increases despite rising costs. Politicians demand coverage for uninsurable risks. Social inflation—rising jury awards and litigation costs—explodes. Progressive's disciplined underwriting becomes impossible when regulators force them to write unprofitable business. The industry returns to the 1980s model of losing money on underwriting and praying for investment returns.

A serious cybersecurity breach exposes millions of customers' driving data from Snapshot. The privacy violation leads to massive lawsuits, regulatory fines, and customer exodus. Trust, built over decades, evaporates overnight. The technology advantage becomes a liability as customers fear surveillance. Progressive has to abandon usage-based insurance entirely, losing their most important innovation.

Bull Case: The Platform Dominance Scenario

Progressive becomes the Amazon of insurance—a platform that sells every type of coverage to every customer segment through every channel. The $300 billion home insurance market, $150 billion commercial auto market, and $100 billion small business insurance market become Progressive's for the taking. Revenue grows from $82 billion to $200 billion by 2030. The market cap reaches $500 billion as investors recognize the platform value.

Autonomous vehicles, rather than destroying Progressive, make them indispensable. As liability shifts from drivers to manufacturers, Progressive becomes the primary insurer for Tesla, Waymo, and others. Their decades of data on accidents, claims, and repairs make them the only insurer capable of properly pricing autonomous vehicle risk. The personal auto market shrinks but the commercial autonomous fleet market explodes, and Progressive owns it.

The technology moat becomes insurmountable. Progressive's AI, trained on billions of claims, predicts risk with accuracy competitors can't match. Their APIs become the industry standard, with other insurers essentially becoming Progressive resellers. They launch Progressive Cloud, selling their actuarial and claims processing capabilities to smaller insurers. The insurance company becomes a technology company with recurring SaaS revenue.

Climate change, paradoxically, strengthens Progressive's position. As weak insurers exit catastrophe-prone markets, Progressive uses superior data and pricing to cherry-pick profitable risks. Their claims processing speed becomes crucial after disasters. Customers pay premium prices for the certainty that Progressive won't abandon them. The property insurance market consolidates around a few strong players, with Progressive gaining share every year.

The brand transcends insurance. Progressive Financial launches, offering auto loans, mortgages, and credit cards to their 35 million customers. Progressive Health enters the insurtech space. Progressive Business provides full-stack financial services to small businesses. The customer lifetime value explodes from hundreds to tens of thousands of dollars. The insurance company becomes a financial services powerhouse.

China and India's growing middle classes demand auto insurance, and Progressive International launches with local partners. The proven model of focusing on underserved segments, superior technology, and operational excellence translates perfectly. Progressive becomes the first truly global auto insurer, adding billions of new customers and trillions in market opportunity.

XII. Epilogue: What Would Joseph and Jack Think?

Picture Joseph Lewis and Jack Green, those two Cleveland lawyers, transported from their borrowed desk in 1937 to Progressive's sprawling Mayfield Village campus in 2025. They walk through buildings filled with thousands of employees, past walls adorned with contemporary art worth millions, into data centers humming with servers processing billions of calculations per second. They learn their little mutual insurance company now insures 35 million policies, generates $82 billion in annual revenue, and is worth $142 billion on the stock market.

Would they recognize it as the same company they founded with less than $10,000?

In some ways, absolutely not. The technology would seem like magic. The scale would be incomprehensible. Flo, the perky brand ambassador known by millions, would baffle them. The idea that Progressive makes money on insurance itself, not just investments, would seem impossible given their experience of barely surviving the Depression.

But in fundamental ways, Progressive remains exactly what Joseph and Jack envisioned: a company that provides vehicle owners with security and protection. The mission hasn't changed, only the methods. They still serve customers other insurers reject. They still price risk more accurately than competitors. They still operate from Cleveland, maintaining the Midwestern values of hard work and straight talk.

The journey from two lawyers with an idea to America's second-largest auto insurer spans 88 years, four major leadership transitions, countless crises, and revolutionary technological changes. Yet the thread connecting 1937 to 2025 remains unbroken: the belief that insurance, done right, is a noble business that helps people recover from life's worst moments.

Joseph Lewis died in 1955 having built a small but solid regional insurer. His son Peter died in 2013 having transformed it into a national innovation leader. Neither lived to see Progressive pass GEICO, dominate the market, or reach today's heights. But each leader built on what came before, adding their own innovations while preserving core principles.

The story of Progressive proves that enduring companies aren't built by disruption alone but by continuous evolution. They don't succeed by abandoning their past but by adapting timeless principles to new realities. They don't grow by doing everything but by doing a few things better than anyone else.

In 1937, two lawyers thought insurance would be "a good investment." They were right, just not in the way they imagined. The investment wasn't just financial—it was an investment in the idea that a company focused on customers, driven by data, and committed to excellence could thrive for generations.

Today, Progressive processes more claims in an hour than Joseph and Jack saw in their entire first year. But each claim is still handled with the same principle: treat the customer fairly, settle quickly, and price accurately for the risk. The tools have changed dramatically. The values haven't changed at all.

As Progressive approaches its centennial, the company faces challenges unimaginable to its founders—autonomous vehicles, climate change, artificial intelligence. But it faces them with advantages Joseph and Jack would have envied—unmatched data, superior technology, powerful brand, and financial strength. Most importantly, it faces them with the same pragmatic optimism that turned two lawyers with a borrowed desk into an insurance titan.

What would Joseph and Jack think? They'd probably be amazed by what their company became. But they'd recognize the spirit—the Cleveland grit, the contrarian thinking, the focus on doing insurance right. They'd see that their "good investment" became something more: a company that proved boring businesses, executed brilliantly over generations, can create extraordinary value.

The Progressive story isn't ending—it's entering its most interesting chapter yet. The company that thrived by insuring bad drivers in the 1960s, pioneered direct sales in the 1990s, and created usage-based insurance in the 2000s, now stands ready to define insurance for the autonomous age. The next 88 years won't look like the last 88, but if history is any guide, Progressive will adapt, evolve, and likely emerge stronger.

From $10,000 to $142 billion. From two employees to 50,000. From less than $10,000 in premiums to $82 billion in revenue. From a borrowed desk to the second-largest auto insurer in America. Not bad for two Cleveland lawyers who just wanted to make a good investment.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube