Progyny: Building the Fertility Benefits Category

I. Introduction & Episode Roadmap

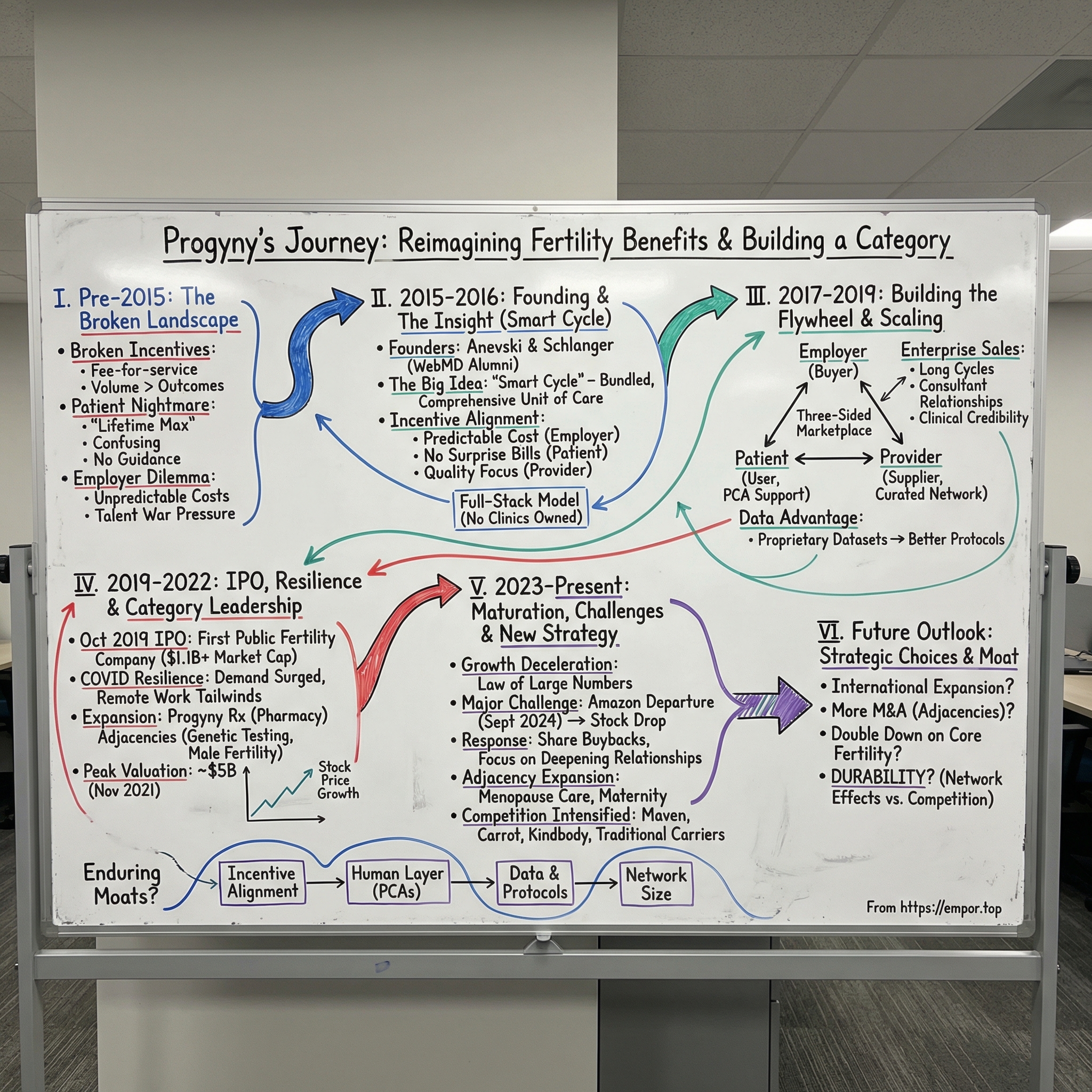

Picture the moment a benefits administrator opens an enrollment packet in 2015 and realizes that fertility coverage consists of a vague "lifetime maximum" buried in dense insurance legalese. No guidance on which clinic to choose. No clarity on what treatments are actually covered. No human being to call when the emotional weight of infertility meets the bureaucratic weight of healthcare administration. This was the landscape that Pete Anevski and David Schlanger surveyed when they joined a small New York startup called Progyny—and decided to rebuild fertility benefits from first principles.

Progyny became, by any measure, one of the most successful healthcare benefits companies of the past decade. From five employer clients at the time of its leadership transition in late 2016, it grew to serve over 470 enterprise clients and nearly seven million covered lives by 2025. Its October 2019 IPO made it the first fertility and family-building company to trade on public markets. At its November 2021 peak, the stock exceeded sixty-six dollars per share, valuing the company at over five billion dollars. The journey from startup obscurity to category leadership offers a masterclass in how to identify broken incentives, design a better mousetrap, and execute relentlessly in a highly regulated market.

The question that makes Progyny compelling for investors and operators alike is deceptively simple: How did a benefits administrator become a multi-billion dollar company by reimagining one of healthcare's most fragmented, emotional journeys?

The answer involves several interlocking themes. First, category creation—Progyny did not merely compete in fertility benefits, it defined what modern fertility benefits should look like. Second, incentive alignment—the company's "Smart Cycle" innovation restructured how every stakeholder, from patients to providers to employers, is compensated and motivated. Third, timing—Progyny caught the intersection of demographic shifts (delayed parenthood, growing LGBTQ+ family formation), cultural changes (destigmatization of infertility treatment), and market forces (employers desperate to differentiate on benefits in a tight labor market).

This episode traces Progyny's arc from founding insight through category leadership to its current maturation challenges. Along the way, it examines what made the model work, why competition is intensifying, and whether the company's competitive advantages can endure as traditional insurers and well-funded startups enter its space. For builders, it is a case study in creating a market rather than merely serving one. For investors, it is a test case in evaluating durability of competitive moats in healthcare services.

II. The Fertility Crisis & Market Context

In the mid-2010s, American fertility treatment resembled the Wild West of healthcare—expensive, confusing, emotionally devastating, and almost entirely uncoordinated. To understand why Progyny's model resonated so powerfully, one must first understand the market it entered.

The economics of infertility treatment were staggering. A single IVF cycle in the United States cost between fifteen thousand and thirty thousand dollars, depending on the clinic, the patient's specific needs, and whether medications and genetic testing were included. Most patients required two to three cycles to achieve pregnancy, pushing total costs to forty thousand dollars or more. Fertility medications alone averaged around five thousand dollars per cycle. For families without employer-sponsored coverage—which in 2015 meant the vast majority of American workers—this financial burden fell entirely on their shoulders.

Traditional health insurance, when it addressed fertility at all, did so poorly. Federal law contained no requirement for fertility coverage. State mandates varied wildly: as of 2024, only twenty-two states plus the District of Columbia had passed any fertility insurance coverage laws, and only sixteen of those included IVF. Even where coverage existed, it typically operated through lifetime dollar maximums—say, fifteen or twenty thousand dollars total for fertility treatment—that patients could exhaust midway through their first IVF cycle. There was no coordination of care, no guidance on selecting providers, no navigation through the byzantine clinical options available.

The patient experience was, in a word, nightmarish. A woman or couple facing infertility had to independently research reproductive endocrinologists in their area, with no reliable way to evaluate quality or outcomes. They scheduled consultations, often waiting weeks for appointments. They received treatment recommendations with no context for how that provider's success rates compared to alternatives. They navigated insurance authorizations, prior approvals, and coverage denials while simultaneously managing the emotional trauma of fertility struggles. If their first cycle failed, they started the process over—often with their lifetime benefits already exhausted.

Providers operated in a fragmented fee-for-service environment that incentivized volume over outcomes. Clinics had little financial motivation to pursue conservative, evidence-based protocols when they could instead recommend more aggressive (and more expensive) treatments. Transfer of multiple embryos—which increases short-term pregnancy rates but dramatically elevates risks of complications, preterm birth, and NICU stays—remained common practice despite clinical guidelines recommending single-embryo transfer. The result was a system that served no one's long-term interests: patients faced poor outcomes and financial ruin, employers absorbed unpredictable costs, and the industry's reputation suffered.

Meanwhile, demographic and cultural forces were building demand pressure that the healthcare system was unprepared to meet. American women increasingly pursued education and careers before starting families. The average age of first-time mothers rose from 21.4 years in 1970 to 26.6 years by 2016 and continued climbing to 27.5 years by 2023. In urban areas, the figure approached 28.5 years. Since fertility declines significantly with maternal age, this delay translated directly into increased demand for assisted reproductive technology.

Simultaneously, LGBTQ+ family formation grew as marriage equality expanded and social acceptance increased. Same-sex couples seeking biological children required assisted reproductive services by definition. Single individuals choosing parenthood added to demand. Egg freezing emerged from medical necessity into mainstream family planning, with women seeking to preserve fertility options while pursuing other life priorities.

For employers, this created a genuine dilemma. The war for talent, particularly in technology, professional services, and other knowledge-economy sectors, intensified through the 2010s. Benefits packages became crucial differentiators. Fertility benefits offered a powerful signal to prospective employees—particularly women—that an employer understood modern family formation. Yet traditional insurance approaches made fertility coverage unpredictable and expensive, with high utilization variability and uncertain cost trajectories.

The jobs-to-be-done framework illuminates why this market was ripe for disruption. Patients needed guidance, advocacy, and financial predictability. Employers needed cost management and competitive differentiation. Providers needed patient volume and support infrastructure. The existing system delivered none of these effectively. The category was waiting for someone to redesign it from scratch.

III. Founding Story & The Insight (2015-2016)

The modern Progyny emerged from a merger in March 2015, but understanding its origins requires tracing two threads backward. The first thread began in 2008 when Gina Bartasi, frustrated by the lack of reliable information during her own fertility journey, founded Fertility Authority as a consumer resource website. Bartasi built the site into a meaningful traffic destination for couples navigating infertility, creating a platform that connected patients with fertility clinics and provided educational content. The second thread was Auxogyn, a life sciences company developing embryo assessment technology to improve IVF outcomes.

In 2014, Kleiner Perkins and TPG Biotech recruited Bartasi to orchestrate a merger of these two entities. The combined company would pair Auxogyn's clinical technology with Fertility Authority's consumer reach and industry relationships. The vision: an end-to-end fertility solution that could work directly with employers to provide a fundamentally better benefit. The merged entity took the name Progyny and raised its Series A financing in April 2015 from those same venture investors.

Bartasi remained CEO through the merger and integration period, but by late 2016, she recognized that scaling Progyny would require a different skill set—one more oriented toward enterprise sales, financial operations, and healthcare benefits infrastructure. She agreed to transition leadership to someone more seasoned in building and running healthcare businesses at scale.

Enter David Schlanger and Pete Anevski, former colleagues from WebMD. Schlanger had served as CEO of WebMD, leading the digital health pioneer through a period of strategic transformation. Anevski had been WebMD's CFO, where he was credited with improving financial performance through pricing strategy changes, market positioning, and operational discipline. Both had spent years navigating the intersection of healthcare, technology, and large enterprise customers.

Schlanger joined as CEO in December 2016. His mandate: transform Progyny from a promising concept into a scalable enterprise benefits platform. One month later, in January 2017, he recruited Anevski as CFO and Chief Operating Officer. The WebMD alumni brought complementary strengths—Schlanger's strategic vision and CEO experience paired with Anevski's financial acumen and operational intensity. Together, they would build the Progyny model that would define the fertility benefits category.

The founding insight they inherited and refined was elegant: traditional fertility insurance was broken by design because it misaligned incentives at every level. The fee-for-service model meant providers earned more revenue when treatments failed and patients required additional cycles. Lifetime dollar maximums meant patients often ran out of coverage mid-treatment, creating enormous financial anxiety during an already emotional process. Lack of care coordination meant patients navigated complex clinical decisions without guidance, leading to suboptimal provider selection and treatment protocols.

Progyny's answer was the "Smart Cycle"—a reimagining of fertility coverage that bundled all services required for a complete treatment cycle into a single unit of care. Instead of tracking individual services against a lifetime maximum, a Smart Cycle encompassed everything: in-cycle monitoring (ultrasounds, blood tests), anesthesia, assisted hatching, genetic testing, intracytoplasmic sperm injection, all fertility medications, and even the first year of tissue storage. No surprise bills mid-cycle. No authorization denials for clinically indicated services. One comprehensive unit of coverage.

The model shifted incentive alignment in several important ways. For patients, Smart Cycles provided financial predictability and eliminated the fear of coverage exhaustion mid-treatment. For providers, participating in Progyny's network meant access to a growing patient population—one that arrived with coverage in place, care coordination support, and clinical education already completed. For employers, Smart Cycles created cost predictability (the employer paid for coverage units, not unpredictable fee-for-service claims) while demonstrating to employees a genuine commitment to supporting family formation.

Why did this approach emerge when it did? Several conditions aligned. The Affordable Care Act had strengthened employer mandates around healthcare coverage, making benefits strategy more central to corporate planning. Consumerization of benefits—employees expecting choice, transparency, and quality in healthcare similar to other consumer experiences—created pressure on traditional insurance approaches. Data infrastructure had matured sufficiently to enable outcome tracking, provider credentialing, and clinical protocol optimization at scale. And venture capital flowing into healthcare services meant capital was available for companies willing to take on complex regulated markets.

Early debates within Progyny centered on business model scope. Should the company build its own clinic network, becoming a vertically integrated fertility provider? Should it focus purely on benefits administration, acting as a technology platform connecting employers with existing clinics? Or should it pursue a "full-stack" solution—managing benefits, coordinating care, curating a provider network, and adding wraparound services like pharmacy benefits and patient advocacy?

The choice would prove consequential. Progyny opted for the full-stack model without owning clinical assets. It would build the most actively managed fertility network in the industry, carefully curating high-quality providers rather than accepting any willing participant. It would layer in human support through Patient Care Advocates who would guide members through their fertility journey. And it would integrate pharmacy benefits through its own Progyny Rx program. This configuration maximized capital efficiency (no need to build clinics) while creating multiple layers of differentiation from traditional insurance.

IV. Building the Flywheel: The Progyny Model

The business Schlanger and Anevski built after 2016 operated as a three-sided marketplace connecting employers (who purchased benefits), patients (who consumed fertility services), and fertility specialists (who delivered care). Each side of the marketplace depended on the others, creating network effects that would become central to Progyny's competitive position.

Start with employers, the buyers in this marketplace. Large self-insured employers—organizations managing their own healthcare risk rather than purchasing traditional insurance—represented Progyny's target customer. These companies, typically with over a thousand employees, had the sophistication to understand outcome-based benefits and the financial motivation to seek alternatives to unpredictable fee-for-service fertility claims. Progyny identified approximately eight thousand such employers in the United States as its addressable market.

For these buyers, Progyny offered a compelling value proposition. First, competitive differentiation in the talent market: fertility benefits had become a must-have for attracting and retaining employees, particularly women. Survey data showed that eighty-four percent of employers considered reproductive and family benefits important or very important for talent acquisition, while sixty-six percent of employees had taken or considered taking a new job because of better fertility benefits. Second, cost management through superior outcomes: Progyny's clinical results—twelve percent higher pregnancy rates per IVF transfer and twenty-one percent lower miscarriage rates compared to national averages—meant fewer treatment cycles, lower medication costs, and reduced high-risk maternity and NICU claims. Third, predictability: employers paid per-employee-per-month fees plus utilization-based charges for Smart Cycles actually used, creating a more predictable cost structure than open-ended fee-for-service.

The pricing model combined these elements. A PEPM (per employee per month) component covered access to Patient Care Advocates and platform services regardless of utilization. A utilization-based component scaled with actual Smart Cycle and pharmacy benefits usage. This structure gave employers budget predictability while ensuring Progyny's financial interests aligned with member engagement and successful outcomes.

Now consider patients, the users of the marketplace. A Progyny member's experience differed dramatically from traditional fertility coverage. Upon enrollment, each member gained access to a dedicated Patient Care Advocate—a fertility expert who served as personal guide, clinical educator, and emotional support throughout the treatment journey. PCAs were not call center workers reading scripts; they were trained specialists who understood reproductive endocrinology, could explain treatment options in accessible terms, and provided continuity across what might be years of fertility treatment.

The PCA model addressed what traditional insurance fundamentally ignored: that fertility treatment is deeply personal, emotionally fraught, and clinically complex. Members reported that seventy-five percent experienced added stress during family building, while over two-thirds credited their PCA with reducing that stress. The human connection created switching costs: patients who had developed relationships with their advocates, who had shared their fears and hopes over multiple conversations, did not casually move to a different benefits provider.

Beyond advocacy, members accessed Progyny's curated network of fertility specialists. The company built what became the industry's largest actively managed women's health network—over 1,100 providers at more than 650 locations across the United States. "Actively managed" was key: Progyny did not accept any willing provider but instead credentialed clinics based on utilization of latest scientific technologies, adherence to best clinical practices, culturally competent care delivery, and transparent outcome reporting. Members could trust that any network provider met rigorous quality standards.

The Smart Cycle benefit structure meant members never worried about coverage running out mid-treatment. If their employer provided two Smart Cycles, they could use those cycles—comprising all necessary services and medications—without tracking authorization limits or worrying about surprise denials. This financial predictability, combined with PCA support and vetted providers, transformed the patient experience from anxious navigation to guided journey.

Finally, consider fertility specialists, the suppliers in this marketplace. Why would high-quality reproductive endocrinologists join Progyny's network? Volume and support infrastructure. As Progyny added employer clients and covered lives, network providers gained access to a growing patient population—one that arrived with comprehensive coverage, care coordination already handled, and clinical education completed. PCAs prepared patients before appointments, ensured compliance with treatment protocols, and managed logistics that would otherwise burden clinical staff.

For elite fertility centers, Progyny membership became attractive. High patient flow supported practice economics while PCA coordination reduced administrative burden. The data-sharing requirements—transparent outcome reporting that fed Progyny's analytics—aligned with practices already committed to clinical excellence. And Progyny's marketing to employer benefits managers drove awareness and credibility for network practices.

The flywheel effect emerged from these interconnected relationships. More employer clients meant more covered lives seeking fertility treatment. More covered lives made network participation more attractive for providers. A stronger, broader network meant better access and outcomes for members. Better outcomes meant higher employer satisfaction and retention. Satisfied employers became references for new logo sales. New logos added more covered lives. The cycle reinforced itself.

Underlying the marketplace sat Progyny's data advantage. In an industry where outcome data had been sparse and inconsistent, Progyny built proprietary datasets from every treatment cycle across its network. This information enabled continuous refinement of clinical protocols, identification of best practices, benchmarking of provider performance, and evidence-based guidance for members and employers. The data advantage compounded over time: more treatment cycles generated more data, which improved algorithms and protocols, which produced better outcomes, which attracted more clients.

By the time Progyny went public in late 2019, this flywheel was spinning. From five employer clients when Schlanger and Anevski joined, the company had grown to 179 large self-insured employers including Google, Facebook, Microsoft, and Amazon. These marquee names validated the model and simplified subsequent sales conversations.

V. Scaling Through Enterprise Sales (2017-2019)

Selling fertility benefits to Fortune 500 companies was not like selling software. The enterprise benefits sales cycle involved multiple stakeholders (HR, benefits administration, finance, risk management, legal), extended timelines (often twelve to eighteen months from initial conversation to implementation), and intense due diligence around actuarial projections, legal compliance, and employee communications. Progyny built a sales organization designed for this complexity.

The go-to-market strategy targeted the decision-makers who controlled benefits purchasing: chief human resources officers, total rewards leaders, and benefits administrators at large self-insured employers. But reaching these buyers required intermediaries. Benefits consultants from firms like Mercer and Willis Towers Watson wielded enormous influence over employer benefits decisions. These consultants advised hundreds of companies on healthcare strategy, conducted annual reviews of benefits programs, and recommended specific vendors. Progyny invested heavily in consultant relationships, educating these influencers on outcome-based fertility benefits and providing data they could use in client recommendations.

The value proposition translated well to the consultant worldview. Consultants earned credibility by bringing innovative solutions that improved outcomes while managing costs. Progyny offered exactly that: clinical differentiation (demonstrably better outcomes than traditional insurance), competitive positioning (a benefit that helped clients attract talent), and actuarial validation (data showing cost predictability and return on investment). When consultants recommended Progyny, they looked smart to their employer clients.

Within employer organizations, Progyny navigated multiple stakeholder concerns. HR leaders cared about talent attraction and employee experience. Finance worried about unpredictable healthcare spending. Risk management examined regulatory compliance and liability exposure. Employee communications teams considered how to explain and roll out new benefits. Progyny developed sales collateral, implementation playbooks, and data presentations for each audience, demonstrating sophistication that smaller competitors struggled to match.

Building credibility required institutional markers. Progyny assembled clinical advisory boards featuring leading reproductive endocrinologists who could vouch for the model's clinical integrity. The company published outcomes data—pregnancy rates, miscarriage rates, single-embryo transfer rates—that demonstrated superior results compared to national benchmarks. Actuarial firms validated Progyny's methodology for calculating fertility outcomes, providing third-party credibility that enterprise buyers demanded.

The sales team emphasized ROI through better outcomes. A client considering Progyny could see projections: higher pregnancy rates meant fewer treatment cycles per successful pregnancy, reducing medication costs and provider fees. Lower miscarriage rates meant fewer emotional and financial setbacks. Higher single-embryo transfer rates (twenty-four percent above national average) meant dramatically lower twin and triplet pregnancies, avoiding the high-cost NICU stays and maternal complications associated with multiples. Seventy-two percent lower IVF multiples rate translated directly to reduced maternity and neonatal claims. For self-insured employers paying those claims directly, the math was compelling.

Geographic expansion presented execution challenges. Fertility treatment is inherently local—patients cannot travel for daily monitoring appointments during an IVF cycle. Progyny needed network coverage wherever its employer clients had employees, which for national and multinational companies meant every major metropolitan area. Building provider networks market by market required identifying, credentialing, and contracting with fertility centers in each geography. This ground game was slow and relationship-intensive, but it created barriers for competitors attempting to replicate Progyny's reach.

Competition began emerging during this period, though often from different angles. Traditional insurance carriers like United, Aetna, and Cigna recognized employer demand for fertility benefits and began enhancing their offerings. However, these carriers faced structural constraints: their fee-for-service infrastructure and existing provider relationships made outcome-based bundled payments difficult to implement. They could offer fertility coverage, but not with Progyny's care coordination, curated networks, or clinical focus.

Point solutions targeting specific aspects of fertility also appeared. Some focused on egg freezing benefits. Others provided fertility education or decision-support tools. These competitors often targeted smaller employers or served as add-ons to existing benefits programs rather than comprehensive replacements. Progyny's positioning as a full-service fertility benefits platform differentiated it from both traditional carriers and point solutions.

The key inflection point came around 2018-2019 when Progyny crossed fifty enterprise clients and demonstrated the model could scale. Each new marquee client—each additional Fortune 500 logo—validated the approach and created reference customers for subsequent sales. The network effects identified earlier began compounding visibly. By the time the company prepared for its IPO, it had proven unit economics, established market credibility, and built infrastructure that would be difficult to replicate quickly.

VI. The IPO Journey (2019)

By mid-2019, Progyny's leadership concluded that public markets offered the right next step. The company had grown revenue to meaningful scale, demonstrated strong client retention, and built infrastructure for continued expansion. A public listing would provide capital for growth, currency for potential acquisitions, and liquidity for early investors and employees. It would also subject the company to quarterly scrutiny that would either validate or challenge the model's durability.

The decision reflected confidence in several competitive advantages. The flywheel was working: more clients begat more members, which strengthened the network, which improved outcomes, which attracted more clients. The data advantage was compounding, with each treatment cycle adding to proprietary datasets that informed clinical protocols and provider benchmarking. And demographic tailwinds—delayed parenthood, growing LGBTQ+ family formation, employer competition for talent—showed no signs of reversing.

The IPO process unfolded in October 2019. Progyny priced ten million shares at thirteen dollars each on October 24, raising approximately one hundred thirty million dollars in gross proceeds. The pricing landed below the company's initial marketing range of fourteen to sixteen dollars per share, reflecting some investor skepticism about the addressable market and competitive dynamics. Nevertheless, the offering achieved its objectives: capital raised, public listing secured, market presence established.

The first day of trading dispelled any concern about demand. Shares closed at $15.94, a twenty-three percent jump from the IPO price. The company's market capitalization exceeded one billion dollars. Progyny had become the first fertility and family-building company to trade on public markets—a category-defining moment that generated significant media attention and industry validation.

Public market skepticism centered on several questions. Was fertility benefits a niche category or a mainstream opportunity? With only a minority of large employers offering comprehensive fertility coverage in 2019, bulls saw enormous penetration headroom while bears worried about a narrow addressable market. What about competition from traditional carriers? United, Aetna, and Cigna commanded massive employer relationships and could theoretically add fertility coordination to existing offerings. Would Progyny's early-mover advantage hold, or would scaled competitors crush the startup?

Management positioned the company around several themes. Total addressable market expansion was central: only around thirty percent of large employers offered comprehensive fertility benefits at IPO, implying years of penetration growth before saturation. Clinical differentiation—the demonstrably better outcomes versus national averages—created value that competitors would struggle to replicate quickly. Data moats from proprietary treatment information strengthened over time. And first-mover advantage in category creation meant Progyny was defining best practices that others would have to follow.

Post-IPO execution focused on proving quarterly consistency to institutional investors. Revenue grew from the mid-two-hundreds (in millions) in 2019 to $347 million in 2020 to over $500 million in 2021. Client count expanded. Covered lives multiplied. Each earnings report that met or exceeded expectations built credibility with a shareholder base learning to understand fertility benefits dynamics.

The stock performance reflected this execution. From the thirteen dollar IPO price, shares climbed through 2020 despite pandemic disruptions, accelerated in 2021 as fertility benefits became mainstream, and peaked above sixty-six dollars in November 2021. At that peak, Progyny's market capitalization exceeded five billion dollars—a staggering multiple on the 2019 IPO valuation.

The journey from skeptical thirteen-dollar pricing to sixty-plus dollar euphoria took just over two years. It validated the category Progyny had created and attracted intense interest from competitors, investors, and imitators alike.

VII. COVID, Demographic Shifts & Category Leadership (2020-2022)

The pandemic initially threatened Progyny's momentum. Fertility clinics shut down or reduced capacity in early 2020 as COVID-19 swept across the country. Elective medical procedures, including IVF, were deferred. Utilization dropped sharply in March and April. The question loomed: would delayed parenthood plans become cancelled parenthood plans?

The answer came quickly: no. As clinics reopened and patients adjusted to the pandemic reality, fertility treatment demand surged. The backlog of delayed cycles worked through. More significantly, the pandemic's disruption to normal life prompted many individuals and couples to reevaluate priorities. Starting families moved up on personal agendas. The combination of pent-up demand and accelerated decision-making drove utilization higher than pre-pandemic baselines.

The work-from-home revolution amplified these dynamics. Remote work erased some of the career-versus-family tradeoffs that had historically delayed childbearing. Geographic flexibility meant employees could pursue treatment at the most convenient clinics rather than those near offices. And the intense competition for talent that emerged as the economy recovered placed enormous pressure on employers to differentiate through benefits.

Fertility coverage transformed from progressive perk to expected benefit in many industries. HR teams found that candidates explicitly asked about fertility benefits during recruiting conversations. Employees contemplating job changes evaluated prospective employers' family-building support. The sixty-six percent of employees who reported considering job changes based on reproductive benefits translated directly into employer demand for providers like Progyny.

The company capitalized on this environment through strategic expansion. In 2020, Progyny launched its integrated pharmacy benefit management solution, Progyny Rx, to provide comprehensive medication support for fertility treatment. Rather than acquiring pharmacies outright, Progyny built a network model partnering with specialty pharmacy providers including VFP Pharmacy Group and Alto Pharmacy. The network delivered next-day medication fulfillment, clinical support from pharmacy specialists, and medication administration training—all coordinated with the member's treatment cycle.

The pharmacy expansion represented classic vertical integration logic. Fertility medications accounted for approximately thirty-five percent of treatment costs. By managing this spend through its own pharmacy benefit, Progyny captured margin that would otherwise flow to external pharmacy benefit managers, improved medication coordination for members, and added another layer of differentiation versus competitors who relied on third-party pharmacy solutions.

Beyond pharmacy, Progyny added adjacent services. Genetic testing coordination helped members navigate the increasingly complex landscape of preimplantation genetic testing. Egg freezing benefits expanded as employers sought to offer fertility preservation alongside treatment coverage. Male fertility services addressed the often-overlooked role of male factor infertility, ensuring comprehensive family-building support regardless of diagnosis.

Data advantages continued compounding. Every treatment cycle across Progyny's network added to proprietary datasets on protocols, outcomes, and patient experiences. The company developed sophisticated outcome reporting that employers could share with their benefits committees—evidence of clinical value that justified continued investment in fertility coverage. Provider scorecarding identified best practices that could be disseminated across the network, creating a continuous improvement loop that raised overall quality.

The client roster expanded impressively. Amazon, already a Progyny client since 2019, scaled its relationship as Amazon's employee population grew. By August 2023, the partnership had supported over thirty thousand Amazonians on their family-building journeys. Beyond Amazon, the company added major employers across industries: Snap, Bumble, Sanofi, Booz Allen Hamilton, and dozens of other Fortune 500 companies.

Markets recognized category leadership. Analyst upgrades accumulated. The stock price climbed from pandemic lows through 2021 highs. Institutional investors who had initially questioned the addressable market revised their views as client count and covered lives expanded quarter after quarter. At its November 2021 peak of $66.66 per share, Progyny commanded a premium multiple reflecting expectations for continued category growth.

Competition intensified as well. Maven Clinic, founded in 2014, expanded from its telehealth and holistic women's health positioning to compete more directly in fertility benefits. Maven's virtual-first model offered a different approach—broader women's health coverage through a single app, with fertility as one component rather than the central focus. By 2024, Maven would claim $268 million in annual recurring revenue and seventeen million people covered globally.

Carrot Fertility, founded in 2016 and headquartered in Menlo Park, targeted global fertility coverage with particular strength in international markets. Carrot served employers including Zoom, Clif Bar, and Lucid Motors. Its estimated five hundred million dollar valuation marked it as a well-funded competitor.

Kindbody pursued yet another model, combining in-house fertility clinics with benefit management. By operating its own clinical assets—twenty-seven clinics across twenty-one cities by the mid-2020s—Kindbody could offer treatment and coverage under one brand. This vertical integration came with capital intensity and geographic limitations but created a differentiated experience for members.

Traditional insurers also invested. Cigna, UnitedHealth, and Aetna (through Meritune Health) enhanced fertility offerings within their broader benefits platforms. While these carriers faced structural challenges in replicating Progyny's outcome-focused model, their existing employer relationships provided distribution advantages.

Progyny responded to competitive intensity by deepening its platform and expanding into adjacencies. The company's market position remained strong through 2022, but the competitive landscape had evolved from a near-monopoly in dedicated fertility benefits to a multi-player market with varied approaches.

VIII. The Maturation Phase & Current Strategy (2023-Present)

The period from 2023 through early 2026 brought both milestone achievements and significant challenges for Progyny. The company crossed four hundred clients and five million covered members, then continued expanding to 473 clients and an estimated 6.7 million covered lives by year-end 2024. Revenue grew from approximately $786 million in 2022 to $1.088 billion in 2023 to $1.167 billion in 2024—the company's ninth consecutive year of growth. Adjusted EBITDA reached record levels, operating cash flow exceeded $179 million annually, and the balance sheet showed over $450 million in working capital with zero debt.

Yet the growth trajectory shifted. Revenue growth decelerated from the thirty-eight percent achieved in 2023 to just seven percent in 2024. The 2025 guidance of $1.185 billion to $1.235 billion implied low-to-mid single-digit growth—a far cry from the hyper-growth rates of the IPO era. The maturation was partly natural (the law of large numbers catching up to a billion-dollar business) and partly circumstantial.

The circumstantial factor landed with seismic impact in September 2024: Amazon announced it would terminate its relationship with Progyny effective January 1, 2025, switching its fertility benefits to Maven Clinic. Amazon had been Progyny's highest-profile client and represented approximately twelve to thirteen percent of revenue. The stock dropped thirty-three percent on the news, from levels around twenty dollars to a November 2024 low of $13.67—barely above the original IPO price from five years earlier.

The Amazon loss illustrated both the risks and realities of enterprise healthcare services. Despite Progyny's outcome data, PCA relationships, and demonstrated value over nearly five years, Amazon chose a competitor. The exact reasoning was not publicly disclosed, but Maven's broader women's health positioning, global capabilities, and potentially aggressive pricing likely factored. Whatever the cause, the departure demonstrated that even satisfied clients could churn when attractive alternatives emerged.

Management responded on multiple fronts. The company secured new clients and expanded within existing accounts to partially offset the Amazon revenue loss. The 2025 guidance of $1.185-1.235 billion, while showing modest growth, indicated that Progyny expected to replace most of the lost Amazon business through organic expansion. The company also executed an aggressive share buyback program, returning $300 million to shareholders in 2024 and reducing shares outstanding by thirteen percent. This capital allocation signaled confidence in the business's cash generation while providing support for the stock price.

Strategic evolution shifted emphasis from pure new-logo acquisition toward deepening relationships within existing clients. Many Progyny clients began with fertility benefits and could expand into adjacent offerings: maternity care, postpartum support, menopause treatment. In 2024, forty percent of new clients adopted maternity, postpartum, or menopause programs alongside fertility benefits, while twenty percent of existing clients added these services. This expansion strategy offered higher capital efficiency than new-logo sales (existing clients required less sales effort and faster implementation) while increasing revenue per account.

The menopause care expansion represented Progyny's most significant category extension. In August 2023, the company announced nationwide access to menopause care through partnerships with Gennev and Midi Health. The offering addressed a genuine market gap: fewer than one in five OB-GYNs received formal training in menopause medicine, leaving millions of women without access to qualified care. By 2025, clients representing 1.5 million covered lives had adopted one or more menopause programs.

Whether menopause care represents a natural adjacency or a distraction from core fertility depends on perspective. Bulls argue that Progyny's employer relationships, PCA infrastructure, and women's health positioning translate directly to menopause, which affects virtually every woman in the workforce. Bears worry that menopause is a different clinical domain, with different provider networks and different competitive dynamics, that may dilute management focus.

Technology investments continued evolving the platform. AI-driven care recommendations, personalized treatment pathways, and telehealth integration enhanced the member experience. These capabilities addressed both member expectations (patients increasingly expected digital-first healthcare interactions) and competitive pressure (Maven's virtual-first model set a technology bar that Progyny needed to match).

International expansion remained limited. The fertility benefits model that Progyny pioneered was inherently tied to the U.S. employer-sponsored healthcare system, which has no direct analog in most other developed countries where government healthcare programs dominate. The April acquisition (a Berlin-based fertility platform) provided some European foothold, but international operations remained a small fraction of the business. Unlike technology companies that could seamlessly scale software globally, Progyny's model required local provider networks, regulatory compliance, and employer relationships that did not transfer across borders easily.

Current competitive dynamics show intensification across multiple dimensions. Traditional payers improved fertility offerings and leveraged existing employer relationships. Point solutions proliferated for specific use cases. Maven, Carrot, and Kindbody each captured meaningful market share with differentiated approaches. The "greenfield" market—large employers without any fertility benefits—shrank as adoption grew from thirty percent to over forty percent. Progyny still led the dedicated fertility benefits category but faced more sophisticated competitors than in its early years.

Financial performance as of early 2026 showed a company in transition. The stock recovered from its November 2024 lows to trade around twenty-one dollars by February 2026. Revenue guidance for 2025 projected continued growth despite the Amazon headwind. Adjusted EBITDA margins remained in the mid-to-high teens. The business remained profitable, cash-generative, and strategically sound—but no longer the hypergrowth story that had propelled the stock from thirteen dollars to sixty-six dollars.

IX. The Business Model Deep Dive

Understanding Progyny's durability requires examining the economic engine beneath the strategic narrative. The business model combines several revenue streams, each with distinct dynamics and margin characteristics.

Revenue flows primarily from utilization-based charges: employers pay for Smart Cycles and pharmacy benefits that members actually use. A secondary component comes from PEPM fees that employers pay regardless of utilization, covering access to Patient Care Advocates and platform services. The utilization-heavy mix creates revenue variability tied to member treatment activity, but also aligns Progyny's financial interests with member engagement.

Unit economics operate at multiple levels. At the client level, Progyny earns revenue from each covered life and each treatment cycle utilized. The company's sales and implementation costs amortize across multi-year client relationships (typical contracts run multiple years with automatic renewals), meaning client acquisition costs recover over time as utilization generates revenue. Client retention historically approached one hundred percent prior to the Amazon departure, demonstrating strong switching costs and satisfaction.

At the member level, each treatment journey generates revenue through Smart Cycle consumption and pharmacy benefit utilization. Superior outcomes—higher pregnancy rates, lower miscarriage rates—paradoxically create both value and revenue moderation: members who achieve successful pregnancies stop utilizing services. This dynamic means Progyny's long-term financial interests align with clinical success rather than extended treatment cycles.

Provider economics reflect network leverage. As Progyny's covered lives grew, individual fertility centers became increasingly dependent on Progyny patient flow. This dependency provided negotiating leverage for contracting terms, though the company balanced margin pressure against the need to maintain high-quality network participation. Too aggressive on provider economics could drive top specialists out of network, undermining clinical differentiation.

The pharmacy benefit represented a margin expansion opportunity. By managing fertility medications through Progyny Rx rather than external pharmacy benefit managers, the company captured margin on a significant cost category. This vertical integration also improved member experience (coordinated medication delivery, clinical support) and generated additional data on treatment patterns.

Gross margins in the low-twenties (around twenty-one percent in recent quarters) reflected the cost structure of a benefits management business with significant pharmacy pass-through revenue. Adjusted EBITDA margins in the high-teens demonstrated operating leverage as fixed costs spread across a larger revenue base. The company generated meaningful operating cash flow—over $179 million in 2024—supporting both organic investment and shareholder returns.

The churn question took on new urgency after Amazon's departure. Progyny's historical near-perfect retention had been a key investment thesis pillar; single-digit retention losses were manageable, but a twelve-to-thirteen percent revenue client leaving demonstrated that even satisfied customers could defect. The switching costs—employee PCA relationships, treatment history continuity, implementation complexity—proved insufficient to prevent departure when a competitor offered compelling alternatives.

Network economics remained a source of strength. Progyny's 1,100-plus providers across 650 locations created geographic coverage that competitors would need years to replicate. Provider credentialing standards maintained quality differentiation. And data-sharing arrangements generated proprietary information that informed clinical protocols across the network.

Capital allocation priorities balanced growth investment with shareholder returns. The company continued organic investment in platform capabilities, provider network expansion, and adjacency development. Simultaneously, the $300 million share buyback in 2024 demonstrated confidence in cash generation and provided support when the stock was under pressure. The absence of meaningful M&A suggested either disciplined valuation standards or limited acquisition targets worth pursuing.

Defensibility assessment yields a mixed picture. Strong elements include network effects (three-sided marketplace dynamics), process power (accumulated operational excellence in care coordination), and switching costs (member relationships, treatment continuity). Weaker elements include limited cornered resources (no unique IP or exclusive provider relationships), fading counter-positioning (traditional insurers now investing seriously in fertility coordination), and replicable talent (PCAs and clinical expertise can be hired by competitors).

X. Porter's Five Forces Analysis

Threat of new entrants: MODERATE-HIGH. Technical barriers to entering fertility benefits are relatively low—building a benefits administration platform and contracting with providers requires capital and expertise but no fundamental technological breakthroughs. However, execution barriers remain meaningful: developing high-quality provider networks requires years of relationship building, achieving clinical credibility demands published outcomes data and advisory board endorsements, and enterprise sales cycles take twelve-to-eighteen months from initial contact to implementation. Well-funded competitors like Maven, Carrot, and Kindbody have entered successfully, while traditional carriers expand internal capabilities. The category is past the "wide open" stage but remains accessible to sufficiently capitalized and persistent entrants.

Bargaining power of suppliers: LOW-MODERATE. Fertility specialists need patient volume to sustain practice economics, and Progyny provides this through its large covered-life population. Individual clinics depend on Progyny referrals, limiting their negotiating leverage. However, the number of top-tier reproductive endocrinology practices is finite, and regional concentration can create local leverage. Elite fertility centers in major markets have alternatives; they can participate in multiple networks or operate direct-to-consumer. Progyny's pharmacy benefit model reduces dependence on external specialty pharmacies, containing a potential supplier power source.

Bargaining power of buyers: MODERATE-HIGH. Large self-insured employers possess significant negotiating leverage. They can evaluate multiple fertility benefit providers, demand competitive pricing, and switch vendors at contract renewal. Benefits consultants influence purchasing decisions and may recommend alternatives for various reasons. High switching costs help Progyny (multi-year contracts, employee experience continuity), but the Amazon departure demonstrated that even long-term clients with apparent satisfaction can defect. The enterprise sales model gives buyers meaningful power in negotiations.

Threat of substitutes: MODERATE. Traditional insurance carriers increasingly enhance fertility coverage, offering some care coordination even if not matching Progyny's outcome focus. Direct-to-consumer fertility services (companies like Kindbody offering self-pay options) represent a different model serving different customer segments but create alternatives for individuals without employer coverage. International treatment tourism remains a limited substitute for U.S. employer benefits given logistics and employee expectations. The most meaningful substitute threat comes from improved traditional carrier offerings that approach Progyny's quality at lower switching costs.

Competitive rivalry: MODERATE-HIGH. The fertility benefits market has evolved from Progyny's early-mover near-monopoly to multi-player competition. Maven won Amazon—a visible competitive defeat. Carrot grows internationally. Kindbody expands its integrated model. Traditional carriers invest in fertility coordination. Multiple well-funded players pursue the same enterprise customers with different approaches (virtual-first, integrated clinical, benefit-only, carrier add-on). While winner-take-most dynamics favor scale, the market appears large enough to support several meaningful competitors.

XI. Hamilton's Seven Powers Analysis

Scale Economies — MODERATE & BUILDING. Progyny's PEPM model benefits from scale as fixed costs (technology platform, clinical protocols, corporate overhead) spread across more covered lives. Network leverage improves with member count: more patients means better provider contracting terms. Technology and clinical pathway development amortize across a larger base. However, fertility benefits is not a winner-take-all market where massive scale creates insurmountable cost advantages; regional provider networks and localized delivery limit pure scale benefits.

Network Economies — STRONG. The three-sided marketplace exhibits classic network effects: more employer clients bring more patients, which strengthens provider network attractiveness, which improves outcomes, which attracts more employers. Data network effects compound this: more treatment cycles generate more clinical insights, enabling better algorithms and protocols, producing superior outcomes that differentiate versus competitors with smaller datasets. Provider quality improves with volume as top specialists gravitate toward high patient flow.

Counter-Positioning — HISTORICALLY STRONG, NOW FADING. Progyny's original positioning exploited traditional insurers' fee-for-service infrastructure. Adopting outcome-based bundled payments would have required carriers to disrupt their own revenue models and provider relationships. This counter-positioning created space for Progyny to establish leadership without immediate carrier response. However, the advantage is fading as traditional carriers invest in fertility coordination and point solutions emerge without legacy constraints. Maven and Carrot built from scratch without inherited fee-for-service business models.

Switching Costs — MODERATE-STRONG. Members develop relationships with their PCAs over fertility journeys that may span years. Treatment history and clinical information reside within Progyny's platform. Mid-treatment switching disrupts care continuity and creates administrative burden. Employers face implementation complexity, employee communication challenges, and consultant relationship impacts when changing providers. However, annual benefits renewal cycles create natural switching opportunities, and the Amazon departure demonstrated that sufficiently motivated clients will overcome switching costs.

Branding — MODERATE & GROWING. Among HR and benefits buyers, Progyny enjoys strong brand recognition as the category creator and leader. Clinical credibility, thought leadership, and published outcomes data establish institutional reputation. Patient-level brand building occurs through word-of-mouth and member reviews—important in an intimate, emotional healthcare category. However, Progyny is not a household consumer brand; general awareness remains limited outside the benefits community.

Cornered Resource — WEAK. Progyny possesses no unique intellectual property, patented technology, or exclusive provider relationships that competitors cannot replicate. Proprietary outcomes data represents valuable accumulated information, but competitors building similar datasets over time will approach comparable insights. Talent and clinical expertise, while high-quality, can be recruited by well-funded competitors.

Process Power — MODERATE-STRONG. Clinical protocols refined over hundreds of thousands of treatment cycles represent accumulated operational knowledge. PCA training programs and care coordination playbooks embody years of experiential learning. Integration with employers' benefits systems creates embedded workflows. These process advantages are difficult to replicate quickly but not impossible over sustained competitor effort.

Overall assessment: Progyny's strongest powers are Network Economies and Process Power, with building Scale Economies. The erosion of Counter-Positioning represents the most significant strategic risk, as traditional carriers and well-funded startups close the gap that initially protected Progyny's market position.

XII. Bull vs. Bear Case

The bull case for Progyny rests on several reinforcing pillars. First, the total addressable market remains underpenetrated: only around forty percent of U.S. employers offer fertility benefits, implying years of adoption growth ahead. Second, demographic tailwinds persist—delayed parenthood, LGBTQ+ family formation, increasing awareness of fertility options—and show no signs of reversing. Third, category leadership creates compounding advantages through network effects, data accumulation, and brand credibility that new entrants require years to match.

Bulls emphasize vertical integration benefits. The pharmacy benefit captures margin and improves member experience. Adjacent expansions into menopause, maternity, and postpartum care leverage existing employer relationships and PCA infrastructure. Each addition increases revenue per account while spreading fixed costs.

The financial profile supports the bull thesis. Strong operating cash flow funds organic investment and shareholder returns. Zero debt provides financial flexibility. Consistent profitability demonstrates unit economics that scale. The aggressive share buyback at depressed valuations signals management confidence.

Path to sustained high margins exists as operating leverage kicks in at scale. Fixed costs (technology, corporate, protocol development) grow slower than revenue, implying margin expansion as the business grows.

The bear case centers on intensifying competition. Maven's Amazon win demonstrated that category leadership does not guarantee client retention. Well-funded competitors attack from multiple directions: Maven's virtual-first platform, Carrot's global coverage, Kindbody's integrated clinics, traditional carrier enhancements. The "greenfield" market of employers without any fertility benefits shrinks as adoption increases, forcing competition into displacement sales.

Bears question market size assumptions. In economic downturns or periods of budget pressure, will employers prioritize fertility benefits or cut them? Utilization volatility creates revenue unpredictability. The employer benefits model limits international expansion, capping geographic growth potential.

Margin pressure concerns arise from multiple sources. Provider costs may increase as fertility specialists gain leverage. Pricing competition from alternatives could compress fees. Pharmacy economics face general industry margin pressure.

Concentration risk remains following Amazon. Although no current client represents comparable revenue percentage, the enterprise model inherently creates client concentration. A few major departures could significantly impact financial performance.

One-product risk persists despite expansion efforts. Core fertility remains the dominant revenue contributor. Menopause, maternity, and other adjacencies have yet to achieve scale that would diversify the business meaningfully.

Key performance indicators for ongoing monitoring include client retention rates (measuring competitive positioning and satisfaction), same-store utilization growth versus new client additions (indicating organic health versus one-time implementation bumps), pharmacy benefit contribution margins (validating vertical integration thesis), competitive wins and losses in enterprise sales (tracking market share dynamics), and adjacent category revenue growth (measuring diversification progress).

XIII. Lessons for Builders & Investors

Progyny's journey offers several transferable insights for operators building in regulated markets and investors evaluating healthcare services companies.

Category creation beats category competition. Progyny did not enter an existing fertility benefits market and attempt to win share from established players. It defined what modern fertility benefits should look like—outcome-based coverage, curated provider networks, dedicated human support—and built the infrastructure to deliver it. Competitors who entered later competed on Progyny's terms, accepting the category definition rather than challenging it. For builders, the lesson is that articulating a new category and establishing its parameters provides first-mover advantages beyond mere timing.

Incentive alignment as strategy transcends tactical optimization. The Smart Cycle innovation was not a feature but a structural realignment of stakeholder motivations. Patients gained financial predictability. Providers earned through quality rather than volume. Employers received measurable outcomes. Progyny benefited when members succeeded. This alignment created a reinforcing system where each stakeholder's self-interest served collective outcomes. For investors, evaluating incentive structures reveals sustainability that product features alone cannot.

The human layer creates defensibility in a digital-first era. Patient Care Advocates seem anachronistic in an industry obsessed with automation and AI. Yet PCA relationships generated switching costs, improved clinical outcomes, reduced member stress, and differentiated Progyny from technology-only competitors. The emotional intensity of fertility treatment demanded human connection that chatbots could not replicate. For builders, recognizing when human touch creates value—and investing in it—can establish moats that technology alone cannot.

Vertical integration timing matters. Progyny launched Progyny Rx after establishing its core benefits platform and employer relationships. The pharmacy expansion leveraged existing covered lives, distribution channels, and clinical coordination rather than building from scratch. Sequential vertical integration allowed capital efficiency and validated each layer before extending further. For investors, the sequence and timing of vertical moves reveals strategic discipline.

Enterprise sales in healthcare requires patience and institutional credibility. Twelve-to-eighteen month sales cycles, consultant relationship development, clinical advisory boards, actuarial validation—Progyny invested in the infrastructure that enterprise buyers require. Shortcuts that might work in consumer or SMB markets fail with Fortune 500 benefits committees. For builders, recognizing the institutional requirements of enterprise healthcare sales prevents strategic errors.

Public market patience rewards sustainable growth. Progyny's stock volatility—from thirteen dollars to sixty-six dollars to fourteen dollars and back toward twenty-two dollars—tested investor patience repeatedly. The company's underlying business grew steadily while market sentiment oscillated between euphoria and despair. Long-term investors who understood the model's durability navigated volatility that short-term traders found punishing.

Adjacent expansion strengthens and dilutes simultaneously. Menopause care leverages Progyny's infrastructure but dilutes management focus. Maternity benefits extend the fertility journey but require different clinical expertise. Each adjacency presents this tension. For investors, evaluating whether expansions reinforce core competitive advantages or distract from them requires ongoing vigilance.

XIV. Epilogue & Future Outlook

As of February 2026, Progyny stands at an inflection point familiar to category creators approaching maturity. The company demonstrated that fertility benefits could be a multi-billion-dollar market, built infrastructure that competitors spent years attempting to replicate, and established brand credibility with enterprise buyers across industries. These achievements do not guarantee continued dominance but provide foundation for the next chapter.

The path forward presents strategic choices. International expansion could open new geographic markets but requires business model adaptation for healthcare systems structured differently than U.S. employer-sponsored coverage. More aggressive M&A could accelerate adjacency development but risks integration challenges and valuation discipline. Doubling down on core fertility with continued product refinement and competitive positioning may offer the most capital-efficient path but limits growth ceilings.

Broader implications extend beyond Progyny itself. The company demonstrated that employer-sponsored healthcare benefits could be reimagined from first principles—that legacy insurance approaches were not immutable constraints. This precedent influences innovation in other benefits categories: mental health, musculoskeletal care, diabetes management, and specialty conditions where fee-for-service misaligns incentives and fragmented care undermines outcomes.

The fertility industry continues evolving independently of Progyny's trajectory. At-home fertility testing creates new entry points for consumers discovering reproductive health issues. AI applications in embryo selection and treatment optimization may transform clinical protocols. Regulatory changes around reproductive rights create uncertainty and opportunity in different jurisdictions. Cultural attitudes toward fertility treatment continue normalizing, expanding the population comfortable seeking care.

Success five years hence might look like sustained market share in a growing category, meaningful revenue contribution from adjacent offerings, improved margins as operating leverage compounds, and demonstrated resilience to competitive pressure. Or it might look like market share erosion as well-funded competitors achieve parity, margin compression from pricing pressure, and strategic confusion as adjacencies proliferate without scale.

The Progyny story ultimately centers on something simpler than strategic frameworks and financial metrics: helping people become parents during one of life's most vulnerable journeys. That mission—genuinely improving deeply personal outcomes for thousands of families each year—created the foundation for everything else. Whether purpose-driven impact is sufficient to sustain a competitive moat remains the essential question for investors weighing Progyny's future.

XV. Key Performance Indicators to Watch

For investors tracking Progyny's ongoing performance, three metrics matter most:

Client Retention Rate: Historical near-perfect retention masked vulnerability that Amazon's departure exposed. Monitoring year-over-year client retention reveals competitive positioning and satisfaction levels. Retention decline signals competitive pressure requiring strategic response.

Same-Store Utilization Growth: Revenue growth combines new client additions with utilization changes within existing clients. Same-store utilization growth (how much existing clients' members utilize services year-over-year) indicates organic health versus one-time implementation bumps. Declining same-store utilization suggests member engagement challenges even as new logos add revenue.

Net Revenue Retention: Combining retention, utilization, and pricing, net revenue retention measures whether existing client relationships generate more or less revenue over time. Values above one hundred percent indicate expansion; below suggests contraction. This metric captures the combined effect of churn, upselling, and utilization dynamics in a single number.

XVI. Further Reading & Resources

For deeper exploration of Progyny, fertility benefits, and the broader employer healthcare landscape:

Progyny's S-1 Filing (2019) on SEC.gov provides the definitive business model explanation as the company prepared for public markets.

The New York Times Magazine's coverage of "The Fertility Business" offers broader industry context beyond any single company.

Progyny Investor Presentations (2020-2025) on the company's IR site document the evolution of strategy and competitive positioning over time.

The a16z Bio + Health Report on "The Future of Fertility" provides venture capital perspective on market landscape and investment themes.

RESOLVE: The National Infertility Association publishes reports offering patient advocacy perspective on coverage gaps and policy needs.

Modern Healthcare covers fertility benefits adoption trends with data on employer decision-making.

The Journal of Assisted Reproduction and Genetics publishes clinical outcomes research underlying treatment protocol development.

Benefits consultant analyses from Mercer and Willis Towers Watson provide the buyer perspective on fertility benefit evaluation.

Maven Clinic and Carrot Fertility blogs offer competitive positioning insights from Progyny's primary competitors.

The "Disrupting Healthcare" podcast features industry expert interviews on benefits innovation and employer healthcare strategy.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube