Procter & Gamble: The Consumer Packaged Goods Colossus

I. Introduction & Episode Teaser

Picture this: Every single day, before the sun rises in Cincinnati, Ohio, five billion people around the world reach for a product bearing the distinctive moon-and-stars logo of Procter & Gamble. From the Tide detergent cleaning clothes in suburban American laundromats to the Gillette razors gliding across faces in Tokyo boardrooms, from Pampers protecting babies in São Paulo to Crest toothpaste brightening smiles in London—P&G's products are so omnipresent they've become invisible infrastructure of modern life.

With $85 billion in annual sales, P&G isn't just big—it's a colossus that has fundamentally shaped how consumer products are made, marketed, and sold globally. The company owns 65 brands, many of which generate over a billion dollars in annual sales: Tide, Gillette, Pampers, Bounty, Crest, Ivory, Head & Shoulders, Scope, Oral-B, Swiffer, Tampax, Charmin, and dozens more. These aren't just products; they're cultural artifacts that have defined cleanliness, hygiene, and household management for generations.

But here's the remarkable part: This empire began in 1837 with two immigrants—a candlemaker from England and a soapmaker from Ireland—who married sisters and went into business together in what was then the frontier town of Cincinnati. How did William Procter and James Gamble's modest partnership evolve into the world's largest consumer products empire? How did a company selling soap to Union soldiers during the Civil War become sophisticated enough to pioneer modern brand management, create the soap opera, and execute one of the largest acquisitions in corporate history with the $57 billion Gillette deal?

The P&G story isn't just about scale—it's about the relentless reinvention required to stay relevant across three centuries. From the birth of mass marketing to the digital disruption of Dollar Shave Club, from managing 170+ brands to ruthlessly culling down to 65, from chemical innovation in Cincinnati labs to crowdsourcing ideas globally through Connect + Develop—this is a masterclass in building, scaling, and periodically rebuilding a consumer empire.

What makes P&G particularly fascinating for investors and entrepreneurs is the playbook it's developed: how to create billion-dollar brands from scratch, how to achieve pricing power in commoditized categories, when to acquire versus build versus divest, and perhaps most importantly, how to touch billions of consumers daily while remaining largely invisible. The company has also been a CEO factory, training executives who've gone on to lead Microsoft, Boeing, eBay, and dozens of other Fortune 500 companies.

As we dive into this epic saga, we'll explore the key inflection points: the Civil War contracts that introduced P&G to a nation, the creation of Ivory soap that revolutionized an industry, the invention of brand management that transformed marketing, the Gillette acquisition that doubled the company's size, and the great simplification under A.G. Lafley that saved P&G from drowning in its own complexity. We'll examine what worked, what didn't, and what it all means for understanding consumer businesses today.

II. Origins: Soap, Candles, and the Cincinnati Dream (1837–1900)

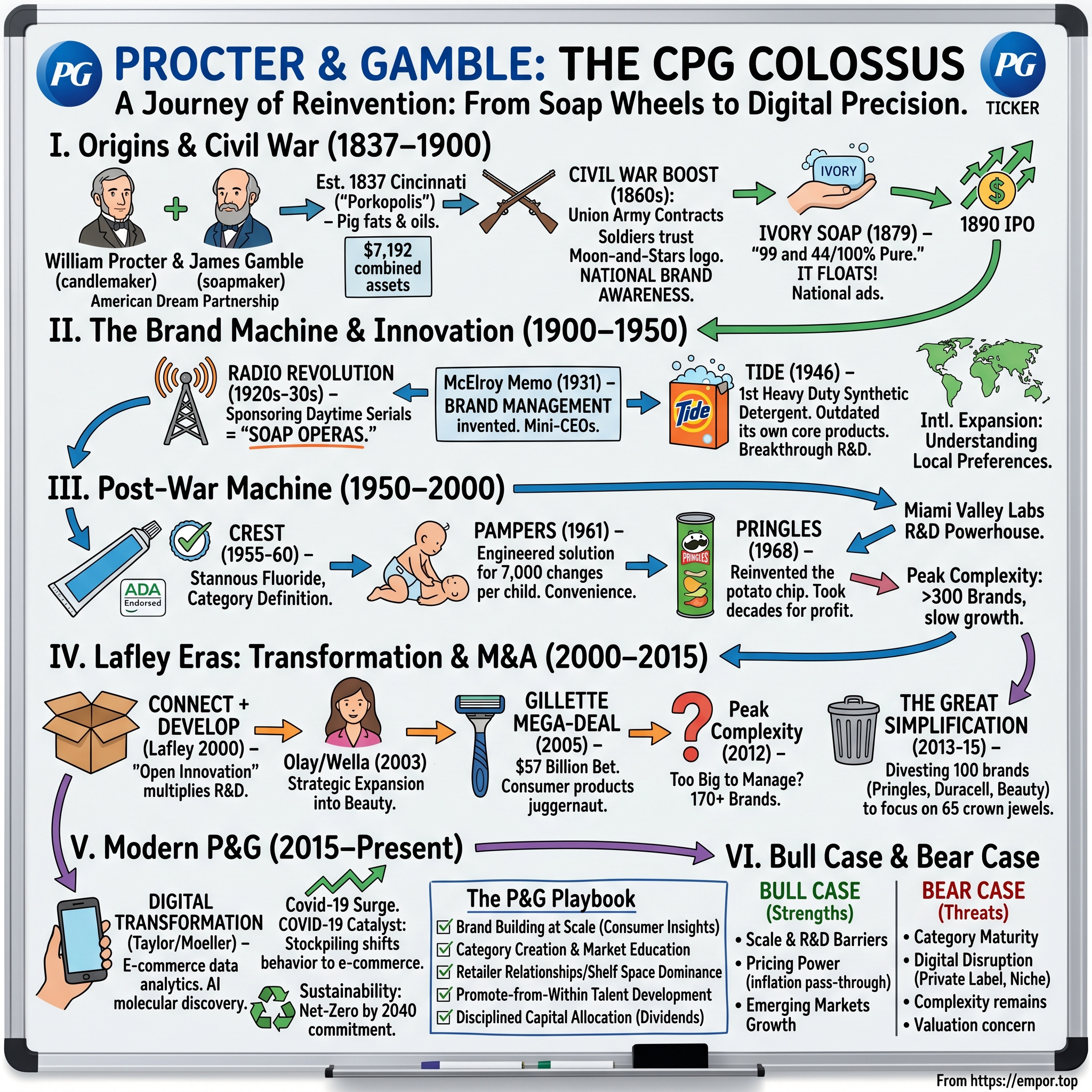

The year was 1837, and Cincinnati was booming. Dubbed "Porkopolis" for its massive meatpacking industry, the city processed more pigs than anywhere else in America. The byproducts—animal fats and oils—made it the perfect location for two specific trades: candlemaking and soap production. Into this frontier boomtown came two immigrants chasing the American dream: William Procter, a candlemaker from England whose shop had been destroyed in London's Great Fire, and James Gamble, a soapmaker from Ireland fleeing the economic devastation of his homeland.

Fate intervened through romance. Both men fell in love with sisters—Procter married Olivia Norris, Gamble married Elizabeth. Their father-in-law, Alexander Norris, saw an opportunity where others might have seen competition. At the dinner table one evening, he made a proposition that would change business history: "You're both buying the same raw materials, competing for the same suppliers. Why not join forces?" On October 31, 1837, with $7,192.24 in combined assets (about $200,000 in today's dollars), Procter & Gamble was born.

The early years were grinding. The partners worked 12-hour days, Procter managing the office and finances while Gamble supervised the factory floor. They made "Cincinnati Soap"—a utilitarian product sold in massive wheels that grocers would slice off by the pound. Nothing fancy, nothing branded, just honest soap for a growing nation. But they had impeccable timing. Cincinnati sat at the crossroads of America's westward expansion, connected by the Ohio River to both the agricultural South and the industrial East.

By 1858-59, just over twenty years in, they hit their first major milestone: $1 million in sales. The company employed 80 workers, substantial for the era but still small enough that both founders knew every employee by name. They were successful local businessmen, respected in Cincinnati, but not yet a national force.

Then came the Civil War—and with it, P&G's first lesson in the power of scale and government contracts. While other businesses struggled with the chaos of war, Procter and Gamble made a calculated bet. They aggressively bid on contracts to supply the Union Army with soap and candles. James Gamble's cousin, Major James N. Gamble, helped secure these deals, but it was the founders' ability to deliver at scale that sealed their reputation.

The numbers were staggering: P&G supplied soap and candles to over a million Union soldiers. But the real genius wasn't just the immediate profits—it was the unintended marketing coup. Soldiers from Maine to Michigan, Iowa to Illinois, all used P&G products in camp. When they returned home after the war, they sought out the familiar moon-and-stars logo they'd grown to trust in the field. Without spending a dollar on advertising, P&G had achieved national brand recognition.

The post-war period brought P&G's first true innovation breakthrough. James N. Gamble, son of the founder, observed something that seems obvious now but was revolutionary then: middle-class families were buying two different bars of soap—harsh yellow laundry soap for clothes and gentler toilet soap for bathing. Why not create one soap pure enough for both uses?

The development of Ivory Soap in 1879 showcased P&G's emerging innovation culture. Legend has it that a worker accidentally left a soap mixer running during lunch, whipping extra air into a batch. The result: soap that floated. Whether true or apocryphal, P&G recognized gold when they saw it. "It Floats!" became one of advertising's first great slogans. But the real masterstroke was Harley Procter's (William's son) decision to have the soap scientifically analyzed. When chemists reported it was "99 and 44/100% pure," a legendary tagline was born.

Ivory transformed P&G from a regional soap maker into a national brand. Harley Procter spent an unprecedented $11,000 on national advertising in 1882—shocking for the era. He pioneered tactics that seem routine now but were revolutionary then: consistent branding, emotional advertising appeals, and scientific claims to support marketing messages.

The financial impact was dramatic. Sales exploded from $3 million in 1879 to over $10 million by 1890. That year, recognizing they'd outgrown the original partnership structure, P&G incorporated and went public on the New York Stock Exchange. The initial stock offering valued the company at $4.5 million—making it one of the oldest continuously listed stocks that still trades today.

By 1900, P&G employed over 1,000 people and operated multiple factories. The second generation—led by William Cooper Procter and James Norris Gamble—had taken the reins. They inherited not just a soap company but a template for American business: quality products, scientific innovation, aggressive marketing, and relentless geographic expansion. As the new century dawned, they were ready to transform from successful soap makers into architects of modern consumer marketing.

III. The Birth of Modern Marketing (1900–1950)

The dawn of the 20th century found William Cooper Procter, grandson of the founder, pacing the executive offices of P&G with a radical idea. "We need to stop thinking like manufacturers," he told his board, "and start thinking like the housewives who buy our products." This simple reframe would revolutionize not just P&G but the entire concept of marketing.

By 1921, P&G had grown into a major international corporation with a diversified portfolio spanning soaps, toiletries, and food products. That year marked a watershed: their annual advertising budget crossed $1 million—an astronomical sum that made competitors gasp. But Cooper Procter saw it differently. "We're not spending money," he'd say, "we're investing in consumer relationships."

The real revolution came through an unlikely medium: radio. In the 1920s, while competitors bought simple spot advertisements, P&G did something unprecedented. They created and produced entire radio programs, weaving product messages into entertainment. The masterstroke came in 1932 when P&G began sponsoring daytime radio serials aimed at housewives—dramatic, continuing storylines that kept audiences tuning in day after day.

These "washboard weepers," as critics dismissively called them, were actually sophisticated psychological tools. P&G's market research (itself a revolutionary concept) showed that housewives, isolated in their daily routines, craved both entertainment and connection. Shows like "Ma Perkins" and "The Guiding Light" provided both, while subtly reinforcing the reliability and trustworthiness of P&G products. The shows became so associated with soap companies that a new term entered the American lexicon: soap operas.

The numbers validated the strategy spectacularly. By 1939, P&G was spending $9 million annually on radio advertising, sponsoring 21 radio programs that reached 40 million listeners daily. Ivory soap sales had quintupled. Crisco shortening, launched with similar marketing intensity, had captured 60% of its market within a decade.

But P&G's most revolutionary innovation wasn't in advertising—it was in organizational structure. In 1931, Neil McElroy, a young advertising manager, wrote a memo that would reshape corporate America. Frustrated by internal competition between P&G's growing product lines, McElroy proposed a radical solution: brand management. Each brand would have its own dedicated team, competing not just with external rivals but with other P&G brands. The brand manager would be a "mini-CEO," responsible for every aspect of their product's success.

The board was skeptical. Why create internal competition? McElroy's answer was prescient: "The consumer doesn't care that Oxydol and Tide are both made by P&G. They care which one cleans better. If we don't compete with ourselves, someone else will." The system worked brilliantly, driving innovation and accountability. McElroy would later become P&G's president, then Secretary of Defense under Eisenhower, spreading the brand management gospel throughout American business.

International expansion accelerated during this period. The 1930 acquisition of Thomas Hedley Co. in Newcastle, England, gave P&G its first major overseas manufacturing base. But unlike American competitors who simply exported U.S. products, P&G invested in understanding local preferences. British housewives, they discovered, preferred harder soaps than Americans. German consumers wanted different scents. Each market required patient study and adaptation.

The scientific revolution within P&G was equally dramatic. In 1946, after seven years of development costing $20 million (roughly $300 million today), P&G introduced Tide—the first heavy-duty synthetic detergent. The product was so superior to soap-based cleaners that P&G essentially obsoleted its own core products. Within two years, Tide was America's leading laundry product. By 1950, it was generating over $100 million in annual sales.

The Tide launch demonstrated P&G's emerging playbook: massive R&D investment, breakthrough innovation, and overwhelming marketing force. The company spent an unprecedented $7 million advertising Tide in its first year—more than most companies' total revenue. They gave away 37 million sample boxes, reaching virtually every American household. The message was clear: P&G didn't just enter markets, they transformed them.

This period also saw P&G's first ventures beyond soap and cleaning. Prell shampoo (1947) and Joy dishwashing liquid (1949) expanded the company's reach throughout the household. Each launch followed the Tide template: superior product performance backed by massive marketing investment and scientific credibility.

By 1950, P&G's sales exceeded $500 million, with international operations contributing nearly 20%. The company employed 25,000 people and operated 12 plants across three continents. But more importantly, they had created the modern consumer products playbook: brand management, scientific R&D, mass media advertising, and global scalability. As America entered the prosperous 1950s, P&G was perfectly positioned to define how the emerging middle class would clean, wash, and care for their families.

IV. The Post-War Innovation Machine (1950–2000)

Howard Morgens stood before P&G's board in 1955 with a tube of toothpaste and a bold prediction: "Gentlemen, this will prevent cavities." The directors were skeptical—P&G had never ventured into oral care, and making medical claims was dangerous territory. But Morgens, who would later become CEO, understood something fundamental: P&G's future lay not in incremental improvements but in category-defining innovations. Crest, with its stannous fluoride formula, would prove him spectacularly right.

The Crest launch exemplified P&G's evolution from soap maker to scientific powerhouse. The company spent years working with Indiana University researchers, conducting clinical trials involving 4,000 children. When the American Dental Association gave Crest its first-ever product endorsement in 1960, sales exploded from $10 million to $100 million within two years. P&G had cracked the code: combine genuine scientific innovation with regulatory credibility and massive marketing muscle.

But the real revolution was happening in Mehoopany, Pennsylvania, where a small P&G team was working on something that would redefine parenthood itself. The disposable diaper project, begun in 1956, was classic P&G—taking a universal problem and engineering an entirely new solution. Early prototypes were disasters. The first test in Dallas during summer 1958 was a fiasco—the plastic backed diapers created horrible heat rashes. Mothers rejected them overwhelmingly.

Victor Mills, the engineer leading the project, refused to quit. "Every mother in America changes 7,000 diapers per child," he calculated. "If we solve this, we transform childhood." Five years and $10 million later, Pampers launched in 1961. Initial sales were modest—the diapers cost 10 cents each when cloth diapers cost virtually nothing after the initial purchase. But P&G understood something competitors missed: parents would pay for convenience and reliability. By 1969, Pampers was a $100 million brand. By 1985, it exceeded $1 billion in sales.

The 1957 acquisition of Charmin Paper Mills seemed mundane compared to these innovations, but it revealed P&G's strategic sophistication. They recognized that as Americans grew wealthier, they'd demand better everything—including toilet paper. P&G transformed Charmin from a regional commodity into a national brand through relentless innovation (two-ply softness) and unforgettable advertising (Mr. Whipple's "Please don't squeeze the Charmin" became one of advertising's most memorable campaigns).

This period also marked P&G's most controversial chapter: the Clorox debacle. In 1957, P&G acquired the bleach manufacturer for $30 million, seeking to dominate another cleaning category. But the Federal Trade Commission saw dangerous monopolistic behavior. The legal battle raged for a decade, ultimately reaching the Supreme Court, which ruled against P&G in 1967. The forced divestiture taught P&G a crucial lesson: there were limits to growth through acquisition, especially in adjacent categories where they already held dominant positions.

The 1960s and 1970s saw P&G systematically conquering every room in the American home. Head & Shoulders (1961) attacked dandruff with zinc pyrithione technology. Downy fabric softener (1960) and Bounce dryer sheets (1972) redefined laundry care. Pringles (1968) attempted to reinvent the potato chip with uniform stackable crisps in a can—though it would take decades to become profitable.

Behind these launches was an R&D operation unlike anything in consumer products. P&G's research centers employed more PhDs than many universities—chemists, biologists, psychologists, even anthropologists studying how consumers actually used products. The Miami Valley laboratories in Cincinnati became a innovation powerhouse, generating hundreds of patents annually. By 1985, P&G was investing $600 million yearly in R&D, more than the GDP of some small nations.

The company's approach to innovation was uniquely systematic. They didn't just create products; they created categories. When P&G entered a market, they sought to fundamentally redefine it through superior technology. This required patience—Pringles took 15 years to become profitable, Olestra (the fat substitute) consumed $500 million over 25 years—but when it worked, the rewards were extraordinary.

International expansion accelerated dramatically. By 1980, P&G operated in 23 countries. By 1990, that number had doubled. Each market required careful adaptation. Japanese consumers, P&G discovered, wanted smaller package sizes for their tiny apartments. Latin American families preferred stronger fragrances. Chinese consumers needed education about categories like disposable diapers that didn't exist in their markets.

The numbers by century's end were staggering. P&G's revenue reached $40 billion by 2000. They commanded leading positions in multiple billion-dollar categories: laundry detergents, diapers, feminine care, shampoo, oral care. The company employed 110,000 people globally and spent $4 billion annually on advertising—more than the entire revenue of most competitors.

Yet beneath this success, cracks were forming. The portfolio had grown unwieldy—over 300 brands by some counts. Growth was slowing as categories matured. New competitors, particularly from Asia, were emerging. And a fundamental shift was underway—the internet was beginning to change how consumers discovered and purchased products. As the new millennium arrived, P&G's century-old playbook would face its greatest test.

V. The Lafley Era I: Crisis and Transformation (2000–2009)

Durk Jager lasted exactly 17 months as CEO of Procter & Gamble. When he was forced out in June 2000, P&G's stock had fallen 50%, evaporating $85 billion in market value. The company had missed earnings forecasts three quarters in a row. Morale was shattered. The board, in desperation, turned to an unlikely savior: A.G. Lafley, a soft-spoken company lifer who was literally on vacation in Cape Cod when he got the call.

"I never wanted the job," Lafley would later admit. At 52, after 23 years at P&G, he was comfortable running the Beauty and Health division. But when he walked into the CEO office that June morning, he found a company in existential crisis. Jager's "Organization 2005" had attempted to transform P&G overnight—new IT systems, new organizational structure, new innovation processes, all at once. The result was chaos. Product launches were failing, retailers were furious about service problems, and employees were paralyzed by confusion. Lafley's first move was radical in its simplicity. He shut down skunkworks projects and pulled flopped launches such as Fit and Olay Cosmetics. He also sold off the Jif and Crisco units, which weren't strategic fits. Together, these measures yielded some $2 billion in savings. "We need to get back to what we do best," he told his leadership team, assembled for an emergency meeting just days into his tenure. "We're going to focus on big brands, big countries, and big customers."

The simplicity of this message—after years of Jager's complex reorganizations—was like oxygen to a drowning organization. Lafley understood something profound: P&G produced a dizzying array of well-known brands including Tide, Pampers, Crest, Always and Pantene, but its portfolio also included coffee, snack foods, peanut butter, shortening and oils, household cleaners and pharmaceutical drugs. Lafley began asking himself: What businesses should P&G be in?

The cultural transformation Lafley orchestrated was as important as the financial turnaround. In the fabled 11th-floor executive suites at P&G's Cincinnati headquarters, Lafley had the oak-paneled walls torn down and donated the 19th-century oil paintings to a local art museum. The CEO and his top brass would sit in cubicles on half the floor. The other half was being transformed into an employee learning center. The symbolism was unmistakable: hierarchy was out, collaboration was in.

But Lafley's masterstroke was recognizing that P&G's innovation model was broken. The company had always prided itself on internal R&D—its labs had invented everything from synthetic detergents to disposable diapers. But by 2000, this model was unsustainable. Newly appointed CEO A.G. Lafley saw that P&G couldn't meet its growth objectives by spending greater and greater amounts on R&D for smaller and smaller payoffs. So he dispensed with the company's age-old "invent it ourselves" approach to innovation and instead embraced a "connect and develop" model. By identifying promising ideas throughout the world and applying its own capabilities to them, P&G realized it could create better and cheaper products, faster.

The Connect + Develop program was revolutionary for a company as prideful as P&G. Rather than seeing external innovation as a threat to internal capabilities, Lafley reframed it as multiplication. "We have 7,500 researchers inside P&G," he'd say. "But there are 1.5 million researchers with relevant expertise outside P&G. Why wouldn't we tap into that?" Procter & Gamble's radical strategy of open innovation now produces more than 35% of the company's innovations and billions of dollars in revenue.

The results of Lafley's first era were spectacular. Between 2000 and 2008 P&G's revenue more than doubled from $40 billion to $83 billion, while earnings took a gigantic leap from $2.5 billion to more than $12 billion. During Lafley's tenure, the Company's market capitalization more than doubled, making P&G one of the five most valuable companies in the U.S. and among the 10 most valuable companies in the world.

The beauty business transformation exemplified Lafley's strategic clarity. When he became CEO, P&G's beauty division was an underperformer. Olay, acquired years earlier, was stuck as a $100 million brand selling basic moisturizers for $5 at drugstores. "Can we create enough new Olay consumers with our brand and our products?" Lafley asked. "Can we build a business of about $1 billion?" In 2000, when they started to redo Olay's strategy, if someone told him the brand was going to do $2 billion to $2.5 billion in sales, he wouldn't have bet on it. Yet that's exactly what happened through premium product innovation and repositioning. The company's strategic expansion into beauty accelerated in 2003 when P&G signed an agreement to purchase a controlling interest in Wella AG, the German beauty company known for its upscale Wella, Sebastian and Koleston hair care brands, for 3.2 billion euros ($3.4 billion). P&G ultimately paid a total of $5.7 billion including shares, purchasing 77.6% of the company. "P&G and Wella are in highly complementary businesses," explained A.G. Lafley. "Wella's strength in professional hair care complements P&G's strength in retail hair care. Wella's strength in color and styling complements P&G's strength in shampoos and conditioners."

By 2009, when Lafley first retired, the transformation was complete. With Lafley leading the company for all of the 2000s, P&G more than doubled sales since the beginning of the decade. The company's portfolio of billion-dollar brands grew from 10 to 24 and the number of brands with sales between $500 million and $1 billion increased five-fold. On average, P&G's annual organic sales grew 5%, annual core earnings-per-share grew 12%, and free cash flow productivity averaged 112% a year since 2001. The Company's market capitalization more than doubled, making P&G one of the five most valuable companies in the U.S. and among the 10 most valuable companies in the world.

VI. The Gillette Mega-Deal: A $57 Billion Bet (2005)

James Kilts picked up the phone on a January morning in 2005 with the kind of call that defines corporate history. The Gillette CEO had been wrestling with a fundamental question: In a world of retail consolidation and private label pressure, could even the mighty Gillette—maker of "The Best a Man Can Get"—remain independent? On the other end of the line was A.G. Lafley, and his message was simple: "Jim, I think we should talk. "On January 28, 2005, P&G announced the largest acquisition in its history to buy Gillette in a $57 billion deal. The backstory, however, began years earlier. In 1999, Procter & Gamble had considered the possibility of acquiring Gillette and was generally familiar with Gillette's brands and operations. But it wasn't until 2005, with both companies operating from positions of strength, that the stars aligned.

The negotiation itself was remarkably swift and cordial. As Lafley later recalled: "It was a no-brainer from a strategy standpoint." On that first call, "I asked him if he had a price in mind. He said the usual things about a fair price. He said, 'Not $60. But not $50.' I said, 'Jim, I can do the math. Are you thinking $55 a share?' Gillette was at $44 or $45 at the time."

The major products of Gillette included its signature razors, Duracell batteries, Braun, and Oral-B brands dental care products. For P&G, this wasn't just about adding brands—it was about transforming the company's entire portfolio. The addition of Gillette's brands accelerated the evolution of P&G's portfolio into faster growing, higher margin and more asset efficient health, personal care and beauty businesses. With the exception of batteries and appliances, all business segments fell into health and beauty, which would now represent a full 50% of P&G's portfolio.

The deal structure was elegant: P&G paid 0.975 share of its common stock for each share of Gillette common stock. On the basis of the closing price of $55.32 per share on January 28, 2005, the deal valued Gillette at about $54 per share which represented an 18% premium over its closing price. To address dilution concerns, Procter & Gamble announced a common stock repurchase program pursuant to which it planned to repurchase up to $18 billion to $22 billion of its common stock over a period of 12-18 months.

Warren Buffett's involvement added credibility and momentum. Berkshire Hathaway Inc. owned 9.7 percent of Gillette, or about 96 million shares. Buffett, Gillette's largest single shareholder, called the combination "a dream deal" and said he planned to buy another 6.4 million P&G shares to reach 100 million by late this year when the sale was expected to close.

The regulatory hurdles were significant but manageable. The consent order permitted The Procter & Gamble Company's acquisition of rival consumer products manufacturer The Gillette Company, provided the companies divest: 1) Gillette's Rembrandt at-home teeth whitening business; 2) P&G's Crest SpinBrush battery-powered and rechargeable toothbrush business; and 3) Gillette's Right Guard men's antiperspirant deodorant business.

The cultural integration challenge was immense. Gillette had its own proud heritage—founded in 1901, it had revolutionized shaving and built one of the world's most recognizable brands. P&G wisely retained James Kilts as vice chairman, ensuring continuity and respecting Gillette's culture. "We believe we can bring these companies together and create a juggernaut," Kilts said at the announcement.

The financial impact exceeded even the optimistic projections. With Gillette acquisition, P&G had 10 billion dollar brands in Beauty and Health and 12 billion dollar brands in Baby, Family and Household segments. More importantly, the average net earnings margin in the post-merger period improved to 13.6% from 10.7% in the premerger period.

The Gillette acquisition represented more than just scale—it was a bet on the future of consumer products. In an era of retail consolidation, where Walmart and other mega-retailers were squeezing suppliers, the combination gave P&G unprecedented negotiating leverage. The deal brought together complementary strengths: P&G's excellence in mass market products with Gillette's premium positioning, P&G's strength in emerging markets with Gillette's dominance in developed ones.

VII. Peak Complexity: Too Big to Manage? (2009–2013)

Bob McDonald stood before Wall Street analysts in 2010 with an audacious promise: P&G would add one billion new consumers by 2015. The West Point graduate and former Army Ranger had succeeded A.G. Lafley with a mandate to continue growth, but his military precision would prove inadequate for the chaos that was about to engulf the consumer products industry.

By 2012, P&G had become a sprawling empire of staggering complexity. The company managed over 170 brands across dozens of categories. The product portfolio had grown so vast that managers joked they needed a directory just to keep track of what P&G actually sold. From Pringles potato chips to Duracell batteries, from pet food to pharmaceuticals, the company seemed to be in every aisle of every store on the planet. The numbers looked good on paper. Under his leadership, P&G significantly recalibrated its product portfolio, expanded its marketing footprint by adding nearly one billion people to its global customer base, and grew the firm's organic sales by an average of three percent per year. This growth was reflected in P&G's stock price, which rose from $51.10 the day he became CEO to $81.64 on the day his last quarterly results were announced—a 60 percent increase from 2009 to 2013.

But beneath the surface, the company was struggling. Amid the 2008 economic downturn, investors criticized McDonald for being too attached to P&G traditions, too slow to pursue layoffs and other cuts, and unable to produce new product innovations, particularly compared to his predecessor A.G. Lafley. The core issue was fundamental: P&G's scale had become a liability rather than an asset.

The disruption came from an unexpected quarter. In 2011, a startup called Dollar Shave Club launched with a viral video and a simple proposition: "Our blades are f***ing great." For $1 a month, they'd mail you quality razors—no retail markup, no fancy packaging, no billion-dollar advertising campaigns. Within two years, they had captured 8% of the U.S. razor market, territory P&G's Gillette had spent a century defending. Dollar Shave Club was more than just competition—it was an existential threat to P&G's entire business model. P&G's first advantage, their willingness to spend money on research and development, was neutralized because razors were already good enough. Stop paying for shave tech you don't need. AWS made it easy for Dollar Shave Club, hosted on AWS servers, to neutralize P&G's distribution advantage: on the Internet, shelf space is unlimited. More than that, an e-commerce model meant that Dollar Shave Club could not only be cheaper but also better: having your blades shipped to you automatically was a big advantage over going to the store.

The disruption spread beyond razors. Private label brands, once dismissed as inferior generics, were suddenly winning with quality products and sophisticated packaging. Retailers like Target and Kroger launched premium private label lines that competed directly with P&G brands at 20-30% lower prices. E-commerce enabled a flood of niche brands—Native deodorant, Quip toothbrushes, Seventh Generation cleaning products—each chipping away at P&G's categories.

Meanwhile, P&G's organizational complexity had become paralyzing. Decision-making required navigating through layers of brand managers, category leaders, regional presidents, and functional heads. A simple packaging change could take 18 months to implement. Innovation slowed to a crawl—the company was launching fewer breakthrough products than at any time in its history.

The financial markets lost patience. Bill Ackman's Pershing Square Capital Management took a significant stake and began agitating for change. Ackman was vocal in calling for McDonald to step down, arguing that P&G needed dramatic restructuring, not incremental improvement. The pressure mounted quarter after quarter as P&G missed earnings expectations and lost market share across key categories.

In May 2013, Robert A. McDonald announced his retirement and was replaced by A.G. Lafley, who returned as chairman, president, and CEO. The board's decision to bring back a retired CEO was unprecedented in P&G history—a clear admission that the company needed radical change, not evolution.

When Lafley walked back into the CEO office, he found a fundamentally different company than the one he'd left in 2009. The portfolio had ballooned to over 170 brands, many generating minimal profits. The organization was bloated with 140,000 employees. Growth had stagnated. Most worryingly, P&G had lost its innovation edge—the very thing that had driven its success for over a century.

VIII. The Great Simplification: Lafley Returns (2013–2015)

A.G. Lafley stood before P&G employees in August 2014 with a message that would have been heresy just years earlier: "We're going to become a much simpler, much less complex company." After 177 years of relentless expansion, P&G was about to embark on the largest divestiture program in corporate history. On August 1, 2014, P&G announced it was streamlining the company, dropping and selling off around 100 brands from its product portfolio in order to focus on the remaining 65 brands, which produced 95% of the company's profits. The announcement was stunning: P&G would be divesting or discontinuing 90 to 100 brands whose sales and profits had been declining over the past three years. The brands in question have seen sales declining 3 percent and profits declining 16 percent, and have margins less than half the company average.

"We will become a much simpler, much less complex company of 70 to 80 brands," Lafley declared. The future P&G would be "a much simpler, much less complex company of leading brands that's easier to manage and operate." It was an admission that bigger wasn't always better, that complexity had become the enemy of performance.

Lafley used the example of P&G's laundry division in the US, which used to have a portfolio of 15 brands just over a decade ago but now had just five. As a result of that simplification, P&G's market share had increased, almost to 60 percent again and its "share of value" was at its highest level ever. "There's a lot of evidence in a number of our business categories that the shopper and consumer really doesn't want more assortment and more choice, they want efficient consumer response."

The divestiture program was executed with military precision. Crisco vegetable oil and shortening, Folgers coffee, Jif peanut butter, and Millstone coffee were sold to the J.M Smucker Company for approximately $3.3 billion. Pringles potato chips was sold to Kellogg for $2.7 billion. Camay and Zest were sold to Unilever for an undisclosed sum. P&G exited the pet food business, selling most of Iams, Eukanuba, and Natura brands to candy bar and Pedigree-maker Mars for $2.9 billion. P&G also disposed of its billion dollar brand Duracell Batteries to Berkshire Hathaway for $4.7 billion. The biggest divestiture came in July 2015 when P&G announced the sale of 43 of its beauty brands to Coty, a beauty-product manufacturer, in a US$13 billion deal. The transaction included P&G's global salon professional hair care and color, retail hair color, cosmetics and fine fragrance businesses, along with select hair styling brands. The beauty division, which had been one of P&G's largest segments, had been struggling with net sales falling 2% in both 2014 and 2013. It cited sluggish growth of its beauty division as the reason for the divestiture. The sale was completed on October 3, 2016.

The portfolio included marquee names: Wella, Clairol, CoverGirl, Max Factor, and a host of luxury fragrance licenses including Hugo Boss, Dolce & Gabbana, and Gucci. These weren't failed brands—many were profitable and growing. But they didn't fit Lafley's vision of a focused P&G built around core categories where the company had structural advantages.

"This represents a significant step forward in the work to focus our portfolio on 10 categories and 65 brands that best leverage P&G's core competencies," Lafley said. The strategic logic was clear: P&G would focus on categories where it could achieve scale advantages, pricing power, and innovation leadership. Everything else, no matter how successful, had to go.

The financial engineering behind these divestitures was sophisticated. Many were structured as Reverse Morris Trust transactions to minimize tax implications. The Coty deal alone generated $11.4 billion in value for P&G shareholders. The company used proceeds to fund a massive share buyback program, returning capital to shareholders while streamlining operations.

The transformation wasn't just about what P&G sold—it was about what remained. The 65 brands that survived the cut were the crown jewels: Tide, Pampers, Gillette, Crest, Bounty, Charmin, Always, Dawn, Olay, Head & Shoulders. These brands generated the vast majority of profits and had defendable market positions.

IX. Modern P&G: Digital Transformation and New Challenges (2015–Present)

David Taylor took the CEO reins from A.G. Lafley in November 2015 with a clear mandate: execute the simplification strategy while preparing P&G for a digital future. A 35-year company veteran who started as a production manager, Taylor understood P&G's operations intimately. But he also recognized that the consumer products industry was undergoing its most fundamental transformation since the invention of television advertising. Taylor's tenure from 2015 to 2021 was marked by operational excellence and digital transformation. He continued Lafley's simplification agenda while investing heavily in e-commerce capabilities. Under his leadership, P&G's e-commerce sales grew from less than 5% of total sales to over 14% by 2021—a critical shift as Amazon became the largest retailer of consumer products globally.

The company's approach to digital wasn't just about selling online. P&G invested billions in data analytics, artificial intelligence, and digital marketing capabilities. They could now track consumer behavior in real-time, adjust marketing campaigns on the fly, and predict demand patterns with unprecedented accuracy. The company's "Smart Audience" program used machine learning to identify and target high-value consumers with precision that would have been unimaginable in the soap opera era.

In December 2018, Procter & Gamble completed the acquisition of the consumer health division of Merck Group (known as EMD Serono in North America) for €3.4 billion ($4.2 billion) and renamed it as Procter & Gamble Health Limited in May 2019. This strategic move expanded P&G's presence in the growing consumer healthcare market.

The COVID-19 pandemic in 2020 became an unexpected catalyst for P&G's transformation. As consumers stockpiled cleaning products and personal care items, P&G's sales surged. But more importantly, consumer behavior shifted permanently toward e-commerce and subscription models. P&G was ready—their digital investments paid off as they could meet demand through multiple channels while competitors struggled with supply chain disruptions.

Jon R. Moeller succeeded David Taylor as president and CEO on November 1, 2021, while Taylor became executive chairman. Moeller, who joined P&G in 1988 and served as CFO and COO, brought deep financial discipline and operational expertise. He played a pivotal role in designing and implementing P&G's portfolio, superiority, productivity and organization design strategy, as part of one of the most significant transformations in the company's history.

Under Moeller's leadership, P&G has embraced artificial intelligence and machine learning not as buzzwords but as fundamental tools for innovation. "We're increasingly moving innovation from the lab bench to very sophisticated computers," Moeller explained. This approach helps the company speed up molecular discovery, explore more areas for innovation, and come up with more successful product ideas.

In 2023, the company began optimizing its product offering further. As part of this strategy, it plans to eliminate the bottom 25% of SKUs, which contribute very little to absolute retail sales. This continuous pruning reflects a new P&G philosophy: complexity is the enemy of growth.

The modern P&G faces challenges unimaginable to William Procter and James Gamble. Climate change demands sustainable packaging and carbon-neutral operations. Social media can destroy a brand's reputation in hours. Startups can go from idea to billion-dollar valuation in years, not decades. Chinese competitors are expanding globally with quality products at lower prices.

Yet P&G's response has been remarkably consistent with its history: innovate, adapt, and focus relentlessly on the consumer. The company has committed to achieving net-zero greenhouse gas emissions by 2040. They're investing in recyclable packaging and waterless products. They're partnering with startups through their ventures arm rather than viewing them solely as threats.

X. Playbook: The P&G Way

After nearly two centuries, what is the P&G playbook? How does a soap and candle company from 1837 remain relevant in the age of TikTok and Amazon? The answer lies not in any single strategy but in a system of interconnected capabilities that create compounding advantages over time.

Brand Building at Scale: The Billion-Dollar Brand Factory

P&G doesn't just create products; it manufactures cultural artifacts. The company's approach to brand building is both art and science, combining massive consumer research with creative storytelling. Every P&G brand starts with a fundamental consumer insight—what the company calls a "consumer truth." Tide isn't just about clean clothes; it's about the confidence that comes from looking your best. Pampers isn't about dryness; it's about babies sleeping through the night so parents can too.

The company invests approximately $2 billion annually in consumer research, conducting over 15,000 research studies involving more than 5 million consumers. This isn't just asking people what they want—P&G ethnographers live with families, shop with them, and observe their daily routines. They've discovered that Mexican consumers want stronger fragrances, Japanese consumers need smaller package sizes, and Indian consumers often wash clothes by hand, requiring different formulations.

Once a brand concept is validated, P&G deploys what insiders call the "launch algorithm"—a systematic process refined over decades. First comes the product itself, which must deliver a noticeable benefit versus competition. Then comes the positioning, communicated through advertising that P&G tests exhaustively before launch. Distribution follows, leveraging P&G's relationships with retailers globally. Finally comes the scaling phase, where successful products are rapidly expanded across geographies and categories.

Category Creation and Market Education

P&G's greatest successes haven't come from competing in existing markets but from creating entirely new ones. Disposable diapers didn't exist before Pampers. The concept of "fabric softener" was invented by P&G with Downy. Even the idea that toothpaste should prevent cavities rather than just clean teeth was a P&G innovation with Crest.

Creating categories requires patience and deep pockets. Pampers took over a decade to become profitable. Febreze initially failed because consumers didn't realize they needed it—P&G had to educate the market about "nose blindness" to odors in their own homes. Swiffer required teaching consumers that traditional mopping was outdated. Each category creation follows a pattern: identify an unarticulated need, develop a solution, educate the market, and then defend the position through continuous innovation.

Retailer Relationships and Shelf Space Dominance

P&G's relationship with retailers is symbiotic and sophisticated. The company doesn't just sell products to Walmart or Target; it partners with them to grow entire categories. P&G's customer teams—sometimes numbering in the hundreds for major accounts—work directly with retailers on everything from shelf layouts to inventory management to joint marketing campaigns.

The company pioneered "category management" in the 1980s, offering to manage entire sections of stores for retailers—not just P&G products but competitors' too. This gave P&G unparalleled insights into shopping behavior and competitive dynamics while making them indispensable to retailers. Today, P&G's data and analytics capabilities help retailers optimize everything from pricing to promotion timing to product placement.

Innovation System: From Internal R&D to Connect + Develop

P&G's innovation model has evolved from purely internal R&D to what they call "Connect + Develop"—a recognition that not all good ideas originate within P&G's walls. The company maintains relationships with thousands of external innovators, from university researchers to startup entrepreneurs to supplier laboratories.

The numbers are staggering: P&G invests about $2 billion annually in R&D, employs over 7,500 researchers, and holds over 25,000 patents. But the real power comes from multiplication—through Connect + Develop, P&G taps into an estimated 1.5 million researchers globally with relevant expertise. This network has produced innovations like Pringles Prints (edible printing technology from an Italian bakery equipment company) and Olay Regenerist (peptide technology from a French partner).

Marketing Excellence: From Soap Operas to Digital Precision

P&G literally invented modern marketing. From soap operas to brand management to digital micro-targeting, the company has consistently been at the forefront of reaching consumers. Today, P&G spends about $7 billion annually on advertising—one of the largest budgets globally—but the approach has evolved far beyond television commercials.

The company's marketing is increasingly digital, personalized, and performance-driven. P&G's "Smart Audience" platform uses artificial intelligence to identify high-value consumers and deliver personalized messages across channels. They can now measure the impact of advertising not just on awareness but on actual sales, adjusting campaigns in real-time based on performance data.

M&A Strategy: When to Buy, When to Build, When to Divest

P&G's M&A strategy reflects a clear philosophy: acquire to enter new categories or geographies, build organically within existing strengths, and divest when competitive advantage erodes. The Gillette acquisition brought P&G into male grooming and batteries. The Wella purchase expanded beauty capabilities. But P&G also knows when to sell—divesting Pringles, Duracell, and 100+ other brands when they no longer fit the strategic focus.

The company's acquisition criteria are stringent: the target must be in an attractive category, offer synergies with existing capabilities, and be available at a reasonable price. P&G walks away from more deals than it completes, showing discipline rare in corporate America.

Talent Development: The CEO Factory

P&G is renowned as a training ground for business leaders. The company has produced CEOs for Microsoft (Steve Ballmer), Boeing (Jim McNerney), eBay (Meg Whitman), and dozens of other major corporations. This isn't accidental—P&G invests heavily in leadership development, rotating high-potential employees through different functions, categories, and geographies.

The company's promote-from-within culture means that most senior executives have 20+ year tenures, ensuring deep institutional knowledge. P&G University offers thousands of training courses, from technical skills to leadership development. The company's alumni network—P&G executives who've moved to other companies—provides valuable intelligence and partnership opportunities.

Capital Allocation and Shareholder Returns

P&G's approach to capital allocation is disciplined and shareholder-friendly. The company has paid dividends for 134 consecutive years and increased them for 68 straight years—one of the longest streaks in corporate history. Share buybacks supplement dividends, with P&G returning over $140 billion to shareholders over the past two decades.

The company maintains a simple capital allocation framework: invest in the business for growth, maintain a strong credit rating, pay a reliable and growing dividend, and return excess cash to shareholders. This predictability has made P&G a favorite among institutional investors and retirees seeking stable income.

XI. Analysis & Investment Case

Bull Case: The Enduring Competitive Advantages

The bullish argument for P&G rests on several structural advantages that remain intact despite industry disruption. Scale still matters enormously in consumer products. P&G's ability to spend $2 billion on R&D and $7 billion on advertising creates barriers that startups can't overcome. The company's manufacturing footprint—110+ plants globally—provides cost advantages through economies of scale that no DTC brand can match.

Pricing power remains robust in P&G's core categories. When inflation spiked in 2021-2023, P&G successfully passed through price increases with minimal volume impact. Consumers proved willing to pay more for trusted brands during uncertain times—a validation of P&G's brand equity. The company's gross margins have expanded from 47% in 2015 to over 50% today, demonstrating pricing discipline and mix improvement.

Emerging markets represent a massive growth opportunity. P&G reaches only about 5 billion of the world's 8 billion people. As income levels rise in India, Southeast Asia, Africa, and Latin America, demand for branded consumer products will explode. P&G's early investments in these markets—often accepting losses for years to build distribution and brand awareness—position them to capture disproportionate growth.

The innovation pipeline remains healthy. P&G's ventures into sustainable products (EC30 laundry sheets), premium segments (Native deodorant acquisition), and new categories (personal health devices) show the company can still innovate. The Connect + Develop model means P&G can access external innovation while leveraging its commercialization capabilities.

Bear Case: Structural Headwinds and Disruption Threats

The bearish perspective focuses on secular challenges facing traditional CPG companies. Category maturity is real—how much innovation can really happen in laundry detergent or toilet paper? Growth in developed markets barely exceeds inflation, forcing P&G to rely on price increases and emerging markets for expansion.

Digital disruption continues to intensify. Amazon's private label ambitions, direct-to-consumer brands, and subscription services all chip away at P&G's model. While Dollar Shave Club was acquired and neutralized, new competitors emerge constantly. The next disruption might come from China, where companies like Unilever-rival Bluemoon have built massive businesses with different models.

Complexity remains a challenge despite simplification efforts. Even with "only" 65 brands, P&G operates across dozens of categories and hundreds of markets. Each requires different capabilities, regulations, and competitive dynamics. The overhead required to manage this complexity weighs on margins and slows decision-making.

Valuation poses another concern. As of today, P&G market cap is 361.57B. Trading at over 25x earnings, P&G is priced for perfection. Any disappointment in growth or margins could trigger significant multiple compression. With interest rates higher than the past decade, investors have alternatives to expensive consumer staples stocks.

Competitive Positioning

P&G's competitive position varies dramatically by category and geography. In laundry care, P&G dominates with 30%+ global share, but faces intense competition from Unilever and Henkel. In beauty, despite divestitures, P&G struggles against L'Oréal's innovation and Estée Lauder's prestige positioning. In razors, the Gillette franchise has stabilized but lost permanent share to Dollar Shave Club, Harry's, and private label.

The company's geographic exposure is both strength and weakness. North America generates 40%+ of sales but grows slowly. Europe faces economic stagnation and aggressive private label competition. China, once a growth engine, has become increasingly challenging with local competition and economic slowdowns. The brightest spots are India, Southeast Asia, and Africa—but these markets are also the most competitive and price-sensitive.

Financial Metrics and Valuation

P&G's financial metrics reflect a mature, high-quality business. Return on invested capital exceeds 20%, among the best in consumer products. Free cash flow conversion consistently exceeds 90% of net income. The balance sheet is conservative with debt/EBITDA under 2x, providing flexibility for acquisitions or shareholder returns.

The valuation debate centers on whether P&G deserves a premium multiple. Bulls argue the quality, consistency, and defensive characteristics justify 25x+ earnings. Bears contend that low growth and disruption risks warrant a discount to historical multiples. The truth likely lies between—P&G is neither the untouchable fortress bulls imagine nor the melting ice cube bears predict.

ESG Considerations

Environmental, social, and governance factors increasingly influence P&G's investment case. The company's 2040 net-zero commitment requires massive investment in renewable energy, sustainable packaging, and product reformulation. Success could provide competitive advantage; failure risks regulatory penalties and reputational damage.

Social considerations around product safety, diversity, and community impact affect brand perception, particularly among younger consumers. P&G's track record is mixed—praised for advertising that promotes gender equality, criticized for chemical ingredients in some products. Governance remains strong with an independent board and aligned executive compensation, though some question whether the promote-from-within culture limits fresh thinking.

XII. Epilogue & Lessons

William Procter and James Gamble would likely be astounded by what their soap and candle company has become. The moon-and-stars logo they created still appears on products, but those products clean clothes with synthetic polymers, protect babies with superabsorbent chemicals, and remove stains with engineered enzymes. The company they founded to serve Cincinnati now operates on every continent, employing over 100,000 people and generating $85 billion in annual sales.

Yet they might also recognize fundamental continuities. P&G still obsesses over product quality—William Procter's insistence on consistent soap formulation echoes in today's Six Sigma manufacturing standards. The company still invests heavily in understanding consumers—James Gamble's recognition that families wanted one soap for multiple uses parallels today's ethnographic research. Most importantly, P&G still believes that business success comes from improving consumers' lives, even in small ways.

The Paradox of Scale

P&G's history illustrates a fundamental paradox: scale enables success but also breeds complexity that undermines it. Every acquisition, every new category, every geographic expansion added revenues but also coordination costs. The company that once made just soap and candles eventually sold everything from potato chips to prescription drugs.

A.G. Lafley's great insight was recognizing that bigger isn't always better. By divesting 100+ brands, P&G acknowledged that focus beats breadth. The challenge for future leaders will be maintaining this discipline as growth becomes harder to find. The temptation to expand into adjacent categories or acquire trendy brands will be constant.

Key Takeaways for Entrepreneurs and Investors

P&G's journey offers several timeless lessons:

First, brand building requires patience and investment. Ivory took years to become profitable. Pampers required a decade of losses. Febreze initially failed completely. But P&G persisted, refined, and eventually dominated. In an era of quarterly capitalism, this long-term orientation is both rare and valuable.

Second, innovation must be systematic, not sporadic. P&G's R&D isn't just about breakthrough products but continuous improvement. Tide has been reformulated over 70 times. Gillette razors evolved from one blade to five. Small innovations compound into insurmountable advantages.

Third, distribution still matters enormously. Despite e-commerce growth, 85% of consumer products are still sold in physical stores. P&G's relationships with retailers, understanding of shopper behavior, and supply chain capabilities remain massive competitive advantages that pure-digital brands can't replicate.

Fourth, culture eats strategy for breakfast. P&G's promote-from-within culture, consensus-driven decision-making, and conservative financial management have survived multiple CEOs and strategies. These cultural elements provide stability but also resistance to change—a double-edged sword in dynamic markets.

P&G's Influence on Modern Business

P&G's impact extends far beyond consumer products. The company pioneered brand management, now standard across industries. Its approach to market research transformed how companies understand consumers. Its advertising innovations, from soap operas to targeted digital marketing, shaped modern media.

The company's alumni network reads like a Who's Who of corporate America. Former P&G executives lead companies across industries, spreading the P&G way of systematic analysis, consumer focus, and operational excellence. Business schools teach P&G cases as canonical examples of marketing, strategy, and leadership.

Perhaps most importantly, P&G proved that consumer products companies could be innovative, global, and enduringly successful. Before P&G, soap was a commodity. After P&G, it became Ivory, a brand worth paying premium prices for. This transformation—from commodity to branded product—became the template for countless companies across industries.

Final Reflections

Procter & Gamble's story is ultimately about the power of compound improvement. Each generation of leaders built upon their predecessors' work, adding new capabilities while preserving core strengths. The company that William Procter and James Gamble founded made soap and candles. Their successors added branding and advertising. The next generation brought scientific R&D. Then came international expansion, category creation, digital transformation.

Today's P&G faces challenges its founders couldn't have imagined: climate change, social media, artificial intelligence, global competition. Yet the company's response remains consistent: understand consumers deeply, innovate relentlessly, execute flawlessly. Whether this formula remains sufficient for the next 187 years remains to be seen.

What's certain is that P&G will continue evolving. The company that started with two immigrants stirring soap in Cincinnati kettles now uses AI to design molecules and predict consumer behavior. The business that once sold door-to-door now reaches billions through e-commerce and subscription services. The only constant, as William Procter might say, is change—and the relentless pursuit of serving consumers just a little bit better each day.

For investors, P&G represents a fascinating paradox: a company simultaneously disrupted and dominant, mature and innovative, global and local. It's neither the obvious buy that dividend investors assume nor the obvious sell that growth investors conclude. Instead, P&G embodies the complexity of modern business—where competitive advantages erode faster than ever, but the best companies find ways to rebuild them.

As P&G approaches its third century, its greatest challenge may be maintaining relevance in an accelerating world while preserving the patient, systematic approach that created its success. The next chapter of the P&G story remains unwritten, but if history is any guide, it will involve equal measures of continuity and change, tradition and innovation, scale and focus. The moon-and-stars will endure, even as everything else transforms.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube