Principal Financial Group: Building America's Retirement Backbone

I. Introduction & Episode Roadmap

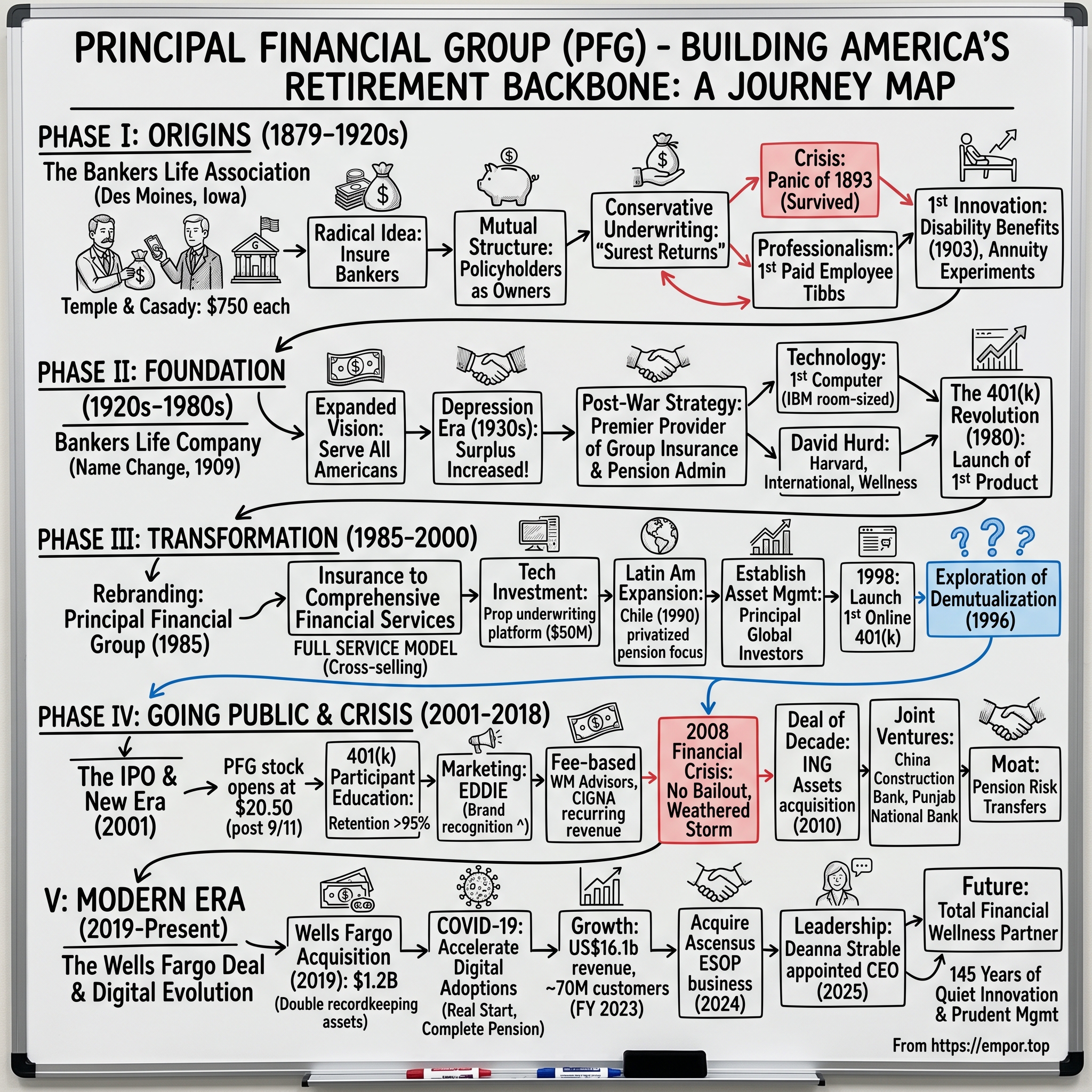

Picture this: Des Moines, Iowa, 1879. While railroad barons and industrial titans dominated the American financial landscape, a quiet revolution began in a modest office where bankers gathered to solve a problem that kept them awake at night—what would happen to their families if they died? This wasn't Wall Street. This wasn't J.P. Morgan's marble halls. This was the heartland, where Edward Temple and Simon Casady each pulled $750 from their pockets—about $23,000 in today's money—to create something that would eventually manage the retirement dreams of millions of Americans. How did a small Iowa insurance company for bankers become a Fortune 500 retirement and asset management powerhouse? The answer lies in 145 years of quiet innovation, strategic pivots, and an almost obsessive focus on something most Americans worry about but rarely plan for properly: retirement. Today, Principal Financial Group manages US$16.1b in revenue, serving approximately 70 million customers across the globe. But to understand how we got here, we need to go back to that Des Moines office where it all began.

This is the story of Principal Financial Group—a company that transformed from The Bankers Life Association into one of America's most important financial institutions. It's a tale of Midwest pragmatism meeting Wall Street sophistication, of surviving multiple financial crises without government bailouts, and of building what might be the most underappreciated moat in financial services: being the boring, reliable backbone of American retirement planning.

Over the next several hours, we'll trace Principal's evolution through five major transformations: from mutual association to insurance giant, from regional player to national powerhouse, from insurance company to financial services conglomerate, from private mutual to public corporation, and finally, from domestic operator to global financial institution. We'll explore how they built dominant positions in 401(k) administration, navigated the 2008 financial crisis, executed transformative acquisitions, and positioned themselves for the retirement wave that's just beginning to crest.

What makes Principal particularly fascinating isn't just its size or longevity—it's how the company has consistently zigged when others zagged. While competitors chased glamorous investment banking or traded complex derivatives, Principal doubled down on the unglamorous but essential business of helping middle America save for retirement. That focus has created a business with remarkable economics: recurring revenue streams, deep customer relationships, and competitive advantages that compound over time.

II. Origins: The Bankers Life Association (1879–1920s)

The summer of 1879 in Des Moines was sweltering, and inside the Equitable Life Insurance building, Edward Temple was sweating for reasons beyond the heat. The 35-year-old banker had just witnessed another colleague's widow left destitute after her husband's sudden death. Life insurance existed, sure, but for bankers—considered high-risk due to their sedentary lifestyle and exposure to financial stress—premiums were astronomical. Temple had an idea that seemed radical: what if bankers insured themselves?

On July 1, 1879, Temple gathered a small group of fellow bankers in that same building. The proposition was simple but revolutionary: create a mutual insurance association by bankers, for bankers. Temple and Simon Casady, another local banker who shared Temple's vision, each contributed $750 in startup capital. In today's dollars, that's roughly $23,000 each—not exactly a fortune, but enough to rent office space and print certificates.

The board of directors read like a who's who of Iowa banking: Phineas Casady (Simon's brother), Dr. George Glick, M.S. Smalley, B.F. Elbert, and Temple himself. These weren't insurance experts; they were bankers who understood risk and saw an opportunity to solve their own problem. The mutual structure was key—policyholders would own the company, ensuring that profits would benefit members rather than outside shareholders.

The economics were compelling. Traditional insurance companies charged bankers premiums that reflected their perceived risk profile. But Temple's insight was that bankers, as a group, actually had lower mortality rates than many other professions. By pooling their risk exclusively among bankers, they could offer coverage at roughly half the market rate. Certificates of membership cost $2,000 each—about $62,000 in today's money. Temple, demonstrating the kind of skin-in-the-game leadership that would become a Principal hallmark, purchased the first one.

Within weeks, the fledgling association faced its first operational crisis. The board members, all successful bankers with their own institutions to run, quickly realized they couldn't manage day-to-day operations while maintaining their primary careers. The solution came in the form of John A. Tibbs, hired as the association's first paid employee. Tibbs, a former newspaper editor with a talent for organization and an understanding of actuarial principles, took over daily management from the officers and board members.

Tibbs brought something crucial: professionalism. He instituted proper record-keeping, developed standardized application processes, and began the careful work of actuarial analysis. Under his management, The Bankers Life Association grew from 137 members in its first year to over 1,000 by 1885. The growth wasn't just in numbers—it was geographic. What started as an Iowa association began attracting bankers from Illinois, Nebraska, and Missouri.

The mutual model created a powerful feedback loop. As more bankers joined, the risk pool improved, allowing for lower premiums, which attracted more members. But perhaps more importantly, it created a culture of conservative underwriting and long-term thinking. Since policyholders were also owners, there was no pressure for short-term profits. Every decision was made with the understanding that the people making it would live with the consequences for decades.

By 1890, The Bankers Life Association had accumulated over $50,000 in surplus—a substantial sum that provided security against unexpected claims. The association's annual reports from this period reveal a fascinating glimpse into 19th-century American banking culture. Members weren't just numbers; they were part of a professional fraternity. Death claims were announced with personal details, and the annual meetings functioned as much as social gatherings as business conferences.

The conservative Midwest values that permeated the organization would prove to be its greatest asset. While other insurance companies of the era engaged in speculative investments or aggressive expansion, Bankers Life stuck to government bonds and high-grade municipals. The board's investment philosophy, articulated in an 1895 report, was simple: "We seek not the highest returns, but the surest returns."

This philosophy was tested during the Panic of 1893, when over 500 banks failed nationwide. Bankers Life not only survived but actually grew during this period. Why? Because dying banks meant dying bankers needed insurance more than ever. The association's strong balance sheet allowed it to pay all claims promptly, building a reputation for reliability that money couldn't buy.

By 1900, The Bankers Life Association had evolved from a small mutual aid society into a legitimate financial institution with over 5,000 members and $500,000 in assets. But Temple and the board recognized that to truly serve their members, they needed to expand beyond simple life insurance. Bankers were living longer but facing new risks: disability, retirement, and the care of dependents.

The early 1900s brought a series of innovations. The association introduced disability benefits in 1903, making it one of the first insurers to recognize that career-ending injury could be as devastating as death. They also began experimenting with what would later be called annuities—products that would pay bankers a steady income in retirement.

But perhaps the most important development of this era was cultural. The association developed what employees called "The Bankers Life Way"—a set of principles that emphasized service over sales, relationships over transactions, and long-term value over short-term gain. This wasn't written in some corporate manual; it was lived every day in the Des Moines headquarters, where executives knew every policyholder by name and where claims were processed not by formula but by understanding individual circumstances.

As the 1920s dawned, The Bankers Life Association stood at a crossroads. The organization had grown beyond its founders' wildest dreams, but America itself was changing. The banking industry was consolidating, cities were growing, and the financial needs of Americans were becoming more complex. The question facing the board was no longer whether to expand beyond bankers, but how to do so while maintaining the mutual spirit and conservative values that had brought them success.

The answer would transform not just the company, but the entire American insurance industry. And it started with a simple realization: if bankers needed financial protection, didn't everyone else?

III. Building the Foundation: Growth & Expansion (1920s–1980s)

The year 1909 marked a pivotal transformation. The board, after months of heated debate, voted to change the company's name from The Bankers Life Association to simply Bankers Life Company. It wasn't just semantics—this signaled a fundamental shift in ambition. The company would no longer limit itself to bankers; it would serve all Americans who needed financial protection. The mutual structure remained, but the vision expanded dramatically.

The timing couldn't have been better. America in the 1910s was experiencing profound social changes. The rise of the middle class, urbanization, and industrialization created a vast new market for insurance products. Bankers Life began offering health insurance alongside life insurance, and more importantly, started developing annuity products that would provide income in retirement—a radical concept when most Americans worked until they died.

Then came the Great Depression. On October 29, 1929, as Wall Street crashed and fortunes evaporated, Bankers Life faced its greatest test. Over the next four years, more than 9,000 banks would fail. Insurance companies collapsed by the dozens. Yet Bankers Life not only survived—it thrived. How? The conservative investment philosophy that seemed quaint during the Roaring Twenties proved prescient. While competitors had chased high-yield railroad bonds and speculative real estate, Bankers Life's portfolio consisted primarily of U.S. Treasuries and high-grade municipal bonds.

The Depression years revealed something profound about insurance: in times of crisis, people don't want innovation or excitement from their insurer—they want certainty. Bankers Life paid every claim, never missed a dividend to policyholders, and actually increased its surplus during the worst economic catastrophe in American history. Word spread. By 1935, new policy applications were up 40% from pre-Depression levels.

World War II brought unexpected challenges and opportunities. With millions of American men overseas, the company pivoted to serve women entering the workforce in unprecedented numbers. They developed specialized products for war workers and began what would become a decades-long relationship with the U.S. government, administering life insurance for federal employees.

But the real transformation came in the post-war boom. The GI Bill, suburban expansion, and the rise of corporate America created entirely new insurance needs. In 1946, Bankers Life made a strategic decision that would define its next four decades: it would become the premier provider of group insurance and pension administration for American businesses.

The logic was compelling. Individual life insurance was becoming commoditized, but helping companies provide benefits to their employees required sophisticated expertise. Bankers Life hired actuaries from Yale and Wharton, built one of the first computers in Iowa (a room-sized IBM machine that cost more than the company's entire headquarters), and developed proprietary methods for pension calculation that became industry standards.

By 1960, Bankers Life was administering pension plans for over 500 companies, including Iowa stalwarts like Maytag and Winnebago. But the company's conservatism was becoming a limitation. Competitors were expanding nationally through aggressive acquisition, while Bankers Life remained primarily a Midwest regional player.

Enter David Hurd, who became the company's 11th president in 1975. Hurd was different from his predecessors—Harvard-educated, internationally minded, and convinced that Bankers Life needed to think bigger. Under his leadership, the company made its first international forays, establishing operations in Hong Kong and São Paulo. More importantly, he recognized that the traditional defined benefit pension was dying, replaced by something called defined contribution plans.

Hurd also pioneered something that seemed radical at the time: corporate wellness programs. In 1978, Bankers Life began offering clients not just insurance but health screenings, fitness programs, and preventive care initiatives. The idea was simple but revolutionary—healthier employees meant lower claims, which meant better economics for everyone. It was the kind of long-term thinking that only a mutual company could pursue.

The late 1970s brought another innovation that would prove transformative: the creation of section 401(k) of the Internal Revenue Code. While most insurers ignored this obscure tax provision, a young executive at Bankers Life named Bill Mills saw its potential. Mills argued that 401(k) plans would revolutionize retirement savings, shifting responsibility from employers to employees while creating massive new pools of assets that needed management.

Mills faced internal skepticism. The company had built its reputation on defined benefit pensions—why cannibalize that business? But Mills persisted, and in 1980, Bankers Life launched one of the first 401(k) products in America. The initial response was modest—just 12 companies signed up in the first year. But Mills was playing a longer game.

By 1984, Bankers Life was administering 401(k) plans for over 1,000 companies. The economics were extraordinary: unlike traditional insurance, which required massive reserves and faced mortality risk, 401(k) administration was essentially a fee-based business with recurring revenue and minimal capital requirements. Every pay period, millions of dollars flowed through Bankers Life's systems, generating steady fees while the company helped Americans build retirement security.

The cultural DNA established in those early years—conservative underwriting, long-term thinking, and genuine care for policyholders—remained intact even as the company grew from a regional mutual to a national financial services firm. Employees still talked about "The Bankers Life Way," though now it was being practiced in offices from Portland to Philadelphia.

As the 1980s progressed, it became clear that Bankers Life had outgrown not just its regional roots but its very name. Banking had become just one industry among hundreds that the company served. The insurance products that once defined the company were now just one piece of a comprehensive financial services offering. The company needed a new identity—one that reflected its evolution while honoring its heritage.

The stage was set for the most dramatic transformation in the company's history. After more than a century as Bankers Life, the company would emerge with a new name, new strategy, and new ambitions that would carry it into the 21st century.

IV. Transformation Era: From Bankers Life to Principal (1985–2000)

The boardroom was silent as CEO John Fitzpatrick unveiled the proposed new logo in March 1985. After 106 years as Bankers Life Company, the organization would become Principal Financial Group. The name change had taken two years of deliberation, $3 million in consulting fees, and countless heated debates. Old-timers worried about losing the company's identity. Marketing executives argued the "Bankers Life" name was holding them back. In the end, pragmatism won: the company was no longer primarily serving bankers, no longer just selling life insurance, and no longer content to remain regional.

The rebrand was about more than aesthetics. Principal Financial Group signaled a fundamental strategic shift—from insurance company to comprehensive financial services provider. The timing aligned perfectly with the Reagan-era deregulation that was reshaping American finance. Glass-Steagall was weakening, financial boundaries were blurring, and Principal intended to compete not just with other insurers but with banks, brokerages, and asset managers.

The 401(k) revolution that Bill Mills had championed was now in full swing. By 1986, Principal was adding 100 new 401(k) plans per month. But the real insight came from studying client behavior. Companies that started with Principal for 401(k) administration often needed help with health insurance, disability coverage, and executive compensation. The cross-selling opportunities were enormous.

Principal developed what it called the "full service model"—a single point of contact for all of a company's employee benefit needs. While competitors specialized in one area, Principal could handle everything from retirement plans to dental insurance. The operational complexity was staggering, but the customer stickiness was even more impressive. Once a company integrated Principal into its HR systems, switching costs became prohibitive.

Technology became the critical enabler. In 1988, Principal invested $50 million—an astronomical sum for an Iowa insurance company—in a proprietary benefits administration platform. The system could handle real-time enrollment, claims processing, and investment allocation for millions of participants. Competitors were still using paper forms and mainframe batch processing; Principal was offering same-day service through desktop terminals.

The international expansion that David Hurd had initiated accelerated dramatically. But instead of trying to compete with local insurers in developed markets, Principal focused on emerging economies where pension systems were being privatized. In 1990, they entered Chile just as the country was mandating private retirement accounts. By 1995, Principal was managing retirement funds for over 1 million Chileans.

The Latin American strategy was brilliant in its simplicity. These countries were essentially creating 401(k)-style systems from scratch, and Principal had more experience running such systems than almost anyone. They partnered with local banks for distribution, brought their technology platform, and adapted their products to local regulations. Within a decade, Principal would be operating in Mexico, Brazil, Argentina, and Hong Kong.

Back in the United States, the 1990s brought unprecedented growth in retirement assets. The bull market, baby boomer demographics, and the continued shift from defined benefit to defined contribution plans created a perfect storm of opportunity. Principal's assets under management grew from $20 billion in 1990 to over $80 billion by 1999.

But growth brought challenges. The mutual structure that had served the company so well for over a century was becoming a constraint. Principal needed capital to fund technology investments, acquisitions, and international expansion. Mutual companies could only raise capital through retained earnings—fine for steady growth, but insufficient for the ambitions Principal harbored.

In 1996, the board began quietly exploring demutualization—converting from a mutual company owned by policyholders to a stock corporation owned by shareholders. It was heretical to even discuss. The mutual structure was part of Principal's DNA, the foundation of its customer-first culture. How could they maintain their values as a public company subject to quarterly earnings pressure?

The late 1990s also saw Principal build significant asset management capabilities. Rather than just administering 401(k) plans, they wanted to manage the actual investments. Principal Global Investors was established as a subsidiary, hiring portfolio managers from Fidelity and PIMCO. The focus was on stable value funds, real estate, and fixed income—boring assets that generated steady returns, perfectly aligned with retirement savings needs.

Technology continued to transform the business. In 1998, Principal launched one of the first online 401(k) platforms, allowing participants to check balances, change allocations, and model retirement scenarios from their home computers. It seems quaint now, but at the time, the idea that individuals could manage their retirement accounts without calling a service center was revolutionary.

The international operations were producing unexpected benefits. The company's experience in Chile had taught them how to operate in inflationary environments, manage currency risk, and navigate emerging market regulations. These skills proved valuable when the Asian Financial Crisis hit in 1997. While competitors retreated, Principal actually expanded, acquiring distressed pension assets in Thailand and Malaysia at attractive valuations.

By 2000, Principal Financial Group had transformed from a regional insurance company into a global financial services powerhouse. Revenue had grown from $2 billion to over $7 billion during the decade. The company operated in 15 countries, served over 10 million customers, and managed more than $100 billion in assets. But the biggest transformation was yet to come.

The demutualization discussions that had begun in 1996 were reaching a crescendo. Investment banks were pitching IPO valuations north of $5 billion. The capital markets were hungry for financial services stocks. And Principal's management believed that going public would provide the currency—both literal and figurative—needed to compete in an increasingly consolidated industry.

Yet as the 20th century ended, questions lingered. Could Principal maintain its conservative culture as a public company? Would the pressure for quarterly earnings growth compromise the long-term thinking that had sustained the company for 121 years? And most importantly, was the market ready for an Iowa-based financial services company that had built its reputation on being boring, stable, and reliable?

The answers would come sooner than anyone expected, and in ways no one could have predicted.

V. Going Public: The IPO and New Era (2001–2008)

October 23, 2001. Just forty-two days after September 11th had brought America to its knees, Principal Financial Group rang the opening bell at the New York Stock Exchange. The timing seemed impossibly wrong—markets were jittery, investors were fleeing to safety, and IPOs were being pulled left and right. Yet CEO Barry Griswell stood confidently at the podium, watching as PFG stock opened at $20.50, above its $18.50 offering price.

The decision to proceed with the IPO despite the post-9/11 chaos was vintage Principal—contrarian, carefully considered, and ultimately correct. While other companies delayed their offerings, Principal recognized that investors were actually hungry for stable, boring financial services companies. The IPO raised $1.85 billion, making it one of the largest financial services debuts in history and certainly the most successful IPO in those dark autumn weeks of 2001.

The demutualization process had been extraordinarily complex. Over 200,000 policyholders became shareholders overnight, receiving stock or cash based on their policy values and tenure. Principal had spent $100 million on systems to track eligibility, calculate distributions, and manage the conversion. Every eligible policyholder from the mutual era—from the Iowa farmer with a $10,000 life policy to major corporations with million-dollar pension plans—received their share of the newly public company.

Barry Griswell, who had taken over as CEO in 2000, understood that going public meant playing by new rules. Wall Street wanted growth, margins, and returns on equity. But Griswell, a Principal lifer who started as an agent in 1968, was determined to preserve the company's culture while delivering for shareholders. His solution was elegant: focus relentlessly on retirement services, where Principal's competitive advantages were strongest.

The first major test came quickly. The dot-com crash had devastated 401(k) balances, and participants were angry. Principal's call centers were overwhelmed with complaints about lost retirement savings. Lesser companies might have retreated, but Principal saw opportunity. They launched a massive education campaign, sending advisors to conduct thousands of workplace seminars on retirement planning, dollar-cost averaging, and staying the course during market volatility.

This focus on participant education paid dividends. While competitors lost 401(k) plans as companies switched providers, Principal actually gained market share. Their client retention rate exceeded 95%, astronomical in an industry where 85% was considered excellent. The key was Principal's recognition that they weren't just serving companies—they were serving the employees who depended on those companies' retirement plans.

In 2005, Principal launched what would become one of the most memorable marketing campaigns in financial services history: Eddie. The character—a charismatic spokesman who used the Principal "Edge" to solve problems—was everywhere: Super Bowl commercials, billboards, even a Times Square spectacular. Eddie represented something important: Principal was no longer content to be the boring Iowa insurance company. They wanted to be a household name.

The campaign worked brilliantly. Brand recognition jumped from 12% to over 40% within two years. More importantly, Eddie humanized a company that had always been seen as institutional and impersonal. The ads showed Eddie helping small business owners, young families, and retirees—real people with real financial challenges. It was aspirational but accessible, sophisticated but not condescending.

Behind the marketing splash, Principal was executing a disciplined acquisition strategy. In 2004, they purchased WM Advisors, Washington Mutual's retirement plan business, adding $28 billion in assets and 1,800 plans. In 2006, they acquired portions of CIGNA's retirement business. Each deal was carefully structured to be immediately accretive to earnings while expanding Principal's distribution and scale advantages.

The international business was flourishing beyond expectations. Principal's operations in Mexico and Brazil were generating returns on equity above 20%, far exceeding the U.S. business. The key was their early-mover advantage in pension privatization. As these countries mandated retirement savings, Principal was already there with technology, expertise, and local partnerships.

Technology investments accelerated dramatically. Principal spent over $500 million between 2001 and 2007 upgrading systems, building data centers, and developing digital capabilities. They were one of the first to offer mobile apps for 401(k) participants, automated rebalancing, and real-time chat support. While these seem standard today, Principal was pioneering digital retirement services when most competitors still relied on quarterly paper statements.

The asset management business was quietly becoming a powerhouse. Principal Global Investors' assets under management grew from $100 billion to over $250 billion during this period. The focus remained on conservative strategies—stable value funds, commercial real estate, agricultural investments—that matched the risk profile of retirement savers. They weren't trying to be the next PIMCO; they were content being the best at boring.

By 2007, Principal had delivered six consecutive years of double-digit earnings growth. The stock had tripled from its IPO price. Return on equity exceeded 15%. The company was generating over $1 billion in free cash flow annually. Wall Street analysts, initially skeptical of this Iowa insurer, were becoming believers. Principal had proven that a conservative, retirement-focused strategy could deliver growth.

But storm clouds were gathering. The subprime mortgage crisis was metastasizing into something much larger. Principal's commercial real estate portfolio, while high-quality, was facing pressure. Their stable value funds, which guaranteed principal protection, were seeing redemptions as nervous participants fled to cash. The international operations, so successful in good times, were exposed to emerging market volatility.

As 2008 began, CEO Larry Zimpleman (who had succeeded Griswell in 2008) faced the greatest challenge in Principal's modern history. The financial crisis was about to test every assumption about risk, growth, and stability. Would Principal's conservative culture and strong balance sheet be enough? Or would they, like so many financial institutions, need government assistance to survive?

The answer would define not just Principal's future, but its very identity as a company. The boring Iowa insurer was about to prove that sometimes, boring is exactly what the world needs.

VI. Crisis & Resilience: Navigating 2008 and Beyond (2008–2018)

September 15, 2008, 6:00 AM. Larry Zimpleman's phone rang. Lehman Brothers had just filed for bankruptcy. As Principal's CEO for barely six months, Zimpleman faced an immediate crisis: Principal had $1.2 billion in Lehman exposure through various instruments. But as his team gathered in the Des Moines war room, a different picture emerged. Thanks to conservative underwriting, most of the exposure was secured, senior debt. The actual loss would be less than $100 million—painful, but manageable.

What followed was Principal's finest hour. While AIG needed $182 billion in government bailouts and Hartford Financial sought TARP funds, Principal weathered the storm without taking a penny of taxpayer money. The difference? Principal had never strayed from its core business, never chased subprime mortgages, never leveraged up to juice returns. The boring Iowa insurer looked brilliant as Wall Street titans collapsed around them.

The crisis created extraordinary opportunities for those with capital and courage. As competitors retreated or failed, Principal went shopping. In 2010, they acquired certain retirement business assets from ING for $450 million, adding 5,000 plans and $20 billion in assets. The price was a fraction of what ING had paid to build the business. It was the deal of the decade.

But Principal didn't just buy distressed assets; they reimagined their entire business model. The crisis had exposed a fundamental truth: the traditional insurance model of taking credit risk and earning spread income was broken. The future belonged to fee-based businesses with recurring revenue and minimal balance sheet risk. Principal accelerated its transformation from insurer to asset manager and retirement services provider.

The numbers tell the story. In 2008, spread-based revenue accounted for 45% of Principal's earnings. By 2015, that had dropped to under 25%. Fee revenue from 401(k) administration, asset management, and advisory services had become the growth engine. It was a less volatile, more predictable business model—exactly what investors wanted post-crisis.

Technology became an even bigger differentiator. While competitors struggled with legacy systems, Principal launched a cloud-based platform that could onboard new 401(k) plans in days rather than months. They introduced robo-advisory services for small balance accounts, automated compliance monitoring, and real-time reporting dashboards. The goal was ambitious: make Principal the Amazon of retirement services.

The international strategy evolved significantly. Rather than owning operations outright, Principal began partnering with local institutions through joint ventures. In China, they partnered with China Construction Bank, gaining access to 400 million potential customers without the capital requirements of full ownership. In India, they joined with Punjab National Bank. These partnerships provided distribution while limiting downside risk.

Principal Global Investors emerged from the crisis as a legitimate force in asset management. Their real estate team, which had avoided the subprime mess, was buying distressed commercial properties at 60 cents on the dollar. Their agricultural investment team was pioneering farmland as an institutional asset class. By 2012, they were managing over $300 billion, making them one of the largest managers most people had never heard of.

The cultural transformation was equally important. Principal had always been conservative, but post-crisis, they became evangelical about risk management. Every product, every investment, every decision was stress-tested against multiple scenarios. They built a proprietary risk dashboard that gave senior management real-time visibility into exposures across the enterprise. It wasn't sexy, but it was exactly what regulators and rating agencies wanted to see.

In 2012, Principal made a bold prediction: the next decade would see $10 trillion in assets move from defined benefit pensions to defined contribution plans and IRAs. They positioned the entire company to capture this "Great American Retirement Migration." They built specialized teams to handle pension risk transfers, expanded their rollover IRA capabilities, and developed products specifically for the 10,000 baby boomers retiring every day.

The strategy worked brilliantly. Principal's pension risk transfer business grew from virtually nothing in 2010 to over $5 billion in annual transactions by 2015. They were helping companies like Verizon and General Motors offload pension obligations while ensuring retirees received their benefits. It was complex, capital-intensive work that required deep expertise—exactly the kind of moat Principal loved to build.

Marketing evolved from the Eddie era to something more sophisticated. Principal launched "We're In This Together," a campaign focused on partnership and long-term relationships rather than products. They sponsored financial literacy programs in schools, funded retirement research at MIT and Wharton, and positioned themselves as thought leaders on America's retirement crisis.

The numbers validated the strategy. Principal's stock price grew from a crisis low of $10 in 2009 to over $60 by 2018. Return on equity consistently exceeded 12%. They returned over $5 billion to shareholders through dividends and buybacks during this period. Most impressively, they did this while maintaining capital ratios well above regulatory requirements.

By 2018, Principal had emerged from the financial crisis not just intact but transformed. They were no longer an insurance company that happened to administer retirement plans; they were a retirement company that happened to sell insurance. The distinction mattered. Insurance was cyclical, capital-intensive, and increasingly commoditized. Retirement services offered secular growth, recurring revenue, and competitive advantages that compounded over time.

But the industry was consolidating rapidly. Empower was rolling up smaller players. Fidelity and Vanguard were leveraging their scale to cut prices. New entrants like Betterment were targeting younger savers with digital-first experiences. Principal needed scale, and they needed it fast.

The opportunity would come from an unexpected source: Wells Fargo, reeling from scandals and looking to shed non-core assets, was shopping its institutional retirement business. It was exactly what Principal needed—immediate scale, blue-chip clients, and complementary capabilities. But the price tag would be steep, and integration would be complex.

The stage was set for Principal's biggest bet since going public.

VII. Modern Era: The Wells Fargo Deal & Digital Evolution (2019–Present)

March 26, 2019. Dan Houston sat in his Des Moines corner office, staring at the final terms sheet for what would be Principal's biggest acquisition ever. Wells Fargo, reeling from years of scandals and regulatory pressure, was selling its institutional retirement and trust business. The price: $1.2 billion for a business with 7.5 million customers and $827 billion in assets. Houston had 48 hours to decide whether to pull the trigger on a deal that would double the size of Principal's record-keeping assets.

The strategic logic was compelling. More than two-thirds of Wells Fargo's institutional retirement assets were in midsize employers' plans ranging from $10 million to $1 billion—exactly the market segment where Principal needed scale. The retirement industry was consolidating rapidly. Empower had been rolling up competitors. Fidelity and Vanguard were using their scale to slash fees. Principal needed to get bigger or risk being marginalized.

But the risks were substantial. Principal would finance the purchase with cash and senior debt, stretching the balance sheet. Integration would be complex—2,500 employees across locations in Charlotte, Minneapolis, Waco, the Philippines, and India. Most concerning: would Wells Fargo's reputational problems contaminate Principal's carefully cultivated brand?

Houston made the call. On April 9, 2019, Principal announced the deal. The market loved it—Principal's stock jumped 4% on the news. But the real work was just beginning. The integration proved more complex than anyone anticipated. Principal closed the acquisition on July 1, 2019, with transition and integration scheduled to occur through March 2022. The company structured the transition in five waves, onboarding different client segments based on their unique requirements. Each wave required meticulous planning—converting data, training employees, migrating systems, and most critically, ensuring zero disruption to participants' retirement savings.

COVID-19 hit just as integration was ramping up. Suddenly, Principal had to coordinate 2,500 Wells Fargo employees working from home across multiple countries while managing the largest systems migration in the company's history. Yet the crisis accelerated digital adoption in ways that would have taken years otherwise. The combined organization delivered new capabilities including digital plan onboarding, the patent-pending Principal Complete Pension Solution, and the Principal Milestones financial wellness program.

The numbers validated the strategy. As a result of the acquisition, Principal added 4.3 million eligible participants and approximately $150 billion in account value, while serving more than 10 million eligible participants representing over $537 billion. The combined business created unprecedented scale advantages—better pricing power with asset managers, lower per-participant technology costs, and the ability to serve everyone from small businesses to Fortune 500 companies. But Principal wasn't resting on the Wells Fargo integration. In May 2024, the company announced it would acquire Ascensus's employee stock ownership plan business, adding approximately 800 plans and more than 165,000 participants. Principal Financial Group announced a definitive agreement with Ascensus to acquire its employee stock ownership plan business, adding approximately 800 plans and more than 165,000 participants to its workplace savings and retirement solutions business that ranks as the No. 1 ESOP service provider in the U.S. The deal, completed on July 1, 2024, strengthened Principal's dominance in a niche but growing market where companies use employee ownership as a talent retention and succession planning tool.

The digital evolution accelerated dramatically during this period. Principal launched Principal Real Start, a simplified and highly personalized onboarding experience available in both English and Spanish. They introduced robo-advisory services for small balance accounts, AI-powered customer service, and predictive analytics that could identify participants at risk of reducing their savings rates. The goal was ambitious: use technology to provide institutional-quality advice to every participant, regardless of account balance.

International operations continued to evolve. Principal's joint ventures in Asia and Latin America were generating strong returns, but the company recognized that owning minority stakes limited strategic control. They began selectively buying out partners where it made sense, while exiting markets where they couldn't achieve scale. The focus narrowed to markets with mandatory retirement savings and growing middle classes—Brazil, Mexico, Chile, Malaysia, and Hong Kong.

Principal Global Investors quietly became a powerhouse. Revenue reached US$16.1b (up 18% from FY 2023), with assets under management approaching $500 billion. The focus remained on strategies aligned with retirement savings—stable value funds, target-date funds, real estate, and infrastructure. They weren't trying to compete with hedge funds or high-frequency traders; they were building boring, reliable portfolios for people saving for retirement.

The leadership transition marked a new chapter. Principal Financial Group's Board of Directors appointed president and chief operating officer Deanna Strable as the company's next president and chief executive officer, effective January 7, 2025, succeeding Houston who had served as president and CEO since 2015. Strable, a Principal lifer who joined as an actuarial assistant in 1990, represented continuity with change. She had been instrumental in the Wells Fargo integration and understood both the operational complexities and strategic opportunities facing the company.

Strable's vision was clear: Principal needed to be more than a retirement recordkeeper. The company should be the financial wellness partner for American workers throughout their careers. This meant expanding beyond traditional 401(k) services to offer student loan assistance, emergency savings accounts, financial coaching, and comprehensive retirement income solutions. The goal was to create lifetime relationships with participants, not just administer their employer's retirement plan.

The pandemic had accelerated trends that Principal had been preparing for. Remote work made digital engagement essential. Economic uncertainty made financial wellness programs critical. The Great Resignation showed that retirement benefits were key to talent retention. Principal was positioned perfectly—they had the scale from Wells Fargo, the technology investments from years of development, and the trust built over 145 years.

By 2024, Principal's transformation was complete. The company that started as a mutual insurance association for Iowa bankers had become a global financial services powerhouse managing the retirement security of tens of millions. They had weathered multiple crises without government assistance, executed transformative acquisitions, and built competitive advantages that would be nearly impossible to replicate.

Yet challenges remained. Fee compression continued as passive investment options gained share. New entrants with venture capital backing were targeting younger workers with mobile-first experiences. Regulatory scrutiny on retirement plan fees intensified. The question facing Strable and her team wasn't whether Principal could survive—it was whether they could maintain their leadership position as the industry continued to evolve.

VIII. Business Model Deep Dive: Three Pillars

Retirement and Income Solutions: The Crown Jewel

The numbers tell a remarkable story. Pre-tax operating earnings increased $60.6 million primarily due to higher net revenue. Net revenue increased $75.0 million primarily due to growth in the business and strong revenue retention, higher net investment income, as well as favorable markets. But behind these figures lies a business model that Warren Buffett would admire: recurring revenue, minimal capital requirements, and competitive advantages that compound over time.

Principal's retirement business operates on multiple revenue streams. First, there's recordkeeping fees—typically 5-25 basis points on assets, charged quarterly regardless of market conditions. Second, investment management fees from proprietary funds, averaging 40-60 basis points. Third, ancillary services like participant education, compliance consulting, and plan design advisory that generate additional revenue. The beauty is that these revenue streams are incredibly sticky—Principal's client retention rate exceeds 95%, and average client tenure is over 15 years.

The 401(k) administration business is particularly attractive. Once a company selects Principal as its recordkeeper, switching costs become prohibitive. HR departments must retrain on new systems, employees need education on new platforms, and there's operational risk in moving millions or billions in assets. This creates what Buffett calls a "moat"—a sustainable competitive advantage that protects the business from competition.

Scale economics are extraordinary. Principal's technology platform, which cost billions to build, can onboard a new 100-person plan or a 10,000-person plan with minimal incremental cost. The same systems that process transactions for small businesses handle Fortune 500 companies. This operating leverage means that revenue growth drops almost directly to the bottom line.

The Wells Fargo acquisition supercharged these economics. By adding 4.3 million participants, Principal spread its fixed costs over a much larger base. Technology costs per participant dropped by 30%. Call center efficiency improved as volume justified 24/7 support. Most importantly, Principal gained negotiating leverage with asset managers, reducing fund expenses and improving margins.

Pension risk transfer has emerged as a massive opportunity. As companies seek to offload defined benefit obligations, Principal helps them purchase group annuities that transfer pension responsibilities to insurers. In 2023 alone, Principal executed over $5 billion in pension risk transfers. These transactions generate large upfront fees plus ongoing administration revenue, with minimal ongoing risk since the liabilities are immediately reinsured.

The retirement income challenge presents Principal's biggest growth opportunity. As 10,000 baby boomers retire daily, they need solutions to convert savings into sustainable income. Principal has developed innovative products like contingent deferred annuities, managed payout funds, and dynamic withdrawal strategies. These products generate higher margins than accumulation products and create even stickier client relationships.

Principal Asset Management: The Hidden Giant

Combined net revenue (at PFG share) increased $33.7 million primarily due to higher assets under management Principal Global Investors manages nearly $500 billion, making it one of the largest asset managers most people have never heard of. The business focuses on institutional clients and specialized strategies where Principal has genuine expertise.

Real estate is the crown jewel of the asset management business. Principal owns and manages over $100 billion in commercial real estate across office, retail, industrial, and multifamily properties. Unlike REITs that must distribute 90% of income, Principal can reinvest proceeds, compound returns, and generate fee income from third-party investors. The vertical integration—from acquisition to property management to disposition—creates margins that pure-play managers can't match.

The agricultural investment strategy showcases Principal's differentiated approach. They own farmland across the Midwest, Australia, and Brazil, generating returns from crop revenue, land appreciation, and sustainability initiatives like carbon credits. It's a perfect match for pension funds seeking inflation protection and uncorrelated returns. Principal charges 100-150 basis points in management fees plus performance fees above hurdle rates.

Fixed income management leverages Principal's insurance heritage. Managing insurance general accounts for over a century has created deep expertise in credit analysis, duration matching, and yield optimization. Principal manages over $200 billion in fixed income, focusing on investment-grade corporate bonds, commercial mortgages, and private placements. The strategy isn't sexy, but it generates consistent fee income with minimal volatility.

The boutique model drives growth. Rather than trying to be everything to everyone, Principal operates specialized investment teams with distinct strategies. Each boutique has its own investment process, compensation structure, and brand identity, but shares Principal's distribution, operations, and compliance infrastructure. This model attracts talented portfolio managers who want entrepreneurial freedom with institutional support.

International asset management offers significant growth potential. Principal's joint ventures in emerging markets provide local expertise and distribution while Principal brings investment capabilities and global best practices. The economics are attractive—Principal typically owns 40-50% of these ventures but receives management fees on 100% of assets.

Benefits and Protection: The Synergy Engine

The benefits and protection segment might seem like the orphan child compared to retirement and asset management, but it's the glue that holds Principal's ecosystem together. Pre-tax operating earnings increased $20.2 million due to growth in the business and lower incurred loss ratio. Premium and fees increased $59.2 million driven by record sales along with employment and wage growth.

Group benefits—dental, disability, life insurance—create multiple touchpoints with employers. A company might start with Principal for group life insurance, add disability coverage, then select Principal for 401(k) administration because of the existing relationship. The cross-selling opportunity is enormous: clients who use Principal for multiple products have retention rates above 98%.

The specialty benefits division focuses on niche markets with less competition. Principal is a leading provider of dental insurance in rural markets, disability coverage for white-collar professionals, and voluntary benefits for small businesses. These markets might be small individually, but collectively they generate billions in premiums with attractive margins.

Individual life insurance might seem anachronistic in the digital age, but Principal has found profitable niches. They focus on business owners needing key person insurance, high-net-worth individuals seeking estate planning solutions, and executives wanting supplemental coverage. These customers value advice over price, generating margins that mass-market insurers can't achieve.

The integration between benefits and retirement creates unique advantages. Principal can offer "total rewards" statements showing employees their complete compensation package. They can coordinate benefits enrollment with 401(k) elections. They can use health data (appropriately anonymized) to design wellness programs that reduce both medical costs and retirement plan leakage.

Underwriting excellence drives profitability. Principal's actuarial expertise, built over 145 years, allows them to price risk more accurately than competitors. They use predictive analytics to identify risks before they become claims. Their claims management focuses on returning people to work rather than just paying benefits, reducing long-term costs.

The capital-light transformation continues. Principal has shifted from traditional insurance products that require significant reserves to fee-based administrative services. They might administer a company's self-funded dental plan, earning fees without taking risk. This model generates returns on equity above 20% compared to low teens for traditional insurance.

Technology investments are paying dividends. Digital enrollment platforms reduce administrative costs by 40%. Automated underwriting approves 70% of applications instantly. Mobile apps allow employees to file claims in minutes rather than weeks. These improvements reduce costs while improving customer satisfaction—a rare win-win.

The benefits business also serves as an early warning system. Rising disability claims might signal economic stress before it shows up in 401(k) withdrawals. Increasing life insurance purchases could indicate demographic shifts. This information helps Principal anticipate trends and adjust strategies across all business lines.

IX. Playbook: Business & Investing Lessons

The Power of Focus: Retirement as the North Star

Principal's success stems from a seemingly simple decision: focus relentlessly on retirement. While competitors diversified into investment banking (and blew up in 2008) or chased high-net-worth wealth management (with mixed results), Principal stayed boring. They recognized that retirement savings represents one of the largest pools of assets in the world—$38 trillion in the U.S. alone—and positioned themselves as the plumbing that makes it work.

This focus created compound advantages. Every product decision, every acquisition, every technology investment was evaluated through the retirement lens. Does it help people save for retirement? Does it help employers offer better retirement benefits? Does it strengthen our retirement ecosystem? This discipline prevented Principal from chasing shiny objects that destroyed value at other financial firms.

Building a Moat Through Distribution and Relationships

Principal's 40,000+ plan sponsor relationships represent a moat that's nearly impossible to replicate. These aren't transactional relationships—they're partnerships built over decades. Principal knows the CFO's name, understands the company's benefits philosophy, and has proven reliable through multiple economic cycles. A startup with better technology or lower fees can't replicate this trust.

The advisor channel amplifies this moat. Principal works with over 25,000 financial advisors who recommend their products. These advisors value Principal's consultative approach, educational resources, and consistent service. While direct-to-consumer models grab headlines, the reality is that most retirement plans are sold through advisors who value relationships over technology.

Capital Allocation Excellence: The Unsung Hero

Returned $1.3 billion of capital to shareholders for full year 2023 Principal's capital allocation framework is a masterclass in financial discipline. They maintain a target capital ratio of 400-450% (RBC ratio), returning excess capital to shareholders while keeping a buffer for opportunities and stress scenarios.

The acquisition strategy is particularly disciplined. Principal doesn't chase transformative deals or enter new markets through acquisition. Instead, they buy complementary businesses at reasonable prices, integrate them methodically, and achieve targeted synergies. The Wells Fargo deal—at roughly 8x EBITDA—looks brilliant compared to the 15-20x multiples competitors have paid.

Share repurchases are executed countercyclically. Principal bought back stock aggressively during the 2009 crisis, the 2020 pandemic selloff, and whenever the stock traded below intrinsic value. This patient approach has reduced share count by 35% since the IPO, dramatically increasing per-share value for remaining shareholders.

The Integrated Model: 1+1=3

Principal's three business segments aren't just co-located—they're genuinely integrated in ways that create competitive advantages. A client's 401(k) plan might use Principal's recordkeeping (Retirement), invest in Principal funds (Asset Management), and offer Principal life insurance (Benefits). This integration creates switching costs, improves economics, and provides better customer outcomes.

Data integration is the hidden advantage. Principal knows more about their clients than almost any financial institution. They know salary progressions, savings rates, health claims, and life events. This data, properly anonymized and analyzed, helps Principal design better products, price risk more accurately, and identify cross-selling opportunities that actually benefit clients.

Managing Through Cycles: The Iowa Advantage

Being headquartered in Des Moines isn't a bug—it's a feature. The Midwest culture of conservatism, long-term thinking, and relationship focus permeates Principal. They didn't get caught up in subprime mortgages because Iowa farmers don't speculate on housing. They didn't need a government bailout because they never levered up chasing returns.

This conservative culture shows up in the numbers. Principal maintains capital ratios well above regulatory requirements. They hedge interest rate risk religiously. They stress-test every product against multiple scenarios. It's boring, but it's also why Principal has survived for 145 years while flashier competitors have disappeared.

Technology as Enabler, Not Disruptor

Principal views technology as a tool to strengthen their existing advantages, not replace their business model. Their $500 million annual technology spend focuses on making human advisors more effective, not replacing them. Digital tools help participants make better decisions, not just reduce call center costs. This pragmatic approach has allowed Principal to modernize without losing what makes them special.

The build-versus-buy decisions are instructive. Principal builds core recordkeeping systems that are strategic differentiators. They buy commodity technologies like cloud infrastructure. They partner on emerging capabilities like AI where they lack expertise. This balanced approach maximizes return on technology investment while minimizing execution risk.

International Expansion: Patience and Discipline

Principal's international strategy offers lessons in patience. Rather than planting flags globally, they focus on markets with three characteristics: mandatory retirement savings, growing middle class, and regulatory stability. They enter through joint ventures to learn the market, then increase ownership as they gain expertise. This measured approach has created profitable businesses in Latin America and Asia while competitors have retreated after expensive failures.

Corporate Culture as Competitive Advantage

Principal's culture—boring, stable, trustworthy—is perfectly aligned with their business. Retirement planning is a 40-year relationship, not a transaction. Clients want a provider who will be there for decades, not the latest fintech startup. Principal's 3% employee turnover rate (versus 15% industry average) means clients work with the same team year after year, building trust that technology can't replicate.

The mutual heritage still influences decision-making. Despite being public since 2001, Principal maintains a long-term orientation. They'll sacrifice quarterly earnings to do right by clients. They'll invest in capabilities that won't pay off for years. They'll maintain conservative underwriting even when competitors loosen standards. This cultural DNA is impossible for competitors to copy.

The Importance of Pricing Power

Principal has pricing power that most financial services companies envy. They've raised recordkeeping fees modestly but consistently, even as passive investment fees have collapsed. How? By bundling services, adding value, and making themselves indispensable. Clients pay for the relationship, expertise, and reliability, not just the commodity service.

X. Analysis & Bear vs. Bull Case

Bull Case: Riding the Demographic Tsunami

The retirement crisis is Principal's opportunity of a lifetime. Consider the numbers: 10,000 Americans turn 65 every day through 2030. The average 401(k) balance for near-retirees is just $289,000—nowhere near enough for a 30-year retirement. Social Security faces insolvency by 2034. The retirement savings gap—the difference between what people have and what they need—exceeds $4 trillion. Principal is positioned to benefit from every dollar that flows into solving this crisis.

The business model improvements are even more compelling. Revenue: US$16.1b (up 18% from FY 2023) demonstrates accelerating growth despite a mature market position. More importantly, the mix shift toward fee-based revenue reduces volatility and improves returns on equity. As spread-based products become a smaller percentage of earnings, Principal becomes more like an asset-light financial technology company than a capital-intensive insurer.

Market consolidation creates extraordinary opportunities. The retirement industry remains fragmented despite recent mergers. Principal could acquire smaller recordkeepers at attractive multiples, immediately achieving cost synergies through platform consolidation. Every acquisition strengthens their scale advantages and makes them harder to displace.

The numbers validate the bull thesis. EPS: US$6.77 (up from US$2.58 in FY 2023) represents 162% earnings growth, though this includes some one-time items. Even normalizing for unusual items, the earnings trajectory is impressive. Returns on equity consistently exceed 12%, well above the cost of capital, indicating value creation.

International expansion remains in early innings. Principal's joint ventures in Latin America and Asia serve growing middle-class populations just beginning to save for retirement. As these markets mature and Principal increases ownership stakes, international could grow from 15% to 30% of earnings over the next decade.

Technology investments are finally paying off. After years of heavy spending, Principal's digital platforms are driving efficiency gains and improved customer acquisition. Cost-per-participant has declined 20% over three years while satisfaction scores have increased. This operating leverage should continue as fixed technology costs are spread over a growing participant base.

Bear Case: Structural Headwinds and Disruption Risks

The fee compression story isn't going away. Vanguard and Fidelity continue to cut prices, using retirement plans as loss leaders to gather assets for their profitable retail businesses. Principal can't match their scale or accept their margins. While Principal has maintained pricing so far, a major client loss to a low-cost competitor could trigger a broader repricing across the industry.

Interest rate sensitivity remains a critical risk. Principal's spread-based products—annuities, life insurance, stable value funds—generate significant earnings from the difference between what they earn on investments and what they credit to policyholders. In a sustained low-rate environment, these spreads compress. Rising rates help, but the Federal Reserve's actions remain unpredictable.

Technology disruption is accelerating. Companies like Guideline, Human Interest, and Vestwell have raised hundreds of millions in venture capital to rebuild retirement administration from scratch. They offer modern interfaces, instant onboarding, and dramatically lower costs. While they currently focus on small plans, they're moving upmarket quickly. Principal's legacy systems, despite upgrades, may struggle to compete.

Regulatory pressures continue mounting. The Department of Labor's fiduciary rule, while currently stalled, could return in a different form. State-mandated retirement programs like CalSavers compete directly with private providers. Fee disclosure requirements make it easier for clients to comparison shop. Each regulatory change increases compliance costs and potentially reduces revenue.

Market volatility impacts multiple revenue streams. A significant market decline would reduce assets under management, cutting fee revenue. It would also increase benefit claims as stressed workers tap retirement savings. Principal weathered 2008 without government assistance, but another crisis could test their capital position.

Competition from unexpected sources is intensifying. Amazon is exploring financial services. PayPal and Square are adding retirement features. Even crypto platforms are pitching "DeFi retirement" solutions. While these seem far-fetched today, Principal seemed far-fetched to established insurers in 1985.

Competitive Benchmarking: Principal vs. The Field

Against Prudential, Principal looks attractive. Prudential has more international exposure but also more volatile earnings from its annuity business. Principal's focus on group retirement gives it more stable, fee-based revenue. Prudential trades at 8x earnings versus Principal at 10x, but Principal's higher quality earnings justify the premium.

MetLife has largely exited the retirement business, focusing on group benefits and international operations. This retreat validates Principal's strategy but also means MetLife isn't a direct competitor. MetLife's higher capital ratios provide more financial flexibility, but Principal's focused strategy generates superior returns on equity.

Voya is Principal's most direct competitor, with similar retirement and benefits businesses. Voya trades at a discount to Principal (7x earnings), reflecting execution challenges and market share losses. Principal's superior scale, technology platform, and track record justify its premium valuation.

Empower (owned by Great-West Life) has been the most aggressive acquirer, rolling up MassMutual's retirement business, Putnam's recordkeeping, and Personal Capital. Empower now rivals Principal in participant count but lacks Principal's asset management capabilities and benefits integration. The private ownership structure makes direct comparison difficult, but industry sources suggest Empower's margins lag Principal's.

The Sustainability Question

ESG considerations increasingly influence Principal's strategy. They've committed to net-zero emissions by 2050, integrated climate risk into underwriting, and launched sustainable investment options. This isn't just virtue signaling—institutional clients increasingly mandate ESG integration, and Principal needs to meet these requirements to win mandates.

The social dimension might be Principal's strongest ESG argument. They're literally helping solve America's retirement crisis. Their financial wellness programs help millions of workers prepare for retirement. Their disability insurance helps people stay productive. In an era where companies need purpose beyond profits, Principal's mission resonates.

Governance remains solid if unspectacular. The board includes relevant expertise, executive compensation aligns with long-term value creation, and risk management proved robust through multiple crises. The CEO transition from Houston to Strable was handled smoothly, demonstrating succession planning strength.

Valuation and Market Position

At current levels, Principal trades at approximately 10x forward earnings, 1.2x book value, and yields about 3.5%. These multiples are reasonable for a financial services company but don't scream either deep value or expensive growth. The market seems to be pricing Principal as a steady, boring financial utility—which might be exactly right.

The capital return story remains compelling. With excess capital above target ratios and limited need for growth investment, Principal should continue returning $1.5+ billion annually to shareholders through dividends and buybacks. At current valuations, this represents an 8-10% annual return even without earnings growth.

XI. Epilogue & "If We Were CEOs"

Standing in Principal's Des Moines headquarters, looking out at the Iowa cornfields that stretch to the horizon, you can't help but think about the journey from that small office in 1879 to today's global financial services powerhouse. The company that Edward Temple and Simon Casady founded with $1,500 has grown to serve 70 million customers with nearly $500 billion under management. But the real question isn't how Principal got here—it's where they go next.

If we were sitting in Deanna Strable's chair, the path forward would require both defending the castle and building new wings. The retirement crisis isn't just an opportunity; it's an obligation. Principal sits at the intersection of one of society's greatest challenges and one of business's greatest opportunities. The company that helps America solve its retirement crisis will generate enormous value for all stakeholders.

Technology Investments: The Digital Imperative

First priority: accelerate the digital transformation. Not the buzzword kind, but real, fundamental reimagination of how retirement services are delivered. Principal needs to build or acquire a mobile-first platform that makes saving for retirement as easy as ordering from Amazon. This means spending $2+ billion over the next five years—painful for a company that thinks in basis points, but essential for survival.

The focus should be on three areas: participant engagement, advisor enablement, and operational automation. On engagement, Principal needs to meet younger workers where they are—TikTok, Instagram, gaming platforms. Financial education through 60-second videos might seem antithetical to Principal's culture, but that's how Gen Z learns. On advisor enablement, give advisors AI-powered tools that make them seem superhuman—instant plan benchmarking, real-time optimization suggestions, predictive analytics on participant behavior. On automation, eliminate every manual process that doesn't add value—use machine learning for claims processing, blockchain for record-keeping, and natural language processing for customer service.

International Strategy: Focus and Depth

The international strategy needs refinement. Principal is subscale in too many markets. The solution: double down on Latin America where they have genuine advantages, exit Asia except for joint ventures that generate fee income without capital requirements, and explore selective acquisition opportunities in English-speaking markets like Australia and the UK where their retirement expertise translates.

Brazil and Mexico should be the focus. These markets have growing middle classes, mandated retirement savings, and cultural appreciation for long-term relationships. Principal should buy out joint venture partners where possible, achieving full control and earnings consolidation. The target: international growing from 15% to 25% of earnings by 2030.

M&A Possibilities: Consolidator or Consolidated?

The retirement industry will continue consolidating, and Principal needs to decide: buyer or seller? As an independent company, Principal could acquire subscale competitors at attractive multiples, immediately achieving synergies through platform consolidation. Targets like Alerus, CAPTRUST, or OneAmerica could add scale without integration complexity.

But there's another possibility: Principal itself could be acquired. At a 30% premium to current prices, Principal would be worth $25+ billion—affordable for companies like BlackRock, Brookfield, or even a large bank looking to enter retirement services. The synergies would be enormous, but the cultural fit would be challenging. Des Moines doesn't naturally merge with Manhattan.

Our preference: remain independent but aggressive. Principal should use its strong balance sheet and stable cash flows to consolidate the fragmented middle market. Buy the 50th through 20th largest recordkeepers, integrate them onto Principal's platform, and achieve unassailable scale advantages.

ESG and Sustainable Investing: From Compliance to Competitive Advantage

The ESG opportunity is misunderstood. This isn't about virtue signaling; it's about product development. Principal should launch a comprehensive suite of sustainable retirement options—fossil-free target-date funds, impact investing strategies, ESG-screened stable value funds. These products command premium pricing and attract sticky assets from institutional clients with mandates.

More ambitiously, Principal should become the leader in "retirement security as a human right." Partner with governments on public-private retirement solutions. Work with unions on multi-employer plans. Collaborate with nonprofits on financial inclusion. This positions Principal as a purpose-driven company that happens to be profitable, rather than a profit-driven company trying to have purpose.

The Future of Workplace Benefits: Total Financial Wellness

The traditional boundaries between retirement, health, and financial wellness are dissolving. Principal should accelerate this convergence. Imagine a single platform where employees manage their 401(k), health savings account, student loans, emergency savings, and insurance benefits. Principal has pieces of this puzzle; they need to assemble the complete picture.

This requires partnerships or acquisitions. Buy a student loan refinancing platform. Partner with a neo-bank for emergency savings accounts. Acquire a financial wellness app. The goal: become employees' complete financial partner from their first job through retirement.

Key Lessons for Founders and Investors

Principal's 145-year journey offers timeless lessons. First, focus beats diversification. Principal succeeded by doing one thing—retirement—extraordinarily well, while competitors who tried to be financial supermarkets struggled. Second, culture is strategy. Principal's Midwest conservatism seemed like a weakness during go-go years but proved to be their salvation during crises.

Third, boring businesses can be beautiful. Retirement administration lacks the excitement of investment banking or the sophistication of hedge funds, but it generates predictable cash flows, enjoys high barriers to entry, and serves a social purpose. Fourth, patience pays. Principal spent decades building capabilities, relationships, and trust that competitors can't replicate with technology or capital.

Finally, the best time to invest is when no one's paying attention. Principal went public six weeks after 9/11, acquired Wells Fargo's business when banks were in retreat, and continued investing through COVID. These contrarian moves, executed when others were fearful, created enormous value.

The Ultimate Question

As we look ahead, the fundamental question isn't whether Principal will survive—they've proven remarkably resilient through multiple crises. The question is whether they can maintain their leadership position as the industry transforms. Can a 145-year-old Iowa insurance company compete with Silicon Valley startups? Can a culture built on relationships thrive in an algorithmic world? Can a company designed for stability adapt to exponential change?

The answer, paradoxically, might be that Principal's perceived weaknesses are actually strengths. In a world of instant everything, long-term relationships become more valuable. In a world of algorithmic trading, human judgment becomes differentiating. In a world of financial engineering, simple products that work become revolutionary.

Principal Financial Group's next chapter won't be written in Silicon Valley or Wall Street. It will be written in Des Moines, by people who understand that helping Americans retire with dignity isn't just a business—it's a calling. And in that sense, Principal's greatest days might still be ahead.

The boring Iowa insurance company might just be the most interesting financial services story of the next decade. Not because they'll disrupt the industry, but because they'll do what they've always done: quietly, competently, and profitably serve the financial needs of middle America. In a world obsessed with disruption, there's something profoundly valuable about dependability.

After all, retirement isn't a sprint—it's a marathon. And Principal has been training for this race for 145 years.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube