PepsiCo: From Brad's Drink to Global Snack & Beverage Empire

I. Introduction & Episode Roadmap

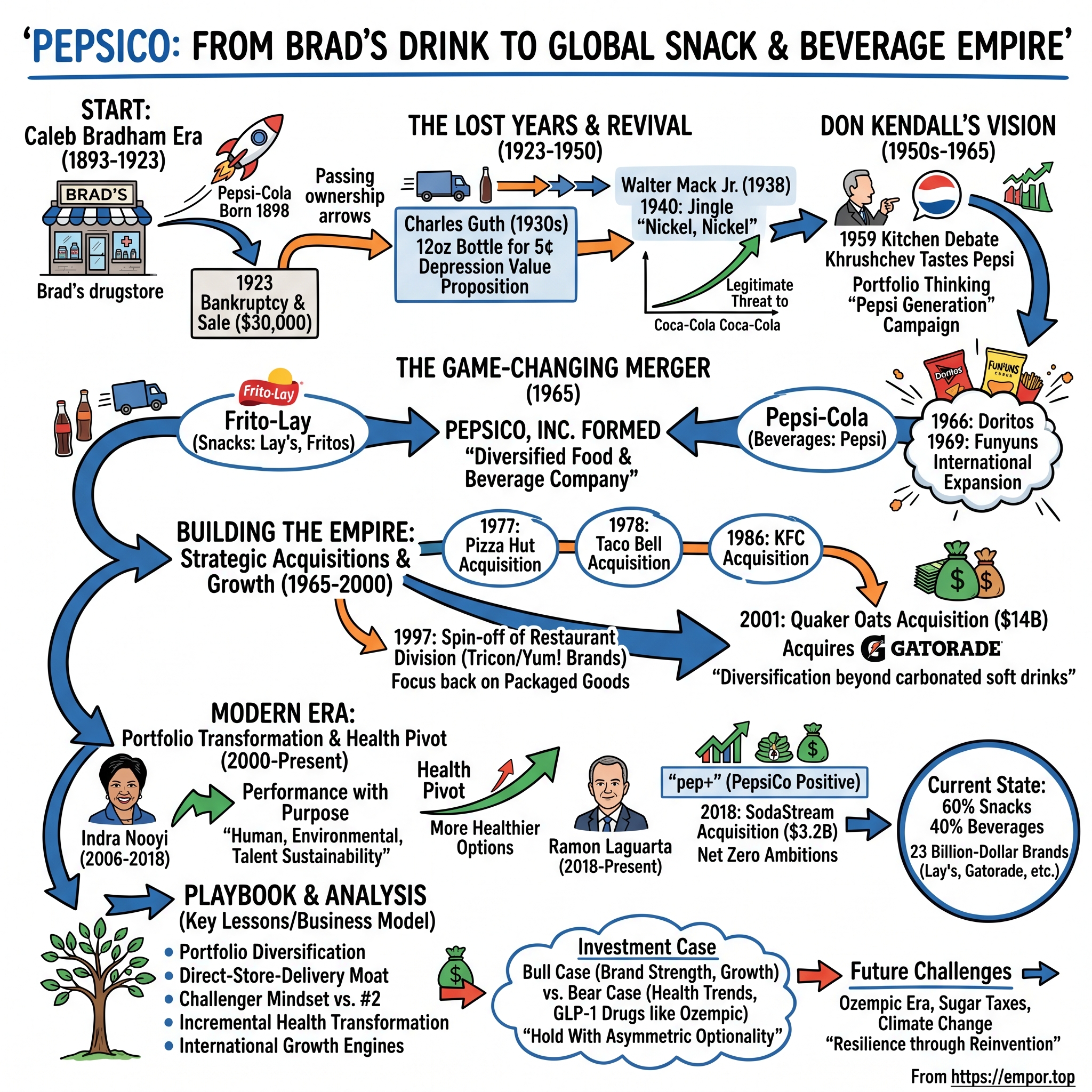

Picture this: A North Carolina pharmacist in 1898, mixing kola nuts and vanilla in the back of his drugstore, trying to create the perfect digestive aid. Fast forward to 2024, and that experimental tonic has morphed into a $91.85 billion behemoth that feeds and hydrates billions across the planet. This is the story of PepsiCo—a company that survived bankruptcy, transcended its original product category, and built one of the most valuable brand portfolios in consumer goods history.

The central question isn't just how Pepsi became Coca-Cola's eternal rival in the cola wars. It's how a company that nearly disappeared in 1923 transformed itself into something far more ambitious: the world's largest snack food company that also happens to sell beverages. While Coca-Cola remained laser-focused on drinks, PepsiCo zigged, building an empire that spans from Doritos to Gatorade, from Quaker Oats to Tropicana.

This journey takes us through multiple near-death experiences, bold merger decisions sketched on napkins, and strategic pivots that redefined what a beverage company could become. We'll explore how PepsiCo turned the disadvantage of being number two in cola into an innovation engine, why they bought Pizza Hut and KFC only to sell them later, and how a company built on sugar is navigating an Ozempic-fueled health revolution.

The themes that emerge are striking: strategic diversification as survival mechanism, the power of distribution networks as competitive moats, and the art of building brands that transcend generations. From Caleb Bradham's $30,000 bankruptcy sale to today's $211 billion market capitalization, this is a masterclass in corporate resilience through reinvention.

II. The Caleb Bradham Era: Birth of Pepsi-Cola (1893–1923)

The summer heat in New Bern, North Carolina, could be oppressive in the 1890s. Without air conditioning, locals sought refuge wherever they could find it—often at the marble-topped soda fountain of Bradham's Drug Company, where the proprietor had a reputation for mixing unusually refreshing drinks. Caleb Davis Bradham, born May 27, 1867, in the small town of Chinquapin, wasn't supposed to be there. He was supposed to be a doctor.

Bradham's path had been carefully laid out: University of North Carolina at Chapel Hill for his undergraduate degree, then on to the University of Maryland's medical school. But life rarely follows neat plans. When his father's business collapsed during the financial panic of 1893, young Caleb was forced to abandon his medical studies and return home. Instead of treating patients, he found himself behind a pharmacy counter, mixing prescriptions and, increasingly, experimenting with fountain drinks.

The late 1890s were the golden age of American soda fountains. Every pharmacy had one, and pharmacists competed to create signature beverages that would draw customers. Bradham had a particular talent for it. His friends started calling his most popular creation "Brad's Drink"—a mix of sugar, water, caramel, lemon oil, nutmeg, and other natural additives. But Bradham had bigger ambitions than being known for a local fountain favorite.

In 1898, he made a decision that would echo through history: he renamed his drink "Pepsi-Cola." The name was brilliant marketing—"Pepsi" from dyspepsia (indigestion), suggesting medicinal benefits, and "Cola" from the kola nut, giving it legitimacy alongside the already-successful Coca-Cola. While Coca-Cola had launched twelve years earlier in Atlanta, Bradham saw opportunity, not intimidation. The market was vast enough for multiple players, and his drink had a distinctly different, sweeter profile.

On December 24, 1902—Christmas Eve—the Pepsi-Cola Company was officially incorporated in North Carolina. Six months later, on June 16, 1903, Bradham secured his first trademark. The timing was perfect. America was urbanizing rapidly, temperance movements were making alcohol less socially acceptable, and carbonated soft drinks were becoming the beverage of choice for a modernizing nation.

By 1905, Bradham made a crucial strategic decision: he began selling Pepsi in six-ounce bottles and awarded his first two franchises. This franchise model—where local bottlers would produce and distribute Pepsi using Bradham's syrup—would become the backbone of the soft drink industry. Within five years, he had built a network of 300 bottlers across 24 states. The first Pepsi-Cola Bottlers Convention in New Bern drew operators from across the country, all eager to capitalize on America's growing thirst for carbonated beverages.

Then came World War I, and with it, disaster. Sugar prices had been relatively stable at around 3 cents per pound before the war. But wartime rationing and speculation drove prices skyward—reaching an astronomical 28 cents per pound by 1920. Bradham, believing prices would remain high, purchased massive quantities of sugar at inflated prices, essentially betting the company's future on a commodity play.

He was catastrophically wrong. When sugar prices crashed in 1921, Bradham was left holding inventory worth a fraction of what he'd paid. The company hemorrhaged money. Bottlers canceled orders. By 1923, the man who had built one of America's most promising beverage brands was forced to declare bankruptcy. The entire Pepsi-Cola Company—trademark, formula, and all remaining assets—was sold to Craven Holding Corporation for just $30,000.

Consider that number for a moment: $30,000. Adjusted for inflation, that's roughly $500,000 today. For context, a single McDonald's franchise today costs more than that. The entire Pepsi brand, which would one day be worth tens of billions, changed hands for less than the price of a modest house. Bradham returned to his drugstore, where he would spend his remaining years as a small-town pharmacist, watching from afar as others tried to revive his creation.

III. The Lost Years & Revival (1923–1950)

After the bankruptcy auction, Pepsi-Cola entered what employees would later call "the wilderness years." The brand passed through multiple hands like a cursed heirloom—each new owner convinced they could revive it, each failing in turn. Meanwhile, Coca-Cola was conquering the world, its distinctive bottle shape becoming as recognizable as the American flag.

Caleb Bradham watched it all from his pharmacy in New Bern. Former employees would occasionally stop by, updating him on the latest ownership change, the latest failed revival attempt. On February 19, 1934, at age 66, Bradham died—never seeing his creation's eventual triumph. Local obituaries noted his contributions to the community as a pharmacist. Few mentioned that he had created one of America's most famous brands.

But even as Bradham passed away, Pepsi was finding its savior in the most unlikely of places: a candy store in Long Island. Charles Guth, president of Loft Inc. candy stores, had been buying Coca-Cola syrup for his soda fountains. When Coca-Cola refused to give him a discount for bulk purchases, Guth did what any rational businessman would do—he bought Pepsi out of bankruptcy court and switched all his fountains to his own brand. Guth's genius wasn't in the formula—though he did have Loft's chemists reformulate it to his taste. It was in understanding Depression-era psychology. During the Great Depression, Pepsi gained popularity following the introduction in 1934 of a 12-ounce bottle. Prior to that, Pepsi and Coca-Cola sold their drinks in 6.5-ounce servings for about $0.05 a bottle. But here's where Guth made history: In late 1933, he dropped the price of the large 12-ounce bottle to the same nickel that others charged for 6 ounces. That one decision changed everything: Pepsi-Cola sales skyrocketed.

Think about that value proposition: twice as much for the same price. In a country where millions were unemployed and every penny counted, Pepsi wasn't just selling cola—it was selling dignity. You could give your family more, even when you had less. From 1936 to 1938, Pepsi-Cola's profits doubled. By 1936, his company was making two million dollars of profit and had become the second largest soda company. That year alone, 500 million bottles of the cola were consumed.

But success bred conflict. Pepsi's success under Charles Guth came while the Loft Candy business was faltering. Since he had initially used Loft's finances and facilities to establish the new Pepsi success, the near-bankrupt Loft Company sued Guth for possession of the Pepsi-Cola company. A long legal battle, Guth v. Loft, then ensued, with the case reaching the Delaware Supreme Court and ultimately ending in a loss for Guth.

Enter Walter Mack Jr., a Wall Street veteran who took over Pepsi in 1938. Where Guth had been a tactician, Mack was a showman. He understood that Pepsi needed more than a price advantage—it needed a personality. "Nickel, Nickel," the first advertising jingle ever broadcast nationwide on radio in 1940, with its infectious lyrics: "Pepsi-Cola hits the spot / Twelve full ounces, that's a lot / Twice as much for a nickel, too / Pepsi-Cola is the drink for you."

The jingle became a cultural phenomenon. It was translated into 55 languages, hummed by children, and even played at baseball games. Mack had turned Pepsi from a bargain brand into a movement. By the end of World War II, Pepsi had achieved something unthinkable just two decades earlier: it had become a legitimate threat to Coca-Cola's dominance.

IV. Don Kendall's Vision: The Transformation Years (1950s–1965)

The scene: Moscow, July 24, 1959. The Cold War is at its peak. Inside the American National Exhibition, Vice President Richard Nixon and Soviet Premier Nikita Khrushchev are engaged in what history would call the "Kitchen Debate"—a heated argument about capitalism versus communism, played out in front of a model American kitchen. As the exchange grows tense, Nixon steers Khrushchev toward a Pepsi booth, where a nervous executive named Donald Kendall stands ready with two paper cups.

"I'd like you to try them both, Premier Khrushchev, and tell me which one tastes better," Kendall said—one bubbling with Pepsi bottled in Manhattan, the other in Moscow. After a few cautious sips, Khrushchev naturally proclaimed the Soviet version superior, declaring it "very refreshing!" The cameras clicked. The photo went global. And Donald Kendall's career trajectory changed forever.

Kendall had approached Nixon the night before at the embassy: "I told him I was in a lot of trouble at home because people thought I was wasting Pepsi's money coming to a Communist country." His bosses at Pepsi thought the whole Soviet exhibition was folly. Coca-Cola had declined to participate. But Kendall saw something others didn't: a market of 200 million thirsty consumers behind the Iron Curtain.

Donald Kendall had risen fast—from bottling plant rookie to executive. Born on a dairy farm in Washington state in 1921, he'd flown Navy seaplanes in World War II, earning three Air Medals and a Distinguished Flying Cross. After the war, he joined Pepsi as a fountain syrup salesman and climbed the ranks with relentless ambition. By 1957, he was running international operations. By 1963, he was CEO.

Kendall's vision extended far beyond cola. He understood that Pepsi's future lay not in beating Coca-Cola at its own game but in changing the game entirely. While Coke focused on perfecting its single product globally, Kendall was thinking portfolio. He launched the "Pepsi Generation" campaign in 1963, positioning Pepsi not as a drink but as a lifestyle choice for the young and young-at-heart. This wasn't just marketing—it was cultural engineering. Pepsi became the cola of youth, of rebellion, of choosing different.

But Kendall's masterstroke came in the boardroom, not the advertising agency. He'd been watching Herman Lay build Frito-Lay into the nation's dominant snack food company through the 1961 merger of the Frito Company and H.W. Lay & Company. Lay had started with a potato chip route in Nashville in 1932 and built it into an empire. Meanwhile, Kendall was running a beverage company with incredible distribution but limited product diversity. The legend goes that in 1965, Herman Lay sketched out a business deal on the back of a napkin while talking to then Pepsi-Cola CEO Don Kendall. What emerged from that napkin wasn't just a merger—it was a reimagining of what a beverage company could be. By 1963, Kendall had become Pepsi's chief executive. He had enough vision to know that the company needed to make a change if they wanted to stay competitive with their ever-growing opponent Coca-Cola. As fate would have it, a few years earlier Kendall had met another successful businessman, Herman W. Lay, at a grocer's convention. Lay was chairman of the Frito-Lay Company, a manufacturer of potato chips and other snack foods. The two men engineered a plan to merge their companies in 1965.

The Soviet connection would prove valuable beyond anyone's imagination. In 1972, Kendall made Pepsi the first U.S. consumer product produced and sold in the Soviet Union. Since the Soviet ruble wasn't convertible, Pepsi had to get creative. In exchange for Pepsi's cola concentrate, the Soviet Union provided Stolichnaya vodka for exclusive distribution within the U.S. This barter arrangement would later escalate to almost comic proportions—but that's a story for the next chapter.

V. The Game-Changing Merger: Frito-Lay + Pepsi-Cola = PepsiCo (1965)

The boardroom at 500 Park Avenue in Manhattan was tense on February 8, 1965. Two sets of executives—one from a beverage company, the other from a snack food empire—sat across from each other, contemplating what would become one of the most consequential mergers in American business history. In February 1965, the boards of directors for Frito-Lay, Inc. and Pepsi-Cola announced a plan for the merger of the two companies.

The logic was elegantly simple yet revolutionary. Herman Lay's Frito-Lay had become a snack food juggernaut after the 1961 merger of his H.W. Lay & Company with the Frito Company. At this point, the company's annual revenues totaled $127 million, largely generated from sales of its four main brands at the time: Fritos, Lay's, Cheetos, and Ruffles. But Lay faced a problem: how to expand internationally without building an expensive global distribution network from scratch.

Meanwhile, Don Kendall's Pepsi-Cola had the opposite challenge. They had distribution in 108 countries but essentially one product category. Coca-Cola's dominance in international markets meant Pepsi needed something else to push through its distribution channels—something to leverage its infrastructure investment.

On June 8, 1965, the merger of Frito-Lay and Pepsi-Cola Company was approved by shareholders of both companies, and a new company called PepsiCo, Inc. was formed. At the time of the merger, Frito-Lay owned 46 manufacturing plants nationwide and had more than 150 distribution centers across the United States.

The strategic rationale went deeper than simple synergy. In an interview with Forbes in 1968, PepsiCo CEO Donald Kendall summarized this by noting that "Potato chips make you thirsty; Pepsi satisfies thirst." It was a perfect consumption cycle—salty snacks driving beverage sales, beverages accompanying snack consumption. The vision was to create bundled promotions, joint displays, and integrated marketing campaigns.

But the dream hit an immediate regulatory wall. Plans to jointly promote the soft drink and snack products were thwarted later that year, when the Federal Trade Commission ruled against it. The FTC worried about anti-competitive bundling, forcing PepsiCo to operate its divisions more independently than originally planned.

PepsiCo reports $510 million in revenue. The combined company went public on the New York Stock Exchange, creating an instant giant. But the real genius of the merger wouldn't become apparent for years. While regulators prevented direct cross-promotion, they couldn't stop the fundamental economics: shared trucks, shared warehouses, shared customer relationships, shared negotiating power with retailers.

The merger also triggered an immediate innovation boom. Doritos launches throughout U.S. and quickly becomes a national sensation. Introduced in 1966, Doritos would eventually become a billion-dollar brand, proving that the combined company could create new products, not just manage existing ones. Funyuns followed in 1969, then Munchos in 1971—each launch leveraging PepsiCo's expanded distribution muscle.

The merger was pursued for multiple factors, one of which was the potential for Frito-Lay snacks to be distributed outside of its initial markets of the United States and Canada—via Pepsi-Cola's existing presence and distribution network in 108 countries at the time of the merger. International distribution of Frito-Lay products expanded soon after the 1965 merger, and its U.S. presence grew at the same time, resulting in Lay's becoming the first potato chip brand to be sold nationwide (in all 50 U.S. states) in 1965.

The cultural integration proved surprisingly smooth. Both companies were run by charismatic Southern entrepreneurs who understood each other's business philosophy. Kendall became CEO of the combined company while Lay served as chairman, a partnership that balanced beverage expertise with snack food mastery.

What nobody fully grasped in 1965 was how this merger would fundamentally reshape the food industry's understanding of portfolio strategy. PepsiCo had invented a new business model: the diversified food and beverage company. It wouldn't just compete with Coca-Cola in beverages—it would build an empire that made Coca-Cola's single-category focus look antiquated. The snack-and-soda combination that regulators tried to prevent would become PepsiCo's greatest competitive advantage, setting the stage for decades of acquisitions and expansions that would follow.

VI. Building the Empire: Strategic Acquisitions & Growth (1965–2000)

The year was 1977, and Don Kendall had a problem. Pepsi was gaining ground in the cola wars, but growth in U.S. carbonated beverage sales had begun slowing. Americans were drinking less soda per capita for the first time in decades. Kendall needed new growth engines, and he found them in an unexpected place: pizza parlors and chicken buckets.

In 1977 Pizza Hut merged with PepsiCo, becoming a division of the global soft drink and food conglomerate. Sales that year reached $436 million, and a new $10 million dollar headquarters office opened in Wichita. The Carney brothers, who had built Pizza Hut from a single location in 1958, sold Pizza Hut to PepsiCo for $300 million. From 1971 to 1977, Pizza Hut's profits grew an average of 40% per year.

A year later, in 1978, PepsiCo acquired Taco Bell from founder Glen Bell. Then came the big one: PepsiCo paid $850 million in 1986 for Kentucky Fried Chicken from RJR Nabisco. At the time PepsiCo bought Kentucky Fried Chicken, the New York Times reported KFC was Coke's second-largest fountain account, behind McDonald's.

The conventional wisdom said PepsiCo was vertically integrating—locking up fountain sales for its beverages. But that narrative misses the real story. About 20% of KFC's stores served Pepsi products, "PepsiCo stressed that the major reason for the acquisition was to expand its restaurant business, not to force Pepsi into every location. The truth was more complex: PepsiCo was building a hedge against the slowing beverage market.

The restaurant empire grew beyond the big three. In the early 1990s, PepsiCo acquired California Pizza Kitchen, Chevy's Fresh Mex, and D'Angelo Grilled Sandwiches. By the mid-1990s, PepsiCo's restaurant division was generating billions in revenue, making it one of the world's largest restaurant operators. The company had essentially built two businesses under one roof—a beverage and snack company, and a restaurant empire.

But running restaurants proved fundamentally different from selling packaged goods. Restaurants required massive capital investment, dealt with perishable inventory, managed thousands of retail locations, and faced intense local competition. The economics were completely different. While a can of Pepsi had consistent margins whether sold in Manhattan or Montana, restaurant profitability varied wildly by location. Wall Street analysts couldn't understand the decision when it was announced on January 23, 1997. PepsiCo Inc. said Thursday it would concentrate on its two strongest businesses– soft drinks and snack foods– and spin off its huge restaurant division as an independent publicly traded company. PepsiCo, based in Purchase, N.Y., owns the Pizza Hut, Taco Bell and KFC chains, which together have 29,000 units around the world.

The spin-off of what would become Tricon Global Restaurants (later Yum! Brands) was an admission that the restaurant experiment, while profitable, had become a distraction. The new CEO, Roger Enrico, wanted to focus on what PepsiCo did best: packaged goods with global brands and predictable margins.

The timing proved prescient. Just four years later, PepsiCo would make the acquisition that truly defined its modern strategy. PepsiCo completed its $13.8 billion acquisition of Quaker Oats Co. Thursday, August 2, 2001. But this wasn't about oatmeal or even the respected Quaker brand—In 2001, PepsiCo bought Quaker Oats for $14 billion, primarily to acquire the Gatorade brand.

Gatorade changed everything. In 1983, Quaker acquired Stokely-Van Camp, Inc., the maker of Van Camp's and Gatorade. By 2001, Gatorade dominated the $2.5 billion sports drink category with over 80% market share. For PepsiCo, it represented something even more valuable: a bridge from carbonated soft drinks to functional beverages.

The merger created a $25 billion food and beverage company sharply focused on the rapidly growing consumer demand for convenience. Under terms of the merger, Quaker shareholders received 2.3 shares of PepsiCo common stock in exchange for each share of Quaker common stock they own. Based on the number of Quaker shares outstanding, PepsiCo issued approximately 306 million additional shares of its common stock to Quaker shareholders.

"With Gatorade, we'll add the leading isotonic brand to our beverage portfolio," said Steve Reinemund, who succeeded Enrico as CEO. But the deal brought more than just Gatorade. The Quaker brand and the company's line of wholesome snacks gave PepsiCo an ideal way to expand beyond salty snacks. Products like Chewy granola bars, Quaker rice cakes, and Cap'n Crunch cereal diversified the portfolio in ways that would prove crucial as health consciousness grew.

The Quaker acquisition also highlighted a new reality: Coca-Cola had abandoned talks to buy Quaker for a reported $15.75 billion two weeks before PepsiCo's bid. While Coke hesitated, worried about diluting its beverage focus, PepsiCo pounced. It was a defining moment—PepsiCo would be the diversified food and beverage company, while Coca-Cola would remain the pure-play beverage specialist.

The international expansion continued throughout this period. The company that had put Pepsi behind the Iron Curtain now pushed snacks and beverages into every corner of the globe. Direct-store-delivery networks built for Pepsi now carried Lay's and Doritos. Distribution centers designed for Frito-Lay now housed Gatorade. The infrastructure investments of decades past created compound advantages that competitors couldn't replicate.

By 2000, PepsiCo had evolved from a soft drink company that happened to own some snacks into something unprecedented: a global convenience food and beverage platform. The journey from Caleb Bradham's pharmacy to a Fortune 100 giant was complete. But the next chapter—navigating health trends, sustainability demands, and changing consumer preferences—would prove even more challenging.

VII. Modern Era: Portfolio Transformation & Health Pivot (2000–Present)

The boardroom at PepsiCo's Purchase, New York headquarters was electric with tension in October 2006. Indra Nooyi (née Krishnamurthy; born October 28, 1955) had just been named chairman and chief executive officer (CEO) of PepsiCo. She was the first woman of color and first immigrant to head a Fortune 50 company. But her appointment came at a moment of existential questioning for the company.

"It was a high-performing company, and you know it's always difficult to take on a high-performing company because you've got to keep this engine going," Nooyi would later reflect. "What I had to do was take stock of the company and look forward 10 to 15 years at the big megatrends that were going to impact the consumer products industry, food and beverage in particular, and PepsiCo even more specifically."

The challenge was stark: consumer preferences were shifting rapidly toward healthier options, environmental concerns were mounting, and PepsiCo's core products—sugary sodas and salty snacks—were increasingly viewed as part of the obesity problem. Many investors saw Pepsi as a bloated giant whose top brands were losing market share. And they were critical of Nooyi's shift toward a more health-oriented overall product line. Prominent activist investor Nelson Peltz fought hard to split the company in two.

Nooyi's response was revolutionary for a company of PepsiCo's scale. She coined the term "Performance with Purpose" as Pepsi's new mantra. At its core, PwP was about harmonizing PepsiCo's business achievements with responsible stewardship for society and the environment. This wasn't just corporate speak – it was a fundamental shift in how the company operated.

The strategy had three pillars: Human Sustainability (healthier products), Environmental Sustainability (reduced footprint), and Talent Sustainability (empowering employees). By 2017, PepsiCo's annual report revealed that healthier alternatives made up the majority of its product offerings. The company reduced salt, fat, and sugar across its portfolio while introducing entirely new product lines focused on nutrition.

To ease the pressure from activists, Indra Nooyi initiated cost-cutting measures that were painful but necessary, including shedding 8,700 jobs and streamlining operations, to save US$1.5bn. Working closely with her leadership team, Nooyi spearheaded a restructuring of PepsiCo's top executives. This included introducing a system of rotating positions within the upper echelons, ensuring a continuous influx of fresh perspectives.

The financial results validated her approach. PepsiCo's annual net profit rose from $2.7 billion to $6.5 billion during her tenure. When she handed over the reins in 2018, revenues reached $63bn. During her tenure, PepsiCo grew net revenue more than 80%, and PepsiCo's total shareholder return was 162%.On August 6, 2018, PepsiCo announced a changing of the guard. Ramon Laguarta, a 22-year PepsiCo veteran, was unanimously elected to succeed Indra K. Nooyi as Chief Executive Officer. Laguarta became the sixth CEO in PepsiCo's 53-year history. All have been appointed from within the organization, a testament to PepsiCo's strong bench of talent and succession planning.

Ramon Laguarta (born 1963) is a Spanish businessman who became the first Spanish CEO of a large American multinational company. His ascent represented continuity but also evolution. Since becoming CEO of PepsiCo, Laguarta named three priorities: accelerating organic revenue growth; becoming a stronger company; and becoming a better company.

In 2021, Laguarta unveiled "pep+" (PepsiCo Positive), the company's strategic transformation agenda. Where Nooyi's Performance with Purpose focused on doing good while doing well, pep+ went further—embedding sustainability directly into PepsiCo's growth strategy. As Chairman and CEO, he has begun pivoting the company toward accelerated growth, embracing a new corporate mission—to Create More Smiles with Every Sip and Every Bite.

The strategy addresses modern challenges head-on. In 2018, Laguarta led the acquisition of SodaStream for $3.2 billion, primarily aimed at cutting plastic waste by promoting reusable bottles and at-home carbonation. "SodaStream continues to be very central to the transformation of the beverage category," Laguarta noted. "We think that there is a huge opportunity to enable consumers to personalize their drinks and have a type of consumption where there's no plastics."

Meanwhile, the portfolio transformation accelerated. In 2010, PepsiCo acquired the Pepsi Bottling Group and PepsiAmericas for $7.8 billion to control supply chain. This vertical integration gave PepsiCo direct control over distribution in key markets, allowing for faster innovation and better margin control.

The health pivot intensified under both CEOs. Current portfolio: ~60% revenue from food/snacks, 40% from beverages; 200+ brands including Mountain Dew, Tropicana, Gatorade, Lay's, Doritos, Cheetos, Quaker. By 2024, the company had successfully diversified far beyond its cola origins. In 2022, PepsiCo took a minority stake in energy drink company Celsius, recognizing the explosive growth in functional beverages.

But the modern era also brought unprecedented challenges. The rise of GLP-1 drugs like Ozempic fundamentally threatens the snack food industry. Sugar taxes proliferate globally. Climate change disrupts agricultural supply chains. Consumer preferences shift faster than ever before.

Yet PepsiCo's transformation from a soft drink company to a diversified food and beverage platform positions it uniquely for these challenges. The company that survived bankruptcy in 1923 had evolved into something far more resilient—a portfolio of brands that could adapt to whatever consumers wanted next.

VIII. Financial Performance & Current State

The morning of February 4, 2025, PepsiCo's earnings call revealed a company at a crossroads. Net revenue of $27.7 billion remained relatively unchanged from the year-ago period. Organic revenue growth was 2.1%. Net income attributable to PepsiCo was $1.52 billion, or $1.11 per share, compared to $1.30 billion, or $0.94 per share, last year. Core EPS was $1.96. Earnings per share: $1.96 adjusted vs. $1.94 expected; Revenue: $27.78 billion vs. $27.89 billion expected—the numbers told a story of resilience amid unprecedented headwinds.

The headline figures masked deeper challenges. The company's North American beverage unit reported a 3% decline in quarterly volume. But there were some bright spots for the division, as Gatorade gained market share and Mountain Dew Baja Blast surpassed $1 billion in annual sales. This marked the fifth consecutive quarter of volume declines in North America—a troubling trend for a company that had built its empire on American consumption habits.

2024 revenue: $91.85B, up 0.42% from 2023 The modest growth reflected a company navigating turbulent waters. Global inflation had forced aggressive price increases, which in turn dampened volumes. The North American challenges were particularly acute: consumers pushed back against higher prices, trading down to private label alternatives or simply consuming less.

Yet the geographic diversification strategy proved its worth. International markets, now representing nearly $40 billion in revenue, continued to show robust growth. Markets like India, China, and Latin America—where per capita consumption remained far below developed markets—offered decades of growth runway. "In 2024, the salty and savory snack categories underperformed broader packaged food, following multiple years in which these categories had outperformed packaged food," CEO Ramon Laguarta and CFO Jamie Caulfield said in prepared remarks.

The portfolio breakdown revealed the transformation's success. Current revenue split stands at approximately 60% from food/snacks and 40% from beverages. The company now owns 23 brands that generate over $1 billion each in annual retail sales, including global powerhouses like Lay's (the world's largest snack brand), Gatorade (dominating sports drinks), and Quaker (leading in nutrition).

Market position metrics paint a picture of dominance despite challenges. PepsiCo holds approximately 15.9% of the global snack market share and 29% of the North American beverage market share. In key categories, the moats remain wide: Gatorade commands over 70% of the sports drink market, Lay's leads potato chips, and Doritos dominates tortilla chips.

The financial strength remains formidable. With a beta of 0.55 and an attractive dividend yield of 3.61%, PepsiCo maintains a strong financial health score of "GOOD" according to InvestingPro's comprehensive analysis The company has achieved "Dividend King" status with 53 consecutive years of dividend increases—a testament to consistent cash generation through multiple economic cycles.

For 2025, Pepsi is projecting a low-single-digit increase in its organic revenue and a mid-single-digit rise in its core constant currency earnings per share. "Looking ahead to 2025, we will continue to build upon the successful expansion of our international business, while also taking actions to improve performance in North America," Laguarta said in a statement.

But new threats loom larger than ever. The segment is growing quickly, fueled in part by the adoption of GLP-1 drugs. The rise of drugs like Ozempic and Wegovy represents an existential challenge to snack food consumption. Early studies suggest GLP-1 users reduce caloric intake by 20-30%, with particular impact on snacking behavior.

The company's response has been swift but measured. Pepsi is also planning to push more into protein drinks, executives said on the company's conference call. This pivot toward functional nutrition—protein shakes, electrolyte drinks, nutrition bars—represents both a hedge against GLP-1 impact and an opportunity to capture higher-margin wellness spending.

The commodity price environment adds another layer of complexity. Input costs for corn, potatoes, sugar, and packaging materials remain volatile. Climate change increasingly disrupts agricultural supply chains, forcing the company to diversify sourcing and invest in agricultural sustainability.

Yet PepsiCo's scale provides unique advantages in this environment. The direct-store-delivery network—trucks going directly to 1 million retail locations weekly—creates a distribution moat that new entrants cannot replicate. The company's purchasing power allows it to secure supplies and negotiate prices that smaller competitors cannot match.

The investment case ultimately rests on a fundamental question: Can a company built on indulgence successfully pivot to wellness while maintaining profitability? The numbers suggest it's possible but challenging. Health-focused products now represent a significant portion of revenue, but margins remain lower than traditional snacks and sodas. The transition requires patience from investors accustomed to steady, predictable returns.

IX. Playbook: Strategic Lessons & Business Model

After studying PepsiCo's 127-year journey from pharmacy tonic to $200 billion enterprise, several strategic lessons emerge that transcend the food and beverage industry. These aren't just historical curiosities—they're blueprints for building enduring businesses in volatile markets.

The Power of Portfolio Diversification vs. Single-Category Focus

PepsiCo's greatest strategic insight was recognizing that diversification could be a competitive advantage, not a distraction. While Coca-Cola remained laser-focused on beverages, achieving remarkable returns through concentration, PepsiCo built resilience through breadth. The 1965 Frito-Lay merger wasn't just about adding snacks—it was about creating a consumption ecosystem where each product reinforces the others.

The numbers validate this approach. During periods when carbonated soft drink consumption declined—as it has for 20 consecutive years in the U.S.—snack revenues provided ballast. When commodity prices spike for potatoes, beverage margins compensate. This portfolio approach transforms PepsiCo from a beverage company that happens to sell snacks into a "share of stomach" company competing for every consumption occasion.

Direct-Store-Delivery as Competitive Advantage

PepsiCo's direct-store-delivery (DSD) system represents one of the most underappreciated moats in consumer goods. Every week, 100,000 PepsiCo employees and contractors visit over 1 million retail locations. They don't just deliver products—they merchandise displays, gather competitive intelligence, and build relationships with store managers.

This system, built over decades at enormous cost, cannot be replicated by startups or even well-funded competitors. It allows PepsiCo to launch new products faster, respond to local preferences, and maintain superior shelf presence. When a trending flavor emerges on social media, PepsiCo can have products in stores within weeks, not months. The DSD network transforms distribution from a cost center into a strategic weapon.

Brand Building Through Marketing Innovation

From the first national radio jingle to today's social media campaigns, PepsiCo has consistently pioneered new marketing channels. But the real insight goes deeper: PepsiCo doesn't just advertise products; it creates cultural moments. The Pepsi Generation wasn't selling cola—it was selling identity. Doritos Super Bowl ads don't promote chips—they create shared experiences.

This approach requires massive investment—PepsiCo spends over $2 billion annually on advertising—but it creates intangible assets that appear nowhere on the balance sheet. Brand value, estimated at over $20 billion for Pepsi alone, provides pricing power that commodity products could never achieve.

M&A Strategy: When to Buy vs. Build

PepsiCo's acquisition history reveals a disciplined framework: buy for capabilities and distribution, build for innovation. The Quaker Oats acquisition brought Gatorade's dominant market position and decades of sports science research—capabilities that would have taken decades to replicate. The Sabra hummus joint venture provided instant credibility in healthy snacking.

But PepsiCo learned hard lessons too. The restaurant ventures of the 1980s proved that operational synergies have limits. Running Pizza Hut required fundamentally different capabilities than selling packaged goods. The discipline to exit—spinning off the restaurants in 1997—proved as important as the courage to enter.

Managing Commodity Price Volatility

Caleb Bradham's bankruptcy from sugar speculation taught a lesson PepsiCo never forgot: commodity exposure can destroy even successful businesses. Today's PepsiCo employs sophisticated hedging strategies, forward contracts, and supplier diversification to manage input costs. But the real innovation is the portfolio itself—diverse input costs across snacks and beverages create natural hedges.

When corn prices spike, affecting Fritos and Tostitos, potato-based Lay's provides stability. When sugar prices soar, non-caloric sweeteners and savory snacks balance the impact. This isn't financial engineering—it's strategic architecture designed for resilience.

Balancing Growth with Health/Wellness Trends

The health transition represents PepsiCo's greatest strategic challenge and opportunity. The playbook emerging under Nooyi and Laguarta: transform gradually, not radically. Rather than abandoning core products, PepsiCo creates "permission structures" for healthier consumption—baked versions of popular chips, zero-sugar sodas that actually taste good, portion-controlled packaging.

The key insight: consumers want health, but they buy taste, convenience, and familiarity. PepsiCo's strategy threads this needle by making existing products better rather than replacing them entirely. Reducing sodium by 25% in chips goes unnoticed by consumers but meaningfully improves nutritional profiles. This incremental approach lacks the drama of radical pivots but preserves the cash flows needed to fund transformation.

The Franchise Bottler Model Evolution

PepsiCo's relationship with bottlers represents a masterclass in strategic evolution. The original franchise model—selling syrup to independent bottlers—provided capital-light growth but limited control. The 2010 acquisition of major bottlers for $7.8 billion reversed this, providing direct control over distribution in key markets.

This hybrid model—owned bottling in strategic markets, franchised in others—optimizes for both control and capital efficiency. It allows PepsiCo to rapidly deploy innovations in key markets while maintaining asset-light operations elsewhere. The model's flexibility proved crucial during COVID-19, when direct control allowed rapid pivots to e-commerce and direct-to-consumer delivery.

Competing as #2: Turning Disadvantage into Innovation Driver

Being second to Coca-Cola forced PepsiCo to think differently. Without Coke's distribution dominance, PepsiCo had to innovate in products. Without Coke's brand heritage, PepsiCo had to be more culturally relevant. This "challenger mindset" became embedded in company culture, driving innovations from the first diet cola to today's functional beverages.

The lesson extends beyond cola wars: sustainable competitive advantage often comes not from being better at the same game, but from changing the game entirely. PepsiCo's expansion into snacks, its focus on convenience stores over restaurants, its early embrace of international markets—all represent strategic zigs when Coca-Cola zagged.

The Ultimate Playbook Insight

Perhaps the most profound lesson from PepsiCo's history: resilience matters more than perfection. The company that nearly disappeared in 1923 survived not through flawless execution but through constant adaptation. Each crisis—from sugar speculation to health trends to GLP-1 drugs—forced evolution that ultimately strengthened the company.

This isn't a playbook for maximizing short-term returns. It's a framework for building businesses that endure across centuries, through wars and recessions, changing consumer preferences and technological disruption. In an era obsessed with disruption, PepsiCo's playbook offers something more valuable: a blueprint for permanence.

X. Analysis & Investment Case

Standing at the intersection of tradition and transformation, PepsiCo presents one of the most complex investment cases in consumer staples. The company that survived the Great Depression, two world wars, and the cola wars now faces what might be its greatest challenge: remaining relevant in an era of health consciousness, climate concerns, and pharmaceutical appetite suppression.

The Bull Case: Diversification, Brand Strength, and Emerging Market Growth

The optimistic view starts with PepsiCo's unmatched portfolio breadth. Unlike pure-play competitors, PepsiCo can lose entire categories and remain profitable. When carbonated soft drinks decline, snacks compensate. When developed markets stagnate, emerging markets accelerate. This diversification isn't just risk mitigation—it's optionality on multiple consumer trends simultaneously.

Brand power remains formidable despite changing preferences. Consumers might drink less soda, but when they do, they reach for familiar brands. The ~$20 billion in estimated brand value for Pepsi alone, plus billion-dollar brands across the portfolio, create pricing power that survives inflation, private label competition, and economic downturns. These aren't just products; they're cultural artifacts embedded in global consumption habits.

Emerging markets offer decades of growth runway. Per capita snack consumption in India is 1/10th of U.S. levels. China's sports drink market is nascent compared to North America. Africa's middle class is emerging. PepsiCo's early investments in these markets—distribution networks, local manufacturing, brand building—position it to capture outsized growth as consumption patterns westernize.

The financial foundation supports aggressive investment. With consistent free cash flow generation exceeding $6 billion annually, PepsiCo can simultaneously fund innovation, maintain its dividend aristocrat status, execute buybacks, and pursue acquisitions. This financial flexibility allows patient transformation rather than desperate pivots.

The Bear Case: Health Trends, GLP-1 Impact, and Structural Headwinds

The pessimistic view sees existential threats mounting. GLP-1 drugs like Ozempic aren't a fad—they're a pharmaceutical revolution that could permanently reduce caloric consumption. With 40% of Americans classified as obese and GLP-1 adoption accelerating, a significant portion of PepsiCo's core consumer base might simply eat less. Early studies suggest 20-30% consumption reduction among users, disproportionately impacting snacks and sugary drinks.

Regulatory headwinds intensify globally. Sugar taxes spread from cities to entire countries. Marketing restrictions target children. Plastic bans threaten packaging. ESG investors increasingly exclude "sin" foods. Unlike tobacco, which faced similar pressures, food and beverage companies can't rely on addiction to maintain consumption.

North American weakness appears structural, not cyclical. Five consecutive quarters of volume decline suggest more than temporary softness. Private label penetration increases as retailers leverage data and improve quality. Digital natives show less brand loyalty than previous generations. The core market that generates disproportionate profits shows signs of permanent impairment.

Competition intensifies from unexpected directions. Energy drinks cannibalize soda. Protein bars replace chips. Meal replacements challenge traditional eating. Technology companies enter food. The competitive landscape isn't just Coca-Cola anymore—it's everyone from Monster to Soylent to Amazon.

Competitive Dynamics: The Evolving Battlefield

The cola wars metaphor feels quaint in today's fragmented market. Coca-Cola remains the beverage rival, but the real competition comes from everywhere. Mondelez competes in snacks. Danone in health. Monster in energy. Private label in value. Startups in innovation.

PepsiCo's response reveals strategic clarity: compete on breadth, not depth. Rather than dominating single categories, PepsiCo aims to be present across all consumption occasions. This "share of stomach" strategy leverages the company's unique assets—distribution, portfolio breadth, innovation capabilities—rather than fighting category-by-category battles.

2025 Outlook: Navigating Near-Term Uncertainty

Management's guidance—low-single-digit organic revenue growth, mid-single-digit EPS growth—reflects measured confidence amid uncertainty. The growth algorithm seems achievable: 2-3% volume growth internationally offsetting North American weakness, 2-3% pricing maintaining margins, cost savings and buybacks bridging to mid-single-digit EPS growth.

But execution risks abound. Input cost inflation could exceed pricing power. GLP-1 adoption could accelerate beyond expectations. Economic recession could pressure volumes and mix. Currency headwinds could intensify. The guidance feels achievable but not conservative.

Valuation and Returns Analysis

At ~$211 billion market capitalization, PepsiCo trades at approximately 22x forward earnings—a premium to historical averages but discount to quality peers. The 3.5% dividend yield provides downside protection while waiting for growth recovery. The company's consistent buyback program—$1 billion planned for 2024—provides additional support.

The return profile depends on your timeline. Near-term (1-2 years): expect mid-single-digit returns from dividends plus modest multiple expansion as North America stabilizes. Medium-term (3-5 years): high-single-digit returns as emerging market growth accelerates and portfolio transformation bears fruit. Long-term (10+ years): the existential questions dominate—can PepsiCo transform into a wellness company while maintaining profitability?

ESG Considerations: From Liability to Asset

Environmental and social factors increasingly influence PepsiCo's investment case. Water usage in water-stressed regions, plastic packaging, agricultural sustainability, labor practices—these aren't just PR concerns but business risks. PepsiCo's pep+ agenda addresses these systematically, but execution remains early.

The opportunity: leadership in sustainability could become competitive advantage. Regenerative agriculture could reduce costs while improving resilience. Sustainable packaging could preempt regulation. Healthier products could capture premium pricing. ESG transformation could convert from cost center to value driver.

The Investment Decision Framework

For conservative investors seeking dividend income: PepsiCo offers rare combination of yield, growth, and safety. The dividend appears secure even in pessimistic scenarios.

For growth investors: Look elsewhere. PepsiCo's growth days of 10%+ returns are likely behind it. This is a mature company managing transformation, not a growth story.

For value investors: The risk-reward appears balanced but not compelling. Current valuation reflects both the challenges and opportunities appropriately.

For long-term investors: PepsiCo represents a bet on management's ability to navigate unprecedented change. The company has survived existential threats before, but never this many simultaneously.

The Verdict: A Hold With Asymmetric Optionality

PepsiCo isn't a screaming buy or obvious sell—it's a complex situation requiring nuanced analysis. The bear case is real and mounting. The bull case requires successful execution of difficult transformation. But the company's history suggests underestimating PepsiCo's resilience is dangerous.

The investment case ultimately reduces to a simple question: In a world of radical change, do you bet on the disruptors or the adapters? PepsiCo has been both—disrupting when necessary, adapting when required. That flexibility, more than any financial metric, might be its greatest investment merit.

For existing shareholders: Hold, collect dividends, and monitor transformation progress. For potential buyers: Wait for better entry points when sentiment reaches pessimistic extremes. For skeptics: Don't short resilience—PepsiCo has disappointed bears for over a century.

XI. Epilogue & Reflections

The rain had stopped in New Bern, North Carolina. If you walk down Middle Street today, past the building where Caleb Bradham once mixed his fountain drinks, you'll find a historical marker—modest, easy to miss. Few tourists stop. Fewer still contemplate the cosmic improbability that a failed medical student's digestive tonic would evolve into a quarter-trillion-dollar enterprise feeding billions.

From $30,000 bankruptcy sale to $200B+ market cap: this isn't just a business success story. It's a testament to the power of brands to transcend their physical products. Pepsi is no longer just flavored sugar water—it's nostalgia, identity, ritual. Doritos aren't just corn chips—they're Super Bowl parties, college memories, guilty pleasures. These intangible associations, built over generations, create value that no algorithm can fully capture.

What would Caleb Bradham think of modern PepsiCo? The pharmacist who marketed Pepsi as a health tonic would likely be bewildered by today's portfolio—products he'd consider confections marketed as mainstream food, alongside genuine nutrition products he'd recognize as medicine. He'd be astounded that his company survived not by staying true to his original vision but by constantly abandoning it for something new.

The ultimate lesson isn't about product innovation or marketing genius or financial engineering. It's about resilience through reinvention. PepsiCo survived by refusing to be wedded to what it was, constantly becoming what it needed to be. The company that started as a fountain drink became a bottled beverage, then a snack conglomerate, then a restaurant operator, then a nutrition company, and now transforms again into... something else. Something we don't have a name for yet.

Future Challenges: The Ozempic Era and Beyond

The GLP-1 revolution represents more than a health trend—it's a fundamental reset of humanity's relationship with food. If pharmaceuticals can control appetite, what happens to companies built on impulse consumption? PepsiCo faces a future where its core consumer base might simply want less of everything it sells.

But history suggests PepsiCo will adapt, as it always has. Perhaps it becomes a functional nutrition company, selling protein supplements to GLP-1 users concerned about muscle loss. Perhaps it pivots to experiential food—premium products for the occasions when people do indulge. Perhaps it discovers entirely new consumption occasions we can't yet imagine.

Climate change poses another existential challenge. Agricultural disruption, water scarcity, extreme weather—these aren't distant risks but current realities. PepsiCo's response will determine not just its financial returns but its social license to operate. Can a company built on abundance adapt to an era of scarcity?

The regulatory environment continues tightening. Sugar taxes, plastic bans, marketing restrictions—governments increasingly treat processed food like tobacco. But unlike tobacco, food companies can reformulate, repackage, reimagine. The question isn't whether PepsiCo can comply with regulation but whether it can lead beyond compliance.

If We Were Running PepsiCo: Strategic Priorities

First, we'd accelerate the health transformation—not through radical pivots but systematic improvement. Every product gets better every year—less sugar, less sodium, cleaner labels, better nutrition. Make the transformation invisible to consumers but material to health outcomes.

Second, we'd build the future portfolio through acquisition and incubation. Buy emerging brands in functional nutrition, plant-based proteins, personalized nutrition. Create internal ventures exploring food technology, cellular agriculture, synthetic biology. Some will fail; a few will define PepsiCo's next century.

Third, we'd restructure for agility. The current geographic and category structure made sense for a stabler world. Tomorrow requires something more adaptive—perhaps organizing around consumption occasions rather than products, or customer segments rather than geographies.

Fourth, we'd embrace radical transparency. In an era of radical transparency, trust becomes the ultimate currency. Share everything—ingredients, sourcing, nutrition impact, environmental footprint. Turn transparency from compliance burden into competitive advantage.

Finally, we'd prepare for portfolio surgery. Some brands won't survive the health transition. Better to divest proactively than manage decline. Use the proceeds to fund transformation rather than prop up dying categories.

The Meta-Lesson for Investors

PepsiCo's story offers a crucial insight for long-term investors: sometimes the best businesses are those that shouldn't exist. By all logic, a company selling sugar water and fried snacks should have disappeared as health consciousness rose. Instead, PepsiCo thrived by constantly evolving just enough to remain relevant while retaining what made it valuable.

This is the paradox of permanent enterprises: they survive not by being permanent but by being perpetually impermanent. They maintain identity while transforming substance. They honor heritage while abandoning tradition. They're simultaneously what they've always been and what they're becoming.

The Final Reflection

In 1898, a pharmacist in North Carolina created a drink he hoped would aid digestion. In 2025, his corporate descendant employs 300,000 people, operates in 200 countries, and shapes how humanity eats and drinks. The journey between those points defies linear narrative—it's a story of boom and bust, vision and luck, genius and folly.

But perhaps that's the real lesson. Business success isn't a formula to be solved but a dance to be danced. PepsiCo survived not by following a master plan but by responding to the music of its times—jazz age exuberance, depression-era frugality, post-war abundance, millennial health consciousness, and whatever comes next.

As we write in 2025, PepsiCo faces its most complex challenges yet. GLP-1 drugs, climate change, regulatory pressure, changing consumer preferences—any one could prove existential. The bear case is real and mounting. But betting against PepsiCo means betting against 127 years of adaptation, resilience, and reinvention.

The smart money might be on disruption. But the patient money—the kind that builds generational wealth—might just be on the company that's survived everything history could throw at it and keeps asking: what's next?

From Brad's Drink to global empire. From bankruptcy to billions. From sugar water to... whatever comes next. The PepsiCo story isn't ending—it's transforming, as it always has, into something we don't yet have words to describe.

That's not just a business story. That's mythology in real-time. And it's far from over.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube