Phillips Edison & Company: The Grocery-Anchored REIT That Mastered Necessity Retail

I. Introduction and Episode Roadmap

Picture a strip mall. Not the gleaming marble atrium of a Westfield or a Simon Property Group mega-mall, but the humble, L-shaped shopping center at the corner of your neighborhood — the one anchored by a Kroger or a Publix, flanked by a Great Clips, a Chipotle, a dentist's office, and an Anytime Fitness. You drive past it twice a day without thinking. You stop there to grab milk, drop off dry cleaning, get your teeth cleaned. It is, by design, the most forgettable piece of commercial real estate in America.

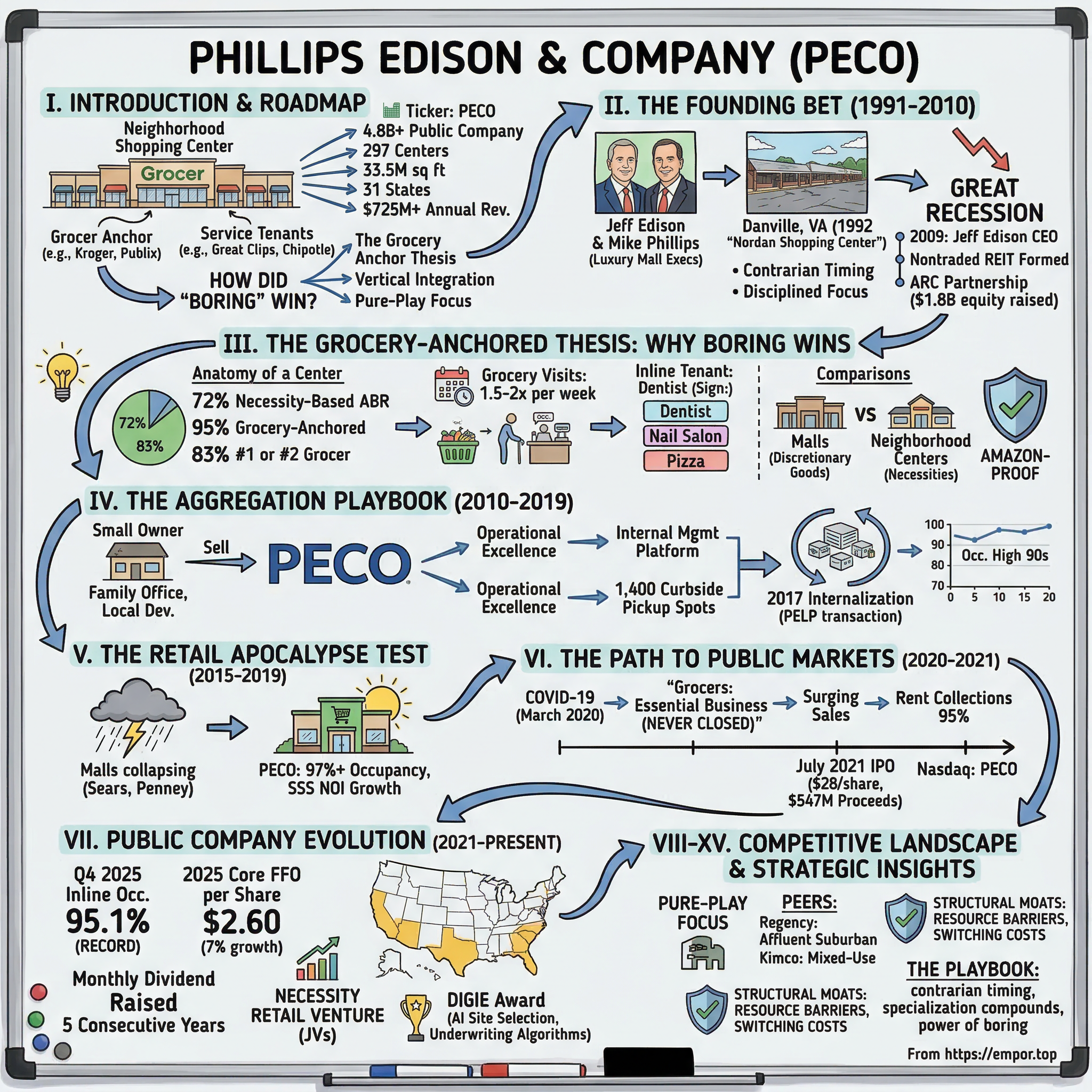

Phillips Edison & Company has built a nearly five-billion-dollar public company by owning 297 of these centers. PECO, as it trades on the Nasdaq, is the pure-play king of grocery-anchored neighborhood shopping centers — a portfolio spanning 33.5 million square feet across 31 states, generating over $725 million in annual revenue. The company's enterprise value hovers around $7.4 billion.

The central question of this story is deceptively simple: how did two former luxury-mall executives build a real estate empire out of the most unglamorous property type in commercial real estate? And more importantly — why did it work when nearly every other bet on physical retail got crushed?

The answer involves contrarian timing, disciplined focus, and a thesis about human behavior that has proven remarkably durable: people will always need groceries, and they will always want to buy them close to home. That might sound obvious in 2026, but when Jeff Edison and Mike Phillips started buying strip centers in the early 1990s — and then doubled down during the worst financial crisis since the Great Depression — the conventional wisdom was that their entire asset class was destined for obsolescence.

The themes running through this story will be familiar to anyone who studies great businesses: the power of boring, the discipline to say no, and the compounding advantage of doing one thing better than anyone else for three decades. PECO's story is not about disruption or moonshot bets. It is about mastering the fundamentals of necessity retail — the unsexy, high-frequency, Amazon-resistant corner of the economy where haircuts, prescriptions, and rotisserie chickens generate the kind of predictable cash flows that compound quietly while flashier investments flame out.

What makes PECO genuinely different from every other retail REIT that got battered by e-commerce? Three things: the grocery anchor thesis, vertical integration of property management, and an almost fanatical commitment to pure-play focus.

While competitors diversified into mixed-use developments, office buildings, and enclosed malls, PECO stayed in its lane — buying one neighborhood shopping center at a time, each one anchored by the dominant grocer in its local market. The result is a portfolio where 95 percent of annual base rent comes from grocery-anchored properties, 83 percent are anchored by the number-one or number-two grocer by sales in their respective trade areas, and 72 percent of tenant revenue flows from necessity-based businesses.

This is the story of how boring won.

II. The Founding Bet: Starting a Real Estate Company During the Great Recession

The origin story of Phillips Edison & Company begins not in 2009, but in 1991 — and it begins, paradoxically, in the world of luxury malls.

Jeff Edison and Mike Phillips met at The Taubman Company, the Michigan-based developer of some of America's most upscale enclosed malls. Taubman was — and still is — synonymous with prestige retail: marble floors, valet parking, Neiman Marcus anchor tenants. Edison and Phillips learned the real estate business there, but they saw something different when they looked at the American retail landscape. The future, they believed, was not in cathedrals of consumption but in the humble neighborhood shopping center — the kind of property most institutional investors considered beneath them.

Jeff Edison's background shaped this contrarian instinct. A mathematics and economics graduate of Colgate University, he earned his MBA at Harvard Business School in 1984 and went on to work at Morgan Stanley Realty and NationsBank's South Charles Realty Corporation before co-founding what would become Phillips Edison. He was, by temperament and training, a numbers person — someone who could see the gap between what institutional investors believed about strip centers and what the cash flows actually showed.

Their first acquisition told the story in miniature. In 1992, Edison and Phillips bought the Nordan Shopping Center in Danville, Virginia — a distressed strip center that nobody wanted. They bought it cheap, invested capital to bring it up to standard, stabilized the tenancy, and watched the cash flows roll in. That deal established the template that would define the next three decades: buy undervalued, community-serving retail real estate in markets where the grocery anchor generates reliable foot traffic, bring it to institutional quality through hands-on management, and hold for the long term.

What made this approach distinctive was the willingness to go where prestige-oriented investors would not. In the early 1990s, the real estate industry's hierarchy of desirability ran from trophy office towers and luxury malls at the top to strip centers and industrial parks at the bottom. Edison and Phillips were Harvard-trained, Morgan Stanley-pedigreed professionals choosing to operate at the bottom of the prestige ladder. They were not doing this out of necessity — they were doing it because the math was better. Cap rates on strip centers were 200 to 300 basis points higher than cap rates on comparable malls, meaning Edison and Phillips could generate more income per dollar invested while taking on arguably less fundamental risk, since grocery-anchored centers had more stable cash flows than discretionary-retail-dependent malls.

For most of the 1990s and 2000s, Phillips Edison operated through private funds for high-net-worth investors. They launched their first private fund in 2001, a second in 2002, building the portfolio deal by deal rather than through splashy portfolio acquisitions. The strategy was deliberate. Jeff Edison has said, "We're not 'big deal' guys. We've assembled the portfolio almost exclusively by buying individual assets one at a time." Each property had to clear proprietary underwriting screens — what the company would later formalize as the Power Score and Gold Score algorithms — before a dollar was committed.

Then came the Great Recession, and with it, the moment that transformed Phillips Edison from a modest private real estate firm into something far more ambitious.

In December 2009, at the absolute nadir of the financial crisis, Jeff Edison assumed the role of Chairman and CEO and the company formally constituted itself as a nontraded REIT. The timing was not accidental — it was the core of the thesis.

Commercial real estate prices had collapsed. Institutional capital had evaporated. Shopping center owners who had overleveraged during the boom were desperate to sell. And the market was making no distinction between enclosed malls selling discretionary goods — which were genuinely in trouble — and neighborhood grocery-anchored centers selling necessities, which were still collecting rent and generating foot traffic throughout the downturn.

The contrarian bet was simple and audacious: everyone thinks retail is dead, but grocery-anchored centers are fundamentally different. People buy food regardless of whether the economy is booming or collapsing. The anchor grocer generates traffic that sustains the surrounding tenants. And those surrounding tenants — barbers, dentists, dry cleaners — provide services that cannot be replicated online. If you could buy these properties at thirty to fifty cents on the dollar, the risk-reward was extraordinary.

The challenge was convincing anyone to invest in retail real estate during peak fear. Edison and Phillips solved this with a critical partnership.

In August 2010, the SEC declared effective an offering for Phillips Edison – ARC Shopping Center REIT Inc., a joint venture between Phillips Edison's operating expertise and American Realty Capital, the nontraded REIT fundraising powerhouse run by Nicholas Schorsch. The structure offered 150 million shares at ten dollars per share, sold through ARC's broker-dealer network. Over the life of this first nontraded REIT, which closed in February 2014, the vehicle raised approximately $1.8 billion in investor equity — a remarkable sum for a company that had operated quietly for nearly two decades.

The ARC partnership gave Edison something most private operators lack: a reliable, retail-investor-funded capital engine at precisely the moment when institutional pipelines were frozen. While competitors retrenched, cut staff, and waited for the storm to pass, Phillips Edison was buying.

The importance of the brand positioning was evident from day one. Edison and Phillips did not call themselves a "retail REIT" or a "strip mall company." They were a "grocery-anchored neighborhood shopping center" operator. The language mattered: it separated them from the dying mall narrative and emphasized the necessity retail thesis that would become their calling card with investors for the next fifteen years.

Building the team during this period meant recruiting talent that shared Edison's conviction. He needed leasing professionals who understood grocery-anchored dynamics, analysts who could evaluate trade areas at the micro-market level, and property managers who could execute rapid turnarounds on newly acquired assets. The early hires were people willing to bet their careers on the contrarian thesis — people who saw what Edison saw in the numbers and believed that the market's panic about retail was creating a generational buying opportunity.

The founding bet was not just on grocery-anchored real estate — it was on the conviction that crises create the best vintages of investment returns. Every great real estate fortune in American history has been built by buying when others were selling. Edison was explicit about this: the chaos of 2009-2010 was not a risk to be avoided but an opportunity to be seized.

III. The Grocery-Anchored Thesis: Why Boring Wins

To understand why Phillips Edison's thesis worked — and why it continues to work — you need to understand the anatomy of a grocery-anchored neighborhood shopping center and why it behaves nothing like its cousin, the enclosed regional mall.

A typical PECO property runs between 100,000 and 200,000 square feet. The anchor tenant is a supermarket — Kroger, Publix, Albertsons, a regional chain — occupying 40,000 to 65,000 square feet along one wing of an open-air, L-shaped or U-shaped complex. The remaining space is divided among fifteen to thirty inline tenants: the Great Clips, the Subway, the H&R Block, the urgent care clinic, the nail salon, the UPS Store, the neighborhood Chinese restaurant. There is nothing exciting about any of this. That is exactly the point.

The concept that Phillips Edison codified early — and marketed relentlessly once they went public — is "necessity retail." Approximately 72 percent of PECO's annual base rent comes from tenants selling goods and services that people need, not goods they want. Groceries, haircuts, medical appointments, prescriptions, quick-service meals, fitness memberships, tax preparation. These are not purchases that consumers research online, compare prices for across twelve websites, and then order from Amazon at a fifteen percent discount. They are habitual, high-frequency, proximity-dependent transactions that happen in person.

Consider the behavioral economics at work. When a consumer needs toothpaste, they do not optimize across fifteen e-commerce platforms — they grab it during their next grocery run. When a parent needs a last-minute birthday cake, they do not order it from an app with a two-hour delivery window — they stop at the bakery in their neighborhood center. These micro-transactions, individually trivial, aggregate into billions of dollars of annual consumer spending that flows through the physical retail infrastructure PECO owns. The key insight is that the most valuable consumer behaviors for a landlord are not the big, deliberate purchases — those have migrated online. The most valuable behaviors are the small, habitual, time-sensitive ones that require physical proximity.

The frequency piece is critical. The average American visits a grocery store 1.5 to 2 times per week — compare that to a department store visit, which might happen once a month or once a quarter. Every grocery trip generates foot traffic past the inline tenants. The dentist who leases 1,200 square feet next to the Publix is not paying for signage or advertising — she is paying for the guaranteed stream of thousands of potential patients walking past her door every week. This traffic-generation dynamic is why the grocery anchor is the economic engine of the entire center, even though the grocer itself typically pays below-market rent per square foot.

Why were these centers undervalued for so long? Institutional bias. In the 2000s and early 2010s, the prestige asset classes in retail real estate were enclosed malls — think Westfield, Simon, Macerich — and big-box power centers anchored by Home Depot and Target. Strip centers were considered "commodity" assets: too small, too fragmented, too boring for institutional capital. Pension funds and sovereign wealth funds wanted trophy properties. Nobody flew to New York to present a pitch deck about a Kroger-anchored strip mall in suburban Ohio.

This institutional disdain created a pricing gap that Phillips Edison exploited for years. They were buying properties at capitalization rates — the ratio of net operating income to purchase price — significantly higher than what institutional investors were paying for malls and big-box centers. In practical terms, they were generating more income per dollar invested because nobody else wanted what they were buying.

The Amazon-proof argument was central to the thesis, and it predated the moment when Amazon became an existential threat to physical retail. Jeff Edison understood early that grocery is the most complex, lowest-margin, and most logistics-intensive category in all of retail. Fresh produce spoils. Frozen food requires cold chain. Customers want to squeeze the avocados. The economics of delivering a twenty-dollar basket of groceries to someone's doorstep — factoring in labor, packaging, fuel, and spoilage — are brutally difficult. Amazon has spent billions trying to crack this problem and still has not achieved profitability in grocery delivery at scale.

The site selection science behind PECO's acquisitions deserves its own chapter. The company analyzes each potential acquisition through a rigorous framework: the three-mile trade area population, household income levels, traffic patterns, competitive grocer presence, and the quality of the anchor tenant. Think of it as a dating app for strip malls — each property gets scored on dozens of variables, and only the ones that pass both the Power Score (which measures the strength of the trade area demographics) and the Gold Score (which evaluates the property's physical characteristics and competitive positioning) make it through to the acquisition committee.

PECO's trademarked "Locally Smart" philosophy means that acquisition decisions are made not at the metro level but at the intersection level — they compete, as Edison has put it, "at the corner of Indian School Road and North 28th Street, not in the greater Phoenix area." A center might sit in a booming metro, but if it is on the wrong side of a highway interchange, in a trade area with declining household formation, or anchored by the third-best grocer in the market, it does not pass the screen. This granularity of analysis is what separates programmatic acquirers from opportunistic buyers.

The tenant mix strategy follows a deliberate logic. The grocery anchor draws traffic. The inline tenants serve that traffic with high-frequency, service-oriented businesses. PECO actively curates the mix — replacing struggling retailers with experiential and service businesses that cannot be replicated online. A shuttered Blockbuster becomes an Orangetheory Fitness. A vacant clothing boutique becomes an urgent care clinic. The evolution of the tenant mix over the past decade has only strengthened the Amazon-proof argument: you cannot get a root canal on the internet.

The difference between a Class A grocery anchor and a struggling one matters enormously. PECO insists that 83 percent of its properties are anchored by the number-one or number-two grocer by sales volume in their specific trade area. This is not a vanity metric — it is a survival metric. A dominant grocer generates higher sales per square foot, invests more in store maintenance and remodels, and attracts more traffic. A struggling grocer does the opposite, creating a downward spiral that drags the entire center with it. PECO's discipline on anchor quality is arguably the single most important underwriting criterion in their investment process.

There is a useful analogy for understanding why this model works. Think of a grocery-anchored shopping center as a small-scale airport. The airline — the grocery anchor — brings the passengers. The restaurants, shops, and services inside the terminal — the inline tenants — exist because of the passenger flow the airline creates. The airport operator — PECO — does not need to be in the airline business or the restaurant business. It simply needs to own the infrastructure where those businesses intersect. The airline pays a modest gate fee (below-market anchor rent), and the terminal shops pay a premium for access to the captive audience (above-market inline rent). The blended economics make the whole system work.

What emerges from all of this is a business model with a structural moat — not the kind of moat that comes from patents or network effects, but the kind that comes from the intersection of proximity, habit, and necessity. People will not drive twenty minutes to save fifty cents on a gallon of milk. They will not wait two days for Amazon to deliver their kid's prescription. They will not get their hair cut on Zoom. And the grocer they visit twice a week anchors an ecosystem of small businesses that serves the same impulse: convenience, proximity, routine.

The investor takeaway from the grocery-anchored thesis is that PECO has identified and exploited a structural mismatch in how the market valued different types of retail real estate. For years, the market treated all retail as one category. PECO saw that grocery-anchored neighborhood centers were a fundamentally different business from enclosed malls — different traffic patterns, different tenant mix, different consumer behavior, different e-commerce exposure. The discipline to build an entire company around that distinction, and to reject every opportunity that deviated from it, is the defining feature of the Phillips Edison story.

IV. The Aggregation Playbook: Roll-Up Strategy and Operational Excellence

The grocery-anchored shopping center market in America is vast and extraordinarily fragmented. PECO has identified approximately 5,800 properties nationally that meet their acquisition criteria — neighborhood centers anchored by a dominant grocer in a strong demographic trade area. The vast majority of these are owned by small private operators: family offices, local developers, individual investors who bought a strip mall in the 1980s and have been collecting rent checks ever since. Many of these owners lack the capital, expertise, or inclination to actively manage their properties — to re-tenant vacant spaces, negotiate with national chains, invest in parking lot resurfacing, or add the curbside pickup infrastructure that modern grocers demand.

This fragmentation was Phillips Edison's opportunity. The aggregation playbook worked like this: source properties one at a time from motivated private sellers, underwrite each acquisition through the Power Score and Gold Score algorithms, close the deal, and immediately bring the property onto PECO's internal management platform. The operational improvement was often significant. A property that had been passively managed by a local owner — with deferred maintenance, below-market rents on expired leases, and vacant inline spaces — could be transformed within twelve to eighteen months through active leasing, capital investment, and the halo effect of being part of a professionally managed national portfolio.

The nontraded REIT capital engine made the pace of acquisition extraordinary. Between 2010 and 2014, fueled by the $1.8 billion raised through the ARC partnership's first vehicle, PECO bought aggressively across the country. A second nontraded REIT, launched in 2013, added billions more in firepower. Combined across both vehicles, the company raised approximately $3 billion in equity from retail investors — a staggering sum for a company focused exclusively on strip malls.

The key inflection point came in 2012-2013, when PECO shifted from being an opportunistic buyer — cherry-picking distressed assets in a down market — to a programmatic acquirer with the infrastructure to evaluate, close, and integrate multiple properties simultaneously. This required building out the internal property management platform from scratch: leasing professionals deployed in every major market, centralized accounting, a national maintenance vendor network, standardized reporting, and the technology backbone to manage it all.

This transition from opportunistic to programmatic is a critical distinction that most observers miss. An opportunistic buyer evaluates each deal on its own merits — is this property cheap enough to generate a good return? A programmatic acquirer has built the systems and processes to evaluate, close, and integrate properties at volume, applying consistent standards across hundreds of transactions. The difference is analogous to the gap between a talented amateur chef cooking a great meal and a restaurant chain that can produce consistently good meals across thousands of locations. The programmatic capability is what allowed PECO to reportedly double in size every three years during this period while maintaining quality standards that preserved the integrity of the portfolio.

The 2017 PELP transaction was the structural masterstroke that made everything else possible. In October 2017, Phillips Edison Grocery Center REIT I completed its acquisition of the real estate assets and the entire third-party asset management business from Phillips Edison Limited Partnership — the private operating company owned by the Edison and Phillips principals.

This was effectively a management internalization: collapsing the complex web of external advisor, private operating company, and nontraded REIT into a single, clean, internally managed entity. The deal created a unified company operating 235 shopping centers across 26.2 million square feet in 32 states, with a third-party asset management platform managing an additional $2 billion in grocery-anchored assets. Critically, management received no cash consideration and was subject to lockup provisions — a signal of alignment that resonated with investors.

Why did vertical integration matter so much? In commercial real estate, the gap between good management and mediocre management shows up directly in the numbers: occupancy rates, releasing spreads, tenant retention, same-center net operating income growth. When PECO manages its own properties — handles its own leasing, its own maintenance, its own tenant relationships — it captures the full economic value of operational improvement rather than sharing it with a third-party manager. It also creates feedback loops: the leasing team in suburban Atlanta learns which tenant categories are working, feeds that intelligence back to the acquisitions team, which uses it to underwrite the next deal in a similar market.

The 2018 REIT II merger was the scale play. In November 2018, PECO completed a 100 percent stock-for-stock merger with Phillips Edison Grocery Center REIT II, creating a combined entity valued at approximately $6.3 billion. The merger added 86 centers and 10.3 million square feet to PECO's existing portfolio, bringing the total to 334 grocery-anchored shopping centers across 37.7 million square feet.

The deal eliminated $14 million in annual advisory expenses for REIT II shareholders — a direct benefit of the internalized management structure. Simultaneously, PECO contributed 17 properties into a joint venture with Northwestern Mutual Life Insurance Company, establishing the capital-partner model that would become a recurring feature of its growth strategy.

A smaller merger followed in October 2019, when PECO absorbed Phillips Edison Grocery Center REIT III — a three-property vehicle that also brought a 10 percent equity interest in a second Northwestern Mutual joint venture. By the time these consolidations were complete, the corporate structure was clean, the portfolio was scaled, and the management platform was fully integrated.

Throughout this entire roll-up, PECO maintained a disciplined relationship with its grocery anchors. The top tenants by annual base rent — Kroger, Publix, Albertsons/Safeway, Ahold Delhaize — were not just tenants; they were strategic partners. PECO invested in the infrastructure these grocers needed: curbside pickup parking spots, expanded loading docks, modernized facades. In return, the grocers committed to long-term leases and invested their own capital in store remodels. This symbiotic relationship — landlord and anchor tenant co-investing in the same property — is the kind of alignment that creates durable competitive advantage.

The re-tenanting strategy evolved over this period as well. When a struggling small tenant vacated — a local gift shop, an outdated video rental store, a failed frozen yogurt concept — PECO did not simply re-lease to the next small retailer willing to sign. They actively recruited tenants from categories with structural tailwinds: fitness studios, urgent care clinics, fast-casual restaurants, pet services. The inline tenant mix shifted measurably toward businesses that benefited from grocery traffic and were immune to e-commerce substitution.

This curation had a compounding effect. A center with an Orangetheory Fitness, a dental practice, and a fast-casual restaurant like Chipotle is not just generating rent — it is generating reasons for consumers to visit beyond the grocery trip. The more reasons people have to visit the center, the longer they stay, the more they spend, and the more attractive the center becomes for the next tenant looking for a location. It is a virtuous cycle that PECO consciously engineered through thousands of individual leasing decisions across hundreds of properties.

Over more than thirty years, the company acquired more than 500 assets, building the most focused grocery-anchored portfolio in the public REIT universe. The aggregation machine — fueled by nontraded REIT capital, refined by proprietary analytics, and executed through an integrated management platform — had transformed Phillips Edison from a small Cincinnati-based real estate firm into a national operator with the scale, systems, and track record to justify a public market listing. The question was no longer whether the thesis worked. The question was whether it could scale further under the bright lights of public market scrutiny.

V. The Retail Apocalypse Test

The years between 2015 and 2019 were a bloodbath for retail real estate. Department stores collapsed: Sears filed for bankruptcy, J.C. Penney spiraled toward insolvency, Macy's closed hundreds of stores. Big-box retailers shuttered locations by the thousands. Mall foot traffic declined year after year. The narrative was simple and relentless: Amazon was killing physical retail, and anyone who owned shopping centers was holding a melting ice cube.

The stock market was merciless. Mall REITs like CBL & Associates and Washington Prime Group — companies that owned enclosed malls anchored by precisely the department stores that were going bankrupt — saw their share prices crater by seventy, eighty, ninety percent. Even diversified retail REITs with strong portfolios suffered significant multiple compression as investors painted the entire sector with the same brush.

Inside this storm, Phillips Edison was having a very different experience. Occupancy across the PECO portfolio remained in the high nineties — above 97 percent in most quarters. Same-center net operating income continued to grow. Tenant sales held steady. The grocery anchors were not just surviving; they were investing in their stores, rolling out online ordering with in-store pickup, and expanding prepared food sections to compete with restaurants. Every time a grocer added curbside pickup, it generated an additional trip to the center — a customer who might also stop at the dry cleaner or grab a coffee.

The data vindicated the thesis in real time. While enclosed malls were losing anchor tenants and watching foot traffic evaporate, grocery-anchored strip centers were gaining tenants from categories that had previously leased space in malls. Fitness concepts like Orangetheory and Planet Fitness discovered that strip center locations — with abundant parking, lower rents, and grocery-driven traffic — outperformed mall locations. Urgent care clinics and dental practices found that the convenience factor of a neighborhood center drove higher patient volumes than medical office buildings. Fast-casual restaurants realized that lunch and dinner traffic from grocery shoppers provided a natural customer base.

PECO used the fear to its advantage. While competitors retrenched — reducing acquisition targets, conserving cash, selling properties to shore up balance sheets — PECO continued buying. The "retail apocalypse" narrative kept prices depressed for precisely the asset type that was performing best. Private sellers who read the headlines about Amazon and dying malls became convinced that their strip center was next, offering it to PECO at attractive cap rates. The irony was exquisite: the worse the narrative got for retail real estate broadly, the better the buying opportunity became for grocery-anchored centers specifically.

This period also saw PECO refine its data-driven approach to portfolio management. The company tracked tenant sales per square foot at the property level, monitoring not just whether spaces were leased but whether the businesses occupying them were healthy. A tenant paying rent but seeing declining sales is a ticking clock — eventually, that lease will not renew, or worse, the tenant will default. By tracking leading indicators of tenant health, PECO could proactively re-tenant spaces before they became vacant, maintaining the occupancy rates and curb appeal that attract other tenants and drive property-level valuations.

The "last mile" narrative emerged during this period and provided an intellectual framework that resonated with growth-oriented investors. As e-commerce grew, retailers and logistics companies realized that physical stores located close to consumers — within a three-mile radius of dense residential areas — were valuable not just as places to sell things, but as distribution nodes for fulfilling online orders. Grocery stores, with their refrigeration infrastructure and high-frequency customer traffic, were ideally positioned as last-mile fulfillment hubs. Every Kroger that added a curbside pickup bay was, in effect, becoming a micro-distribution center embedded in PECO's shopping center.

The tenant evolution during this period represented a structural shift in the composition of neighborhood retail. Traditional retail tenants — clothing boutiques, gift shops, bookstores — gave way to service and experiential businesses that Amazon could not replicate. The PECO portfolio emerged from the 2015-2019 period with a fundamentally more resilient tenant base than it had entering it. This was not accidental — it was the result of deliberate curation, active leasing, and the willingness to accept short-term vacancy to hold out for the right tenant rather than filling space with marginal retailers who would fail within two years.

There is a myth worth dispelling here: the idea that grocery-anchored centers were "safe" throughout this period. They were not immune to all disruption. PECO lost tenants during these years — small retailers who could not compete with online alternatives, restaurants that failed, fitness concepts that did not achieve critical mass. The difference was that PECO could replace these tenants, often at higher rents, because the grocery anchor kept drawing traffic. A vacant inline space in a center doing 40,000 grocery transactions per week is a very different proposition from a vacant space in a power center that lost its Target anchor. The demand for space near a thriving grocery store remained strong even as demand for space near a struggling department store evaporated.

For investors watching the carnage in mall REITs and wondering whether any retail real estate could survive the Amazon onslaught, PECO's performance through this period was a proof point. The grocery-anchored strip center was not a variant of the dying mall — it was a fundamentally different asset class, serving fundamentally different consumer needs, with fundamentally different economic dynamics. The retail apocalypse was real. It just was not PECO's apocalypse.

VI. The Path to Public Markets: From Private Equity to Public REIT

By early 2020, Phillips Edison had spent three years preparing for the transition from private to public company. The management internalization was complete. The REIT II merger had created scale. Non-core assets had been pruned from the portfolio. The balance sheet was being optimized. Everything was pointing toward a public listing — and then the world shut down.

The COVID-19 pandemic arrived in March 2020, and for a few terrifying weeks, it appeared to threaten every thesis that underpinned PECO's business. At peak shutdown, approximately 37 percent of PECO's 5,550 tenant spaces were temporarily closed. Rent collections plummeted — May 2020 collections hit just 80 percent of monthly billings. The question hanging over the company was existential: if governments could order businesses to close, was any physical retail truly safe?

The answer came faster than anyone expected, and it came from the grocery anchors. Supermarkets were classified as essential businesses from day one. They never closed. In fact, grocery sales surged as Americans stopped eating at restaurants and cooked at home. The panic buying of March and April 2020 — empty shelves, long lines, hoarding — was dystopian, but it produced record sales volumes for the Krogers and Publixes anchoring PECO's centers. The foot traffic these essential businesses generated provided a lifeline for inline tenants that were permitted to reopen with modifications.

The contrast with other retail property types was stark. Enclosed malls — with their recirculated air, crowded common areas, and discretionary-retail anchor tenants — became the physical embodiment of pandemic risk. Many remained closed or operated at severely restricted capacity for months. Power centers anchored by non-essential retailers like department stores and electronics chains also suffered extended closures. But the open-air, neighborhood shopping center — with its outdoor walkways, its essential-business anchor, and its proximity to residential neighborhoods — was positioned almost perfectly for a pandemic world. Consumers could walk to their neighborhood Kroger, pick up groceries, stop by the pharmacy, and grab a coffee without ever entering an enclosed space shared with hundreds of strangers.

PECO's management team moved with impressive speed. The company added 1,400 "Front Row 2 Go" curbside parking spots across the portfolio, completed 79 projects to expand outdoor dining areas, add drive-through windows, and install pickup capabilities. These were not long-term capital projects — they were rapid-response adaptations completed in weeks, not months. By July 2020, tenants representing 98 percent of PECO's annual base rent were open for business. By the fourth quarter of 2020, rent collections had recovered above 95 percent.

The pandemic turned out to be the ultimate proof of concept. By June 2021, foot traffic at PECO centers had recovered to 102 percent of the average 2019 monthly level — not just back to pre-pandemic norms, but exceeding them. Second-quarter 2021 same-center NOI came in 4.5 percent above the second quarter of 2019, the pre-COVID baseline.

The behavioral shifts catalyzed by COVID actually reinforced the grocery-anchored thesis in ways nobody anticipated. Americans who had been eating out five nights a week discovered home cooking. Suburban households that had commuted to urban offices now worked from home, spending more time — and more money — in their neighborhoods. The neighborhood shopping center became not just a place to buy groceries but the social and commercial hub of a newly homebound population. The dry cleaner, the coffee shop, the fitness studio — all of these businesses benefited from the suburbanization of daily life that COVID accelerated.

The grocery-anchored strip center had not just survived the most severe disruption to physical retail in modern history — it had emerged stronger. And that was exactly the story PECO needed to tell on its roadshow.

This performance gave PECO exactly the narrative it needed for the IPO.

The offering was priced on July 14, 2021, and shares began trading on the Nasdaq Global Select Market on July 15, 2021, under the ticker PECO. Prior to the IPO, the company executed a one-for-three reverse stock split to bring the share price into an institutional range. The offering priced at $28.00 per share — the low end of the preliminary $28 to $31 range — and comprised 17 million initial shares plus a 2.55 million share overallotment option that was exercised in full the following month. Total gross proceeds came to approximately $547 million.

The underwriting syndicate was a who's-who of Wall Street: Goldman Sachs and Morgan Stanley as joint lead book-runners, flanked by Bank of America, J.P. Morgan, BMO, KeyBanc, Mizuho, and Wells Fargo. The primary use of proceeds was prosaic but strategically important — repayment of a $375 million unsecured term loan maturing in 2022, plus funding for new acquisitions.

Market reception was cautiously positive. Retail REITs still carried the stigma of the apocalypse narrative, and the IPO priced at the bottom of its range.

But the stock closed its first day at $27.83 and climbed to $31.18 by early October — a twelve percent gain in its first few months, suggesting that the market was beginning to appreciate the distinction between grocery-anchored necessity retail and the broader retail category.

The transition from private company to public company discipline required cultural adaptation. PECO had operated for decades with the flexibility of a private firm — making acquisition decisions quickly, communicating with a limited group of institutional investors, and running the business without the quarterly scrutiny of public market analysts.

Going public meant earnings calls, guidance ranges, proxy statements, and the relentless pressure to deliver sequential improvement. Jeff Edison remained as Chairman and CEO, providing continuity. But the company added public-company infrastructure: investor relations, expanded financial reporting, enhanced corporate governance, and a board composition reflecting the independence requirements of a listed company.

The strategic rationale for going public extended beyond the immediate capital raise. As a public REIT, PECO gained access to cheaper, more diverse sources of capital — unsecured bonds, at-the-market equity offerings, preferred stock — that simply were not available to a nontraded vehicle. Public company stock could be used as currency for acquisitions. And the listing provided liquidity for early investors who had been locked into the nontraded REIT structure for years, finally giving them a market in which to realize their returns.

The corporate governance transformation deserves mention. As a nontraded REIT, PECO had operated with a relatively concentrated decision-making structure — the founders and a small board controlled strategy, capital allocation, and operations with minimal external oversight. Going public meant building out an independent board of directors, establishing audit and compensation committees, adopting Say-on-Pay provisions, and submitting to the proxy advisory firms' governance frameworks. Jeff Edison's dual role as Chairman and CEO — common in founder-led companies but increasingly scrutinized by institutional investors — reflected the market's willingness to accept concentrated leadership when the track record justified it. The board composition included directors with deep backgrounds in real estate, finance, and retail operations, providing the institutional credibility that public market investors demand.

The IPO also marked the moment when PECO's story shifted from "private equity fund with great returns" to "public company with a quarterly scorecard." The first few quarters of public life established the cadence: earnings calls, guidance ranges, analyst days, investor conferences. Edison and his team adapted to this rhythm while maintaining the long-term orientation that had defined the company's approach for three decades — a balancing act that many newly public companies struggle with.

VII. Public Company Evolution: Strategy and Execution

The post-IPO era has been defined by disciplined execution rather than dramatic pivots. PECO's playbook as a public company looks remarkably similar to its playbook as a private one: buy high-quality grocery-anchored centers one at a time, integrate them onto the internal management platform, drive same-center growth through active leasing, and maintain a conservative balance sheet.

The acquisition pace has been steady and accelerating. In 2022, PECO acquired seven properties and four outparcels for $280.5 million while selling four properties and four outparcels for $54 million. In 2023, the portfolio grew to 281 wholly-owned properties as the company deployed approximately $250 to $300 million in net acquisitions. The 2024 vintage was stronger still — 14 shopping centers and four land parcels for approximately $306 million, exceeding the midpoint of revised guidance. And 2025 brought the most aggressive deployment yet: $395.5 million in acquisitions, including 18 shopping centers and outparcels, offset by $145.4 million in dispositions. The 2026 guidance calls for $400 to $500 million in gross acquisitions — continuing the upward trajectory.

What is notable about this acquisition ramp is that it occurred during a period of rising interest rates and tightening capital markets — conditions under which most real estate buyers slow down or stop entirely. PECO was able to continue acquiring because its investment-grade balance sheet, its access to the unsecured bond market, and its joint venture partnerships provided capital sources that were not available to smaller, more leveraged competitors. The dispositions side of the equation matters too: by selling $145 million in lower-quality assets while buying $395 million in higher-quality ones, PECO is actively upgrading the portfolio — recycling capital from properties that no longer meet the Power Score and Gold Score thresholds into properties that exceed them.

The capital allocation framework balances three priorities: acquisitions, redevelopment, and balance sheet management. Acquisitions drive external growth — adding new properties to the portfolio at cap rates that exceed PECO's cost of capital. Redevelopment drives internal growth — investing in existing properties to add density, modernize facades, and create outparcel opportunities. In 2025 alone, PECO completed 23 development and redevelopment projects totaling 400,000 square feet with a total investment of $53.8 million, with another 20 projects in the pipeline at an estimated cost of $69 million. Balance sheet management ensures that the whole enterprise stays on solid financial footing: net debt to adjusted EBITDA at 5.2 times, 95 percent of debt at fixed rates, a weighted-average interest rate of 4.4 percent, and no meaningful debt maturities until February 2027.

The same-center growth story has been remarkably consistent. Same-center NOI growth came in at 4.5 percent in 2022, 4.2 percent in 2023, 3.8 percent in both 2024 and 2025, with 2026 guidance of 3 to 4 percent. These are not explosive growth numbers, but they do not need to be. In a business with high operating margins, minimal capital expenditure requirements, and 97 percent occupancy, three to four percent annual same-center growth compounds into substantial value creation over time. The drivers are straightforward: contractual rent escalators built into existing leases (typically 2 to 3 percent annually), releasing spreads when leases roll (new leases in 2025 were signed at 30.9 percent above expiring rents), and incremental occupancy gains in the small shop portfolio.

The small shop strategy is where the real economic value lies. While grocery anchors typically pay below-market rent — often in the range of eight to twelve dollars per square foot — they generate the traffic that allows inline tenants to pay twenty, thirty, or even forty dollars per square foot. PECO's record-high inline occupancy of 95.1 percent, achieved in the fourth quarter of 2025, represents a meaningful inflection. Every hundred basis points of inline occupancy gain translates directly into higher-rent revenue with minimal incremental cost.

The joint venture strategy has emerged as a capital-efficient growth lever. PECO holds a 20 percent equity interest in Necessity Retail Venture LLC, a partnership with an affiliate of Cohen & Steers Income Opportunities REIT, through which the companies co-acquire grocery-anchored properties. By year-end 2025, PECO managed 27 joint venture shopping centers across three institutional partnerships. This model allows PECO to deploy its operating platform and earn management fees while sharing the capital burden — particularly valuable when the stock trades below levels that make equity issuance attractively priced.

On the technology front, PECO won the Digie Award for Best Use of AI at the 2024 Realcomm Conference, a major commercial real estate technology gathering. The company has built custom in-house AI solutions for organizational productivity, automation, and cross-functional collaboration. More tangibly, the proprietary underwriting algorithms — the Power Score and Gold Score — continue to evolve with larger datasets, and machine learning tools are being deployed for predictive analytics on tenant performance and trade area dynamics.

This technology investment is worth pausing on, because it illustrates how even "boring" industries can derive competitive advantage from data and analytics. When PECO evaluates a potential acquisition, it draws on performance data from 500-plus historical transactions to predict how a specific property will perform under its management. It can estimate the releasing spread on inline tenants based on comparable properties in similar trade areas. It can model the impact of a grocer remodel on foot traffic and inline tenant sales. These are not theoretical capabilities — they are the accumulated intellectual property of three decades of focused operation in a single property type. A generalist investor or a diversified REIT that owns hotels, offices, and shopping centers simply cannot match this depth of proprietary insight.

Perhaps the most consequential development of the 2023-2025 period has been the transformation of the grocery industry itself. America's leading supermarket chains have invested billions of dollars in their physical store infrastructure — remodeling stores, expanding prepared food offerings, adding curbside pickup bays, deploying delivery capabilities, and building private-label brands that drive traffic. Kroger's "store-centric" model, which uses existing store locations as both retail destinations and last-mile fulfillment hubs, is a direct bet on the physical footprint that PECO provides. Every dollar a grocer invests in a PECO-owned location strengthens the anchor tenancy and increases the traffic that supports the inline tenant ecosystem.

The dividend story has been a quietly powerful element of the shareholder return. PECO has raised its monthly dividend for five consecutive years, with the most recent increase of 5.7 percent in September 2025 bringing the annualized payout to $1.30 per share. The current yield of approximately 3.5 to 3.6 percent, paid monthly rather than quarterly, appeals to income-oriented investors. Total dividend growth since the 2021 IPO exceeds 20 percent.

The monthly payment cadence is worth noting — most REITs pay dividends quarterly, but PECO's monthly payments create a more consistent income stream for investors who rely on dividends for living expenses. This is not a trivial differentiator in the income-investing world: retirees and income-focused funds value the regularity and predictability of monthly payments, and it creates a loyal shareholder base that tends to be less volatile in its trading behavior than momentum-driven institutional investors.

In February 2026, PECO priced $350 million of 4.750 percent senior unsecured notes due March 2033, using the proceeds to repay revolving credit and term loan balances. This kind of opportunistic debt capital markets activity — locking in fixed-rate financing at manageable costs while extending the maturity profile — reflects the balance sheet discipline that earns and maintains an investment-grade credit rating.

VIII. The Competitive Landscape and Market Position

The grocery-anchored shopping center space has four significant public competitors, each pursuing a distinct strategy. Understanding where PECO fits — and where it does not — requires a clear-eyed look at each.

Regency Centers is the largest and most direct comparable. With more than 480 shopping centers spanning 56 million square feet, Regency is nearly twice PECO's size and carries a market capitalization of approximately $13.1 billion. The company focuses on affluent suburban demographics and "trade area dominance" — similar in philosophy to PECO but executed at larger scale and with a broader geographic footprint that includes coastal and northeastern markets following its 2023 all-stock acquisition of Urstadt Biddle Properties for $1.4 billion.

Regency's 2025 results were strong: same-property NOI growth of 5.3 percent and, for the first time in company history, more than $1 billion in annual EBITDA. Its BBB+ credit rating from S&P sits one notch above PECO's BBB.

Brixmor Property Group operates approximately 365 retail centers and pursues a meaningfully different strategy — value-add transformation. Brixmor buys older, undermanaged community centers and repositions them with higher-credit tenants, density improvements, and outparcel development. It is, in many ways, the private-equity approach applied to a public REIT platform. Brixmor's 2025 same-property NOI growth of 4.2 percent and record small shop occupancy of 92.2 percent demonstrate the returns available from active repositioning. It trades at a valuation discount to peers — roughly 11.4 times forward FFO — reflecting both the higher execution risk of the value-add model and the market's perception of lower portfolio quality relative to PECO and Regency.

Kimco Realty is the scale leader, with 565 properties comprising 100 million square feet and a market capitalization approaching $16 billion. Kimco's distinction is its mixed-use component — adding residential density above retail, building ground-floor retail into apartment developments, and concentrating in first-ring suburbs of major metros.

The company's 2024 acquisition of RPT Realty for more than $2 billion further cemented its scale advantage. Kimco's 2025 same-property NOI growth of 3.0 percent was modest relative to peers, but its development pipeline and redevelopment yields (19 percent on 2025 completions) add a growth vector that pure play operators like PECO lack.

PECO's differentiation in this competitive set comes down to focus. Where Regency has broader geographic exposure, Brixmor pursues repositioning plays, and Kimco adds mixed-use density, PECO does one thing: owns and operates neighborhood shopping centers anchored by the dominant grocer in each local market. This pure-play positioning has advantages and disadvantages. The advantage is clarity — investors know exactly what they are buying, tenants know exactly what to expect, and the operating platform is optimized for a single property type. The disadvantage is limited growth optionality. PECO cannot pivot into mixed-use development or industrial logistics if grocery-anchored centers ever fall out of favor.

The geographic footprint strategy concentrates the portfolio in Sunbelt and growth markets — areas with population in-migration, strong employment trends, and favorable demographics. This means heavy exposure to states like Florida, Texas, Georgia, and the Carolinas, with underweight positions in declining industrial metros and high-cost coastal markets. The geographic concentration creates risk — a regional economic downturn in the Sun Belt would disproportionately affect PECO — but it aligns with the demographic trends that have driven American population growth for the past two decades.

Scale in the REIT world is a double-edged sword. The advantages are real: lower per-property overhead, better access to capital markets, and the ability to attract institutional investor attention. But the disadvantages are often underappreciated: as a portfolio grows, the marginal acquisition becomes harder to find, the geographic diversification can dilute local market expertise, and the organizational complexity of managing hundreds of properties across dozens of states can introduce bureaucratic inefficiency. PECO's current size of roughly 300 properties appears to be in the sweet spot — large enough to command scale advantages and institutional recognition, but small enough that every property still gets meaningful attention from the operating platform.

Tenant relationships function as a genuine competitive moat, though a subtle one. When Kroger needs a landlord to accommodate a store expansion, add curbside pickup infrastructure, or co-invest in a facade renovation, they turn to operators they trust — companies with a track record of responsiveness, flexibility, and fair dealing. PECO's three-decade history of working with the same grocer partners creates the kind of institutional relationship that a new entrant cannot replicate quickly.

The August 2024 upgrade from S&P Global Ratings — moving PECO from BBB- to BBB with a stable outlook — was a significant milestone. Investment-grade credit ratings unlock access to the unsecured bond market at more favorable rates, reduce borrowing costs across the capital structure, and signal balance sheet credibility to institutional investors. The spread between a BBB and a BBB- issuer can translate into tens of millions of dollars in annual interest savings on a $2.4 billion debt load.

The termination of the Kroger-Albertsons merger in December 2024 — blocked by a federal district court on antitrust grounds — was widely viewed as a net positive for PECO.

The $24.6 billion proposed combination would have created a grocery behemoth with the leverage to pressure landlords on rent concessions and potentially consolidate overlapping store locations. Kroger and Albertsons/Safeway together represent roughly 8 to 9 percent of PECO's annual base rent — a meaningful concentration that would have been amplified by a merged entity's enhanced bargaining power.

As separate, competing companies, both Kroger and Albertsons have stronger incentives to invest in their existing store networks and maintain favorable lease terms with landlords like PECO. The post-merger fallout has been messy — Albertsons sued Kroger for failing to adequately pursue regulatory approvals and sought the $600 million termination fee plus billions in damages, while Kroger countersued in March 2025 — but the competitive dynamics that result from two independent grocery giants fighting for market share are generally constructive for the landlords who provide their physical footprint.

PECO has been notably disciplined in avoiding over-concentration with any single anchor tenant. No individual tenant represents more than about 6 percent of annual base rent, and only eight tenants exceed 1 percent. This diversification within the grocery-anchored category provides a buffer against idiosyncratic tenant risk — if any single grocer stumbles, the portfolio-level impact is contained.

IX. Business Model Deep Dive: How PECO Makes Money

The economics of a grocery-anchored REIT are deceptively simple on the surface but contain several non-obvious dynamics that are worth understanding.

Revenue comes from three primary sources. Base rent is the contractual monthly payment each tenant makes for the right to occupy their space — this is the largest and most predictable revenue stream. Expense reimbursements are the tenants' pro-rata share of property taxes, insurance, and common area maintenance costs, which PECO passes through under triple-net lease structures. Percentage rent, a smaller component, is additional rent some tenants pay when their sales exceed specified thresholds — more common with restaurant and specialty retail tenants than with grocery anchors.

The lease structure is the architectural foundation of PECO's business model. Most PECO leases are triple-net, meaning the tenant pays not just rent but also their share of property taxes, insurance, and common area maintenance. This effectively shifts operating cost inflation from the landlord to the tenant — when property taxes rise or insurance premiums increase, the tenant absorbs those costs, not PECO. Anchor leases typically run 10 to 25 years with multiple renewal options, providing long-term visibility into the income stream. Inline leases run shorter — typically 5 to 10 years — but command significantly higher rents per square foot.

The math of REIT investing revolves around a set of metrics that differ from traditional corporate finance. Net operating income, or NOI, is the property-level revenue minus operating expenses — the fundamental building block. Funds from operations, or FFO, adjusts GAAP net income by adding back real estate depreciation and amortization (since buildings do not actually lose value the way a piece of machinery does — in fact, well-maintained commercial real estate often appreciates). Core FFO strips out one-time items like acquisition costs or severance payments to reveal the underlying earnings power. Adjusted FFO, or AFFO, further deducts maintenance capital expenditures to approximate the true free cash flow available for dividends.

In 2025, PECO generated Core FFO of $360.7 million, or $2.60 per diluted share — a 7 percent increase over the prior year. Total revenue reached $726.6 million. Same-center NOI of $454.7 million grew 3.8 percent. These numbers illustrate the operating leverage inherent in the model: because most of PECO's costs are fixed (interest expense, corporate overhead, property-level staffing), incremental revenue from rent escalators and occupancy gains flows through to NOI and FFO at high margins.

For readers unfamiliar with REIT metrics, here is the simplest way to think about it: NOI is the profit generated by the properties themselves, before corporate overhead and financing costs. FFO is the company-level profit adjusted for the accounting fiction that buildings depreciate (they often do not — well-maintained shopping centers frequently appreciate in value). And the cap rate — the ratio of NOI to property value — is the yield an investor earns on the real estate. When PECO buys a property at a 7 percent cap rate using capital that costs 5 percent, the 2 percent spread is where value gets created. The entire acquisition strategy revolves around maintaining a positive spread between the yield on acquired assets and the cost of the capital used to buy them.

The grocery anchor rent dynamic is one of the most counterintuitive aspects of the business. Grocery stores typically pay below-market rent on a per-square-foot basis — often $8 to $12 per square foot compared to $20 to $40 for inline tenants. At first glance, this looks like a bad deal for the landlord. But the grocer is not paying for space alone — they are paying for the right to anchor a center, and the landlord is accepting below-market rent in exchange for the traffic generation that allows inline tenants to pay premium rents. The blended economics work: the grocer occupies perhaps 40 percent of the square footage but generates the traffic that supports the remaining 60 percent at much higher rents. This is why the small shop strategy — maximizing inline occupancy and releasing spreads — is the primary lever for revenue growth.

The REIT structure itself imposes a distinctive financial discipline. To qualify for favorable tax treatment, a REIT must distribute at least 90 percent of its taxable income as dividends to shareholders. This means PECO cannot retain earnings the way a traditional corporation can — almost all cash flow gets paid out. Growth capital must come from external sources: equity offerings, debt issuance, asset sales, or joint venture partnerships. This structural requirement makes capital allocation decisions — and the cost of capital — existentially important for REITs in a way that does not apply to companies that can fund growth from retained earnings.

Capital expenditures divide into two categories: maintenance capex (keeping existing properties in good condition) and value-add capex (repositioning spaces, adding outparcels, modernizing facades). Maintenance capex is a cost of doing business — think parking lot resurfacing, HVAC replacements, roof repairs. Value-add capex is an investment that should generate returns above the cost of capital — think converting a vacant big-box space into three smaller inline suites, or building a pad site for a Starbucks drive-through on an underutilized corner of the parking lot. PECO's 2025 investment of $53.8 million across 23 development and redevelopment projects, generating returns meaningfully above its weighted-average cost of debt, illustrates the disciplined approach to value-add spending.

The key insight for investors is that the REIT structure creates a business where capital allocation is the primary strategic lever. Because 90 percent of taxable income must be distributed, management cannot hoard cash or build up a war chest for a rainy day. Every dollar of growth capital must be raised externally — through equity offerings that dilute existing shareholders, debt issuance that adds leverage, or asset sales that shrink the portfolio. This means the cost of capital is not just a financial metric but a strategic constraint: PECO can only grow accretively when the yield on new acquisitions exceeds the blended cost of the capital used to fund them. When the stock price is high and debt is cheap, the math works beautifully. When the stock price is depressed and rates are elevated, growth slows. This structural dynamic explains why REIT management teams talk about cost of capital more than almost any other topic.

X. Strategic Analysis: Moats, Powers, and Competitive Dynamics

Understanding PECO's competitive position requires examining the structural forces that shape the grocery-anchored shopping center industry. Rather than cataloging each force in isolation, the picture that emerges is one of moderate but durable defensibility in a capital-intensive industry.

The barriers to entry in grocery-anchored retail real estate are surprisingly high despite the apparent simplicity of the product. Building a new shopping center requires zoning approvals (which can take years and face fierce community opposition), environmental reviews, infrastructure investment, and — most critically — a grocery anchor tenant willing to commit to a long-term lease before construction begins. The dominant grocers in any given market have well-established store networks and are reluctant to add locations that cannibalize existing sales. This means that the most attractive trade areas — affluent suburban neighborhoods with high household density and limited existing grocery supply — are effectively closed to new development. The scarcity of prime grocery-anchored locations in high-density, high-income areas is a genuine, if partial, resource barrier.

Tenant bargaining power operates on a spectrum. Grocery anchors wield significant leverage — PECO needs them more than they need any single landlord — which is why anchors pay below-market rent. National chain tenants like Starbucks or Anytime Fitness can negotiate across portfolios, comparing lease terms at PECO properties to those offered by Regency or Brixmor. But local tenants — the independent dentist, the family-owned restaurant, the neighborhood tax preparer — have much less bargaining power and face high switching costs. A dentist who has built a patient base around a specific location cannot easily relocate without losing patients. This creates stickiness that supports high renewal rates and positive releasing spreads.

The substitute threat from e-commerce has been the defining strategic question for a decade. The answer, at least for now, is clear: online grocery penetration has grown but remains a modest share of total grocery spending, and most online grocery orders still involve a trip to a physical store for curbside pickup. Fresh produce, meat, dairy, and prepared foods resist the frictionless delivery model that works for books and electronics. The more meaningful substitute threat comes from "dark stores" — warehouse-style facilities used exclusively for online order fulfillment — but these have struggled economically, as evidenced by the contraction of rapid grocery delivery startups in 2022-2023.

Where PECO's competitive advantages are most visible is in what Hamilton Helmer's framework would call process power and switching costs. The process power manifests in PECO's proprietary underwriting methodology — the Power Score and Gold Score algorithms refined over three decades of acquisition activity — and in the integrated property management platform that produces measurably better operating outcomes than fragmented private ownership. This is not the kind of advantage that can be copied by reading a manual; it is embedded in systems, relationships, and institutional knowledge accumulated over fifteen-plus years of focused execution in a single property type.

The switching costs for established tenants are real and measurable. A Kroger that has operated in a PECO center for fifteen years — investing millions in store buildout, building customer loyalty, optimizing its supply chain for that specific location — faces enormous costs to relocate. The same logic applies, at a smaller scale, to inline tenants. These switching costs support the 97-plus percent occupancy rates and the 20-plus percent renewal releasing spreads that drive PECO's organic growth.

The counter-positioning power that characterized PECO's early years — buying grocery-anchored strip centers when institutional investors dismissed them as commodity assets — has diminished as the thesis became consensus. Today, grocery-anchored shopping centers are widely recognized as resilient, attractive assets. Cap rates have compressed. Competition for acquisitions has intensified. The pricing gap that Edison and Phillips exploited in the 2010s is narrower, though PECO's sourcing capabilities and grocer relationships still provide some advantage in accessing off-market deals.

Competitive rivalry in the sector is moderate to high. PECO competes with Regency, Brixmor, Kimco, and hundreds of private owners for acquisitions, and this competition compresses yields on acquired properties. Differentiation comes through operational execution and tenant relationships rather than product differentiation — one grocery-anchored strip center looks much like another from a tenant's perspective. The most meaningful source of competitive advantage may be the simplest: PECO does one thing, has done it for three decades, and does it better than operators who split their attention across multiple property types.

The overall strategic assessment is that PECO operates with moderate but durable moats. This is not a software business with zero marginal costs and winner-take-all network effects. It is a capital-intensive, asset-heavy business where returns are earned through disciplined underwriting, operational excellence, and patient compounding. The strongest competitive advantages — the proprietary underwriting algorithms refined over 500-plus acquisitions, the integrated management platform, the three-decade grocer relationships — are real but not impregnable. Any well-capitalized competitor with patience and talent could theoretically build something similar. The question is whether they would want to: the returns in grocery-anchored strip centers are steady but not spectacular, which means the business attracts operators who value durability over disruption. That self-selection dynamic may be the most underrated moat of all.

The scale economics question is worth dwelling on. PECO's internal property management platform — leasing, maintenance, accounting, vendor management — creates per-unit cost advantages as the portfolio grows. A 300-property platform can spread corporate overhead, technology investments, and senior management compensation across far more revenue-generating units than a 30-property platform. Purchasing power with landscaping contractors, paving companies, and HVAC vendors improves with scale. But there are limits: real estate is fundamentally local, and the leasing agent in suburban Atlanta gains no benefit from PECO's scale in suburban Phoenix. The optimal scale for a grocery-anchored REIT may be smaller than the optimal scale for a data center or industrial logistics REIT, where standardization and national tenant relationships create more pronounced scale advantages.

Network effects are minimal in traditional real estate ownership, but PECO has built a modest data network effect. Every acquisition, every lease renewal, every tenant bankruptcy, and every trade area demographic shift feeds the proprietary analytics that inform the next underwriting decision. After 500-plus transactions, PECO's database of grocery-anchored center performance data is arguably the most comprehensive in the industry. This informational advantage compounds over time and is difficult for new entrants to replicate.

XI. Bull Case, Bear Case, and Investment Considerations

The investment case for Phillips Edison rests on several structural arguments. Grocery stores have proven remarkably resistant to e-commerce disruption, and the major chains are investing billions in omnichannel capabilities that strengthen rather than diminish the value of physical store locations. Demographic trends favor the suburban, affluent communities where PECO concentrates its portfolio. Service and experiential tenants — fitness, healthcare, restaurants — are growing categories that require physical space. The portfolio's 83 percent concentration in properties anchored by market-dominant grocers provides a quality floor. Embedded rent growth from below-market leases and contractual escalators creates organic revenue expansion. And the dividend yield of approximately 3.5 percent, paid monthly and growing at more than 5 percent annually, offers an attractive income proposition.

The operational metrics support the thesis. Inline occupancy reached a record 95.1 percent in Q4 2025. New lease rent spreads came in at 30.9 percent for the full year, meaning new tenants are paying nearly a third more than outgoing tenants for the same space. Core FFO per share has grown at a 7 percent compound rate since the IPO. Five consecutive dividend increases total more than 20 percent of cumulative growth.

On the other side of the ledger, the bear case starts with interest rates. REITs are capital-intensive businesses that rely on debt financing, and periods of rising rates compress REIT valuations while increasing borrowing costs. PECO's weighted-average interest rate of 4.4 percent and 95 percent fixed-rate debt profile provide near-term insulation, but the $350 million in notes priced in February 2026 at 4.750 percent illustrate the higher cost of new capital relative to debt originated during the era of near-zero rates.

The e-commerce acceleration scenario, while not imminent, remains a structural overhang. If Amazon, Instacart, or a next-generation competitor cracks the unit economics of last-mile grocery delivery at scale, the traffic-generation thesis that underpins inline tenant economics could weaken. Amazon Fresh, despite setbacks, continues iterating. Autonomous delivery vehicles and robotics could change the cost structure of home delivery. The thesis is strong today, but "today" is not "forever."

Geographic concentration creates weather, economic, and regulatory risk. Heavy exposure to Sun Belt markets — Florida, Texas, Georgia — means that a severe hurricane season, a regional recession, or changes in state tax policy could disproportionately affect the portfolio. Similarly, while PECO's tenant base is diversified (only eight tenants represent more than 1 percent of annual base rent), the anchor tenant concentration in a handful of grocery chains means that operational distress at Kroger or Albertsons would reverberate across the portfolio.

Valuation is a persistent debate. PECO trades at approximately 13.4 times forward FFO, a premium to Brixmor's roughly 11.4 times but below Regency's and Kimco's multiples. Whether this premium to some peers is warranted depends on one's view of the durability of PECO's same-center growth, the quality of its portfolio, and the terminal value of pure-play grocery-anchored real estate.

The growth runway question is worth flagging. PECO has identified approximately 5,800 properties nationally that meet its acquisition criteria, and it currently owns around 300. The whitespace is large — PECO owns roughly 5 percent of its addressable market, which is an unusually low penetration rate for a public company in a mature industry. But the pace of acquisition is constrained by capital availability, competitive pricing, and the discipline not to sacrifice quality for growth. As cap rates compress and competition intensifies, the accretion math on new acquisitions gets harder.

There is also a material legal and regulatory consideration to monitor. As a REIT, PECO must comply with complex tax rules governing the structure of its income, assets, and distributions. Any failure to meet REIT qualification tests could trigger a loss of tax-advantaged status, forcing the company to pay corporate income taxes and potentially eliminating the dividend tax advantage that makes REITs attractive to investors. While this risk is theoretical for a well-advised company like PECO, it is a structural feature of the REIT model that investors should understand. Additionally, environmental regulations governing the remediation of contaminated properties, the Americans with Disabilities Act requirements for commercial buildings, and evolving local zoning codes all create ongoing compliance costs and occasional surprises that can affect property-level economics.

For investors tracking PECO's ongoing performance, two key performance indicators stand above the rest. Same-center NOI growth is the single best measure of whether the existing portfolio is generating increasing value — it captures the combined effect of rent escalators, releasing spreads, and occupancy changes, and it strips out the noise of acquisition activity. Inline occupancy is the leading indicator that predicts future same-center growth, because every hundred basis points of inline occupancy gained translates into high-margin revenue from tenants paying $20-plus per square foot. If same-center NOI growth holds above 3 percent and inline occupancy continues climbing from its current record of 95.1 percent, the compounding machine is working. If either metric deteriorates, something has changed in the fundamental demand for grocery-anchored neighborhood retail.

XII. Lessons for Founders and Investors: The Playbook

The Phillips Edison story contains a set of principles that extend well beyond real estate investing.

The contrarian timing lesson is perhaps the most valuable and the hardest to implement. Jeff Edison and Mike Phillips did not start buying grocery-anchored strip centers because they were popular — they started because they were despised. The best time to invest in an asset class is when conventional wisdom has written it off, prices are depressed, and the sellers are motivated. The 2009-2010 vintage of PECO's acquisitions generated extraordinary returns precisely because nobody else wanted to touch retail real estate during the financial crisis. This principle applies across industries: the best founders start companies when the macro environment looks worst for their category, not when it looks best.

The discipline of pure-play focus runs counter to every instinct of empire-building. As PECO grew, the temptation to diversify was constant — into office buildings, into industrial properties, into mixed-use developments, into enclosed malls that could be acquired at distressed prices. Edison resisted every one of these temptations, maintaining an almost monastic commitment to a single property type. This focus created the expertise, the operating platform, and the grocer relationships that constitute PECO's competitive advantage. The lesson: specialization compounds. Doing one thing for thirty years creates advantages that cannot be replicated by doing ten things for three years each.