PDD Holdings: The "Costco + Disney" Disruptor

I. Introduction: The $200 Billion Stealth Fighter

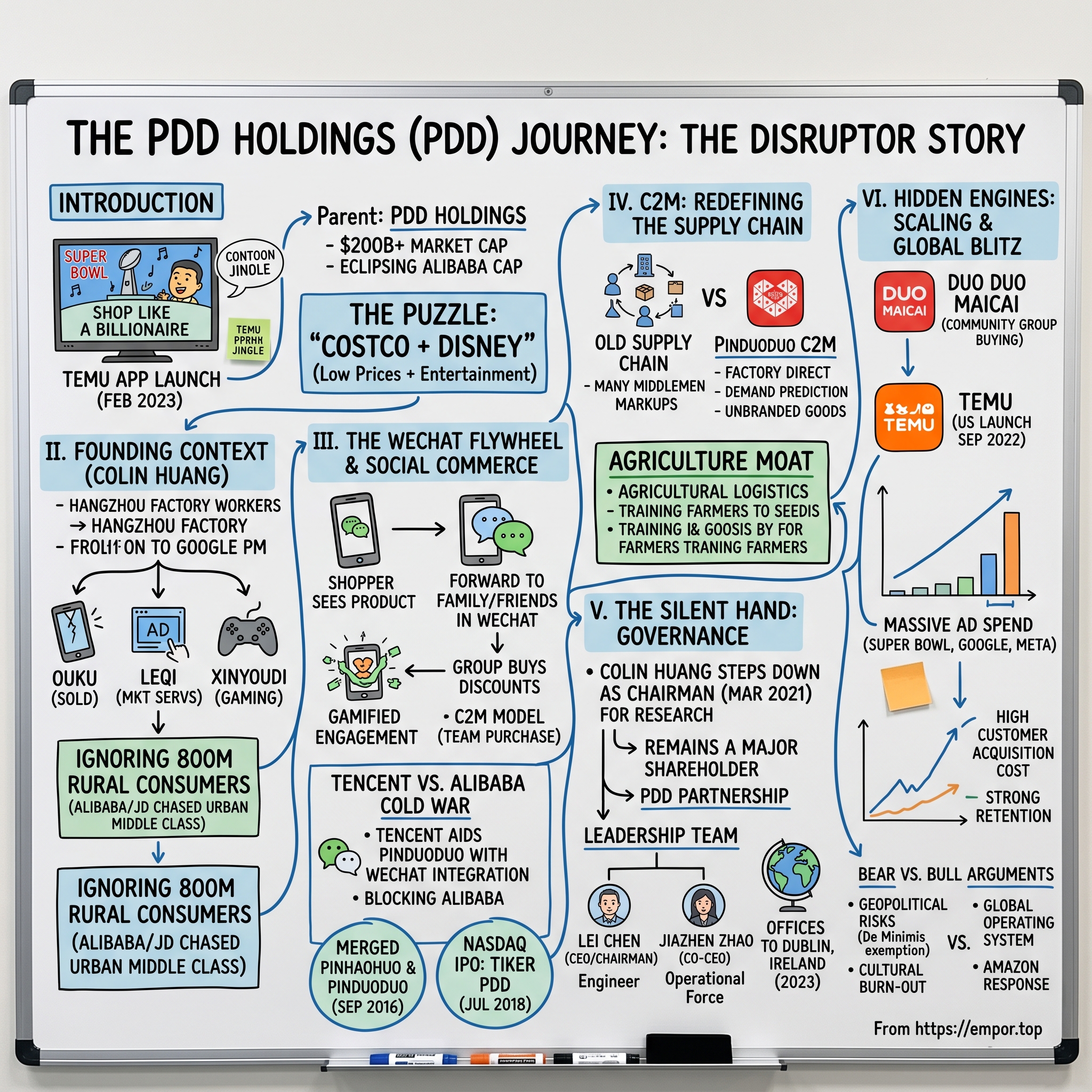

Picture the scene in February 2023. Forty-two million Americans were sprawled on couches, beers in hand, watching Patrick Mahomes dismantle the Eagles in Super Bowl LVII. Somewhere between a Bud Light spot and an Avocados From Mexico gag, a cartoon jingle burrowed into the cultural subconscious. "Shop like a billionaire." The ad was for Temu, an app most viewers had never opened, owned by a parent company most viewers had never heard of, listed on NASDAQ under a three-letter ticker that sounded like a typo: PDD.

Thirty minutes and roughly $14 million of ad spend later, Temu was the most-downloaded free app on the US App Store. Within a week it had displaced Amazon, Walmart, and TikTok at the top of the charts. Within a year it would be advertised across five more Super Bowl spots and lodged in the phones of about 50 million Americans. And the parent company behind it, a Shanghai-bred platform founded only in 2015, would briefly eclipse Alibaba in market capitalization—crossing north of $200 billion and becoming, by one measure, the most valuable Chinese internet company on the planet.

Here is the puzzle. Alibaba had spent twenty years and tens of billions of dollars building an empire that everyone, including Jack Ma, believed had locked up Chinese e-commerce. JD.com had spent another decade building the Amazon of China. Tencent owned the social graph. The game was supposed to be over. And yet, quietly, through the basement of WeChat chat groups and the neglected streets of fourth-tier Chinese cities, a founder named Colin Huang built a company that today processes more orders per day than Amazon's global marketplace. The prospectus he filed in 2018 described the platform with a now-famous phrase: "Costco plus Disney." Low prices and entertainment. A mall you played games inside of.

The thesis of this episode is simple. PDD Holdings did not out-execute Alibaba. It counter-positioned against Alibaba. It took a market that sophisticated investors considered closed, identified an ignored customer segment, built a shopping experience that the incumbents structurally could not copy, and then—once the playbook had been refined—ported the entire machine to the rest of the planet under a new brand. Its "Team Purchase" model was not a feature; it was a new unit of retail demand, the first meaningful one since Amazon Prime welded free shipping to subscription psychology in 2005.

Over the next roughly two and a half hours of reading, we will trace the arc from Colin Huang's fruit-selling app in Shanghai to the Ireland-based holding company remitting orders from Guangdong factories to doorsteps in Boise. We will dig into who really runs PDD today (hint: it is not the man on the cover of Forbes), unpack the economics of a customer acquisition cost that scared even Meta's own ad team, and examine why this "cheap stuff" company might be the most interesting case study in industrial strategy since Walmart discovered the satellite. By the end, the Super Bowl jingle may still annoy you. But you will understand why it worked.

II. Founding Context: The Serial Entrepreneur

Most Chinese tech founding stories have a garage, or a dorm room, or a cramped Beijing apartment where someone codes by the light of a desk lamp. PDD's origin story has none of that. It has a hedge fund office in New York, a stint as a product manager for Larry Page, and a young man named Huang Zheng—Colin to the Americans he worked with—who had already become quietly, extraordinarily wealthy before he ever thought about selling fruit.

Huang grew up in Hangzhou in the 1980s, the son of two factory workers. The biographical details he has shared are spare but telling. His mother worked a production line. His family was, by his own description, "poor but not destitute." He tested into Hangzhou Foreign Language School, which funneled him to Zhejiang University, which in turn sent him to the University of Wisconsin-Madison for a master's in computer science. Along the way, a chance introduction linked him to Duan Yongping—the legendary Chinese investor and founder of BBK Electronics, the holding company that eventually spawned Oppo, Vivo, and OnePlus. Duan took Huang to a now-famous charity lunch with Warren Buffett in 2006, when Huang was twenty-six. That relationship mattered. Duan would later seed Huang's companies, and the Buffett influence shows up in Huang's letters to shareholders, which read like someone who has actually read the Berkshire annuals rather than merely quoting them.

After Wisconsin, Huang landed at Google in 2004, just as Page and Brin were taking it public. He spent three years as a product manager, joined the team that launched Google China in 2006, and left in 2007 when he decided that neither climbing the corporate ladder nor sitting on post-IPO equity interested him. What did interest him was shipping things. He went home to Shanghai and, over the next eight years, built three companies that taught him three very specific lessons.

The first was Ouku, an e-commerce site for consumer electronics launched in 2007. Ouku was small, competent, and completely overrun by the Alibaba juggernaut. Huang sold it in 2010 for a modest sum and learned his first lesson: competing with Alibaba on Alibaba's own terms was a death sentence. The second was Leqi, an e-commerce marketing services firm that helped foreign brands sell into Tmall. Leqi taught Huang the seams of Alibaba's merchant relationships—specifically, how much Alibaba extracted from sellers in advertising fees, and how brittle the "branded mall" model became once sellers started seeking alternatives. The third was Xinyoudi, a mobile gaming company that at one point employed several hundred people and produced a steady stream of casual social games on WeChat. Xinyoudi taught Huang the grammar of gamified engagement on mobile—streaks, group invites, limited-time offers—which would later become the genetic code of Pinduoduo.

By 2014, Huang had banked enough wealth to retire several times over. He was thirty-four. He had a small team, three cash-flowing businesses, and a recurring medical problem with his ears that gave him long stretches of bedridden time to think. What he thought about, in those months, was a thesis. The "consumption upgrade" narrative that animated Alibaba and JD.com was aiming at a Chinese middle class of roughly 200 million urban professionals. But China had a billion people. The other 800 million—rural, small-city, grandparent-headed households with modest disposable incomes—were being systematically ignored by the e-commerce giants. Alibaba's Tmall was chasing LVMH. JD was chasing Apple. Nobody was chasing the retiree in Anhui province who wanted a dozen mangoes for seven yuan and did not care whether the app had a Material Design interface.

In 2015, Huang spun out two new ventures from Xinyoudi. One, Pinhaohuo, sold fruit directly to consumers in group-buy format inside WeChat. The other, Pinduoduo, was a broader marketplace—a Taobao-like bazaar where shoppers assembled into teams to unlock bulk pricing. Neither was a lightning bolt. Both were, at first, dismissed as gimmicks. Huang himself has described the early months as "chaotic and underestimated." But the two ideas sat on top of a structural asymmetry nobody else was exploiting: WeChat's one-billion-user social graph, and the enormous overhang of unsold factory production in Guangdong and Zhejiang that could not find its way to the Alibaba-dominated digital shelf.

The calculated architect had found his inefficiency. And he had, crucially, not told anyone it was an inefficiency.

III. The WeChat Flywheel and Social Commerce

The single most important thing to understand about Pinduoduo's early years is that it was not really an app. It was a WeChat feature. From 2015 through 2018, the vast majority of orders originated inside Tencent's messenger—specifically, inside family chat groups, village chat groups, and the sprawling WeChat Moments feed that functioned as the Chinese equivalent of Facebook. A shopper would see a product she liked. She would see a price, say thirty yuan. Below that price she would see a second, lower price, say eighteen yuan, available if she could round up one other person to buy the same product. She would then forward the link to her family group chat, her neighbor, her daughter. If anyone clicked and bought, the discount unlocked. The deal closed.

Nothing about this was technologically novel. Groupon had done group-buying a decade earlier. Taobao had had social sharing features forever. What was novel was the psychological reframing. The discount was not a coupon; it was a reward for recruiting. The shopping act became indistinguishable from the messaging act. And because WeChat's API allowed lightweight mini-programs to render inside a chat, you could complete a purchase without ever leaving the conversation. The friction between "I am talking to my cousin" and "I have bought mangoes" collapsed to roughly three taps.

This is why the Costco-plus-Disney label, which Huang wrote into the 2018 prospectus, was more than a marketing flourish. Costco is a bulk-buying mechanism that delivers lower unit prices because it aggregates demand. Disney is an entertainment format that holds attention through serial engagement. Pinduoduo wove them together. The aggregation was social. The entertainment was the feeling, reinforced by little coin drops and confetti animations, that shopping was a game you were playing with your family rather than a transaction you were completing by yourself. It was retail as group chat. And it was enormously, unexpectedly, structurally sticky in a demographic that Alibaba had decided was not worth designing for.

The numbers moved with a speed that embarrassed the analysts who had written Pinduoduo off. By the end of 2015, the platform had roughly 10 million users. By the end of 2016, it had over 100 million. By mid-2018, when Huang filed the S-1 ahead of a NASDAQ listing, the company reported 343 million annual active buyers—already more than JD.com, and closing on Alibaba's Taobao. And it had gotten there by spending roughly a third of what Alibaba had spent to acquire comparable users, because Tencent, which had taken a stake in Pinduoduo in 2016, was effectively subsidizing distribution by refusing to let Alibaba link into WeChat.

The Tencent-Alibaba cold war is worth pausing on, because it is load-bearing for PDD's story. Jack Ma and Pony Ma—no relation, but forever confused in Western press—had spent years building moats against each other. Alibaba blocked Tencent's payments product, WeChat Pay, from working in Taobao. Tencent, in retaliation, blocked every Alibaba-branded link from sharing inside WeChat. The effect was that Alibaba, the largest e-commerce platform in the world, was structurally denied access to the largest social graph in the world. Pinduoduo walked into that gap. Tencent put in equity in 2016 and again at IPO, Pinduoduo got unimpeded WeChat integration, and Alibaba could only watch as its best growth vector for the next 400 million users was cut off behind barbed wire it had helped erect.

The first inflection point came in September 2016, when Huang merged the fruit-focused Pinhaohuo and the broader Pinduoduo marketplace into a single platform. This was a chess move disguised as a housekeeping decision. Groceries, and specifically fruit, are the highest-frequency consumer purchase in most households. Merging them into the marketplace meant that shoppers had a reason to open the app several times a week, not monthly, and each open exposed them to higher-margin discretionary goods. Frequency built habit. Habit built distribution. Distribution meant that when, in 2017, Pinduoduo began onboarding household goods, apparel, and consumer electronics at a rapid clip, the users were already there.

The second inflection came on July 26, 2018, when Pinduoduo listed on NASDAQ under the ticker PDD. The company raised $1.6 billion at a fully diluted valuation of roughly $24 billion, priced at the top of its range. Huang, wearing a crisp white shirt rather than the more conventional IPO suit, rang the opening bell remotely from Shanghai. The stock popped roughly 40 percent on the first day. The financials were polarizing. Revenue had nearly tripled year-over-year. Losses had also tripled. The company was burning cash on subsidies and user acquisition at a rate that, to a Western analyst trained on unit economics, looked deranged. But buried in the prospectus was a line that the market slowly learned to take seriously: Huang described the company's marketing spend as "investment in platform fundamentals," not operating expense. The distinction mattered, because it signaled that PDD intended to keep losing money, on purpose, for years.

That conviction would be tested almost immediately. Within months of the IPO, JD.com launched Jingxi, a lookalike group-buy app targeting the same sinking market. Alibaba launched Taobao Tejia, a discount channel that ran on the same supply chain as Taobao. Both competitors outspent Pinduoduo on user subsidies. Both failed to dislodge it. The reason, which took the market a year or two to appreciate, brings us to the part of the story that most Western coverage still does not understand: the supply side.

IV. C2M: Redefining the Supply Chain

Here is a useful way to picture what PDD did to the Chinese supply chain. Imagine a factory in Dongguan that makes blenders. It has a thousand production workers, an owner who inherited the business from his father, and a single large customer—a Western brand that orders 100,000 units a quarter and slaps its own logo on every one. The factory earns maybe four dollars of margin per blender after the brand takes its cut. The factory owner has no idea who buys his blenders, no idea what features they want, and no way to sell directly even if he did, because he does not own a brand, a storefront, or a relationship with an end customer. He is, in the classical supply-chain sense, a ghost.

Pinduoduo's Consumer-to-Manufacturer model, known in the company as C2M, was designed to turn those ghosts into principals. The pitch to the factory was simple. Pinduoduo would aggregate demand for a product category—say, 10,000 confirmed buyers wanting a blender under 100 yuan—and hand that demand directly to the factory. The factory would produce against a confirmed order rather than a speculative forecast. The brand would be skipped entirely. The product would ship under a generic or Pinduoduo-native label. The factory would keep more of the margin. The consumer would pay less. Pinduoduo would take a thin slice of the transaction.

Stated that way, C2M sounds like a classic wholesale-to-retail disintermediation. But the operational reality was messier and more interesting. To make it work, Pinduoduo had to build a demand prediction engine that could tell factories, with reasonable accuracy, how many units to make. It had to build quality control systems so that the blenders did not explode on arrival. It had to build a logistics layer that could move unbranded goods from interior factory parks to rural consumers without relying on the branded carriers that JD owned. And it had to convince factory owners, most of whom had spent thirty years being bullied by export brokers, that this upstart platform would not simply squeeze them the same way Alibaba had squeezed its merchants.

The convincing was easier in agriculture, which is where PDD made its most distinctive operational bet. Chinese agriculture is a supply chain disaster. Hundreds of millions of smallholder farmers, most operating plots of less than two acres, produce fruit and vegetables that historically wind their way through four to six intermediaries before reaching a city supermarket. The markups accumulate. The produce spoils. By the time the mango reaches the consumer, it has been marked up 500 percent and lost half its shelf life. Pinduoduo's team, starting with the Pinhaohuo fruit operation and eventually expanding into a full agricultural supply platform, went into villages and trained farmers directly. They set up collection points. They aggregated orders from urban consumers and routed them to specific farms. They cut the intermediaries from six to two. They digitized inventory, scheduling, and quality grading in places that had never seen a smartphone-based business process before.

This was not a tech story. This was a boots-on-the-ground, bad-roads, rural-logistics story. It was heavy, unglamorous work that Alibaba and JD were structurally disinclined to do, because their supply chains were optimized for urban fulfillment and branded manufacturing. And it produced a moat that has turned out to be one of the most durable in Chinese consumer internet. By 2022, PDD was the largest agricultural e-commerce platform in China, responsible for over $100 billion in annualized GMV of fresh produce. The farmer in Anhui who once sold mangoes to a local broker was now shipping to a grandmother in Shanghai via PDD's logistics network, and cutting three middlemen out of the chain.

The segmentation inside PDD's financials hints at how far this has gone. The company historically reported its business in two main buckets: online marketing services, which is the advertising revenue that merchants pay to appear in search results and feeds; and transaction services, which is the take rate on payments and the fees associated with logistics and fulfillment. In the 2023 annual report, online marketing services still accounted for the larger share, but transaction services were the faster-growing segment, reflecting the rise of Temu and the increasing monetization of the full-stack logistics operation. In plain English: PDD was transitioning from a pure advertising platform, like Alibaba, into a full-service commerce rail, like Amazon. That rail, built on the bones of the C2M model, is what it would eventually rent out to the world.

V. The Silent Hand: Governance and the Men Behind the Curtain

On March 17, 2021, at 7:30 a.m. Shanghai time, Pinduoduo published a shareholder letter that, on first read, sounded like a retirement announcement. Colin Huang, aged forty-one, was stepping down as chairman. He was leaving the board. He was, in his own words, retreating to pursue research in "food science and life sciences." He framed the decision with characteristic understatement. "A company's DNA shapes its destiny," he wrote. "I am gladder to step back and let the next generation take it forward." The Wall Street reaction was swift and binary. The stock dropped roughly 7 percent. Analysts wrote up notes asking whether China's most successful self-made billionaire of the decade was really walking away at the peak.

To understand what actually happened, you have to rewind to late 2020. That was the season Jack Ma gave the speech in Shanghai criticizing Chinese financial regulators, the Ant Group IPO got suspended, and Beijing's tech crackdown began in earnest. Within three months, Didi's CEO had been scolded, Tencent's gaming division had been reined in, and "common prosperity" had become the operating mantra of every policy document coming out of Zhongnanhai. Founders with too much personal profile became political liabilities overnight. Huang, whose personal stake in Pinduoduo had briefly made him the second-richest person in China, read the room faster than most. He had already relinquished the CEO title in July 2020, handing it to Lei Chen. In March 2021, he gave up the chair as well. By the time the crackdown peaked, Huang was, on paper, just a large shareholder with no formal role.

The "retiring to do research" narrative was not entirely for show. Huang has, by all available reporting, been spending time on life-sciences investing and academic pursuits in the years since. But the more operationally important story is that Huang did not actually give up control. He remained the largest shareholder, with a stake of roughly 26 percent. And the company's governance structure, similar to Alibaba's "Partnership" model, concentrates strategic and personnel authority in a small inner circle whose membership and voting rules are not fully transparent to outside shareholders. The "PDD Partnership" is the shadow owner of the company's direction, and it is the vehicle through which Huang's influence, formal or otherwise, continues to shape the business.

The men running the day-to-day deserve more attention than they usually get. Lei Chen, who took over as CEO in 2020 and became chairman in 2021, is an engineer by training and temperament. He holds a master's degree in computer science from the University of Wisconsin-Madison, joining PDD in 2016 from a role at Google. Inside the company, he is known for running meetings in a bare conference room with no branding, no slides, and a whiteboard. He famously refuses to give media interviews. When he does speak publicly, it is almost always in the prepared remarks of an earnings call. His strategic instinct has been to double down on engineering—over 60 percent of PDD's employees are engineers—and to relentlessly flatten the organization so that decisions move faster than at any competitor.

The co-CEO, Jiazhen Zhao, was elevated alongside Chen in March 2023. Zhao is younger, blunter, and the operational force behind Duo Duo Maicai and the early Temu rollout. She joined PDD in 2018 after stints at Hudson Education and is the first female co-CEO of a major Chinese internet platform. Inside the company, her reputation is for being the person who actually makes the trains run on time. She is credited with driving Temu's warp-speed entry into the US market in 2022 and with holding the line on the C2M model as Temu expanded into over 70 countries.

The culture these two lead is not for everyone. PDD's internal norms have come to be known, even among China's notoriously intense tech companies, as "hardcore." Employees at the Shanghai headquarters reportedly work on a schedule that exceeds even the infamous 996—a reference to 9 a.m. to 9 p.m., six days a week. LatePost, one of China's best business publications, ran a long investigation in 2022 documenting a culture of mandatory late nights, a fanatical focus on metrics, and a compensation structure that is generous at the top end but punishing for underperformance. Two deaths of young employees in the early months of 2021—one a 22-year-old woman who collapsed on her walk home after midnight, the other an engineer who took his own life shortly thereafter—triggered a wave of public criticism. PDD apologized. It did not, notably, meaningfully change the schedule.

The final governance move, and arguably the most strategically brilliant, was the company's quiet shift of its principal executive offices to Dublin, Ireland, completed in early 2023. On paper, PDD Holdings is incorporated in the Cayman Islands—the default for Chinese companies listed offshore—and maintains its operating headquarters in Shanghai. But the "Ireland move" created a secondary center of gravity in the European Union, with real tax and regulatory implications. It positioned Temu to argue that it is not a Chinese company but a global one. It allowed PDD to tap into Ireland's competitive corporate tax regime and the EU single market simultaneously. And it telegraphed to Washington, well before the 2024 trade hearings, that PDD was prepared to shape-shift faster than any regulator could keep up with. Whether that convinces anyone long-term is another question, and one we will return to in the bear case.

The point, for now, is this. The Colin Huang exit was not an exit. It was a decoupling—of the founder's identity from the company, of the political risk from the operational risk, and of the Chinese center of gravity from the global ambition. With the machine in the hands of Chen, Zhao, and the Partnership, PDD was free to pursue two projects that would define the next chapter: groceries at home, and everything else abroad.

VI. Hidden Engines: Duo Duo Maicai and the Temu Blitz

If the first five years of Pinduoduo were about inventing a new kind of domestic retail, the five years that followed were about extending that invention across two very different frontiers. The first frontier was thirty miles from the user's home. The second was across the Pacific.

Start with Duo Duo Maicai, which launched quietly in August 2020. The concept was community group-buying, a model borrowed from several Chinese startups that had blown up on VC money during the 2018-2019 frenzy. A neighborhood resident, typically a stay-at-home mother or a local shop owner, would become a "group leader." She would collect next-day orders for groceries—rice, oil, vegetables, fresh meat—from her WeChat neighbors. Orders would close by 11 p.m. By 3 p.m. the next day, a refrigerated truck would deliver everything in bulk to the group leader's pickup point, and neighbors would walk over to collect. The model was brilliant because it solved the last-mile cost problem that had bankrupted a generation of Chinese grocery startups. Instead of building an Instacart-like shopper network, you had a voluntary community organizer who batched demand and accepted aggregated delivery.

By 2020, every major Chinese tech company was piling into community group-buying. Meituan had Meituan Select. Didi had Chengxin Youxuan. Alibaba had Taocaicai. Every one of them was losing billions a year. And then, predictably, Beijing dropped the hammer in late 2020 with a "nine no's" directive forbidding predatory pricing in groceries. Within 18 months, Chengxin Youxuan was in retreat. Meituan Select had cut scope. Alibaba had quietly deprioritized Taocaicai. Duo Duo Maicai, almost alone, survived and scaled. Why?

The answer is that PDD's Maicai operation was built on top of existing Pinduoduo infrastructure—the same logistics backbone, the same supplier relationships, the same C2M agricultural sourcing. The unit economics, from day one, were less awful than everyone else's because PDD was not building a grocery business from scratch; it was renting capacity from a business it already owned. By 2022, when the smoke cleared, Duo Duo Maicai was one of the top two community group-buying platforms in China, with a footprint spanning more than 200 cities. It has been the quietest, most underappreciated win in the PDD story—a business that, by some estimates, now generates tens of billions of yuan in annualized GMV and that the company has never broken out separately in its financials.

Now, the other frontier. In September 2022, Temu went live in the United States. The name comes from the phrase "Team Up, Price Down"—a direct port of the Pinduoduo social-shopping concept, albeit stripped of the WeChat group-buy mechanic because, obviously, Americans were not going to invite their cousins to buy pressure cookers together. What survived in the port was the supply-side story: cheap, direct-from-factory, unbranded goods, shipped via a cross-border logistics model that leveraged the De Minimis customs exemption to ship small packages from China to US doorsteps duty-free as long as the declared value was under $800.

The marketing spend that Temu unleashed to seed this operation was, and is, one of the most aggressive capital deployments in internet history. In its first full year of operation, Temu reportedly spent $1.7 billion on US advertising. The two Super Bowl appearances cost roughly $14 million each, plus production. Google and Meta reportedly told investors that Temu had become, at peak, the single largest ad buyer on their platforms. Customer acquisition costs in the early quarters were reportedly in the range of $30-$50 per first-time buyer—numbers that, at any other e-commerce company, would have triggered an immediate board intervention. At PDD, they triggered a nod and a request for more budget.

Why? The arithmetic is counterintuitive. Temu's gross margin per order, once you strip out shipping subsidies, is reportedly modest—perhaps in the teens as a percentage. Average order values in the first year were in the $25-$35 range. To recoup a $40 CAC at 15 percent gross margin, you need roughly ten orders from the customer. That requires retention that most e-commerce apps only dream of. And yet, based on publicly available third-party data, Temu's repeat-purchase rates have held up far better than skeptics expected. The dopamine loop—the spinning wheels, the timed discounts, the "free gift for your next friend"—ported across cultures better than anyone predicted.

The alternative path, which PDD considered and rejected, would have been to acquire one of the existing Western low-price players. Wish.com, the obvious target, had listed in December 2020 at an $17 billion valuation and then spent the next three years shedding 95 percent of its market cap as its logistics failed, its quality complaints piled up, and its US customers defected. By 2023, Wish was a zombie, ultimately selling itself to Qoo10 for a fraction of its IPO valuation. PDD, watching all of this, declined to buy any of it. Colin Huang's stated preference, echoed in internal communications and later interviews with company leadership, was that the company "does not buy companies; we build markets." Building Temu from scratch meant owning the code, the supplier relationships, the shipping integrations, and—crucially—the cost structure. Wish's problem was never its top line; it was that it had rented every piece of its operational stack and could not reduce its unit costs fast enough to survive. Temu, by contrast, was vertically integrated from day one.

The supply chain arbitrage underneath it all is the part that keeps Walmart's executives up at night. The same factories in Guangdong and Zhejiang that supply Pinduoduo's domestic marketplace now supply Temu's global one. The same demand-prediction software that tells a blender factory how many units to make for the Shanghai market now also slices in orders for Indianapolis. The same sparse-inventory, fast-ship, direct-from-factory logistics lane now spans three continents. In operational terms, Temu is not a separate business; it is an international distribution channel for the same C2M production engine that has been refining its efficiency for a decade inside China.

What Temu means for the global retail stack is something we are only beginning to measure. In the United States, Amazon responded in late 2024 by launching Amazon Haul, a low-price storefront explicitly designed to compete with Temu's price points. Shein, the other Chinese fast-fashion giant, accelerated its own cross-border buildout. Walmart quietly began experimenting with direct-factory sourcing for private label. The retail industry, which had spent twenty years arguing over whether Amazon was the final form of commerce, suddenly had a new reference point: a platform that could price goods at half of Amazon's, ship them in a week, and absorb user acquisition losses longer than any Western CFO would sanction. That, it turns out, is what happens when a company has decided that marketing is R&D.

VII. The Playbook: Seven Powers and Five Forces

Every company that earns a sustained return above its cost of capital does so because it has at least one durable source of power—a structural advantage that competitors cannot easily copy. Hamilton Helmer, in his book 7 Powers, enumerates seven of them. Most successful companies have one, maybe two. PDD has, arguably, four, and the way they interlock is the single best argument for why this company is not a flash in the pan.

The primary power is counter-positioning. Helmer defines counter-positioning as a position so asymmetric that the incumbent cannot adopt it without destroying its own existing business. Alibaba built Tmall as a high-end, branded mall. To copy Pinduoduo, Alibaba would have to embrace unbranded, low-margin, direct-from-factory goods—which would immediately dilute Tmall's brand-partner relationships and cannibalize the higher-margin transactions that fund the business. Alibaba did try, with Taobao Tejia and later Taobao Deals, but the attempt was half-hearted because the internal politics of cannibalization were impossible to resolve. PDD had no such constraint. It was born into the cheap-goods segment and had nothing to lose. That asymmetry is the foundation of everything else.

The second power is scale economies. The logistics density inside China, across both the core Pinduoduo marketplace and Duo Duo Maicai, means that incremental orders get served at incrementally lower cost. Outside China, Temu's cross-border shipping volume has grown to a scale where it can negotiate directly with carriers at rates that smaller rivals cannot touch. The agricultural supply chain, with its thousands of village-level collection points, has a fixed cost base that gets amortized across more orders every quarter. All of these are classic declining-average-cost curves, and they are the reason PDD's gross margins have steadily expanded even as the company has entered less-mature markets.

The third power is network effects, though with an important caveat. In the early Pinduoduo years, the social sharing of deals inside WeChat created a classic two-sided network: more buyers meant more incentive for sellers to list, which meant more deals, which attracted more buyers. That network effect has weakened as the platform has matured, because the marginal shopper today arrives via app download rather than via a friend's WeChat link. But the supply-side network effect—more merchants competing for more consumer spend—remains intact and has, if anything, strengthened as Temu has added a global demand layer on top of the same Chinese supply base.

The fourth power is process power. This is the one analysts most often miss. The demand-prediction engine, the factory onboarding playbook, the last-mile logistics coordination, the dopamine-loop app design—all of these are processes that have been refined over a decade of iteration inside the PDD organization. A competitor cannot buy them off the shelf. They have to be built, and building them requires a decade of operational learning and a culture that tolerates the mistakes along the way. The hardcore culture inside PDD, for all its human cost, is the organizational expression of this power.

Porter's five forces gives us another useful lens. The bargaining power of suppliers, in PDD's case, is strikingly low. The company treats factories as service providers rather than strategic partners. A blender factory that does not accept a given price is replaced by another blender factory, of which there are many, in a landscape of excess Chinese manufacturing capacity. This is the structural advantage that lets PDD maintain the lowest prices on the internet. It also, to be fair, is the structural vulnerability that keeps Chinese factory owners complaining to regulators about predatory pricing. The bargaining power of buyers, conversely, is moderate but manageable. Consumers are price-sensitive, but the switching cost between Temu and its rivals is essentially zero, which means the platform has to keep winning every day on price and selection. The threat of new entrants is material, especially from Shein and now Amazon Haul, but new entrants have to replicate the decade of supplier relationships that PDD has already paid for. The threat of substitutes—the idea that consumers might simply stop buying cheap goods—is probably the most underrated risk in the stack, and we will return to it in the bear case. And competitive rivalry, within China and increasingly within global cross-border commerce, is intensifying.

The net of all of this is a company with, by our read, one of the most durable strategic moats in the global internet sector. It is not a moat made of brand. It is not a moat made of user lock-in. It is a moat made of operational density, of supplier relationships forged in the specific conditions of Chinese manufacturing, and of an organizational culture that is willing to endure losses for years in pursuit of markets it believes it can eventually own. You can dislike many things about PDD. You cannot, if you are being intellectually honest, dismiss it.

VIII. Bear Versus Bull: The Financial Philosophy

Over eight years as a public company, PDD has developed a financial philosophy that is at once deeply unconventional and, on closer inspection, borrowed from a specific tradition of American retail. The philosophy can be summarized in a single sentence: marketing is R&D. On the company's earnings calls, when analysts have pressed on the trajectory of sales and marketing expense—which has at times exceeded 40 percent of revenue—the response from Chen and Zhao has been consistent. Sales and marketing, they argue, is not an expense incurred to generate current-quarter revenue. It is an investment in platform fundamentals: in users acquired, in merchant relationships cemented, in markets entered, in operating leverage that will compound over a decade. This is the same logical frame that Jeff Bezos used for AWS, that Reed Hastings used for Netflix content, and that Sam Walton used for retail expansion. It works, right up until the moment capital markets stop believing it.

The market, for PDD's entire post-IPO history, has oscillated between belief and disbelief. The stock has had several drawdowns of 50 percent or more—during the tech crackdown in 2021, during the post-COVID reopening trade in 2022, and during the Temu-related SHEIN legal war in 2024. Each time, the bear case has been a variant on the same theme: that the marketing-as-R&D logic is actually just a euphemism for building a business that does not work without subsidy, and that once subsidies end, the unit economics reveal themselves to be structurally unprofitable. Each time, the bull case has been the mirror image: that the subsidies are, as advertised, investments in a moat that will eventually produce operating leverage like few other businesses in the world.

The 2023 annual report gave the bulls a lot to work with. Revenue roughly doubled year-over-year. Net income margins expanded materially despite heavy Temu losses. The core domestic marketplace produced operating cash flow at a scale that effectively cross-subsidized Temu's global buildout, meaning that the single largest expansion in cross-border commerce history was being paid for not by debt or dilution but by the free cash flow of the Chinese marketplace. That is the Amazon-on-AWS playbook, and it is extraordinarily hard for competitors to counter. If you are Walmart, and your US retail business must fund its own international e-commerce expansion, you cannot compete with a rival whose profitable domestic mothership is willing to subsidize the land-grab for a decade.

The bear case, to be fair, is not frivolous. It comes in three flavors. The first is geopolitical. Temu's cross-border model relies heavily on the De Minimis customs exemption, which allows packages under $800 in declared value to enter the US duty-free. In 2024 and 2025, there has been rising bipartisan pressure in Washington to close that loophole. If De Minimis is eliminated or narrowed—and as of this writing in April 2026, multiple legislative proposals are in play—Temu's cost structure would face a meaningful tax shock. The company has been preparing for this scenario by building US-based warehouses and partial fulfillment from within the country, but the transition would not be free, and the economics of a warehouse-based Temu are less advantageous than those of a direct-ship Temu.

The second bear flavor is the "race to the bottom" on quality. Temu has faced persistent complaints about counterfeit goods, poor build quality, and product safety. The EU has opened investigations. US state attorneys general have filed complaints. Class-action lawsuits are working their way through American courts. If quality concerns translate into regulatory action or a durable shift in consumer perception, the trajectory of the business could compress. The company has invested in quality controls and counterfeit detection, but the structural reality is that a platform with millions of third-party sellers, each pushing direct-from-factory goods, will inevitably have a long tail of bad actors. Managing that tail is a forever problem.

The third flavor is cultural, and it is the one most often discussed by former employees. The 996-plus culture that drove PDD's early operational intensity is not infinitely sustainable. Engineer burnout rates are high. The two deaths in early 2021 triggered at least a nominal reckoning. In competitive Chinese labor markets, and especially in overseas hiring for Temu, the PDD model is increasingly at odds with the expectations of top talent. If the culture breaks, or if a generation of senior engineers leaves for competitors, the process power we described earlier could erode faster than the financials let on.

The bull case, on the other side, is simpler. PDD has built what is effectively a global operating system for unbranded manufacturing. The factories it works with are the same factories that produce goods for every major Western retailer. The logistics rails it operates are the same rails that will ship the vast majority of cross-border commerce over the next decade. The demand-prediction engine it runs is, increasingly, the most sophisticated commercial demand model outside of Amazon's. If you believe that the future of retail is a collapse of the brand layer—that consumers will increasingly buy directly from factories and demand lower prices—then PDD is the company best positioned to own that future. It has a head start of close to a decade, a cost structure nobody can match, and a cultural willingness to absorb losses that no Western public company can replicate.

The one-to-three KPIs that matter most for tracking PDD over the next several years come out of this framing. The first is the gross merchandise value (GMV) trajectory of the total platform, separated into domestic Pinduoduo and Temu cross-border. GMV growth is the cleanest measure of whether the flywheel is still spinning. The second is the operating margin of the core domestic marketplace, stripped of Temu-related losses. This is the number that tells you whether the cash engine funding the global expansion is still healthy. The third is Temu's cost to acquire and retain a customer, relative to that customer's annualized repeat-purchase value. That is the unit economic that answers the question of whether the marketing-as-R&D logic is justified, or whether it is the same old subsidy game wearing a new shirt.

IX. Conclusion and Epilogue

There is a story that floats around the Chinese internet industry, probably apocryphal but instructive. In 2017, as Pinduoduo was approaching 100 million users, an Alibaba executive in Hangzhou is said to have dismissed the company in an internal meeting by pointing out that its merchants were selling "fake Crocs and thirty-cent tissue paper." The dismissiveness is the point. For the better part of three years, the smartest people in Chinese e-commerce watched PDD scale past their customer count and did not notice, because the goods being sold were beneath their attention. By the time they looked up, the game was over. That, in a sentence, is what counter-positioning looks like from the inside.

PDD Holdings in 2026 is not the same company it was in 2015, or in 2018 at IPO, or in 2022 when Temu launched. It has metamorphosed, at each inflection point, into a version of itself that its previous incarnation would not have recognized. Huang built a fruit app. Chen and Zhao built a global commerce operating system. Somewhere in between, the company stopped being a Chinese story and started being a story about what happens when excess manufacturing capacity meets consumer dopamine on a global scale. The factories that produce the world's goods were always there. The consumers who wanted those goods cheap were always there. What was missing was the matching layer—the piece of software, the logistical rail, and the cultural willingness to lose money for a decade to connect them. PDD built that layer.

The legacy, for investors and for the broader retail industry, is still being written. Amazon has begun to copy the playbook. Walmart is learning to source direct-from-factory. Shein and PDD between them now collectively control a meaningful share of small-parcel international shipments. The De Minimis fight in Washington will be one of the most consequential trade-policy stories of the next several years, and the outcome will shape how the cross-border commerce model evolves. The Temu app may or may not still be ubiquitous in five years. The company itself, though—the Shanghai-built, Dublin-headquartered, factory-connected, algorithmically-priced machine underneath the app—will almost certainly still be there.

The most honest way to think about PDD is probably the way Colin Huang framed it in the 2018 prospectus. Costco plus Disney. Low prices and entertainment. A mall you play games inside of. That sentence sounded like a marketing flourish when it was written. Eight years later, it sounds like the operating manual for a new category of global retail. Whether that category ends up controlling 5 percent or 25 percent of world commerce is a question that the next decade will answer. What is not in question is who wrote the manual.

The man who wrote it is, officially, doing research in life sciences from a private office somewhere in Shanghai. The company he built continues to ship pressure cookers and mangoes and blenders and confetti animations to hundreds of millions of doorsteps every day. The ticker trades on NASDAQ, on a North American exchange, owned by an Irish holding company, driven by a Chinese supply chain, animated by an algorithm that nobody outside the inner Partnership fully understands. That is the most audacious piece of capital structure arbitrage in the modern internet era. And, like everything else about PDD, it is being executed with almost perfect, almost boring, almost frustrating silence.

X. Top 10 Reference Links

- PDD 2018 IPO Prospectus (Form F-1) — the original "Costco plus Disney" framing and first disclosed financials.

- Colin Huang's archived personal blog, including the essays on insurance, matching, and the evolution of e-commerce that underpin the company's strategic mental model.

- LatePost (晚点 LatePost) investigative series on PDD's "hardcore" culture and the 2021 employee deaths.

- Snow Lake Capital 2020 investor report on the economics of Duo Duo Maicai and community group-buying.

- PDD Holdings 2023 Annual Report (Form 20-F) — segment data for online marketing services and transaction services.

- MIT Technology Review coverage of PDD's agricultural digitization program in rural China.

- CB Insights and SimilarWeb data on Temu's US customer acquisition cost, download rankings, and repeat-purchase behavior post-Super Bowl launch.

- The Wish.com SEC filings and subsequent sale to Qoo10, as a comparison case against which to benchmark Temu's build-versus-buy decision.

- Hamilton Helmer, 7 Powers: The Foundations of Business Strategy — the canonical framework used in this analysis.

- US Customs and Border Protection statements and pending legislative text on the De Minimis exemption, relevant to the most material regulatory overhang on the Temu cross-border model.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube