Pacific Gas & Electric: From Gold Rush to Climate Crisis

I. Introduction & Episode Roadmap

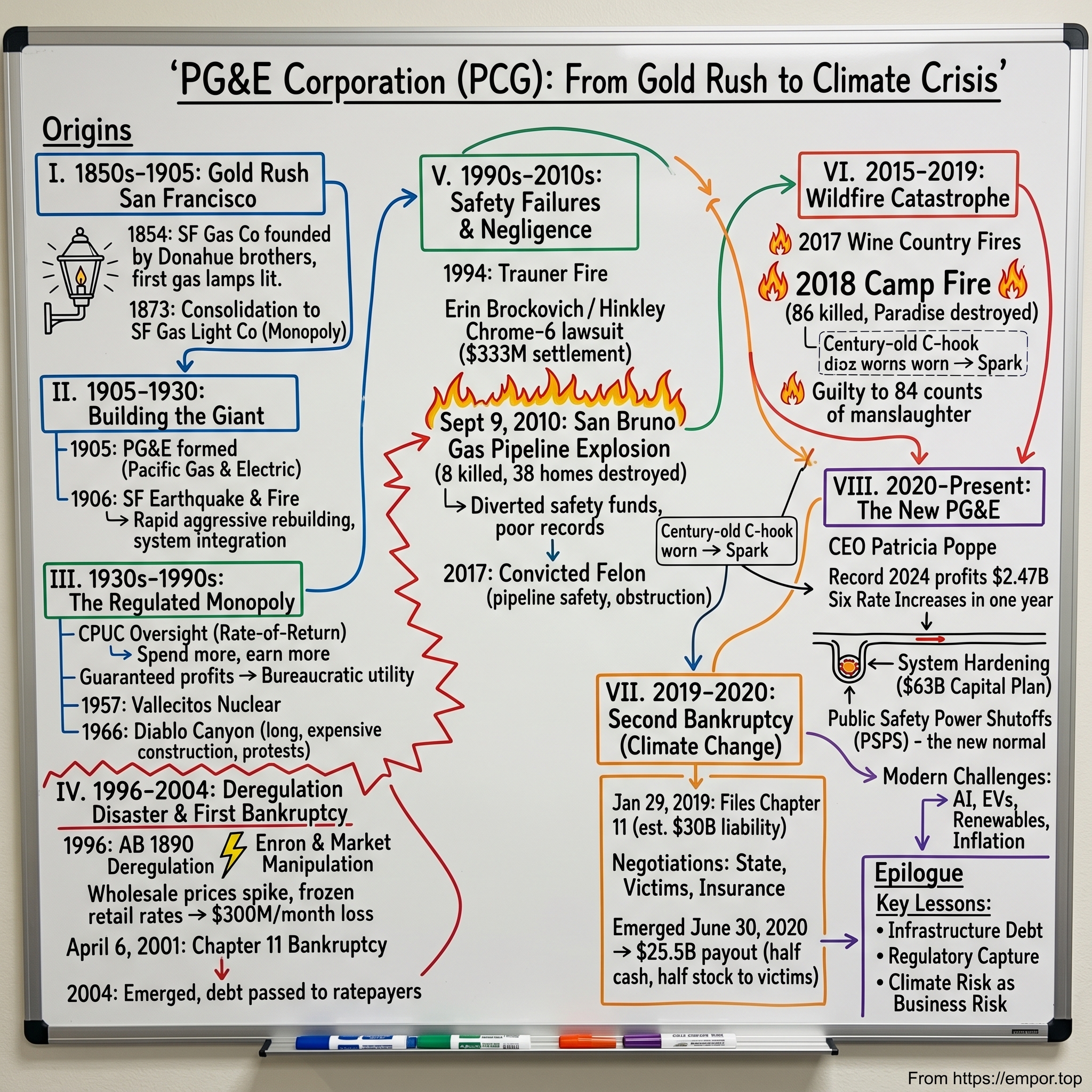

Picture this: January 29, 2019. A utility company with 16 million customers, powering Silicon Valley's tech giants and Napa Valley's wineries, files for bankruptcy protection. Not because of fraud or mismanagement in the traditional sense, but because its power lines sparked wildfires that killed 86 people and destroyed entire towns. Pacific Gas and Electric Company had just become the first major corporate casualty of climate change—a $34.9 billion market cap company brought to its knees by drought, wind, and decades of deferred maintenance.

Today, PG&E trades on the New York Stock Exchange under the ticker PCG, generating $24.4 billion in annual revenue. It's California's largest utility, serving 70,000 square miles across central and northern California. Yet this is a company that has declared bankruptcy twice, been convicted of federal crimes, and faces an existential question: How do you run critical infrastructure when climate change has weaponized your entire network?

The story of PG&E is really three stories intertwined. First, it's the quintessential American infrastructure story—entrepreneurs harnessing rivers and building networks that literally powered the development of the American West. Second, it's a cautionary tale about regulatory capture, where the watchers and the watched became so entangled that safety took a backseat to profits. And third, it's a preview of coming attractions for every utility in the climate change era—when your hundred-year-old infrastructure becomes a liability measured in human lives.

We'll journey from 1850s San Francisco, where gas lamps first illuminated muddy Gold Rush streets, through the great consolidation that created California's energy monopoly. We'll examine how a company once synonymous with progress became convicted of federal crimes after a gas pipeline explosion leveled a neighborhood. We'll dissect the 2018 Camp Fire—the deadliest wildfire in California history—and how a single worn C-hook on a century-old transmission tower led to 86 deaths and $30 billion in liabilities.

Most importantly, we'll explore what PG&E's journey means for investors, policymakers, and society. Because while this is a story about one company, it's really about a fundamental question: Who bears the cost when essential infrastructure meets climate catastrophe? The answer shapes not just PG&E's future, but the entire model of privately-owned utilities in an era of escalating climate risk.

II. Origins: Gas Lights and Gold Rush San Francisco (1850s–1905)

The muddy streets of 1850s San Francisco were a testament to human ambition and chaos. The Gold Rush had transformed a sleepy port of 1,000 souls into a boomtown of 25,000 in just two years. Ships arrived daily, their crews abandoning them for the gold fields, leaving a forest of masts in the harbor. The city burned to the ground six times between 1849 and 1851. Yet each time, it rebuilt bigger, more ambitious—and desperately in need of modern infrastructure.

Enter the Donahue brothers—Peter, James, and Michael—Irish immigrants who saw opportunity not in gold dust but in the machinery of civilization itself. Peter Donahue had already established the first iron foundry on the Pacific Coast, Union Iron Works, casting everything from mining equipment to ship engines. But in 1852, walking through San Francisco's dark streets after sunset, he saw the future: gas lighting.

On February 11, 1854, Peter and his brothers incorporated the San Francisco Gas Company with a mere $150,000 in capital. They built their first gas works at First and Howard Streets, importing coal from Australia and later Nanaimo, British Columbia. The technology was proven—coal gasification had lit London since 1812—but executing it in frontier California required extraordinary engineering. They laid cast-iron pipes through streets that were more suggestion than reality, navigating around buildings that might not exist next month.

The first gas lamps flickered to life on February 14, 1854. Suddenly, San Francisco's main thoroughfares glowed after dark. The Alta California newspaper proclaimed it "the dawn of a new era." Within months, 154 street lamps illuminated the city, and private customers clamored for connections. The Donahues had created something more powerful than lighting—they'd created a network effect. Every new customer made the system more valuable, every street lamp increased property values, every connection justified more infrastructure.

But monopoly attracted competition. By 1873, three rival gas companies battled for San Francisco's streets, literally racing to lay parallel pipes, sometimes sabotaging each other's lines. The price wars and redundant infrastructure were economically insane. That year, the companies merged into the San Francisco Gas Light Company, creating the city's first true utility monopoly. The pattern was set: competition was wasteful, consolidation was efficient, and monopoly was inevitable.

Then came electricity. In 1879, while Thomas Edison was still perfecting his incandescent bulb, a young engineer named George H. Roe built California's first central electric station for the California Electric Light Company. Using arc lamps—blindingly bright but perfect for street lighting—Roe's system beat Edison's Pearl Street Station by three full years. San Francisco became one of the first electrically lit cities in the world.

The real revolution, however, was happening 150 miles east in the Sierra Nevada mountains. Engineers realized that California's geography—massive elevation changes and powerful rivers—was perfect for hydroelectric generation. In 1895, the Folsom Powerhouse began transmitting electricity 22 miles to Sacramento, then the longest transmission distance in the world. The implications were staggering: power could be generated in the mountains and consumed in the cities. Geography became destiny.

Two visionaries understood this better than anyone: Eugene de Sabla Jr. and John Martin. De Sabla, heir to a San Francisco trading fortune, had the capital. Martin, a brilliant engineer, had the technical expertise. Together, they began acquiring water rights and building hydroelectric plants throughout Northern California. Their strategy was elegant: control the water, control the power, control the future.

By 1905, de Sabla and Martin had assembled a portfolio of hydroelectric assets that could power the entire Bay Area. But they needed scale—scale to justify transmission lines, scale to negotiate with cities, scale to fend off competitors. They needed to create something that had never existed before: a truly integrated utility combining gas and electric service across an entire region. The age of consolidation was about to begin.

III. The Great Consolidation: Building PG&E (1905–1930)

October 10, 1905, should have been a day of celebration. In a wood-paneled boardroom in San Francisco's financial district, executives from California Gas & Electric Corporation and San Francisco Gas & Electric Company signed papers creating the Pacific Gas and Electric Company. The new entity commanded $55 million in assets, controlled 520 miles of transmission lines, and served 80,000 customers. John Martin, now president, declared it would become "the greatest public utility on the Pacific Coast."

Six months later, at 5:12 AM on April 18, 1906, San Francisco shook itself apart.

The Great San Francisco Earthquake registered 7.9 on the Richter scale, but the real devastation came from fire. Ruptured gas mains fed flames that consumed 80% of the city over three days. PG&E's entire San Francisco infrastructure—gas works, power plants, offices—reduced to twisted metal and ash. The company's two-story headquarters on Beale Street collapsed, killing several employees. Total damage: $5 million, nearly 10% of the company's entire value.

Yet disaster bred opportunity. N.W. Halsey, PG&E's new president (Martin had been bought out), saw the rebuilding as a chance to create a modern, integrated system from scratch. While competitors hesitated, PG&E borrowed aggressively, issuing $25 million in bonds—a staggering sum for 1906. They didn't just rebuild; they revolutionized. New gas mains included automatic shutoff valves. Electric lines went underground in the business district. Most importantly, they connected their isolated systems into an integrated grid.

The strategy was pure network economics: every acquisition made the next one more valuable. Buy a small municipal system? Connect it to the grid and immediately reduce costs through centralized generation. Acquire a competitor's gas franchise? Eliminate redundant infrastructure and use the savings to expand. Between 1905 and 1914, PG&E absorbed 25 companies, including major players like California Gas & Electric Corporation and United Railroads' electric properties.

The numbers told the story: customers grew from 80,000 to 315,000. Revenue jumped from $11 million to $28 million. By 1914, PG&E served 1.3 million people across 37 counties—the largest integrated utility system on the Pacific Coast. But Halsey wasn't satisfied. He envisioned something unprecedented: a single company providing all gas and electric service for central and northern California.

The technical challenges were immense. Transmitting power from Sierra Nevada hydroelectric plants to coastal cities required spanning 200 miles of mountains, valleys, and seismically active terrain. PG&E engineers pioneered high-voltage transmission—first 60,000 volts, then 110,000, eventually 220,000. Each voltage increase meant power could travel farther with less loss. They invented new tower designs to withstand Pacific storms, new insulators to handle fog and salt air, new switching systems to route power around failures. But the strategic masterstroke came in 1930. PG&E purchased majority stock holdings in two major Californian utility systems—Great Western Power and San Joaquin Light and Power—from The North American Company, a New York investment firm. In return, North American received shares of PG&E's common stock worth $114 million. This wasn't just an acquisition; it was the culmination of 25 years of consolidation. Through this final major consolidation, PG&E soon served nearly all of Northern and Central California through one integrated system.

The Great Western Power Company brought massive hydroelectric capacity from the Feather River. San Joaquin Light and Power controlled the Central Valley, California's agricultural heartland. Together, they eliminated PG&E's last significant competitors. The company now controlled electricity generation from the Sierra Nevada to the Pacific, gas distribution from San Francisco to Fresno, and transmission lines connecting it all. It was a natural monopoly achieved through relentless acquisition—and it would define California's energy landscape for the next century.

IV. The Regulated Monopoly Era (1930s–1990s)

The California Public Utilities Commission chambers in San Francisco, 1935. Commissioners sit across from PG&E executives, negotiating not prices but returns. The conversation had fundamentally changed. No longer was PG&E a company competing for customers; it was now a regulated monopoly guaranteed profits in exchange for universal service. The rate-of-return model was elegant in its simplicity: invest capital, provide service, earn a guaranteed return. What could go wrong?

This regulatory compact transformed PG&E from entrepreneurial risk-taker to bureaucratic utility. The company's mandate was clear: build infrastructure, serve everyone, recover costs plus profit through rates. The California Public Utilities Commission, created in 1911 but only now fully empowered, would ensure "just and reasonable" rates while PG&E ensured reliable service. It was capitalism with training wheels—competition eliminated, profits guaranteed, innovation optional.

The post-World War II boom tested this model at unprecedented scale. California's population exploded from 7 million in 1940 to 10.5 million by 1950. Returning veterans needed homes, those homes needed power, and PG&E needed to build faster than ever. The company launched what it called "the greatest construction program ever undertaken by an American utility"—and the numbers backed the claim. Between 1946 and 1955, PG&E added 14 hydroelectric plants, five steam plants, and thousands of miles of transmission lines.

By 1955 PG&E's network extended into 46 counties in northern and central California. It supplied electricity to 168 cities and towns and gas to 146 cities and towns. The company had become California's circulatory system, as essential as highways or water. Employment swelled to 18,000 workers—linemen stringing wire across mountains, engineers designing substations, meter readers walking every neighborhood. PG&E wasn't just a company; it was an institution.

The nuclear age arrived in 1957 with typical PG&E ambition. The company made history when it teamed up with General Electric to establish the Vallecitos atomic energy plant—the world's first privately owned and operated nuclear facility. Located 35 miles east of San Francisco, Vallecitos was a five-megawatt proof of concept that atoms could be split for profit. PG&E executives saw nuclear as the future—clean, limitless, modern. They began planning something far more ambitious: Diablo Canyon.

The Diablo Canyon saga would define PG&E's relationship with California for decades. Announced in 1966, the twin-reactor plant on the Central Coast was supposed to cost $350 million and open by 1973. Instead, it became a 20-year, $5.8 billion odyssey through regulatory changes, seismic discoveries, and mass protests. When geologists discovered the Hosgri Fault just three miles offshore, PG&E had to retrofit the nearly-complete plant to withstand a 7.5 magnitude earthquake. When protesters blockaded the site in 1981, 1,900 were arrested in the largest anti-nuclear demonstration in U.S. history.

Yet throughout these battles, the rate-of-return model protected PG&E. Every dollar spent on Diablo Canyon—whether for construction, retrofitting, or lawyers—went into the "rate base" on which PG&E earned its guaranteed return. The more expensive the plant became, the more profit PG&E could earn. Ratepayers would cover everything. This perverse incentive—spend more, earn more—would shape PG&E's DNA in ways that would prove catastrophic decades later.

The mid-20th century was PG&E's heyday. The company was beloved by its employees, appreciated by its customers and admired by its peers. "People loved PG&E in those days, they really did," said Harry Jackson, who began his career with PG&E as a clerk in 1960.

But cracks were forming. Environmental consciousness was rising. In 1963, PG&E's plan for a nuclear plant at Bodega Bay, practically atop the San Andreas Fault, collapsed under public outrage. The company's assumption that it could build anything anywhere was suddenly questionable. More fundamentally, the cozy relationship between PG&E and its regulators was breeding complacency. Why innovate when profits were guaranteed? Why maintain infrastructure aggressively when repairs could be capitalized and earn returns?

By 1973, PG&E had become the second-largest utility in the United States, serving 4.5 million electric customers and 2.9 million gas customers. It operated 141,000 circuit miles of electric transmission and distribution lines, 37,000 miles of gas mains, and generated revenue of $1.4 billion. On paper, it was an American success story. In reality, it was an aging monopoly insulated from market forces, political pressure, or competitive innovation. The stage was set for disaster—it would just take California's deregulation experiment to light the fuse.

V. Deregulation Disaster & First Bankruptcy (1996–2004)

The wood-paneled conference room at the California Public Utilities Commission, September 23, 1996. Commissioners vote unanimously to approve AB 1890, deregulating California's electricity market. PG&E executives applaud. Consumer advocates celebrate. Everyone believes they're ushering in a new era of competition and lower prices. Instead, they've just lit a $45 billion bonfire that would consume PG&E, bankrupt the state's largest utility, and trigger rolling blackouts across the world's fifth-largest economy.

The logic seemed impeccable. Electricity generation would be competitive—let the market set prices. Transmission and distribution would remain regulated monopolies. PG&E would sell its power plants, buy electricity on the open market, and pass savings to consumers. To sweeten the deal, the state guaranteed PG&E could recover $28 billion in "stranded costs"—bad investments in nuclear plants and expensive contracts. Rates would be frozen at high 1996 levels until these costs were recovered, then fall as competition worked its magic.

But the California experiment had a fatal flaw: PG&E had to buy power at fluctuating wholesale prices but sell it at frozen retail rates. It was like forcing someone to buy gasoline at market prices but sell it at $1 per gallon regardless of cost. As long as wholesale prices stayed below retail rates, the model worked. If they spiked, PG&E would hemorrhage money. Nobody thought prices could spike that much. Nobody counted on Enron.

By summer 2000, wholesale electricity prices had gone insane. Power that cost $30 per megawatt-hour in 1999 spiked to $1,400. California's hot summer and low rainfall reduced hydroelectric supply. Natural gas prices tripled. But the real culprit was market manipulation. Enron traders—who gave their schemes names like "Death Star" and "Get Shorty"—deliberately created artificial shortages. They'd schedule power deliveries on constrained transmission lines, collect payments to relieve the congestion they created, then cancel the deliveries. They'd ship California power to Oregon, then sell it back at inflated prices.PG&E's CFO was blunt in a January 2001 investor call: "We're buying power that averaged about 20 cents per kilowatt-hour and were forced to resell that power for about 6 cents per kilowatt-hour." The math was catastrophic. PG&E was losing $300 million per month. By March 2001, the company had accumulated $8.9 billion in unrecovered wholesale costs—and California's politicians refused to raise rates. Governor Gray Davis, facing re-election, declared he wouldn't bail out utilities on the backs of ratepayers.

On January 17, 2001, California experienced its first rolling blackouts since World War II. Traffic lights went dark. Silicon Valley chip fabs lost millions in ruined production. Elevators trapped office workers. The state that invented the internet couldn't keep its lights on. The blackouts weren't from lack of generation—California had adequate capacity. They were from market manipulation so brazen that Enron traders were caught on tape laughing about "grandmothers in the dark."

PG&E Company entered bankruptcy under Chapter 11 on April 6, 2001. The company possessed $2.3 billion in cash but chose bankruptcy over negotiation. It was a strategic default—using bankruptcy to force the state to either raise rates or buy PG&E's transmission system. The politics were brutal. Consumer groups accused PG&E of holding California hostage. The state accused PG&E of illegally transferring billions to its parent company. PG&E accused everyone of forcing it into an impossible position.

Some experts put the total damage to California's economy at more than $40 billion. PG&E went bankrupt, and Southern California Edison came close. The state stepped in as buyer of last resort, signing long-term contracts at inflated prices that would burden ratepayers for decades. Enron collapsed in scandal. Several traders went to prison. But the real cost was trust—Californians no longer believed in deregulation, competitive markets, or PG&E.

PG&E Company, the utility, emerged from bankruptcy in April 2004, after paying $10.2 billion to its hundreds of creditors. As part of the reorganization, PG&E's 5.1 million electricity customers will have to pay above-market prices for several years to cancel the debt. The company survived, but something fundamental had changed. PG&E was no longer California's trusted utility. It was a convicted monopolist that had gamed bankruptcy to force a bailout. The stage was set for an even greater catastrophe—one measured not in dollars but in lives.

VI. Safety Failures & Criminal Negligence (1990s–2010s)

The courtroom in San Francisco federal court, January 27, 2017. U.S. District Judge Thelton Henderson looks down at PG&E's lawyers. "Pacific Gas and Electric Company is hereby adjudged guilty of obstruction of justice and five violations of pipeline safety regulations," he declares. The company that powered California had become a convicted felon. But this was just the latest chapter in a decades-long pattern of putting profits over safety—a pattern that began with chrome-6 in groundwater and would end with entire towns consumed by fire.

In 1994, PG&E caused the Trauner Fire in Nevada County, California through criminal negligence. It was a preview of catastrophes to come—improperly maintained equipment, ignored warnings, devastating consequences. But in 1994, wildfires weren't yet weapons of mass destruction. Climate change hadn't yet transformed California into kindling. PG&E paid its fines and moved on.

The real warning came from Hinkley, California, a dusty Mojave Desert town of 2,000 souls. For decades, PG&E had used chromium-6 as an anti-corrosion agent at its natural gas compressor station. The chemical leaked into groundwater, poisoning an entire community. Cancer rates spiked. Children developed rare tumors. PG&E's response? Cover it up. The company held town meetings claiming chrome-6 was actually good for you, that it improved metabolism.

Enter Erin Brockovich, a legal clerk with a high school education who uncovered PG&E's deception. The residents of Hinkley filed a successful lawsuit against PG&E in which the company paid $333 million—the largest settlement ever paid in a direct-action lawsuit in U.S. history. The legal case, dramatized in the 2000 film Erin Brockovich, became an international cause célèbre. Julia Roberts won an Oscar playing Brockovich. PG&E became Hollywood's villain, the faceless corporation poisoning innocent families.

But Hinkley taught PG&E the wrong lesson. The company learned to manage litigation, not prevent disasters. It perfected the art of regulatory capture—hiring former regulators, funding studies that muddied scientific waters, settling lawsuits with gag orders. When California Chrome-6 standards were reviewed in 2001, PG&E's expert witnesses dominated the committee, producing a report that found in the company's favor.

The real reckoning came on September 9, 2010, at 6:11 PM in San Bruno, a middle-class suburb south of San Francisco. Residents reported smelling gas for weeks. PG&E classified it as a minor leak. Then Line 132, a 30-inch transmission pipeline installed in 1956, exploded with the force of a small earthquake. The fireball reached 1,000 feet high, visible from space. Eight people died instantly. Thirty-eight homes vaporized. The crater measured 167 feet long and 26 feet deep. The investigation revealed a horror show of negligence. PG&E had illegally diverted over $100 million from a fund used for safety operations, and instead used it for executive compensation and bonuses. The pipeline that exploded had been installed in 1956 with a defective seam weld that PG&E charts had labeled seamless. PG&E hadn't properly tested the line for decades. When residents reported gas smells, the company classified them as minor.

The jury found PG&E guilty of 5 out of the 11 separate violations of the PSA charged, concluding the company knowingly and willfully violated the PSA and its regulations between 2007 and 2010. More damning was the obstruction charge. The charge centers around PG&E's use of a letter in an attempt to mislead the NTSB during an investigation. The company had actively lied to federal investigators about its safety practices.

The state Public Utilities Commission fined the company a record $1.6 billion for the explosion. The PUC action requires PG&E to pay $850 million for improvements to its natural gas pipeline system. Another $300 million will go to the state's general treasury, $400 million will be refunded to PG&E gas customers as a one-time credit and $50 million will pay for a variety of safety activities by PUC staff and contractors. The entire $1.6 billion fine would be paid for by the company and shareholders—not by ratepayers.

On January 27, 2017, U.S. District Judge Thelton Henderson sentenced PG&E for its crimes. PG&E's sentence includes a $3 million fine, a five-year probation period, independent safety monitoring and 10,000 hours of community service. But the most publicly visible punishment is an advertising mandate. In the next 60 days, PG&E must take out full-page ads in the San Francisco Chronicle and Wall Street Journal, in addition to 60-second television ads, detailing the nature of PG&E's offenses and the steps they're taking to prevent future offenses and disasters.

The company was now a convicted felon on probation. But the pattern was clear: defer maintenance, maximize profits, manage disasters through litigation. This wasn't incompetence; it was strategy. And in a warming, drying California, this strategy was about to collide with climate change in the most catastrophic way imaginable.

VII. The Wildfire Catastrophe (2015–2019)

The morning of November 8, 2018, started like any other for the residents of Paradise, California. A pleasant town of 26,000 nestled in the Sierra Nevada foothills, known for its tall pines and retirement communities. By noon, Paradise no longer existed. The Camp Fire—sparked by a century-old PG&E transmission line—had become the deadliest wildfire in California history. Eighty-six people died. Most were elderly, trapped in their homes or cars as flames moved faster than evacuation orders. The fire destroyed 18,804 structures, wiped out 90% of Paradise, and burned 153,336 acres. All from a single worn C-hook on a tower built in 1921.Cal Fire's investigation was damning. After a very meticulous and thorough investigation, CAL FIRE has determined that the Camp Fire was caused by electrical transmission lines owned and operated by Pacific Gas and Electricity (PG&E) located in the Pulga area of Butte County. The specific culprit was Tower 27/222 on the Caribou-Palermo transmission line—a century-old structure whose C-hook had worn through after decades hanging in the windy Feather River Canyon.

But the Camp Fire wasn't an isolated incident. It was the culmination of years of escalating wildfire disasters. Cal Fire previously found PG&E at fault for 17 wine country fires in 2017, including the Redwood Fire, which resulted in nine fatalities. The 2017 fire season alone had seen PG&E equipment spark multiple catastrophic blazes. The Tubbs Fire destroyed 5,643 structures. The Atlas Fire burned 51,624 acres. Each investigation revealed the same pattern: aging equipment, deferred maintenance, ignored warnings.

Climate change had transformed California into a tinderbox. The winter of 2016-2017 saw above-average precipitation, creating massive grass growth. This was followed by a hot, dry summer that turned all that vegetation into fuel. Add hurricane-force winds—the Diablo winds in the north, Santa Anas in the south—and you had conditions where a single spark could destroy a city.

PG&E knew this. Internal documents showed the company tracked "Red Flag" warnings—extreme fire weather conditions. They had protocols for "Public Safety Power Shutoffs" (PSPS), preemptively cutting power during high winds. But shutoffs meant angry customers, lost revenue, political backlash. On November 8, 2018, despite Red Flag conditions, PG&E kept the Caribou-Palermo line energized. The worn C-hook couldn't withstand the wind.

The fire's speed defied comprehension. Due to the conditions at the time and the overgrown forest and with climate change, you had searing temperatures really late into November. This fire chewed through an acre - roughly an acre of forest every few seconds, came into Paradise, went from a forest fire to an urban wildfire. Evacuation orders couldn't keep pace. Roads became death traps as abandoned cars blocked escape routes. Many victims died in their vehicles, overcome by smoke and flames.

The human toll was staggering. 84 souls were lost in the most horrific way imaginable - burned to death. The youngest victim was 20-year-old Jessica Morales. The oldest was 99-year-old Rose Farrell. Most were elderly or disabled, unable to evacuate quickly. Their names would be read aloud in court, one by one, as PG&E pleaded guilty to their deaths.

Pacific Gas & Electric pleaded guilty on Tuesday to 84 separate counts of involuntary manslaughter and one felony count of unlawfully starting a fire in a case stemming from a horrific 2018 blaze that destroyed much of the town of Paradise in Northern California. PG&E CEO and President Bill Johnson entered the guilty pleas in Butte County Superior Court one at a time as he watched photographs of each of the victims flash on a screen. With hands clasped, Johnson rocked back and forth while Judge Michael Deems called out the names of the dead. Each time, Johnson responded in an even voice, saying, "Guilty your honor."

"Our equipment started that fire," Johnson admitted, after waiving the company's right to appeal the case. It was the first time any major utility had been charged with homicide. But even this unprecedented criminal conviction came with a caveat: no individual executives were prosecuted. The corporation was guilty, but no person would go to prison.

The financial implications were catastrophic. PG&E could face liabilities exceeding $30 billion in connection with fires in 2017 and 2018. Insurance claims alone totaled billions. Victim lawsuits sought punitive damages. Cities and counties demanded compensation for firefighting costs. The company's stock price collapsed from $48 to $5. Credit ratings plummeted to junk status. California's largest utility was heading toward its second bankruptcy in two decades—but this time, the cause wasn't market manipulation or bad regulation. It was climate change meeting criminal negligence.

VIII. Second Bankruptcy: Climate Change Meets Corporate Failure (2019–2020)

The boardroom at PG&E's San Francisco headquarters, January 14, 2019, 5:47 AM. CEO Geisha Williams sits alone, watching pre-market trading on her laptop. PG&E stock has already fallen 52% since the Camp Fire. In twelve hours, she'll resign. In fifteen days, the company will file for Chapter 11 bankruptcy protection. The phrase being whispered in financial circles has made it to mainstream media: "the first climate change bankruptcy." But Williams knows better. This isn't about climate change alone—it's about a century of choices catching up with a warming world.

In early 2019, PG&E filed for Chapter 11 bankruptcy after fires caused by its powerlines burned hundreds of thousands of acres in Northern California and led to more than 100 deaths. The utility says it has no choice but to file for Chapter 11 given the flood of lawsuits and wildfire liabilities it estimates could be up to $30 billion. The mathematics were brutal: potential liabilities exceeded the company's entire market capitalization. Unlike 2001's bankruptcy—a financial engineering problem—this was existential.

The bankruptcy filing on January 29, 2019, was strategic timing. By filing before Cal Fire officially determined fault for the Camp Fire, PG&E could negotiate from a position of some uncertainty. PG&E formally initiated proceedings under Chapter 11 of the federal bankruptcy code on January 29, 2019, citing its exposure to wildfire liability claims of $30 billion or more. The company made sure to emphasize it wasn't insolvent—it had cash, could operate, would keep the lights on. This was about managing liabilities, not liquidation.

Governor Gavin Newsom was furious. He also wants the option of taking over the utility if it fails to meet safety and performance criteria. In public, he talked about protecting ratepayers and ensuring reliable service. In private, his administration explored the nuclear option: state takeover. Could California run its own utility? Should PG&E be broken up? The politics were explosive—a Democratic governor potentially nationalizing a private company while climate activists demanded public power.

The bankruptcy proceedings became a three-way negotiation between PG&E, the state, and victims. The victims, represented by a Tort Claimants Committee, wanted maximum compensation—ideally all $30 billion. The state wanted PG&E restructured to prevent future disasters, with new management, new board, new safety culture. PG&E wanted to survive with its monopoly intact, shareholders preserved, business model unchanged.

The negotiations were brutal. The bankruptcy judge on Tuesday approved PG&E's plans to pay $13.5 billion to wildfire victims and $11 billion to insurance firms. But the devil was in the details. Half the victim compensation would be in PG&E stock—forcing fire survivors to bet on their tormentor's future success. The irony was cruel: Paradise residents would become PG&E shareholders.

It paid out $25.5 billion to resolve its fire-related liabilities, and expects to spend $11.7 billion on strategies to mitigate wildfire risk between 2019 and 2022. The total settlement broke down as follows: $13.5 billion to fire victims (half cash, half stock), $11 billion to insurance companies (all cash), and $1 billion to local governments. It was the largest utility settlement in history—and everyone knew it wouldn't be enough.

Governor Newsom extracted significant concessions. PG&E agreed to replace its entire board of directors, bring in new management, and submit to enhanced state oversight. The company has obtained the financing needed to exit bankruptcy, it announced in a press release, and has put in place a new board of directors. Bill Johnson, former CEO of the Tennessee Valley Authority, was brought in to lead the company—an outsider tasked with changing a century-old culture.

The company also agreed to massive safety investments. It expects to spend $11.7 billion on strategies to mitigate wildfire risk between 2019 and 2022. This included vegetation management, system hardening, and expanded Public Safety Power Shutoffs. But everyone understood the fundamental problem remained: PG&E's infrastructure was a weapon in a warming world.

California also created a $21 billion wildfire insurance fund, with utilities contributing based on their role in past fires. The company's timely exit from bankruptcy allows it to participate in California's wildfire insurance fund, a $21 billion pool. The fund would cover future wildfire damages—but only if utilities weren't found negligent. It was a Band-Aid on a bullet wound.

Now, PG&E has resolved those liabilities with a $25.5 billion payout. It has set up a trust worth around $13.5 billion to compensate victims of the fires, funded by a $5.4 billion payout made last week, two installments amounting to $1.35 billion in 2021 and 2022, and stock payments. In addition, the company settled with insurance companies holding wildfire claims for $11 billion, and paid out another $1 billion in an agreement with local government entities affected by the fires.

On June 30, 2020, PG&E emerged from bankruptcy. But the phrase stuck: "climate change bankruptcy." While PG&E may be the first climate bankruptcy, it will likely not be the last, according to a report by Columbia University's Center on Global Energy Policy. "Wildfires alone could become up to 900 percent more destructive in certain regions by midcentury, and utility assets will also be increasingly exposed to threats stemming from hurricanes, rising sea levels, and other climate-related events," it said.

The company emerged financially restructured but fundamentally unchanged. Same business model, same infrastructure, same climate. The only difference: now everyone knew what that combination could produce.

IX. The New PG&E: Wildfire Mitigation & Modern Challenges (2020–Present)

The Vacaville operations center, 4:30 AM, October 14, 2024. Red Flag warnings light up the weather monitors. Wind speeds projected to hit 60 mph. Humidity below 10%. Temperature still 85 degrees at dawn. The Public Safety Power Shutoff decision looms. Cut power to 800,000 customers or risk another Paradise. Five years after emerging from bankruptcy, PG&E faces the same impossible choice—but now with $63 billion in capital improvements, 23,000 employees, and the entire state watching.

The numbers tell a remarkable story of financial recovery. GAAP earnings were $1.15 per share for the full year of 2024, compared to earnings of $1.05 per share for the same period in 2023. But dig deeper and you find something extraordinary: Pacific Gas & Electric's $2.47 billion record-smashing profit for 2024 comes as the California Public Utilities Commission, or CPUC has approved an outrageous six rate increases in the same year. PG&E CEO Patricia Poppe announced the company's 2024 eye-popping profits on Thursday, February 13, during an investor call.

Record profits while implementing the most expensive wildfire mitigation program in history—it's a paradox only possible in the regulated utility world. Equity needs fully satisfied to fund the five-year capital plan of $63 billion through 2028. Every dollar spent on safety goes into the rate base. Every underground power line earns a guaranteed return. The more PG&E spends to prevent fires, the more profit it makes.

The transformation under CEO Patricia Poppe has been dramatic. For long-term wildfire risk reduction, completed 366 miles of system hardening including 258 miles of underground powerlines and 108 miles of stronger poles and overhead powerlines in the highest fire-risk areas. The undergrounding program alone costs $3.75 million per mile—making it one of the most expensive infrastructure projects in American history. Critics call it gold-plating. PG&E calls it essential.

Public Safety Power Shutoffs have become the new normal. When fire weather arrives, PG&E preemptively cuts power to hundreds of thousands. The October 2024 shutoff affected 800,000 customers across 34 counties. Hospitals run on generators. Traffic lights go dark. Food spoils. Businesses close. The economic impact runs into billions—but it's better than another Camp Fire.

The operational metrics are impressive. The company achieved significant operational milestones, including zero major wildfires for the second consecutive year and completed 366 miles of system hardening. Zero major wildfires—a phrase that would have been unremarkable in 1990 but represents triumph in 2024. Climate change has made not killing people an achievement worth celebrating.

But the fundamental tension remains. The jump in profit arrives as PG&E customers express increasing frustration with skyrocketing monthly bills. PG&E Chief Executive Officer Patricia Poppe acknowledged rising customer bills in comments during a conference call to discuss the financial results. "We appreciate that near-term bill pressure…is difficult for some of our customers," Poppe told Wall Street analysts.

The rate increases are staggering. Last November, the state Public Utilities Commission that oversees the utility authorized a 13% increase in customer monthly bills to finance an array of tasks, including efforts to mitigate wildfire risks. Average residential bills have increased 110% since 2019. A typical household now pays $380 per month for electricity and gas—the highest in the continental United States.

The federal government has stepped in with unprecedented support. Signed a $15 billion loan guarantee agreement with the U.S. Department of Energy's Loan Programs Office to finance grid modernization projects and potentially save customers up to $1 billion on a net present value basis through lower-cost financing. It's the largest utility loan guarantee in DOE history—a recognition that PG&E is too big to fail and too important to leave to market forces alone.

Meanwhile, California's energy landscape is transforming. Tech companies building AI data centers need massive amounts of reliable power. Electric vehicle adoption is accelerating. Building electrification mandates are eliminating natural gas in new construction. Connected nearly 14,000 new customers to the electric system, approximately 30% more than plan. Demand is surging just as the grid becomes more vulnerable.

The renewable transition adds another layer of complexity. Solar farms in the desert. Offshore wind proposals. Battery storage facilities. All require new transmission lines through fire-prone areas. Every mile of new infrastructure is another potential ignition source. The clean energy future runs headlong into wildfire reality.

PG&E's workforce has been transformed. Enhanced safety protocols. Drone inspections. AI-powered vegetation management. Real-time weather monitoring with 1,400 weather stations. The company now employs more meteorologists than some government agencies. Technology that would have seemed like science fiction in 2018 is now standard operating procedure.

Exceeded non-fuel O&M cost reduction target through continuous efforts to deliver longer-term energy bill stability for customers. Translation: PG&E is cutting operational costs even while spending billions on safety. It's financial engineering at its finest—or most cynical, depending on your perspective. Efficiency gains fund safety improvements which increase rate base which drives profits which fund dividends.

The investment community has noticed. The 10% increase in non-GAAP core earnings to $1.36 per share, coupled with a remarkable 70% jump in operating cash flow to $8.0 billion, signals robust fundamental performance. PG&E stock has recovered from its bankruptcy lows of $3 to trade above $20. Wall Street sees a utility with a captive customer base, guaranteed returns, and government backing.

But climate change continues to accelerate. 2024 saw the hottest summer on record. The Sierra snowpack hit historic lows. Drought and deluge alternate with increasing violence. Fire season now runs year-round. The question isn't whether PG&E equipment will spark another catastrophic fire, but when—and whether the company's massive investments will prevent it from killing people.

X. Playbook: Lessons from PG&E's Journey

Step back from the daily headlines, the quarterly earnings, the regulatory filings. What does PG&E's 120-year arc teach us about business, infrastructure, and society? The lessons are uncomfortable, especially for investors accustomed to simple narratives about good companies and bad companies, efficient markets and rational actors.

Natural Monopolies and Regulatory Capture

The first lesson is that natural monopolies inevitably capture their regulators. It's not conspiracy—it's convergence. PG&E and the California Public Utilities Commission have been locked in a 110-year dance where opposition becomes partnership becomes identity. Regulators need expertise; they hire from utilities. Utilities need regulatory approval; they hire former regulators. Information flows through a revolving door until it's impossible to say where the company ends and the oversight begins.

The rate-of-return model intensifies this dynamic. When profits are guaranteed as a percentage of capital invested, the incentive is always to build more, spend more, capitalize more. Why spend $1 million on maintenance when you can spend $10 million on new equipment and earn returns on the larger number? The regulator's job becomes blessing capital plans, not questioning them. Everyone wins—except ratepayers who foot the bill and communities that burn when maintenance gets deferred.

Infrastructure Debt: The Cost of Deferred Maintenance

PG&E's story is fundamentally about infrastructure debt—not financial debt, but the accumulated cost of delayed maintenance, outdated equipment, and systems pushed beyond their design life. A gas pipeline installed in 1956 with defective welds. A transmission tower from 1921 with worn C-hooks. Wooden poles in fire country that should have been replaced decades ago.

Infrastructure debt is insidious because it's invisible until catastrophe. A transmission line works until it doesn't. A gas main holds pressure until it explodes. Every year of deferred maintenance saves money and increases risk, but the risk is probabilistic, abstract, easy to rationalize. Until eight people die in San Bruno. Until Paradise burns.

The business incentive is always to defer. Maintenance is an expense that reduces profits. New construction is capital that increases rate base. Under traditional utility regulation, a company literally profits more from building new than maintaining old. It took criminal convictions and bankruptcy to change this calculus—and even now, the incentives remain misaligned.

Climate Risk as Systemic Business Risk

PG&E represents the first clear example of climate change destroying a major corporation's business model. Not through sea level rise or supply chain disruption, but through the weaponization of existing infrastructure. Power lines that safely delivered electricity for a century became murder weapons when drought, heat, and wind transformed California into kindling.

The terrifying insight is that PG&E isn't unique. Every utility with overhead lines in fire-prone areas faces similar risks. Every pipeline company in flood zones. Every coastal facility facing hurricanes. Climate change doesn't just create new risks—it transforms existing infrastructure into liabilities. The accumulated capital stock of the carbon economy becomes a massive stranded asset, dangerous to operate and impossible to abandon.

Wildfires alone could become up to 900 percent more destructive in certain regions by midcentury, and utility assets will also be increasingly exposed to threats stemming from hurricanes, rising sea levels, and other climate-related events. That's not an environmental projection—it's a business reality that will drive multiple sectors into crisis.

Corporate Culture and Safety Priorities

Culture eats strategy for breakfast, and PG&E's culture ate safety for decades. The company that emerged from the 1906 earthquake with entrepreneurial vigor had become, by the 2000s, a financial engineering operation that happened to deliver electricity. Safety became a slogan, not a practice. Risk management meant managing regulatory risk, not physical risk.

The pattern is consistent across decades: San Bruno, Camp Fire, multiple smaller disasters. Each time, investigations revealed the same issues: known problems, ignored warnings, maintenance deferred, records falsified or lost. This isn't individual failure—it's systematic, cultural, embedded in incentives and assumptions.

Changing culture requires trauma. PG&E required bankruptcy, criminal conviction, and public vilification to begin transforming. Even now, with new management and billions in safety spending, the question remains whether culture can change fast enough to meet accelerating climate risks.

Political Economy of Utility Regulation

PG&E's story reveals the profound political nature of utility regulation. Rates aren't set by markets but by political appointees. Safety standards emerge from political pressure, not economic calculation. Whether to underground power lines or implement shutoffs or allow rate increases—these are political decisions dressed up as technical ones.

This political dimension creates profound instability. Governors change, commissioners rotate, public attention wanders. PG&E has survived 23 governors, dozens of CPUC presidents, multiple political philosophies. The company's real expertise isn't engineering—it's political navigation, regulatory management, legislative influence.

The climate crisis intensifies these politics. Every wildfire becomes a political crisis. Every rate increase triggers backlash. Every shutoff affects voters. PG&E operates at the intersection of essential service and political lightning rod—a position that grows more precarious as climate impacts accelerate.

First-Mover Disadvantage in Climate Liability

PG&E faces a cruel irony: being first to confront climate liability makes it the test case for everyone else. The company is developing playbooks—for wildfire mitigation, for bankruptcy navigation, for victim compensation—that other utilities will eventually need. But being first means bearing full cost of learning.

The $63 billion capital plan, the undergrounding program, the shutoff protocols—these are experiments in climate adaptation at utility scale. Some will work, others won't, but PG&E bears the cost of finding out. Meanwhile, other utilities watch, learn, and adapt without the same financial burden.

This first-mover disadvantage extends to litigation. Legal precedents set in PG&E cases will determine liability standards for utilities nationwide. Regulatory responses to PG&E's crisis shape rules for everyone. The company has become an involuntary pioneer in climate liability—a position that benefits society but punishes shareholders.

The "Too Big to Fail" Utility Problem

Perhaps the most troubling lesson is that PG&E has become too essential to fail regardless of its crimes or incompetence. 16 million people depend on it for power. Silicon Valley's tech companies need reliable electricity. California's renewable energy goals require PG&E's grid. The company could burn down half the state and still be indispensable.

This creates massive moral hazard. PG&E knows—and more importantly, creditors know—that California cannot allow it to liquidate. Bankruptcy becomes a negotiating tactic, not an existential threat. Criminal convictions result in fines, not imprisonment. The company externalizes catastrophic risks while privatizing profits, knowing the state will always backstop disaster.

The traditional solution—municipal ownership—faces its own challenges. Would politicians manage wildfire risk better than profit-seeking executives? Would public ownership mean better maintenance or just different political pressures? The track record of municipal utilities is mixed, and none face PG&E's combination of scale, geography, and climate exposure.

XI. Analysis & Investment Perspective

The investment case for PG&E is either compelling or terrifying, depending on your risk tolerance and time horizon. This is not a normal utility trading on dividend yield and steady growth. It's a climate adaptation play, a regulatory arbitrage, a bet on California's economic future, and a speculation on whether American capitalism can manage existential infrastructure challenges.

Financial Performance Post-Bankruptcy

The numbers are undeniably strong. GAAP earnings were $1.15 per share for the full year of 2024. Operating cash flow hit $8 billion, up 70% year-over-year. The company generated $2.47 billion in profit—a record. These aren't the metrics of a distressed company but of a thriving monopoly.

The balance sheet has been restructured for growth. Debt-to-equity ratios are manageable. The $15 billion federal loan guarantee provides cheap capital for infrastructure investment. The company has pre-funded its equity needs through 2028. Financially, PG&E looks stronger than it has in decades.

But these numbers come with an asterisk: they're enabled by massive rate increases. Customers are paying for PG&E's recovery through the highest utility bills in America. This is politically unsustainable. Either rates moderate (killing earnings growth) or political intervention intensifies (threatening the regulatory compact).

Rate Base Growth and Guaranteed Returns Model

PG&E's $63 billion capital plan through 2028 represents one of the largest infrastructure investments in American history. Every dollar invested grows rate base, earning approximately 8% returns. Simple math suggests earnings should compound at high single digits for years.

The undergrounding program alone could add $20+ billion to rate base. Grid modernization, renewable interconnection, electrification support—each creates investment opportunities that regulators have pre-approved. It's a perpetual motion machine of capital deployment and guaranteed returns.

Yet this model assumes regulatory stability that may not exist. California faces a affordability crisis. Industrial customers are exploring self-generation to escape PG&E rates. Distributed solar and batteries threaten grid defection. The regulatory compact that guarantees returns could crack under political pressure.

Competitive Position vs. Other California Utilities

Within California, PG&E enjoys effective monopoly status across 70,000 square miles. Southern California Edison serves the south, SDG&E has San Diego, but PG&E controls the economic heart of California—Silicon Valley, San Francisco, the Central Valley.

This geographic monopoly is both blessing and curse. The blessing: captive customers including the world's most valuable companies who need reliable power regardless of cost. The curse: PG&E territory includes the most fire-prone regions of California. SCE and SDG&E face wildfire risk, but not at PG&E's scale.

Nationally, PG&E trades at a discount to utility peers—and should. No other utility faces comparable wildfire liability. But that discount may be excessive. PG&E's P/E ratio implies perpetual crisis when the company may have turned the corner on safety.

Climate Liability Overhang

This is the existential question: Has PG&E solved wildfire risk or just postponed the next catastrophe? The company points to two years without major wildfires, billions in safety investments, enhanced protocols. Critics note that two years is weather luck, not systematic improvement.

Climate science suggests conditions will worsen. Droughts will intensify. Heat waves will extend. Winds will strengthen. Every year, the baseline fire risk increases regardless of PG&E's mitigation efforts. The company is running ever faster just to stand still.

The $21 billion wildfire fund provides some protection, but it's finite. One or two Camp Fire-scale events would exhaust it. Then what? Another bankruptcy? State takeover? Federal bailout? The liability tail risk remains enormous and growing.

Political and Regulatory Risks

California politics are increasingly hostile to PG&E. Governor Newsom publicly excoriates the company. Legislators propose municipal takeover. Regulators face pressure to deny rate increases. The political environment has never been worse.

Yet PG&E has survived political hostility for decades through strategic adaptation. Campaign contributions, lobbying, strategic hiring—the company knows how to navigate California politics. The question is whether traditional influence can overcome post-Paradise public rage.

Federal involvement adds complexity. The DOE loan guarantee comes with strings. Federal criminal probation continues. Climate policy could mandate changes that destroy PG&E's business model. Political risk isn't just state-level anymore.

Bull Case

The bull case is straightforward: PG&E is a regulated monopoly providing essential service in the world's fifth-largest economy. It will earn guaranteed returns on $63 billion of necessary investment. California has no choice but to support PG&E because alternatives don't exist. Buy the discount, collect growing earnings, wait for multiple expansion as wildfire risk recedes.

Bulls point to operational improvements, safety investments, regulatory support for capital plans. They note that even assuming periodic wildfire liabilities, the base business generates enormous cash flow. At current valuations, the market prices in perpetual crisis when the reality may be steady improvement.

The strategic position is unassailable. California needs massive grid investment for electrification. Only PG&E can deliver it. The state will complain but ultimately support whatever rates PG&E needs. It's too big to fail with a growth runway measured in decades.

Bear Case

Bears see a company one wildfire away from third bankruptcy. Climate change is accelerating. Safety investments can't overcome physics—hot, dry, windy conditions will cause fires regardless of maintenance. Political pressure will cap rates below cost recovery. Distributed energy will erode the customer base. PG&E is a melting ice cube dressed up as a growth story.

The liability tail is unlimited. Inverse condemnation means PG&E is liable for fires regardless of negligence. Jury awards trend higher. Insurance is increasingly unavailable. The next Paradise could trigger $50 billion in claims. The wildfire fund is a bandaid on a bullet wound.

Most damning: PG&E's culture hasn't truly changed. Same management DNA, same regulatory capture, same financial engineering. The company has learned to manage bankruptcy, not prevent disasters. It's not a question of if but when the next catastrophe strikes.

XII. Epilogue: The Future of Energy Infrastructure

Stand at Donner Pass in the Sierra Nevada, where transcontinental railroad builders battled blizzards in the 1860s. Look west toward Sacramento, where hydraulic mining destroyed rivers for gold. Look east toward Nevada, where atomic bombs tested the limits of human power. This landscape tells the story of American infrastructure—ambitious, destructive, essential, tragic.

PG&E embodies all these contradictions. It brought light to California, powered Silicon Valley's rise, enabled the state's economic miracle. It also killed people through negligence, destroyed Paradise through deferred maintenance, represents everything wrong with American capitalism's treatment of public goods.

The future requires reimagining utility business models for a climate-changed world. Grid modernization isn't just upgrading equipment—it's rethinking the fundamental relationship between infrastructure and environment. Can overhead lines exist in fire country? Should critical infrastructure be privately owned? How do we price existential risk?

Distributed energy offers one path: rooftop solar, home batteries, microgrids. If every building generates and stores power, transmission lines become less critical. But distributed systems have their own challenges—reliability, equity, technical complexity. The utility death spiral—where departing customers raise rates on those remaining—could strand poor communities with deteriorating infrastructure.

Public ownership presents another option. Municipal utilities, public power authorities, cooperative models. But government ownership doesn't eliminate climate risk or maintenance challenges. It just changes who bears the cost when systems fail. The track record of public power is mixed—sometimes better, sometimes worse, always political.

Climate adaptation costs will transform utility economics regardless of ownership structure. Undergrounding lines, hardening infrastructure, managing shutoffs—these are expensive necessities, not optional upgrades. Someone must pay, whether through rates, taxes, or reduced returns. The era of cheap, reliable electricity may be ending just as electrification becomes essential for decarbonization.

PG&E's story offers lessons but no easy answers. Natural monopolies require regulation but capture their regulators. Essential infrastructure requires maintenance but incentives favor new construction. Climate change requires adaptation but costs are staggering. Private ownership brings efficiency but externalizes risk. Public ownership ensures service but politicizes operations.

What's certain is that PG&E represents the beginning, not the end, of utility climate crisis. Every utility with exposed infrastructure faces similar challenges. Hurricane-prone utilities in the Southeast. Flood-exposed systems in the Midwest. Drought-threatened hydroelectric in the Southwest. PG&E is the canary in the coal mine—if a canary could burn down towns and declare bankruptcy twice.

The investment implications are profound. Utilities have been widow-and-orphan stocks, safe harbors for conservative capital. That era is over. These are now climate speculation vehicles, betting on weather patterns and political responses. The stable 4% dividend yield has been replaced by binary outcomes—steady returns or catastrophic losses.

For California, PG&E remains inescapable. The company is woven into the state's infrastructure, economy, and future. Every electric vehicle needs PG&E's grid. Every renewable energy project needs PG&E's transmission. Every economic development depends on PG&E's reliability. The state and company are locked in an unhappy marriage—unable to live together, unable to divorce.

The human dimension transcends financial analysis. 86 people died in Paradise. Families lost everything in fires sparked by century-old equipment. Communities live in fear each fire season. Behind every earnings report and regulatory filing are real people bearing the cost of infrastructure failure.

Yet PG&E employees—linemen, engineers, tree trimmers—also serve communities, restore power after storms, maintain the systems that enable modern life. They're not villains but workers trapped in a broken system. The tragedy isn't individual evil but systematic failure—incentives that made disasters inevitable.

Looking forward, PG&E will likely survive and even thrive financially. The regulatory model ensures it. California needs it. Climate adaptation spending will drive earnings for decades. But survival isn't success if it comes through extracting maximum rates for minimum service while communities burn.

The ultimate question isn't whether PG&E is a good investment—it's whether American capitalism can manage essential infrastructure in an era of climate change. PG&E suggests the answer is: yes, but at enormous cost, with periodic disasters, through repeated crises, and only when forced by catastrophe to change.

Perhaps that's the best we can expect—muddling through climate change one bankruptcy at a time, learning from disasters, adapting reluctantly, paying whatever it costs because alternatives don't exist. It's not inspiring, but it's human. And in the end, PG&E is a human institution—flawed, essential, tragic, enduring.

The lights are still on in California. For now.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube