PACCAR: From Railway Cars to Global Truck Dominance

I. Introduction & Episode Overview

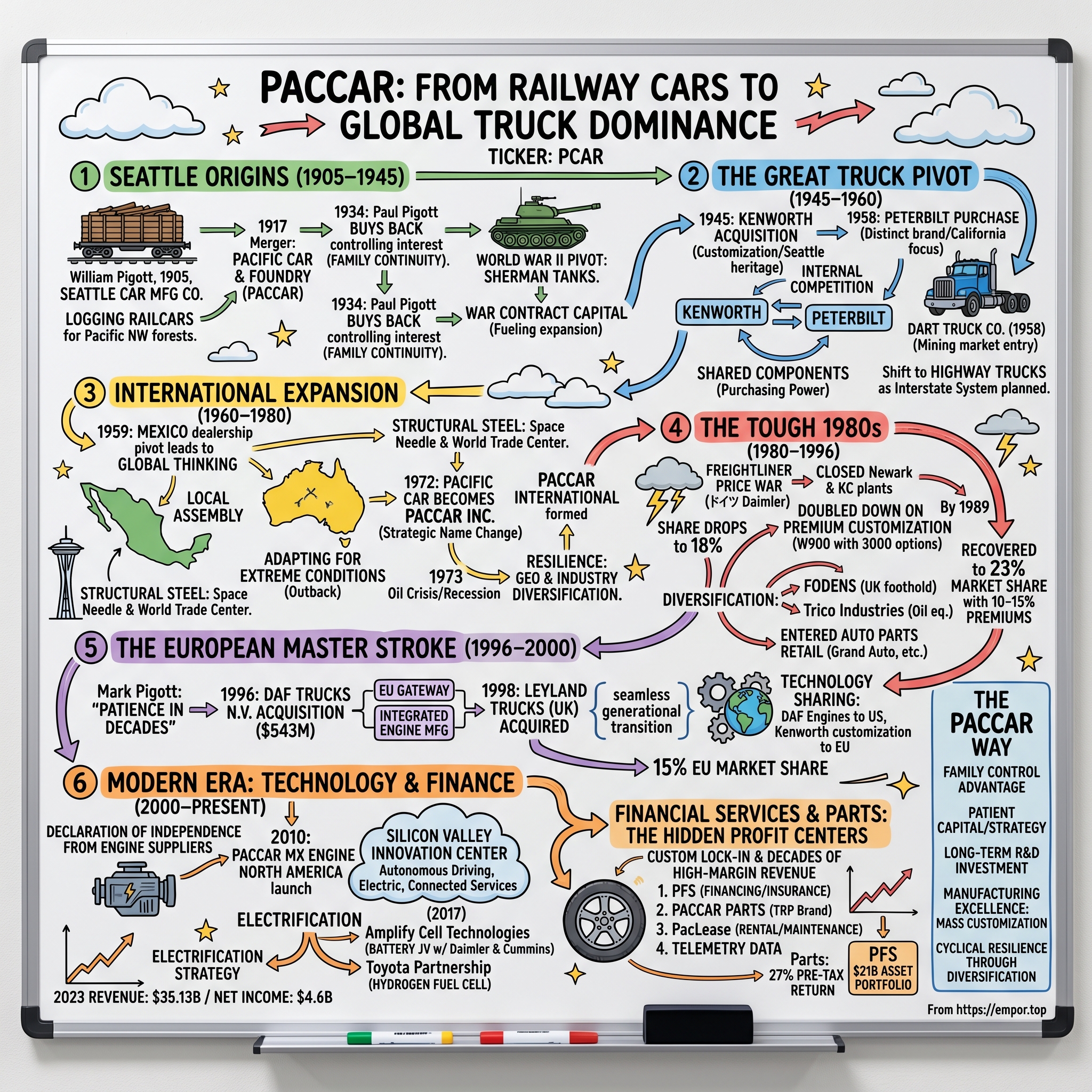

Picture this: A century-old company that most Americans have never heard of, yet whose products thunder past them on highways every single day. A business that started building railway cars for logging operations in the Pacific Northwest forests, pivoted into tanks during World War II, and somehow emerged as one of the most profitable truck manufacturers on the planet. This is PACCAR—a $60 billion market cap giant hiding in plain sight, owner of the iconic Peterbilt and Kenworth brands that dominate American highways, plus DAF trucks that rule European roads.

Here's what's remarkable: In an industry known for brutal cyclicality and razor-thin margins, PACCAR consistently generates returns on equity above 20%. While competitors struggle through downturns, PACCAR has paid dividends for 83 consecutive years. The company ranks second in U.S. heavy-duty truck production behind only Daimler, and third globally—yet it commands premium prices that would make luxury carmakers envious.

The central question isn't just how a railway car manufacturer became a trucking powerhouse. It's how four generations of the Pigott family built what might be the best-run industrial company nobody talks about. While Tesla captures headlines with electric semi-trucks and autonomous driving promises, PACCAR quietly generates $5 billion in annual profits selling trucks that cost $200,000 each—and customers gladly pay the premium. This is a story of engineering excellence, financial discipline, and perhaps most remarkably, family continuity. As trucks haul America's commerce across interstates today, PACCAR generates over $3 billion in annual profits with gross margins approaching 31%—metrics that would make Silicon Valley companies envious. The journey from timber railway cars to this industrial powerhouse reveals crucial lessons about patient capital, brand building, and the power of thinking in decades rather than quarters.

What follows is the untold story of how the Pigott family built an American industrial dynasty that has quietly outperformed nearly every company in the S&P 500 over the past half-century. It's a playbook for building enduring value in capital-intensive industries—one acquisition, one truck, and one generation at a time.

II. The Pigott Dynasty & Seattle Origins (1905–1945)

The rain was coming down hard in Seattle on that February morning in 1905 when William Pigott signed the papers to establish the Seattle Car Manufacturing Company. At 45 years old, Pigott had already spent a decade in the Pacific Northwest, watching the timber industry explode around him. The forests of Washington and Oregon held billions of board feet of lumber, but getting those massive logs out of the woods required specialized equipment—heavy-duty railway cars that could handle loads no standard railcar could bear.

Pigott didn't just see logs; he saw infrastructure. The logging railroads snaking through the Northwest forests needed cars built like tanks, capable of carrying Douglas firs so large it took a dozen men just to load one. His Seattle Car Manufacturing Company absorbed Railway Steel and Supply, instantly gaining the metalworking expertise to build these behemoths. Within months, orders were pouring in from timber companies desperate for equipment that wouldn't buckle under the weight of old-growth giants.

By 1917, Pigott recognized he needed scale. The merger with Portland's Twohy Brothers created Pacific Car and Foundry Company—a name that would endure for the next 55 years. The combined entity could now bid on contracts that Seattle Car alone couldn't handle. They built freight cars, logging cars, refrigerated cars for the booming Pacific fish trade. But William Pigott's real genius wasn't in what he built—it was in how he built it. Quality over quantity became the company mantra. While competitors churned out standard designs, Pacific Car customized. Every customer got exactly what they needed, even if it meant lower volumes and longer build times.

Then came 1924, a year that nearly ended the Pigott dynasty before it truly began. William sold control to American Car and Foundry Company, the industry giant based back East. Perhaps he was tired, perhaps the offer was too good to refuse. But his son Paul watched this transaction with different eyes. Paul Pigott had grown up in the Seattle yards, understood the business in his bones. When the Depression hammered American Car and Foundry a decade later, Paul saw opportunity where others saw disaster. In 1934, he scraped together financing and bought back a controlling interest in Pacific Car. The prodigal son had returned—and with him, a vision that extended far beyond railway cars.

World War II transformed everything. Suddenly, Pacific Car's heavy metalworking expertise was exactly what the U.S. military needed. The company pivoted from railway cars to Sherman tanks, producing these 30-ton war machines with the same obsessive attention to quality that had defined their logging cars. Workers who had spent years perfecting welds on railcars now applied those skills to armor plating. The company built tank recovery vehicles, military cargo carriers, anything the war effort demanded.

But Paul Pigott was thinking beyond the war. As he walked the factory floors in 1944, watching Sherman tanks roll off the line, he saw something else entirely. The highways being planned across America—Eisenhower's interstate system was still a decade away, but the vision was already forming. The economy would boom after the war. Goods would need to move. And trains, for all their efficiency, couldn't deliver to every corner of America.

"We're going to build trucks," Paul told his board in late 1944. Some thought he was crazy. Pacific Car knew metal fabrication, but trucks? That was a different business entirely—engines, drivetrains, complex mechanical systems they'd never touched. Paul didn't care about the skeptics. He'd already identified his target: a small Seattle company called Kenworth that built custom heavy-duty trucks. They had the expertise Pacific Car lacked. All Paul needed was the right moment to strike.

The war had taught Pacific Car something invaluable: how to pivot quickly while maintaining quality. They'd gone from railway cars to tanks in months. The leap to trucks would be harder, but Paul Pigott had patience. More importantly, he had capital from those profitable war contracts. As 1945 dawned and victory in Europe seemed assured, Paul prepared his masterstroke. The age of railways was giving way to the age of highways. Pacific Car would transform with it.

III. The Great Truck Pivot: Kenworth & Peterbilt Acquisitions (1945–1960)

The telegram arrived at Pacific Car's Seattle headquarters in March 1945: Kenworth Motor Truck Company was for sale. Paul Pigott had been circling this opportunity for months, watching as Kenworth's owners grew tired of the truck business's brutal cycles. Within weeks, Pacific Car made its move, acquiring Kenworth for a price that would seem laughable today—just over $1 million for a company that would become the crown jewel of a $60 billion empire.

Kenworth wasn't just any truck company. Founded in 1923 by Harry Kent and Edgar Worthington (hence Ken-worth), it had built its reputation on the same principle that defined Pacific Car: customization over commoditization. While Ford and General Motors cranked out standardized trucks, Kenworth would build anything a customer dreamed up. Need a truck to haul logs through mountain passes? Kenworth would engineer it. Want something to survive Alaska's ice roads? They'd figure it out. During the war, they'd built specialized military trucks, learning lessons that would prove invaluable in peacetime.

Paul Pigott kept Kenworth's management team intact—a decision that would become a PACCAR hallmark. He understood something fundamental: you don't buy a company for its factories; you buy it for its people and culture. The Kenworth engineers who had spent the war years perfecting military vehicles now turned their attention to the booming postwar economy. America was building—subdivisions, shopping centers, highways—and all that construction required trucks.

But Paul wasn't satisfied with just Kenworth. As he studied the truck market through the late 1940s and early 1950s, he noticed something interesting: Kenworth dominated the Northwest, but struggled to penetrate California and the Southwest. Down in Oakland, another custom truck manufacturer was facing its own challenges. Peterbilt Motors Company had been founded by T.A. Peterman, a plywood manufacturer and entrepreneur who needed trucks to haul logs and decided to build his own. After Peterman's death in 1944, the company had passed through several hands, each owner struggling to find the right strategy. In 1958, Pacific Car and Foundry greatly expanded its heavy-duty truck capability with the purchase of Peterbilt Motors Company. The Oakland company had gone through turmoil since founder T.A. Peterman's death in 1945. His widow Ida had sold the assets to seven management employees who tried to keep the company going. But when Mrs. Peterman announced her plans to develop the plant site into a shopping center in 1958, the aging management team faced a choice: raise $2 million for a new facility or sell.

Paul Pigott saw his opening. Here was a truck manufacturer with an impeccable reputation for quality, a loyal customer base in California and the Southwest, and a product line that perfectly complemented Kenworth. The genius wasn't just in buying Peterbilt—it was in how Paul structured the deal and what he did afterward.

First, he kept the brands completely separate. While Ford and General Motors were consolidating brands and standardizing platforms, Paul maintained Peterbilt's Oakland identity and Kenworth's Seattle heritage. "Let them compete," he told his executives. "Competition makes both stronger." This internal rivalry would become one of PACCAR's secret weapons. Peterbilt and Kenworth salesmen competed fiercely for customers, engineers raced to outdo each other with innovations, and both brands pushed quality standards ever higher.

The companies also targeted different psychographics. Kenworth positioned itself as the engineer's truck—practical, durable, built for the long haul. Peterbilt became the driver's truck—chrome everywhere, that distinctive red oval logo, a machine that made its owner feel like king of the road. One company joke went: "Kenworth builds trucks for companies that employ drivers. Peterbilt builds trucks for drivers who own companies."

Paul also acquired Dart Truck Company in 1958, which permitted its entry into the entirely new market of mining vehicles. While less glamorous than highway trucks, these specialized vehicles for mines and construction sites offered fat margins and minimal competition. It was classic Pigott thinking: find niches where quality matters more than price.

By 1960, Pacific Car had transformed from a regional railcar manufacturer into a diversified vehicle powerhouse. The company was building highway trucks, mining vehicles, and still producing railcars and structural steel. But Paul Pigott's masterstroke wasn't diversification—it was integration. Kenworth and Peterbilt began sharing certain components while maintaining distinct identities. Purchasing power doubled. Engineering insights crossed between brands. Financial strength from railcar contracts supported truck R&D during downturns.

The timing proved perfect. As Paul had predicted back in 1944, America's interstate highway system was finally becoming reality. The Federal-Aid Highway Act of 1956 had authorized 41,000 miles of highways. Suddenly, trucking could compete with rail for long-distance freight. And who better to supply those trucks than the company that had spent 15 years perfecting customization and quality while competitors chased volume?

IV. International Expansion & Becoming PACCAR (1960–1980)

Charles Pigott was standing in a Kenworth dealer's lot in Mexico City in 1959 when he had his epiphany. The dealer, struggling to import trucks from Seattle, was pleading for local assembly. "Senior Pigott," he said, "Mexico is building highways everywhere. We need hundreds of trucks. But the import duties are killing us." Charles, who had just taken over day-to-day operations from his father Paul, saw opportunity where others saw obstacles.

Within a year, PACCAR became an international truck manufacturer. Kenworth moved into Mexico with 49 percent participation in an affiliate company, Kenworth Mexicana S.A. de C.V., and in 1966 PACCAR entered the Australian truck market with the establishment of a Kenworth Truck assembly plant near Melbourne. These weren't just satellite operations—they were laboratories for learning how to operate globally while thinking locally.

The Australian venture particularly showcased PACCAR's adaptive genius. Australian trucks faced conditions American engineers couldn't imagine: road trains hauling three trailers across thousand-mile stretches of outback, temperatures that could melt asphalt, dust that infiltrated everything. Rather than simply shipping Seattle-designed trucks, Kenworth Australia began modifying designs for local conditions. Larger radiators, modified air filters, reinforced suspensions—each adaptation taught the company something new about engineering extremes.

Meanwhile, back in Seattle, Pacific Car's structural steel division was entering its golden age. The Space Needle, that impossible-looking flying saucer on a stick that would define Seattle's skyline, rose from Pacific Car steel in 1961. The technical challenge—building a structure that could withstand earthquakes and 200 mph winds while looking impossibly delicate—pushed the company's engineering capabilities to new heights.

But the project that truly displayed Pacific Car's industrial might came a few years later. The company provided 5,668 steel panels, weighing 58,000 tons, which formed a major part of the load bearing walls for New York City's World Trade Center twin towers. Think about the logistics: fabricating panels in Seattle to tolerances measured in millimeters, shipping them on 1,600 railcars across the continent, knowing that a single error could delay the world's tallest buildings. It was a testament to the precision culture William Pigott had instilled 60 years earlier.

By 1970, Charles Pigott faced a different challenge than his father or grandfather. The company had become so diversified—trucks, steel, railcars, international operations—that the old name no longer fit. "Pacific Car and Foundry Company" sounded like a regional railcar manufacturer, not a global industrial conglomerate. Directors and shareholders voted to adopt PACCAR Inc as the new name in 1972.

The name change symbolized more than corporate evolution—it marked a strategic shift. In 1972 PACCAR formed PACCAR International, which promoted company exports. Charles understood that American trucking was maturing. Growth would come from emerging markets where highways were just being built, where trucking industries were nascent, where PACCAR's reputation for quality could command premium prices.

The 1970s should have been triumphant, but they turned brutal. The 1973 oil crisis doubled fuel prices overnight. The 1974-75 recession hammered truck sales. Inflation hit double digits. Lesser companies folded or merged. But PACCAR had something others didn't: patient family capital and diversification across geographies and industries. When U.S. truck sales collapsed, Australian mining trucks kept cash flowing. When steel construction slowed, international exports grew.

Charles Pigott used the downturn to invest in the future. The PACCAR Technical Center was established in 1980 in Mount Vernon, Washington, as a research and testing facility. While competitors cut R&D, PACCAR built a state-of-the-art facility for testing everything from aerodynamics to component durability. The message was clear: PACCAR would emerge from the recession stronger, more technologically advanced, and ready for whatever came next.

V. The Tough 1980s: Competition, Crisis & Strategic Repositioning

The 1980s opened with PACCAR facing its darkest hour since the Depression. Interest rates hit 20%. Truck sales nationwide plummeted 50%. But the real threat came from an unexpected source: Freightliner, the trucking subsidiary of German giant Daimler-Benz, had declared war on the premium truck market. Their strategy was brutal in its simplicity—undercut Kenworth and Peterbilt on price while claiming equal quality.

By the mid-1980s, PACCAR's share of Class 8 trucks dropped to about 18% owing to aggressive competition from Freightliner Trucks. The company that had never competed on price suddenly found customers defecting for cheaper alternatives. Freightliner's corporate parent could absorb losses indefinitely. Volvo and Mack merged operations to gain scale. General Motors' truck division slashed prices. It was a bloodbath.

Charles Pigott faced an agonizing decision in 1986. PACCAR was forced to close its Kenworth assembly plant in Kansas City in April 1986 and its Peterbilt plant in Newark, California, the following October. For a company that prided itself on loyalty to employees and communities, the closures were devastating. But Charles understood a fundamental truth: survival required focus. PACCAR would concentrate production in fewer, more efficient facilities while doubling down on what differentiated them—customization and quality.

The company's response to the crisis revealed strategic thinking that would define PACCAR for decades. First, rather than chase Freightliner down-market, they moved further upmarket. If customers wanted cheap, standardized trucks, they could buy Freightliner. If they wanted a truck tailored exactly to their needs, with the best components money could buy, they bought Kenworth or Peterbilt.

Second, PACCAR diversified beyond Class 8 trucks entirely. In 1980 they acquired Fodens Limited, a British company and one of the oldest truck producers in the world. Foden gave PACCAR a foothold in Europe and expertise in different truck configurations. PACCAR acquired Trico Industries in 1986, a manufacturer of oil exploration equipment based in Gardena, California, for $65 million. When oil prices rebounded, Trico's specialized pumps would generate enormous margins.

The third move seemed bizarre at the time: In 1987, PACCAR entered the automotive parts & accessories retail market by acquiring Al's Auto Supply and Grand Auto Incorporated. Why would a truck manufacturer buy auto parts stores? Charles Pigott understood something Wall Street missed—parts and service generated higher margins than selling trucks. These retail chains would teach PACCAR about inventory management, customer service, and aftermarket dynamics that would prove invaluable later.

But the real genius of the 1980s strategy was in what PACCAR didn't do. They didn't panic and slash quality to cut costs. They didn't merge with competitors to gain false scale. They didn't abandon their customization strategy to chase volume. While competitors commoditized their products, PACCAR made each truck more specialized, more customized, more premium.

A typical Kenworth W900 from this era might have 3,000 different option combinations. Customers could specify everything from gear ratios to seat fabrics. Yes, this complexity was expensive. Yes, it slowed production. But it also meant that once a customer speced out their perfect truck, they couldn't easily switch to a competitor. The truck became part of their business identity.

The strategy worked. By 1989, PACCAR's market share had recovered to 23%. More importantly, they commanded price premiums of 10-15% over competitors. A Freightliner might haul freight just fine, but owner-operators wanted that Peterbilt badge on the grille. Fleet managers knew Kenworth's residual values stayed higher. The crisis of the mid-1980s had forced PACCAR to clarify its identity: they weren't in the truck business; they were in the premium truck business.

VI. The European Master Stroke: DAF & Leyland (1996–2000)

Mark Pigott was sitting in a conference room in Eindhoven, Netherlands, in February 1996, staring at spreadsheets that would determine PACCAR's future. Across the table sat the board of DAF Trucks N.V., a Dutch company that had emerged from bankruptcy just three years earlier. The meeting was the culmination of a chess game that Charles and Mark Pigott had been playing for over a decade.

During the mid-80's PACCAR had been negotiating with the Rover Group for acquiring its British Leyland truck division. However, Rover management decided to sell the truck division to DAF Trucks. That deal had taught the Pigotts patience. They watched as DAF struggled to integrate Leyland, eventually collapsing under debt in 1993. When DAF emerged from bankruptcy, cleaned up and reorganized, PACCAR was ready.

In 1996, the company spent $543 million to acquire DAF Trucks N.V. The price seemed steep for a recently bankrupt company, but Mark Pigott saw what others missed. DAF wasn't just a truck manufacturer—it was a gateway to the European Union's 350 million consumers. More importantly, DAF had something PACCAR desperately needed: fully integrated engine manufacturing.

While Kenworth and Peterbilt had always sourced engines from suppliers like Caterpillar and Cummins, DAF had been building its own engines since 1957. These weren't just any engines—they were among the most fuel-efficient in the world, designed for European regulations that were years ahead of American standards. As emissions rules tightened globally, owning engine technology would become crucial.

In 1997 Mark Pigott assumed PACCAR's presidency as Charles Pigott retired. The generational transition was seamless—Charles had been grooming Mark for years, and the board barely blinked. But Mark brought a different perspective. While his grandfather Paul had been an engineer and his father Charles a manufacturer, Mark was a financier. He'd worked on Wall Street, understood capital markets, and saw opportunities in financial engineering that previous generations had ignored.

Mark's first major move was completing the European consolidation. In 1998, PACCAR acquired UK-based Leyland Trucks, a manufacturer known for its light and medium truck (6 to 44 metric tons) design and manufacture capability. This was the same Leyland division PACCAR had tried to buy in the 1980s, now available at a fraction of the cost. The irony wasn't lost on Mark—patience in the Pigott family was measured in decades, not quarters.

With DAF and Leyland combined, PACCAR suddenly controlled 15% of the European heavy truck market. But more importantly, they had a complete product portfolio—light, medium, and heavy trucks, plus engines, all designed for global markets. The American Kenworth and Peterbilt brands gave them premium positioning. The European DAF brand provided volume and technology. It was a combination no competitor could match.

The integration strategy was vintage PACCAR. Rather than forcing American management on European operations, Mark kept DAF's Dutch leadership team intact. Rather than standardizing products globally, each brand maintained its regional identity. But beneath the surface, PACCAR began sharing technologies. DAF's engines would eventually power American trucks. Kenworth's customization systems would enhance DAF's offerings. Purchasing power doubled overnight.

Wall Street initially hated the deal. Why was a profitable American truck maker buying troubled European assets? The answer became clear during the 2001 recession. When American truck sales collapsed after 9/11, European operations kept generating cash. When European markets slumped, American operations compensated. PACCAR had become recession-resistant through geographic diversification.

The DAF acquisition also transformed PACCAR's financial profile. DAF's integrated operations—they made everything from engines to axles—meant higher margins on parts and services. European customers expected full-service lease agreements, teaching PACCAR new financial products. The company was evolving from a truck manufacturer into a transportation solutions provider.

By 2000, PACCAR had achieved something remarkable: they were simultaneously the most American and most international truck company. Peterbilt still embodied the American trucker mythos. DAF dominated European highways. Yet behind these distinct brands operated a single, highly efficient global company. Mark Pigott had completed the transformation his grandfather started—from a Seattle railcar maker to a global transportation powerhouse.

VII. Modern Era: Technology, Engines & Financial Power (2000–Present)

The engineers at PACCAR's Columbus, Mississippi facility held their breath on a humid morning in September 2010 as the first PACCAR MX engine rolled off the assembly line. This wasn't just another product launch—it was PACCAR's declaration of independence from engine suppliers after 65 years of dependence on Caterpillar and Cummins.

PACCAR unveiled its PACCAR MX engine line for North America in 2010. While the MX engine was new to the North American market, DAF has been building engines in Europe since 1957. PACCAR invested $400 million in the PACCAR Engine factory and technology center in Columbus, Mississippi. The facility represented the largest single capital investment in company history, but Mark Pigott knew the stakes. Emissions regulations were tightening. Customers demanded better fuel economy. Controlling engine technology meant controlling their destiny.

The MX engine showcased PACCAR's evolved strategy: leverage global expertise for local markets. European DAF engines, refined over 50 years, were adapted for American conditions—longer distances, heavier loads, different fuel blends. The result was an engine that delivered European fuel efficiency with American durability. Within five years, over 40% of Kenworth and Peterbilt trucks would carry PACCAR power.

In 2013, PACCAR expanded its global operations with the opening of a new DAF factory in Ponta Grossa, Brasil. The company invested $320 million in the 300,000 sq ft assembly facility. Brazil represented the last frontier in global trucking—a continental market dominated by local manufacturers but hungry for premium quality. PACCAR's entry was methodical: start with assembly, build dealer networks, then gradually increase local content to avoid import duties.

But the real revolution was happening in Silicon Valley. PACCAR announced its Silicon Valley Innovation Center in Sunnyvale, California in 2017. The location was strategic—recruiting software engineers was easier in Sunnyvale than Seattle, and proximity to tech giants facilitated partnerships. The center focused on three areas: autonomous driving, electric powertrains, and connected vehicle services.

The financial results of this technology-focused strategy were staggering. PACCAR achieved record revenues of $35.13 billion in 2023, compared to revenues of $28.82 billion in 2022. The company earned $4.60 billion in 2023, excluding a one-time European litigation charge. These weren't just good numbers—they were spectacular margins for a capital-intensive manufacturer. What's striking about PACCAR's modern strategy is the balance between cutting-edge technology and old-fashioned conservatism. The expanded agreement with Toyota supports ongoing development and commercialized zero-emission versions of the Kenworth T680 and Peterbilt 579 models featuring Toyota's hydrogen fuel cell powertrain kit, with initial customer deliveries planned for 2024. Yet simultaneously, Amplify, their battery joint venture with Daimler and Cummins, will soon begin construction of a 21-gigawatt hour factory in Marshall County, Mississippi, expected to create more than 2,000 U.S. manufacturing jobs and targeting the start of production operations in 2027.

This dual-track approach to electrification—betting on both batteries and hydrogen—exemplifies the Pigott family's risk management philosophy. They're not trying to pick winners in the energy transition. They're positioning to win regardless of which technology prevails. It's the same strategy that led them to maintain separate Kenworth and Peterbilt brands, to diversify globally while staying rooted in America, to build engines while still offering competitor powertrains.

The numbers validate this approach. For the first nine months of 2024, PACCAR achieved net sales and revenues of $25.76 billion with net income of $3.29 billion. These aren't just good results—they're exceptional for a cyclical industrial company. The secret lies in the transformation from truck manufacturer to financial services powerhouse, a shift that began decades ago but has accelerated under Mark Pigott's leadership.

VIII. Financial Services & Parts: The Hidden Profit Centers

Walk into any truck stop in America and you'll hear drivers arguing about engines, transmissions, and fuel economy. What they don't discuss—but what Wall Street should obsess over—is how PACCAR has built two businesses that generate higher returns than actually making trucks: financial services and parts distribution.

The evolution of PACCAR Financial Services represents one of the greatest untold stories in industrial finance. What began as a simple dealer financing program in the 1960s has morphed into a $21 billion asset portfolio generating consistent 15%+ returns on equity. The genius isn't just in financing truck purchases—it's in creating customer lock-in that spans decades.

Consider the lifecycle of a typical owner-operator who buys a Peterbilt. PACCAR Financial provides the loan, often at competitive rates because they understand truck values better than any bank. PACCAR's insurance subsidiary covers the vehicle. When maintenance is needed, PACCAR Parts supplies components through 2,200+ dealer locations worldwide. When it's time to upgrade, PACCAR Financial handles the trade-in and finances the new truck. The customer never leaves the ecosystem.

PACCAR Parts achieved record quarterly pre-tax income of $455.8 million in Q1 2024, compared to $438.6 million earned in the first quarter of 2023. First quarter 2024 revenues were a record $1.68 billion compared to $1.62 billion reported in the same period last year. Think about those margins—roughly 27% pre-tax returns on parts sales. For context, that's better than most software companies.

The parts business benefits from several structural advantages that competitors can't replicate. First, PACCAR trucks are famously customized, meaning generic aftermarket parts often don't fit properly. Second, the company's TRP (The Reliable Parts) brand, celebrating 30 years in 2024, offers over 157,000 parts for all makes of trucks—not just PACCAR brands. This positions them as a one-stop shop for mixed fleets.

But the real moat comes from technology investments most investors never see. PACCAR's managed dealer inventory system uses AI to predict parts demand, ensuring dealers stock exactly what customers need without tying up capital in slow-moving inventory. Their e-commerce platform allows customers to order parts 24/7 with same-day shipping in many markets. The company's fleet management software provides predictive maintenance alerts, driving parts sales before breakdowns occur.

The financial services division has evolved even more dramatically. PFS has a portfolio of 228,000 trucks and trailers, with total assets of $21.15 billion. This isn't just about loans—it's about data. Every truck financed provides telemetry on usage patterns, maintenance needs, and residual values. This information advantage allows PACCAR to price risk better than any competitor.

During downturns, this advantage becomes decisive. When used truck prices collapse, banks retreat from truck financing. PACCAR Financial stays, supporting dealers and customers through the cycle. This countercyclical lending builds loyalty that pays dividends when markets recover. Customers remember who stood by them when times were tough.

The integration between trucks, parts, and financing creates powerful network effects. A Kenworth truck with a PACCAR engine, financed by PACCAR Financial, maintained with PACCAR Parts, generates revenue streams that continue for 10-15 years after the initial sale. The company estimates that over a truck's lifetime, parts and service revenues can equal or exceed the original purchase price.

PacLease, the company's full-service leasing operation with over 41,000 vehicles, represents another hidden gem. As logistics companies increasingly prefer leasing to ownership, PacLease offers turnkey solutions—truck, maintenance, insurance, even driver training. The monthly recurring revenue from leasing provides stability during the volatile truck sales cycles.

What's remarkable is how PACCAR has achieved this transformation while maintaining its manufacturing excellence. They didn't abandon making trucks to become a financial company. Instead, they recognized that in mature industries, the real profits come from controlling the entire customer lifecycle. Every truck sold is just the beginning of a relationship that, if managed properly, generates decades of high-margin revenue.

IX. Playbook: The PACCAR Way

There's a moment in every PACCAR factory tour when visitors stop and stare. It's not at the robotic welders or the massive assembly lines. It's when they see a worker stop the entire production line because a bolt doesn't feel right. No manager approval needed. No questions asked. The line stops, the problem gets fixed, and only then does production resume. This seemingly small detail reveals everything about why PACCAR commands premium prices in a commodity industry.

The premium strategy starts with a fundamental rejection of transportation economics orthodoxy. Business schools teach that trucks are commodities—steel boxes that move freight from point A to point B. Price and fuel economy determine purchase decisions. Volume drives profitability. PACCAR's entire strategy refutes these assumptions.

Kenworth and Peterbilt achieved an "excellent" U.S. and Canadian Class 8 market share of 30.7% in 2024. But here's what's remarkable: they achieve this while charging 10-15% premiums over competitors. A fully loaded Peterbilt 589 can cost $200,000+, while a comparable Freightliner might be $170,000. Yet customers gladly pay the premium. Why?

First, customization creates emotional ownership. PACCAR offers thousands of option combinations—everything from seat materials to chrome packages to gear ratios optimized for specific routes. When a driver specs out their perfect truck, it becomes their truck in a way a standardized Freightliner never could. This is why Peterbilt and Kenworth have the highest residual values in the industry—buyers will pay more for a truck that was built just for them.

Second, the dealer network provides unmatched support. PACCAR dealers aren't just sales outlets—they're full-service transportation consultants. They'll analyze a customer's routes, recommend optimal specifications, arrange financing, and provide 24/7 service support. When a truck breaks down at 2 AM in Nebraska, that dealer relationship becomes priceless.

The family control advantage cannot be overstated. Four generations of Pigott leadership have provided something public companies can't: patient capital and consistent strategy. While competitors chase quarterly earnings, PACCAR invests in 10-year payback projects. While others cut R&D during downturns, PACCAR doubles down. The family owns enough stock to ignore Wall Street's short-term pressures.

This long-term orientation enables contrarian capital allocation. During the 2008 financial crisis, while competitors were desperately conserving cash, PACCAR increased capital expenditures by 20%. They emerged from the recession with newer factories, better technology, and gained market share from weakened rivals. The same pattern repeated during COVID—investing while others retreated.

Manufacturing excellence at PACCAR goes beyond quality control. They've mastered the art of "mass customization"—building highly personalized trucks at near-mass-production efficiency. The secret lies in modular design and sophisticated production planning. Core components are standardized, but customer-facing elements can be endlessly customized. It's the same strategy that powers Dell's computer business, applied to 80,000-pound trucks.

The company's capital allocation discipline deserves its own Harvard Business School case study. Over the past decade, PACCAR has returned over $15 billion to shareholders through dividends and buybacks while simultaneously investing $8 billion in capital expenditures and R&D. They've maintained net cash positions through multiple cycles. They've never diluted shareholders with equity raises. They've walking away from acquisitions when prices got silly.

Cyclical resilience through diversification is perhaps PACCAR's most underappreciated strength. When North American Class 8 sales collapse, European medium-duty trucks often thrive. When truck sales slump, parts and service revenues remain stable. When new truck demand drops, used truck financing picks up. The company has engineered itself to generate positive cash flow even in severe downturns.

The cultural elements are harder to quantify but equally important. PACCAR promotes from within—most senior executives have spent decades at the company. They maintain engineering offices at truck stops to get direct driver feedback. They still build trucks in small batches to maintain craftsmanship. These aren't just feel-good policies—they create institutional knowledge and customer loyalty that competitors can't buy.

What's most impressive is how PACCAR has maintained this playbook while adapting to technological change. They're investing heavily in electric and hydrogen trucks, but not abandoning diesel. They're developing autonomous driving technology, but not forgetting that drivers still matter. They're embracing digital tools while maintaining personal dealer relationships. It's evolution, not revolution—and that's exactly how the Pigott family likes it.

X. Analysis & Investment Case

The investment community consistently misunderstands PACCAR, viewing it through the lens of cyclical industrial companies when it's actually something far more sophisticated—a technology-enabled transportation finance company that happens to manufacture excellent trucks. This misperception creates opportunity for investors willing to look deeper.

Start with competitive positioning. Yes, Daimler Truck's Freightliner brand leads North American Class 8 sales with roughly 38% market share versus PACCAR's 31%. But market share tells you nothing about quality of earnings. Daimler competes primarily on price and volume. PACCAR competes on value and lifetime customer relationships. One strategy generates commodity returns; the other generates luxury goods margins.

Volvo's North American presence through Mack and Volvo Trucks presents a different challenge—they're pursuing PACCAR's premium strategy. But they lack PACCAR's dealer network density and customization capabilities. More importantly, Volvo must balance global standardization pressures with local customization needs. PACCAR's decentralized brand structure handles this tension better.

Navistar, now owned by Volkswagen's TRATON, represents the disruptive threat. They're investing heavily in electric trucks and autonomous technology, leveraging VW's massive R&D budget. But PACCAR has a crucial advantage: they don't need to be first in new technology, they need to be best. Their customers—owner-operators and small fleets—won't buy unproven technology. They'll wait for PACCAR to perfect it.

The electric truck transition presents both existential threat and generational opportunity. The threat is obvious: electric powertrains are simpler than diesel, potentially commoditizing the product and enabling new entrants. Tesla's Semi, Nikola's offerings, and Rivian's commercial vehicles all target PACCAR's profit pool.

But the opportunity might be greater. PACCAR owns 30% of Amplify Cell Technologies alongside Daimler and Accelera by Cummins, with EVE Energy serving as technology partner with 10% ownership contributing battery cell design and manufacturing expertise. This positions PACCAR to control battery costs—the largest component of electric truck economics. Moreover, electric trucks require sophisticated charging infrastructure and energy management—services PACCAR Financial is perfectly positioned to provide.

The hydrogen strategy provides optionality. Initial customer deliveries of hydrogen fuel cell trucks are planned for 2024, with serial production set to begin in 2025. While battery electric works for short-haul and urban delivery, long-haul trucking might require hydrogen's superior energy density. PACCAR's partnership with Toyota gives them access to leading fuel cell technology without bearing full development costs.

Financial metrics reveal PACCAR's true quality. The company consistently generates 20%+ returns on equity without leverage—almost unheard of in capital-intensive manufacturing. Gross margins approach 20%, operating margins exceed 15%, and the company maintains net cash positions through cycles. These aren't industrial company metrics; they're luxury goods metrics.

The bear case centers on four concerns. First, trucking cyclicality remains brutal—Class 8 sales can drop 50% in downturns. Second, autonomous trucks could eliminate owner-operators, PACCAR's most profitable customers. Third, new entrants with electric trucks could fragment the market. Fourth, a recession would hammer near-term earnings regardless of long-term positioning.

But the bull case is compelling. Brand strength in trucking rivals consumer brands—Peterbilt and Kenworth have generational loyalty. The aftermarket moat grows stronger as the installed base expands and trucks become more complex. Financial discipline means PACCAR can acquire distressed assets in downturns while competitors struggle to survive. Most importantly, the family control structure ensures long-term thinking in an increasingly short-term world.

Valuation presents the most interesting puzzle. PACCAR trades at roughly 12-15x forward earnings, a discount to the S&P 500 despite superior returns on capital. The market prices it like a cyclical industrial, not a high-quality compounder. This valuation gap exists because investors fear the next downturn, missing the secular growth in parts, services, and financial products.

What the market might be missing is the platform value. PACCAR isn't just selling trucks; they're building a transportation ecosystem. As logistics becomes increasingly complex—with electric charging, hydrogen refueling, autonomous operations, and predictive maintenance—customers need integrated solutions. PACCAR's combination of hardware excellence, financial strength, and service infrastructure positions them as the platform provider.

The real insight is that PACCAR has transformed from a cyclical manufacturer into an annuity-like business model. A truck sale initiates a 10-15 year revenue stream through financing, parts, and service. As the installed base grows and technology complexity increases, these recurring revenues become stickier and more profitable. The market values the volatile truck sales; it undervalues the growing annuity streams.

XI. Epilogue & Future Vision

Standing in PACCAR's boardroom in Bellevue, you can trace 120 years of American industrial evolution on the walls. Photos of William Pigott with his railway cars. Paul Pigott inspecting Sherman tanks. Charles in front of the first Kenworth assembly line. Mark shaking hands at the DAF acquisition. Four generations, one consistent vision: build the best, not the most.

The battery manufacturing joint venture with Daimler and Cummins represents PACCAR's next evolution. Rather than betting everything on one technology, they're hedging intelligently—batteries for urban delivery, hydrogen for long-haul, diesel for developing markets. It's portfolio theory applied to powertrains, and it's exactly what you'd expect from a company that has survived everything from the Great Depression to COVID-19.

PACCAR estimates it will invest $700-800 million on capital projects in 2025 and $460-500 million on research and development. The company is investing in truck factories, including expansions at Kenworth Chillicothe, Ohio, PACCAR Mexico, and the DAF electric truck assembly plant in Eindhoven, Netherlands, plus additional manufacturing and remanufacturing capacity for engines. The company expects to invest a total project amount of $600-900 million in its battery joint venture, Amplify Cell Technologies.

The autonomous trucking revolution poses fascinating questions. Will robot trucks eliminate owner-operators, PACCAR's core customers? Or will they create new business models where PACCAR provides Trucking-as-a-Service, managing autonomous fleets for logistics companies? The company's response has been characteristically pragmatic: partner with Aurora and Waymo to understand the technology, but don't abandon the human drivers who built the business.

The next generation of Pigott leadership remains unclear—Mark has led for over 25 years, longer than any previous family CEO. But the governance structure ensures continuity. Independent directors dominate the board. Professional managers run day-to-day operations. The family provides long-term vision, not nepotistic management. It's a model for multi-generational industrial companies.

If we were CEO, the strategy would be clear: double down on the platform approach. PACCAR should become the iOS of trucking—an integrated ecosystem where everything works better together. Imagine PACCAR-optimized routing software that minimizes fuel consumption. Predictive maintenance that schedules service during mandatory driver breaks. Financial products that adjust payments based on freight market conditions. The possibilities are endless when you control the truck, the data, and the customer relationship.

The key insight for founders is patience. PACCAR didn't become dominant overnight—it took four generations of consistent execution. They didn't chase every trend or pivot with market fashions. They picked a strategy—premium customized trucks—and refined it relentlessly. In an era of rapid disruption, there's something profound about building a business that your great-grandchildren will run.

For investors, PACCAR offers a masterclass in quality at a reasonable price. This isn't a high-growth story that will triple in three years. It's a compound wealth creator that will double every 5-7 years with minimal risk of permanent capital loss. In a market obsessed with disruption, sometimes the best investment is the company doing the disrupting slowly, methodically, and profitably.

The story of PACCAR is ultimately the story of American manufacturing evolution. From railway cars to tanks to trucks to transportation solutions, the company has repeatedly transformed itself while maintaining its core identity. As the industry faces its next transformation—electrification, automation, servitization—PACCAR's century of adaptation suggests they'll not just survive but thrive.

The Seattle rain still falls on PACCAR's headquarters, just as it did on William Pigott's railway car factory in 1905. But where William saw logs that needed moving, Mark sees data that needs analyzing, batteries that need managing, and transportation problems that need solving. The tools change, the challenges evolve, but the mission remains: build the best products, treat customers fairly, think in decades not quarters.

That's the PACCAR way. It's worked for 120 years. Smart money says it'll work for 120 more.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube