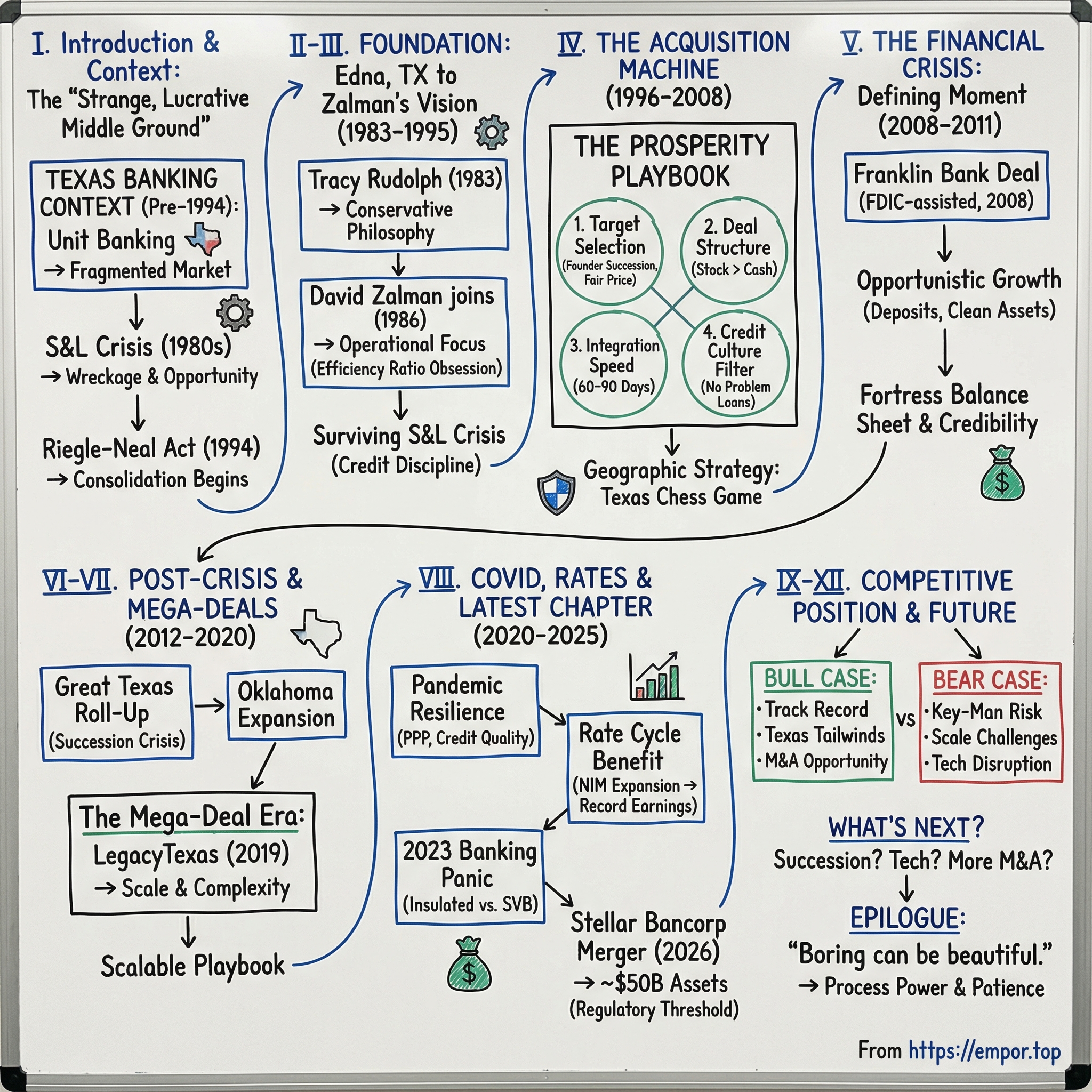

Prosperity Bancshares: The Story of Texas's Serial Acquirer

I. Introduction and Episode Roadmap

There is a certain kind of company that Wall Street never quite knows how to categorize. Not flashy enough to be a growth stock. Not distressed enough to be a turnaround. Not boring enough to be ignored. Prosperity Bancshares sits in that strange, lucrative middle ground — a nearly forty-billion-dollar Texas banking machine built not on innovation or disruption, but on the oldest strategy in capitalism: buy smart, run lean, repeat.

With over three hundred banking locations spread across Texas and Oklahoma, Prosperity Bancshares ranks as the second-largest Texas-headquartered bank by deposits. It has completed more than thirty acquisitions since the early 2000s alone, grown from a single branch in tiny Edna, Texas to a top-fifty U.S. bank, and maintained an efficiency ratio that makes its competitors look wasteful by comparison. It has navigated the savings and loan crisis, the 2008 financial meltdown, a global pandemic, and the 2023 regional banking panic — not just surviving each one, but using each one as a springboard for growth.

The central question of this story is deceptively simple: How did a small-town bank in rural Texas become one of America's most successful serial acquirers? The answer involves a banker named David Zalman who has spent nearly four decades perfecting a playbook so reliable it borders on boring. Conservative credit underwriting. Ruthless cost discipline. Lightning-fast acquisition integration. And an almost supernatural patience for waiting for the right deal at the right price.

What makes Prosperity's story worth telling is not any single dramatic moment. It is the compounding. The way one disciplined acquisition leads to the next, each one slightly larger, each one executed with the same methodical precision.

In an industry littered with blowups, fraud, and overleveraged collapses, Prosperity proves that boring and disciplined wins — consistently, repeatedly, profitably.

This is the story of how a forty-million-dollar community bank became a forty-billion-dollar powerhouse, and what it teaches us about the power of process, patience, and Texas.

One note before we dive in: banking stories often get dismissed as dry, numbers-heavy affairs. This one is different. Behind the spreadsheets and regulatory filings is a genuinely human story about a small-town Texan who figured out something fundamental about how to build lasting value — and then did it, over and over again, while the industry around him burned.

II. The Texas Banking Context and Regulatory Foundation

To understand Prosperity Bancshares, you first need to understand why Texas banking is different from banking anywhere else in America. And that difference starts with a peculiar regulatory history that created the very conditions Prosperity would later exploit.

For most of the twentieth century, Texas operated under what were called "unit banking" laws. Unlike states where banks could freely open branches across counties and cities, Texas restricted banks to operating from a single location — one bank, one building, one town. The result was a financial landscape unlike anything else in the country: thousands of tiny, independent banks, each serving a small community, each run by a local family or group of businessmen. By the early 1980s, Texas had more independent banks than almost any other state. It was a fragmented market of extraordinary proportions.

Then came the savings and loan crisis. The late 1980s devastated Texas banking with a ferocity that reshaped the entire state economy. Between 1980 and 1994, more than 1,600 banks and savings institutions failed in Texas — a staggering number that represented roughly a third of all bank failures nationwide during that period. The root causes were a toxic cocktail: reckless commercial real estate lending, oil price collapses that gutted the Texas economy, and regulatory frameworks that encouraged excessive risk-taking. Entire banking dynasties were wiped out. The FDIC and the Resolution Trust Corporation spent billions cleaning up the wreckage.

But from the rubble emerged opportunity — the kind of opportunity that only becomes visible to those who understand what they are looking at. Every crisis in banking history has produced two things: wreckage and a new generation of winners. Texas in the early 1990s was no different.

The Riegle-Neal Interstate Banking and Branching Efficiency Act of 1994 fundamentally changed the rules, allowing banks to acquire across state lines and consolidate branches across counties. For non-banking readers, this is crucial context: before Riegle-Neal, a bank in Houston could not acquire a bank in Dallas without navigating a labyrinth of state-by-state restrictions. After the act, the barriers to consolidation fell away, and banking became a national marketplace for the first time. Texas, with its thousands of small independent banks, suddenly became the richest consolidation opportunity in American banking. The regulatory barriers that had kept these banks small and independent were falling away just as many of their founders were aging out, their children uninterested in running a community bank, and the costs of regulatory compliance — particularly after Dodd-Frank in 2010 — were making small-bank economics increasingly painful.

This is the landscape that shaped Prosperity's strategy. Texas was not just a big state with a growing economy. It was a banking market with a structural surplus of acquisition targets — founder-led institutions with succession problems, regulatory fatigue, and a willingness to sell to the right buyer at the right price. The question was never whether Texas banking would consolidate. The question was who would do the consolidating.

The Texas economy itself added fuel. Oil and gas cycles created volatility, but the state's fundamental trajectory was unmistakable: population growth that outpaced the national average for decades, a business-friendly regulatory environment that attracted corporate relocations, no state income tax, and a diversifying economy that was steadily reducing its dependence on energy. Houston, Dallas, San Antonio, and Austin were all booming. Every new Texan needed a bank. And every retiring Texas banker needed an exit.

Think about it this way: if you wanted to design the perfect laboratory for a disciplined bank acquirer, you could not do better than late-twentieth-century Texas. A massive state with a booming economy. Thousands of independent banks with aging owners. Regulatory changes enabling consolidation. And a banking customer base that valued local relationships over national brands.

The ingredients were all there. Someone just needed the recipe.

This was the opportunity that a small community bank in Edna, Texas — population roughly five thousand — was about to seize.

III. Founding and Early Years: The Vision Takes Root (1983-1995)

Edna, Texas sits about a hundred miles southwest of Houston, the kind of place where everyone knows the bank president by first name and the biggest building in town might be the high school football stadium. In 1983, a businessman named Tracy T. Rudolph purchased a former Allied Bank branch there and renamed it First Bank. The institution had approximately forty million dollars in assets and ten employees. It was, by any objective measure, one of the smallest and most unremarkable banks in a state full of them.

Rudolph was not building a banking empire. He was building a community institution, and he brought to it a philosophy that would prove remarkably durable: serve the local community, lend conservatively, keep costs low, and treat deposits as the lifeblood of the business.

These sound like platitudes — the kind of bromides you find on the "About Us" page of every community bank's website.

But in the context of 1980s Texas, they were radical acts of restraint. This was an era when Texas banks were leveraging themselves into oblivion on speculative real estate and oil patch loans, when bankers were flying to Las Vegas to celebrate record earnings funded by loans that would never be repaid, when the phrase "Texas-sized" described not just the state's ambitions but its risk appetite. Against that backdrop, a small-town banker who simply refused to make risky loans was engaging in a kind of quiet rebellion.

The move that would define everything came in 1986 when a young banker named David Zalman joined as Executive Vice President. Zalman had graduated from the University of Texas at Austin in 1978 with a business degree and started his career as a cashier at a community bank with roughly forty million dollars in assets — almost exactly the same size as Prosperity itself. He had worked his way through various positions at community banks, learning the mechanics of small-bank operations from the ground up. He understood something fundamental about community banking: the margins were thin, the competition was local, and the only sustainable advantages were discipline in lending and efficiency in operations. It was not glamorous work. But it was the kind of work that compounded.

Zalman was elected to the parent company's board in 1987, rising quickly through the organization. What set him apart was not charisma or financial wizardry but a relentless operational focus. He obsessed over the efficiency ratio — the percentage of revenue consumed by operating expenses. For readers unfamiliar with banking metrics, think of the efficiency ratio as the banking equivalent of a restaurant's food cost percentage: it tells you how much of every dollar you bring in gets eaten by the cost of running the operation. In banking, an efficiency ratio below fifty-five percent is considered good. Below fifty percent is excellent. Zalman would eventually drive Prosperity's below forty percent, a level that borders on absurd in an industry laden with compliance costs, technology investments, and branch overhead. To put that in perspective: if the average bank spends fifty-five cents to generate a dollar of revenue, Prosperity spends less than forty-four cents. That eleven-cent difference, compounded across billions of dollars of revenue over decades, creates an almost unfathomable economic advantage.

Zalman also served on the board of the Federal Reserve Bank of Dallas — Houston Branch, giving him a front-row seat to the regulatory and economic forces shaping Texas banking. He was active in civic life too, serving on the El Campo City Council and various charitable organizations. But it was always the bank that consumed his focus. Colleagues described him as a details person, someone who could recite branch-level efficiency metrics from memory and who personally reviewed loan portfolios of acquisition targets.

While Texas banks were failing by the hundreds during the late 1980s and early 1990s, Prosperity survived by doing the opposite of what had killed its peers. No speculative commercial real estate lending. No concentrated oil and gas exposure. No reaching for yield with exotic financial products. Instead, the bank focused on bread-and-butter community banking: mortgage loans, small business lending, deposit gathering, and keeping overhead razor-thin.

This period also gave Prosperity its first taste of acquisition. Between 1988 and 1992, as the Texas banking crisis created a landscape of distressed institutions, Prosperity capitalized by acquiring deposits and select assets from failed banks. These were modest transactions — small-town branches, local deposit bases — but they taught the young organization something invaluable: how to absorb another bank's customers and operations without disrupting either. The integration muscle that would later become Prosperity's defining competitive advantage was being developed in these early, unglamorous deals.

By the mid-1990s, Prosperity had grown from its single Edna branch into a multi-location community bank, still small by any national standard but increasingly sophisticated in its understanding of acquisition-driven growth. The foundation was set: conservative credit culture, operational efficiency, and an emerging capability in bank integration.

There is an important counterfactual worth dwelling on here.

Why did Prosperity survive the S&L crisis when over 1,600 Texas institutions did not? The answer is not luck. It is temperament. The banks that failed in the 1980s had chased growth — making aggressive commercial real estate loans, lending into the oil patch at the peak of the cycle, leveraging their balance sheets to maximize short-term returns. Prosperity, under Rudolph's conservative philosophy and Zalman's operational discipline, simply refused to play that game. The returns were lower in the boom years, certainly. But when the music stopped, Prosperity still had a chair. This pattern — underperformance during manias, outperformance during panics — would repeat itself throughout the company's history. It is, in many ways, the defining characteristic of the Prosperity story.

What the company needed next was scale — and the capital markets access to pursue it.

IV. The Acquisition Machine Takes Shape (1996-2008)

The late 1990s marked a turning point. In 1999, Prosperity went public, listing on NASDAQ under the ticker PB. The IPO was not the kind of flashy debut that generates breathless CNBC coverage. It was a small Texas bank selling shares to fund its growth ambitions. But the significance was enormous.

Going public gave Prosperity two things it had lacked: access to capital markets for funding and — critically — stock as acquisition currency. Both would prove transformational. In banking M&A, the ability to offer stock rather than cash is a strategic weapon. Cash depletes capital ratios, which regulators watch closely. Stock preserves capital while using the market's valuation of the company as purchasing power. A well-run bank with a strong stock price can acquire without weakening its balance sheet. This asymmetry would become central to Prosperity's strategy.

In a banking industry where acquisition discipline often evaporates the moment a CEO gets access to cheap capital, what happened next at Prosperity was unusual: the discipline intensified.

Tracy Rudolph continued as Chairman and CEO through 2001, steering the company through its transition from private community bank to publicly traded institution. But it was David Zalman who increasingly shaped the company's strategic direction. Rudolph retired from active employment in 2001 after twenty-five years of cultivating the conservative banking philosophy that would become Prosperity's foundation. His legacy was not scale or headline-grabbing deals but something more durable: a credit culture so deeply embedded in the organization that it outlasted its creator.

When Zalman formally assumed the CEO title in 2001 — later becoming Senior Chairman and CEO in 2005 — he crystallized a set of acquisition principles so specific and so rigorously followed that they deserve to be called a playbook.

The Prosperity Playbook worked like this, and it is worth examining each element closely because this is the engine that powers everything.

Target selection came first. Prosperity focused on smaller community banks in Texas facing succession issues. The ideal seller was a founder in his sixties or seventies, running a well-managed bank with good deposits and conservative loans, but with no heir interested in taking over and no appetite for the increasing regulatory burden of banking in the modern era. Pay fair prices — typically at or near tangible book value, occasionally at modest premiums — but never get into bidding wars. Structure deals primarily in stock rather than cash, which accomplished two things: it preserved Prosperity's capital and it kept the selling banker invested in the combined company's future, aligning incentives in a way that cash deals cannot.

Deal structure was the second element. Structure deals primarily in stock rather than cash, which accomplished two things: it preserved Prosperity's capital and it kept the selling banker invested in the combined company's future, aligning incentives in a way that cash deals cannot.

Integration speed was the third element, and this is the part that truly separated Prosperity from its competitors. While most bank acquirers take six to twelve months to integrate a target — converting systems, consolidating back offices, rationalizing branches — Prosperity aimed to complete integrations within sixty to ninety days. This was not just fast. It was unheard of. The logic was counterintuitive but sound: prolonged integrations create uncertainty for employees and customers, leading to talent departures and deposit runoff. A fast integration is painful but brief, like ripping off a bandage. And it allowed Prosperity to harvest cost synergies almost immediately, with expense reductions often running forty to fifty percent of the target's pre-acquisition cost base.

The credit culture filter was the fourth and final element, and it was non-negotiable. No matter how attractive a deal looked on price, Prosperity walked away from banks with problematic loan books. The company's underwriting standards applied not just to its own originations but to every loan portfolio it acquired. This discipline meant that Prosperity could execute acquisition after acquisition without accumulating the hidden credit landmines that have destroyed so many serial acquirers in banking history.

Through the early and mid-2000s, Prosperity executed this playbook across the Houston metropolitan area, then expanded into Dallas, penetrating new markets while maintaining the local knowledge that community banking requires. Each acquisition added branches, deposits, and lending relationships. Each integration proved the model worked. And each successful deal enhanced Prosperity's reputation among the community of Texas bankers who might themselves be thinking about selling someday.

The geographic strategy was deliberate and highly analytical: blanket Texas with a branch network dense enough to offer convenience but lean enough to maintain efficiency. Think of it as a chess game played on a map of Texas — each acquisition was a move designed to control a market, fill a geographic gap, or strengthen a position in a growing corridor. Unlike national banks that parachuted into Texas with big marketing budgets and standardized products, Prosperity understood that Texas banking was still fundamentally local. The rancher in Lubbock and the small business owner in The Woodlands wanted a banker who understood their community, even if that banker now worked for a Houston-headquartered holding company.

There is a myth in banking — and in M&A more broadly — that serial acquirers eventually trip over their own ambition. The logic seems sound: each deal adds complexity, each integration strains management bandwidth, and sooner or later, a bad acquisition poisons the portfolio. The academic literature is full of studies showing that most M&A destroys value for acquirers. And yet here was Prosperity, deal after deal, growing faster, getting more efficient, and maintaining credit quality that would be the envy of banks a fraction of its size. The myth of inevitable acquirer self-destruction simply did not apply.

The reason, which would become clearer with each passing year, was that Prosperity was not really in the business of financial engineering. It was in the business of operational execution. The deals were not about financial arbitrage or clever structuring. They were about buying good banks cheaply, stripping out unnecessary costs, and running them better. This is much harder than it sounds, and it requires a kind of institutional discipline that cannot be acquired through a single hire or a consulting engagement. It has to be built, one deal at a time, over decades.

By the time the financial crisis began gathering force in 2007 and 2008, Prosperity had built something remarkable: a fortress balance sheet with minimal credit issues, a proven integration capability, and a stock price strong enough to serve as acquisition currency. While other banks were about to fight for survival, Prosperity was about to find its finest hour.

V. The Financial Crisis: Prosperity's Defining Moment (2008-2011)

On November 7, 2008, the Texas Department of Savings and Mortgage Lending closed Franklin Bank, S.S.B., and the FDIC was named receiver. Franklin Bank had been a fast-growing, aggressive lender — the opposite of Prosperity in almost every way. It held over five billion dollars in assets, much of it in the kind of speculative lending that Prosperity had spent decades avoiding. The FDIC estimated the failure would cost its Deposit Insurance Fund between 1.4 and 1.6 billion dollars.

And then Prosperity stepped in. While other potential acquirers were paralyzed by their own balance sheet problems, Zalman saw what he had been trained over twenty-five years to see: a good franchise trapped inside a bad institution, available at a price that might never recur.

In the FDIC-assisted transaction, Prosperity assumed approximately 3.7 billion dollars of Franklin's deposits — including all uninsured deposits — and purchased 850 million dollars of assets. The FDIC retained the remaining toxic assets. For Prosperity, this was transformational. In a single transaction, the company roughly doubled its deposit base. The deal structure was elegant from a risk perspective: Prosperity took the deposits and the clean assets while the FDIC absorbed the credit losses on the problematic loans. It was the kind of deal that only becomes available during a crisis, and only to banks strong enough to execute it.

This was not an act of courage born from ignorance.

It was the culmination of everything Prosperity had built over twenty-five years. The conservative credit culture meant no subprime exposure of its own to worry about. The strong capital ratios meant regulators trusted Prosperity to absorb a large institution. The integration capability — honed on dozens of smaller deals — meant management had the operational confidence to absorb Franklin's operations without stumbling.

While the nation's attention was focused on the spectacular failures of Washington Mutual, Wachovia, IndyMac, and dozens of other institutions, Prosperity was quietly executing one of the most strategically important transactions in Texas banking history. The Franklin acquisition gave Prosperity scale, market presence, and deposits at a cost that would never be replicated in normal times.

In 2009, Prosperity continued its crisis-era expansion. When FBOP Corporation's nine subsidiary banks were closed by chartering agencies and the FDIC stepped in as receiver on October 30, 2009, the resulting restructuring created additional opportunities. Prosperity eventually acquired three Texas branches — Madisonville State Bank, Citizens National Bank, and North Houston Bank — from U.S. Bank, which had acquired all nine FBOP banks from the FDIC. These were smaller transactions, but they reinforced Prosperity's position as the buyer of choice when distressed Texas banking assets needed a new home.

The contrast with the broader industry during this period was striking. Across America, banks were raising emergency capital, slashing dividends, and receiving government bailouts through TARP. Citigroup, Bank of America, and dozens of regional banks teetered on the edge. The banking industry shed hundreds of thousands of jobs. Prosperity, meanwhile, was growing — adding branches, adding deposits, adding market share — and doing it profitably.

The cultural discipline during this period cannot be overstated.

When markets are panicking, the temptation to hunker down and stop all activity is enormous. Many well-capitalized banks did exactly that during 2008-2009, sitting on their hands while opportunities passed them by. Zalman and his team did the opposite: they stuck to the model, trusted their credit underwriting, and executed with the same precision they applied to every deal. No panic. No deviation. No hand-wringing.

The financial crisis also built Prosperity's national credibility. Before 2008, the company was known primarily within Texas banking circles. After the crisis, it was recognized as one of America's most capable bank acquirers — a company that could absorb large, complex institutions in chaotic conditions and emerge stronger. This reputation would prove invaluable in the years ahead, as the next wave of Texas banking consolidation gathered force.

It is worth pausing to appreciate just how rare Prosperity's crisis-era performance was. The 2008-2009 period was the worst banking environment since the Great Depression. More than five hundred banks failed between 2008 and 2013. The survivors were generally those who hunkered down, conserved capital, and waited for the storm to pass. The number of banks that actively grew and strengthened during this period — through disciplined, value-creating acquisitions — could be counted on one hand. Prosperity was not just a survivor. It was an apex predator in a financial ecosystem where most participants were struggling to avoid extinction.

The Franklin Bank deal alone is worth studying as a case in M&A opportunism. Consider the economics: Prosperity acquired 3.7 billion dollars in deposits — the lifeblood of any bank — and 850 million in clean assets, while the FDIC absorbed over a billion dollars in losses on the toxic remainder. In a normal market, acquiring that volume of deposits would have cost multiples of what Prosperity paid. The crisis created a once-in-a-generation pricing dislocation, and Prosperity was prepared to act because it had spent twenty-five years building the balance sheet strength, regulatory relationships, and operational capability to do so. Luck favors the prepared, as the saying goes, but it also favors the disciplined.

VI. Post-Crisis Dominance and The Great Texas Banking Roll-Up (2012-2016)

If the financial crisis gave Prosperity its credentials, the years that followed gave it its kingdom. The period from 2012 through 2016 represented the most sustained and concentrated burst of acquisition activity in the company's history, driven by a convergence of forces that made Texas banking consolidation not just likely but inevitable.

The succession crisis that had been building for years finally reached critical mass.

Across Texas, the founders who had built community banks in the 1960s, 1970s, and 1980s were now in their seventies and eighties. Their children had gone off to become lawyers, doctors, or tech entrepreneurs. The prospect of managing a bank in an era of Dodd-Frank compliance requirements — with annual stress tests, Volcker Rule restrictions, and ever-expanding regulatory documentation — held no appeal for the next generation. Compliance costs that a billion-dollar bank could absorb across thousands of loans were crushing for a two-hundred-million-dollar bank that might have a single compliance officer splitting duties with other roles.

Prosperity became the acquirer of choice. When a Texas community banker decided it was time to sell, Prosperity's phone rang first. The company's reputation for fair dealing, quick execution, and respectful treatment of acquired employees and customers made it the preferred partner. This was not just a financial advantage — it was a moat. Deal flow in community banking is driven by relationships and reputation, not investment banker pitch books.

The transactions came in rapid succession. In July 2012, Prosperity completed its merger with American State Financial Corporation, adding thirty-seven banking offices across eighteen counties in West Texas — Lubbock, Midland, Odessa, Abilene. This was Prosperity's first meaningful presence in West Texas, a region booming with Permian Basin oil activity. The deal brought approximately three billion dollars in assets. W.R. Collier, American State's Chairman and CEO, joined Prosperity's board and became Senior Chairman for the West Texas area, maintaining the local leadership continuity that was central to Prosperity's integration model.

In April 2013, Prosperity made a strategically significant move: it acquired Coppermark Bancshares, which operated nine full-service banking offices — six in Oklahoma City and surrounding areas, three in the Dallas area. With 1.3 billion dollars in assets and 1.2 billion in deposits, Coppermark represented Prosperity's first expansion beyond Texas borders.

The Oklahoma entry was a calculated bet that the same consolidation dynamics playing out in Texas would eventually unfold in the neighboring state. Oklahoma's banking market shared many of Texas's characteristics — a large number of small, independent banks, founder succession challenges, and an economy tied to energy and agriculture. But it was also a test of whether Prosperity's playbook could work in a market where the company had no pre-existing relationships or reputation. The initial results suggested it could: the Coppermark integration proceeded smoothly, and the Oklahoma footprint would later be deepened through additional acquisitions.

Later that year, Prosperity completed its merger with FVNB Corp., adding thirty-four banking offices in Texas. In April 2014, the acquisition of F&M Bancorporation brought thirteen more branches, including several in Tulsa, Oklahoma, deepening the company's Oklahoma footprint.

The pace did not relent. Tradition Bancshares brought seven Houston-area banking offices in January 2016, strengthening Prosperity's presence in key submarkets including Bellaire, Katy, and The Woodlands — some of Houston's most affluent and fastest-growing communities.

Through all of this, the numbers told a story of almost mechanical execution. Assets grew from roughly fourteen billion dollars in 2010 to approximately twenty-eight billion dollars by 2016 — doubling in six years. And here is the remarkable part: the efficiency ratio stayed below forty percent. In most industries, rapid growth through acquisition degrades operational efficiency as integration costs mount and organizational complexity increases. At Prosperity, the opposite happened. Each acquisition was an opportunity to cut redundant costs, consolidate back-office operations, and spread fixed technology and compliance expenses across a larger asset base. The machine was not just growing. It was getting more efficient as it grew.

Competition was intensifying. Other Texas consolidators were emerging — some homegrown, some backed by private equity capital. But Prosperity's combination of reputation, speed, and discipline kept it ahead. The company had something its competitors could not easily replicate: organizational muscle memory from dozens of successful integrations. When Prosperity acquired a bank, every step — from system conversion to branch signage to customer communication — followed a proven protocol. This was not just efficiency. It was process power in its purest form.

A word on how Prosperity maintained the "community" in community banking even as it grew to a scale that most community bankers would find unrecognizable. The trick was decentralized relationship management combined with centralized operations. The loan officer in Lubbock and the branch manager in The Woodlands maintained their local relationships, knew their customers by name, and made credit decisions informed by local knowledge. But the back office — compliance, technology, accounting, HR — was centralized in Houston, run with the efficiency that comes from scale. This hybrid model allowed Prosperity to offer the personal touch of a small bank with the cost structure of a large one. It was, in many ways, the best of both worlds — and it was very difficult for competitors at either end of the spectrum to replicate. The megabanks could not match the local relationships. The community banks could not match the cost efficiency.

The period also saw Prosperity garner recognition that reinforced its brand. Beginning in 2010, the company was named to Forbes's "America's Best Banks" list — a distinction it would maintain for more than a decade. For a company that did not advertise aggressively or cultivate media relationships, the Forbes recognition served as a quiet but powerful endorsement, particularly among the business customers and banking executives who constituted Prosperity's two most important audiences.

VII. The Mega-Deal Era: Scale Begets Scale (2017-2020)

By the late 2010s, Prosperity faced a strategic inflection point. The company had spent two decades mastering the acquisition of small to mid-sized community banks. But the math was changing. At nearly thirty billion dollars in assets, absorbing a three-hundred-million-dollar bank — the kind of transaction that had been Prosperity's bread and butter — barely moved the needle. To continue growing at a meaningful rate, Prosperity needed to shift to larger targets.

The paradigm shift arrived on November 1, 2019, when Prosperity completed its merger with LegacyTexas Financial Group.

This was a different kind of deal. LegacyTexas was not a sleepy community bank with a retiring founder. It was a 10.5-billion-dollar institution with forty-two banking centers in the Dallas-Fort Worth metroplex, a sophisticated wealth management platform, and a more polished corporate culture than the scrappy Houston operator that was acquiring it.

The transaction was valued at approximately 2.1 billion dollars, structured as roughly eighty-five percent stock and fifteen percent cash — consistent with Prosperity's longstanding preference for equity-funded deals. Each LegacyTexas share received 0.528 Prosperity shares plus 6.28 dollars in cash, valuing the target at roughly 41.78 dollars per share. The stock-heavy structure was vintage Prosperity: preserve capital, keep the selling management team invested in the combined entity's success, and maintain the financial flexibility to continue acquiring.

The strategic logic was compelling. Dallas-Fort Worth was the fastest-growing major metropolitan area in Texas, and Prosperity's presence there had been relatively thin. LegacyTexas gave Prosperity instant scale in the market, along with a lending platform that included warehouse lending and wealth management capabilities that Prosperity had not previously possessed. The combined company commanded thirty-two billion dollars in assets, twenty-four billion in deposits, and twenty billion in loans.

But the market was skeptical. Prosperity's track record was built on integrating smaller, simpler banks. LegacyTexas was larger, more complex, and culturally distinct. Dallas banking culture tends toward the polished and corporate; Houston banking culture — particularly at Prosperity — was more hands-on and operational. Could the integration machine handle a target this different?

Zalman and his team answered by executing precisely the same playbook, scaled up. Kevin Hanigan, LegacyTexas's President and CEO, was brought into Prosperity as President and Chief Operating Officer — maintaining leadership continuity while ensuring cultural knowledge was preserved. Cost synergies were targeted at twenty-five percent of LegacyTexas's non-interest expense base. The deal was projected to be 10.3 percent accretive to earnings in its first full year. The integration was completed without the credit surprises or customer attrition that skeptics had predicted.

The LegacyTexas deal proved that Prosperity's playbook was scalable. It was not limited to tiny community banks in rural towns. The same principles — disciplined pricing, stock-based consideration, rapid integration, ruthless cost harvesting, credit culture preservation — worked for multi-billion-dollar targets in major metropolitan markets. This was a critical proof of concept that expanded Prosperity's addressable universe of acquisition targets significantly.

The leadership succession question surfaced during this period as well. Zalman, who had joined Prosperity in 1986, was now in his mid-sixties. He remained firmly in control, showing no signs of stepping back, but the concentration of institutional knowledge and deal-making expertise in a single individual was becoming a topic of discussion among analysts and investors.

Then COVID hit. Nobody saw it coming. But the question was not whether Prosperity would survive — the question was whether it would once again use crisis as a catalyst.

Before we get there, it is worth reflecting on what the LegacyTexas deal revealed about Prosperity's evolution. The company had started as a rural Texas community bank acquiring other rural Texas community banks. Now it was acquiring sophisticated metropolitan institutions and absorbing them into its model. The playbook had not changed — the principles remained identical — but the scale and complexity of execution had increased dramatically. This was no longer a one-trick pony. It was a scalable platform.

The deal also brought new leadership talent into the organization. Kevin Hanigan, with his experience running a larger, more complex institution, added a dimension to Prosperity's management bench that had been lacking. Whether by design or by happy accident, the LegacyTexas merger addressed the succession depth concern by importing seasoned talent through the acquisition itself — a form of management development through M&A that few companies execute deliberately but that Prosperity stumbled into and embraced.

Entering 2020, Prosperity commanded thirty-three billion dollars in assets and held the undisputed title of Texas's most prolific bank acquirer. The company had proven its model across market cycles, across deal sizes, and across geographic markets. What remained to be tested was something no one could have predicted: a global pandemic that would shut down the economy and stress-test every assumption about credit quality, operational resilience, and customer relationships.

VIII. COVID-19, Rate Cycles, and The Latest Chapter (2020-2025)

The pandemic arrived as a stress test that nobody had planned for but that Prosperity was uniquely equipped to handle. While banks across America scrambled to assess credit exposure to shuttered businesses and furloughed workers, Prosperity's conservative underwriting meant its loan book was built to withstand exactly this kind of economic shock.

The company's response to the Paycheck Protection Program illustrated its community banking DNA. Prosperity obtained SBA approvals on approximately 18,700 PPP loans totaling over two billion dollars — a massive operational lift for a bank of its size. By the end of 2021, forgiveness had reduced the outstanding balance to roughly 170 million dollars across 1,512 remaining loans. The PPP program generated fee income while deepening relationships with thousands of small business customers — many of whom came to Prosperity specifically because their larger banks could not process applications fast enough.

Credit quality held up remarkably.

By the fourth quarter of 2021, non-performing assets had fallen to just 0.09 percent of average interest-earning assets — essentially zero for practical purposes. To understand how extraordinary this is, consider that many banks were reporting non-performing asset ratios ten to fifty times higher during the same period. Prosperity's loan book, built on decades of conservative underwriting, proved nearly impervious to the worst economic shock since the Great Depression. The pandemic, which had been expected to generate widespread loan losses, instead validated the credit culture that Zalman had spent his entire career building.

The COVID experience also revealed something about Prosperity's customer base that is easy to overlook. The company's borrowers — small and mid-sized Texas businesses, commercial real estate owners, farmers and ranchers — tend to be conservative operators themselves. They carry less leverage, maintain larger cash reserves, and operate in industries with tangible assets and real cash flows. Conservative lenders tend to attract conservative borrowers, creating a self-reinforcing cycle of credit quality that is difficult for competitors to replicate.

The interest rate environment that followed created both opportunity and challenge. When the Federal Reserve began raising rates aggressively in 2022, Prosperity's asset-sensitive balance sheet benefited significantly. To explain what "asset-sensitive" means in plain terms: when interest rates rise, a bank's loan portfolio reprices upward faster than its deposit costs increase. The bank earns more on the money it lends out while — at least temporarily — continuing to pay relatively low rates on the deposits it takes in. This spread between earning and paying is the net interest margin, and it is the single most important driver of bank profitability.

For Prosperity, the rate-rising cycle produced dramatic results. Net interest margin expanded from 2.78 percent in 2023 to 3.05 percent in the fourth quarter of 2024 and continued climbing to 3.30 percent by the fourth quarter of 2025 — a fifty-two basis point improvement that may sound modest but is enormous when applied against a nearly forty-billion-dollar asset base. Each basis point of NIM improvement on that asset base translates to roughly four million dollars in additional annual pre-tax income. Fifty-two basis points, then, represents more than two hundred million dollars in incremental earning power. This was the primary engine behind Prosperity's record 2025 earnings.

The 2023 regional banking crisis provided yet another demonstration of Prosperity's defensive strength. When Silicon Valley Bank collapsed on March 10, 2023 — followed by Signature Bank and First Republic — the banking industry experienced its most acute stress since 2008. Depositors fled institutions perceived as risky. Bank stocks plunged. Regulators scrambled to contain the damage.

Prosperity was insulated by the same characteristics that had protected it through every prior crisis: conservative loan-to-deposit ratios, no concentrated exposure to cryptocurrency or venture-backed technology companies, strong capital ratios, and a diversified deposit base rooted in commercial and consumer relationships rather than institutional hot money.

The SVB collapse in particular offered a striking contrast to the Prosperity model. Silicon Valley Bank had grown rapidly by concentrating on a single customer segment — venture-backed technology companies — and investing heavily in long-duration bonds that lost value as rates rose. When depositors panicked and withdrew billions in a single day, SVB lacked the liquidity to meet redemptions and failed within forty-eight hours. It was the second-largest bank failure in American history.

Everything about SVB's model was the opposite of Prosperity's: concentrated versus diversified, aggressive versus conservative, growth-at-all-costs versus disciplined expansion. The two banks could have been designed as a controlled experiment in banking philosophy. The contrast could not have been more instructive. While peers grappled with deposit flight and confidence crises, Prosperity continued operating as if the panic were happening on a different planet. In a sense, it was — the crisis affected banks that had deviated from the fundamentals that Prosperity had never abandoned.

The company maintained its twenty-five consecutive years of dividend increases through the crisis, a streak that speaks to both the stability of cash flows and management's confidence in the balance sheet. By 2025, the annual dividend had grown to 2.32 dollars per share, with a conservative payout ratio of roughly forty-one percent.

The company's dividend streak is worth underscoring because it reveals something deeper about management's philosophy. A company can only sustain twenty-five consecutive years of dividend increases if its earnings are genuinely stable and growing. Cutting a dividend is among the most painful signals a bank can send to shareholders — it implies that cash flows are uncertain or declining. By maintaining the streak through 2008, through COVID, and through the 2023 banking panic, Prosperity demonstrated not just financial strength but management confidence in the durability of its business model.

Recent strategic moves have demonstrated that the acquisition machine remains fully operational. Prosperity completed its merger with Lone Star State Bancshares in April 2024, adding Lone Star State Bank of West Texas. On January 1, 2026, the acquisition of American Bank Holding Corporation brought American Bank of Corpus Christi into the fold, strengthening the South Texas presence. Southwest Bancshares, which operated Texas Partners Bank in San Antonio, was absorbed on February 1, 2026, giving Prosperity enhanced positioning in one of the state's fastest-growing markets.

And then came the headline deal.

On January 28, 2026, Prosperity announced its merger with Stellar Bancorp — a 2.002-billion-dollar transaction that, if completed as expected in the second quarter of 2026, will add 10.8 billion dollars in assets and fifty-two banking offices concentrated in greater Houston, Beaumont, and Dallas. The combined entity will operate more than 330 banking centers and become the second-largest Texas-headquartered bank by deposits. The deal terms follow the familiar Prosperity template: stock-heavy consideration at 0.3803 Prosperity shares plus 11.36 dollars in cash per Stellar share.

David Zalman remains at the helm, now approaching four decades at the company. His presence provides continuity and strategic coherence, but the succession question has become more prominent. At approximately sixty-eight or sixty-nine years old, Zalman shows no public signs of stepping back, and recent deals suggest the acquisition engine is, if anything, accelerating. Fourth quarter 2025 earnings came in at 139.9 million dollars, bringing the full year to a record 542.8 million — up 13.2 percent year over year. Earnings per share reached 5.72 dollars, with capital ratios at fortress levels: common equity tier one at 17.55 percent and leverage ratio at 11.93 percent.

The balance sheet at the end of 2025 stood at 38.5 billion dollars in assets. Once the Stellar merger closes, that number will push past forty-nine billion — approaching the fifty-billion-dollar threshold that triggers enhanced regulatory scrutiny under Dodd-Frank.

This threshold deserves a brief explanation for those unfamiliar with banking regulation. Under the Dodd-Frank Act, banks with more than fifty billion dollars in assets are subject to "enhanced prudential standards" — a set of more rigorous regulatory requirements that include company-run stress tests, more detailed capital planning, heightened liquidity requirements, and enhanced risk management standards. For banks approaching this threshold, the incremental compliance cost can be substantial — potentially tens of millions of dollars annually in additional staffing, technology, and reporting expenses. Some banks have deliberately managed their asset growth to stay below the threshold. Prosperity, by contrast, appears ready to cross it, suggesting that management views the long-term benefits of scale as outweighing the incremental regulatory burden.

How Prosperity navigates that regulatory milestone will be one of the most consequential strategic decisions of the next several years. The Stellar deal also signals something broader: the Prosperity acquisition machine is not slowing down. Three transactions closed in a twelve-month span — Lone Star State Bancshares, American Bank, and Southwest Bancshares — followed by the announcement of the largest deal since LegacyTexas. If there was any doubt about whether Prosperity's M&A appetite was diminishing with age and scale, the recent activity puts that question to rest.

IX. The Prosperity Playbook: What Makes Them Different

To understand why Prosperity has succeeded where so many serial acquirers in banking have failed, it helps to dissect the playbook into its component parts. Each element is individually straightforward. The competitive advantage comes from executing all of them simultaneously, consistently, for decades.

Credit Culture Above All. This is the foundation upon which everything else rests. Prosperity's lending standards are conservative by design and by temperament. The loan-to-deposit ratio has consistently run below peer averages, meaning the bank never stretches to deploy every dollar of deposits into loans — it maintains a buffer that provides liquidity and reduces credit risk. Real estate lending and commercial and industrial loans form the core of the portfolio, with a deliberate avoidance of exotic products, structured finance, and speculative categories. The most remarkable statistic in Prosperity's history may be this: zero loan losses during acquisition integrations. In an industry where acquired loan portfolios routinely harbor hidden problems that surface after closing, Prosperity's pre-acquisition credit diligence has been essentially flawless.

M&A Discipline. The preference for stock-based consideration is not just about conserving cash — it is a mechanism for aligning incentives. When a selling banker receives Prosperity stock, he or she becomes a Prosperity shareholder with a vested interest in the combined company's success. This reduces the adversarial dynamic that can poison acquisitions structured as pure cash deals, where the seller takes the money and walks away. Quick integrations — sixty to ninety days rather than the industry-standard six to twelve months — minimize the uncertainty that drives talent departures and customer attrition. Cost harvesting is ruthless but targeted: redundant back-office operations, duplicate compliance functions, and overlapping branch locations are eliminated, while customer-facing relationship managers are retained. Geographic focus means every acquisition adds to markets Prosperity already understands intimately — no speculative entries into unfamiliar states or regions.

Operational Excellence. The efficiency ratio tells the story most succinctly. A sub-forty-four-percent efficiency ratio — Prosperity reported 43.6 percent for the fourth quarter of 2025 — means that for every dollar of revenue, less than forty-four cents goes to operating expenses. The industry average hovers above fifty-five percent. This gap represents real economic value: the ability to price loans more competitively, absorb credit losses more easily, and still generate superior returns for shareholders. Technology investments at Prosperity are focused on efficiency rather than flash — core banking systems that enable rapid integration, digital banking capabilities that meet customer expectations, but no expensive experiments with blockchain or artificial intelligence for their own sake.

Leadership Continuity. David Zalman's nearly four-decade tenure is extraordinary in any industry. In banking, where CEO tenures average perhaps seven to ten years, it is almost without precedent for a company of Prosperity's size. The advantage of continuity at this level is not just institutional memory — though that matters enormously in a business driven by relationships and reputation. It is the cultural consistency that comes from having the same person set the tone for decades. Every Prosperity employee knows what the company values because those values have not changed with each new CEO. Management team longevity extends beyond Zalman: many of Prosperity's senior leaders have been with the company for fifteen to twenty years or more, and insider ownership ensures alignment between management and shareholders.

Capital Allocation. Prosperity is a consistent dividend payer, having increased its dividend for twenty-five consecutive years — a streak that encompasses the financial crisis, COVID, and the 2023 banking panic. Share buybacks are deployed when the stock is attractively valued. Acquisitions are pursued patiently, with management willing to wait for the right deal rather than chasing growth for its own sake. This patience is harder than it sounds. The pressure on public company CEOs to "do something" — to announce deals, to demonstrate growth, to justify their salaries — is intense. Zalman's willingness to let quarters pass without a deal, waiting for the right target at the right price, is a form of discipline that compounds over decades.

The combination of these elements creates something greater than the sum of its parts. Any bank can say it has conservative credit standards. Any bank can announce an acquisition. But the ability to execute thirty-plus acquisitions over two decades, each one integrated rapidly, each one accretive, each one strengthening rather than diluting the credit culture — that is process power. And process power, once established, is extraordinarily difficult for competitors to replicate.

X. Competitive Position: Porter's Five Forces and Hamilton's Seven Powers

Understanding Prosperity's competitive moat requires looking at the business through two complementary strategic lenses. The first is Michael Porter's Five Forces framework, which maps the external competitive pressures facing the business. The second is Hamilton Helmer's Seven Powers framework, which identifies the sources of durable competitive advantage.

Competitive Rivalry in Texas banking is intense and getting more so. National banks including JPMorgan Chase, Bank of America, and Wells Fargo all have significant Texas operations, bringing massive technology budgets and brand recognition. Among Texas-headquartered banks, Cullen/Frost Bankers — with 42.5 billion dollars in deposits as of late 2025 — remains the largest and a formidable competitor with deep customer loyalty, particularly in San Antonio. Texas Capital Bancshares offers specialized commercial banking services that compete for Prosperity's business customers. And with Comerica's pending sale to Fifth Third Bancorp, the competitive landscape is actively reshuffling. Despite this intensity, community banking retains a meaningful advantage in relationship-driven lending — the kind of nuanced credit decisions where knowing the borrower personally still matters.

The Threat of New Entrants is moderate to low. Banking is one of the most heavily regulated industries in America. Obtaining a new bank charter requires substantial capital, years of regulatory process, and demonstrated management expertise. The compliance costs alone — especially for institutions approaching the fifty-billion-dollar regulatory threshold — create a natural barrier. Fintech companies have disrupted specific banking functions like payments and personal lending, but the full-service commercial banking relationship that Prosperity provides — treasury management, credit lines, deposits, wealth management — remains difficult for digital-only competitors to replicate.

Supplier Power in banking manifests primarily through deposits and labor. Deposits are the raw material of banking, and Prosperity's deep community relationships provide a stable and relatively low-cost funding base. Interest rates are set by the Federal Reserve, not by individual banks, which limits pricing power but also means no single supplier can dictate terms. The labor market for experienced community bankers is competitive but manageable — and Prosperity's acquisition model actually helps on this front, as acquired bankers often stay with the company.

Buyer Power is moderate. Commercial clients have alternatives and will shop for the best lending terms, but switching costs in business banking are real: changing treasury management platforms, re-establishing credit relationships, and migrating payroll and payment systems all create friction. Retail customers are somewhat less sticky in an era of digital banking, but Prosperity's deep Texas branch network provides convenience that purely digital competitors cannot match.

The Threat of Substitutes is the area of greatest long-term concern. Fintech lending platforms, neobanks, and payment processing companies are steadily unbundling traditional banking services. However, for the core Prosperity customer — the Texas small business owner or commercial real estate developer who needs a relationship banker, a line of credit, and a treasury management platform — full-service substitutes remain limited. Texas's business-friendly environment and strong economic growth support traditional banking demand for the foreseeable future.

Turning to Helmer's Seven Powers, the picture of Prosperity's competitive moat becomes sharper.

Scale Economies are strong and growing. Fixed costs for technology, compliance, and corporate overhead are spread across a base of more than three hundred branches and nearly forty billion dollars in assets. This scale advantage is directly visible in the efficiency ratio: Prosperity can run its operations for less than forty-four cents per revenue dollar while peers spend fifty-five cents or more. This efficiency gap enables pricing flexibility — Prosperity can offer competitive loan rates and still generate superior returns.

Network Effects are weak, as banking is not a network business in the way that social media or payments platforms are. There are some benefits from having multiple branch touchpoints that allow customers to bank across Texas, but this is a convenience advantage rather than a true network effect.

Counter-Positioning is moderate but meaningful. Prosperity's conservative credit culture represents a strategic choice that aggressive competitors find difficult to replicate — not because they cannot be conservative, but because their business models, incentive structures, and growth expectations make it economically unattractive to do so. A bank that has promised Wall Street fifteen percent loan growth cannot suddenly adopt Prosperity's underwriting discipline without cratering its growth metrics.

Switching Costs are moderate. Business banking relationships are genuinely sticky — treasury management, credit facilities, and the personal relationships between bankers and business owners create meaningful friction against switching. Retail banking switching costs are lower but still present.

Branding carries moderate strength within Texas. Prosperity has been named to Forbes's "America's Best Banks" list since 2010 and was recognized by Money magazine as the "Best Overall Bank in Texas" in 2025. The brand carries weight within the professional and business community even if it lacks the consumer recognition of a Chase or Wells Fargo.

Cornered Resource is strong. David Zalman's institutional knowledge, his relationships across the Texas banking community, and the deal flow that results from Prosperity's reputation as the preferred acquirer are genuine cornered resources. The FDIC relationships built during the crisis era, the personal networks that generate acquisition opportunities, and the cultural DNA around credit discipline are not easily transferable to competitors.

Process Power is Prosperity's primary moat. More than thirty acquisitions over two decades have created an integration playbook of extraordinary depth and reliability. Every aspect of bank acquisition — due diligence, credit review, system conversion, branch rebranding, personnel decisions, customer communication, regulatory filings — has been done so many times that it operates with the reliability of a factory assembly line. Competitors can see exactly what Prosperity does but cannot easily replicate the organizational muscle memory that comes from decades of repetitive execution. This is the essence of process power: it looks simple from the outside, but the accumulated institutional knowledge required to execute it consistently is the product of irreplaceable experience.

The primary moat, then, is the combination of process power in M&A execution, scale economies that enable superior efficiency, and the cornered resource of management expertise and deal flow relationships. This is a defensible competitive position — not impregnable, but one that would take a competitor decades to replicate.

There is an important nuance here that separates Prosperity from many companies that claim to have competitive moats. Prosperity's advantages are not static — they are dynamic and self-reinforcing. Each successful acquisition strengthens the process power by adding to the institutional knowledge base. Each deal that closes smoothly enhances the reputation that drives deal flow. Each integrated bank improves the scale economies that fund competitive pricing. This is a flywheel, not a wall. And flywheels, once spinning, are extremely hard to stop.

How does Prosperity stack up against its primary Texas competitors on these dimensions? Cullen/Frost Bankers, the larger Texas-headquartered rival, competes primarily on brand loyalty and customer service rather than M&A-driven growth. Frost has chosen a largely organic growth model, building new branches and winning customers one relationship at a time. This is a perfectly valid strategy, but it yields slower growth and does not benefit from the acquisition-driven scale economies that Prosperity enjoys. Texas Capital Bancshares takes yet another approach, focusing on specialized commercial banking and investment banking services for a narrower customer base. Neither competitor has attempted the volume of acquisitions that defines Prosperity's model, which means neither has developed the process power that such volume creates.

The competitive comparison illustrates an important point: there is no single "right" strategy in Texas banking. What matters is the alignment between strategy, culture, and execution. Prosperity's model works because the culture supports the strategy and the execution validates the culture. Disrupting this alignment — through a leadership change, a botched acquisition, or a shift in strategic direction — represents the most significant risk to the company's competitive position.

XI. The Bull and Bear Case

The Bull Case

The argument for Prosperity starts with track record. Forty years of conservative management through multiple economic cycles — S&L crisis, dot-com bust, financial crisis, pandemic, regional banking panic — with consistent profitability and dividend growth is not something that can be dismissed or easily replicated. When investors pay for Prosperity, they are paying for proven resilience.

Texas demographics provide a structural tailwind. The state has been the fastest-growing major state in America by population for years, driven by corporate relocations, business-friendly regulation, no state income tax, and a diversifying economy. Every new Texan needs banking services. Every new Texas business needs a commercial banking relationship. This organic growth supplements the acquisition-driven growth that has defined Prosperity's history.

The consolidation opportunity remains vast.

There are still over four thousand banks in the United States, with hundreds in Texas alone. The same dynamics that have driven consolidation for twenty years — founder succession problems, rising compliance costs, technology investment requirements — continue to intensify. Prosperity's reputation, balance sheet, and integration capability position it as the primary beneficiary of ongoing consolidation.

The fortress balance sheet — with a common equity tier one ratio of 17.55 percent, well above regulatory minimums — provides enormous optionality. In a credit downturn, Prosperity can absorb losses without existential risk. In a market dislocation, it can acquire distressed assets opportunistically. In a stable environment, it can return capital through dividends and buybacks. This kind of financial flexibility is rare and valuable.

Recent earnings momentum adds to the case. The net interest margin expansion from 2.78 percent to 3.30 percent over two years, combined with strong deposit growth and continued acquisition activity, drove record earnings of 542.8 million dollars in 2025. The pending Stellar Bancorp merger, if completed, will push assets past forty-nine billion dollars and create the second-largest Texas-headquartered bank by deposits.

Myth vs. Reality: Consensus Narratives Worth Challenging

Before laying out the bear case, it is worth addressing a few consensus narratives about Prosperity that deserve scrutiny.

The first myth is that Prosperity is "just a rollup." The rollup label carries negative connotations — it implies financial engineering, aggressive accounting, and inevitable collapse when the acquisition pipeline dries up. But Prosperity is fundamentally different from the classic rollup. Its acquisitions are operationally driven, not financially driven. The value creation comes from running the acquired banks more efficiently, not from financial leverage or accounting tricks. The company's organic business — apart from acquisitions — is healthy and profitable. Remove every acquisition from Prosperity's history, and you still have a well-run, profitable Texas community bank. The acquisitions accelerate growth; they do not mask weakness.

The second myth is that Texas banking is a commodity business where no bank can sustain an advantage. While it is true that loans and deposits are commodity products in the economic sense, the delivery mechanism — the relationship between banker and customer — is not. In commercial banking especially, the trust built over years of relationship lending creates switching costs that pure price competition cannot overcome. Prosperity's branch density and local market knowledge create a distribution advantage that digital-only competitors and out-of-state banks struggle to match.

The third myth is that Prosperity's efficiency ratio is unsustainable — that the company has cut costs to the bone and there is nothing left. While it is true that improving from a 43.6 percent efficiency ratio is harder than improving from a 55 percent ratio, Prosperity's efficiency advantage is structural, not temporary. It is the result of a fundamentally different operating model — centralized back office, decentralized relationships, scale-driven cost spreading — not of one-time cost cuts that will eventually reverse.

The Bear Case

The most prominent risk is key-man concentration.

David Zalman has been the architect of Prosperity's strategy for nearly four decades. His institutional knowledge, relationship network, and strategic vision are deeply embedded in the company's success. While Kevin Hanigan's elevation to President and COO after the LegacyTexas deal suggests succession planning is underway, no formal succession timeline has been publicly announced. The market will need to see evidence that Prosperity's playbook is transferable beyond Zalman before this risk can be fully discounted.

The acquisition model itself faces structural challenges.

As Prosperity grows larger, the universe of targets that can meaningfully impact its financials shrinks. The bank needs bigger deals to move the needle, but bigger deals bring bigger integration risks, more complex cultures to absorb, and higher purchase prices. The Stellar Bancorp merger at two billion dollars is the latest test of whether the playbook scales to ever-larger transactions.

Interest rate sensitivity cuts both ways. While higher rates have expanded margins over the past two years, a rapid decline in rates would compress net interest margins and reduce earnings power. Prosperity's asset-sensitive balance sheet — which benefited from rising rates — would work against it in a falling-rate environment.

Technology disruption remains a slow-burning concern. Fintech companies and neobanks are steadily chipping away at traditional banking functions. While Prosperity's core commercial banking relationships are relatively protected, the long-term trajectory of banking toward digital delivery could erode the branch-based model that underpins Prosperity's community banking approach.

Geographic concentration is a double-edged sword. Texas's economic strength is Prosperity's tailwind, but the state's economy retains meaningful exposure to oil and gas, commercial real estate, and other cyclical sectors. A severe Texas-specific economic shock — an oil price collapse combined with a commercial real estate downturn, for example — would hit Prosperity's loan portfolio disproportionately.

The approaching fifty-billion-dollar asset threshold deserves attention. The Stellar merger will push Prosperity into this enhanced regulatory tier, adding compliance costs and operational complexity that could pressure the efficiency ratio. For a company whose identity is built around operational leanness, the incremental regulatory burden of being a fifty-billion-dollar-plus bank is not trivial.

Finally, there is the risk that Prosperity's model simply runs out of runway. The company has been a serial acquirer for over three decades. At some point, the number of attractive acquisition targets in Texas and Oklahoma will diminish to the point where the M&A engine cannot generate the growth that investors have come to expect. When that happens — and it may already be beginning — Prosperity will need to demonstrate that it can grow organically at rates sufficient to justify its valuation. The transition from acquisition-driven growth to organic growth is one that many serial acquirers have struggled to make.

Key Metrics to Watch

For investors tracking Prosperity's ongoing performance, two metrics deserve primary focus.

The first is net interest margin. As the single largest driver of bank profitability, NIM captures the spread between what Prosperity earns on its loans and investments and what it pays on deposits and borrowings. NIM trends reflect interest rate positioning, deposit pricing discipline, and loan portfolio quality all at once. The expansion from 2.78 percent to 3.30 percent over the past two years has been the primary engine of earnings growth. Monitoring whether this margin holds, expands, or compresses will tell investors more about Prosperity's near-term earnings trajectory than any other single number.

The second is the efficiency ratio. Prosperity's sub-forty-four-percent efficiency ratio is the quantitative expression of its operational moat. If this ratio begins creeping upward — particularly after the Stellar merger integration and the crossing of the fifty-billion-dollar regulatory threshold — it could signal that the company's core competitive advantage is eroding. Conversely, maintaining or improving the ratio through these transitions would confirm that the operational discipline remains intact regardless of scale.

XII. Epilogue: What Comes Next for Prosperity

The question that now hangs over Prosperity Bancshares is whether the next decade can look anything like the last four. The ingredients that fueled the company's rise — a fragmented Texas banking market, a founder-CEO with unmatched institutional knowledge, a proven acquisition playbook, and a growing state economy — remain present, but the context is shifting.

The succession question is the elephant in the room.

Zalman has built something extraordinary, but extraordinary things built around extraordinary individuals face an inherent vulnerability. The playbook is well-documented and the senior team is experienced, but translating one person's judgment, relationships, and instincts into institutional capability is one of the hardest challenges in corporate management. How Prosperity handles this transition — whenever it comes — will determine whether the company's competitive advantages prove durable or personal.

The M&A environment has evolved. Private equity firms have entered community banking with aggressive roll-up strategies, competing for the same acquisition targets that Prosperity has historically dominated. Valuations for attractive community banks have risen accordingly. The days of acquiring well-run banks at tangible book value may be behind us. Prosperity's response — as evidenced by the Stellar Bancorp deal — has been to shift toward larger transactions that offer scale benefits even at higher prices. Whether this strategy preserves the same economic returns as the smaller deals of prior decades remains to be seen.

Geographic expansion beyond Texas and Oklahoma is a strategic question that management has been reluctant to address publicly. The company's competitive advantages are deeply rooted in its Texas relationships and market knowledge. Expanding into Louisiana, Arkansas, or New Mexico would leverage geographic proximity but would require building new relationships and local expertise in markets where Prosperity is unknown. The risk-reward calculus of geographic diversification versus Texas deepening is one of the most consequential strategic decisions facing the next generation of Prosperity leadership.

The technology question looms as well. Prosperity has invested in digital banking capabilities sufficient to meet current customer expectations, but the bank has not positioned itself as a technology leader. In an industry where JPMorgan Chase spends more than fifteen billion dollars annually on technology, the gap between what a forty-billion-dollar bank can invest and what a three-trillion-dollar bank can invest is vast. Whether technology becomes a competitive disadvantage for mid-sized banks or whether the relationship-driven nature of community banking provides protection from digital disruption is an open question with no definitive answer.

The potential strategic alternatives deserve consideration as well. Prosperity could remain independent and continue its acquisition-driven growth strategy. It could pursue a merger of equals with another mid-sized bank to create a super-regional institution. Or, in a scenario that Prosperity shareholders have historically not had to contemplate, the company could itself become an acquisition target for a national bank seeking to deepen its Texas presence. Each path carries different implications for shareholders, employees, and customers — and the choice will ultimately be shaped by market conditions, regulatory dynamics, and the preferences of whoever is leading the company when the decision must be made.

The optimistic scenario sees another decade of disciplined consolidation. The Stellar merger integrated successfully, a few more strategic acquisitions in growing Texas and Oklahoma markets, steady organic growth driven by state demographics, and a smooth leadership transition to a successor who maintains the credit culture and operational discipline that Zalman instilled. In this scenario, Prosperity approaches or exceeds one hundred billion dollars in assets by the mid-2030s, firmly established as a super-regional powerhouse.

The pessimistic scenario imagines a different world. One where growth stalls — targets become too expensive, the efficiency ratio deteriorates under regulatory pressure, technology disruption accelerates, and a key-man departure shakes institutional confidence. In this scenario, Prosperity itself becomes an acquisition target for a larger regional or national bank, its shareholders cashing in on the premium that its Texas franchise would command. There is an irony embedded in this possibility: the company that built its empire through acquisitions could eventually be acquired itself, its playbook absorbed into a larger organization's strategy. In banking, very few remain independent forever.

There is also the question of what happens if Prosperity's two primary growth levers — acquisition and margin expansion — both stall simultaneously. If interest rates decline and NIM compresses at the same time that acquisition targets become scarce or prohibitively expensive, the company would need to find new sources of growth. Fee income from wealth management, treasury services, and other non-interest revenue streams could fill some of the gap, but Prosperity has not historically been a fee-income-heavy bank. Building those capabilities takes time, talent, and investment — and represents a strategic shift that the company has not yet been forced to make.

The truth, as always, will likely land somewhere in between. What seems most certain is that the principles that built Prosperity — conservative credit, operational discipline, patient capital allocation, and deep market knowledge — remain as relevant today as they were when Tracy Rudolph bought that Allied Bank branch in Edna four decades ago. In a financial industry that too often rewards recklessness and punishes patience, Prosperity Bancshares stands as proof that the opposite approach can work. Not just for a quarter or a year, but for a generation.

Boring can be beautiful.

There is one final lesson from the Prosperity Bancshares story that extends beyond banking and beyond Texas. In an era obsessed with disruption, innovation, and exponential growth, Prosperity reminds us that there is another path to extraordinary value creation: find a proven model, execute it with discipline, and repeat. No pivots. No moonshots. No "move fast and break things." Just the patient, unglamorous work of buying good businesses at fair prices, running them efficiently, and compounding the returns over decades.

Warren Buffett once said that his ideal holding period was "forever." David Zalman's ideal acquisition model was "again." And again. And again.

XIII. Further Reading and Resources

Top 10 Resources:

- Prosperity Bancshares Annual Reports (2008, 2017, 2023, 2025) — Best primary source for understanding strategy evolution through different market environments

- "The Acquirer's Multiple" by Tobias Carlisle — Framework for understanding how disciplined acquirers create value by avoiding overpayment

- "The History of Texas Banking" by Joseph M. Grant — Essential context on the regulatory and economic forces that shaped Texas's fragmented banking landscape

- SNL Financial / S&P Global Market Intelligence archives — Comprehensive deal data and comparative analysis for every Prosperity acquisition

- FDIC Failed Bank Database — Detailed records of crisis-era FDIC-assisted transactions including the pivotal Franklin Bank deal

- "The Outsiders" by William Thorndike — Capital allocation case studies with direct applicability to Zalman's approach at Prosperity

- American Banker articles on Texas banking consolidation — Contemporary reporting on the competitive dynamics driving Texas bank M&A

- Federal Reserve Bank of Dallas reports — Texas economic context including population growth, GDP trends, and industry diversification data